EXHIBIT 99.1

EMPIRE STATE REALTY TRUST ANNOUNCES FOURTH QUARTER 2015 RESULTS

- Reports Core FFO of $0.25 Per Fully Diluted Share -

New York, New York, February 22, 2016 - Empire State Realty Trust, Inc. (NYSE: ESRT) (the “Company”), a real estate investment trust with office and retail properties in Manhattan and the greater New York metropolitan area, today reported its operational and financial results for the fourth quarter of 2015.

“We are pleased with our strong fourth quarter and full year 2015 results, including a 9% increase in full year Core FFO per share, which reflect the successful execution of our strategy to consolidate, redevelop and re-lease space to larger, higher credit quality tenants. During 2015, we leased approximately 1.2 million square feet of office and retail space, which represents 54% growth from the prior year. Most importantly, our leasing team achieved rent spreads in excess of 73.5% on the total portfolio and over 43% on new leases signed in our Manhattan office portfolio. Additionally, we overcame challenging New York City tourist trends and the opening of One World Trade Center’s observatory and produced full year revenue from our Observatory that was slightly in excess of the prior year,” stated John B. Kessler, Empire State Realty Trust’s President and Chief Operating Officer.

Mr. Kessler continued, “Finally, our well-capitalized, low-levered balance sheet, with limited near term debt maturities, enables us to support our future growth plans. In the coming years, we will continue to unlock the embedded, de-risked growth within our portfolio and create long term value for our shareholders, with whom our management team remains highly aligned. We had limited new net borrowings during the year and continue to maintain high levels of liquidity.”

Fourth Quarter Highlights

| • | Achieved Core Funds From Operations (“Core FFO”) of $0.25 per fully diluted share and net income attributable to the Company of $0.07 per fully diluted share. |

| • | Total portfolio was 87.3% occupied; including signed leases not commenced (“SLNC”), the total portfolio was 89.1% leased at December 31, 2015. |

1

| • | Manhattan office portfolio (excluding the retail component of these properties) was 84.9% occupied; including SLNC, the Manhattan office portfolio was 87.2% leased at December 31, 2015. |

| • | Retail portfolio was 94.3% occupied; including SLNC, the retail portfolio was 94.6% leased at December 31, 2015. |

| • | Empire State Building was 86.7% occupied; including SLNC, the Empire State Building was 90.7% leased at December 31, 2015. |

| • | Executed 39 leases, representing 198,216 rentable square feet across the total portfolio, achieving a 34.0% increase in mark-to-market rent over previous fully escalated rents on new, renewal, and expansion leases. |

| • | Signed 23 new leases representing 111,307 rentable square feet in the fourth quarter 2015 for the Manhattan office portfolio (excluding the retail component of these properties), achieving an increase of 57.5% in mark-to-market rent over previous fully escalated rents. |

| • | The Empire State Building Observatory revenue for the fourth quarter 2015 was $27.6 million. |

| • | Declared a dividend in the amount of $0.085 per share for the fourth quarter 2015, which was paid on December 31, 2015. |

Full Year Highlights

| • | Achieved Core FFO of $0.97 per fully diluted share and net income attributable to the Company of $0.29 per fully diluted share. |

| • | Executed 245 leases, representing 1,209,145 rentable square feet across the total portfolio, achieving a 73.7% increase in mark-to-market rent over previously fully escalated rents on new, renewal, and expansion leases; 177 of these leases, representing 958,704 rentable square feet, were within the Manhattan office portfolio (excluding the retail component of these properties) capturing a 43.3% increase in mark-to-market rent over previously fully escalated rents on new, renewal and expansion leases. |

| • | Executed 12 leases, representing 70,940 rentable square feet within the Manhattan retail portfolio, achieving a 474.1% increase in mark-to-market rent over previously fully escalated rents on new, renewal, and expansion leases. |

| • | Signed 93 new leases representing 728,264 rentable square feet in 2015 for the Manhattan office portfolio (excluding the retail component of these properties), achieving an increase of 53.8% in mark-to-market rent over expired previously fully escalated rents. |

2

| • | The Empire State Building Observatory revenue grew 0.6% to $112.2 million from $111.5 million in 2014. |

| • | Declared and paid aggregate dividends of $0.34 per share during 2015. |

Financial Results for the Fourth Quarter 2015

Core FFO was $66.2 million, or $0.25 per fully diluted share, compared to $65.2 million, or $0.25 per fully diluted share, in the fourth quarter of 2014.

Modified FFO was $66.2 million, or $0.25 per fully diluted share, compared to $61.4 million, or $0.23 per fully diluted share, in the fourth quarter of 2014.

FFO was $64.2 million, or $0.24 per fully diluted share, compared to $59.4 million, or $0.22 per fully diluted share, in the fourth quarter of 2014.

Net income attributable to common stockholders was $8.3 million, or $0.07 per fully diluted share, compared to $4.1 million, or $0.04 per fully diluted share, in the fourth quarter of 2014.

Financial Results for the Year Ended December 31, 2015

Core FFO was $257.7 million, or $0.97 per fully diluted share, compared to $227.4 million, or $0.89 per fully diluted share, for the year ended December 31, 2014.

Modified FFO was $257.8 million, or $0.97 per fully diluted share, compared to $219.5 million, or $0.86 per fully diluted share, for the year ended December 31, 2014.

FFO was $249.9 million, or $0.94 per fully diluted share, compared to $214.8 million, or $0.84 per fully diluted share, for the year ended December 31, 2014.

Net income attributable to common stockholders was $33.7 million, or $0.29 per fully diluted share, compared to $26.7 million, or $0.27 per fully diluted share, for the year ended December 31, 2014.

3

Portfolio Operations

As of December 31, 2015, the Company’s total portfolio contained 10.1 million rentable square feet of office and retail space and was 87.3% occupied. Percentage occupied was down 10 basis points from 87.4% at the end of the third quarter 2015, and down 130 basis points from 88.6% at the end of the fourth quarter 2014 as we continue to execute on our redevelopment plan. Including SLNC, the Company’s portfolio was 89.1% leased at December 31, 2015.

The Company’s office portfolio (excluding the retail component of these properties), containing 9.3 million rentable square feet, was 86.7% occupied at the end of the fourth quarter 2015, down 30 basis points from the end of the third quarter 2015, and down 150 basis points from the end of the fourth quarter 2014. Including SLNC, the Company’s office portfolio (excluding the retail component of these properties) was 88.6% leased at December 31, 2015.

The Manhattan office portfolio (excluding the retail component of these properties), containing 7.5 million rentable square feet was 84.9% occupied at the end of the fourth quarter 2015, down 50 basis points from the end of the third quarter 2015, and down 260 basis points from the end of the fourth quarter 2014. Including SLNC, the Company’s Manhattan office portfolio (excluding the retail component of these properties) was 87.2% leased at December 31, 2015.

The Company’s retail portfolio, containing approximately 723,000 rentable square feet, was 94.3% occupied at the end of the fourth quarter 2015, up 160 basis points from the end of the third quarter 2015, and up 110 basis points from the end of the fourth quarter 2014. Including SLNC, the Company’s retail portfolio was 94.6% leased at December 31, 2015.

Leasing

For the three months ended December 31, 2015, the Company executed 39 office leases within the total portfolio, comprising 198,216 rentable square feet.

4

On a blended basis, the 39 new, renewal and expansion office leases signed within the total portfolio during the quarter had an average starting rental rate of $50.60 per rentable square foot, representing an increase of 34.0% over the prior in-place rent on a fully escalated basis.

Leases signed in the Fourth Quarter 2015 for the Manhattan office portfolio

| • | 23 new leases comprising 111,307 rentable square feet, with an average starting rental rate of $61.44 per rentable square foot, representing an increase of 57.5% over the prior in-place rent on a fully escalated basis, and |

| • | 13 renewal leases, comprising 62,862 rentable square feet, with an average starting rental rate of $41.84 per rentable square foot, representing an increase of 1.8% over the prior in-place rent on a fully escalated basis. |

Empire State Building

The Company continues to renovate and lease the 2.8 million rentable square foot Empire State Building, its flagship property. At December 31, 2015, the Empire State Building was 86.7% occupied; including SLNC, the Empire State Building was 90.7% leased.

During the fourth quarter 2015, the Company executed seven office leases at the Empire State Building, representing 27,235 rentable square feet in the aggregate.

The Observatory revenue for the fourth quarter 2015 was $27.6 million, compared to $28.2 million in the fourth quarter 2014. The Observatory hosted approximately 949,000 visitors in the fourth quarter 2015 compared to 997,000 visitors in the fourth quarter 2014. In the critical week between Christmas Eve and New Year’s Eve, there were three bad weather days in 2015 compared to one bad weather day in 2014. In the fourth quarter 2015, there was one bad weather day which fell on a weekend. This compares to the fourth quarter 2014, in which there were four bad weather days which fell on weekends.

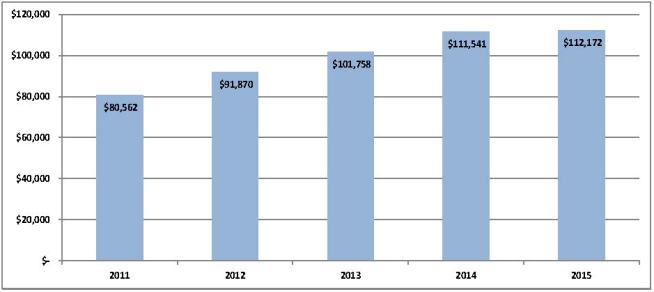

For the year ended December 31, 2015, the Observatory hosted 4.1 million visitors, compared to 4.3 million visitors for the same period in 2014. Observatory revenue for the year ended December 31, 2015 was $112.2 million, a 0.6% increase from $111.5 million for the year ended December 31, 2014. Both full year 2015 and 2014 had 15 bad weather weekend days.

5

Balance Sheet

As of December 31, 2015, the outstanding balance on the Company’s $800.0 million unsecured revolving credit facility was $40.0 million. The unsecured revolving credit facility has an accordion feature allowing for an increase in its maximum aggregate principal balance to $1.25 billion under certain circumstances.

At December 31, 2015, the Company had total debt outstanding of approximately $1.6 billion, with a weighted average interest rate of 4.12% per annum, and a weighted average term to maturity of 5.4 years. At December 31, 2015, the Company had no debt maturing during 2016. The Company’s consolidated debt to total market capitalization was approximately 25% as of December 31, 2015 and consolidated net debt to EBITDA was 4.9x.

Dividend

On December 31, 2015, the Company paid a dividend of $0.085 per share for the fourth quarter 2015 to holders of the Company’s Class A common stock and Class B common stock and to holders of the operating partnership’s Series ES, Series 250 and Series 60 operating partnership units (NYSE Arca: ESBA, FISK and OGCP, respectively) and Series PR operating partnership units. The Company paid a dividend of $0.15 per unit for the fourth quarter 2015 to holders of the operating partnership’s private perpetual preferred units.

Webcast and Conference Call Details

Empire State Realty Trust, Inc. will host a webcast and conference call, open to the general public, on Tuesday, February 23, 2016 at 8:30 am Eastern time.

The webcast will be available in the Investors section of the Company’s website at www.empirestaterealtytrust.com. To listen to a live broadcast, go to the site at least five minutes prior to the scheduled start time in order to register, download and install any necessary audio software. Shortly after the call, a replay of the webcast will be available for 90 days on the Company’s website.

6

The conference call can be accessed by dialing 1-877-407-3982 for domestic callers or 1-201-493-6780 for international callers. A replay will be available shortly after the call and can be accessed by dialing 1-877-870-5176 for domestic callers or 1-858-384-5517 for international callers. The passcode for the replay is 13628305. A replay of the conference call will be available until March 1, 2016.

The Supplemental Report will be available prior to the conference call in the Investors section of the Company’s website, www.empirestaterealtytrust.com.

About Empire State Realty Trust

Empire State Realty Trust, Inc. (NYSE: ESRT), a leading real estate investment trust (REIT), owns, manages, operates, acquires and repositions office and retail properties in Manhattan and the greater New York metropolitan area, including the Empire State Building, the world’s most famous building. Headquartered in New York, New York, the Company’s office and retail portfolio covers 10.1 million rentable square feet, as of December 31, 2015, consisting of 9.3 million rentable square feet in 14 office properties, including nine in Manhattan, three in Fairfield County, Connecticut and two in Westchester County, New York; and approximately 723,000 rentable square feet in the retail portfolio.

Non-GAAP Financial Measures

The Company has used non-GAAP financial measures in this press release. A reconciliation of each non-GAAP financial measure and the comparable GAAP financial measure can be found on pages 11 and 12 of this release and in the Company’s supplemental report.

Forward-Looking Statements

This press release includes “forward looking statements” within the meaning of the federal securities laws. Forward-looking statements may be identified by the use of words such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “approximately,” “intends,” “plans,” “pro forma,” “estimates,” “contemplates,” “aims,” “continues,” “would” or “anticipates” or the negative of these words and phrases or similar words

7

or phrases. The following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements: changes in our industry, the real estate markets, either nationally or in Manhattan or the greater New York metropolitan area; resolution of the litigations and arbitration involving the company; reduced demand for office or retail space; general volatility of the capital and credit markets and the market price of our Class A common stock and our publicly-traded OP Units; changes in technology and market competition, which affect utilization of our broadcast or other facilities; changes in domestic or international tourism, including geopolitical events and currency exchange rates; defaults on, early terminations of, or non-renewal of leases by tenants; fluctuations in interest rates; declining real estate valuations and impairment charges; our failure to obtain necessary outside financing, including our unsecured revolving credit facility; decreased rental rates or increased vacancy rates; our failure to redevelop and reposition properties successfully or on the anticipated timeline or at the anticipated costs; difficulties in identifying properties to acquire and completing acquisitions; risks of real estate development (including our Metro Tower development site), including the cost of construction delays and cost overruns; and conflicts of interest affecting any of our senior management team.

While forward-looking statements reflect the Company’s good faith beliefs, they are not guarantees of future performance. The Company disclaims any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors, or new information, data or methods, future events or other changes after the date of this press release, except as required by applicable law. For a further discussion of these and other factors that could impact the Company’s future results, performance or transactions, see the section entitled “Risk Factors” in the Annual Report on Form 10-K for the year ended December 31, 2014, and other risks described in documents subsequently filed by the Company from time to time with the Securities and Exchange Commission. Prospective investors should not place undue reliance on any forward-looking statements, which are based only on information currently available to the Company (or to third parties making the forward-looking statements).

Contact:

Investors

Empire State Realty Trust Investor Relations

(212) 850-2678

IR@empirestaterealtytrust.com

Media

Brandy Bergman/Hugh Burns

8

Sard Verbinnen & Co.

(212) 687-8080

Empire State Realty Trust, Inc.

Condensed Consolidated Statements of Income

(unaudited and amounts in thousands, except per share data)

| Three Months Ended December 31, | ||||||||

| 2015 | 2014 | |||||||

| Revenues |

||||||||

| Rental revenue |

$ | 113,957 | $ | 112,259 | ||||

| Tenant expense reimbursement |

19,638 | 18,160 | ||||||

| Observatory revenue |

27,647 | 28,167 | ||||||

| Construction revenue |

— | 4,918 | ||||||

| Third-party management and other fees |

475 | 451 | ||||||

| Other revenue and fees |

3,483 | 6,456 | ||||||

|

|

|

|

|

|||||

| Total revenues |

165,200 | 170,411 | ||||||

| Operating expenses |

||||||||

| Property operating expenses |

38,918 | 41,748 | ||||||

| Ground rent expenses |

2,332 | 2,375 | ||||||

| Marketing, general and administrative expenses |

9,678 | 9,251 | ||||||

| Observatory expenses |

8,162 | 7,831 | ||||||

| Construction expenses |

— | 5,423 | ||||||

| Real estate taxes |

23,622 | 23,702 | ||||||

| Depreciation and amortization |

45,258 | 48,799 | ||||||

|

|

|

|

|

|||||

| Total operating expenses |

127,970 | 139,129 | ||||||

|

|

|

|

|

|||||

| Total operating income |

37,230 | 31,282 | ||||||

| Interest expense |

(17,194 | ) | (19,816 | ) | ||||

|

|

|

|

|

|||||

| Income before income taxes |

20,036 | 11,466 | ||||||

| Income tax expense |

(666 | ) | (502 | ) | ||||

|

|

|

|

|

|||||

| Net income |

19,370 | 10,964 | ||||||

| Preferred unit distributions |

(234 | ) | (235 | ) | ||||

| Net income attributable to non-controlling interests |

(10,884 | ) | (6,587 | ) | ||||

|

|

|

|

|

|||||

| Net income attributable to common stockholders |

$ | 8,252 | $ | 4,142 | ||||

|

|

|

|

|

|||||

| Total weighted average shares |

||||||||

| Basic |

118,706 | 103,022 | ||||||

|

|

|

|

|

|||||

| Diluted |

266,048 | 265,779 | ||||||

|

|

|

|

|

|||||

| Net income per share attributable to common stockholders |

||||||||

| Basic |

$ | 0.07 | $ | 0.04 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.07 | $ | 0.04 | ||||

|

|

|

|

|

|||||

9

Empire State Realty Trust, Inc.

Condensed Consolidated Statements of Income

(unaudited and amounts in thousands, except per share data)

| Year Ended December 31, | ||||||||

| 2015 | 2014 | |||||||

| Revenues |

||||||||

| Rental revenue |

$ | 447,784 | $ | 400,825 | ||||

| Tenant expense reimbursement |

79,516 | 67,651 | ||||||

| Observatory revenue |

112,172 | 111,541 | ||||||

| Construction revenue |

1,981 | 38,648 | ||||||

| Third-party management and other fees |

2,133 | 2,376 | ||||||

| Other revenue and fees |

14,048 | 14,285 | ||||||

|

|

|

|

|

|||||

| Total revenues |

657,634 | 635,326 | ||||||

| Operating expenses |

||||||||

| Property operating expenses |

160,969 | 151,048 | ||||||

| Ground rent expenses |

9,326 | 5,339 | ||||||

| Marketing, general and administrative expenses |

38,073 | 39,037 | ||||||

| Observatory expenses |

29,843 | 29,041 | ||||||

| Construction expenses |

3,222 | 38,596 | ||||||

| Real estate taxes |

93,165 | 82,131 | ||||||

| Acquisition expenses |

193 | 3,382 | ||||||

| Depreciation and amortization |

171,474 | 145,431 | ||||||

|

|

|

|

|

|||||

| Total operating expenses |

506,265 | 494,005 | ||||||

|

|

|

|

|

|||||

| Total operating income |

151,369 | 141,321 | ||||||

| Interest expense |

(67,492 | ) | (66,456 | ) | ||||

|

|

|

|

|

|||||

| Income before income taxes |

83,877 | 74,865 | ||||||

| Income tax expense |

(3,949 | ) | (4,655 | ) | ||||

|

|

|

|

|

|||||

| Net income |

79,928 | 70,210 | ||||||

| Preferred unit distributions |

(936 | ) | (476 | ) | ||||

| Net income attributable to non-controlling interests |

(45,262 | ) | (43,067 | ) | ||||

|

|

|

|

|

|||||

| Net income attributable to common stockholders |

$ | 33,730 | $ | 26,667 | ||||

|

|

|

|

|

|||||

| Total weighted average shares |

||||||||

| Basic |

114,245 | 97,941 | ||||||

|

|

|

|

|

|||||

| Diluted |

266,621 | 254,506 | ||||||

|

|

|

|

|

|||||

| Net income per share attributable to common stockholders |

||||||||

| Basic |

$ | 0.30 | $ | 0.27 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.29 | $ | 0.27 | ||||

|

|

|

|

|

|||||

10

Empire State Realty Trust, Inc.

Reconciliation of Net Income to Funds From Operations (“FFO”),

Modified Funds From Operations (“Modified FFO”) and Core Funds From Operations (“Core FFO”)

(unaudited and amounts in thousands, except per share data)

| Three Months Ended December 31, | ||||||||

| 2015 | 2014 | |||||||

| Net income |

$ | 19,370 | $ | 10,964 | ||||

| Preferred unit distributions |

(234 | ) | (235 | ) | ||||

| Real estate depreciation and amortization |

45,085 | 48,711 | ||||||

|

|

|

|

|

|||||

| FFO attributable to common stockholders and non-controlling interests |

64,221 | 59,440 | ||||||

| Amortization of below-market ground leases |

1,958 | 2,001 | ||||||

|

|

|

|

|

|||||

| Modified FFO attributable to common stockholders and non-controlling interests |

66,179 | 61,441 | ||||||

| Prepayment penalty expense and deferred financing cost write-off |

— | 3,771 | ||||||

|

|

|

|

|

|||||

| Core FFO attributable to common stockholders and non-controlling interests |

$ | 66,179 | $ | 65,212 | ||||

|

|

|

|

|

|||||

| Total weighted average shares |

||||||||

| Basic |

266,048 | 265,779 | ||||||

|

|

|

|

|

|||||

| Diluted |

266,048 | 265,779 | ||||||

|

|

|

|

|

|||||

| FFO per share |

||||||||

| Basic |

$ | 0.24 | $ | 0.22 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.24 | $ | 0.22 | ||||

|

|

|

|

|

|||||

| Modified FFO per share |

||||||||

| Basic |

$ | 0.25 | $ | 0.23 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.25 | $ | 0.23 | ||||

|

|

|

|

|

|||||

| Core FFO per share |

||||||||

| Basic |

$ | 0.25 | $ | 0.25 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.25 | $ | 0.25 | ||||

|

|

|

|

|

|||||

11

Empire State Realty Trust, Inc.

Reconciliation of Net Income to Funds From Operations (“FFO”),

Modified Funds From Operations (“Modified FFO”) and Core Funds From Operations (“Core FFO”)

(unaudited and amounts in thousands, except per share data)

| Year Ended December 31, | ||||||||

| 2015 | 2014 | |||||||

| Net income |

$ | 79,928 | $ | 70,210 | ||||

| Preferred unit distributions |

(936 | ) | (476 | ) | ||||

| Real estate depreciation and amortization |

170,932 | 145,115 | ||||||

|

|

|

|

|

|||||

| FFO attributable to common stockholders and non-controlling interests |

249,924 | 214,849 | ||||||

| Amortization of below-market ground leases |

7,831 | 4,603 | ||||||

|

|

|

|

|

|||||

| Modified FFO attributable to common stockholders and non-controlling interests |

257,755 | 219,452 | ||||||

| Acquisition break-up fee |

(2,500 | ) | — | |||||

| Prepayment penalty expense and deferred financing costs write-off |

1,749 | 3,771 | ||||||

| Construction severance expenses, net of income taxes |

480 | — | ||||||

| Acquisition expenses |

193 | 3,382 | ||||||

| Gain on settlement of lawsuit related to the Observatory, net of income taxes |

— | (540 | ) | |||||

| Private perpetual preferred exchange offering expenses |

— | 1,357 | ||||||

|

|

|

|

|

|||||

| Core FFO attributable to common stockholders and non-controlling interests |

$ | 257,677 | $ | 227,422 | ||||

|

|

|

|

|

|||||

| Total weighted average shares |

||||||||

| Basic |

265,914 | 254,506 | ||||||

|

|

|

|

|

|||||

| Diluted |

265,914 | 254,506 | ||||||

|

|

|

|

|

|||||

| FFO per share |

||||||||

| Basic |

$ | 0.94 | $ | 0.84 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.94 | $ | 0.84 | ||||

|

|

|

|

|

|||||

| Modified FFO per share |

||||||||

| Basic |

$ | 0.97 | $ | 0.86 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.97 | $ | 0.86 | ||||

|

|

|

|

|

|||||

| Core FFO per share |

||||||||

| Basic |

$ | 0.97 | $ | 0.89 | ||||

|

|

|

|

|

|||||

| Diluted |

$ | 0.97 | $ | 0.89 | ||||

|

|

|

|

|

|||||

12

Empire State Realty Trust, Inc.

Condensed Consolidated Balance Sheets

(unaudited and amounts in thousands)

| December 31, | December 31, | |||||||

| 2015 | 2014 | |||||||

| Assets |

||||||||

| Commercial real estate properties, at cost |

$ | 2,276,330 | $ | 2,139,863 | ||||

| Less: accumulated depreciation |

(465,584 | ) | (377,552 | ) | ||||

|

|

|

|

|

|||||

| Commercial real estate properties, net |

1,810,746 | 1,762,311 | ||||||

| Cash and cash equivalents |

46,685 | 45,732 | ||||||

| Restricted cash |

65,880 | 60,273 | ||||||

| Tenant and other receivables |

18,782 | 23,745 | ||||||

| Deferred rent receivables |

122,048 | 102,104 | ||||||

| Prepaid expenses and other assets |

50,460 | 48,504 | ||||||

| Deferred costs, net |

310,679 | 357,462 | ||||||

| Acquired below market ground leases, net |

383,891 | 391,887 | ||||||

| Goodwill |

491,479 | 491,479 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 3,300,650 | $ | 3,283,497 | ||||

|

|

|

|

|

|||||

| Liabilities and equity |

||||||||

| Mortgage notes payable |

$ | 747,661 | $ | 898,998 | ||||

| Senior unsecured notes |

587,018 | 234,980 | ||||||

| Unsecured term loan facility |

262,545 | — | ||||||

| Unsecured revolving credit facility |

35,192 | — | ||||||

| Term loan and credit facility |

— | 464,676 | ||||||

| Accounts payable and accrued expenses |

111,099 | 96,563 | ||||||

| Acquired below market leases, net |

104,171 | 138,859 | ||||||

| Deferred revenue and other liabilities |

31,388 | 27,876 | ||||||

| Tenants’ security deposits |

48,890 | 40,448 | ||||||

|

|

|

|

|

|||||

| Total liabilities |

1,927,964 | 1,902,400 | ||||||

| Total equity |

1,372,686 | 1,381,097 | ||||||

|

|

|

|

|

|||||

| Total liabilities and equity |

$ | 3,300,650 | $ | 3,283,497 | ||||

|

|

|

|

|

|||||

13