Exhibit 99.5

ANNUAL INFORMATION FORM

for the fiscal year ended December 31, 2020

SPROTT PHYSICAL PLATINUM AND PALLADIUM TRUST

(the “Trust”)

March 22, 2021

TABLE OF CONTENTS

1 | |

1 | |

1 | |

4 | |

6 | |

16 | |

18 | |

24 | |

25 | |

33 | |

58 | |

59 | |

60 | |

63 | |

65 | |

79 | |

96 | |

96 | |

97 | |

97 | |

98 |

i

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

The statements contained in this annual information form that are not purely historical are forward-looking statements. The Trust’s forward-looking statements include, but are not limited to, statements regarding its or its management’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates”, “believe”, “continue”, “could”, “estimate”, “expect”, “intends”, “may”, “might”, “plan”, “possible”, “potential”, “predicts”, “project”, “should”, “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements contained in this annual information form are based on the current expectations and beliefs of the Trust and Sprott Asset Management LP (the “Manager”) concerning future developments and their potential effects on the Trust. There can be no assurance that future developments affecting the Trust will be those that it or the Manager has anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond the Trust’s control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors”. Should one or more of these risks or uncertainties materialize, or should any of the Trust’s or the Manager’s assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Each of the Trust and the Manager undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Unless otherwise noted herein, all references to “$”, “U.S.$” or “dollars” are to the currency of the United States of America (the “United States” or the “U.S.”) and all references to “Cdn$” or “Canadian dollars” are to the currency of Canada. On March 11, 2021, the daily rate of exchange as reported by the Bank of Canada for the conversion of U.S. dollars into Canadian dollars was U.S.$1.00 equals Cdn$1.2561.

History and Development of the Trust

Sprott Physical Platinum and Palladium Trust (the “Trust”) was established under the laws of the Province of Ontario, Canada, pursuant to a trust agreement between the Trust’s settlor, Sprott Asset Management LP (the “Manager”) and RBC Investor Services Trust (“RBC Investor Services” or the “Trustee”), as trustee, dated as of December 23, 2011, as amended and restated as of June 6, 2012 (the “Trust Agreement”).

On December 21, 2012, the Trust closed its initial public offering with the sale of 28,000,000 units at $10.00 per unit, for gross proceeds of $280,000,000.

On March 29, 2016, the Manager, on behalf of the Trust, and the Royal Canadian Mint (the “Mint”) entered into a precious metals storage agreement in respect of the Trust’s physical palladium bullion and a precious metals storage agreement in respect of the Trust’s physical platinum bullion. These agreements replaced the previous storage agreements pursuant to which the Mint acted as

1

custodian for the Trust’s physical platinum and palladium bullion. For further details concerning the Storage Agreements, see “Responsibility for Operation of the Trust - Custodians - Custodian for the Trust’s Physical Platinum and Palladium Bullion”.

On June 24, 2016, the Trust entered into a sales agreement, as amended on January 29, 2020 (the “Sales Agreement”) with Cantor Fitzgerald & Co. (“Cantor”) whereby the Trust may, in its sole discretion and subject to its operating and investment restrictions, offer and sell up to $9,240,888 in value of units of the Trust (the “Placement Units”) through an “at the market offering” program (the “ATM Program”) in transactions on the NYSE Arca or any other existing trading market for the units of the Trust in the United States or to or through a market maker in the United States pursuant to a registration statement filed with the U.S. Securities and Exchange Commission and a prospectus supplement to a short form base shelf prospectus filed with the Ontario Securities Commission, as principal regulator, and with each of the securities commissions or similar regulatory authorities in each of the provinces and territories of Canada. Under the Sales Agreement, the Trust will pay to Cantor in cash, upon each sale of Placement Units, an amount equal to up to 3.0% of the aggregate gross proceeds from each sale of Placement Units.

On June 4, 2018, the Manager, for and on behalf of the Trust, and the Mint entered into: (a) a precious metals storage and custody agreement with the Mint in respect of the Trust’s physical platinum bullion (the “Platinum Storage Agreement”); and (b) a precious metals storage and custody agreement in respect of the Trust’s physical palladium bullion (the “Palladium Storage Agreement” and together with the Platinum Storage Agreement, the “Storage Agreements”) to replace the former versions thereof. For further details concerning the Storage Agreements, see “Responsibility for Operation of the Trust - Custodians - Custodian for the Trust’s Physical Platinum and Palladium Bullion”.

On June 28, 2018, pursuant to the Trust’s ATM Program, the Trust offered for sale trust units of the Trust having an aggregate sale price of up to $9,353,296 by way of a prospectus supplement dated June 28, 2018 to a final base shelf prospectus dated June 20, 2018. The ATM Program is implemented pursuant to the Sales Agreement. As at December 31, 2018, the Trust sold 0 units of the Trust through the ATM Program.

On January 29, 2020, the Trust, Cantor and Virtu Americas LLC (“Virtu”) entered into an amendment agreement to the Sales Agreement (“Amendment No. 1 to Sales Agreement”) pursuant to which, among other things, Virtu became a sales agent of trust units on and subject to the terms and conditions of the Sales Agreement, as amended.

On January 29, 2020, the Trust amended and restated its prospectus supplement dated March 9, 2019 to a final base shelf prospectus dated February 25, 2019 to, among other things, reflect the terms and conditions of the Amendment No. 1 to the Sales Agreement. During the period from January 1, 2019 to December 31, 2019, the Trust issued 190,715 units of the Trust through the ATM Program. 511,924 trust units of the Trust were sold pursuant to such prospectus supplement.

On October 21, 2020, the Trust entered into an amended and restated sales agreement dated October 21, 2020 (the “Amended and Restated Sales Agreement”) with the Manager, Cantor Fitzgerald & Co. (“CF&Co”), Virtu Americas LLC (“Virtu” and together with CF&Co, the “U.S. Agents”) and Virtu ITG Canada Corp. (together with the U.S. Agents, the “Agents”) relating to trust units offered by this prospectus supplement and the accompanying prospectus. The Amended and Restated Sales Agreement, as amended by Amendment No. 1 to the Sales Agreement. In accordance with the Amended and Restated Sales Agreement, the Rust may distribute trust units having an aggregate

2

offering price of up to U.S.$90,811,290 through the Agents. As at December 31, 2020, 92,195 trust units of the Trust were sold pursuant to such prospectus supplement.

During the period from January 1, 2020 to December 31, 2020, the Trust issued an aggregate of 702,185 units of the Trust through the ATM Program.

The Trust’s office is located at Royal Bank Plaza, South Tower, 200 Bay Street, Suite 2600, Toronto, Ontario, Canada M5J 2J1. The Manager’s head and registered office is located at Royal Bank Plaza, South Tower, 200 Bay Street, Suite 2600, Toronto, Ontario, Canada M5J 2J1 and its telephone number is (416) 943-8099 (toll free: 1-855-943-8099). The Trustee is located at 155 Wellington Street West, Street Level, Toronto, Ontario, Canada M5V 3L3. The custodian for the Trust’s physical platinum and palladium bullion, the Mint, has its premises located at 320 Sussex Drive, Ottawa, Ontario, Canada K1A 0G8. The Mint has engaged Loomis International (USA) Inc. (“Loomis”) (formerly known as Via Mat International Ltd., through its subsidiary, Via Mat International (USA) Inc.) as a sub-custodian for the Trust’s physical palladium bullion. The principal office of Loomis is located at 130 Sheridan Blvd., Inwood, New York, USA 11096. The custodian for the Trust’s assets other than physical platinum and palladium bullion, RBC Investor Services, is located at 155 Wellington Street West, Street Level, Toronto, Ontario, Canada M5V 3L3.

Investment Objectives of the Trust

The Trust was created to invest and hold substantially all of its assets in physical platinum and palladium bullion. The Trust seeks to provide a convenient and exchange-traded investment alternative for investors interested in holding physical platinum and palladium bullion without the inconvenience that is typical of a direct investment in physical platinum and palladium bullion. The Trust invests primarily in long-term holdings of unencumbered, fully allocated, physical platinum and palladium bullion and will not speculate with regard to short-term changes in platinum and palladium prices. The Trust does not anticipate making regular cash distributions to unitholders.

Investment Strategies of the Trust

The Trust is expressly prohibited from investing in units or shares of other investment funds or collective investment schemes other than money market mutual funds and then only to the extent that its interest does not exceed 10% of the total net assets of the Trust.

The Trust may not borrow funds except under limited circumstances as set out in National Instrument – 81-102 – Investment Funds (“NI 81-102”) and, in any event, not in excess of 10% of the total net assets of the Trust.

Borrowing Arrangements

The Trust has no borrowing arrangements in place and is unleveraged. The Trust has historically not used leverage and the Manager has no intention of doing so in the future (save for the short-term borrowings to settle trades). Unitholders will be notified of any changes to the Trust’s use of leverage.

3

INVESTMENT RESTRICTIONS AND OPERATING RESTRICTIONS

Mutual funds are subject to certain restrictions and practices contained in securities legislation, including NI 81-102, which are designed in part to ensure that investments of the mutual fund are diversified and relatively liquid and to ensure the proper administration of the mutual fund. Subject to the specific exceptions from NI 81-102 set out under “Exemptions and Approvals” of this annual information form, the Trust is managed in accordance with these restrictions and practices.

In making investments on behalf of the Trust, the Manager is subject to certain investment and operating restrictions (the “Investment and Operating Restrictions”), which are set out in the Trust Agreement. The Investment and Operating Restrictions may not be changed without the prior approval of unitholders by way of an extraordinary resolution, which must be approved, in person or by proxy, by unitholders holding units representing in aggregate not less than 662/3% of the value of the net assets of the Trust as determined in accordance with the Trust Agreement, at a duly constituted meeting of unitholders, or at any adjournment thereof, called and held in accordance with the Trust Agreement, or a written resolution signed by unitholders holding units representing in aggregate not less than 662/3% of the value of the net assets of the Trust as determined in accordance with the Trust Agreement, unless such change or changes are necessary to ensure compliance with applicable laws, regulations or other requirements imposed from time to time by applicable securities regulatory authorities. See “Responsibility for Operation of the Trust – The Trustee – Unitholder Approval”.

The Investment and Operating Restrictions provide that the Trust:

(a) | will invest in and hold a minimum of 90% of the total net assets of the Trust in physical platinum and palladium bullion conforming to the Good Delivery Standards (as defined below) of the London Platinum and Palladium Market (“LPPM”) plate or ingot form and hold no more than 10% of the total net assets of the Trust, at the discretion of the Manager, in physical platinum and palladium bullion (in Good Delivery plate or ingot form or otherwise), debt obligations of or guaranteed by the Government of Canada or a province of Canada or by the Government of the United States or a state thereof, short-term commercial paper obligations of a corporation or other person whose short-term commercial paper is rated R-1 (or its equivalent, or higher) by DBRS Limited or its successors or assigns or F-1 (or its equivalent, or higher) by Fitch Ratings or its successors or assigns or A-1 (or its equivalent, or higher) by Standard & Poor’s or its successors or assigns or P-1 (or its equivalent, or higher) by Moody’s Investor Service or its successors or assigns, interest-bearing accounts and short-term certificates of deposit issued or guaranteed by a Canadian chartered bank or trust company, money market mutual funds, short-term government debt or short-term investment grade corporate debt, or other short-term debt obligations approved by the Manager from time to time (for the purpose of this paragraph, the term “short-term” means having a date of maturity or call for payment not more than 182 days from the date on which the investment is made), except during the 60-day period following the closing of additional offerings or prior to the distribution of the assets of the Trust. “Good Delivery Standards” means the specifications for weight, dimensions, fineness (or purity), identifying marks and appearance, being a minimum fineness (or purity) of 99.95% weighing between 32.151 and 192.904 troy ounces as set forth in “The Good Delivery Rules for Platinum and Palladium Plates and Ingots” published by the LPPM. Pursuant to the Exemptive Relief (as defined in the section entitled “Exemptions and Approvals”), the Trust is permitted |

4

to invest up to 100% of its net assets, taken at market value of the time of purchase, in physical platinum and palladium bullion. See “Exemptions and Approvals”.

(b) | will not invest in platinum or palladium certificates, futures or other financial instruments that represent platinum or palladium or that may be exchanged for platinum or palladium; |

(c) | will store all physical platinum and palladium bullion owned by the Trust at the Mint and/or a sub-custodian of the Mint on a fully allocated basis, provided that physical platinum and palladium bullion held in Good Delivery plate or ingot form may be stored with a custodian or a sub-custodian, as the case may be, only if the physical platinum and palladium bullion will remain Good Delivery while with that custodian or sub-custodian; |

(d) | will not hold any property described in paragraphs (a) and (c) through (j) (inclusive) of the definition of “taxable Canadian Property” in subsection 248(1) of the Income Tax Act (Canada) (the “Tax Act”); |

(e) | will not purchase, sell or hold derivatives; |

(f) | will not issue units except: (i) if the net proceeds per unit to be received by the Trust are not less than 100% of the most recently calculated net asset value (“NAV”) per unit prior to, or upon, the determination of the pricing of such issuance; or (ii) by way of unit distribution in connection with an income distribution; |

(g) | will ensure that no part of the stored physical platinum and palladium bullion may be delivered out of safekeeping by the Mint (except to an authorized sub-custodian thereof) or, if the physical platinum and palladium bullion is held by another custodian, that custodian, without receipt of an instruction from the Manager in the form specified by the Mint or such custodian indicating the purpose of the delivery and giving direction with respect to the specific amount; |

(h) | will ensure that no director or officer of the Manager or the Manager’s general partner, or representative of the Trust or the Manager will be authorized to enter into the physical platinum and palladium bullion storage vaults without being accompanied by at least one representative of the Mint or its authorized sub-custodian or, if the physical platinum and palladium bullion is held by another custodian, that custodian, as the case may be; |

(i) | will ensure that the physical platinum and palladium bullion remains unencumbered; |

(j) | will inspect or cause to be inspected the stored physical platinum and palladium bullion periodically on a spot-inspection basis and, together with a representative of the Trust’s external auditor, physically audit the platinum and palladium bars annually to confirm respective bar numbers; |

(k) | will not guarantee the securities or obligations of any person other than the Manager, and then only in respect of the activities of the Trust; |

5

(l) | in connection with requirements of the Tax Act, will not make or hold any investment that would result in the Trust failing to qualify as a “mutual fund trust” within the meaning of the Tax Act; |

(m) | in connection with requirements of the Tax Act, will not invest in any security that would be a “tax shelter investment” within the meaning of section 143.2 of the Tax Act; |

(n) | in connection with requirements of the Tax Act, will not invest in the securities of any non-resident corporation, trust or other non-resident entity (or of any partnership that holds such securities) if the Trust (or the partnership) would be required to include any significant amount in income under sections 94, 94.1 or 94.2 of the Tax Act; |

(o) | in connection with requirements of the Tax Act, will not invest in any security of an issuer that would be a foreign affiliate of the Trust for purposes of the Tax Act; and |

(p) | in connection with requirements of the Tax Act, will not carry on any business and make or hold any investments that would result in the Trust itself being subject to the tax for specified investment flow-through (“SIFT”) trusts as provided for in section 122 of the Tax Act (the “SIFT Rules”). |

OVERVIEW OF THE PLATINUM AND PALLADIUM SECTORS

Platinum and Palladium Industries

Platinum and palladium are two of six precious metals comprising the platinum group metals (“PGMs”). Platinum and palladium are the PGMs produced in the greatest quantities and are generally viewed as the most significant PGMs in the global marketplace. The other four PGMs (rhodium, ruthenium, iridium and osmium) are produced as co-products of platinum and palladium. PGMs have unique physical attributes, including powerful catalytic properties, strong conductivity and ductility, high levels of resistance to corrosion, strength, durability and high melting points.

PGMs are mined primarily in South Africa and Russia. South Africa is the world’s leading platinum producer and the second largest palladium producer. In South Africa, PGMs occur chiefly in the Bushveld Igneous Complex, an irregular oval area approximately 15,000 square miles in size and centrally located in the Transvaal Basin. This complex hosts the world’s largest reserve of platinum metals. Russia is the largest producer of palladium, with production concentrated in the Norilsk region. Together, South Africa and Russia accounted for approximately 79% of global platinum mine production and 76% of global palladium mine production in 2020.

Due to their rarity and relative inertness, platinum and palladium are considered precious metals. Total 2020 mine production of platinum and palladium was approximately 4.89 and 6.17 million ounces, respectively.

Platinum and Palladium Supply

Platinum

Mine Production

6

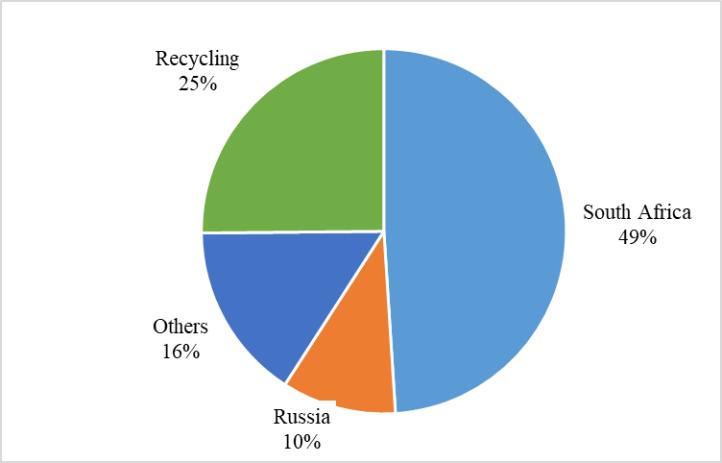

In 2020, 65% of global platinum mine production came from South Africa. The second largest producer in 2020 was Russia with an approximate 14% of mined supply. Platinum mine production dropped significantly in 2020 from 6.07 to 4.89 million ounces. It had previously been relatively stable since 2015.

Scrap and Recycling

According to Johnson Matthey (“JM”), recycling levels in 2020 contracted sharply from weak diesel scrap volumes in Europe and processing capacity constraints.

2020 Platinum Supply by Source

Source: JM PGM Market Report February 2021

Palladium

Mine Production

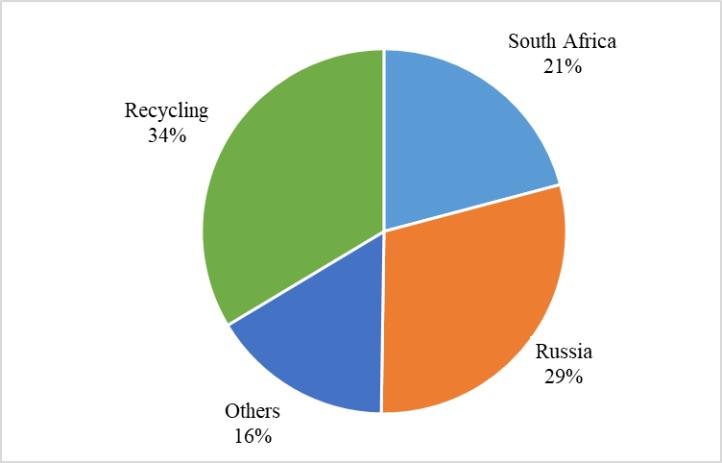

During 2020, mine production of palladium was dominated by Russia and South Africa, which was approximately 44% and 31% of global production (excludes supply from Russian stock sales and recycled palladium), respectively. Global mine production decreased significantly in 2020 from 6.17 million ounces in 2019 to 7.12 million ounces.

Scrap and Recycling

According to Johnson Matthey (“JM”), recycling levels in 2020 slowed in response to lower car sales and logistical difficulties in scrap collection.

7

2020 Palladium Supply by Source

Source: JM PGM Market Report February 2021 Platinum and Palladium Demand

Platinum

Demand for platinum is driven primarily by the following sources, in order of relative importance:

(i) | the automotive sector; |

(ii) | jewelry; |

(iii) | other (non-automotive) industrial manufacturing, including chemical production, electronics manufacturing and glass and petroleum refinement; and |

(iv) | investment. |

8

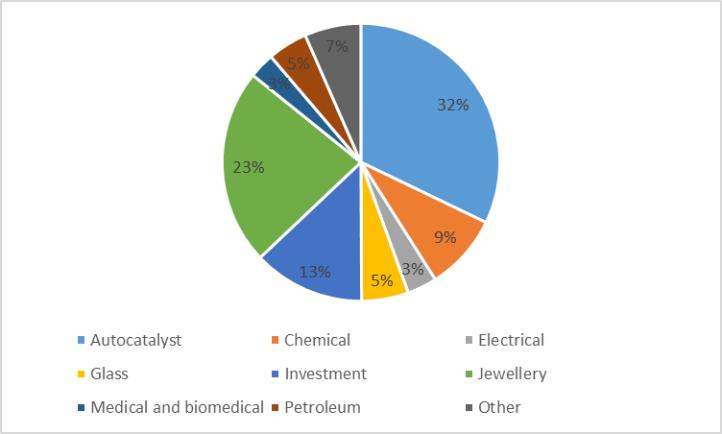

2020 Platinum Demand by Source

Source: JM PGM Market Report February 2021

The Automotive Sector

Platinum is a required component in the manufacturing of automobiles, primarily through its use in Autocatalysts. Platinum is used to form the surface catalyst upon which critical chemical reactions occur, converting exhaust emissions into neutral compounds. Diesel powered vehicles require platinum-based Autocatalysts, whereas gasoline vehicle manufacturers have the option of using palladium-based Autocatalysts. At present, there are no widely used substitutes for platinum or palladium used in Autocatalysts.

Platinum demand for use in Autocatalysts is 2.22 million ounces in 2020, or approximately 32% of global demand. Sales of new diesel cars in Europe continued to fall in 2020, as consumer attitudes and preferences about diesel cars remains subdued following the “dieselgate crisis” in 2015.

Jewelry

The second largest source of demand for platinum in 2020 was jewelry manufacturing, which represented approximately 23% of the global demand for platinum. Gross demand for platinum for jewelry manufacturing decreased significantly in 2020 to 1.58 million ounces as Chinese jewelry demand slumped to a twenty-year low. Platinum is sought after for its rarity, silvery-white lustre and resistance to wear and tarnish.

Other (Non-Automotive) Industrial Manufacturing

Industrial manufacturing includes the chemical sector, the petroleum refining sector, the electrical sector, the glass manufacturing sector, the medical, biomedical and dental sectors and other manufacturing sectors, such as turbines. Total non-automotive industrial demand for platinum is approximately 32% in 2020. Demand for platinum in industrial applications in 2020 was approximately 2.21 million ounces. Robust industrial demand is expected to offset the small decrease in autocatalyst and jewelry use of platinum.

9

Investment

This sector includes the investment and trading activities of both professional and private investors and speculators. These participants range from large hedge funds and mutual funds to day-traders on futures exchanges and retail-level coin collectors.

Physically-backed investment demand, comprising coins, bars, investments held in allocated accounts and exchange traded products, were a source of supply as investors liquidated some of their holdings as gains in platinum prices from the expectation of low supply failed to materialize.

Investment demand also fell in 2020 to 0.90 million ounces compared to 1.1 million ounces in 2019. This is still significantly higher than the 67 thousand ounces in 2018.

Palladium

Demand for palladium is driven primarily by the following sources, in order of relative importance:

(i) | the automotive sector; |

(ii) | other (non-automotive) industrial manufacturing; and |

(iii) | jewelry. |

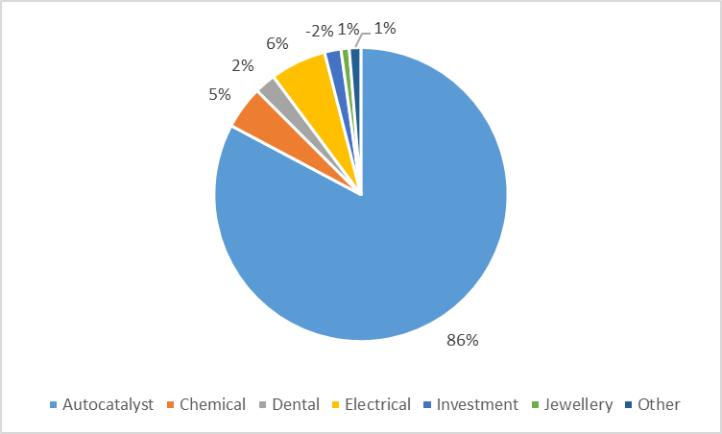

2020 Palladium Demand by Source

Source: JM PGM Market Report February 2021.

The Automotive Sector

Palladium, like platinum, is a key component in the manufacturing of automobiles, primarily through its use in gasoline Autocatalysts. Like platinum, palladium can be used to form the surface catalyst upon which critical chemical reactions occur, converting exhaust emissions into neutral compounds. In this regard, palladium is the only known substitute for platinum.

10

Autocatalyst demand for palladium decreased to 8.50 million ounces in 2020 making up approximately 86% of total demand. Rising consumer preferences for gasoline engine vehicles over diesel is driving demand for palladium.

Other (Non-Automotive) Industrial Manufacturing

Industrial manufacturing includes demand primarily from the electronics, dental and chemical industries. Electronics manufacturing includes palladium resistors and capacitors which are used in the manufacturing of circuit boards.

According to JM, the use of palladium in various industrial sectors declined slightly to 1.49 million ounces in 2020.

Investment

Net physical investment demand for palladium was negative 186,000 ounces in 2020, as redemptions of ETF holdings continued.

Jewelry

Jewelry demand dropped in 2020 to 93,000 ounces from 130,000 ounces in 2019.

World Platinum and Palladium Supply and Demand

The following tables illustrate the global supply (by region and through recycling) and demand (by usage) from 2017-2019. These tables are based on information provided in the JM Platinum reports.

World Platinum Supply and Demand (2018-2020)

Platinum Supply and Demand '000 oz | |||

Supply | 2018 | 2019 | 2020 |

South Africa | 4,467 | 4,398 | 3,199 |

Russia | 687 | 721 | 662 |

Others | 972 | 958 | 1,027 |

Total Supply | 6,126 | 6,077 | 4,888 |

Gross Demand | |||

Autocatalyst | 3,017 | 2,858 | 2,224 |

Jewellery | 2,258 | 2,056 | 1,581 |

Industrial | 2,585 | 2,415 | 2,214 |

Investment | 67 | 1,131 | 901 |

Total Gross Demand | 7,927 | 8,460 | 6,920 |

Recycling | -2,066 | -2,082 | -1,642 |

Total Net Demand | 5,861 | 6,378 | 5,278 |

Movement in Stocks | 265 | -301 | -390 |

Source: JM PGM Market Report February 2021

11

World Palladium Supply and Demand (2018-2020)

Palladium Supply and Demand '000 oz | |||

Supply | 2018 | 2019 | 2020 |

South Africa | 2,543 | 2,626 | 1,939 |

Russia | 2,976 | 2,987 | 2,727 |

Others | 1,506 | 1,504 | 1,501 |

Total Supply | 7,025 | 7,117 | 6,167 |

Gross Demand | |||

Autocatalyst | 8,876 | 9,672 | 8,497 |

Jewellery | 148 | 130 | 93 |

Industrial | 1,902 | 1,702 | 1,490 |

Investment | -574 | -87 | -186 |

Total Gross Demand | 10,352 | 11,417 | 9,894 |

Recycling | -3,108 | -3,407 | -3,121 |

Total Net Demand | 7,244 | 8,010 | 6,773 |

Movement in Stocks | -219 | -893 | -606 |

Source: JM PGM Market Report February 2021

Operation of the Platinum and Palladium Markets

Physical platinum and palladium can be bought and sold through various intermediaries such as precious metal traders and various precious metal exchanges. Additionally, physical platinum and palladium coins and bars can also be purchased through government mints.

Futures on platinum and palladium are traded on two major exchanges: The New York Mercantile Exchange, which we will refer to as NYMEX, and Tokyo Commodities Exchange, which we will refer to as the TOCOM. The NYMEX accounts for the majority of palladium trading volume and has seen increased levels of activity over the past five years. Smaller markets include Shanghai, Mumbai and Johannesburg. The LPPM is a London-based trade association that acts as the coordinator for activities conducted on behalf of its members and other participants in the London platinum and palladium markets. Members of the LPPM act as the over-the-counter, which we will refer to as the OTC, market-makers for platinum and palladium. Most OTC market trades are cleared through London. The LPPM plays an important role in setting OTC precious metals trading industry standards. Members of the LPPM typically trade with each other and with their clients on a principal-to-principal basis. All risks, including those of credit, are between the two parties to a transaction. This is known as an OTC market, as opposed to an exchange-traded environment. The OTC market allows flexibility unlike a futures exchange, where trading is based around standard contract units, settlement dates and delivery specifications. It also provides confidentiality, as transactions are conducted solely between the two principals involved.

In the OTC market, platinum and palladium that meet the specifications for weight, dimensions, fineness (or purity), identifying marks (including the assay stamp of an LPPM-acceptable refiner) and appearance set forth in the LPPM “London/Zurich Good Delivery List” are a standard “Good

12

Delivery plate or ingot”. A Good Delivery plate or ingot must contain between 32.151 troy ounces and 192.904 troy ounces of platinum or palladium with a minimum fineness (or purity) of 999.5 parts per 1,000. A Good Delivery plate or ingot must also bear the stamp of one of the refiners listed on the LPPM-approved list.

Rationale for an Investment in Platinum and Palladium

Essential elements

Platinum and palladium have incredible properties that can make them very valuable. They are among the rarest elements found on earth. They are critical for autocatalysts in both gasoline and diesel vehicles.

Limited Sources of Supply

About 89% of platinum and 82% of palladium are produced from just three countries – South Africa, Russia and Zimbabwe. As a result, platinum and palladium are susceptible to supply disruptions, geopolitical risks, labour strikes and price volatility. Both platinum and palladium markets were in a supply deficit in 2020.

The primary PGM producing countries are experiencing issues that may lead to a decline in production

The Manager believes that the PGM industry globally will experience increasing challenges that will impact both the cost and quantities of PGM production. As noted above, while demand for platinum and palladium has grown over the past few years, supply from mining operations has remained relatively flat. In particular, PGM producers with operations in South Africa are experiencing production challenges, caused by both internal and external factors. Ore grades of existing operations are generally declining and mining operations are progressing to lower depths, with associated increased costs of production.

Pressure to increase wages is an ongoing threat which can lead to worker strikes and unrest. Labour settlements could have a significant impact on overall costs, since labour costs constitute roughly 60% of total production costs. Ongoing issues with the reliability of the national electric power grid in South Africa exacerbates the risk as it leads to production shut downs.

The Manager believes that demand for PGMs for automobile and industrial applications will continue to grow

Platinum and palladium are essential components in Autocatalysts—they are the catalyst upon which the reaction converting exhaust emissions into neutral substances occurs. At present, there are no widely used substitutes for platinum and palladium in catalytic converters. As pollution standards around the world become increasingly strict, the use of additional platinum and palladium required in the manufacturing of Autocatalysts to meet these stricter standards is expected to increase. As new industrial applications for platinum and palladium, such as fuel cells continue to emerge, the Manager believes that industrial demand will require increasingly larger amounts of platinum and palladium in the future.

In addition, the continued expansion of more stringent emissions standards across Asia and Europe is increasing both palladium and platinum loadings per vehicle. Overall, the Manager believes that

13

global demand growth for autocatalysts, while sensitive to economic factors, should remain relatively steady despite potential near-term economic instability.

Promising new growth in the production of fuel cells

Platinum is widely used in the production of hydrogen fuel cells, forming the catalytic surface upon which the reaction separating hydrogen from oxygen occurs. Platinum is the most efficient of these surfaces, a platinum-ruthenium alloy is the only close substitute. Fuel cells are becoming increasingly commercialized, recently for stationary power generation and niche vehicles such as forklifts, as well as longer term for light duty vehicles and buses. The Manager believes demand for platinum will increase over time to address environmental concerns. These prospects should continue to support platinum demand and prices.

14

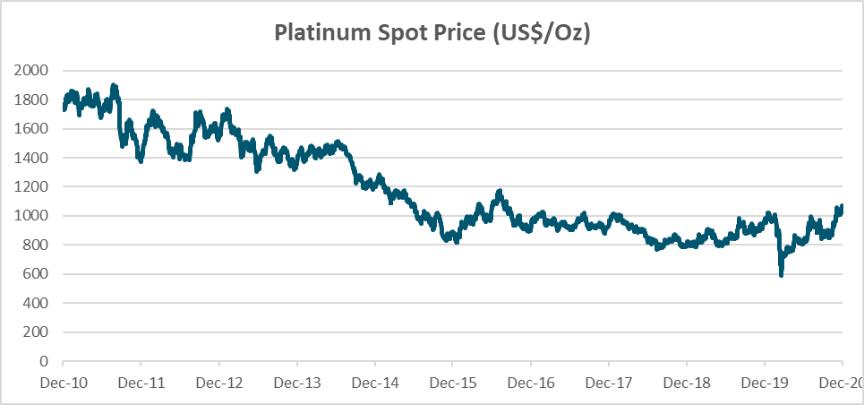

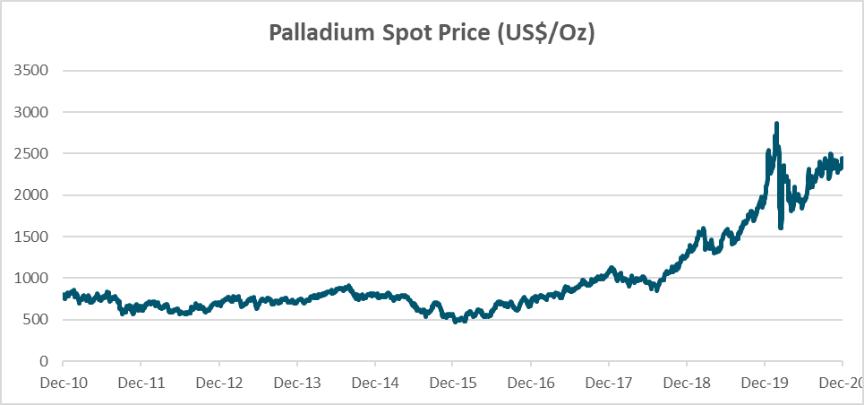

Historical Price Chart

10 Year Price History of Platinum (US$/troy ounce)(1)

10 Year Price History of Palladium (US$/troy ounce)(1)

Source: Bloomberg, December 31, 2020

(1) | The information provided in these graphs is historical and should not be taken as an indication of the future price of platinum or palladium. |

15

General

The Trust is authorized to issue an unlimited number of units in one or more classes and series of a class. Currently, the Trust has issued only one class or series of units. Each unit of a class or series of a class represents an undivided ownership interest in the net assets of the Trust attributable to that class or series of a class of units. Units are transferable and redeemable at the option of the unitholder in accordance with the provisions set forth in the Trust Agreement. All units of the same class or series of a class have equal rights and privileges with respect to all matters, including voting, receipt of distributions from the Trust, liquidation and other events in connection with the Trust. Units and fractions thereof are issued only as fully paid and non-assessable. Units have no preference, conversion, exchange or pre-emptive rights. Each whole unit of a particular class or series of a class entitles the holder thereof to a vote at meetings of unitholders where all classes vote together, or to a vote at meetings of unitholders where that particular class or series of a class of unitholders votes separately as a class.

The Trust may not issue additional units of the class except: (i) if the net proceeds per unit to be received by the Trust are not less than 100% of the most recently calculated NAV per unit immediately prior to, or upon, the determination of the pricing of such issuance; or (ii) by way of unit distribution in connection with an income distribution.

Meetings of Unitholders

Each unitholder is entitled to one vote for each whole unit held by the unitholder. Meetings of unitholders will be held by the Manager or the Trustee at such time and on such day as the Manager or the Trustee may from time to time determine for the purpose of considering the matters required to be placed before such meetings in accordance with the Trust Agreement or applicable laws and for the transaction of such other related matters as the Manager or the Trustee determines. Unitholders holding units representing in aggregate not less than 50% of the value of the net assets of the Trust as determined in accordance with the Trust Agreement may requisition a meeting of unitholders by giving a written notice to the Manager or the Trustee setting out in detail the reason(s) for calling and holding such a meeting. The Trustee will, upon the written request of the Manager or the unitholders holding units representing in aggregate not less than 50% of the value of the net assets of the Trust as determined in accordance with the Trust Agreement, requisition a meeting of unitholders, provided that in the event of a request to call a meeting of unitholders made by such unitholders, the Trustee will not be obligated to call any such meeting until it has been satisfactorily indemnified by such unitholders against all costs of calling and holding such meeting. Unless otherwise required by applicable securities laws or stock exchange rules, the Trust need only hold meetings of unitholders as described above and is not required to hold annual or other periodic meetings.

Meetings of unitholders will be held at the principal office of the Trust or elsewhere in the municipality in which its office is located or, if the Manager so determines, at any other place in Canada. Notice of the time and place of each meeting of unitholders will be given not less than 21 days before the day on which the meeting is to be held to each unitholder of record at 4:00 p.m., Toronto time, on the day on which the notice is given. Notice of a meeting of unitholders will state the general nature of the matters to be considered by the meeting. A meeting of unitholders may be held at any time and place without notice if all the unitholders entitled to vote thereat are present in person or represented by proxy or, if those not present or represented by proxy waive notice of, or otherwise consent to, such meeting being held.

16

A quorum for the transaction of business at any meeting of unitholders will be at least two unitholders holding not less than 5% of the outstanding units on such date present in person or represented by proxy and entitled to vote thereat. The chairman at a meeting of unitholders may, with the consent of the meeting and subject to such conditions as the meeting may decide, adjourn the meeting from time to time and from place to place.

At any meeting of unitholders every person will be entitled to vote who, as of the end of the business day immediately preceding the date of the meeting, is entered in the register of the Trust, unless in the notice of meeting and accompanying materials sent to unitholders in respect of the meeting a record date is established for persons entitled to vote thereat. The Trust is permitted to establish a record date for distributions in accordance with the policies of the Toronto Stock Exchange (the “TSX”) and NYSE Arca pursuant to the Exemptive Relief. See “Exemptions and Approvals”.

For the purpose of determining the unitholders who are entitled to receive notice of and to vote at any meeting or any adjournment thereof, or for the purpose of any action other than as provided in the Trust Agreement for valuation, computation and distribution of net income and net realized capital gains, any other additional distributions, and taxes, the Manager may fix a date not more than 60 days nor fewer than 30 days prior to the date of any meeting of unitholders or other action as a record date for the determination of unitholders entitled to receive notice of and to vote at such meeting, or any adjournment thereof, or to receive such distributions or to be treated as unitholders of record for purposes of such other action, and any unitholder who was a unitholder at the time so fixed will be entitled to receive notice of and to vote at, such meeting, or any adjournment thereof, or to be treated as a unitholder of record for purposes of such other action, even though he or she has since that date disposed of his or her units and no unitholder becoming such after that date will be entitled to receive notice of and to vote at such meeting, or any adjournment thereof, or to be treated as a unitholder of record for purposes of such other action.

At any meeting of unitholders, any unitholder entitled to vote thereat may vote by proxy and a proxy need not be a unitholder, provided that no proxy may be voted at any meeting unless it has been placed on file with the Manager, or with such other agent of the Trust as the Manager may direct, prior to the commencement of such meeting. If approved by the Manager, proxies may be solicited naming the Manager as proxy and the cost of such solicitation will be paid out of the property of the Trust. When any unit is held jointly by several persons, any one of them may vote at any meeting in person or by proxy in respect of such unit, but if more than one of them is present at such meeting in person or by proxy, and such joint owners or their proxies so present disagree as to any vote to be cast, such vote will not be received in respect of such unit. The instrument appointing any proxy will be in such form and executed in such manner as the Manager may from time to time determine.

At any meeting of unitholders every question will, unless otherwise required by the Trust Agreement or applicable laws, be determined by an ordinary resolution on the question which must be approved by the vote, in person or by proxy, of unitholders holding units representing in aggregate not less than 50% of the value of the net assets of the Trust as determined in accordance with the Trust Agreement. See “Responsibility for Operation of the Trust – The Trustee – Unitholder Approval”.

Subject to the provisions of the Trust Agreement or applicable laws, any question at a meeting of unitholders will be decided by a show of hands unless a poll thereon is required or demanded. Upon a show of hands every person who is present and entitled to vote will have one vote. If demanded by any unitholder at a meeting of unitholders or required by applicable laws, any question at such meeting will be decided by a poll. Upon a poll each person present will be entitled, in respect of

17

the units which the unitholder is entitled to vote at the meeting upon the question, to one vote for each whole unit held and the result of the poll so taken will be the decision of the unitholders upon the said question.

A resolution in writing forwarded to all unitholders entitled to vote on such resolution at a meeting of unitholders and signed by the requisite number of unitholders required to obtain approval of the matter addressed in such resolution is as valid as if it had been passed at a meeting of unitholders in accordance with the Trust Agreement.

Any resolution passed in accordance with the Trust Agreement will be binding on all unitholders and their respective heirs, executors, administrators, other legal representatives, successors and assigns, whether or not such unitholder was present or represented by proxy at the meeting at which such resolution was passed and whether or not such unitholder voted against such resolution.

Unitholder Liability

The Trust Agreement provides that no unitholder will be held to have any personal liability as a unitholder and that there will be no resort to the unitholder’s private property for satisfaction of any obligation or claim arising out of or in connection with any contract or obligation of any of the Trust, the Manager or the Trustee or any obligation that a unitholder would otherwise have to indemnify the Trustee for any personal liability incurred by the Trustee as such, but rather, only the Trust’s assets are intended to be liable and subject to levy or execution for such satisfaction. If the Trust acquires any investments subject to existing contractual obligations, the Manager, or the Trustee on the direction of the Manager, as the case may be, will use its best efforts to have any obligations modified so as to achieve disavowal of contractual liability. Further, the Trust Agreement provides that the Manager will cause the operations of the Trust to be conducted, with the advice of counsel, in such a way and in such jurisdictions as to avoid, as far as possible, any material risk of liability on the unitholders of claims against the Trust and will, to the extent it determines to be possible and reasonable, including the cost of premiums, cause the Trust to carry insurance for the benefit of the unitholders in such amounts as it considers adequate to cover any such foreseeable non-contractual or non-excluded contractual liability.

Unitholder Reporting

The Manager sends annually to unitholders a request form the unitholder may use to instruct the Manager to deliver a copy of the audited annual financial statements of the Trust within 90 days of each fiscal year-end as well as unaudited interim financial statements of the Trust within 60 days of the end of each interim period. Within 45 days of the end of each fiscal quarter, the Manager will make also available to unitholders an unaudited quarterly summary of the assets of the Trust and the value of the net assets of the Trust as of the end of such quarter.

CALCULATION OF NET ASSET VALUE

The calculation of the value of net assets of the Trust is the responsibility of the Manager, who may consult with the Trust’s valuation agent, the Mint and the Trust’s custodians. Pursuant to a Valuation Service Agreement (as hereinafter defined), the Manager appointed RBC Investor Services as valuation agent to calculate the value of the net assets of the Trust and the Class Net Asset Value (as hereinafter defined) for each class or series of a class of units as of 4:00 p.m., Toronto time, on each business day. In addition, the Manager may calculate the value of the net assets of the Trust, the Class Net Asset Value and the NAV per unit at such other times as the Manager deems appropriate.

18

Pursuant to the Trust Agreement, the value of the net assets of the Trust will be determined for the purposes of subscriptions and redemptions as of the valuation time on each business day in U.S. dollars. The value of the net assets of the Trust determined on the last day of each year that is also a valuation date of the Trust will include all income, expenses of the Trust or any other items to be accrued to December 31 of such year and since the last calculation of the NAV or the Class Net Asset Value per unit (as hereinafter defined), for the purpose of the distribution of net income and net realized capital gains of the Trust to unitholders.

The value of the net assets of the Trust as of the valuation time on each business day is the amount obtained by deducting from the aggregate fair market value of the assets of the Trust as of such date an amount equal to the fair value of the liabilities of the Trust (excluding all liabilities represented by outstanding units, if any) as of such date. The value of net assets per unit is determined by dividing the value of the net assets of the Trust on a date by the total number of units then outstanding on such date. Subject to directions from the Manager as required, the value of the net assets of the Trust as of the valuation time on a date is determined by the Trust’s valuation agent in accordance with the following:

(a) | The assets of the Trust are deemed to include the following property: |

(i) | all physical platinum and palladium bullion owned by or contracted for the Trust; |

(ii) | all cash on hand or on deposit, including any interest accrued thereon adjusted for accruals deriving from trades executed but not yet settled; |

(iii) | all bills, notes and accounts receivable; |

(iv) | all interest accrued on any interest-bearing securities owned by the Trust other than interest, the payment of which is in default; and |

(v) | prepaid expenses. |

(b) | The market value of the assets of the Trust is determined as follows: |

(i) | the value of physical platinum and palladium bullion is its market value based on the price provided by a widely recognized pricing service as directed by the Manager (as described below) and, if such service is not available, such physical platinum and palladium bullion is valued at prices provided by another pricing service as determined by the Manager, in consultation with the valuation agent; |

(ii) | the value of any cash on hand or on deposit, bills, demand notes, accounts receivable, prepaid expenses, and interest accrued and not yet received, is deemed to be the full amount thereof unless the Manager determines that any such deposit, bill, demand note, account receivable, prepaid expense or interest is not worth the full amount thereof, in which event the value thereof is deemed to be such value as the Manager determines to be the fair value thereof; |

(iii) | short-term investments including notes and money market instruments are valued at cost plus accrued interest; |

19

(iv) | the value of any security or other property for which no price quotations are available or, in the opinion of the Manager (which may delegate such responsibility to the Trust’s valuation agent under the Valuation Service Agreement), to which the above valuation principles cannot or should not be applied, will be the fair value thereof determined from time to time in such manner as the Manager (or the Trust’s valuation agent, as the case may be) will from time to time provide; and |

(v) | the value of all assets and liabilities of the Trust valued in terms of a currency other than the currency used to calculate the value of the net assets of the Trust is converted to the currency used to calculate the value of the net assets of the Trust by applying the rate of exchange obtained from the best available sources to the Trust’s valuation agent as agreed upon by the Manager including, but not limited to, the Trustee or any of its affiliates. |

The Trust currently uses the platinum and palladium spot price provided by Bloomberg Finance L.P. (“Bloomberg”) under the symbols PLAT COMDTY (USD) and PALL COMDTY (USD), respectively. According to information received from Bloomberg, PLAT COMDTY (USD) and PALL COMDTY (USD) are composite prices for platinum and palladium that are calculated according to a set algorithm by Bloomberg from data provided to Bloomberg by third party contributors. If the Manager deems it necessary, the Manager may determine, without prior notice, that a different widely recognized pricing service or services should be used to calculate the value of platinum and palladium bullion set forth in (b)(i) above.

(c) | The liabilities of the Trust are calculated on a fair value basis and deemed to include the following: |

(i) | all bills, notes and accounts payable; |

(ii) | all fees (including management fees) and administrative and operating expenses payable and/or accrued by the Trust; |

(iii) | all contractual obligations for the payment of money or property, including distributions of net income and net realized capital gains of the Trust, if any, declared, accrued or credited to the unitholders but not yet paid on the day before the valuation date as of which the value of the net assets of the Trust is being determined; |

(iv) | all allowances authorized or approved by the Manager or the Trustee for taxes or contingencies; and |

(v) | all other liabilities of the Trust of whatsoever kind and nature, except liabilities represented by outstanding units. |

(d) | For the purposes of determining the market value of any security or property pursuant to paragraph (b) above to which, in the opinion of the Trust’s valuation agent in consultation with the Manager, the above valuation principles cannot be applied (because no price or yield equivalent quotations are available as provided |

20

above, or the current pricing option is not appropriate, or for any other reason), is the fair value as determined in such manner by the Trust’s valuation agent in consultation with the Manager and generally adopted by the marketplace from time to time, provided that any change to the standard pricing principles as set out above will require prior consultation and written agreement with the Manager. For greater certainty, fair valuing an investment comprising the property of the Trust may be appropriate if:

(i) | market quotations do not accurately reflect the fair value of an investment; |

(ii) | an investment’s value has been materially affected by events occurring after the close of the exchange or market on which the investment is principally traded; |

(iii) | a trading halt closes an exchange or market early; or |

(iv) | other events result in an exchange or market delaying its normal close. |

(e) | For the purposes of determining the value of physical platinum and palladium bullion, the Manager relies solely on weights provided to the Manager by third parties. The Manager, the Trustee or the Trust’s valuation agent are not required to make any investigation or inquiry as to the accuracy or validity of such weights. |

(f) | Portfolio transactions (investment purchases and sales) are reflected in the first computation of the value of the net assets of the Trust made after the date on which the transaction becomes binding. |

(g) | The value of the net assets of the Trust and NAV on any day are deemed to be equal to value of the net assets of the Trust (or per unit, as the case may be) on such date after accrual of all fees, including management fees, and after processing of all subscriptions and redemptions of units in respect of such date. |

(h) | The value of the net assets of the Trust and the NAV determined by the Manager (or, if so delegated under the Valuation Service Agreement, the Trust’s valuation agent) in accordance with the provisions of the Trust Agreement is conclusive and binding on all unitholders. |

(i) | The Manager and any investment manager retained by the Manager may determine such other rules regarding the calculation of the value of the net assets of the Trust and the NAV which they deem necessary from time to time, which rules may deviate from International Financial Reporting Standards (“IFRS”). |

Calculation of Class Net Asset Value and Class Net Asset Value per Unit

(a) | The net asset value for a particular class or series of a class of units (the “Class Net Asset Value”), as of 4:00 p.m., Toronto time, on each business day will be determined for the purposes of subscriptions and redemptions in accordance with the following calculation: |

(i) | the Class Net Asset Value last calculated for that class or series of a class; plus |

21

(ii) | the increase in the assets attributable to that class or series of a class as a result of the issue of units of that class or series of a class or the redesignation of units into that class or series of a class since the last calculation; minus |

(iii) | the decrease in the assets attributable to that class or series of a class as a result of the redemption of units of that class or series of a class or the redesignation of units out of that class or series of a class since the last calculation; plus or minus |

(iv) | the proportionate share of the net change in non-portfolio assets attributable to that class or series of a class since the last calculation; plus or minus |

(v) | the proportionate share of market appreciation or depreciation of the portfolio assets attributable to that class or series of a class since the last calculation; minus |

(vi) | the proportionate share of the common expenses of the Trust (other than expenses that are specifically chargeable to a particular class) allocated to that class or series of a class since the last calculation; minus |

(vii) | any expenses of the Trust (including management fees) that are specifically chargeable to a particular class or series of a class allocated to that class or series of a class since the last calculation. |

(b) | A unit of a class or series of a class of the Trust being issued or a unit that has been redesignated as a part of that class or series of a class will be deemed to become outstanding as of the next calculation of the applicable Class Net Asset Value immediately following the date at which the applicable Class Net Asset Value per unit that is the issue price or redesignation basis of such unit is determined, and the issue price received or receivable for the issuance of the unit will then be deemed to be an asset of the Trust attributable to the applicable class or series of a class. |

(c) | A unit of a class or series of a class of the Trust being redeemed or a unit that has been redesignated as no longer being a part of that class or series of a class will be deemed to remain outstanding as part of that class or series of a class until immediately following the valuation date as of which the applicable Class Net Asset Value per unit that is the redemption price or redesignation basis of such unit is determined; thereafter, the redemption price of the unit being redeemed, until paid, will be deemed to be a liability of the Trust attributable to the applicable class or series of a class and the unit which has been redesignated will be deemed to be outstanding as a part of the class or series of a class into which it has been redesignated. |

(d) | On any valuation date that a distribution is paid to unitholders of a class or series of a class of units, a second Class Net Asset Value will be calculated for that class or series of a class, which will be equal to the first Class Net Asset Value calculated on that valuation date minus the amount of the distribution. The second Class Net Asset Value will be used for determining the Class Net Asset Value per unit on such valuation date for purposes of determining the issue price and redemption |

22

price for units on such valuation date, as well as the redesignation basis for units being redesignated into or out of such class or series of a class, and units redeemed or redesignated out of that class or series of a class as of such valuation date will participate in such distribution while units subscribed for or redesignated into such class or series of a class as of such valuation date will not.

(e) | The Class Net Asset Value per unit of a particular class or series of a class of units as of any date is the quotient obtained by dividing the applicable Class Net Asset Value as of such date by the total number of units of that class or series of a class outstanding at such valuation date. This calculation will be made without taking into account any issuance, redesignation or redemption of units of that class or series of a class to be processed by the Trust immediately after the valuation time of such calculation on that valuation date. The Class Net Asset Value per unit for each class or series of a class of units for the purpose of the issue of units or the redemption of units will be calculated on each valuation date by or under the authority of the Manager (which may delegate such responsibility to the Trust’s valuation agent under the Valuation Service Agreement) as of the valuation time on every valuation date as fixed from time to time by the Manager, and the Class Net Asset Value per unit so determined for each class or series of a class will remain in effect until the valuation time as of which the Class Net Asset Value per unit for that class or series of a class is next determined. |

For the purposes of the foregoing disclosure the following capitalized terms have the meanings set forth below:

“Net change in non-portfolio assets” on a date means:

(i) | the aggregate of all income accrued by the Trust as of that date, including cash dividends and distributions, interest and compensation since the last calculation of Class Net Asset Value or Class Net Asset Value per unit, as the case may be; minus |

(ii) | the common expenses of the Trust (other than expenses that are specifically chargeable to a particular class or series of a class) to be accrued by the Trust as of that date which have been accrued since the last calculation of Class Net Asset Value or Class Net Asset Value per unit, as the case may be; plus or minus |

(iii) | any change in the value of any non-portfolio assets or liabilities stated in any foreign currency accrued on that date since the last calculation of Class Net Asset Value or Class Net Asset Value per unit, as the case may be, including, without limitation, cash, accrued dividends or interest and any receivables or payables; plus or minus |

(iv) | any other item accrued on that date determined by the Manager to be relevant in determining the net change in non-portfolio assets. |

“Proportionate share”, when used to describe (i) an amount to be allocated to any one class or series of a class of the Trust, means the total amount to be allocated to all classes or series of classes of the Trust multiplied by a fraction, the numerator of which is the Class Net Asset Value of such class or series of a class and the denominator of which is the value of the net assets of the Trust at

23

such time, and (ii) a unitholder’s interest in or share of any amount, means, after an allocation has been made to each class or series of a class as provided in clause (i), that allocated amount multiplied by a fraction, the numerator of which is the number of units of that class or series of a class registered in the name of that unitholder and the denominator of which is the total number of units of that class or series of a class then outstanding (if such unitholder holds units of more than one class or series of a class, then such calculation is made in respect of each class or series of a class and aggregated).

The calculation of the value of the net assets of the Trust and the NAV for each class or series of a class of units as of the valuation time on each valuation date is for the purposes of determining subscription prices and redemption values of units and not for the purposes of accounting in accordance with IFRS. The value of the net assets of the Trust calculated in this manner will be used for the purpose of calculating the Manager’s and other service providers’ fees and will be published net of all paid and payable fees.

Suspension of Calculation of Net Asset Value Per Unit

During any period in which the right of unitholders to request a redemption of their units for physical platinum and palladium bullion and/or cash is suspended, the Manager, on behalf of the Trust, will direct the Trust’s valuation agent to suspend the calculation of the value of the net assets of the Trust, the NAV, the Class Net Asset Value and the net asset value per unit for each class or series of a class of units. During any such period of suspension, the Trust will not issue or redeem any units. As noted in “Redemption of Units—Suspension of Redemptions”, in the event of any such suspension or termination thereof, the Manager will issue a press release announcing the suspension or the termination of such suspension, as the case may be.

Reporting of Net Asset Value

The value of the net assets of the Trust and the NAV per unit is updated on a daily basis or as determined by the Manager in accordance with the Trust Agreement and is made available as soon as practicable at no cost on the Trust’s website (www.sprottphysicalbullion.com/sprott-physical-platinum-and-palladium-trust) or by calling the Manager at (416)-943-8099 or toll free at 1-855-943-8099 (9:00 a.m. to 5:00 p.m., Toronto time). Information contained in, or connected to, the Manager’s website is not incorporated into, and does not form part of, this annual information form.

The Trust’s units are traded on NYSE Arca under the symbol “SPPP” and the TSX under the symbols “SPPP” and “SPPP.U”. Purchases of units can be made on NYSE Arca and the TSX pursuant to the Exemptive Relief. See “Exemptions and Approvals”. Purchases of units are made through registered dealers. Please contact your dealer to find out how to place an order. Some dealers may charge you a fee for their services.

The following table sets forth, for the periods indicated, the reported high and low daily trading prices and the monthly average trading volume of the trust units on the TSX (as reported by TSX) and the NYSE ARCA (as reported by NYSE ARCA) for 2020.

24

| NYSE ARCA | TSX | |||||||

|---|---|---|---|---|---|---|---|---|---|

Calendar Period | High | Low | Average | High | Low | Average | High | Low (Cdn$) | Average |

January 2020 | 17.54 | 14.35 | 13,228 | 18.29 | 14.44 | 1,144 | 24.13 | 18.95 | 1,219 |

February 2020 | 19.31 | 15.65 | 15,951 | 18.56 | 15.89 | 375 | 25.36 | 21.00 | 1,216 |

March 2020 | 17.30 | 8.83 | 27,009 | 17.99 | 9.09 | 1,204 | 22.95 | 13.82 | 1,493 |

April 2020 | 15.52 | 12.26 | 21,899 | 15.06 | 12.69 | 224 | 21.96 | 17.47 | 916 |

May 2019 | 15.00 | 12.24 | 14,560 | 14.74 | 12.25 | 321 | 21.00 | 16.92 | 775 |

June 2020 | 14.52 | 13.41 | 9,505 | 14.41 | 13.71 | 559 | 19.60 | 17.50 | 799 |

July 2020 | 16.92 | 13.65 | 13,288 | 17.10 | 13.76 | 653 | 22.50 | 18.74 | 1,376 |

August 2020 | 17.35 | 15.44 | 11,853 | 17.30 | 15.58 | 614 | 23.31 | 20.38 | 1,489 |

September 2020 | 17.48 | 14.80 | 12,660 | 17.20 | 14.58 | 302 | 22.95 | 19.39 | 1,316 |

October 2020 | 16.70 | 15.00 | 4,988 | 16.30 | 15.18 | 200 | 22.07 | 19.57 | 689 |

November 2020 | 16.76 | 15.00 | 7,371 | 16.52 | 15.46 | 245 | 21.66 | 20.21 | 556 |

December 2020 | 18.30 | 16.32 | 8,703 | 17.67 | 16.72 | 567 | 23.30 | 20.93 | 1,235 |

Note:

(1) Includes volume traded on other United States exchanges and trading markets.

Subject to the terms of the Trust Agreement and the Manager’s right to suspend redemptions in the circumstances described below, units may be redeemed at the option of a unitholder in any month for physical platinum and palladium bullion or cash. All redemptions will be determined using U.S. dollars, regardless of whether the redeemed units were acquired on NYSE Arca or the TSX. Redemption requests will be processed on the last business day of the applicable month.

Redemptions for Physical Platinum and Palladium Bullion

Subject to the terms of the Trust Agreement, a unitholder may redeem Units for physical platinum and palladium bullion, provided the redemption request is for a minimum of 25,000 units. Units redeemed for physical platinum and palladium bullion will have a redemption value equal to the aggregate value of the NAV per unit of the redeemed units on the last day of the month on which NYSE Arca is open for trading in the month during which the redemption request is processed. Certain expenses described below will be subtracted from the value of the redeemed units and the resulting amount the unitholder will receive (the “Redemption Amount”). The amount of physical platinum and palladium bullion a redeeming unitholder is entitled to receive will be determined by the Manager, who will allocate the Redemption Amount to physical platinum and palladium bullion in direct proportion to the value of physical platinum and palladium bullion held by the Trust at the time of redemption (the “Bullion Redemption Amount”). The quantity of each particular metal delivered to a redeeming unitholder will be dependent on the applicable Bullion Redemption Amount and the sizes of plates and ingots of that metal that are held by the Trust on the redemption date. A redeeming unitholder may not receive physical platinum and palladium bullion in the proportions then held by the Trust and, if the Trust does not have a Good Delivery plate or ingot, as the case may be, of a particular metal in inventory of a value equal to or less than the applicable

25

Bullion Redemption Amount, the redeeming unitholder will not receive any of that metal. Because the Trust’s physical platinum bullion will be stored at the Mint in Canada and the Trust’s physical palladium bullion will be stored at Loomis in London or Zurich, in the event of a redemption, the physical platinum bullion and the physical palladium bullion the redeeming unitholder will receive will be shipped separately.

Any Bullion Redemption Amount in excess of the value of the Good Delivery plates or ingots, as the case may be, of the particular metal to be delivered to the redeeming unitholder will be paid in cash, as such excess amount will not be combined with any excess amounts in respect of the other metal for the purpose of delivering additional physical platinum and palladium bullion. A unitholder redeeming units for physical platinum and palladium bullion will be responsible for expenses incurred by the Trust in connection with such redemption. These expenses include expenses associated with the handling of the written notice of the unitholder’s intention to redeem units for physical platinum and palladium bullion (the “Bullion Redemption Notice”), the delivery and transportation of physical platinum and palladium bullion for units that are being redeemed, the applicable fees charged by the Mint or any sub-custodian, including but not limited to platinum and palladium storage in-and-out fees, and administrative charges, and applicable taxes, including, without limitation, harmonized sales tax (“HST”) or federal goods and services tax (“GST”) and any provincial sales tax, including Quebec sales tax (“PST”) associated with the importation, or delivery and transportation, of physical palladium bullion to a location in Canada and any PST applicable to physical platinum bullion being brought by or on behalf of such redeeming unitholder into any province which imposes PST on such bullion. Costs associated with the redemption of units and the delivery and transportation of physical platinum and palladium bullion will be borne by the redeeming unitholder, and current rates are estimated to be approximately $0.50 per troy ounce of platinum and $5.00 per troy ounce of palladium in connection with delivery to addresses in the continental United States and Canada. The fee per troy ounce could differ depending on the delivery location. Also, the redeeming unitholder will be responsible for reimbursing the Trust for fees charged to the Trust by the Mint, currently approximately $4.00 per plate or ingot of physical platinum bullion and approximately $0.30 per kilogram (with a minimum of $40.00 per shipment) for physical palladium bullion.

From inception to December 31, 2020, 21,983,771 units have been redeemed for physical platinum and palladium bullion.

Procedure to Redeem for Physical Platinum and Palladium Bullion

A unitholder that owns a sufficient number of units who desires to exercise redemption privileges for physical platinum and palladium bullion must do so by instructing his, her or its broker, who must be a direct or indirect participant of CDS Clearing and Depository Services Inc. (“CDS”) or The Depository Trust Company (“DTC”), to withdraw such position with CDS or DTC, as applicable, and to deliver to the transfer agent on behalf of the unitholder a written notice (the “Bullion Redemption Notice”), of the unitholder’s intention to redeem units for physical platinum and palladium bullion (the registrar and transfer agent of the Trust is permitted to directly accept redemption requests pursuant to the Exemptive Relief. See “Exemptions and Approvals”). If a unitholder desires to redeem units for bullion, and such unitholder holds his, her or its units through DRS, the holder first has to request and then receive a unit certificate before engaging in the redemption process. A Bullion Redemption Notice must be received by the Trust’s transfer agent no later than 4:00 p.m., Toronto time, on the 15th day of the month in which the Bullion Redemption Notice will be processed or, if such day is not a business day, then on the immediately following day that is a business day. Any Bullion Redemption Notice received after such time will

26

be processed in the next month. Any Bullion Redemption Notice must include a valid signature guarantee to be deemed valid by the Trust.

Except as provided under “Redemption of Units – Suspension of Redemptions” below, by delivering to the Trust’s transfer agent a Bullion Redemption Notice, the unitholder will be deemed to have irrevocably surrendered his, her or its units for redemption and appointed such broker to act as his, her or its exclusive settlement agent with respect to the exercise of such redemption privilege and the receipt of payment in connection with the settlement of obligations arising from such exercise.

Once a Bullion Redemption Notice is received by the Trust’s transfer agent, the transfer agent, together with the Manager, will determine whether such Bullion Redemption Notice complies with the applicable requirements including a minimum redemption of 25,000 units and contains delivery/transportation instructions that are acceptable to the armored service transportation carrier. If the Trust’s transfer agent and the Manager determine that the Bullion Redemption Notice complies with all applicable requirements, it will provide a notice to such redeeming unitholder’s broker confirming that such redemption notice was received and determined to be complete.

Any Bullion Redemption Notice delivered to the Trust’s transfer agent regarding a unitholder’s intent to redeem units that the transfer agent or the Manager, in their sole discretion, determines to be incomplete, not in proper form, not duly executed or for a minimum redemption of 25,000 units will for all purposes be void and of no effect, and the redemption privilege to which it relates will be considered for all purposes not to have been exercised thereby. If the Trust’s transfer agent and the Manager determine that the Bullion Redemption Notice does not comply with the applicable requirements, the transfer agent will provide a notice explaining the deficiency to the unitholder’s broker.

If the Bullion Redemption Notice is determined to have complied with the applicable requirements, the Manager will determine on the last business day of the applicable month the amount of physical platinum and palladium bullion and the amount of cash that will be delivered to the redeeming unitholder. Also on the last business day of the applicable month, the redeeming unitholder’s broker will deliver the redeemed units to the Trust’s transfer agent for cancellation.

The Manager has some discretion on the amount of physical platinum and palladium bullion the redeeming unitholder will receive based on the weight of plates and ingots owned by the Trust and the amount of cash necessary to cover the expenses associated with the redemption and delivery and transportation that must be paid by the redeeming unitholder. The amount of physical platinum and palladium bullion a redeeming unitholder may be entitled to receive will be determined by the Manager by allocating the Redemption Amount to physical platinum and palladium bullion in direct proportion to the value of physical platinum and palladium bullion held by the Trust at the time of redemption in addition to meeting the requirement for a minimum aggregate redemption amount. Once such determination has been made, the Trust’s transfer agent will inform the broker through which the unitholder has delivered its Bullion Redemption Notice of the proportionate amount of physical platinum and palladium bullion and cash that the redeeming unitholder will receive.

Based on instructions from the Manager, the Mint and/or the sub-custodian of the Mint will release the requisite amount of physical platinum and palladium bullion from such custodian or sub-custodian’s custody to the armored transportation service carrier, and such release shall constitute delivery of such physical platinum and palladium bullion by the Trust to the redeeming unitholder and the payment of the portion of the applicable Bullion Redemption Amount that is to be paid in

27

physical platinum and palladium bullion. See “Redemption of Units – Redemptions for Physical Platinum and Palladium Bullion – Transporting Physical Platinum and Palladium Bullion to the Redeeming Unitholder”. As directed by the Manager, any cash to be received by a redeeming unitholder in connection with a redemption of units for physical platinum and palladium bullion will be delivered or caused to be delivered by the Manager to the unitholder’s account within 10 business days after the month in which the redemption is processed. The Trust is permitted to pay the redemption price later than three business days after calculating the NAV per unit pursuant to the Exemptive Relief. See “Exemptions and Approvals”.

Transporting Physical Platinum and Palladium Bullion to the Redeeming Unitholder