UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of | (I.R.S. Employer |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

The |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ |

| Accelerated filer | ☐ |

| Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

The aggregate market value of common stock held by non-affiliates of the registrant as of June 30, 2023, the last business day of the most recently completed second fiscal quarter, was $

As of March 5, 2024, the registrant had

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2024 Annual Meeting of Stockholders, which the registrant intends to file with the Securities and Exchange Commission not later than 120 days after the registrant’s fiscal year ended December 31, 2023, are incorporated by reference into Part II and Part III of this Annual Report on Form 10-K.

908 Devices Inc.

Table of Contents

We own various trademark registrations and applications, and unregistered trademarks, including MX908, Rebel, ZipChip, Maverick, Maven, 908 Devices and our corporate logo. All other trade names, trademarks and service marks of other companies appearing in this Annual Report on Form 10-K are the property of their respective holders. Solely for convenience, the trademarks and trade names in this Annual Report on Form 10-K may be referred to without the ®,™ or RTM symbols, but such references should not be construed as any indicator that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend to use or display other companies’ trademarks and trade names to imply a relationship with, or endorsement or sponsorship of us, by any other companies.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements, which reflect our current views with respect to, among other things, our operations and financial performance. All statements other than statements of historical facts contained in this Annual Report on Form 10-K, including statements regarding our future results of operations and financial position, business strategy and plans and our objectives for future operations, are forward-looking statements, and are made under the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “could,” “target,” “predict,” “seek” and similar expressions are intended to identify forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy, short- and long-term business operations and objectives, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in the “Summary of Risk Factors”, Part I, Item 1A “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Moreover, we operate in a very competitive and rapidly changing environment and new risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this Annual Report on Form 10-K may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

The forward-looking statements included in this Annual Report on Form 10-K are made only as of the date of this report. You should not rely upon forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that the future results, levels of activity, performance or events and circumstances reflected in the forward-looking statements will be achieved or occur. Moreover, neither we nor any other person assumes responsibility for the accuracy and completeness of the forward-looking statements. We undertake no obligation to update publicly any forward-looking statements for any reason after the date of this Annual Report on Form 10-K to conform these statements to actual results or to changes in our expectations.

The market data and certain other statistical information used throughout this Annual Report on Form 10-K are based on independent industry publications, governmental publications, reports by market research firms or other independent sources that we believe to be reliable sources. Some data are also based on our good faith estimates. Industry publications and third party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. We are responsible for all of the disclosure contained in this Annual Report on Form 10-K, and we believe these industry publications and third party research, surveys and studies are reliable. While we are not aware of any misstatements regarding any third party information presented in this Annual Report on Form 10-K, their estimates, in particular, as they relate to projections, involve numerous assumptions, are subject to risks and uncertainties and are subject to change based on various factors, including those described in Part I, Item 1A “Risk Factors” in this Annual Report on Form 10-K.

Investors and others should note that we may announce material business and financial information to our investors using our investor relations website (ir.908devices.com), our filings with the Securities and Exchange Commission, or SEC, webcasts, press releases, and conference calls. We use these mediums, including our website, to communicate with investors and the general public about our company, our products, and other issues. It is possible that the information that we make available on our website may be deemed to be material information. We therefore encourage investors and others interested in our company to review the information that we make available on our website.

2

SUMMARY OF RISK FACTORS

The following is a summary of the principal risks described below in Part I, Item 1A “Risk Factors” in this Annual Report on Form 10-K. We believe that the risks described in the “Risk Factors” section are material to investors, but other factors not presently known to us or that we currently believe are immaterial may also adversely affect us. The following summary should not be considered an exhaustive summary of the material risks facing us, and it should be read in conjunction with the “Risk Factors” section and the other information contained in this Annual Report on Form 10-K.

Risks related to macroeconomic conditions

| • | Uncertainties in global economic conditions or a decline in economic conditions, such as recession, economic downturn, and/or inflationary conditions in the U.S. and other regions of the world in which we do business could impact customer spending patterns and materially and adversely affect our financial condition and operating results. |

| • | A pandemic, epidemic or outbreak of an infectious disease in the United States such as the COVID 19 pandemic may adversely affect our business. |

Risks related to our business and industry

| • | We have a history of net losses and may not be able to achieve profitability for any period in the future or sustain cash flow from operating activities. |

| • | Our operating results may fluctuate significantly from period-to-period and may fall below expectations in any particular period, which could adversely affect the market price of our common stock. |

| • | We have experienced growth of our business in recent years, and our inability to manage this growth could have a material adverse effect on our business, the quality of our products and services and our ability to retain key personnel. |

| • | We must develop new products, as well as enhancements to existing products, and adapt to rapid and significant technological change to remain competitive. |

| • | We need to continue to build and develop our sales, marketing and customer service organization, and to engage with domestic and international channel partners to support our planned growth. |

| • | We face intense and growing competition from leading technology companies as well as from emerging companies. Our inability to compete effectively with any or all of these competitors could affect our ability to achieve our anticipated market penetration and achieve or sustain profitability. |

| • | Currently, we derive the majority of our revenue from our handheld products in the field forensics market, and are seeking to grow the revenue we derive from our desktop products in the life science market. If we fail to maintain significant market acceptance in existing markets or fail to successfully increase our penetration in new and expanding markets, we will not generate expected revenue growth and our prospects may be harmed. |

| • | Our sales cycles can be long and unpredictable, and our sales efforts require considerable time and expense, which contribute to the unpredictability and variability of our financial performance and may adversely affect our profitability. |

| • | We may need additional capital in the future, which may not be available to us, and if it is available, may dilute your ownership of our common stock and have a material adverse effect on our business, operating results and financial condition. |

| • | If we experience a significant disruption in our information technology systems or breaches of data security, our business could be adversely affected. |

3

Risks related to sales of products to the U.S. Government

| • | A significant portion of our business depends on sales to the public sector, and our failure to receive and maintain government contracts or changes in the contracting or fiscal policies of the public sector could have a material adverse effect on our business. |

| • | U.S. government programs are limited by budgetary constraints and political considerations and are subject to uncertain future funding levels that could result in the termination of programs. |

Risks related to litigation and our intellectual property

| • | We rely on in-bound licenses granted to us from third parties. If we lose these rights, our business may be materially adversely affected, our ability to develop improvements to our existing products and to develop new products may be negatively and substantially impacted, and if disputes arise, we may be subjected to future litigation as well as the potential loss of or limitations on our ability to develop and commercialize products and technology covered by these license agreements. |

Risks related to ownership of our common stock

| • | If securities or industry analysts do not publish research or reports about our business or if they issue unfavorable commentary or downgrade our common stock, the price of our common stock could decline. |

| • | The market price of our common stock has been volatile and could continue to be volatile. |

| • | Our actual operating results may differ significantly from any operating guidance we may provide. |

| • | Sales of a significant number of shares of our common stock in the public markets, or the perception that such sales could occur, could depress the market price of our common stock. |

4

PART I

Except where the context otherwise requires or where otherwise indicated, the terms “908 Devices,” “we,” “us,” “our,” “our company,” “the company,” and “our business” refer to 908 Devices Inc. and its consolidated subsidiaries.

Item 1. Business.

Analysis at the Speed of Life

We are making revolutionizing chemical and biochemical analysis simple, smart and speedy with our purpose-built handheld and desktop devices that empower people to take swift action in life-altering applications.

Company Overview

We have developed an innovative suite of purpose-built handheld and desktop devices for the point-of-need chemical and biochemical analysis. Leveraging our proprietary mass spectrometry, or Mass Spec, microfluidics, and analytics and machine learning technologies, we make devices that are significantly smaller and more accessible than conventional laboratory instruments. Our devices are used at the point-of-need to interrogate unknown and invisible materials and provide quick, actionable answers to directly address some of the most critical problems in life sciences research, bioprocessing, pharma/biopharma, forensics and adjacent markets. The term “products” or “devices” used in this “Business” section each refer to the MX908, Rebel, ZipChip Interface, Maverick, and Maven and related sampling devices.

We create simplified measurement devices that our customers can use as accurate tools where-and-when their work needs to be done, rather than overly complex and centralized analytical instrumentation. We believe the insights and answers our devices provide accelerate workflows, reduce costs, and offer transformational opportunities for our end users.

Since the launch of our first device, we have sold more than 2,800 handheld and desktop devices to over 700 customers in 56 countries, including all 20 of the top 20 pharmaceutical companies by revenue, as well as numerous domestic and foreign government agencies and leading academic institutions.

Our current products are available for both battery-powered handheld and desktop applications.

Front-line workers rely upon our handheld devices to combat the opioid crisis and detect counterfeit pharmaceuticals and illicit materials in the air or on surfaces at levels 1,000 times below their lethal dose. Our desktop devices are accelerating development and production of biotherapeutics by identifying and quantifying extracellular species in bioprocessing critical to cell health and productivity. They sit alongside or are directly connected to bioreactors and fermenters producing drug candidates, functional proteins, cell and gene therapies, and synthetic biology derived products. We believe the insights and answers our devices provide accelerate workflows, reduce costs, and offer transformational opportunities for our end users.

Mass Spec is the gold-standard analytical technology for laboratory-based molecular analysis and can identify and quantify sample components via molecular weight measurements. Mass Spec is highly regarded for its ability to provide an extraordinarily detailed analysis of a wide variety of samples -- from small molecules to large complex proteins. While Mass Spec is an extremely powerful analytical tool, conventional Mass Spec instruments are very large, expensive, and highly complex, which has profoundly bottlenecked market opportunities and relegated them to the equivalent of mainframe computers in central facilities. We are reimagining where Mass Spec technology can be used if it is sufficiently small in size, low in cost, and simple to operate.

Our proprietary Mass Spec platform relies on extreme miniaturization of the core of Mass Spec -- the ion trap and its vacuum system. Using semiconductor microfabrication techniques, we design and produce components that are more than a thousand-fold smaller in volume when compared with most laboratory Mass Spec instruments and costs only

5

dollars to manufacture. The vacuum system alone in a typical laboratory instrument weighs hundreds of pounds and requires several hundred watts of power, 24 hours per day, 365 days per year. Our miniaturized vacuum system weighs less than a pound, and our Mass Spec in total requires less power than a 20-watt LED light bulb. These landmark proprietary advances have enabled the first truly handheld Mass Spec devices and compact desktops.

Sample preparation and separation can be a painfully slow hours-long process, and we have invested heavily in the development of microfluidic sample preparation and microscale separation technologies to reduce preparation and separation time from hours to minutes. The size of a business card, our microfluidic capillary-electrophoresis, or CE, chip has demonstrated world-class performance and speed in separating everything from small molecules such as metabolites and drugs, to biopharmaceutical proteins, antibodies, and oligonucleotides.

With our acquisition of Trace Analytics GmbH, renamed 908 Devices GmbH, in August 2022, we obtained microfluidic aseptic sampling technology that enables on-line automated monitoring and control in bioprocess applications. This validated technology provides cell-free and sterile bioreactor sampling with no volume or prep required. We expect this technology to serve as the interface for future on-line devices, those directly connected to a bioreactor.

Lastly, it is imperative that a point-of-need solution is operable by the widest possible user base. We have an industry-leading software automation and machine learning team comprised of eleven members, each with advanced scientific degrees, who have collective experience working on 30 commercial product launches and have won numerous research and innovation awards. They have applied advanced software automation and machine learning techniques to both control the hardware in our devices and interpret the incredibly rich and complex data streaming off of them. Our team can provide answers immediately to maximize value to the customer in critical-to-life applications where minutes matter.

Our team applied its deep expertise in data analytics, machine learning and optical spectroscopy to develop a proprietary modeling approach that automatically processes Raman spectra from a wide variety of mammalian cell culture media types and cell lines. This proprietary modeling approach powers our Maverick desktop device. Introduced in 2023, Maverick offers bioprocess scientists easy-to-integrate in-line analysis and control without the need for substantial expert configuration or setup.

We fundamentally believe that the technology platform we have built and the investments we are making will allow people to answer chemical and biochemical questions in times and places that were previously inconceivable. Given the market opportunity, we expect to face substantial competition from large established manufacturers of laboratory-based instruments and from new entrants; however, our proprietary advances have enabled us to manufacture the first truly handheld Mass Spec devices and compact desktops and we believe we are well-positioned to face future competition.

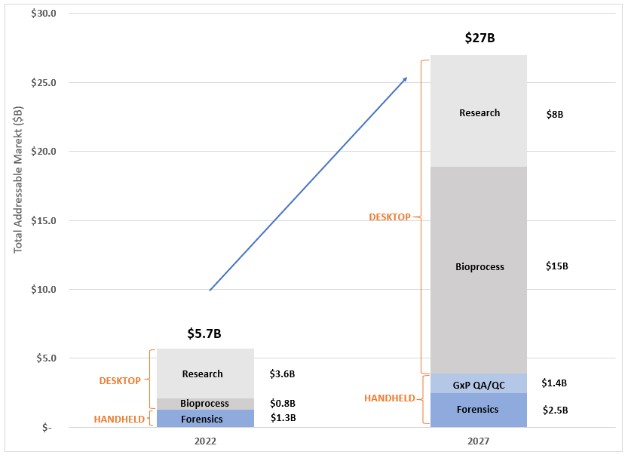

We believe our technology platform can expand in future opportunities far beyond the conventional central laboratory market for Mass Spec and associated front-end separations. We estimate our total addressable market, or TAM, for our devices was $5.7 billion in 2022 and is growing to an estimated $27 billion by 2027. The TAM for our handhelds was estimated to be $1.3 billion in 2022 with expansion to over $3.9 billion with software application extensions for GxP cleaning validation, and other related quality control assays by 2027. Our desktop devices supporting bioprocess development represented an estimated TAM of $0.8 billion in 2022 expanding significantly to approximately $15 billion with execution of our roadmap and the rapid growth of cell therapy by 2027. We see additional opportunity to service the estimated TAM of $3.6 billion in 2022 across the research chromatography market space growing to more than $8.1 billion with further market growth and roadmap expansion into complex metabolomics and proteomics by 2027. Our estimates of our TAM are based on potential customer research and development spending, addressable aspects of potential customers’ end product development process, and potential platform usage. We also utilize estimated penetration and placement rates for our platform with potential customers in our target markets and historical patterns for consumables usage.

6

Our Strengths

We believe the following competitive strengths provide us the ability to address point-of-need applications in forensics, life sciences research, bioprocessing, quality assurance/quality control, and synthetic biology:

| ● | Our proprietary microscale Mass Spec platform leverages well established, gold-standard technology. Mass Spec is already ubiquitous in the laboratory. Users do not need to take a risk on a completely unknown technology. We bring laboratory-grade capability to handhelds and desktops. We have developed a proprietary Mass Spec platform and approach that allow us to move the capabilities of conventional Mass Spec beyond the central laboratory. Our proprietary High-Pressure Mass Spec, or HPMS, technology enables us to produce significantly smaller, purpose-built Mass Spec devices that are better suited for use in point-of-need settings, in contrast to conventional mainframe Mass Spec solutions. The combination of HPMS, our proprietary microfluidic sampling and separation technology, and our data analytics, and machine-learning technology provides the foundations of an adaptable platform that can serve a growing number of new and adjacent applications and markets. |

| ● | Point-of-need technologies disrupting Mass Spec and creating new product categories. Leveraging our Mass Spec platform, we have developed a portfolio of desktop and handheld devices that are reinventing the Mass Spec industry by accessing a variety of point-of-need market segments that were historically considered impossible for conventional Mass Spec manufacturers. Our products are small, purpose-built devices that avoid the typical size and complexity issues related to conventional Mass Spec while also offering real-time, actionable answers to new classes of users. As we continue to expand the capabilities of our Mass Spec platform, we believe our devices will continue to penetrate new and adjacent opportunities in life sciences, quality assurance and control, diagnostics and applied markets. |

| ● | Highly attractive business model validated by rapidly growing installed base of devices.We have over 700 customers, including all 20 of the top 20 pharmaceutical companies by revenue, academic and major government institutions, including the Department of Homeland Security, the U.S. Army and the U.S. Air Force and other international, federal and state agencies. These customers have validated our platform through the collective purchase of more than 2,800 devices, with more than 14,000 users trained on our devices. As we continue to grow our installed base, we expect to increase our recurring revenue derived from the sale of consumables and support services. |

| ● | Talented team with significant domain expertise. We are a technology driven company that has built vertically integrated capabilities to design, manufacture, and commercialize our products. We are led by a dedicated and highly experienced senior management team with significant industry experience and proven ability to deliver novel products. Each member of our senior management team has more than 20 years of relevant experience. Members of our technical team have been collectively responsible for numerous commercial product launches prior to joining the company, in varying markets such as point-of-care clinical diagnostics, handheld pharmaceutical inspection devices, high-throughput cell culture control systems, autonomous warehouse logistics, motion capture animation, high-volume telecom transmitters and receivers, and consumer wearables. The team possesses deep expertise in Mass Spec, system design and engineering, usability and ergonomics, thermal and mechanical engineering, software development, artificial intelligence, and optical spectroscopy, as well as microfluidics and separations science. We had 71 full-time employees dedicated to research and development as of December 31, 2023. Of these, approximately 40% have advanced degrees in science and engineering. |

7

Our Growth Strategy

We are making chemical and biochemical analysis simple, smart and speedy by incorporating our microscale Mass Spec, microfluidics, and analytics and machine learning technology platform into handheld and desktop devices that provide users with robust answers at the point of need. Our growth strategy includes the following key elements:

| ● | A continued focus on simplicity, speed, convenience and cost increases measurement consumption. We are a technology-driven company with significant core expertise in engineering, hard sciences and data analytics and a proven track record of delivering products that delight our customers by making things easy. We believe a relentless focus on these fundamentals drives consumption of consumables. |

| ● | Drive enterprise adoption in our seeded accounts. We intend to continue to aggressively invest in and support our field applications team to accelerate the development of post-sale partnerships with customers and to drive broader adoption across the organization. We will focus on building upon our track record of leveraging our customers’ success in trials and pilots into enterprise-wide adoption of both devices and consumables. As an example, for our handheld device, it is typical for government organizations to conduct a one week or longer trial prior to purchase to test our technology in their real-world setting. A trial generally results in budgeting for a pilot that can range in size from ten to more than 50 units. During the pilot, we support our customers closely to ensure their success. Data is compiled throughout to assist our customer in making a larger enterprise-wide justification, purchase and deployment. It is our belief that investment pre- and post-sale with prospects that have the potential for enterprise adoption creates a predictable pipeline of opportunity for our devices and their entrenchment as they become the organizational standard for our customers. Enterprise customers range from large government organizations with full fielding potential of more than 1,000 handheld devices to leading biopharma companies with capacity for ten or more desktop devices per site. |

| ● | Grow the installed base through expansion of commercial channels. Since the commercial launch of our first handheld, the installed base of our handheld and desktop devices has grown to more than 2,800 devices in 56 countries. With our handheld and desktop device installations now taking root in the United States, we will focus on expanding our commercial channels to better serve the forensics, life sciences research, bioprocessing, quality assurance/quality control, and synthetic biology markets. We look to expand both our direct channel in the United States and our international reach. We anticipate growing our network of international channel partners focused in regions with a concentrated and rapidly expanding life sciences presence, specifically, Europe, China, Japan, India, and South Korea. We look to have local application and support specialists and sales managers supporting our channel partners. |

| ● | Deepen our footprint in the bioprocessing market. Our desktop devices are designed to accelerate development and enhance production by identifying and quantifying extracellular species critical to cell health and productivity. They sit alongside or are directly connected to bioreactors and fermenters producing drug candidates, functional proteins, cell and gene therapies, and synthetic biology derived products. We look to expand our product line with additional panels, for example focused extracellular panels, and intracellular analysis, such as cellular flux, and pathway analysis. We believe our technology platform can serve as the cornerstone of an integrated “bioprocess brain” by monitoring and managing the comprehensive extracellular environment. |

| ● | Expand our customer-driven pipeline of new point-of-need applications. We will continue to leverage our integrated sample preparation and microfluidic separations platform to expand our pipeline of new, customer-driven point-of-need applications that can be addressed by both our handheld and desktop devices. As our customers continue to prove out new applications in areas such as diagnostics, metabolomics, and proteomics, we will look to incorporate select assays investigated by these customers into our handheld and desktop devices where those form factors can accelerate usage. We have already incorporated a number of customer-driven assays into both MX908 and Rebel and will continue to do so as we believe this will provide us with an expanding list of new point-of-need applications and market opportunities within forensics, life sciences research, bioprocessing, quality assurance/quality control and synthetic biology. In addition, we continue to |

8

| make advancements in our core technologies to drive the evolution of our product portfolio beyond current applications and needs to enter new markets. |

Our Technology

Our Technology Platform

We have developed a core technology platform designed to bring Mass Spec out of the confines of central laboratories and to the point-of-need with high-fidelity handheld and desktop devices. We believe that providing simple, smart, and speedy devices that provide robust answers when and where people need them gives rise to:

| ● | an expanded and more diverse set of users; |

| ● | more frequent measurements; and |

| ● | new use cases that were previously untenable. |

These results are possible as our handheld and desktop devices are designed for extreme convenience and speed, requiring minimal training and maintenance. Our platform is centered around using proprietary microscale Mass Spec and microfluidic technologies to prepare, separate, and characterize species at the molecular level, with integrated machine learning and analytics to automatically provide answers regarding identity, purity, and quantity. The core elements of our technology platform include:

| ● | Our High-Pressure Mass Spec, or HPMS, approach, which enables Mass Spec at the point-of-need; |

| ● | microfluidics enable convenient sample preparations, fast separations, and aseptic sampling; and |

| ● | analytics and machine learning technology, which provides actionable answers versus raw data. |

HPMS Approach Enables Mass Spec at the Point-of-Need

Mass Spec is the gold-standard analytical technique for molecular analysis. This technology is highly regarded for its ability to provide an extraordinarily detailed analysis of a wide variety of molecular samples -- from small molecule chemicals to large complex proteins. Mass Spec instruments identify the components of samples via highly detailed mass-to-charge (m/z) measurements, and in some cases, can quantify those components. Together with its associated front-end separation technologies, Mass Spec can resolve and analyze the most complex of samples with high fidelity.

However, while Mass Spec is an extremely powerful analytical technique, the capabilities of conventional Mass Spec instruments are largely relegated to centralized laboratory settings due to their size, complexity, and high price. Given the inherent limitations of conventional mainframe Mass Spec instruments, we believe there is a compelling opportunity for handheld and compact desktop Mass Spec devices.

A key component of our technology is our proprietary microscale ion trap, which we estimate is 1,000 times smaller than those in conventional laboratory Mass Spec instruments. These microfabricated traps are able to operate a million times closer to atmospheric pressures than conventional Mass Spec instruments. This HPMS approach results in devices with dramatically smaller size and lower cost-of-goods through a reduction of vacuum pump requirements and power consumption, and an overall simplification of the hardware topology.

9

Conventional laboratory Mass Spec | Our Mass Spec |

HPMS allows us to build ultracompact, high-fidelity measurement devices that are purpose-built for specific applications and deployable at the point-of-need. HPMS allows us to circumvent the complexities associated with the conventional and much larger, general-purpose, central laboratory Mass Spec instruments.

Our technology operates at size and cost scales that are multiple orders of magnitude smaller than conventional mainframe laboratory instruments. And while large, expensive, high maintenance vacuum systems have been a historical requirement for Mass Spec, our HPMS approach is capable of running with extreme efficiency on very small, robust, low-cost scroll pumps of our own proprietary designs. Our technology requires significantly less power than a 20-watt light bulb, allowing for up to 100x lower power consumption when compared to a competing product. The flexibility afforded by our approach provides access to existing and new market segments that were previously inconceivable for conventional Mass Spec instruments. We believe the insights and answers our devices provide will accelerate workflows, reduce costs and offer transformational opportunities for our end users.

Microfluidics Enable Convenient Sampling and Fast Separations

Today, most central laboratory Mass Spec instruments are paired with large, complex solid and liquid handling systems for sample preparation and separation. Common examples include liquid chromatography stacks and robotic sample preparation systems. These systems are engineered for general applications and require large quantities of solvents, high level of maintenance, and expertly trained users, leading to higher operating costs.

Our approach integrates proprietary microfluidic sample preparation, separation, and ionization technologies on a single chip that can be produced efficiently at scale using semiconductor microfabrication techniques. These microfluidic chips can be paired with our microscale Mass Spec technology to create devices with extraordinary performance that are accessible and usable at the point-of-need by non-experts.

10

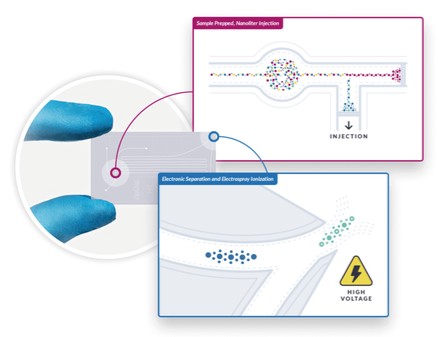

Our integrated microfluidics—sample injection, preparation, separation and electrospray simplified

Our integrated microfluidic chip brings the benefits of:

| ● | highly controlled small sample injections at the nanoliter, or nL, scale; |

| ● | integrated preparation such as desalting; |

| ● | extractions and preconcentration by physical and chemical properties; |

| ● | capillary electrophoresis, or CE, for extremely high-resolution separations of complex samples; and |

| ● | integrated nanoscale electrospray ionization. |

The integrated microfluidic CE can perform extremely high-performance separations of a wide range of molecular species from small molecule metabolites, amino acids, and vitamins, to intact antibodies and other proteins. Importantly for our platform, microfluidic CE is electrically driven and requires no bulky liquid pumping and valving systems. The microfluidic chip consumes only 100-200 nL of electrolyte per minute making it remarkably efficient with source and waste fluids. Microfluidic CE separations can be an order of magnitude or faster than similar chromatography separations. This allows for highly complex separations with high resolution to be completed in minutes.

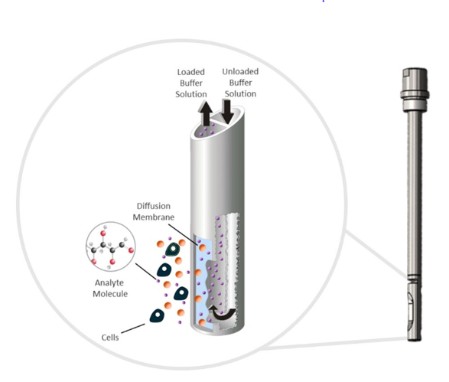

In 2022, we strengthened our core microfluidic technology with the acquisition of Trace Analytics GmbH, which enables us to provide on-line aseptic sampling technology used in bioprocess monitoring and control. Aseptic sampling allows for highly precise, on-line monitoring without any loss of bioreactor volume. A reusable or single-use probe that incorporates a diffusion membrane is inserted in the bioreactor, preserving precious media and product in cell culture and fermentation processes.

Complementing our mass spec analysis, Trace Analytics GmbH also brings to us an enzyme-based electrochemical biosensor technology that generates an electrical signal proportional to concentration of targeted analytes enabling real-time monitoring and control of additional analytes, some of which are difficult to measure with mass spec (e.g., glucose and lactate).

11

Aseptic sampling enables on-line automated monitoring and control of bioprocesses.

Aseptic sampling provides many benefits, including cell-free, sterile and safe sampling with no loss of volume or prep required, thereby saving operator time and reducing lab costs. We expect our microfluidic aseptic sampling to serve as the interface for future on-line mass spec based devices.

Analytics and Machine Learning Technology Provide Actionable Answers, Not Just Raw Data

The third crucial element of our technology platform is holistic device design with embedded analytics and machine learning. Our development team designs devices for a specific purpose, rather than for a wide scope of often disparate needs. Conventional Mass Spec manufacturers focus their attention on canonical analytical specifications such as “instrument resolution” or “detection limit” or “data rate” in the hopes of appealing to a wide range of laboratory specialist needs. Our devices are designed to do a job quickly, easily, and cost effectively. Achieving that aim requires very sophisticated autonomous and adaptive control systems and the machine learning engine to interpret the data and produce a clear, accurate result.

Our devices are designed to provide fast, statistically rigorous answers by providing autonomous control systems and applying rigorous machine learning methods.

12

Control/optimization: Conventional Mass Spec configuration and tuning is highly complex. Our devices need to manage themselves autonomously for maximum value to the customer. They can manage themselves by adapting to environmental factors like elevation, humidity, temperature, and vibration, and by optimizing themselves for the analytical objectives of the user, such as looking for traces of potent drug substances or sniffing for airborne hazards. This ability to automatically control the system reduces or eliminates the user’s responsibility and opportunity for error in set up, optimization, and troubleshooting. Our product’s screen shown above right looks very simple, but the embedded analytics and machine learning system controls and optimizes more than a hundred parameters continuously in real-time.

Machine learning/embedded analytics: The integrated analysis of our platform’s data is also critical to our customers’ success. Conventional platforms may give the user basic tools to view data, and some limited analysis functionality, but they fall far short of completing the analysis loop. “Out of the box” machine and statistical learning methods are not really applicable to complex analytical sensor data and real-life molecular systems. Our data team has a commercial track record of embedding a “scientist in the box” with highly customized statistical and machine learning methods for our platforms to complete the customer experience. Several examples of these elements are highlighted below in the “Our Products” section.

Our Products

We were founded on a vision to deliver high quality Mass Spec to a broad set of users at the point-of-need. We offer handheld and desktop devices, each of which are capable of providing quick, high-fidelity and actionable results. These aspects are important to our customers, who previously have had to choose between a slow and thorough analysis by Mass Spec in a laboratory or a point-of-need result that may have been more timely, but provided only a partial measurement picture prone to false-positives. For instance, forensics customers who do not have access to laboratory-based Mass Spec instruments have at best had access to the field techniques of Ion-mobility spectrometry and Raman/FTIR spectroscopy, each with its own limitation of specificity (ability to distinguish one chemical from another) and sensitivity (ability to detect minute amounts), respectively. Our bioprocess customers have likewise only had access to a cropped measurement picture by largely relying on simple enzymatic and electrochemical sensors that can measure just a few simple gases and other analytes with poor accuracy. Our devices are changing this paradigm and providing laboratory-like results at the point-of-need.

The 908 Devices suite of devices includes (from left to right): MX908, ZipChip, Rebel, Maven and Maverick.

13

MX908

Launched in June 2017, MX908 is a handheld, battery-powered, Mass Spec device designed for rapid analysis of solid, liquid, vapor and aerosol materials of unknown identity. It is an agile, multi-purpose device utilized by a wide spectrum of user segments for a variety of forensic field applications such as chemical, explosive, priority drug and HazMat operations, detecting materials at the trace level.

We have sold 2,422 MX908s into every U.S. state, in 56 countries and across five continents. More than 10,000 operators, including in numerous domestic and foreign government agencies, have been trained to use the MX908.

When a civilian or military first responder, customs agent, or front-line worker is presented with residue on a package, a powder in the emergency room, pills at a border crossing, an apparent overdosing individual, or a mass casualty event, immediate actionable information is needed. The U.S. opioid crisis in particular is driving demand for broadly capable point-of-need measurement devices that can detect a multitude of hazards at trace quantities.

The MX908 detects trace quantities of more than 160 named dangerous materials, including fentanyl and its many derivatives, explosives, and hazardous chemical agents with sensitivity comparable to existing field-based technologies, but with much higher specificity. This allows users to conduct rapid field analysis for a broad range of unknown substances at trace levels that would typically lead to confusion and false positives in other instruments. The device is also able to identify a far greater number of substances than other trace technologies and with one million times the dynamic range of those other handheld or mobile technologies. Compared to a leading transportable Mass Spec product, the MX908 is up to 15x faster, up to 10x smaller and up to 2x cheaper. The MX908 is able to start up in less than a minute, completing analysis of gas and vapor materials in less than ten seconds, and solids, liquids, and aerosols in less than a minute.

The MX908 was designed to operate in harsh outdoor environments such as pervasive rain and dust, and scorching to freezing temperatures in a nimble 4.3 kg (approximately 10 lb) handheld form factor. Our systems also undergo extensive mechanical shock, drop, vibration, and environmental testing as part of the development and certification process.

Designed with the non-technical user in mind, the user interface on the MX908 requires no Mass Spec knowledge for navigation, operation or interpretation of results. The MX908 user interface is very mission driven. These mission modes provide a categorization of functionality, allow the device to guide operators through proper procedures with visual cues, and present results in a manner most relevant for that operational intent. The mission modes also allow the software to optimize the hardware operation of the MX908 to maximize sensitivity and specificity for a given class of chemicals, much as a laboratory chemist would do by changing the settings on their conventional Mass Spec.

The MX908’s machine-learning software, enabled by our proprietary technology platform, serves as a critical element of the device. For example, one of the challenges associated with analyzing fentanyl derivatives is that there are potentially thousands of pharmacologically-active variants for this same compound. However, MX908 is pre-programmed to evaluate against the dozen most common fentanyl variants and is then able to utilize a machine learning classifier to look for characteristic mass fragment loss patterns that are suggestive of the more than 2,000 fentanyl analogs.

Since introducing the MX908, we have continued to expand the device’s capability through mission add-ons such as offering an Aerosol Module accessory to detect and identify aerosolized chemical hazards, adding targets to allow responders to identify additional priority drug substances, and providing a Bluetooth capability that enables seamless data transfer and accelerates support in the field. We recently added the MX908 Beacon accessory, which is a remote area monitoring system secured in a rugged case that can detect and identify aerosolized and vapor threats. The MX908 Beacon accessory leverages the MX908 and Aerosol Module combined with a cloud-based solution to enable remote identification of toxic chemical hazards. All these added capabilities are aimed to address gaps in responders’ workflows, increase engagement, and drive utilization.

14

We have a roadmap to continue to expand the MX908’s mission add-ons to support the detection of adulterated and counterfeit pharmaceuticals and to develop applications in quality control and quality assurance, including GxP cleaning validation.

Rebel

The Rebel is a small desktop analyzer providing real-time information on the extracellular environment in bioprocesses. Compared to a traditional central laboratory high-performance liquid chromatography, or HPLC, Mass Spec assay, Rebel’s price per sample is up to 10 times lower, at approximately one-third of the capital cost, and delivers answers up to 2,000 times faster. Rebel provides results within seven minutes, enabling critical on-the-spot decisions regarding bioprocess media optimization, accelerating process-development cycles and maximizing bioreactor efficiency. Customers are using Rebel in environments subject to U.S. Food and Drug Administration, or FDA, and other regulatory guidelines regarding biological and pharmaceutical product quality, or GxP environments, to evaluate fresh media for conformity to standards, track the extracellular environment and metabolic flux during growth cycles, monitor performance during stress experiments, and characterize spent media.

Since the launch of the Rebel in November 2019, we have sold 165 units and 52 of those units have been placed with the top-20 pharmaceutical companies by revenue and 25 organizations have purchased multiple units. Our focus has been on increasing U.S. placements, but we also have a meaningful international opportunity and have sold Rebels in China, Japan, South Korea and Europe.

Cells have been harnessed to serve as microscopic factories producing myriad molecular species large and small. The markets for cellular-derived products include therapeutics, including cell therapy and personalized medicine, new and sustainable foods and beverages, and industrial materials. Many of these products, such as protein-based therapeutics, can only be economically produced by cells in a bioreactor. Making these products in an efficient and reproducible way remains a challenge to our customers in bioprocessing. Cell culture media forms the critical growth environment for the cell. Our customers’ measurement of this extracellular environment in bioprocesses is critical to their development and operational efficiency.

However, it is rare that researchers conducting these types of experiments have analytical tools for extracellular media characterization on their local bench, which means samples need to be frozen, packaged, and transported to core laboratories for analysis with large HPLC Mass Spec instruments. This adds substantial delays and cost and typically takes three to six weeks to produce lab reports equivalent to those produced by the Rebel in only 15 minutes.

Rebel is currently configured to report concentrations of 33 critical extracellular metabolites in cell culture media, such as amino acids, vitamins, and biogenic amines, which are known to substantially affect the growth profile and properties of the resulting biological entities and their expressed materials. Incorporating our microfluidic sample handling and CE technology, as well as our microscale Mass Spec technology, Rebel’s internal autosampler is capable of queueing approximately 96 such samples for unattended analysis and delivering reported concentrations for each sample.

A fit-for-purpose at-line system, the Rebel is designed to be located within the same laboratory as a bioreactor, enabling more frequent monitoring of key cell media parameters. To run this analysis, the Rebel requires as little as one microliter of cell culture media with little sample preparation. This allows customers to run more tests while preserving precious cell culture media, which is extremely valuable for small batches as used in cell therapy and personalized medicine.

The Rebel, using its onboard algorithms, eliminates the need for manual calibration and delivers processed and actionable results in real-time. As runs are completed, users can access the report either as a PDF print out or a laboratory information system compatible file exported to the network. The Rebel software is compliant for operation in GxP environments.

15

Maverick

The Maverick, launched in September 2023 to complement our Mass Spec technology, is an optical in-line analyzer that provides real-time monitoring and control of multiple bioprocess parameters, including glucose, lactate and total biomass, in mammalian cell cultures. The device also provides rich process fingerprint data to support large-scale efforts in predictive bioprocess modeling.

The Maverick utilizes Raman spectroscopy, a largely non-invasive and non-destructive technology that provides rich, chemical data. The use of Raman spectroscopy for characterizing critical process parameters, or CPPs, and critical quality attributes, or CQAs, in bioprocessing has grown considerably during the last 10 years.

Unlike conventional spectroscopic methods that utilize a multivariate empirical calibration approach requiring expert configuration, Maverick requires no complex modeling and can be set up in minutes. We have developed a proprietary approach that we refer to as the de novo model, which means “from the beginning.” Maverick’s purpose-built de novo model automatically processes Raman spectra from a wide variety of cell culture media types and cell lines, thereby delivering actionable process parameters or direct process control actions. We also provide open access to the raw spectral data enabling spectroscopic experts to extend the device’s capabilities for more advanced predictive control of CPPs and CQAs.

The Maverick hub can monitor up to six bioreactor models simultaneously, with independent analog/digital control of feed systems for each. Remote, real-time web access to bioreactor status and settings is also supported through the Maverick hub. As a spectroscopic-based device, Maverick is extensible to other analytes and parameters.

Maverick enables biopharmaceutical process development scientists and manufacturers to enhance understanding of their process and implement dynamic control strategies more quickly and easily, which can accelerate workflows and improve process efficiency.

Maven and Trace C2

The Maven, launched in January 2023, to complement our Mass Spec technology, is our first on-line device for bioprocess monitoring and control. Connecting directly to a single bioreactor, Maven provides real-time continuous monitoring and control of glucose and lactate in cell culture and fermentation processes. Glucose and lactate are critical parameters that biopharmaceutical process development scientists must monitor to ensure optimal cell viability and to improve product yield, quality, efficacy and safety. Taking measurements as frequently as every two minutes, Maven operates without having to manually draw samples out of the bioreactor due to its aseptic sampling probe. This approach preserves precious media and product and reduces the risk of cell culture contamination. Maven precisely monitors nutrient and metabolite concentrations at low levels—0.01 g/L of glucose and 0.05 g/L of lactate. This is especially beneficial in cell therapy applications where tight control of cell culture conditions is vital.

In addition to providing real-time measurements, Maven comes with integrated proportional-integral-derivative, or PID, and on/off controllers that enable out-of-the-box feeding automation. The Maven is Good Manufacturing Practices, or GMP, compliant, takes up a small footprint, and in keeping with our focus on simplicity, is easy to use. Maven can be used in concert with our at-line Rebel device, which quantitates over 30 analytes, to improve and optimize cell culture feeding strategies.

The Trace C2 provides on-line monitoring of methanol or ethanol and control of substrate feeding in fermentation processes. Integrated into the device is an aseptic sampling probe that enables sampling with no loss of bioreactor volume and no increased risk of process contamination. The device includes a dedicated on-board peristaltic pump and an integrated PID controller that can be used for feeding substrates without any additional auxiliary equipment. The Trace C2 and related sampling products were developed by Trace Analytics GmbH, which we acquired in August of 2022.

16

ZipChip

Our ZipChip solution is a plug-and-play, high-resolution separation platform that optimizes Mass Spec sample analysis. Our ZipChip platform consists of a ZipChip Interface, which is installed into a conventional Mass Spec instrument, and consumable microfluidic chips, or ZipChips. We designed this technology to be compatible with third party Mass Spec instruments. Powered by our integrated microfluidic technology, the ZipChip platform allows researchers to consolidate a host of time-consuming biotherapeutic, metabolomic, and proteomic applications typically run on multiple instruments or configurations onto a single platform. With ZipChip, researchers can switch applications in minutes, instead of hours typical with an alternative such as liquid chromatography.

Since launch of the ZipChip platform in March 2016, we have sold 234 ZipChip Interfaces and have established 28 multi-unit accounts in leading, global pharmaceutical organizations and academic institutions. Our ZipChip platform is compatible with market-leading conventional Mass Spec instruments found in laboratories worldwide.

As an open-access discovery platform that can interface with more than 10,000 conventional Mass Spec instruments, ZipChip provides us the ability to leverage the growing list of newly established applications and publications from customers who have incorporated the device into their projects. By incorporating select assays investigated on the ZipChip by customers into our MX908 and Rebel devices, we can create an evolving pipeline of new customer-driven, point-of-need Mass Spec applications as the scope of analytes our devices can detect and analyze will continue to expand. We have already incorporated a number of the customer-driven assays in our MX908 and Rebel devices, and we are investigating several more for our future product pipeline.

Consumables and Services

Handheld Device

Our MX908 comes with a standard warranty for up to one year from purchase. Our customers also can purchase extended warranty service plans, which include hardware repair and replacement coverage, technical support, and software updates. We designed the MX908 to be intuitive and easy-to-use, as it is critical to our customers to know that the MX908 is operating as intended. The annual and extended warranty service plans provide the customer the ability to contact us to assist in validating their results given the severity and context of the situations in which our devices operate. Our technical support, also known as our Reachback program, allows any participating MX908 user to email, text, or call a 908 Devices Scientific Support Team member to receive support 24 hours per day, 365 days per year to ensure the MX908 is working as intended. The Scientific Support Team is staffed by M.Sc. and Ph.D. chemists and forensic scientists expert in the operation of the MX908 and other field analytical technologies. Our extended warranty service plans are sold with multiyear commitments, which allows us to deepen our relationship with customers and provides us with an upfront payment, a predictable recurring revenue stream, and an opportunity to offer additional future services.

For simplicity and convenience, we also sell single-use swab samplers for the analysis of liquid and solid materials. These swab samplers are most heavily used today by customers who are evaluating drug substances. However, we designed the MX908 so that it does not require swab samplers or any other consumables for a number of other applications. Our customers value the low-logistics tail of our MX908.

Desktop Devices

Annual and extended warranty and service plans are available for the Rebel, Maven, Maverick, ZipChip Interface, and Trace C2 devices.

Rebel’s operation requires a consumable kit that includes a microfluidic and separation chip, electrolytes, and performance qualification and calibration standards. Currently, customers of Rebel who are actively utilizing the device are consuming on average approximately half of a 200-sample kit per month. With continuous operation, the Rebel is capable of consuming approximately one 200-sample kit a day.

17

We also offer an annual certification kit for the Rebel. The certification kit is shipped to the customer, who loads the provided samples, and executes a certification protocol. The system is remotely qualified and certified based on the data acquired meeting factory specifications.

Calibration kits are required for the Maverick.

We offer a variety of kits for the ZipChip Interface that include microfluidic ZipChips and different reagents optimized for a wide scope of applications. These kits include intact antibody, charge variance, metabolomics, peptide and oligonucleotides.

Consumable sets of buffers, probes and biosensors are required for the Maven, Trace C2 and related sampling devices.

Market Opportunities

We have developed ultracompact, high-fidelity Mass Spec devices to interrogate the unknown and invisible and provide actionable results in life-altering point-of-need applications. Our first products are purpose-built handheld and desktop Mass Spec devices that currently address a range of applications and markets. We estimate our TAM for our devices was $5.7 billion in 2022, and is growing to an estimated $27 billion by 2027. The TAM for our handhelds was estimated to be $1.3 billion in 2022 with expansion to over $3.9 billion with software application extensions for GxP cleaning validation, and other related quality control assays by 2027. Our desktop devices supporting bioprocess development represented a TAM of $0.8 billion in 2022 expanding significantly to approximately $15 billion with execution of our roadmap and the rapid growth of cell therapy by 2027. We see additional future opportunity to service an estimated TAM of $3.6 billion in 2022 across the laboratory chromatography market space growing to more than $8.1 billion with further market growth and roadmap expansion into metabolomics and complex proteomics by 2027. Our estimates of our TAM are based on potential customer research and development spending, addressable aspects of potential customers’ end product development process, and potential platform usage. We also utilize estimated penetration and placement rates for our platform with potential customers in our target markets and historical patterns for consumables usage.

Our TAM for all device placements in 2022 and expanding in 2027 with product roadmap and market growth

18

Our Initial Market—Field Forensics

Forensic labs have historically used conventional Mass Spec instruments to chemically analyze a diverse array of submitted samples. Testing for controlled substances is one of the major drivers for the use of Mass Spec in the field forensics setting.

In the field forensics setting, high accuracy and fidelity can be just as important at the point-of-need as it is in the laboratory. Simple and inexpensive colorimetric tests are being abandoned in many jurisdictions due to their extremely narrow and poor performance capabilities, in favor of handheld technologies with broad lab-like capabilities. This is creating an expanded market of individual users that is a multiple of the centralized laboratory Mass Spec instrument market.

The need for such field technologies is acute for controlled substances and identification of other priority chemicals and hazards at trace levels. The toxicity of fentanyl and its analogs is 100 to 10,000 times the potency of morphine, creating an opioid crisis of unprecedented scale and breadth.

Fentanyl is considered to be the deadliest drug threat facing the United States today, according to the U.S. Drug Enforcement Administration, or DEA. The DEA also seized more than 77 million fentanyl-laced fake prescription pills in 2023, up from 50.6 million such pills in 2021. DEA laboratory testing also showed that seven out of ten pills tested contained a potentially deadly dose of fentanyl, an increase from four out of ten pills in 2021 and six out of ten pills in 2022. In addition, in March 2023, the DEA issued its third public safety alert in just three years warning the American public of a sharp increase in pills containing fentanyl mixed with xylazine, a powerful sedative that the U.S. Food and Drug Administration approved for veterinary use. The alert noted that xylazine and fentanyl drug mixtures place users at a higher risk of suffering a fatal drug poisoning.

The potency and diversity of these emerging classes pose a major challenge for point-of-need measurements. Near invisible quantities of opioids can be fatal, and street drugs are often heavily obscured with filler materials, making trace detection with high-fidelity technologies an imperative for success. The diversity of the problem also drives the need for agility with devices that can be rapidly updated in the field with new machine learning updates. There are thousands of variants of these highly potent opioids, and other emerging classes such as cathinones and cannabinoids that will further exacerbate the problem.

In addition to controlled substances, point-of-need Mass Spec instruments can address a wide variety of other use cases, including:

| ● | first responders and local, state, and federal law enforcement; |

| ● | U.S. and international defense and homeland security; |

| ● | forensic laboratories’ case management and triage; |

| ● | package inspection for postal services, couriers, customs agencies, and corporate mail rooms; |

| ● | facility safety for hotels, local, state and federal government facilities, and private enterprises; and |

| ● | quality assurance and control. |

We estimate that the TAM for our handhelds was $1.3 billion per year in 2022 for trace detection of drugs, explosives, priority chemicals, and other hazards on surfaces and in the air. Our TAM expands to $3.9 billion with software application extensions for GxP cleaning validation, and other related quality control assays.

19

Life Sciences

Mass Spec addresses a significant number of applications along the life sciences research and biopharma value chain. It is integral in research and discovery, drug development, product validation and quality control. Biologic therapeutic modalities and all cell-based products more broadly, use bioreactors to manufacture product in two stages – process development and clinical and GxP manufacturing.

Within a cell, thousands of intertwined processes govern the cells ability to produce various proteins, its ability to perform a specific function, and its energy and waste expenditure. But efficient intracellular operations are also highly reliant on the extracellular environment – the cell culture media. In bioreactors, the timely influx of raw materials, environmental controls, and management of waste can be not only essential to efficiency, but literally to the life or death of the cells. The worldwide cell culture media market itself was estimated to be a $6.2 billion business in 2023. Regardless of how carefully the starting cell culture media has been designed and selected, bioprocessing is by definition a dynamic and inhomogeneous process. Cellular biology is complicated and unpredictable.

Due to issues with both the existing point-of-need solutions and alternative laboratory-based workflows, development scientists currently lack an ideal solution to accurately analyze the extracellular environment during or after the growth cycle without having to compromise between timing or completeness.

High-pressure Mass Spec combined with microfluidic sampling and separations will allow for significant efficiencies and new applications for these technologies within life sciences. With real-time access to comprehensive media profiles, bioprocess development scientists can:

| ● | accelerate their product development cycles with feedback in minutes rather than weeks; |

| ● | improve process yield and lower costs throughout their value chain; |

| ● | enable a broad range of complex therapeutic modalities in biopharmaceuticals; and |

| ● | increase the probability of successfully developing cell-based products. |

We believe these efficiencies will lead to substantial growth opportunities in biologic-based therapeutics where a better understanding of the extracellular environment is a crucial element of bioprocessing.

For antibody therapeutics, a key requirement is that monoclonal production cell lines not only produce high titers of antibody but with acceptable Critical Quality Attributes, or CQAs. The extracellular media properties can greatly impact both the titer and the CQAs of the produced antibody. Likewise, for cell and gene therapeutics, management of the complex mammalian cell culture system and measurement and control of the extracellular environment is crucial. Historically, bioprocessing has been focused on large-scale batched production of monoclonal antibodies, or mAbs, using genetically stable clones, whose production has largely been optimized over many years of refinement. Today, newer advanced modalities, like cell and gene therapies, are fueling growth in the market while introducing variability of input materials (e.g., patient or donor cells, transient transfected cell lines), higher cost of goods sold, and the necessity for small-batched production – driven by smaller patient populations and the need to scale out. This change is driving manufacturers toward increased monitoring and optimization at a level of intensity beyond what is seen historically.

While mAbs are forecasted to continue to dominate end-product sales over the near term, it is estimated that by 2027 the pipeline of cell and gene therapies will be approximately 7,000 assets, representing more than 50% of the total biologics pipeline. A massive retooling of global bioprocessing capabilities is underway to accommodate the needed small batched production – one per patient in some cases. We estimated our bioprocessing TAM to be $0.8 billion in 2022, across approximately 1,800 sites and 175,000 batches to support process development, and this is expected to expand to approximately $15 billion TAM by 2027 with the execution of our roadmap and the rapid growth of cell therapy.

20

Our product development roadmap for the Rebel platform includes the extension of current capabilities and move to an on-line and, ultimately, a real-time “bioreactor brain”. In process development today, smaller scale bioreactors are outfitted with a variety of disconnected multi-party simple sensors and controllers. With the increasing trend toward highly parallelized systems with many small-scale bioreactors running simultaneously, manual sampling becomes a significant bottleneck. The roadmap expansion of Rebel’s analyte panel to address core culture kinetics (e.g., glucose, lactate, ammonium, pH, dissolved oxygen) and attributes like cell count, and viable cell density means that this future on-line Rebel+ system could have a uniquely comprehensive assessment of the present state and trajectory of the extracellular environment. Historical data profiles across parallel bioreactors and designed experiments form an excellent basis for machine learning and multivariable predictive control to optimize experimental variables to maximize yield, minimize risk of loss, and improve kinetics – the “bioreactor brain”. An outsize portion of this opportunity is driven by testing in autologous cell therapies and is commensurate with the total expected cell batches produced.

Customers

We sell our products worldwide through an experienced direct sales force as well as through domestic and international channel partners. Our customers are primarily in the pharmaceutical and biotech market, the government market and to a lesser extent, the academic market. Primary users of our handheld device include law enforcement, military and civilian first responders, and customs and border protection personnel. Primary users of our desktop devices include process development scientists, process engineers, and research scientists.

Manufacturing and Supply

Our manufacturing strategy has two components: to outsource subassemblies or assemblies to domestic contract manufacturers where it is cost and capital favorable, and to use our internal manufacturing facilities for the balance of our production needs. Our primary in-house manufacturing facilities are located at our headquarters in Boston, Massachusetts. These facilities are ISO 9001:2015 certified and include approximately 5,100 square feet of configurable production assembly floor, 1,800 square feet of advanced machining space, and 2,000 square feet of configurable cleanroom. Inventory is held in our Boston facilities in a 700 square foot controlled-access cage. As a result of the acquisition of Trace Analytics GmbH, we also have in-house manufacturing facilities in Braunschweig, Germany.

Devices

The MX908, Rebel, Maverick and ZipChip Interface are manufactured, tested and shipped from our Boston facility. The Maven and related sampling devices are manufactured, tested and shipped from our Braunschweig facility. Several custom components are fabricated by third party suppliers, including printed circuit boards and cables, and metal and plastic mechanical components. The assembly of technology-sensitive components such as our proprietary vacuum pumps and ion trap/ionization module is completed in-house.

Currently, our Boston manufacturing facility is capable of supporting the production of approximately 2,000 MX908, Rebel, Maverick and ZipChip Interface units combined per year. When our annual sales exceed 2,000 units, we expect that we would need to either expand our in-house production operations, or transfer some or all aspects of assembly to contract manufacturers, to accommodate larger run-rates. We believe there are numerous domestic and international contract manufacturers that could be qualified to produce the MX908, Rebel, Maverick and/or ZipChip Interface when third party demand for our products outpace our current manufacturing capacity. The autosampler subassembly of the Rebel and ZipChip are supplied by a single supplier. The Raman spectrometer, and optical probe and fiber assemblies, for Maverick are supplied by a single supplier. The Maven device subassembly is supplied by a single supplier under a contract manufacturing arrangement.

We are continuously evaluating and updating our supply chain to ensure our ability to respond to customer demand for our products. For example, we have relationships with a number of machine shops and electronics suppliers that can provide components for our devices, including components currently provided by a single source. We plan to continue the diversification of our supply chain as we scale. We use our annual demand planning to assess initial device needs for

21

each year, and we update and reassess those estimates as needed, including with respect to the levels of inventory that we believe will be required to support anticipated customer demand.

Consumables

The MX908 incorporates a number of non-proprietary consumables that are commercial-off-the-shelf available and sourced from a number of reputable suppliers. Sampling swabs that are used for the analysis of liquid and solid materials in the MX908 are currently single-sourced. While we believe that alternatives are available, it would take time to identify and validate replacement swab samples, which could compromise our ability to supply these to our MX908 customers on a timely basis.

Consumable kits for the Rebel and ZipChip Interface include electrolytes, standards, and microfluidic chips. All assay kits and standards are assembled in our Boston cleanroom facilities. Component reagents and standards are widely available from multiple suppliers. Our microfluidic chips are produced and assembled in our Boston cleanroom facilities. The substrate is supplied by a single supplier. While we believe that alternative suppliers would be available, it would take time to identify and qualify alternate suppliers and transfer design requirements to them, which could negatively affect our ability to supply these chips to our Rebel and ZipChip customers on a timely basis.

Sales and Marketing

We distribute our devices and consumables via direct field sales and support organizations located in North America and through a combination of our own sales force and more than 42 third party channel partners in domestic and international markets which include Australia, Canada, China, Czech Republic, Germany, Japan, Saudi Arabia, Singapore, Turkey, and the United Kingdom, or UK. In North America, we use channel partners to provide our products to end customers where a contract vehicle is required. Since the commercial launch of our first handheld, the installed base of our devices has grown to more than 2,800 devices across more than 56 countries.

Our domestic sales force and international partners inform our current and potential customers of current product offerings, new target applications, and advances in our technologies and products. As our primary point of contact in the marketplace, our sales force focuses on delivering a consistent marketing message and high level of customer service, while also attempting to help us better understand the evolving market and customer needs.