SUNOCO LP

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Some of the information in this Annual Report on Form 10-K may contain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements, other than statements of historical fact included in this Annual Report on Form 10-K, regarding our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. Statements using words such as “believe,” “plan,” “could,” “expect,” “anticipate,” “intend,” “forecast,” “assume,” “estimate,” “continue,” “position,” “predict,” “project,” “goal,” “strategy,” “budget,” “potential,” “will” and other similar words or phrases are used to help identify forward-looking statements, although not all forward-looking statements contain such identifying words. Descriptions of our objectives, goals, targets, plans, strategies, costs, anticipated capital expenditures, expected cost savings and benefits are also forward-looking statements. These forward-looking statements are based on our current plans and expectations and involve a number of risks and uncertainties that could cause actual results and events to vary materially from the results and events anticipated or implied by such forward-looking statements, including:

•our ability to make, complete and integrate acquisitions from affiliates or third parties;

•business strategy and operations of Energy Transfer LP (“Energy Transfer”) and its conflicts of interest with us;

•changes in the price of and demand for the motor fuel that we distribute and our ability to appropriately hedge any motor fuel we hold in inventory;

•our dependence on limited principal suppliers;

•competition in the wholesale motor fuel distribution and retail store industry;

•changing customer preferences for alternate fuel sources or improvement in fuel efficiency;

•volatility of fuel prices or a prolonged period of low fuel prices and the effects of actions by, or disputes among or between, oil producing countries with respect to matters related to the price or production of oil;

•any acceleration of the domestic and/or international transition to a low carbon economy as a result of the Inflation Reduction Act of 2022 (“IRA 2022”) or otherwise;

•the possibility of cyber and malware attacks;

•changes in our credit rating, as assigned by rating agencies;

•a deterioration in the credit and/or capital markets, including as a result of recent increases in cost of capital resulting from Federal Reserve policies and changes in financial institutions’ policies or practices concerning businesses linked to fossil fuels;

•general economic conditions, including sustained periods of inflation, supply chain disruptions and associated central bank monetary policies;

•environmental, tax and other federal, state and local laws and regulations;

•the fact that we are not fully insured against all risks incident to our business;

•dangers inherent in the storage and transportation of motor fuel;

•our ability to manage growth and/or control costs;

•our reliance on senior management, supplier trade credit and information technology; and

•our partnership structure, which may create conflicts of interest between us and Sunoco GP LLC (our “General Partner”) and its affiliates, and limits the fiduciary duties of our General Partner and its affiliates.

All forward-looking statements, express or implied, are expressly qualified in their entirety by the foregoing cautionary statements.

New factors that could impact forward-looking statements emerge from time to time, and it is not possible for us to predict all such factors. Should one or more of the risks or uncertainties described or referenced in this Annual Report on Form 10-K occur, or should underlying assumptions prove incorrect, actual results and plans could differ materially from those expressed in any forward-looking statements.

For a discussion of these and other risks and uncertainties, please refer to “Item 1A. Risk Factors” included herein. The list of factors that could affect future performance and the accuracy of forward-looking statements is illustrative but by no means exhaustive. Accordingly, all forward-looking statements should be evaluated with the understanding of their inherent uncertainty. The forward‑looking statements included in this report are based on, and include, our estimates as of the filing of this report. We anticipate

3

that subsequent events and market developments will cause our estimates to change. However, while we may elect to update these forward-looking statements at some point in the future, we specifically disclaim any obligation to do so except as required by law, even if new information becomes available in the future.

In addition to risks and uncertainties in the ordinary course of business that are common to all businesses, important factors that are specific to our structure as a limited partnership, our industry and our company could materially impact our future performance and results of operations.

PART I

Item 1. Business

General

See information previously included in our Form 10-K filed on February 16, 2024.

Overview

See information previously included in our Form 10-K filed on February 16, 2024.

Operating Subsidiaries

See information previously included in our Form 10-K filed on February 16, 2024.

Recent Developments

See information previously included in our Form 10-K filed on February 16, 2024.

Available Information

See information previously included in our Form 10-K filed on February 16, 2024.

Our Relationship with Energy Transfer LP

See information previously included in our Form 10-K filed on February 16, 2024.

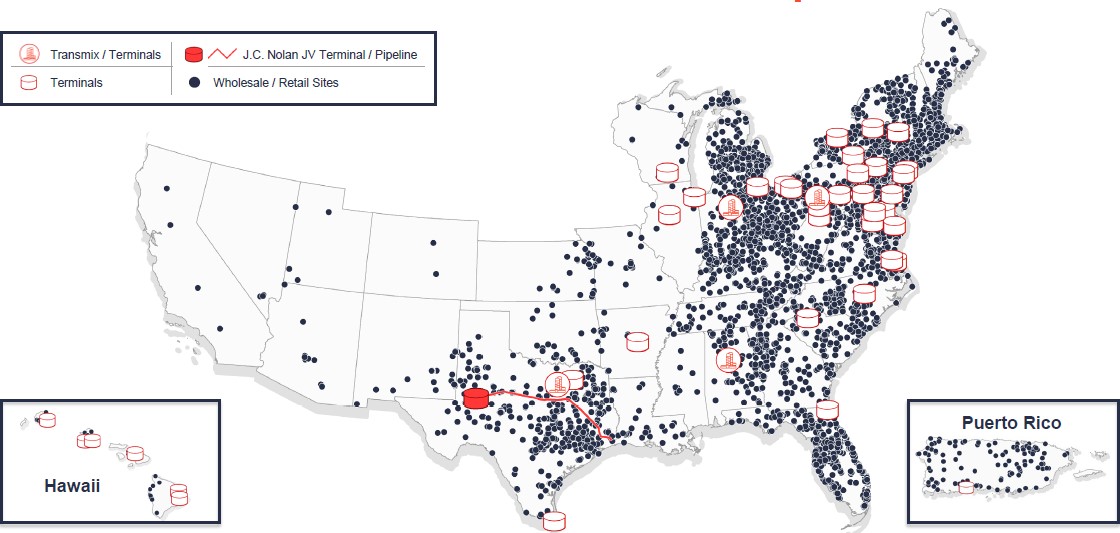

Our Business and Operations

Our business is comprised of three reportable segments: Fuel Distribution, Pipeline Systems and Terminals.

The map below depicts the major assets of our business and excludes corporate and field offices and certain assets that are less significant to SUN.

4

Fuel Distribution Segment

We are a distributor of motor fuels and other petroleum products which we supply to third-party dealers and distributors, to independent operators of commission agent locations, other commercial consumers of motor fuel and to our retail locations.

We are the exclusive wholesale supplier of the Sunoco and EcoMaxx-branded motor fuels, supplying an extensive distribution network of approximately 5,534 company and third-party operated locations throughout the United States and Puerto Rico. We believe we are one of the largest independent motor fuel distributors, by gallons, in the United States. We also are one of the largest distributors of Chevron, Texaco, ExxonMobil and Valero branded motor fuel in the United States. In addition to distributing motor fuels, we also distribute other petroleum products such as propane and lubricating oil, and we receive lease income from real estate that we lease or sublease.

We purchase motor fuel primarily from independent refiners and major oil companies and distribute it across more than 40 U.S. states and territories throughout the United States, including Hawaii and Puerto Rico, to:

•75 company-operated retail stores;

•476 independently operated commission agent locations where we sell motor fuel to retail customers under commission agent arrangements with such operators;

•6,828 retail stores operated by independent operators, which we refer to as “dealers” or “distributors,” pursuant to long-term distribution agreements; and

•approximately 1,600 other commercial customers, including unbranded retail stores, other fuel distributors, school districts, municipalities and other industrial customers.

The Fuel Distribution segment also includes the Partnership’s retail operations in Hawaii and New Jersey, credit card services and franchise royalties.

Dealer Incentives

In addition to motor fuel distribution, we offer dealers the opportunity to participate in merchandise purchasing and promotional programs arranged with vendors. We believe the vendor relationships we have established through our retail operations and our ability to develop programs provide us with an advantage over other distributors when recruiting new dealers into our network as well as with retaining current dealers. Our dealer incentives give our dealers access to discounted rates on products and services that they would likely not be able to obtain on their own.

Sales to Contracted Third Parties

We distribute fuel under long-term contracts to branded distributors, branded and unbranded convenience stores, and branded and unbranded retail fuel outlets operated by third parties. 7-Eleven, Inc. is the only third-party dealer or distributor which is individually over 10% of our Fuel Distribution segment or individually over 10%, in terms of revenue, of our aggregate business.

Sunoco-branded supply contracts with distributors generally have both time and volume commitments that establish contract duration. These contracts have an initial term of approximately ten years with an estimated volume-weighted term remaining of approximately five years.

Distribution contracts with retail stores generally commit us to distribute branded (including, but not limited to, Sunoco branded) or unbranded motor fuel to a location or group of locations and arrange for all transportation and logistics. These contracts require, among other things, that dealers maintain the standards established by the applicable fuel brand, if any. The initial term of these contracts range from three to 20 years, with most contracts for 10 years.

Our supply contracts and distribution contracts are typically constructed so that we receive either (i) a fee per gallon equal to the posted rack rate, less any applicable commercial discounts, plus transportation costs, taxes and a fixed, volume-based fee, which is usually expressed in cents per gallon, or (ii) a variable cent per gallon margin (“dealer tank wagon pricing”).

During 2023, our Fuel Distribution business distributed fuel to 476 commission agent locations. Under these arrangements, we generally provide and control motor fuel inventory and price at the site and receive actual retail selling price for each gallon sold, less a commission paid to the independent commission agents.

We continually seek to expand through the addition of new branded dealers, distributors and commission agent locations, new unbranded commercial customers and through acquisitions of contracts for existing independently operated sites from other distributors. We evaluate potential independent site operators based on their creditworthiness and the quality of their sites and operations, including the site’s size and location, projected monthly volumes of motor fuel, monthly merchandise sales, overall financial performance and previous operating experience. We may extend credit to certain dealers based on our credit evaluation process.

5

Sales to Other Commercial Customers

We distribute unbranded fuel to numerous other customers, including retail stores, unattended fueling facilities and certain other commercial customers. These customers are primarily commercial, governmental and other parties who buy motor fuel by the load or in bulk and who do not generally enter into exclusive contractual relationships with us, if they enter into a contractual relationship with us at all. Sales to these customers are typically made at a quoted price based upon our cost plus taxes, cost of transportation and a margin determined at time of sale, and may provide for immediate payment or the extension of credit for up to 45 days. We also sell propane, lubricating oil and other petroleum products, such as heating fuels, to our commercial customers on both a spot and contracted basis. In addition, we receive income from the manufacture and distribution sale of race fuels at our Marcus Hook, Pennsylvania manufacturing facility.

Fuel Supplier Arrangements

We distribute branded motor fuel under the Aloha, Chevron, Citgo, Conoco, EcoMaxx, Exxon, Mahalo, Mobil, Phillips 66, Shamrock, Shell, Sunoco, Texaco and Valero brands. We purchase branded motor fuel from major oil companies and refiners under supply agreements. Our largest branded fuel suppliers in terms of volume are Chevron, Exxon, Phillips 66 and Valero. The branded fuel supply agreements generally have an initial term of three to five years. Each supply agreement typically contains provisions relating to payment terms, use of the supplier’s brand names, credit card processing, compliance with other of the supplier’s requirements, insurance coverage and compliance with legal and environmental requirements, among others.

We also distribute unbranded motor fuel, which we purchase in bulk, on a rack basis based upon prices posted by the refiner at a fuel supply terminal or on a contract basis with the price tied to one or more market indices.

Bulk Fuel Purchases

We purchase motor fuel in bulk and hold it in inventory or transport it via pipeline. To mitigate inventory risk, we use commodity futures contracts or other derivative instruments, which are matched in quantity and timing to the anticipated usage of the inventory. We also blend in various additives, including ethanol and biomass-based diesel.

Transportation Logistics

We provide transportation logistics for most of our motor fuel deliveries through our own fleet of fuel transportation vehicles as well as third-party and affiliated transportation providers. We arrange for motor fuel to be delivered from the storage terminals to the appropriate sites in our distribution network at prices consistent with those historically charged to third parties for the delivery of fuel. We also deliver motor fuel, propane and lubricating oils to commercial customers involved in petroleum exploration and production.

Technology

Technology is an important part of our Fuel Distribution segment. We utilize a proprietary web-based system that allows our wholesale customers to access their accounts at any time from a personal computer to obtain prices, place orders and review invoices, credit card transactions and electronic funds transfer notifications. Substantially all of our customer payments are processed by electronic funds transfer. We use an Internet-based system to assist with fuel inventory management and procurement and an integrated distribution fuel system for financial accounting, procurement, billing and inventory management.

Sale of Regulated Products

In certain areas where our convenience stores are located, state or local laws limit the hours of operation for the sale of alcoholic beverages and restrict the sale of alcoholic beverages and tobacco products to persons younger than a certain age. State and local regulatory agencies have the authority to approve, revoke, suspend or deny applications for and renewals of permits and licenses relating to the sale of alcoholic beverages, as well as to issue fines to convenience stores for the improper sale of alcoholic beverages and tobacco products. Failure to comply with these laws may result in the loss of necessary licenses and the imposition of fines and penalties on us.

Pipeline Systems Segment

J.C. Nolan Joint Venture

Through our investment in the J.C. Nolan Terminal, a joint venture with Energy Transfer, we provide diesel fuel storage in Midland, Texas. Additionally, through our investment in J.C. Nolan Pipeline, we transport diesel fuel from a tank farm in Hebert, Texas to Midland, Texas, with a throughput capacity of approximately 36 MBbls/d.

Terminals Segment

We operate four transmix processing facilities and 42 refined product terminals (one in Puerto Rico, six in Hawaii and 35 in the continental United States). Transmix is the mixture of various refined products (primarily gasoline and diesel) created in the supply chain (primarily in pipelines and terminals) when various products interface with each other. Transmix processing plants separate this mixture and return it to salable products of gasoline and diesel. Our refined product terminals provide storage and distribution services

6

used to supply our own retail stations as well as third-party customers. In addition, we provide services at our terminals to various third-party throughput customers.

Real Estate and Lease Arrangements

See information previously included in our Form 10-K filed on February 16, 2024.

Competition

See information previously included in our Form 10-K filed on February 16, 2024.

Seasonality

See information previously included in our Form 10-K filed on February 16, 2024.

Working Capital Requirements

See information previously included in our Form 10-K filed on February 16, 2024.

Environmental Matters

See information previously included in our Form 10-K filed on February 16, 2024.

Water

See information previously included in our Form 10-K filed on February 16, 2024.

Other Government Regulation

See information previously included in our Form 10-K filed on February 16, 2024.

Employee Safety

See information previously included in our Form 10-K filed on February 16, 2024.

Store Operations

See information previously included in our Form 10-K filed on February 16, 2024.

Human Capital Management

See information previously included in our Form 10-K filed on February 16, 2024.

7

Part II

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

(Tabular dollar and unit amounts, except per unit data, are in millions)

The following discussion and analysis of our financial condition and results of operations for the years ended December 31, 2023, 2022, and 2021 should be read in conjunction with our audited consolidated financial statements and notes to audited consolidated financial statements included elsewhere in this report.

Adjusted EBITDA is a non-GAAP financial measure of performance that has limitations and should not be considered as a substitute for net income or cash provided by operating activities. Please see “Key Measures Used to Evaluate and Assess Our Business” below for a discussion of our use of Adjusted EBITDA in this “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and a reconciliation to net income for the periods presented.

Overview

As used in this Management’s Discussion and Analysis of Financial Condition and Results of Operations, the terms “Partnership,” “SUN,” “we,” “us” or “our” should be understood to refer to Sunoco LP and our consolidated subsidiaries, unless the context clearly indicates otherwise.

We are a Delaware master limited partnership primarily engaged in the distribution of motor fuels to independent dealers, distributors and other customers as well as the distribution of motor fuels to end-use customers at retail sites operated by commission agents. In addition, we receive lease income through the leasing or subleasing of real estate used in the retail distribution of motor fuels. As of December 31, 2023, we also operated 75 retail stores located in Hawaii and New Jersey.

We are the exclusive wholesale supplier of the Sunoco and EcoMaxx-branded motor fuels, supplying an extensive distribution network of approximately 5,534 company and third-party operated locations throughout the United States and Puerto Rico. We believe we are one of the largest independent motor fuel distributors, by gallons, in the United States. We also are one of the largest distributors of Chevron, Texaco, ExxonMobil and Valero branded motor fuel in the United States. In addition to distributing motor fuel, we also distribute other petroleum products such as propane and lubricating oil.

We purchase motor fuel primarily from independent refiners and major oil companies and distribute it across more than 40 states and territories throughout the United States, including Hawaii and Puerto Rico, to:

•75 company-operated retail stores;

•476 independently operated commission agent locations where we sell motor fuel to retail customers under commission agent arrangement with such operators;

•6,828 retail stores operated by independent operators, which we refer to as “dealers” or “distributors,” pursuant to long-term distribution agreements; and

•approximately 1,600 other commercial customers, including unbranded retail stores, other fuel distributors, school districts, municipalities and other industrial customers.

Our retail stores operate under several brands, including our proprietary brands APlus and Aloha Island Mart, and offer a broad selection of food, beverages, snacks, grocery and non-food merchandise, motor fuels and other services.

Acquisitions

On January 22, 2024, we entered into a definitive agreement with NuStar Energy L.P. (“NuStar”) to acquire NuStar in an all-equity transaction valued at approximately $7.3 billion, including assumed debt. Under the terms of the agreement, NuStar common unitholders will receive 0.400 Sunoco common units for each NuStar common unit. NuStar has approximately 9,500 miles of pipeline and 63 terminal and storage facilities that store and distribute crude oil, refined products, renewable fuels, ammonia and specialty liquids. The transaction is expected to close in the second quarter of 2024, subject to customary closing conditions.

On January 11, 2024, we entered into a definitive agreement with 7-Eleven, Inc. to sell 204 convenience stores located in West Texas, New Mexico, and Oklahoma for approximately $1.0 billion, including customary adjustments for fuel and merchandise inventory. As part of the sale, SUN will also amend its existing take-or-pay fuel supply agreement with 7-Eleven, Inc. to incorporate additional fuel gross profit. The transaction is expected to close promptly upon receipt of regulatory approvals and satisfaction of customary closing conditions.

On January 11, 2024, we announced that we will acquire liquid fuels terminals in Amsterdam, Netherlands and Bantry Bay, Ireland from Zenith Energy for €170 million including working capital. The transaction is expected to close in the first quarter of 2024, subject to customary closing conditions.

8

On May 1, 2023, the Partnership completed the acquisition of 16 refined product terminals located across the East Coast and Midwest from Zenith Energy for $111 million, including working capital.

Market and Industry Trends and Outlook

We expect that certain trends and economic or industry-wide factors will continue to affect our business, both in the short-term and long-term. Inflation has a minimal impact on our results of operations, because we are generally able to pass along energy cost increases in the form of increased sales prices to our customers. We have recently completed and recently announced multiple strategic transactions, which we expect will continue to diversify the Partnership’s business, add scale and expand cash for reinvestment and distribution growth. We base our expectations on information currently available to us and assumptions made by us. To the extent our underlying assumptions about or interpretation of available information prove to be incorrect, our actual results may vary materially from our expected results. Read “Item 1A. Risk Factors” included herein for additional information about the risks associated with purchasing our common units.

Seasonality

Our business exhibits some seasonality due to our customers’ increased demand for motor fuel during the late spring and summer months, as compared to the fall and winter months. Travel, recreation, and construction activities typically increase in these months, driving up the demand for motor fuel sales. Our gallons sold are typically somewhat higher in the second and third quarters of our fiscal years due to this seasonality. Results of operations may therefore vary from period to period.

Key Measures Used to Evaluate and Assess Our Business

Management uses a variety of financial measurements to analyze business performance, including the following key measures:

•Motor fuel gallons sold. One of the primary drivers of our business is the total volume of motor fuel sold through our channels. Fuel distribution contracts with our customers generally provide that we distribute motor fuel at a fixed, volume-based profit margin or at an agreed upon level of price support. As a result, profit is directly tied to the volume of motor fuel that we distribute. Total motor fuel profit dollars earned from the product of profit per gallon and motor fuel gallons sold are used by management to evaluate business performance.

•Profit per gallon. Profit per gallon is calculated as the profit on motor fuel (excluding non-cash inventory adjustments) divided by the number of gallons sold, and is typically expressed as cents per gallon. Our profit per gallon varies amongst our third-party relationships and is impacted by the availability of certain discounts and rebates from suppliers. Retail profit per gallon is heavily impacted by volatile pricing and intense competition from retail stores, supermarkets, club stores and other retail formats, which varies based on the market.

•Adjusted EBITDA. Adjusted EBITDA, as used throughout this document, is defined as earnings before net interest expense, income taxes, depreciation, amortization and accretion expense, allocated non-cash unit-based compensation expense, unrealized gains and losses on commodity derivatives, inventory adjustments and certain other operating expenses reflected in net income that we do not believe are indicative of ongoing core operations, such as gain or loss on disposal of assets and non-cash impairment charges. Inventory adjustments that are excluded from the calculation of Adjusted EBITDA represent changes in lower of cost or market reserves on the Partnership's inventory. These amounts are unrealized valuation adjustments applied to fuel volumes remaining in inventory at the end of the period.

Adjusted EBITDA is a non-GAAP financial measure. For a reconciliation of Adjusted EBITDA to the most directly comparable financial measure calculated and presented in accordance with GAAP, read “Key Operating Metrics and Results of Operations” below.

We believe Adjusted EBITDA is useful to investors in evaluating our operating performance because:

•Adjusted EBITDA is used as a performance measure under our Credit Facility;

•securities analysts and other interested parties use Adjusted EBITDA as a measure of financial performance; and

•our management uses Adjusted EBITDA for internal planning purposes, including aspects of our consolidated operating budget and capital expenditures.

Adjusted EBITDA is not a recognized term under GAAP and does not purport to be an alternative to net income as a measure of operating performance. Adjusted EBITDA has limitations as an analytical tool, and one should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations include:

•it does not reflect interest expense or the cash requirements necessary to service interest or principal payments on our Credit Facility;

9

•although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and Adjusted EBITDA does not reflect cash requirements for such replacements; and

•as not all companies use identical calculations, our presentation of Adjusted EBITDA may not be comparable to similarly titled measures of other companies.

Adjusted EBITDA reflects amounts for unconsolidated affiliates based on the same recognition and measurement methods used to record equity in earnings of unconsolidated affiliates. Adjusted EBITDA related to unconsolidated affiliates excludes the same items with respect to the unconsolidated affiliates as those excluded from the calculation of Adjusted EBITDA, such as interest, taxes, depreciation, depletion, amortization and other non-cash items. Although these amounts are excluded from Adjusted EBITDA related to unconsolidated affiliates, such exclusion should not be understood to imply that we have control over the operations and resulting revenues and expenses of such affiliate. We do not control our unconsolidated affiliates; therefore, we do not control the earnings or cash flows of such affiliates. The use of Adjusted EBITDA or Adjusted EBITDA related to unconsolidated affiliates as an analytical tool should be limited accordingly.

Results of Operations

Year Ended December 31, 2023 Compared to the Year Ended December 31, 2022

Consolidated Results of Operations

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | Change | |||||||||||||||

| Segment Adjusted EBITDA: | |||||||||||||||||

| Fuel Distribution | $ | 865 | $ | 838 | $ | 27 | |||||||||||

| Pipeline Systems | 11 | 10 | 1 | ||||||||||||||

| Terminals | 88 | 71 | 17 | ||||||||||||||

| Total | $ | 964 | $ | 919 | $ | 45 | |||||||||||

| Year Ended December 31, | Year Ended | ||||||||||||||||

| 2023 | 2022 | Change | |||||||||||||||

| Reconciliation of net income to Adjusted EBITDA: | |||||||||||||||||

| Net income | $ | 394 | $ | 475 | $ | (81) | |||||||||||

| Depreciation, amortization and accretion | 187 | 193 | (6) | ||||||||||||||

| Interest expense, net | 217 | 182 | 35 | ||||||||||||||

| Non-cash unit-based compensation expense | 17 | 14 | 3 | ||||||||||||||

| Gain on disposal of assets | (7) | (13) | 6 | ||||||||||||||

| Unrealized (gains) losses on commodity derivatives | (21) | 21 | (42) | ||||||||||||||

| Inventory valuation adjustments | 114 | (5) | 119 | ||||||||||||||

| Equity in earnings of unconsolidated affiliates | (5) | (4) | (1) | ||||||||||||||

| Adjusted EBITDA related to unconsolidated affiliates | 10 | 10 | — | ||||||||||||||

| Other non-cash adjustments | 22 | 20 | 2 | ||||||||||||||

| Income tax expense | 36 | 26 | 10 | ||||||||||||||

| Adjusted EBITDA (consolidated) | $ | 964 | $ | 919 | $ | 45 | |||||||||||

The following discussion of results compares the operations for the years ended December 31, 2023 and 2022.

Net Income and Comprehensive Income. Total net income and comprehensive income for 2023 was $394 million, a decrease of $81 million from 2022. The decrease was primarily attributable to the following changes:

•an increase in interest expense, general and administrative expenses and other operating expense of $59 million in the aggregate. These increases are discussed in more detail below; and

•a decrease in motor fuel profit of $51 million (including unrealized valuation adjustments), which was primarily due to unfavorable inventory adjustments in the current year (see below for explanation of inventory adjustments), partially offset by an increase in volume; partially offset by

•an increase in non-motor fuel profit and lease income of $37 million in the aggregate. These items are discussed in more detail below.

10

Adjusted EBITDA. Total Adjusted EBITDA for 2023 was $964 million, an increase of $45 million from 2022. The increase was primarily attributable to the following changes:

•an increase in the profit on motor fuel sales of $34 million, primarily due to an 8.1% increase in gallons sold; and

•an increase in non-motor fuel profit of $37 million, primarily due to increased throughput and storage margin from the Gladieux and Zenith acquisitions and increased rental income; partially offset by

•an increase in operating costs of $26 million, including other operating expense, general and administrative expense and lease expense. The increase was primarily due to higher costs as a result of the recent acquisitions of refined product terminals and the transmix processing and terminal facility.

Interest Expense. Interest expense was $217 million in 2023, an increase of $35 million from 2022. This increase was primarily attributable to higher interest rates on floating rate debt for the respective periods.

Gain on Disposal of Assets. Gains on disposals of assets reflect the difference between the net book value of disposed assets and the proceeds received upon disposal of those assets. For 2023 and 2022, proceeds from disposal of property and equipment were $31 million and $32 million, respectively.

Unrealized (Gain) Loss on Commodity Derivatives. The unrealized gains and losses on our commodity derivatives represent the changes in fair value of our commodity derivatives. The change in unrealized gains and losses between periods was impacted by the notional amounts and commodity price changes on our commodity derivatives. Additional information on commodity derivatives is included in “Item 7A. Quantitative and Qualitative Disclosures about Market Risk” in our Form 10-K filed on February 16, 2024.

Inventory Adjustments. Inventory adjustments represent changes in lower of cost or market reserves on the Partnership’s inventory. These amounts are unrealized valuation adjustments applied to fuel volumes remaining in inventory at the end of the period. For 2023, a decline in fuel prices caused lower of cost or market reserve requirements to increase by $114 million, which reduced net income. For 2022, an increase in fuel prices caused lower of cost or market reserve requirements to decrease by $5 million, which increased net income.

Income Tax Expense. Income tax expense for 2023 was $36 million, an increase of $10 million from 2022. The increase was primarily attributable to a favorable state rate change in the prior period.

Segment Operating Results

We evaluate segment performance based on Segment Adjusted EBITDA, which we believe is an important performance measure of the core profitability of our operations. This measure represents the basis of our internal financial reporting and is one of the performance measures used by senior management in deciding how to allocate capital resources among business segments.

The following tables identify the components of Segment Adjusted EBITDA, which is calculated as follows:

•Segment profit, operating expenses and selling, general and administrative expenses. These amounts represent the amounts included in our consolidated financial statements that are attributable to each segment.

•Adjusted EBITDA related to unconsolidated affiliates. Adjusted EBITDA related to unconsolidated affiliates excludes the same items with respect to the unconsolidated affiliate as those excluded from the calculation of Segment Adjusted EBITDA, such as interest, taxes, depreciation, depletion, amortization and other non-cash items. Although these amounts are excluded from Adjusted EBITDA related to unconsolidated affiliates, such exclusion should not be understood to imply that we have control over the operations and resulting revenues and expenses of such affiliates. We do not control our unconsolidated affiliates; therefore, we do not control the earnings or cash flows of such affiliates.

The following analysis of segment operating results includes a measure of segment profit. Segment profit is a non-GAAP financial measure and is presented herein to assist in the analysis of segment operating results and particularly to facilitate an understanding of the impacts that changes in sales revenues have on the segment performance measure of Segment Adjusted EBITDA. Segment profit is similar to the GAAP measure of gross profit, except that segment profit excludes charges for depreciation, depletion and amortization. Among the GAAP measures reported by the Partnership, the most directly comparable measure to segment profit is Segment Adjusted EBITDA; a reconciliation of segment profit to Segment Adjusted EBITDA is included in the following tables for each segment where segment profit is presented.

In addition, for the Fuel Distribution segment, the following sections include information on the components of segment profit by sales type, which components are included in order to provide additional disaggregated information to facilitate the analysis of segment profit and Segment Adjusted EBITDA. These components of segment profit are calculated consistent with the calculation of segment profit; therefore, these components also exclude charges for depreciation, depletion and amortization.

11

Fuel Distribution

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | Change | |||||||||||||||

| Motor fuel gallons sold | 8,317 | 7,587 | 730 | ||||||||||||||

| Motor fuel profit cents per gallon | 12.5 | ¢ | 12.5 | ¢ | — | ¢ | |||||||||||

| Fuel profit | $ | 926 | $ | 956 | $ | (30) | |||||||||||

| Non-fuel profit | 148 | 142 | 6 | ||||||||||||||

| Lease profit | 151 | 143 | 8 | ||||||||||||||

Fuel Distribution segment profit(1) | $ | 1,225 | $ | 1,241 | $ | (16) | |||||||||||

| Expenses | $ | 480 | $ | 453 | $ | 27 | |||||||||||

| Segment Adjusted EBITDA | $ | 865 | $ | 838 | $ | 27 | |||||||||||

(1)For the year ended December 31, 2023, Fuel Distribution segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $480 million and adding non-cash unit based compensation of $17 million, subtracting unrealized gains on commodity derivatives of $21 million, adding inventory valuation adjustments of $95 million and adding other of $29 million. For the year ended December 31, 2022, Fuel Distribution segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $453 million and adding non-cash unit based compensation of $13 million, adding unrealized loss of $21 million, subtracting inventory valuation adjustments of $5 million and adding other of $21 million.

Volumes. For the year ended December 31, 2023 compared to the same period last year, volumes increased primarily due to growth from investments and profit optimization strategies.

Segment Adjusted EBITDA. For the year ended December 31, 2023 compared to the same period last year, Segment Adjusted EBITDA related to our Fuel Distribution segment increased due primarily to increase in profit on motor fuel sales due primarily to an increase in gallons sold.

Pipeline Systems

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | Change | |||||||||||||||

| Pipelines throughput (barrels per day) | — | — | — | ||||||||||||||

Pipeline Systems segment profit(1) | $ | 3 | $ | — | $ | 3 | |||||||||||

| Expenses | $ | 2 | $ | — | $ | 2 | |||||||||||

| Segment Adjusted EBITDA | $ | 11 | $ | 10 | $ | 1 | |||||||||||

(1)For the year ended December 31, 2023, Pipeline Systems segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $2 million and adding $10 million of Adjusted EBITDA related to unconsolidated affiliates. For the year ended December 31, 2022, Pipeline Systems segment profit reconciles to Segment Adjusted EBITDA by adding $10 million of Adjusted EBITDA related to unconsolidated affiliates.

Terminals

| Year Ended December 31, | |||||||||||||||||

| 2023 | 2022 | Change | |||||||||||||||

| Throughput (thousand barrels per day) | 399 | 343 | 56 | ||||||||||||||

Terminals segment profit(1) | $ | 137 | $ | 138 | $ | (1) | |||||||||||

| Expenses | $ | 68 | $ | 68 | $ | — | |||||||||||

| Segment Adjusted EBITDA | $ | 88 | $ | 71 | $ | 17 | |||||||||||

(1)For the year ended December 31, 2023, Terminals segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $68 million and adding inventory valuation adjustments of $19 million. For the year ended December 31, 2022, Terminals segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $68 million and adding non-cash unit based compensation of $1 million.

12

Volumes. For the year ended December 31, 2022 compared to the same period last year, volumes increased due to recently acquired assets.

Segment Adjusted EBITDA. For the year ended December 31, 2023 compared to the same period last year, Segment Adjusted EBITDA related to our Terminals segment increased due to an increase in throughput related to recently acquired assets.

Year Ended December 31, 2022 Compared to the Year Ended December 31, 2021

Consolidated Results of Operations

| Year Ended December 31, | Year Ended | Year Ended | |||||||||||||||

| 2022 | 2021 | Change | |||||||||||||||

| Segment Adjusted EBITDA: | |||||||||||||||||

| Fuel Distribution | $ | 838 | $ | 701 | $ | 137 | |||||||||||

| Pipeline Systems | 10 | 9 | 1 | ||||||||||||||

| Terminals | 71 | 44 | 27 | ||||||||||||||

| Total | $ | 919 | $ | 754 | $ | 165 | |||||||||||

| Year Ended December 31, | Year Ended | Year Ended | |||||||||||||||

| 2022 | 2021 | Change | |||||||||||||||

| Reconciliation of net income to Adjusted EBITDA: | |||||||||||||||||

| Net income | $ | 475 | $ | 524 | $ | (49) | |||||||||||

| Depreciation, amortization and accretion | 193 | 177 | 16 | ||||||||||||||

| Interest expense, net | 182 | 163 | 19 | ||||||||||||||

| Non-cash unit-based compensation expense | 14 | 16 | (2) | ||||||||||||||

| Gain on disposal of assets | (13) | (14) | 1 | ||||||||||||||

| Loss on extinguishment of debt | — | 36 | (36) | ||||||||||||||

| Unrealized (gains) losses on commodity derivatives | 21 | (14) | 35 | ||||||||||||||

| Inventory valuation adjustments | (5) | (190) | 185 | ||||||||||||||

| Equity in earnings of unconsolidated affiliates | (4) | (4) | — | ||||||||||||||

| Adjusted EBITDA related to unconsolidated affiliates | 10 | 9 | 1 | ||||||||||||||

| Other non-cash adjustments | 20 | 21 | (1) | ||||||||||||||

| Income tax expense | 26 | 30 | (4) | ||||||||||||||

| Adjusted EBITDA (consolidated) | $ | 919 | $ | 754 | $ | 165 | |||||||||||

The following discussion of results compares the operations for the years ended December 31, 2022 and 2021.

Net Income and Comprehensive Income. Total net income and comprehensive income for 2022 was $475 million, a decrease of $49 million from 2021. The decrease is primarily attributable to the following changes:

•an increase in operating costs, interest expense and depreciation, amortization and accretion of $118 million in the aggregate. These increases are discussed in more detail below; and

•a decrease in motor fuel profit of $42 million (including unrealized valuation adjustments), which was primarily due to a favorable inventory adjustments in the prior year (see below for explanation of inventory adjustments), partially offset by an increase in both profit per gallon sold and volume; partially offset by

•an increase in non motor fuel profit, lease income and a reduction of tax expense of $75 million in the aggregate. These items are discussed in more detail below.

Adjusted EBITDA. Total Adjusted EBITDA for 2022 was $919 million, an increase of $165 million from 2021. The increase is primarily attributable to the following changes:

•an increase in the profit on motor fuel sales of $178 million, primarily due to a 14.2% increase in profit per gallon sold and a 2.3% increase in gallons sold; and

•an increase in non motor fuel profit of $70 million, primarily due to an increase in storage tanks and terminals profit in 2022. This increase was primarily a result of the 2021 fourth quarter acquisition of refined product terminals. In addition, increased credit card transactions and merchandise gross profit contributed $18 million to the overall increase; partially offset by

13

•an increase in operating costs of $84 million. These expenses include other operating expense, general and administrative expense and lease expense. The increase was primarily due to higher costs as a result of the recent acquisitions of refined product terminals and the transmix processing and terminal facility, higher employee costs, credit card processing fees, advertising costs, legal costs, insurance costs and maintenance costs.

Depreciation, Amortization and Accretion. Depreciation, amortization and accretion was $193 million in 2022, an increase of $16 million from 2021. This increase is primarily due to the acquisitions of refined product terminals and the transmix processing and terminal facility.

Interest Expense. Interest expense was $182 million in 2022, an increase of $19 million from 2021. This increase is primarily attributable to an increase in average total long-term debt and increase in the weighted average interest rate on long-term debt for the respective periods.

Non-Cash Unit-Based Compensation Expense. Non-cash unit-based compensation expense was $14 million in 2022, a slight decrease of $2 million from 2021.

Gain on Disposal of Assets. Gains on disposals of assets reflect the difference between the net book value of disposed assets and the proceeds received upon disposal of those assets. For 2022 and 2021, proceeds of disposal from property and equipment were $32 million and $34 million, respectively.

Loss on Extinguishment of Debt. Loss on extinguishment of debt of $36 million in 2021 was related to the repurchase of the Partnership’s outstanding 2026 senior notes.

Unrealized Gain (Loss) on Commodity Derivatives. The unrealized gains and losses on our commodity derivatives represent the changes in fair value of our commodity derivatives. The change in unrealized gains and losses between periods is impacted by the notional amounts and commodity price changes on our commodity derivatives. Additional information on commodity derivatives is included in “Item 7A. Quantitative and Qualitative Disclosures about Market Risk” in our Form 10-K filed on February 16, 2024.

Inventory Adjustments. Inventory adjustments represent changes in lower of cost or market reserves on the Partnership’s inventory. These amounts are unrealized valuation adjustments applied to fuel volumes remaining in inventory at the end of the period. For 2022 and 2021, an increase in fuel prices reduced lower of cost or market reserve requirements for the period by $5 million and $190 million, respectively, creating a favorable impact to net income.

Income Tax Expense. Income tax expense for 2022 was $26 million, a decrease of $4 million from income tax expense of $30 million in 2021. The decrease is primarily attributable to a favorable state rate change in the current period.

Segment Operating Results

We evaluate segment performance based on Segment Adjusted EBITDA, which we believe is an important performance measure of the core profitability of our operations. This measure represents the basis of our internal financial reporting and is one of the performance measures used by senior management in deciding how to allocate capital resources among business segments.

The following tables identify the components of Segment Adjusted EBITDA, which is calculated as follows:

•Segment profit, operating expenses and selling, general and administrative expenses. These amounts represent the amounts included in our consolidated financial statements that are attributable to each segment.

•Adjusted EBITDA related to unconsolidated affiliates. Adjusted EBITDA related to unconsolidated affiliates excludes the same items with respect to the unconsolidated affiliate as those excluded from the calculation of Segment Adjusted EBITDA, such as interest, taxes, depreciation, depletion, amortization and other non-cash items. Although these amounts are excluded from Adjusted EBITDA related to unconsolidated affiliates, such exclusion should not be understood to imply that we have control over the operations and resulting revenues and expenses of such affiliates. We do not control our unconsolidated affiliates; therefore, we do not control the earnings or cash flows of such affiliates.

The following analysis of segment operating results includes a measure of segment profit. Segment profit is a non-GAAP financial measure and is presented herein to assist in the analysis of segment operating results and particularly to facilitate an understanding of the impacts that changes in sales revenues have on the segment performance measure of Segment Adjusted EBITDA. Segment profit is similar to the GAAP measure of gross profit, except that segment profit excludes charges for depreciation, depletion and amortization. Among the GAAP measures reported by the Partnership, the most directly comparable measure to segment profit is Segment Adjusted EBITDA; a reconciliation of segment profit to Segment Adjusted EBITDA is included in the following tables for each segment where segment profit is presented.

In addition, for the Fuel Distribution segment, the following sections include information on the components of segment profit by sales type, which components are included in order to provide additional disaggregated information to facilitate the analysis of segment profit and Segment Adjusted EBITDA. These components of segment profit are calculated consistent with the calculation of segment profit; therefore, these components also exclude charges for depreciation, depletion and amortization.

14

Fuel Distribution

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Change | |||||||||||||||

| Motor fuel gallons sold | 7,587 | 7,539 | 48 | ||||||||||||||

| Motor fuel profit cents per gallon | 12.5 | ¢ | 10.8 | ¢ | 1.7 | ¢ | |||||||||||

| Fuel profit | $ | 956 | $ | 1,006 | $ | (50) | |||||||||||

| Non-fuel profit | 142 | 123 | 19 | ||||||||||||||

| Lease profit | 143 | 138 | 5 | ||||||||||||||

Fuel Distribution segment profit(1) | $ | 1,241 | $ | 1,267 | $ | (26) | |||||||||||

| Expenses | $ | 453 | $ | 400 | $ | 53 | |||||||||||

| Segment Adjusted EBITDA | $ | 838 | $ | 701 | $ | 137 | |||||||||||

(1)For the year ended December 31, 2022, Fuel Distribution segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $453 million and adding non-cash unit based compensation of $13 million, adding unrealized loss of $21 million, subtracting inventory valuation adjustments of $5 million and adding other of $21 million. For the year ended December 31, 2021, Fuel Distribution segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $400 million and adding non-cash unit based compensation of $15 million, subtracting unrealized gain of $14 million, inventory valuation adjustments of $188 million and adding other of $21 million.

Volumes. For the year ended December 31, 2022 compared to the same period last year, volumes increased primarily due to growth from investments and profit optimization strategies.

Segment Adjusted EBITDA. For the year ended December 31, 2023 compared to the same period last year, Segment Adjusted EBITDA related to our Fuel Distribution segment increased due primarily to increase in profit on motor fuel sales due primarily to an increase in gallons sold.

Pipeline Systems

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Change | |||||||||||||||

| Pipelines throughput (barrels per day) | — | — | — | ||||||||||||||

Pipeline Systems segment profit(1) | $ | — | $ | — | $ | — | |||||||||||

| Expenses | $ | — | $ | — | $ | — | |||||||||||

| Segment Adjusted EBITDA | $ | 10 | $ | 9 | $ | 1 | |||||||||||

(1)For the years ended December 31, 2022 and 2021, Pipeline Systems segment profit reconciles to Segment Adjusted EBITDA by adding $10 million and $9 million, respectively, of Adjusted EBITDA related to unconsolidated affiliates.

Terminals

| Year Ended December 31, | |||||||||||||||||

| 2022 | 2021 | Change | |||||||||||||||

Throughput (thousand barrels per day) (1) | 343 | — | 343 | ||||||||||||||

Terminals segment profit (2) | $ | 138 | $ | 83 | $ | 55 | |||||||||||

| Expenses | $ | 68 | $ | 38 | $ | 30 | |||||||||||

| Segment Adjusted EBITDA | $ | 71 | $ | 44 | $ | 27 | |||||||||||

(1)Beginning in 2024, the Partnership reports terminal throughput as a key performance measure. Prior to 2022, the Partnership measured terminal volumes using a different methodology than it currently uses. Given this difference in methodology, as well as the impact of recent acquisitions, terminal volumes for these periods not meaningful for comparison purposes and therefore have been excluded herein.

(2)For the year ended December 31, 2022, Terminals segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $68 million and adding non-cash unit based compensation of $1 million. For the year ended December 31, 2021, Terminals segment profit reconciles to Segment Adjusted EBITDA by subtracting expenses of $38 million and adding non-cash unit based compensation of $1 million and subtracting inventory valuation adjustments of $2 million.

15

Segment Adjusted EBITDA. For the year ended December 31, 2022 compared to the same period last year, Segment Adjusted EBITDA related to our Terminals segment increased due to an increase in throughput related to recently acquired assets.

Liquidity and Capital Resources

Liquidity

Our principal liquidity requirements are to finance current operations, to fund capital expenditures, including acquisitions from time to time, to service our debt and to make distributions. We expect our ongoing sources of liquidity to include cash generated from operations, borrowings under our Credit Facility and the issuance of additional long-term debt or partnership units as appropriate given market conditions. We expect that these sources of funds will be adequate to provide for our short-term and long-term liquidity needs.

Our ability to meet our debt service obligations and other capital requirements, including capital expenditures and acquisitions, will depend on our future operating performance which, in turn, will be subject to general economic, financial, business, competitive, legislative, regulatory and other conditions, many of which are beyond our control. As a normal part of our business, depending on market conditions, we will from time to time consider opportunities to repay, redeem, repurchase or refinance our indebtedness. Changes in our operating plans, lower than anticipated sales, increased expenses, acquisitions or other events may cause us to seek additional debt or equity financing in future periods. There can be no guarantee that financing will be available on acceptable terms or at all. Debt financing, if available, could impose additional cash payment obligations and additional covenants and operating restrictions. In addition, any of the items discussed in detail under “Item 1A. Risk Factors” included in this Annual Report on Form 10-K may also significantly impact our liquidity.

The Partnership is party to a Second Amended and Restated Credit Agreement among the Partnership, as borrower, the lenders from time to time party thereto and Bank of America, N.A., as administrative agent, collateral agent, swingline lender and a line of credit issuer (the "Credit Facility"). As of December 31, 2023, we had $29 million of cash and cash equivalents on hand and borrowing capacity of $1.084 billion under the Credit Facility. Based on our current estimates, we expect to utilize capacity under the Credit Facility, along with cash from operations, to fund our announced growth capital expenditures and working capital needs; however, we may issue debt or equity securities prior to that time as we deem prudent to provide liquidity for new capital projects or other partnership purposes.

Cash Flows

Our cash flows may change in the future due to a number of factors, some of which we cannot control. These factors include regulatory changes, the price of products and services, the demand for such products and services, margin requirements resulting from significant changes in commodity prices, operational risks, the successful integration of our acquisitions and other factors.

| Year Ended December 31, | |||||||||||

| 2023 | 2022 | ||||||||||

| Net cash provided by (used in) | |||||||||||

| Operating activities | $ | 600 | $ | 561 | |||||||

| Investing activities | (288) | (464) | |||||||||

| Financing activities | (365) | (40) | |||||||||

| Net increase (decrease) in cash and cash equivalents | $ | (53) | $ | 57 | |||||||

Operating Activities

Changes in cash flows from operating activities between periods primarily result from changes in earnings, excluding the impacts of non-cash items and changes in operating assets and liabilities (net of effects of acquisitions). Non-cash items include recurring non-cash expenses, such as depreciation, depletion and amortization expense and non-cash unit-based compensation expense. Cash flows from operating activities also differ from earnings as a result of non-cash charges that may not be recurring, such as impairment charges. Our daily working capital requirements fluctuate within each month, primarily in response to the timing of payments for motor fuels, motor fuels tax and rent.

Cash Flows Provided by Operations.

Net cash provided by operations was $600 million and $561 million, for 2023, and 2022, respectively. The increase in cash flows provided by operations was primarily due to a $26 million net increase in cash basis net income compared to the prior year; partially offset by a decrease in net cash flow from operating assets and liabilities of $13 million compared to the prior year.

16

Investing Activities

Cash flows from investing activities primarily consist of capital expenditures, cash contributions to unconsolidated affiliates, cash amounts paid for acquisitions and cash proceeds from sale or disposal of assets. Changes in capital expenditures between periods primarily result from increases or decreases in our growth capital expenditures to fund our expansion projects.

Cash Flows Used in Investing Activities.

Net cash used in investing activities was $288 million and $464 million, for 2023 and 2022, respectively. Net cash used in investing activities included $111 million and $318 million of cash paid for acquisitions in 2023 and 2022, respectively. Capital expenditures were $215 million and $186 million for 2023 and 2022, respectively. Proceeds from disposal of property and equipment were $31 million and $32 million in 2023 and 2022, respectively. Distributions from unconsolidated affiliates in excess of cumulative earnings were $9 million in 2023 and $8 million in 2022.

Financing Activities

Changes in cash flows from financing activities between periods primarily result from changes in the levels of borrowings and equity issuances, which are primarily used to fund our acquisitions and growth capital expenditures. Distributions increase between the periods based on increases in the number of common units outstanding or increases in the distribution rate.

Cash Flows Used in Financing Activities.

Net cash used in financing activities was $365 million and $40 million for 2023 and 2022, respectively.

Year Ended December 31, 2023

During the year ended December 31, 2023 we:

•issued $500 million of 7.000% senior notes due 2028;

•borrowed $3.3 billion and repaid $3.8 billion under the Credit Facility to fund daily operations; and

•paid $371 million in distributions to our unitholders, of which $171 million was paid to Energy Transfer.

Year Ended December 31, 2022

During the year ended December 31, 2022 we:

• borrowed $4.1 billion and repaid $3.8 billion under the Credit Facility to fund daily operations; and

• paid $359 million in distributions to our unitholders, of which $166 million was paid to Energy Transfer.

We intend to pay cash distributions to the holders of our common units and Class C Units on a quarterly basis, to the extent we have sufficient cash from our operations after establishment of cash reserves and payment of fees and expenses, including payments to our General Partner and its affiliates. Class C unitholders receive distributions at a fixed rate equal to $0.8682 per quarter for each Class C Unit outstanding. There is no guarantee that we will pay a distribution on our units. On January 25, 2024, we declared a quarterly distribution of $0.8420 per common unit based on the results for the three months ended December 31, 2023, excluding distributions to Class C unitholders. The distribution will be approximately $71 million in the aggregate for common units and approximately $19 million with respect to IDRs, and will be paid on February 20, 2024 to all unitholders of record on February 7, 2024.

Capital Expenditures

Included in our capital expenditures for 2023 was $70 million in maintenance capital and $145 million in growth capital. Growth capital relates primarily to dealer and distributor supply contracts and terminals.

We currently expect to spend approximately $70 million in maintenance capital and at least $200 million in growth capital for the full year 2024.

17

Description of Indebtedness

Our outstanding consolidated indebtedness was as follows:

| December 31, 2023 | December 31, 2022 | ||||||||||

| Credit Facility | $ | 411 | $ | 900 | |||||||

| 6.000% Senior Notes due 2027 | 600 | 600 | |||||||||

| 5.875% Senior Notes due 2028 | 400 | 400 | |||||||||

| 7.000% Senior Notes due 2028 | 500 | — | |||||||||

| 4.500% Senior Notes due 2029 | 800 | 800 | |||||||||

| 4.500% Senior Notes due 2030 | 800 | 800 | |||||||||

| Lease-related financing obligations | 94 | 94 | |||||||||

| Total debt | 3,605 | 3,594 | |||||||||

| Less: debt issuance costs | 25 | 23 | |||||||||

| Long-term debt, net of current maturities | $ | 3,580 | $ | 3,571 | |||||||

Credit Facility

As of December 31, 2023, the balance on the Credit Facility was $411 million, and $5 million in standby letters of credit were outstanding. The unused availability on the Credit Facility at December 31, 2023 was $1.1 billion. The weighted average interest rate on the total amount outstanding at December 31, 2023 was 7.54%. The Partnership was in compliance with all financial covenants at December 31, 2023.

Recent Financing Transaction

On September 20, 2023, we and Sunoco Finance Corp. completed a private offering of $500 million in aggregate principal amount of 7.000% senior notes due 2028. The Partnership used the proceeds from the private offering to repay a portion of the outstanding borrowings under the Credit Facility.

Pending NuStar Acquisition

In connection with our acquisition of NuStar, we expect to assume NuStar’s debt and issue additional debt, aggregating approximately $4.2 billion, subsequent to which the Partnership expects to remain in compliance with all existing financial covenants.

Contractual Obligations

We periodically enter into derivatives, such as futures and options, to manage our fuel price risk on inventory in the distribution system. Fuel hedging positions are not significant to our operations. On a consolidated basis, the Partnership had a position of 1.1 million barrels with an aggregated unrealized loss of $8.6 million at December 31, 2023.

Off-Balance Sheet Arrangements

We do not maintain any off-balance sheet arrangements for the purpose of credit enhancement, hedging transactions or other financial or investment purposes.

Critical Accounting Estimates

We prepare our consolidated financial statements in conformity with GAAP. The preparation of these consolidated financial statements requires us to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues, expenses and disclosure of contingent assets and liabilities as of the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Critical accounting policies are those we believe are both most important to the portrayal of our financial condition and results of operations, and require our most difficult, subjective or complex judgments, often as a result of the need to make estimates about the effects of matters that are inherently uncertain. Judgments and uncertainties affecting the application of those policies may result in materially different amounts being reported under different conditions or using different assumptions.

We believe the following policies will be the most critical in understanding the judgments that are involved in preparation of our consolidated financial statements.

18

Fair Value Estimates in Business Combination Accounting and Impairment of Long-Lived Assets, Goodwill, Intangible Assets and Investments in Unconsolidated Affiliates. Business combination accounting and quantitative impairment testing are required from time to time due to the occurrence of events, changes in circumstances, or annual testing requirements. For business combinations, assets and liabilities are required to be recorded at estimated fair value in connection with the initial recognition of the transaction. For impairment testing, long-lived assets are required to be tested for recoverability whenever events or changes in circumstances indicate that the carrying amount of the asset may not be recoverable. Goodwill and intangibles with indefinite lives must be tested for impairment annually or more frequently if events or changes in circumstances indicate that the related asset might be impaired. An impairment of an investment in an unconsolidated affiliate is recognized when circumstances indicate that a decline in the investment value is other than temporary. An impairment loss should be recognized only if the carrying amount of the asset/goodwill is not recoverable and exceeds its fair value. Calculating the fair value of assets or reporting units in connection with business combination accounting or impairment testing requires management to make several estimates, assumptions and judgements, and in some circumstances management may also utilize third-party specialists to assist and advise on those calculations.

In order to allocate the purchase price in a business combination or to test for recoverability when performing a quantitative impairment test, we must make estimates of projected cash flows related to the asset, which include, but are not limited to, assumptions about the use or disposition of the asset, estimated remaining life of the asset, and future expenditures necessary to maintain the asset’s existing service potential. In order to determine fair value, we make certain estimates and assumptions, including, among other things, changes in general economic conditions in regions in which our markets are located, the availability and prices of commodities, our ability to negotiate favorable sales agreements, the risks that exploration and production activities will not occur or be successful, our dependence on certain significant customers and producers, and competition from other companies, including major energy producers. While we believe we have made reasonable assumptions to calculate the fair value, if future results are not consistent with our estimates, we could be exposed to future impairment losses that could be material to our results of operations.

The Partnership determines the fair value of our reporting units using the discounted cash flow method, the guideline company method, or a weighted combination of these methods. Determining the fair value of a reporting unit requires judgment and the use of significant estimates and assumptions. Such estimates and assumptions include revenue growth rates, operating margins, weighted average costs of capital and future market conditions, among others. The Partnership believes the estimates and assumptions used in our impairment assessments are reasonable and based on available market information, but variations in any of the assumptions could result in materially different calculations of fair value and determinations of whether or not an impairment is indicated. Under the discounted cash flow method, the Partnership determines fair value based on estimated future cash flows of each reporting unit including estimates for capital expenditures, discounted to present value using the risk-adjusted industry rate, which reflect the overall level of inherent risk of the reporting unit. Cash flow projections are derived from one year budgeted amounts plus an estimate of later period cash flows, all of which are determined by management. Subsequent period cash flows are developed for each reporting unit using growth rates that management believes are reasonably likely to occur. Under the guideline company method, the Partnership determines the estimated fair value of each of our reporting units by applying valuation multiples of comparable publicly-traded companies to each reporting unit’s projected EBITDA and then averaging that estimate with similar historical calculations using a three year average. In addition, the Partnership estimates a reasonable control premium representing the incremental value that accrues to the majority owner from the opportunity to dictate the strategic and operational actions of the business.

One key assumption in these fair value calculations is management’s estimate of future cash flows and EBITDA. In accounting for a business combination, these estimates are generally based on the forecasts that were used to analyze the deal economics. For impairment testing, these estimates are based on the annual budget for the upcoming year and forecasted amounts for multiple subsequent years. The annual budget process is typically completed near the annual goodwill impairment testing date, and management uses the most recent information for the annual impairment tests. The forecast is also subjected to a comprehensive update annually in conjunction with the annual budget process and is revised periodically to reflect new information and/or revised expectations. The estimates of future cash flows and EBITDA are subjective in nature and are subject to impacts from the business risks described in “Item 1A. Risk Factors.” Therefore, the actual results could differ significantly from the amounts used for business combination accounting and impairment testing, and significant changes in fair value estimates could occur in a given period. Such changes in fair value estimates could result in changes to the fair value estimates used in business combination accounting, which could significantly impact results of operations in a period subsequent to the business combination, depending on multiple factors, including the timing of such changes. In the case of impairment testing, such changes could result in additional impairments in future periods; therefore, the actual results could differ significantly from the amounts used for goodwill impairment testing, and significant changes in fair value estimates could occur in a given period, resulting in additional impairments.

In addition, we may change our method of impairment testing, including changing the weight assigned to different valuation models. Such changes could be driven by various factors, including the level of precision or availability of data for our assumptions. Any changes in the method of testing could also result in an impairment or impact the magnitude of an impairment.

Management does not believe that any of the Partnership’s goodwill balances, long-lived assets or investments in unconsolidated affiliates is currently at significant risk of a material impairment.

19

Income Taxes. As a limited partnership, we are generally not subject to state and federal income tax and would therefore not recognize deferred income tax liabilities and assets for the expected future income tax consequences of temporary differences between financial statement carrying amounts and the related income tax basis. We are, however, subject to a statutory requirement that our non-qualifying income cannot exceed 10% of our total gross income, determined on a calendar year basis under the applicable income tax provisions. If the amount of our non-qualifying income exceeds this statutory limit, we would be taxed as a corporation. Accordingly, certain activities that generate non-qualifying income are conducted through our wholly owned taxable corporate subsidiaries for which we have recognized deferred income tax liabilities and assets. These balances, as well as any income tax expense, are determined through management’s estimations, interpretation of tax laws of multiple jurisdictions and tax planning strategies. If our actual results differ from estimated results due to changes in tax laws, our effective tax rate and tax balances could be affected. As such, these estimates may require adjustments in the future as additional facts become known or as circumstances change.

The benefit of an uncertain tax position can only be recognized in the consolidated financial statements if management concludes that it is more likely than not that the position will be sustained with the tax authorities. For a position that is likely to be sustained, the benefit recognized in the consolidated financial statements is measured at the largest amount that is greater than 50% likely of being realized. In determining the future tax consequences of events that have been recognized in our consolidated financial statements or tax returns, judgment is required. Differences between the anticipated and actual outcomes of these future tax consequences could have a material impact on our consolidated results of operations or financial position.

Item 8. Financial Statements and Supplementary Data

20

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

F-2 | |||||

F-4 | |||||

F-5 | |||||

F-6 | |||||

Consolidated Statements of Cash Flows | F-7 | ||||

F-8 | |||||

F-8 | |||||

F-8 | |||||

F-13 | |||||

F-14 | |||||

F-14 | |||||

F-15 | |||||

F-15 | |||||

F-16 | |||||

F-17 | |||||

F-18 | |||||

F-19 | |||||

F-19 | |||||

F-21 | |||||

F-24 | |||||

F-24 | |||||

F-24 | |||||

F-25 | |||||

F-27 | |||||

F-27 | |||||

F-29 | |||||

F-1

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Board of Directors of Sunoco GP LLC and

Unitholders of Sunoco LP

Opinion on the financial statements

We have audited the accompanying consolidated balance sheets of Sunoco LP (a Delaware limited partnership) and subsidiaries (the “Partnership”) as of December 31, 2023 and 2022, the related consolidated statements of operations and comprehensive income, equity, and cash flows for each of the three years in the period ended December 31, 2023, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Partnership as of December 31, 2023 and 2022, and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2023, in conformity with accounting principles generally accepted in the United States of America.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (“PCAOB”), the Partnership’s internal control over financial reporting as of December 31, 2023, based on criteria established in the 2013 Internal Control—Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”), and our report dated February 16, 2024 (not separately included herein), expressed an unqualified opinion.

Basis for opinion

These financial statements are the responsibility of the Partnership’s management. Our responsibility is to express an opinion on the Partnership’s financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Partnership in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

Critical audit matter

The critical audit matter communicated below is a matter arising from the current period audit of the financial statements that was communicated or required to be communicated to the audit committee and that: (1) relates to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective, or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the financial statements, taken as a whole, and we are not, by communicating the critical audit matter below, providing a separate opinion on the critical audit matter or on the accounts or disclosures to which it relates.

Fair value of property and equipment acquired in the Zenith Energy acquisition