0001493152-21-006671.txt : 20210324

0001493152-21-006671.hdr.sgml : 20210324

20210324061923

ACCESSION NUMBER: 0001493152-21-006671

CONFORMED SUBMISSION TYPE: 10-K

PUBLIC DOCUMENT COUNT: 60

CONFORMED PERIOD OF REPORT: 20201231

FILED AS OF DATE: 20210324

DATE AS OF CHANGE: 20210324

FILER:

COMPANY DATA:

COMPANY CONFORMED NAME: Power REIT

CENTRAL INDEX KEY: 0001532619

STANDARD INDUSTRIAL CLASSIFICATION: REAL ESTATE INVESTMENT TRUSTS [6798]

IRS NUMBER: 453116572

STATE OF INCORPORATION: MD

FISCAL YEAR END: 1231

FILING VALUES:

FORM TYPE: 10-K

SEC ACT: 1934 Act

SEC FILE NUMBER: 001-36312

FILM NUMBER: 21766508

BUSINESS ADDRESS:

STREET 1: 301 WINDING ROAD

CITY: OLD BETHPAGE

STATE: NY

ZIP: 11804

BUSINESS PHONE: 212-750-0373

MAIL ADDRESS:

STREET 1: 301 WINDING ROAD

CITY: OLD BETHPAGE

STATE: NY

ZIP: 11804

10-K

1

form10-k.htm

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D. C. 20549

FORM

10-K

(Mark

One)

[X]ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OFTHE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended December 31, 2020

OR

[ ]TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission

File Number: 001-36312

POWER

REIT

(Exact

name of registrant as specified in its charter)

Maryland

45-3116572

(State

or Other Jurisdiction

of

Incorporation or organization)

(I.R.S.

Employer

Identification

No.)

301

Winding Road, Old Bethpage, New York 11804

(Address

of principal executive offices) (Zip Code)

Registrant’s

telephone number, including area code (212) 750-0371

Securities

registered pursuant to Section 12(b) of the Act:

Title

of Each Class

Trading

Symbol

Name

of Each Exchange on Which Registered

Common

Shares

PW

NYSE

American, LLC

7.75%

Series A Cumulative Redeemable Perpetual Preferred Stock, Liquidation Preference $25 per Share

PW.A

NYSE

American, LLC

Securities

Registered Pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ]

No [X]

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ]

No [X]

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports),

and (2) has been subject to such filing requirement for the past 90 days.

Yes

[X] No [ ]

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant

to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit such files).

Yes

[X] No [ ]

Indicate

by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting

company or an emerging growth company. See definitions of “large accelerated filer”, “accelerated filer”,

“smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large

accelerated filer

[ ]

Accelerated

filer

[ ]

Non-accelerated

filer

[X]

Smaller

reporting company

[X]

Emerging

growth company

[ ]

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for

complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report. [ ]

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes

[ ] No [X]

The

aggregate market value of the voting and non-voting common equity of the Registrant held by non-affiliates as of June 30, 2020,

the Registrant’s most recently completed second fiscal quarter, was approximately $39,752,194 computed by reference to the

closing price of the Registrant’s shares of beneficial interest (“common shares” or “common stock”)

on June 30, 2020 of $28.75.

As

of March 24, 2021, there were 3,299,233 common shares outstanding.

This

Annual Report on Form 10-K (this “Annual Report”) document contains forward-looking statements within the meaning

of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended. Forward-looking statements are

those that predict or describe future events or trends and that do not relate solely to historical matters. You can generally

identify forward-looking statements by the use of words such as “believe,” “expect,” “will,”

“anticipate,” “intend,” “estimate,” “would,” “should,” “project,”

“plan,” “assume” or other similar words or expressions, or negatives of such words or expressions, although

not all forward-looking statements can be identified in this way. All statements contained in this document regarding strategy,

plans, future operations, projected financial condition or results of operations, prospects, the future of Power REIT’s

industries and markets, outcomes that might be obtained by pursuing management’s plans and objectives, and similar subjects,

are forward-looking statements. Over time, Power REIT’s actual performance, results, financial condition and achievements

may differ from the anticipated performance, results, financial condition and achievements that are expressed or implied by Power

REIT’s forward-looking statements, and such differences may be significant and materially adverse to Power REIT and its

security holders.

All

forward-looking statements reflect Power REIT’s good-faith beliefs, assumptions and expectations, but they are not guarantees

of future performance. Furthermore, Power REIT disclaims any obligation to publicly update or revise any forward-looking statements

to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes. For

a further discussion of factors that could cause Power REIT’s future performance, results, financial condition or achievements

to differ materially from that which is expressed or implied in Power REIT’s forward-looking statements, see “Risk

Factors” under Item 1A of this document.

Summary

Risk Factors

The

following is a summary of the risks relating to the Company. A more detailed description of each of the risks can be found below

under the section captioned “Risk Factors”.

Risks

Related to our Operations

●

Our

business activities, and the business activities of our cannabis tenant, while believed to be compliant with applicable U.S.

state and local laws, are currently illegal under U.S. federal law.

●

Our

business strategy includes growth plans. Our financial condition and results of operations could be negatively affected if

we fail to grow or fail to manage our growth or investments effectively.

●

Even

if we are able to execute our business strategy, that strategy may not be successful.

●

We

operate in a highly competitive market for investment opportunities and we may be unable to identify and complete acquisitions

of real property assets.

●

Because

we may distribute a significant portion of our income to our stockholders or lenders, we will continue to need additional

capital to make new investments. If additional funds are unavailable or not available on favorable terms, our ability to make

new investments will be impaired.

●

The

investment portfolio is, and in the future may continue to be, concentrated in its exposure to a relatively few number of

investments, industries and lessees.

●

Our

Property portfolio has a high concentration of properties located in certain states.

●

If

our acquisitions or our overall business performance fail to meet expectations, the amount of cash available to us to pay

dividends may decrease and we could default on our loans, which are secured by collateral in our properties and assets.

●

Our

operating results may be negatively affected by potential development and construction delays and resultant increased costs

and risks.

3

●

The

issuance of securities with claims that are senior to those of our common shares, including our Series A Preferred Stock,

may limit or prevent us from paying dividends on its common shares. There is no limitation on our ability to issue securities

senior to the Trust’s common shares or incur indebtedness.

●

The

ability of the Trust to service its obligations and pay dividends depends on the ability of its wholly-owned subsidiaries

to make distributions to it.

●

We

are dependent upon Mr. David H. Lesser for our success. On occasion, his interests may conflict with ours.

●

From

time to time, our management team may own interests in our lessees or other counterparties, and may thereby have interests

that conflict or appear to conflict with the Trust’s interests.

●

Our

lessees and many future lessees will likely be structured as special purpose vehicles (“SPVs”), and therefore

their ability to pay us is expected to be dependent solely on the revenues of a specific project, without additional credit

support.

●

Some

losses related to our real property assets may not be covered by insurance or indemnified by our lessees, and so could adversely

affect us.

●

Discovery

of previously undetected environmentally hazardous conditions may adversely affect our operating results.

●

Legislative,

regulatory, accounting or tax rules, and any changes to them or actions brought to enforce them, could adversely affect us.

●

Changes

in interest rates may negatively affect the value of our assets, our access to debt financing and the trading price of our

securities.

●

Our

quarterly results may fluctuate.

●

We

may not be able to sell our real property assets when we desire. In particular, in order to maintain our status as a REIT,

we may be forced to borrow funds or sell assets during unfavorable market conditions.

●

We

may fail to remain qualified as a REIT, which would reduce the cash available for distribution to our shareholders and may

have other adverse consequences.

●

If

an investment that was initially believed to be a real property asset is later deemed not to have been a real property asset

at the time of investment, we could lose our status as a REIT or be precluded from investing according to our current business

plan.

●

If

we were deemed to be an investment company under the Investment Company Act of 1940, applicable restrictions could make it

impractical for us to continue our business as contemplated and could have a material adverse effect on the price of our securities.

●

Net

leases may not result in fair market lease rates over time.

●

If

a sale-leaseback transaction is recharacterized in a lessee’s bankruptcy proceeding, our financial condition could be

adversely affected.

●

Provisions

of the Maryland General Corporation Law and our Declaration of Trust and Bylaws could deter takeover attempts and have an

adverse impact on the price of our common shares.

Risks

Related to Our Investment Strategy

●

Our

focus on non-traditional real estate asset classes including CEA, alternative energy and transportation infrastructure sectors

will subject us to more risks than if we were broadly diversified to include other asset classes.

●

Renewable

energy resources are complex, and our investments in them rely on long-term projections of resource and equipment availability

and capital and operating costs; if our or our lessees’ projections are incorrect, we may suffer losses.

●

Infrastructure

assets may be subject to the risk of fluctuations in commodity prices and in the supply of and demand for infrastructure consumption.

4

●

Infrastructure

investments are subject to obsolescence risks.

●

Renewable

energy investments may be adversely affected by variations in weather patterns.

●

If

the development of renewable energy projects slows, we may have a harder time sourcing investments.

●

Investments

in renewable energy may be dependent on equipment or manufacturers that have limited operating histories or financial or other

challenges.

Risks

Related to our Securities

●

There

is a 9.9% limit on the amount of our equity securities that any one person or entity may own.

●

Factors

could lead to the Trust losing one or both of its NYSE listings.

●

Low

trading volumes in the Trust’s listed securities may adversely affect holders’ ability to resell their securities

at prices that are attractive, or at all.

●

Our

stock price has fluctuated in the past, has recently been volatile and may be volatile in the future, and as a result, investors

in our common stock could incur substantial losses.

●

Our

ability to issue preferred stock in the future could adversely affect the rights of existing holders of our equity securities.

●

The

issuance of additional equity securities may dilute existing equity holders.

●

Our

equity securities is subject to interest rate risk.

●

Inflation

may negatively affect the value of our equity securities and the dividends we pay.

●

Our

Series A Preferred Stock has not been rated and is junior to our existing and future debt, and the interests of holders of

Series A Preferred Stock could be diluted by the issuance of additional parity-preferred securities and by other transactions.

●

Holders

of Series A Preferred Stock have limited voting rights.

●

The

change of control conversion and delisting conversion features of our Series A Preferred Stock may not adequately compensate

a holder of such securities upon a Change of Control or Delisting Event (as such terms as defined in regard to our Series

A Preferred Stock), and the change of control conversion, delisting conversion and redemption features of our Series A Preferred

Stock may make it more difficult for a party to take over our trust or may discourage a party from taking over our trust.

●

We

may issue additional Series A Preferred Stock at a discount to liquidation value or at a discount to the issuance value of

shares of Series A Preferred Stock already issued.

Risks

Related to Regulation

●

We

cannot assure you that our equity securities will remain listed on the NYSE American.

●

The

U.S. federal government’s approach towards cannabis laws may be subject to change or may not proceed as previously outlined.

●

Laws,

regulations and the policies with respect to the enforcement of such laws and regulations affecting the cannabis industry

in the United States are constantly changing, and we cannot predict the impact that future regulations may have on us.

●

We

may be subject to anti-money laundering laws and regulations in the United States.

●

Litigation,

complaints, enforcement actions and governmental inquiries could have a material adverse effect on our business, financial

condition and results of operations.

●

We

and our cannabis tenant may have difficulty accessing the service of banks, which may make it difficult for us and for them

to operate.

PART

I

Item

1. Business.

Overview

Power

REIT (the “Registrant” or the “Trust”, and together with its consolidated subsidiaries, “we”,

“us”, or “Power REIT”, unless the context requires otherwise) is a Maryland-domiciled real estate investment

trust (a “REIT”) that owns a portfolio of real estate assets related to transportation, energy infrastructure and

Controlled Environment Agriculture (“CEA”) in the United States. In 2019, we expanded the focus of our real estate

acquisitions to include CEA properties in the United States. CEA is an innovative method of growing plants that involves creating

optimized growing environments for a given crop indoors. CEA in the form of a greenhouse uses approximately 70% less energy than

indoor growing, 95% less water usage than outdoor growing, and does not have any agricultural runoff of fertilizers or pesticides.

We typically enter into long-term triple net leases where our tenants are responsible for all costs related to the property, including

insurance, taxes and maintenance.

Our

growth strategy focuses on identifying attractive real estate opportunities that exhibit attractive risk adjusted yields on investment

relative to traditional real estate sectors. We are currently focused on making new acquisitions of real estate within the CEA

sector related to cannabis cultivation. We believe there will be continued strong demand for cannabis related CEA in the form

of greenhouses which we believe is the sustainable business model that can produce plants at a lower cost in an environmentally

friendly way. We believe a convergence of changing public attitudes and increased cannabis legalization momentum in certain states

creates an attractive opportunity to invest in cannabis related real estate. We expect that acquisition opportunities will continue

to expand as additional states legalize the use of cannabis.

5

We

believe there is strong demand for capital from licensed cannabis cultivators that currently do not have access to traditional

financing sources such as bank debt. Our construction financing and sale leaseback solutions provide attractive financing that

allows cannabis operators to add additional growing capacity and/or invest in the growth of their business. Our tenants that are

cannabis operators are able to achieve strong rent coverage based on the growing capacity of their facilities and the current

wholesale price of cannabis. In addition, we believe our unique and flexible lease structure for cannabis operators, which typically

includes a period of higher rent in the initial years of the lease and a reset to a lower rent for the remainder of the lease

term provides strong protection to our investment basis while setting the tenant up for long-term success in the event cannabis

prices decrease or federal legalization of cannabis is enacted.

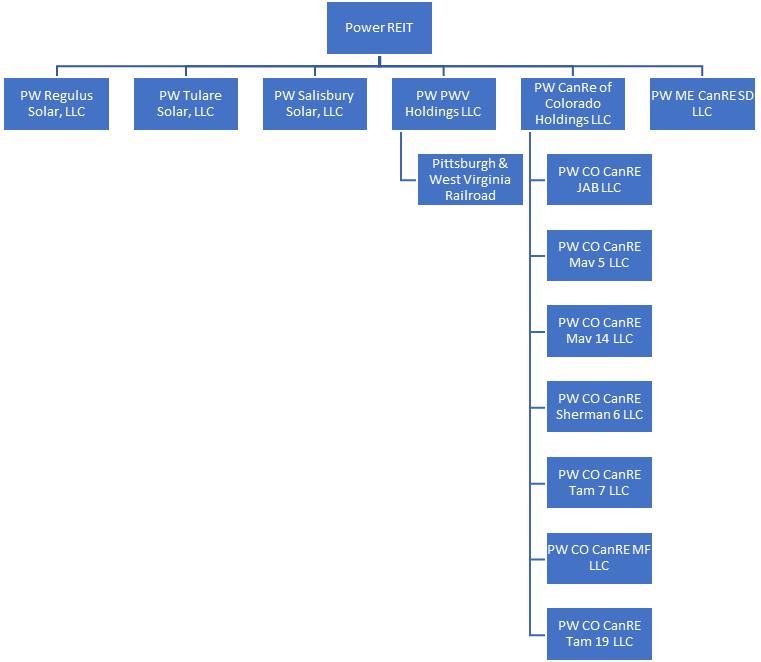

Corporate

Structure

Power

REIT was formed as part of a reorganization and reverse triangular merger of P&WV that closed on December 2, 2011. P&WV

survived the reorganization as a wholly-owned subsidiary of the Registrant. Currently, the Trust is structured as a holding company

and owns its assets through fourteen wholly-owned, special purpose subsidiaries that have been formed in order to hold real estate

assets, obtain financing and generate lease revenue.

The

chart below shows the organizational structure of the Trust as of December 31, 2020.

6

2020

Highlights

During

2020, we acquired nine CEA properties in Colorado and Maine totaling approximately 187,000 square feet of greenhouses and cultivation/processing

buildings representing a total capital commitment of approximately $17.9 million (consisting of purchase price and development

costs but excluding transaction costs). Power REIT entered into seven new triple-net leases and three lease amendments with state-licensed

medical cannabis operators related to these acquisitions which generate straight-line annualized rent of approximately $3.4 million,

representing greater than over 18% yield on invested capital.

Year Ended December 31,

Three

Months Ended

December

31,

2020

2019

2020

2019

Revenue

$

4,272,709

$

2,180,898

$

1,394,613

$

626,823

Net Income Attributable to Common Shareholders

$

1,891,644

$

666,662

$

793,914

$

192,440

Net Income per Common Share (diluted)

0.96

0.36

0.40

0.10

Core FFO Available to Common Shareholders

$

2,560,225

$

1,173,958

$

973,578

$

327,070

Core FFO per Common Share

1.34

0.63

0.51

0.17

Growth Rates:

Revenue

96

%

122

%

Net Income Attributable to Common Shareholders

184

%

313

%

Net Income per Common Share (diluted)

167

%

300

%

Core FFO Available to Common Shareholders

118

%

198

%

Core FFO per Common Share

113

%

200

%

*see Net Income to Core FFO reconciliation in Item 7 below.

2020

Acquisitions

On

January 31, 2020, PW CO CanRe Mav 14, LLC (“PW Mav 14”), one of our indirect subsidiaries, acquired 5.54 acres

of land in Colorado (the “Mav 14 Property”) with an existing greenhouse and processing facility totaling 9,300 square-feet

for the cultivation of cannabis for $850,000. Concurrent with the closing, PW Mav 14 entered into a triple-net lease (the “Mav

14 Lease”) with its current tenant (the “Mav 14 Tenant”) who is responsible for paying all expenses related

to the Mav 14 Property including maintenance expenses, insurances and taxes. As part of the transaction, PW Mav 14 agreed to fund

the construction of 15,120 square feet of greenhouse space for $1,058,400 and the Mav 14 Tenant has agreed to fund the construction

of approximately 2,520 additional square feet of head-house/processing space on the Mav 14 Property. Accordingly, the Trust’s

total capital commitment is $1,908,400. The term of the Mav 14 Lease is 20 years and provides two options to extend for additional

five-year periods. The Mav 14 Lease also has financial guarantees from affiliates of the Mav 14 Tenant. The Mav 14 Tenant intends

to operate as a licensed medical cannabis cultivation and processing facility. The rent for the Mav 14 Lease is structured whereby

after a six-month deferred-rent period, the rental payments provide PW Mav 14 a full return of invested capital over the

next three years in equal monthly payments. Thereafter, rent is structured to provide a 12.5% return based on invested capital

with annual rent increases of 3% rate per annum. At any time after year six, if cannabis is legalized at the federal level, the

rent will be adjusted down to an amount equal to a 9% return on the original invested capital amount and will increase at a 3%

rate per annum based on a starting date of the start of year seven. The Mav 14 Lease requires the Mav 14 Tenant to maintain a

medical cannabis license and operate in accordance with all Colorado and local regulations with respect to its operations. The

Mav 14 Lease prohibits the retail sale of cannabis and cannabis-infused products from the Mav 14 Property. The straight-line annual

rent of approximately $354,000 represents an estimated yield of over 18%. The construction on the project is substantially completed

and the project is currently operational.

7

On

February 20, 2020, PW CO CanRe Sherman 6, LLC (“PW Sherm 6”), one of our indirect subsidiaries, closed on the acquisition

of 5.0 acres of vacant land in Colorado (the “Sherman 6 Property”) for $150,000. As part of the transaction, PW Sherm

6 agreed to fund the immediate construction of 15,120 square feet of greenhouse space and 8,776 square feet of head-house/processing

space on the Sherman 6 Property for $1,693,800. Accordingly, Power REIT’s total capital commitment is $1,843,800. On February

1, 2020, PW Sherm 6 entered into a triple-net lease (the “Initial Sherman Lease”) with its tenant (the “Sherman

6 Tenant”) such that the Sherman 6 Tenant is responsible for paying all expenses related to the Sherman 6 Property including

maintenance expenses, insurances and taxes. The term of the Initial Sherman Lease is 20 years and provides two options to extend

for additional five-year periods. The Initial Sherman Lease also has financial guarantees from affiliates of the tenants. The

tenant intends to operate as a licensed cannabis cultivation and processing facility. The rent for the Initial Sherman Lease is

structured whereby after a nine-month deferred-rent period, the rental payments provide PW Sherm 6 a full return of invested

capital over the next three years in equal monthly payments. Thereafter, rent is structured to provide a 12.9% return based on

invested capital with annual rent increases of 3% rate per annum. At any time after year six, if cannabis is legalized at the

federal level, the rent will be adjusted down to an amount equal to a 9% return on the original invested capital amount and will

increase at a 3% rate per annum based on a starting date of the start of year seven. The Initial Sherman Lease requires the tenant

to maintain a medical cannabis license and operate in accordance with all Colorado and local regulations with respect to its operations.

The Initial Sherman Lease prohibits the retail sale of the tenant’s cannabis and cannabis-infused products from the Sherman

6 Property. The additional straight-line annual rent of approximately $346,000 represents an estimated yield of over 18%. The

construction on the project is substantially completed and the project is currently operational.

On

August 25, 2020, PW Sherm 6 entered into an agreement (as amended, the “Sherman Lease”) for the expansion of the Sherman

6 Property with the Sherman 6 Tenant. The expansion consists of approximately 2,520 square feet of additional greenhouse/headhouse

space. The Sherman 6 Tenant is responsible for implementing the expansion and PW Sherm 6 will fund the cost of such expansion

up to a total of $151,301, with any additional amounts funded by the Sherman 6 Tenant. Once completed, Power REIT’s total

investment in the Sherman 6 Property will be $1,995,101. As part of the agreement, PW Sherm 6 and the Sherman 6 Tenant have amended

the Lease whereby after a nine month period, the additional rental payments provide PW Sherm 6 with a full return of its original

invested capital over the next three years and thereafter, provide a 12.9% return increasing 3% rate per annum. The additional

straight-line rent of approximately $29,000 represents an estimated yield of over 18%.

On

March 19, 2020, PW CO CanRe Mav 5, LLC (“PW Mav 5”), one of our indirect subsidiaries purchased a 5.2 acre of vacant

land in Colorado for $150,000 (the “Mav 5 Property”). As part of the acquisition, the Trust agreed to fund the immediate

construction of 5,040 square feet of greenhouse space and 4,920 square feet of head-house/processing space for $868,125. Accordingly,

Power REIT’s total capital commitment is $1,018,125. Concurrent with the closing, PW Mav 5 entered into a triple-net lease

(the “Mav 5 Lease”) with its current tenant (the “Mav 5 Tenant”) who is responsible for paying all expenses

related to the property including maintenance expenses, insurances and taxes. The term of the Mav 5 Lease is 20 years and provides

two options to extend for additional five-year periods. The Mav 5 Lease also has financial guarantees from affiliates of the Mav

5 Tenant. The Mav 5 Tenant intends to operate as a licensed cannabis cultivation and processing facility. The rent for the Mav

5 Lease is structured whereby after a six-month deferred-rent period, the rental payments provide PW MAV 5 a full return of

invested capital over the next three years in equal monthly payments. Thereafter, rent is structured to provide a 12.5% return

based on invested capital with annual rent increases of 3% rate per annum. At any time after year six, if cannabis is legalized

at the federal level, the rent will be adjusted down to an amount equal to a 9% return on the original invested capital amount

and will increase at a 3% rate per annum based on a starting date of the start of year seven. The lease requires the tenant to

maintain a medical cannabis license and operate in accordance with all Colorado and local regulations with respect to its operations.

The Mav 5 Lease prohibits the retail sale of cannabis and cannabis-infused products from the Mav 5 Property. The straight-line

annual rent of approximately $193,000 represents an estimated yield of over 18%.

8

On

May 1, 2020, PW Mav 5, entered into an agreement for a 5,040 square-foot greenhouse expansion. Our investment in the expansion

is $340,539 and a lease amendment, entered into on May 1, 2020 is structured to provide rent on similar economics to the original

Mav 5 Lease and provides additional straight-line annual rent of approximately $63,000, representing an estimated yield of over

18%. The construction on the project is substantially completed and the project is currently operational.

On

May 15, 2020, PW ME CanRe SD, LLC (“PW SD”), one of our indirect subsidiaries, acquired a 3.06-acre property in York

County, Maine for $1,000,000 (the “495 Property”). The SD Property includes a 32,800 square-foot greenhouse and 2,800

square foot processing/distribution building that are both under active construction. Simultaneous with the acquisition, PW SD

entered into a lease (the “SD Lease”) with an operator (“Sweet Dirt”). As part of the acquisition, PW

SD reimbursed Sweet Dirt for $950,000 of the approximately $1.5 million Sweet Dirt has incurred related to the construction and

agreed to fund up to approximately $2.97 million of costs to complete the construction. Accordingly, our total investment in the

495 Property will be approximately $4.92 million which translates to approximately $138 per square foot for a state-of-the-art

Controlled Environment Agriculture Greenhouse (“CEAG”). The rent for the Sweet Dirt Lease is structured whereby after

a six-month deferred-rent period, the monthly rental payments over the next three years will provide us with a full return of

invested capital. Thereafter, rent is structured to provide a 12.9% return based on invested capital with annual rent increases

of 3% rate per annum. At any time after year six, if cannabis is legalized at the federal level, we have agreed to decrease the

rent to an amount equal to a 9% return on the original invested capital amount with increases at a 3% rate per annum based on

a starting date of the start of year seven. SD Lease is structured to provide straight-line annual rent of approximately $920,000,

representing an estimated yield of over 18.5% with the tenant responsible for all operating expenses. The SD Lease requires Sweet

Dirt to maintain a medical cannabis license and operate in accordance with all Maine and local regulations with respect to its

operations. In addition, we received an option to acquire an adjacent 3.58 vacant parcel (the “505 Property”) that

is owned by Sweet Dirt for $400,000 which provides us the option to finance additional cultivation and processing space for Sweet

Dirt.

On

September 18, 2020, PW SD completed the acquisition of the 505 Property in York County, Maine by exercising its option

received at the time of the 495 Property acquisition. The 505 Property is a 3.58-acre property purchased for $400,000 plus

closing costs and is adjacent to the 495 Property. Concurrently with the closing of the acquisition of the 505 Property, PW

SD and Sweet Dirt entered into an amendment to the SD Lease whereby after a nine-month deferred-rent period, the rental

payments provide PW SD a full return of invested capital over the next three years. Thereafter, rent is structured to

provide a 13.2% return based on invested capital with annual rent increases of 3% per annum. At any time after year six, if

cannabis is legalized at the federal level in the United States, the rent will be adjusted down to an amount equal to a 9%

return on the original invested capital amount and will increase at a 3% rate per annum based on a starting date of the start

of year seven. The amended SD Lease provides for a straight-line annual rent of approximately $373,000, representing an

estimated yield of over 18.5% with the tenant responsible for all operating expenses. As part of the transaction, the Trust

agreed to fund the construction of an additional 9,900 square feet of processing space and renovate an existing 2,738 square

foot building for approximately $1.56 million. Accordingly, the Trust’s total investment in the 505 Property will be

approximately $1.96 million.

9

On

September 18, 2020, PW CO CanRE Tam 7, LLC (“Tam 7”), one of our indirect subsidiaries, acquired a 4.32-acre property

in Crowley County, Colorado for $150,000 (the “Tam 7 Property”). As part of the transaction, Tam 7 agreed to fund

the immediate construction of 18,000 square feet of greenhouse and processing space on the Tam 7 Property for approximately $1.22

million. Accordingly, the Trust’s total capital commitment will be $1,364,585. Concurrent with the closing, Tam 7 entered

into a triple-net lease (the “Tam 7 Lease”) with its current tenant (the “Tam 7 Tenant”) who is

responsible for paying all expenses related to the Tam 7 Property including maintenance expenses, insurances and taxes. The term

of the Tam 7 Lease is 20 years and provides two options to extend for additional five-year periods. The Tam 7 Lease also has financial

guarantees from affiliates of the Tam 7 Tenant. The Tam 7 Tenant intends to operate as a licensed cannabis cultivation and processing

facility. The rent for the Tam 7 Lease is structured whereby after a six-month deferred-rent period, the rental payments provide

Tam 7 a full return of invested capital over the next three years in equal monthly payments. Thereafter, rent is structured

to provide a 12.9% return based on invested capital with annual rent increases of 3% rate per annum. At any time after year six,

if cannabis is legalized at the federal level in the United States, the rent will be adjusted down to an amount equal to a 9%

return on the original invested capital amount and will increase at a 3% rate per annum based on a starting date of the start

of year seven. The Tam 7 Lease requires the Tam 7 Tenant to maintain a medical cannabis license and operate in accordance with

all Colorado and local regulations with respect to its operations and prohibits the retail sale of cannabis and cannabis-infused

products from the property. The additional straight-line annual rent of approximately $262,000 represents an estimated yield of

over 18.5% on invested capital. The project is currently under construction and should be completed by May 2021.

On

October 2, 2020, PW CO CanRE MF, LLC (“PW MF”), one of our indirect subsidiaries, acquired two properties in Crowley

County, Colorado approved for cannabis cultivation for $150,000 (the “PW MF Properties”). One parcel is 2.37 acres,

and the other parcel is 2.09 acres. As part of the transaction, the PW MF agreed to fund the immediate construction of 33,744

square feet of greenhouse and processing space on the PW MF Properties for $2,912,300. Accordingly, the Trust’s total capital

commitment will be approximately $3,062,000. On October 15, 2020, PW MF entered into a triple-net lease (the “PSP Lease”)

with PSP Management LLC (“PSP”) who is responsible for paying all expenses related to the PW MF Properties including

maintenance expenses, insurances and taxes. The term of the lease is 20 years and provides two options to extend for additional

twenty-year periods. The PSP Lease also has financial guarantees from affiliates of PSP. PSP intends to operate as a licensed

cannabis cultivation and processing facility. The rent for the PSP Lease is structured whereby after deferred-rent period, the

rental payments provide PW MF a full return of invested capital over the next three years in equal monthly payments. Thereafter,

rent is structured to provide a 13.3% return based on invested capital with annual rent increases of 3% rate per annum. At any

time after year six, if cannabis is legalized at the federal level in the United States, the rent will be adjusted down to an

amount equal to a 9% return on the original invested capital amount and will increase at a 3% rate per annum based on a starting

date of the start of year seven. The PSP Lease requires the tenant to maintain a medical cannabis license and operate in accordance

with all Colorado and local regulations with respect to its operations. The PSP Lease prohibits the retail sale of the tenant’s

cannabis and cannabis-infused products from the PW MF Properties. The additional straight-line annual rent of approximately $579,000

represents an estimated yield of approximately 18.9%. The project is currently under construction and should be completed by August

2021.

10

On

December 4, 2020, PW CO CanRE Tam 19, LLC (“PW Tam 19”), one of our indirect subsidiaries, acquired a 2.11 parcel

of land in Crowley County, Colorado approved for cannabis cultivation for $75,000 (the “PW Tam 19 Property”). As part

of the transaction, PW Tam 19 agreed to fund the immediate construction of 18,528 square feet of greenhouse and processing space

on the PW Tam 19 Property for $1,236,116. Accordingly, the Trust’s total capital commitment will be approximately $1,311,000.

Concurrent with the closing, PW Tam 19 entered into a triple-net lease (the “Tam19 Lease”) with Green Mile Cultivation,

LLC (“Tam 19 Tenant”) who is responsible for paying all expenses related to PW Tam 19 Property including maintenance

expenses, insurances and taxes. The term of the lease is 20 years and provides two options to extend for additional five-year

periods. The Tam 19 Lease has financial guarantees from affiliates of Tam 19 Tenant. The Tam 19 Tenant intends to operate as a

licensed cannabis cultivation and processing facility. The rent for the Tam 19 Lease is structured whereby after a deferred-rent

period, the rental payments provide PW Tam 19 a full return of invested capital over the next three years in equal monthly

payments. Thereafter, rent is structured to provide a 12.9% return based on invested capital with annual rent increases of 3%

rate per annum. At any time after year six, if cannabis is legalized at the federal level in the United States, the rent will

be adjusted down to an amount equal to a 9% return on the original invested capital amount and will increase at a 3% rate per

annum based on a starting date of the start of year seven. The Tam 19 Lease requires the tenant to maintain a medical cannabis

license and operate in accordance with all Colorado and local regulations with respect to its operations. The Tam 19 Lease prohibits

the retail sale of the tenant’s cannabis and cannabis-infused products from the PW Tam 19 Property. The additional straight-line

annual rent of approximately $252,000 represents an estimated yield of approximately 18.5%. The project is currently under construction

and should be completed by August 2021.

2021

Acquisitions

On

January 4, 2021, we acquired two properties located in southern Colorado through a newly formed wholly owned subsidiary (“PW

Grail”) of our wholly owned subsidiary for $150,000. The properties (the “Grail Properties”) are comprised

of 4.41 acres. As part of the transaction, we agreed to fund the immediate construction of an approximately 21,732 square foot

greenhouse and processing facility for approximately $1.84 million including the land acquisition cost. Concurrent with the acquisition,

PW Grail entered into a 20-year “triple-net” lease (the “Grail Project Lease”) with The Grail Project

LLC (“Grail Project”) which will operate a cannabis cultivation facility. The lease requires Grail Project to pay

all property related expenses including maintenance, insurance and taxes. After the initial 20-year term, the Grail Project’s

Lease provides four, five-year renewal options. The lease also has a personal guarantee from the owner of Grail Project. Grail

Project intends to operate the Grail Properties as licensed cannabis cultivation and processing facilities. The rent for the Grail

Project Lease is structured whereby after a six-month free-rent period, the rental payments provide Power REIT a full return of

invested capital over the next three years in equal monthly payments. After the 42nd month, rent is structured to provide

a 12.9% return on the original invested capital amount which will increase at a 3% rate per annum. At any time after year six,

if cannabis is legalized at the federal level, the rent will be readjusted down to an amount equal to a 9% return on the original

invested capital amount and will increase at a 3% rate per annum based on a starting date of the start of year seven. On February

23, 2021 PW Grail amended the Grail Project Lease making approximately $518,000 of more funds available to construct an

additional 6,256 square feet to the cannabis cultivation and processing space. Accordingly, the Trust’s total capital commitment

is approximately $2.4 million.

On

January 14, 2021, we acquired a property (the “Apotheke Property”) for $150,000 located in southern Colorado

through a newly formed wholly owned subsidiary (“PW Apotheke”) of our wholly owned subsidiary which is comprised of

4.31 acres. As part of the transaction, we agreed to fund the immediate construction of an approximately 21,548 square foot greenhouse

and processing facility for approximately $1.8 million including the land acquisition cost. Concurrent with the acquisition, PW

Apotheke entered into a 20-year “triple-net” lease (the “Apotheke Lease”) with DOM F, LLC (“Dom

F”) which will operate a cannabis cultivation facility. The lease requires Dom F to pay all property related expenses including

maintenance, insurance and taxes. After the initial 20-year term, Apotheke Lease provides two, five-year renewal options. The

lease also has a personal guarantee from the owner of Dom F. and Dom F intends to operate the Apotheke Property as a licensed

cannabis cultivation and processing facility. The rent for the Apotheke Lease is structured whereby after an eight-month free-rent

period, the rental payments provide Power REIT a full return of invested capital over the next three years in equal monthly

payments. After the 44th month, rent is structured to provide a 12.9% return on the original invested capital amount which will

increase at a 3% rate per annum. At any time after year six, if cannabis is legalized at the federal level, the rent will be readjusted

down to an amount equal to a 9% return on the original invested capital amount and will increase at a 3% rate per annum based

on a starting date of the start of year seven.

11

On

January 29, 2021, we acquired a property located in Riverside County, CA (the “Canndescent Property”) through a newly

formed wholly owned subsidiary (“PW Canndescent”). The purchase price was $7.685 million and we paid for the property

with $2.685 million cash on hand and the issuance of 192,678 shares of Power REIT’s Series A Preferred Stock. PW Canndescent

received an assignment of a lease (the “Canndescent Lease”) to allow the tenant (“Canndescent”) to operate

the 37,000 square foot greenhouse cultivation facility on the Canndescent Property. Canndescent is a premium flower brand for

luxury cannabis in California. The Canndescent Lease requires Canndescent to pay all property related expenses including maintenance,

insurance and taxes. The rent for the Canndescent Lease is structured to provide straight-line annual rent of approximately $1,074,000.

On

March 12, 2021, we acquired a property (the “Gas Station Property”) for $85,000 located in southern Colorado

through a newly formed wholly owned subsidiary (“PW Gas Station”) of our wholly owned subsidiary which is comprised

of 2.2 acres. As part of the transaction, we agreed to fund the immediate construction of an approximately 24,512 square foot

greenhouse and processing facility for approximately $2.1 million including the land acquisition cost. Concurrent with the acquisition,

PW Gas Station entered into a 20-year “triple-net” lease (the “Gas Station Lease”) with The Gas Station,

LLC (“Gas Station”) which will operate a cannabis cultivation facility. The lease requires Gas Station to pay all

property related expenses including maintenance, insurance and taxes. After the initial 20-year term, Gas Station Lease provides

two, five-year renewal options. The lease also has a personal guarantee from the owners of Gas Station and they intend to operate

the Gas Station Property as a licensed cannabis cultivation and processing facility. The rent for the Gas Station Lease is structured

whereby after an eight-month free-rent period, the rental payments provide Power REIT a full return of invested capital

over the next three years in equal monthly payments. After the 43rd month, rent is structured to provide a 13.3% return on the

original invested capital amount which will increase at a 3% rate per annum. At any time after year six, if cannabis is legalized

at the federal level, the rent will be readjusted down to an amount equal to a 9% return on the original invested capital amount

and will increase at a 3% rate per annum based on a starting date of the start of year seven.

Management

and Trustees - Human Capital

Mr.

David H. Lesser serves as a member and Chairman of our Board of Trustees. He also serves as our Chief Executive Officer, Chief

Financial Officer, Secretary and Treasurer. In July, 2020 Susan Hollander was named Chief Accounting Officer with responsibility

for all strategic accounting, compliance and financial reporting functions. In July, 2020 we also announced the appointment of

Paula Poskon to our board of Trustees. Ms. Poskon has 20+ years expertise in real estate and capital markets with a particular

focus on REITS. Currently, Power REIT has no other officers or employees but as Power REIT’s business grows, the Trust will

from time to time evaluate its staffing and third-party service needs and adjust its staffing as necessary.

We

believe that our success depends on our ability to retain our key personnel, primarily David Lesser, our Chairman and Chief Executive

Officer. We believe that the skills, experience and industry knowledge of our key employees significantly benefit our operations

and performance.

Employee

health and safety in the workplace is one of our core values. The COVID-19 pandemic has underscored for us the importance of keeping

our employees safe and healthy. In response to the pandemic, we have taken actions aligned with the World Health Organization

and the Centers for Disease Control and Prevention in an effort to protect our workforce so they can more safely and effectively

perform their work.

Employee

levels are managed to align with the pace of business and management believes it has sufficient human capital to operate its business

successfully.

12

Growth

and Investment Strategies

In

2019 and 2020, we expanded the focus of our real estate acquisitions to include CEA properties in the United States. CEA is an

innovative method of growing plants that involves creating optimized growing environments for a given crop indoors. CEA uses approximately

70% less energy than indoor growing, 95% less water usage than outdoor growing, and does not have any agricultural runoff of fertilizers

or pesticides. We typically enter into long-term triple net leases where our tenants are responsible for all costs related to

the property, including insurance, taxes and maintenance.

Our

growth strategy focuses on identifying attractive real estate opportunities that exhibit attractive risk adjusted yields on investment

relative to traditional real estate sectors. We are currently focused on making new acquisitions of real estate within the CEA

sector related to cannabis cultivation. We believe there will be continued strong demand for cannabis related CEA which we believe

is the sustainable business model that can produce plants at a lower cost in an environmentally friendly way. We believe a convergence

of changing public attitudes and increased cannabis legalization momentum in certain states creates an attractive opportunity

to invest in cannabis related real estate. We expect that acquisition opportunities will continue to expand as additional states

legalize the use of cannabis.

We

believe there is strong demand for capital from licensed cannabis cultivators that currently do not have access to traditional

financing sources such as bank debt. Our construction financing and sale leaseback solutions provide attractive financing that

allows cannabis operators to add additional growing capacity and/or invest in the growth of their business. Our tenants that are

cannabis operators are able to achieve strong rent coverage based on the growing capacity of their facilities and the current

wholesale price of cannabis. In addition, we believe our unique and flexible lease structure for cannabis operators, which typically

includes a period of higher rent in the initial years of the lease and a reset to a lower rent for the remainder of the lease

term provides strong protection to our investment basis while setting the tenant up for long-term success in the event cannabis

prices decrease or federal legalization of cannabis is enacted.

Properties

As

of December 31, 2020, the Trust’s assets consisted of a total of approximately 112 miles of railroad infrastructure plus

branch lines and related real estate, approximately 601 acres of fee simple land leased to seven utility scale solar power generating

projects with an aggregate generating capacity of approximately 108 Megawatts (“MW”), and approximately 41 acres of

land with 216,278 square feet of greenhouse/processing space for medical cannabis cultivation. We are actively seeking to grow

our portfolio of real estate related to CEA for food and cannabis cultivation.

13

Below

is a chart that summarizes our properties as of December 31, 2020:

Property Type/Name

Location

Acres

Size1

Lease Start

Term (yrs)2

Rent ($)

Gross Book Value

Railroad Property

P&WV (Norfolk Southern)

PA/WV/OH

112 miles

Oct-64

99

$

915,000

$

9,150,000

Solar Farm Land

PWSS

Salisbury, MA

54

5.7

Dec-11

22

89,494

1,005,538

PWTS

Tulare County, CA

18

4.0

Mar-13

25

32,500

310,000

PWTS

Tulare County, CA

18

4.0

Mar-13

25

37,500

310,000

PWTS

Tulare County, CA

10

4.0

Mar-13

25

16,800

310,000

PWTS

Tulare County, CA

10

4.0

Mar-13

25

29,900

310,000

PWTS

Tulare County, CA

44

4.0

Mar-13

25

40,800

310,000

PWRS

Kern County, CA

447

82.0

Apr-14

20

803,117

9,183,548

Solar Farm Land Total

601

107.7

$

1,050,111

$

11,739,086

CEA (Cannabis) Property34

JAB - Tam Lot 18

Crowley County, CO

2.11

12,996

Jul-19

20

201,810

1,075,000

JAB - Mav Lot 1

Crowley County, CO

5.20

16,416

Jul-19

20

294,046

1,594,582

Grassland - Mav Lot 14

Crowley County, CO

5.54

26,940

Feb-20

20

354,461

1,908,400

Chronic - Sherman Lot 6

Crowley County, CO

5.00

26,416

Feb-20

20

375,159

1,995,101

Original - Mav Lot 5

Crowley County, CO

5.20

15,000

Apr-20

20

256,743

1,358,664

Sweet Dirt 495

York County, ME

3.06

35,600

May-20

20

919,849

4,917,134

Sweet Dirt 505

York County, ME

3.58

12,638

Sep-20

20

373,055

1,964,723

Fifth Ace - Tam Lot 7

Crowley County, CO

4.32

18,000

Sep-20

20

261,963

1,364,585

Monte Fiore - Tam Lot 13

Crowley County, CO

2.37

9,384

Oct-20

20

87,964

425,000

Monte Fiore - Tam Lot 14

Crowley County, CO

2.09

24,360

Oct-20

20

490,700

2,637,300

Green Mile - Tam Lot 19

Crowley County, CO

2.11

18,528

Dec-20

20

252,061

1,311,116

CEA Total

40.58

216,278

$

3,867,811

$

20,551,605

Grand Total

$

5,832,922

$

41,440,691

1

Solar Farm Land

size represents Megawatts and CEA property size represents square feet

2

Not including renewal options

3

Rent represents straight line net rent

4

Gross Book Value represents total commitment

Note: Size, Rent

and Gross Book Value assume completion of approved construction

Railway

Properties

Pittsburgh

& West Virginia Railroad (“P&WV”) is a business trust organized under the laws of Pennsylvania for the purpose

of owning railroad assets that are currently leased to Norfolk Southern Railway (“NSC”) pursuant to a 99-year lease

that became effective in 1964 and is subject to an unlimited number of 99-year renewal periods under the same terms and conditions,

including annual rent payments, at the option of NSC (the “Railroad Lease”). Norfolk Southern Corporation has an investment

grade rating of Baa1 by Moody’s Investor Services. P&WV’s assets consist of a railroad line of approximately 112

miles in length plus branch lines, extending through Connellsville, Washington and Allegheny Counties in the Commonwealth of Pennsylvania,

through Brooke County in the State of West Virginia and through Jefferson and Harrison Counties in the State of Ohio, to Pittsburgh

Junction in Harrison County, Ohio. There are also branch lines that total approximately 20 miles in length located in Washington

and Allegheny Counties in Pennsylvania and Brooke County in West Virginia. NSC pays P&WV base cash rent of $915,000 per year,

payable in quarterly installments.

Solar

Properties

PW

Salisbury Solar, LLC (“PWSS”) is a Massachusetts limited liability company and a wholly owned subsidiary of the Trust

that owns approximately 54 acres of land located in Salisbury, Massachusetts that is leased to a 5.7 Megawatts (MW) utility scale

solar farm. Pursuant to the lease agreement, PWSS’ tenant was required to pay PWSS rent of $80,800 cash for the year

December 1, 2012 to November 30, 2013, with a 1.0% escalation in each corresponding year thereafter. Rent is payable quarterly

in advance and is recorded by Power REIT for accounting purposes on a straight-line basis. At the end of the 22-year lease period,

which commenced on December 1, 2011 (prior to being assumed by PWSS), the tenant has certain renewal options, with terms to be

mutually agreed upon.

14

PW

Tulare Solar, LLC (“PWTS”) is a California limited liability company and a wholly owned subsidiary of the Trust that

owns approximately 100 acres of land leased to five (5) utility scale solar farms, with an aggregate generating capacity of approximately

20MW, located near Fresno, California. The solar farm tenants pay PWTS an aggregate annual rent of $157,500 cash following an

abatement period, payable annually in advance, and without escalation during the 25-year term of the leases. The tenants have

up to two renewal options, the first of which is for 5 years, and the second of which is for 4 years and 11 months. At

the end of the 25-year terms, which commenced in March 2013 (prior to being assumed by PWTS), the tenants have certain renewal

options, with terms to be mutually agreed upon.

PW

Regulus Solar, LLC (“PWRS”) is a California limited liability company and a wholly owned subsidiary of the Trust

that owns approximately 447 acres of land leased to a utility scale solar farm with an aggregate generating capacity of approximately

82 Megawatts in Kern County, California near Bakersfield. PWRS’s lease was structured to provide it with initial quarterly

rental payments until the solar farm achieved commercial operation which occurred on November 11, 2014. During the primary term

of the lease which extends for 20 years from achieving commercial operations, PWRS receives an initial annual rent of approximately

$735,000 per annum which grows at 1% per annum. The lease is a “triple net” lease with all expenses to be paid by

the tenant. At the end of the primary term of the lease, the tenants have three options to renew the lease for 5-year terms in

the first two options, and 4 years and 11 months in the third renewal option. With each such extension option are required to

be undertaken by tenant under certain circumstances. Rent during the renewal option periods is to be calculated as the greater

of a minimum stated rental amount or a percentage of the total project-level gross revenue. The acquisition price, not including

transaction and closing costs, was approximately $9.2 million. For each of the twelve months ended December 31, 2020 and 2019,

PWRS recorded rental income of $803,116.

CEA

Properties

In

July 2019, PW CO CanRE JAB, LLC (“PW JAB”), one of our indirect subsidiaries, acquired two properties (the “JAB

Properties”) in southern Colorado that have approximately 7.3 acres with 18,612 square feet of greenhouse cultivation and

processing space. At the time of the acquisition, PW JAB entered into two cross-collateralized and cross-defaulted triple-net

leases with JAB Industries Ltd. (doing business as Wildflower Farms) (the “JAB Tenant”) for the JAB Properties. The

leases provide that the JAB Tenant is responsible for paying all expenses related to the JAB Properties, including maintenance

expenses, insurance and taxes. The term of each of the leases is 20 years and provides two options to extend for additional five-year

periods. The leases also have financial guarantees from affiliates of the JAB Tenant. The JAB Tenant intends to operate the JAB

Properties as licensed medical cannabis cultivation and processing facilities. The rent for each of the leases is structured whereby

after a six-month free-rent period, the rental payments provide the PW JAB a full return of invested capital over the next

three years in equal monthly payments. Thereafter, rent is structured to provide a 12.5% return on invested capital, which will

increase at a 3% rate per annum. At any time after year six, if cannabis is legalized at the federal level, the rent will be adjusted

down to an amount equal to a 9% return on the original invested capital amount and will increase at a 3% rate per annum based

on a starting date of the start of year seven. The JAB Tenant is an affiliate of a company that owns and operates two indoor cannabis

cultivation facilities and five dispensary locations in the State of Colorado along with several other cannabis related projects

under development. The leases require the JAB Tenant to maintain a medical cannabis license and operate in accordance with all

Colorado and local regulations with respect to its operations. The leases prohibit the retail sale of the JAB Tenant’s cannabis

and cannabis-infused products from the JAB Properties. The straight-line annual rent of approximately $331,000 represents an estimated

yield of over 18%.

15

On

November 1, 2019, PW JAB, entered into an agreement with the JAB Tenant to expand the greenhouse at the 5.2-acre property from

approximately 5,616 rentable square feet of greenhouse to approximately 16,416 square feet. Our investment in the expansion was

$900,000 and the lease amendment is structured to provide rent on similar economics to the original leases and provides additional

straight-line annual rent of approximately $165,000, representing an estimated yield of over 18%. The completion of this expansion

occurred in July 2020.

On

January 31, 2020, PW CO CanRe Mav 14, LLC (“PW Mav 14”), one of our indirect subsidiaries, acquired 5.54 acres

of land in Colorado (the “Mav 14 Property”) with an existing greenhouse and processing facility totaling 9,300 square-feet

for the cultivation of cannabis for $850,000. Concurrent with the closing, PW Mav 14 entered into a triple-net lease (the “Mav

14 Lease”) with its current tenant (the “Mav 14 Tenant”) who is responsible for paying all expenses related

to the Mav 14 Property including maintenance expenses, insurances and taxes. As part of the transaction, PW Mav 14 agreed to fund

the construction of 15,120 square feet of greenhouse space for $1,058,400 and the Mav 14 Tenant has agreed to fund the construction

of approximately 2,520 additional square feet of head-house/processing space on the Mav 14 Property. Accordingly, the Trust’s

total capital commitment is $1,908,400. The term of the Mav 14 Lease is 20 years and provides two options to extend for additional

five-year periods. The Mav 14 Lease also has financial guarantees from affiliates of the Mav 14 Tenant. The Mav 14 Tenant intends

to operate as a licensed medical cannabis cultivation and processing facility. The rent for the Mav 14 Lease is structured whereby

after a six-month deferred-rent period, the rental payments provide PW Mav 14 a full return of invested capital over the

next three years in equal monthly payments. Thereafter, rent is structured to provide a 12.5% return based on invested capital

with annual rent increases of 3% rate per annum. At any time after year six, if cannabis is legalized at the federal level, the

rent will be adjusted down to an amount equal to a 9% return on the original invested capital amount and will increase at a 3%

rate per annum based on a starting date of the start of year seven. The Mav 14 Lease requires the Mav 14 Tenant to maintain a

medical cannabis license and operate in accordance with all Colorado and local regulations with respect to its operations. The

Mav 14 Lease prohibits the retail sale of cannabis and cannabis-infused products from the Mav 14 Property. The straight-line annual

rent of approximately $354,000 represents an estimated yield of over 18%. The construction on the project is completed and the

project is currently operational.

On

February 20, 2020, PW CO CanRe Sherman 6, LLC (“PW Sherm 6”), one of our indirect subsidiaries, closed on the acquisition

of 5.0 acres of vacant land in Colorado (the “Sherman 6 Property”) for $150,000. As part of the transaction, PW Sherm

6 agreed to fund the immediate construction of 15,120 square feet of greenhouse space and 8,776 square feet of head-house/processing

space on the Sherman 6 Property for $1,693,800. Accordingly, Power REIT’s total capital commitment is $1,843,800. On February

1, 2020, PW Sherm 6 entered into a triple-net lease (the “Initial Sherman Lease”) with its tenant (the “Sherman

6 Tenant”) such that the Sherman 6 Tenant is responsible for paying all expenses related to the Sherman 6 Property including

maintenance expenses, insurances and taxes. The term of the Initial Sherman Lease is 20 years and provides two options to extend

for additional five-year periods. The Initial Sherman Lease also has financial guarantees from affiliates of the tenants. The

tenant intends to operate as a licensed cannabis cultivation and processing facility. The rent for the Initial Sherman Lease is

structured whereby after a nine-month deferred-rent period, the rental payments provide PW Sherm 6 a full return of invested

capital over the next three years in equal monthly payments. Thereafter, rent is structured to provide a 12.9% return based on

invested capital with annual rent increases of 3% rate per annum. At any time after year six, if cannabis is legalized at the

federal level, the rent will be adjusted down to an amount equal to a 9% return on the original invested capital amount and will

increase at a 3% rate per annum based on a starting date of the start of year seven. The Initial Sherman Lease requires the tenant

to maintain a medical cannabis license and operate in accordance with all Colorado and local regulations with respect to its operations.

The Initial Sherman Lease prohibits the retail sale of the tenant’s cannabis and cannabis-infused products from the Sherman

6 Property. The additional straight-line annual rent of approximately $346,000 represents an estimated yield of over 18%. The

construction is complete and the project is currently operational.

16

On

August 25, 2020, PW Sherm 6 entered into an agreement (as amended, the “Sherman Lease”) for the expansion of the Sherman

6 Property with the Sherman 6 Tenant. The expansion consists of approximately 2,520 square feet of additional greenhouse/headhouse

space. The Sherman 6 Tenant is responsible for implementing the expansion and PW Sherm 6 will fund the cost of such expansion

up to a total of $151,301, with any additional amounts funded by the Sherman 6 Tenant. Once completed, Power REIT’s total

investment in the Sherman 6 Property will be $1,995,101. As part of the agreement, PW Sherm 6 and the Sherman 6 Tenant have amended

the Lease whereby after a nine-month period, the additional rental payments provide PW Sherm 6 with a full return of its original

invested capital over the next three years and thereafter, provide a 12.9% return increasing 3% rate per annum. The additional

straight-line rent of approximately $29,000 represents an estimated yield of over 18%.

On

March 19, 2020, PW CO CanRe Mav 5, LLC (“PW Mav 5”), one of our indirect subsidiaries purchased a 5.2 acre of vacant

land in Colorado for $150,000 (the “Mav 5 Property”). As part of the acquisition, the Trust agreed to fund the immediate

construction of 5,040 square feet of greenhouse space and 4,920 square feet of head-house/processing space for $868,125. Accordingly,

Power REIT’s total capital commitment is $1,018,125. Concurrent with the closing, PW Mav 5 entered into a triple-net lease

(the “Mav 5 Lease”) with its current tenant (the “Mav 5 Tenant”) who is responsible for paying all expenses

related to the property including maintenance expenses, insurances and taxes. The term of the Mav 5 Lease is 20 years and provides

two options to extend for additional five-year periods. The Mav 5 Lease also has financial guarantees from affiliates of the Mav

5 Tenant. The Mav 5 Tenant intends to operate as a licensed cannabis cultivation and processing facility. The rent for the Mav

5 Lease is structured whereby after a six-month deferred-rent period, the rental payments provide PW MAV 5 a full return of

invested capital over the next three years in equal monthly payments. Thereafter, rent is structured to provide a 12.5% return

based on invested capital with annual rent increases of 3% rate per annum. At any time after year six, if cannabis is legalized

at the federal level, the rent will be adjusted down to an amount equal to a 9% return on the original invested capital amount

and will increase at a 3% rate per annum based on a starting date of the start of year seven. The lease requires the tenant to

maintain a medical cannabis license and operate in accordance with all Colorado and local regulations with respect to its operations.

The Mav 5 Lease prohibits the retail sale of cannabis and cannabis-infused products from the Mav 5 Property. The straight-line

annual rent of approximately $193,000 represents an estimated yield of over 18%.

On

May 1, 2020, PW Mav 5, entered into an agreement for a 5,040 square-foot greenhouse expansion. Our investment in the expansion

is $340,539 and a lease amendment, entered into on May 1, 2020 is structured to provide rent on similar economics to the original

Mav 5 Lease and provides additional straight-line annual rent of approximately $63,000, representing an estimated yield of over

18%. The construction on the project is complete and the project is currently operational.

On

May 15, 2020, PW ME CanRe SD, LLC (“PW SD”), one of our indirect subsidiaries, acquired a 3.06-acre property in York

County, Maine for $1,000,000 (the “495 Property”). The SD Property includes a 32,800 square-foot greenhouse and 2,800

square foot processing/distribution building that are both under active construction. Simultaneous with the acquisition, PW SD

entered into a lease (the “SD Lease”) with an operator (“Sweet Dirt”). As part of the acquisition, PW

SD reimbursed Sweet Dirt for $950,000 of the approximately $1.5 million Sweet Dirt has incurred related to the construction and

agreed to fund up to approximately $2.97 million of costs to complete the construction. Accordingly, our total investment in the

495 Property will be approximately $4.92 million which translates to approximately $138 per square foot for a state-of-the-art

Controlled Environment Agriculture Greenhouse (“CEAG”). The rent for the Sweet Dirt Lease is structured whereby after

a six-month deferred-rent period, the monthly rental payments over the next three years will provide us with a full return of

invested capital. Thereafter, rent is structured to provide a 12.9% return based on invested capital with annual rent increases

of 3% rate per annum. At any time after year six, if cannabis is legalized at the federal level, we have agreed to decrease the

rent to an amount equal to a 9% return on the original invested capital amount with increases at a 3% rate per annum based on

a starting date of the start of year seven. SD Lease is structured to provide straight-line annual rent of approximately $920,000,

representing an estimated yield of over 18.5% with the tenant responsible for all operating expenses. The SD Lease requires Sweet

Dirt to maintain a medical cannabis license and operate in accordance with all Maine and local regulations with respect to its

operations. The construction on the 495 property is complete and the property is operational. In addition, we received an option

to acquire an adjacent 3.58 vacant parcel (the “505 Property”) that is owned by Sweet Dirt for $400,000 which provides

us the option to finance additional cultivation and processing space for Sweet Dirt.

17

On

September 18, 2020, PW SD completed the acquisition of the 505 Property in York County, Maine by exercising its option

received at the time of the 495 Property acquisition. The 505 Property is a 3.58-acre property purchased for $400,000 plus

closing costs and is adjacent to the 495 Property. Concurrently with the closing of the acquisition of the 505 Property, PW

SD and Sweet Dirt entered into an amendment to the SD Lease whereby after a nine-month deferred-rent period, the rental

payments provide PW SD a full return of invested capital over the next three years. Thereafter, rent is structured to

provide a 13.2% return based on invested capital with annual rent increases of 3% per annum. At any time after year six, if

cannabis is legalized at the federal level in the United States, the rent will be adjusted down to an amount equal to a 9%

return on the original invested capital amount and will increase at a 3% rate per annum based on a starting date of the start

of year seven. The amended SD Lease provides for a straight-line annual rent of approximately $373,000, representing an

estimated yield of over 18.5% with the tenant responsible for all operating expenses. As part of the transaction, the Trust

agreed to fund the construction of an additional 9,900 square feet of processing space and renovate an existing 2,738 square

foot building for approximately $1.56 million. Accordingly, the Trust’s total investment in the 505 Property will be

approximately $1.96 million.

On

September 18, 2020, PW CO CanRE Tam 7, LLC (“Tam 7”), one of our indirect subsidiaries, acquired a 4.32-acre property

in Crowley County, Colorado for $150,000 (the “Tam 7 Property”). As part of the transaction, Tam 7 agreed to fund

the immediate construction of 18,000 square feet of greenhouse and processing space on the Tam 7 Property for approximately $1.22

million. Accordingly, the Trust’s total capital commitment will be $1,364,585. Concurrent with the closing, Tam 7 entered

into a triple-net lease (the “Tam 7 Lease”) with its current tenant (the “Tam 7 Tenant”) who responsible

for paying all expenses related to the Tam 7 Property including maintenance expenses, insurances and taxes. The term of the Tam

7 Lease is 20 years and provides two options to extend for additional five-year periods. The Tam 7 Lease also has financial guarantees

from affiliates of the Tam 7 Tenant. The Tam 7 Tenant intends to operate as a licensed cannabis cultivation and processing facility.

The rent for the Tam 7 Lease is structured whereby after a six-month deferred-rent period, the rental payments provide Tam 7 a

full return of invested capital over the next three years in equal monthly payments. Thereafter, rent is structured to

provide a 12.9% return based on invested capital with annual rent increases of 3% rate per annum. At any time after year six,

if cannabis is legalized at the federal level in the United States, the rent will be adjusted down to an amount equal to a 9%

return on the original invested capital amount and will increase at a 3% rate per annum based on a starting date of the start

of year seven. The Tam 7 Lease requires the Tam 7 Tenant to maintain a medical cannabis license and operate in accordance with

all Colorado and local regulations with respect to its operations and prohibits the retail sale of cannabis and cannabis-infused

products from the property. The additional straight-line annual rent of approximately $262,000 represents an estimated yield of

over 18.5% on invested capital. The project is currently under construction and should be completed by May 2021.

18

On

October 2, 2020, PW CO CanRE MF, LLC (“PW MF”), one of our indirect subsidiaries, acquired two properties in Crowley

County, Colorado approved for cannabis cultivation for $150,000 (the “PW MF Properties”). One parcel is 2.37 acres,

and the other parcel is 2.09 acres. As part of the transaction, the PW MF agreed to fund the immediate construction of 33,744

square feet of greenhouse and processing space on the PW MF Properties for $2,912,300. Accordingly, the Trust’s total capital

commitment will be approximately $3,062,000. On October 15, 2020, PW MF entered into a triple-net lease (the “PSP Lease”)

with PSP Management LLC (“PSP”) who is responsible for paying all expenses related to the PW MF Properties including

maintenance expenses, insurances and taxes. The term of the lease is 20 years and provides two options to extend for additional

twenty-year periods. The PSP Lease also has financial guarantees from affiliates of PSP. PSP intends to operate as a licensed

cannabis cultivation and processing facility. The rent for the PSP Lease is structured whereby after deferred-rent period, the

rental payments provide PW MF a full return of invested capital over the next three years in equal monthly payments. Thereafter,