UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form

Amendment No. 1

For the fiscal year ended

or

For the Transition Period from to .

Commission File Number

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

Liaoning Province,

(Address of principal executive offices) (Zip Code)

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

| Title of each class | Trading Symbol(s) | Name of the principal U.S. market |

share |

OTCQB marketplace of OTC Markets, Inc. |

Indicate by check mark if the Registrant is a

well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ¨

Indicate by check mark if the Registrant is not

required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨

Indicate by check mark whether the Registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding

12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days.

| 1 |

Indicate by check mark whether the

registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T

(§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to

submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or, an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company”, in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as

defined in Rule 12b-2 of the Exchange Act). Yes ¨

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: As of September 29, 2021, there were shares of common stock issued and outstanding, par value $0.0001 per share.

As of September 29, 2021, there were 5,000,000 shares of preferred stock issued and outstanding, par value $0.0001 per share.

The aggregate market value of the voting and non-voting

common equity held by non-affiliates of the registrant was $

DOCUMENTS INCORPORATED BY REFERENCE: None

Explanatory Note

This Amendment does not reflect any subsequent events occurring after the original filing date of the Report and does not modify or update in any way disclosures made in the Report except to furnish the exhibit described above.

| 2 |

TABLE OF CONTENTS

| Page No. | |||

| PART I | |||

| Item 1. | Business | 5 | |

| Item 1A. | Risk Factors | 20 | |

| Item 1B. | Unresolved Staff Comments | 20 | |

| Item 2. | Properties | 20 | |

| Item 3. | Legal Proceedings | 20 | |

| Item 4. | Mine Safety Disclosures | 20 | |

| PART II | |||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

21 | |

| Item 6. | Selected Financial Data | 25 | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 25 | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 31 | |

| Item 8. | Financial Statements and Supplementary Data | 32 | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 33 | |

| Item 9A. | Controls and Procedures | 34 | |

| Item 9B. | Other Information | 35 | |

| PART III | |||

| Item 10. | Directors, Executive Officers and Corporate Governance | 36 | |

| Item 11. | Executive Compensation | 45 | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

50 | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 52 | |

| Item 14. | Principal Accounting Fees and Services | 55 | |

| PART IV | |||

| Item 15. | Exhibits and Financial Statement Schedules | 56 | |

| Signatures | 57 |

| 3 |

PART I

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements are not historical facts but rather are based on current expectations, estimates and projections. We may use words such as “anticipate,” “expect,” “intend,” “plan,” “believe,” “foresee,” “estimate” and variations of these words and similar expressions to identify forward-looking statements. These statements are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, some of which are beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or forecasted. These risks and uncertainties include the following:

| · | The availability and adequacy of our cash flow to meet our requirements; |

| · | Economic, competitive, demographic, business and other conditions in our local and regional markets; |

| · | Changes or developments in laws, regulations or taxes in our industry; |

| · | Actions taken or omitted to be taken by third parties including our suppliers and competitors, as well as legislative, regulatory, judicial and other governmental authorities; |

| · | Competition in our industry; |

| · | The loss of or failure to obtain any license or permit necessary or desirable in the operation of our business; |

| · | Changes in our business strategy, capital improvements or development plans; |

| · | The availability of additional capital to support capital improvements and development; and |

| · | Other risks identified in this report and in our other filings with the Securities and Exchange Commission or the SEC. |

This report should be read completely and with the understanding that actual future results may be materially different from what we expect. The forward looking statements included in this report are made as of the date of this report and should be evaluated with consideration of any changes occurring after the date of this Report. We will not update forward-looking statements even though our situation may change in the future and we assume no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Use of Term

Except as otherwise indicated by the context, references in this Annual Report to the words "we,""our,""us," the "Company,""IINX," or “Ionix” refers to Ionix Technology, Inc. All references to “USD” or United States Dollars refer to the legal currency of the United States of America.

| 4 |

| Item 1. | Business |

Corporate Background

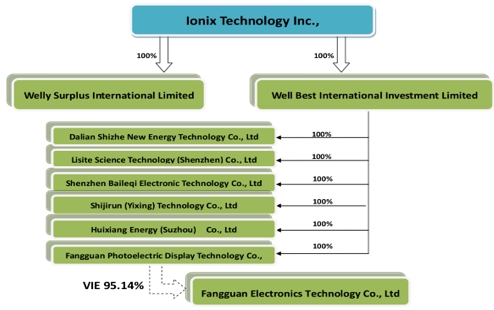

Ionix Technology, Inc. (the “Company”, formerly known as Cambridge Projects Inc.), a Nevada corporation, was formed on March 11, 2011. The Company was originally formed to pursue a business combination through the acquisition of, or merger with, an operating business. The Company filed a registration statement on Form 10 with the U.S. Securities and Exchange Commission (the “SEC”) on August 23, 2011, and focused on identifying a potential business combination opportunity.

On November 20, 2015, the Company’s former majority shareholder and chief executive offer, Locksley Samuels (“Seller”), completed a private common stock purchase agreement (the “SPA”) to sell his entire 21,600,000 shares of the Company’s common stock to Shining Glory Investments Limited (“Purchaser”). In connection with the SPA, the Board appointed Ms. Doris Zhou as the Company’s Chief Executive Officer, Chief Financial Officer, Secretary, Treasurer, and director on November 20, 2015, and Seller concurrently resigned from all positions with the Company. As a result of the SPA, a change in control occurred as (i) Purchaser acquired approximately 65.45% of the Company’s common stock, and (ii) the Company’s sole officer and director after the SPA was Ms. Zhou, who has since resigned.

On November 30, 2015, the Company’s board of directors (the “Board”) and the majority of its shareholders approved that (i) the Company change its name from “Cambridge Projects Inc.” to “Ionix Technology, Inc.”, (ii) the Company voluntarily changed its ticker symbol in connection with the name change, and (iii) the Company execute a 3:1 forward stock split, which will increase the Company’s issued and outstanding shares of common stock from 33,001,000 to 99,003,000 (the “Corporate Actions). The Company filed an application with the Financial Industry Regulatory Authority (“FINRA”) to effectuate the Corporate Actions and filed a Form 8-K on December 10, 2015, in regards to the Corporate Actions. On February 3, 2016, FINRA approved the Corporate Actions, which took effect on the market on February 4, 2016. As a result, (i) the Company’s name is now “Ionix Technology, Inc.”, (ii) its new trading symbol is “IINX”, (iii) the 3:1 forward stock split is effective, payable upon surrender, and (iv) the Company’s new CUSIP number is 46222Q107.

On February 17, 2016, the Board ratified, approved, and authorized the Company’s acquisition of a wholly-owned subsidiary, Well Best International Investment Limited, a limited liability company formed under the laws of Hong Kong Special Administrative Region (“Well Best”) on September 14, 2015. Well Best was acquired by Qingchun Yang, its current director, on November 10, 2015. One hundred percent interest in Well Best was transferred to Ionix Technology on February 15, 2016.Well Best’s purpose is to act as an investment holding company and pursue new business ventures conducted in the Asia Pacific region excluding China. Well Best has had no activities since inception.

On November 7, 2016, the Company’s Board of Directors approved and ratified the incorporation of Lisite Science Technology (Shenzhen) Co., Ltd ("Lisite Science"), a limited liability company formed under the laws of China on June 20, 2016. Well Best is the sole shareholder of Lisite Science. As a result, Lisite Science is an indirect, wholly-owned subsidiary of the Company. Lisite Science focused on marketing the high-end intelligent electronic equipment, specifically a power bank which is a 5 volt 2 amp, 20000mAh lithium ion battery powered portable device offering charging time of 12-18 hours that is intended to be utilized as a power source for electronic devices such as the iphone, ipad, mp3/mp4 players, PSP gaming systems, and cameras. Lisite Science commenced operations in September of 2016.

On November 7, 2016, the Company’s Board of Directors approved and ratified the incorporation of Shenzhen Baileqi Electronic Technology Co., Ltd. ("Baileqi Electronic"), a limited liability company formed under the laws of China on August 8, 2016. Well Best is the sole shareholder of Baileqi Electronic. As a result, Baileqi Electronic is an indirect, wholly-owned subsidiary of the Company. Baileqi Electronic focused on marketing the LCD and module for civil electronic products. The module of new energy power system refers to an LCD screen that is manufactured for small devices such as video capable baby monitors, electronic devices such as tablets and cell phones, and for use in televisions or computer monitors. Baileqi Electronics commenced operations in September of 2016.On September 1, 2016, Baileqi Electronics entered into a manufacturing agreement with Shenzhen Baileqi Science and Technology Co., Ltd. ("Shenzhen Baileqi S&T") to manufacture products for Baileqi Electronics.

| 5 |

On December 29, 2016, the Company’s Board of Directors approved and ratified the acquisition of 99.9% of the issued and outstanding stock of Welly Surplus International Limited, a limited company formed under the laws of Hong Kong on January 18, 2016, in exchange for 99,999 HK dollars (the “Acquisition”). As a result of the Acquisition, the Company became the majority shareholder of Welly Surplus, owning 99.99% of the issued and outstanding stock of Welly Surplus, and Welly Surplus is now a majority owned subsidiary of the Company. As the closing of the Acquisition, Ms. Zhou was appointed as a member of the board of directors of Welly Surplus. Welly Surplus will act as the accounting and financial base for the Company and shall focus on assisting the Company with all of the Company’s financial affairs. Welly surplus had no activities since inception.

On April 7, 2017, Ben William Wong (“Wong”) and Yubao Liu, an individual (“Liu”) entered into a Stock Purchase Agreement (the “Agreement”) whereby Wong agreed to sell and Liu agreed to purchase 5,000,000 shares of the Company’s restricted preferred stock, representing 100% of the total issued and outstanding preferred stock (“Company Preferred Stock”). In consideration for the Company Preferred Stock, Liu agreed to pay to Wong a total of 5,000,000 RMB on or before April 30, 2017. The Agreement closed on April 20, 2017 (the “Closing”). Additionally, on April 5, 2017, Liu and Shining Glory Investments Limited, a British Virgin Islands company (“Shining Glory”), of which Wong is the sole officer and director, entered into a purchase agreement whereby Liu acquired 1 ordinary common stock share (the “Shining Glory Share”) representing approximately 100% of Shining Glory’s outstanding shares of common stock. In consideration for the Shining Glory Share, Liu paid to Wong a total of $1 USD and Wong resigned as a Director of Shining Glory. Concurrently, Liu was appointed as the sole director of Shining Glory. The agreement between Shining Glory and Liu closed on April 20, 2017.

On February 20, 2018, the Company ratified and approveda the appointment of Jialin Liang as President and a member of the board of directors of Changchun Fangguan Photoelectric Display Technology Co. Ltd ("Fangguan Photoelectric"). On February 20, 2018, the Company’s Board of Directors approved and ratified the incorporation of Fangguan Photoelectric. Fangguan Photoelectric is a wholly owned subsidiary of Well Best International Investment Limited and an indirect wholly-owned subsidiary of the Company. Fangguan Photoelectric focused on marketing LCDs for the Company. In October 2018, Jialin Liang resigned as President and Director of Fangguan Photoelectric. Mr Biao Shang became his successor.

On June 28, 2018, the Board of Directors of Ionix Technology, Inc. (the “Company”) approved and ratified the incorporation of Dalian Shizhe New Energy Technology Co., Ltd. (“Shizhe New Energy”) and the Company ratified and approved the appointment of Mr. Liang Zhang as President and a member of the board of directors of Shizhe New Energy . Shizhe New Energy is a wholly owned subsidiary of Well Best International Investment Limited and an indirect wholly-owned subsidiary of Ionix Technology, Inc. In May 2019, Liang Zhang resigned as President and Director of Shizhe New ENERGY. Mr Shikui Zhang became his successor.

On December 27, 2018, the Company entered into a Share Purchase Agreement (the “Purchase Agreement”) with Jialin Liang and Xuemei Jiang, each of whom is shareholder (the “Shareholders”) of Changchun Fangguan Electronics Technology Co., Ltd. (PRC) (“Fangguan Electronics”). Pursuant to the terms of the Purchase Agreement, the Shareholders, who together own 95.14% of the ownership rights in Fangguan Electronics, agreed to execute and deliver the Business Operation Agreement dated December 27, 2018 (the “Business Operation Agreement”), the Equity Interest Pledge Agreement dated December 27, 2018 (the “Equity Interest Pledge Agreement”), the Equity Interest Purchase Agreement dated December 27, 2018 (the “Equity Interest Purchase Agreement”), the Exclusive Technical Support Service Agreement dated December 27, 2018 (the “Services Agreement”) and the Power of Attorney dated December 27, 2018 (the “Power of Attorney” and together with the Business Operation Agreement, the Equity Interest Pledge Agreement, the Equity Interest Pledge Agreement and the Services Agreement, the “VIE Transaction Documents”) to the Company in exchange for the issuance of an aggregate of 15,000,000 shares of the Company’s common stock, par value $.0001 per share (the “Common Stock”), thereby causing Fangguan Electronics to become the Company’s variable interest entity. Together with Purchase Agreement, in exchange of 15 million shares of the Company’s common stock, the Shareholders also agreed to convert shareholder loan of RMB 30 million (approximately $4.4 million) to capital and make cash contribution of RMB 9.7 million (approximately $1.4 million) to capital. The entirety of the transaction will hereafter be referred to as the “Transaction.”

On February 7, 2021, the Board of Directors of the Company approved and ratified the incorporation of Shijirun (Yixing) Technology Co., Ltd. (“Shijirun”), a limited liability company formed under the laws of the Peoples Republic of China (PRC) on February 7, 2021. Well Best International Investment Limited is the sole shareholder of Shijirun. As a result, Shijirun is an indirect, wholly-owned subsidiary of the Company. Shijirun focuses on developing and producing high-end intelligent new energy equipment in Yixing City, Jiangsu Province, China.

On March 30, 2021, the Board of Directors of Ionix Technology, Inc. approved and ratified the incorporation of Huixiang Energy Technology (Suzhou) Co., Ltd. (“Huixiang Energy”), a limited liability company formed under the laws of the Peoples Republic of China (PRC) on March 18, 2021. Well Best is the sole shareholder of Huixiang Energy. As a result, Huixiang Energy is an indirect, wholly-owned subsidiary of the Company. Huixiang Energy shall conduct research and development of next generation advanced battery technologies, manufacture and sales of relevant battery products, including the solid-state rechargeable lithium ion battery for next generation EV and energy storage systems. Huixiang Energy also focuses on the operation of battery packs, battery systems and electric vehicles sharing business with its own internet sharing platform relating to the electric vehicles (online EV hailing services) and its relevant batteries and battery systems. Huixiang Energy operates in Suzhou City, Jiangsu Province, China.

On May 6, 2021, the Board of Directors and the holders of the majority of issued and outstanding voting securities of the Company approved an amendment (the “Amendment”) to our Articles of Incorporation to increase the authorized number of shares of common stock from 200,000,000 to 400,000,000 shares consisting of: (i) 395,000,000 shares of common stock, par value $0.0001 per share (“Common Stock”); and (ii) 5,000,000 shares of preferred stock par value $0.0001 per share (“Preferred Stock”) (the “Authorized Share Increase”) and related Certificate of Amendment to Articles of Incorporation. The approval was made in accordance with Sections 78.320 and 78.390 of the Nevada Revised Statues, which provide that a corporation’s articles may be amended by written consent of the stockholders representing at least a majority of the voting power. The Amendment was filed with the Nevada Secretary of State on June 7, 2021.

| 6 |

Description of VIE Transaction Documents

The material contractual agreements between Changchun Fangguan Photoelectric Display Technology Co. Ltd. (PRC) (“Fangguan Photoelectric”), Fangguan Electronics and its shareholders consist of the following agreements:

Business Operation Agreement – This agreement allows Fangguan Photoelectric to manage and operate Fangguan Electronics. Under the terms of the Business Operation Agreement, Fangguan Photoelectric may direct the business operations of Fangguan Electronics, including, but not limited to, borrowing money from any third party, distributing dividends or profits to shareholders, adopting corporate policy regarding daily operations, financial management, and employment, and appointment of directors and senior officers.

Exclusive Technical Support Service Agreement – This agreement allows Fangguan Photoelectric to collect 100% of the net profits of Fangguan Electronics. Under the terms of the Service Agreement, Fangguan Photoelectric is the exclusive provider of equipment, advice and consultancy to Fangguan Electronics related to its general business operations, among other things. Fangguan Photoelectric owns all intellectual property rights arising from its performance under the Service Agreement.

Power of Attorney – The Shareholders have each executed and delivered to Fangguan Photoelectric a Power of Attorney pursuant to which Fangguan Photoelectric has been granted the Shareholders’ voting power in Fangguan Electronics. Each Power of Attorney is irrevocable and does not have an expiration date.

Equity Interest Purchase Agreement – Fangguan Photoelectric and the Shareholders entered into an exclusive option agreement pursuant to which the Shareholders have granted Fangguan Photoelectric or its designee(s) the irrevocable right and option to acquire all or a portion of such Shareholders’ equity interests in Fangguan Electronics. Pursuant to the terms of the agreement, Fangguan Photoelectric and the Shareholders have agreed to certain restrictive covenants to safeguard the rights of Fangguan Photoelectric under the Equity Interest Purchase Agreement. Fangguan Photoelectric may terminate the Equity Interest Purchase Agreement upon prior written notice. The Option Agreement is valid for a period of five (5) years from the effective date, which may be extended by Fangguan Photoelectric.

Equity Interest Pledge Agreement – Fangguan Photoelectric and the Shareholders entered into an agreement pursuant to which the Shareholders have pledged all of their equity interests in Fangguan Electronics to Fangguan Photoelectric. The Equity Interest Pledge Agreement serves to guarantee the performance by Fangguan Electronics of its obligations under the VIE Transaction Documents. Pursuant to the terms of the Equity Interest Pledge Agreement, the Shareholders have agreed to certain restrictive covenants to safeguard the rights of Fangguan Photoelectric. Upon an event of default under the agreement, Fangguan Photoelectric may foreclose on the pledged equity interests.

As a result of the Transaction, the Company, through its subsidiaries and variable interest entity, is now engaged in the business of the research and development, manufacturing, and marketing of liquid crystal materials, displays and modules in the PRC. All business operations are conducted through our wholly-owned subsidiaries, including Fangguan Photoelectric, and through Fangguan Electronics, our variable interest entity. Fangguan Electronics is considered to be a variable interest entity because we do not have any direct ownership interest in it, but, as a result of a series of contractual agreements between Fangguan Photoelectric, our wholly-owned subsidiary, and Fangguan Electronics and its shareholders, we are able to exert effective control over Fangguan Electronics and receive 100% of the net profits or net losses derived from the business operations of Fangguan Electronics.

Prior Operations and Agreements

On August 19, 2016, the Board ratified, approved, and authorized the Company, as the sole member of Well Best, on the formation of Xinyu Ionix Technology Company Limited (“Xinyu Ionix”), a company formed under the laws of China on May 19, 2016. As a result Xinyu Ionix is a wholly-owned subsidiary of Well Best and an indirect wholly-owned subsidiary of the Company. The initial plan of Xinyu Ionix was about to focus on developing and designing lithium batteries as well as to act as an investment company that may acquire other businesses located in China. However, due to the high cost and low efficiency, since the approval date of May 19, 2016, Xinyu Ionix conducted no business.

| 7 |

On April 30, 2017, Well Best International Investment Limited (“Well Best”), a wholly-owned subsidiary of the Company, transferred all of its rights, title and interest to all 100% of the issued and outstanding common stock of Xinyu Ionix Technology Company Limited (“Xinyu Ionix”) to Zhengfu Nan for RMB 100($14.49) pursuant to a Share Transfer Agreement dated April 30, 2017 (the “Agreement”). Following the execution of the Agreement, Mr. Nan owns 100% of Xinyu Ionix and assumes all liabilities of Xinyu Ionix. As a result Xinyu Ionix is no longer a wholly-owned subsidiary of Well Best or an indirect wholly-owned subsidiary of the Company.

Business Summary

Since January 2016, the Company has shifted its focus to becoming an aggregator of energy cooperatives to achieve optimum price and efficiency in creating and producing technology and products that emphasize long life, high output, high energy density, and high reliability. By and through its wholly owned subsidiary, Well Best and the indirect subsidiaries, Baileqi Electronics, Lisite Science, Welly Surplus, Fangguan Photoelectric, Fangguan Electronics,Huixiang Energy, Shijirun and Shizhe New Energy, the Company has commenced its main operations of high-end intelligent electronic equipment and photoelectric display products, became the New energy service provider and IT solution provider, which are in the new-type rising industries.

The Company applied various operating approacehs. Baileqi Electronics, Lisite Science, Fangguan Photoelectric, Huixiang Energy, Shijirun and Shizhe New Energy focus on the sales of goods and the rendering of service while Fangguan Electronics has been engaged in the business of the research and development, manufacturing, and marketing of liquid crystal materials, displays and modules in the PRC.

The Company, Well Best, Welly Surplus, Baileqi Electronics, Lisite Science, Fangguan Photoelectric, Fangguan Electronics, Huixiang Energy, Shijirun and Shizhe New Energy are actively seeking additional new prospects for technology enhancements, design, manufacturing and production of the Company’s operation of high-end intelligent electronic equipment and more cutting-edge LCD technologies, such as Liquid Crystal Module (“LCM“), the portable power banks, the battery packs and the electric furnace used in firing for lithium battery.

We are engaged in the business of research and development, manufacturing, and marketing of liquid crystal materials, displays and modules, the battery packs and the electric furnace used in firing for lithium battery in the PRC. The Company operates through a corporate structure consisting of subsidiaries, variable interest entities (“VIE”), and contractual arrangements. A VIE is a term used by the U.S. Financial Accounting Standards Board to describe a legal business structure whose financial support comes from another corporation which exerts control over the VIE. All of the Company’s business operations are structured around a series of contractual agreements, the VIE Transaction Documents, including the ones between Fangguan Photoelectric, our wholly-owned subsidiary, and Fangguan Electronics and its shareholders. Through the VIE Transaction Documents, we are able to exert effective control over Fangguan Electronics and receive 100% of the net profits derived from the business operations of Fangguan Electronics.

Products and Projects

Civil Electronics

With the high-speed development in the new energy industry, the high-tech and relevant key accessories still play an essential role in the energy industry supply chain. LCD displays and lithium battery packs are widely used in the end products of the new energy industry.

Since the beginning of 2017, the Company has expanded its focus to development and production of LCD’s and modules for civil electronic products, lithium battery packs. By and through its wholly owned subsidiary, Well Best and the indirect wholly owned subsidiary, Baileqi Electronics and Fangguan Photoelectric, the Company has commenced its operations in China. Baileqi is working on an upgrade to traditional LCD screens with display modules that use the crystal method (“TCM”) and control muddle system integration for professional manufacturing. Today, TCM is widely used in many areas, including electronic operation data displays for renewable energy vehicles, BMS information feedback, HD projectors, communication equipment, and particularly in intelligent robots.

| 8 |

The LCD screens are manufactured for small devices such as video capable baby monitors, electronic devices such as tablets and cell phones, and for use in televisions or computer monitors.

Since the beginning of 2021, we has explored the business opportunities in lithium battery -related industry and have formulated a vertically integrated business model that will cover all important aspects of the value chain including deep processing of upstream Lithium Compounds, production and installation of midstream kun furnaces used in firing the lithium battery, and production of downstream LFP battery packs

The lithium battery packs and the electric furnace used in firing for lithium battery have been supplied by the subsidiaries of the Company.

The Company also provides service and IT solution for new energy industry.

1. Fanguguan Electronic

| Products of Fanguguan Electronic | |

|

Product Model: FG814B-

Resolution: Segment LCD LCD Active Area: 44*67 Outline Dimensions:

Display Colors: Black and View Direction: 6 O’clock

|

|

| 9 |

|

Product Model: FG12832B-

Resolution: 128*32 LCD Active Area: Outline

Display Colors: Black and View Direction: 12 O’clock |

|

|

Product Model: FG160100J-

Resolution: 160*100 LCD Active Area: Outline Dimensions:

Display Colors: Black and View Direction: 6 O’clock |

|

| 10 |

2. Fangguan Photoelectric

| Products of Fangguan Photoelectric | |

|

Product Model:

Resolution: 240*160 LCD Active Area: Outline Dimensions:

Display Colors: Black and Viewing Direction: 6 |

|

| 11 |

|

Product Model:

Resolution: 128*64 LCD Active Area: 66*38 Outline Dimensions:

Display Colors: Black and View Direction: 6 O’clock |

|

|

Product Model:

Resolution: 128*64 LCD Active Area: Outline Dimensions:

Display Colors: Black and View Direction: 6 O’clock |

|

| 12 |

3. Lisite Science

| Products of Lisite Science | |

|

Product Model: W200

Battery Type: 18650-2500mAh*8 Rated Output: 5V / 2.1A (Max)

Input: Micro-USB、Lightning Input Parameter: MAX10W USB -A-1 : DC5V/1A

Size: 165.2*78*23MM Weight: 437g |

|

|

Product Model: T3

Battery Type: Polymer 805573*2 Rated Output: 5V/2.1A (Max) Input Parameter: MAX10W Output Parameter: MAX10.5W USB-A-2: DC5V/2.1A Shared 2.1A |

|

| 13 |

4.Shijirun

|

Large atmosphere kun furnace for firing lithium batteries |

|

| 14 |

5.Huixiang Energy

|

Product Model: lithium iron phosphate ("LFP") battery packs

Specification::16S1P General Use type

Unit: NH-33138-HE_15Ah_LFP |

|

| 15 |

6.Baileqi Electronic:

| Products of Baileqi Electronic | |

|

Module No.: Y50029N00T Size:5.0 inch

Resolution:800(H)*3(RGB)*480(V)TFT LCD Active Area:108.00*64.80mm Outline Interface Type:24BITRGBInterface

Display Colors:16.7M Brightness:300cd/mm View Direction:12O’clock |

|

|

Module No.:Y43001N04N Size:4.3 inch

Resolution:480RGB×272 LCD Active Area:95.04(H)×53.86(V) Outline Dimensions: Interface Type: RGB 24 BIT

Display Colors:16.7M Brightness:480cd/mm(7S) View Direction:12O’clock |

|

|

Module No.:Y10108M00N Size:10.1 inch

Resolution:1280RGB×800 LCD Active Area:216.96(H)×135.60(V) Outline Dimensions: 229.46(H)× Interface Type: LVDS (Low Voltage

Display Colors:16.7M Brightness:300cd/mm(3S-13P) View Direction:6O’clock |

|

| 16 |

Industry Overview

Synergies throughout the lithium battery Industry Value Chain

In China, the current explosive growth in the new energy vehicle industry has led to a significant increase in demand for lithium iron phosphate batteries and the corresponding increase in demand for lithium compounds, with the industry gradually shifting from a balanced supply and demand to a tight supply situation. Under the dual stimulation of the gradually weakening impact of policies and the rising industry demand, the price of lithium compound is gradually rebounding. As a "rising star" start-up player in the lithium battery-related business, we endeavor to capitalize on the opportunities arising from industry reshuffle, continue to enhance our competitiveness and further improve our industrial position.

We have a vertically integrated business model that will cover all important aspects of the value chain including deep processing of upstream Lithium Compounds, production and installation of midstream kun furnaces used in firing the lithium battery, and production of downstream LFP battery packs. We started as a supplier of the midstream kun furnaces used in firing the lithium battery and has been striving for expanding to the upstream and downstream of the industrial value chain to obtain a competitive supply of LFP battery packs, thereby ensuring cost and operational efficiency, synergy among multiple business lines, and access to the latest market information and development of cutting-edge technologies.

We adhere to the development strategy of “upstream and downstream integration of the LFP battery-related industry” given the features of LFP (higher value for money and safer than other kinds of lithium batteries)

Our products as below are expected to be widely used in the manufacturing of electric vehicles, aerospace products, and functional materials in the future. And we will focus on developing the major players in their respective industries aforementioned as our customers.

We strive for offering our customers the comprehensive suite of product as below to effectively address the unique and diverse needs of our customers.

Furnace used in firing for lithium battery: At the core of our "throughout value chain" business model is the furnace used in firing for lithium battery, mainly including (1) large atmosphere kun furnace for firing lithium batteries (2) Atmosphere kun furnace for firing lithium batteries(3) Push plate furnace used in ferrite firing. Such furnaces are widely used in manufacturing lithium battery fields. Our customers are expected to be primarily global lithium battery manufacturers.

Lithium compounds: Our lithium compounds are expected to be mainly including (1) battery-grade lithium hydroxide; (2) battery-grade lithium carbonate; (3)lithium nickel cobalt manganate. Such lithium compounds are widely used as lithium battery materials for electric vehicles, portable electronics, as well as in chemical and pharmaceutical fields. Our customers are expected to primarily consist of global battery cathode materials manufacturers, battery suppliers.

Lithium batteries: The Company produces lithium battery. Such batteries are mainly used in electric vehicles, a variety of energy storage equipment and all kinds of consumer electronic devices, such as mobile phones, tablets, and laptops. Meanwhile, we will also proactively carries forward the research, development, production and commercial application of solid-state lithium batteries. As per the electric vehicles, our most important end- users, the monthly sales in China’s electric vehicle market has continued to show a significant year-on-year growth since July 2020. In 2020, the production and sales amounted to 1.366 million and 1.367 million respectively, representing a year-on-year increase of 7.5% and 10.9% respectively, and hitting a record high. With reference to the target of 20% sales of new electric vehicles as mentioned in the Electric Vehicle Industry Development Plan (2021–2035), there still exists broad development space for the electric vehicle industry, and remains high certainty on the long-term growth trend of the electric vehicle industry chain.

Our vertically integrated business model contributes to the constant launches of new products and services, which allows us to solidify the strategic relationships with our customers and end-users.

Development trend of photoelectric display products:

IINX is active in promoting the worldwide application of green energy solutions. We are always pursuing more optimized green energy solutions together with our customers. Recently, we confronted the rapid growth of the new energy industry, however, high and new technology and its relevant accessories still play pivotal roles in the existing industrial chain. In the meantime, we have also chosen a more extensive applied terminal product in new energy industry- the Liquid Crystal Displays (LCD), as an important composition part of our business.

| 17 |

LCD-From Global Perspective

The global demand of LCD panels is continually increasing. The output area of global LCD panels achieved 181 million square meters in 2017, this figure was tripled compared to 2007, and the average annual growth is approximately 13 million square meters. According to the prediction, the global demand of LCD panels will be 215 million square meters in 2021.From 2017 to 2021, the compound average growth rate (CAGR) of such demand will be about 4.37%, though the growth seems to slow down compared with the CAGR of 5% for the most recent 3 years, however, without considering base effect, the demand will maintain an average increase of approximately 8.5 million square meters per annum.

The demand of twisted nematic (TN) and supper twisted nematic (STN) liquid crystal materials remains generally stable. Due to their characteristics such as low cost, wide range of applications, the low-end TN and STN liquid crystal materials will still take a certain portion of market for terminal products which require a relatively low level of display. Basically, since 2004, the market demand of TN and STN liquid crystal materials has been stable, with the annual quantity demand maintaining at approximately between 60 and 70 tons, to compute based on the average price of about 5000 Yuan/kg for TN and STN liquid crystal materials, the predicted market scale for TN and STN liquid crystal materials would be approximately 300 million to 350 million Yuan.

There is a strong demand of thin film transistor (TFT) liquid crystal materials in the global market as well. TFT liquid crystal materials account for over 80% of total output value in the global liquid crystal materials market. With the rapid development of LCD television, laptop, desktop display and mobile communication, the demand of TFT liquid crystal panel keeps increasing. To measure and calculate on the basis of 80% of effective display area, a liquid crystal material usage of 4.5kg per square meter area of panel and an average price of 15,000 Yuan per kilogram for mixed liquid crystal materials, the quantity demand of global TFT mixed liquid crystals in 2016 was about 617 tons and market scale was around 9.3 billion Yuan. The global quantity of TFT mixed liquid crystals is estimated to be about 666 tons and the market scale will be about 10 billion Yuan in 2021.

LCD-From China’s Perspective

China is one of the largest display panel producers in the world, according to the data provided by China Optics and Optoelectronics Industry Association LCB. Recently, the liquid crystal panels in mainland China reached the top rank in the world in terms of both revenue and output area. China is and has been a big display manufacturing country, however, China is now at a crucial time for change and attempting to evolve from a big country to a powerful display manufacturing country. China is developing out of a “catch up” position into a phase of advance or equal footing with other competing countries and has an opportunity to become an industrial leader in the near future. It is understood that in the past year, there were multiple panel manufacturing lines have been put into production or started construction in China, especially the Gen 10.5/11 panel manufacturing lines and many Gen 6 AMOLED manufacturing lines were under construction, which just brings China closer and closer to the position of being one of, if not the largest production regions for display panels in the world. China has a number of OLED panel lines put into production or expansion. The scale of investment in OLED is expected to reach $30 billion to $50 billion over the next 3-5 years. BOE, CSOT, Visionox, Tianma and many other manufacturers have launched products such as flexible display, full-screen display, special-shaped display and so on, the domestic high-end displays in China are developing rapidly. The capacity of display panels of China is expected to become the first among all the countries in 2022.

LCD-From Industrial Perspective

At present, the OLED panel Market for mobile phones is almost monopolized by South Korea, with Samsung display accounting for 93.5% and LGD accounting for 2.1%. The influence of Chinese manufacturers is very small, with 2.0% of VINSIONOX, 1.4% of EverDisplay Optronics (EDO) and 0.6% of BOE, which together are less than 5%. From 2019, China began to exert influence on the OLED market. It is estimated that BOE's shipment will reach 50 million pieces (with an annual increase of 1900%), EDO 30 million (with an annual increase of 417%), Vinsionox's 20 million pieces (with an annual increase of 150%), and Tianma's 10 million pieces (with an annual increase of 1011%).

Distribution Methods of Products

The Company’s products are currently directly shipped from the manufacturers to the distributors and retailers. Marketing and sales departments were established through the Company’s indirect subsidiaries to cope with the growth of the Company. We explore the potential customer bases using internal resources. Currently, we have both the long-term contracts with our customers and manufacture according to the purchase orders received. In the future, we will continue to seek additional channels of distribution for our products to include wholesale stores and mass retailers. The Company plans to focus primarily on distributing its products regionally, starting in Greater China, and will then seek to expand its distribution channels across the U.S. and internationally.

| 18 |

Suppliers of Materials

The elements necessary for our products are and will be sourced from several different suppliers located primarily in China on an order-by-order basis. These materials include ITO coated conductive glasses, liquid crystals, lithium material for battery, integrated circuits and etc. Some of the materials in our products are not readily available in large quantities or are available on a limited basis only. Further, the limited availability of some of these materials could cause significant fluctuations in their costs.

The Company, Baileqi Electronics, Fangguan Electronics, Huixiang Energy and Shijirun acquire materials from the following list of principal suppliers, dependent on availability and price points:

| · | Panshi Tengfei Electronics Ltd |

| · | Shenzhen Yonglitong Electric Technology Ltd |

| · | Yixing Weifeng Regong Technology Ltd |

| · | Shenzhen Huachuang Zhongwei Electric Ltd. |

*This list of suppliers is subject to change at any time.

Our management researches and develops our sources of materials used in the manufacturing of our products. The materials that we source are and will be sent to our manufacturer in China to create our products. The Company does not have any long-term contracts with our suppliers and we cannot be assured that they will be able to meet our demands.

Intellectual Property

As part of our business, we will seek to protect our intellectual property rights in various ways, including through trademarks, copyrights, trade secrets, including know-how, patents, patent applications, employee and third-party nondisclosure agreements, intellectual property licenses and other contractual rights.

Government Regulations Affecting Our Business

At this stage in our business, we are unaware of any government regulations that are directly affecting our business, however, as we grow our business activities may become subject to various governmental regulations in different countries in which we operates, including regulations relating to: various business/investment approvals; trade affairs, including customs, import and export control; competition and antitrust; anti-bribery; advertising and promotion; intellectual property; broadcasting, consumer and business taxation; foreign exchange controls; personal information protection; product safety; labor; human rights; conflict; occupational health and safety; environmental; and recycling requirements.

Employees of the Company

The Company has no significant employees other than our officers and directors. As of June 30, 2021, the Company has no employees, however, our indirect subsidiary Baileqi Electronic has four employees, Lisite Science has three employees, Fangguan Photoelectric has 2 employees, Shijirun has 6 employees, Fangguan Electronics has about 207 employees and Dalian Shizhe New Energy has 6 employees. We intend to increase the size of our management team and hire additional employees in the future to manage the continued growth of our company and to increase our sales force and marketing efforts.

| 19 |

WHERE YOU CAN GET ADDITIONAL INFORMATION

We file annual, quarterly and current reports, proxy statements and other information with the SEC. You may read and copy our reports or other filings made with the SEC at the SEC’s Public Reference Room, located at 100 F Street, N.E., Washington, DC 20549. You can obtain information on the operations of the Public Reference Room by calling the SEC at 1-800-SEC-0330. You can also access these reports and other filings electronically on the SEC’s web site, www.sec.gov.

| Item 1A. | Risk Factors |

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

Our mailing address in the US is that of our registered agent, at 3773 Howard Hughes Pkwy, Suite 500S, Las Vegas, NV 89169. Our address in China is Rm 608, Block B, Times Square, No. 50 People Road Zhongshan District, Dalian City, Liaoning Province, China.

Lisite Science,one of our subsidiaries’leases office and warehouse space from Keenest, a related party, with annual rent of approximately $1,500 (RMB10,000) for one year until July 20, 2021.On July 20, 2021, Lisite Science further extended the lease with Keenest for one more year until July 20, 2022 with annual rent of approximately $295 (RMB2,000).

We believe that this space is adequate for our current and immediately foreseeable operating needs.

| Item 3. | Legal Proceedings |

We know of no material, existing or pending legal proceedings against our company, nor are we involved as a plaintiff in any material proceeding or pending litigation. There are no proceedings in which any of our directors, officers or affiliates, or any registered or beneficial stockholder, is an adverse party or has a material interest adverse to our interest.

| Item 4. | Mine Safety Disclosure |

Not applicable.

| 20 |

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Small Business Issuer Purchases of Equity Securities |

Market Information

Our common stock is currently quoted on OTCQB. Our common stock commenced quotation on the OTCQB under the trading symbol “CPJT”. On February 4, 2016, our symbol was changed to “IINX” to reflect the Company’s name change to Ionix Technology, Inc. Our common stock began trading in April 2015. Because we are quoted on the OTCQB, our common stock may be less liquid, receive less coverage by security analysts and news media, and generate lower prices than might otherwise be obtained if it were listed on a national securities exchange.

The following table sets forth the high and low bid prices for our Common Stock per quarter as reported by the OTCQB for the quarterly periods indicated below based on our fiscal year end June 30. These prices represent quotations between dealers without adjustment for retail mark-up, markdown or commission and may not represent actual transactions.

| Fiscal Quarter | High | Low | ||||||

| First Quarter (Jul. 1, 2018– Sept. 30, 2018) | $ | 2.50 | $ | 1.75 | ||||

| Second Quarter (Oct. 1, 2018 – Dec. 31, 2018) | 2.47 | 2.05 | ||||||

| Third Quarter (Jan. 1, 2019– Mar. 31, 2019) | 3.00 | 2.50 | ||||||

| Fourth Quarter (Apr. 1, 2019– Jun. 30, 2019) | 2.70 | 2.11 | ||||||

| First Quarter (Jul. 1, 2019– Sept. 30, 2019) | $ | 2.00 | $ | 1.70 | ||||

| Second Quarter (Oct. 1, 2019– Dec. 31, 2019) | 1.93 | $ | 1.33 | |||||

| Third Quarter (Jan. 1, 2020 – Mar. 31, 2020) | 1.85 | $ | 0.95 | |||||

| Fourth Quarter (Apr. 1, 2020 – Jun. 30, 2020) | 1.91 | $ | 0.975 | |||||

| First Quarter (Jul. 1, 2020– Sept. 30, 2020) | $ | 0.975 | $ | 0.045 | ||||

| Second Quarter (Oct. 1, 2020– Dec. 31, 2020) | 0.18 | 0.02 | ||||||

| Third Quarter (Jan. 1, 2021– Mar. 31, 2021) | 0.403 | 0.11 | ||||||

| Fourth Quarter (Apr. 1, 2021 – Jun. 30, 2021) | 0.301 | 0.40 | ||||||

Record Holders

As of June 30, 2021, the approximate number of registered holders of our common stock was 214. As of June 30, 2021, there were 164,041,058 shares of common stock issued and outstanding and there were 5,000,000 shares of preferred stock issued and outstanding. There were no shares of common stock subject to outstanding warrants, and there were no shares of common stock subject to outstanding stock options.

Dividends

On November 30, 2015, the Company’s board of directors and majority of its shareholders approved a 3:1 forward stock split which increased the Company’s issued and outstanding shares of common stock from 33,001,000 to 99,003,000 (the “Forward Split”). The Forward Split was approved by FINRA and took effect on the market on February 4, 2016. The Forward Split shares were payable upon surrender of certificates to the Company’s transfer agent.

We have not declared or paid any cash dividends on our common stock nor do we anticipate paying any in the foreseeable future. Furthermore, we expect to retain any future earnings to finance our operations and expansion. The payment of cash dividends in the future will be at the discretion of our Board of Directors and will depend upon our earnings levels, capital requirements, any restrictive loan covenants and other factors the Board considers relevant.

Securities Authorized for Issuance under Equity Compensation Plans

None.

| 21 |

Recent Sales of Unregistered Securities; Use of Proceeds from Registered Securities

The following sets forth certain information concerning securities which were sold or issued by us without the registration of the securities under the Securities Act of 1933 in reliance on exemptions from such registration requirements within the past three years:

On February 17, 2016, the Company entered into a subscription agreement to sell 5,000,000 preferred shares (the “Preferred Shares”) for $50,000 in cash ($0.01 per share). No commissions were paid to any broker or third party for this transaction.

On January 31, 2020, the Company issued a total of 12,775 shares of common stock to Power Up Lending Group Ltd for the conversion of debt in the principal amount of $12,000 according to the conditions of the convertible note dated as July 25, 2019.

In December 2019, the Company engaged Maxim Group LLC (“Maxim”) for financial advisory and investment banking services to assist the Company in articulating its growth strategy to the investment community and up-list its securities to a National Securities Exchange. On February 10, 2020, the Company issued 150,000 shares of common stock valued at $262,500 to Maxim Group LLC as a part of its compensation for the services. On May 19, 2020, the Company and Maxim mutually agreed to terminate all rights and obligations under their agreements and in May 2020, Maxim returned 75,000 shares of common stock shares to the Company for cancellation.

On February 18, 2020, the Company issued a total of 11,834 shares of common stock to Power Up Lending Group Ltd for the conversion of debt in the principal amount of $10,000 according to the conditions of the convertible note dated as July 25, 2019.

On February 28, 2020, the Company issued a total of 15,448 shares of common stock to Power Up Lending Group Ltd for the conversion of debt in the principal amount of $12,000 according to conditions of the convertible note dated as July 25, 2019.

On May 19, 2020, the Company issued a total of 16,484 shares of common stock to Power Up Lending Group Ltd for the conversion of debt in the principal amount of $15,000 according to the conditions of the convertible note dated as July 25, 2019.

On May 29 2020, the Company issued a total of 19,724 shares of common stock to Power Up Lending Group Ltd for the conversion of debt in the principal amount of $15,000 according to the conditions of the convertible note dated as July 25, 2019.

On June 18, 2020, the Company issued a total of 20,000 shares of common stock to Crown Bridge Partners, LLC for the conversion of debt in the principal amount of $3,615.6 according to the conditions of the convertible note dated as November 12, 2019.

On July 9, 2020, the Company issued a total of 42,079 shares of common stock to Power Up Lending Group Ltd for the conversion of debt in the principal amount of $20,000 according to the conditions of the convertible note dated as July 25, 2019.

On July 13, 2020, the Company issued a total of 68,500 shares of common stock to Labrys Fund, LP for the conversion of debt in the principal amount of $37,503.75 according to the conditions of the convertible note dated as January 10, 2020.

On August 19, 2020, the Company issued a total of 222,891 shares of common stock to Power Up Lending Group Ltd for the conversion of debt in $19,000.00 of the principal amount of the Note together with $4,916.22 of accrued and unpaid interest thereto, totaling $23,916.22 according to the conditions of the convertible note dated as July 25, 2019.

On August 20,2020, the Company issued a total of 600,000 shares of common stock to Labrys Fund, LP for the conversion of debt in the principal amount of $54,180 according to the conditions of the convertible note dated as January 10, 2020. The remaining principal balance due under this convertible note after these conversions is $55,166.

On September 1, 2020, the Company issued a total of 75,000 shares of common stock to Firstfire Global Opportunities Fund LLC for the conversion of debt in the principal amount of $10,200 according to the conditions of the convertible note dated as September 11, 2019.

On September 14, 2020, the Company issued a total of 350,000 shares of common stock to Firstfire Global Opportunities Fund LLC for the conversion of debt in the principal amount of $13,550 according to the conditions of the convertible note dated as September 11, 2019.The remaining principal balance due under this convertible note after these conversions is $141,250.

| 22 |

On September 24, 2020, the Company issued a total of 568,182 shares of common stock to Morningview Financial, LLC for the conversion of debt in the principal amount of $15,000 according to the conditions of the convertible note dated as November 20, 2019.The remaining principal balance due under this convertible note after these conversions is $150,000.

On September 24, 2020, the Company issued a total of 400,000 shares of common stock to Labrys Fund, LP for the conversion of debt in the principal amount of $6,065.11 according to the conditions of the convertible note dated as January 10, 2020.

On October 12, 2020, the Company issued a total of 650,000 shares of common stock to Labrys Fund, LP for the conversion of debt in the principal amount of $14,844.39 according to the conditions of the convertible note dated as January 10, 2020.

On October 16, 2020, the Company issued a total of 181,500 shares of common stock to Labrys Fund, LP for the conversion of debt in the principal amount of $2,722.5 according to the conditions of the convertible note dated as January 10, 2020.

On October 16, 2020, the Company issued a total of 1,200,000 shares of common stock to Firstfire Global Opportunities Fund LLC for the conversion of debt in the principal amount of $14,100 according to the conditions of the convertible note dated as September 11, 2019.

On October 16, 2020, the Company issued a total of 500,000 shares of common stock to Crown Bridge Partners, LLC for the conversion of debt in the principal amount of $3,500 according to the conditions of the convertible note dated as November 12, 2019.

On October 19, 2020, the Company issued a total of 2,112,478 shares of common stock to Labrys Fund, LP for the conversion of debt in the principal amount of $31,674.16 according to the conditions of the convertible note dated as January 10, 2020.

On October 29, 2020, the Company issued a total of 2,500,000 shares of common stock to Firstfire Global Opportunities Fund LLC for the conversion of debt in the principal amount of $31,000 according to the conditions of the convertible note dated as September 11, 2019.

On December 5, 2020, the Company issued a total of 20,370,000 shares of common stock to five Chinese citizen subscribers for an aggregate purchase price of $305,500 at $0.015 per share, according to the conditions of the five subscription agreements dated as November 20, 2020 signed by the between the Company and the subscribers.

On December 21, 2020, the Company issued a total of 1,500,000 shares of common stock to FirstFire Global Opportunities Fund, LLC for the full exercise of the warrants, according to the conditions of the convertible note dated as September 11, 2019.

On December 29, 2020, the Company issued a total of 8,499,999 shares of common stock to four Chinese citizen subscribers for an aggregate purchase price of $127,500 at $0.015 per share, according to the conditions of the four subscription agreements dated as December 9, 2020 and December 28, 2020 signed by the between the Company and the subscribers.

On December 31, 2020, the Company issued a total of 447,762 shares of common stock (the “First Commitment Shares”) and 1,119,402 shares of common stock (the “Second Commitment Shares”) to Labrys Fund, LLP related to the promissory note as a commitment fee. The Second Commitment Shares must be returned to the Company’s treasury if the promissory note is fully repaid and satisfied on or prior to the maturity date.

On January 13, 2021, the Company issued a total of 7,000,000 shares of common stock to a Chinese citizen subscriber for an aggregate purchase price of $105,000 at $0.015 per share, according to the conditions of the subscription agreement dated as January 13, 2021 between the Company and the subscriber.

On March 10, 2021, the Company issued 417,000 shares of common stock (the “First Commitment Shares”) and 1,042,000 shares of common stock (the “Second Commitment Shares”) to Labrys Fund, LLP related to the promissory note as a commitment fee. The Second Commitment Shares must be returned to the Company’s treasury if the promissory note is fully repaid and satisfied on or prior to the maturity date.

On July 8, 2021, the Company issued 300,000 shares of common stock (the “First Commitment Shares”) and 1,042,000 shares of common stock (the “Second Commitment Shares”) to FirstFire Global Opportunities Fund, LLC related to the promissory note as a commitment fee. The Second Commitment Shares must be returned to the Company’s treasury if the promissory note is fully repaid and satisfied on or prior to the maturity date.

| 23 |

The sales of the above securities were exempt from registration under the Securities Act of 1933, as amended (Securities Act), in reliance upon Section 4(2) of the Securities Act, or Rule 701 promulgated under Section 3(b) of the Securities Act as transactions by an issuer not involving any public offering or pursuant to benefit plans and contracts relating to compensation as provided under Rule 701. The recipients of the securities in each of these transactions represented their intentions to acquire the securities for investment only and not with a view to or for sale in connection with any distribution thereof, and appropriate legends were placed upon the stock certificates issued in these transactions.

Exemption From Registration. The shares of Common Stock and Preferred Stock referenced herein were issued in reliance upon one of the following exemptions:

(a)The shares of Common Stock referenced herein were issued in reliance upon the exemption from securities registration afforded by the provisions of Section 4(2) of the Securities Act of 1933, as amended, ("Securities Act"), based upon the following: (a) each of the persons to whom the shares of Common Stock were issued (each such person, an "Investor") confirmed to the Company that it or he is an "accredited investor," as defined in Rule 501 of Regulation D promulgated under the Securities Act and has such background, education and experience in financial and business matters as to be able to evaluate the merits and risks of an investment in the securities, (b) there was no public offering or general solicitation with respect to the offering of such shares, (c) each Investor was provided with certain disclosure materials and all other information requested with respect to the Company, (d) each Investor acknowledged that all securities being purchased were being purchased for investment intent and were "restricted securities" for purposes of the Securities Act, and agreed to transfer such securities only in a transaction registered under the Securities Act or exempt from registration under the Securities Act and (e) a legend has been, or will be, placed on the certificates representing each such security stating that it was restricted and could only be transferred if subsequently registered under the Securities Act or transferred in a transaction exempt from registration under the Securities Act.

(b)The shares of common stock referenced herein were issued pursuant to and in accordance with Rule 506 of Regulation D and Section 4(2) of the Securities Act. We made this determination in part based on the representations of the Investor(s), which included, in pertinent part, that such Investor(s) was an “accredited investor” as defined in Rule 501(a) under the Securities Act, and upon such further representations from the Investor(s) that (a) the Investor is acquiring the securities for his, her or its own account for investment and not for the account of any other person and not with a view to or for distribution, assignment or resale in connection with any distribution within the meaning of the Securities Act, (b) the Investor agrees not to sell or otherwise transfer the purchased securities unless they are registered under the Securities Act and any applicable state securities laws, or an exemption or exemptions from such registration are available, (c) the Investor either alone or together with its representatives has knowledge and experience in financial and business matters such that he, she or it is capable of evaluating the merits and risks of an investment in us, and (d) the Investor has no need for the liquidity in its investment in us and could afford the complete loss of such investment. Our determination is made based further upon our action of (a) making written disclosure to each Investor prior to the closing of sale that the securities have not been registered under the Securities Act and therefore cannot be resold unless they are registered or unless an exemption from registration is available, (b) making written descriptions of the securities being offered, the use of the proceeds from the offering and any material changes in the Company’s affairs that are not disclosed in the documents furnished, and (c) placement of a legend on the certificate that evidences the securities stating that the securities have not been registered under the Securities Act and setting forth the restrictions on transferability and sale of the securities, and upon such inaction of the Company of any general solicitation or advertising for securities herein issued in reliance upon Rule 506 of Regulation D and Section 4(2) of the Securities Act.

(c) The shares of Common Stock referenced herein were issued pursuant to and in accordance with Rule 903 of Regulation S of the Act. We completed the offering of the shares pursuant to Rule 903 of Regulation S of the Act on the basis that the sale of the shares was completed in an "offshore transaction", as defined in Rule 902(h) of Regulation S. We did not engage in any directed selling efforts, as defined in Regulation S, in the United States in connection with the sale of the shares. Each investor represented to us that the investor was not a "U.S. person", as defined in Regulation S, and was not acquiring the shares for the account or benefit of a U.S. person. The agreement executed between us and each investor included statements that the securities had not been registered pursuant to the Act and that the securities may not be offered or sold in the United States unless the securities are registered under the Act or pursuant to an exemption from the Act. Each investor agreed by execution of the agreement for the shares: (i) to resell the securities purchased only in accordance with the provisions of Regulation S, pursuant to registration under the Act or pursuant to an exemption from registration under the Act; (ii) that we are required to refuse to register any sale of the securities purchased unless the transfer is in accordance with the provisions of Regulation S, pursuant to registration under the Act or pursuant to an exemption from registration under the Act; and (iii) not to engage in hedging transactions with regards to the securities purchased unless in compliance with the Act. All certificates representing the shares were or upon issuance will be endorsed with a restrictive legend confirming that the securities had been issued pursuant to Regulation S of the Act and could not be resold without registration under the Act or an applicable exemption from the registration requirements of the Act.

| 24 |

Purchases of Equity Securities by the Small Business Issuer and Affiliated Purchasers

None.

| Item 6. | Selected Financial Data |

We are a smaller reporting company as defined by Rule 12b-2 of the Securities Exchange Act of 1934 and are not required to provide the information under this item.

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operation |

The following discussion should be read in conjunction with our audited financial statements and notes thereto included herein. We caution readers regarding certain forward looking statements in the following discussion and elsewhere in this report and in any other statement made by, or on our behalf, whether or not in future filings with the Securities and Exchange Commission. Forward-looking statements are statements not based on historical information and which relate to future operations, strategies, financial results or other developments. Forward looking statements are necessarily based upon estimates and assumptions that are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond our control and many of which, with respect to future business decisions, are subject to change. These uncertainties and contingencies can affect actual results and could cause actual results to differ materially from those expressed in any forward looking statements made by, or our behalf. We disclaim any obligation to update forward-looking statements.

Results of Operation for the Years Ended June 30, 2021 and 2020

Calendar year 2020 and the first half of 2021 was challenging and disruptive for the world, with the COVID-19 pandemic adding to the headwind of an already challenging global economy. Almost no industry was unaffected by the pandemic. The unprecedentedly adverse global operating environment had a major impact on our business and reversed the Company's continuous growth.

The operations of the Company During the year ended June 30, 2021 experienced some minor delays and were adversely affected by the COVID-19 travel restrictions and lockdowns implemented nationwide. Decreases in revenue and operating profits during the year ended June 30, 2021 were a result of the unprecedented adverse market condition caused by the outbreak of COVID-19 pandemic since January 2020.

During the year ended June 30, 2021, the significant decrease in sales revenue is mainly attributable to the adverse impact of COVID-19 in various ways, from the continuous weakening demand in the PRC consumer market and continuous competition from other brands against the goods which the Company has been trading coupled with the unfavorable and ongoing adverse trading environment and the disruptions caused by COVID-19, limitation of marketing efforts, disruptions of product delivery to the Company’s customers due to certain customers 's reducing their budgets or delaying their procurement plans, leading to a decrease in the new orders placed with the Company. The Company believes that such effect is temporary and will not have major impact on the long-term performance of the Company.

During the year ended June 30, 2021, the gross profit decreases were mainly attributable to: (1) the drop in production volume of the Company as a result of the adverse impact of the COVID-19; (2) in certain areas in Northeast of China, the PRC government, as a preventive measure in response to the COVID-19, had implemented the movement control order which involved prohibition of movement of people which adversely affected the Company’s supply chain in raw materials. And the poor market sentiment has led to the significant drop in demand and selling prices of the Company’s products, while the prices of glass, which is the raw material for the Company's production, have increased substantially due to tightened supply of glass from the supply chain reform in the PRC; and (3) in addition to the economic contraction caused by prolonged outbreak of COVID-19, the fact that Changchun City where Fangguan Electronics was located had endured dozens of blizzards in November and December 2020, also led to the slow-down of the businesses of the Company.

Nevertheless, the Company survived and thrived against all odds: besides carrying out a more stringent cost control through the Company’s persistent effort in cost reduction, the Company implemented the workplace safety measures as per government guidelines, including work from home arrangements whenever appropriate, and protected the client relationships by maintaining communication and working with them to deal with the delaying or canceling orders. With the gradual stabilization of the domestic photoelectric display industry, the Company would anticipate a steady increase in the sales of LCM and LCD.

Based on the Company’s well-established reputation in the market, management of the Company believes that the demand for the Company's products would increase during the economic rebounding and the overall financial and business positions of the Company would remain sound, and the Company is well positioned to take advantage of any upturn in the market.

| 25 |

Considering that such effects of COVID-19 is temporary and will not have major impact on the long-term performance of the Company, the Company believes that the increase in turnover and gross profit margin of the Company as caused by the gradual recovery of the economy of PRC would maintain in the future. As such, the Company remains cautiously optimistic about its sustainable development.

During the first half of calendar year 2021, the anticipated recovery in the economy of PRC realized gradually while the negative impact of COVID-19 remains. The Company maintains optimistic cautious and is paying close attention to the evolving development of, and the disruption to business and economic activities caused by the COVID-19 outbreak and evaluates its impact on the financial position, cash flows and operating results of the Company. Given the dynamic nature of the COVID-19 outbreak, it is not practicable to provide a reasonable estimate of its impacts on the Company’s financial position, cash flows and operating results at the present.

Revenues

During the year ended June 30, 2021, COVID-19 continued to affect the operational and financial performance of the Company. However, the gradual recovery of revenue that was ever expected previously already realized.

During the year ended June 30, 2021 and 2020, total revenues were $14,328,326 and $20,599,228 respectively. The total revenues decreased by $6,270,902 or 30% from the year ended June 30, 2020 to the year ended June 30, 2021.

Among the significant decrease of $6,270,902 in total revenues for the year ended June 30, 2021, the decrease of $3,998,841 came from the decrease in revenue of Fangguan Electronics which was acquired on December 27, 2018 The decrease during the year ended June 30, 2021 can be directly attributed to the fact that in certain cities and provinces the continuous outbreak of COVID-19 induced the numerous shutdowns and commercial activities suspensions which have made the significantly adverse effects on the business of the Company. In addition, the decrease in total revenues during the year ended June 30, 2021 was partially attributed to the decreases of $2,374,200 in service contract and smart energy segments as compared with the year ended June 30, 2020.as under the negative impact of COVID-19 on service contract business, none of any new contracts were signed while majority of the existing contracts in this business segment had been completed.

The decrease in total revenues during the year ended June 30, 2021 was partially offset by the increase in revenues of $1,084,083 sourced from lithium battery - related business which was the new business segment established by the Company in 2021.

Cost of Revenue

Cost of revenues included the cost of raw materials, labor, depreciation, overhead and finished products purchased.

During the year ended June 30, 2021 and 2020, the total cost of revenues was $12,050,402 and $17,506,433 respectively. The total cost of revenues decreased by $5,456,031 or 31% from the year ended June 30, 2020 to the year ended June 30, 2021.

Among the significant decrease of $5,456,031 in total cost of revenues for the year ended June 30, 2021, the decrease of $3,649,199 came from the decrease in cost of revenue of Fangguan Electronics which was acquired on December 27, 2018. In addition, the decrease in total cost of revenues during the year ended June 30, 2021 was partially attributed to the decreases of $2,065,078 in cost of revenue of service contract and smart energy segments as compared with the year ended June 30, 2020.

The decrease in cost of revenues can be directly attributed to the decrease of revenues.

The decrease in total cost of revenues during the year ended June 30, 2021 was partially offset by the increase in cost of revenues of $982,814 sourced from lithium battery - related business which was the new business segment established by the Company in 2021.

Gross Profit

During the year ended June 30, 2021 and 2020, the gross profit was $2,277,924 and $3,092,795, respectively.

The gross profit decreased by 26% from the year ended June 30, 2020 to the year ended June 30, 2021. Our gross profit margin maintained stable as it was 15.9% during the year ended June 30, 2021 as compared to 15.0% for the year ended June 30, 2020.

| 26 |

Selling, General and Administrative Expenses

Our selling, general and administrative expenses are mainly comprised of payroll expenses, transportation, office expense, professional fees, freight and shipping costs, rent, and other miscellaneous expenses.

During the year ended June 30, 2021 and 2020, selling, general and administrative expenses were $1,372,589 and $1,937,054 respectively.

The decrease in selling, general and administrative expenses can be attributed to the stricter cost control during the year ended June 30, 2021.

Research and Development Expenses

Our research and development expenses are mainly comprised of payroll expenses of research staff, costs of materials used for research and other miscellaneous expenses.

During the year ended June 30, 2021 and 2020, research and development expenses were $598,338 and $805,570 respectively. All research and development expenses were incurred by Fangguan Electronics (a variable interest entity of the Company since December 27, 2018).

The decrease in research and development expenses during the year ended June 30, 2021 can be attributed to the decrease of materials expenditures used for research during the year ended June 30, 2021.

Other Incomes (Expenses)