UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended August 31, 2016 or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________to ___________

000-55513

Commission file number

BOOKEDBYUS INC. |

(Exact name of registrant as specified in its charter) |

Nevada |

| 26-1679929 |

State or other jurisdiction of incorporation or organization |

| (I.R.S. Employer Identification No.) |

|

|

|

c/o Fred Person 619 S. Ridgeley Drive, Los Angeles, CA |

| 90036 |

(Address of principal executive offices) |

| (Zip Code) |

(323) 634-1000

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). o Yes x No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ¨ | Non-accelerated filer | ¨ |

Accelerated filer | ¨ | Smaller reporting company | x |

(Do not check if a smaller reporting company) |

|

| |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). x Yes o No

At February 28, 2016, the last business day of the Registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting common stock held by non-affiliates of the Registrant (without admitting that any person whose shares are not included in such calculation is an affiliate) was approximately $400,000.

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. o Yes o No

(APPLICABLE ONLY TO CORPORATE REGISTRANTS)

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. As of December 2, 2016, 22,170,000 common shares are Issued and Outstanding

PART I

Item 1. Business.

Bookedbyus Inc. is a development stage company, which was formed on December 27, 2007. We have commenced only limited operations, primarily focused on organizational matters in connection with this offering. The Company has not yet implemented its business model and for the fiscal year ended August 31, 2016, has generated $Nil in revenues and has incurred losses of $93,867.

On 1 January 2011, the Company entered into an agreement (the “License Agreement”) with Digital Programa Inc. The Company has licensed the Digital Programa System which is digital media management software which emphasizes a touch-optimized web framework for smart phones and tablets. The basic terms of the License Agreement are as follows:

1) Digital Programa Inc. has granted exclusive license to the Company to market and sell certain software systems, as defined in the License Agreement, which consists of eDrive and iDrive (the “System”), exclusively in Canada and the United States;

2) The Company issued 1,000,000 common shares of the Company, valued at $0.005 per share, to Digitial Programa Inc. for initial, non-recurring, non-refundable license fee (Notes 6 and 8);

3) The Company is required to pay Digial Programa Inc. a 5% royalty on gross revenues for each month from the sales of the System software; and

4) The License Agreement shall remain in effect for a period of 10 years, commencing on 1 January 2011, and the Company has the option to renew the License Agreement for an additional 10 year term provided that the Company pay then current renewal fee, which shall be no greater than 10% of the then current license fee charged by Digital Programa Inc. for new licensees.

Digital Programa Inc. (“DP”) is a privately owned and controlled corporation located at Plaza 2000 Building, P.O. Box 0815-01117, 50th Street Panama, Republic of Panama. DP develops digital media management and workflow automation system software for the entertainment business. DP has developed an online digital collaboration management system that corporations who create and distribute rich media (photo, audio and video as well as other digital assets like documents), find, organize, securely share, distribute, store and view such rich media. The DP software solution is a group of web services that permits enterprises to upload, download, search, collaborate, notify, track usage and authenticate users to perform authorized transactions with digital media, all of which are easily logged and reported.

We intend to market two software applications developed by DP: “eDrive” and “iDrive”. eDrive is a web and email based rich media application that allows clients to push rich media marketing material to its customers with a fully integrated back end including business analytics. eDrive, allows companies to market their message or product directly to their customers.

The Company has not yet implemented its business model. We must raise cash to implement our strategy and stay in business. In the event we do not raise any proceeds from this offering, the Company’s existing cash will not be sufficient to fund the expenses related to this offering, to maintaining a reporting status and to implement its planned business. Over the next twelve months, we plan to introduce iDrive and eDrive.

The Company has impaired the license agreement with Digital Programma, due to the lack of visibility of the Company's ability to generate any future economic benefit from the use of license as well as lack of capital funds and timelines. This resulted in an impairment loss of $3,167 during the year ended August 31, 2014.

Product Overview

The Digital Programa System is digital media management software which emphasizes a touch-optimized web framework for smart phones and tablets. It allows users to design a single highly branded and customized web application that will work on most popular smart phone and tablet platforms. It uses a unified user interface system (“UI”) across mobile device platforms, including iOS, Symbian, Android, Windows mobile, Blackberry and Nokia. It’s built on a dependable user interface frame with efficient code that is flexible, updateable, and easily branded. The software provides touch friendly web pages that plays on most available web browsers while adding rich client functionality.

| 2 |

iDrive

iDrive is a pre-built application for mobile phones and tablets that pushes rich media information (Video, Text, Photos, Audio) to end users. Clients purchase the base application, add their colors and branding logo to make the app uniquely their own. Each client can add more functions as they see fit to service their end users/customers. These iDrive applications are built once but re-branded for each client’s individual use. A base application that pushes rich media information can be licensed for as little as $10,000 compared to custom built applications that can cost as much as $50,000. Because each client adds their colors and logo to the iDrive application, it becomes their unique corporate application that can be provided to end users/customers through Apples iTunes or the client’s own website. With these applications, clients can push daily information alerts, videos, coupons, etc to their end users/customers hand held device simply and easily.

eDrive

eDrive is a web and email based rich media application that allows clients to push rich media marketing material to its end users/customers with a fully integrated back end including business analytics. eDrive, allows companies to market their message or product directly to their customers. eDrive places the power in the client’s hands to easily produce rich media messaging including video, photos and text in a graphic interactive interface. Our clients log into their eDrive account where they assemble rich media emails. They choose the look and feel of the email add their client email list and press send. Through eDrive clients can easily record a video message informing customers of a great deal or simple information regarding the state of the market. Clients can package this up and send it off to their end user/customers. These end users/customers receive on their iDrive application a graphical email message that is completely branded. Any area they click on be it the video, text photos or if they forward the email to a friend, eDrives backend analytics accumulates this information and presents it to the client.

Benefits

Unlike custom built applications that can cost as much as $50,000, clients can license a completely branded iDrive application for smart phones, together with eDrive for as little as $10,000. This enables prospective clients to readily market their products and services to their end users/customers on a branded smart phone application without the development time and expense of custom applications. In addition, iDrive and eDrive provide full business analytics so that clients can measure responses to active marketing campaigns.

Market Opportunity

While the market for Rich Media Marketing Software (“RMMS”) is still in its infancy stage, management believes the market will rapidly develop over the next 18 months. This is primarily due to changes in technology that greatly affect advertisement, such as the release of Apples iPad and the growing number smart phones entering the market. It is our opinion that the need for push technology (software that pushes select information to the recipient) over the web/through email or through mobile device applications is rapidly growing. Large enterprises, financial services companies and entertainment/gaming companies who are currently using the web to market their business can utilize our planned software to deliver data to their customer’s smart phone at prescribed intervals or based on some event that occurs rather than the customer performing a search or requesting an existing report, video or other data type. By sending information directly to the customer, the customer needs are better served and there is less risk of the customer browsing the web and seeing what a competitor is doing or offering.

Bookedbyus plans to engage value added resellers (VARs) who have and can leverage their existing supplier-customer relationships within the Financial Services industry and VARS that have existing relationships with companies in Entertainment /Gamming and large enterprises who are currently using the web to market their business (i.e. Insurance, Real Estate, and Personal products).

By affiliating with these companies through a VAR (Value Added Reseller) model, Bookedbyus intends to extend our planned RMMS products and marketing solutions to wireless users through Smartphone applications and push technology. Bookedbyus plans to work thereafter with customers, encompassing all aspects of managing and using the eDrive and iDrive platforms including value added services such as installation, training, local presence and ongoing support.

eDrive application

eDrive is web based software that deals with the day-to-day operations of email and web marketing. eDrive places the power in the client’s hands to easily produce a rich media messaging that can include video, photos and text in a graphic interactive interface.

iDrive application

iDrive is a white wrapper or generic smart phone application. A client can choose one of our planned pre-built applications and then add their own branding logo; it becomes their unique corporate application that can be provided to customers either through Apples iTunes or from there own website. With the applications our clients can push daily information alerts, videos, coupons, etc to their customers simply and easily directly to their customers hand held device.

| 3 |

Installation services: Under the Bookedbyus business model, we plan to provide installation services to our clients.

Training: We plan to develop training programs for our clients in conjunction with both eDrive and our planned pre-built iDrive applications. Our planned training programs will be designed so that participating clients get highest utilization and therefore most value from our planned software products.

Ongoing Support: In conjunction with Digital Programa Inc., we plan to provide follow up training, telephone and email support as required.

Local Presence: We are committed to demonstrating a strong commitment to quality customer service, and thus we expect to be able to secure long-term relationships with our customers, which will result in a high customer retention rate and long-term customer loyalty.

Industry Overview

The Bookedbyus business model relies heavily upon the state of the online video advertising market and mobile wireless industry since our planned products and services will be designed to ease the administrative burden of the delivery of information over these platforms.

Advertisers and marketers, struggling to keep up with changing consumer habits, are making massive investments in new digital media platforms, especially the mobile platform, according to research firm PQ Media. Companies are shifting dollars away from traditional media, including broadcast TV, newspapers and magazines.

Wireless Advertising

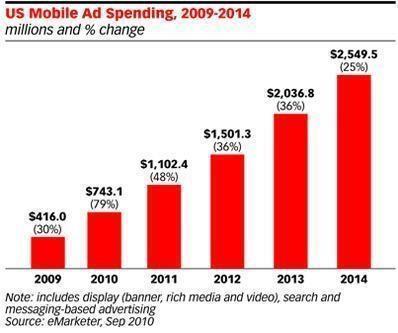

As early as October of 2010, organizations like AdAge.com forecast that mobile spending will cross the $1 billion mark in 2011 with sustained growth and within mobile spending, video is the fastest growing ad medium, albeit from a tiny base, and will continue to be through 2014.

Source: http://adage.com/digital/article?article_id=146553 1

____________

1 Management has reviewed reports from existing and other sources after the dates of these sources and we are of the opinion that the conclusions do not vary materially from these cited reports.

| 4 |

Competition

There are many providers of rich media marketing software. The market for rich media marketing software is still in its infancy stage it is ripe to develop in the next 18 months due to changes in technology that greatly affect advertisement, such as the release of Apples iPad, and the growing number smart phones entering the market. The need for push technology over the web /through email or through mobile device applications is rapidly growing.

Competition in the markets is likely to remain intense but is expected to increasingly center on integrated rather than stand-alone applications. Software providers are continuously looking for third party resellers to add value to their products and increase their market share.

As a provider of wireless solutions, Bookedbyus has assessed its potential competitors based primarily on their functionality of wireless product, the security and scalability of their architecture, and industry focus. Due to our strong emphasis in the application software sector we have also compared ourselves to software providers focused solely in the software design sector.

FOCUSED PROVIDERS: These are companies that have built a wireless set of tools that attempt to address the needs of a specific vertical market. Currently most of the competition in this sector derive their revenue from infra-structure and ongoing professional services and build to a specific device type (i.e.Blackberry, Palm, and Pocket/PC). For these companies to adapt their offering to next generation devices would mean re-architecting the way they conduct business and losing the infra-structure and professional services components of their business. They have, to date, focused on financial institutions or carriers for penetration. These include Aligo, Infowave, Aether, 724, and iAnywhere. Our difference should come from our ability to support over 1,000 device types allowing us to go after the consumer application also.

Application SPECIFIC PROVIDERS: There are a number of SMS and mobile phone download application providers in today's market, including Cellectivity, Mfuse, and Airborne Entertainment. These companies sell their applications and content and therefore are competing with the existing software providers.

Our difference should be that we never produce content. Whether it is an eDrive or iDrive solution we provide the frame work application. We focus exclusively on delivering content on behalf of our clients or partners. Therefore we should never compete against the companies that have an established client base in the Internet market. They become our partners and introduce us to that client base.

SYSTEMS INTEGRATORS: Custom solutions should still consume some of the wireless market share as large organizations continually try to build ground-up solutions for each client, under the assumption that wireless is easy and can be built without the aid of tools and wireless platforms. These companies include IBM, EDS, Accenture, Bearing Point, and BEA Systems. However, these companies may also be potential clients and Value Added Resellers of Bookedbyus suite of products.

With any growing and expanding market, Bookedbyus also expects new competitors to emerge. The wireless market is not expected to be any different, particularly with the prevalence of open standards. Although various competitors have emerged, the mobile application market is still in its infancy. There are no dominant players that address our target market with these types of capabilities.

Item 1A. Risk Factors.

As a “smaller reporting company,” as defined in Rule 12b-2 of the Exchange Act, we are not required to provide the information called for by this Item.

Item 1B. Unresolved Staff Comments.

None

Item 2. Properties.

We do not own any real estate or other properties and have not entered into any long term lease or rental agreements for property.

Item 3. Legal Proceedings.

There are no pending legal proceedings to which the Company is a party or in which any director, officer or affiliate of the Company, any owner of record or beneficially of more than 5% of any class of voting securities of the Company, or stockholder is a party adverse to the Company or has a material interest adverse to the Company.

Item 4. (Removed and Reserved)

| 5 |

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Although our common stock is not listed on a public exchange, we intend to apply for quotation on the Over-the-Counter Bulletin Board (OTCBB). In order to be quoted on the OTCBB, a market maker must file an application on our behalf in order to make a market for our common stock. There can be no assurance that a market maker will agree to file the necessary documents with FINRA, who, generally speaking, must approve the first quotation of a security by a market maker on the OTCBB, nor can there be any assurance that such an application for quotation will be approved.

Item 6. Selected Financial Data

As a “smaller reporting company,” as defined in Rule 12b-2 of the Exchange Act, we are not required to provide the information called for by this Item.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Management’s Discussion and Analysis

This section of the Registration Statement includes a number of forward-looking statements that reflect our current views with respect to future events and financial performance. Forward-looking statements are often identified by words like believe, expect, estimate, anticipate, intend, project and similar expressions, or words which, by their nature, refer to future events. You should not place undue certainty on these forward-looking statements. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our predictions.

Capital Resources and Liquidity

Our auditors have issued a “going concern” opinion, meaning that there is substantial doubt if we can continue as an on-going business unless we obtain additional capital. No substantial revenues from our planned business model are anticipated until we have completed financing the Company.

We need to seek capital from resources such as private placements in the Company’s common stock or debt financing, which may not even be available to the Company. However, if such financing were available, because we are a development stage company with no or limited operations to date, it would likely have to pay additional costs associated with such financing and in the case of high risk loans be subject to an above market interest rate. At such time these funds are required, management would evaluate the terms of such financing. If the company cannot raise additional proceeds via such financing, it would be required to cease business operations.

As of August 31, 2016, we had $980 in cash as compared to $515 as at August 31, 2015. As of the date of this Form 10-K, the current funds available to the Company will not be sufficient to fund the expenses related to maintaining a reporting status. We are in the process of seeking additional equity financing in the form of private placements to fund our operations over the next 12 months.

Management believes that if subsequent private placements are successful, we will generate sales revenue within twelve months thereof. However, additional equity financing may not be available to us on acceptable terms or at all, and thus we could fail to satisfy our future cash requirements.

We do not anticipate researching any further products nor the purchase or sale of any significant equipment. We also do not expect any significant additions to the number of employees.

Results of Operations

At August 31, 2016, the Company was not engaged in continued business and has been primarily involved in development stage activities to date. There is minimal historical operational information about us on which to base an evaluation of our performance. We have been in existence since December 27, 2007, and entered into a licensing agreement with Digital Programma, Inc. on January 1, 2011. We are a development stage company with minimal operations and have generated $Nil in revenue for the year ended August 31, 2016. Due to a lack of funding, we have not implemented our Plan of Operations. We cannot guarantee we will be successful in our business operations. Our business is subject to risks inherent in the establishment of a new business enterprise, including limited capital resources, and possible delays in our planned product development.

| 6 |

We had $Nil in revenue for the fiscal year ended August 31, 2016 as compared to revenue for the fiscal year ended August 31, 2015 of $Nil.

Total expenses in the fiscal year ended August 31, 2016 were $93,867 as compared to total expenses for the fiscal year ended August 31, 2015 of $68,494 resulting in a net loss for the fiscal year ended August 31, 2016 of $93,867 as compared to a net loss of $68,494 for the fiscal year ended August 31, 2015. The net loss for the fiscal year ended August 31, 2016 is a result of Professional fees of $12,961 comprised primarily of legal and accounting expense, General and administrative expense of $7,306, Management fees of $36,800, and Rent of $36,800 as compared to the net loss for the fiscal year ended August 31, 2015 of $68,494 which was a result of Professional fees of $14,500 comprised primarily of legal and accounting expense, General and administrative expense of $5,994, Management fees of $24,000 and Rent of $24,000.

Off-balance sheet arrangements

The Company has no off-balance sheet arrangements that have or are reasonably likely to have a current or future effect or change on the company’s financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources that are material to investors. The term “off-balance sheet arrangement” generally means any transaction, agreement or other contractual arrangement to which an entity unconsolidated with the company is a party, under which the company has (i) any obligation arising under a guarantee contract, derivative instrument or variable interest; or (ii) a retained or contingent interest in assets transferred to such entity or similar arrangement that serves as credit, liquidity or market risk support for such assets.

Plan of Operations

Over the 12 month period, our company must raise capital to introduce its planned products and start its sales. We have a need to seek capital from other resources such as private placements in the Company’s common stock or debt financing, which may not even be available to the Company. However, if such financing were available, because we are a development stage company with no or limited operations to date, it would likely have to pay additional costs associated with such financing and in the case of high risk loans be subject to an above market interest rate. At such time these funds are required, management would evaluate the terms of such financing. If the company cannot raise additional proceeds via such financing, it would be required to cease business operations.

Over the next twelve months, we intend to introduce two initial products: 1) eDrive, a web and email based rich media application that allows clients to push rich media marketing material to its customers with a fully integrated back end including business analytics and 2) iDrive, a software development tool that builds iPhone, iPad and smart phone applications designed to access and view rich media managed by eDrive. These applications, once developed, can easily be branded by the client using the client’s logo and color scheme.

The first phase of our planned operations over this period would be to develop and beta test our eDrive software solution. Upon completion of our Beta testing we intend to enter into a licensing agreement with a major film studio and a financial institution. Simultaneously we will develop our product website that will include a training component for clients.

The Company will retain consultants to develop its brand including packaging for its products, website and outsource programming for development of its eDrive software for its planned initial products. We have budgeted $170,000 to develop eDrive software. Software development expense will include Beta testing eDrive, expanding the database to accept additional data types and enhancing “push technology to include imbedded graphical designs, The Company feels that within 150 days of the date of this offering it plans to launch its product package design, initial website development, logo development, beta testing of the eDrive product and it is our hope to enter into a licensing agreement with a major studio and a financial institute.

The Company has budgeted 149,550 for Sales and Marketing expense which includes $10,000 for logo development, $30,000 for brochure and print publication, $35,050 for advertising and $54,000 for sales commissions. In addition, the Company has budgeted website development cost of $20,000, website hosting cost of $500. We do not anticipate further expenses for website development.

The company intends to primarily target four markets: Entertainment/Gamming; Financial Services; and large Enterprises who are currently using the web to market their business (i.e. Insurance, Real Estate, and Personal products).

During the second phase of planned operations, we intend to introduce iDrive a white label smart phone application. We have budgeted $293,750 for software development and programming of iDrive which will include updating the iDrive support for iOS6, OSX11, and newer version of operating systems like Blackberry, Windows and Android, adding security enhancements like 3D facial recognition and providing secure payment applications supporting Apples IOS6 Passport. In addition, the Company plans to provide customer driven feature enhancements to its software at a planned expense of $171,250. The Company plans to implement the second stage of its marketing strategy through additional online advertising with an estimated cost of an additional $20,000 (total online advertising costs for the first phase and the second phase is estimated to cost $35,050). BBU will target Value Added Resellers that have relationships in the target end user companies. By affiliating with these companies through a VAR (Value Added Reseller) model, Bookedbyus intends to extend their finance solutions and marketing to the wireless users through Smartphone applications and push technology. In essence we should leverage the existing supplier-customer relationships within the industry in a non-threatening way.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

As a “smaller reporting company,” as defined in Rule 12b-2 of the Exchange Act, we are not required to provide the information called for by this Item.

| 7 |

Item 8. Financial Statements and Supplementary Data.

Bookedbyus Inc.

Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

| F-1 |

Report of Independent Registered Public Accounting Firm

Board of Directors and Stockholders

Bookedbyus, Inc.

Los Angeles, California

We have audited the accompanying balance sheets of Bookedbyus, Inc. (the "Company") as of August 31, 2016 and 2015 and the related statements of operations, stockholders' deficit and cash flows for each of the years ended August 31, 2016 and 2015. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform an audit to obtain reasonable assurance about whether the financial statements are free of material misstatements. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company's internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall consolidated financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Bookedbyus, Inc. as of August 31, 2016 and 2015 and the result of its operations and its cash flows for each of the years ended August 31, 2016 and 2015, in conformity with accounting principles generally accepted in the United States of America.

The accompanying financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the financial statements, the Company incurred net losses and has a working capital deficit, which raises substantial doubt about the Company's ability to continue as a going concern. Management's plans in regard to these matters are also described in Note 1. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ MaloneBailey, LLP

www.malonebailey.com

Houston, Texas

December 2, 2016

| F-2 |

Bookedbyus Inc.

Balance Sheets

(Expressed in U.S. Dollars)

|

| August 31, 2016 |

|

| August 31, 2015 |

| ||

|

|

|

|

|

|

| ||

Assets |

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

Current assets |

|

|

|

|

|

| ||

Cash and cash equivalents |

| $ | 980 |

|

| $ | 515 |

|

Total current assets |

|

| 980 |

|

|

| 515 |

|

|

|

|

|

|

|

|

|

|

Total Assets |

| $ | 980 |

|

| $ | 515 |

|

|

|

|

|

|

|

|

|

|

Liabilities and Stockholders’ Deficit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current liabilities |

|

|

|

|

|

|

|

|

Accounts payable and accrued liabilities |

| $ | 3,391 |

|

| $ | 3,132 |

|

Accounts payable due to related parties (Note 3) |

|

| 153,874 |

|

|

| 80,274 |

|

Due to related parties (Note 3) |

|

| 57,373 |

|

|

| 36,900 |

|

Total current liabilities |

|

| 214,638 |

|

|

| 120,306 |

|

|

|

|

|

|

|

|

|

|

Total Liabilities |

|

| 214,638 |

|

|

| 120,306 |

|

|

|

|

|

|

|

|

|

|

Stockholders’ deficit |

|

|

|

|

|

|

|

|

Capital stock (Note 4) |

|

|

|

|

|

|

|

|

Authorized 75,000,000 of common shares, par value $0.001 |

|

|

|

|

|

|

|

|

Issued and outstanding 22,170,000 common shares issued and outstanding as of August 31, 2016 and 2015, par value $0.001 |

|

| 22,170 |

|

|

| 22,170 |

|

Additional paid in capital |

|

| 86,180 |

|

|

| 86,180 |

|

Accumulated deficit |

|

| (322,008 | ) |

|

| (228,141 | ) |

|

|

|

|

|

|

|

|

|

Total stockholders’ deficit |

|

| (213,658 | ) |

|

| (119,791 | ) |

|

|

|

|

|

|

|

|

|

Total Liabilities and Stockholders’ Deficit |

| $ | 980 |

|

| $ | 515 |

|

The accompanying notes are an integral part of these financial statements.

| F-3 |

Bookedbyus Inc.

Statements of Operations

(Expressed in U.S. Dollars)

|

| For the year ended |

|

| For the year ended |

| ||

|

|

|

|

|

|

| ||

Revenue |

| $ | - |

|

| $ | - |

|

|

|

|

|

|

|

|

|

|

Expenses |

|

|

|

|

|

|

|

|

Professional fees |

|

| 12,961 |

|

|

| 14,500 |

|

General and administrative |

|

| 7,306 |

|

|

| 5,994 |

|

Management fees (Note 3) |

|

| 36,800 |

|

|

| 24,000 |

|

Rent (Note 3) |

|

| 36,800 |

|

|

| 24,000 |

|

|

|

|

|

|

|

|

|

|

Total expenses |

|

| 93,867 |

|

|

| 68,494 |

|

|

|

|

|

|

|

|

|

|

Net loss |

| $ | (93,867 | ) |

| $ | (68,494 | ) |

|

|

|

|

|

|

|

|

|

Basic and diluted loss per common share |

| $ | (0.00 | ) |

| $ | (0.00 | ) |

|

|

|

|

|

|

|

|

|

Weighted average number of common shares – basic and diluted |

|

| 22,170,000 |

|

|

| 22,170,000 |

|

The accompanying notes are an integral part of these financial statements.

| F-4 |

Bookedbyus Inc.

Statements of Stockholders’ Deficit

(Expressed in U.S. Dollars)

|

| Number of |

|

| Capital |

|

| Additional |

|

| Accumulated |

|

| Stockholders’ deficit |

| |||||

|

|

|

|

| $ |

|

| $ |

|

| $ |

|

| $ |

| |||||

Balance at August 31, 2014 |

|

| 22,170,000 |

|

|

| 22,170 |

|

|

| 86,180 |

|

|

| (159,647 | ) |

|

| (51,297 | ) |

Net loss for the year |

|

| - |

|

|

| - |

|

|

| - |

|

|

| (68,494 | ) |

|

| (68,494 | ) |

Balance at August 31, 2015 |

|

| 22,170,000 |

|

|

| 22,170 |

|

|

| 86,180 |

|

|

| (228,141 | ) |

|

| (119,791 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance at August 31, 2015 |

|

| 22,170,000 |

|

|

| 22,170 |

|

|

| 86,180 |

|

|

| (228,141 | ) |

|

| (119,791 | ) |

Net loss for the year |

|

| - |

|

|

| - |

|

|

| - |

|

|

| (93,867 | ) |

|

| (93,867 | ) |

Balance at August 31, 2016 |

|

| 22,170,000 |

|

|

| 22,170 |

|

|

| 86,180 |

|

|

| (322,008 | ) |

|

| (213,658 | ) |

The accompanying notes are an integral part of these financial statements.

| F-5 |

Bookedbyus Inc.

Statements of Cash Flows

(Expressed in U.S. Dollars)

|

| For the year ended |

|

| For the year ended |

| ||

|

|

|

|

|

|

| ||

Cash flows from operating activities |

|

|

|

|

|

| ||

Net loss |

| $ | (93,867 | ) |

| $ | (68,494 | ) |

Changes in operating assets and liabilities |

|

|

|

|

|

|

|

|

Increase in accounts payable and accrued liabilities |

|

| 259 |

|

|

| 978 |

|

Increase in accounts payable due to related parties |

|

| 73,600 |

|

|

| 48,000 |

|

|

|

|

|

|

|

|

|

|

Cash flows used in operating activities |

|

| (20,008 | ) |

|

| (19,516 | ) |

|

|

|

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

|

|

|

|

Advances from related parties |

|

| 20,473 |

|

|

| 19,700 |

|

|

|

|

|

|

|

|

|

|

Cash provided by financing activities |

|

| 20,473 |

|

|

| 19,700 |

|

|

|

|

|

|

|

|

|

|

Net increase in cash |

|

| 465 |

|

|

| 184 |

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents, beginning of year |

|

| 515 |

|

|

| 331 |

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents, end of year |

| $ | 980 |

|

| $ | 515 |

|

|

|

|

|

|

|

|

|

|

Supplemental disclosures of cash flow information |

|

|

|

|

|

|

|

|

Cash paid for interest |

| $ | - |

|

| $ | - |

|

Cash paid for income taxes |

|

| - |

|

|

| - |

|

The accompanying notes are an integral part of these financial statements.

| F-6 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

1. Nature and Continuance of Operations

Bookedbyus Inc. (the “Company”) was incorporated under the laws of the State of Nevada on December 27, 2007. The Company will carry on the business of computer software sales and marketing when all financing is in place.

In the opinion of the management, all normal recurring adjustments which are necessary for a fair presentation of financial statements of the results for the year ended August 31, 2016, have been included.

On January 9, 2008, the Company affected a thousand (1,000) for one (1) forward stock split of all outstanding common shares and a corresponding forward increase in the Company’s authorized common stock. The effect of the forward split was to increase the number of the Company’s authorized common shares from 75,000 shares par value $0.001 to 75,000,000 shares par value $0.001. At the time of the stock split, the Company had no commons shares issued and outstanding. All references in these financial statements to number of common shares, price per share and weighted average number of common shares have been adjusted to reflect the stock split on a retroactive basis, unless otherwise noted. (Note 4).

The Company’s financial statements as at August 31, 2016 and for the year then ended have been prepared on a going concern basis, which contemplates the realization of assets and the settlement of liabilities and commitments in the normal course of business. The Company has a loss of $93,867 for the year ended August 31, 2016 and $68,494 for the year ended August 31, 2015 and has a working capital deficit of $213,658 at August 31, 2016 (2015 - $119,791). These factors raise substantial doubt about the ability of the Company to continue as a going concern.

Management cannot provide assurance that the Company will ultimately achieve profitable operations or become cash flow positive, or raise additional debt and/or equity capital. Management believes that the Company’s capital resources should be adequate to continue operating and maintaining its business strategy during the fiscal year ended August 31, 2016. However, if the Company is unable to raise additional capital in the near future, due to the Company’s liquidity problems, management expects that the Company will need to curtail operations, liquidate assets, seek additional capital on less favorable terms and/or pursue other remedial measures. These financial statements do not include any adjustments related to the recoverability and classification of assets or the amounts and classification of liabilities that might be necessary should the Company be unable to continue as a going concern.

As at August 31, 2016, the Company was not engaged in continued business, and had significant expenses from development stage activities. Although management is currently attempting to implement its business plan and is seeking additional sources of financing, there is no assurance the activity will be successful. Accordingly, the Company must rely on its president to perform essential functions without compensation until a business operation can be commenced. The financial statements do not include any adjustments that may result from the outcome of this uncertainty.

| F-7 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

2. Significant Accounting Policies

The following is a summary of significant accounting policies used in the preparation of these financial statements.

Definition of fiscal year

The Company’s fiscal year end is August 31st.

Basis of presentation

The financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”).

Cash and cash equivalents

Cash and cash equivalents include highly liquid investments with original maturities of three months or less.

Financial instruments

Accounting Standards Codification (“ASC”) 820, “Fair Value Measurements and Disclosures”, requires disclosing fair value to the extent practicable for financial instruments that are recognized or unrecognized in the balance sheet. Fair value of financial instruments is the amount at which the instruments could be exchanged in a current transaction between willing parties. The Company considers the carrying amounts of cash, restricted cash, accounts receivable, related party and other receivables, accounts payable, notes payable, related party and other payables, customer deposits, and short term loans approximate their fair values because of the short period of time between the origination of such instruments and their expected realization. The Company considers the carrying amount of long term bank loans to approximate their fair values based on the interest rates of the instruments and the current market rate of interest.

Level 1 The preferred inputs to valuation efforts are “quoted prices in active markets for identical assets or liabilities,” with the caveat that the reporting entity must have access to that market. Information at this level is based on direct observations of transactions involving the same assets and liabilities, not assumptions, and thus offers superior reliability. However, relatively few items, especially physical assets, actually trade in active markets.

Level 2 FASB acknowledged that active markets for identical assets and liabilities are relatively uncommon and, even when they do exist, they may be too thin to provide reliable information. To deal with this shortage of direct data, the board provided a second level of inputs that can be applied in three situations.

| F-8 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

2. Significant Accounting Policies (Continued)

Financial instruments (Continued)

Level 3 If inputs from levels 1 and 2 are not available, FASB acknowledges that fair value measures of many assets and liabilities are less precise. The board describes Level 3 inputs as “unobservable,” and limits their use by saying they “shall be used to measure fair value to the extent that observable inputs are not available.” This category allows “for situations in which there is little, if any, market activity for the asset or liability at the measurement date”. Earlier in the standard, FASB explains that “observable inputs” are gathered from sources other than the reporting company and that they are expected to reflect assumptions made by market participants.

As at August 31, 2016, the fair value of cash and cash equivalents and accounts payable approximates carrying value because of their short maturities.

Credit Risk

Financial instruments that potentially subject the Company to credit risk consist of cash and cash equivalents. The Company deposits cash and cash equivalents with high credit quality financial institutions as determined by rating agencies.

Currency Risk

The Company’s assets and liabilities are in U.S. dollars, which is the Company’s functional and presentation currency. The Company has no transactions in currencies other than U.S. dollar. As a result, foreign currency risk is insignificant.

Interest Rate Risk

The Company has cash balances and no interest-bearing debt. It is management’s opinion that the Company is not exposed to significant interest risk arising from these financial instruments.

Liquidity Risk

Liquidity risk is the risk that an entity will encounter difficulty in meeting obligations associated with its financial liabilities. The Company is reliant upon equity issuances and advances from related parties as its sole source of cash. The Company has been successful in raising equity financing in the past; however, there is no assurance that it will be able to do so in the future.

| F-9 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

2. Significant Accounting Policies (Continued)

Income taxes

Deferred income taxes are reported for timing differences between items of income or expense reported in the financial statements and those reported for income tax purposes in accordance with ASC 740, “Income Taxes”, which requires the use of the asset/liability method of accounting for income taxes. Deferred income taxes and tax benefits are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases, and for tax loss and credit carry-forwards. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The Company provides for deferred taxes for the estimated future tax effects attributable to temporary differences and carry-forwards when realization is more likely than not.

Basic and diluted net loss per share

The Company computes net loss per share in accordance with ASC 260 “Earnings per Share”. ASC 260 requires presentation of both basic and diluted earnings per share (“EPS”) on the face of the income statement. Basic EPS is computed by dividing net loss available to common shareholders (numerator) by the weighted average number of shares outstanding (denominator) during the period. Diluted EPS gives effect to all potentially dilutive common shares outstanding during the period using the treasury stock method and convertible preferred stock using the if-converted method. In computing diluted EPS, the average stock price for the period is used in determining the number of shares assumed to be purchased from the exercise of stock options or warrants. Diluted EPS excludes all potentially dilutive shares if their effect is anti-dilutive.

| F-10 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

2. Significant Accounting Policies (Continued)

Related Parties

Accounts payable due to related party represents an obligation to pay for services that were used in the ordinary course of business. The amount is classified as a current liability as payment is due on demand.”

Comprehensive loss

ASC 220, “Comprehensive Income”, establishes standards for the reporting and display of comprehensive loss and its components in the financial statements. As at August 31, 2016, the Company has no items that represent a comprehensive loss and, therefore, has not included a schedule of comprehensive loss in the financial statements.

Start-up expenses

The Company has adopted ASC 720-15, “Start-Up Costs”, which requires that costs associated with start-up activities be expensed as incurred. Accordingly, start-up costs associated with the Company's formation have been included in the Company's general and administrative expenses for the period from the date of inception on December 27, 2007 to August 31, 2016.

Foreign currency translation

The Company’s functional and reporting currency is in U.S. dollars. The financial statements of the Company are translated to U.S. dollars in accordance with ASC 830, “Foreign Currency Matters”. Monetary assets and liabilities denominated in foreign currencies are translated using the exchange rate prevailing at the balance sheet date. Gains and losses arising on translation or settlement of foreign currency denominated transactions or balances are included in the determination of income. The Company has not, to the date of these financial statements, entered into derivative instruments to offset the impact of foreign currency fluctuations.

Use of estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenditures during the reporting period. Actual results could differ from these estimates.

Stock-based compensation

ASC 718, “Compensation – Stock Compensation”, which establishes accounting for equity instruments exchanged for employee services. Under the provisions of ASC 718, stock-based compensation cost is measured at the grant date, based on the calculated fair value of the award, and is recognized as an expense over the employees’ requisite service period (generally the vesting period of the equity grant). Adoption of ASC 718 does not change the way the Company accounts for share-based payments to non-employees, with guidance provided by ASC 505-50, “Equity-Based Payments to Non-Employees”.

| F-11 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

2. Significant Accounting Policies (Continued)

Recent accounting pronouncements

The Company's management has evaluated all the recently issued accounting pronouncements through the filing date of these financial statements and does not believe that any of these pronouncements will have a material impact on the Company's financial position and results of operations.

3. Due to Related Parties and Related Party Transactions

During the year ended August 31, 2016, the Company accrued management fees in the amount of $36,800 (2015 - $24,000) to a consultant, Brad Kersch, who is under contract. The outstanding balance of management fees payable was $76,800 and $40,274 as of August 31, 2016 and 2015, respectively.

| F-12 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

3. Due to Related Parties and Related Party Transactions (Continued)

During the year ended August 31, 2016, the Company accrued rent expense in the amount of $36,800 (2015 - $24,000) to a company with an officer in common. The outstanding balance of rent payable was $76,800 and $40,000 as of August 31, 2016 and 2015, respectively.

As at August 31, 2016, related parties of the Company have provided a series of loan, totaling $57,373 (2015 - $36,900), for working capital purposes. These amount are unsecured, interest-free and are due on demand.

4. Capital Stock

The total authorized capital is 75,000,000 common shares with a par value of $0.001 per common share.

On January 9, 2008, the Company affected a thousand (1,000) for one (1) forward stock split of all outstanding common shares and a corresponding forward increase in the Company’s authorized common stock. The effect of the forward split was to increase the number of the Company’s authorized common shares from 75,000 shares par value $0.001 to 75,000,000 shares par value $0.001. At the time of the stock split, the Company had no common shares issued and outstanding.

All references in these financial statements to number of common shares, price per share and weighted average number of common shares have been adjusted to reflect the stock split on a retroactive basis, unless otherwise noted.

Issued and outstanding

The Company had 22,170,000 common shares issued and outstanding as at August 31, 2016 and 2015.

5. Income Taxes

The Company accounts for income taxes under FASB Accounting Standard Codification ASC 740 "Income Taxes". ASC 740 requires use of the liability method. ASC 740 provides that deferred tax assets and liabilities are recorded based on the differences between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes, referred to as temporary differences. Deferred tax assets and liabilities at the end of each period are determined using the currently enacted tax rates applied to taxable income in the periods in which the deferred tax assets and liabilities are expected to be settled or realized.

As of August 31, 2016 and 2015, the Company had net operating loss carry forwards of $322,008 and $228,141 that may be available to reduce future years' taxable income. Future tax benefits which may arise as a result of these losses have not been recognized in these financial statements, as their realization is determined not likely to occur and accordingly, the Company has recorded a valuation allowance for the deferred tax asset relating to these tax loss carry-forwards. Net operation losses will begin to expire in 2030.

| F-13 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

5. Income Taxes (Continued)

Components of net deferred tax assets, including a valuation allowance, are as follows at August 31, 2016 and 2015:

|

| 2016 |

|

| 2015 |

| ||

Deferred tax assets: |

|

|

|

|

|

| ||

Net operating loss carry forward |

|

| 112,703 |

|

|

| 79,849 |

|

Less: valuation allowance |

|

| (112,703 | ) |

|

| (79,849 | ) |

Net deferred tax assets |

|

| - |

|

|

| - |

|

The valuation allowance for deferred tax assets as of August 31, 2016 was $112,703, as compared to $79,849 as of August 31, 2015. In assessing the recovery of the deferred tax assets, management considers whether it is more likely than not that some portion or all of the deferred tax assets will not be realized. The ultimate realization of deferred tax assets is dependent upon the generation of future taxable income in the periods in which those temporary differences become deductible. Management considers the scheduled reversals of future deferred tax assets, projected future taxable income, and tax planning strategies in making this assessment. As a result, management determined it was more likely than not the deferred tax assets would not be realized as of August 31, 2016.

The provision for income taxes differs from the amount computed by applying the statutory federal income tax rate to income before provision for income taxes. The sources and tax effects of the differences are as follows:

U.S federal statutory rate (35.0%)

Valuation reserve 35.0%

Total -%

At August 31, 2016, we had an unused net operating loss carryover approximating $322,008 with a full valuation allowance of $112,703 that is available to offset future taxable income which expires beginning 2030.

6. Contracts Under Commitment

The Company has leased an office in Los Angeles California for a period of twelve months commencing January 1, 2014. The office is located at Suite 101, 619 S. Ridgley Los Angeles CA 90036 ($2,000 per month) due on the first calendar day of each month. This twelve month term automatically renews if no written notice of termination is given 30 days prior to the end on each term. The landlord agrees to accept either cash or shares as settlement for each months' rent. The landlord will defer rent in lieu of shares at $0.10 a share as per the Registration Statement or cash. As a concession for this deferment, the landlord will charge an additional 20% per month for each month deferred. (ie. $400 or 4,000 shares at $0.10 per share.)

The California lease agreement was terminated effective Aug 31, 2016.

Both parties agree to the deferment schedule being at the end of the term. All deferred rent subject to the 20% per month will be collectable only at the end of the term.

| F-14 |

Bookedbyus Inc.

Notes to Financial Statements

(Expressed in U.S. Dollars)

For the years ended August 31, 2016 and 2015

6. Contracts Under Commitment (Continued)

The Company has entered into a consulting agreement with Brad Kersch for marketing and business consulting. The term of the agreement is one year beginning January 1, 2014. Consideration for such consulting services is $2,000 per month payable in cash or common shares, at the Company’s election. The Consultant agrees to accept either cash or shares as settlement for each months' pay. The Consultant agrees to defer payments in lieu of shares at $0.10 a share as per the Registration Statement. As a concession for this deferment, the Consultant will charge an additional 20% per month for each month deferred. (ie. $400 or 4,000 shares at $0.10 per share.)

Both parties agree to the deferment schedule to be calculated only at the end of the term. All deferred rent subject to the 20% per month will be calculated and collectable only at the end of the term.

7. Subsequent Events

On November 4, 2016, related parties of the Company provided a loan, totaling $5,000 for working capital purposes. This amount is unsecured, interest-free and due on demand.

| F-15 |

Item 9. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure.

None

Item 9A. Controls and Procedures.

The management of the Company is responsible for establishing and maintaining adequate internal control over financial reporting, as required by Sarbanes-Oxley (SOX) Section 404 A. The Company’s internal control over financial reporting is a process designed under the supervision of the Company’s Chief Executive Officer and Chief Financial Officer to provide reasonable assurance regarding the reliability of financial reporting and the preparation of the Company’s financial statements for external purposes in accordance with U.S. generally accepted accounting principles.

Management assessed the effectiveness of the Company’s internal control over financial reporting based on the criteria for effective internal control over financial reporting established in SEC guidance on conducting such assessments as of the end of the period covered by this report. Management conducted the assessment based on certain criteria established in Internal Control - Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. Based on this assessment, management concluded that our internal control over financial reporting was not effective as of August 31, 2016.

The matters involving internal controls and procedures that the Company’s management considered to be material weaknesses under the standards of the Public Company Accounting Oversight Board were: (1) lack of a functioning audit committee and lack of a majority of outside directors on the Company's board of directors, resulting in ineffective oversight in the establishment and monitoring of required internal controls and procedures; (2) inadequate segregation of duties consistent with control objectives; (3) insufficient written policies and procedures for accounting and financial reporting with respect to the requirements and application of US GAAP and SEC disclosure requirements; and (4) ineffective controls over period end financial disclosure and reporting processes. The aforementioned material weaknesses were identified by the Company's Chief Financial Officer in connection with the audit of our financial statements as of August 31, 2016 and communicated the matters to our management.

Management believes that the material weaknesses set forth in items (2), (3) and (4) above did not have an affect on the Company's financial results. However, management believes that the lack of a functioning audit committee and lack of a majority of outside directors on the Company's board of directors, resulting in ineffective oversight in the establishment and monitoring of required internal controls and procedures can result in the Company's determination to its financial statements for the future years.

We are committed to improving our financial organization. As part of this commitment, we will create a position to segregate duties consistent with control objectives and will increase our personnel resources and technical accounting expertise within the accounting function when funds are available to the Company: i) Appointing one or more outside directors to our board of directors who shall be appointed to the audit committee of the Company resulting in a fully functioning audit committee who will undertake the oversight in the establishment and monitoring of required internal controls and procedures; and ii) Preparing and implementing sufficient written policies and checklists which will set forth procedures for accounting and financial reporting with respect to the requirements and application of US GAAP and SEC disclosure requirements.

Management believes that the appointment of one or more outside directors, who shall be appointed to a fully functioning audit committee, will remedy the lack of a functioning audit committee and a lack of a majority of outside directors on the Company's Board. In addition, management believes that preparing and implementing sufficient written policies and checklists will remedy the following material weaknesses (i) insufficient written policies and procedures for accounting and financial reporting with respect to the requirements and application of US GAAP and SEC disclosure requirements; and (ii) ineffective controls over period end financial close and reporting processes. Further, management believes that the hiring of additional personnel who have the technical expertise and knowledge will result proper segregation of duties and provide more checks and balances within the department. Additional personnel will also provide the cross training needed to support the Company if personnel turn over issues within the department occur. This coupled with the appointment of additional outside directors will greatly decrease any control and procedure issues the company may encounter in the future.

We will continue to monitor and evaluate the effectiveness of our internal controls and procedures and our internal controls over financial reporting on an ongoing basis and are committed to taking further action and implementing additional enhancements or improvements, as necessary and as funds allow.

This annual report does not include an attestation report of the company’s registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by the company’s registered public accounting firm pursuant to temporary rules of the Securities and Exchange Commission that permit the Company to provide only management’s report in this annual report.

There have been no changes in our internal control over financial reporting identified in connection with the evaluation required by paragraph (d) of Rules 13a-15 or 15d-15 under the Exchange Act that occurred during the small business issuer's last fiscal year that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

Item 9B. Other Information.

None

| 8 |

PART III

Item 10. Directors, Executive Officers and Corporate Governance.

Identification of directors and executive officers

Our sole director serves until his successor is elected and qualified. Our officers are elected by the Board of Directors to a term of one (1) year and serves until their successor(s) is duly elected and qualified, or until they are removed from office. The Board of Directors has no nominating or compensation committees.

The name, address, age and position of our present sole officer and director is set forth below:

Name | Age | Position(s) | ||

|

|

|

| |

Fred Person1 | 67 | President, Treasurer, Chief Financial Officer and Chairman of the Board of Directors. | ||

Susan Fox2 | 60 | Secretary |

1 The person named above has held his office since October 22nd, 2009 and is expected to hold his offices/positions at least until the next annual meeting of our stockholders.

2 The person named above has held her office since October 22nd, 2009 and is expected to hold her offices/positions at least until the next annual meeting of our stockholders.

Fred Person

From April 2004 to January 2009, Mr. Person was employed by Wyndham Worldwide Inc. as a Sales Manager for the timeshare division of Wyndham Worldwide Inc. of California. From January 2009 to date Mr. Person is self-employed as an Independent Sales Contractor in the travel industry.

Susan Fox

Ms. Fox was formerly the vice president of sales and marketing for Keystone Entertainment and First Pacific Pictures. Ms. Fox is currently president of Casting Workbook Inc. in Los Angeles, California and Casting Workbook Services Inc., Vancouver, British Columbia. From 2004 to date Ms. Fox has served as President of Casting Workbook Inc. and Casting Workbook Services Inc. In addition, Ms. Fox has been an independent contractor to the entertainment industry and worked as a professional actor, dancer, singer, and model.

Our sole director and officers do not hold positions on the board of directors of any other U.S. reporting companies and has no affiliation with any company that has filed for bankruptcy within the last five years. The Company is not aware of any proceedings to which any of the Company’s officers or directors, or any associate of any such officer or director, is a party adverse to the Company or any of the Company’s subsidiaries or has a material interest adverse to it or any of its subsidiaries.

The Company believes that Mr. Person’s and Ms. Fox’s business experience and their entrepreneurial success make them well suited to serve as our officers and director.

Significant Employees

The Company does not, at present, have any employees other than the current officer and director. We have not entered into any employment agreements, as we currently do not have any employees other than the current officer and director.

| 9 |

Family Relations

There are no family relationships among the Directors and Officers of Bookedbyus Inc.

Involvement in Legal Proceedings

No executive Officer or Director of the Company has been convicted in any criminal proceeding (excluding traffic violations) or is the subject of a criminal proceeding that is currently pending. No executive Officer or Director of the Company is the subject of any pending legal proceedings.

No Executive Officer or Director of the Company is involved in any bankruptcy petition by or against any business in which they are a general partner or executive officer at this time or within two years of any involvement as a general partner, executive officer, or Director of any business.

Item 11. Executive Compensation.

The table below summarizes all compensation awarded to, earned by, or paid to our named executive officers and director for all services rendered in all capacities to us for the period from inception through August 31, 2016.

There has been no compensation to neither Fred Person – President nor Susan Fox - Secretary for the years 2015 and 2016.

During the stages of formation and development, the Company agreed to pay management fees to its executive officers. The Company arbitrarily determined $1,000 per month was reasonable. No written agreement exists. We did not agree to pay nor did we accrue any salaries in 2011, 2012, 2013, 2014, 2015 and 2016. We do not anticipate beginning to pay salaries until we have adequate funds to do so. There are no other stock option plans, retirement, pension, or profit sharing plans for the benefit of our officer and director other than as described herein.

Both Fred Person – President & Susan Fox - Secretary a have agreed to no compensation for the period.

Outstanding Equity Awards at Fiscal Year-End

The table below summarizes all unexercised options, stock that has not vested, and equity incentive plan awards for each named executive officer as of August 31, 2016.

OUTSTANDING EQUITY AWARDS AT FISCAL YEAR-END | ||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||

OPTION AWARDS |

|

| STOCK AWARDS |

| ||||||||||||||||||||||||||||||||

Name |

| Number of Securities Underlying Unexercised Options (#) Exercisable |

|

| Number of Securities Underlying Unexercised Options (#) Unexercisable |

|

| Equity Incentive Plan Awards: Number of Securities Underlying Unexercised Unearned Options (#) |

|

| Option Exercise Price ($) |

|

| Option Expiration Date |

|

| Number of Shares or Units of Stock That Have Not Vested (#) |

|

| Market Value of Shares or Units of Stock That Have Not Vested ($) |

|

| Equity Incentive Plan Awards: Number of Unearned Shares, Units or Other Rights That Have Not Vested (#) |

|

| Equity Incentive Plan Awards: Market or Payout Value of Unearned Shares, Units or Other Rights That Have Not Vested (#) |

| |||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||

Fred Person |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

Susan Fox |

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

|

| - |

|

There were no grants of stock options since inception to the date of this Form 10-K.

We do not have any long-term incentive plans that provide compensation intended to serve as incentive for performance.

| 10 |

The Board of Directors of the Company has not adopted a stock option plan. The company has no plans to adopt it but may choose to do so in the future. If such a plan is adopted, this plan may be administered by the board or a committee appointed by the board (the “Committee”). The committee would have the power to modify, extend or renew outstanding options and to authorize the grant of new options in substitution therefore, provided that any such action may not impair any rights under any option previously granted. Bookedbyus may develop an incentive based stock option plan for its officers and directors and may reserve up to 10% of its outstanding shares of common stock for that purpose.

Stock Awards Plan

The company has not adopted a Stock Awards Plan, but may do so in the future. The terms of any such plan have not been determined.

Director Compensation

The table below summarizes all compensation awarded to, earned by, or paid to our directors for all services rendered in all capacities to us for the period from inception (December 27, 2007) through August 31, 2016:

DIRECTOR COMPENSATION | ||||||||||||||||||||||||||||

Name |

| Fees Earned or Paid in Cash ($) |

|

| Stock ($) |

|

| Option ($) |

|

| Non-Equity Incentive Plan Compensation ($) |

|

| Non-Qualified Deferred Compensation Earnings ($) |

|

| All Other Compensation ($) |

|

| Total ($) |

| |||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fred Person |

|

| 0 |

|

|

| 0 |

|

|

| 0 |

|

|

| 0 |

|

|

| 0 |

|

|

| 0 |

|

|

| 0 |

|

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters.