UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____________ to ___________

Commission File Number 000-54557

ARGENTUM 47, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 27-3986073 | |

| (State of Incorporation) | (I.R.S. Employer Identification No.) |

34 St. Augustine’s Gate, Hedon, HU12 8EX Hull, United Kingdom.

(Address of principal executive offices)

Registrant’s telephone number, including area code: +(1) 321 200 0142 / +(44) 1482 891 591

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class

Common Stock, $.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by check mark whether the registrant: (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that he registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Sec. 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit or post such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] | |

| Non-accelerated filer [ ] | Smaller reporting company [X] | |

| (Do not check if a smaller reporting company) | Emerging growth company [X] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [X]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day (June 28, 2019) of the Registrant’s most recently completed second fiscal quarter (June 30, 2019) was approximately $1,524,110.

As of March 25, 2020, there were 590,989,409 shares of our common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None

TABLE OF CONTENTS

| 2 |

CAUTION REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (“Annual Report”), in particular, the Management’s Discussion and Analysis of Financial Condition and Results of Operations appearing in Item 7 herein (“MD&A”) contains certain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements give expectations or forecasts of future events. The reader can identify these forward-looking statements by the fact that they do not relate strictly to historical or current facts. They use words such as “believe(s),” “goal(s),” “target(s),” “estimate(s),” “anticipate(s),” “forecast(s),” “project(s),” plan(s),” “intend(s),” “expect(s),” “might,” may” and other words and terms of similar meaning in connection with a discussion of future operations, financial performance or financial condition. Forward-looking statements, in particular, include statements relating to future actions, prospective services or products, future performance or results of current and anticipated services or products, sales efforts, expenses, the outcome of contingencies such as legal proceedings, trends of operations and financial results.

Any or all forward-looking statements may turn out to be wrong, and, accordingly, readers are cautioned not to place undue reliance on such statements, which speak only as of the date of this Annual Report. These statements are based on current expectations and the current economic environment. They involve several risks and uncertainties that are difficult to predict. These statements are not guaranteeing future performance. Actual results could differ materially from those expressed or implied in the forward-looking statements. Forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Many such factors will be important in determining the Company’s actual results and financial condition. The reader should consider the following list of general factors that could affect the Company’s future results and financial condition.

Among the general factors that could cause actual results and financial condition to differ materially from estimated results and financial condition are:

| ● | the success or failure of management’s efforts to implement their business strategy; | |

| ● | the ability of the Company to raise sufficient capital to meet operating requirements; | |

| ● | the uncertainty of consumer demand for our products and services; | |

| ● | the ability of the Company to compete with major established companies; | |

| ● | heightened competition, including, with respect to pricing, entry of new competitors and the development of new products or services by new and existing competitors; | |

| ● | absolute and relative performance of our products or services; | |

| ● | the effect of changing economic conditions; | |

| ● | the ability of the Company to attract and retain quality employees and management; | |

| ● | the current global recession and financial uncertainty; | |

| ● | uncertainties due to the current pandemic COVID-19 virus on the global market and its possible impact on the Company’s business; and | |

| ● | other risks which may be described in our future filings with the U.S. Securities and Exchange Commission (“SEC”). |

No assurances can be given that the results contemplated in any forward-looking statements will be achieved or will be achieved in any particular timetable. We assume no obligation to publicly correct or update any forward-looking statements as a result of events or developments subsequent to the date of this Annual Report. The reader is advised, however, to consult any further disclosures we make on related subjects in our filings with the SEC.

| 3 |

| ITEM 1. | BUSINESS. |

BUSINESS DEVELOPMENT

BACKGROUND

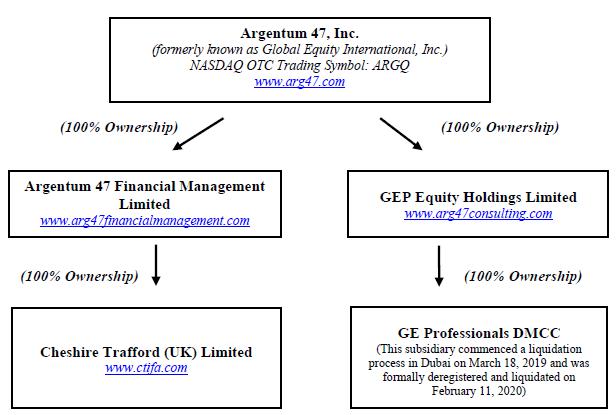

Argentum 47, Inc. (“Company” or “ARG”) was incorporated on October 1, 2010, as a Nevada corporation, for the express purpose of acquiring Global Equity Partners Plc., a corporation formed under the laws of the Republic of Seychelles (“GEP”) on September 2, 2009. On August 22, 2014, GE Professionals DMCC was incorporated in Dubai as a wholly owned subsidiary of Global Equity Partners Plc. On June 10, 2016, ARG incorporated its wholly owned subsidiary, called GEP Equity Holdings Limited, under the laws of the Republic of Seychelles.

On March 24, 2017, the Board of Directors of Global Equity Partners Plc. approved the assignment and transfer of GE Professionals DMMC to GEP Equity Holdings Limited.

On June 5, 2017, the Company sold 100% of the common stock of Global Equity Partners Plc. to a private citizen of the Kingdom of Thailand. The consideration for the purchase of Global Equity Partners Plc. was the assumption by the purchaser of all liabilities and indebtedness of Global Equity Partners Plc. in the approximate amount of $626,000. At the time of this sale, Global Equity Partners Plc. had assets consisting of common shares of other companies having a book value of approximately $603,000.

GEP Equity Holdings Limited provides consulting services, such as corporate restructuring, Exchange Listings and development for corporate marketing, investor and public relations, regulatory compliance and introductions to financiers, to companies desiring to be listed on stock exchanges in various parts of the world.

On December 12, 2017, we incorporated a United Kingdom company under the name of Argentum 47 Financial Management Limited (“Argentum FM”). Argentum FM is a wholly owned subsidiary of the Company. Argentum FM was formed to serve as a holding company for the acquisition of United Kingdom based advisory firms. During 2020, the Company intends to acquire more licensed financial advisory firms.

On January 12, 2018, the Company secured a 12-month fixed price convertible loan from Xantis Private Equity Fund (Luxembourg) for a minimum of 2,000,000 Great Britain Pounds (equivalent to approximately U.S. $2,680,000) carrying an interest at the rate of 6% per annum. The Company has a right to pay this note on the maturity date by issuing shares of common stock at a conversion price equal to the greater of $0.02 or the average closing price of the Company’s common stock on the OTCBB for the prior 60 trading days. To date, the Company received $400,000 under this loan, which including the accrued interest of $24,000 was converted into 21,200,000 shares of the Company’s common stock on January 14, 2019.

On January 12, 2018, the Company secured a 12-month fixed price convertible loan from William Marshal Plc., a United Kingdom Public Limited Company listed on the Cyprus Public Exchange Emerging Companies Market, for a maximum of 2,000,000 Great Britain Pounds (equivalent to approximately U.S. $2,680,000) carrying an interest at the rate of 6% per annum. The Company has a right to pay this note on the maturity date, by issuing shares of common stock at a conversion price equal to the greater of $0.02 or the average closing price of the Company’s common stock on the OTCBB for the prior 60 trading days. To date, the Company received $100,000 under this loan, which including the accrued interest of $6,000 was converted to 5,300,000 common shares of the Company on January 24, 2019.

On March 29, 2018, we changed our corporate name to Argentum 47, Inc.

| 4 |

On June 6, 2018, the Company secured a 12-month fixed price convertible loan, from Xantis Aion Securitization Fund (Luxembourg), for a minimum of 1,700,000 Great Britain Pounds (equivalent to approximately $1,940,000) carrying an interest at the rate of 6% per annum. The Company has a right to pay this note no earlier than 366 days’ post investment of each tranche of funding, by issuing common shares at a conversion price equal to the greater of $0.02 or the average closing ask price of the Company’s common stock on the OTCBB for the prior 60 trading days. To date, the Company has received $1,388,040 under this loan, of which $735,000 and related accrued interest was converted into 38,955,000 shares of the Company’s common stock on June 5, 2019.

On August 1, 2018, Argentum FM consummated a Share Purchase Agreement with Mr. Rodney Leonard and Equilibrium Pensions Limited (trustees of The Leonard R. Personal Pension), pursuant to which Argentum FM would acquire 100% of the ordinary shares (equity) of Cheshire Trafford (U.K.) Limited of Hull, United Kingdom (“Cheshire Trafford”) from Mr. Leonard and Equilibrium Pensions Limited (trustees of The Leonard R. Personal Pension).

In March 2019, Management decided that it made overall economic sense for the Company to close its employment placement services business in Dubai; hence, on March 18, 2019, in order to fully concentrate on its core business of Independent Financial Advisory services and Consultancy Business, the Board of Directors decided to initiate liquidation proceedings of the Dubai subsidiary “GE Professionals DMCC” (with an effective date of March 31, 2019). As a result of this decision to liquidate the subsidiary, the Board of Directors also decided to discontinue its Human Resources and Placement business in Dubai. On February 11, 2020, the deregistration and liquidation process of our Dubai subsidiary was formally completed.

Cheshire Trafford (U.K.) Limited (www.cheshire-trafford.co.uk) was incorporated under the laws of the United Kingdom on January 26, 1976, as a limited liability company. Cheshire Trafford is a very well established and UK FCA regulated Independent Financial Advisory firm that offers a fully computerized investment management service, including advising on investments in Unit Trusts, Investment Bonds, Shares, Investment Trusts, Government Bonds and Individual Savings Accounts. In addition, Cheshire Trafford advises investors on various types of Pension contracts, including Personal Pensions, Executive Pensions, Small Self-Administered Plans, Pension Mortgages and many more.

Cheshire Trafford acts as a broker for the sale of Lump Sum or Single Premium Insurance Policies and Regular Premium Investment or “Insurance” Policies that are issued by reputable third-party insurance companies.

| 5 |

Cheshire Trafford currently has four full time employees and in excess of 430 clients.

The funds that Cheshire Trafford currently has under administration are invested with well-known and reputable Investment Houses such as:

| ● | AJ Bell | |

| ● | Canada Life International | |

| ● | Fidelity International | |

| ● | Old Mutual International | |

| ● | Old Mutual Wealth Life | |

| ● | Royal London | |

| ● | Aviva | |

| ● | Prudential Assurance |

Cheshire Trafford’s primary customer base resides in the United Kingdom. Cheshire Trafford is licensed (Register Number 115194) and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom. Confirmation of Cheshire Trafford’s license can be made by visiting the FCA’s website: www.fca.gov.uk/register.

The purchase consideration for the acquisition of Cheshire Trafford is based on a formula of 2.7 times Cheshire Trafford’s projected annualized recurring revenues for the calendar year ending December 31, 2018. We took the gross revenues of Cheshire Trafford for the five months ended May 31, 2018 and annualized those recurring revenues and multiplied those revenues by 2.7 times in arriving at the contractual purchase consideration of U.S.$516,795 (389,300 Great Britain Pounds or “GBP”).

The purchase consideration is payable in three tranches. The first and initial tranche of U.S. $175,710 (132,362 GBP) was paid upon closing of the transaction. The second tranche of U.S. $170,542 (128,469 GBP) would be due 18 months after the closing. The August 31, 2018 acquisition agreement contemplated that the third and final tranche payment of U.S. $170,542 (128,469 GBP) that is due 36 months after the closing could be adjusted down (but not increased). This adjustment would only happen if Cheshire Trafford’s trail or recurring revenues between August 1, 2018 and July 31, 2019 (agreed testing period) was less than the “Recurring Target” of 144,185 GBP or, at current exchange rates, $168,365. At December 31, 2019, management carried out this testing and determined that the fair value of third and final tranche payment will be reduced by approximately $100,000.

The funds for the first tranche were obtained via a June 8, 2018 loan in the amount of U.S. $735,000 from the Xantis Aion Securitisation Fund, as previously reported in the Company’s Form 8-K Current Report filed with the Securities and Exchange Commission on June 11, 2018.

On December 18, 2019, the Company secured a 24-month convertible loan, from Aegeus Securitization Fund (Luxembourg), for 500,000 Great Britain Pounds (equivalent to approximately $658,200) carrying an interest at the rate of 6% per annum. The lender has an option to convert this note into common stock of the Company after (2) years and one (1) day from December 18, 2019 at a conversion price equivalent to the closing market price two days prior the new conversion date. Aegeus Securitization Fund and Xantis AION Securitization Fund both have the same fund administrators, Xantis S.A., hence Aegeus Securitization Fund is treated as a related party of the Company as at December 31, 2019. The Company simultaneously also entered into a Receivables Assignment Agreement whereby an amount of the receivables from the Company and/or the next Independent Financial Advisory Firm acquired will be securitized to the lender. Pursuant to the terms of this Assignment Agreement, the Company assigned its receivables for the period from June 2020 to May 2025 to the lender. To date, the Company has received GBP 250,000 (equivalent to approximately $329,000) under this loan.

Our authorized capital consists of 950,000,000 shares of common stock having a par value of $0.001 per share and 50,000,000 shares of preferred stock having a par value of $0.001. As of December 31, 2018, we had 525,534,409 shares of common stock issued and outstanding. As of December 31, 2019, we had 590,989,409 shares of common stock issued and outstanding. We also have two series of preferred stock designated and authorized: Series “B” Preferred Stock and Series “C” Preferred Stock. As of December 31, 2018, and 2019, we had 45,000,000 shares of Series “B” Preferred Stock authorized, issued and outstanding. As of December 31, 2018, and 2019, we had designated and authorized 5,000,000 shares of Series “C” Preferred Stock, 3,200,000 shares of which were issued and outstanding. In March 2020, we issued an additional 100,000 shares of Series “C” Preferred Stock to Mr. Nicholas Tuke, our new Chief Executive Officer, so we currently have a total of 3,300,000 shares of Series “C” Preferred Stock issued and outstanding on the date of this report. We do not have any Series “A” Preferred Stock authorized, issued or outstanding. We have 1,700,000 shares of Series “C” Preferred Stock designated and authorized, which could be issued in the future. All shares of our Series “B” and Series “C” Preferred Stock are contractually locked-up until September 27, 2020; hence, they cannot be sold or converted into common stock at any time prior to that date.

We provide corporate advisory services to companies desiring to have their shares listed on stock exchanges or quoted on quotation bureaus in various parts of the world. We had an office in Dubai until March 31, 2019. Our current offices are located in the United Kingdom. We have affiliations with firms located in some of the world’s leading financial centers such as London, New York, Frankfurt and Dubai. These affiliations are informal and are comprised of personal relationships with groups of people or people with whom our Company or our management has done, or attempted to do, business in the past. We do not have any contractual arrangements, written or otherwise, with our affiliations.

| 6 |

Argentum 47 Financial Management Limited is a United Kingdom based holding company that will acquire, in due course, more financial advisory firms with funds under administration around the world. These financial advisory firms act as intermediaries between their clients and the insurance companies. In effect, the advisory firms sell insurance policies to their clients. These types of financial advisory firms receive recurring and non-recurring trail fees for each insurance policy that is sold. Cheshire Trafford U.K. Limited is the first acquisition of Argentum 47 Financial Management Limited and it provides corporate and retail independent financial advisory services and generates our revenues by acting as broker for sale of Lump Sum or Single Premium Insurance Policies and/or the sale of Regular Premium Investment or Insurance Policies that are issued by third party insurance companies.

GEP Equity Holdings Limited looks for companies that require capital funding for growth and acquisition, and ultimately a listing of their shares on a recognized stock exchange or quotation on the OTC Markets quotation boards. The Company introduces these clients to private and institutional investors in our network of over 100 “financial introducers” around the world. These financial introducers are groups of people or institutions that are presently introducing new clients to us or who have introduced new clients to our management in the past. We do not have any contractual arrangements, written or otherwise, with these financial introducers.

Presently, GEP Equity Holdings Limited, Argentum 47 Financial Management Limited and Cheshire Trafford (U.K.) Limited are our only operating businesses. ARG´s present operations are limited to ensuring compliance with regional, state and national securities regulatory agencies and organizations. In addition, ARG, as the parent company, is charged with (i) handling our periodic reporting obligations under the Securities Exchange Act of 1934; (ii) managing our investor relations; and (iii) raising debt and equity capital necessary to fund our operations in order to enhance and grow our business. ARG does not offer or conduct any consulting or advisory services, as such services are now performed solely by GEP Equity Holdings Limited. As stated above, Argentum 47 Financial Management Limited will serve as a holding company for the financial advisory firms to be acquired. Cheshire Trafford (U.K.) Limited is a financial advisory firm with funds under administration.

We currently offer the following services to our clients:

| ● | General business consulting | |

| ● | Corporate restructuring | |

| ● | Fund administration | |

| ● | Exchange listings and quotations on OTC Markets quotation boards |

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY

As a Company with less than $1 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (also known as the “JOBS Act”). As an emerging growth company, we are entitled to take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. These provisions include:

| ● | Only two years of audited financial statements in addition to any required unaudited interim financial statements with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; | |

| ● | Reduced disclosure about our executive compensation arrangements; | |

| ● | Not having to obtain non-binding advisory votes on executive compensation or golden parachute arrangements; and | |

| ● | Exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting. |

| 7 |

We may take advantage of these exemptions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1 billion in annual revenues, if we have more than U.S.$700 million in market value of our stock held by non-affiliates, or if we issue more than U.S.$1 billion of non-convertible debt over a three-year period. We may take advantage of these exemptions until the last day of the fiscal year of the Company following the fifth anniversary of the date of the first sale of our common equity securities in an effective registration statement under the Securities Act of 1933, as amended. Note: To date, we have not sold or issued any of our common equity securities under an effective Form S-1, Form S-3, Form S-4 or Form S-8 or other form of registration statement under the Securities Act of 1933, as amended. We may choose to take advantage of some but not all of these reduced burdens in the future. We have irrevocably elected to opt out of the extended transition period for complying with new or revised accounting standards pursuant Section 107(b) of the JOBS Act.

FUND MANAGEMENT

In common with the overall financial services sector, the micro fund management market is undergoing significant changes. We intend to take advantage of these changes and acquire a significant selection of international and United Kingdom based financial advisory firms with funds under administration. These acquisitions will form part of Argentum 47 Financial Management Limited, which is under one efficient and cost-effective umbrella. Argentum 47 Financial Management Limited’s wholly owned subsidiary, Cheshire Trafford (U.K.) Limited currently has approximately 430 clients that have authorized our company to administrate between $8,000 and $650,000 of their money, the total representing tens of millions of dollars of funds under administration.

EXCHANGE LISTINGS

We also assist our clients with the selection of stock exchanges and over the counter quotation boards and markets that may be suitable to our clients. Various exchanges have listing requirements and standards that vary from one exchange to another. Typical listing requirements and standards relate to a number of things, such as pre-tax income, cash flows, revenue, net tangible assets, market value of a company’s listed securities, minimum trading prices of a company’s securities, minimum shareholders’ equity, operating history, number of shareholders, number of market makers, and corporate governance. We will try to identify appropriate exchanges for our clients based on the particular client’s operating history, pre-tax income, cash flow, revenue, net tangible assets, shareholder base and other factors described above.

We will assist our clients with retention of attorneys and accountants having experience with publicly held companies and stock exchanges in various countries. We will also assist our clients in locating market makers, investment bankers and broker-dealers to assist them with accessing capital markets.

INTRODUCTIONS TO FINANCIERS

After reviewing the business plans, prospects and problems that are unique to each of our clients, we will use our best efforts to introduce our clients to various third party financial resources around the world who may be able to assist them with their capital funding requirements.

Special Note: As used throughout this Annual Report, references to “Argentum 47, Inc.”, “ARG”, “Company”, “we”, “our”, “ours”, and “us” refer to Argentum 47, Inc. and our subsidiaries, unless the context otherwise requires. In addition, references to “financial statements” are to our consolidated financial statements contained herein, except as the context otherwise requires. References to “fiscal year” are to our fiscal year which ends on December 31 of each calendar year. Unless otherwise indicated, the terms “Common Stock,” “common stock” and “shares” refer to our shares of $0.001 par value, common stock.

| 8 |

HISTORICAL BUSINESS TRANSACTED

BUSINESS TRANSACTED IN 2016

During 2016, we provided our consultancy services to the following 9 clients:

| 1. | Granite Power Limited | |

| 2. | Deutsche Oel and Gas SA | |

| 3. | Majestic Wealth Limited | |

| 4. | Unite Global AS | |

| 5. | Teralight FZ LLC | |

| 6. | The Stakis Collections Limited | |

| 7. | Ali Group MENA FZ LLC | |

| 8. | Veolia Middle East | |

| 9. | Emaar, The Economic City |

BUSINESS TRANSACTED IN 2017

During 2017, we provided our consultancy services to the following 8 clients:

| 1. | Blackstone Natural Resources S.A. | |

| 2. | Graphite Resources (DEP) Limited | |

| 3. | OCS ROH | |

| 4. | Fly-A-Deal | |

| 5. | Falcon Eye Technology | |

| 6. | Ali Group MENA FZ LLC | |

| 7. | Veolia Middle East | |

| 8. | Emaar, The Economic City |

BUSINESS TRANSACTED IN 2018

During 2018, we provided our consultancy services to the following 4 clients:

| 1. | Emaar, The Economic City. | |

| 2. | OCS ROH. | |

| 3. | Blackstone Natural Resources S.A. | |

| 4. | Creditum Limited. |

| 9 |

After the acquisition of Cheshire Trafford U.K. Limited on August 1, 2018, the Company also gained access to the Cheshire Trafford U.K. Limited’s client’s database, currently comprised of more than 430 individual clients, which are now part of our insurance brokerage business segment.

OUR BUSINESS IN 2019

Since August 1, 2018, the Company operated in two reportable business segments:

| 1) | Management Consultancy Services (the “Consultancy” segment); and | |

| 2) | A segment which concentrates on third party insurance policy sales and renewals (the “Insurance brokerage” segment). The Company’s reportable segments were strategic business units that offered different products. |

Both business segments are managed separately based on the fundamental differences in their operations and locations.

Under the Consultancy segment, we have three distinct divisions (none of which will be treated as a segment for financial reporting purposes):

| 1. | Introducers Network. We have developed and continue to develop several finance professionals, accountants, attorneys and financial advisers who will introduce us to their clients. We will review businesses introduced to us through these introducers and we will compensate them in manners “to be determined” based on the event that we are engaged to assist the companies they introduce to us. | |

| 2. | Project Review. Our management team and advisors will carefully review and vet each business plan and opportunity submitted to us. Our management team and advisors will determine which services we can offer these clients and assess the potential propositions to best assist our clients in achieving their goals. | |

| 3. | Placing. Working with our business associates in Dubai, Europe and the United States, we will use our best efforts to assist our clients with listings on stock exchanges in these cities and countries in order to maximize their exposure to capital markets and to access funding via debt and equity offerings. |

FUTURE PLANS

Our specific plan of operations and milestones from March 2020 through March 2021 are as follows:

| 1. | CONTINUE TO DEVELOP AND GROW ALREADY ACQUIRED IFA BUSINESSES – CHESHIRE TRAFFORD (U.K.) LIMITED. |

In January 2020, we revised the Terms of Business that we send out to all current and new clients. This revision contemplates offering these clients two types of services packages, “Basic” and “Comprehensive,” at a fee rate of 0.75% per annum (a minimum annual fee of 750 GBP or $980) and 1% per annum (a minimum annual fee of 1,000 GBP or $1,300), respectively. The “Basic” service package is what we are legally obliged to offer under U.K. FCA guidelines and the “Comprehensive” service package is much more complete and contemplates additional added value for the client. Within the revised Terms of Business, we have also implemented an upfront 3% fee that is payable by each new client that is onboarded to our client base. Both the upfront fee and annual fee are based on the amount of Funds that legacy clients and new clients authorize our Company to Administrate and ultimately look after their financial affairs.

| 10 |

So far this year, we have 25 new business clients that have sent us signed letters of authority and wish to engage our Company. Most of these new clients have opted for the “Comprehensive” service package. It is important to note that the Funds that we currently administrate range from $8,000 to $650,000 per client (equivalent to 6,000 GBP to 500,000 GBP) and that we have calculated that the average amount of Funds that we administrate per client, taking into consideration our historical data, is approximately $72,500.

Our goal for 2020, is to attract at least 100 new business clients (25 of which already are in the process of being onboarded as new business clients) hence our intent is to raise the Funds that we currently administrate by between $7.25 million to up $10 million. Between the 3% initial upfront fee and the ongoing/recurring 1% or 0.75% administration fee, we are aiming to raise our gross income by at least $250,000 on the low side and up to $400,000 on the high side in 2020. This uplift in gross revenue would represent 2 to 3 times the currently gross income.

Finally, it is our intent in 2020 to continue to leverage the licenses that we now own as believe that we can significantly increase our business and revenues at very little extra cost and improve profitability.

| 2. | SEEK FURTHER FUNDING FOR FURTHER INORGANIC GROWTH VIA ACQUISITION |

The Company is looking into entering a long-term funding agreement up to $10 million U.S. Dollars with a with a new European based Regulated Fund in order to accelerate our inorganic growth and acquisition plan with a view to consolidate our Company in the marketplace. Currently all negotiations are verbal negotiations.

| 3. | ACQUIRE CERTAIN INDEPENDENT FINANCIAL ADVISORY FIRMS WITH FUNDS UNDER ADMINISTRATION: |

During the year ended December 31, 2019, management commenced certain negotiations to acquire 100% of an Independent Financial Advisory (IFA) firm based in London (United Kingdom). This targeted IFA currently has 136 Million GBP (approximately U.S. $179 Million) of Funds under Administration and historical recurring revenues of a little more than One Million GBP (approximately U.S. $1.32 million). However, we do not currently have any written agreements as management is still in verbal negotiations with the owners of this IFA.

The Company intends to target and acquire more Independent Financial Advisory firms with funds under administration during the next 12 to 24 months.

As the Company acquires more Financial Advisory firms, each book of business will be analyzed to achieve the maximum return and revenue from the client bank without affecting the client offering. In addition, certain cost savings will be managed into the budgets by using technology for the administration, looking for duplication of services and by managing the client and the funds under administration in a more efficient way.

The acquisition of these entities will open a new network for the services of:

| o | New capital markets clients. | |

| o | Distribution of new funds / products. | |

| o | Maximizing the current books of business being bought. | |

| o | Expand and thus increase business via more financial advisors. | |

| o | Seek products that offer both a minimum of 1% trail (recurring) income and a secure risk averse home for clients’ funds. | |

| o | Seek cost savings, where possible, due to elimination of duplicate services. | |

| o | Implement rapid and efficient systems in order to allow information to flow to the clients and to management more effectively. | |

| o | Acquiring smaller, active client banks into our licenses and procedures for cost effective growth. |

| 4. | COMMENCE A TARGETED MARKETING PLAN |

During 2020, our United Kingdom regulated business, Cheshire Trafford (U.K.) Limited, will continue with the direct marketing campaign that commenced in the second quarter of 2019, within the region using traditional print media, radio advertising, social media and editorial pieces. In conjunction with this campaign, the website and marketing of the Company will be refocused with a completely new image based around “Over 40 years of serving the community.” Two days per month in our office in the United Kingdom, we will offer free consultation to prospective clients that come and visit us, thus enabling us to potentially recruit them as new clients.

| 11 |

| 5. | FURTHER EXPAND OUR RANGE OF SERVICES TO OUR FINANCIAL SERVICES CLIENTS |

We will bring additional products to the client bank in order to maximize the potential returns per client with complementary products such as mortgages, trusts and more attractive funds.

| 6. | CAPITAL MARKETS |

The Company intends to continue its mandate to assist its client, Creditum Limited, with the listing of the Creditum Limited´s shares on the London Stock Exchange (“LSE”). Management believes that this public listing should be fully executed and finalized by sometime in the year 2020.

COMPETITION

We face intense competition in every aspect of our business, and particularly from other firms that offer management, compliance and other consulting services to private and public companies. We would prefer to accept a relatively low cash component as our fee for management consulting and regulatory compliance services and take a greater portion of our fee in the form of restricted shares of our private clients’ common stock. We also face competition from many consulting firms, investment banks, venture capitalists, merchant banks, financial advisors and other management consulting and regulatory compliance services firms similar to ours. Many of our competitors have greater financial and management resources and some have greater market recognition than we do. There are many institutions around the globe that are executing a roll-up strategy by acquiring Financial Advisory firms around the world; hence, we will face completion, but we believe that there is plenty of room for our Company to compete within the Financial Advisory world.

REGULATORY REQUIREMENTS.

Regarding the Corporate Consultancy Service segment of our business, we are not required to obtain any special licenses, nor meet any special regulatory requirements before establishing our business, other than a simple business license. If new government regulations, laws, or licensing requirements are passed that would restrict or eliminate delivery of any of our intended products, then our business may suffer. Presently, to the best of our knowledge, no such regulations, laws, or licensing requirements exist or are likely to be implemented in the near future that would reasonably be expected to have a material impact on our sales, revenues, or income from our business operations. Furthermore, we are not a broker-dealer. We are not an investment adviser or an investment company. We are not a hedge fund or a mutual fund or any similar type of fund.

Regarding the Independent Financial Advisory (IFA) segment of our business, our subsidiary Cheshire Trafford UK Limited is required to be fully registered and licensed by the United Kingdom Financial Conduct Authority (FCA).

EFFECT OF EXISTING OR PROBABLE GOVERNMENTAL REGULATIONS.

The Company’s common stock is registered pursuant to Section 12(g) of the Securities Exchange Act of 1934 (“1934 Act”). As a result of such registration, the Company is subject to Regulation 14A of the “1934 Act,” which regulates proxy solicitations. Section 14(a) requires all companies with securities registered pursuant to Section 12(g) thereof to comply with the rules and regulations of the Commission regarding proxy solicitations, as outlined in Regulation 14A. Matters submitted to stockholders of the Company at a special or annual meeting thereof or pursuant to a written consent will require the Company to provide its stockholders with the information outlined in Schedules 14A or 14C of Regulation 14; preliminary copies of this information must be submitted to the Securities and Exchange Commission (“Commission”) at least 10 days prior to the date that definitive copies of this information are forwarded to stockholders.

| 12 |

The Company is also required to file annual reports on Form 10-K and quarterly reports on Form 10-Q with the Commission on a regular basis, and will be required to disclose certain events in a timely manner (e.g., changes in corporate control; acquisitions or dispositions of a significant amount of assets other than in the ordinary course of business, etc.) in Current Reports on Form 8-K.

WE ARE SUBJECT TO THE REQUIREMENTS OF SECTION 404 OF THE SARBANES-OXLEY ACT OF 2002. IF WE ARE UNABLE TO TIMELY COMPLY WITH SECTION 404 OR IF THE COSTS RELATED TO COMPLIANCE ARE SIGNIFICANT, OUR PROFITABILITY, STOCK PRICE AND RESULTS OF OPERATIONS AND FINANCIAL CONDITION COULD BE MATERIALLY ADVERSELY AFFECTED.

The Company is required to comply with the provisions of Section 404 of the Sarbanes-Oxley Act of 2002, which requires that we document and test our internal controls and certify that we are responsible for maintaining an adequate system of internal control procedures for the 2019 and 2020 fiscal years. We are currently evaluating our existing controls against the standards adopted by the Committee of Sponsoring Organizations of the Treadway Commission. During the course of our ongoing evaluation and integration of the internal controls of our business, we may identify areas requiring improvement, and we may have to design enhanced processes and controls to address issues identified through this review (see Item 9A., below, for a discussion of our internal controls and procedures).

We believe that the out-of-pocket costs, the diversion of management’s attention from running the day-to-day operations and operational changes caused by the need to comply with the requirement of Section 404 of the Sarbanes-Oxley Act could be significant. If the time and costs associated with such compliance exceed our current expectations, our results of operations and the future filings of our Company could be materially adversely affected.

DEPENDENCE ON KEY EMPLOYEES.

The Company is heavily dependent on the abilities of our newly appointed President and CEO, Mr. Nicholas Tuke, and our Chief Financial Officer, Enzo Taddei. The loss of the services of Mr. Tuke and/or Mr. Taddei would seriously undermine our ability to carry out our business plan.

In the event of future growth in administration, advisory, marketing and customer support functions, the Company may have to increase the depth and experience of its management team by adding new members. The Company’s success will depend to a large degree upon the active participation of our key officers and employees, as well as the continued service of our key management personnel and our ability to identify, hire, and retain additional qualified personnel. There can be no assurance that we will be able to recruit such qualified personnel to enable us to conduct our proposed business successfully.

REPORTS TO SECURITY HOLDERS.

We are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and in accordance therewith, we file annual, quarterly and current reports, proxy and information statements and other information with the Securities and Exchange Commission. Such reports, proxy statements and other information can be read and copied at the Securities and Exchange Commission’s public reference facilities at 100 F Street, N.E., Washington, D.C. 20549, at prescribed rates. Please call the Securities and Exchange Commission at 1-800-732-0330 for further information on the operation of the public reference facilities. In addition, the Securities and Exchange Commission maintains a website that contains reports, proxy and information statements and other information regarding registrants that file electronically with the Securities and Exchange Commission. The address of the Securities and Exchange Commission’s website is www.sec.gov.

We make available free of charge on or through our website at www.arg47.com, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with or otherwise furnish it to the Securities and Exchange Commission. Information on our website is not incorporated by reference in this Annual Report and is not a part of this Annual Report.

| 13 |

An investment in our Common Stock involves a high degree of risk. Prospective investors should carefully consider the following risk factors and the other information in this Annual Report and in our other filings with the Securities and Exchange Commission (sometimes referred to herein as the “SEC”) before investing in our Common Stock. Our business and results of operations could be seriously harmed by any of the following risks. You should carefully consider the risks described below, the other information in this Annual Report and the documents incorporated by reference herein when evaluating our Company and our business. If any of the following risks actually occurs, our business could be harmed. In such case, the trading price of our Common Stock could decline and investors could lose all or a part of the money paid for our Common Stock.

INVESTING IN OUR COMMON STOCK INVOLVES A HIGH DEGREE OF RISK. IF ANY OF THE FOLLOWING RISKS ACTUALLY MATERIALIZES, OUR BUSINESS, FINANCIAL CONDITION AND RESULTS OF OPERATIONS WOULD SUFFER AND OUR SHAREHOLDERS COULD LOSE ALL OR PART OF THEIR INVESTMENT IN OUR SHARES.

RISKS ASSOCIATED WITH OUR COMPANY

THERE IS SUBSTANTIAL UNCERTAINTY THAT WE WILL CONTINUE OPERATIONS. IN THAT CASE, INVESTORS COULD LOSE THEIR INVESTMENTS IN OUR COMMON STOCK.

Our auditors have issued a going concern opinion. This means that there is substantial doubt that we can continue as an ongoing business for the next twelve months. The consolidated financial statements do not include any adjustments that might result from the uncertainty about our ability to continue in business. As such, we may have to cease operations and you could lose your investment.

WE ARE AN “EMERGING GROWTH COMPANY” AND WE CANNOT BE CERTAIN IF WE WILL BE ABLE TO MAINTAIN SUCH STATUS OR IF THE REDUCED DISCLOSURE REQUIREMENTS APPLICABLE TO EMERGING GROWTH COMPANIES WILL MAKE OUR COMMON STOCK LESS ATTRACTIVE TO INVESTORS.

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012 or “JOBS Act,” and we may adopt certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of 2002, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirement of holding a nonbinding advisory vote on executive and stockholder approval of any golden parachute payments not previously approved. We may remain an “emerging growth company” for up to five full fiscal years following our initial public offering of our common equity securities. Note: To date, we have not sold or issued any of our common equity securities under an effective Form S-1, Form S-3, Form S-4 or Form S-8 or other form of registration statement under the Securities Act of 1933, as amended. We would cease to be an emerging growth company, and, therefore, ineligible to rely on the above exemptions, if we have more than $1 billion in annual revenue in a fiscal year, if we issue more than $1 billion of non-convertible debt over a three-year period, or if we have more than $700 million in market value of our common stock held by non-affiliates as of June 30 in the fiscal year before the end of the five full fiscal years. Additionally, we cannot predict if investors will find our common stock less attractive because we may rely on these exemptions. If some investors find our common stock less attractive as a result of our reduced disclosures, there may be less active trading in our common stock and our stock price may be more volatile.

| 14 |

AS A RESULT OF OUR INTENSELY COMPETITIVE INDUSTRY, WE MAY NOT GAIN ENOUGH MARKET SHARE TO BE PROFITABLE.

The corporate consulting and funds management businesses are intensely competitive and due to our small size and limited resources, we may be at a competitive disadvantage, especially as a public company. There are several firms offering similar services. Many of our competitors have proven track records and substantial human and financial resources, as opposed to our Company who has limited human resources and little cash. Also, the financial burden of being a public company, which will cost us approximately U.S.$65,000 per year in auditing fees and legal fees to comply with our reporting obligations under the Securities Exchange Act of 1934 and compliance with the Sarbanes-Oxley Act of 2002, will strain our finances and stretch our human resources to the extent that we may have to price our consultancy service fees higher than our non-publicly held competitors just to cover the costs of being a public company.

WE ARE VULNERABLE TO THE CATASTROPHIC EVENTS WHICH MAY NEGATIVELY AFFECT OUR PROFITABILITY AND ABILITY TO CARRY OUT OUR BUSINESS PLAN.

We are potentially vulnerable to catastrophic events that could affect our profitability and our ability to carry out our business plan. For example, sudden disruptions in business conditions may result from terrorist attacks similar to the events of September 11, 2001 in the United States, many other terrorist attacks in Europe and the United States in the past three years, including further attacks, retaliation and the threat of further attacks or retaliation, war, civil unrest in the Middle East, chaotic immigration problems in Europe, adverse weather conditions or other natural disasters, such as hurricanes and tsunamis, pandemic situations such as the current COVID-19 virus spreading around the world, interruptions to the Internet or large scale power outages can have a short term or, sometimes, long term impact on spending.

BECAUSE OUR FORMER BUSINESS MODEL ANTICIPATED OUR RECEIVING EQUITY STAKES IN OUR CLIENTS, MOST OF WHOM WERE DEVELOPMENT STAGE COMPANIES, WE MAY NOT BE ABLE TO RESELL SUCH EQUITY AT SUITABLE PRICES, IF AT ALL, WHICH COULD MATERIALLY IMPACT OUR EARNINGS AND ABILITY TO REMAIN IN BUSINESS.

Our former business model anticipated that we would receive, as partial compensation for our consulting services, equity stakes in our clients, many of whom were development stage companies. We valued those equity stakes at the time we received them. Investments in development stage companies are risky because many of such companies’ securities are illiquid, thinly traded (if at all) and the value of such securities will be subject to adjustments should the value of such securities decline, should such securities be delisted from an exchange or cease being quoted on a stock quotation medium or should such businesses fail, which could cause us to write-down or write-off the value of such securities and result in a negative impact to our earnings and possibly cause us to cease or curtail our operations.

OUR SHAREHOLDERS MAY BE DILUTED THROUGH OUR EFFORTS TO OBTAIN FINANCING, FUND OUR OPERATIONS AND SATISFY OUR OBLIGATIONS THROUGH ISSUANCE OF ADDITIONAL SHARES OF OUR COMMON STOCK.

We will likely have to issue additional shares of our common Stock to fund our operations and to implement our plan of operation. Wherever possible, our board of directors will attempt to use non-cash consideration to satisfy obligations. In many instances, we believe that the non-cash consideration will consist of restricted shares of our common stock issued in lieu of cash. Our board of directors has authority, without action or vote of the shareholders, to issue all or part of the 359,010,591 authorized, but unissued, shares of our common stock. Future issuances of shares of our common stock will result in dilution of the ownership interests of existing shareholders, may further dilute common stock book value and that dilution may be material.

FINRA SALES PRACTICE REQUIREMENTS MAY LIMIT A STOCKHOLDER’S ABILITY TO BUY AND SELL OUR STOCK.

The FINRA has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low-priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may have the effect of reducing the level of trading activity and liquidity of our common stock. Further, many brokers charge higher transactional fees for penny stock transactions. As a result, fewer broker-dealers may be willing to make a market in our common stock, which may limit your ability to buy and sell our stock.

| 15 |

OUR ARTICLES OF INCORPORATION AUTHORIZE THE ISSUANCE OF PREFERRED STOCK.

Our Articles of Incorporation authorize the issuance of up to 50,000,000 shares of preferred stock with designations, rights and preferences determined from time to time by its Board of Directors. Accordingly, our Board of Directors is empowered, without stockholder approval, to issue preferred stock with dividend, liquidation, conversion, voting, or other rights which could adversely affect the voting power or other rights of the holders of the common stock.

We have 45,000,000 shares of Series “B” Preferred Stock outstanding at this time, which shares are owned by our management. We have 3,300,000 shares of Series “C” Preferred Stock outstanding at this time, 2,900.000 of which shares are owned by our management. All shares of our Series “B” and “C” Preferred Stock are contractually locked-up until September 27, 2020; hence, such shares cannot be sold or converted into common stock on any prior date.

We have an additional 1,700,000 shares of Series “C” Preferred Stock authorized and designated, but not issued or outstanding.

We no longer have any shares of Series “A” Preferred Stock authorized, designated or outstanding.

THIS ANNUAL REPORT CONTAINS FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO US, OUR INDUSTRY AND TO OTHER BUSINESSES.

These forward-looking statements in this Annual Report are based on the beliefs of our management, as well as assumptions made by and information currently available to our management. When used in this Annual Report, the words “estimate,” “project,” “believe,” “anticipate,” “intend,” “expect” and similar expressions are intended to identify forward-looking statements. These statements reflect our current views with respect to future events and are subject to risks and uncertainties that may cause our actual results to differ materially from those contemplated in our forward-looking statements. We caution you not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report. We do not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of this Annual Report or to reflect the occurrence of unanticipated events.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not applicable.

The Company does not own any property. Our executive offices are located at 34 St. Augustine’s Gate, Hedon, HU12 8EX, Hull, United Kingdom; we pay a monthly rent of U.S. $1,230 (1,000 GBP) for this office. Mr. Nicholas Tuke, our President and Chief Executive Officer and Mr. Peter Smith, a member of the Board of Directors, are both based in the United Kingdom, and Mr. Enzo Taddei, our Chief Financial Officer, is based on mainland Europe.

We are not subject to any other pending or threatened litigation.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

| 16 |

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

As of December 31, 2019, the Company’s Common Stock was quoted on the Over-the-Counter Bulletin Board under the symbol ARGQ. The market for the Company’s Common Stock is limited, volatile and sporadic and the price of the Company’s Common Stock could be subject to wide fluctuations in response to quarterly variations in operating results, news announcements, trading volume, sales of Common Stock by officers, directors and principal shareholders of the Company, general market trends, changes in the supply and demand for the Company’s shares, and other factors. The following table sets forth the high and low sales prices for each quarter relating to the Company’s Common Stock for the last two fiscal years. These quotations reflect inter-dealer prices without retail mark-up, markdown, or commissions, and may not reflect actual transactions.

| Fiscal 2019 | High | Low | ||||||

| First Quarter (1) | $ | 0.0042 | $ | 0.0029 | ||||

| Second Quarter (1) | $ | 0.0048 | $ | 0.0031 | ||||

| Third Quarter (1) | $ | 0.0039 | $ | 0.0022 | ||||

| Fourth Quarter (1) | $ | 0.0037 | $ | 0.0022 | ||||

| Fiscal 2018 | High | Low | ||||||

| First Quarter(1) | $ | 0.0071 | $ | 0.0035 | ||||

| Second Quarter (1) | $ | 0.0070 | $ | 0.0038 | ||||

| Third Quarter (1) | $ | 0.0084 | $ | 0.0040 | ||||

| Fourth Quarter (1) | $ | 0.0061 | $ | 0.0022 | ||||

| (1) | This represents the closing bid information for the stock on the OTC Bulletin Board. The bid and ask quotations represent prices between dealers and do not include retail markup, markdown or commission. They do not represent actual transactions and have not been adjusted for stock dividends or splits. |

The Securities and Exchange Commission has adopted Rule 15g-9 which establishes the definition of a “Penny Stock,” for purposes relevant to us, as any equity security that has a market price of less than $5.00 per share or with an exercise price of less than $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require: (i) that a broker or dealer approve a person’s account for transactions in penny stocks and (ii) the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased. In order to approve a person’s account for transactions in penny stocks, the broker or dealer must (i) obtain financial information and investment experience and objectives of the person; and (ii) make a reasonable determination that the transactions in penny stocks are suitable for that person and that person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks. The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prepared by the SEC relating to the penny stock market, which, in highlight form, (i) sets forth the basis on which the broker or dealer made the suitability determination and (ii) that the broker or dealer received a signed, written agreement from the investor prior to the transaction. Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading, and about commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements must be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

| 17 |

Shareholders should be aware that, according to SEC Release No. 34-29093 dated April 17, 1991, the market for penny stocks has suffered in recent years from patterns of fraud and abuse. Such patterns include (1) control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer; (2) manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases; (3) boiler room practices involving high-pressure sales tactics and unrealistic price projections by inexperienced sales persons; (4) excessive and undisclosed bid-ask differential and markups by selling broker dealers; and (5) the wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the resulting inevitable collapse of those prices and with consequent investor losses. The occurrence of these patterns or practices could increase the volatility of our share price.

Our management is aware of the abuses that have occurred historically in the penny stock market.

HOLDERS.

As of the date of this filing, there were 89 record holders of the shares of the Company’s issued and outstanding Common Stock.

DIVIDENDS.

The Company has not paid any cash dividends to date and does not anticipate or contemplate paying dividends in the foreseeable future. It is the present intention of management to utilize all available funds for the development of the Company’s business.

RECENT ISSUANCES OF UNREGISTERED SECURITIES

SECURITIES ISSUED IN 2020

In March 2020, the Company issued 100,000 shares of Series “C” Preferred Stock to Nicholas Tuke, our new Chief Executive Officer, as a signing bonus.

All of the foregoing stock was issued in reliance on the exemption from registration requirements of the 33 Act provided by Section 4.(a)(2) of the 33 Act and/or the exclusion from registration requirements of the 33 Act provided by Regulation S promulgated under the 33 Act.

SECURITIES ISSUED IN 2019

On January 14, 2019, the Company issued 21,200,000 common shares valued at a contractually agreed value of $0.02 per share or $424,000 (including $400,000 of principal and $24,000 of accrued interest) to Xantis Aion Securitisation Fund (at Xantis Private Equity Fund´s request) upon conversion of a convertible promissory note.

On January 24, 2019, the Company issued 5,300,000 common shares valued at a contractually agreed value of $0.02 per share or $106,000 (including $100,000 of principal and $6,000 of accrued interest) to William Marshal Plc. upon conversion of a convertible promissory note.

On June 9, 2019, the Company issued 38,955,000 common shares valued at a contractually agreed value of $0.02 per share or $779,100 (including $735,000 of principal and $44,100 of accrued interest) to Xantis Aion Securitisation Fund upon conversion of a convertible promissory note.

All of the foregoing stock was issued in reliance on the exemption from registration requirements of the 33 Act provided by Section 4.(a)(2) of the 33 Act and/or the exclusion from registration requirements of the 33 Act provided by Regulation S promulgated under the 33 Act.

| 18 |

SECURITIES ISSUED IN 2018

We did not issue any shares of our Common Stock in 2018.

We issued 800,000 shares of Series “C” Preferred stock in 2018 to two of our officers in lieu of accrued salaries. These preferred shares are contractually locked up until September 27, 2020.

SECURITIES ISSUED IN 2017

On February 2, 2017, the Company issued 5,000,000 common shares valued at an agreed value of $0.01 per share or $50,000 to Mammoth Corporation upon conversion of a portion of a convertible promissory note.

On March 28, 2017, the Company issued 6,178,560 common shares valued at an agreed value of $0.0080925 per share or $50,000 to Mammoth Corporation upon conversion of a portion of a convertible promissory note.

On April 13, 2017, the Company issued 10,224,676 common shares valued at an agreed value of $0.006565 per share or $67,125, with the common shares valued at their fair value of $133,652 based on the quoted trading price, to Mammoth Corporation upon conversion of a portion of a convertible promissory note.

On May 12, 2017, the Company issued 7,823,310 common shares valued at an agreed value of $0.00429 per share or $33,562, with the common shares valued at their fair value of $88,543 based on the quoted trading price, to Mammoth Corporation upon conversion of a portion of a convertible promissory note.

On June 2, 2017, the Company issued 9,388,252 common shares valued at an agreed value of $0.003575 per share or $33,563, with the common shares valued at their fair value of $92,133 based on the quoted trading price, to Mammoth Corporation upon conversion of remaining portion of a convertible promissory note.

On July 10, 2017, the Company issued 10,000,000 common shares valued at an agreed value of $0.00234 per share or $23,400, with the common shares valued at their fair value of $54,795 based on the quoted trading price, to Mammoth Corporation upon conversion of a portion of a convertible promissory note.

On August 2, 2017, the Company issued 10,000,000 common shares valued at an agreed value of $0.00204 per share or $20,400, with the common shares valued at their fair value of $51,940 based on the quoted trading price, to Mammoth Corporation upon conversion of a portion of a convertible promissory note.

On September 11, 2017, the Company issued 20,000,000 common shares valued at an agreed value of $0.00169 per share or $33,800, with the common shares valued at their fair value of $102,533 based on the quoted trading price, to Mammoth Corporation upon conversion of a portion of a convertible promissory note.

On October 25, 2017, the Company issued 20,000,000 common shares valued at an agreed value of $0.00108 per share or $21,600, with the common shares valued at their fair value of $59,820 based on the quoted trading price, to Mammoth Corporation upon conversion of a portion of a convertible promissory note.

On December 4, 2017, the Company issued 47,000,000 common shares valued at an agreed value of $0.0013362 per share or $62,800, with the common shares valued at their fair value of $313,400 based on the quoted trading price, to Mammoth Corporation upon conversion of final portion of a convertible promissory note.

On December 27, 2017, the Company issued 5,443,836 common shares valued at an agreed value of $0.012 per share or $65,326, with the common shares valued at their fair value of $27,764 based on the quoted trading price, to private investor based in Malta upon conversion of a convertible promissory note.

All of the foregoing stock was issued in reliance on the exemption from registration requirements of the 33 Act provided by Section 4.(a)(2) of the 33 Act and/or the exclusion from registration requirements of the 33 Act provided by Regulation S promulgated under the 33 Act.

| 19 |

ISSUER REPURCHASES OF EQUITY SECURITIES

None.

ITEM 6. SELECTED FINANCIAL DATA.

Not applicable.

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION. |

CAUTIONARY FORWARD - LOOKING STATEMENT

The following discussion and analysis of the results of operations and financial condition of Argentum 47, Inc. should be read in conjunction with our financial statements and related notes. References to “we”, “our,” or “us” in this section refers to the Company and its subsidiaries. Our discussion includes forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. We use words such as “anticipate”, “estimate”, “plan”, “project”, “continuing”, “ongoing”, “expect”, “believe”, “intend”, “may”, “will”, “should”, “could”, and similar expressions to identify forward-looking statements.

Certain matters discussed herein may contain forward-looking statements that are subject to risks and uncertainties. Such risks and uncertainties include, but are not limited to, the following:

| ● | the volatile and competitive nature of our industry, | |

| ● | the uncertainties surrounding the rapidly evolving markets in which we compete, | |

| ● | the uncertainties surrounding technological change of the industry, | |

| ● | our dependence on our intellectual property rights, | |

| ● | the success of marketing efforts by third parties, | |

| ● | the changing demands of customers, | |

| ● | uncertainties due to the current pandemic COVID-19 virus on the global market and its possible impact on the Company’s business, and | |

| ● | the arrangements with present and future customers and third parties. |

Should one or more of these risks or uncertainties materialize or should any of the underlying assumptions prove incorrect, actual results of current and future operations may vary materially from those anticipated.

Our MD&A is comprised of the following sections:

| A. | Critical accounting estimates and policies. | |

| B. | Business overview. | |

| C. | Results of operations for the years ended December 31, 2019 and 2018. | |

| D. | Financial condition as at December 31, 2019 and 2018. | |

| E. | Liquidity and capital reserves. | |

| F. | Business development. |

| A. | Critical Accounting Estimates and Policies: |

Our consolidated financial statements are prepared in accordance with generally accepted accounting principles in the United States (“GAAP”), which requires management to make estimates and assumptions that affect reported and disclosed amounts of assets and liabilities and the reported amounts of revenues and expenses during the reporting period.

| 20 |

We believe that the critical accounting policies set forth in the accompanying consolidated financial statements describe the more significant judgments and estimates used in the preparation of our consolidated financial statements. These critical accounting policies pertain to revenues recognition, valuation of investments, convertible notes and derivatives and stock-based compensation.

If actual events differ significantly from the underlying judgments or estimates used by management in the application of these accounting policies, there could be a material effect on our results of operations and financial condition.

| B. | Business overview: |

Argentum 47, Inc. (“Company” or “ARG”) was incorporated on October 1, 2010, as a Nevada corporation, for the express purpose of acquiring Global Equity Partners Plc., a corporation formed under the laws of the Republic of Seychelles (“GEP”) on September 2, 2009. On August 22, 2014, GE Professionals DMCC was incorporated in Dubai as a wholly owned subsidiary of Global Equity Partners Plc. On June 10, 2016, ARG incorporated its wholly owned subsidiary, called GEP Equity Holdings Limited, under the laws of the Republic of Seychelles.

On March 24, 2017, the Board of Directors of Global Equity Partners Plc. approved the assignment and transfer of GE Professionals DMMC to GEP Equity Holdings Limited.

On June 5, 2017, the Company sold 100% of the common stock of Global Equity Partners Plc. to a private citizen of the Kingdom of Thailand. The consideration for the purchase of Global Equity Partners Plc. was the assumption by the purchaser of all liabilities and indebtedness of Global Equity Partners Plc. in the approximate amount of $626,000. At the time of this sale, Global Equity Partners Plc. had assets consisting of common shares of other companies having a book value of approximately $603,000.

GEP Equity Holdings Limited provides consulting services, such as corporate restructuring, Exchange Listings and development for corporate marketing, investor and public relations, regulatory compliance and introductions to financiers, to companies desiring to be listed on stock exchanges in various parts of the world.

On December 12, 2017, we incorporated a United Kingdom company under the name of Argentum 47 Financial Management Limited (“Argentum FM”). Argentum FM is a wholly owned subsidiary of the Company. Argentum FM was formed to serve as a holding company for the acquisition of United Kingdom based advisory firms. During 2019, the Company intends to acquire more licensed financial advisory firms.

On January 12, 2018, the Company secured a 12-month fixed price convertible loan from Xantis Private Equity Fund (Luxembourg) for a minimum of 2,000,000 Great Britain Pounds (equivalent to approximately U.S. $2,680,000) carrying an interest at the rate of 6% per annum. The Company has a right to pay this note on the maturity date by issuing shares of common stock at a conversion price equal to the greater of $0.02 or the average closing price of the Company’s common stock on the OTCBB for the prior 60 trading days. To date, the Company received $400,000 under this loan, which including the accrued interest of $24,000 was converted into 21,200,000 shares of the Company’s common stock on January 14, 2019.

On January 12, 2018, the Company secured a 12-month fixed price convertible loan from William Marshal Plc., a United Kingdom Public Limited Company listed on the Cyprus Public Exchange Emerging Companies Market, for a maximum of 2,000,000 Great Britain Pounds (equivalent to approximately U.S. $2,680,000) carrying an interest at the rate of 6% per annum. The Company has a right to pay this note on the maturity date, by issuing shares of common stock at a conversion price equal to the greater of $0.02 or the average closing price of the Company’s common stock on the OTCBB for the prior 60 trading days. To date, the Company received $100,000 under this loan, which including the accrued interest of $6,000 was converted to 5,300,000 common shares of the Company on January 24, 2019.

| 21 |

On March 29, 2018, we changed our corporate name to Argentum 47, Inc.

On June 6, 2018, the Company secured a 12-month fixed price convertible loan, from Xantis Aion Securitization Fund (Luxembourg), for a minimum of 1,700,000 Great Britain Pounds (equivalent to approximately $1,940,000) carrying an interest at the rate of 6% per annum. The Company has a right to pay this note on earlier than 366 days’ post investment of each tranche of funding, by issuing common shares at a conversion price equal to the greater of $0.02 or the average closing ask price of the Company’s common stock on the OTCBB for the prior 60 trading days. To date, the Company has received $1,388,040 under this loan, of which $735,000 and related accrued interest was converted into 38,955,000 shares of the Company’s common stock on June 5, 2019.

On August 1, 2018, Argentum FM consummated a Share Purchase Agreement with Mr. Rodney Leonard and Equilibrium Pensions Limited (trustees of The Leonard R. Personal Pension), pursuant to which Argentum FM would acquire 100% of the ordinary shares (equity) of Cheshire Trafford (U.K.) Limited of Hull, United Kingdom (“Cheshire Trafford”) from Mr. Leonard and Equilibrium Pensions Limited (trustees of The Leonard R. Personal Pension).

In March 2019, Management decided that it made overall economic sense for the Company to close its employment placement services business in Dubai; hence, on March 18, 2019, in order to fully concentrate on its core business of Independent Financial Advisory services and Consultancy Business, the Board of Directors decided to initiate liquidation proceedings of the Dubai subsidiary “GE Professionals DMCC” (with an effective date of March 31, 2019). As a result of this decision to liquidate the subsidiary, the Board of Directors also decided to discontinue its Human Resources and Placement business in Dubai. On February 11, 2020, the deregistration and liquidation process of our Dubai subsidiary was formally completed.

Cheshire Trafford (U.K.) Limited (www.cheshire-trafford.co.uk) was incorporated under the laws of the United Kingdom on January 26, 1976, as a limited liability company. Cheshire Trafford is a very well established and UK FCA regulated Independent Financial Advisory firm that offers a fully computerized investment management service, including advising on investments in Unit Trusts, Investment Bonds, Shares, Investment Trusts, Government Bonds and Individual Savings Accounts. In addition, Cheshire Trafford advises investors on various types of Pension contracts, including Personal Pensions, Executive Pensions, Small Self-Administered Plans, Pension Mortgages and many more.

Cheshire Trafford acts as a broker for the sale of Lump Sum or Single Premium Insurance Policies and Regular Premium Investment or “Insurance” Policies that are issued by reputable third-party insurance companies.

Cheshire Trafford currently has four full time employees and approximately 430 clients that have authorized our company to administrate between $8,000 and $650,000 of their money.

The funds that Cheshire Trafford currently has under administration are invested with well-known and reputable Investment Houses such as:

| ● | AJ Bell | |

| ● | Canada Life International | |

| ● | Fidelity International | |

| ● | Old Mutual International | |

| ● | Old Mutual Wealth Life | |

| ● | Royal London | |

| ● | Aviva | |

| ● | Prudential Assurance |

Cheshire Trafford’s primary customer base resides in the United Kingdom. Cheshire Trafford is licensed (Register Number 115194) and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom. Confirmation of Cheshire Trafford’s license can be made by visiting the FCA’s website: www.fca.gov.uk/register.

| 22 |

The purchase consideration for the acquisition of Cheshire Trafford is based on a formula of 2.7 times Cheshire Trafford’s projected annualized recurring revenues for the calendar year ending December 31, 2018. We took the gross revenues of Cheshire Trafford for the five months ended May 31, 2018 and annualized those recurring revenues and multiplied those revenues by 2.7 times in arriving at the contractual purchase consideration of U.S.$516,795 (389,300 Great Britain Pounds or “GBP”).