UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended: | |

or | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from: to

Commission file number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction | (I.R.S. Employer | |

of incorporation or organization) | Identification No.) |

(Address of principal executive offices) (Zip Code)

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the voting and non-voting stock held by non-affiliates of the registrant was approximately $

The number of shares of the registrant’s common stock outstanding as of March 16, 2023 was

DOCUMENTS INCORPORATED BY REFERENCE

None.

2022 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

| Page | ||

Cautionary Note Regarding Forward Looking Statements and Industry Data | ||||

Risk Factor Summary | ||||

4 | ||||

20 | ||||

38 | ||||

38 | ||||

38 | ||||

38 | ||||

39 | ||||

[Reserved] | 39 | |||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 39 | |||

44 | ||||

44 | ||||

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 45 | |||

45 | ||||

46 | ||||

Disclosure Regarding Foreign Jurisdictions the Prevent Inspections | 46 | |||

46 | ||||

50 | ||||

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 53 | |||

Certain Relationships and Related Transactions, and Director Independence | 54 | |||

55 | ||||

56 | ||||

57 | ||||

58 | ||||

In this report, unless otherwise stated or as the context otherwise requires, references to “Semler Scientific,” “the Company,” “we,” “us,” “our” and similar references refer to Semler Scientific, Inc. The Semler Scientific logo, QuantaFlo and other trademarks or service marks of Semler Scientific, Inc. appearing in this report are the property of Semler Scientific, Inc. This report also contains registered marks, trademarks and trade names of other companies. All other trademarks, registered marks and trade names appearing in this report are the property of their respective holders.

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS AND INDUSTRY DATA

This annual report on Form 10-K contains forward-looking statements. Such forward-looking statements include those that express plans, anticipation, intent, contingency, goals, targets or future development and/or otherwise are not statements of historical fact. These forward-looking statements are based on our current expectations and projections about future events and they are subject to risks and uncertainties known and unknown that could cause actual results and developments to differ materially from those expressed or implied in such statements.

In some cases, you can identify forward-looking statements by terminology, such as “expects,” “anticipates,” “intends,” “estimates,” “plans,” “believes,” “seeks,” “may,” “should,” “continue,” “could” or the negative of such terms or other similar expressions. Accordingly, these statements involve estimates, assumptions and uncertainties that could cause actual results to differ materially from those expressed in them. Any forward-looking statements are qualified in their entirety by reference to the factors discussed throughout this annual report on Form 10-K.

You should read this annual report on Form 10-K and the documents that we reference herein and therein and have filed as exhibits, completely and with the understanding that our actual future results may be materially different from what we expect. You should assume that the information appearing in this annual report on Form 10-K is accurate as of the date on the front cover of this annual report only. Because the risk factors referred to herein could cause actual results or outcomes to differ materially from those expressed in any forward-looking statements made by us or on our behalf, you should not place undue reliance on any forward-looking statements. These risks and uncertainties, along with others, are described under the heading “Risk Factors.” Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. New factors emerge from time to time, and it is not possible for us to predict which factors will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We qualify all of the information presented in this annual report on Form 10-K, and particularly our forward-looking statements, by these cautionary statements.

This annual report on Form 10-K includes statistical and other industry and market data that we obtained from industry publications and research, surveys and studies conducted by third parties. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe these industry publications and third-party research, surveys and studies are reliable, we have not independently verified such data.

1

RISK FACTOR SUMMARY

Our business involves significant risks. Below is a summary of the material risks that our business faces, which makes an investment in our common stock speculative and risky. This summary does not address all these risks. These risks are more fully described below under the heading “Risk Factors” in Part I, Item 1A of this annual report on Form 10-K. Before making investment decisions regarding our common stock, you should carefully consider these risks. The occurrence of any of the events or developments described below could have a material adverse effect on our business, results of operations, financial condition, prospects and stock price. In such event, the market price of our common stock could decline, and you could lose all or part of your investment. In addition, there are also additional risks not described below that are either not presently known to us or that we currently deem immaterial, and these additional risks could also materially impair our business, operations or market price of our common stock.

| ● | If we do not successfully implement our business strategy, our business and results of operations will be adversely affected. |

| ● | We predominantly market only one U.S. Food and Drug Administration, or FDA, cleared product, QuantaFlo, a cardiac and vascular testing product, and it may not achieve broad market acceptance or be commercially successful. We may also fail to generate meaningful revenues from our Insulin Insights distribution arrangement, which includes prepaid licenses, or benefit from our recent investments in other companies developing other complementary products. |

| ● | Changes in the regulatory reimbursement landscape, such as the recent “Advance Notice” issued by Centers for Medicare and Medicaid Services, or CMS, could impact the perceived profitability of using our products to aid diagnosis of cardiovascular diseases. |

| ● | Physicians and other customers may not widely adopt our products unless they determine, based on experience, long-term clinical data and published peer reviewed journal articles, that the use of our products provides a safe and effective alternative to other existing devices, including ankle brachial index, or ABI devices. |

| ● | If healthcare providers are unable to obtain adequate coverage and reimbursement either for procedures performed using our product or patient care incorporating the use of our product, it is unlikely that our product will gain widespread acceptance. |

| ● | Our cardiac and vascular testing product is generally but not specifically approved for reimbursement under any third-party payor codes; if third-party payors refuse to reimburse our customers for their use of our product, it could have a material adverse effect on our business. |

| ● | Our business has been and could continue to be adversely affected by the ongoing COVID-19 pandemic. |

| ● | We rely heavily upon the talents of a small number of key personnel, the loss of whom could severely damage our business. |

| ● | We rely on a small number of employees in our direct sales force and face challenges and risk in managing and maintaining our distribution network and the parties who make up that network. |

| ● | To adequately commercialize our products and any new products we add, we may need to increase our sales and marketing network, which will require us to hire, train, retain and supervise employees and other independent contractors. |

| ● | We do not require our customers to enter into long-term licenses or maintenance contracts for our products or services and may therefore lose customers on short notice. |

| ● | We are exposed to risk as a significant portion of our revenues and accounts receivables are with a limited number of customers. |

| ● | We rely on a small number of independent suppliers and facilities for the manufacturing of our cardiac and vascular testing product. Any delay or disruption in the supply of the product or facility may negatively impact our operations. |

| ● | Because we operate in an industry with significant product liability risk, and we may not be sufficiently insured against this risk, we may be subject to substantial claims against our product or services that we may provide. |

| ● | We may implement a product recall or voluntary market withdrawal or stop shipment of our product due to product defects or product enhancements and modifications, which would significantly increase our costs. |

| ● | If we fail to properly manage our anticipated growth, our business could suffer. |

| ● | An information security incident, including a cybersecurity breach, could have a negative impact on our business or reputation. |

2

| ● | Fluctuations in insurance cost and availability could adversely affect our profitability or our risk management profile. |

| ● | We will need to generate significant revenues to remain profitable. |

| ● | Our future financial performance will depend in part on the successful improvements and software updates to our vascular testing product on a cost-effective basis. |

| ● | We operate in an intensely competitive and rapidly changing business environment, and there is a substantial risk our products or service offerings could become obsolete or uncompetitive. |

| ● | One of our business strategies is developing additional products and service offerings that allow healthcare providers to deliver cost-effective wellness and receive increased compensation for their services. The development of new products and service offerings involves time and expense and we may never realize the benefits of this investment. |

| ● | We have used our cash resources to invest in other companies, and there is no guarantee that we will be repaid on maturity nor realize any other expected benefits from such investments, which could harm our business. |

| ● | Our business is subject to many laws and government regulations governing the manufacture and sale of medical devices, including the FDA’s 510(k) clearance process, and laws and regulations governing patient data and information, among others. |

| ● | The FDA may change its policies, adopt additional regulations, or revise existing regulations, in particular relating to the 510(k) clearance process. |

| ● | Our business is subject to unannounced inspections by FDA to determine our compliance with FDA requirements. |

| ● | Although part of our business strategy is based on payment provisions enacted under government healthcare reform, we also face significant uncertainty in the industry regarding the implementation, transformation or repeal and replacement of the Health Care Reform Law. |

| ● | The applicable healthcare fraud and abuse laws and regulations, along with the increased enforcement environment, may lead to an enforcement action targeting us, which could adversely affect our business. |

| ● | Changes in, or interpretations of, tax rules and regulations may adversely affect our effective tax rates. |

| ● | Our ability to use net operating loss, or NOL, carryforwards to offset future taxable income may be subject to limitations. |

| ● | We have had material weaknesses in our internal control over financial reporting. Although we have remedied our prior material weaknesses, if we identify additional material weaknesses in the future, or if our former material weaknesses recur, it could have an adverse effect on our company. |

| ● | Our success largely depends on our ability to obtain and protect the proprietary information on which we base our product. |

| ● | We may need to license intellectual property from third parties, and such licenses may not be available or may not be available on commercially reasonable terms. |

| ● | We may be subject to claims by third parties asserting that our employees or we have misappropriated their intellectual property, or claiming ownership of what we regard as our own intellectual property. |

| ● | If we are unable to protect the confidentiality of our trade secrets, our business and competitive position would be harmed. |

| ● | Our business could be impacted by macroeconomic factors, such as the effects of the Russian invasion of Ukraine on the global economy and supply chain and inflation. |

| ● | Our executive officers, directors and significant stockholders, if they choose to act together, have the ability to significantly influence all matters submitted to stockholders for approval. |

| ● | Provisions in our corporate charter documents and under Delaware law could make an acquisition of our company, which may be beneficial to our stockholders, more difficult and may prevent attempts by our stockholders to replace or remove our current management. |

3

PART I

ITEM 1. BUSINESS

General

We are a company providing technology solutions to improve the clinical effectiveness and efficiency of healthcare providers. Our mission is to develop, manufacture and market innovative products and services that assist our customers in evaluating and treating chronic diseases. Our patented and U.S. Food and Drug Administration, or FDA, cleared product, QuantaFlo, measures arterial blood flow in the extremities to aid in the diagnosis of peripheral arterial disease, or PAD, and serves as an aid to measure hemodynamics related to heart dysfunction.

We have an agreement with Mellitus Health, Inc, or Mellitus, a private company to exclusively market and distribute Insulin Insights, an FDA-cleared software product that recommends optimal insulin dosing for diabetic outpatients in the United States, including Puerto Rico, except for selected accounts.

We have also made cash investments in Mellitus, in Monarch Medical Technology, LLC, or Monarch, a privately-held digital health company whose proprietary product, EndoTool Glucose Management System, or EndoTool, offers a technology-enabled approach to inpatient glycemic management, and in NeuroDiagnostics Inc., a privately-held company that is doing business as SYNAPS Dx, or SYNAPS, whose product, Discern, is a test for early Alzheimer’s disease. We continue to develop additional complementary proprietary products in-house (such as our recently released QuantaFlo extension as an aid to measure hemodynamics related to heart dysfunction), and seek out other arrangements for additional products and services that we believe will bring value to our customers and to our company. We believe our current products and services, and any future products or services that we may offer, position us to provide valuable information to our customer base, which in turn permits them to better guide patient care.

In the year ended December 31, 2022, we had total revenues of $56.7 million and net income of $14.3 million compared to total revenues of $53.0 million and net income of $17.2 million in 2021.

Our Products and Services

We currently market a patented and FDA-cleared, cardiac and vascular testing product, QuantaFlo, to our customers, who include insurance plans, physician groups, risk assessment groups, hospitals and retailers. We also have an exclusive distribution arrangement for the United States, including Puerto Rico, to distribute Insulin Insights, an FDA-cleared, software solution designed to provide insulin dosing recommendations to clinicians for the adjustment and maintenance of blood glucose levels in insulin-dependent patients with Type 2 diabetes. We believe this product will be attractive to our existing customers as well as help expand our customer base.

4

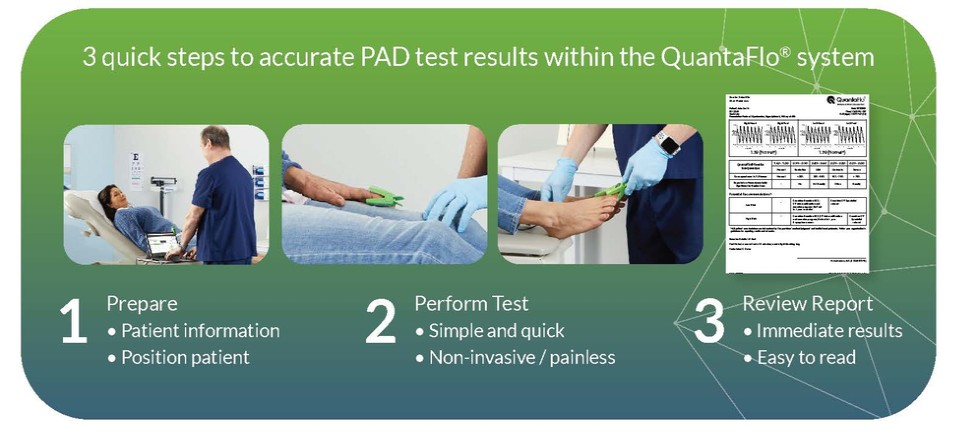

QuantaFlo

QuantaFlo is a four-minute in-office blood flow test. Healthcare providers can use blood flow measurements as part of their examinations of a patient’s vascular condition, including assessments of patients who have vascular disease. The following diagram illustrates the use of QuantaFlo:

QuantaFlo features a sensor clamp that is placed on the toe or finger. Infrared light emitted from the clamp on the dorsal surface of the digit is scattered and reflected by the red blood cells coursing through the area of illumination. Returning light is ‘sensed’ by the sensor. A blood flow waveform is instantaneously constructed by our proprietary software algorithm. Both index fingers and both large toes are interrogated, which takes about 30 seconds for each. The product may be used with provocative maneuvers.

We have primarily developed a license model rather than an outright sales model for QuantaFlo. This license model eliminates the need to make a capital equipment sale. Consequently, we generally require no down payment or long-term commitment from our customers. QuantaFlo has an expected average lifetime of at least three years. To date, we roughly estimate that routine office usage of the QuantaFlo has ranged from a few tests per week up to 10 tests per day. We also offer contracts in which we invoice on a per test basis for use of QuantaFlo. Approximately 62% of our customers are on the fixed-fee software licensing model, whereas 38% are on the variable fee model based on usage.

We have placed our QuantaFlo product with healthcare insurance plans, integrated delivery networks, independent physician groups, hospitals and companies contracting with the healthcare industry such as risk assessment groups and retailers in addition to doctors’ offices. Our two largest customers are U.S. diversified healthcare companies and affiliated plans, and in the year ended December 31, 2022, they accounted for 40.4% and 29.0% of our revenues, respectively, compared to 40.8% and 28.6%, respectively, in the prior year.

5

Other Blood Flow Testing Methods

Blood flow is the amount of blood delivered to a given region per unit time, whereas blood pressure is the force exerted by circulating blood on the walls of arteries. Given a fixed resistance, blood flow and blood pressure are proportional. The ABI with Doppler test uses a blood pressure cuff to measure the systolic blood pressure in the lower legs and in the arms. A blood pressure cuff is inflated proximal to the artery in question. Using a Doppler device, the inflation continues until the pulse in the artery ceases. The blood pressure cuff is then slowly deflated. When the artery’s pulse is re-detected through the Doppler probe the pressure in the cuff at that moment indicates the systolic pressure of that artery. The test is repeated on all four extremities. Well-established criteria for the ratio of the blood pressure in a leg compared to the blood pressure in the arms are used to assess the presence or absence of flow obstruction. Generally, these tests take 15 minutes to perform and require a vascular technician to be done properly. Like QuantaFlo, the traditional analog ABI test with Doppler is a non-invasive physiologic measurement that may be abnormal in the presence of PAD. Alternatively, primary care physicians may palpate the pedal pulses to assess blood flow in the lower extremities. However, pulse palpation is generally not sensitive for the detection of vascular disease. Other options to detect arterial obstructions or hemodynamic problems are imaging systems that use ultrasound, x-ray technology or magnetic resonance to obtain anatomic information about blood vessels in the legs. However, as compared to QuantaFlo, imaging tests are much more expensive, time consuming and are performed by specialists in special laboratories or offices.

Insulin Insights

Insulin Insights is a software program that is used by a healthcare provider to optimize outpatient insulin dosing. In April 2021, we entered into an agreement with Mellitus to exclusively market and distribute this software program in the United States, including Puerto Rico, except for selected accounts. Under this agreement and its December 2022 amendment, we have pre-paid for an aggregate of $2.5 million of licenses ($2.0 million in April 2021 and $0.5 million in December 2022).

We currently are distributing Insulin Insights using a software as a service, or SaaS, license model on a per patient per month fee rather than an outright sales model. We generally require no down payment or long-term commitment from our customers. We intend to reevaluate the price periodically. As we have only recently deployed Insulin Insights with customers, we do not have enough experience with the product to be able estimate routine usage of Insulin Insights in terms of patients per location.

We seek to distribute Insulin Insights to healthcare insurance plans, integrated delivery networks, independent physician groups, and companies that contract with the healthcare industry, such as risk assessment groups, long-term care, or remote patient monitoring organizations, in addition to doctors’ offices. We believe that this software product will be of interest to our existing customer base, as well as help us to expand interest in QuantaFlo to additional customers.

Market Opportunity

QuantaFlo

Fee-for-service is a payment model where services are unbundled and paid for separately. In health care, it gives an incentive for physicians to provide more treatments because payment is dependent on the quantity of care, rather than quality of care. Capitation is a payment arrangement that pays a physician or group of physicians a set amount for each enrolled person assigned to them, per period of time, whether or not that person seeks care. The amount of remuneration is based on the average expected healthcare utilization of that patient, with greater payment for patients with significant medical history. For Medicare Advantage patients CMS pays a fee per patient, also known as capitation. CMS uses risk adjustment to adjust capitation payments to health plans, either higher or lower, to account for the differences in expected health costs of individuals. Accordingly, under CMS guidelines, risk factor adjustments per patient will provide payment that is higher for sicker patients who have conditions that are codified.

6

The current coding system used by CMS for the Medicare Advantage program is a hierarchical condition category, or HCC, diagnostic classification system that began by classifying over 14,000 diagnosis codes into approximately 1,500 diagnostic groups, or DXGs. Each code maps to exactly one DXG, which represents a well-specified medical condition, such as DXG 96.01 pre-cerebral or cerebral arterial occlusion with infarction. DXGs are further aggregated into 204 condition categories, or CCs. CCs describe a broader set of similar diseases. Diseases within a CC are related clinically and with respect to cost. An example is CC100 Ischemic or Unspecified Stroke, which includes DXG 95.02 iatrogenic cerebrovascular infarction or hemorrhage (e.g., postoperative stroke), DXG 96.01 precerebral or cerebral arterial occlusion with infarction, DXG 96.02 acute but ill-defined cerebrovascular disease (ICD-9), and DXG 170.59 neonatal cerebral infarction.

Undiagnosed cardiac and vascular diseases are major under-diagnosed health problems in the United States. These conditions are common and deadly cardiovascular disease is often undiagnosed. As with clogged arteries in the heart, clogged arteries in the legs place patients at an increased risk of heart attack and stroke. Published studies have shown that persons with PAD are four times more likely to die of heart attack, and two to three times more likely to die of stroke. According to a study by P.G. Steg published in the JAMA, patients with PAD have a 21% event rate of cardiovascular death, heart attack, stroke or cardiovascular hospitalization within 12 months. The SAGE Group has estimated that as many as 20 million people are affected with PAD in the United States alone and A.T. Hirsch et al. in a JAMA published article further estimate that only 11% have claudication (pain on exertion), a classic symptom of PAD.

The spectrum of heart dysfunction includes heart failure. Published studies have shown that there are over one million hospitalizations per year in the United States from heart failure and the annual cost of care exceeds $30 billion. According to a study published in AHA Journals by S.L. Jackson, et al, heart failure affects ~approximately 6.5 million adults in the United States and the lifetime risk of heart failure is estimated to be one in five at 40 years of age. The study also notes persons with heart failure have mortality rates 20% to 25% higher after hospitalization within one year after diagnosis.

Many people affected with cardiac and vascular diseases do not have noticeable symptoms. When symptoms are present, they often include fatigue, heaviness, cramping or pain during activity, leg or foot pain, sores, wounds or ulcers on the toes, feet, or legs, which are slow to heal, shortness of breath, peripheral edema, or enlarged liver. Persons with cardiac and vascular diseases may become disabled and not be able to work.

Risk factors for developing cardiac and vascular diseases include:

• | Age (over 50 years) |

• | Race (African-American) |

• | History of smoking |

• | Diabetes |

• | High blood pressure |

• | High blood cholesterol |

• | Personal history of vascular disease, heart attack, or stroke. |

We believe medical personnel and insurance plans who care for those older than 50 years are the target market for QuantaFlo. Based on U.S. Census data, we believe there are more than 80 million older Americans who could be evaluated for the presence of cardiac and vascular diseases.

There are over 400,000 medical professionals practicing primary care in the United States. In addition, based on American Heart Association data, there are over 20,000 cardiologists and 7,500 vascular and cardiovascular surgeons. Also, there are millions of diabetic patients seen routinely by endocrinologists. Many podiatrists who see patients with these problems and orthopedic surgeons may see value in screening patients for circulation issues prior to leg

7

procedures. Neurologists may need a tool to differentiate leg pain from vascular versus neurologic etiology. Nephrologists see patients with kidney disease, who have a higher frequency of cardiac and vascular diseases. Wound care centers need to know the adequacy of limb perfusion. We expect that each physician will have many patient visits annually from people older than 50 years. While it is standard practice to ask about symptoms of cardiac and vascular diseases and to look for signs on physical exam, we believe that it is often the case in busy practices that the questions go unasked.

Generally speaking, individual products are not specifically approved by name under a third-party payor code. Physicians who seek reimbursement for testing procedures are likely to use codes that describe non-invasive physiologic testing. We do not track directly how physicians code for and receive payment for such procedures.

Insulin Insights

Of the growing diabetic population in the United States, over a quarter use insulin according to the Center for Disease Control and Prevention. Insulin is a necessary medication as nearly all Type 1 diabetics (approximately 1.6 million people in the United States, and roughly 21% of Type 2 diabetics (of the over 30 million people in the United States with Type 2 diabetics) must also use insulin to bring their blood glucose levels down to a healthy range. Without insulin, patients are likely to suffer from blurred vision, weight loss, and intolerable thirst. Eventually, uncontrolled diabetes can lead to blindness, kidney failure, gangrene, loss of limbs, and ultimately death. Tighter control of glucose is proven to improve the outcomes in diabetes care.

In the United States, about 90% of diabetic patients treating with insulin are managed by primary care practitioners. Insulin Insights is designed to be used by such practitioners to recommend optimal insulin dosing for each individual patient.

CMS has established a star rating system to measure and report on the quality of health services received by consumers in Medicare Advantage plans. Based on the star ratings, high performing health plans are also eligible to be paid bonuses by CMS. Among measures factored into plans’ star ratings are measures assessing diabetes care, including a measure adapted from the Healthcare Effectiveness Data and Information Set (HEDIS) that assesses the percentage of diabetic plan enrollees aged 18-75 who demonstrate good blood sugar control (HbA1c <9.0%). We believe this provides a financial incentive to potential customers for an Insulin Insights software license, as it will assist them in working with their diabetic patients to optimize insulin dosing and achieve better control of their blood glucose levels.

Other Products and Services

In addition to our internal research and development efforts, in October 2020, we invested in SYNAPS, whose product, Discern, is a test for early Alzheimer’s disease. In December 2022, we purchased a senior secured convertible promissory note of Monarch, maker of EndoTool, a technology-enabled approach to inpatient glycemic management. We do not have a distribution agreement for Discern or EndoTool.

Strategy

Our mission is to develop, manufacture and market products and services that assist healthcare providers in evaluating and treating chronic diseases. We intend to do this by:

| ● | Targeting customers with patients at risk of developing cardiac and vascular diseases. Healthcare providers use blood flow measurements as part of their assessment of a patient’s cardiac and vascular condition. Our strategy is to keep marketing QuantaFlo on a recurrent revenue model to insurance plans and medical personnel who care for those older than 50 years, including cardiologists, internists, nephrologists, endocrinologist, podiatrists, and family practitioners. Specifically, we believe there are more than 400,000 physicians and other potential customers in the United States alone, many of whom care for patients will be more than 50 years old and at increased risk of developing cardiac and vascular diseases. Based on U.S. Census data, the evaluable patient population for QuantaFlo is estimated to be more than 80 million patients in the United States annually. |

8

| ● | Expanding the tools available to internists and non-peripheral vascular experts. Our intention is to provide a tool to internists and non-cardiovascular experts, for whom it was previously impractical to conduct a blood flow measurement unless in a specialized vascular laboratory. For cardiovascular specialists, QuantaFlo does not require the use of blood pressure cuffs (which should not be used on some breast cancer patients), and measures without blood pressure in obese patients and patients with non-compressible, hard, calcified arteries. Currently, these patients often are unable to be measured satisfactorily with traditional devices. |

| ● | Developing additional product and service offerings that allow healthcare providers to deliver cost-effective wellness and receive increased compensation for their services. In March 2015, we received FDA 510(k) clearance of our product, QuantaFlo, reflecting several updates and modifications to the original model that were developed in conjunction with our consultant engineering groups. We recently began marketing QuantaFlo as an aid to measure hemodynamics related to heart dysfunction and continue to explore potential new product and service offerings through our research and development programs. Our goal is to provide cost-effective wellness solutions for our growing, established customer base, achieve a reputation for outstanding service, all while leveraging our gains in the marketplace for such product and service offerings. |

| ● | Exploring additional product and service offerings through arrangements or potential acquisitions. In addition to our in-house research and development efforts, we are also seeking out opportunities to expand our product and service offerings through marketing, distribution and licensing arrangements, such as our agreement to exclusively market and distribute Insulin Insights line in the United States, including Puerto Rico. Such arrangements will allow us to sell products related to chronic disease management through our network of physicians and other customers. We may also consider opportunistically acquiring additional products if we believe they fit within our strategy. |

Sales and Marketing

We provide our QuantaFlo product to our customers through our salespersons, who have experience selling products and services to our anticipated market.

We deliver our QuantaFlo testing product directly to our customers, and in-service training to the customers is provided either on-line or in person. Because QuantaFlo is relatively easy to use, training can generally be accomplished in less than one day.

Customers who have licensed our QuantaFlo product may pay by credit card or check generally on the 15th of each month as an advance for usage during the next 30 days. In some cases, customers prefer an annual license paid in advance. We provide technical support daily, coupled directly to the manufacturing operation so that replacement products, if needed, can be shipped overnight directly to the customer. The majority of the support is over the telephone and focuses on software and connectivity issues, rather than hardware. We upgrade QuantaFlo operating systems as appropriate by direct shipments or electronically.

In addition to the license model with a fixed monthly fee, we also have contracts that charge a variable monthly fee, in which we invoice based on the number of tests performed with QuantaFlo. In addition to licensing the QuantaFlo software, we have sold QuantaFlo equipment and accessories.

We have an agreement with Mellitus to exclusively market and distribute Insulin Insights, a new software product, in the United States, including Puerto Rico, except for selected accounts. Under this April 2021 agreement as amended in December 2022, we pre-paid for an aggregate $2.5 million of licenses ($2.0 million in April 2021 and $0.5 million in December 2022. We signed several customers to a license for this product in late 2022. As of December 31, 2022, we had not generated any material revenues from this product.

Manufacturing

We manufacture our product, QuantaFlo, in the United States through independent contractors whom we pay for finished goods. Our contracts provide for subassemblies, product final assembly, test, serialization, finished goods,

9

inventory and shipping operations. Our current contracts will remain in force until terminated by us upon three months written notice, or until terminated by either party for cause. Although we believe we have a good working relationship with our current contract manufacturers, there are many such qualified contract manufacturers available around the country should we need to replace them or if they are not able to meet demand as we grow our business as anticipated. While our current independent contract manufacturers source some supplies from China, we believe QuantaFlo is relatively easy to manufacture, and should we encounter issues due to supply chain disruptions as a result of the ongoing COVID-19 pandemic or other global supply chain constraints, we believe alternative sources should be available. We employ a consultant vendor qualification expert to monitor and test the quality controls and quality assurance procedures of our contract manufacturer.

Competition

The principal competitor for QuantaFlo is the standard blood pressure cuff ABI device. QuantaFlo does not include a blood pressure cuff. There are several companies that manufacture the traditional ABI device, which range in price from $2,500 to $20,000. Some of these companies are much larger than us and have more financial resources and their own distributor network. The traditional ABI devices are differentiated by the degree of automation designed into each product. ABI devices that rely more heavily on operator assessment (i.e., listening to the return of pulse while decreasing cuff pressure), are thought to have less objectivity in their measurement. Because standard ABI devices require a better trained operator, the products are usually sold to specialized vascular labs that are supervised by a vascular surgeon, with the tests performed by a licensed vascular technician. It is not uncommon for such ABI devices to be marketed to the offices of internists, podiatrists, endocrinologists or most cardiologists.

Our intention is to provide a tool to internists and non-cardiovascular experts, for whom it was previously impractical to conduct a blood flow measurement unless in a specialized vascular laboratory. For cardiovascular specialists, QuantaFlo does not require the use of blood pressure cuffs (which should not be used on some breast cancer patients), and measures without blood pressure in obese patients and patients with non-compressible, hard, calcified arteries. Currently, these patients often are unable to be measured with traditional devices.

Competitors are beginning to market competing digital devices seeking to provide fast results that may be used outside of a specialized vascular laboratory. Given the potential size of the market, we expect competitors to continue to enter the space.

Research and Development Program

We have dedicated engineering consultants that are well integrated into our overall business, ranging from customer requirements to technical support. The engineering group uses our in-house quality system as its framework for new product development and release. The majority of the engineering is circuit design and software development. We are currently developing several updates and modifications to QuantaFlo in conjunction with our consultant engineering groups, as well as exploring potential new product and service offerings. These product and service offerings are being designed to provide cost-effective wellness solutions for our growing, established customer base. The new products and service offerings under development or that may be developed may incorporate some of our current technology or new technology. We are also directing much of our activity to building our trade secrets and protecting proprietary positions.

Clinical Experience

Several studies of our blood flow measurement products have been conducted by our customers or authors facilitated by access to our database. Other studies were conducted by our customers using their own independently generated datasets.

One of these studies, the results of which were compiled in 2012 and published in a peer reviewed journal in 2013, sought to determine the frequency of finding undiscovered vascular disease in primary care practices using our vascular testing product. In the study of 632 patients at 19 office practices, the frequency of flow obstruction was 12% and of these patients, 75% did not have classic symptoms of PAD. Among other limitations of the study, the publication

10

mentioned the study’s retrospective design, no direct comparison to other vascular tests and passive data collection such that 8% of patients had one or more missing data fields.

Another study was designed to assess the side-by-side performance of our vascular testing product compared with traditional analog ABI with Doppler measurements in medical practices. In the study of 181 limbs from 121 patients at 5 medical practices during 2012 and 2013, three techniques were used on all limbs: our test, traditional analog ABI with Doppler, and Duplex ultrasound imaging as a gold standard. Traditional analog ABI with Doppler was unable to perform a conclusive study in 8.7% of limbs. In the remaining limbs, our vascular testing product and the ABI with Doppler measurements were in agreement, or in other words concordant, in 78% of limbs. Among the discordant limbs, Duplex imaging judged that the true positive rate of our vascular testing product was significantly higher than that of ABI with Doppler by a 2 to 1 margin. The results of the study are available as a white paper that may be shown to potential customers or other interested parties. Among other limitations of the study, the study had a small sample size, was conducted at specialty practices not primary care practices, had a retrospective design with incomplete collection of demographic information and clinical characteristics of the population, was not peer reviewed and was not peer reviewed.

Another study also was designed to assess the side-by-side performance of our vascular testing product compared with traditional analog ABI with Doppler measurements in medical practices. In this prospective study at five medical practices during 2013 through 2015, 360 limbs from 180 patients were examined with three techniques: Our vascular testing product, traditional analog ABI with Doppler, and Duplex ultrasound imaging as a gold standard. Results demonstrated that our test demonstrated greater sensitivity, greater accuracy and equivalent specificity compared to ABI with Doppler measurements. The results of the study are available as a white paper. Among limitations of the study are that it had a small sample size, was conducted at a mix of primary care and specialty practices, had no formal tracking of consecutive patients, and was not peer reviewed.

Another study, the results of which were compiled and published in a peer reviewed journal in 2018, reported an analysis of a registry of screening PAD testing with our product between January 2017 and July 2017. In this study, 226,565 patients were tested and 31.3% had moderate to severe flow impairment in the lower extremities. Further analysis of a subset of 26,459 patients for whom clinical characteristics were recorded showed that 95% were asymptomatic. The authors concluded that earlier recognition of PAD may lead to earlier secondary preventive measures and improved outcomes for a population with a high-risk of cardiovascular mortality and morbidity. Among other limitations of the study, the publication mentioned the study’s retrospective design and that clinical factors were recorded for only approximately 10% of patients.

A retrospective case series compiled and published in a peer reviewed journal in 2018 reported on 48 patients that were tested with our product and subsequently had a contrast angiography procedure for clinical indications. Using contrast angiography as the gold standard for determining PAD, the author concluded the data supports the use of our product as an aid for practicing physicians to accurately diagnose PAD in combination with clinical judgment. Among other limitations of the study, the sample size was small, tests were performed at specialty centers, and the analysis was done retrospectively.

Certain racial and economic groups in the United States are underserved by the medical community with limited access to specialists, a lack of early detection programs and inadequate preventive disease management. There is abundant evidence that certain ethnic populations are more at risk for cardiovascular disease and suffer sequelae of untreated PAD. A study was compiled and published in a peer reviewed journal in 2018 that presented a retrospective analysis of 1,901 patients tested with our product at 22 medical practices that serve predominately lower-income, non-white populations. The author concluded that our product can be effectively utilized by primary care clinicians in poor and underserved communities to identify PAD. The author posited that identifying PAD earlier in the disease process can be an important step towards filling the unmet need of higher intensity vascular care for minority populations. Limitations of the study include that it was a retrospective analysis and that there was no protocol to unveil the identity or ethnicity of any of the individual patients.

Women may lack early detection programs and have inadequate preventive disease management. A study was compiled and published in a peer reviewed journal in 2019 that presented a retrospective analysis of 68,402 female

11

patients tested with our product at primary care medical practices in the United States. The author concluded that our product was an efficient means to aid in the diagnosis of PAD in vulnerable women who are currently underserved by their health care providers. Limitations of the study include that it was a retrospective analysis with self-reporting of clinical characteristics.

A February 2022 published peer-reviewed study analyzed screening tests using QuantaFlo for undetected and asymptomatic heart failure in a Medicare Advantage population between January 2016 and December 2016. In this study, 13,971 patients were tested and 31.6% had a positive result for PAD. Almost 60% had lower socio-economic income level with 15.1% living under the poverty level. The risk associated with detecting PAD was substantial with a 60-70% increased risk of all-cause mortality or morbidity at one year and a 40-50% increased risk of all-cause mortality or morbidity at three years. The risk was not modified by a history of coronary or cerebrovascular artery disease. The authors concluded that these findings highlight an enormous potential to realize cost-savings by reducing cardiovascular event rates and deploying population-based PAD risk mitigation strategies. Among other limitations of the study, the publication mentioned that they were not able to study the potential impact of PAD risk management strategies used after a positive PAD screen was communicated with the primary care provider and patient. This may have led to an underestimation of the true risk as targeted PAD risk management and behavior modification strategies may have been initiated at the discretion of the provider and patient.

A September 2022 a peer-reviewed study under real-world conditions, illustrating the benefits of PAD in-home screening was published. The study analyzed screening tests using QuantaFlo for Medicare Advantage beneficiaries aged ≥65 years participating in the Optum HouseCalls program in the U.S. between April 1, 2017 and February 1, 2019. Of the 192,500 patients tested in their homes, 27.7% had a positive result for PAD. One-year all-cause mortality, 1- and 2-year major adverse cardiovascular events (MACE), and major adverse limb events (MALE) in the PAD positive patients were all significantly increased versus those patients who screened negative for PAD (p <.001). Moreover, the severity of the test results was associated with worse outcomes. The authors stated, “Detecting previously undiagnosed peripheral artery disease is a way to risk stratify a population that would benefit from further cardiovascular risk management.” Among other limitations of the study, the publication mentioned that the findings are only generalizable to individuals aged ≥65 years and the study could not assess the proportion of deaths due to cardiovascular causes.

A February 2023 a peer-reviewed study was published assessing the accuracy our vascular testing product using cardiac echocardiography (Echo) as a gold standard of heart failure. Results were that our test showed a significant correlation with Echo (p<.01). Among other limitations of the study, the publication mentioned that data on severity were not including and outcomes following preventative measures were not studied.

Patents and Licenses

We have been issued one patent for our apparatus, U.S. Patent No. 7,628,760, which expires December 11, 2027.

Government Regulation

U.S. Food and Drug Administration Regulation

QuantaFlo is a medical device subject to extensive regulation by the FDA and other federal, state, local and foreign regulatory bodies. FDA regulations govern, among other things, the following activities that we or our partners perform and will continue to perform:

| ● | product design and development; |

| ● | product testing; |

| ● | product manufacturing; |

| ● | product safety; |

12

| ● | post-market adverse event reporting; |

| ● | post-market surveillance; |

| ● | product labeling; |

| ● | product storage; |

| ● | record keeping; |

| ● | pre-market clearance or approval; |

| ● | post-market approval studies; |

| ● | advertising and promotion; and |

| ● | product sales and distribution. |

FDA’s Pre-market Clearance and Approval Requirements

To commercially distribute QuantaFlo or any future medical device we develop requires or will require either prior 510(k) clearance or prior approval of a pre-market approval, or PMA, application or de novo classification from the FDA. The FDA classifies medical devices into one of three classes. Devices deemed to pose lower risk are placed in either class I or II, which requires the manufacturer to submit to the FDA a pre-market notification requesting permission for commercial distribution. This process is known as 510(k) clearance. Some low risk devices are exempt from this requirement. Class I devices are those for which safety and effectiveness can be reasonably assured by adherence to FDA’s “general controls”, which include compliance with the applicable portions of the FDA’s Quality System Regulation, or QSR, facility registration and product listing, reporting of adverse medical events and malfunctions through the submission of Medical Device Reports, or MDRs, and appropriate, truthful and non-misleading labeling, advertising and promotional materials. Class II devices are subject to FDA’s general controls and any other “special controls” deemed necessary by FDA to ensure the safety and effectiveness of the device, such as performance standards, product-specific guidance documents, special labeling requirements, patient registries or post-market surveillance. Devices deemed by the FDA to pose the greatest risk, such as life-sustaining, life-supporting or implantable devices, or devices deemed not substantially equivalent to a previously cleared 510(k) device are placed in class III, requiring approval of a PMA application. To market low to moderate risk devices that are automatically placed into class III, a manufacturer may request a de novo classification from FDA. Both pre-market clearance, PMA applications and de novo classification requests are subject to the payment of user fees, paid at the time of submission for FDA review. The FDA can also impose restrictions on the sale, distribution or use of devices at the time of their clearance or approval or authorization, or subsequent to marketing.

510(k) Clearance Pathway

To obtain 510(k) clearance, a medical device manufacturer must submit a pre-market notification demonstrating that the proposed device is substantially equivalent to a previously cleared 510(k) device or a device that was in commercial distribution before May 28, 1976 for which the FDA has not yet called for the submission of a PMA application or a device that has been reclassified from class III to class II or class I. A device is substantially equivalent if, with respect to the predicate device, it has the same intended use and has either (i) the same technological characteristics, or (ii) different technological characteristics, but the information provided in the 510(k) submission demonstrates that the device does not raise new questions of safety and effectiveness and is at least as safe and effective as the predicate device. The FDA’s 510(k) clearance pathway usually takes from three to 12 months from the date the notification is submitted, but it can take significantly longer, and clearance is never assured. Although many 510(k) pre-market notifications are cleared without clinical data, in some cases, the FDA requires significant clinical data to support substantial equivalence. In reviewing pre-market notification, the FDA may request additional information, including

13

clinical data, which may significantly prolong the review process. After a device receives 510(k) clearance, any modification that could significantly affect its safety or effectiveness, or that would constitute a major change in its intended use, will require a new 510(k) clearance or could require a PMA application. The FDA requires each manufacturer to make this determination initially, but the FDA can review any such decision and can disagree with a manufacturer’s determination. If the FDA disagrees with a manufacturer’s determination regarding whether a new pre-market submission is required for the modification of an existing device, the FDA can require the manufacturer to cease marketing and/or recall the modified device until 510(k) clearance or approval of a PMA application is obtained.

Pre-market Approval Pathway

A PMA application must be submitted if the device cannot be cleared through the 510(k) clearance process and requires proof of the safety and effectiveness of the device to the FDA’s satisfaction. Accordingly, a PMA application must be supported by extensive data including, but not limited to, technical information regarding device design and development, preclinical studies and clinical trials, data and manufacturing and labeling to support the FDA’s determination that the device is safe and effective for its intended use. After FDA determines that a PMA application is sufficiently complete to permit a substantive review, the FDA begins an in-depth review of the submitted information, which generally takes between one and three years, but may take significantly longer. During this review period, the FDA may request additional information or clarification of information already provided. Also, during the review period, an advisory panel of experts from outside the FDA may be convened to review and evaluate the application and provide recommendations to the FDA as to the approvability of the device. In addition, the FDA will conduct a preapproval inspection of the manufacturing facility to ensure compliance with the QSR, which impose elaborate design development, testing, control, documentation and other quality assurance procedures in the design and manufacturing process. The FDA may approve a PMA application with post-approval conditions intended to ensure the safety and effectiveness of the device including, among other things, restrictions on labeling, promotion, sale and distribution and collection of long-term follow-up data from patients in the clinical study that supported approval. Failure to comply with the conditions of approval can result in materially adverse enforcement action, including the loss or withdrawal of the approval. New PMA applications or PMA application supplements are required for significant modifications to the manufacturing process, labeling and design of a device that is approved through the PMA process. PMA supplements often require submission of the same type of information as a PMA application, except that the supplement is limited to information needed to support any changes from the device covered by the original PMA application, and may not require as extensive clinical data or the convening of an advisory panel.

De Novo Classification Pathway

Device types that the FDA has not previously classified as class I, II or III are automatically classified into class III regardless of the level of risk they pose. To market low to moderate risk devices that are automatically placed into class III due to the absence of a predicate device, a manufacturer may request a de novo classification. This procedure allows a manufacturer whose novel device is automatically classified into class III to request classification of its device into class I or II on the basis that the device presents low or moderate risk, rather than requiring the submission and approval of a PMA application. A device may be eligible for de novo classification if the manufacturer first submitted a 510(k) premarket notification and received a determination from the FDA that the device was not substantially equivalent or a manufacturer may request de novo classification directly without first submitting a 510(k) premarket notification to the FDA and receiving a not substantially equivalent determination. The FDA is required to classify the device within 120 days following receipt of the de novo classification request, although in practice, the FDA’s review may take significantly longer. If the manufacturer seeks reclassification into class II, the manufacturer must include a draft proposal for special controls that are necessary to provide a reasonable assurance of the safety and effectiveness of the device. The FDA may reject the de novo classification request if it identifies a legally marketed predicate device that would be appropriate for a 510(k) or determines that the device is not low to moderate risk or that general controls would be inadequate to control the risks and special controls cannot be developed. In the event FDA determines the data and information submitted demonstrate that general controls or general and special controls are adequate to provide reasonable assurance of safety and effectiveness, FDA will grant the de novo request for classification. When FDA grants a de novo request for classification, the device is granted marketing authorization and further can serve as a predicate for future devices of that type through a 510(k) premarket notification.

14

Clinical Trials

Clinical trials are typically required to support a PMA and often for a de novo classification request, and are sometimes required to support a 510(k) submission. All clinical investigations of devices to determine safety and effectiveness must be conducted in accordance with the FDA’s investigational device exemption, or IDE, regulations which govern investigational device labeling, prohibit promotion of the investigational devices, and specify an array of recordkeeping, reporting and monitoring responsibility of study sponsors and study investigators. If the device presents a “significant risk,” as defined by the FDA, to human health, the FDA requires the device sponsor to submit an IDE application to the FDA, which must be approved prior to commencing human clinical trials. A significant risk device is one that presents a potential for serious risk to the health, safety or welfare of a patient and either is implanted, purported or represented to be used in supporting or sustaining human life, is for a use that is substantially important in diagnosing, curing, mitigating or treating disease or otherwise preventing impairment of human health, or otherwise presents a potential for serious risk to a subject. An IDE application must be supported by appropriate data, such as animal and laboratory test results, showing that it is safe to test the device in humans and that the testing protocol is scientifically sound. A clinical trial may begin 30 days after receipt of the IDE application by the FDA unless the FDA notifies the company that the investigation may not begin. If the FDA determines that there are deficiencies or other concerns with an IDE for which it requires modification, the FDA may permit a clinical trial to proceed under a conditional approval. Acceptance of an IDE application for review does not guarantee that the FDA will approve the IDE and, if it is approved, the FDA may or may not determine that the date derived from the trials support the safety and effectiveness of the device or warrant the continuation of clinical trials. An IDE supplement must be submitted to, and approved by, the FDA before a sponsor or investigator may make a change to the investigational plan that may affect its scientific soundness, study plan or the rights, safety or welfare of human subjects.

In addition, the study must be approved by, and conducted under the oversight of, an institutional review board, or IRB, for each clinical site. The IRB is responsible for the initial and continuing review of the IDE, and may pose additional requirements for the conduct of the study. If an IDE application is approved by the FDA and one or more IRBs, human clinical trials may begin a specific number of investigational sites with a specific number of patients, as approved by the FDA.

If the device is considered a “non-significant risk,” an IDE application to the FDA is not required. Instead, only approval from the IRB overseeing the investigation at each clinical trial site is required. Abbreviated IDE requirements, such as monitoring the investigation, ensuring that the investigators obtain informed consent, and labeling and record-keeping requirements also apply to non-significant risk device studies.

During a study, the sponsor is required to comply with the applicable FDA requirements, including, for example, trial monitoring, selecting clinical investigators and providing them with the investigational plan, ensuring IRB review, adverse event reporting, record keeping and prohibitions on the promotion of investigational devices or on making safety or effectiveness claims for them. The clinical investigators in the clinical study are also subject to FDA’s regulations and must obtain patient informed consent, rigorously follow the investigational plan and study protocol, control the disposition of the investigational device, and comply with all applicable reporting and record keeping requirements.

Additionally, after a trial begins, we, the FDA or the IRB could suspend or terminate a clinical trial at any time for various reasons, including a belief that the risks to study subjects outweigh the anticipated benefits. Even if a clinical trial is completed, there can be no assurance that the data generated during a clinical study will meet the safety and effectiveness endpoints or otherwise produce results that will lead the FDA to grant marketing clearance or approval. Information about certain device clinical trials must be posted on clinicaltrials.gov.

15

Pervasive and Continuing FDA Regulation

After a device is placed on the market, regardless of its classification or pre-market pathway, numerous regulatory requirements apply. These include, but are not limited to:

| ● | establishment registration and device listings with the FDA; |

| ● | QSR, which require manufacturers to follow stringent design, testing, process control, documentation and other quality assurance procedures; |

| ● | labeling regulations, which prohibit the promotion of products for uncleared or unapproved, i.e., “off-label,” uses and impose other restrictions on labeling; |

| ● | medical device reporting regulations, which require that manufacturers report to the FDA if their device may have caused or contributed to a death or serious injury or malfunctioned in a way that would likely cause or contribute to a death or serious injury if it were to recur; |

| ● | corrections and removal reporting regulations, which require that manufacturers report to the FDA field corrections and product recalls or removals if undertaken to reduce a risk to health posed by the device or to remedy a violation of the U.S. Federal Food, Drug, and Cosmetic Act, or FDCA, that may present a risk to health; and |

| ● | requirements to conduct post-market surveillance studies to establish continued safety data. |

The FDA enforces these requirements by inspection and market surveillance. Failure to comply with applicable regulatory requirements can result in enforcement action by the FDA, which may include any of the following sanctions:

| ● | untitled letters or warning letters; |

| ● | fines, injunctions and civil penalties; |

| ● | recall or seizure of our products; |

| ● | operating restrictions, partial suspension or total shutdown of production; |

| ● | refusing our request for 510(k) clearance or pre-market approval or de novo classification of new products; |

| ● | withdrawing pre-market approvals that are already granted or reclassifying the devices; and |

| ● | criminal prosecution. |

We are subject to unannounced device inspections by the FDA and the California Food and Drug Branch. These inspections may include our suppliers’ facilities.

Third-Party Coverage and Reimbursement

We cannot control whether or not providers who use QuantaFlo will seek third-party coverage for such procedures or reimbursement. If providers intend to seek third-party coverage or reimbursement for use of QuantaFlo, the success of our product could become dependent on the availability of coverage and reimbursement from third-party payors, such as governmental programs including Medicare and Medicaid, private insurance plans and managed care programs. Reimbursement is contingent on established coding for a given procedure, coverage of the codes by the third-party payors and adequate payment for the resources used.

16

Physician coding for procedures is established by the American Medical Association. CMS, the agency responsible for administering Medicare and Medicaid, and the National Center for Health Statistics, are jointly responsible for overseeing changes and modifications to billing codes used by hospitals for reporting inpatient procedures, and many private payors use coverage decisions and payment amounts determined by CMS as guidelines in setting their coverage and reimbursement policies. All physician and hospital coding is subject to change, which could impact coverage and reimbursement and physician practice behavior. We do not track denial of requests for reimbursement made by the users of QuantaFlo. It is our belief that such denials have occurred and might occur in the future with more or less frequency. We are not in the business of performing QuantaFlo measurements that require us to seek reimbursement from third-party payors, including governmental healthcare programs, such as Medicare and Medicaid, commercial health insurers, including those that offer Medicare Advantage plans, and managed care programs. Many of our customers are third-party payors who pay us directly for use of our product and services.

Independent of the coding status, third-party payors may deny coverage based on their own criteria, such as if they believe that the clinical efficacy of a device or procedure is not well established and is deemed experimental or investigational, is not the most cost-effective treatment available, or is used for an unapproved indication. We will continue to provide the appropriate resources to patients, physicians, hospitals and insurers in order to promote the best in patient care and clarity regarding reimbursement and work to obtain appropriate coverage policies. For some governmental programs, such as Medicaid, coverage and reimbursement differ from state to state, and some state Medicaid programs may not pay an adequate amount for the procedures performed with our products, if any payment is made at all. As the portion of the U.S. population over the age of 65 and eligible for Medicaid continues to grow, we may be more vulnerable to coverage and reimbursement limitations imposed by CMS. National and regional coverage policy decisions are subject to unforeseeable change and have the potential to impact physician behavior. For example, if CMS decreases the monthly payment for a 65-year-old patient, then the provider will have to decide which steps to eliminate from his or her routine office visits in order to maintain a profitable business model. If the time of an office visit will need to be reduced to maintain a profitable business, a provider may decide to eliminate certain services or conducting certain procedures, such as deciding not to use a thermometer, take someone’s blood pressure or use a QuantaFlo to run an ABI test. Thus, reimbursement limitations imposed by CMS on providers may affect their decision making about which services to provide during an office visit, which could affect our company.

Particularly in the United States, third-party payors carefully review, have undertaken cost-containment initiatives, and increasingly challenge, the prices charged for procedures and medical products as well as any technology that they, in their own judgment, consider experimental or investigational. In addition, an increasing percentage of insured individuals are receiving their medical care through managed care programs, which monitor and often require pre-approval or pre-authorization of the services that a member will receive. Many managed care programs are paying their providers on a capitated basis, which puts the providers at financial risk for the services provided to their patients by paying them a predetermined amount per member per month. The percentage of individuals covered by managed care programs is expected to grow in the United States over the next decade.

There can be no assurance that third-party coverage and reimbursement will be available or adequate, or that future legislation, regulation, or coverage and reimbursement policies of third-party payors will not adversely affect the demand for our products or our ability to sell these products on a profitable basis. The unavailability or inadequacy of third-party payor coverage or reimbursement could have a material adverse effect on our business, operating results and financial condition.

Healthcare Fraud and Abuse

Our operations may be subject to federal and state healthcare laws and regulations including fraud and abuse laws, such as anti-kickback and false claims laws, data privacy and security laws and transparency laws related to payments and/or other transfers of value made to physicians and other healthcare professionals and teaching hospitals.

The federal Anti-Kickback Law prohibits unlawful inducements for the referral of business reimbursable under federally-funded healthcare programs, such as remuneration provided to physicians to induce them to use certain tissue products or medical devices reimbursable by Medicare or Medicaid. The federal Anti-Kickback Law is subject to evolving interpretations. For example, the government has enforced the federal Anti-Kickback Law to reach large

17

settlements with healthcare companies based on, among other things, inappropriate consultant arrangements with physicians or questionable joint venture arrangements. The majority of states also have anti-kickback laws, which establish similar prohibitions that may apply to items or services reimbursed by any third-party payor, including commercial insurers. Further, the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act of 2010, or collectively the Health Care Reform Law, among other things, amended the intent requirement of the federal Anti-Kickback Law and criminal healthcare fraud statutes. A person or entity no longer needs to have actual knowledge of this statute or specific intent to violate it in order to have committed a violation. In addition, the Health Care Reform Law provided that the government may assert that a claim including items or services resulting from a violation of the federal Anti-Kickback Law constitutes a false or fraudulent claim for purposes of the civil False Claims Act and certain criminal healthcare fraud statutes.

Additionally, the civil False Claims Act prohibits knowingly presenting or causing the presentation of a false, fictitious or fraudulent claim for payment to the U.S. government. Actions under the False Claims Act may be brought by the Attorney General or as a qui tam action by a private individual in the name of the government. The federal government is using the civil False Claims Act, and the accompanying threat of significant liability, in its investigations of healthcare providers and suppliers throughout the country for a wide variety of Medicare billing practices and has obtained multi-million and multi-billion dollar settlements in addition to individual criminal convictions. In addition, off-label promotion has been pursued as a violation of the federal False Claims Act. Pursuant to FDA regulations, we can only market our products for cleared or approved uses. Although physicians are permitted to use medical devices for indications other than those cleared or approved by the FDA based on their independent medical judgment, we are prohibited from promoting products for such off-label uses. Given the significant size of actual and potential settlements, it is expected that the government will continue to devote substantial resources to investigating healthcare providers’ and suppliers’ compliance with the healthcare reimbursement rules and fraud and abuse laws.

Additionally, the majority of states in which we market our products have similar fraud and abuse laws, such as anti-kickback, false claims, anti-fee splitting and self-referral laws, which may apply to items or services reimbursed by any third-party payor, including commercial insurers, and violations may result in substantial civil, criminal and administrative penalties.