As filed with the Securities and Exchange Commission on July 3, 2012

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

MANCHESTER UNITED LTD.

(Exact name of Registrant as specified in its charter)

| Cayman Islands | 7941 | N/A | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

||

Old Trafford Manchester M16 0RA United Kingdom +44 (0) 161 868 8000 |

||||

| (Address, including zip code, and telephone number, including area code, of registrant's principal executive offices) |

||||

Corporation Service Company

1180 Avenue of the Americas, Suite 210

New York, NY 10036

(800) 927-9801

(Name, address, including zip code, and telephone number, including

area code, of agent for service)

Copies to:

| Marc D. Jaffe Ian D. Schuman Latham & Watkins LLP 885 Third Avenue New York, New York 10022 (212) 906-1281 |

Mitchell S. Nusbaum Christopher R. Rodi Woods Oviatt Gilman LLP 2 State Street 700 Crossroads Building Rochester, NY 14614 (585) 987-2800 |

Michael P. Kaplan John B. Meade Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

|

||||

| Title Of Each Class Of Securities To Be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount Of Registration Fee |

||

|---|---|---|---|---|

Class A ordinary shares, par value $0.01 per share |

$100,000,000 | $11,460 | ||

|

||||

- (1)

- Estimated

solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended.

- (2)

- Includes shares that the underwriters have the option to purchase to cover over-allotments, if any.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 3, 2012

PRELIMINARY PROSPECTUS

Shares

Manchester United Ltd.

Class A Ordinary Shares

This is the initial public offering of Manchester United Ltd. We are selling Class A ordinary shares.

We expect the public offering price to be between $ and $ per share. Currently, no public market exists for the shares. We intend to apply to list our Class A ordinary shares on the New York Stock Exchange under the symbol " ."

Following this offering, we will have two classes of ordinary shares outstanding: Class A ordinary shares and Class B ordinary shares. The rights of the holders of our Class A ordinary shares and our Class B ordinary shares are identical, except with respect to voting and conversion. Each Class A ordinary share is entitled to one vote per share and is not convertible into any other shares of our capital stock. Each Class B ordinary share is entitled to 10 votes per share and is convertible into one Class A ordinary share at any time. For special resolutions, which require the vote of two-thirds of the votes cast, at any time that the holders of the Class B ordinary shares together hold at least 10% of the total number of ordinary shares outstanding, the voting power permitted to be exercised by the holders of the Class B ordinary shares will be weighted such that the Class B ordinary shares shall represent, in the aggregate, 67% of the voting power of all shareholders. Our Class B ordinary shares also will automatically convert into shares of our Class A ordinary shares upon certain transfers. See "Description of Share Capital — Ordinary Shares — Conversion."

We are an "emerging growth company" under the US federal securities laws and will be subject to reduced public company reporting requirements. Investing in our Class A ordinary shares involves a high degree of risk. See "Risk Factors" beginning on page 14 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| |

PER SHARE | TOTAL | |||||

|---|---|---|---|---|---|---|---|

Public offering price |

$ | $ | |||||

Underwriting discounts and commissions |

$ | $ | |||||

Proceeds to Manchester United Ltd. before expenses |

$ | $ | |||||

Delivery of the Class A ordinary shares is expected to be made on or about , 2012. The selling shareholder named in this prospectus has granted the underwriters an option for a period of 30 days to purchase an additional Class A ordinary shares solely to cover over-allotments. We will not receive any proceeds from the sale of the Class A ordinary shares by the selling shareholder. If the underwriters exercise the option in full, the total proceeds to the selling shareholder, before expenses, will be $ , and the total underwriting discounts and commission payable by the selling shareholder will be $ . We will not pay any of the underwriting discounts and commissions in connection with the over-allotment option.

| Jefferies | Credit Suisse | J.P. Morgan |

BofA Merrill Lynch |

Deutsche Bank Securities |

Prospectus dated , 2012

Table of Contents

We have historically conducted our business through Red Football Shareholder Limited and its subsidiaries, but prior to the completion of this offering we will engage in the Reorganization Transactions described in "Prospectus Summary — The Reorganization Transactions" pursuant to which Red Football Shareholder Limited will become a wholly-owned subsidiary of Manchester United Ltd., an exempted newly formed holding company with limited liability formed under the laws of the Cayman Islands. Except where the context otherwise requires or where otherwise indicated, the terms "Manchester United," the "Company," "we," "us," "our," "our company" and "our business" refer, prior to the Reorganization Transactions discussed below, to Red Football Shareholder Limited and, after the Reorganization Transactions, to Manchester United Ltd., in each case together with its consolidated subsidiaries as a consolidated entity. Except as otherwise indicated, the term "Manchester United Limited (UK)" refers to our wholly-owned United Kingdom subsidiary, Manchester United Limited.

The terms "dollar," "USD" or "$" refer to US dollars, the terms "pound sterling," "pence," "p" or "£" refer to the legal currency of the United Kingdom and the terms "€" or "euro" are to the currency introduced at the start of the third stage of European economic and monetary union pursuant to the treaty establishing the European Community, as amended.

Throughout this prospectus, we refer to the following football leagues and cups:

- •

- the Football Association Premier League sponsored

by Barclays (the "Premier League");

- •

- the Football Association Cup in association with

Budweiser (the "FA Cup");

- •

- the Football League Cup sponsored by Capital One

(the "League Cup");

- •

- the Union of European Football Associations

Champions League (the "Champions League"); and

- •

- the Union of European Football Associations Europa League (the "Europa League").

The terms "matchday" and "Matchday" refer to all domestic and European football match day activities from Manchester United games at Old Trafford, the Manchester United football stadium, along with receipts for domestic cup (such as the League Cup and the FA Cup) games not played at Old Trafford. Fees for arranging other events at the stadium are also included as matchday revenue.

The term "first team" refers to the players selected to play for our most senior team and is comprised of the players listed on pages 81 and 82 of this prospectus.

We have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, Class A ordinary shares only in jurisdictions where such offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the Class A ordinary shares.

PRESENTATION OF FINANCIAL INFORMATION

We report under International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board (the "IASB"). None of the financial statements were prepared in accordance with generally accepted accounting principles in the United States. We have historically conducted our business through Red Football Shareholder Limited and its subsidiaries, and therefore our historical financial statements present the results of operations of Red Football Shareholder Limited. Prior to the completion of this offering, we will engage in the Reorganization Transactions described in "Prospectus Summary — The Reorganization Transactions" pursuant to which Red Football Shareholder Limited will become a wholly-owned subsidiary of Manchester United Ltd., a newly formed holding company. Following these Reorganization Transactions and this offering, our financial statements will present the results of operations of Manchester United Ltd. and its consolidated subsidiaries.

i

This prospectus contains industry, market, and competitive position data that are based on the six industry publications and studies conducted by third parties listed below as well as our own internal estimates and research. These industry publications and third-party studies generally state that the information that they contain has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. While we believe that each of these publications and third-party studies is reliable, we have not independently verified the market and industry data obtained from these third-party sources. While we believe our internal research is reliable and the definition of our market and industry are appropriate, neither such research nor these definitions have been verified by any independent source.

References to our "659 million followers" are based on a survey conducted by Kantar Media (a division of WPP plc) and paid for by us. As in the survey conducted by Kantar Media, we define the term "followers" as those individuals who answered survey questions, unprompted, with the answer that Manchester United was either their favorite football team in the world or a football team that they enjoyed following. For example, we and Kantar Media included in the definition of "follower" a respondent who either watched live Manchester United matches, followed highlights coverage or read or talked about Manchester United regularly. Although the survey solicited unprompted responses, we do not distinguish between those respondents who answered that Manchester United was their favorite football team in the world and those who enjoy following Manchester United. Since we believe that each of our followers engage with our brand in some capacity, including through watching matches on television, attending matches live, buying retail merchandise or monitoring the team's highlights on the internet, we believe identifying our followers in this manner provides us with the best data to use for purposes of developing our business strategy and measuring the penetration of our brand. However, we expect there to be differences in the level of engagement with our brand between individuals, including among those who consider Manchester United to be their favorite team, as well as between those who enjoy following Manchester United. We have not identified any practical way to measure these differences in consumer behavior and any references to our followers in this prospectus should be viewed in that light.

This internet-based survey identified Manchester United as a supported team of 659 million followers and was based on 53,287 respondents from 39 countries around the world. In order to calculate our 659 million followers from the 53,287 responses, Kantar Media applied estimates and assumptions to certain factors including population size, country specific characteristics such as wealth and GDP per capita, affinity for sports and media penetration. Kantar Media then extrapolated the results to the rest of the world, representing an extrapolated adult population of 5 billion people. However, while Kantar Media believes the extrapolation methodology was robust and consistent with consumer research practices, as with all surveys, there are inherent limitations in extrapolating survey results to a larger population than those actually surveyed. As a result of these limitations, our number of followers may be significantly less or significantly more than the extrapolated survey results. Kantar Media also extrapolated survey results to account for non-internet users in certain of the 39 countries, particularly those with low internet penetration. To do so, Kantar Media had to make assumptions about the preferences and behaviors of non-internet users in those countries. These assumptions reduced the number of our followers in those countries and there is no guarantee that the assumptions we applied are accurate. Survey results also account only for claimed consumer behavior rather than actual consumer behavior and as a result, survey results may not reflect real consumer behavior with respect to football or the consumption of our content and products.

In addition to the survey conducted by Kantar Media, this prospectus references the following five industry publications and third-party studies:

- •

- television viewership data compiled by futures sports + entertainment—Mediabrands International Limited for the 2010/11 season (the "Futures Data");

ii

- •

- Deloitte Touche Tohmatsu Limited's "Annual Review

of Football Finance 2009" (the "Deloitte Annual Review");

- •

- an article published by Sports Business

International (a division of SBG Companies Limited) in May 2009 entitled "Growing a Giant" (the "SBI Article"); and

- •

- a paper published by AT Kearney, Inc. in 2011 entitled "The Sports Market" ("AT Kearney").

We have proprietary rights to trademarks used in this prospectus which are important to our business, many of which are registered under applicable intellectual property laws. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the "®" or "™" symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other companies' trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. Each trademark, trade name or service mark of any other company appearing in this prospectus is the property of its respective holder.

iii

This prospectus summary highlights certain information appearing elsewhere in this prospectus. As this is a summary, it does not contain all of the information that you should consider in making an investment decision. You should read the entire prospectus carefully, including the information under "Risk Factors," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and the related notes thereto included in this prospectus, before investing. This prospectus includes forward-looking statements that involve risks and uncertainties. See "Special Note Regarding Forward-Looking Statements."

Except where the context otherwise requires or where otherwise indicated, the terms "Manchester United," the "Company," "we," "us," "our," "our company" and "our business" refer, prior to the Reorganization Transactions discussed below, to Red Football Shareholder Limited and, after the Reorganization Transactions, to Manchester United Ltd., in each case together with its consolidated subsidiaries as a consolidated entity. After the Reorganization Transactions, which will occur prior to the completion of this offering, Red Football Shareholder Limited will become a wholly-owned subsidiary of Manchester United Ltd.

Our Company — Manchester United

We are one of the most popular and successful sports teams in the world, playing one of the most popular spectator sports on Earth. Through our 134-year heritage we have won 60 trophies, enabling us to develop what we believe is one of the world's leading brands and a global community of 659 million followers. Our large, passionate community provides Manchester United with a worldwide platform to generate significant revenue from multiple sources, including sponsorship, merchandising, product licensing, new media & mobile, broadcasting and matchday. We attract leading companies such as Nike, Aon and DHL that want access and exposure to our community of followers and association with our brand.

Our global community of followers engages with us in a variety of ways:

- •

- During the 2010/11 season, our games generated a

cumulative audience reach of over 4 billion viewers, according to the Futures Data, across 211 countries. On a per game basis, our 60 games attracted an average live cumulative audience reach

of 49 million per game, based on the Futures Data.

- •

- Over 5 million items of Manchester United

branded licensed products were sold in the last year, including over 2 million Manchester United jerseys. Manchester United branded products are sold through over 200 licensees in over 130

countries.

- •

- Our products are sold through more than 10,000

doors worldwide.

- •

- Our brand and content has enabled us to partner

with mobile telecom providers in 44 countries and television providers in 54 countries.

- •

- Our website, www.manutd.com, is published in 7

languages and over the last 12 months attracted an average of more than 60 million page views per month.

- •

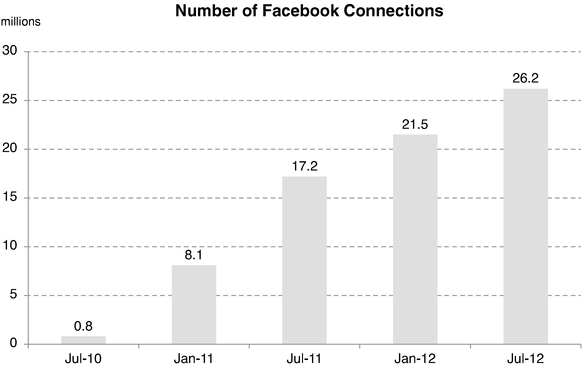

- We have a very popular brand page on Facebook with

more than 26 million connections. In comparison, the New York Yankees have approximately 5.8 million Facebook connections and the Dallas Cowboys have approximately 4.9 million

Facebook connections.

- •

- Premier League games at our home stadium, Old

Trafford, have been sold out since the 1997/98 season. In the 2010/11 season, our 29 home games were attended by over 2 million people.

- •

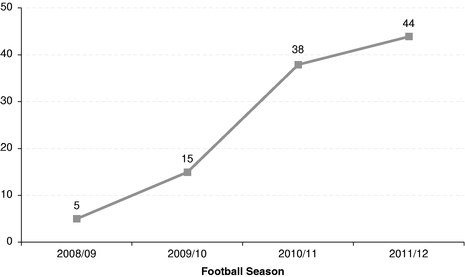

- We undertake exhibition games and promotional tours on a global basis, enabling our followers to see our team play. Over the last 3 years, we have played 15 exhibition games in the United States, Canada, Ireland, Mexico, Malaysia, South Korea and China.

1

Our Business Model and Revenue Drivers

We operate and manage our business as a single reporting segment — the operation of a professional sports team. We review our revenue through three principal sectors — Commercial, Broadcasting and Matchday.

- •

- Commercial: Within

the Commercial revenue sector, we have three revenue streams which monetize our global brand: sponsorship revenue; retail, merchandising, apparel & product licensing revenue; and new

media & mobile revenue. We believe these will be our fastest growing revenue streams over the next few years.

- •

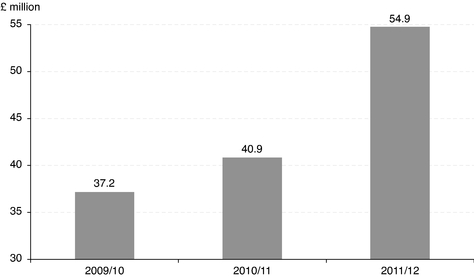

- Sponsorship: We

monetize the value of our global brand and community of followers through marketing and sponsorship relationships with leading international and regional companies across all geographies. Our

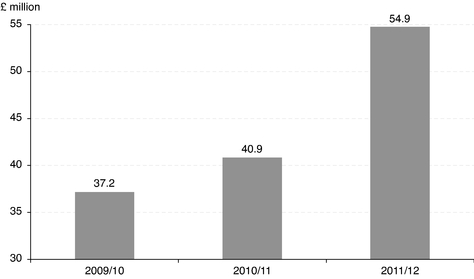

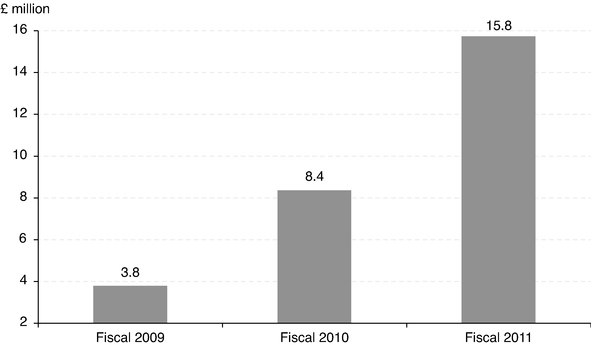

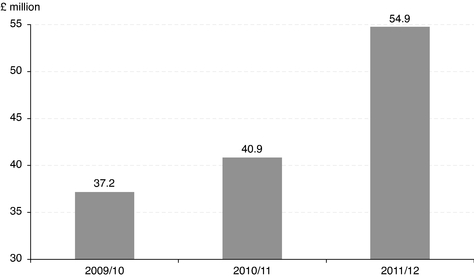

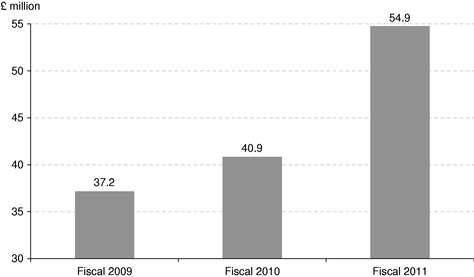

sponsorship revenue was £37.2 million, £40.9 million and £54.9 million for each of the years ended June 30, 2009, 2010 and 2011,

respectively.

- •

- Retail, Merchandising,

Apparel & Product Licensing: We market and sell competitive sports apparel, training and leisure wear and other clothing featuring the Manchester United

brand on a global basis. In addition, we also sell other licensed products, from coffee mugs to bed spreads, featuring the Manchester United brand and trademarks. These products are distributed

through Manchester United branded retail centers and e-commerce platforms, as well as our partners' wholesale distribution channels. Our retail, merchandising, apparel & product

licensing business is currently managed by Nike, who pays us a minimum guaranteed amount and a share of the business' cumulative profits. During the 2010/11 season, we received

£25.6 million, which reflects the minimum guaranteed amount. We also recognized an additional £5.7 million, which represents a proportion of the 50% cumulative

profits due under the Nike agreement during the 2010/11 season as compared to the £3.2 million profit share we recognized during the 2009/10 season. Our retail, merchandising,

apparel & product licensing revenue was £23.3 million, £26.5 million and £31.3 million for each of the years ended June 30, 2009,

2010 and 2011, respectively.

- •

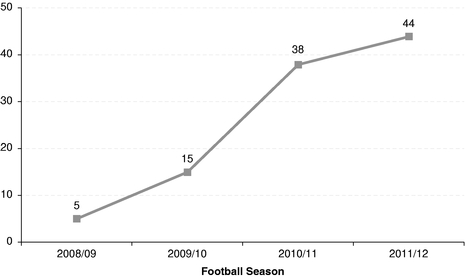

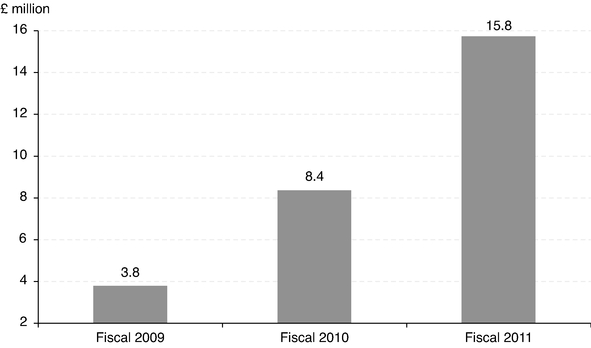

- New Media & Mobile: Due to the power of our brand and the quality of our content, we have formed mobile telecom partnerships in 44 countries. In addition, we market content directly to our followers through our website, www.manutd.com, and associated mobile properties. Our new media & mobile revenue was £5.5 million, £9.9 million and £17.2 million for each of the years ended June 30, 2009, 2010 and 2011, respectively.

Our Commercial revenue was £66.0 million, £77.3 million and £103.4 million for each of the years ended June 30, 2009, 2010 and 2011, respectively, and grew at a compound annual growth rate of 25.2% from fiscal year 2009 through fiscal year 2011. The growth rate of our Commercial revenue from fiscal year 2009 to fiscal year 2010 was 17.2% and from fiscal year 2010 to fiscal year 2011 was 33.7%. Our historical growth rates do no guarantee that we will achieve comparable rates in the future.

Our other two revenue sectors, Broadcasting and Matchday, provide consistent cash flow and global media visibility that enables us to continue to invest in the success of the team and expand our brand.

- •

- Broadcasting: We benefit from the distribution and broadcasting of live football content directly from the revenue we receive and indirectly through increased global exposure for our commercial partners. Broadcasting revenue is derived from the global television rights relating to the Premier League, Champions League and other competitions. In addition, our global television channel, MUTV, delivers Manchester United programming to 54 countries around the world. Our Broadcasting revenue was £98.0 million, £103.3 million and £117.2 million for each of the years ended June 30, 2009, 2010 and 2011, respectively, and grew at a compound annual growth rate of 9.4% from fiscal year 2009 through fiscal year 2011. The growth rate of our Broadcasting revenue from fiscal year 2009 to fiscal year 2010 was 5.4% and from fiscal year 2010 to fiscal year 2011 was 13.5%. Our historical growth rates do no guarantee that we will achieve comparable rates in the future.

2

- •

- Matchday: We believe Old Trafford is one of the world's iconic sports venues. It currently seats 75,766 and we have averaged over 99% of attendance capacity for our Premier League matches in each of the last 15 years. Our Matchday revenue was £114.5 million, £105.8 million and £110.8 million for each of the years ended June 30, 2009, 2010 and 2011, respectively.

Total revenue for the years ended June 30, 2009, 2010 and 2011 was £278.5 million, £286.4 million and £331.4 million, respectively. During this same period, Adjusted EBITDA was £93.0 million, £102.4 million and £109.7 million, respectively. For a discussion of our use of Adjusted EBITDA and a reconciliation to profit/(loss) for the period from continuing operations, see " — Summary Financial Data" and "Selected Consolidated Financial Data." Operating profit for the years ended June 30, 2009, 2010 and 2011 was £123.5 million, £64.3 million and £63.3 million, respectively. Profit/(loss) for the period from continuing operations for the years ended June 30, 2009, 2010 and 2011 was £5.3 million, £(47.5) million and £13.0 million, respectively.

The costs associated with operating a professional sports team principally comprise staff costs, depreciation of fixed assets, amortization of player registrations and other operating expenses associated with the facilities and management of the club. Less than 12% of our total operating costs are specifically allocated across our three principal sectors. Those operating costs that we do allocate across our three principal sectors are variable costs relating to sponsorship and marketing (allocated to our Commercial sector), television rights (allocated to our Broadcasting sector) and police and security, membership packages, catering and domestic cup gateshare (allocated to our Matchday sector).

Our Competitive Strengths

We believe our key competitive strengths are:

- •

- One of the most successful

sports teams in the world: Founded in 1878, Manchester United is one of the most successful sports teams in the world — playing one of the

world's most popular spectator sports. We have won 60 trophies in nine different leagues, competitions and cups since 1908. Our on-going success is supported by our highly developed

football infrastructure and global scouting network.

- •

- A globally recognized brand

with a large, worldwide following: Our 134-year history, our success and the global popularity of our sport have enabled us to become what we believe to be one of

the world's most recognizable brands. We enjoy the support of our global community of 659 million followers. The composition of our follower base is far-reaching and diverse,

transcending cultures, geographies, languages and socio-demographic groups, and we believe the strength of our brand goes beyond the world of sports.

- •

- Ability to successfully

monetize our brand: The popularity and quality of our globally recognized brand make us an attractive marketing partner for companies around the world. We have

built a diversified portfolio of sponsorships with leading brands such as Nike, Aon, DHL, Epson, Turkish Airlines and Singha. Our community of followers is strong in emerging markets, particularly in

certain regions of Asia, which enables us to deliver media exposure and growth to our partners in these markets.

- •

- Sought-after content

capitalizing on the proliferation of digital and social media: We produce content that is followed year-round by our global community of followers. Our

content distribution channels are international and diverse, and we actively adopt new media channels to enhance the accessibility and reach of our content. We believe our ability to generate

proprietary content, which we distribute on our own global platforms as well as via popular third party social media platforms such as Facebook, constitutes an on-going growth opportunity.

- •

- Well established global media and marketing infrastructure driving commercial revenue growth: We have a large global team dedicated to the development and monetization of our brand and to the sourcing of new revenue opportunities. The team has considerable experience and expertise in

3

- •

- Seasoned management team and committed ownership: Our senior management has considerable experience and expertise in the football, commercial, media and finance industries.

sponsorship sales, customer relationship management, marketing execution, advertising support and brand development. This experience and infrastructure enables us to deliver an effective set of marketing capabilities to our partners on a global basis. Our team is dedicated to the development and monetization of our brand and to the sourcing of new revenue opportunities.

Our Strategy

We aim to increase our revenue and profitability by expanding our high growth businesses that leverage our brand, global community and marketing infrastructure. The key elements of our strategy are:

- •

- Expand our portfolio of

global and regional sponsors: We are well positioned to continue to secure sponsorships with leading brands. Over the last few years, we have implemented a

proactive approach to identifying, securing and supporting sponsors. This has resulted in a 21.5% compound annual growth rate in our sponsorship revenue from fiscal year 2009 through fiscal year 2011

(the growth rate from fiscal year 2009 to fiscal year 2010 was 10.0% and from fiscal year 2010 to fiscal year 2011 was 34.2%). Our historical growth rates do not guarantee that we will achieve

comparable rates in the future. In addition to developing our global sponsorship portfolio, we are focused on expanding a regional sponsorship model, segmenting new opportunities by product category

and territory. As part of this strategy, we have opened an office in Asia and are in the process of opening an office in North America. These are in addition to our London and Manchester offices.

- •

- Further develop our retail,

merchandising, apparel & product licensing business: We will focus on growing this business on a global basis by increasing our product range and improving

distribution through further development of our wholesale, retail and e-commerce channels. Manchester United branded retail locations have opened in Singapore, Macau, India and Thailand,

and we plan to expand our global retail footprint over the next several years. In addition, we will also invest to expand our portfolio of product licensees to enhance the range of product offerings

available to our followers.

- •

- Exploit new media & mobile opportunities: The rapid shift of media consumption towards internet, mobile and social media platforms presents us with multiple growth opportunities and new revenue streams. Our digital media platforms, such as mobile sites, applications and social media, are expected to become one of the primary methods by which we engage and transact with our followers around the world.

- •

- Enhance the reach and distribution of our broadcasting rights: The value of live sports programming has grown dramatically in recent years due to changes in how television content is distributed and consumed. Specifically, television consumption has become more fragmented and audiences for traditional scheduled television programming have declined as consumer choice increased with the emergence of multi-channel television, the development of technologies such as the digital video recorder and the emergence of digital viewing on the internet and mobile devices. The unpredictable outcomes of live sports ensures that individuals consume sports programming in real time and in full, resulting in higher audiences and increased interest from television broadcasters and advertisers. We are well positioned to benefit from the increased value and the growth in distribution associated with the Premier League, the Champions League and other competitions. Furthermore, MUTV, our global broadcasting platform, delivers Manchester United programming to 54 countries around the world. We plan to expand the distribution of MUTV by improving the quality of its content and its production capabilities.

In addition to developing our own digital properties, we intend to leverage third party media platforms and other social media as a means of further engaging with our followers and creating a source of traffic for our digital media assets. Our new media & mobile offerings are in the early stages of development and present opportunities for future growth.

4

- •

- Diversify revenue and improve margins: We aim to increase the revenue and operating margins of our business as we further expand our high growth commercial businesses, including sponsorship, retail, merchandising, licensing and new media & mobile. By increasing the emphasis on our commercial businesses, we will further diversify our revenue, enabling us to generate improved profitability.

Our Market Opportunity

We believe that we are one of the world's most recognizable global brands with a community of 659 million followers. The global sports industry is expected to grow from $119 billion in 2011 to $145 billion by 2015. Manchester United is at the forefront of live football, which is a key component of this market.

While our business represents only a small portion of our addressable markets and may not grow at corresponding rates, we believe our global reach and access to emerging markets positions us for continued growth.

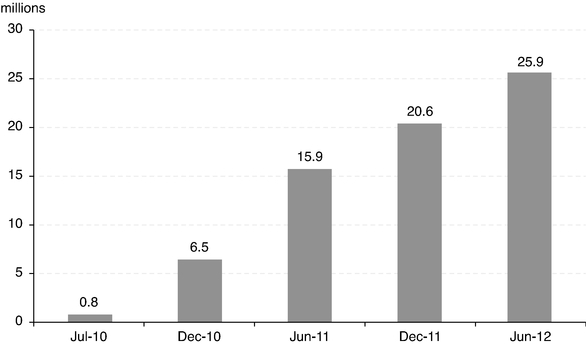

In addition, the explosion of growth in mobile technology and social media has driven a surge in demand for content, from news to video, which has resulted in a ten-fold increase in our revenue from new media & mobile over the five years ending June 30, 2011. Our new media & mobile revenue was £17.2 million for the year ended June 30, 2011, which represents 5.2% of annual revenue for the year ended June 30, 2011. The mobile technology and social media markets in China and certain other developing countries are, however, still early in their growth process.

Risks Affecting Us

We are subject to numerous risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flow and prospects. Please read the section entitled "Risk Factors" beginning on page 14 for a discussion of some of the factors you should carefully consider before deciding to invest in our Class A ordinary shares.

In particular, we have and will continue to be subject to the challenges of operating in our industry. These challenges and risks include, among other things, competition for key players and other personnel, increases in operating costs, such as player salaries and transfer costs, and our ability to manage our growth efficiently. For example, net of profit on disposal of players' registrations, we realized a loss from continuing operations in two out of the last three fiscal years (largely the result of finance costs that have since been significantly reduced through our deleveraging in fiscal year 2010). Although we are currently profitable and growing (even on a basis net of the £22.5 million tax credit realized during the nine months ended March 31, 2012), there can be no assurance that we will continue to be profitable or grow our profitability at the same rate in the future or at all.

Corporate Information

We were incorporated in the Cayman Islands on April 30, 2012, as an exempted company with limited liability under the Companies Law (2011 Revision) of the Cayman Islands, as amended and restated from time to time. Exempted companies are Cayman Islands companies whose operations are conducted mainly outside the Cayman Islands. Pursuant to a group reorganization as described in the section entitled " — The Reorganization Transactions", which will be completed immediately prior to the consummation of this offering, we became the holding company of the subsidiaries comprising the Company.

Our principal executive office is located at Old Trafford, Manchester M16 0RA, United Kingdom and our telephone number is +44 (0) 161 868 8000. Our website is www.manutd.com. The information on our website is not incorporated by reference into this prospectus, and you should not consider information contained on our website to be a part of this prospectus or in deciding whether to purchase our Class A ordinary shares.

5

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an "emerging growth company" as defined in the Jumpstart our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other burdens that are otherwise applicable generally to public companies. These provisions include:

- •

- a requirement to have only two years of audited

financial statements and only two years of related Management's Discussion and Analysis of Financial Condition and Results of Operations disclosure; and

- •

- an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002.

We may take advantage of these provisions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1.0 billion in annual revenue, have more than $700 million in market value of our ordinary shares held by non-affiliates, or issue more than $1.0 billion of non-convertible debt over a three-year period. We may choose to take advantage of some but not all of these reduced burdens. We have not taken advantage of any of these reduced reporting burdens in this prospectus, although we may choose to do so in future filings and if we do, the information that we provide shareholders may be different than you might get from other public companies in which you hold equity.

The JOBS Act permits an "emerging growth company" like us to take advantage of an extended transition period to comply with new or revised accounting standards applicable to public companies. We are choosing to "opt out" of this provision and, as a result, we will comply with new or revised accounting standards as required when they are adopted. This decision to opt out of the extended transition period is irrevocable.

6

| Issuer | Manchester United Ltd. | |

| The offering | Class A ordinary shares offered by us | |

| Class A ordinary shares to be outstanding after this offering | shares | |

| Class B ordinary shares to be outstanding after this offering | shares | |

| Over-allotment option | The selling shareholder has granted the underwriters a 30-day option to purchase up to Class A ordinary shares to cover over-allotments. | |

| Voting rights | Following this offering, we will have two classes of ordinary shares outstanding: Class A ordinary shares and Class B ordinary shares. The rights of the holders of our Class A ordinary shares and our Class B ordinary shares are identical, except with respect to voting and conversion. Each Class A ordinary share is entitled to one vote per share and is not convertible into any other shares of our capital stock. Each Class B ordinary share is entitled to 10 votes per share and is convertible into one Class A ordinary share at any time. The Class A ordinary shares and Class B ordinary shares outstanding after this offering will represent approximately % and %, respectively, of the total number of shares of our Class A and Class B ordinary shares outstanding after this offering ( % and % if the underwriters exercise their over-allotment option in full) and % and %, respectively, of the combined voting power of our Class A and Class B ordinary shares outstanding after this offering ( % and % if the underwriters exercise their over-allotment option in full). Our Class B ordinary shares also will automatically convert into shares of our Class A ordinary shares upon certain transfers and other events. See "Description of Share Capital — Ordinary Shares — Conversion." | |

| Use of proceeds | We estimate that our net proceeds from the sale of Class A ordinary shares in this offering will be approximately $ million, assuming an initial offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses. | |

| We intend to use all of our net proceeds from this offering to reduce our indebtedness by exercising our option to redeem £ million in aggregate principal amount of our 83/8% US dollar senior secured notes due 2017 at a redemption price equal to 108.375% of the principal amount of such notes and £ million in aggregate principal amount of our 83/4% pound sterling senior secured notes due 2017 at a redemption price equal to 108.750% of the principal amount of such notes, plus, in each case, accrued and unpaid interest to the date of such redemption. |

7

| We estimate that net proceeds to the selling shareholder will be approximately $ million if the underwriters exercise the over-allotment option in full. We will not receive any proceeds from the sale of any Class A ordinary shares by the selling shareholder pursuant to the exercise of the underwriters' over-allotment option. See "Use of Proceeds." | ||

| Dividend policy | We do not currently intend to pay cash dividends on our Class A ordinary shares in the foreseeable future. However, if we do pay a cash dividend on our Class A ordinary shares in the future, we will pay such dividend out of our profits or share premium (subject to solvency requirements) as permitted under Cayman Islands law. Our board of directors has complete discretion regarding the declaration and payment of dividends, and our principal shareholder will be able to influence our dividend policy. See "Dividend Policy." | |

| Proposed symbol for trading on the New York Stock Exchange | " " | |

| Risk factors | Investing in our Class A ordinary shares involves risks. See "Risk Factors" beginning on page 14 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our Class A ordinary shares. |

Unless otherwise indicated, all information in this prospectus relating to the number of shares of our Class A ordinary shares to be outstanding immediately after this offering:

- •

- excludes Class A

ordinary

shares issuable upon the exercise of options and Class A ordinary shares

subject to restricted share units that we expect to grant in connection with this offering under our

2012 Equity Incentive Award Plan, which we plan to adopt in connection with this offering; and

- •

- excludes Class A ordinary shares that will be reserved for future issuance under our 2012 Equity Incentive Award Plan, excluding the option grant and restricted share unit issuance described above.

Unless otherwise indicated, all information in this prospectus assumes (i) the completion of our Reorganization Transactions in preparation of this offering, (ii) no exercise by the underwriters of their option to purchase up to additional shares and (iii) an initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus.

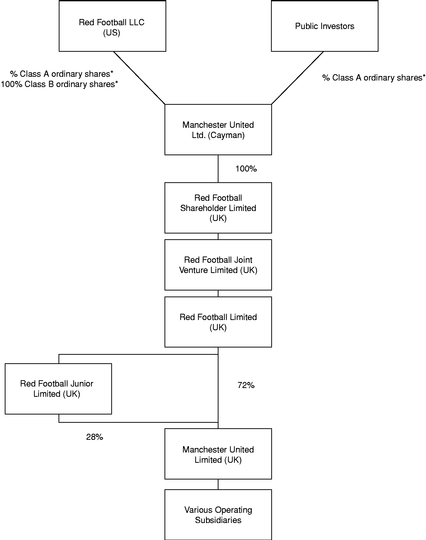

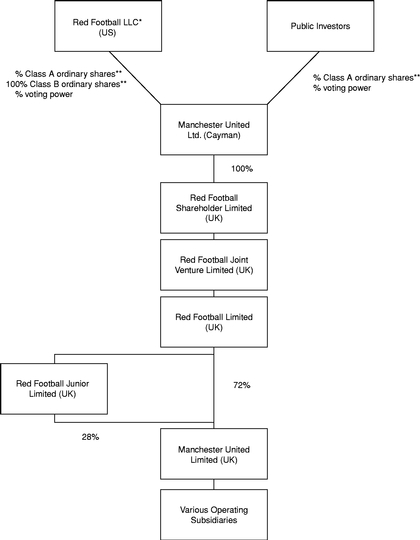

The Reorganization Transactions

We have historically conducted our business through Red Football Shareholder Limited, a private limited company incorporated in England and Wales, and its subsidiaries. Currently, Red Football Shareholder Limited is a direct, wholly-owned subsidiary of Red Football LLC, a Delaware limited liability company. On April 30, 2012, Red Football LLC formed a wholly-owned subsidiary, Manchester United Ltd., an exempted company with limited liability incorporated under the Companies Law (2011 Revision) of the Cayman Islands, as amended and restated from time to time.

Prior to the completion of this offering, Red Football LLC will cause all of the equity interest of Red Football Shareholder Limited to be contributed to Manchester United Ltd. As a result of these reorganization transactions, which will occur prior to the completion of this offering, Red Football Shareholder Limited will become a direct, wholly-owned subsidiary of Manchester United Ltd. and our

8

business will be conducted through Manchester United Ltd. and its subsidiaries. In this prospectus, we refer to all of these events as the "Reorganization Transactions."

The following diagram illustrates our corporate structure immediately following the Reorganization Transactions and the completion of this offering:

- *

- Upon completion of this offering, Red Football LLC will remain our principal shareholder and will continue to

be owned and controlled by the six lineal descendants of Mr. Malcolm Glazer. See "Principal and Selling Shareholder."

- **

- Each Class A ordinary share is entitled to one vote per share and is not convertible into any other shares of our capital stock. Each Class B ordinary share is entitled to 10 votes per share and is convertible into one Class A ordinary share at any time. For special resolutions (which are required for certain important matters including mergers and changes to our governing documents), which require the vote of two-thirds of the votes cast, at any time that the holders of the Class B ordinary shares together hold at least 10% of the total number of ordinary shares outstanding, the voting power permitted to be exercised by the holders of the Class B ordinary shares will be weighted such that the Class B ordinary shares shall represent, in the aggregate, 67% of the voting power of all shareholders. As a result, our principal shareholder will have the ability to significantly influence or determine the outcome of all matters submitted to our shareholders for approval, including the election and removal of directors and any merger, consolidation, or sale of all or substantially all of our assets. See "Risk Factors — Risks Related to Our Initial Public Offering and the Ownership of Our Class A Ordinary Shares — Because of its significant share ownership, our principal shareholder will be able to exert control over us and our significant corporate decisions." In addition, our

9

Class B ordinary shares will automatically convert into shares of our Class A ordinary shares upon certain transfers. See "Description of Share Capital — Ordinary Shares — Conversion."

Our governing documents also prohibit the transfer of shares to any person in breach of the rules of the Premier League, which prohibit any person who holds an interest of 10% or more of the total voting rights exercisable in a Premier League football club from holding an interest in voting rights in any other Premier League football club. See "Description of Share Capital — Ordinary Shares — Transfer of ordinary shares and notices."

A description of the material terms of Manchester United Ltd.'s amended and restated memorandum and articles of association, Class A ordinary shares and Class B ordinary shares as will be in effect following the Reorganization Transactions and the completion of this offering are described in the section entitled "Description of Share Capital."

10

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following summary consolidated financial data should be read in conjunction with, and is qualified in its entirety by reference to, the section of this prospectus entitled "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our consolidated financial statements and the related notes included elsewhere in this prospectus.

We have historically conducted our business through Red Football Shareholder Limited and its subsidiaries, and therefore our historical financial statements present the results of operations of Red Football Shareholder Limited. Prior to the completion of this offering, we will engage in the Reorganization Transactions pursuant to which Red Football Shareholder Limited will become a wholly-owned subsidiary of Manchester United Ltd., a newly formed holding company with nominal assets and liabilities, which will not have conducted any operations prior to the completion of this offering. Following these Reorganization Transactions and this offering, our financial statements will present the results of operations of Manchester United Ltd., and its consolidated subsidiaries.

We prepare our consolidated financial statements in accordance with IFRS as issued by IASB. The summary consolidated financial and other data presented as of and for the years ended June 30, 2009, 2010 and 2011 has been derived from our audited consolidated financial statements and the notes thereto included elsewhere in this prospectus. Our historical results for any prior period are not necessarily indicative of results expected in any future period.

The summary consolidated financial and other data presented for the nine months ended March 31, 2011 and 2012, and as of March 31, 2012, has been derived from our unaudited interim condensed consolidated financial statements and the notes thereto included elsewhere in this prospectus. In the opinion of management, the unaudited interim condensed consolidated financial data presented in this prospectus have been prepared on the same basis as our audited consolidated financial statements and reflect all adjustments, consisting only of normal recurring adjustments, which we consider necessary for a fair presentation of our financial position and results of operations for such periods. The summary consolidated financial and other data for the nine months ended March 31, 2011 and 2012, and as of March 31, 2012, are not necessarily indicative of the financial and other data to be expected as of and for the year ended June 30, 2012 or any future period.

| |

Year ended June 30, (audited) |

Nine months ended March 31, (unaudited) |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2010 | 2011 | 2011 | 2012 | |||||||||||

| |

(in £ thousands, except share and per share data) |

|||||||||||||||

Income Statement Data: |

||||||||||||||||

Revenue |

278,476 | 286,416 | 331,441 | 231,640 | 245,828 | |||||||||||

Analyzed as: |

||||||||||||||||

Commercial revenue |

65,977 | 77,322 | 103,369 | 76,676 | 89,535 | |||||||||||

Broadcasting revenue |

98,013 | 103,276 | 117,249 | 73,352 | 76,433 | |||||||||||

Matchday revenue |

114,486 | 105,818 | 110,823 | 81,612 | 79,860 | |||||||||||

Operating expenses — before exceptional items |

(232,034 | ) | (232,716 | ) | (267,986 | ) | (185,540 | ) | (196,638 | ) | ||||||

Analyzed as: |

||||||||||||||||

Employee benefit expenses |

(123,120 | ) | (131,689 | ) | (152,915 | ) | (102,275 | ) | (112,386 | ) | ||||||

Other operating expenses |

(62,311 | ) | (52,306 | ) | (68,837 | ) | (48,664 | ) | (48,814 | ) | ||||||

Depreciation |

(8,962 | ) | (8,634 | ) | (6,989 | ) | (5,252 | ) | (5,671 | ) | ||||||

Amortization of players' registrations |

(37,641 | ) | (40,087 | ) | (39,245 | ) | (29,349 | ) | (29,767 | ) | ||||||

Operating expenses — exceptional items |

(3,097 | ) | (2,775 | ) | (4,667 | ) | — | (6,363 | ) | |||||||

Total operating expenses |

(235,131 | ) | (235,491 | ) | (272,653 | ) | (185,540 | ) | (203,001 | ) | ||||||

11

| |

Year ended June 30, (audited) |

Nine months ended March 31, (unaudited) |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2010 | 2011 | 2011 | 2012 | |||||||||||

| |

(in £ thousands, except share and per share data) |

|||||||||||||||

Profit on disposal of players' registrations |

80,185 | 13,385 | 4,466 | 3,370 | 7,896 | |||||||||||

Operating profit |

123,530 | 64,310 | 63,254 | 49,470 | 50,723 | |||||||||||

Finance costs |

(118,743 | ) | (110,298 | ) | (52,960 | ) | (38,993 | ) | (35,724 | ) | ||||||

Finance income |

1,317 | 1,715 | 1,710 | 1,354 | 676 | |||||||||||

Net finance costs |

(117,426 | ) | (108,583 | ) | (51,250 | ) | (37,639 | ) | (35,048 | ) | ||||||

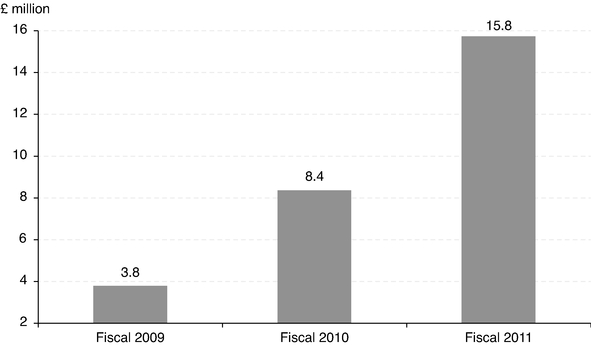

Profit/(loss) on ordinary activities before taxation |

6,104 | (44,273 | ) | 12,004 | 11,831 | 15,675 | ||||||||||

Tax (expense)/credit |

(844 | ) | (3,211 | ) | 986 | 1,510 | 22,543 | |||||||||

Profit/(loss) for the period from continuing operations |

5,260 | (47,484 | ) | 12,990 | 13,341 | 38,218 | ||||||||||

Attributable to: |

||||||||||||||||

Owners of the Company |

5,343 | (47,757 | ) | 12,649 | 13,150 | 37,984 | ||||||||||

Non-controlling interest |

(83 | ) | 273 | 341 | 191 | 234 | ||||||||||

Basic and diluted earnings/(loss) per share (pound sterling) |

5.40 | (48.24 | ) | 12.78 | 13.28 | 38.37 | ||||||||||

Weighted average number of shares |

990 | 990 | 990 | 990 | 990 | |||||||||||

Pro forma earnings/(loss) per share(1) |

||||||||||||||||

Basic |

— | — | — | |||||||||||||

Diluted |

— | — | — | |||||||||||||

Pro forma weighted average number of shares(1) |

||||||||||||||||

Basic |

— | — | — | |||||||||||||

Diluted |

— | — | — | |||||||||||||

Other Data: |

||||||||||||||||

Commercial revenue |

65,977 | 77,322 | 103,369 | 76,676 | 89,535 | |||||||||||

Analyzed as: |

||||||||||||||||

Sponsorship revenue |

37,228 | 40,938 | 54,925 | 42,378 | 48,796 | |||||||||||

Retail, merchandising, apparel & products licensing revenue |

23,250 | 26,471 | 31,268 | 21,651 | 25,230 | |||||||||||

New media & mobile revenue |

5,499 | 9,913 | 17,176 | 12,647 | 15,509 | |||||||||||

EBITDA(2) |

170,133 | 113,031 | 109,488 | 84,071 | 86,161 | |||||||||||

Adjusted EBITDA(2) |

93,045 | 102,421 | 109,689 | 80,701 | 71,902 | |||||||||||

Net cash generated from/(used in) investing activities |

40,178 | (35,119 | ) | (18,569 | ) | (17,681 | ) | (28,463 | ) | |||||||

| |

As of June 30, (audited) |

As of March 31, (unaudited) |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2010 | 2011 | 2012 | |||||||||

| |

(in £ thousands) |

||||||||||||

Balance Sheet Data (at period end): |

|||||||||||||

Cash and cash equivalents |

150,530 | 163,833 | 150,645 | 25,576 | |||||||||

Total assets |

993,644 | 989,670 | 1,017,188 | 865,564 | |||||||||

Total liabilities |

987,106 | 1,030,611 | 796,765 | 606,184 | |||||||||

Total equity |

6,538 | (40,941 | ) | 220,423 | 259,380 | ||||||||

12

- (1)

- Unaudited

pro forma earnings/(loss) per share gives effect to the Reorganization Transactions and also includes the shares offered by us in

this offering, assuming the Reorganization Transactions and this offering were consummated at the beginning of the referenced period.

- (2)

- We

define EBITDA as profit/(loss) for the period from continuing operations before net finance costs, tax (expense)/credit, depreciation, and

amortization of players' registrations, and we define Adjusted EBITDA as EBITDA adjusted for the items set forth in the table below. EBITDA and Adjusted EBITDA are non-IFRS measures and

not uniformly or legally defined financial measures. Such measures are not a substitute for IFRS measures in assessing our overall financial performance. Because EBITDA and Adjusted EBITDA are not

measurements determined in accordance with IFRS, and are susceptible to varying calculations, EBITDA and Adjusted EBITDA may not be comparable to other similarly titled measures presented by other

companies. Adjusted EBITDA is included in this prospectus because it is a measure of our operating performance and we believe that Adjusted EBITDA is useful to investors because it is frequently used

by securities analysts, investors and other interested parties in their evaluation of the operating performance of companies in industries similar to ours. We also believe Adjusted EBITDA is useful to

our management and investors as a measure of comparative operating performance from period to period and among companies as it is reflective of changes in pricing decisions, cost controls and other

factors that affect operating performance, and it removes the effect of our capital structure (primarily interest expense), asset base (primarily depreciation and amortization) and items outside the

control of our management (primarily income taxes and interest income and expense). Our management also uses Adjusted EBITDA for planning purposes, including the preparation of our annual operating

budget and financial projections. EBITDA and Adjusted EBITDA have limitations as an analytical tool, and you should not consider them in isolation, or as a substitute for an analysis of our results as

reported under IFRS as issued by IASB.

The following is a reconciliation of EBITDA and Adjusted EBITDA to profit for the year from continuing operations for the periods presented:

| |

Year ended June 30, (audited) |

Nine months ended March 31, (unaudited) |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2010 | 2011 | 2011 | 2012 | |||||||||||

| |

(in £ thousands) |

|||||||||||||||

Profit/(loss) for the period from continuing operations |

5,260 | (47,484 | ) | 12,990 | 13,341 | 38,218 | ||||||||||

Adjustments |

||||||||||||||||

Net finance costs |

117,426 | 108,583 | 51,250 | 37,639 | 35,048 | |||||||||||

Tax expense/(credit) |

844 | 3,211 | (986 | ) | (1,510 | ) | (22,543 | ) | ||||||||

Depreciation |

8,962 | 8,634 | 6,989 | 5,252 | 5,671 | |||||||||||

Amortization of players' registrations |

37,641 | 40,087 | 39,245 | 29,349 | 29,767 | |||||||||||

EBITDA |

170,133 | 113,031 | 109,488 | 84,071 | 86,161 | |||||||||||

Adjustments |

||||||||||||||||

Profit on disposal of players' registrations |

(80,185 | ) | (13,385 | ) | (4,466 | ) | (3,370 | ) | (7,896 | ) | ||||||

Operating expenses — exceptional items |

3,097 | 2,775 | 4,667 | — | (6,363 | ) | ||||||||||

Adjusted EBITDA |

93,045 | 102,421 | 109,689 | 80,701 | 71,902 | |||||||||||

13

An investment in our Class A ordinary shares involves a high degree of risk. You should carefully read and consider the following risks before deciding to invest in our Class A ordinary shares. If any of the following risks actually occurs, our business, results of operations, financial condition and cash flow could be materially impaired. The trading price of our Class A ordinary shares could decline due to any of these risks, and you could lose all or part of your investment. When determining whether to buy our Class A ordinary shares in this offering, you should also read carefully the other information in this prospectus, including our financial statements and related notes thereto.

Risks Related to Our Business

If we are unable to maintain and enhance our brand and reputation, particularly in new markets, or if events occur that damage our brand and reputation, our ability to expand our follower base, sponsors, and commercial partners or to sell significant quantities of our products may be impaired.

The success of our business depends on the value and strength of our brand and reputation. Our brand and reputation are also integral to the implementation of our strategies for expanding our follower base, sponsors and commercial partners. To be successful in the future, particularly outside of Europe, we believe we must preserve, grow and leverage the value of our brand across all of our revenue streams. For instance, we have in the past experienced, and we expect that in the future we will continue to receive, a high degree of media coverage. Unfavorable publicity regarding our first team's performance in league and cup competitions or their behavior off the field, our ability to attract and retain certain players and coaching staff or actions by or changes in our ownership, could negatively affect our brand and reputation. Failure to respond effectively to negative publicity could also further erode our brand and reputation. In addition, events in the football industry as whole, even if unrelated to us, may negatively affect our brand or reputation. As a result, the size, engagement, and loyalty of our follower base and the demand for our products may decline. Damage to our brand or reputation or loss of our followers' commitment for any of these reasons could impair our ability to expand our follower base, sponsors and commercial partners or our ability to sell significant quantities of our products, which would result in decreased revenue across our five revenue streams, and have a material adverse effect our business, results of operations, financial condition and cash flow, as well as require additional resources to rebuild our brand and reputation.

In addition, maintaining and enhancing our brand and reputation may require us to make substantial investments. We cannot assure you that such investments will be successful. Failure to successfully maintain and enhance the Manchester United brand or our reputation or excessive or unsuccessful expenses in connection with this effort could have a material adverse effect on our business, results of operations, financial condition and cash flow.

Our business is dependent upon our ability to attract and retain key personnel, including players.

We are highly dependent on members of our management, coaching staff and our players. Competition for talented players and staff is, and will continue to be, intense. Our ability to attract and retain the highest quality players for our first team, reserve team and youth academy as well as coaching staff is critical to our first team's success in league and cup competitions and increasing popularity and, consequently, critical to our business, results of operations, financial condition and cash flow. Any successor to our current manager may not be as successful as our current manager. A downturn in the performance of our first team could adversely affect our ability to attract and retain coaches and players. In addition, our popularity in certain countries or regions may depend, at least in part, on fielding certain players from those countries or regions. While we enter into employment contracts with each of our key personnel with the aim of securing their services for the term of the contract, the retention of their services for the full term of the contract cannot be guaranteed due to possible contract disputes or approaches by other clubs. Our failure to attract and retain key personnel could have a negative impact on our ability to effectively manage and grow our business.

14

We are dependent upon the performance and popularity of our first team.

Our revenue streams are driven by the performance and popularity of our first team. Significant sources of our revenue are the result of historically strong performances in English domestic and European competitions, specifically the Premier League, the FA Cup, the League Cup, the Champions League and the Europa League. Our income varies significantly depending on our first team's participation and performance in these competitions. Our first team's performance affects all five of our revenue streams:

- •

- sponsorship revenue through sponsorship

relationships;

- •

- retail, merchandising, apparel & product

licensing revenue through product sales;

- •

- new media & mobile revenue through telecom

partnerships and our website;

- •

- broadcasting revenue through the frequency of

appearances and performance based share of league broadcasting revenue and Champions League prize money; and

- •

- matchday revenue through ticket sales.

Our first team currently plays in the Premier League, the top football league in England. Our performance in the Premier League directly affects, and a weak performance in the Premier League could adversely affect, our business, results of operations, financial condition and cash flow. For example, our revenue from the sale of products, media rights, tickets and hospitality would fall considerably if our first team were relegated from (or otherwise ceased to play in) the Premier League, the Champions League or the Europa League.

We cannot ensure that our first team will be successful in the Premier League or in the other leagues and tournaments in which it plays. Relegation from the Premier League or a general decline in the success of our first team, particularly in consecutive seasons, would negatively affect our ability to attract or retain talented players and coaching staff, as well as supporters, sponsors and other commercial partners, which would have a material adverse effect on our business, results of operations, financial condition and cash flow.

If we fail to properly manage our anticipated growth, our business could suffer.

The planned growth of our commercial operations may place a significant strain on our management and on our operational and financial resources and systems. To manage growth effectively, we will need to maintain a system of management controls, and attract and retain qualified personnel, as well as, develop, train and manage management-level and other employees. Failure to manage our growth effectively could cause us to over-invest or under-invest in infrastructure, and result in losses or weaknesses in our infrastructure, which could have a material adverse effect on our business, results of operations, financial condition and cash flow. Any failure by us to manage our growth effectively could have a negative effect on our ability to achieve our development and commercialization goals and strategies.

If we are unable to maintain, train and build an effective international sales and marketing infrastructure, we will not be able to commercialize and grow our brand successfully.

As we grow, we may not be able to secure sales personnel or organizations that are adequate in number or expertise to successfully market and sell our brand and products on a global scale. If we are unable to expand our sales and marketing capability, train our sales force effectively or provide any other capabilities necessary to commercialize our brand internationally, we will need to contract with third parties to market and sell our brand. If we are unable to establish and maintain compliant and adequate sales and marketing capabilities, we may not be able to increase our revenue, may generate increased expenses, and may not continue to be profitable.

15

It may not be possible to renew or replace key commercial agreements on similar or better terms, or attract new sponsors.

Our Commercial revenue for each of the years ended June 30, 2009, 2010 and 2011 represented 23.7%, 27.0% and 31.2% of our total revenue, respectively. The substantial majority of our commercial revenue is generated from commercial agreements with our sponsors, and these agreements have finite terms. When these contracts do expire, we may not be able to renew or replace them with contracts on similar or better terms or at all. Our most important commercial contracts include contracts with global, regional, mobile, media and supplier sponsors representing industries including financial services, automotive, beverage, airline, timepiece, betting and telecommunications, which typically have contract terms of two to five years.

If we fail to renew or replace these key commercial agreements on similar or better terms, we could experience a material reduction in our Commercial and sponsorship revenue. Such a reduction could have a material adverse effect on our overall revenue and our ability to continue to compete with the top football clubs in England and Europe.

As part of our business plan, we intend to continue to grow our sponsorship portfolio by developing and expanding our geographic and product categorized approach, which will include partnering with additional global sponsors, regional sponsors, and mobile and media operators. We may not be able to successfully execute our business plan in promoting our brand to attract new sponsors. We are subject to certain contractual restrictions under our sponsorship agreement with Nike that may affect our ability to expand on our categories of sponsors, including certain restrictions on our ability to grant sponsorship, suppliership, advertising and promotional rights to certain types of businesses. We cannot assure you that we will be successful in implementing our business plan or that our Commercial and sponsorship revenue will continue to grow at the same rate as it has in the past or at all. Any of these events could negatively affect our ability to achieve our development and commercialization goals, which could have a material adverse effect on our business, results of operations, financial condition and cash flow.

Negotiation and pricing of key media contracts are outside our control and those contracts may change in the future.

For each of the years ended June 30, 2009, 2010 and 2011, 32.7%, 39.4% and 39.8% of our Broadcasting revenue, respectively, was generated from the media rights for Champions League matches, and 53.1%, 51.3% and 51.4% of our Broadcasting revenue, respectively, was generated from the media rights for Premier League matches. Contracts for these media rights and certain other revenue for those competitions (both domestically and internationally) are negotiated collectively by the Premier League and the Union of European Football Associations ("UEFA"). We are not a party to the contracts negotiated by the Premier League and UEFA. Further, we do not participate in and therefore do not have any direct influence on the outcome of contract negotiations. As a result, we may be subject to media rights contracts with media distributors with whom we may not otherwise contract or media rights contracts that are not as favorable to us as we might otherwise be able to negotiate individually with media distributors. Furthermore, the limited number of media distributors bidding for Premier League and Champions League media rights may result in reduced prices paid for those rights and, as a result, a decline in revenue received from our media contracts.

In addition, although an agreement has been reached for the sale of Premier League domestic broadcasting rights through the end of the 2015/16 football season and Premier League international broadcasting rights through the end of the 2012/13 football season and for the sale of Champions League broadcasting rights through the end of the 2014/15 football season, future agreements may not maintain our current level of Broadcasting revenue. Or, if international broadcasting revenue becomes an increasingly large portion of total revenue for the Premier League, a single club's domestic success and corresponding revenue may be outweighed by international media rights, which are distributed among all domestic clubs in even proportion. As a result, success of our first team in the Premier League could become less of an overall competitive advantage.

16

Future intervention by the European Commission, the European Court of Justice (the "ECJ") or other competent authorities and courts having jurisdiction may also have a negative effect on our revenue from media rights. For example, on October 4, 2011, the ECJ ruled on referrals it had received from English courts involving the cases of the Premier League & others vs. QC Leisure & Others / Karen Murphy vs. Media Protection Services. The ruling held that any agreement designed to guarantee country-by-country exclusivity within the European Union (the "EU") (i.e. by stopping any cross-border provision of broadcasting services) is deemed to be anti-competitive and prohibited by EU competition law. The ECJ also addressed copyright matters and determined that (i) there is no copyright in an actual football match itself but there is copyright in other elements such as the broadcast of the match or the copyright holder's logo and music; (ii) a copyright is not infringed where a member of the public in the EU buys a decoder and card from within the EU and watches a match in his own home; and (iii) a copyright may be infringed where commercial premises broadcast a match to the public. This decision has created uncertainty as to the commercial viability of copyright holders continuing to adopt the same country-by-country sales model within the EU as they have adopted previously. A change of sales model could negatively affect the amount which copyright holders, such as the Premier League, are able to derive from the exploitation of rights within the EU. As a result, our Broadcasting revenue from the sale of those rights could decrease. Any significant reduction in our Broadcasting revenue could materially adversely affect our business, results of operations, financial condition and cash flow.

European competitions cannot be relied upon as a source of income.

Qualification for the Champions League is dependent upon our first team's performance in the Premier League and, in some circumstances, the Champions League itself in the previous season. Qualification for the Champions League cannot, therefore, be guaranteed. Failure to qualify for the Champions League would result in a material reduction in revenue for each season in which our first team did not participate.

In addition, our participation in the Champions League or Europa League may be influenced by factors beyond our control. For example, the number of places in each league available to the clubs of each national football association in Europe can vary from year to year based on a ranking system. If the performance of English clubs in Europe declines, the number of places in each European competition available to English clubs may decline and it may be more difficult for our first team to qualify for each league in future seasons. Further, the rules governing qualification for European competitions (whether at the European or national level) may change and make it more difficult for our first team to qualify for each league in future seasons.

Moreover, because of the prestige associated with participating in the European competitions, particularly the Champions League, failure to qualify for any European competition, particularly for consecutive seasons, would negatively affect our ability to attract and retain talented players and coaching staff, as well as supporters, sponsors and other commercial partners. Any one or more of these events could have a material adverse effect on our business, results of operation, financial condition and cash flow.

Our business depends in part on relationships with certain third parties.

We consider the development of both our commercial and digital media assets to be central to our ongoing business plan and drivers of future growth. However, we do not currently have retail, merchandising and apparel operations in-house. For example, our contract with Nike provides them with certain rights to operate our global merchandising, product licensing and retail operations. While we have a significant degree of control over MUTV, we rely on MUTV for certain production capabilities with respect to video content for our digital media assets. While we have been able to execute our business plan to date with the support of Nike and MUTV, we remain subject to these contractual provisions and our business plan could be negatively impacted by non-compliance or poor execution of our strategy by these partners. Further, any interruption in our ability to obtain the services of these or other third parties or deterioration in their performance could negatively impact these portions of our operations. Furthermore, if our arrangements with

17

any of these third parties are terminated or modified against our interest, we may not be able to find alternative solutions for these portions of our business on a timely basis or on terms favorable to us or at all.