UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

Form 10-K

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2013

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-35630

Hi-Crush Partners LP

(Exact name of registrant as specified in its charter)

Delaware | 90-0840530 |

(State or Other Jurisdiction of | (I.R.S. Employer |

Incorporation or Organization) | Identification No.) |

Three Riverway, Suite 1550 | |

Houston, Texas | 77056 |

(Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code (713) 960-4777

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common units representing limited partnership interests | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes þ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

¨ Yes þ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

þ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

¨ Yes þ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

þ Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ | Accelerated filer þ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

(Do not check if a smaller reporting company.) | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

¨ Yes þ No

As of June 28, 2013, the last business day of the registrant's most recently completed second fiscal quarter, the aggregate market value of common units held by non-affiliates was approximately $329,389,211 based on the closing price of $23.55 per common unit on that date.

The registrant had 15,233,335 common units, 13,640,351 subordinated units and 3,750,000 convertible class B units outstanding on February 28, 2014.

INDEX TO FORM 10-K

PART I | Page | |

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

PART II | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

PART III | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

PART IV | ||

Item 15. | ||

Forward-Looking Statements

Some of the information in this Annual Report on Form 10-K may contain forward-looking statements. Forward-looking statements give our current expectations, contain projections of results of operations or of financial condition, or forecasts of future events. Words such as “may,” “assume,” “forecast,” “position,” “predict,” “strategy,” “expect,” “intend,” “plan,” “estimate,” “anticipate,” “believe,” “project,” “budget,” “potential,” or “continue,” and similar expressions are used to identify forward-looking statements. They can be affected by assumptions used or by known or unknown risks or uncertainties. Consequently, no forward-looking statements can be guaranteed. When considering these forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this Annual Report on Form 10-K. Actual results may vary materially. You are cautioned not to place undue reliance on any forward-looking statements. You should also understand that it is not possible to predict or identify all such risk factors and as such should not consider the following to be a complete list of all potential risks and uncertainties. Factors that could cause our actual results to differ materially from the results contemplated by such forward-looking statements include those described under “Risk Factors” in Item 1A of this Annual Report on Form 10-K, and the following factors, among others:

• | the amount of frac sand we are able to excavate and process, which could be adversely affected by, among other things, operating difficulties and unusual or unfavorable geologic conditions; |

• | the volume of frac sand we are able to buy and sell; |

• | the price at which we are able to buy and sell frac sand; |

• | changes in the price and availability of natural gas, diesel fuel or electricity; |

• | changes in prevailing economic conditions; |

• | unanticipated ground, grade or water conditions; |

• | inclement or hazardous weather conditions, including flooding, and the physical impacts of climate change; |

• | environmental hazards; |

• | difficulties in obtaining or renewing environmental permits; |

• | industrial accidents; |

• | changes in laws and regulations (or the interpretation thereof) related to the mining and hydraulic fracturing industries, silica dust exposure or the environment; |

• | the outcome of litigation, claims or assessments, including unasserted claims; |

• | inability to acquire or maintain necessary permits or mining or water rights; |

• | facility shutdowns in response to environmental regulatory actions; |

• | inability to obtain necessary production equipment or replacement parts; |

• | reduction in the amount of water available for processing; |

• | technical difficulties or failures; |

• | labor disputes and disputes with our excavation contractor; |

• | late delivery of supplies; |

• | difficulty collecting receivables; |

• | inability of our customers to take delivery; |

• | fires, explosions or other accidents; |

• | cave-ins, pit wall failures or rock falls; |

• | our ability to borrow funds and access capital markets; |

• | changes in the political environment of the drilling basins in which we and our customers operate; and |

• | changes in railroad infrastructure, price, capacity and availability, including the potential for rail line washouts. |

All forward-looking statements are expressly qualified in their entirety by the foregoing cautionary statements. You should assess any forward-looking statements made within this Annual Report on Form 10-K within the context of such risks and uncertainties.

1

PART I

2

ITEM 1. BUSINESS

References in this Annual Report on Form 10-K to “Hi-Crush Partners LP,” “we,” “our,” “us” or like terms when used in a historical context to reference operations or matters prior to August 16, 2012 refer to the business of Hi-Crush Proppants LLC, which is our accounting predecessor that contributed certain of its subsidiaries to Hi-Crush Partners LP on August 16, 2012 in connection with our initial public offering. Otherwise, those terms refer to Hi-Crush Partners LP and its subsidiaries. References in this Annual Report on Form 10-K to “Hi-Crush Proppants LLC,” “our predecessor,” “our sponsor” and “the selling unitholder” refer to Hi-Crush Proppants LLC.

General

Hi-Crush Partners LP (together with its subsidiaries, the “Partnership”) is a Delaware limited partnership formed on May 8, 2012 to acquire selected sand reserves and related processing and transportation facilities of Hi-Crush Proppants LLC. In connection with its formation, the Partnership issued a non-economic general partner interest to Hi-Crush GP LLC, our general partner and a 100.0% limited partner interest to our sponsor, its organizational limited partner.

Initial Public Offering

On August 16, 2012, we completed our initial public offering (“IPO”) of 12,937,500 common units (amount includes 1,687,500 common units issued pursuant to the exercise of the underwriters’ over-allotment option) representing limited partner interests in the Partnership at a price to the public of $17.00 per common unit. Total net proceeds paid to our sponsor from the sale of common units in our IPO were $206.5 million after taking into account our underwriting discount.

Acquisition of Preferred Interest in Augusta Facility

On January 31, 2013, we entered into a contribution agreement with our sponsor to acquire a preferred interest in Hi-Crush Augusta LLC (“Augusta”), the entity that owns the sponsor’s Augusta raw frac sand processing facility, for $37.5 million in cash and 3.75 million of our convertible Class B Units (the “Class B Units”) representing limited partner interests in the Partnership. As of December 31, 2013, Augusta’s principal assets include 46.8 million tons of proven recoverable reserves of frac sand meeting API specifications on 1,187 acres, and its processing facilities with an annual rated capacity of 1,600,000 tons.

Our sponsor will not receive distributions on the Class B Units until converted into common units of the Partnership. The Class B Units are eligible for conversion into common units once we have, for two consecutive quarters, (i) generated operating surplus at least equal to $2.31 per common unit, subordinated unit and Class B Unit on an annualized basis and (ii) paid $2.10 per unit in annualized distributions on each common and subordinated unit, or 110% of the current minimum quarterly distribution for a period of two consecutive quarters, and our general partner has determined, with the concurrence of the conflicts committee of the board of directors of our general partner, that we are expected to maintain such performance for at least two succeeding quarters.

Under the contribution agreement, our acquired interest in Augusta entitles us to a preferred distribution of up to $3.75 million per quarter, or $15.0 million annually, in distributable cash flow. Upon the satisfaction of certain conditions, but no sooner than March 31, 2018 without the approval of the conflicts committee of the board of directors of our general partner, our acquired interest in Augusta will convert into a 20% common ownership position in Augusta.

In addition, in connection with the transaction, our sponsor waived its right to require that we assign to our sponsor a long-term customer contract for sand produced from our Wyeville facility. This contract was initially scheduled to be assigned to Augusta on May 1, 2013.

Acquisition of D & I Silica, LLC

On June 10, 2013, the Partnership acquired an independent frac sand supplier, D & I Silica, LLC (“D&I”), transforming the Partnership into an integrated Northern White frac sand producer, transporter, marketer and distributor. The Partnership acquired D&I for $95.2 million in cash and 1,578,947 common units. Founded in 2006, D&I was the largest independent frac sand supplier to the oil and gas industry drilling in the Marcellus and Utica shales, operating through an extensive logistics network of rail-served origin and destination terminals located in the Midwest near supply sources and strategically throughout Pennsylvania, Ohio and New York.

Overview

We are a pure play, low-cost, domestic producer and supplier of premium monocrystalline sand, a specialized mineral that is used as a proppant to enhance the recovery rates of hydrocarbons from oil and natural gas wells. Our reserves consist of “Northern White” sand, a resource existing predominately in Wisconsin and limited portions of the upper Midwest region of the United States, which is highly valued as a preferred proppant because it exceeds all American Petroleum Institute (“API”) specifications. We own, operate and develop sand reserves and related excavation and processing facilities and will seek to acquire or develop additional facilities. Our 651-acre facility with integrated rail infrastructure located near Wyeville, Wisconsin (the “Wyeville

3

facility”), enables us to process and cost-effectively deliver approximately 1,600,000 tons of frac sand per year. We also own a preferred interest in Hi-Crush Augusta LLC, a subsidiary of our sponsor, which owns a 1,187-acre facility with integrated rail infrastructure located in Eau Claire County, Wisconsin (the “Augusta facility”) and enables our sponsor to process and cost-effectively deliver approximately 1,600,000 tons of frac sand per year. A substantial portion of our frac sand production is sold to leading pressure pumping service providers under long-term contracts that require our customers to pay a specified price for a specified volume of frac sand each month.

Over the past decade, exploration and production companies have increasingly focused on exploiting the vast hydrocarbon reserves contained in North America’s unconventional oil and natural gas reservoirs through advanced techniques, such as horizontal drilling and hydraulic fracturing. In recent years, this focus has resulted in exploration and production companies drilling more and longer horizontal wells, completing more hydraulic fracturing stages per well and utilizing more proppant per stage in an attempt to efficiently maximize the volume of hydrocarbon recovery per wellbore. As a result, North American demand for proppant has increased rapidly, growing at an average annual rate of 33.5% from 2007 to 2012, with total annual sales of $4.7 billion in 2012, according to The Freedonia Group, Inc. We believe that the market for raw frac sand will continue to grow based on the expected long-term development of North America’s unconventional oil and natural gas reservoirs and the previously highlighted market dynamics.

We utilize the significant oil and natural gas industry experience of our management team to take advantage of what we believe are favorable, long-term market dynamics as we execute our growth strategy, which includes the acquisition of additional frac sand reserves, the development of new excavation and processing facilities and the development of new terminal facilities. We expect to have the opportunity to acquire significant additional acreage and reserves currently owned or under an agreement to be acquired by our sponsor, including the Augusta facility with 1,187 acres of land and associated reserves in western Wisconsin to which we have a right of first offer until August 20, 2015, in addition to potential acquisitions from third parties. Our sponsor will not, however, be required to accept any offer we make, and may, following good faith negotiations with us, sell the assets subject to our right of first offer to third parties that may compete with us. Our sponsor may also elect to develop, retain and operate properties in competition with us or develop new assets that are not subject to our right of first offer.

We intend to remain solely focused on the frac sand market as we believe it offers attractive long-term growth fundamentals.

Assets and Operations

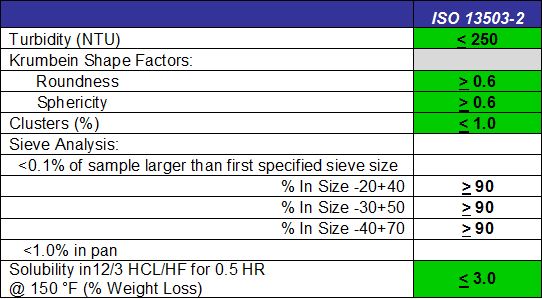

We own and operate the Wyeville facility, which is located in Monroe County, Wisconsin and, as of December 31, 2013, contained 62.6 million tons of proven recoverable reserves of frac sand meeting API specifications. We also own a preferred interest in our sponsor’s Augusta facility, which is located in Eau Claire County, Wisconsin and, as of December 31, 2013, contained 46.8 million tons of proven recoverable reserves of frac sand meeting API specifications. According to John T. Boyd Company, a leading mining consulting firm focused on the mineral and natural gas industries (“John T. Boyd”), our proven reserves consist entirely of coarse grade “Northern White” sand exceeding API specifications. Analysis of our sand by independent third-party testing companies indicates that it demonstrates characteristics in excess of API specifications with regard to crush strength (ability to withstand high pressures), turbidity (low levels of contaminants) and roundness and sphericity (facilitates hydrocarbon flow, or conductivity).

As a result of the D&I acquisition, as of December 31, 2013, we operated 12 destination rail-based terminal locations throughout the Marcellus and Utica shale basins and leased or owned 1,202 railcars used to transport our sand from origin to destination. Each terminal location is strategically positioned in the Marcellus and Utica shale plays to facilitate our customers' operations. Our terminals include rail-to-truck and rail-to-storage capabilities and serve as the base for most of our terminal resources and materials management services. Our terminal facilities include origin and distribution material staging areas, rail track capabilities, material handling equipment, private rail fleet, bulk storage and quality assurance services.

Wyeville Production Facility

We acquired the Wyeville acreage and commenced construction of the Wyeville facility in January 2011. We completed construction of the Wyeville facility and commenced sand excavation and processing in June 2011 with an initial plant processing capacity of 950,000 tons per year, and customer shipments were initiated in July 2011. We completed an expansion in March 2012 that increased our annual processing capacity to approximately 1,600,000 tons per year. From the Wyeville in-service date to December 31, 2013, we processed and delivered 2,996,563 tons of frac sand. As of January 1, 2014, we have contracted approximately 89% of this capacity for 2014. Assuming production at the rated capacity of 1,600,000 tons per year, and based on a reserve report prepared by John T. Boyd, our Wyeville facility has an implied reserve life of 39 years as of December 31, 2013.

We operate two dryer facilities at Wyeville with a combined nameplate input capacity, based on manufacturer specifications, of 250 tons per hour. Unless processing operations are suspended to conduct maintenance, our dryer facilities are run on a 24-hour basis. Our estimate of annual expected processing capacity assumes a 15% loss factor due to waste and an uptime efficiency of 85% of nameplate capacity, which allows approximately 55 days for downtime and maintenance. We processed and delivered 1,502,015 tons of sand during the year ended December 31, 2013.

4

All of our product from the Wyeville facility is shipped by rail from our three 5,000-foot rail spurs that connect our processing and storage facilities to a Union Pacific Railroad mainline. The length of these rail spurs and the capacity of the associated product storage silos allow us to accommodate a large number of rail cars. It also enables us to accommodate unit trains, which significantly increases our efficiency in meeting our customers’ frac sand transportation needs. Unit trains, typically 80 rail cars in length or longer, are dedicated trains chartered for a single delivery destination. Generally, unit trains receive priority scheduling and do not switch cars at various intermediate junctions, which results in a more cost-effective and expedited method of shipping than the standard method of rail shipment.

Augusta Production Facility

On January 31, 2013, we acquired a preferred interest in our sponsor’s Augusta facility. Our sponsor acquired the Augusta acreage and commenced construction of the Augusta facility in April 2012. Our sponsor completed construction of the Augusta facility and commenced sand excavation and processing in July 2012 with a plant processing rated capacity of 1,600,000 tons per year, and customer shipments were initiated in August 2012. The cash flow stream attributable to our preferred interest in Augusta is supported by a long-term contract with an investment grade customer that requires our customer to pay a specified price for a specified volume of frac sand each month.

Destination Terminal Facilities

As of December 31, 2013, we operated 12 destination rail-based terminal locations throughout the Marcellus and Utica shale basins. Our destination terminals include 251,600 tons of rail storage capacity and 31,600 tons of silo storage capacity. Our Minerva, Pittston, Smithfield and Wellsboro terminals are capable of accommodating unit trains.

We are continuously looking to increase the number of destination terminals we operate and expand our geographic footprint, allowing us to further enhance our customer service and putting us in a stronger position to take advantage of opportunistic short term pricing agreements. Our destination terminals are strategically located to provide access to Class I railroads, which enables us to cost effectively ship product from our production facilities in Wisconsin. We also have the ability to connect to short-line railroads as necessary to meet our customers’ evolving in-basin product needs. As of December 31, 2013, we leased or owned 1,202 railcars used to transport our sand from origin to destination.

Competitive Strengths

We believe that we are well positioned to successfully execute our strategy and achieve our primary business objective because of the following competitive strengths:

• | Long-term contracted cash flow stability. We generate a substantial portion of our revenues from the sale of frac sand under long-term contracts that require our customers to pay specified prices for specified volumes of product each month. We believe the volume requirements and pricing provisions and the long-term nature of our contracts provide us with a stable base of cash flows and limit the risks associated with price movements in the spot market and any changes in product demand during the contract period. As of January 1, 2014, we had contracted to sell 1,420,000 tons of frac sand annually from our Wyeville facility, with an average remaining contractual term of 2.6 years. |

• | Long-lived, high quality reserve base. Our Wyeville facility contains approximately 62.6 million tons of proven recoverable saleable coarse grade reserves as of December 31, 2013, based on a third-party reserve report by John T. Boyd and has an implied reserve life of 39 years, assuming production at the rated capacity of 1,600,000 tons per year. We also own a preferred interest in our sponsor’s Augusta facility, which, as of December 31, 2013, contained 46.8 million tons of proven reserves and has an implied reserve life of 30 years, assuming production at the rated capacity of 1,600,000 tons per year. These reserves consist of high quality Northern White frac sand. Analysis by independent third-party testing companies indicates that our sand demonstrates characteristics exceeding API specifications with regard to crush strength, turbidity and roundness and sphericity. As a result, our raw frac sand is particularly well suited for and is experiencing significant demand from customers for use in the hydraulic fracturing of unconventional oil and natural gas wells. |

• | Intrinsic logistics and infrastructure advantage. The strategic location and logistics capabilities of the Wyeville and Augusta facilities enable us to serve all major U.S. oil and natural gas producing basins. At our Wyeville and Augusta facilities, our on-site transportation assets include three 5,000-foot rail spurs off a Union Pacific Railroad mainline that are capable of accommodating unit trains, allowing our customers to receive priority scheduling, expedited delivery and a more cost-effective shipping alternative. Our logistics capabilities enable efficient loading of sand and minimize rail car turnaround times at the facility, and we expect to acquire or develop similar logistics capabilities at any facilities we own in the future. We believe we are one of the few frac sand producers with a facility initially designed to deliver frac sand exceeding API specifications to all of the major U.S. oil and natural gas producing basins by on-site rail facilities, including on-site storage capacity accommodating unit trains. |

• | Strategically located terminal facilities. We operate through an extensive logistics network of rail-served destination terminals strategically located throughout Pennsylvania, Ohio and New York to serve our customers' operations in the |

5

Marcellus and Utica basins. Our extensive distribution network allows us to better service our customers’ short-notice needs in these basins and provide our customers with solutions to the logistical challenges presented by the large volume of sand required for each fracturing job. To further enhance our customer service in the Marcellus and Utica basins, we anticipate opening additional rail-served destination terminals in that region in the second quarter of 2014. In addition, we expect to expand our geographic footprint into Texas in the second quarter of 2014 with the opening of a strategically located rail-served destination terminal to serve our customers’ needs in the Permian basin.

• | Competitive operating cost structure. Our plant operations have been strategically designed to provide low per-unit production costs with a significant variable component for the excavation and processing of our sand. Our sand reserves at the Wyeville facility do not require blasting or crushing to be processed and, due to the shallow overburden at both our Wyeville and Augusta facilities, we are able to use surface mining equipment in our operations, which provides for a lower cost structure than underground mining operations. Our mining operations are subcontracted to Gerke Excavating, Inc. at a fixed cost per ton excavated, subject to a diesel fuel surcharge. Unlike some competitors, our processing and rail loading facilities are located on-site, which eliminates the requirement for on-road transportation, lowers product movement costs and minimizes the reduction in sand quality due to handling. |

• | Experienced and incentivized management team. Our management team has extensive experience investing and operating in the oil and natural gas industry and is focused on optimizing our current business and expanding our operations through disciplined development and accretive acquisitions. We believe our management team’s substantial experience and relationships with participants in the oilfield services and exploration and production industries provide us with an extensive operational and commercial understanding of the markets in which our customers operate. The expertise of our management and operations teams covers a wide range of disciplines, with an emphasis on development, construction and operation of frac sand processing and terminal facilities, frac sand supply chain management and consulting and bulk solids material handling. Members of our management team are strongly incentivized to profitably grow our business and cash flows through their 22% direct and indirect ownership interest in our limited partnership units, and their 39% interest in our sponsor, which owned all of our subordinated units, Class B Units and incentive distribution rights as of February 28, 2014. |

Business Strategies

Our primary business objective is to increase our cash distributions per unit over time. We intend to accomplish this objective by executing the following strategies:

• | Focusing on stable, long-term contracts with key customers. A key component of our business model is our contracting strategy, which seeks to secure a high percentage of our cash flows under long-term contracts that require our customers to pay a specified price for a specified volume of frac sand each month, while also staggering the tenors of our contracts so that they expire at different times. We believe this contracting strategy significantly mitigates our exposure to the potential price volatility of the spot market for frac sand in the short-term, allows us to take advantage of any increase in frac sand prices over the medium-term and provides us with long-term cash flow stability. As current contracts expire or as we add new processing capacity, we intend to pursue similar long-term contracts with our current customers and with other leading pressure pumping service providers. We intend to utilize a substantial majority of our processing capacity to fulfill these contracts, with any excess processed frac sand sold to existing and new customers through our distribution network. |

• | Pursuing accretive acquisitions from our sponsor and third parties. On January 31, 2013, we acquired a preferred interest in our sponsor’s Augusta facility, which entitles us to a preferred distribution of up to $3.75 million per quarter, or $15.0 million annually, in distributable cash flow. On June 10, 2013, we acquired D&I, which operates through an extensive logistics network of rail-served origin and destination terminals located in the Midwest near supply sources and strategically throughout Pennsylvania, Ohio and New York. We expect to continue pursuing accretive acquisitions of frac sand facilities from our sponsor, including through our right of first offer to acquire the Augusta facility, as well as from third-party frac sand operations. As we evaluate acquisition opportunities, we intend to remain focused on operations that complement our reserves of premium frac sand and that provide or would accommodate the development and construction of rail or other advantaged logistics and distribution capabilities. We believe these factors are critical to our business model and are important characteristics for any potential acquisitions. |

• | Expanding our proved reserve base and processing capacity. We seek to identify and evaluate economically attractive expansion and facility enhancement opportunities to increase our proved reserves and processing capacity. At Wyeville and any future sites, we expect to pursue add-on acreage acquisitions near our facilities to expand our reserve base and increase our reserve life. During 2013, we commenced an additional expansion of our Wyeville facility allowing us to produce 100 mesh sand. We will continue to analyze and pursue organic expansion efforts that will similarly allow us to cost-effectively optimize our existing assets and meet the customer demand for our high quality frac sand. |

• | Expanding our distribution network. We seek to identify and evaluate destination terminal sites to expand our geographic footprint allowing us to enhance our distribution network and ensure that sand is available to meet the in-basin needs of our customers. At our existing and future sites, we expect to pursue additional storage capabilities to enhance our ability |

6

to meet short-term customer demands for the various mesh sizes of frac sand. We will continue to analyze and pursue third-party acquisition opportunities that would similarly allow us to cost-effectively expand our geographic footprint, optimize our existing assets and meet our customers' demand for our high quality frac sand.

• | Capitalizing on compelling industry fundamentals. We intend to continue to position ourselves as a pure play producer of high quality frac sand, as we believe the frac sand market offers attractive long-term growth fundamentals. The growth in horizontal drilling in the various North American shale plays and other unconventional oil and natural gas plays has resulted in greater demand for frac sand. The growth in demand is underpinned by increased horizontal drilling, higher proppant use per well and cost advantages over resin-coated sand and manufactured ceramics. We believe frac sand supply will continue to be constrained by the difficulty in finding reserves that meet or exceed API technical specifications in contiguous quantities large enough to justify the capital investment required and the challenges associated with successfully obtaining the necessary local, state and federal permits required for operations. |

• | Maintaining financial flexibility and conservative leverage. We plan to pursue a disciplined financial policy and maintain a conservative capital structure. As of February 28, 2014, we had $138.3 million of outstanding indebtedness and $60.2 million of undrawn borrowing capacity ($200 million, net of $138.3 of indebtedness and $1.5 million letter of credit commitments) under our revolving credit facility. The revolving credit facility is available to fund working capital and general corporate purposes, including the making of certain restricted payments permitted therein. Borrowings under our revolving credit facility are secured by substantially all of our assets. We believe that our borrowing capacity and ability to access debt and equity capital markets provides us with the financial flexibility necessary to achieve our organic expansion and acquisition strategy. |

Our Industry

The oil and natural gas proppant industry is comprised of businesses involved in the mining or manufacturing of the propping agents used in the drilling and completion of oil and natural gas wells. Hydraulic fracturing is the most widely used method for stimulating increased production from wells. The process consists of pumping fluids, mixed with granular proppants, into the geologic formation at pressures sufficient to create fractures in the hydrocarbon-bearing rock. Proppant-filled fractures create conductive channels through which the hydrocarbons can flow more freely from the formation into the wellbore and then to the surface.

Industry Data

The market and industry data included throughout this Annual Report on Form 10-K was obtained through our own internal analysis and research, coupled with industry publications, surveys, reports and other analysis conducted by third parties. We relied on Industry Study #3048, Proppants in North America, August 2013 (“The Freedonia Group Report”), an industry report provided by The Freedonia Group, Inc., a leading international business research company, as our primary source for third-party industry data. Industry publications, surveys, reports and other analysis generally state that the information contained therein has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe that the industry reports are generally reliable, we have not independently verified the industry data from third-party sources. While we believe our internal analysis and research is reliable and appropriate, such internal analysis and research has not been verified by any independent source.

The Freedonia Group Report pertains to North American proppant industry data through the year ended December 31, 2012. Reference herein to 2013 proppants pricing is based on our own observations, internal estimates, and consultations with third parties. We believe that such data, as it relates to the proppants industry, is accurate and we have included such 2013 pricing observations throughout this Annual Report on Form 10-K.

Types of Proppant

There are three primary types of proppant that are commonly utilized in the hydraulic fracturing process: raw frac sand, which is the product we produce, resin-coated sand and manufactured ceramic beads. The following chart illustrates the composition of the North American market for proppant by type.

7

2012 Proppant Consumed by Weight

Source: The Freedonia Group Report

Raw Frac Sand

Of the three primary types of proppant, raw frac sand is the most widely used due to its broad applicability in oil and natural gas wells and its cost advantage relative to other proppants. Raw frac sand may be used as a proppant in all but the highest pressure and temperature drilling environments, such as in the Haynesville Shale, and has been employed in nearly all major U.S. oil and natural gas producing basins.

Raw frac sand is generally mined from the surface or underground, and in some cases crushed, and then cleaned and sorted into consistent mesh sizes. The API has a range of guidelines it uses to evaluate frac sand grades and mesh sizes. In order to meet API specifications, frac sand must meet certain thresholds related to crush strength (ability to withstand high pressures), roundness and sphericity (facilitates hydrocarbon flow, or conductivity), particle size distribution, and turbidity (low levels of contaminants). Oil and gas producers generally require that frac sand used in their drilling and completion processes meet API specifications.

Raw frac sand can be further delineated into two main types: Northern White and Brady Brown. Northern White, which is the type of frac sand we produce, is considered to be of higher quality than Brady Brown and is known for its high crush strength, turbidity, roundness and sphericity and monocrystalline grain structure. Brady Brown has historically been considered the lower quality raw frac sand, as it is less monocrystalline in nature, more angular, has lower crush strength and often contains greater impurities, including feldspars and clays. Due to its quality, Northern White frac sand commands premium prices relative to Brady Brown. Northern White has historically experienced the greatest market demand relative to supply, due both to its superior physical characteristics and the fact that it is a limited resource that exists predominately in Wisconsin and other limited parts of the upper Midwest region of the United States. However, even within this superior class of Northern White sand, its quality can vary significantly across deposits due to the differing geological processes that formed the various Northern White reserves.

The term “Northern White” is a commonly-used designation for premium white sand produced in Wisconsin and other limited parts of the upper Midwest region of the United States.

Resin-Coated Frac Sand

Resin-coated frac sand consists of raw frac sand that is coated with a flexible resin that increases the sand’s crush strength and prevents crushed sand from dispersing throughout the fracture. The strength and shape of the end product are largely determined by the quality of the underlying raw frac sand. Pressured (or tempered) resin-coated sand primarily enhances crush strength, thermal stability and chemical resistance, allowing the sand to perform under harsh downhole conditions. Curable (or bonding) resin-coated frac sand uses a resin that is designed to bond together under closure stress and high temperatures, preventing proppant flowback. In general, resin-coated frac sand is better suited for higher pressure, higher temperature drilling operations commonly associated with deep wells and natural gas wells. In 2013, pricing for resin-coated frac sand was generally more than 5 times the price of raw frac sand.

Ceramics

Ceramic proppant is a manufactured product of comparatively consistent size and spherical shape that typically offers the highest crush strength relative to other types of proppants. As a result, ceramic proppant use is most applicable in the highest pressure and temperature drilling environments, such as the Haynesville Shale. Ceramic proppant derives its product strength from the molecular

8

structure of its underlying raw material and is designed to withstand extreme heat, depth and pressure environments. The deepest, highest temperature and highest pressure wells typically require heavy weight ceramics with high alumina/bauxite content and coarser mesh sizes. The lower crush resistant ceramic proppants are lighter weight and derived from kaolin clay, with densities closer to raw frac sand. In 2013, pricing for ceramic proppants was generally more than 10 times the price of raw frac sand, with bauxite-based, heavy grade ceramics commanding the highest prices.

Comparison of Key Proppant Characteristics

The following table sets forth what we believe to be the key comparative characteristics of our frac sand and the three primary types of proppant.

Products and Characteristics | ||||||

Hi-Crush Partners LP | Raw Frac Sand | Resin-Coated | Ceramics | |||

• Natural resource–Northern White sand, which is considered highest quality raw frac sand | • Natural resource, primary types include Northern White, Brady Brown | • Raw frac sand substrate with resin coating; Bond together to prevent proppant flowback | • Manufactured product | |||

• Monocrystalline in nature, exhibiting crush strength, turbidity and roundness and sphericity in excess of API specifications | • Quality of sand varies widely depending on source | • Coating increases crush strength | • Typically highest crush strength | |||

• Crush strength for 30/50 and 40/70 frac sand of 8,000 to 10,000 psi | • Crush strength for 30/50 and 40/70 frac sand typically between 5,000 to 10,000 psi | • Crush strength of 10,000 to 15,000 psi | • Crush strength of 10,000 to 18,000 psi | |||

Proppant Mesh Sizes

Mesh size is used to describe the size of the proppant and is determined by sieving the proppant through screens with uniform openings corresponding to the desired size of the proppant. Each type of proppant comes in various sizes, categorized as mesh sizes, and the various mesh sizes are used in different applications in the oil and natural gas industry. Generally, larger grain sizes are used in wells targeting oil and liquids-rich formations, and smaller grain sizes are used in wells targeting primarily gas bearing formations. The mesh number system is a measure of the number of equally sized openings there are per square inch of screen through which the proppant is sieved. For example, a 30 mesh screen has 30 equally sized openings per linear inch. Therefore, as the mesh size increases, the granule size decreases. In order to meet API specifications, 90% of the proppant described as 30/50 mesh size proppant must consist of granules that will pass through a 30 mesh screen but not through a 50 mesh screen. We excavate various mesh sizes at our Wyeville facility, and are contracted to sell 20/40, 30/50, 40/70 and 100 mesh frac sand used in the hydraulic fracturing process.

Frac Sand Extraction, Processing and Distribution

Raw frac sand is a naturally occurring mineral that is mined and processed. While the specific extraction method utilized depends primarily on the geologic setting, most raw frac sand is mined using conventional open-pit bench extraction methods. The composition, depth and chemical purity of the sand also dictate the processing method and equipment utilized. For example, broken rock from a sandstone deposit may require one, two or three stages of crushing to produce sand grains required to meet API specifications. In contrast, unconsolidated deposits (loosely bound sediments of sand), like those found at our Wyeville facility, may require little or no crushing during the excavation process. After extraction, the raw frac sand is washed with water to remove fine impurities such as clay and organic particles, with additional procedures used when contaminants are not easily removable. The final steps in the production process involve the drying and sorting of the raw frac sand according to mesh size.

Most frac sand is shipped in bulk from the processing facility to customers by truck, rail or barge. For bulk raw frac sand, transportation costs often represent a significant portion of the customer’s overall product cost. Consequently, shipping in large quantities, particularly when shipping over long distances, provides a significant cost advantage to the customer, emphasizing the importance of rail or barge access for low cost delivery. As a result, facility location and logistics capabilities are among the most important considerations for producers, distributors and customers.

All of our product from our Wyeville facility is shipped by rail from our three 5,000-foot rail spurs that connect our processing and storage facilities to a Union Pacific Railroad mainline. The length of these rail spurs and the capacity of the associated product storage silos allow us to accommodate a large number of rail cars. It also enables us to accommodate unit trains, which significantly increases our efficiency in meeting our customers’ frac sand transportation needs.

Transportation costs can be a large part of the final proppant cost for end users. As a result, designing and using an optimized logistics system is a key strategy for many proppant suppliers. As locating proppant production close to key markets is not always

9

possible, proppant suppliers will often have transload facilities in regions that they serve. The ability to deliver sand shorter distances with fewer intermediate steps is instrumental in remaining cost competitive or gaining cost advantages. Proppants are moved from their production site by rail or barge to transload or storage facilities. From there, they are typically transported by truck to the well site. Strategically locating transload facilities can therefore reduce the amount of conveyance by truck, which is typically the most expensive mode of transport.

Demand Trends

According to The Freedonia Group Report, the North American proppant market, including raw frac sand, ceramic and resin-coated proppants, was approximately 30 million tons in 2012. Industry estimates for 2012 indicate that the raw frac sand market represented approximately 24 million tons, or 79.6% of the total proppant market by weight. From 2007 through 2012, proppant demand by weight increased by 33.0% annually, and the market is projected to continue growing by 11.6% per year through 2017, representing an increase of approximately 21.7 million tons in annual proppant demand over that time period. The total North American proppant market size in dollars was $4.7 billion in 2012 and is projected to grow 14.9% annually through 2017. The following chart illustrates historical and projected demand for raw frac sand and other proppants for certain years from 2002 to 2022.

Historical and Projected Proppant Demand

Source: The Freedonia Group Report

Demand growth for frac sand and other proppants is primarily due to advancements in oil and natural gas drilling and well completion technology and techniques, such as horizontal drilling and hydraulic fracturing. These advancements have made the extraction of oil and natural gas increasingly cost-effective in formations that historically would have been unprofitable to develop. According to a January 2014 Baker Hughes, Inc. report, during the five year period beginning January 1, 2009 through December 31, 2013, North American horizontal rig count increased by 15.4% annually. Comparatively, The Freedonia Group Report noted that demand for proppant by weight grew at a rate of 33.5% annually during the five year period ended December 31, 2012. We believe that demand for proppant has and will continue to increase at a rate greater than horizontal rig count as a result of the following additional demand drivers:

10

• | improved drilling rig productivity (from, among other things, pad drilling), resulting in more wells drilled per rig per year; |

• | increases in the number of wells drilled per acre; |

• | increases in the length of the typical horizontal wellbore; |

• | increases in the number of fracture stages per foot in the typical completed horizontal wellbore; |

• | increases in the volume of proppant used per fracturing stage; and |

• | recurring efforts to offset steep production declines in unconventional oil and natural gas reservoirs, including the drilling of new wells and secondary hydraulic fracturing of existing wells. |

Furthermore, recent growth in demand for raw frac sand has outpaced growth in demand for other proppants, and industry analysts predict that this trend will continue. According to The Freedonia Group Report, North American demand for all types of proppants, in dollar terms, is projected to increase 14.9% annually through 2017, while demand for raw frac sand is projected to increase 15.7% annually over that time period. As well completion costs have increased as a proportion of total well costs, operators have increasingly looked for ways to improve per well economics by lowering costs without sacrificing production performance. To this end, the oil and natural gas industry is shifting away from the use of higher-cost proppants towards more cost-effective proppants, such as raw frac sand. The substantial increase in activity in North American oil and liquids-rich resource plays has further accelerated the demand growth for raw frac sand. Within these oil and liquids-rich basins, Northern White sand with coarser mesh sizes is often preferred due to its performance characteristics.

Supply Trends

As demand for raw frac sand has increased dramatically in recent years, the supply of raw frac sand failed to keep pace, resulting in a supply-demand disparity. As a result, a number of existing and new competitors have announced supply expansions and greenfield projects. However, there are several key constraints to increasing raw frac sand production on an industry-wide basis, including:

• | the difficulty of finding frac sand reserves that meet API specifications; |

• | the difficulty of securing contiguous frac sand reserves large enough to justify the capital investment required to develop a processing facility; |

• | the challenges of identifying frac sand reserves with the above characteristics that either are located in close proximity to oil and natural gas reservoirs or have rail access needed for low-cost transportation to major shale basins; |

• | the hurdles of securing mining, production, water, air, refuse and other federal, state and local operating permits from the proper authorities; |

• | local opposition to development of facilities, especially those that require the use of on-road transportation, including hours of operations and noise level restrictions, in addition to moratoria on raw frac sand facilities in multiple counties in Wisconsin which hold potential sand reserves; and |

• | the typically long lead time required to design and construct sand processing facilities that can efficiently process large quantities of high quality frac sand. |

Pricing

We believe raw frac sand has generally exhibited steady price increases over the past decade, reaching a peak in the first half of 2011. Prices were believed to have decreased in the latter half 2012, reaching a low point in the fourth quarter of 2012. Since that time, we believe that prices have stabilized and are trending upward as demand for raw frac sand continues to increase. There are numerous grades and sizes of proppant which sell at various prices, dependent upon quality, grade of proppant, deliverability and many other factors, including the delivery point. Pricing of proppant sold at the destination is higher than pricing of proppant sold FOB plant as a result of the associated rail cost to transport the sand from the mine to the destination terminal. No publicized pricing information for raw sand exists, however, it is believed that the overall pricing trends tend to be consistent across the various sizes. We believe the majority of proppant is sold under long-term contracts, with the remainder being sold under short-term pricing agreements.

Customers and Contracts

Our current contracted customer base includes subsidiaries of four of North America’s largest providers of pressure pumping services. For the year ended December 31, 2013, sales to each of FTS International, LLC ("FTS International"), Halliburton Company ("Halliburton") and Weatherford International Ltd. ("Weatherford") accounted for greater than 10% of our total revenues.

11

We sell the majority of the frac sand we produce under long-term contracts that require our customers to pay a specified price for a specified volume of frac sand each month, which significantly reduces our exposure to short-term fluctuations in the price of and demand for frac sand. For the year ended December 31, 2013, we generated 53% of our revenues from frac sand that we produced and delivered under our long-term contracts. We expect to continue selling a majority of our sand under long-term contracts in 2014 and future years. As of January 1, 2014, we have four long-term contracts with an average remaining contractual term of 2.6 years and with remaining terms ranging from 6 to 72 months. The following table presents a summary of our contracted volumes and revenues.

2011 | 2012 | 2013 | 2014 | ||||||||||||

Contracted Volumes (Tons) | 331,667 | 1,216,667 | 1,347,500 | 1,420,000 | |||||||||||

% of Processing Capacity (1) | 79 | % | 85 | % | 84 | % | 89 | % | |||||||

Contracted Revenue (in thousands) | $ | 19,917 | $ | 78,967 | $ | 77,825 | $ | 82,188 | |||||||

(1) | Percentage of processing capacity based on weighted average processing capacity for such period. |

The terms of our customer contracts, including sand quality requirements, quantity parameters, permitted sources of supply, effects of future regulatory changes, force majeure and termination and assignment provisions, vary by customer. Our long-term customer contracts contain penalties for non-performance by our customers, with make-whole prices averaging $35 per ton in 2014. If one of our customers fails to meet its minimum obligations to us, we would expect that the make-whole payment, combined with a decrease in our variable costs (such as royalty payments and excavation costs), would substantially mitigate any adverse impact on our cash flow from such failure. We would also have the ability to sell these sand volumes for which we receive make-whole payments to third parties. Our long-term customer contracts also contain penalties for our non-performance. If we are unable to deliver contracted volumes within three months of contract year end, or otherwise arrange for delivery from a third party, we are required to pay make-whole payments averaging $35 per ton in 2014. We believe our Wyeville facility, substantial reserves and our on-site processing and logistics capabilities reduce our risk of non-performance. We also have the ability to supply our customers from third party facilities and facilities owned by our sponsor. We believe our levels of inventory combined with our three month cure period starting at contract year end are sufficient to prevent us from paying make-whole payments as a result of plant shutdowns due to repairs to our facilities necessitated by reasonably foreseeable mechanical interruptions.

In addition to the contracted volumes, revenues and pricing in the above table, we have sold raw frac sand through our distribution network under short-term pricing and other agreements. The terms of our short-term pricing agreements, including sand quality requirements, quantity parameters, permitted sources of supply, effects of future regulatory changes, force majeure and termination and assignment provisions, vary by customer.

Suppliers

Although the majority of the frac sand that we sell is produced from our Wyeville facility, we purchase a certain amount of frac sand from various third parties for use in our distribution network. A significant portion of this third party sourced frac sand is purchased under contracts that require our suppliers to produce certain quantities and grades of frac sand and specifies the purchase prices for such produced frac sand.

Production Operations

Excavation Operations

The surface excavation operations at our Wyeville facility and our sponsor’s Augusta facility are conducted by a third-party contractor, Gerke Excavating, Inc. The mining technique at our Wyeville facility is open-pit excavation of approximately 20-acre panels of unconsolidated silica deposits. The excavation process involves clearing vegetation and trees overlying the proposed mining area. The initial two to five feet of overburden is removed and utilized to construct perimeter berms around the pit and property boundary. No underground mines are operated at our Wyeville facility or our sponsor’s Augusta facility.

A track excavator and articulated trucks are utilized for excavating the sand at several different elevation levels of the active pit. The pit is dry mined, and the water elevation is maintained below working level through a dewatering and pumping process. The mined material is loaded and hauled from different areas of the pit and different elevations within the pit to the primary loading facility at our mine’s on-site wet processing facility. At our Wyeville facility and our sponsor's Augusta facility, Gerke Excavating, Inc. is paid a fixed fee per ton of sand excavated, subject to a diesel fuel surcharge.

Processing Facilities

Our processing facilities are designed to wash, sort, dry and store our raw frac sand. Our Wyeville processing plant started operations in June 2011 and our sponsor’s Augusta processing plant started operations in July 2012, with each plant employing modern and efficient wet and dry processing technology.

Our mined raw frac sand is initially stockpiled before processing. The material is recovered by a mounted belt feeder, which extends beneath a surge pile, and is fed onto a conveyor. The sand exits the tunnel on the conveyor belt and is fed into the 600-

12

ton per hour wet plant where impurities and unusable fine grain sand are removed from the raw feed. The wet processed sand is then stockpiled in advance of being fed into the dry plant for further processing. The wet plant operates for seven to eight months per year due to the limitations arising from sustained freezing temperatures during winter months. When the wet plant is operating, however, it processes more sand per day than the dry plant to build up stockpiles of frac sand to be processed by the dry plant during the winter months.

The dry plant, which operates throughout the entire year, has a rated capacity of 250 tons per hour. The wet processed sand stockpile is fed into the dry plant hopper using a front end loader. The material is processed in a natural gas fired vibratory fluid bed dryer contained in an enclosed building. After drying, the sand is screened through gyratory screens and separated into industry standard product sizes. The finished product is then conveyed to multiple on-site storage silos for each size specification and our railcar loads are tested to ensure that the delivery meets API specifications. Oil and gas producers increasingly require current testing and proof that frac sand used in their drilling and completion processes meet API specifications.

Logistics Capabilities

All of our product sold from the Wyeville facility is shipped by rail from our three 5,000-foot rail spurs that connect our processing and storage facilities to a Union Pacific Railroad mainline. The length of these rail spurs and the capacity of the associated product storage silos allow us to accommodate a large number of rail cars. It also enables us to accommodate unit trains, which significantly increases our efficiency in meeting our customers’ frac sand transportation needs. Unit trains, typically 80 rail cars in length or longer, are dedicated trains chartered for a single delivery destination. Generally, unit trains receive priority scheduling and do not switch cars at various intermediate junctions, which results in a more cost-effective and efficient method of shipping than the standard method of rail shipment. We believe the Wyeville facility is one of the first frac sand facilities in the industry initially designed to accommodate large scale rail and unit train logistics, which require sufficient acreage, loading facilities and rail spurs to accommodate a unit train on site.

Logistics capabilities of frac sand producers are important to our customers, who focus on both the reliability and flexibility of product delivery. Because our customers generally find it impractical to store frac sand in large quantities near their job sites, they seek to arrange for product to be delivered where and as needed, which requires predictable and efficient loading and shipping of product. The integrated nature of our logistics operations and our three 5,000 foot rail spurs enables us to handle railcars for multiple customers simultaneously, minimizing the number of days required to successfully load shipments, even at times of peak activity, and avoid the use of trucks and minimize transloading within the facility. At the same time, we believe our ability to ship using unit trains differentiates us from most other frac sand producers that ship using manifest, or mixed freight, trains, which may make multiple stops to switch cars before delivering cargoes, or transport their products by truck or barge. In addition, unlike some competitors, our processing and rail loading facilities are located on-site, which eliminates the requirement for on-road transportation, lowers product movement costs and minimizes the reduction in sand quality due to handling. Together, these advantages provide our customers with a reliable and efficient delivery method from our facility to each of the major U.S. oil and natural gas producing basins, and allow us to take advantage of the increasing demand for such a delivery method.

Terminal Operations

As of December 31, 2013, we operated 12 destination rail-based terminal locations throughout Pennsylvania, Ohio and New York. Each terminal location is strategically positioned in the Marcellus and Utica shale plays so that our customers typically do not need to travel more than 75 miles from the well-site to purchase their frac sand requirements. Our terminals include rail-to-truck and, at our Bradford, Minerva, Sheffield, Smithfield and Wellsboro locations, rail-to-storage capabilities.

We generally operate our destination terminal locations under long-term lease agreements with the Class I railroad or applicable short-line rail company. Most of these lease agreements include performance requirements, which typically specify a minimum number of rail cars that must be processed by us each year through the terminal.

We have an extensive network of Class I and short-line railroads that service our destination terminals. Once the frac sand is loaded into rail cars at the origin, we utilize a combination of Class I and short-line railroads to move the sand to our destination terminals. Frac sand that is transported to our destination terminals by rail is then unloaded to delivery trucks directly via a conveyor. For our Bradford, Minerva, Sheffield, Smithfield and Wellsboro locations, which comprise our destinations that have silo storage capabilities, frac sand can also be loaded into delivery trucks directly from our silos. Our silos deploy sand via gravity at 10 tons per minute to trucks stationed directly on scales under each silo with the loading, electronic recording of weight and dispatch of the truck capable of being completed in less than five minutes. Silos are considerably more efficient than conveyors, which require trucks to be loaded and then moved to separate scales to be weighed. As of December 31, 2013, we had the ability to store 31,600 tons of frac sand in our silos, with additional tons of capacity under construction and expected to be completed in 2014.

13

Quality Control

We employ an automated process control system that efficiently manages our mining, loading, shipping, storage, processing and preventative maintenance functions. Furthermore, our co-located storage and loading facilities and shipment via unit trains reduce the incidence of contamination during the delivery process and result in higher quality sand being delivered to our customers. We monitor the quality and consistency of our products by conducting hourly tests throughout the production process to detect variances. These tests are conducted on several different machines to ensure that the results are repeatable and accurate. We take product samples from every rail car that is loaded and provide customers with reports per their request. Samples are retained for three months for testing upon customer request. We have a third-party calibration company certify all measurement devices at our facility on a monthly basis. We also provide customers with documentation verifying that all products shipped meet customer specifications. We continually refine our processes to ensure repeatable results in our processing plant and product quality accountability for our customers.

We have established sand testing processes to monitor sand sieve and turbidity and pre-test all railcars destined for silos at Minerva, Smithfield and Wellsboro. Our testing processes have also been developed to obtain samples from railcars to verify the grade of sand being delivered by railcar.

Competition

There are numerous large and small producers in all sand producing regions of the United States with whom we compete. Our main competitors include:

• | Badger Mining Corporation |

• | Emerge Energy Services LP |

• | Fairmount Minerals, Ltd. |

• | Preferred Proppants LLC |

• | Unimin Corporation |

• | U.S. Silica Holdings, Inc. |

The most important factors on which we compete are product quality, performance and sand characteristics, transportation capabilities, reliability of supply and price. Demand for frac sand and the prices that we will be able to obtain for our products, to the extent not subject to a long-term contract, are closely linked to proppant consumption patterns for the completion of oil and natural gas wells in North America. These consumption patterns are influenced by numerous factors, including the price for hydrocarbons, the drilling rig count and hydraulic fracturing activity, including the number of stages completed and the amount of proppant used per stage. Further, these consumption patterns are also influenced by the location, quality, price and availability of raw frac sand and other types of proppants such as resin-coated sand and ceramic proppant.

Our History and Relationship with Our Sponsor

Overview and History

Hi-Crush Proppants LLC, our sponsor, was formed in 2010 in Houston, Texas. Members of our sponsor’s management team have, on average, more than 20 years of experience investing in and operating businesses in the oil and natural gas and sand mining industries. Members of our management team have partnered with major oilfield services companies and exploration and production companies in the development of oil and natural gas reservoirs. In this capacity, members of our management team gained valuable expertise and developed strong relationships in the oilfield services industry. Recognizing the increasing demand for proppants as a result of rapidly evolving hydraulic fracturing techniques, members of our management team chose to leverage their expertise and relationships to capitalize on this increasing demand by developing raw frac sand reserves and facilities. In addition, our Chief Operating Officer has overseen the design, construction and staffing for multiple sand mining and processing facilities. The expertise of our management and operations teams covers a wide range of disciplines, with an emphasis on development, construction and operation of frac sand processing facilities, frac sand supply chain management and consulting and bulk solids material handling.

Our sponsor’s lead investor is Avista Capital Partners, a leading private equity firm with significant investing and operating expertise in the energy industry. Founded in 2005 by senior investment professionals who worked together at DLJ Merchant Banking Partners (“DLJMB”), then one of the world’s largest and most successful private equity franchises, Avista makes controlling or influential minority investments in connection with various transaction structures. The energy team at Avista is comprised of experienced professionals and industry executives with relevant expertise in the energy sector. Avista principals have led over $3.0 billion in equity investments in energy companies while at Avista and DLJMB, including Basic Energy Services, Inc., Brigham Exploration Company, Copano Energy, L.L.C., Seabulk International, Inc., and joint-ventures with Carrizo Oil & Gas, Inc.

14

Our Sponsor’s Assets and Our Right of First Offer

In connection with our IPO, our sponsor contributed to us its sand reserves and related excavation and processing facilities located in Wyeville, Wisconsin. On January 31, 2013, we acquired a preferred interest in our sponsor’s Augusta facility for $37.5 million in cash and 3.75 million of our Class B Units representing limited partner interests in the Partnership. John T. Boyd estimated that, as of December 31, 2013, the Augusta site had 46.8 million tons of proven recoverable coarse grade sand reserves located on 1,187 acres. In addition, our sponsor is constructing its third 1,600,000 tons per year processing facility near Whitehall, Wisconsin, expected to be completed in the second quarter of 2014. Our sponsor also has options to acquire several other sand mining locations where it could develop similar production facilities with similar logistics capabilities as the Wyeville and Augusta facilities. Pursuant to the terms of an omnibus agreement we entered into with our sponsor, we have a right of first offer with respect to certain of our sponsor’s assets.

Our sponsor continually evaluates acquisitions and may elect to acquire, construct or dispose of assets in the future, including in sales of assets to us. As the owner of our general partner, all of our subordinated units, Class B Units and incentive distribution rights, our sponsor is well aligned and highly motivated to promote and support the successful execution of our business strategies, including utilizing our partnership as a growth vehicle for its sand mining operations. Although we expect to have the opportunity to make additional acquisitions directly from our sponsor in the future, including the sand excavation and processing facilities described above that are subject to our right of first offer, our sponsor is under no obligation to accept any offer we make, and may, following good faith negotiations with us, sell the assets subject to our right of first offer to third parties that may compete with us. Our sponsor may also elect to develop, retain and operate properties in competition with us or develop new assets that are not subject to our right of first offer.

In addition, while we believe our relationship with our sponsor is a significant positive attribute, it may also be a source of conflict. For example, our sponsor is not restricted in its ability to compete with us, and since the commencement of operations at its Augusta facility in August 2012 our sponsor has been competing directly with us for new and existing customers. In addition, we expect that our sponsor will develop additional frac sand excavation and processing facilities in the future, which may also compete with us. While we expect that our management team, which also manages our sponsor’s retained assets, and our sponsor will allocate new and replacement customer contracts between us and our sponsor in a manner that balances the interests of both parties, they are under no obligation to do so.

Omnibus Agreement

On August 20, 2012, we entered into an omnibus agreement with our general partner and our sponsor. Pursuant to the terms of this agreement, our sponsor will indemnify us and our subsidiaries for certain liabilities over specified periods of time, including but not limited to certain liabilities relating to (a) environmental matters pertaining to the period prior to our initial public offering and the contribution of the Wyeville assets from our sponsor, provided that such indemnity is capped at $7.5 million in aggregate, (b) federal, state and local tax liabilities pertaining to the period prior to our initial public offering and the contribution of the Wyeville assets from our sponsor, (c) inadequate permits or licenses related to the contributed assets, and (d) any losses, costs or damages incurred by us that are attributable to our sponsor’s ownership and operation of the Wyeville assets prior to our initial public offering and our sponsor’s contribution of such assets. In addition, we have agreed to indemnify our sponsor from any losses, costs or damages it incurs that are attributable to our ownership and operation of the contributed assets following the closing of the IPO, subject to similar limitations as on our sponsor’s indemnity obligations to us.

The omnibus agreement had provided that we would assign to our sponsor all of our rights and obligations under our long-term contract with one customer on May 1, 2013, and our sponsor would be obligated to accept such assignment and assume our obligations under such contract. In connection with our acquisition of a preferred interest in Augusta on January 31, 2013, our sponsor waived its right to require that we assign to our sponsor such contract.

In addition, the omnibus agreement also grants us, for a period of three years, a right of first offer on our sponsor’s sand reserves and any related assets that have been or will be constructed on its current acreage in Augusta, Wisconsin in the event our sponsor proposes to transfer such reserves and assets to a third party other than in connection with a sale of all or substantially all of its assets. On January 31, 2013, we entered into an agreement with our sponsor to acquire a preferred interest in Augusta, the entity that owns our sponsor’s Augusta raw frac sand processing facility, for $37.5 million in cash and 3.75 million of Class B Units. Our sponsor will not receive distributions on the Class B Units unless certain thresholds are met and until they convert into common units. The preferred interest in Augusta entitles us to receive a preferred distribution of up to $3.75 million per quarter, or $15.0 million annually.

Our Management and Employees

We are managed and operated by the board of directors and executive officers of our general partner, Hi-Crush GP LLC, a wholly owned subsidiary of our sponsor. As a result of owning our general partner, our sponsor has the right to appoint all members of the board of directors of our general partner, including at least three independent directors meeting the independence standards

15

established by the New York Stock Exchange (“NYSE”). Our unitholders are not entitled to elect our general partner or its directors or otherwise directly participate in our management or operations. Even if our unitholders are dissatisfied with the performance of our general partner, they have limited ability to remove the general partner without its consent, because our general partner and its affiliates own a sufficient number of units. Our unitholders are able to indirectly participate in our management and operations only to the limited extent actions taken by our general partner require the approval of a percentage of our unitholders and our general partner and its affiliates do not own sufficient units to guarantee such approval.

We have entered into an omnibus agreement with our sponsor and our general partner which governs our relationship with them regarding the provisions of certain administrative services to us. In addition, under our partnership agreement, we reimburse our general partner and its affiliates, including our sponsor, for all expenses they incur and payments they make on our behalf, to the extent such expenses are not contemplated by the omnibus agreement. Our partnership agreement does not set a limit on the amount of expenses for which our general partner and its affiliates may be reimbursed. Our partnership agreement provides that our general partner will determine in good faith the expenses that are allocable to us.

Hi-Crush Partners LP does not have any employees. All of the employees who conduct our business pursuant to the omnibus agreement are employed by Hi-Crush Proppants LLC or its wholly owned subsidiaries. As of December 31, 2013, Hi-Crush Proppants LLC had 232 employees. In addition, we contract out our excavation operations to a third party, Gerke Excavating, Inc., and accordingly have no employees involved in those operations.

Environmental and Occupational Safety and Health Regulation

Mining and Workplace Safety

Federal Regulation

The U.S. Mine Safety and Health Administration (“MSHA”) is the primary regulatory agency with jurisdiction over the commercial silica industry. Accordingly, MSHA regulates quarries, surface mines, underground mines, and the industrial mineral processing facilities associated with quarries and mines. The mission of MSHA is to administer the provisions of the Federal Mine Safety and Health Act of 1977 and to enforce compliance with mandatory safety and health standards. As part of MSHA’s oversight, its representatives must perform at least two unannounced inspections annually for each surface mining facility in its jurisdiction. To date, these inspections have not resulted in any citations for material violations of MSHA standards.

We also are subject to the requirements of the U.S. Occupational Safety and Health Act (“OSHA”) and comparable state statutes that regulate the protection of the health and safety of workers. In addition, the OSHA Hazard Communication Standard requires that information be maintained about hazardous materials used or produced in operations and that this information be provided to employees, state and local government authorities, and the public. OSHA regulates the users of commercial silica and provides detailed regulations requiring employers to protect employees from overexposure to silica through the enforcement of permissible exposure limits and the OSHA Hazard Communication Standard.

Health and Safety Programs