UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

For the fiscal year ended December 31 , 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

Commission file number 001-36103

(Exact name of Registrant as specified in its charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (IRS Employer Identification No.) | ||||

( | |||||

| (Address of Principal Executive Offices and Zip Code) | Registrant's telephone number, including area code | ||||

Securities registered pursuant to Section 12(g) of the Securities Exchange Act: Common Stock, $.001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer o

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. Yes ☐ No ý

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to (§240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).Yes ☐ No ý

As of June 30, 2023, the last day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting and non-voting common equity held by non-affiliates was: $14,886,556 . Solely for purposes of this disclosure, shares of common stock held by executive officers and directors of the registrant as of such date have been excluded because such persons may be deemed to be affiliates. This determination of executive officers and directors as affiliates is not necessarily a conclusive determination for any other purposes.

As of March 25, 2024, 24,850,261 shares of common stock, $.001 par value per share, of the registrant were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required for Part III of this Annual Report on Form 10-K is incorporated by reference to Tecogen Inc.'s definitive proxy statement for its 2024 Annual Meeting of Stockholders which will be filed with the Securities and Exchange Commission ("SEC") pursuant to Regulation 14A under the Securities Act of 1934, as amended, within 120 days following its fiscal year ended December 31, 2023.

CAUTIONARY NOTE CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the documents incorporated herein by reference contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (“Securities Act”), Section 21E of the Securities Exchange Act of 1934, as amended (“Securities Exchange Act”), the Private Securities Litigation Reform Act of 1995 and other federal securities laws that involve a number of risks and uncertainties. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “anticipates,” “believes,” “contemplates,” “continues,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “predicts,” “pro forma,” “potential” “seeks,” “should,” “target,” or other variations thereof (including their use in the negative), or by discussions of strategies, plans or intentions. All statements, other than statements of historical fact, included in this report regarding our strategy, future operations, future financial position, future revenues, projected costs, prospects and plans and objectives of management are forward-looking statements.

The outcome of the events described in these forward-looking statements is subject to known and unknown risks, uncertainties and other factors that may cause us, our customers’ or our industry’s actual results, levels of activity, performance or achievements expressed or implied by these forward-looking statements to differ. See "Item 1A. Risk Factors," "Item 7.Management's Discussion and Analysis of Financial Condition and Results of Operations," and "Item 1. Business," as well as other sections in this report that discuss some of the factors that could contribute to these differences.

In addition, such forward-looking statements are necessarily dependent upon assumptions and estimates that may prove to be incorrect. Although we believe that the assumptions and estimates reflected in such forward-looking statements are reasonable, we cannot guarantee that our plans, intentions, or expectations will be achieved. The information contained in this report, including the section discussing risk factors, identify important factors that could cause such differences.

The cautionary statements made in this report are intended to be applicable to all related forward-looking statements wherever they appear in this report. The forward-looking statements made in this Annual Report on Form 10-K relate only to events as of the date on which the statements are made. Except as required by law, we undertake no obligation to update or release any forward-looking statements as a result of new information, future events, or otherwise, and assume no obligation to update the reasons why actual results could differ materially from those anticipated in such forward-looking statements.

This report also contains or may contain market data related to our business and industry and any such market data may include projections that are based on certain assumptions. If these assumptions turn out to be incorrect, actual results may differ from the projections based on these assumptions. As a result, our markets may not grow at the rates projected by this data, or at all. The failure of these markets to grow at these projected rates may have a material adverse effect on our business, results of operations, financial condition, and the market price of our common stock.

TECOGEN INC.

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2023

TABLE OF CONTENTS

PART I | ||||||||

Item 1. | Business. | |||||||

| Item 1A. | Risk Factors. | |||||||

| Item 1B. | Unresolved Staff Comments. | |||||||

| Item 1C. | Cybersecurity Risk Management. | |||||||

| Item 2. | Properties. | |||||||

| Item 3. | Legal Proceedings. | |||||||

| Item 4. | Mine Safety Disclosures. | |||||||

| PART II | ||||||||

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. | |||||||

| Item 6. | [Reserved]. | |||||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. | |||||||

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk. | |||||||

| Item 8. | Financial Statements and Supplementary Data. | |||||||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. | |||||||

| Item 9A. | Controls and Procedures. | |||||||

| Item 9B. | Other Information. | |||||||

| Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections. | |||||||

| PART III | ||||||||

| Item 10. | Directors, Executive Officers and Corporate Governance. | |||||||

| Item 11. | Executive Compensation. | |||||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | |||||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence. | |||||||

| Item 14. | Principal Accounting Fees and Services. | |||||||

| PART IV | ||||||||

| Item 15. | Exhibits and Financial Statement Schedules. | |||||||

| Item 16. | Form 10-K Summary. | |||||||

| SIGNATURES | ||||||||

TECOGEN INC.

PART 1

Item 1. Business

The Company

Tecogen Inc. (together with its subsidiaries, “we,” “our,” or “us,” or “Tecogen”) designs, manufactures, markets, and maintains high efficiency, ultra-clean cogeneration products. These include natural gas engine driven combined heat and power (CHP) systems and chillers for multi-family residential, commercial, recreational and industrial use. We are known for products that provide customers with substantial energy savings, resiliency from utility power outages and for significantly reducing a customer’s carbon footprint. Our products are sold with our patented Ultera® emissions technology which nearly eliminates all criteria pollutants such as nitrogen oxide ("NOx") and carbon monoxide ("CO"). We developed Ultera® for other applications including stationary engines and forklifts. We were incorporated in the State of Delaware on September 15, 2000.

We have wholly-owned subsidiaries American DG Energy, Inc. ("ADGE") and Tecogen CHP Solutions, Inc., and we own a 51% interest in American DG New York, LLC ("ADGNY"), a joint venture. ADGE and ADGNY distribute, own, and operate clean, on-site energy systems that produce electricity, hot water, heat and cooling. ADGE and ADGNY own the equipment that is installed at customers' facilities and sell the energy produced to the customer on a long-term contractual basis.

Our operations are comprised of three business segments:

•our Products segment, which designs, manufactures and sells industrial and commercial cogeneration systems;

•our Services segment, which provides operations and maintenance ("O&M") services for our products under long term service contracts, and

•our Energy Production segment, which installs, operates and maintains distributed generation electricity systems that we own and sells energy generated by such systems in the form of electricity, heat, hot water and cooling to our customers under long-term energy sales agreements.

The majority of our customers are located in regions with the highest utility rates, typically California, the Midwest and the Northeast.

Recent Developments

Assumption of Aegis Energy Services Maintenance Agreements

On March 15, 2023, we entered into an agreement ("Agreement") with Aegis Energy Services, LLC (“Aegis”) pursuant to which Aegis agreed to assign to us and we agreed to assume certain Aegis maintenance agreements, we agreed to purchase certain assets, and related matters (“Acquisition”). On April 1, 2023, the Acquisition closed. Under the Agreement, we agreed to acquire from Aegis and assume Aegis' rights and obligations arising on or after April 1, 2023 under maintenance agreements pursuant to which Aegis provided maintenance services for approximately 200 cogeneration systems, and acquired certain vehicles and inventory used by Aegis in connection with the performance of such maintenance services, and, following closing hired eight (8) Aegis employees to provide services with respect to such maintenance agreements. At closing, we acquired eight (8) Aegis vehicles for consideration consisting of $170,000 in cash. Also, we issued credits against outstanding accounts receivable due from Aegis in the amount of $300,000 for the acquisition of inventory that Aegis used to provide maintenance services. On February 1, 2024, Tecogen and Aegis amended the Agreement to add eighteen (18) additional maintenance contracts (the "Amendment"). The Amendment includes an undertaking by Aegis to use commercially reasonable efforts to support and assist our execution of maintenance service agreements for an additional thirty-six (36) cogeneration units sold to customers by Aegis. See Note 5."Aegis Contract and Related Asset Acquisition" of the Notes to the Consolidated Financial Statements.

Tecochill Hybrid-Drive Air-Cooled Chiller Development

During the third quarter of 2021 we began development of the Tecochill Hybrid-Drive Air-Cooled Chiller. We recognized that there were many applications where the customer wanted an easy to install roof top chiller. Using the inverter design from our InVerde e+ cogeneration module, the system can simultaneously take two inputs, one from the grid or a renewable energy source and one from our natural gas engine. This allows a customer to seek the optimum blend of operational cost savings and greenhouse gas benefits while providing added resiliency from two power sources. We introduced the Tecochill Hybrid-Drive Air-Cooled Chiller at the AHR Expo in February 2023 and received an order on February 8, 2024 for three hybrid-drive air-cooled chillers for a utility in Florida. A patent application based on this concept has been filed with the US Patent and Trademark Office.

1

TECOGEN INC.

Controlled Environment Agriculture

On July 20, 2022, we announced our intention to focus on opportunities for low carbon Controlled Environment Agriculture ("CEA"). We believe that CEA offers an exciting opportunity to apply our expertise in clean cooling, power generation, and greenhouse gas reduction to address critical issues affecting food and energy security. We propose to address this challenge by developing a highly efficient energy solution for CEA grown produce using our cogeneration products in conjunction with solar energy generation, energy storage, and other technologies.

CEA facilities enable multiple crop cycles (15 to 20 cycles) in one year compared to one or two crop cycles in conventional farming. In addition, growing produce close to the point of sale reduces food spoilage during transportation. Food crops grown in greenhouses typically have lower yields per square foot than in CEA facilities, and the push to situate facilities close to consumers in cities requires minimizing land area and maximizing yield per square foot. Yields are increased in CEA facilities by supplementing or replacing natural light with grow lights in a climate-controlled environment - which requires significant energy use.

In recent years our cogeneration equipment has been used in numerous cannabis cultivation facilities because our systems significantly reduce operating costs, reduce the facility GHG footprint and offer resiliency to grid outages. Our experience providing clean energy solutions to cannabis cultivation facilities has given us significant insight into requirements relating to energy-intensive indoor agriculture applications that we expect to be transferable to CEA facilities for food production.

Impact of the Russian Invasion of Ukraine

Presently, we have no operations or customers in Russia or the Ukraine. The higher energy prices for natural gas as a result of the war may affect the performance of our Energy Production Segment. However, we have also seen higher electricity prices as much of the electricity production in the United States is generated from fossil fuels. If the electricity prices continue to rise, the economic savings generated by our products are likely to increase. In addition to the direct result of changes in natural gas and electricity prices, the war in Ukraine may result in higher cybersecurity risks, increased or ongoing supply chain challenges, and volatility related to the trading prices of commodities.

Overview of Our Business

Products

Our products offer customers energy savings, resiliency and a cleaner environmental footprint. Our cogeneration, chiller and heat pump systems use an engine to generate electricity or shaft work and recover the waste heat from the engine. Our systems are greater than 88% efficient compared to typical electrical grid efficiencies of 40% to 50%. As a result, our greenhouse gas (GHG) emissions are typically half that of the electrical grid. Our systems generate electricity and hot water or in the case of our Tecochill product, both chilled water and hot water. Our products are expected to run on Renewable Natural Gas (RNG) as it is introduced into the US gas pipeline infrastructure.

Our natural gas-powered cogeneration systems (also known as combined heat and power or “CHP”) are efficient because they drive electric generators or compressors, which reduce the amount of electricity purchased from the utility while recovering the engine’s waste heat for water heating, space heating, and/or air conditioning at the customer’s building.

Our commercial product lines include:

•the InVerde e+® and TecoPower® cogeneration units; these systems supply electricity and hot water;

•Tecochill® air-conditioning and refrigeration chillers; these systems produce chilled water and hot water;

•Tecochill® hybrid-drive air-cooled chiller; gas engine-driven chillers that provide air conditioning and hot water;

•Tecofrost® gas engine-driven refrigeration compressors; these systems circulate refrigerant and provide hot water as a byproduct; and,

•Ultera® emissions control technology.

Traditional customers for our InVerde and Tecopower products have a simultaneous need for electrical power and hot water. These include hospitals, nursing homes, schools, universities, health clubs, spas, hotels and motels, office and multi-unit residential buildings. Conversely our Tecochill product benefits customers who have a simultaneous need for cooling and hot water which is typical in sites such as hospitals, ice rinks, indoor agriculture and food processing. Our Tecofrost refrigeration compressors are applied primarily to industrial applications that include cold storage, wineries, dairies, ice rinks and food processing. Market drivers include the price of natural gas, local electricity rates, environmental regulations, and governmental energy policies, as well as customers’ desire to become more environmentally responsible.

2

TECOGEN INC.

Our cooling and refrigeration products provide both cooling and make use of high grade waste heat. This is of particular advantage in facilities that control both temperature and humidity. In such facilities, climate control is achieved by cooling the facility to remove humidity and then reheating to the required temperature. Using engine waste heat to perform the reheat while utilizing natural gas to generate the cooling provides significant economic and environmental benefits. As a result our product has significant competitive advantages in applications that operate year round such as controlled environment agriculture, indoor ice rinks, and hospitals.

Through our factory service centers in California, Connecticut, Florida, Massachusetts, Michigan, New Jersey, New York, and Ontario, our specialized technical staff maintains our products via long-term service contracts. To date we have shipped over 3,200 units, some of which have been operating for almost 35 years. We established a service center in Toronto, Canada in August 2020 to support our existing population of chillers and cogeneration units including 26 cogeneration units sold in this territory during 2020 to serve public housing facilities.

In 2009, in response to the changing regulatory requirements for stationary engines, our research team developed an economically feasible process for removing air pollutants from engine exhaust. This technology's U.S. and foreign patents were granted beginning in October 2013 and other domestic and foreign patents granted or applications are pending. Branded Ultera®, the ultra-clean emissions technology repositions our engine driven products in the marketplace, making them comparable environmentally with other technologies such as fuel cells, but at a much lower cost and greater efficiency. In 2018, a group of natural gas engine-generators fitted with the Ultera system were successfully permitted in the Los Angeles region for unrestricted operation, the first natural gas engines to do so without operating time limits or other exemption. These engines were permitted to levels matching the California Air Resources Board ("CARB") stringent 2007 emissions requirements, the same emissions standard used to certify fuel cells, and the same emissions levels as a state-of-the-art central power plant. We now offer our Ultera emissions control technology as an option on all our products or as a stand-alone application for retrofitting other rich-burn spark-ignited reciprocating internal combustion engines such as the engine-generators described above.

Our products are designed as compact modular units that are intended to be installed in multiples. This approach has significant advantages over utilizing a single larger cogeneration or chiller unit, allowing placement in constrained urban settings and redundancy to mitigate service outages. Redundancy is particularly relevant in regions where the electric utility has formulated tariff structures that include high “peak demand” charges. Such tariffs are common in many areas of the country, and are applied by such utilities as Southern California Edison, Pacific Gas and Electric, Consolidated Edison of New York, and National Grid of Massachusetts. Because these tariffs are assessed based on customers’ peak monthly demand charge over a very short interval, typically only 15 minutes, a brief service outage for a system comprised of a single unit can create a high demand charge, and therefore be highly detrimental to the monthly savings of the system. For multiple unit sites, the likelihood of a full system outage that would result in a high demand charge is dramatically reduced, consequently, these customers have a greater probability of capturing peak demand savings.

Our products are sold directly to customers by our in-house marketing team, and by established independent sales agents and representatives.

Our operations are comprised of three business segments. Our Products segment designs, manufactures and sells industrial and commercial cogeneration systems as described above. Our Services segment provides O&M services for our products under long term service contracts. Our Energy Production segment sells energy in the form of electricity, heat, hot water and cooling to our customers under long-term sales agreements.

Ultera Low-Emissions Technology

All of our CHP products are available with the patented Ultera® low-emissions technology as an equipment option. This breakthrough technology was developed in 2009 and 2010 as part of a research effort partially funded by the California Energy Commission and Southern California Gas Company.

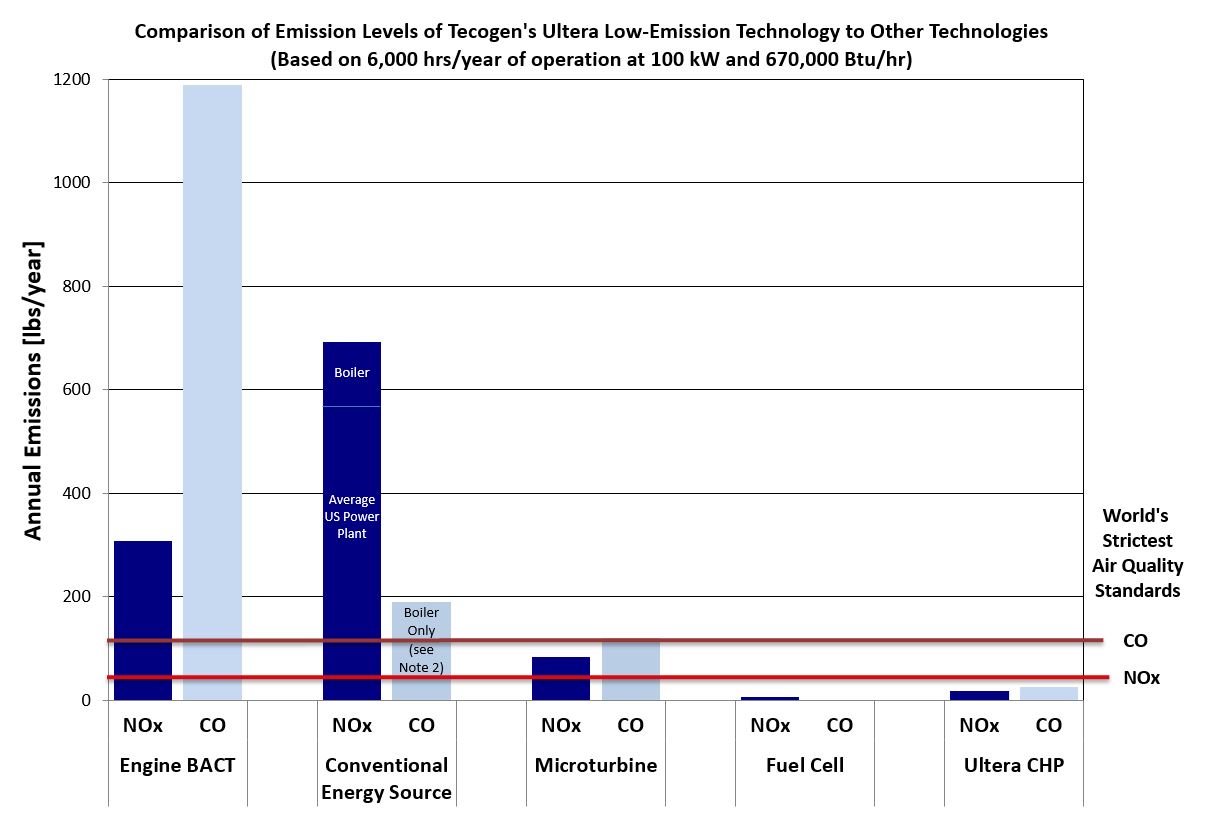

The chart below compares emission levels of our Ultera technology to other technologies. As of December 31, 2023, our Ultera CHP and fuel cell technologies are the only technologies that we know of which comply with California's air quality standards for CO and NOx, represented in the chart by the colored horizontal lines, shown as the world's strictest air quality standards on the lower right of the chart. We believe that as environmental regulation becomes more stringent in the United States, our emissions technology may be used in markets including generators, fork trucks and biogas engines.

3

TECOGEN INC.

(5) (2) (4) (4) (3) (1)

(1) California has the strictest air quality standards for engines in the world

(2) Conventional Energy Source is U.S. power plant and gas boiler. Average U.S. power plant NOx emission rate of 0.9461 lb/MWh from (USEPA eGrid 2012),

CO data not available. Gas boiler efficiency of 78% (www.eia.gov) with emissions of 20 ppm NOx @ 3% O2 (California Regulation SCAQMD Rule 1146.2

and <50 ppmv CO @ 3% O2 (California Regulation SCAQMD BACT).

(3) Tecogen emissions based upon actual third party source test data.

(4) Microturbine and Fuel Cell emissions from EPA CHP Partnership - Catalog of CHP Technologies- March 2015.

(5) Stationary Engine BACT as defined by SCAQMD.

After successfully developing the Ultera technology for our own equipment, our research and development team began exploring other possible emissions control applications in an effort to expand the market for the ultra-clean emissions system. Retrofit kits were developed in 2014 for other stationary engines and in 2015 the Ultera Retrofit Kit was applied successfully to natural gas stand-by generators from other manufacturers, including Generac and Caterpillar.

Historically, standby generators have not been subjected to the strict air quality emissions standards of traditional power generation. However, generators which run for more than 200 hours per year or run for non-emergency purposes (other than routine scheduled maintenance) in some territories are subject to compliance with the same stringent regulations applied to a typical electric utility. As demand response programs become more economically attractive and air quality regulations continue to become more stringent, there could be increased demand for retrofitting standby generators with our Ultera® emissions control technology, thus providing a cost-effective solution to keeping the installed base of standby generators operational and in compliance with regulatory requirements.

In 2017, a group of generators owned by a single customer in Southern California were supplied Ultera kits because of their particular requirement to exceed the 200-hour annual limit. These units are now operational and have been tested by the customer and shown to be compliant with the local pollution limits which we believe to be the strictest anywhere in the United States, and potentially the world. Our CHP products have been permitted to this same standard. However, CHP products are

4

TECOGEN INC.

given a heat credit which effectively increases the allowable limit. In 2018, permitting was completed making these certification levels the lowest we have achieved. We believe no other engines have been certified to these levels since the current regulations in the Los Angeles region became effective.

It is noteworthy that these engine-generators have been used in California to power dispersed loads in a fire-prone area where frequent de-energizing of the electric overhead power lines is required for safety. We believe this application to be a new and significant application for the Ultera technology in light of the widely publicized widespread outages in California which have occurred in recent years.

Services

We provide long-term maintenance contracts, parts sales, and turnkey installation for our products through a network of eleven well-established field service centers in California, the Midwest, the Northeast, the Southeast and in Ontario, Canada. These centers are staffed by our full-time technicians, working from local leased facilities. The facilities provide office and warehouse space for inventory. We encourage our customers to provide internet connections to our units so that we may maintain remote monitoring and communications with the installed equipment. For connected installations, the machines are contacted daily to download their status and provide regular operational reports (daily, monthly, and quarterly) to our service managers. This communications link is used to support the diagnostic efforts of our service staff, and to send messages to pre-programmed phones if a unit has experienced an unscheduled shutdown. In many cases, communications received by service technicians from connected devices allow for proactive maintenance, minimizing equipment downtime and improving operating efficiency for the customer.

The work of our service managers, supervisors, and technicians focuses on our products. Because we manufacture our own equipment, our service technicians bring hands-on experience and competence to their jobs. They are trained at our corporate headquarters and primary manufacturing facility in Waltham, Massachusetts.

Most of our service revenue is in the form of annual service contracts, which are typically of an all-inclusive “bumper-to-bumper” type, with billing amounts proportional to the equipment's achieved operating hours for the period. Customers are thus invoiced in level, predictable amounts without unforeseen add-ons for such items as unscheduled repairs or engine replacements. We strive to maintain these contracts for many years, and work to maintain the integrity and performance of our equipment.

Our products have a long history of reliable operation. Since 1995, we have had a remote monitoring system in place that connects to hundreds of units daily and reports their “availability,” which is the amount of time a unit is running or is ready to run. More than 80% of the units operate above 90% availability, with the average being 93.8%. Our factory service agreements have directly impacted these positive results and represent an important long-term annuity-like stream of revenue for us.

New equipment sold beginning in 2016 and select upgrades to the existing installed equipment fleet include industrial internet solution which enables us to collect, analyze, and manage valuable asset data continuously and in real-time. This provides the service team with improved insight into the functionality of our installed CHP fleet. Specifically, it enables the service department to perform remote monitoring and diagnostics and to view system results in real time via a computer, smart phone or tablet. Consequently, we can better utilize monitoring data ensuring customers are capturing maximum possible savings and efficiencies from their cogeneration equipment.

Energy Production

Our Energy Production segment sells energy in the form of electricity, heat, hot water and cooling to our customers under long-term sales agreements which represented 7.0% of our consolidated revenues for the years ended December 31, 2023 and 2022. See Note 18. "Segments" of the Notes to the Consolidated Financial Statements.

Sales & Distribution

Our products are sold directly to end-users by our sales team and by established independent sales agents and representatives. We have agreements with manufacturers' representatives and outside sales representatives who are compensated by commissions for designated territories and product lines. During the years ended December 31, 2023 and December 31, 2022, no customer accounted for more than 10% of our revenues. We typically sell our chiller products through our manufacturing representatives with assistance from our internal sales team. Our combined heat and power products are typically sold direct to end customers by our internal sales team.

Markets and Customers

Worldwide, stationary power generation applications vary from huge central stationary generating facilities (traditional electric utility providers) to back-up generators as small as 2 kW. Historically, power generation in most developed countries such as the United States has been part of a regulated central utility system utilizing high-temperature steam turbines powered

5

TECOGEN INC.

by fossil-fuels. This turbine technology, though steadily refined over the years, reached a maximum efficiency (where efficiency means electrical energy output per unit of fuel energy input) of approximately 40% to 50%.

A number of developments related primarily to the deregulation of the utility industry as well as significant technological advances have now broadened the range of power supply choices available to all types of customers. Cogeneration, which harnesses waste energy from power generation processes and puts it to work for other uses on-site, can boost the energy conversion efficiency to nearly 90%, a better than two-fold improvement over the average efficiency of a fossil fuel plant. This distributed generation, or power generated on-site at the point of consumption rather than power generated centrally, eliminates the cost, complexity, and inefficiency associated with electric transmission and distribution. The implications of the CHP distributed generation approach are significant. We believe that if cogeneration were applied on a large scale, global fuel usage might be dramatically curtailed and the utility grid made far more resilient. Furthermore, with technology we have introduced, like the Ultera low-emissions technology, our products can now contribute to better air quality level while complying with the strictest air quality regulations in the United States.

We estimate that our products can often reduce the customer’s operating costs (for the portion of the facility loads to which they are applied) by approximately 30% to 60%, which provides an excellent rate of return on the equipment’s capital cost in many areas of the country with high electricity rates. Our chillers are especially suited to regions where utilities impose extra charges during times of peak usage, commonly called “demand” charges. In these cases, the gas-fueled chiller reduces the use of electricity during the summer, the costliest time of year.

Decentralizing power generation or reducing energy requirements at a customer's site not only relieves the capacity burden on existing power plants, but also lessens the burden on transmission and distribution lines. This ultimately improves the grid’s reliability and reduces the need for costly upgrades.

Increasingly favorable economic conditions may improve our business prospects domestically and abroad. Specifically, we believe that natural gas prices are expected to increase from their current values, and that electric rates are expected to continue to rise more significantly over the long-term as utilities pay for grid expansion, better emission controls, efficiency improvements, and the integration of renewable power sources.

Most potential new customers in the U.S. require less than 1 MW of electric power and less than 1,200 tons of cooling capacity. We are targeting customers in states with high electricity rates in the commercial sector, such as California, Connecticut, Massachusetts, New Hampshire, New Jersey, and New York. Most of these states also have high peak demand rates, which favor utilization of our modular units in groups so as to assure redundancy and peak demand savings. Governmental agencies in some of these regions may also provide generous rebates that can improve the economic viability of our systems.

The Inflation Reduction Act of 2022 increased Federal tax credits, including the investment tax credit (ITC), to up to thirty percent (30%) of the project cost for projects incorporating certain low emission technologies, including CHP equipment, that begin construction before January 1, 2025 and provides for an additional ten percent (10%) credit if the taxpayer satisfies additional requirements relating to domestic content. State and local governments and tax-exempt entities may also benefit from certain tax credits through direct payments or transfers of tax credits to unrelated third parties. This particular new direct pay option is especially impactful given the fact that many ideal facilities for CHP systems are not-for-profit, including many healthcare and hospital facilities, schools and universities, as well as recreation centers. These customers historically have not been able to benefit from previous iterations of the ITC. Under the federal definition for CHP systems, all of our products, including our air-conditioning and cooling models (Tecochill and Tecofrost) qualify for the tax credit when heat recovery is incorporated into the system design.

We aggressively market to potential customers where utility pricing aligns with our advantages. These areas include regions that have strict emissions regulations, such as California, or those that reward CHP systems that are especially non-polluting, such as New Jersey. Currently, more than 23 states recognize CHP as part of their Renewable Portfolio Standards or Energy Efficiency Resource Standards.

The traditional markets for CHP systems are buildings with long hours of operation and with corresponding demand for electricity or cooling and heat. Traditional customers for our cogeneration systems include controlled environment agriculture, hospitals, nursing homes, colleges, universities, health clubs, spas, hotels, motels, office and retail buildings, food and beverage processors, multi-unit residential buildings, laundries, ice rinks, swimming pools, factories, municipal buildings, and military installations.

Traditional customers for our chillers, refrigeration compressors and heat pumps overlap with those for our cogeneration systems. Engine-driven chillers are often used as replacements for aging electric chillers because they both occupy similar amounts of floor space and require similar maintenance schedules. This is also the case with refrigeration compressors.

6

TECOGEN INC.

Competition

The markets for our products are highly competitive, though we believe that we offer customers a suite of premier best-in-class clean energy and thermal solutions.

InVerde and Tecopower

Our combined heat and power products that produce electricity and hot water compete with the utility grid, existing technologies such as other reciprocating engine and microturbine CHP systems, and other emerging distributed generation technologies including solar power, wind-powered systems, and fuel cells. Our products are highly competitive between 60KW and 1.5MW in electrical generation capacity. In this size range we have other reciprocating engine competitors, although we have strong competitive advantages when it comes to ease of utility interconnection, ease of installation in tight spaces and our microgrid capabilities. We believe that Capstone Turbine Corporation is the only microturbine manufacturer with a commercial presence in CHP.

Although operating solar and wind powered systems produce no emissions, the main drawbacks to these renewable powered systems are their dependence on weather conditions, their reliance on backup utility grid-provided power, and high capital costs that can often make these systems uneconomical without government subsidies. Similarly, while the market for fuel cells is still developing, a number of fuel cell companies are focused on markets similar to ours. Fuel cells, like solar and wind powered systems, have received higher levels of incentives for the same type of applications as CHP systems in many territories. We believe that, notwithstanding these higher government incentives, our CHP solutions provide a better value and more robust solution to end users in most applications.

Additionally, our patents relating to the Ultera ultra-low emissions technology give our products a strong competitive advantage in markets where severe emissions limits are imposed or where very clean power is favored, such as New Jersey, California, and Massachusetts.

Overall, we compete with end users’ other options for electrical power, heating, and cooling on the basis of our technology’s ability to:

•Provide a more efficient solution that provides operational savings for a facility's energy needs including cooling, electricity and hot water;

•Provide power when a utility grid is not available or goes out of service;

•Reduce emissions of criteria pollutants (NOx and CO) to near-zero levels and cut the emission of greenhouse gases such as carbon dioxide due to increased efficiencies compared to the electric grid;

•Provide reliable on-site power generation, heating and cooling services.

We believe that no other company has developed a product that provides the features and benefits provided by our inverter-based InVerde e+, which offers UL-certified grid connection and sophisticated off-grid and microgrid capabilities. An inverter-based product with at least some of these features has been introduced by others, but we believe that they face serious challenges in duplicating all the unique features of the InVerde e+. Competitors' product development time and costs could be significant. We have exclusive license rights to Microgrid algorithms developed by the University of Wisconsin researchers. We have exclusive rights for engine-driven systems utilizing natural gas or diesel fuel in the application of power generation where the per-unit output is less than 500kW. The software allows our products to be integrated as a Microgrid, where multiple InVerde e+® units can be seamlessly isolated from the main utility grid in the event of an outage and re-connected to it afterward. We expect that our patents and license for Microgrid software will deter others from offering certain important functions. See "Business-Intellectual Property."

Similarly, in the growing Microgrid segment, neither fuel cells nor microturbines can respond to changing energy loads when the system is disconnected from the utility grid. Engines such as those used in our equipment inherently have a fast-dynamic response to step load changes, which is why they are the primary choice for emergency generators. Fuel cells and microturbines require additional energy storage systems to be utilized for time-limited off-grid operation, giving our engine-driven solutions an advantage for Microgrid and resiliency applications.

Tecochill Chillers

Our Tecochill line of chillers are the only gas-engine-driven chillers available on the market. Natural gas can also fuel absorption chillers, which use fluids to transfer heat without an engine drive. However, engine driven chillers continue to have an efficiency advantage over absorption machines. Tecochill chillers reach efficiencies well above levels achieved by similarly sized absorption systems. Low natural gas prices in the United States improve the economics of natural gas-fueled chillers while their minimal electric demand on backup power systems make them ideal for facilities requiring critical precision climate control. In 2023 we expanded our Tecochill range of products with the introduction of a hybrid air cooled chiller based on the inverter design used in the InVerde. The hybrid-drive air-cooled chiller will take simultaneous inputs from the electrical grid

7

TECOGEN INC.

and the natural gas engine so that it can operate with the lowest cost and/or greenhouse gas footprint at any time based on changing conditions.

Research & Development

Our long and rich research and development tradition and sustained programs have allowed us to cultivate deep engineering expertise. We have strong core technical knowledge that is critical to product support and continuous product improvement efforts. Our TecoDrive engine, permanent magnet generator, cogeneration and chiller products, InVerde, pumps, Ultera emissions control system, and our hybrid-drive air-cooled chiller were all created and optimized in-house with support from third-parties.

We continue to seek alliances with utilities, government agencies, universities, research facilities, and manufacturers. We have succeeded in developing new technologies and products in collaboration with several entities, including:

•Sacramento Municipal Utility District has provided test sites to us since 2010.

•Southern California Gas Company and San Diego Gas & Electric Company, each a Sempra Energy subsidiary, have granted us research and development contracts since 2004.

•Department of Energy’s Lawrence Berkeley National Laboratory, with whom we have had research and development contracts since 2005, including ongoing Microgrid development work related to the InVerde.

•Eastern Municipal Water District in Southern California has co-sponsored demonstration projects to retrofit both a natural-gas powered municipal water pump engine and a biofuel powered pumping station engine with the Ultera low emissions technology since 2012.

•Consortium for Electric Reliability Technology Solutions executed research and development contracts with us, and has provided a test site to us since 2005.

•California Energy Commission with whom we had a research and development contract from 2004 until March 2013.

•The AVL California Technology Center performed a support role in research and development contracts as well as internal research and development on our Ultera emission control system from August 2009 to November 2011. In addition, the Center supported our research on emissions from gasoline vehicles from January of 2016 through October 2017. AVL researchers collaborated with our engineers on several peer reviewed papers published by technology association SAE International in 2017 and 2018.

Certain components of our InVerde product were developed through a grant from the California Energy Commission. This grant includes a requirement that we pay royalties on all sales of all products related to the grant, which obligation expired in 2022. As of December 31, 2023, royalties accrued in accordance with this grant agreement were less than $10,000 on an annual basis.

We also continue to leverage our resources with government and industry funding, which has yielded a number of successful developments, including the Ultera low-emissions technology, sponsored by the California Energy Commission and Southern California Gas Company. Pursuant to the terms of the grants from the California Energy Commission, the California Energy Commission has a royalty-free, perpetual, non-exclusive license to these technologies for government purposes.

Our current internal R&D efforts are focused on the hybrid-drive air-cooled chiller that utilizes the basic inverter design used in the InVerde e+. Management believes that this chiller will address a significant market segment that is currently not addressed by our existing Tecochill product. For the years ended December 31, 2023 and 2022, we spent $840,011 and $732,873, respectively, on research and development activities.

Intellectual Property

Currently, we hold twelve United States patents for our technologies:

•10,774,720: “NOx Reduction Using a Dual-Stage Catalyst System with Intercooling in Vehicle Gasoline Engines under Real Driving Condition.” This patent, granted in September 2020, improves the removal of Non-Methane Organic Gases (NMOG) and Carbon Monoxide (CO) from vehicle emissions. The improved performance, consisting of up to 90% reductions in NMOG and CO results from increased oxidation of NMOG and CO due to a lower temperature environment in the second stage catalyst.

•10,774,724: “Dual Stage Internal Combustion Engine Aftertreatment System Using Exhaust Gas Intercooling and Charger Driven Air Ejector.” This patent, granted in September 2020, relates to the use of turbo

8

TECOGEN INC.

compressors and exhaust gas intercoolers in turbocharged engines to reduce the complexity and cost of Ultera emissions reduction systems.

•9,995,195: “Emissions control systems and methods for vehicles.” This patent, granted in June 2018, is a method for vehicle cold start to enhance the removal of CO and hydrocarbons emissions, which are extremely problematic for cold engines. Air is injected in the exhaust between the engine’s close-coupled catalyst and underbody catalyst. Once the engine is warmed (> 500 F exhaust) this air stream is shut off. This method synergizes well with the Ultera system by utilizing the injection air feed for an alternative purpose during engine start.

•9,956,526: “Poison-Resistant Catalyst and Systems Containing Same.” This patent, granted in May 2018, relates to a special catalyst formulation that is resistant to contaminant induced corrosion in conditions like those of the Ultera second stage. These poisons or contaminants are most commonly sulfur compounds.

•9,702,306: “Internal Combustion Engine Controller.” This patent granted in July of 2017 relates to the unique control methodology used in the InVerde e+ CHP unit that maximizes engine fuel economy under variable speed operation.

•9,470,126: "Assembly and method for reducing ammonia in exhaust of internal combustion engines." This patent, granted in October 2016, is related to the Ultera emission control system applicable to all our products.

•9,856,767: “Systems and methods for reducing emissions in exhaust of vehicles and producing electricity." This patent, filed in November 2015 and published in March 2016, relates to the development of the Ultera emission control system for vehicle applications.

•9,121,326: “Assembly and method for reducing nitrogen oxides, carbon monoxide and hydrocarbons in exhausts of internal combustion engines.” This patent, granted in September 2015, is related to the Ultera emission control system applicable to all our products.

•9,651,534: "Assembly and Method for reducing nitrogen oxides, carbon monoxide, hydrocarbons and hydrocarbon gas in exhausts of internal combustion engines and producing and electrical output." This patent granted in April 2017, is related to the Ultera emission control system applicable to all our products.

•8,578,704: “Assembly and method for reducing nitrogen oxides, carbon monoxide, and hydrocarbons in exhausts of internal combustion engines.” This patent, granted in November 2013, is for the Ultera emission control system applicable to all our products.

•7,243,017: “Method for controlling internal combustion engine emissions.” This patent, granted in July 2007, applies to the specific algorithms used in our engine controller for metering fuel usage to obtain the correct combustion mixture and is technology used by most of our engines.

•7,239,034: “Engine driven power inverter system with cogeneration.” This patent, granted in July 2007, pertains to the utilization of an engine-driven CHP module combined with an inverter and applies to our InVerde product specifically.

Our patents expire between 2024 and 2037.

In addition, we have licensed specific rights to Microgrid software algorithms developed by University of Wisconsin researchers for which we pay royalties to the assignee, The Wisconsin Alumni Research Foundation (WARF). Pursuant to U.S. Patent 7,116,010, titled “Control of small distributed energy resources”, granted in 2006 and expires on March 27, 2024. Our exclusive rights are for engine-driven systems utilizing natural gas or diesel fuel in the application of power generation where the per-unit output is less than 500 kW. The software allows our products to be integrated as a Microgrid, where multiple InVerde units can be seamlessly isolated from the main utility grid in the event of an outage and re-connected to it afterward. The licensed software allows us to implement such a Microgrid with minimal control devices and associated complexity and cost. We consider the Microgrid software algorithm licensed from WARF to be a key feature of our InVerde product, and one that would be difficult to duplicate outside the patent. We pay WARF a royalty for each cogeneration module sold using the licensed technology. Such royalty payments have been in the range of $5,000 to $15,000 on an annual basis through the year ended December 31, 2023. In addition, WARF reserved the right to grant non-profit research institutions and governmental agencies non-exclusive licenses to practice and use, for non-commercial research purposes, the technology developed by us that is based on the licensed software.

9

TECOGEN INC.

We consider our patents and licensed intellectual property to be important in the operation of our business. The expiration, termination, or invalidity of one or more of these patents may have a material adverse effect on our business.

One other company has developed a product that seeks to compete with our inverter-based InVerde, although it does not offer all of the same benefits and features offered by our InVerde products. We anticipate that an inverter-based product with at least some of the features offered by our InVerde products will be introduced by others, but we believe that our competitors will face serious challenges in duplicating the InVerde. Product development time and costs would likely be significant, and we expect that our patent for the inverter-based CHP system, U.S. Patent 7,239,034, provides significant protections for key features.

In 2013, we purchased rights to designs and technology, including patents granted or pending for our permanent magnet generators. A key component of our InVerde module uses this acquired technology.

Our patents for the Ultera low-emissions control technology applies to all our gas engine-driven products and may have applications to other rich-burn spark-ignited internal combustion engines. We have been granted patents for this technology in Europe, Australia, Brazil, Canada, Japan, Mexico, Korea and Singapore.

Copyrights

Our control software is protected by copyright laws or through an exclusive license agreement.

Trademarks

We have registered the brand names of our equipment and logos used on our equipment. These registered and pending trademarks include Tecogen, Tecochill, Tecopower, Ultera, InVerde, InVerde e+ and the associated logos. We will continue to trademark our product names and symbols.

We rely on treatment of our technology as trade secrets through confidentiality agreements, which our employees and vendors are required to sign. Also, we rely on non-disclosure agreements with others that have or may have access to confidential information to protect our trade secrets and proprietary knowledge.

Sourcing & Manufacturing

We are focused on continuously strengthening our manufacturing processes and increasing operational efficiencies. Many of the components used in the manufacture of our highly-efficient clean energy equipment are readily fabricated from commonly available raw materials or are standard available parts sourced from multiple suppliers. We believe that adequate supplies exist to meet our near to medium term manufacturing needs. We have an on-going focus on developing and implementing new systems to simplify our manufacturing processes, product sourcing methods, and our supply chain.

We have a combined total of approximately 27,000 square feet of manufacturing and warehouse space running on a single 5-day per week shift at our Waltham, Massachusetts facility. We believe we have sufficient spare capacity to meet near to medium term demand without incurring additional fixed costs. The lease for our headquarters located in Waltham, Massachusetts was extended on March 1, 2024 and expires on April 30, 2024.

On March 31, 2023, we entered into two lease agreements for two adjoining buildings, located in Billerica, Massachusetts, containing approximately 26,412 square feet of manufacturing, storage and office space to serve as our headquarters and manufacturing facilities. We have a total of approximately 21,000 square feet of manufacturing and warehouse space at the Billerica, Massachusetts facility. The lease agreements which commenced on January 1, 2024, provide for initial lease terms of five (5) years, expiring on December 31, 2028, with two successive options to renew for additional terms of five (5) years.

Government & Regulation

Several kinds of federal, state and local government regulations affect our products and services, including but not exclusive to:

•product safety certifications and interconnection requirements;

•air pollution regulations which govern the emissions allowed in engine exhaust;

•state and federal incentives for CHP technology;

•various local building and permitting codes and third-party certifications;

•electric utility pricing and related regulations; and

•federal and state laws regarding the legalization of cannabis for medicinal and recreational use.

10

TECOGEN INC.

Our markets can be positively or negatively impacted by the effects of governmental and regulatory matters. We are impacted not only by energy policy, laws, regulations and incentives of governments in the markets in which we sell, but also by rules, regulations and costs imposed by utilities. Utility companies or governmental entities may place barriers on the installation or interconnection of our products with the electric grid. Further, utility companies may charge additional fees to customers who install on-site power generation to reduce the electricity they take from the utility and to preserve electric capacity available from the grid for back-up or standby purposes. These types of restrictions, fees or charges could hamper the ability to install or effectively use our product or increase the cost to our potential customers for using our systems. This could make our systems less desirable, adversely impacting our revenue and profitability. In addition, utility rate reductions can make our products less competitive, causing a material adverse effect on our operations. These costs, incentives and rules are not always the same as those faced by technologies with which we compete.

Similarly, rules, regulations, laws and incentives could also provide an advantage to our distributed generation solutions as compared with competing technologies because they enable compliance in a lower cost, more efficient manner with reduced emissions and higher fuel efficiency which helps our customers combat the effects of global warming. We may benefit from increased government regulations that impose tighter emission and fuel efficiency standards. We encourage investors and potential investors to carefully consider the risks described under "Item 1A. Risk Factors" below regarding various aspects of the regulatory environment and other related risks.

Our products are well-suited to meet the needs of the rapidly emerging indoor agriculture market, including cannabis and other high volume leafy greens. To date our focus in the indoor agricultural market has primarily involved cannabis, a product with high revenue generating potential. However, we have sold to other indoor agricultural growers, and we believe that the indoor food production market will provide significant opportunities for us. The indoor agriculture market in particular has the potential to be a major driver of growth as states move to legalize the use of cannabis for medicinal purposes and recreational use. However, under the Controlled Substances Act (CSA) cannabis continues to be categorized as a Schedule I drug, so that cannabis growers continue to face significant uncertainty regarding their ability to conduct business.

First passed by Congress in 2014, the Rohracher-Farr Amendment is an amendment to the annual appropriations bill that, among other things, funds the Department of Justice. It prohibits the US Attorney General from using funds to prosecute the medical use of cannabis. It does not address recreational use. On January 4, 2018, US Attorney General Jeff Sessions rescinded the Cole memo. Written in 2013, the Cole memo had directed US Attorneys not to allocate resources to prosecute "individuals whose actions are in clear and unambiguous compliance with existing state laws" regarding the cannabis market. As of the date of the filing of this report, we are not aware of any US Attorney who has taken action against participants in the recreational cannabis market operating in accordance with state law. The uncertainty we face regarding the potential for growth from the sales to the cannabis industry is due in part to uncertainty regarding prosecutorial priorities of the current Presidential administration as well as the ability of cannabis growers to obtain funding in an environment where national bankers are not permitted to fund cannabis growth facilities.

Our Energy Production segment is subject to extensive government regulation. We are required to file for local construction permits (electrical, mechanical and the like) and utility interconnects, and are required to make various local and state filings related to environmental emissions.

In the past, many electric utility companies have raised opposition to distributed generation of energy, a critical element of our business model. Such resistance has generally taken the form of stringent standards for interconnection and the use of target rate structures as disincentives to combined generation of on-site power and heating or cooling services. A distributed generation facility's ability to obtain reliable and affordable back-up power through interconnection with the grid is essential to our business model. Utility policies and regulations in most states often do not accommodate widespread on-site generation. Barriers erected by electric utility companies and unfavorable regulations, where applicable, make our ability to connect to the electric grid at customer sites more difficult or uneconomic and is an impediment to the growth of our business. The development of our business could be adversely affected by any slowdown or reversal in the utility deregulation process or by difficulties in negotiating back-up power supply agreements with electric providers in the areas where we seek to do business.

Environmental Matters

We are regulated by federal, state and international environmental laws governing our use, transport and disposal of substances and control of emissions. In addition to governing our manufacturing and service operations, these laws often impact the development of our products, including, but not limited to, required compliance with air emissions standards applicable to internal combustion engines. We have made, and will continue to make, the necessary research and development and capital expenditures to comply with these emissions standards.

11

TECOGEN INC.

Human Capital Resources

We believe our success in delivering energy efficient, ultra clean cogeneration systems, chillers and energy production services relies on our culture, values, and the creativity and commitment of our people. We strive to maintain healthy, safe, and secure working conditions and a workplace where our employees are treated with respect and dignity. Our vision is to create an inclusive, diverse and authentic community that inspires collaboration, integrity, engagement, and innovation. We are striving to create employee experience that offers opportunity for personal and professional growth, and enables work-life balance that aligns with our core values.

Employee Health and Safety

Employee health and safety continues to be a priority in every aspect of our business. We have taken a common-sense approach to safety that helps us understand and reduce hazards in our business. Training, risk assessment, safety coaching, and employee engagement are all programs that help us consistently manage our facility and employee safety. As resources are available, we expect to continue to expand and evolve our safety programs to better meet our employee needs and workplace conditions as our business grows.

We understand the benefits of employee health and safety and continue to invest in programs, products, and resources. We also understand the environment of trust and fairness that exists when information is openly shared. We also continue to invest in products and services to meet the health and safety needs of our customers and communities.

Talent Acquisition and Development

Our values are integral to our employment process and serve as guideposts for leadership. The ultimate goal is straightforward: find great people, ask them to join, and give them a reason to stay. Reasons include fair compensation, a complete array of employee benefits to include: health, dental and life insurance; short-term and long-term disability insurance; HSA account funding; generous time off benefits; and the grant of options or awards to purchase shares of our common stock. Recently we instituted web-based training for all of our employees.

Employees

As of December 31, 2023, we employed 92 full-time employees and 1 part-time employee, including 4 sales and marketing personnel, 63 service personnel, 17 manufacturing personnel and 9 finance and administrative personnel. Nine of our New Jersey service employees are represented by a collective bargaining agreement which expires on December 31, 2025 and thereafter renews annually unless terminated by either party by written notice within sixty days prior to the expiration date.

Working Capital Requirements

Our ability to maintain sufficient working capital is highly dependent upon achieving expected operating results and cash flows. Failure to achieve the operating results could have a material adverse effect on our working capital, our ability to obtain financing, and our operations in the future.

The consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting

principles assuming that we will continue as a going concern, which contemplates the realization of assets and the settlement of obligations in the normal course of business. As of December 31, 2023, our cash and cash equivalents were $1,351,270, compared to $1,913,969 at December 31, 2022, a decrease of $562,699. For the year ended December 31, 2023 we used $823,315 in cash from operations and generated net operating losses of $4,413,612, due to due to lower Products sales, a decrease in gross margin due to higher products material costs and the increased provision for obsolete inventory and an increase in operating expenses due primarily to increased bad debt expense and a general increased in other administrative expenses. Working capital at December 31, 2023 was $9,822,546, compared to $14,344,288 at December 31, 2022, a decrease of $4,521,742 and our accumulated deficit was $42,879,656.

As a result of the above factors, management has performed an analysis to evaluate the entity’s ability to continue as a going concern for one year after the financial statements issuance date. Management’s analysis includes forecasting future revenues, expenditures and cash flows, taking into consideration past performance as well as key initiatives recently undertaken. Our forecasts are dependent on our ability to maintain margins based on the Company's ability to close on new and expanded business, leverage existing working capital, and effectively manage expenses. New and expanded business includes the sale and shipment of newly developed hybrid-drive air-cooled chillers and the acquisition of additional maintenance contracts in February 2024 (see Note 20. "Subsequent Events"). Our backlog at December 31, 2023 was $7,388,145, which is an increase of $666,007 from the December 31, 2022 backlog. We may also be required to borrow funds under note subscription agreements with related parties (see Note 11. "Related Party Notes"). Based on management's analysis, we believe that cash flows from operations and the note agreements will be sufficient to fund operations over the next twelve months. There can, however, be no assurance we will be able to do so. Based on our analysis, the consolidated financial statements do not include any adjustments to the carrying amounts and classification of assets, liabilities, and reported expenses that may be necessary if we were unable to continue as a going concern.

12

TECOGEN INC.

Our liquidity and cash flows are discussed in "Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations."

Available Information

Our internet website address is http://www.tecogen.com. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other reports and filings with the SEC are available free of charge on our website as soon as reasonably practicable after the reports are filed with, or furnished to, the SEC. Information contained on our website is not incorporated into this Annual Report on Form 10-K or our other securities filings with the SEC. The SEC maintains an internet website at www.sec.gov which contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Item 1A. Risk Factors

Our business operations, financial condition, results of operations and stock price may be affected by a number of factors. In addition to the other information in this Form 10-K, the following factors and the information contained under the heading ''Cautionary Note Concerning Forward-Looking Statements'' should be considered in evaluating our company and our business. The risks described below may not be the only risks we face. Additional risks that we do not yet know of, or that we currently think are immaterial, may also impair our business operations or financial results. If any of the events or circumstances described in the following risks occur, our business, financial condition and results of operations could suffer and the trading price of our common stock could decline.

Risks Relating to Our Business Strategy and Industry

We may need to raise additional financing if cash generated from our operations is insufficient.

During the year ended December 31, 2023, our revenues continued to be negatively impacted due to supply chain issues and project deferrals. The extent to which the coronavirus will continue to impact our business and our financial results will depend on future developments, which are highly uncertain and cannot be predicted. As part of our pandemic response plan, our sales, engineering, and select administrative functions may be operated remotely when necessary or appropriate while our manufacturing and service teams continues to function normally, subject to customer-initiated disruptions in service.

To the extent cash generated from operations in the future is insufficient to fund our operating requirements, we will be required to seek additional outside financing. Our inability to obtain necessary capital or financing to fund these working capital needs will adversely affect our ability to expand our operations.

If the cash generated by operations together with proceeds of funds available under our related party loans with John N. Hastopoulos, a director and principal shareholder and Earl R. Lewis, III, a director, are insufficient to fund our future operating requirements, we will need to raise additional funds through public or private equity or debt financings. Such financing may not be available to us when needed, or if available, may not be available on terms that are favorable to us and could result in significant dilution to the holdings of our stockholders. Furthermore, any such debt financing is likely to include financial and other covenants that may impede our ability to react to changes in the economy or industry. If adequate financing is not available when needed, we may be required to implement cost-cutting strategies, delay production, curtail research and development efforts, or implement other measures, which may adversely affect our results of operations and financial conditions and the price of our stock.

Based upon our operating and cash flow plan, we believe existing resources, including cash and cash flows from operations will be sufficient to meet our working capital needs for the next twelve months. If adequate financing is not available when needed, we may be required to implement cost-cutting strategies, delay production, curtail research and development efforts, or implement other measures, which may adversely affect our overall results of operations and financial condition and the price of our stock.

If we experience a period of significant growth or expansion, it could place a substantial strain on our resources.

If our cogeneration and chiller products penetrate the market rapidly, we may be unable to deliver large volumes of technically complex products or components to our customers on a timely basis and at a reasonable cost to us. We have never ramped up our manufacturing capabilities to meet significant large-scale production requirements. If we were to commit to deliver large volumes of products, we may not be able to satisfy these commitments on a timely and cost-effective basis.

Our operating history is characterized by losses and there can be no assurance we will be able to increase our sales and sustain profitability in the future.

We have historically incurred annual net losses, including a net loss of $4,598,108 in 2023. Our business is capital intensive and, because our products generally are built to order with customized configurations, the lead time to build and deliver a unit can be significant. We may be required to purchase key components long before we can deliver a unit and receive

13

TECOGEN INC.

payment. Changes in customer orders or lack of demand may also impact our profitability. There can be no assurance we will be able to increase our sales and achieve and sustain profitability in the future.

We are dependent on a limited number of third-party suppliers for the supply of key components for our products.

We use third-party suppliers for components in all of our products. Our engines and generators required in our cogeneration products (other than the InVerde), and the compressor and vessel sets in our chillers, are all purchased from large multinational equipment manufacturers. The loss of one or more of our suppliers could materially and adversely affect our business if we are unable to replace them. While alternate suppliers for the manufacture of our engine, generators and compressors have been identified, should the need arise, there can be no assurance that alternate suppliers will be available and able to provide such items on acceptable terms or on a timely basis.

From time to time, shipments of components for our products can be delayed because of industry-wide or other shortages of necessary materials and components from third-party suppliers, as well as shipping delays at points of importation. A supplier's failure to supply components in a timely manner, or to supply components that meet our quality, quantity, or cost requirements, or our inability to obtain substitute sources of these components on a timely basis or on terms acceptable to us, could impair our ability to deliver our products in accordance with contractual obligations.

The amount of our backlog is subject to fluctuation due to our customers’ experiencing unexpected delays in financing, permitting or modifications in specifications of the equipment.

Our total product and installation backlog as of December 31, 2023 was $7,388,145 compared to $6,722,138 as of December 31, 2022. Although we expect our customers to issue definitive purchase orders with respect to such backlog, there can be no assurance that such amounts will not be subject to modification in the event customers experience unexpected delays in obtaining permits, interconnection agreements or financing. We have experienced order delays and deferrals for our products due to business closures or the inability to obtain government issued permits to conduct product installations. Any of such events may result in customers modifying the equipment or the terms or timing of the expected installation, which may result in changes to the amount of backlog attributed to those projects.

We experience significant fluctuations in revenues from quarter to quarter on our product sales which may make period to period comparisons difficult.

We have low volume, high dollar sales for projects that are generally non-recurring, and therefore our sales have fluctuated significantly from period to period. Fluctuations cannot be predicted because they are affected by the purchasing decisions and timing requirements of our customers, which are unpredictable. Such fluctuations may make quarter to quarter and year to year comparisons difficult.

We expect significant competition for our products and services.

Many of our competitors and potential competitors are well established and have substantially greater financial, research and development, technical, manufacturing and marketing resources than we do. If these larger competitors decide to focus on the development of distributed power or cogeneration, they have the manufacturing, marketing and sales capabilities to complete research, development, and commercialization of these products more quickly and effectively than we can. There can also be no assurance that current and future competitors will not develop new or enhanced technologies or more cost-effective systems, and therefore, there can be no assurance that we will be successful in this competitive environment.

We may not achieve production cost reductions necessary to competitively price our products, which would adversely affect our sales.