UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form 10-Q

x Quarterly

Report PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the quarterly period ended December 31, 2020

or

¨ TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from

to .

Commission File Number 000-54485

IONIX TECHNOLOGY, INC.

(Exact Name of Registrant as Specified

in Its Charter)

| Nevada |

|

45-0713638 |

(State or other jurisdiction of

incorporation or organization) |

|

(I.R.S. Employer

Identification No.) |

Rm 608, Block B, Times Square,No.50

People Road, Zhongshan District, Dalian City, Liaoning Province, China 116001

(Address of Principal Executive Offices)

(Zip Code)

+86-411-88079120

(Registrant’s Telephone Number, Including

Area Code)

__Not applicable_

(Former Name, Former Address and Former

Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding

12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§

232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit

such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated

filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions

of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging

growth company” in Rule 12b-2 of the Exchange Act.

| |

Large accelerated filer ¨ |

Accelerated filer ¨ |

| |

Non-accelerated filer x |

Smaller reporting company x |

| |

Emerging growth company ¨ |

|

If an emerging growth company, indicate by check mark if the

registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards

provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company

(as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x.

Securities registered pursuant to Section

12(b) of the Act: None

| Title of each class |

Trading Symbol(s) |

Name of the principal U.S. market |

| Common

Stock, par value $0.0001 per share |

IINX |

OTCQB marketplace of OTC Markets, Inc. |

Indicate the number of shares outstanding of each of the issuer’s

classes of common stock, as of the latest practicable date: As of February 14, 2021, there were 162,582,058 shares of common stock

issued and outstanding, par value $0.0001 per share.

SPECIAL NOTE REGARDING FORWARD-LOOKING

STATEMENTS

Certain information included in this Quarterly

Report on Form 10-Q and other filings of the Registrant under the Securities Act of 1933, as amended (the “Securities Act”),

and the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as well as information communicated orally

or in writing between the dates of such filings, contains or may contain “forward-looking statements” within the meaning

of Section 27A of the Securities Act and Section 21E of the Exchange Act. Forward-looking statements in this Quarterly Report on

Form 10-Q, including without limitation, statements related to our plans, strategies, objectives, expectations, intentions and

adequacy of resources, are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995.

Such statements are subject to certain risks, trends and uncertainties that could cause actual results to differ materially from

expected results. Among these risks, trends and uncertainties are the availability of working capital to fund our operations, the

competitive market in which we operate, the efficient and uninterrupted operation of our computer and communications systems, our

ability to generate a profit and execute our business plan, the retention of key personnel, our ability to protect and defend our

intellectual property, the effects of governmental regulation, and other risks identified in the Registrant’s filings with

the Securities and Exchange Commission from time to time.

In some cases, forward-looking statements

can be identified by terminology such as “may,” “will,” “should,” “could,” “expects,”

“plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential”

or “continue” or the negative of such terms or other comparable terminology. Although the Registrant believes that

the expectations reflected in the forward-looking statements contained herein are reasonable, the Registrant cannot guarantee future

results, levels of activity, performance or achievements. Moreover, neither the Registrant, nor any other person, assumes responsibility

for the accuracy and completeness of such statements. The Registrant is under no duty to update any of the forward-looking statements

contained herein after the date of this Quarterly Report on Form 10-Q.

IONIX TECHNOLOGY, INC.

FORM 10-Q

December 31, 2020

INDEX

| |

|

Page |

| Part I - Financial Information |

F-1 |

| |

|

|

| Item 1. |

Financial Statements (Unaudited) |

F-1 |

| Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operation |

33 |

| Item 3. |

Quantitative and Qualitative Disclosures about Market Risk |

43 |

| Item 4. |

Controls and Procedures |

44 |

| |

|

|

| Part II - Other Information |

45 |

| |

|

|

| Item 1. |

Legal Proceedings |

45 |

| Item 1A. |

Risk Factors |

45 |

| Item 2. |

Unregistered Sales of Equity Securities and Use of Proceeds |

45 |

| Item 3. |

Defaults Upon Senior Securities |

50 |

| Item 4. |

Mine Safety Disclosures |

50 |

| Item 5. |

Other Information |

50 |

| Item 6. |

Exhibits |

51 |

| |

|

|

| Signatures |

53 |

| |

|

|

| Certifications |

|

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements.

IONIX TECHNOLOGY, INC.

CONSOLIDATED BALANCE SHEETS

(Unaudited)

| | |

December 31, 2020 | | |

June 30, 2020 | |

| ASSETS | |

| | |

| |

| Current Assets: | |

| | |

| |

| Cash and cash equivalents | |

$ | 1,121,104 | | |

$ | 1,285,373 | |

| Notes receivable | |

| 35,320 | | |

| 125,798 | |

| Accounts receivable | |

| 3,350,910 | | |

| 3,273,141 | |

| Inventory | |

| 3,565,448 | | |

| 3,263,850 | |

| Advances to suppliers - non-related parties | |

| 657,592 | | |

| 540,259 | |

| - related parties | |

| 429,264 | | |

| 357,577 | |

| Prepaid expenses and other current assets | |

| 370,150 | | |

| 320,296 | |

| Total Current Assets | |

| 9,529,788 | | |

| 9,166,294 | |

| | |

| | | |

| | |

| Property, plant and equipment, net | |

| 7,001,152 | | |

| 6,573,937 | |

| Intangible assets, net | |

| 1,508,762 | | |

| 1,424,404 | |

| Deferred tax assets | |

| 47,778 | | |

| 20,743 | |

| Total Assets | |

$ | 18,087,480 | | |

$ | 17,185,378 | |

| | |

| | | |

| | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |

| | | |

| | |

| Current Liabilities: | |

| | | |

| | |

| Short-term bank loan | |

$ | 1,681,906 | | |

$ | 2,034,735 | |

| Accounts payable | |

| 2,455,750 | | |

| 2,637,792 | |

| Advance from customers | |

| 206,666 | | |

| 43,077 | |

| Promissory notes payable, net of debt discount and loan cost | |

| 186,714 | | |

| - | |

| Convertible notes payable, net of debt discount and loan cost | |

| - | | |

| 514,390 | |

| Derivative liability | |

| - | | |

| 276,266 | |

| Due to related parties | |

| 2,535,927 | | |

| 1,716,919 | |

| Accrued expenses and other current liabilities | |

| 55,099 | | |

| 359,577 | |

| Total Current Liabilities | |

| 7,122,062 | | |

| 7,582,756 | |

| Total Liabilities | |

| 7,122,062 | | |

| 7,582,756 | |

| | |

| | | |

| | |

| COMMITMENT AND CONTINGENCIES | |

| | | |

| | |

| | |

| | | |

| | |

| Stockholders’ Equity: | |

| | | |

| | |

Preferred stock, $.0001 par value, 5,000,000 shares authorized,

5,000,000 shares issued and outstanding | |

| 500 | | |

| 500 | |

Common stock, $.0001 par value, 195,000,000 shares authorized,

155,582,058 and 114,174,265 shares issued and outstanding as of December 31,

2020 and June 30, 2020 respectively | |

| 15,558 | | |

| 11,417 | |

| Additional paid in capital | |

| 10,595,485 | | |

| 9,243,557 | |

| Retained earnings (accumulated deficit) | |

| (626,226 | ) | |

| 262,198 | |

| Accumulated other comprehensive income (loss) | |

| 538,140 | | |

| (357,011 | ) |

| Total Stockholders' Equity attributable to the Company | |

| 10,523,457 | | |

| 9,160,661 | |

| Noncontrolling interest | |

| 441,961 | | |

| 441,961 | |

| Total Stockholders’ Equity | |

| 10,965,418 | | |

| 9,602,622 | |

| Total Liabilities and Stockholders’ Equity | |

$ | 18,087,480 | | |

$ | 17,185,378 | |

The accompanying notes are an integral part of these consolidated

financial statements.

IONIX TECHNOLOGY, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

| | |

For the Three Months Ended | | |

For the Six Months Ended | |

| | |

December 31, | | |

December 31, | |

| | |

2020 | | |

2019 | | |

2020 | | |

2019 | |

| | |

| | |

| | |

| | |

| |

| Revenues (See Note 3 and Note 11 for related party amounts) | |

$ | 2,982,883 | | |

$ | 7,332,968 | | |

$ | 5,941,348 | | |

$ | 14,833,298 | |

| | |

| | | |

| | | |

| | | |

| | |

| Cost of Revenues (See Note 11 for related party amounts) | |

| 2,588,055 | | |

| 6,270,572 | | |

| 5,269,444 | | |

| 12,343,676 | |

| | |

| | | |

| | | |

| | | |

| | |

| Gross profit | |

| 394,828 | | |

| 1,062,396 | | |

| 671,904 | | |

| 2,489,622 | |

| | |

| | | |

| | | |

| | | |

| | |

| Operating expenses | |

| | | |

| | | |

| | | |

| | |

| Selling, general and administrative expense | |

| 349,398 | | |

| 497,197 | | |

| 657,901 | | |

| 878,625 | |

| Research and development expense | |

| 131,055 | | |

| 284,028 | | |

| 277,240 | | |

| 506,851 | |

| Total operating expenses | |

| 480,453 | | |

| 781,225 | | |

| 935,141 | | |

| 1,385,476 | |

| | |

| | | |

| | | |

| | | |

| | |

| Income (loss) from operations | |

| (85,625 | ) | |

| 281,171 | | |

| (263,237 | ) | |

| 1,104,146 | |

| | |

| | | |

| | | |

| | | |

| | |

| Other income (expense): | |

| | | |

| | | |

| | | |

| | |

| Interest expense, net of interest income | |

| (45,499 | ) | |

| (200,370 | ) | |

| (219,733 | ) | |

| (257,233 | ) |

| Subsidy income | |

| 922 | | |

| 7,231 | | |

| 14,086 | | |

| 50,018 | |

| Change in fair value of derivative liability | |

| (586,980 | ) | |

| 115,563 | | |

| (647,632 | ) | |

| 131,452 | |

| Gain on extinguishment of debt | |

| 351,819 | | |

| - | | |

| 202,588 | | |

| - | |

| Total other expense | |

| (279,738 | ) | |

| (77,576 | ) | |

| (650,691 | ) | |

| (75,763 | ) |

| | |

| | | |

| | | |

| | | |

| | |

| Income (loss) before income tax provision (benefit) | |

| (365,363 | ) | |

| 203,595 | | |

| (913,928 | ) | |

| 1,028,383 | |

| Income tax provision (benefit) | |

| (9,245 | ) | |

| 67,937 | | |

| (25,504 | ) | |

| 181,449 | |

| Net income (loss) | |

| (356,118 | ) | |

| 135,658 | | |

| (888,424 | ) | |

| 846,934 | |

| | |

| | | |

| | | |

| | | |

| | |

| Other comprehensive income (loss) | |

| | | |

| | | |

| | | |

| | |

| Foreign currency translation adjustment | |

| 464,870 | | |

| 255,703 | | |

| 895,151 | | |

| (161,082 | ) |

| Comprehensive income | |

$ | 108,752 | | |

$ | 391,361 | | |

$ | 6,727 | | |

$ | 685,852 | |

| | |

| | | |

| | | |

| | | |

| | |

| Earnings (Loss) Per Share - Basic and Diluted | |

$ | (0.00 | ) | |

$ | 0.00 | | |

$ | (0.01 | ) | |

$ | 0.01 | |

| Weighted average number of common shares outstanding - Basic and Diluted | |

| 128,017,085 | | |

| 114,003,000 | | |

| 121,402,466 | | |

| 114,003,000 | |

The accompanying notes are an integral part of these consolidated

financial statements.

IONIX TECHNOLOGY, INC.

CONSOLIDATED STATEMENTS

OF STOCKHOLDERS' EQUITY

(Unaudited)

| | |

Preferred

Stock | | |

Common

Stock | | |

Additional | | |

Retained

Earnings | | |

Accumulated

Other | | |

| | |

| |

| | |

Number

of

Shares | | |

Amount | | |

Number

of

Shares | | |

Amount | | |

Paid-in

Capital | | |

(Accumulated

Deficit) | | |

Comprehensive

Income (loss) | | |

Non-controlling

interest | | |

Total | |

| Balance at June 30, 2020 | |

| 5,000,000 | | |

$ | 500 | | |

| 114,174,265 | | |

$ | 11,417 | | |

$ | 9,243,557 | | |

$ | 262,198 | | |

$ | (357,011 | ) | |

$ | 441,961 | | |

$ | 9,602,622 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

Issuance of common stock for conversion of

convertible notes | |

| - | | |

| - | | |

| 2,326,652 | | |

| 233 | | |

| 390,768 | | |

| - | | |

| - | | |

| - | | |

| 391,001 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net loss | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (532,306 | ) | |

| - | | |

| - | | |

| (532,306 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Foreign currency translation adjustment | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 430,281 | | |

| - | | |

| 430,281 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance at September 30, 2020 | |

| 5,000,000 | | |

| 500 | | |

| 116,500,917 | | |

| 11,650 | | |

| 9,634,325 | | |

| (270,108 | ) | |

| 73,270 | | |

| 441,961 | | |

| 9,891,598 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

Issuance of common stock for conversion of

convertible notes | |

| - | | |

| - | | |

| 7,143,978 | | |

| 714 | | |

| 455,429 | | |

| - | | |

| - | | |

| - | | |

| 456,143 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

Issuance of common stock for exercise of

warrants | |

| - | | |

| - | | |

| 1,500,000 | | |

| 150 | | |

| 66,878 | | |

| - | | |

| - | | |

| - | | |

| 67,028 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

Issuance of common stock as commitment

shares for promissory note | |

| - | | |

| - | | |

| 1,567,164 | | |

| 157 | | |

| 67,903 | | |

| - | | |

| - | | |

| - | | |

| 68,060 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

Issuance of common stock for private

placement | |

| - | | |

| - | | |

| 28,869,999 | | |

| 2,887 | | |

| 430,113 | | |

| - | | |

| - | | |

| - | | |

| 433,000 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

Settlement of warrants in relation to

extinguishment of debt | |

| - | | |

| - | | |

| - | | |

| - | | |

| (59,163 | ) | |

| - | | |

| - | | |

| - | | |

| (59,163 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net loss | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (356,118 | ) | |

| - | | |

| - | | |

| (356,118 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Foreign currency translation adjustment | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 464,870 | | |

| - | | |

| 464,870 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance at December

31, 2020 | |

| 5,000,000 | | |

$ | 500 | | |

| 155,582,058 | | |

$ | 15,558 | | |

$ | 10,595,485 | | |

$ | (626,226 | ) | |

$ | 538,140 | | |

$ | 441,961 | | |

$ | 10,965,418 | |

The

accompanying notes are an integral part of these consolidated financial statements.

IONIX TECHNOLOGY, INC.

CONSOLIDATED STATEMENTS

OF STOCKHOLDERS' EQUITY (continued)

(Unaudited)

| | |

Preferred

Stock | | |

Common

Stock | | |

Additional | | |

| | |

Accumulated

Other | | |

| | |

| |

| | |

Number

of

Shares | | |

Amount | | |

Number

of

Shares | | |

Amount | | |

Paid-in

Capital | | |

Retained

Earnings | | |

Comprehensive

Income (loss) | | |

Non-controlling

interest | | |

Total | |

| Balance at June 30, 2019 | |

| 5,000,000 | | |

$ | 500 | | |

| 114,003,000 | | |

$ | 11,400 | | |

$ | 8,829,487 | | |

$ | 539,866 | | |

$ | (45,840 | ) | |

$ | 441,961 | | |

$ | 9,777,374 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Stock warrants issued with convertible notes | |

| - | | |

| - | | |

| - | | |

| - | | |

| 20,022 | | |

| - | | |

| - | | |

| - | | |

| 20,022 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net income | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 711,276 | | |

| - | | |

| - | | |

| 711,276 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Foreign currency translation adjustment | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (416,785 | ) | |

| - | | |

| (416,785 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance at September 30, 2019 | |

| 5,000,000 | | |

| 500 | | |

| 114,003,000 | | |

| 11,400 | | |

| 8,849,509 | | |

| 1,251,142 | | |

| (462,625 | ) | |

| 441,961 | | |

| 10,091,887 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Stock warrants issued with convertible notes | |

| - | | |

| - | | |

| - | | |

| - | | |

| 84,613 | | |

| - | | |

| - | | |

| - | | |

| 84,613 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net income | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 135,658 | | |

| - | | |

| - | | |

| 135,658 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Foreign currency translation adjustment | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 255,703 | | |

| - | | |

| 255,703 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance at December

31, 2019 | |

| 5,000,000 | | |

$ | 500 | | |

| 114,003,000 | | |

$ | 11,400 | | |

$ | 8,934,122 | | |

$ | 1,386,800 | | |

$ | (206,922 | ) | |

$ | 441,961 | | |

$ | 10,567,861 | |

The accompanying notes are

an integral part of these consolidated financial statements.

IONIX TECHNOLOGY, INC.

CONSOLIDATED STATEMENTS

OF CASH FLOWS

(Unaudited)

| | |

For the Six

Months Ended | |

| | |

December 31, | |

| | |

2020 | | |

2019 | |

| CASH FLOWS FROM OPERATING ACTIVITIES | |

| | |

| |

| Net income (loss) | |

$ | (888,424 | ) | |

$ | 846,934 | |

Adjustments required to reconcile net income

(loss) to net cash provided by (used in) operating

activities: | |

| | | |

| | |

| Depreciation and amortization | |

| 335,067 | | |

| 399,080 | |

| Deferred taxes | |

| (24,322 | ) | |

| 28,879 | |

| Change in fair value of

derivative liability | |

| 647,632 | | |

| (131,452 | ) |

| Gain on extinguishment of

debt | |

| (202,588 | ) | |

| - | |

| Non-cash interest | |

| 139,673 | | |

| 181,336 | |

| Changes in operating assets and liabilities: | |

| | | |

| | |

| Accounts receivable - non-related

parties | |

| 184,522 | | |

| (1,606,240 | ) |

| Accounts receivable - related

parties | |

| - | | |

| (11,500 | ) |

| Inventory | |

| (31,178 | ) | |

| 323,148 | |

| Advances to suppliers -

non-related parties | |

| (69,901 | ) | |

| 37,082 | |

| Advances to suppliers -

related parties | |

| (40,530 | ) | |

| 120,295 | |

| Prepaid expenses and other

current assets | |

| (22,753 | ) | |

| (161,718 | ) |

| Accounts payable | |

| (383,729 | ) | |

| 729,495 | |

| Advance from customers | |

| 153,698 | | |

| (8,120 | ) |

| Accrued

expenses and other current liabilities | |

| (271,108 | ) | |

| (158,651 | ) |

| Net

cash provided by (used in) operating activities | |

| (473,941 | ) | |

| 588,568 | |

| | |

| | | |

| | |

| CASH FLOWS FROM INVESTING

ACTIVITIES | |

| | | |

| | |

| Acquisition of property,

plant and equipment | |

| (190,623 | ) | |

| (190,675 | ) |

| Acquisition

of intangible assets | |

| (2,339 | ) | |

| - | |

| Net

cash used in investing activities | |

| (192,962 | ) | |

| (190,675 | ) |

| | |

| | | |

| | |

| CASH FLOWS FROM FINANCING

ACTIVITIES | |

| | | |

| | |

| Notes receivable | |

| 96,857 | | |

| 95,582 | |

| Proceeds from bank loans | |

| 1,408,992 | | |

| - | |

| Repayment of bank loans | |

| (1,908,985 | ) | |

| - | |

| Proceeds from issuance of

convertible notes payable | |

| - | | |

| 585,190 | |

| Proceeds from issuance of

promissory note | |

| 253,500 | | |

| - | |

| Proceeds from issuance of

common stock for private placement | |

| 433,000 | | |

| - | |

| Repayment of convertible

notes payable | |

| (555,747 | ) | |

| - | |

| Proceeds

from loans from related parties | |

| 679,438 | | |

| 2,789 | |

| Net

cash provided by financing activities | |

| 407,055 | | |

| 683,561 | |

| | |

| | | |

| | |

| Effect of exchange rate

changes on cash | |

| 95,579 | | |

| (13,367 | ) |

| | |

| | | |

| | |

| Net increase (decrease) in cash and cash equivalents | |

| (164,269 | ) | |

| 1,068,087 | |

| | |

| | | |

| | |

| Cash and cash equivalents, beginning of period | |

| 1,285,373 | | |

| 509,615 | |

| | |

| | | |

| | |

| Cash and cash equivalents,

end of period | |

$ | 1,121,104 | | |

$ | 1,577,702 | |

| | |

| | | |

| | |

| Supplemental disclosure

of cash flow information | |

| | | |

| | |

| Cash paid for income tax | |

$ | 10,776 | | |

$ | 102,167 | |

| Cash paid for interests | |

$ | 66,972 | | |

$ | 68,967 | |

| | |

| | | |

| | |

| Non-cash investing and financing

activities | |

| | | |

| | |

| Issuance of 9,470,630 shares

of common stock for conversion of convertible notes | |

$ | 847,144 | | |

$ | - | |

| Issuance of 1,500,000 shares of common stock

for exercise of warrants | |

$ | 67,028 | | |

$ | - | |

| Issuance of 1,567,164 shares

of common stock as commitment shares for promissory note | |

$ | 68,060 | | |

$ | - | |

The accompanying notes are

an integral part of these consolidated financial statements.

IONIX TECHNOLOGY, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

December 31, 2020

(Unaudited)

NOTE 1 - NATURE OF OPERATIONS

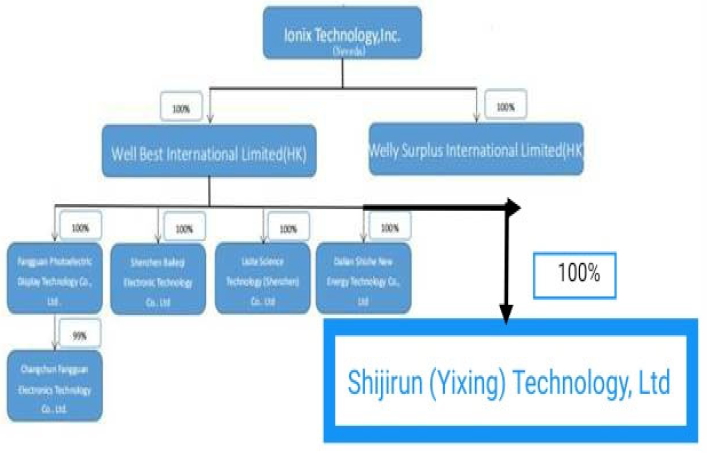

Ionix Technology,

Inc. (the “Company” or “Ionix”), formerly known as Cambridge Projects Inc., is a Nevada corporation that

was formed on March 11, 2011. By and through its wholly owned subsidiaries and an entity controlled through VIE agreements

in China, the Company sells the high-end intelligent electronic equipment, which includes the portable power banks for electronic

devices, LCM and LCD screens and provides IT and solution-oriented services in China.

Acquisition

On December 27, 2018, the Company entered into a Share

Purchase Agreement (the “Purchase Agreement”) with Jialin Liang and Xuemei Jiang, each of whom are shareholders (the

“Shareholders”) of Changchun Fangguan Electronics Technology Co., Ltd. (“Fangguan Electronics”). Pursuant

to the terms of the Purchase Agreement, the Shareholders, who together own 95.14% of the ownership rights in Fangguan Electronics,

agreed to execute and deliver the Business Operation Agreement, the Equity Interest Pledge Agreement, the Equity Interest Purchase

Agreement, the Exclusive Technical Support Service Agreement (the “Services Agreement”) and the Power of Attorney,

all together dated December 27, 2018 are referred to the “VIE Agreements”, to the Company in exchange for the issuance

of an aggregate of 15,000,000 shares of the Company’s common stock, par value $.0001 per share, thereby causing Fangguan

Electronics to become the Company’s variable interest entity. Together with VIE agreements, the Shareholders also agreed

to convert shareholder loan of RMB 30 million (approximately $4.4 million) to capital and make cash contribution of RMB 9.7 million

(approximately $1.4 million) to capital. The entirety of the transaction will hereafter be referred to as the “Transaction”.

As a result of the Transaction, the Company is able to exert effective control over Fangguan Electronics and receive 100% of the

net profits or net losses derived from the business operations of Fangguan Electronics. Fangguan Electronics manufactures and sells

Liquid Crystal Module (" LCM") and LCD screens in China based in Changchun City, Jilin Province, People’s Republic

of China. (See Note 4).

The Transaction was accounted for as a business combination

using the acquisition method of accounting. The assets, liabilities and the operations of Fangguan Electronics subsequent to the

Transaction date were included in the Company’s consolidated financial statements.

NOTE 2 - GOING CONCERN

The accompanying consolidated financial statements have

been prepared assuming that the Company will continue as a going concern. The Company had an accumulated deficit of $626,226 as

of December 31, 2020. The Company incurred loss from operation and did not generate sufficient cash flow from its operating activities

for the six months ended December 31, 2020. These factors, among others, raise substantial doubt about the Company’s ability

to continue as a going concern. The consolidated financial statements do not include any adjustments that might result from the

outcome of this uncertainty.

The Company plans to rely on the proceeds from loans

from both unrelated and related parties to provide the resources necessary to fund the development of the business plan and operations. The

Company is also pursuing other revenue streams which could include strategic acquisitions or possible joint ventures of other business

segments. However, no assurance can be given that the Company will be successful in raising additional capital.

NOTE 3 – BASIS OF PRESENTATION AND SUMMARY OF

SIGNIFICANT ACCOUNTING POLICIES

Basis of presentation

The unaudited consolidated financial statements have

been prepared in accordance with accounting principles generally accepted in the United States for interim financial information

and the rules and regulations of the Securities and Exchange Commission. In the opinion of management, the unaudited consolidated

financial statements have been prepared on the same basis as the annual consolidated financial statements and reflect all adjustments,

which include only normal recurring adjustments, necessary to present fairly the financial position as of December 31, 2020 and

the results of operations and cash flows for the periods ended December 31, 2020 and 2019. The financial data and other information

disclosed in these notes to the interim financial statements related to these periods are unaudited. The results for the three

and six months ended December 31, 2020 are not necessarily indicative of the results to be expected for the entire year ending

June 30, 2021 or for any subsequent periods. The balance sheet at June 30, 2020 has been derived from the audited consolidated

financial statements at that date.

Certain information and footnote disclosures normally

included in financial statements prepared in accordance with accounting principles generally accepted in the United States have

been condensed or omitted pursuant to the Securities and Exchange Commission's rules and regulations. These unaudited consolidated

financial statements should be read in conjunction with our audited consolidated financial statements and notes thereto for the

year ended June 30, 2020 as included in our Annual Report on Form 10-K as filed with the SEC on September 28, 2020.

Basis of consolidation

The consolidated financial statements include the accounts

of Ionix, its wholly owned subsidiaries and an entity which the Company controls 95.14% and receives 100% of net income or net

loss through VIE agreements. All significant inter-company balances and transactions have been eliminated upon consolidation.

Noncontrolling Interests

The Company follows FASB ASC Topic 810,

“Consolidation,” governing the accounting for and reporting of noncontrolling interests (“NCIs”) in partially

owned consolidated subsidiaries and the loss of control of subsidiaries. Certain provisions of this standard indicate, among other

things, that NCIs (previously referred to as minority interests) be treated as a separate component of equity, not as a liability,

that increases and decreases in the parent’s ownership interest that leave control intact be treated as equity transactions

rather than as step acquisitions or dilution gains or losses, and that losses of a partially-owned consolidated subsidiary be allocated

to NCIs even when such allocation might result in a deficit balance.

The net income (loss) attributed to NCIs

was separately designated in the accompanying statements of comprehensive income (loss). Losses attributable to NCIs in a subsidiary

may exceed an NCI’s interests in the subsidiary’s equity. The excess attributable to NCIs is attributed to those interests.

NCIs shall continue to be attributed their share of losses even if that attribution results in a deficit NCI balance. The Primary

beneficiary receives 100% of the income and losses of the VIE as disclosed in Note 4, therefore no income or loss is allocated

to NCI.

Use of Estimates

The Company’s consolidated financial statements

have been prepared in accordance with US GAAP and this requires management to make estimates and assumptions that affect the reported

amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial

statements and reported amounts of revenue and expenses during the reporting period. The significant areas requiring the use of

management estimates include, but are not limited to, the allowance for doubtful accounts receivable and advance to suppliers,

the valuation of inventory, provision for staff benefit, recognition and measurement of deferred income taxes and valuation allowance

for deferred tax assets. Although these estimates are based on management’s knowledge of current events and actions management

may undertake in the future, actual results may ultimately differ from those estimates and such differences may be material to

our consolidated financial statements.

Cash and cash equivalents

Cash consists of cash on hand and cash in bank. Cash

equivalents represent investment securities that are short-term, have high credit quality and are highly liquid. Cash equivalents

are carried at fair market value and consist primarily of money market funds.

Accounts Receivable

Accounts receivable are recorded at the invoiced amount

and do not bear interest, which are due within contractual payment terms, generally 30 to 90 days from shipment. Credit is extended

based on evaluation of a customer's financial condition, the customer’s credit-worthiness and their payment history. Accounts

receivable outstanding longer than the contractual payment terms are considered past due. Past due balances over 90 days and over

a specified amount are reviewed individually for collectability. At the end of each period, the Company specifically evaluates

individual customer’s financial condition, credit history, and the current economic conditions to monitor the progress of

the collection of accounts receivables. The Company will consider the allowance for doubtful accounts for any estimated losses

resulting from the inability of its customers to make required payments. For the receivables that are past due or not being paid

according to payment terms, the appropriate actions may be taken to exhaust all means of collection, including seeking legal resolution

in a court of law. Account balances are charged off against the allowance after all means of collection have been exhausted and

the potential for recovery is considered remote. The Company does not have any off-balance-sheet credit exposure related to its

customers. As of December 31, 2020 and June 30, 2020, the Company has accounts receivable balance from non-related party of $3,350,910

and $3,273,141, net of allowance for doubtful accounts of $151,121 and $139,609, respectively. No bad debt expense was recorded

during the three and six months ended December 31, 2020 and 2019.

Inventories

Inventories consist of raw materials, working-in-process

and finished goods. Inventories are valued at the lower of cost or net realizable value. We determine cost on the basis of the

weighted average method. The Company periodically reviews inventories for obsolescence and any inventories identified as obsolete

are written down or written off. Although we believe that the assumptions we use to estimate inventory write-downs are reasonable,

future changes in these assumptions could provide a significantly different result.

Advances to suppliers

Advances to suppliers represent prepayments for merchandise,

which were purchased but had not been received. The balance of the advances to suppliers is reduced and reclassified to inventories

when the raw materials are received and pass quality inspection.

Property, plant and equipment

Property, plant and equipment are recorded at cost less

accumulated depreciation and any impairment. The cost of an asset comprises its purchase price and any directly attributable costs

of bringing the asset to its present working condition and location for its intended use. Repairs and maintenance costs are normally

expensed as incurred. In situations where it can be clearly demonstrated that the expenditure has resulted in an increase in the

future economic benefits expected to be obtained from the use of the asset, the expenditure is capitalized as an additional cost

of the asset.

When assets are retired or disposed of, the cost and

accumulated depreciation are removed from the accounts, and any resulting gains or losses are included in the statement of comprehensive

income (loss) in the reporting period of disposition.

Depreciation is calculated on a straight-line basis over

the estimated useful life of the assets after taking into account their respective estimated residual value. The estimated useful

life of the assets is as follows:

| Buildings | |

10 – 20 years |

| Machinery and equipment | |

5 – 10 years |

| Office equipment | |

3 – 5 years |

| Automobiles | |

5 years |

Intangible assets

Land use right is recorded as cost less accumulated amortization.

Land use rights represent the prepayments for the use of the parcels of land in the PRC where the Company’s production facilities

are located, and are charged to expense over their respective lease periods of 50 years. According to the laws of the PRC, the

government owns all of the land in the PRC. Company or individuals are authorized to use the land only through land use rights

granted by the PRC government for a certain period (usually 50 years).

Purchased intangible assets are recognized and measured

at fair value upon acquisition. Intangible assets acquired separately and with finite useful lives are carried at costs less accumulated

amortization and any accumulated impairment losses. Amortization for intangible assets with finite useful lives is provided on

a straight-line basis over their estimated useful lives. Alternatively, intangible assets with indefinite useful lives are carried

at cost less any subsequent accumulated impairment losses. The estimated useful lives of the intangible assets are as follows:

| Land use right |

|

50 years |

| Computer software |

|

2-5 years |

Gains or losses arising from derecognition of the intangible

asset are measured at the difference between the net disposal proceeds and the carrying amount of the assets and are recognized

in the statement of comprehensive income (loss) when the asset is disposed.

Impairment of long-lived assets

In accordance with the provisions of ASC Topic 360, “Impairment

or Disposal of Long-Lived Assets”, all long-lived assets such as property, plant and equipment held and used by the Company

are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be

recoverable. Recoverability of assets to be held and used is evaluated by a comparison of the carrying amount of an asset to its

estimated future undiscounted cash flows expected to be generated by the asset. If such assets are considered to be impaired, the

impairment to be recognized is measured by the amount by which the carrying amounts of the assets exceed the fair value of the

assets.

Revenue recognition

The Company adopted the new accounting standard, ASC

606, Revenue from Contracts with Customers, and all the related amendments (new revenue standard) to all contracts using the modified

retrospective method beginning on July 1, 2018. The adoption did not result in an adjustment to the retained earnings as of June

30, 2018. The comparative information was not restated and continued to be reported under the accounting standards in effect for

those periods. The adoption of the new revenue standard has no impact on either reported sales to customers or net earnings.

The Company estimates return based on historical results,

taking into consideration the type of customers, the type of transactions and the specifics of each arrangement.

Revenues are recognized when control of the promised

goods or services are transferred to a customer, in an amount that reflects the consideration that the Company expects to receive

in exchange for those goods or services. The Company applies the following five steps in order to determine the appropriate amount

of revenue to be recognized as it fulfills its obligations under each of its agreements:

| · | identify the contract with a customer; |

| · | identify the performance obligations in the contract; |

| · | determine the transaction price; |

| · | allocate the transaction price to performance obligations in the contract; and |

| · | recognize revenue as the performance obligation is satisfied. |

Under these criteria, for revenues from sale of products,

the Company generally recognizes revenue when its products are delivered to customers in accordance with the written sales terms.

The control of the products is transferred to the customer upon receipt of goods by the customer. For service revenue, the Company

recognizes revenue when services are performed and accepted by customers.

The following tables disaggregate our revenue by major

source for the three and six months ended December 31, 2020 and 2019, respectively:

| | |

For the Six Months Ended December 31, | |

| | |

2020 | | |

2019 | |

| Sales of LCM and LCD screens - Non-related parties | |

$ | 5,939,602 | | |

$ | 12,030,911 | |

| Sales of LCM and LCD screens - Related parties | |

| - | | |

| 644,392 | |

| Sales of portable power banks | |

| - | | |

| 1,538,094 | |

| Service contracts | |

| 1,746 | | |

| 619,901 | |

| Total | |

$ | 5,941,348 | | |

$ | 14,833,298 | |

| | |

For the Three Months Ended December 31, | |

| | |

2020 | | |

2019 | |

| Sales of LCM and LCD screens - Non-related parties | |

$ | 2,982,577 | | |

$ | 5,864,945 | |

| Sales of LCM and LCD screens - Related parties | |

| - | | |

| 330,435 | |

| Sales of portable power banks | |

| - | | |

| 910,391 | |

| Service contracts | |

| 306 | | |

| 227,197 | |

| Total | |

$ | 2,982,883 | | |

$ | 7,332,968 | |

All the operating entities of the Company are domiciled

in the PRC. All the Company’s revenues are derived in the PRC during the three and six months ended December 31, 2020 and

2019.

Cost of revenues

Cost of revenues includes cost of raw materials purchased,

inbound freight cost, cost of direct labor, depreciation expense and other overhead. Write-down of inventory for lower of cost

or net realizable value adjustments is also recorded in cost of revenues.

Related parties and transactions

The Company identifies related parties, and accounts

for, discloses related party transactions in accordance with ASC 850, "Related Party Disclosures" and other relevant

ASC standards.

Parties, which can be a corporation or individual, are

considered to be related if the Company has the ability, directly or indirectly, to control the other party or exercise significant

influence over the other party in making financial and operational decisions. Companies are also considered to be related if they

are subject to common control or common significant influence.

Transactions between related parties commonly occurring

in the normal course of business are considered to be related party transactions. Transactions between related parties are also

considered to be related party transactions even though they may not be given accounting recognition. While ASC does not provide

accounting or measurement guidance for such transactions, it requires their disclosure nonetheless.

Income taxes

Income taxes are determined in accordance with the provisions

of ASC Topic 740, “Income Taxes” (“ASC 740”). Under this method, deferred tax assets and liabilities are

recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing

assets and liabilities and their respective tax basis. Deferred tax assets and liabilities are measured using enacted income tax

rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled.

Any effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period that includes

the enactment date.

ASC 740 prescribes a comprehensive model for how companies

should recognize, measure, present, and discloses in their financial statements uncertain tax positions taken or expected to be

taken on a tax return. Under ASC 740, tax positions must initially be recognized in the financial statements when it is more likely

than not the position will be sustained upon examination by the tax authorities. Such tax positions must initially and subsequently

be measured as the largest amount of tax benefit that has a greater than 50% likelihood of being realized upon ultimate settlement

with the tax authority assuming full knowledge of the position and relevant facts.

As of December 31, 2020 and June 30, 2020, the Company

did not have any significant unrecognized uncertain tax positions.

Comprehensive income (loss)

Comprehensive income (loss) is defined as the change

in equity of a company during a period from transactions and other events and circumstances excluding transactions resulting from

investments from owners and distributions to owners. Comprehensive income (loss) for the periods presented includes net income

(loss), change in unrealized gains (losses) on marketable securities classified as available-for-sale (net of tax), foreign currency

translation adjustments, and share of change in other comprehensive income of equity investments one quarter in arrears.

Leases

In February 2016, the FASB established Topic 842, Leases,

by issuing Accounting Standards Update (ASU) No. 2016-02, which requires lessees to recognize leases on balance sheet and disclose

key information about the leasing arrangements. The new standard establishes a right-of-use model (“ROU”) that requires

a lessee to recognize a ROU asset and lease liability on the balance sheet for all leases with a term longer than 12 months.

The new standard is effective for us on July 1, 2019,

with early adoption permitted. An entity may choose to use either (1) its effective date or (2) the beginning of the earliest comparative

period presented in the financial statements as its date of initial application. The Company adopted the new standard on July 1,

2019 and use the effective date as our date of initial application. Consequently, financial information is not provided for the

dates and periods before July 1, 2019. The new standard provides a number of optional expedients in transition. The Company elected

the package of practical expedients which permits us not to reassess under the new standard our prior conclusions about lease identification,

lease classification and initial direct costs.

The new standard has no material effect on our consolidated

financial statements as the Company does not have a lease with a term longer than 12 months as of December 31, 2020 (See Note 6).

Earnings (losses) per share

Basic earnings (losses) per share is computed by dividing

net income (loss) by the weighted-average number of common shares outstanding during the period. Diluted earnings (losses) per

share is computed giving effect to all dilutive potential common shares that were outstanding during the period. Dilutive potential

common shares consist of incremental shares issuable upon exercise of stock options and warrants and conversion of convertible

debt. Such potentially dilutive shares are excluded when the effect would be to reduce a net loss per share or increase a net income

per share.

During the six months ended December 31, 2020 and 2019,

the Company had outstanding convertible notes and warrants which represent 1,096,705 and 720,382 shares of commons stock respectively.

These shares of common stock were excluded from the computation of diluted earnings per share since their effect would have been

antidilutive.

During the three months ended December 31, 2020 and 2019,

the Company had outstanding convertible notes and warrants which represent 11,675,729 and 720,382 shares of commons stock respectively.

These shares of common stock were excluded from the computation of diluted earnings per share since their effect would have been

antidilutive.

Foreign currencies translation

The reporting currency of the Company is the United States

Dollar (“US$”). The Company’s subsidiaries in the People’s Republic of China (“PRC”) maintain

their books and records in their local currency, the Renminbi Yuan (“RMB”), which is the functional currency as being

the primary currency of the economic environment in which these entities operate.

In general, for consolidation purposes, assets and liabilities

of its subsidiaries whose functional currency is not the US$ are translated into US$, in accordance with ASC Topic 830-30, “Translation

of Financial Statement”, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average

rates prevailing during the period. Stockholders’ equity is translated at historical rates. The gains and losses resulting

from translation of financial statements of foreign subsidiaries are recorded as a separate component of accumulated other comprehensive

income within the statements of stockholders’ equity.

Transactions denominated in currencies other than the

functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction.

Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional

currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the

statements of comprehensive income (loss).

The exchange rates used to translate amounts in RMB into

U.S. Dollars for the purposes of preparing the consolidated financial statements are as follows:

| | |

December 31, 2020 | | |

June 30, 2020 | |

| | |

| | |

| |

| Balance sheet items, except for equity accounts | |

| 6.5402 | | |

| 7.0795 | |

| | |

Six Months Ended December 31, | |

| | |

2020 | | |

2019 | |

| | |

| | |

| |

| Items in statements of comprehensive income (loss) and cash flows | |

| 6.8099 | | |

| 6.9255 | |

Fair Value of Financial Instruments

The carrying value of the Company’s financial instruments:

cash and cash equivalents, accounts receivable, inventory, prepayments and other receivables, accounts payable, income tax payable,

other payables and accrued liabilities approximate at their fair values because of the short-term nature of these financial instruments.

The Company also follows the guidance of the ASC Topic

820-10, “Fair Value Measurements and Disclosures” (“ASC 820-10”), with respect to financial assets and

liabilities that are measured at fair value. ASC 820-10 establishes a three-tier fair value hierarchy that prioritizes the inputs

used in measuring fair value as follows:

Level 1: Inputs are based upon unadjusted quoted prices

for identical instruments traded in active markets;

Level 2: Inputs are based upon quoted prices for similar

instruments in active markets, quoted prices for identical or similar instruments in markets that are not active, and model-based

valuation techniques (e.g. Black-Scholes Option-Pricing model) for which all significant inputs are observable in the market or

can be corroborated by observable market data for substantially the full term of the assets or liabilities. Where applicable, these

models project future cash flows and discount the future amounts to a present value using market-based observable inputs; and

Level 3: Inputs are generally unobservable and typically

reflect management’s estimates of assumptions that market participants would use in pricing the asset or liability. The fair

values are therefore determined using model-based techniques, including option pricing models and discounted cash flow models.

Fair value estimates are made at a specific point in

time based on relevant market information about the financial instrument. These estimates are subjective in nature and involve

uncertainties and matters of significant judgment and, therefore, cannot be determined with precision. Changes in assumptions could

significantly affect the estimates.

The Company has the derivative liabilities measured at

fair value on a recurring basis which are valued at level 3 measurement (See Note 14).

Convertible Instruments

The Company evaluates and accounts for conversion options

embedded in convertible instruments in accordance with ASC 815 “Derivatives and Hedging Activities”.

Applicable GAAP requires companies to bifurcate conversion

options from their host instruments and account for them as free standing derivative financial instruments according to certain

criteria. The criteria include circumstances in which (a) the economic characteristics and risks of the embedded derivative instrument

are not clearly and closely related to the economic characteristics and risks of the host contract, (b) the hybrid instrument that

embodies both the embedded derivative instrument and the host contract is not re-measured at fair value under other GAAP with changes

in fair value reported in earnings as they occur and (c) a separate instrument with the same terms as the embedded derivative instrument

would be considered a derivative instrument.

The Company accounts for convertible instruments (when

it has been determined that the embedded conversion options should not be bifurcated from their host instruments) as follows: The

Company records when necessary, discounts to convertible notes for the intrinsic value of conversion options embedded in debt instruments

based upon the differences between the fair value of the underlying common stock at the commitment date of the note transaction

and the effective conversion price embedded in the note. Debt discounts under these arrangements are amortized over the term of

the related debt to their stated date of redemption.

The Company accounts for the conversion of convertible

debt when a conversion option has been bifurcated using the general extinguishment standards. The debt and equity linked derivatives

are removed at their carrying amounts and the shares issued are measured at their then-current fair value, with any difference

recorded as a gain or loss on extinguishment of the two separate accounting liabilities.

Common Stock Purchase Warrants

The Company classifies as equity any contracts that require

physical settlement or net-share settlement or provide a choice of net-cash settlement or settlement in the Company’s own

shares (physical settlement or net-share settlement) provided that such contracts are indexed to our own stock as defined in ASC

815-40 ("Contracts in Entity's Own Equity"). The Company classifies as assets or liabilities any contracts that require

net-cash settlement (including a requirement to net cash settle the contract if an event occurs and if that event is outside our

control) or give the counterparty a choice of net-cash settlement or settlement in shares (physical settlement or net-share settlement).

Recent accounting pronouncements

The Company considers the applicability and impact of

all accounting standards updates (“ASUs”). Management periodically reviews new accounting standards that are issued.

Fair Value Measurement. In August 2018, the FASB issued

ASU 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework—Changes to the Disclosure Requirements for Fair Value

Measurement, which eliminates, adds and modifies certain disclosure requirements for fair value measurements. Under the guidance,

public companies will be required to disclose the range and weighted average used to develop significant unobservable inputs for

Level 3 fair value measurements. The guidance is effective for all entities for Calendar years beginning after December 15, 2019

and for interim periods within those Calendar years, but entities are permitted to early adopt either the entire standard or only

the provisions that eliminate or modify the requirements. The Company is currently in the process of evaluating the impact of the

adoption of this guidance on its consolidated financial statements.

In January 2020, the FASB issued ASU 2020-01, Investments

- Equity Securities (Topic 321), Investments - Equity Method and Joint Ventures (Topic 323), and Derivatives and Hedging (Topic

815) (“ASU 2020-01”), which is intended to clarify the interaction of the accounting for equity securities under Topic

321 and investments accounted for under the equity method of accounting in Topic 323 and the accounting for certain forward contracts

and purchased options accounted for under Topic 815. The guidance is effective for public entities for Calendar years beginning

after December 15, 2020 and interim periods within those Calendar years and all other entities for Calendar years beginning after

December 15, 2021 and interim periods within those Calendar years, with early adoption permitted. The Company is currently evaluating

the effect of adopting this ASU on the Company’s consolidated financial statements.

Risk factor

Due to the outbreak of the Coronavirus Disease 2019 (COVID-19)

in the PRC, the Company’s operational and financial performance, has been affected by the epidemic during the six months

ended December 31, 2020. The Company has been keeping continuous attention on the situation of the COVID-19, assessing and reacting

actively to its impacts on the financial position and operating results of the Company as below:

| · | During PRC national economic shutdown that was imposed to limit the spread of COVID-19 from early

February to mid-March of 2020, our financial condition and results of operations were adversely affected. Since the restarting

of our operation near the end of March 2020, our financial performances had been recovering slowly but continuously. However, COVID-19

resurgence which occurred in October 2020 had caused one and off traffic restrictions and lockdowns and prolonged the economic

contraction nationwide and disrupted our business operation. |

| · | During the outbreak of COVID-19 in China, the Chinese government responded with the package of

support including tax-cut and financial assistance, we keep our continuous attention on the situation of the COVID-19, assess and

react actively to its impacts on our future operating results or near-and-long-term financial condition. Up to the date of this

report, the assessment is still in progress. |

| · | Since we restored our operation near the end of March 2020, even COVID-19 resurgence occurred in

October 2020, we are of the view that COVID-19 would be under control in near future. We assessed that 1) COVID-19-related impacts

on our cost of capital or access to capital and funding sources and our sources or uses of cash have been insignificant; 2) There

is no material uncertainty about our ongoing ability to meet the covenants of our credit agreements; 3) No material liquidity deficiency

has been identified and we do not expect to disclose or incur any material COVID-19-related contingencies;4) COVID-19-related impacts

on the assets on our balance sheet or our ability to timely account for those assets have been insignificant; and 5) The possibilities

for COVID-19 to trigger any material impairments, increases in allowances for credit losses, restructuring charges, other expenses,

or changes in accounting judgments that have had or are reasonably likely to have a material impact on our financial statements

are low. Looking forward, we keep our continuous attention on the situation of the COVID-19, assess and react actively to its impacts

on issues mentioned above. |

| · | During PRC national economic shutdown that was imposed to limit the spread of COVID-19 from early

February to mid-March of 2020, COVID-19-related circumstances such as remote work arrangements adversely affected our ability to

maintain operations. Since the lifting of the national shutdown order near the end of March 2020, our operations including financial

reporting systems, internal control over financial reporting and disclosure controls and procedures have already resumed. Currently

we keep our continuous attention on the situation of the COVID-19, assess and react actively to its impacts on our future business

continuity plans or whether material resource constraints in implementing these plans. Up to the date of this report, the assessment

is still in progress. |

| · | During

PRC national economic shutdown that was imposed to limit the spread of COVID-19 from early February to mid-March of 2020, the

demands for our products or services were severely affected. Since the restarting of our operation near the end of March 2020,

the demands had been rebounding slowly but continuously. However, COVID-19 resurgence which occurred in October 2020 had caused

one and off traffic restrictions and lockdowns and put numerous business negotiations and sales contracts signing on hold. Notwithstanding

the difficulty at the present, we are capable to take the blows on the product demands and are optimistic about an eventual recovery

in demand to pre-pandemic levels. |

| · | During PRC national economic shutdown that was imposed to limit the spread of

COVID-19 from early February to mid-March of 2020, our supply chain or the methods used to distribute our products or

services were severely affected. Since the lift of the national shutdown order near the end of March 2020, all of our supply

chains or the methods had returned to normal gradually. However, COVID-19 resurgence which occurred in October 2020 had

caused one and off traffic restrictions and lockdowns then inevitably made the adverse impacts on our supply chains. And

COVID-19 highlights the need to transform our current supply chain models. We shall take the actions to respond to business

disruption and supply chain challenges from the global spread of COVID-19 and looks ahead to the longer-term solution of

digital supply networks. |

NOTE 4 - VARIABLE INTEREST ENTITY

The VIE contractual arrangements

On December 27, 2018, the Company entered into VIE agreements

with two shareholders of Fangguan Electronics to control 95.14% of the ownership rights and receive 100% of the net profit or net

losses derived from the business operations of Fangguan Electronics. In exchange for VIE agreements and additional capital contribution,

the Company issued 15 million shares of common stock to two shareholders of Fangguan Electronics. (See Note 1).

The transaction was accounted for as a business combination

using the acquisition method of accounting. The assets, liabilities and the operations of Fangguan Electronics subsequent to the

acquisition date were included in the Company’s consolidated financial statements.

Through power of attorney, equity interest purchase agreement,

and equity interest pledge agreement, 95.14% of the voting rights of Fangguan Electronics’ shareholders have been transferred

to the Company so that the Company has effective control over Fangguan Electronics and have the power to direct the activities

of Fangguan Electronics that most significantly impact its economic performance.

Through business operation agreement with the shareholders

of VIE, the Company shall direct the business operations of Fangguan Electronics, including, but not limited to, adopting corporate

policy regarding daily operations, financial management, and employment, and appointment of directors and senior officers.

Through the exclusive technical support service agreement

with the shareholders of VIE, the Company shall provide VIE with necessary technical support and assistance as the exclusive provider.

And at the request of the Company, VIE shall pay the performance fee, the depreciation and the service fee to the Company. The

performance fee shall be equivalent to 5% of the total revenue of VIE in any Calendar year. The depreciation amount on equipment

shall be determined by accounting rules of China. The Company has the right to set and revise annually this service fee unilaterally

with reference to the performance of VIE.

The service fee that the Company is entitled to earn

shall be the total business incomes of the whole year minus performance fee and equipment depreciation. This agreement allows the

Company to collect 100% of the net profits of the VIE. Except for technical support, the Company did not provide, nor does it intend

to provide, any financial or other support either explicitly or implicitly during the periods presented to its variable interest

entity.

If facts and circumstances change such that the conclusion

to consolidate the VIE has changed, the Company shall disclose the primary factors that caused the change and the effect on the

Company’s financial statements in the periods when the change occurs.

There are no restrictions on the consolidated VIE’s

assets and on the settlement of its liabilities and all carrying amounts of VIE’s assets and liabilities are consolidated

with the Company’s financial statements. In addition, the net income of Fangguan Electronics after Fangguan Electronics became

the VIE of the Company is free of restrictions for payment of dividends to the shareholders of the Company.

Assets of Fangguan Electronics that are collateralized

or pledged are not restricted to settle its own obligations. The creditors of Fangguan Electronics do not have recourse to the

primary beneficiary’s general credit.

Risks associated with the VIE structure

The Company believes that the contractual arrangements

with its VIE and respective shareholders are in compliance with PRC laws and regulations and are legally enforceable. However,

uncertainties in the PRC legal system could limit the Company’s ability to enforce the contractual arrangements. If the legal

structure and contractual arrangements were found to be in violation of PRC laws and regulations, the PRC government could:

| · | revoke the business and operating licenses of the Company’s PRC subsidiary and its VIE; |

| · | discontinue or restrict the operations of any related-party transactions between the Company’s

PRC subsidiary and its VIE; |

| · | limit the Company’s business expansion in China by way of entering into contractual arrangements; |

| · | impose fines or other requirements with which the Company’s PRC subsidiary and its VIE may

not be able to comply; |

| · | require the Company or the Company’s PRC subsidiary and its VIE to restructure the relevant

ownership structure or operations; or |

| · | restrict or prohibit the Company’s use of the proceeds from public offering to finance the

Company’s business and operations in China. |

The Company’s ability to conduct its business through

its VIE may be negatively affected if the PRC government were to carry out of any of the aforementioned actions. As a result, the

Company may not be able to consolidate its VIE in its consolidated financial statements as it may lose the ability to exert effective

control over its VIE and its respective shareholders and it may lose the ability to receive economic benefits from its VIE. The

Company, however, does not believe such actions would result in the liquidation or dissolution of the Company, its PRC subsidiary

and its VIE. There has been no change in facts and circumstances to consolidate the VIE. The following financial statement amounts

and balances of its VIE were included in the accompanying consolidated financial statements after elimination of intercompany transactions

and balances:

| | |

Balance as of

December 31,

2020 | | |

Balance as of

June 30, 2020 | |

| Cash and cash equivalents | |

$ | 855,616 | | |

$ | 1,266,426 | |

| Notes receivable | |

| 35,320 | | |

| 125,798 | |

| Accounts receivable - non-related parties | |

| 3,189,072 | | |

| 3,069,629 | |

| Inventory | |

| 3,017,700 | | |

| 2,639,839 | |

| Advances to suppliers - non-related parties | |

| 625,484 | | |

| 530,670 | |

| Prepaid expenses and other current assets | |

| 81,424 | | |

| 58,103 | |

| Total Current Assets | |

| 7,804,616 | | |

| 7,690,465 | |

| | |

| | | |

| | |

| Property, plant and equipment, net | |

| 6,996,421 | | |

| 6,568,874 | |

| Intangible assets, net | |

| 1,508,762 | | |

| 1,424,404 | |

| Deferred tax assets | |

| 47,778 | | |

| 20,743 | |

| Total Assets | |

$ | 16,357,577 | | |

$ | 15,704,486 | |

| | |

| | | |

| | |

| Short-term bank loan | |

$ | 1,681,906 | | |

$ | 2,034,735 | |

| Accounts payable | |

| 2,455,750 | | |

| 2,637,792 | |

| Advance from customers | |

| 30,967 | | |

| 27,501 | |

| Due to related parties | |

| 1,981,879 | | |

| 1,407,145 | |

| Accrued expenses and other current liabilities | |

| 4,923 | | |

| 61,856 | |

| Total Current Liabilities | |

| 6,155,425 | | |

| 6,169,029 | |

| Total Liabilities | |

$ | 6,155,425 | | |

$ | 6,169,029 | |

NOTE 5 - INVENTORIES

Inventories are stated at the lower of cost (determined

using the weighted average cost) or net realizable value. Inventories consist of the following:

| | |

December 31, 2020 | | |

June 30, 2020 | |

| Raw materials | |

$ | 633,073 | | |

$ | 666,981 | |

| Work-in-process | |

| 960,245 | | |

| 500,331 | |

| Finished goods | |

| 1,972,130 | | |

| 2,096,538 | |

| Total Inventories | |

$ | 3,565,448 | | |

$ | 3,263,850 | |

The Company recorded no inventory markdown for the three

and six months ended December 31, 2020 and 2019.

NOTE 6 - OPERATING LEASE

For the six months ended December 31, 2020, the Company

had two real estate operating leases for office, warehouses and manufacturing facilities under the terms of one year.

Lisite Science Technology (Shenzhen) Co., Ltd ("Lisite

Science") leases office and warehouse space from Shenzhen Keenest Technology Co., Ltd. (“Keenest”), a related

party, with annual rent of approximately $1,500 (RMB10,000) for one year until July 20, 2020. On July 20, 2020, Lisite Science

further extended the lease with Keenest for one more year until July 20, 2021 with annual rent of approximately $1,500 (RMB10,000).

(See Note 11).

Shenzhen Baileqi Electronic Technology Co., Ltd. ("Baileqi

Electronic") leases office and warehouse space from Shenzhen Baileqi Science and Technology Co., Ltd. (“Shenzhen Baileqi

S&T”), a related party, with monthly rent of approximately $2,500 (RMB17,525) and the lease period is from June 1, 2019

to May 31, 2020. On June 5, 2020, Baileqi Electronic further extended the lease with Shenzhen Baileqi S&T for one more year

until May 31, 2021 with monthly rent of approximately $2,500 (RMB17,525). (See Note 11).

The Company made an accounting policy election not to

recognize lease assets and liabilities for the leases listed above as all lease terms are 12 months or shorter.

NOTE 7 – PROPERTY, PLANT AND EQUIPMENT, NET

The components of property, plant and equipment were

as follows:

| | |

December 31, 2020 | | |

June 30, 2020 | |

| | |

| | |

| |

| Buildings | |

$ | 5,011,200 | | |

$ | 4,601,685 | |

| Machinery and equipment | |

| 3,222,821 | | |

| 2,822,686 | |

| Office equipment | |

| 73,665 | | |

| 67,091 | |

| Automobiles | |

| 106,999 | | |

| 98,848 | |

| Subtotal | |

| 8,414,685 | | |

| 7,590,310 | |

| Less: Accumulated depreciation | |

| (1,413,533 | ) | |

| (1,016,373 | ) |

| Property, plant and equipment, net | |

$ | 7,001,152 | | |

$ | 6,573,937 | |

Depreciation expense related to property, plant and equipment

was $300,941 and $384,408 for the six months ended December 31, 2020 and 2019, respectively.

Depreciation expense related to property, plant and equipment

was $135,731 and $183,340 for the three months ended December 31, 2020 and 2019, respectively.