0001213900-24-018689.txt : 20240301

0001213900-24-018689.hdr.sgml : 20240301

20240229202058

ACCESSION NUMBER: 0001213900-24-018689

CONFORMED SUBMISSION TYPE: 10-K/A

PUBLIC DOCUMENT COUNT: 55

CONFORMED PERIOD OF REPORT: 20230131

FILED AS OF DATE: 20240301

DATE AS OF CHANGE: 20240229

FILER:

COMPANY DATA:

COMPANY CONFORMED NAME: VanEck Merk Gold Trust

CENTRAL INDEX KEY: 0001546652

STANDARD INDUSTRIAL CLASSIFICATION: [6221]

ORGANIZATION NAME: 09 Crypto Assets

IRS NUMBER: 000000000

STATE OF INCORPORATION: NY

FISCAL YEAR END: 0131

FILING VALUES:

FORM TYPE: 10-K/A

SEC ACT: 1934 Act

SEC FILE NUMBER: 001-36459

FILM NUMBER: 24706448

BUSINESS ADDRESS:

STREET 1: 2 HANSON PLACE

CITY: BROOKLYN

STATE: NY

ZIP: 11217

BUSINESS PHONE: 650-323-4341 X109

MAIL ADDRESS:

STREET 1: 2 HANSON PLACE

CITY: BROOKLYN

STATE: NY

ZIP: 11217

FORMER COMPANY:

FORMER CONFORMED NAME: Van Eck Merk Gold Trust

DATE OF NAME CHANGE: 20151020

FORMER COMPANY:

FORMER CONFORMED NAME: Merk Gold Trust

DATE OF NAME CHANGE: 20120405

10-K/A

1

ea0200989-10ka1_vaneck.htm

AMENDMENT NO. 1 TO FORM 10-K

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K/A

(Amendment

No. 1)

(Mark

One)

☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended January 31, 2023

or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the transition period from to

Commission

File No. 001-36459

VANECK

MERK GOLD TRUST

(Exact

name of registrant as specified in its charter)

New York

46-6582016

(State or Other Jurisdiction of Incorporation or Organization)

(I.R.S. Employer Identification No.)

c/o Merk Investments LLC 1150 Chestnut St, Menlo Park, California

94025

(Address of principal executive offices)

(Zip Code)

(650)323-4341

(Registrant’s

Telephone Number, Including Area Code)

Securities

registered pursuant to Section 12(b) of the Act:

Title of each class

Trading Symbol

Name of each exchange on which registered

VanEck Merk Gold Shares

OUNZ

NYSE Arca

Securities

registered pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No

☒

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No

☒

Indicate

by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). Yes ☒ No ☐

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained

herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated

by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller

reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☐

Accelerated filer

☒

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. ☒

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate

by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation

received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As

of July 31, 2022, the aggregate market value of the VanEck Merk Gold Shares held by non-affiliates of the registrant was approximately

$625,792,032.51.

As

of February 28, 2024, there were 39,925,409 VanEck Merk Gold Shares outstanding.

Documents

incorporated by reference: None.

EXPLANATORY

NOTE

This

Amendment No. 1 on Form 10-K/A (this “Amendment”) amends certain items of the Annual Report on Form 10-K for the fiscal year

ended January 31, 2023 of VanEck Merk Gold Trust (the “Trust”), originally filed with the Securities and Exchange Commission

(“SEC”) on April 13, 2023 (the “Original Form 10-K”). This Amendment amends the Original Form 10-K include the

audit report of BBD, LLP with respect to the assets and liabilities of the Trust, including the schedules of investment, as of January

31, 2022 and 2021, and the related statements of operations and changes in net assets for each of the years in the three-year period

ended January 31, 2022, the financial highlights for each of the years in the five-year period ended January 31, 2022, and the related

notes (the “BBD Audit Report”). The BBD Audit Report was inadvertently omitted from the Original Form 10-K.

This

Amendment amends only the following items of the Original Form 10-K and only with such modifications as necessary to reflect the inclusion

of the BBD Audit Report:

●

Part

II, Item 8, Financial Statements, solely with respect to the audited financial statements

required by Regulation S-X that are incorporated by reference therein;

●

Pages

F-1 to F-14 (Report of Independent Registered Public Accounting Firm, Audited Financial Statements,

and Notes to Financial Statements); and

●

Exhibits

23.1, 23.2, 31.1 and 32.1.

In

order to preserve the nature and character of the disclosures set forth in the Original Form 10-K, this Amendment speaks as of the date

of the filing of the Original Form 10-K and the disclosures contained in this Amendment have not been updated to reflect events occurring

subsequent to that date, other than those associated with the inclusion of the BBD Audit Report. Among other things, forward-looking

statements made in the Original 10-K have not been revised to reflect events that occurred or facts that became known to the Trust after

the filing of the Original 10-K, and such forward looking statements should be read in their historical context. Currently dated auditor

consents and certifications from the Trust’s Principal Executive Officer are also attached to this Amendment as Exhibits 23.1,

23.2, 31.1 and 32.1. For clarity, exhibits that are not listed in this Amendment shall remain the same as filed with the original Form

10-K. This Amendment should be read in conjunction with the Original Form 10-K and the Trust’s other SEC filings.

The

audited financial statements required by Regulation S-X, with the respective reports of the Trust’s independent registered public

accounting firms for the periods set forth therein, appear on pages F-1 to F-15 of this Report and are incorporated in this Item 8 by

reference to such information.

1

PART

IV

Item

15. Exhibits, Financial Statement Schedules.

(a)(1)

Financial Statements

See

Index to Financial Statements on Page F-1 for a list of the financial statements being filed herein.

(a)(2)

Financial Statement Schedules

Schedules

have been omitted since they are either not required, not applicable, or the information has otherwise been included.

REPORT

OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To

the Sponsor, Trustee and the Shareholders of VanEck Merk Gold Trust

Opinions

on the Financial Statements and Internal Control Over Financial Reporting

We

have audited the accompanying statement of assets and liabilities, including the schedule of investment, of VanEck Merk Gold Trust (the

“Trust”) as of January 31, 2023, and the related statements of operations and changes in net assets, and the financial highlights

for the year then ended, and the related notes (collectively referred to as the “financial statements”). We have also audited

the Trust’s internal control over financial reporting as of January 31, 2023, based on criteria established in Internal Control-Integrated

Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). In our opinion, the financial

statements present fairly, in all material respects, the financial position of the Trust as of January 31, 2023, and the results of its

operations, the changes in its net assets and the financial highlights for the year then ended, in conformity with accounting principles

generally accepted in the United States of America. Also, in our opinion, the Trust maintained, in all material respects, effective internal

control over financial reporting as of January 31, 2023, based on criteria established in Internal Control-Integrated Framework (2013)

issued by COSO.

The

Trust’s financial statements, financial highlights, and internal control over financial reporting for the years ended January 31,

2022, and prior, were audited by other auditors whose report dated April 12, 2022, expressed an unqualified opinion on those financial

statements, financial highlights and internal control over financial reporting.

Basis

for Opinions

The

Trust’s management is responsible for these financial statements, for maintaining effective internal control over financial reporting,

and for its assessment of the effectiveness of internal control over financial reporting included in the accompanying Management’s

Report on Internal Control over Financial Reporting. Our responsibility is to express an opinion on the Trust’s financial statements

and an opinion on the Trust’s internal control over financial reporting based on our audit. We are a public accounting firm registered

with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect

to the Trust in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange

Commission and the PCAOB.

We

conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain

reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud, and whether

effective internal control over financial reporting was maintained in all material respects.

Our

audit of the financial statements included performing procedures to assess the risks of material misstatement of the financial statements,

whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis,

evidence regarding the amounts and disclosures in the financial statements. Our audit also included evaluating the accounting principles

used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our audit

of internal control over financial reporting included obtaining an understanding of internal control over financial reporting, assessing

the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based

on the assessed risk. Our audit also included performing such other procedures as we considered necessary in the circumstances. We believe

that our audit provides a reasonable basis for our opinions.

Definition

and Limitations of Internal Control over Financial Reporting

A

company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability

of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting

principles. A company’s internal control over financial reporting includes those policies and procedures that (1) pertain to the

maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the

company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in

accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance

with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection

of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because

of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of

any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions,

or that the degree of compliance with the policies or procedures may deteriorate.

Critical

Audit Matters

Critical

audit matters are matters arising from the current period audit of the financial statements that were communicated or required to be

communicated to those charged with governance and that: (1) relate to accounts or disclosures that are material to the financial statements

and (2) involved our especially challenging, subjective, or complex judgments. We determined that there are no critical audit matters.

We

have served as the VanEck Merk Gold Trust’s auditor since 2023.

/s/ COHEN & COMPANY, LTD.

COHEN & COMPANY, LTD.

Philadelphia, Pennsylvania

April 12, 2023

F-2

REPORT

OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To

the Sponsor, Trustee and the Shareholders of VanEck Merk Gold Trust

Opinions

on the Financial Statements and Internal Control over Financial Reporting

We

have audited the accompanying statements of assets and liabilities of VanEck Merk Gold Trust (the “Trust”), including the

schedules of investment, as of January 31, 2022 and 2021, and the related statements of operations and changes in net assets for each

of the years in the three-year period ended January 31, 2022, the financial highlights for each of the years in the five-year period

ended January 31, 2022, and the related notes (collectively referred to as the “financial statements”). We also have audited

the Trust’s internal control over financial reporting as of January 31, 2022, based on criteria established in Internal

Control-Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO).

In

our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the Trust

as of January 31, 2022 and 2021, and the results of its operations, changes in its net assets and financial highlights for each of the

periods referred to above, in conformity with accounting principles generally accepted in the United States of America. Also, in our

opinion, the Trust maintained, in all material respects, effective internal control over financial reporting as of January 31,

2022, based on criteria established in Internal Control-Integrated Framework (2013) issued by COSO.

Basis

for Opinion

The

Trust’s management is responsible for these financial statements, for maintaining effective internal control over financial

reporting, and for its assessment of the effectiveness of internal control over financial reporting included in the accompanying Management’s

Report on Internal Control over Financial Reporting. Our responsibility is to express an opinion on the Trust’s financial statements

and an opinion on the Trust’s internal control over financial reporting based on our audits. We are a public accounting firm registered

with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Trust

in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission

and the PCAOB.

We

conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain

reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud, and whether

effective internal control over financial reporting was maintained in all material respects.

Our

audits of the financial statements included performing procedures to assess the risks of material misstatement of the financial statements,

whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis,

evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles

used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our audit

of internal control over financial reporting included obtaining an understanding of internal control over financial reporting,

assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control

based on the assessed risk. Our audits also included performing such other procedures as we considered necessary in the circumstances.

We believe that our audits provide a reasonable basis for our opinions.

Definition

and Limitations of Internal Control over Financial Reporting

A

company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability

of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting

principles. A company’s internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance

of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company;

(2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance

with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with

authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection

of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because

of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of

any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions,

or that the degree of compliance with the policies or procedures may deteriorate.

Critical

Audit Matters

Critical

audit matters are matters arising from the current period audit of the financial statements that were communicated or required to be

communicated to those charged with governance and that: (1) relate to accounts or disclosures that are material to the financial statements

and (2) involved our especially challenging, subjective, or complex judgments. We determined that there are no critical audit matters.

BBD,

LLP

We

have served as the auditor of the VanEck Merk Gold Trust since 2014.

Philadelphia,

Pennsylvania

April

12, 2022

F-3

VanEck

Merk Gold Trust

Statements

of Assets and Liabilities

January 31, 2023

January 31, 2022

Assets

Investments in gold bullion (cost $572,123,322 and $533,769,944, respectively)

$

656,592,807

$

586,245,778

Capital shares receivable

3,730,709

-

Total Assets

660,323,516

586,245,778

Liabilities

Gold Bullion purchased payable

3,730,707

-

Sponsor’s fee payable

9

6

Other payables

2

-

Total Liabilities

3,730,718

6

Net Assets

$

656,592,798

$

586,245,772

Net Assets Consists of:

Paid-in-capital

$

571,416,810

$

532,684,047

Accumulated earnings

85,175,988

53,561,725

$

656,592,798

$

586,245,772

Shares issued and outstanding (no par value)

35,203,259

33,599,843

Net asset value per share

$

18.65

$

17.45

See

notes to financial statements.

F-4

VanEck

Merk Gold Trust

Statements

of Operations

For the Year ended January 31, 2023

For the Year ended January 31, 2022

For the Year ended January 31, 2021

Expenses

Sponsor’s fees

$

1,557,794

$

1,271,275

$

1,013,291

Total expenses

1,557,794

1,271,275

1,013,291

Net investment loss

(1,557,794

)

(1,271,275

)

(1,013,291

)

Net Realized and Unrealized Gain (Loss)

Net realized gain from gold bullion distributed for redemptions

1,178,406

1,756,856

7,325,362

Net change in unrealized appreciation (depreciation) on investment in gold bullion

31,993,651

(18,669,013

)

32,005,146

Net realized and unrealized gain (loss) from operations

33,172,057

(16,912,157

)

39,330,508

Net Increase (Decrease) in Net Assets resulting from operations

$

31,614,263

$

(18,183,432

)

$

38,317,217

See

notes to financial statements.

F-5

VanEck

Merk Gold Trust

Statements

of Changes in Net Assets

For the Year ended January 31, 2023

For the Year ended January 31, 2022

For the Year ended January 31, 2021

Net Assets—beginning of year

$

586,245,772

$

442,483,105

$

198,479,743

Creations

137,482,147

179,243,246

244,523,754

Redemptions

(98,749,384

)

(17,297,147

)

(38,837,609

)

Net investment loss

(1,557,794

)

(1,271,275

)

(1,013,291

)

Net realized gain from gold bullion distributed for redemptions

1,178,406

1,756,856

7,325,362

Net change in unrealized appreciation (depreciation) on investment in gold bullion

31,993,651

(18,669,013

)

32,005,146

Net Assets—end of year

$

656,592,798

$

586,245,772

$

442,483,105

See

notes to financial statements.

F-6

VanEck

Merk Gold Trust

Financial

Highlights

Per

Share Performance (for a share outstanding throughout each year)

For the

Year Ended

January 31,

2023

For the

Year Ended

January 31, 2022

For the

Year Ended

January 31, 2021

For the

Year Ended

January 31, 2020

For the

Year Ended

January 31, 2019

Net asset value per share, beginning of year

$

17.45

$

18.16

$

15.48

$

12.99

$

13.25

Net investment loss (a)

(0.04

)

(0.04

)

(0.05

)

(0.06

)

(0.05

)

Net realized and unrealized gain (loss) on investment in gold bullion

1.24

(0.67

)

2.73

2.55

(0.21

)

Net change in net assets from operations

1.20

(0.71

)

2.68

2.49

(0.26

)

Net asset value per share, end of year

$

18.65

$

17.45

$

18.16

$

15.48

$

12.99

Total return, at net asset value

6.88

%

(3.91

)%

17.31

%

19.17

%

(1.96

)%

Ratio to average net assets

Net investment loss

(0.25

)%

(0.25

)%

(0.30

)%

(0.40

)%

(0.40

)%

Net expenses

0.25

%

0.25

%

0.30

%

0.40

%

0.40

%

(a)

Calculated

using average shares outstanding.

See

notes to financial statements.

F-7

VanEck

Merk Gold Trust

Schedules

of Investment

January

31, 2023

Fine Ounces

Cost

Value

% of Net Assets

Gold Bullion

341,282

$

572,123,322

$

656,592,807

100.00

%

Total Investments

341,282

$

572,123,322

$

656,592,807

100.00

%

Liabilities in excess of other assets

(9

)

(0.00

)%(a)

Net Assets

$

656,592,798

100.00

%

January

31, 2022

Fine Ounces

Cost

Value

% of Net Assets

Gold Bullion

326,554

$

533,769,944

$

586,245,778

100.00

%

Total Investments

326,554

$

533,769,944

$

586,245,778

100.00

%

Liabilities in excess of other assets

(6

)

(0.00

)%(a)

Net Assets

$

586,245,772

100.00

%

(a)

Amount is less than 0.005%.

See

notes to financial statements.

F-8

VanEck

Merk Gold Trust

Notes

to Financial Statements

1.

ORGANIZATION

The

VanEck Merk Gold Trust (the “Trust”; known as the Merk Gold Trust prior to October 26, 2015 and then as the Van Eck Merk

Gold Trust prior to April 28, 2016) is an investment trust formed on May 6, 2014 under New York law pursuant to a depositary trust agreement.

After consideration of Financial Accounting Standards Topic 946, Merk Investments LLC (the “Sponsor”) has concluded the Trust

meets the fundamental characteristics of an investment company. In addition, while the Trust does not currently possess all of the typical

characteristics of an investment company, it believes its activities are consistent with those of an investment company and will therefore

apply the guidance in Financial Accounting Standards Topic 946, including disclosure of the financial support contractually required

to be provided by an investment company to any of its investees. The Sponsor is responsible for, among other things, overseeing the performance

of The Bank of New York Mellon (the “Trustee”) and the Trust’s principal service providers, including the preparation

of financial statements. The Trustee is responsible for the day-to-day administration of the Trust.

Virtu

Financial, also known as the Lead Market Maker, was the Initial Purchaser and contributed 1,000 Ounces of Gold in exchange for 100,000

shares on May 6, 2014. At contribution, the value of the gold deposited with the Trust was based on the price of an Ounce of Gold of

$1,306.25. The Initial Purchaser is not affiliated with the Sponsor or the Trustee.

The

Trust’s primary objective is to provide investors with an opportunity to invest in gold through the shares and be able to take

delivery of physical gold bullion and gold coins (physical gold) in exchange for their shares (the “Shares”). The Trust’s

secondary objective is for the shares to reflect the performance of the price of gold less the expenses of the Trust’s operations.

The Trust is not actively managed.

The

fiscal year end of the Trust is January 31st.

2.

SIGNIFICANT ACCOUNTING POLICIES

In

preparing financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”),

management makes estimates and assumptions that affect the reported amounts of assets, liabilities and disclosures of contingent assets

and liabilities at the date of the financial statements, as well as the reported amount of revenue and expenses reported during the period.

Actual results could differ from these estimates.

The

accompanying audited financial statements were prepared in accordance with GAAP and with the instructions for the Form 10-Q and the rules

and regulations of the United States Securities and Exchange Commission. In the opinion of the Trust’s management, all adjustments

(which consists of normal recurring adjustments) necessary to present fairly the financial position and the results of operations, as

presented, have been made.

The

following is a summary of significant accounting policies followed by the Trust.

2.1.

Valuation of Gold

Financial

Accounting Standards Board Accounting Standards Codification 820, “Fair Value Measurements and Disclosures” (“ASC 820”),

provides a single definition of fair value, a hierarchy for measuring fair value and expanded disclosures about fair value adjustments.

Various

inputs are used in determining the fair value of the Trust’s assets or liabilities. These inputs are categorized into three broad

levels. Level 1 includes unadjusted prices in active markets for identical assets or liabilities. Level 2 includes other significant

observable market based inputs (including prices for similar securities, interest rates, prepayment speed, and credit risk). Level 3

includes unobservable inputs, which may include management’s own assumptions in determining the fair value of investments. The

Trust does not hold any derivative instruments, and its assets only consist of allocated gold bullion and gold receivable; representing

gold covered by contractually binding orders for the creation of shares where the gold has not yet been transferred to the Trust’s

account and, from time to time, cash, which is used to pay expenses.

F-9

The

following table summarizes the inputs used as of January 31, 2023 in determining the Trust’s investments at fair value for purposes

of ASC 820:

Level 1

Level 2

Level 3

Investment in Gold

$

656,592,807

$

—

$

—

Total

$

656,592,807

$

—

$

—

The

following table summarizes the inputs used as of January 31, 2022 in determining the Trust’s investments at fair value for purposes

of ASC 820:

Level 1

Level 2

Level 3

Investment in Gold

$

586,245,778

$

—

$

—

Total

$

586,245,778

$

—

$

—

London

Gold Delivery Bars are held by JPMorgan Chase Bank, N.A. (the “Custodian”), on behalf of the Trust, at the London, United

Kingdom vaulting premises. All gold is valued based on its Fine Ounce content, calculated by multiplying the weight of gold by its purity;

the same methodology is applied independent of the type of gold held by the Trust; similarly, the value of up to 430 Fine Ounces of unallocated

gold the Trust may hold is calculated by multiplying the number of Fine Ounces with the price of gold determined by the Trustee as follows.

The Trustee determines the net asset value (the “NAV”) of the Trust on each day that NYSE Arca is open for regular trading,

as promptly as practical after 4:00 PM New York time. The NAV of the Trust is the aggregate value of the Trust’s assets less its

estimated accrued but unpaid liabilities (which include accrued expenses). The Trustee computes the NAV per Share by dividing the net

assets of the Trust by the number of the shares outstanding on the date the computation is made.

In

determining the Trust’s NAV, the Trustee values the gold held by the Trust based on the afternoon session of the twice daily fix

of the price of a Fine Ounce of gold which starts at 3:00 PM London, England time and is performed in London by the ICE Benchmark Administration

as an independent third-party administrator (the “LBMA PM Gold Price”). The Trustee also determines the NAV per Share. If

on a day when the Trust’s NAV is being calculated the LBMA PM Gold Price for that day is not available, the Trustee will value

the gold held by the Trust based on that day’s morning session of the twice daily fix of the price of a Fine Ounce of gold, which

starts at 10:30 AM London, England time and is performed in London by the ICE Benchmark Administration as an independent third-party

administrator (the “LBMA AM Gold Price”). If no fix is available for the day, the Trustee will value the Trust’s gold

based on the most recently announced LBMA AM Gold Price or LBMA PM Gold Price. Prior to March 20, 2015, the Trustee utilized the daily

fix of the price of a Fine Ounce of gold as performed by the five members of the London gold fix, which has now been replaced by the

ICE Benchmark Administration as an independent third-party administrator.

2.2.

Expenses

The

Trustee issues shares to pay the Sponsor’s fee; the Sponsor pays the Trust’s ordinary expenses. The NAV of the Trust is used

to compute the Sponsor’s fee, and the Trustee subtracts from the NAV of the Trust the amount of accrued Sponsor’s fee. To

the extent the Trust issues additional shares to pay the Sponsor’s fee or sells gold to cover expenses or liabilities, the amount

of gold represented by each share will decrease. New deposits of gold, received in exchange for new shares issued by the Trust, would

not reverse this trend.

2.3.

Creations and Redemptions of Shares

Shares

are issued and redeemed by the Trust in blocks of 50,000 shares called “Baskets” in exchange for gold from certain registered

broker-dealers or other securities market participants (“Authorized Participants”). Investors that are not Authorized Participants

may also take delivery of physical gold in exchange for their shares (“Delivery Applicants”).

Authorized

Participants

The

Trust issues and redeems Baskets only to Authorized Participants. The creation and redemption of Baskets will only be made in exchange

for the delivery to the Trust or the distribution by the Trust of the amount of gold represented by the Baskets being created or redeemed,

the amount of which will be based on the combined Fine Ounces represented by the number of shares included in the Baskets being created

or redeemed determined on the day the order to create or redeem Baskets is properly received.

F-10

Orders

to create and redeem Baskets may be placed only by Authorized Participants. An Authorized Participant must: (1) be a registered broker-dealer

or other securities market participant, such as a bank or other financial institution, which, but for an exclusion from registration,

would be required to register as a broker-dealer to engage in securities transactions, (2) be a participant in DTC, and (3) must have

an agreement with the Custodian establishing an unallocated account in London or have an existing unallocated account meeting the standards

described herein. To become an Authorized Participant, a person must enter into an Authorized Participant Agreement with the Sponsor

and the Trustee. The Authorized Participant Agreement provides the procedures for the creation and redemption of Baskets and for the

delivery of the gold required for such creations and redemptions. The Authorized Participant Agreement and the related procedures attached

thereto may be amended by the Trustee and the Sponsor, without the consent of any investor or Authorized Participant. A transaction fee

of $500 will be assessed on all creation and redemption transactions. Multiple Baskets may be created on the same day, provided each

Basket meets the requirements described below and that the Custodian is able to allocate gold to the Trust Allocated Account such that

the Trust Unallocated Account holds no more than 430 Fine Ounces of gold at the close of a business day.

Authorized

Participants who make deposits with the Trust in exchange for Baskets will receive no fees, commissions or other form of compensation

or inducement of any kind from either the Sponsor or the Trust, and no such person has any obligation or responsibility to the Sponsor

or the Trust to effect any sale or resale of shares.

Delivery

Applicants

In

exchange for its shares and payment of a processing fee, a Delivery Applicant will be entitled to one or more bars or coins of physical

gold having approximately the total Fine Ounces represented by the shares on the day on which the Delivery Applicant’s broker-dealer

submits his or her shares to the Trust in exchange for physical gold. As it is unlikely that the total Fine Ounces of physical gold will

exactly correspond to the Fine Ounces represented by a specific number of shares, a Delivery Applicant will likely receive some cash

representing the net sale proceeds of any excess Fine Ounces (the “Cash Proceeds”). To minimize the Cash Proceeds of any

exchange, the delivery application requires that the number of shares submitted closely correspond in Fine Ounces to the Fine Ounces

of physical gold that is held or that is to be acquired by the Trust for which the delivery is sought. Share submissions are processed

in the order approved.

Changes

in the shares for the year ending January 31, 2023 are as follows:

Shares

Amount

Shares, beginning of year at February 1, 2022

33,599,843

$

532,684,047

Shares issued

7,638,953

137,482,147

Shares redeemed

(6,035,537

)

(98,749,384

)

Shares, end of year at January 31, 2023

35,203,259

$

571,416,810

Changes

in the shares for the year ending January 31, 2022 are as follows:

Shares

Amount

Shares, beginning of year at February 1, 2021

24,366,372

$

370,737,948

Shares issued

10,223,025

179,243,246

Shares redeemed

(989,554

)

(17,297,147

)

Shares, end of year at January 31, 2022

33,599,843

$

532,684,047

Changes

in the shares for the year ending January 31, 2021 are as follows:

Shares

Amount

Shares, beginning of year at February 1, 2020

12,817,945

$

165,051,803

Shares issued

13,807,611

244,523,754

Shares redeemed

(2,259,184

)

(38,837,609

)

Shares, end of year at January 31, 2021

24,366,372

$

370,737,948

F-11

2.4.

Income Taxes

The

Trust is treated as a “grantor trust” for U.S. federal tax purposes. As a result, the Trust itself is not subject to U.S.

federal income tax. Instead, the Trust’s income and expenses “flow through” to the shareholders and the Trustee reports

the Trust’s income, gains, losses and deductions to the Internal Revenue Service on that basis.

The

Sponsor has evaluated whether or not there are uncertain tax positions that require financial statement recognition and has determined

that no reserves for uncertain tax positions are required as of January 31, 2023.

2.5.

Revenue Recognition Policy

A

gain or loss is recognized based on the difference between the selling price and the average cost method of the gold sold on a trade

date basis.

3.

INVESTMENT IN GOLD

The

following represents the changes in Ounces of gold and the respective fair value at January 31, 2023:

Ounces

Fair Value

Beginning balance as of February 1, 2022

326,554

$

586,245,778

Gold bullion contributed

73,293

135,924,342

Gold bullion distributed

(58,565

)

(98,749,370

)

Realized gain (loss) from gold distributed from in-kind

—

1,178,406

Change in unrealized appreciation (depreciation)

—

31,993,651

Ending balance as of January 31, 2023

341,282

$

656,592,807

The

following represents the changes in Ounces of gold and the respective fair value at January 31, 2022:

Ounces

Fair Value

Beginning balance as of February 1, 2021

237,409

$

442,483,116

Gold bullion contributed

98,772

177,971,942

Gold bullion distributed

(9,627

)

(17,297,123

)

Realized gain (loss) from gold distributed from in-kind

—

1,756,856

Change in unrealized appreciation (depreciation)

—

(18,669,013

)

Ending balance as of January 31, 2022

326,554

$

586,245,778

The

following represents the changes in ounces of gold and the respective fair value at January 31, 2021:

Ounces

Fair Value

Beginning balance as of February 1, 2020

125,287

$

198,479,752

Gold bullion contributed

134,167

243,510,455

Gold bullion distributed

(22,045

)

(38,837,599

)

Realized gain (loss) from gold distributed from in-kind

—

7,325,362

Change in unrealized appreciation (depreciation)

—

32,005,146

Ending balance as of January 31, 2021

237,409

$

442,483,116

F-12

4.

RELATED PARTIES—SPONSOR, TRUSTEE, CUSTODIAN AND MARKETING FEES

Fees

paid are to the Sponsor as compensation for services performed under the Trust Agreement. Effective July 24, 2020, the Sponsor’s

fee is payable at an annualized rate of 0.25% of the Trust’s NAV, accrued on a daily basis computed on the prior Business Day’s

NAV and paid monthly in arrears. Prior to July 24, 2020, the Sponsor’s fee accrued at an annualized rate of 0.40% of the Trust’s

NAV.

The

Sponsor has agreed to assume the following administrative and marketing expenses incurred by the Trust: the Trustee’s monthly fee

and out-of-pocket expenses; the Custodian’s fee; the marketing support fees and expenses (including the fees and expenses of Foreside

Fund Services, LLC); expenses reimbursable under the Custody Agreement; the precious metals dealer’s fees and expenses reimbursable

under its agreement with the Sponsor; exchange listing fees; Securities and Exchange Commission (the “SEC”) registration

fees; printing and mailing costs; maintenance expenses for the Trust’s website; audit fees; and up to $100,000 per annum in legal

expenses.

Affiliates

of the Trustee, as well as affiliates of the Custodian may from time to time act as Authorized Participants to purchase or sell gold

or shares for their own account, as agent for their customers and for accounts over which they exercise investment discretion.

On

October 22, 2015, the Sponsor, for the benefit of the Trust, entered into a Marketing Agent Agreement (as amended to date, the “Marketing

Agreement”) with Van Eck Securities Corporation (“VanEck” or “Marketing Agent”). Pursuant to the Marketing

Agreement, VanEck provides assistance in the marketing of the shares. The obligations created by the Marketing Agreement are obligations

of the Sponsor of the Trust and any fees payable under the Marketing Agreement to VanEck are payable from the Sponsor’s fee (as

calculated and defined in the Trust Agreement). The Trust will not incur additional financial or other performance obligations pursuant

to the Marketing Agreement.

5.

CONCENTRATION OF RISK

The

Trust’s sole business activity is the investment in gold bullion. Several factors could affect the price of gold: (i) global gold

supply and demand, which is influenced by such factors as forward selling by gold producers, purchases made by gold producers to unwind

gold hedge positions, central bank purchases and sales, and production and cost levels in major gold-producing countries; (ii) investors’

expectations with respect to the rate of inflation; (iii) currency exchange rates; (iv) interest rates; (v) investment and trading activities

of hedge funds and commodity funds; and (vi) global or regional political, economic or financial events and situations. In addition,

there is no assurance that gold will maintain its long-term value in terms of purchasing power in the future. In the event that the price

of gold declines, the Sponsor expects the value of an investment in the shares to decline proportionately. Each of these events could

have a material adverse effect on the Trust’s financial position and results of operations.

6.

UNCERTAINTY REGARDING THE EFFECT OF COVID-19

The

price of the Shares could be adversely affected by the effects of COVID-19

COVID-19

has not had a significant impact on the Trust. There have been some signs of increased demand for physical gold as well as some supply

constraints for certain coins at times during the pandemic. As a result, precious metals dealers have increased coin and bar premiums

at times. The Sponsor regularly updates available coins and Processing Fees on merkgold.com/fees.

F-13

7.

INDEMNIFICATION

Under

the Trust’s organizational documents, each of the Trustee (and its directors, employees and agents) and the Sponsor (and its members,

managers, directors, officers, employees, affiliates) is indemnified against any liability, cost or expense it incurs without gross negligence,

bad faith or willful misconduct on its part and without reckless disregard on its part of its obligations and duties under the Trust’s

organizational documents. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims

that may be made against the Trust that have not yet occurred. However, based on industry experience, management believes the risk of

loss is remote.

8.

SUBSEQUENT EVENTS

The

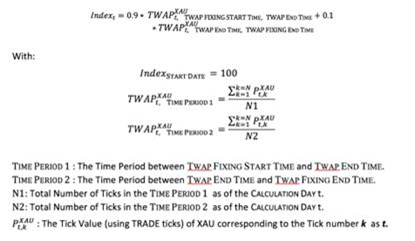

pricing index the Sponsor uses in relation to the Shares issued by the Trust intends to change to reference the Solactive Gold Spot Index

(the “Solactive Index”) in lieu of the LBMA PM Gold Price. The date on which such change becomes effective is referred to

herein as the “Index Change Date.”

Following

the Index Change Date, in determining the Trust’s NAV, the Trustee will value the gold held by the trust based on the Solactive

Index. Solactive AG (“Solactive”) will own, calculate, and disseminate the Solactive Index. The Solactive Index is a U.S.

Dollar denominated index that aims to provide a price fixing for the gold spot price quoted as U.S. Dollars per Troy Ounce (“XAU”)

and determined for the close of trading on the New York Stock Exchange (“NYSE”). The Solactive Index calculates gold bullion

fixing prices by taking Time Weighted Average Prices (“TWAP”) of XAU trading prices provided via ICE Data Services (“IDS”)

data feed.

Specifically,

the Solactive Index uses a TWAP calculation to determine an average price that is time-weighted, using tick values of actual transactions

(“Trade Ticks”) for two specified time periods around the scheduled close of trading on the NYSE (generally, 4:00 PM Eastern

Time). The TWAP is derived for (1) the period ahead of the fixing (“Time Period 1”), which consists of the five minutes before

the close of trading, and (2) the period directly after the fixing (“Time Period 2”), which consists of the six seconds after

the close of trading. The TWAPs for Time Period 1 and Time Period 2 are then aggregated, with 90% weighting given to Time Period 1 and

10% weighting given to Time Period 2, to calculate the Solactive Index.

For

any calculation day t, the Solactive Index (Indext), is determined in accordance with the following formula:

The

Solactive Index is calculated and published by Solactive no later than 30 minutes following the close of trading on the NYSE, disseminated

to major financial data providers, and made publicly available via the Trust’s website.

The

Solactive Index calculation is based on XAU market data from IDS, which is a major provider of financial market data. The data is available

through IDS’s data streaming service, which covers 2,700 spot rates and over 7,500 forwards and non-deliverable forwards, with

an average of over 130 million updates per day for spot. IDS compiles data from over 100 sources, including market makers, execution

venues, banks and brokers from across the globe, and every updating Trade Tick of spot streaming data is available via IDS’s Integrated

Data Viewer service in a file-based format.

F-14

It

is unlikely that, on any given trading day for the Shares, there would be no Trade Ticks recorded for XAU in either Time Period 1 or

Time Period 2, such that the Solactive Index calculation could not be performed on such day. Trade Ticks representing XAU are the closing

prices for specific gold bullion transactions posted in a 24-hour, global, over-the-counter gold bullion market, which is not subject

to trading suspensions, trading halts, or market closures. However, in the unlikely event that IDS is unable to publish pricing information

for XAU, for whatever reason, during either Time Period 1 or Time Period 2 on a given trading day, the last available Solactive Index

calculation will be used in accordance with Solactive’s published and publicly available disruption policy.

If

the Sponsor determines that such price is inappropriate to use, it shall identify an alternate basis for evaluation to be employed by

the Trustee. The Sponsor may instruct the Trustee to use a different publicly available price which the Sponsor determines to fairly

represent the commercial value of the Trust’s gold.

The

Trustee’s estimation of accrued but unpaid fees, expenses and liabilities will be conclusive upon all persons interested in the

Trust, and no revision or correction in any computation made under the Trust Agreement will be required by reason of any difference in

amounts estimated from those actually paid.

The

Sponsor and the investors may rely on any evaluation or determination of any amount made by the Trustee, and except for any determination

by the Sponsor as to the price to be used to evaluate gold, the Sponsor will have no responsibility for the evaluation’s accuracy.

The determinations the Trustee makes will be made in good faith upon the basis of, and the Trustee will not be liable for any errors

contained in, information reasonably available to it. The Trustee will not be liable to the Sponsor, Authorized Participants, the investors

or any other person for errors in judgment. However, the preceding liability exclusion will not protect the Trustee against any liability

resulting from bad faith or gross negligence in the performance of its duties.

The

Sponsor will give 60 day notice of the Index Change Date by issuing a press release and filing an 8-K.

Management

has evaluated the events and transactions that have occurred through the date the financial statements were issued and noted no items

requiring adjustment of the financial statements.

*

* *

This

report is submitted for the general information of the shareholders. It is not authorized for distribution to prospective investors unless

preceded or accompanied by an effective prospectus, which includes information regarding the Trust’s risks, objectives, fees and

expenses and other information.

F-15

SIGNATURES

Pursuant

to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed

on its behalf by the undersigned in its capacities* thereunto duly authorized.

MERK INVESTMENTS LLC

Sponsor of the VanEck Merk Gold Trust

Date: February 29, 2024

/s/ Axel Merk

Axel Merk

President and Chief Investment Officer

(Principal Executive Officer and

Principal Financial Officer)

*

The

Registrant is a trust and the person is signing in his capacity as an officer of Merk Investments LLC, the Sponsor of the Registrant.

EX-23.1

2

ea0200989ex23-1_vaneck.htm

CONSENT OF COHEN & COMPANY, LTD., INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Exhibit

23.1

CONSENT

OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

We

consent to the use of our report dated April 12, 2023, with respect to the statement of assets and liabilities of VanEck Merk Gold Trust

(the “Trust”), including the schedule of investment, as of January 31, 2023, and the related statements of operations and

changes in net assets, and the financial highlights for the year then ended and the effectiveness of internal control over financial

reporting as of January 31, 2023, incorporated herein by reference.

COHEN & COMPANY, LTD.

Philadelphia, Pennsylvania

February 29, 2024

COHEN & COMPANY, LTD.

800.229.1099

| 866.818.4538 fax | cohencpa.com

Registered

with the Public Company Accounting Oversight Board

EX-23.2

3

ea0200989ex23-2_vaneck.htm

CONSENT OF BBD, LLP, INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Exhibit

23.2

CONSENT

OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

We

consent to the use of our report dated April 12, 2022, with respect to the statements of assets and liabilities of VanEck Merk Gold Trust

(the “Trust”), including the schedules of investment, as of January 31, 2022 and 2021, and the related statements of operations

and changes in net assets for the three-year period ended January 31, 2022 and the financial highlights for the five-year period ended

January 31, 2022 and the effectiveness of internal control over financial reporting as of January 31, 2022, incorporated herein by reference.

UNDER

THE SECURITIES EXCHANGE ACT OF 1934, AS AMENDED

I,

Axel Merk, certify that:

1.

I

have reviewed this Report on Form 10-K/A of VanEck Merk Gold Trust (the “Trust”);

2.

Based

on my knowledge, this report does not contain any untrue statement of a material fact or

omit to state a material fact necessary to make the statements made, in light of the circumstances

under which such statements were made, not misleading with respect to the period covered

by this report;

3.

Based

on my knowledge, the financial statements, and other financial information included in this

report, fairly present in all material respects the financial condition, results of operations

and cash flows of the registrant as of, and for, the periods presented in this report;

4.

[Intentionally

Omitted.]

5.

[Intentionally

Omitted.]

Date: February 29, 2024

/s/ Axel Merk

Axel Merk*

President and Chief Investment Officer

(Principal Executive Officer and Principal Financial Officer)

*

The

Registrant is a trust and Mr. Merk is signing in his capacities as officers of Merk Investments LLC, the Sponsor of the Registrant.

**

The

original executed copy of this Certification will be maintained at the Sponsor’s offices and will be made available for inspection

upon request.

CERTIFICATION

PURSUANT TO 18 U.S.C. SECTION 1350 AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In

connection with the Annual Report of VanEck Merk Gold Trust (the “Trust”) on Form 10-K/A for the year ended January 31, 2023

as filed with the Securities and Exchange Commission on the date hereof (the “Report”), the undersigned, in the capacity

and on the date indicated below, hereby certifies pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley

Act of 2002, that:

1.

The

Report fully complies with the requirements of section 13(a) or 15(d) of the Securities Exchange

Act of 1934, as amended; and

2.

The

information contained in the Report fairly presents, in all material respects, the financial

condition and results of operations of the Trust.

Date: February 29, 2024

/s/ Axel Merk

Axel Merk*

President and Chief Investment Officer

(Principal Executive Officer and

Principal Financial Officer)

*

The Registrant is a trust and Mr. Merk is signing in his capacities as officers of Merk Investments LLC, the Sponsor of the Registrant.

**

The

original executed copy of this Certification will be maintained at the Sponsor’s offices and will be made available for inspection

upon request.

This

Amendment No. 1 on Form 10-K/A (this “Amendment”) amends certain items of the Annual Report on Form 10-K for the fiscal year

ended January 31, 2023 of VanEck Merk Gold Trust (the “Trust”), originally filed with the Securities and Exchange Commission

(“SEC”) on April 13, 2023 (the “Original Form 10-K”). This Amendment amends the Original Form 10-K include the

audit report of BBD, LLP with respect to the assets and liabilities of the Trust, including the schedules of investment, as of January

31, 2022 and 2021, and the related statements of operations and changes in net assets for each of the years in the three-year period

ended January 31, 2022, the financial highlights for each of the years in the five-year period ended January 31, 2022, and the related

notes (the “BBD Audit Report”). The BBD Audit Report was inadvertently omitted from the Original Form 10-K.

Fiscal period values are FY, Q1, Q2, and Q3. 1st, 2nd and 3rd quarter 10-Q or 10-QT statements have value Q1, Q2, and Q3 respectively, with 10-K, 10-KT or other fiscal year statements having FY.

This is focus fiscal year of the document report in YYYY format. For a 2006 annual report, which may also provide financial information from prior periods, fiscal 2006 should be given as the fiscal year focus. Example: 2006.

Line items represent financial concepts included in a table. These concepts are used to disclose reportable information associated with domain members defined in one or many axes to the table.

For the EDGAR submission types of Form 8-K: the date of the report, the date of the earliest event reported; for the EDGAR submission types of Form N-1A: the filing date; for all other submission types: the end of the reporting or transition period. The format of the date is YYYY-MM-DD.

The type of document being provided (such as 10-K, 10-Q, 485BPOS, etc). The document type is limited to the same value as the supporting SEC submission type, or the word 'Other'.

Indicate number of shares or other units outstanding of each of registrant's classes of capital or common stock or other ownership interests, if and as stated on cover of related periodic report. Where multiple classes or units exist define each class/interest by adding class of stock items such as Common Class A [Member], Common Class B [Member] or Partnership Interest [Member] onto the Instrument [Domain] of the Entity Listings, Instrument.

Indicate 'Yes' or 'No' whether registrants (1) have filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that registrants were required to file such reports), and (2) have been subject to such filing requirements for the past 90 days. This information should be based on the registrant's current or most recent filing containing the related disclosure.

Commission file number. The field allows up to 17 characters. The prefix may contain 1-3 digits, the sequence number may contain 1-8 digits, the optional suffix may contain 1-4 characters, and the fields are separated with a hyphen.

Indicate whether the registrant is one of the following: Large Accelerated Filer, Accelerated Filer, Non-accelerated Filer. Definitions of these categories are stated in Rule 12b-2 of the Exchange Act. This information should be based on the registrant's current or most recent filing containing the related disclosure.

Boolean flag that is true when the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant's most recently completed second fiscal quarter.

Indicate 'Yes' or 'No' if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Is used on Form Type: 10-K, 10-Q, 8-K, 20-F, 6-K, 10-K/A, 10-Q/A, 20-F/A, 6-K/A, N-CSR, N-Q, N-1A.

Carrying value as of the balance sheet date of obligations incurred and payable, pertaining to costs that are statutory in nature, are incurred on contractual obligations, or accumulate over time and for which invoices have not yet been received or will not be rendered. Examples include taxes, interest, rent and utilities.

Amount of excess of issue price over par or stated value of stock and from other transaction involving stock or stockholder. Includes, but is not limited to, additional paid-in capital (APIC) for common and preferred stock.

Sum of the carrying amounts as of the balance sheet date of all assets that are recognized. Assets are probable future economic benefits obtained or controlled by an entity as a result of past transactions or events.

Sum of the carrying amounts as of the balance sheet date of all liabilities that are recognized. Liabilities are probable future sacrifices of economic benefits arising from present obligations of an entity to transfer assets or provide services to other entities in the future.

Amount to be paid per share that is classified as temporary equity by entity upon redemption. Temporary equity is a security with redemption features that are outside the control of the issuer, is not classified as an asset or liability in conformity with GAAP, and is not mandatorily redeemable. Includes any type of security that is redeemable at a fixed or determinable price or on a fixed or determinable date or dates, is redeemable at the option of the holder, or has conditions for redemption which are not solely within the control of the issuer. If convertible, the issuer does not control the actions or events necessary to issue the maximum number of shares that could be required to be delivered under the conversion option if the holder exercises the option to convert the stock to another class of equity. If the security is a warrant or a rights issue, the warrant or rights issue is considered to be temporary equity if the issuer cannot demonstrate that it would be able to deliver upon the exercise of the option by the holder in all cases. Includes stock with put option held by ESOP and stock redeemable by holder only in the event of a change in control of the issuer.

The number of securities classified as temporary equity that have been issued and are held by the entity's shareholders. Securities outstanding equals securities issued minus securities held in treasury. Temporary equity is a security with redemption features that are outside the control of the issuer, is not classified as an asset or liability in conformity with GAAP, and is not mandatorily redeemable. Includes any type of security that is redeemable at a fixed or determinable price or on a fixed or determinable date or dates, is redeemable at the option of the holder, or has conditions for redemption which are not solely within the control of the issuer. If convertible, the issuer does not control the actions or events necessary to issue the maximum number of shares that could be required to be delivered under the conversion option if the holder exercises the option to convert the stock to another class of equity. If the security is a warrant or a rights issue, the warrant or rights issue is considered to be temporary equity if the issuer cannot demonstrate that it would be able to deliver upon the exercise of the option by the holder in all cases. Includes stock with put option held by ESOP and stock redeemable by holder only in the event of a change in control of the issuer.

Amount after tax of income (loss) from a discontinued operation including the portion attributable to the noncontrolling interest. Includes, but is not limited to, the income (loss) from operations during the phase-out period, gain (loss) on disposal, gain (loss) for reversal of write-down (write-down) to fair value, less cost to sell, and adjustments to a prior period gain (loss) on disposal.

Amount, after investment expense, of income earned from investments in securities and real estate. Includes, but is not limited to, real estate investment, policy loans, dividends, and interest. Excludes realized gain (loss) on investments.

Generally recurring costs associated with normal operations except for the portion of these expenses which can be clearly related to production and included in cost of sales or services. Includes selling, general and administrative expense.

Fees paid to advisors who provide certain management support and administrative oversight services including the organization and sale of stock, investment funds, limited partnerships and mutual funds.

The increase (decrease) during the reporting period in the aggregate value of all inventory held by the reporting entity, associated with underlying transactions that are classified as operating activities.

Amount, after investment expense, of income earned from investments in securities and real estate. Includes, but is not limited to, real estate investment, policy loans, dividends, and interest. Excludes realized gain (loss) on investments.

The entire disclosures of supplemental information, including descriptions and amounts, related to the balance sheet, income statement, and/or cash flow statement.

The

VanEck Merk Gold Trust (the “Trust”; known as the Merk Gold Trust prior to October 26, 2015 and then as the Van Eck Merk

Gold Trust prior to April 28, 2016) is an investment trust formed on May 6, 2014 under New York law pursuant to a depositary trust agreement.

After consideration of Financial Accounting Standards Topic 946, Merk Investments LLC (the “Sponsor”) has concluded the Trust

meets the fundamental characteristics of an investment company. In addition, while the Trust does not currently possess all of the typical

characteristics of an investment company, it believes its activities are consistent with those of an investment company and will therefore

apply the guidance in Financial Accounting Standards Topic 946, including disclosure of the financial support contractually required

to be provided by an investment company to any of its investees. The Sponsor is responsible for, among other things, overseeing the performance

of The Bank of New York Mellon (the “Trustee”) and the Trust’s principal service providers, including the preparation

of financial statements. The Trustee is responsible for the day-to-day administration of the Trust.

Virtu

Financial, also known as the Lead Market Maker, was the Initial Purchaser and contributed 1,000 Ounces of Gold in exchange for 100,000

shares on May 6, 2014. At contribution, the value of the gold deposited with the Trust was based on the price of an Ounce of Gold of

$1,306.25. The Initial Purchaser is not affiliated with the Sponsor or the Trustee.

The

Trust’s primary objective is to provide investors with an opportunity to invest in gold through the shares and be able to take

delivery of physical gold bullion and gold coins (physical gold) in exchange for their shares (the “Shares”). The Trust’s

secondary objective is for the shares to reflect the performance of the price of gold less the expenses of the Trust’s operations.

The Trust is not actively managed.

In

preparing financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”),

management makes estimates and assumptions that affect the reported amounts of assets, liabilities and disclosures of contingent assets

and liabilities at the date of the financial statements, as well as the reported amount of revenue and expenses reported during the period.

Actual results could differ from these estimates.

The

accompanying audited financial statements were prepared in accordance with GAAP and with the instructions for the Form 10-Q and the rules

and regulations of the United States Securities and Exchange Commission. In the opinion of the Trust’s management, all adjustments

(which consists of normal recurring adjustments) necessary to present fairly the financial position and the results of operations, as

presented, have been made.

The

following is a summary of significant accounting policies followed by the Trust.

2.1.

Valuation of Gold

Financial

Accounting Standards Board Accounting Standards Codification 820, “Fair Value Measurements and Disclosures” (“ASC 820”),

provides a single definition of fair value, a hierarchy for measuring fair value and expanded disclosures about fair value adjustments.

Various

inputs are used in determining the fair value of the Trust’s assets or liabilities. These inputs are categorized into three broad

levels. Level 1 includes unadjusted prices in active markets for identical assets or liabilities. Level 2 includes other significant

observable market based inputs (including prices for similar securities, interest rates, prepayment speed, and credit risk). Level 3

includes unobservable inputs, which may include management’s own assumptions in determining the fair value of investments. The

Trust does not hold any derivative instruments, and its assets only consist of allocated gold bullion and gold receivable; representing

gold covered by contractually binding orders for the creation of shares where the gold has not yet been transferred to the Trust’s

account and, from time to time, cash, which is used to pay expenses.

The

following table summarizes the inputs used as of January 31, 2023 in determining the Trust’s investments at fair value for purposes

of ASC 820:

Level 1

Level 2

Level 3

Investment in Gold

$

656,592,807

$

—

$

—

Total

$

656,592,807

$

—

$

—

The

following table summarizes the inputs used as of January 31, 2022 in determining the Trust’s investments at fair value for purposes

of ASC 820:

Level 1

Level 2

Level 3

Investment in Gold

$

586,245,778

$

—

$

—

Total

$

586,245,778

$

—

$

—

London

Gold Delivery Bars are held by JPMorgan Chase Bank, N.A. (the “Custodian”), on behalf of the Trust, at the London, United

Kingdom vaulting premises. All gold is valued based on its Fine Ounce content, calculated by multiplying the weight of gold by its purity;

the same methodology is applied independent of the type of gold held by the Trust; similarly, the value of up to 430 Fine Ounces of unallocated

gold the Trust may hold is calculated by multiplying the number of Fine Ounces with the price of gold determined by the Trustee as follows.

The Trustee determines the net asset value (the “NAV”) of the Trust on each day that NYSE Arca is open for regular trading,

as promptly as practical after 4:00 PM New York time. The NAV of the Trust is the aggregate value of the Trust’s assets less its

estimated accrued but unpaid liabilities (which include accrued expenses). The Trustee computes the NAV per Share by dividing the net

assets of the Trust by the number of the shares outstanding on the date the computation is made.

In

determining the Trust’s NAV, the Trustee values the gold held by the Trust based on the afternoon session of the twice daily fix

of the price of a Fine Ounce of gold which starts at 3:00 PM London, England time and is performed in London by the ICE Benchmark Administration

as an independent third-party administrator (the “LBMA PM Gold Price”). The Trustee also determines the NAV per Share. If

on a day when the Trust’s NAV is being calculated the LBMA PM Gold Price for that day is not available, the Trustee will value

the gold held by the Trust based on that day’s morning session of the twice daily fix of the price of a Fine Ounce of gold, which

starts at 10:30 AM London, England time and is performed in London by the ICE Benchmark Administration as an independent third-party

administrator (the “LBMA AM Gold Price”). If no fix is available for the day, the Trustee will value the Trust’s gold

based on the most recently announced LBMA AM Gold Price or LBMA PM Gold Price. Prior to March 20, 2015, the Trustee utilized the daily

fix of the price of a Fine Ounce of gold as performed by the five members of the London gold fix, which has now been replaced by the

ICE Benchmark Administration as an independent third-party administrator.

2.2.

Expenses

The

Trustee issues shares to pay the Sponsor’s fee; the Sponsor pays the Trust’s ordinary expenses. The NAV of the Trust is used

to compute the Sponsor’s fee, and the Trustee subtracts from the NAV of the Trust the amount of accrued Sponsor’s fee. To

the extent the Trust issues additional shares to pay the Sponsor’s fee or sells gold to cover expenses or liabilities, the amount

of gold represented by each share will decrease. New deposits of gold, received in exchange for new shares issued by the Trust, would

not reverse this trend.

2.3.

Creations and Redemptions of Shares

Shares

are issued and redeemed by the Trust in blocks of 50,000 shares called “Baskets” in exchange for gold from certain registered

broker-dealers or other securities market participants (“Authorized Participants”). Investors that are not Authorized Participants

may also take delivery of physical gold in exchange for their shares (“Delivery Applicants”).

Authorized

Participants

The

Trust issues and redeems Baskets only to Authorized Participants. The creation and redemption of Baskets will only be made in exchange

for the delivery to the Trust or the distribution by the Trust of the amount of gold represented by the Baskets being created or redeemed,

the amount of which will be based on the combined Fine Ounces represented by the number of shares included in the Baskets being created

or redeemed determined on the day the order to create or redeem Baskets is properly received.

Orders

to create and redeem Baskets may be placed only by Authorized Participants. An Authorized Participant must: (1) be a registered broker-dealer