Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

COMMISSION FILE NO.: 001-35612

Northern Tier Energy LP

(Exact name of registrant as specified in its charter)

| Delaware | 80-0763623 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

38C Grove Street, Suite 100

Ridgefield, Connecticut 06877

(Address of principal executive offices and Zip Code)

(203) 244-6550

(Registrant’s telephone number including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Units Representing Limited Partner Interests | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one)

| Large Accelerated Filer | ¨ | Accelerated Filer | ¨ | |||

| Non-Accelerated Filer | x | Smaller Reporting Company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

As of June 29, 2012, the last business day of the registrant’s most recently completed second fiscal quarter, the registrant’s equity was not listed on any domestic exchange or over-the-counter market. The registrant’s common units began trading on the New York Stock Exchange on July 26, 2012.

As of March 13, 2013, 91,949,017 common units were outstanding. The common units trade on the New York Stock Exchange under the ticker symbol “NTI.”

DOCUMENTS INCORPORATED BY REFERENCE: None

Table of Contents

NORTHERN TIER ENERGY LP

FORM 10-K FOR THE YEAR ENDED DECEMBER 31, 2012

i

Table of Contents

CAUTIONARY NOTICE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements that may constitute forward-looking statements. You can identify these statements by forward-looking words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “should,” “will,” “would,” or similar words. You should read statements that contain these words carefully because they discuss our current plans, strategies, prospects, and expectations concerning our business, operating results, financial condition, and other similar matters. While we believe that these forward-looking statements are reasonable as and when made, there may be events in the future that we are not able to predict accurately or control, and there can be no assurance that future developments affecting our business will be those that we anticipate. Our forward-looking statements involve significant risks and uncertainties (some of which are beyond our control) and assumptions that could cause actual results to differ materially from our historical experience and our present expectations or projections. Known material factors that could cause our actual results to differ from those in the forward-looking statements are those described in Part I, “Item 1A. Risk Factors.”

Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date hereof. We undertake no obligation to publicly update or revise any forward-looking statements after the date they are made, whether as a result of new information, future events or otherwise.

ii

Table of Contents

GLOSSARY FOR SELECTED TERMS

“3:2:1 crack spread” refers to the approximate refining margin resulting from processing three barrels of crude oil to produce two barrels of gasoline and one barrel of distillate;

“Barrel” refers to a common unit of measure in the oil industry, which equates to 42 gallons;

“Barrels per stream day” as defined by the EIA, represents the maximum number of barrels of input that a distillation facility can process within a 24-hour period when running at full capacity under optimal crude and product slate conditions with no allowance for downtime;

“Blendstocks” refers to various compounds that are combined with gasoline or diesel from the crude oil refining process to make finished gasoline and diesel; these may include natural gasoline, fluid catalytic cracking unit or FCCU gasoline, ethanol, reformate or butane, among others;

“Bpd” refers to an abbreviation for barrels per calendar day, which is defined by the EIA as the amount of input that a distillation facility can process under usual operating conditions reduced for regular limitations that may delay, interrupt, or slow down production such as downtime due to such conditions as mechanical problems, repairs, and slowdowns;

“Catalyst” refers to a substance that alters, accelerates, or instigates chemical changes, but is neither produced, consumed nor altered in the process;

“Coke” refers to a coal-like substance that is produced during the refining process;

“Complexity” refers to the number, type and capacity of processing units at a refinery, measured by an index, which is often used as a measure of a refinery’s ability to process lower cost crude oils into higher value light refined products, including transportation fuels, such as gasoline and distillates;

“Crack spread” refers to a simplified calculation that measures the difference between the price for light products and crude oil;

“Distillates” refers to primarily diesel, kerosene and jet fuel;

“EIA” refers to the Energy Information Administration. An independent agency within the U.S. Department of Energy that develops surveys, collects energy data, and analyzes and models energy issues;

“Ethanol” refers to a clear, colorless, flammable oxygenated hydrocarbon. Ethanol is typically produced chemically from ethylene, or biologically from fermentation of various sugars from carbohydrates found in agricultural crops and cellulosic residues from crops or wood. It is used in the United States as a gasoline octane enhancer and oxygenate;

“Feedstocks” refers to petroleum products, such as crude oil, that are processed and blended into refined products;

“Group 3 3:2:1 crack spread” refers to the 3:2:1 crack spread calculated using the market value of PADD II Group 3 conventional gasoline and ultra low sulfur diesel against the market value of NYMEX WTI;

“Light products” refers to the group of refined products with lower boiling temperatures, including gasoline and distillates;

“Mechanical availability” refers to unit rate capacity less lost capacity due to unplanned downtime less downtime due to planned maintenance divided by unit rated capacity less downtime due to planned maintenance;

“OSHA Recordable Rate” means the injury frequency rate reported by the Company to OSHA, which is equal to the number of recordable injures in a particular period multiplied by 200,000 and divided by the total hours worked in such period, including both employees and contractors;

iii

Table of Contents

“PADD II” refers to the Petroleum Administration for Defense District II region of the United States, which covers Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Ohio, Oklahoma, Tennessee and Wisconsin;

“Refined products” refers to petroleum products, such as gasoline, diesel and jet fuel, which are produced by a refinery;

“Sour crude oil” refers to a crude oil that is relatively high in sulfur content, requiring additional processing to remove the sulfur. Sour crude oil is typically less expensive than sweet crude oil;

“Sweet crude oil” refers to a crude oil that is relatively low in sulfur content, requiring less processing to remove the sulfur. Sweet crude oil is typically more expensive than sour crude oil;

“Throughput” refers to the volume processed through a unit or a refinery;

“Turnaround” refers to a periodically required standard procedure to refurbish and maintain a refinery that involves the shutdown and inspection of major processing units and occurs every three to four years on industry average;

“Upper Great Plains” refers to a portion of the PADD II region and includes Minnesota, North Dakota, South Dakota and Wisconsin;

“WTI” refers to West Texas Intermediate crude oil, a light, sweet crude oil, characterized by an American Petroleum Institute gravity, or API gravity, between 39 and 41 and a sulfur content of approximately 0.4 weight percent that is used as a benchmark for other crude oils; and

“Yield” refers to the percentage of refined products that is produced from crude oil and other feedstocks.

iv

Table of Contents

PART I

| Item 1. | Business. |

Overview

We are an independent downstream energy limited partnership with refining, retail and pipeline operations that serves the PADD II region of the United States. We operate our assets in two business segments: the refining business and the retail business. For the year ended December 31, 2012, we had total revenues of approximately $4.7 billion, operating income of $571.0 million, net income of $197.6 million and Adjusted EBITDA of $739.7 million. For the year ended December 31, 2011, we had total revenues of $4.3 billion, operating income of $422.6 million, net income of $28.3 million and Adjusted EBITDA of $430.7 million. A definition and reconciliation of Adjusted EBITDA to net income is included herein under the caption “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Adjusted EBITDA.”

Partnership Structure and Management

We were formed as a Delaware limited partnership by Northern Tier Holdings LLC (“Northern Tier Holdings”) in July 2012. Our non-economic general partner interest is held by Northern Tier Energy GP LLC, a Delaware limited liability company. References to our “general partner,” as the context requires, include only Northern Tier Energy GP LLC. Our operations are conducted directly and indirectly through our primary operating subsidiaries. On July 31, 2012, we completed our initial public offering (“IPO”) of 18,687,500 common units, representing an approximate 20.3% ownership interest in the Partnership. In exchange for contributing all of the interests in our operating subsidiaries, Northern Tier Holdings LLC received 57,282,000 common units and 18,383,000 payment-in-kind (“PIK”) common units. In November 2012, the PIK common units automatically converted to common units.

Refining Segment

Our refining segment primarily consists of an 81,500 barrels per calendar day (“bpd”) (84,500 barrels per stream day) refinery located in St. Paul Park, Minnesota. Our refinery has a complexity index of 11.5, which refers to the ability of a refinery to produce finished products based on its investment intensity and cost relative to other refineries. Our refinery’s complexity allows us to process a variety of light, heavy, sweet and sour crudes into higher value refined products.

We are one of only two refineries in Minnesota and one of four refineries in the Upper Great Plains area within the PADD II region. The PADD II region covers Illinois, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Missouri, Nebraska, North Dakota, South Dakota, Ohio, Oklahoma, Tennessee and Wisconsin. Our strategic location allows us direct access, primarily via the Minnesota Pipeline, to what we believe are abundant supplies of advantageously priced crude oils. Of the crude oil processed at our refinery in the years ended December 31, 2012 and 2011, approximately 47% and 51%, respectively, was Canadian crude oil and the remainder was primarily comprised of light sweet crude oil from the Bakken Shale in North Dakota. Many of these crude oils have historically priced at a discount to the NYMEX WTI. Further, over the past twelve months, NYMEX WTI has traded at an additional discount relative to waterborne crude oils.

We expect to continue to benefit from our access to these growing crude oil supplies. By 2030, according to the Canadian Association of Petroleum Producers (“CAPP”), total Canadian crude oil production is expected to grow to 6.2 million bpd from 2011 production of 3.0 million bpd. Crude oil production from the Bakken Shale in North Dakota has also increased significantly, helping to grow crude oil production in North Dakota from approximately 98,000 bpd in 2005 to approximately 769,000 bpd as of December 2012, and is expected to continue to grow due to improvements in unconventional resource production techniques.

Our location also allows us to distribute our refined products throughout the midwestern United States. Our refinery produces a broad slate of refined products including gasoline, diesel, jet fuel and asphalt, which are then

1

Table of Contents

marketed to resellers and consumers primarily in the PADD II region. Approximately 80% and 79% of our total refinery production for the years ended December 31, 2012 and 2011, respectively, was comprised of higher value, light refined products, including gasoline and distillates.

We also own various storage and transportation assets, including a light products terminal, a heavy products terminal, storage tanks, rail loading/unloading facilities and a Mississippi river dock. Approximately 78% and 83% of our gasoline and diesel volumes for the years ended December 31, 2012 and 2011, respectively, were sold via our light products terminal to our company-operated and franchised SuperAmerica branded convenience stores, Marathon branded convenience stores and other resellers. We have a contract with Marathon to supply substantially all of the gasoline and diesel requirements for the independently owned and operated Marathon branded convenience stores in our marketing area. Beginning in December 2012, we initiated a crude oil transportation business in North Dakota to allow us to purchase crude oil at the wellhead in the Bakken Shale while limiting the impact of rising trucking costs for crude oil in North Dakota.

Our refining business also includes our 17% interest in the Minnesota Pipe Line Company, which owns and operates the Minnesota Pipeline, a 455,000 bpd crude oil pipeline system that transports crude oil (primarily from Western Canada and North Dakota) for approximately 300 miles from the Enbridge pipeline hub at Clearbrook, Minnesota to our refinery. The Minnesota Pipeline has historically transported the majority of the crude oil used and processed in our refinery.

Retail Segment

As of December 31, 2012, our retail segment operated 166 convenience stores under the SuperAmerica brand and also supported 70 franchised convenience stores, which are also operated under the SuperAmerica brand. These convenience stores are located primarily in Minnesota and Wisconsin and sell various grades of gasoline and diesel, tobacco products and immediately consumable items such as beverages, prepared food and a large variety of snacks and prepackaged items. Our refinery supplied substantially all of the gasoline and diesel sold in our company-operated and franchised convenience stores for the years ended December 31, 2012 and 2011.

We also own and operate SuperMom’s Bakery, which prepares and distributes baked goods and other prepared food items for sale in our company-operated and franchised convenience stores and other third party locations.

Refining Industry Overview

Crude oil refining is the process of separating the hydrocarbons present in crude oil for the purpose of converting them into marketable finished, or refined, petroleum products such as gasoline, diesel, jet fuel, asphalt and other products. Refining is primarily a margin-based business where both the feedstock (primarily crude oil) and the refined products are commodities with fluctuating prices. In order to increase profitability, it is important for a refinery to maximize the yields of high value finished products and to minimize the costs of feedstock and operating expenses.

According to the EIA, as of January 1, 2012, there were 134 oil refineries operating in the United States, with the 14 smallest each having a refining capacity of 14,000 bpd or less, and the 10 largest having capacities ranging from 327,000 bpd to 560,500 bpd.

High capital costs, historical excess capacity and environmental regulatory requirements have limited the construction of new refineries in the United States over the past 30 years. According to the EIA, domestic operating refining capacity has increased approximately 4% between January 1982 and January 2012 from 16.1 million bpd to 16.7 million bpd. Much of this increase in capacity is generally the result of efficiency measures and moderate expansions at various refineries, known as “capacity creep,” but some significant expansions at existing refineries have occurred as well. During this same time period, more than 110 generally smaller and less efficient refineries that had limited access to a wide variety of crude oils or were unable to profitably process feedstock into a marketable product mix were closed.

2

Table of Contents

According to the EIA, total demand for refined products in PADD II, which is the region in which we operate, has represented approximately 26% of total U.S. refined products demand from 2007 to 2011. Within PADD II, refined product production capacity is currently insufficient to meet demand. For example, according to the EIA, due to product supply shortfalls within PADD II, net receipts of gasoline, distillate (inclusive of jet fuel and kerosene) and jet fuel/kerosene from domestic sources outside of PADD II comprised approximately 17%, 14% and 14%, respectively, of demand for these products. Refining capacity in the PADD II region has decreased approximately 3% between January 1982 and January 2012 from approximately 3.8 million bpd to approximately 3.6 million bpd, while more than 25 refineries in the PADD II region have ceased operations. The refined product volumes that are necessary to satisfy the demand in excess of PADD II production are primarily sourced from domestic refineries located outside of PADD II, specifically from the U.S. Gulf Coast.

The following tables illustrate the balance of certain refined products in PADD II from 2005—2011:

PADD II Gasoline Balance (mbpd)

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||||||||||||||||||||||

| Production by Refineries Within PADD II |

1,816 | 1,796 | 1,769 | 1,713 | 1,778 | 1,807 | 1,837 | |||||||||||||||||||||

| Net Receipts of Products from Domestic Sources Outside PADD II |

673 | 691 | 673 | 594 | 550 | 482 | 417 | |||||||||||||||||||||

| Ethanol |

136 | 138 | 179 | 243 | 222 | 231 | 225 | |||||||||||||||||||||

| Exports to Non-U.S. Sources |

0 | (2 | ) | (11 | ) | (19 | ) | (1 | ) | (5 | ) | (8 | ) | |||||||||||||||

| Imports from Non-U.S. Sources |

2 | 1 | 2 | 1 | 1 | 3 | 3 | |||||||||||||||||||||

| Other |

(1 | ) | 5 | 7 | 12 | (15 | ) | 8 | (11 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total |

2,626 | 2,629 | 2,619 | 2,544 | 2,535 | 2,526 | 2,463 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

PADD II Distillate Balance (mbpd)

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||||||||||||||||||||||

| Production by Refineries Within PADD II |

908 | 914 | 927 | 987 | 898 | 963 | 989 | |||||||||||||||||||||

| Net Receipts of Products from Domestic Sources Outside PADD II |

344 | 332 | 336 | 249 | 180 | 195 | 155 | |||||||||||||||||||||

| Exports to Non-U.S. Sources |

(9 | ) | (2 | ) | (6 | ) | (12 | ) | (6 | ) | (3 | ) | (5 | ) | ||||||||||||||

| Imports from Non-U.S. Sources |

4 | 6 | 6 | 5 | 4 | 6 | 2 | |||||||||||||||||||||

| Other |

2 | 5 | (8 | ) | (7 | ) | 1 | 1 | (3 | ) | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total |

1,249 | 1,255 | 1,255 | 1,222 | 1,077 | 1,162 | 1,138 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

PADD II Jet Fuel/Kerosene Balance (mbpd)

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||||||||||||||||||||||

| Production by Refineries Within PADD II |

230 | 220 | 202 | 209 | 208 | 219 | 229 | |||||||||||||||||||||

| Net Receipts of Products from Domestic Sources Outside PADD II |

145 | 119 | 115 | 74 | 49 | 41 | 36 | |||||||||||||||||||||

| Exports to Non-U.S. Sources |

(1 | ) | (4 | ) | (7 | ) | (10 | ) | (5 | ) | (4 | ) | (7 | ) | ||||||||||||||

| Imports from Non-U.S. Sources |

0 | 0 | 0 | 0 | 0 | 0 | 0 | |||||||||||||||||||||

| Other |

(3 | ) | 2 | 1 | 2 | (4 | ) | (1 | ) | (2 | ) | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total |

371 | 337 | 311 | 275 | 248 | 255 | 256 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

Source: EIA; see “Market and Industry Data and Forecasts.”

3

Table of Contents

Our Refining Business

Our refinery occupies approximately 170 acres along the Mississippi River in the southeast of St. Paul Park, Minnesota and was originally built in 1939. The refinery was acquired by Ashland Oil, Inc. in 1970 from Northwestern Refining, was jointly owned by Ashland Oil, Inc. and Marathon from 1998 through 2005 and became fully owned by Marathon in 2005. Our refinery is an 81,500 bpd (84,500 barrels per stream day) cracking facility with operations including crude fractionation, catalytic cracking, hydrotreating, reforming, alkylation, sulfur recovery and a hydrogen plant. A major refinery improvement and expansion project was completed in 1993 to enable the refinery to produce environmentally compatible low sulfur fuels. In 2006, the gas oil hydrotreater was revamped at a capital cost of approximately $24 million, which enables us to produce ultra low sulfur diesel. The fluid catalytic cracking unit was expanded in 2007 for a total capital cost of approximately $37 million, which improved gasoline yield and increased capacity from 27,100 bpd to 28,500 bpd. We completed a multi-year boiler replacement project, which entailed $19.9 million of capital expenditures over the project life, $12.7 million during the period from 2008 through November 30, 2010 and $7.2 million during the period from December 1, 2010 through December 31, 2011. Our refining capital expenditures in the year ended December 31, 2012 were $24.2 million.

A refinery’s location can have an important impact on its refining margins because location can influence access to feedstocks and efficient distribution for refined products. There are five regions in the United States, the PADDs, that have historically experienced varying levels of refining profitability due to regional market conditions. Refiners located in the U.S. Gulf Coast region operate in a highly competitive market due to the fact that this region (“PADD III”) accounts for approximately 39% of the total number of operable U.S. refineries as of January 2012 and approximately 47% of the country’s refining capacity as of January 2012. Our refinery is located in the strategically advantageous PADD II region. In recent years, demand for refined products in the PADD II region has exceeded regional capacity, resulting in a need for imports from other regions, specifically from the U.S. Gulf Coast region. Our inland location means that foreign and coastal domestic refiners seeking to access our marketing area would incur additional transportation costs. This favorable supply/demand imbalance has allowed our refinery to generate higher refining margins, compared to the U.S. Gulf Coast 3:2:1 crack spread. We have realized, on average, a premium of $4.14 per barrel, inclusive of refined product and crude differentials, relative to the benchmark Group 3 3:2:1 crack spread over the past five years through December 31, 2012 assuming a comparable rate of two barrels of Group 3 gasoline and one barrel of Group 3 distillate for every three barrels of WTI crude oil.

The refinery is an integrated refining operation with significant storage and transportation assets. Our transportation assets include our 17% interest in the Minnesota Pipe Line Company, an eight-bay light product terminal located approximately two miles from the refinery, a seven-bay heavy product loading rack located on the refinery property, rail facilities for shipping liquefied petroleum gas (“LPG”) and asphalt and receiving butane, isobutane and ethanol and a barge dock on the Mississippi River used primarily for shipping vacuum residue and slurry. As of December 31, 2012, our storage assets included 84 hydrocarbon storage tanks with a total capacity of 3.7 million barrels, 0.8 million barrels of crude oil storage and 2.9 million barrels of feedstock and product storage.

Process Summary

Our refinery is an 81,500 bpd (84,500 barrels per stream day) cracking facility with operations including crude fractionation, catalytic cracking, hydrotreating, reforming, alkylation, sulfur recovery and a hydrogen plant. We have significant redundancy in our refining assets, which include two crude oil distillation and vacuum towers, two reformers, two sulfur recovery units and five hydrotreating units. This redundancy allows us to continue to receive and process crude oil even if one tower goes out of service and also allows for increased maintenance flexibility as a redundant unit may be used without having to shut down the entire refinery in the case of a major unit turnaround. During the year ended December 31, 2012 and the year ended December 31, 2011, the refinery processed 81,779 bpd and 77,452 bpd of crude oil, respectively, and 2,072 bpd and 3,698 bpd of other charge and blendstocks, respectively. The facility processes a mix of light sweet, synthetic and heavy sour crude oils, predominately from Canada and North Dakota, into products such as gasoline, diesel, jet fuel, asphalt, kerosene, propane, LPG, propylene and sulfur. Our refinery utilization rates, using standard industry

4

Table of Contents

methodologies for utilization measurement, have been 80%, 75% and 72% for the years ended December 31, 2012 and 2011 and for the period from December 1, 2010 to December 31, 2010, respectively. Please see below for a simplified process flow diagram of the major refining units at our refinery.

The following table summarizes our refinery’s major process unit capacities as of December 31, 2012. Unit capacities are shown in barrels per stream day.

| Process Unit |

Capacity | % of Crude Oil Capacity | ||||||

| No. 1 Crude Oil Unit |

37,000 | 44 | % | |||||

| No. 2 Crude Oil Unit |

47,500 | 56 | % | |||||

| Vacuum Distillation Unit #1 |

19,000 | 22 | % | |||||

| Vacuum Distillation Unit #2 |

22,500 | 27 | % | |||||

| Catalytic Reforming Unit #1 |

13,500 | 16 | % | |||||

| Catalytic Reforming Unit #2 |

9,000 | 11 | % | |||||

| Fluid Catalytic Cracking Unit |

28,500 | 34 | % | |||||

| HF Alkylation Unit |

5,500 | 7 | % | |||||

| C4/C5/C6 Isom Unit |

8,500 | 10 | % | |||||

| Isom Desulfurizer |

8,500 | 10 | % | |||||

| Naphtha Hydrotreater #1 |

13,500 | 16 | % | |||||

| Naphtha Hydrotreater #2 |

9,500 | 11 | % | |||||

| Kerosene Hydrotreater |

7,800 | 9 | % | |||||

| Distillate Hydrotreater |

24,900 | 29 | % | |||||

| Gas Oil Hydrotreater |

29,500 | 35 | % | |||||

| Hydrogen Plant (MSCF/D) |

8,000 | — | ||||||

| Sulfur Recovery Units (Long Tons/day) |

100 | — | ||||||

| TailGas Recovery Units (Long Tons/day) |

4 | — | ||||||

5

Table of Contents

The complexity of a refinery refers to the number, type and capacity of processing units at the refinery and is measured by its complexity. Our refinery has a complexity index of 11.5. Our refinery’s complexity allows us to process lower cost crude oils into higher value light refined products or transportation fuels (gasoline and distillates), which comprised approximately 80% and 79% of our total refinery production for the years ended December 31, 2012 and 2011, respectively.

Raw Material Supply

The primary input for our refinery is crude oil, which represented approximately 98%, 95% and 92% of our total refinery throughput volumes for the years ended December 31, 2012, 2011 and 2010, respectively. We processed 81,779 bpd, 77,452 bpd and 74,142 bpd of crude oil for the years ended December 31, 2012, 2011 and 2010, respectively. The following table describes the historical feedstocks for our refinery:

| Year Ended December 31, | ||||||||||||||||||||||||

| 2012 | % | 2011 | % | 2010 | % | |||||||||||||||||||

| (bpd) | ||||||||||||||||||||||||

| Refinery Throughput Crude Oil Feedstocks by Location: |

||||||||||||||||||||||||

| Canadian and Other International |

38,332 | 47 | % | 39,295 | 51 | % | 41,156 | 56 | % | |||||||||||||||

| Domestic |

43,447 | 53 | % | 38,157 | 49 | % | 32,986 | 44 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Crude Oil |

81,779 | 100 | % | 77,452 | 100 | % | 74,142 | 100 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Crude Oil Feedstocks by Type: |

||||||||||||||||||||||||

| Light and Intermediate(1) |

60,326 | 74 | % | 56,722 | 73 | % | 55,782 | 75 | % | |||||||||||||||

| Heavy(1) |

21,453 | 26 | % | 20,730 | 27 | % | 18,360 | 25 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Crude Oil |

81,779 | 100 | % | 77,452 | 100 | % | 74,142 | 100 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Other Feedstocks/ Blendstocks(2): |

||||||||||||||||||||||||

| Natural Gasoline |

145 | 7 | % | 1,910 | 52 | % | 3,839 | 64 | % | |||||||||||||||

| Butanes |

1,294 | 62 | % | 1,236 | 33 | % | 1,242 | 21 | % | |||||||||||||||

| Gasoil |

58 | 3 | % | 0 | 0 | % | 446 | 7 | % | |||||||||||||||

| Other |

575 | 28 | % | 552 | 15 | % | 488 | 8 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Other Feedstocks/ Blendstocks |

2,072 | 100 | % | 3,698 | 100 | % | 6,015 | 100 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Inputs |

83,851 | 81,150 | 80,157 | |||||||||||||||||||||

| (1) | Crude oil is classified as light, intermediate or heavy, according to its measured American Petroleum Institute, or API, gravity. API gravity, which is expressed in degrees, is a scale developed for measuring the relative density of various petroleum liquids. It also serves as an approximate measure of crude oil’s value, as the higher the API gravity, the richer the yield in high value refined oil products, such as gasoline, diesel and jet fuel. For purposes of categorizing our crude oil feedstocks by type, light crude oil has an API gravity of 33 degrees or more, intermediate crude oil has API gravity between 28 and 33 degrees, and heavy crude has an API gravity of 28 degrees or less. |

| (2) | Other Feedstocks/Blendstocks includes only feedstocks/blendstocks that are used at the refinery, and does not include ethanol and biodiesel. Although we also purchase ethanol and biodiesel to supplement the fuels produced at the refinery, we do not include these in the table as those items are blended at the terminal located adjacent to the refinery or at terminals on the Magellan Pipe Line system. |

Of the crude oil processed at our refinery for the years ended December 31, 2012 and 2011, approximately 47% and 51%, respectively, was Canadian crude oil and the remainder was comprised of mostly light sweet crude oil from North Dakota. There is an abundant supply of Canadian crude oil, according to the EIA. Canada exported approximately 2.2 million bpd of crude oil into the United States in 2011, making it the largest exporter to the United States and representing 25% of all U.S. imports from foreign sources. By 2030, according to CAPP, total Canadian crude oil production is expected to grow to 6.2 million bpd from 2011 production of 3.0 million bpd. Additionally, U.S. demand for western Canadian oil supply is expected to reach 3.7 million bpd by 2020.

6

Table of Contents

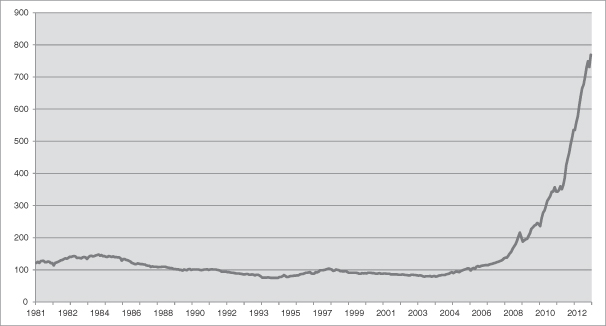

Crude production from North Dakota has increased significantly from approximately 98,000 bpd in 2005 to approximately 769,000 bpd as of December 2012, according to the EIA. The chart below shows crude oil bpd production in North Dakota, and illustrates the rapid increase in production attributable to the Bakken Shale. We believe production from the Bakken Shale will continue to increase due to continued growth in unconventional production.

North Dakota Crude Oil Production (thousands of BPD)

Source: EIA; see “Market and Industry Data and Forecasts.”

Crude Oil Supply

In March 2012, we entered into an amended and restated crude oil supply and logistics agreement with JPM CCC pursuant to which J.P. Morgan Commodities Canada Corporation (“JPM CCC”) assists us in the purchase of most of the crude oil requirements of our refinery. Once we identify cargos of crude oil and pricing terms that meet our requirements, we notify JPM CCC, which then provides, for a fee, credit, transportation and other logistical services for delivery of the crude oil to the Cottage Grove, Minnesota, storage tanks, which are approximately two miles from our refinery. Title to the crude oil passes from JPM CCC to us as the crude oil enters our refinery from the storage tanks located at Cottage Grove. The Cottage Grove storage tanks are leased by JPM CCC from us for the duration of the crude oil supply and logistics agreement. We believe our crude oil supply and logistics agreement significantly reduces the investment that we are required to maintain in crude inventories and allows us to take title to, and price our crude oil, at the refinery, as opposed to the crude oil origination point. We also benefit from the reduction in the time we are exposed to market fluctuations before the finished product output is sold.

The approximately 455,000 bpd Minnesota Pipeline system is the primary supply route for crude oil to our refinery and has transported a significant majority of our crude oil since its major expansion in 2008. The Minnesota Pipeline extends from Clearbrook, Minnesota to the refinery and receives crude oil from Western Canada and North Dakota through connections with various Enbridge pipelines. The Minnesota Pipeline is an interstate crude oil pipeline regulated by the Federal Energy Regulatory Commission (“FERC”) pursuant to the Interstate Commerce Act (“ICA”). Access to capacity on the Minnesota Pipeline is governed by the pipeline’s

7

Table of Contents

tariff, which is filed with FERC and must comply with the applicable provisions of the ICA. Pursuant to the rules and regulations applicable to the Minnesota Pipeline, if nominations are received for more crude oil than the pipeline can transport in a given month, capacity is pro-rated based on each shipper’s relative use of the line over the preceding twelve-month period ending the month prior to the month the excess nominations were received, with further reductions as necessary to accommodate new shippers. For the years ended December 31, 2012 and 2011, our shipments comprised approximately 24% of the total volumes shipped on the Minnesota Pipeline. Our 17% interest in the Minnesota Pipe Line Company mitigates the impact of tariff rate increases on the pipeline, as we receive a pro rata share of tariffs. See “—Pipeline Assets” for more information regarding the Minnesota Pipeline system.

In addition to the Minnesota Pipeline, the refinery is also capable of receiving crude oil from the Wood River Pipeline (owned and operated by affiliates of Koch Industries, Inc.). The Wood River Pipeline extends from Wood River, Illinois to a connection with the Minnesota Pipeline near Pine Bend, Minnesota, allowing for deliveries to the refinery and providing the refinery with access to crude supply from the Cushing, Oklahoma area via the Ozark Pipeline and to crude supply from the U.S. Gulf Coast and foreign markets via Capline and Capwood pipelines.

Below is a map illustrating the pipelines that provide the refinery with access to its crude oil supply:

Other Feedstocks/Blendstocks

The refinery also purchases ethanol and biodiesel, as well as conventional petroleum based blendstocks such as natural gasoline to supplement the fuels produced at the refinery. We purchase ethanol for blending with gasoline to meet the oxygenated fuel mandate levels of the United States Environmental Protection Agency (“EPA”). The state of Minnesota has a current mandate for all gasoline power motor vehicles for 10% ethanol blending in gasoline or the maximum amount of ethanol allowed under federal law, whichever is greater. The same legislation will require 20% ethanol blending in gasoline or the maximum amount of ethanol allowed under federal law, whichever is greater, effective August 30, 2013. Federal law currently allows a maximum of 15% ethanol for cars and light trucks manufactured since 2001, and 10% ethanol for all other vehicles. In addition,

8

Table of Contents

there is a biodiesel mandate in Minnesota requiring the blending of diesel with 5% bio-fuel. If certain preconditions are met, the minimum biodiesel content in diesel sold in the state was to increase to 10% beginning on May 1, 2012, and to 20% beginning on May 1, 2015. The increase to 10% did not occur on May 1, 2012, because the Minnesota Commissioners of Agriculture, Commerce and Pollution Control did not certify that all statutory pre-conditions were satisfied by the statutory deadline, but instead jointly recommended delaying the increase to 10% by one year, to May 1, 2013. We purchase ethanol and biodiesel blendstocks pursuant to month-to-month agreements with market related pricing provisions and receive those volumes primarily via truck. We purchase natural gasoline blendstock from third parties that is delivered to us via third party pipeline.

Refined Products—Production, Sales and Transportation

On average over the last three fiscal years, the refinery produced approximately 82,548 bpd of refined products, of which 49% was gasoline, 30% were distillates (including ultra low sulfur diesel and jet fuel), 12% was asphalt and the remainder was made up of propane, heavy fuel and other specialty products. The following table identifies the product yield of our refinery for each of the periods indicated.

| Year Ended December 31, | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| Refinery product yields (bpd): |

||||||||||||

| Gasoline |

40,825 | 40,240 | 41,199 | |||||||||

| Distillate |

27,113 | 24,841 | 22,546 | |||||||||

| Asphalt |

11,434 | 9,888 | 9,495 | |||||||||

| Other |

5,158 | 7,110 | 7,794 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total Production |

84,530 | 82,079 | 81,034 | |||||||||

|

|

|

|

|

|

|

|||||||

For the years ended December 31, 2012, 2011 and 2010, gasoline accounted for 52%, 54%, and 51% of our total revenue for the refining business for such periods, respectively, and distillates accounted for 35%, 33%, and 28% of our total revenue for the refining business for such periods, respectively.

Approximately 78% and 90% of the refinery business’s gasoline and diesel volumes were sold within the state of Minnesota for the years ended December 31, 2012 and 2011, respectively, with the remainder being sold within Iowa, Nebraska, Oklahoma, South and North Dakota and Wisconsin. Our refinery supplied substantially all of the gasoline and diesel sold in our company-operated or franchised convenience stores for the years ended December 31, 2012 and 2011, as well as supplied the independently owned and operated Marathon branded stores in our marketing area.

Primary distribution for the fuels is through our light products terminal, which is equipped with an eight-bay, bottom-loading truck rack and located adjacent to the refinery. Approximately 78% and 83% of our gasoline and diesel volumes for the years ended December 31, 2012 and 2011, respectively, were sold through this light products terminal to our company-operated or franchised SuperAmerica convenience stores, Marathon branded convenience stores and other resellers throughout our market area. Light refined products, which include gasoline and distillates, are distributed from the refinery through a pipeline and terminal system owned by Magellan, which has facilities throughout the Upper Great Plains. Asphalt and heavy fuel oil are transported from the refinery via truck from our seven-bay heavy products terminal and via rail and barge through our rail facilities and Mississippi River barge dock and are sold to a broad customer base. See “—Refining Operations Customers” below.

Refining Operations Suppliers

The primary input for our refinery is crude oil, which represented approximately 98% and 95% of our total refinery throughput volumes for the years ended December 31, 2012 and 2011, respectively. JPM CCC assists us

9

Table of Contents

in the purchase of most of the crude oil requirements of our refinery and provides transportation and other logistical services for delivery of the crude oil to our storage tanks at Cottage Grove, Minnesota, which are approximately two miles from our refinery. We also purchase ethanol and biodiesel, as well as conventional petroleum based blendstocks such as natural gasoline to supplement the fuels produced at the refinery. For more information, see “—Crude Oil Supply” and “—Other Feedstocks/Blendstocks.”

Refining Operations Customers

Our refinery supplies substantially all of the gasoline and diesel sold in our company-operated and franchised convenience stores, as well as substantially all of the gasoline and diesel sold in independently owned and operated Marathon branded stores in our marketing area. For the years ended December 31, 2012 and 2011, Marathon branded stores accounted for approximately 8% and 9%, respectively, of our refined product sales volumes. For more information about the risks associated with our commercial relationship with Marathon, see “Item 1A. Risk Factors—General Business and Industry Risks—Our arrangements with Marathon expose us to Marathon related credit and performance risk.”

Asphalt and heavy fuel oil are sold to a broad customer base, including asphalt paving contractors, government entities (states, counties, cities and townships), and asphalt roofing shingle manufacturers.

Turnaround and Refinery Reliability

Periodically, we have planned maintenance turnarounds at our refinery, which require the temporary shutdown of certain operating units. The refinery generally undergoes a major facility turnaround every five to six years, and the last full plant turnaround was completed in 2007. The length of the turnaround is contingent upon the scope of work to be completed. A major turnaround of either the fluid catalytic cracking unit or alkylation unit, two of the main refinery units, generally takes two to four weeks to complete, and is planned and accomplished in a manner that allows for reduced production during maintenance instead of a complete shutdown. We completed a partial turnaround in April 2011, during which we replaced a catalyst in the distillate and gas oil hydrotreaters and conducted basic maintenance on the No. 1 crude unit. At the end of March 2012, we started a planned turnaround of the alkylation unit that was completed in early May 2012. We are currently planning a major plant turnaround to occur during April 2013 and another partial turnaround for our fluid catalytic cracking unit during October 2013, for which we have budgeted aggregate spending of approximately $55 to $60 million. The refinery is currently expected to have reduced throughputs during the months of April and October 2013 to complete the turnarounds.

Seasonality

Our refining business experiences seasonal effects, as the demand for gasoline products is generally higher during summer months than during winter months due to seasonal increases in highway traffic. Demand for diesel during winter months also decreases due to declines in agricultural work. As a result, our results of operations related to our refinery business for the first and fourth calendar quarters are generally lower than for those for the second and third calendar quarters. In addition, unseasonably cool weather in summer months and/or unseasonably warm weather in winter months in the markets in which we sell our refined products can impact the demand for gasoline and diesel.

Seasonal fluctuations in traffic also affect sales of motor fuels and merchandise in our convenience stores. Weather conditions in our operating area also have a significant effect on our retail operating results. Customers are more likely to purchase higher profit margin items at our convenience stores, such as fast foods, fountain drinks and other beverages and more gasoline during the spring and summer months, thereby typically generating higher revenues and gross margins for us in these periods. Unfavorable weather conditions during these months and a resulting lack of the expected seasonal upswings in traffic and sales could impact the demand for such higher profit margin items in those months.

10

Table of Contents

Pipeline Assets

We own 17% of the outstanding common interests of the Minnesota Pipe Line Company and a 17% interest in MPL Investments, Inc. (“MPL Investments”) which owns 100% of the preferred interests of the Minnesota Pipe Line Company. The Minnesota Pipe Line Company owns the Minnesota Pipeline, a crude oil pipeline system in Minnesota that transports crude oil to the St. Paul area and which supplies most of our crude oil input. The remaining interests in the Minnesota Pipe Line Company are held by a subsidiary of Koch Industries, Inc., the owner of the only other refinery in Minnesota, with a 74.16% interest, and TROF, Inc. with an 8.84% interest. The Minnesota Pipeline system is also operated by a subsidiary of Koch Industries, Inc. Because we do not operate the Minnesota Pipeline or control the board of managers of the Minnesota Pipe Line Company, we do not control how the Minnesota Pipeline tariff is applied, including the tariff provisions governing the allocation of capacity, or control the decision-making with respect to tariff changes for the pipeline.

The Minnesota Pipeline system has multiple lines that run approximately 300 miles from Clearbrook in Clearwater County, Minnesota to Dakota County, Minnesota, transporting crude oil received through the Enbridge pipeline connections at Clearbrook from Western Canada and North Dakota to our refinery and Koch Industries’ Flint Hills Resources refinery in Minnesota. The system consists of a 24” pipeline, two parallel 16” pipelines and a partial third 16” pipeline with a combined capacity of approximately 455,000 bpd with further expansion capability to 640,000 bpd with the construction of an additional compressor station.

We also own an 8.6 mile 8” products pipeline, referred to as the Aranco Pipeline, which is leased to Magellan pursuant to an amended and restated agreement dated February 28, 2013, and used to ship refined products. The Aranco Pipeline extends from the refinery to a pipeline operated by Magellan as part of its products pipeline system. The Aranco Pipeline is operated by Magellan as part of their products system. The current annual lease amount is $750,000. The initial term of the lease agreement is for three years, subject to one-year auto renewals, and both parties have the right to terminate upon notice at least 180 days prior to the expiration of the then-current initial or renewal term. In addition, we own the Cottage Grove pipelines, which are 16” and 12” pipelines extending from the Cottage Grove tank farm, which is used to house the Cottage Grove storage tanks, to the refinery.

Our Retail Business

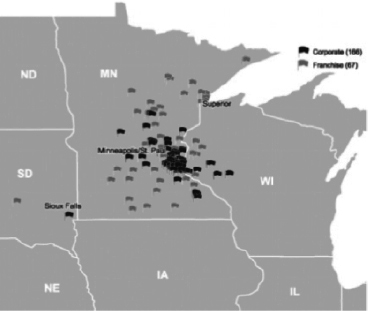

We have a retail-marketing network of 236 convenience stores, as of December 31, 2012, located throughout Minnesota, Wisconsin and South Dakota, of which we operate 166 stores and support 70 franchised stores, as set forth by location in the table below. All of our company-operated and franchised convenience stores are operated under the SuperAmerica brand. We also own and operate SuperMom’s Bakery, which prepares and distributes baked goods and other prepared items for sale in our retail outlets and for other third parties. Substantially all of the fuel gallons sold at the convenience stores for the years ended December 31, 2012 and 2011 was supplied by our refining business.

In December 2010, we entered into a lease arrangement with Realty Income Properties 3 LLC (“Realty Income”), pursuant to which we leased 135 SuperAmerica convenience stores and one support facility over a 15-year initial term at an aggregate annual rent fixed for five years at an annual rate of $20.3 million, with consumer price index-based rent increases thereafter. The stores covered under the lease are located in Minnesota and Wisconsin, and average approximately 3,500 leasable square feet on approximately 1.14 acres. In addition, the individual locations have, on average, 6.5 multi-pump gasoline dispensers, and are seasoned stores with long-term operating histories. Additionally, 30 of our other company-operated properties are leased pursuant to a combination of ground leases and real property leases with third parties and one company-operated property is owned by us.

11

Table of Contents

The table below sets forth our company-operated and franchised stores by state as of December 31, 2012.

| Location |

Company- Operated |

Franchised | Total | |||||||||

| Minnesota |

159 | 64 | 223 | |||||||||

| Wisconsin |

6 | 5 | 11 | |||||||||

| South Dakota |

1 | 1 | 2 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

166 | 70 | 236 | |||||||||

|

|

|

|

|

|

|

|||||||

Below is a map illustrating the locations of our convenience stores as of December 31, 2012:

Of our company-operated sites, approximately 80% are open 24 hours per day and the remaining sites are open at least 16 hours per day. Our average store size is approximately 3,400 square feet with approximately 95% of our stores being 2,400 or more square feet. Our convenience stores typically offer tobacco products and immediately consumable items such as beverages and a large variety of snacks and prepackaged items. A significant number of the sites also offer state sanctioned lottery games, ATM services, money orders and car washes. We also provide support to 70 franchised convenience stores, selling gasoline, merchandise, and other services through SuperAmerica Franchising LLC (“SAF”). SAF has license agreements in place with each franchisee that, among other things, cover the term of the franchise (generally 10 years), set forth the monthly royalty payments to be paid by franchisees to SAF, authorize the use of proprietary marks and provide for consultation services for the construction and opening of stores. Franchisees are required to pay to SAF an initial license fee (generally, $10,000 for licensees located in Minnesota and Wisconsin and $2,000 for licensees located in South Dakota) and a royalty fee for all products and merchandise sold at the convenience store, including motor fuel, along with a separate diesel royalty fee. The license agreements also require that, if a franchise store is located within our distribution area, then the franchise store must purchase a high minimum percentage (often 85% to 100%) of its motor fuel supply, including gasoline and distillate, from us. However, if a franchise store is not located within our distribution area, then the franchise store is not required to purchase any portion of its motor fuel supply from us. As of December 31, 2012, 35 of the 70 existing franchise stores are located within our distribution area and, thus, are required to purchase a high minimum percentage of their motor fuel supply from us.

12

Table of Contents

Annual sales of refined products through our 166 owned and leased convenience stores averaged 327 million gallons over the period 2012-2010. The demand for gasoline is seasonal in nature, with higher demand during the summer months. 24% of the retail segment’s revenues were generated from non-fuel sales, including items like cigarettes, beer, milk, food, general merchandise, car wash and other commission-based revenue for the year ended December 31, 2012. The following table summarizes the results of our retail business for the periods indicated.

| Year Ended December 31, | ||||||||||||

| 2012 | 2011 | 2010 | ||||||||||

| Company-operated |

||||||||||||

| Fuel gallons sold (in millions) |

312.4 | 324.0 | 345.1 | |||||||||

| Retail fuel margin ($/gallon)(1) |

$ | 0.18 | $ | 0.21 | $ | 0.17 | ||||||

| Merchandise sales ($ in millions) |

$ | 340.1 | $ | 340.3 | $ | 336.4 | ||||||

| Merchandise margin(%)(2) |

25.7 | % | 25.4 | % | 26.1 | % | ||||||

| Number of outlets at year end |

166 | 166 | 166 | |||||||||

| Franchised Stores |

||||||||||||

| Fuel gallons sold (in millions) |

45.4 | 51.5 | 52.4 | |||||||||

| Royalty income (in millions) |

$ | 2.1 | $ | 1.7 | $ | 1.6 | ||||||

| Number of outlets at year end |

70 | 67 | 67 | |||||||||

| (1) | Retail fuel margin per gallon is calculated by dividing retail fuel gross margin by the fuel gallons sold at company-operated stores. Retail fuel gross margin is a non-GAAP performance measure that we believe is important to investors in evaluating our retail performance. Our calculation of retail fuel gross margin may differ from similar calculations of other companies in our industry, thereby limiting its usefulness as a comparative measure. For a reconciliation of retail fuel gross margin to retail segment operating income, the most directly comparable GAAP measure, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—Other Non-GAAP Performance Measures.” |

| (2) | Merchandise margin is expressed as a percentage of the merchandise sales, calculated by subtracting the costs of merchandise from the merchandise sales, and then dividing by merchandise sales. Merchandise margin is a non-GAAP performance measure that we believe is important to investors in evaluating our retail performance. Our calculation of merchandise margin may differ from similar calculations of other companies in our industry, thereby limiting its usefulness as a comparative measure. Merchandise margin includes all non-fuel sales at our company-operated stores including items like cigarettes, beer, milk, food, general merchandise, car wash and other commission-based revenue. For a reconciliation of merchandise margin to retail segment operating income, the most directly comparable GAAP measure, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—Other Non-GAAP Performance Measures.” |

Retail Operations Suppliers

Our refinery supplies substantially all of the gasoline and diesel sold in our company-operated and franchised convenience stores. We also own and operate SuperMom’s Bakery, which prepares and distributes baked goods and other prepared food items for sale in our SuperAmerica company-operated and franchised convenience stores and other third party locations.

Eby-Brown has been the primary supplier of general retail merchandise, including most tobacco and grocery items, for all our company-operated and franchised convenience stores since 1993. For the years ended December 31, 2012 and 2011, our retail business purchased approximately 76% and 75%, respectively, of its convenience store inside merchandise requirements from Eby-Brown. Our retail business also purchases a variety of merchandise, including soda, beer, bread, dairy products, ice cream and snack foods, directly from a number of third-party manufacturers and their wholesalers. All merchandise is delivered directly to our stores by Eby-Brown, other third-party vendors or our SuperMom’s Bakery business. We do not maintain additional product

13

Table of Contents

inventories other than what is in our stores and at SuperMom’s Bakery. For information about the risks associated with our commercial relationship with Eby-Brown, see “Item 1A. Risk Factors—Risks Related to Our Business and Industry—Risks Primarily Related to Our Retail Business—Our retail business depends on one principal supplier for a substantial portion of its merchandise inventory. A change of merchandise suppliers, a disruption in merchandise supply, a significant change in our relationship with our principal merchandise supplier or material changes in the payment terms or availability of trade credit provided by our merchandise suppliers could have a material adverse effect on our retail business and results of operations or liquidity.”

Retail Operations Customers

Our retail customers primarily include retail end-users, motorists and commercial drivers. We have a retail-marketing network of 236 convenience stores, as of December 31, 2012, located throughout Minnesota, Wisconsin and South Dakota, of which we operate 166 stores and support 70 franchised stores.

Competition

Petroleum refining and marketing is highly competitive. With respect to our wholesale gasoline and distillate sales and marketing, we compete directly with Koch Industries’ Flint Hills Resources Refinery in Pine Bend, Minnesota, as well as the other refiners in the PADD II region and, to a lesser extent, major U.S. and foreign refiners. In addition, we compete with producers and marketers in other industries that supply alternative forms of energy and fuels to satisfy the requirements of our industrial, commercial and individual customers. Certain of our competitors have larger, more complex refineries, and may be able to realize lower per-barrel costs or higher margins per barrel of throughput. Many of our principal competitors are integrated, multinational oil companies that are substantially larger and more recognized than we are. Unlike these competitors, we obtain substantially all of our feedstocks from unaffiliated sources. Because of their integrated operations and larger capitalization, these companies may be more flexible in responding to volatile industry or market conditions, such as shortages of crude oil supply and other feedstocks or intense price fluctuations. The principal competitive factors affecting our refining segment are costs of crude oil and other feedstocks, refinery efficiency, refinery product mix and costs of product distribution and transportation. We have no crude oil reserves and are not engaged in the exploration or production of crude oil. We believe that we will be able to obtain adequate crude oil and other feedstocks at generally competitive prices for the foreseeable future.

Our major retail competitors include Holiday and Kwik Trip. The principal competitive factors affecting our retail segment are location of stores, product price and quality, appearance and cleanliness of stores and brand identification. We expect to continue to face competition from large, integrated oil companies, as well as from other convenience stores that sell motor fuels. Increasingly, grocery and dry goods retailers such as Wal-Mart are entering the motor fuel retailing business. Many of these competitors are substantially larger than we are. In addition, these retailers may use promotional pricing or discounts, both at the pump and in the store, to encourage in-store merchandise sales. Our convenience stores compete in large part based on their ability to offer convenience to customers. Consequently, changes in traffic patterns and the type, number and location of competing stores could result in the loss of customers and reduced sale and profitability at affected stores.

Insurance and Risk Management

Our operations are subject to significant hazards and risks inherent in refining operations and in transporting and storing crude oil, intermediate products and refined products. Our property damage and business interruption coverage at the refinery has a maximum loss limit of $1 billion combined, with no sublimit for business interruption. Our business interruption coverage is for 24 months from the date of the loss, subject to a deductible of 60 days with a minimum loss of $15 million. Our property damage insurance has a deductible of $1 million. In addition, we have a full suite of insurance covering workers compensation, general products liability, directors’ and officers’ liability, environmental liability, safety and other applicable risk management programs. See also “Item 1A. Risk Factors—General Business and Industry Risks—Our insurance policies may be inadequate or expensive.”

14

Table of Contents

Environmental Regulations

Refining Operations

Our refinery operations are subject to stringent and complex federal, state and local laws and regulations governing the discharge of materials into the environment or otherwise relating to environmental protection. These laws and regulations may obligate us to obtain and renew permits to conduct regulated activities; incur significant capital expenditures to install pollution control equipment; restrict the manner in which we may release materials into the environment; require remedial activities to mitigate pollution from former or current operations; apply specific health and safety criteria addressing worker protection; and impose substantial liabilities on us for pollution resulting from our operations. Certain of these environmental laws impose joint and several, strict liability for costs required to remediate and restore sites where petroleum hydrocarbons, wastes or other materials have been released or disposed. Failure to comply with environmental laws and regulations may result in the triggering of administrative, civil and criminal measures, including the assessment of monetary penalties, the imposition of remedial obligations, and the issuance of injunctions limiting or prohibiting some or all of our operations.

The clear trend in environmental regulation is to place more restrictions and limitations on activities that may affect the environment and any changes in environmental laws and regulations that result in more restrictive and costly emission limits, operational controls, fuel specifications, waste handling, disposal or remediation requirements could have a material adverse effect on our operations and financial position. In the event of future increases in costs, we may be unable to pass on those increases to our customers. There can be no assurance that our future environmental compliance expenditures will not become material.

Air Emissions

Our operations are subject to the federal Clean Air Act, as amended, and comparable state and local laws and regulations. Under the Clean Air Act, facilities that emit regulated pollutants, including volatile organic compounds, particulates, carbon monoxide, sulfur dioxide, nitrogen oxides or hazardous air pollutants, face increasingly stringent regulations, including requirements to install various levels of control technology on sources of pollutants. For example, the EPA published final amendments to the New Source Performance Standards (NSPS) for petroleum refineries on September 12, 2012 to be effective November 13, 2012. These amendments include standards for emissions of nitrogen oxides from process heaters and work practice standards and monitoring requirements for flares. To comply with the amendments, we plan to install and operate a continuous emissions monitoring system for nitrogen oxides on a process heater. We have already installed and will operate additional instrumentation on our flare. We anticipate the total cost for these two projects will be approximately $700,000 to be spent from 2012 through 2014. We continue to evaluate the regulation and amended standards, as may be applicable to the operations at our refinery. We cannot currently predict what additional costs that we may have to incur, if any, to comply with the amended NSPS. The costs could be material, but the time frame for compliance may extend over a number of years or upon changes or modifications to our refinery. In addition, the petroleum refining sector is subject to stringent new regulations adopted by the EPA, that impose maximum achievable control technology (“MACT”) requirements on refinery equipment emitting certain listed hazardous air pollutants. Air permits are required for our refining operations that result in the emission of regulated air contaminants. These permits incorporate stringent control technology requirements and are subject to extensive review and periodic renewal.

Over the past decade, the EPA has pursued a National Petroleum Refinery Initiative, which is a coordinated, integrated compliance and enforcement strategy to address federal Clean Air Act compliance issues at the nation’s largest petroleum refineries. In connection with the initiative, Marathon (which previously owned the St. Paul Park Refinery) entered into an environmental settlement agreement with the EPA, the U.S. Department of Justice and the state of Minnesota in May 2001 (the “2001 Consent Decree”), pursuant to which pollution control equipment was installed to significantly reduce emissions from stacks, wastewater vents, valves and flares at the refinery, and which imposes additional, and in some cases more stringent, standards and requirements on the

15

Table of Contents

refinery beyond applicable regulatory requirements. We are currently participating in negotiations with the EPA, the Minnesota Pollution Control Authority (“MPCA”) and Marathon concerning termination of the 2001 Consent Decree as to our refinery. The EPA and the MPCA have proposed that the MPCA issue an amended Title V Air Permit to the refinery that incorporates the emission limits and requirements of the 2001 Consent Decree into the permit before (or coincidental with) terminating the 2001 Consent Decree as to our refinery. We submitted an application to the MPCA in June 2012 to make the proposed amendments to the Title V Air Permit, and the MPCA is currently evaluating our amendment application. The MPCA released a draft amended Title V Air Permit for public comment on February 22, 2013. The public comment period closes on March 25, 2013. If the MPCA issues an amended Title V Air Permit incorporating the 2001 Consent Decree requirements, we anticipate that the EPA and MPCA will file a motion with the court to terminate the 2001 Consent Decree as to our refinery. Alternatively, the EPA and MPCA may propose to first modify the 2001 Consent Decree to add our subsidiary as a named party and then move to terminate the decree as to our refinery. Negotiations regarding termination of the 2001 Consent Decree are ongoing.

In August 2012, the EPA issued an Enforcement Alert announcing that it is devoting significant resources to a new enforcement initiative targeting flares used in the petroleum refining and chemical manufacturing industries. Through the initiative, the EPA seeks to improve the operation of flares by, among other things, requiring enhanced monitoring and control systems and work practice standards. The EPA has already entered into flaring consent decrees with two refiners and will likely pursue similar consent decrees with additional refiners. In April 2012, EPA personnel visited our refinery to conduct a flare inspection. On August 14, 2012, we received a request for information from the EPA regarding the flare at our refinery. We responded on September 27, 2012. To date, the EPA has not alleged that we have violated any requirements applicable to our flare or requested that we enter into a flaring consent decree. Some of the additional flare instrumentation that we anticipate the EPA would require under a flaring consent decree has already been installed on our flare and will be put into operation to comply with the EPA’s recent amendments to the NSPS for petroleum refineries, as discussed above. We cannot currently predict the costs that we may have to incur if we were to enter into a flaring consent decree with the EPA, but they could be material.

The refinery is obligated to comply with the conditions of its Title V Permit as well as emissions limitations and other requirements imposed under the Clean Air Act and similar state and local laws and regulations. These requirements are complex and stringent. Any failure to comply with such requirements may result in fines, penalties, and corrective action orders. Such fines, penalties, and corrective action orders could reduce the profitability of our refining operations.

Fuel Quality Requirements

Pursuant to the Energy Policy Act of 2005 and the Energy Independence and Securing Act of 2007, the EPA has issued Renewable Fuels Standards (“RFS”) implementing mandates to blend renewable fuels into petroleum fuels produced and sold in the United States. We are subject to RFS. Under the RFS, the EPA establishes a volume of renewable fuels that obligated refineries must blend into their finished petroleum fuels. The obligated volume increases annually over time until 2022. Our refinery currently generates a surplus of renewable identification number credits (“RINS”) under the RFS for some fuel categories, but we must purchase RINS on the open market for other fuel categories. We must also purchase waiver credits for cellulosic biofuels from the EPA. In the future, we may be required to purchase additional RINS on the open market and waiver credits from the EPA to comply with the RFS. We cannot currently predict the future prices of RINS or waiver credits, but the costs to obtain the necessary number of RINS and waiver credits could be material.

Minnesota law currently requires that all diesel sold in the state for combustion in internal combustion engines must contain at least 5% biodiesel. Under this statute, if certain preconditions are met, the minimum biodiesel content in diesel sold in the state was to increase to 10% beginning on May 1, 2012, and to 20% beginning on May 1, 2015. The increase to 10% did not occur on May 1, 2012, because the Minnesota

16

Table of Contents

commissioners of agriculture, commerce, and pollution control did not certify that all statutory pre-conditions were satisfied by the statutory deadlines, but instead jointly recommended delaying the increase to 10% by one year, to May 1, 2013. We recently completed installing a new tank at our refinery to store biodiesel to enable us to comply with this mandate at a total cost of approximately $3 million dollars. Minnesota law also currently requires, with limited exceptions, that all gasoline sold or offered for sale in the state must contain the maximum amount of ethanol allowed under federal law for use in all gasoline powered motor vehicles. Federal law currently allows a maximum of 15% ethanol for cars and light trucks manufactured since 2001, and 10% ethanol for all other vehicles. Fuels produced at our refinery are currently blended with the appropriate amounts of ethanol or biodiesel to ensure that they comply with applicable federal and state renewable fuel standards. Blending renewable fuels into our finished petroleum fuels to comply with these requirements will displace an increasing volume of a refinery’s product pool.

We also are required to meet the new Mobile Source Air Toxics (“MSAT II”) regulations to reduce the benzene content of gasoline. Under the MSAT II regulations, benzene in the finished gasoline pool was required to be reduced to an annual average of 0.62 volume percent by January 1, 2011 with or without the use of benzene credits and compliance was required to be demonstrated by January 1, 2012. Beginning on July 1, 2012, we must also maintain an annual average of 1.30 volume percent benzene without the use of benzene credits. A refinery may generate benzene credits by making reductions in the benzene content of the gasoline that it produces beyond what is required by the applicable regulations. These credits may be utilized by the refinery that generates them for future compliance, or they may be sold to other refineries. In 2012, our refinery’s average benzene content was less than 0.62%. Our refinery’s average benzene content for future years, however, could exceed the 0.62% limit. If that occurs, we anticipate using benzene credits we have accumulated in prior years and benzene credits purchased on the open market in order to comply with MSAT II requirements. We would also consider operational changes to lower the benzene content of the gasoline we produce. We cannot predict the costs associated with implementing such operational changes, but they could be material. We may be required to purchase additional benzene credits to meet our compliance obligations in the future. The cost for purchase of credits is variable and market driven. If the market price of credits increases in the future, the costs to obtain the necessary number of benzene credits could become material.

We are also subject to other fuel quality requirements under federal and state law, including federal standards governing the maximum sulfur content of gasoline and diesel fuel manufactured at the refinery. If we fail to comply with any of these fuel quality requirements, we could be subject to fines, penalties and corrective action orders. Moreover, fuel quality standards could change in the future requiring us to incur significant costs to ensure that the fuels we produce continue to comply with all applicable requirements. For example, the EPA has announced that it plans to propose new “Tier 3” motor vehicle emission and fuel standards sometime in 2013. It has been reported that these new Tier 3 regulations may, among other things, lower the maximum average sulfur content of gasoline from 30 parts per million to 10 parts per million. If the Tier 3 regulations are eventually implemented and lower the maximum allowable content of sulfur or other constituents in fuels that we produce, we may at some point in the future be required to make significant capital expenditures and/or incur materially increased operating costs to comply with the new standards.

Climate Change

In response to certain scientific studies suggesting that emissions of greenhouse gases (“GHGs”) including carbon dioxide and methane, are contributing to the warming of the Earth’s atmosphere and other climatic conditions, both houses of Congress have actively considered legislation to reduce emissions of GHGs, and almost one-half of the states have already taken legal measures to reduce emissions of GHGs, primarily through the planned development of GHG emission inventories and/or regional GHG cap and trade programs. Most of these cap and trade programs work by requiring either major sources of emissions or major producers of fuels to acquire and surrender emission allowances, with the number of allowances available for purchase reduced each year until the overall GHG emission reduction goal is achieved. These allowances would be expected to escalate significantly in cost over time. Although it is not possible at this time to predict if or when Congress may pass

17

Table of Contents