Free Writing Prospectus

To Preliminary Prospectus dated March 14, 2012

Filed pursuant to Rule 433

Registration Statement No. 333-179839

Dated March 15, 2012

Rebirth: Innovations

Michiel Herkemij CEO

Ingrid Baron CMO

Disclaimer

DE International Holdings B.V. has filed a registration statement (including a prospectus) with the U.S. Securities and Exchange Commission (SEC) for the offering to which this communication relates. You should read the prospectus in that registration statement and other documents DE International Holdings B.V. has filed with the SEC for more complete information about DE International Holdings B.V. and this offering. You may get these documents for free by visiting EDGAR on the SEC website at

ov. Alternatively, you can obtain a copy of the prospectus by writing to DE International Holdings at: DE International Holdings, Attn: Investor Relations, Vleutensevaart 100, Utrecht, 3532 AD, The Netherlands or by sending an email to offeeteaco@saralee.com

These materials do not constitute an offer to acquire securities or a prospectus within the meaning of the Dutch Financial Markets Supervision Act (Wet op het financieel toezicht). In connection with the admission to trading on NYSE Euronext in Amsterdam, a prospectus approved by the Netherlands Authority for the Financial Markets (Stichting Autoriteit Financiele Markten or “AFM”) will be made generally available in The Netherlands. Any investor should make his investment decision solely on the basis of the information contained in the prospectus. When made generally available, copies of the AFM-approved prospectus may be obtained at no cost by writing to DE International Holdings at: DE International Holdings, Attn: Investor Relations, Vleutensevaart 100, Utrecht, 3532 AD, The Netherlands or by sending an email to offeeteaco@saralee.com

Some of the information presented herein contains forward-looking statements. All statements other than statements of historical fact regarding our business, financial condition, results of operations and certain of our plans, objectives, assumptions, projections, expectations or beliefs with respect to these items and statements regarding other future events or prospects, are forward-looking statements. These statements include, without limitation, those concerning: the anticipated costs and benefits of restructuring actions taken to prepare for the separation; our ability to complete the separation; the timetable for completion of the separation; the expected benefits of the separation; CoffeeCo’s ability to declare and pay the CoffeeCo Special Dividend; our access to credit markets; and the funding of pension plans. These statements may be preceded by terms such as “expects,” “anticipates,” “projects” or “believes.”

In addition, this presentation may include forward-looking statements relating to our potential exposure to various types of market risks, such as commodity price risks, foreign exchange rate risks, interest rate risks and other risks related to financial assets and liabilities. We have based these forward-looking statements on our management’s current view with respect to future events and financial performance. These forward-looking statements are based on currently available competitive, financial and economic data, as well as management’s views and assumptions regarding future events, and are inherently uncertain. Although we believe that the estimates reflected in the forward-looking statements are reasonable, such estimates may prove to be incorrect. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements. These factors include, among other things, those listed in the section of the prospectus entitled “Risk Factors.”

We urge you to read the sections of the prospectus entitled “Risk Factors,” “Operating and Financial Review,” “Industry Overview” and “Business” for a discussion of the factors that could affect our future performance and the industry in which we operate. Additionally, new risk factors can emerge from time to time, and it is not possible for us to predict all such risk factors. Given these risks and uncertainties, you should not place undue reliance on forward-looking statements as a prediction of actual results.

All forward-looking statements included herein are based on information available to us on the date of this presentation. We undertake no obligation to update publicly or revise any forward-looking statement in this presentation, whether as a result of new information, future events or otherwise, except as may be required by applicable law. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained throughout the prospectus.

| 2 |

Creating the Senseo Sensation

Source: Company analysis based on Euromonitor, Nielsen and company estimates 4

Single Serve is the Fastest Growing

Segment in Coffee

Estimated world single serve sales (in € bn)

Estimated world single serve volumes (in mln ton)

CAGR +30%

CAGR+25%

2006 2011 2006 2011

5.4

1.6

191

64

Estimated company shares global single serve market (in %)

Others Private Labels

MASTER

BLENDERS Nestle

Source: Company analysis based on Euromonitor, Nielsen and company estimates 5

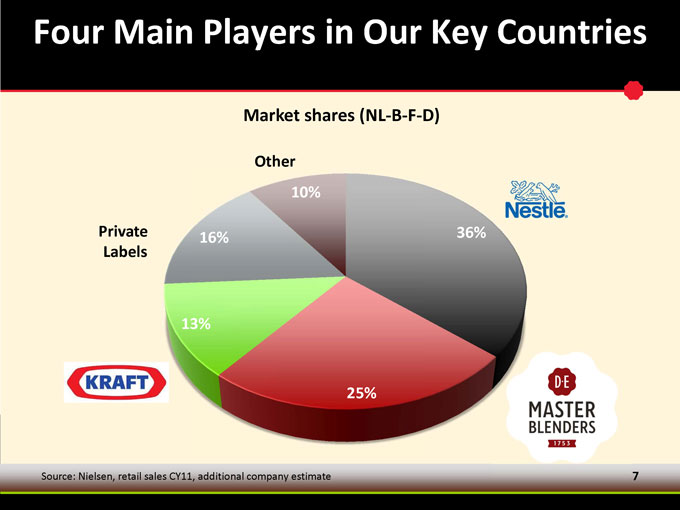

Senseo Today

• 11 years in the market

• € 400 mln business

• 95% of sales in 4 key countries (NL, B, F, D)

• Successfully launched in Spain in 2009

Market shares (NL-B-F-D)

Other

Private

Labels

MASTER

BLENDERS

1753

Source: Nielsen, retail sales CY11, additional company estimate 7

Four Main Appliance Platforms

MASTER

BLENDERS

TQSSIMO

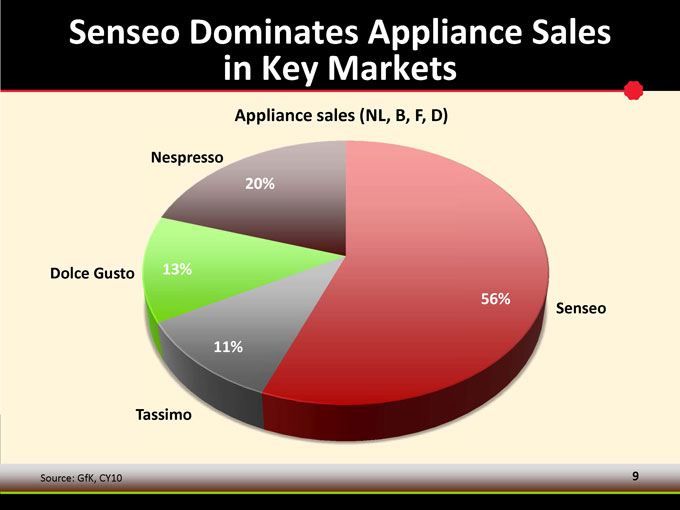

Senseo Dominates Appliance Sales

in Key Markets

Appliance sales (NL, B, F, D)

Nespresso

Dolce Gusto

Senseo

Tassimo

Source: GfK, CY10

Senseo Outsells the Other Appliance Platforms in Its Key Markets

Annual appliances sales single serve (in mln units)

Senseo Tassimo Dolce Gusto Nespresso

Source: GfK, 2010, NL-B-F-D

26 mln Senseo Machines Being Used

Senseo installed base (in mln units, excl. US)

CY01 CY02 CY03 CY04 CY05 CY06 CY07 CY08 CY09 CY10 CY11

Source: Company data

Solid 4-Year Sales Growth

Retail sales growth Senseo (1)

FY08 FY09 FY10 FY11

| (1) |

Indexed FY 08 = 100, retail ales Source: Company data |

Solid Brand KPIs

Brand KPIs—The Netherlands

Awareness Consideration Current buyer Committed buyer

Consumers Value Senseo for its Simplicity and Convenience

Drivers of preference (% of consumers)

Simplicity

Convenience

Senseo

Other Looks

Passion Variety

Product

Simplicity Convenience

Nespresso

Dolce

Looks

Source: U&A Research NL 2009

Summary

• We are fortunate to play in the growth market

• We are solid but not fully participating in the growth

• Large user base

• Leadership position in single serve machines

• Positive brand imagery

• Strong market position, with potential to take back from PL

15

Insights For Future Growth

We Can Broaden our Purchase Appeal

Beyond Convenience

Main purchase driver (% of consumers)

Convenience (42%)

Looks (42%)

Product (28%)

Senseo

Dolce Gusto

Nespresso

Source: U&A Research NL 2009

We Have an Opportunity to Build Milk as a Consumption Partner

Share of milk in total cups consumed and Senseo sales (in %)

Germany France Netherlands Belgium

% cups consumed with milk

% Senseo sales with milk

Source: U&A survey program, Synovate 2009/2011

We Can Build Consumer Loyalty

Through Sampling

• Example: in Germany 50% increase in loyalty

Source: Company data

We Must Accelerate our Innovation Rate

2001

2011

Senseo Strategy: Creating the Future

Re-Launch The Senseo Brand Aggressively

• Institutionalize regular appliance innovation

• Strengthen brand through:

• Improved differentiation

• Segmentation

• Expansion to new countries

• Senseo as master brand for aM high-tech offers

22

Strengthen the Brand

• Upgrade taste quality and experience

• Introduce more varieties

• Premiumize offering

• Provide specific offers for defined consumer segments

• Focus investments behind innovations

Brick Pack: Brings Basic R&G into the 21st Century with Modernity, Style, Variety

L’OR: Makes Range More Competitive by Moving Upscale with Improved Variety

Senseo: Aesthetic Captures Brand Essence of Simplicity and Elegance

Senseo Base: Upgraded for Better Taste

While Retaining Simplicity

Senseo Black: Designed for More Sophisticated Tastes and Palates

Senseo Milk: Only 1 Pad Solution

Patented Technology

Sarista: Machine/Bean System is Ownable, Flexible, Accessible

Sarista Beans: Offer Freshness, High Quality and Convenience

R&D: Creating the Future

Jos Sluys

VP Research & Development

We Have Organized Ourselves for Growth

• 125 people with a passion for Coffee & Tea

• 12 nationalities

• Deliver innovations (90 people)

• Integrated in category business teams

• Resource deployment in line with business needs

• Project driven and results oriented

We Have Organized Ourselves for Growth

• Leading technology platforms (35 people)

• Exceptional technical and scientific expertise

• Entrepreneurial and external oriented

• Aggressive patent strategy

• Leverage innovations synergistically across categories

34

Way of Working

Flexible

Focused

Fast

Flexible by Working with the Best

Science partners

Global innovators

Integrated suppliers

Strategic alliances

? Build knowledge

? Explore new technologies Generate new innovations

? Reduce cost ?Fast implementation

? Route-to-market

Focus on Key Competences

Consumer science

Sensorial profiling (preference mapping)

Technology platforms

Liquid roast Appliances Aroma and taste Innovative packaging

We Have a Unique Liquid Roast Platform

Pure, liquid coffee concentrate

50 years of continuous development

High quality coffee, Barista standard

Difficult to replicate, delicate product, sensitive to degradation

Proprietary technology

Packing

Freezing

Roast & Ground

Extracting

Concentrating

Recent Breakthrough: Ambient Liquid

Roast

New aroma preservation technology Maintaining pure coffee character Product stable at ambient temperature

• Providing access to ambient distribution channels

• Enabling future innovations building upon high quality and versatility of the liquid format

Inventing the Future Senseo Sarista

Consumer insights:

• Aroma is key

• Fresh beans give the best coffee experience

• Varying consumer preferences

Current systems

• ln-cup quality suboptimal

• Cumbersome and expensive

Develop proprietary system that

maximizes freshness

Sarista Challenge:

Our inventions (1) Bean packs

• Clicked onto appliance

• Top quality beans

• Stored under nitrogen Precise measuring Cup-by-cup dosing

Maximum Freshness

41

Sarista Challenge: Maximum Freshness

Our inventions (2) Non-contamination grinder

• Cup-by-cup grinding

• Optimal grind size

• Full discharge of ground coffee

Sarista Challenge: Making it

Non-Refillable

• Bean pack recognition

• Countdown mechanism

• Dosing falls into disuse

Proprietary system further developed with our domestic appliance partner Philips

43

Delivering Coffee-Milk Solutions:

Senseo

Consumer insights:

• Perfect cappuccino and cafe latte at home

• Simple and easy to prepare

• Variation

No 1-step single serve solutions on the market Develop proprietary pads, technically solving:

• Low milk powder solubility and dissolving rate

• Clogging of systems due to coffee-milk interaction

_14

Design honeycomb-filter combination

Swirling motion inside pad at multiple, specific places

High dissolving rate, clogging avoided

Delivers high flexibility of innovations in flavored cappuccinos

Our Proprietary Solution: One-Step

Cappuccino

Fast to Market with Innovations

Conventional stage gating innovation process

Opportunity Concept

Prototype

Technical Supplier solution selection

mplementation

• Long time-to-market

• Risks and failures saved for last

Fast to Market with Innovations

Our approach

Get Inspired Go create

Make it happen

Twice as fast in market

• L’Or Espresso Lungo range (4 months)

• R&G new brick product range (6 months)

• New Senseo product range (Q3 12) (9 months)

Strong Number 2 Position in Coffee Patent Applications

First filings (2006—July 2010)

250 200 150 100 50

Comp 1

MASTER Comp 2 Comp 3 Comp 4 Comp 5

BLENDERS

Number of Patent applications increased 5-fold vs period 2002—July 2006

Source: Thomson Innovation

Unique Proprietary Technology

R&G

Superior taste profiles thru preference mapping

Senseo

Portioned espresso

Patented honeycomb pads Sarista (patents pending)

Patented capsules

Instant

Patented aroma and processing technologies

Liquid roast

Patented aroma, packing and dosing technologies

49

Operations: First Impressions

Luc Volatier SVP Supply Chain

Luc Volatier

| * |

Nationality French |

• Current Position

SVP Supply Chain (2012)

• Previous Experience GrandVision—3 yrs Numico—6 yrs

Upstream Purchasing Consulting—4 yrs Danone—9 yrs

Manufacturing Footprint

*2 process steps split over two locations and move to 1 in CY13

Coffee

RG Roast & Ground L Liquid I Instant

Tea

12 locations

Brazil

Thailand

Australia

A

Brazil SP 135

Netherlands Utrecht 55

Belgium 40

Poland_20_

France_20_

Netherlands Joure 20 7

Brazil Bahia 15

Spain 10

Hungary 10 3

Thailand 10

Australia <5

Greece <5

Good Fundamentals

• High competency in coffee and tea sourcing

• Solid manufacturing expertise and footprint

• Some re-alignment and optimization has been done

• Supply chain is well organized and ready for the challenge

54

Observations

• Very different asset utilization rates and efficiencies

• Available capacity in roasters and grinders to accommodate innovations

• Some bottlenecks in specific processing and packaging

• Majority of new investments will be innovation specific

• Weak link between Operations and the Business

Areas for Investigation

• Ways to increase speed to market

• Opportunities to take further costs out

• A plan to drive best practices across the organization

• Concrete actions to drastically reduce working capital

• A road map to develop an end-to-end holistic supply chain

Out Of Home: Living the Cafe Culture

Nick Snow COO Out of Home

Nationality British

Current Position

COO Out of Home (2006)

Previous Experience Johnson Diversey—4 yrs Unilever -15 yrs

Nick Snow

58

Coffee and Tea the Largest Beverage Category Within OOH

Other

Coffee

Juices

Soft Drinks

Tea

Water

Source: European Segment Research Foodstep, Share of OOH non-alcoholic beverage categories (in %, 2011, Europe)

OOH Represents 23% of the Global Coffee Market

77%

23%

The Market is Relatively Stable

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

CAGR +3%

Source: Euromonitor OOH volumes (mln kg)

Business & Institutions are the Largest European Customer Segments

Source: European Segment Research Foodstep, volume segment split, CY11

62

Leisure & other

Petrol stations

Fast food

BaReCa

Hotels & gaming

Education

Healthcare

Business

Our OOH Business

A Profitable Solid Business

Net sales 606 614 634

Growth vLY n/a 1.3% 3.4%

Adjusted EBIT 102 109 110

Adjusted EBIT margin 16.8% 17.7% 17.3%

We are Number Three in a Highly Fragmented European Market

Unbranded

Nestle

Kraft

Lavazza

Branded Others

Source: Company data, excluding coffee shops, market share Europe in % of volume

Our Portfolio Covers all Segments of the

Coffee Categor

Espresso

Instant

Liquid Roast

Liquid Roast

Filter

Espresso

Instant

Source: Master Blenders’ share of coffee categories in value

Liquid Roast is our Proprietary System

• High-quality coffee

• Concentrated

• Packed in ‘closed7 Bag-in-Box

• Deep frozen to preserve full flavour and aroma

• Ready to use pack = 400 servings

• Compatible only with our machines

67

It Provides Major Advantages Over Conventional Coffee Systems

• Low operating cost

• Consistent taste delivery

• Fast dosing, high volume

• No waste, limited cleaning

• Simple to operate

• Hygienically sealed

68

A Major Competitive Advantage for High Volume Customers

• Hotels

• Large business

• Hospitals

• Gaming

• Event parks

We Have Two

Direct

Consumer brand

Liquid roast & complete portfolio Direct selling & technical service Brand synergies with retail

Scale is profit driver

Strategic partner branded or DE branded

Supply liquid roast product and equipment

Bridge to future retail presence

Liquid roast

Distributor

The Direct Model is Most Important

Distributors

Note: ‘Distributors’ in this context means sales in countries where we only have distributors and no physical presence. We also sell through distributors where we have a direct business model

Source: Company data, sales split FY11

71

Direct

Distributors are More Profitable

Distributors

Note: ‘Distributors’ in this context means sales in countries where we only have distributors and no physical presence. We also sell through distributors where we have a direct business model

Source: Company data, EBIT split FY11

72

Direct

The Direct Business Model

Our Business is Highly Concentrated

Denmark

Other

Australi

Spain

Belgium

Germany

Netherlands

Source: Company data

The Netherlands: Our Success Model

• 45% market share

• 65,000 customers

• 124,000 coffee machines

• 1,100 employees

• 250 service engineers

• 450 operators

• 200 mln DE branded cups per year

Source: POS Research Foodstep, company data

Liquid Roast 50% of Coffee Sales

in the Netherlands

Instant

Source: Master Blenders’ share of coffee categories in value

Liquid Roast

Espresso

Roast & Ground

We Have a Unique Operating Model

We are market leaders

We Have a Unique Operating Model

Liquid roast is our unique competitive advantage

78

Liquid Roast

We Have a Unique Operating Model

We offer a full portfolio to cover all customer needs

Full

Portfolio

79

Technical Service to ensure good quality coffee

• Technical service (250 FTE)

Technical service

80

We Have a Unique Operating Model

Service organization to deep sell and provide value added services

Operating service (450 FTE)

Route sales(50 FTE)

Value-added services

81

Organization focused on the needs of OOH customers

Dedicated OOH Organization (350 FTE)

Customer

Support

We Have a Unique Operating Model

Long term customer satisfaction creates loyalty

High Customer Satisfaction & Retention

83

40% of Sales is from Value Added Services

Coffee & tea Accessories Equipment & Operation &

spares technical service

Source: Company data, indicative split of sales NL

84_

Strong OOH Company Supports Brand Awareness in the Netherlands

The Distributor Model

We Have Four Major Strategic Distributor Partners

Source: Company data

Our Distributor Model Serves

Three Goals

• Leverage liquid technology to drive profitability

• Create a network of strategic partners

• Create brand presence in countries where we do not have a retail brand

88

UCC our Strategic Partner in Japan

• Leading branded Coffee Company

| • |

€ 1 bn sales |

• Highly innovative coffee market

• We provide:

• Liquid roast ingredient & machines

• Sales & technical training

• Key account support

• Marketing assistance

Source: Company data, company website, Factiva, D&B,

89

Using Distributors for Brand Visibility -

Example Turkey

• Two distributor partners

• Non coffee roasters

• Complete portfolio

• Leader in 5 star hotels and resorts

• Building DE brand

90

Going Forward

Further Innovate our Liquid Roast Technology

• Upgrade our Liquid Roast quality to match espresso taste

• Further deploy ambient Liquid Roast to increase distribution and open new channels

92

Strengthen Quality Perception

• Upgrade equipment design and appearance existing park

• Innovate consumer interface

93

Use OOH Touch Points as Brand Building Tool

Brazil

Spain

94

Grow our Business Geographically

• Selectively drive scale in countries with retail presence

• Look for further distribution opportunities

95

France: The Growth Engine of W-Europe

Luc Van Gorp GM France

Luc Van Gorp

• Nationality Belgian

• Current Position GM France (2010)

• Previous Experience Sara Lee—9 yrs Campbell’s-4 yrs Diageo—3 yrs

| 2 |

Facts About France

63.1 mln citizens

27.2 mln households

2.3 persons per household 3.9 cups of coffee per day

Source: INSEE, Government of France, Liquid intake monitor

98

Third Largest Coffee Market in Europe

4,874

2,920

2,472

1,627

1,244

Germany Russia France Italy UK

Source: Euromonitor retail sales (fixed 2011 exchange rates), € mln

99

Room to Grow in Terms of Consumption

Daily cups per consumer

8.3

7.0

6.2

5.2

5.0

4.1

4.0

3.9

3.8

3.6

3.3

3.3

3.1

2.8

2.7

2.6

2.5

2.5

Source: Company analysis based on U&A, Euromonitor, ABIC and company estimates

100

A Growing Market

100

103

106

113

127

2007 2008 2009 2010 2011

Source: Nielsen 2011, Retail sales, € mln

101

Market Growth is Driven by Single Serve

Avg. Price / kg

% market

2011 vs 2006

Single Serve caps

€28.00

17%

+36%

Single Serve pads

€15.40

22%

+15%

Premium R&G

€10.80

46%

+1%

Mainstream R&G

€5.30

15%

+1%

Source: Nielsen, value share CY11

The French have a Distinctive

Coffee Culture

• 48% drink coffee black

• 37% drink coffee black with sugar

• Indulgence and energy are main consumption drivers

• 56% of Roast & Ground is consumed in the morning

• 63% of Single Serve is consumed in the afternoon

• 66% of households has both R&G and Single Serve appliance

103

A Highly Branded Market

Other

PL

Nestle

Kraft

MASTER

BLENDERS

Source: Nielsen retail value shares CY11

104

13%

21%

17%

12%

37%

France

MASTER

BLENDERS

Our Portfolio in 2009

Roast & Ground

Single Serve

Private label

Mainstream

Premium

Pads

106

Strategic Decision to Unlock French Market Growth Potential

• The 3 strategic pillars to take full advantage of the great French market opportunity :

• Premiumize Roast & Ground

• Significantly grow Single Serve

• Step up Senseo

• Create super premium portioned espresso in retail

• Improve our trade approach

107_

Premiumize Roast & Ground

• Exit Private Label manufacturing

• Stabilize our mainstream Maison du Cafe business

• Grow premium L’Or brand

L’Or Premium Business Growth

• Introduce innovations: L’Or Elixir

• Consistent advertising with strong ownable codes

• Qualitative in store promo to stimulate multiple L’Or purchases

109

L’Or In Store Activation

110

Impressive Results for L’Or R&G

FY09-FY11 Results

2% volume growth

12% sales growth

Record high market share of 14.3%

Source: Company data, Nielsen retail value share MAT Jan 2012

111

Significantly Step Up Senseo

Strategy:

• Aggressively build appliance-park penetration

• Extend portfolio

• Focus communication on indulgence & quality

112

Aggressively Build Appliance Penetration

• Limited editions

• Strong consumer activation

• Demo’s

• Tastings

• Consumer advertising

• Strong cooperation with Philips France

113

Christmas 2011 Limited Edition

Senseo

114

Sneak Preview: Limited Edition Mother’s Day 2012

115

Strong Results in Appliance Penetration

• Leading Single Serve appliance with 34% penetration

• 10% penetration increase in 2011

• Record high sales in 2011:1.2 mln appliances

• 9 mln appliances sold

since launch in 2002

34%

12%

9%

4%

116

Significant Portfolio Innovation

Launch FY10 FY10 FY11 FY11

Consumer Heavy Pure Premium Sustainable

need user loyalty indulgence Black range development

117

Key Advertising Messages

• Focus on “indulgence” and “trust”

• Not on “convenience”

• Build on appliance news

118

Impressive Results in Senseo Coffee Sales

FY09—FY11

18% volume growth

23% sales growth

Senseo already 30% of Single Serve category

Source: Company data, Nielsen retail value share, MAT Jan 2012

119

Create Retail Portioned Espresso Category

• Use strong L’Or equity as brand platform

• Super Premium price positioning

• >200% premium vs retail capsules

• Only 10% price discount vs Nespresso

• No trade promos / no price deals

• Swiftly extend portfolio

Successful Launch

• 95% distribution in four weeks

• 4% penetration after 6 months

• Brand awareness at 87% after 6 months

• Market share 10% of single serve

• “Best Innovation” 2010 Nielsen nomination

Source: Company data 2010, Kantar 2010, Nielsen MAT Jan 2012

121

Successful Portfolio Roll Out

October 2011:

Lungo and Strong

May 2011:

Premium range

February 2011:

Extension of base

April 2010:

Base Range

122

L’Or Espresso Shows Significant Constant Growth Since Launch

L’Or Espresso sales growth (indexed)

236

Apr 10-Aug 10 Sep 10-Feb 11 Mar 11—May 11 Junll-Octll Nov 11—Feb 12

236

206

177

147

100

Source: Company data

123

Excellent Point of Sale Execution

Improve Our Trade Approach

• Shopper marketing

• Category Captain for Single Serve in all customers

• Central and field sales people driven by value and margin

• Optimized price & promotion management

Results of Our Strategy

Reached Record Market Share Levels

CAGR+6%

21.2

20.0

18.8

19.1

18.5

2007 2008 2009 2010 2011

Source: Nielsen, Value Share CY11

Significantly Improved Volume Mix

k Tons

35.4 363 363 35.8

Premium Mainstream

FY07 FY08 FY09 FY10 FY11

Source: Company data base on GAAP

Premiumization Driving Growth

• Sales and margin improvement

• Achieved with a stable 9% A&P/Sales

296

247

231 233

Sales € mln 205

Premium Mainstream

FY07 FY08 FY09 FY10 FY11

Source: Company data, based on US GAAP

129

NL: A Multi-Tier Strategy in Action

Harm-Jan van Pelt Regional COO

Sm

Nationality Dutch

Current Position Regional COO

Previous Experience Sara Lee -13 yrs Henkel—9 yrs

Harm-Jan van Pelt

Facts About The Netherlands

16.7 mln citizens

7.5 mln households

2.2 persons per household

Source: CBS

Dutch Coffee and Tea Culture

4.5 cups of coffee per day

• 70% is in home consumption

• 40% of coffee drinks are pure black

• 47% with milk

• 40% of all coffee consumption is in the morning

• 3.1 cups of tea per day

• 80% is in home consumption

• 67% of consumers drink pure tea

• Important moments: breakfast 25%, afternoon 30%

Source: Liquid intake monitor

The Coffee Market is Diversified

includes all Single Serve except Espresso Capsules which are shown separately Source: Nielsen, value share, total coffee market incl. instants, total tea market, CY11

134

Instant

Espresso Capsules

Roast & Ground

Beans

Single Serve1

The Tea Market is Segmented

Source: Nielsen, value share, total coffee market incl. instants, total tea market, CY11

Well Being Tea

Black Tea

Pleasure Tea

Coffee is a Growing Market

FY07 FY08 FY09 FY10 FY11

Source: Nielsen, € mln

546

572

612

619

676

CAGR +5.5%

Tea is a Growing Market

104

109

119

CAGR+4:2%

125

123

FY07 FY08 FY09 FY10 FY11

Source: Nielsen, € mln

Our Business

Tea

Instant 1% 1%

Capsules ^% Beans

Senseo ‘

Roast & Ground

We are Present in all Segments

Roast & Senseo Beans Capsules Instant Tea

Ground

Source: Master Blenders’ share of categories in value, FY11, non-core category excluded 139

We Have a Very Strong Market

Position in Coffee

Private Labels

Other

Nestle

Source: Nielsen, FY11

We Have an Equally Strong Market

Private Labels

Other

Wessanen

Unilever

Source: Nielsen, FY11

Position in Tea

Flat Sales Development over Last Five Years

100 101 99 101

FY07 FY08 FY09 FY10 FY11

Sales The Netherlands (indexed)

Source: Company data, based on US GAAP

Company was Managed for Profit

• Lowered A&P spend

• Stopped investment behind Senseo

• No innovations or big introductions

• Limited in store and consumer activation

Market Shares have only Declined Slowly

Coffee

52.7%

51.3%

50.1%

48.6%

58.5%

Tea

55.0%

53.8%

52.9%

FY08 FY09 FY10 FY11 FY08 FY09 FY10 FY11

Source: Nielsen, value share, total coffee market incl. instant, total tea market

Why We Still Have a 50% Market Share

• Strong Brands

• High Loyalty

• Social Connectivity

Douwe Egberts is the Fourth Strongest

Brand in the Netherlands

Brand Asset™ Valuator 2011

1. Google

2. IKEA

3. Coca-Cola

^4. Douwe Egberts _

5. Eftellng

6. Albert Heijn

7. Marktplaats,nl

8. Philips

9. Bol.com

| 10. |

Microsoft |

Douwe Egberts is the Third Most Sold Brand in Retail

*1 Campina

*2

Marlboro

*3 Douwe Egberts

*4

Coca-Cola

*5

Heineken

#27 Nescafe

#43 Pickwick

Source: GfK, supermarket sales in the Netherlands € mln

147

We Have a Strong Savings Program that Has Driven Loyalty Since 1924

• Loyalty points on all DE and Pickwick products

• 65% of Dutch households collect our loyalty points

• Points can be reimbursed for coffee & tea related products

148

Consumers Visit our Shops to Collect Gifts

75% of all points redeemed

People collect their gifts at our 13 stores

Result: 550,000 qualitative consumer contacts per year

Website www.de.nl takes 11% of total gifts

149

Our Consumers are Very Loyal

150

Loyalty %

51

56

46

23

31

32

Coca Cola

Pepsi

Heineken

Grolsch

Source: GfK

Participation is a Cornerstone of

Douwe Egberts

• Douwe Egberts Neighbors’ day connects communities

• Brings people together to activate their neighborhood

• 1.3 mln participants

• Sales up 6% vs last year

• Sponsorship at large events

• 150,000 youngsters

• 300,000 cups of coffee sold

23

2011 Changing Course

Strategic Decision to Bring Back Growth

• Change Culture

• Focus on value added offerings and innovation

• Premiumization

• Increase marketing support

25

Major Turnaround in Culture

• Full replacement of Dutch leadership team

• Inject sense of urgency, accountability and entrepreneurship in the team

• Focus on profitable growth and market share

Innovate Tea: Introduced Spices Segment

• Developed a new premium tea segment

with a surprising taste • Launch date: October 2011

Results:

• Total market share 9.3% for new Pickwick segment

• 2.9% market share new variants only

Source: Nielsen, week 4 CY12

Launched Dutch Blend

• Premium Black Tea, co-created with consumers

• Launch date: October 2010 Results:

• Black tea segment +4.1% m.s.

• Total tea market +1.3% m.s.

Source: Nielsen, week 4 CY12

Coffee: Launched Portioned Espresso

New retail segment

• Launch date: April 2011 Results:

• Awareness 77%

• Market share 5.5% in Single Serve segment in one year

Source: Nielsen, week 4 CY12

100% ARABICA

10

CAPSULES

Introduced a New Senseo Fresh Milk-Based Machine

New Senseo innovation with fresh milk compartment in machine to make cappuccino

• Launch date: November 2011

Results:

• Total machine sales December 2011 + 50% vs. 2010

158

Source: Company data

Premiumized Coffee: Douwe Egberts Beans

• Beans is the fastest growing segment: +54% vs LY

• Premium Douwe Egberts beans, specially selected for the true coffee connoisseur

• +20% cons, price difference

• Activation date: December 2011

Source: Nielsen and Company data

159

Strengthened Category Leadership

• Introduced shopper marketing into the company

• We increased category leadership in the 4 main retailers

• To work jointly in driving category growth

160

Rejuvenate DE Cafe’s

• 25 DE cafe’s

• Use cafe’s to activate innovations

• Restyle in line with new brand image

• Rollout in mainstream areas

Acquired

• 35 cafe’s

• Connect with early coffee adopters

• Use as laboratory for new coffee experiences

• Leverage knowledge base for new innovations and customer insights

Company

Coffee

Initial Signs of Recovery

Coffee

Tea

FY08 FY09 FY10 FY11 FY12 FY12 FY08 FY09 FY10 FY11 FY12 FY12

Ql Q2 Ql Q2

Source:Nielsen, value share, total coffee market incl. instant, total tea market

52.7%

51.3% _ 50.1%

48.6% 48.6% 48.8%

58.5%

55.0% 53% 5290/o 53.3%

2012: The Year of Acceleration

Our Strategic Objectives

• Become the launch platform for all product innovations

• Become the preferred supplier for 100% of the trade

• Utilize our unique loyalty system to create a one-on-one relationship with our consumers

• Use the coffee cafe’s as an innovation laboratory

39

March April Sept Oct

2012 2012 2012 2012

Brazil: Focus on Profitable Growth

Dantes Hurtado GM Brazil

Dantes Hurtado

| * |

Nationality Brazilian |

Current Position GM Brazil (2003)

Previous Experience Best Foods—2 yrs Philip Morris—3 yrs Unilever—24 yrs

Brazil is Five Countries in One

North Pop.: 16 mln $6,960/capita,

West Pop.: 14 mln $13,910/capita

Northeast Pop.: 78 mln $6,690/capita

SP AND RIO * Pop.: 58 mln $16,150/capita

! South Pop.: 28 mln $12,460/ca pita

4,400 km

Source: IBGE 2010 Census and Company Estimates

Sao Paulo and Rio are 44% of the Economy

North

Northeast

SP&Rio

South

Source: IBGE 2010 Census and Company Estimates

West

The Brazilian Coffee Market

USA Germany Brazil Japan Russia France

Brazil is the Third Largest Coffee Market

$bn

9.1

6.9

6.6

5.4

4.1

3.5

Source: Euromonitor 2011

Growing Steadily

Coffee Consumption (billions of cups)

98

165

236

CAGR+3.6%

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Source: ABIC 2011

With Potential for Further Growth

Daily cups per consumer

Source: Company analysis based on U&A, Euromonitor, ABIC and company estimates

8.3

7.0

6.2

“ 5.0

4.5

? 4.1 4.0

3.8 3.6

Li 3.3. 3.1

2.8 2.7 2.6 2.5 2.5

Coffee is Part of our Daily Routine

• 95% of people drink coffee

• Children drink coffee with milk from the age of 3

• 40% of total coffee is consumed during breakfast

• 50% with milk

• 91% with sugar

Source: U&A study

We Drink Mainly Roast and Ground

Instant Beans

Single Serve

Roast & Ground

Source: Nielsen 2011, retail sales value

Roast and Ground is Premiumizing

Premium 6.70 11% +22%

Mainstream 5.20 83% +1%

Economy 4.40 6% (33)%

Source: Nielsen 2011, R&G coffee value share

Four Large Players and Many Locals

Other

(1,200 players)

Source: Nielsen 2011, Retail value share

Leaders are Geographically Focussed

Source: Nielsen 2011, total coffee value share

SP and Rio South and SP Northeast and

Metro Inland Others

(46%) 21% 9%

20% 7% 28%)

12% (19%) 2%

4% 10% 5%

Brazil

MASTER

BLENDERS

Our Brand Portfolio

Source: Company data

182

Do Ponto Others

Caboclo

Damasco

Moka

Pilao

Pilao is the Biggest Coffee Brand in Brazil

• The strong coffee of Brazil1

15% national share (40% in SP and Rio)

55% top of mind

47% loyalty

10% premium price

PIIAO

O Cafe Forte

Caboclo: Tradition and Heritage

• The country flavor in your home’

• 5th largest brand

• 7-8% in Sao Paulo and South

• Since 1930

Damasco: A Valuable Acquisition

• Acquired November 2010

• To strengthen the presence in the South

• Leader in Parana state (40% of the South)

• 10% premium price

• OOH presence

Presence Across Regions and Segments

SP and Rio SP Inland and Northeast and

Metro South Other

Premium

Mainstream

Economy

State of the Art Factory in Jundiai

• Operating since 2006

• One of the largest coffee factories in the world

• 135,000 tons/year

• High technology equipment

• ISO 14.000 certified

• Process will be carbon neutral as of Apr’12

100

110

126

127

135

Organic: +4%

With acquisitions: +8%

Our Sales are Growing

FY07 FY08 FY09 FY10 FY11

Source: Company data, in BRL, indexed, based on US GAAP

Our Mainstream is Growing

Net Sales

Premium

Mainstream

Economy

FY07 FY08 FY09 FY10 FY11

31% 27% 28% 27% 24%

Note: Acquisitions excluded

Source: Company data, in BRL, based on US GAAP

65%

69%

69%

70%

74%

Our Strategy

Focus growth on Sao Paulo and Rio Metro Maintain position in the rest of the country

Sao Paulo and Rio Metro are the Most Affluent Areas

• Highest income region

• Population 32 mln, with 40% AB class

• Higher prices than average (111 Rio, 102 SP)

• Pilao grew 2x faster than the market over the last 3 years

191

• 50% of our sales

• Higher margins

Sao Paulo and Rio Metro are Important and Profitable for us

SP and Rio SP Inland Northeast

Metro and South and Others

GP index 100 88 65

Strategy for Sao Paulo and Rio Metro

• Fortify the Economy range

• Launch value added propositions and premiumize

• Innovate, starting with Senseo

• Extend presence in Out of Home

• Take trade to the next level

Fortify the Economy Range

• Position range correctly against price competition

• Rebuild distribution

• Get fair share of shelf space

Started Launching Value Added Line

Extensions

Mild and more aromatic Ideal for the summer season Launched October 2009

Intense and extra-dark Strengthens brand positioning ‘The strong coffee of Brazil’ Launched March 2010

Innovation: SP and Rio, the Perfect Region for Senseo

• Single Serve starting to emerge

• Nespresso and Dolce Gusto already launched

• 4.4 mln high income households (Sao Paulo and Rio metro)

• Smaller (3.3 persons/HH) family size seeking convenience

196

Senseo: Full Roll-Out in 2013

Encouraging market test results

• 62,000 machines during test period

• 56% “definitely buy” intention

• High output per machine

• Capturing critical breakfast consumption

• Price/cup 9x higher than regular coffee

Extend Presence in OOH

• Three pillars:

• Liquid roast

• Espresso operating servic

• Branding

• Drinking experience

• Selective M&A

Liquid Roast as our Entry Point

• Pilao Cafitesse in leading hotels

CAFITESSE’

I

FASANO

S O F I T E L_

luxury hotels CuarujA Jequitimar

O Sol Mel id

HOTELS & RESORTS

HOTELS & RESORTS

ES rANPJ .AZA

HOEtllfilmm AlITi Br killtil*.

ATLANTIC A

HOTFLS I NTFR NATIONAL

NOVOTEL

GOLDEN TULIP

HOTfLS . SUITES ? RESOHTL

199

Building Pilao Presence in Padarias

• Espresso in 156 padarias

Building Pilao Presence in Coffee Shops

• 91 coffee shops

Taking Trade Management to the Next Level

• From ‘category captain” to ‘shopper marketing expert7 at WalMart, Carrefour and Casino

• Leverage our Cash & Carry position to expand national distribution

• Perfect store program

‘A Perfect Store’

Like France in 2000

We are.

• refreshing and premiumizing our R&G base

• launching Senseo

• building strong trade partnerships

. while developing an OOH presence

Australia: An Instant Success Story

Lara Brans GM Australia

Nationality Dutch

Current Position GM Australia (2007)

Previous Experience Sara Lee -10 yrs VODW Marketing—6 yrs

206

Lara Brans

Our Instant Success Story ‘Down Under’

• Coffee market

• Our business & brands

• Growth strategy

• Our results

Facts About Australia

22.8 mln citizens

8.6 mln households

2.6 persons per household

Moderate Coffee Consumption

Daily cups per consumer

Source: Company analysis based on U&A, Euromonitor, ABIC and company estimates

Mainly an Instant Coffee Market

Source: Aztec Scan Data 2011

210

81%

19%

A Unique Coffee Culture

• In home:

• 55% of coffee consumption is in the morning

• 83% drink coffee with milk and 67% with sugar

Source: Company data

A Unique Coffee Culture

• Out of Home:

• Emerging boutique coffee cafe’s

A Growing Coffee Market

2005 2006 2007 2008 2009 2010 2011

Source: Aztec Scan Data Jan 2012, AUD mln

573

652

693

767

835

835

868

CAGR~

A Concentrated Branded Market

Source: Aztec Scan Data Jan 2012, Value Shares

Cantarella Group

Nestle

Other

PL

The Instant Market is Premiumizing

Avg. CAGR

% market

Price/cup 2002—2011

Single serve mixes $ 0.37 25% +24.8%

Premium $0.16 35% +11.7%

Mainstream $0.10 34% (0.3)%

Economy $0.06 6% (6.3)%

Source: Aztec Scan Data Jan 2012, AUD

Australia

MASTER

BLENDERS

Harris: our Mainstream R&G Brand

from Down Under

• 12% of sales

• 17% market share R&G

• Australian heritage

• Locally roasted

• Over 128 years old

Source: Company data, Aztec Scan Data Jan 2012

Moccona: the Premium Instant Brand

from Europe

• 88% of sales

• 29% instant market share

• European heritage

• Iconic jar

• 10% price premium

• Imported from NL

• High loyalty 52%

Source: Aztec Scan Data Jan 2012, Company data

218

We were a Small Player 11 Years ago

• Nescafe market leader

• Little differentiation and variety in market

• Mainly lower quality coffees

• Moccona offered two qualities: mainstream and premium

Source: Aztec Scan Data Jan 2012, Moccona value share of the instant market CY99

Our Growth Strategy: Drive Value and Increase Margins

• Premiumization

• Focus on better quality coffee

• Value growth

• Margin focus

• Trading consumers up in $/cup

We Extended and Premiumized

our Portfolio

Base range

“Every Day Classic”

AUD 14 cts/cup 3 variants

We Extended and Premiumized

our Portfolio

Base Inspirations

range range

AUD 14 cts/cup AUD 15 cts/cup 3 variants 3 variants

“Every Day Classic”

“Escape”

We Extended and Premiumized

our Portfolio

Base Inspirations Gourmet

range range range

AUD 14 cts/cup AUD 15 cts/cup AUD 21 cts/cup 3 variants 3 variants 3 variants

“Every Day Classic”

“Escape”

“Indulgence”

We Extended and Premiumized

our Portfolio

Base Inspirations Gourmet Mixes

range range range range

AUD 14 cts/cup AUD 15 cts/cup AUD 21 cts/cup AUD 51 cts/cup 3 variants 3 variants 3 variants 11 variants

“Every Day Classic”

“Escape”

“Indulgence”

“Your Moment”

We Built Strong Trade Relationships

• Effective pricing & promotional management

• Thorough promotional analysis

• Established partnerships with top 3 customers, driving growth via joint customer plans

coles

Woolworths

We Claimed Category Captain Position

• Credible coffee experts across all segments

Leverage on premium brand positioning

Extensive shopper insights translated into shelf navigation tools and displays

226

We Build Very Consistent Brand Positioning

• 1989: Rolls

• 2009: Cinderella

• 2012: Key

Our Results

Double-Digit Top-line Growth with Consistent High Margins

FY06 FY07 FY08 FY09 FY10 FY11

Source: Company data, indexed sales, based on US GAAP

100

116

124

147

160

171

CAGK ,__+11.3%^

Growth Through Premiumization

100

116

124

147

160

171

Premium

Mainstream

FY06 FY07 FY08 FY09 FY10 FY11

Source: Company data, indexed sales, based on US GAAP

Strong Market Share Development

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: Aztec Scan Data Jan 2012, value shares

13%”

23%

The Way Forward

Keep Momentum Going

• Keep leadership in premium instant

• Continue to add local & global innovations

• Continue to claim category captainship as coffee expert

Extend Premiumization into R&G

Extend into upper premium R&G

• Launch of our OOH Piazza d’Oro cafe brand into Retail

Leverage OOH & Retail

SERVED IN ALL GOOD CAFES.

AND NOW IN ALL GOOD HOMES

Notes

Notes

Notes

Notes