Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2012

Or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 333-177498

RXi PHARMACEUTICALS CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 45-3215903 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

1500 West Park Drive, Suite 210 Westborough, Massachusetts 01581

(Address of principal executive offices and Zip Code)

(508) 767-3861

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of exchange on which registered | |

| None | None |

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class

Common Stock

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on it corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for any such shorter time that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | x | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): ¨ Yes x No

The aggregate market value of the voting common stock held by non-affiliates of the registrant, based on the closing sale price of the registrant’s common stock as reported on OTCQB on June 30, 2012, was approximately $10,537,000.

As of March 15, 2013, RXi Pharmaceuticals Corporation had 321,627,134 shares of common stock, $0.0001 par value, outstanding.

Documents incorporated by reference:

Portions of the registrant’s definitive proxy statement for its 2013 annual meeting of stockholders, to be filed with the Securities and Exchange Commission not later than 120 days after the registrant’s fiscal year end of December 31, 2012, are incorporated by reference into Part III in this Form 10-K.

Table of Contents

RXI PHARMACEUTICALS CORPORATION

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended December 31, 2012

| Page | ||||||

| Item 1. | 2 | |||||

| Item 1A. | 14 | |||||

| Item 1B. | 25 | |||||

| Item 2. | 25 | |||||

| Item 3. | 25 | |||||

| Item 4. | 25 | |||||

| Item 5. | 25 | |||||

| Item 6. | 26 | |||||

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

26 | ||||

| Item 7A. | 36 | |||||

| Item 8. | F-1 | |||||

| Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURES |

II-1 | ||||

| Item 9A. | II-1 | |||||

| Item 9B. | II-1 | |||||

| Item 10. | II-2 | |||||

| Item 11. | II-2 | |||||

| Item 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

II-2 | ||||

| Item 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

II-2 | ||||

| Item 14. | II-2 | |||||

| Item 15. | II-3 | |||||

| Signatures | II-4 | |||||

Table of Contents

FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as “intends,” “believes,” “anticipates,” “indicates,” “plans,” “intends,” “expects,” “suggests,” “may,” “should,” “potential,” “designed to,” “will” and similar references. Such statements include, but are not limited to, statements about: our ability to successfully develop RXI-109 and our other product candidates; the future success of our clinical trials with RXI-109; the timing for the commencement and completion of clinical trials; and our ability to implement cost-saving measures. Forward-looking statements are neither historical facts nor assurances of future performance. These statements are based only on our current beliefs, expectations and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy and other future conditions. Because forward-looking statements relate to the future, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict and many of which are outside of our control. Our actual results and financial condition may differ materially from those indicated in the forward-looking statements. Therefore, you should not rely on any of these forward-looking statements. Important factors that could cause our actual results and financial condition to differ materially from those indicated in the forward-looking statements include, among others: the risk that our clinical trials with RXI-109 may not be successful in evaluating the safety and tolerability of RXI-109 or providing preliminary evidence of surgical scar reduction; the successful and timely completion of clinical trials; uncertainties regarding the regulatory process; the availability of funds and resources to pursue our research and development projects, including our clinical trials with RXI-109; general economic conditions; and those identified in this Annual Report on Form 10-K under the heading “Risk Factors” and in other filings the Company periodically makes with the Securities and Exchange Commission. Forward-looking statements contained in this Annual Report on Form 10-K speak as of the date hereof and the Company does not undertake to update any of these forward-looking statements to reflect a change in its views or events or circumstances that occur after the date of this Annual Report on Form 10-K.

1

Table of Contents

| ITEM 1. | BUSINESS |

Overview

We are a biotechnology company focused on discovering, developing and commercializing innovative therapies based on our proprietary, new-generation RNA interference (“RNAi”) platform. Therapeutics that use RNAi have great promise because of their ability to “silence,” or down-regulate, the expression of a specific gene that may be over-expressed in a disease condition. Prior to September 8, 2011, our business was operated as an unincorporated division within Galena Biopharma, Inc. (“Galena” or the “Parent Company”), our former parent company. We were incorporated in Delaware as a wholly owned subsidiary of Galena on September 8, 2011 in preparation for our planned spin-off from Galena, which was completed on April 27, 2012. Since that date, we have operated as an independent, publicly traded company.

By utilizing the expertise in RNAi and the comprehensive RNAi platform that we have established, we believe that we will be able to discover and develop lead compounds and progress them into and through clinical development for potential commercialization. Our proprietary therapeutic platform is comprised of novel RNAi compounds, referred to as rxRNA® compounds, that are distinct from, and we believe convey significant advantages over, classic siRNA (conventionally-designed “small interfering RNA” compounds), and offer many of the properties that we believe are important to the clinical development of RNAi-based drugs. We have developed a number of unique forms of rxRNA® compounds, all of which have been shown to be highly potent both in vitro and in preclinical in vivo models. These RNAi compounds include rxRNAori® and sd-rxRNA®, or “self-delivering” RNA. Based on our research, we believe that these different, novel siRNA configurations have various potential advantages for therapeutic use. These potential advantages include high potency, increased resistance to nucleases and off-target effects, and, in the case of the sd-rxRNA® compounds, access to cells and tissues with no additional formulation required, and, hence, reduced cell toxicity, which is known to be an issue with unmodified siRNAs.

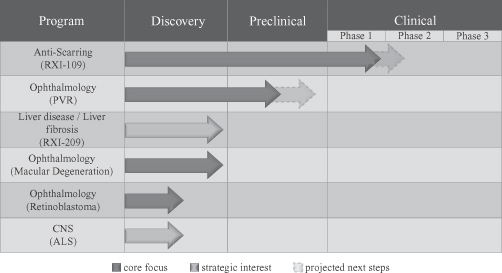

Our Therapeutic Pipeline

The following is a summary of our therapeutic development programs.

RXI-109 Clinical Development Program

Our lead clinical product candidate is RXI-109, a self-delivering RNAi compound (sd-rxRNA®) being developed for the reduction of dermal scarring in planned surgeries. RXI-109 is designed to reduce the

2

Table of Contents

expression of connective tissue growth factor (“CTGF”), a critical regulator of several biological pathways involved in scarring and fibrotic diseases. RXI-109 is being developed to prevent or reduce dermal scarring following surgery or trauma, as well as for the management of hypertrophic scars and keloids.

In June 2012, we initiated our first clinical trial of RXI-109, known as Study 1201. Study 1201 was designed to evaluate the safety and tolerability of several dose levels of RXI-109 in humans and may provide preliminary evidence of reduction of surgical scarring. Study 1201 enrolled fifteen subjects in a single-center, randomized, single-dose, double-blind, ascending dose, within-subject controlled study of RXI-109 for the treatment of incision scars, during which single, intradermal injections of escalating doses were administered. Subjects received an injection of RXI-109 in 2 separate areas on the abdomen and placebo injections in two other areas of the abdomen. RXI-109 was well tolerated by intradermal injection. No serious local or systemic side effects were observed in the subjects at any of the doses administered, and maximum systemic exposure after intradermal administration was assessed at approximately 5% of the total dose administered.

In December 2012, we initiated a second Phase 1 clinical trial with RXI-109, known as Study 1202. Study 1202 was designed to evaluate the safety of multi-dose administration of RXI-109 in healthy volunteers, including an evaluation of surrogate end points of clinical efficacy. Nine subjects (3 cohorts of 3 subjects each) were enrolled in a single-center, randomized, multi-dose, double-blind, ascending dose, within-subject controlled study of RXI-109 for the treatment of incision scars, during which subjects received intradermal injections of RXI-109. Subjects received injections of RXI-109 in 4 separate areas of the abdomen and placebo injections in four other areas of the abdomen, all of which were administered on multiple occasions over multiple weeks.

While the primary focus of Studies 1201 and 1202 is to establish the safety and tolerability of RXI-109 in healthy subjects, there are also several surrogate end points being evaluated that may provide evidence of surgical scar prevention.

In Study 1201, RXI-109 has shown excellent safety and tolerability with ascending single doses. Study 1202 uses multiple doses and is designed to evaluate the safety and side effects of those doses, while also exploring possible effects of RXI-109 on the healing process. We expect to report topline results from Study 1201 in the second quarter of 2013 and from Study 1202 in mid-2013. In the second half of 2013, we expect to initiate Phase 2 clinical trials in which RXI-109 is administered following scar revision surgery.

As there are currently no Food and Drug Administration (“FDA”)-approved drugs to prevent scar formation, a therapeutic of this type could have great benefit for trauma and surgical patients, as a treatment during the surgical revision of existing unsatisfactory scars, and in the treatment, removal and inhibition of keloids (scars that extend beyond the original skin injury).

Future Novel Applications of RXI-109

Abnormal overexpression of CTGF is implicated in dermal scarring and fibrotic disease, and because of this, we believe that RXI-109 or other CTGF-targeting RNAi compounds may be able to treat other fibrotic indications, including pulmonary fibrosis, liver fibrosis, acute spinal injury, ocular scarring and vascular restenosis. If the current clinical trials of RXI-109 produce successful results in dermal anti-scarring, we may explore opportunities in these additional indications, as well as other possible dermatology applications (e.g., cutaneous scleroderma).

Other Development Programs

While focusing our efforts on our RXI-109 development program, we also intend to continue to advance additional development programs both on our own and through collaborations with academic and corporate third parties. Current programs in the discovery and preclinical stages include:

| • | a collaboration with Dr. Robert Brown at the University of Massachusetts Medical School (“UMMS”) for the treatment of amyotrophic lateral sclerosis (“ALS”); |

3

Table of Contents

| • | a Small Business Innovation Research (“SBIR”) grant to evaluate and develop sd-rxRNAs® as potential therapeutics for the treatment of retinoblastoma; and |

| • | a collaboration evaluating the potential to use a CTGF-targeting sd-rxRNA® as a therapeutic to reduce or inhibit retinal scarring, which often occurs as a consequence of some retinal diseases and following retinal detachment. |

On March 1, 2013, we entered into an asset purchase agreement with OPKO Health, Inc. (“OPKO”) pursuant to which we have acquired substantially all of OPKO’s RNAi-related assets, including patents, licenses, clinical and preclinical data and other assets (the “OPKO Asset Purchase”). The assets purchased from OPKO are at an early stage of development, and we expect to commence development work with preclinical testing to identify potential lead compounds and targets.

Market Opportunity

There are currently no FDA-approved therapeutics in the United States for the treatment and prevention of scars in the skin. However, there are over 42 million procedures in the United States each year that could benefit from a therapeutic that could successfully reduce or prevent scarring; thus, the market potential is quite large. In addition to cosmetic and reconstructive surgeries, medical interventions which could incorporate an anti-scarring agent include scarring that results from trauma, surgery or burns (especially relating to raised or hypertrophic scarring or contracture scarring), surgical revision of existing unsatisfactory scars, and in the treatment, removal and inhibition of keloids (scars which extend beyond the original skin injury).

Recent Business Developments

During 2012 and in the first quarter of 2013, we announced several important developments that are outlined below.

| • | In April 2012, we completed the offering and sale of our Series A Convertible Preferred Stock. Pursuant to the Securities Purchase Agreement (the “Series A SPA”), dated as of September 24, 2011, by and among the Company, Galena, and Tang Capital Partners, LP (“TCP”) and RTW Investments, LLC (“RTW” and together with TCP, the “Investors”), on April 27, 2012, the Investors purchased a total of 9,500 shares of Series A Preferred Stock in consideration for $9.5 million, payable in cash and through the extinguishment of approximately $1 million of aggregate indebtedness owed to the Investors by the Company. |

| • | In April 2012, we completed our spinoff from Galena. |

| • | In May 2012, our common stock began trading under the symbol “RXII” on the OTC Bulletin Board. |

| • | In May 2012, we presented new preclinical data at the annual meeting of the Association for Research in Vision and Ophthalmology (ARVO). The preclinical data showed a reduction of VEGF mRNA as a consequence of targeted reduction of CTGF in the rodent retina following intraocular administration of RXI-109. |

| • | In June 2012, we appointed two independent directors to our Board of Directors, Mr. Robert Bitterman and Mr. Keith Brownlie. |

| • | In June 2012, we initiated Study 1201, our first clinical trial with RXI-109. The trial is designed to evaluate the safety and tolerability of several single-dose levels of RXI-109 in humans and may also provide preliminary evidence of reduction of surgical scarring. |

| • | In July 2012, we appointed two new members to our Scientific Advisory Board (“SAB”), Dr. Jeannette Graf, M.D. and Dr. Leroy Young, M.D., and re-appointed Craig Mello, Ph.D., Nobel Laureate for the discovery of the RNAi mechanism, as Chairman of the SAB. |

4

Table of Contents

| • | In September 2012, we received an SBIR grant from the National Cancer Institute (“NCI”) of the National Institutes of Health (“NIH”). The grant provides approximately $300,000 in funding for a project enabling the discovery and preclinical development of sd-rxRNAs® as potential therapy for retinoblastoma, a pediatric ocular malignancy. The project will be completed in collaboration with Dr. David Cobrinik and colleagues at USC Children’s Hospital, Los Angeles and the Memorial Sloan-Kettering Cancer Center. |

| • | In December 2012, we initiated Study 1202, our second Phase 1 clinical trial of RXI-109. Study 1202 is designed to evaluate the safety and tolerability of multi-dose administration of RXI-109 in healthy volunteers and may also provide preliminary evidence of reduction of surgical scarring. |

| • | In March 2013, we entered into an asset purchase agreement with OPKO pursuant to which we have acquired substantially all of OPKO’s RNAi-related assets, including patents, licenses, clinical and preclinical data and other assets. |

| • | In March 2013, we raised $16.4 million in a financing led by OPKO Health, Inc. and Frost Gamma Investments Trust, a trust controlled by Phillip Frost, M.D., as described more fully below. |

Financial Condition

We have generated significant losses to date. Additionally, we have not generated any product revenue to date and may not generate product revenue in the foreseeable future, if ever. We expect to incur significant operating losses as we advance our product candidates through the drug development and regulatory process. We will need to generate significant revenues to achieve profitability and might never do so. In the absence of product revenues, our potential sources of operational funding are expected to be the proceeds from the sale of equity, funded research and development payments and payments received under partnership and collaborative agreements.

On March 6, 2013, we entered into a securities purchase agreement (the “Common Stock SPA”) pursuant to which we agreed to issue 112,956,011 shares of our common stock at a price of $0.145 per share (the “March 2013 Offering”). The gross proceeds from the March 2013 Offering, which closed on March 12, 2013, were approximately $16.4 million, and the net proceeds to us, after payment of commissions, were approximately $16.0 million. We intend to use the proceeds from the March 2013 Offering for general corporate purposes, including the advancement of our RXI-109 program, research and development and general and administrative expenses.

We believe that our existing cash and cash equivalents, including the proceeds from the March 2013 Offering, should be sufficient to fund our operations, including the Phase 2 program for RXI-109, into fiscal 2015. In the future, we will be dependent on obtaining funding from third parties, such as proceeds from the sale of equity, funded research and development programs and payments under partnership and collaborative research and business development agreements, in order to maintain our operations and meet our obligations to licensors. There is no guarantee that debt, additional equity or other funding will be available to us on acceptable terms, or at all. If we fail to obtain additional funding when needed, we would be forced to scale back, or terminate, our operations or to seek to merge with or to be acquired by another company.

Introduction to the Field of RNAi Therapeutics

RNAi is a naturally occurring phenomenon where short, double-stranded RNA molecules interfere with the expression of targeted genes. RNAi technology takes advantage of this phenomenon and potentially allows us to effectively interfere with particular genes within living cells by designing RNA-derived molecules targeting those genes.

RNAi offers a novel approach to the drug development process because, as described below under “The RNAi Mechanism,” RNAi compounds can potentially be designed to target any one of the thousands of human genes, many of which are “undruggable” by other modalities. The specificity of RNAi is achieved by an intrinsic, well-understood biological mechanism based on designing the sequence of an RNAi compound to match the

5

Table of Contents

sequence of the targeted gene. The sequence of the entire human genome is now known, and the mRNA coding sequence for many proteins is already available. Supported by numerous gene-silencing reports and our own research, we believe that this sequence information can be used to design RNAi compounds to interfere with the expression of almost any specific gene.

The RNAi Mechanism

The genome is made of a double-strand of DNA (the double helix) that acts as an instruction manual for the production of the roughly 30,000 to 50,000 human proteins. Proteins are important molecules that allow cells and organisms to live and function. With rare exceptions, each cell in the human body has the entire complement of genes. However, only a subset of these genes directs the production of proteins in any particular cell type. For example, a muscle cell produces muscle-specific protein, whereas a skin cell does not.

In order for a gene to guide the production of a protein, it must first be copied into a single-stranded chemical messenger (messenger RNA or mRNA), which is then translated into protein. RNAi is a naturally occurring process by which a particular messenger RNA can be destroyed before it is translated into protein. The process of RNAi can be artificially induced by introducing a small, double-stranded fragment of RNA corresponding to a particular messenger RNA into a cell. A protein complex within the cell called RISC (RNA-Induced Silencing Complex) recognizes this double-stranded RNA fragment and binds to it. RISC then splits the double strands apart, retaining one strand in the RISC complex. The RISC then helps this guide strand of RNA bind to and destroy its corresponding cellular messenger RNA target. Thus, RNAi provides a method to potentially block the creation of the proteins that cause disease.

Since gene expression controls most cellular processes, the ability to inhibit gene expression provides a potentially powerful tool to treat human diseases. Furthermore, since the human genome has already been decoded, and based on numerous gene-silencing reports, we believe that RNAi compounds can readily be designed to interfere with the expression of any specific gene. Based on our internal research and our review of certain scientific literature, we also believe that our RNAi platform may allow us to develop therapeutics with significant potential advantages over therapeutics developed using traditional methods, including:

| • | High specificity for targeted genes; |

| • | High potency (low doses); |

| • | Ability to interfere with the expression of potentially any gene; |

| • | Accelerated generation of lead compounds; and |

| • | Low toxicity due to a natural mechanism of action. |

RXi’s RNAi Therapeutic Platform

RNAi Compound Design

Synthetic RNAi compounds are made from a strand or strands of RNA that are manufactured by a nucleic acid synthesizer. The synthesizer is programmed to assemble a strand of RNA of a particular sequence using primarily four nucleotide units (Adenine (“A”), Uracil (“U”), Cytidine (“C”) and Guanosine (“G”)) that match a small segment of the targeted gene. The hallmark of an RNAi compound is that it has a double-stranded region. The compounds can be of various lengths of nucleotide units (nt) and can contain various modifications of the nucleotide units or linkages. The two strands can have overhangs or blunt ends. A single strand can form an RNAi compound by forming a structure referred to as a hairpin.

The length and shape of the compound can affect the activity and hence the potency of the RNAi in cells. The first design of RNAi compounds to be pursued for development as human therapeutics were short, double-stranded RNAs that included at least one overhanging single-stranded region and limited modifications, known as small-interfering RNA, or siRNA, which we also refer to as classic siRNA.

6

Table of Contents

We believe that classic siRNAs have drawbacks that may limit the usefulness of those agents as human therapeutics, and that we may be able to utilize the technologies we have licensed and developed internally to optimize RNAi compounds for use as human therapeutic agents. It is the combination of the length, the nucleotide sequence and the configuration of chemical modifications that are important for effective RNAi therapeutics.

Our internal research leads us to believe that next generation rxRNA® compounds offer significant advantages over classic siRNA used by other companies developing RNAi therapeutics, highlighted by the following characteristics:

| • | Potent RNAi activity; |

| • | More resistant to nuclease degradation; |

| • | Readily manufactured; |

| • | Potentially more specific for the target gene; |

| • | More reliable at blocking immune side effects than classic siRNA; and |

| • | In the case of sd-rxRNA®, the unique ability to be “self-delivering,” without the need for any additional delivery vehicle. |

Based on our own research, we have developed a variety of novel siRNA configurations with potential advantages for therapeutic use. The first of these has been termed rxRNAori®. This configuration has some similarities to classic siRNA in that it is composed of two, short RNA strands. We have found that by using a somewhat longer length (25-29 bp), removing the overhangs and using proprietary chemical modification patterns, we achieve a higher hit rate of very potent (picomolar potency) compounds in a given target sequence. These rxRNAori® compounds are modified to increase resistance to nucleases and to prevent off-target effects including induction of an immune response. These novel RNAi compounds are distinct from the siRNA compounds used by many other companies developing RNAi therapeutics in that they are designed specifically for therapeutic use and offer many of the properties that we believe are important to the clinical development of RNAi-based drugs.

The second novel configuration has been called “sd-rxRNA” to indicate its novel “self-delivering” properties, which make additional delivery vehicles unnecessary for efficient cellular uptake and RISC-mediated silencing. A combination of at least three characteristics is required for activity: (1) specific, proprietary chemical modifications; (2) a precise number of chemical modifications; and (3) reduction in oligonucleotide content. Kinetic analyses of fluorescently-labeled compounds demonstrate that efficient cellular internalization is observed within minutes of exposure. These molecules are taken up efficiently and cause target gene silencing in diverse cell types (cell lines and primary cells). This novel class of RNAi compounds may afford a broad opportunity for therapeutic development.

We believe that both chemical modification and formulation of RNAi compounds may be utilized to develop RNA drugs suitable for therapeutic use. The route by which an RNAi therapeutic is brought into contact with the body depends on the intended organ or tissue to be treated. Delivery routes can be simplified into two major categories: (1) local (when a drug is delivered directly to the tissue of interest); and (2) systemic (when a drug accesses the tissue of interest through the circulatory system). Local delivery may avoid some hurdles associated with systemic approaches such as circulation clearance and tissue extravasation (crossing the endothelial barrier from the blood stream). However, the local delivery approach can only be applied to a limited number of organs or tissues (e.g., skin, eye, lung and potentially the central nervous system).

The key to therapeutic success with RNAi lies in delivering intact RNAi compounds to the target tissue and the interior of the target cells. To accomplish this, we have developed a comprehensive platform that includes local and systemic delivery approaches. We work with chemically synthesized RNAi compounds that are

7

Table of Contents

optimized for stability and efficacy and combine delivery at the site of action and formulation with delivery agents to achieve optimal delivery to specific target tissues.

Local Delivery

sd-rxRNA® molecules have unique properties that improve tissue and cell uptake. Delivery of sd-rxRNA® by a local route of administration may avoid hurdles associated with systemic approaches such as rapid clearance from the bloodstream and inefficient extravasation (e.g., crossing the endothelial barrier from the blood stream). We have studied sd-rxRNA® molecules in a rat model of dermal delivery. Direct application of sd-rxRNA® with no additional delivery vehicle to the skin (incision introduced) demonstrates that target gene silencing can be measured after local administration. The dose levels required for these direct-injection methods are small and suitable for clinical development, suggesting that local delivery indications will be very accessible with the sd-rxRNA® technology platform. Target tissues that are potentially accessible for local delivery using sd-rxRNA® compounds include the skin, the eye, the lung, the CNS, mucosal tissues, sites of inflammation and tumors (direct administration).

Systemic Delivery

Systemic delivery occurs when a drug accesses the tissue of interest through the circulatory system. In some cases, such as in targeting a treatment to the liver, the optimal route of delivery may be by a systemic route. We have developed a portfolio of systemic delivery solutions utilizing our RNAi therapeutic platforms. One novel approach involves the use of sd-rxRNA® compounds. The self-delivering technology introduces properties required for in vivo efficacy such as cell and tissue penetration and improved blood clearance and distribution properties. Systemic delivery of these compounds to mice has resulted in gene specific inhibition in the liver with no additional delivery vehicle required, albeit at high concentrations. A proof-of-concept study using rxRNA® in conjunction with a standard lipid-based delivery vehicle has enabled us to demonstrate gene-specific inhibition in liver at much lower doses in a mouse model after intravenous, system delivery. While delivery of RNAi to the liver may be critical for the treatment of many diseases, additional target tissues that are potentially accessible using rxRNA® compounds by systemic delivery include kidney, fat, heart, lung, bone marrow, sites of inflammation, tumors and vascular endothelium.

Intellectual Property

We protect our proprietary information by means of United States and foreign patents, trademarks and copyrights. In addition, we rely upon trade secret protection and contractual arrangements to protect certain of our proprietary information and products. We have pending patent applications that relate to potential drug targets, compounds we are developing to modulate those targets (described throughout herein as rxRNA®), methods of making or using those compounds and proprietary elements of our drug discovery platform.

Much of our technology and many of our processes depend upon the knowledge, experience and skills of key scientific and technical personnel. To protect our rights to our proprietary know-how and technology, we require all employees, as well as our consultants and advisors when feasible, to enter into confidentiality agreements that require disclosure and assignment to us of ideas, developments, discoveries and inventions made by these employees, consultants and advisors in the course of their service to us, and we vigorously defend that position with partners, as well as with employees who leave the Company.

We have also obtained rights to various patents and patent applications under licenses with third parties, which require us to pay royalties or milestone payments, or both. The degree of patent protection for biotechnology products and processes, including ours, remains uncertain, both in the United States and in other important markets, because the scope of protection depends on decisions of patent offices, courts and lawmakers in these countries. There is no certainty that our existing patents or others, if obtained, will afford us substantial protection or commercial benefit. Similarly, there is no assurance that our pending patent applications or patent

8

Table of Contents

applications licensed from third parties will ultimately be granted as patents or that those patents that have been issued or are issued in the future will stand if they are challenged in court. We assess our license agreements on an ongoing basis, and may from time to time terminate licenses to technology that we do not intend to employ in our immunotherapy or RNAi technology platforms, or in our product discovery or development activities.

Patents and Patent Applications

We are actively prosecuting eleven patent families covering our rxRNA® compounds and technologies, including RXI-109. Additionally, as part of our acquisition of the OPKO RNAi-related assets in March 2013, we acquired rights to a total of 97 patents and 62 patent applications. A summary of these patents and patent applications is set forth below in the following table.

| RXi Platform |

OPKO Platform1 |

|||||||||||

| Pending Applications |

Pending Applications |

Issued Patents |

||||||||||

| United States |

12 | 14 | 13 | |||||||||

| Canada |

4 | 6 | 0 | |||||||||

| Europe |

5 | 11 | 71 | |||||||||

| Japan |

4 | 9 | 0 | |||||||||

| Other Markets |

4 | 22 | 13 | |||||||||

RXi RNAi Platform Patent Applications

Our portfolio does not include any issued patents. The patent applications encompass what we believe to be important new RNAi compounds and their use as therapeutics, chemical modifications of RNAi compounds that improve the compounds’ suitability for therapeutic uses (including delivery) and compounds directed to specific targets (i.e., that address specific disease states). Any patents that may issue from these pending patent applications will be set to expire between 2028 and 2031, not including any patent term extensions that may be afforded under the Federal Food, Drug and Cosmetic Act (and the equivalent provisions in foreign jurisdictions) for any delays incurred during the regulatory approval process relating to human drug products (or processes for making or using human drug products).

OPKO RNAi Platform Patent Applications

The OPKO RNAi patents and patent applications encompass 12 patent families, covering RNAi compounds and their use as therapeutics and compounds directed to specific targets (i.e., that address specific disease states). The patents and any patents that may issue from the pending applications will be set to expire between 2022 and 2030, not including any patent term extensions that may be afforded under the Federal Food, Drug and Cosmetic Act (and the equivalent provisions in foreign jurisdictions) for any delays incurred during the regulatory approval process relating to human drug products (or processes for making or using human drug products).

License Agreements

We have secured exclusive and non-exclusive rights to develop RNAi therapeutics by licensing key RNAi technologies and patent rights from third parties. These rights relate to chemistry and configuration of RNAi compounds, delivery technologies of RNAi compounds to cells and therapeutic targets. As we continue to develop our own proprietary compounds, we continue to evaluate both our in-licensed portfolio as well as the field for new technologies that could be in-licensed to further enhance our intellectual property portfolio and unique position in the RNAi space.

University of Massachusetts Medical School. We hold a non-exclusive license from the University of Massachusetts Medical School (“UMMS”). This license grants to us rights under certain UMMS patent

| 1 | Includes patents the Company owns, have licensed or otherwise has rights to use. |

9

Table of Contents

applications to make, use and sell products related to applications of RNAi technologies in particular fields, including HCMV and retinitis, amyotrophic lateral sclerosis, known as “ALS” or “Lou Gehrig’s Disease,” diabetes and obesity. Throughout the term of the license, we must pay UMMS an annual maintenance fee of $15,000. We also will be required to pay to UMMS customary royalties of up to 10% of: (i) any future net sales of licensed products; (ii) income received from any sublicensees under this license; and (iii) net sales of commercial clinical laboratory services, subject to a minimum royalty of $50,000 beginning in 2016. We also agreed to pay expenses incurred by UMMS in prosecuting and maintaining the licensed patents.

The UMMS license was effective on April 15, 2003, and will remain in effect until: (i) the expiration of all issued patents within the “patent rights” (as defined); or (ii) for a period of ten years after the effective date if no such patents have issued within the ten-year period, unless earlier terminated in accordance with the provisions of the license. In the event that either party commits a material breach of its obligations under the UMMS license and fails to cure that breach within 60 days after receiving written notice thereof, the other party may terminate the UMMS license immediately upon written notice to the party in breach.

The UMMS license may be amended, supplemented, or otherwise modified only by signed written agreement of the parties.

Dharmacon. We have entered into a license agreement with Dharmacon, Inc. (now part of Thermo Fisher Scientific Inc.), pursuant to which we obtained an exclusive license to certain RNAi sequences for a number of target genes for the development of our rxRNA® compounds. Furthermore, we hold the right to license additional RNAi sequences, under the same terms, disclosed by Thermo Fisher Scientific Inc. in its pending patent applications against target genes and have received an option for exclusivity for other siRNA configurations. As partial consideration for this license, we have agreed to pay future clinical milestone payments in an aggregate amount of up to $2,000,000 and royalty payments of either 0.25% or 0.5% based on the level of any future sales of siRNA compositions developed in connection with the licensed technology.

The Dharmacon license will remain in effect for the duration of any patents issued with respect to the technologies covered by such agreement, unless otherwise terminated earlier by us.

The Dharmacon license may be amended, supplemented or otherwise modified only by signed written agreement of the parties.

Advirna. We have entered into agreements with Advirna, LLC pursuant to which Advirna assigned to us its existing patent and technology rights related to sd-rxRNA® technology in exchange for our agreement to pay Advirna an annual maintenance fee of $100,000 and a one-time milestone payment of $350,000 upon the issuance of the first patent with valid claims covering the assigned technology. Additionally, we will be required to pay a 1% royalty to Advirna on any licensing revenue received by us with respect to future licensing of the assigned Advirna patent and technology rights. We also granted back to Advirna a license under the assigned patent and technology rights for fields of use outside human therapeutics and diagnostics, and issued to Advirna, upon the completion of the spin-off transaction from Galena, 41,849,934 shares of common stock.

Our rights under the Advirna agreement will expire upon the later of: (i) the expiration of the last-to-expire of the “patent rights” (as defined) included in the Advirna agreement; or (ii) the abandonment of the last-to-be abandoned of such patents, unless earlier terminated in accordance with the provisions of the agreement.

We may terminate the Advirna agreement at any time upon 90 days’ written notice to Advirna, and Advirna may terminate the agreement upon 90 days’ prior written notice in the event that we cease using commercially reasonable efforts to research, develop, license or otherwise commercialize the patent rights or “royalty-bearing products” (as defined), provided that we may refute such claim within such 90-day period by showing budgeted expenditures for the research, development, licensing or other commercialization consistent with other

10

Table of Contents

technologies of similar stage of development and commercial potential as the patent rights or royalty-bearing products. Further, either party at any time may provide to the other party written notice of a material breach of the agreement. If the other party fails to cure the identified breach within 90 days after the date of the notice, the aggrieved party may terminate the agreement by written notice to the party in breach.

The Advirna agreement may only be altered or supplemented by written mutual agreement by the parties.

OPKO. In March 2013, we acquired from OPKO substantially all of its RNAi-related assets, which included patents and patent applications, licenses, clinical and preclinical data and other related assets (collectively, the “OPKO RNAi Assets”). In exchange for the OPKO RNAi Assets, we issued to OPKO 50,000,000 shares of our common stock and agreed to pay, if applicable: (i) up to $50,000,000 in development and commercialization milestones for the successful development and commercialization of each “Qualified Drug” (as defined in the Asset Purchase Agreement with OPKO) (collectively, the “Milestone Payments”); and (ii) royalty payments equal to: (a) a mid-single-digit percentage of “Net Sales” (as defined in the Asset Purchase Agreement) with respect to each Qualified Drug sold for an ophthalmologic use during the applicable “Royalty Period” (as defined in the Asset Purchase Agreement); and (b) a low-single-digit percentage of Net Sales with respect to each Qualified Drug sold for a non-ophthalmologic use during the applicable Royalty Period (collectively, the “Royalty Payments”). The OPKO RNAi Assets are at an early stage of development, and we expect to commence development work with preclinical testing to identify potential lead compounds and targets.

Research and Development

To date, our research programs have focused on identifying product candidates and optimizing the delivery method and technology necessary to make RNAi compounds available by local or systemic administration, as appropriate, for diseases for which we intend to develop an RNAi therapeutic. Since we commenced operations, research and development has comprised a significant proportion of our total operating expenses and is expected to comprise the majority of our spending for the foreseeable future.

There are risks in any new field of drug discovery that preclude certainty regarding the successful development of a product. We cannot reasonably estimate or know the nature, timing and costs of the efforts necessary to complete the development of, or the period in which material net cash inflows are expected to commence from, any product candidate.

For more information on our research and development activity, see Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Research and Development” of this annual report on Form 10-K.

Competition

We believe numerous companies are investigating or plan to investigate a variety of proposed anti-scarring therapies in clinical trials. The companies include large and small pharmaceutical, chemical and biotechnology companies, as well as universities, government agencies and other private and public research organizations. Such companies include Renovo Group plc, CoDa Therapeutics, Inc., Sirnaomics, Inc., FirstString Research, Inc., Merz Pharmaceuticals, LLC, Capstone Therapeutics, Halscion, Inc., Garnet Bio Therapeutics, Inc., AkPharma Inc., Promedior, Inc., Kissei Pharmaceutical Co., Ltd., Eyegene, Derma Sciences, Inc., Healthpoint Biotherapeutics, FibroGen, Inc. and Pharmaxon. In particular, Excaliard Pharmaceuticals, Inc., which has been acquired by Pfizer, Inc., has successfully advanced an anti-CTGF antisense oligonucleotide through several Phase 1 and Phase 2 trials and has demonstrated improved scar outcome over placebo.

We believe that other companies working in the RNAi area, generally, include Alnylam Pharmaceuticals, Inc., Marina Biotech, Inc., Tacere Therapeutics, Inc., Benitec Limited, Silence Therapeutics plc, Quark Pharmaceuticals, Inc., Rosetta Genomics Ltd., Lorus Therapeutics, Inc., Tekmira Pharmaceuticals Corporation, Arrowhead Research Corporation, Regulus Therapeutics Inc. and Santaris, as well as a number of large

11

Table of Contents

pharmaceutical companies. Many other companies are pursuing non-RNAi-based therapies for one or more fibrotic disease indications, including ocular scarring or other indications that we may seek to pursue. See Item 1A, “Risk Factors—Risks Relating to RXi’s Business and Industry”.

Government Regulation

The United States and other developed countries extensively regulate the preclinical and clinical testing, manufacturing, labeling, storage, record-keeping, advertising, promotion, export, marketing and distribution of drugs and biologic products. The FDA regulates pharmaceutical and biologic products under the Federal Food, Drug, and Cosmetic Act, the Public Health Service Act and other federal statutes and regulations.

To obtain approval of our future product candidates from the FDA, we must, among other requirements, submit data supporting safety and efficacy for the intended indication as well as detailed information on the manufacture and composition of the product candidate. In most cases, this will require extensive laboratory tests and preclinical and clinical trials. The collection of these data, as well as the preparation of applications for review by the FDA involve significant time and expense. The FDA also may require post-marketing testing to monitor the safety and efficacy of approved products or place conditions on any approvals that could restrict the therapeutic claims and commercial applications of these products. Regulatory authorities may withdraw product approvals if we fail to comply with regulatory standards or if we encounter problems at any time following initial marketing of our products.

The first stage of the FDA approval process for a new biologic or drug involves completion of preclinical studies and the submission of the results of these studies to the FDA. These data, together with proposed clinical protocols, manufacturing information, analytical data and other information submitted to the FDA, in an investigational new drug application (“IND”), must become effective before human clinical trials may commence. Preclinical studies generally involve FDA regulated laboratory evaluation of product characteristics and animal studies to assess the efficacy and safety of the product candidate.

After the IND becomes effective, a company may commence human clinical trials. These are typically conducted in three sequential phases, but the phases may overlap. Phase 1 trials consist of testing the product candidate in a small number of patients or healthy volunteers, primarily for safety at one or more doses. Phase 2 trials, in addition to safety, evaluate the efficacy of the product candidate in a patient population somewhat larger than Phase 1 trials. Phase 3 trials typically involve additional testing for safety and clinical efficacy in an expanded population at multiple test sites. A company must submit to the FDA a clinical protocol, accompanied by the approval of the Institutional Review Boards (“IRB”) at the institutions participating in the trials, prior to commencement of each clinical trial.

To obtain FDA marketing authorization, a company must submit to the FDA the results of the preclinical and clinical testing, together with, among other things, detailed information on the manufacture and composition of the product candidate, in the form of a new drug application (an “NDA”), or, in the case of a biologic, a biologics license application (a “BLA”).

The amount of time taken by the FDA for approval of an NDA or BLA will depend upon a number of factors, including whether the product candidate has received priority review, the quality of the submission and studies presented, the potential contribution that the compound will make in improving the treatment of the disease in question and the workload at the FDA.

The FDA may, in some cases, confer upon an investigational product the status of a fast track product. A fast track product is defined as a new drug or biologic intended for the treatment of a serious or life threatening condition that demonstrates the potential to address unmet medical needs for this condition. The FDA can base approval of an NDA or BLA for a fast track product on an effect on a surrogate endpoint, or on another endpoint that is reasonably likely to predict clinical benefit. If a preliminary review of clinical data suggests that a fast track product may be effective, the FDA may initiate review of entire sections of a marketing application for a fast track product before the sponsor completes the application.

12

Table of Contents

We anticipate that our products will be manufactured by our strategic partners, licensees or other third parties. Before approving an NDA or BLA, the FDA will inspect the facilities at which the product is manufactured and will not approve the product unless the manufacturing facilities are in compliance with the FDA’s current good manufacturing practices (“cGMP”), which are regulations that govern the manufacture, holding and distribution of a product. Manufacturers of biologics also must comply with the FDA’s general biological product standards. Our manufacturers also will be subject to regulation under the Occupational Safety and Health Act, the Nuclear Energy and Radiation Control Act, the Toxic Substance Control Act and the Resource Conservation and Recovery Act and other applicable environmental statutes. Following approval, the FDA periodically inspects drug and biologic manufacturing facilities to ensure continued compliance with the good manufacturing practices regulations. Our manufacturers will have to continue to comply with those requirements. Failure to comply with these requirements subjects the manufacturer to possible legal or regulatory action, such as suspension of manufacturing or recall or seizure of product. Adverse patient experiences with the product must be reported to the FDA and could result in the imposition of marketing restrictions through labeling changes or market removal. Product approvals may be withdrawn if compliance with regulatory requirements is not maintained or if problems concerning safety or efficacy of the product occur following approval.

The labeling, advertising, promotion, marketing and distribution of a drug or biologic product also must be in compliance with FDA and Federal Trade Commission requirements which include, among others, standards and regulations for off-label promotion, industry sponsored scientific and educational activities, promotional activities involving the internet, and direct-to-consumer advertising. We also will be subject to a variety of federal, state and local regulations relating to the use, handling, storage and disposal of hazardous materials, including chemicals and radioactive and biological materials. In addition, we will be subject to various laws and regulations governing laboratory practices and the experimental use of animals. In each of these areas, as above, the FDA has broad regulatory and enforcement powers, including the ability to levy fines and civil penalties, suspend or delay issuance of product approvals, seize or recall products and deny or withdraw approvals.

We will also be subject to a variety of regulations governing clinical trials and sales of our products outside the United States. Whether or not FDA approval has been obtained, approval of a product candidate by the comparable regulatory authorities of foreign countries and regions must be obtained prior to the commencement of marketing the product in those countries. The approval process varies from one regulatory authority to another and the time may be longer or shorter than that required for FDA approval. In the European Union, Canada and Australia, regulatory requirements and approval processes are similar, in principle, to those in the United States.

Environmental Compliance

Our research and development activities involve the controlled use of potentially harmful biological materials as well as hazardous materials, chemicals and various radioactive compounds. We are subject to federal, state and local laws and regulations governing the use, storage, handling and disposal of these materials and specific waste products. We are also subject to numerous environmental, health and workplace safety laws and regulations, including those governing laboratory procedures, exposure to blood-borne pathogens and the handling of bio-hazardous materials. The cost of compliance with these laws and regulations could be significant and may adversely affect capital expenditures to the extent we are required to procure expensive capital equipment to meet regulatory requirements.

Human Resources

As of March 15, 2013, we had ten full-time employees, seven of whom were engaged in research and development, and three of whom were engaged in management, administration and finance. None of our employees is represented by a labor union or covered by a collective bargaining agreement, nor have we experienced any work stoppages.

13

Table of Contents

| ITEM 1A. RISK | FACTORS |

Risks Relating to RXi’s Business and Industry

We are dependent on the success of our lead drug candidate, which may not receive regulatory approval or be successfully commercialized.

RXI-109, our first RNAi-based product candidate, targets CTGF and may have a variety of medical applications. We began Phase 1 clinical trials for RXI-109 in 2012 and are planning to begin Phase 2 clinical trials for RXI-109 in the second half of 2013. The FDA, however, may require additional information before we are allowed to commence our planned Phase 2 clinical trials, and such information may be costly to provide or cause potentially significant delays in development. There is no assurance that we will be able to successfully develop RXI-109 or any other product candidate.

We have no commercial products and currently generate no revenue from commercial sales or collaborations and may never be able to develop marketable products. The FDA or similar foreign governmental agencies must approve our products in development before they can be marketed. The process for obtaining FDA approval is both time-consuming and costly, with no certainty of a successful outcome. Before obtaining regulatory approval for the sale of any drug candidate, we must conduct extensive preclinical tests and successful clinical trials to demonstrate the safety and efficacy of our product candidates in humans. We have not yet shown safety or efficacy in humans for any RNAi-based product candidates, including RXI-109. A failure of any preclinical study or clinical trial can occur at any stage of testing. The results of preclinical and initial clinical testing of these products may not necessarily indicate the results that will be obtained from later or more extensive testing. Additionally, any observations made with respect to blinded clinical data are inherently uncertain as we cannot know which set of data come from patients treated with an active drug versus the placebo vehicle. Investors are cautioned not to rely on observations coming from blinded data and not to rely on initial clinical trial results as necessarily indicative of results that will be obtained in subsequent clinical trials.

A number of different factors could prevent us from obtaining regulatory approval or commercializing our product candidates on a timely basis, or at all.

We, the FDA or other applicable regulatory authorities or an IRB may suspend clinical trials of a drug candidate at any time for various reasons, including if we or they believe the subjects or patients participating in such trials are being exposed to unacceptable health risks. Among other reasons, adverse side effects of a drug candidate on subjects or patients in a clinical trial could result in the FDA or other regulatory authorities suspending or terminating the trial and refusing to approve a particular drug candidate for any or all indications of use.

Clinical trials of a new drug candidate require the enrollment of a sufficient number of patients, including patients who are suffering from the disease or condition the drug candidate is intended to treat and who meet other eligibility criteria. Rates of patient enrollment are affected by many factors, and delays in patient enrollment can result in increased costs and longer development times.

Clinical trials also require the review and oversight of IRBs, which approve and continually review clinical investigations and protect the rights and welfare of human subjects. An inability or delay in obtaining IRB approval could prevent or delay the initiation and completion of clinical trials, and the FDA may decide not to consider any data or information derived from a clinical investigation not subject to initial and continuing IRB review and approval.

Numerous factors could affect the timing, cost or outcome of our drug development efforts, including the following:

| • | Delays in filing or acceptance of initial drug applications for our product candidates; |

| • | Difficulty in securing centers to conduct clinical trials; |

14

Table of Contents

| • | Conditions imposed on us by the FDA or comparable foreign authorities regarding the scope or design of our clinical trials; |

| • | Problems in engaging IRBs to oversee trials or problems in obtaining or maintaining IRB approval of studies; |

| • | Difficulty in enrolling patients in conformity with required protocols or projected timelines; |

| • | Third-party contractors failing to comply with regulatory requirements or to meet their contractual obligations to us in a timely manner; |

| • | Our drug candidates having unexpected and different chemical and pharmacological properties in humans than in laboratory testing and interacting with human biological systems in unforeseen, ineffective or harmful ways; |

| • | The need to suspend or terminate clinical trials if the participants are being exposed to unacceptable health risks; |

| • | Insufficient or inadequate supply or quality of our drug candidates or other necessary materials necessary to conduct our clinical trials; |

| • | Effects of our drug candidates not being the desired effects or including undesirable side effects or the drug candidates having other unexpected characteristics; |

| • | The cost of our clinical trials being greater than we anticipate; |

| • | Negative or inconclusive results from our clinical trials or the clinical trials of others for similar drug candidates or inability to generate statistically significant data confirming the efficacy of the product being tested; |

| • | Changes in the FDA’s requirements for testing during the course of that testing; |

| • | Reallocation of our limited financial and other resources to other clinical programs; and |

| • | Adverse results obtained by other companies developing similar drugs. |

It is possible that none of the product candidates that we may develop will obtain the appropriate regulatory approvals necessary to begin selling them or that any regulatory approval to market a product may be subject to limitations on the indicated uses for which we may market the product. The time required to obtain FDA and other approvals is unpredictable, but often can take years following the commencement of clinical trials, depending upon the complexity of the drug candidate. Any analysis we perform of data from clinical activities is subject to confirmation and interpretation by regulatory authorities, which could delay, limit or prevent regulatory approval. Any delay or failure in obtaining required approvals could have a material adverse effect on our ability to generate revenue from the particular drug candidate.

We also are subject to numerous foreign regulatory requirements governing the conduct of clinical trials, manufacturing and marketing authorization, pricing and third-party reimbursement. The foreign regulatory approval process includes all of the risks associated with the FDA approval described above as well as risks attributable to the satisfaction of local regulations in foreign jurisdictions. Approval by the FDA does not assure approval by regulatory authorities outside of the United States.

The approach we are taking to discover and develop novel therapeutics using RNAi is unproven and may never lead to marketable products.

RNA interference is a relatively new scientific discovery. Our RNAi technologies have been subject to only limited clinical testing. To date, no company has received regulatory approval to market therapeutics utilizing RNAi, and a number of clinical trials of RNAi technologies by other companies have been unsuccessful. The scientific evidence to support the feasibility of developing drugs based on these discoveries is both preliminary and

15

Table of Contents

limited. To successfully develop RNAi-based products, we must resolve a number of issues, including stabilizing the RNAi material and delivering it into target cells in the human body. We may spend large amounts of money trying to resolve these issues and may never succeed in doing so. In addition, any compounds that we develop may not demonstrate in patients the chemical and pharmacological properties ascribed to them in laboratory studies, and they may interact with human biological systems in unforeseen, ineffective or even harmful ways.

The FDA could impose a unique regulatory regime for RNAi therapeutics.

The substances we intend to develop may represent a new class of drug, and the FDA has not yet established any definitive policies, practices or guidelines in relation to these drugs. While we expect any product candidates that we develop will be regulated as a new drug under the Federal Food, Drug, and Cosmetic Act, the FDA could decide to regulate them or other products we may develop as biologics under the Public Health Service Act. The lack of policies, practices or guidelines may hinder or slow review by the FDA of any regulatory filings that we may submit. Moreover, the FDA may respond to these submissions by defining requirements that we may not have anticipated.

Even if we receive regulatory approval to market our product candidates, our product candidates may not be accepted commercially, which may prevent us from becoming profitable.

The RNAi product candidates that we are developing are based on new technologies and therapeutic approaches. RNAi products may be more expensive to manufacture than traditional small molecule drugs, which may make them more costly than competing small molecule drugs. Additionally, RNAi products do not readily cross the so-called blood brain barrier and, for various applications, are likely to require injection or implantation, which will make them less convenient to administer than drugs administered orally. Key participants in the pharmaceutical marketplace, such as physicians, medical professionals working in large reference laboratories, public health laboratories and hospitals, third-party payors and consumers may not accept products intended to improve therapeutic results based on RNAi technology. As a result, it may be more difficult for us to convince the medical community and third-party payors to accept and use our products or to provide favorable reimbursement. If medical professionals working with large reference laboratories, public health laboratories and hospitals choose not to adopt and use our RNAi technology, our products may not achieve broader market acceptance.

Additionally, although we expect that we will have intellectual property protection for our technology, certain governments may elect to deny patent protection for drugs targeting diseases with high unmet medical need (e.g., as in the case of HIV) and allow in their country internationally unauthorized generic competition. If this was to happen, our commercial prospects for developing any such drugs would be substantially diminished in these countries.

We are subject to competition and may not be able to compete successfully.

We believe numerous companies are investigating or plan to investigate a variety of proposed anti-scarring therapies in clinical trials. The companies include large and small pharmaceutical, chemical and biotechnology companies, as well as universities, government agencies and other private and public research organizations. Such companies include Renovo Group plc, CoDa Therapeutics, Inc., Sirnaomics, Inc., FirstString Research, Inc., Merz Pharmaceuticals, LLC, Capstone Therapeutics, Halscion, Inc., Garnet Bio Therapeutics, Inc., AkPharma Inc., Promedior, Inc., Kissei Pharmaceutical Co., Ltd., Eyegene, Derma Sciences, Inc., Healthpoint Biotherapeutics, FibroGen, Inc. and Pharmaxon. In particular, Excaliard Pharmaceuticals, Inc., which has been acquired by Pfizer, Inc., has successfully advanced an anti-CTGF antisense oligonucleotide through several Phase 1 and Phase 2 trials and has demonstrated improved scar outcome over placebo.

We believe other companies working in the RNAi area, generally, include Alnylam Pharmaceuticals, Inc., Marina Biotech, Inc., Tacere Therapeutics, Inc., Benitec Limited, Silence Therapeutics plc, Quark

16

Table of Contents

Pharmaceuticals, Inc., Rosetta Genomics Ltd., Lorus Therapeutics, Inc., Tekmira Pharmaceuticals Corporation, Arrowhead Research Corporation, Regulus Therapeutics Inc. and Santaris, as well as a number of large pharmaceutical companies. Many other companies are pursuing non-RNAi-based therapies for one or more fibrotic disease indications, including ocular scarring or other indications that we may seek to pursue.

Most of these competitors have substantially greater research and development capabilities and financial, scientific, technical, manufacturing, marketing, distribution and other resources than we have, and we may not be able to successfully compete with them. In addition, even if we are successful in developing our product candidates, in order to compete successfully we may need to be first to market or to demonstrate that our RNAi based products are superior to therapies based on different technologies. A number of our competitors have already commenced clinical testing of RNAi product candidates and may be more advanced than we are in the process of developing products. If we are not first to market or are unable to demonstrate superiority, any products for which we are able to obtain approval may not be successful.

We are dependent on technologies we license, and if we lose the right to license such technologies or fail to license new technologies in the future, our ability to develop new products would be harmed.

Many patents in the RNAi field have already been exclusively licensed to third parties, including our competitors. If any of our existing licenses are terminated, the development of the products contemplated by the licenses could be delayed or terminated and we may not be able to negotiate additional licenses on acceptable terms, if at all, which would have a material adverse effect on our business.

We may be unable to protect our intellectual property rights licensed from other parties; our intellectual property rights may be inadequate to prevent third parties from using our technologies or developing competing products; and we may need to license additional intellectual property from others.

Therapeutic applications of gene silencing technologies, delivery methods and other technologies that we license from third parties are claimed in a number of pending patent applications, but there is no assurance that these applications will result in any issued patents or that those patents would withstand possible legal challenges or protect our technologies from competition. The United States Patent and Trademark Office and patent granting authorities in other countries have upheld stringent standards for the RNAi patents that have been prosecuted so far. Consequently, pending patents that we have licensed and those that we own may continue to experience long and difficult prosecution challenges and may ultimately issue with much narrower claims than those in the pending applications. Third parties may hold or seek to obtain additional patents that could make it more difficult or impossible for us to develop products based on RNAi technology without obtaining a license to such patents, which licenses may not be available on attractive terms, or at all.

In addition, others may challenge the patents or patent applications that we currently license or may license in the future or that we own and, as a result, these patents could be narrowed, invalidated or rendered unenforceable, which would negatively affect our ability to exclude others from using RNAi technologies described in these patents. There is no assurance that these patent or other pending applications or issued patents we license or that we own will withstand possible legal challenges. Moreover, the laws of some foreign countries may not protect our proprietary rights to the same extent as do the laws of the United States. Any patents issued to us or our licensors may not provide us with any competitive advantages, and there is no assurance that the patents of others will not have an adverse effect on our ability to do business or to continue to use its technologies freely. Our efforts to enforce and maintain our intellectual property rights may not be successful and may result in substantial costs and diversion of management time. Even if our rights are valid, enforceable and broad in scope, competitors may develop products based on technology that is not covered by our licenses or patents or patent application that we own.

We have received a letter from Alnylam Pharmaceuticals, Inc. (“Alnylam”), claiming that we require access to Alnylam’s patent and patent applications and demanding that we stop engaging in unspecified alleged

17

Table of Contents

infringing activities unless we obtain a license from Alnylam. We understand that other companies working in the RNAi area have received similar letters from Alnylam. Although we believe that our current and planned activities do not infringe any valid patent rights of Alnylam, there is no assurance that we will not need to alter our development candidates or products or obtain a license to Alnylam’s rights to avoid any such infringement. Interactions with senior management of Alnylam at several occasions have not resulted in material indications of breach, but this does not exclude an unexpected claim by that company.

There is no guarantee that future licenses will be available from third parties for our product candidates on timely or satisfactory terms, or at all. To the extent that we are required and are able to obtain multiple licenses from third parties to develop or commercialize a product candidate, the aggregate licensing fees and milestones and royalty payments made to these parties may materially reduce our economic returns or even cause us to abandon development or commercialization of a product candidate.

Our success depends upon our ability to obtain and maintain intellectual property protection for our products and technologies.

The applications based on RNAi technologies claim many different methods, compositions and processes relating to the discovery, development, delivery and commercialization of RNAi therapeutics. Because this field is so new, very few of these patent applications have been fully processed by government patent offices around the world, and there is a great deal of uncertainty about which patents will issue, when, to whom and with what claims. Although we are not aware of any blocking patents or other proprietary rights, it is likely that there will be significant litigation and other proceedings, such as interference and opposition proceedings in various patent offices, relating to patent rights in the RNAi field. It is possible that we may become a party to such proceedings.

We may not be able to obtain sufficient financing and may not be able to develop our product candidates.

With the proceeds from our March 2013 Offering, we believe that we have sufficient working capital to fund our currently planned operations, including the planned Phase 2 program for RXI-109, into fiscal 2015. However, in the future, we may need to incur debt or issue equity in order to fund our planned expenditures as well as to make acquisitions and other investments. We cannot assure you that debt or equity financing will be available to us on acceptable terms or at all. If we cannot, or are limited in the ability to, incur debt, issue equity or enter into strategic collaborations, we may be unable to fund discovery and development of our product candidates, address gaps in our product offerings or improve our technology.

We anticipate that we will need to raise substantial amounts of money to fund a variety of future activities integral to the development of our business, which may include but are not limited to the following:

| • | To conduct research and development to successfully develop our RNAi technologies; |

| • | To obtain regulatory approval for our products; |

| • | To file and prosecute patent applications and to defend and assess patents to protect our technologies; |

| • | To retain qualified employees, particularly in light of intense competition for qualified scientists; |

| • | To manufacture products ourselves or through third parties; |

| • | To market our products, either through building our own sales and distribution capabilities or relying on third parties; and |

| • | To acquire new technologies, licenses or products. |

In addition, our common stock is not a “covered security” for purposes of the Securities Act of 1933, as amended (the “Securities Act”). The term “covered security” applies to securities exempt from state registration because of their oversight by federal authorities and national regulatory bodies, such as national securities exchanges, pursuant to Section 18 of the Securities Act. Because our common stock is not a “covered security,”

18

Table of Contents

the sale of our shares may be subject to registration in various states. This could make it more difficult or costly to conduct an equity financing, which could have a material adverse effect on our business.

We cannot assure you that any needed financing will be available to us on acceptable terms or at all. If we cannot obtain additional financing in the future, our operations may be restricted and we may ultimately be unable to continue to develop and potentially commercialize our product candidates.

Future financing may be obtained through, and future development efforts may be paid for by, the issuance of debt or equity, which may have an adverse effect on our stockholders or may otherwise adversely affect our business.

If we raise funds through the issuance of debt or equity, any debt securities or preferred stock issued will have rights, preferences and privileges senior to those of holders of our common stock in the event of a liquidation. In such event, there is a possibility that once all senior claims are settled, there may be no assets remaining to pay out to the holders of common stock. In addition, if we raise funds through the issuance of additional equity, whether through private placements or public offerings, such an issuance would dilute your ownership in us.