UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from __________ to __________

Commission file number: 000-55453

ENDONOVO THERAPEUTICS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 45-2552528 | |

State or other jurisdiction of incorporation or organization |

(I.R.S. Employer Identification No.) | |

6320 Canoga Avenue, 15th Floor Woodland Hills, CA |

91367 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (800) 489-4774

Securities registered under Section 12(g) of the Act: None

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

| Title of each class | Trading Symbol(s) | Name of principal U.S. market on which traded | ||

| Common stock, par value $0.0001 | ENDV | OTCMKTS |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] | Accelerated filer | [ ] | |

Non-accelerated filer (Do not check if a smaller reporting company) |

[ ] | Smaller reporting company | [X] | |

| Emerging growth company | [X] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [X]

The aggregate market value of the voting Common Stock held by non-affiliates, computed by reference to the price at which the voting Common Stock was sold as of the last business day of the Company’s most recently completed second fiscal quarter is $18,419,338.

As of May 1, 2020, the registrant had 8,813,704 shares of its common stock, par value $0.0001 per share, outstanding.

Documents Incorporated by Reference: None.

TABLE OF CONTENTS

| 2 |

FORWARD-LOOKING STATEMENTS

When used in this Report, the words “may,” “will,” “expect,” “anticipate,” “continue,” “estimate,” “intend,” and similar expressions are intended to identify forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) regarding events, conditions and financial trends which may affect the Company’s future plans of operations, business strategy, operating results, and financial position. Such statements are not guarantees of future performance and are subject to risks and uncertainties and actual results may differ materially from those included within the forward-looking statements for various reasons, including those identified under “Risk Factors.” Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date made. Except as required under federal securities laws and the rules and regulations of the United States Securities and Exchange Commission, the Company does not undertake, and specifically declines, any obligation to update any of these statements or to publicly announce the results of any revisions to any forward-looking statements after the distribution of this report, whether as a result of new information, future events, changes in assumptions, or otherwise.

This Report contains certain estimates and plans related to us and the industry in which we operate, which assume certain events, trends, and activities will occur and the projected information based on those assumptions. We do not know all of our assumptions are accurate. In particular, we do not know what level of acceptance our strategy will achieve, how many acquisitions we will be able to consummate or finance, or the size thereof. If our assumptions are wrong about any events, trends, or activities, then our estimates for future growth for our business also may be wrong. There can be no assurances any of our estimates as to our business growth will be achieved.

| 3 |

Overview

Endonovo Therapeutics, Inc. (Endonovo or the “Company”) is an innovative biotechnology company that has developed a bio-electronic approach to regenerative medicine.

The Company develops, manufactures and distributes evolutionary medical devices focused on the rapid healing of wounds and reduction of pain, edema and inflammation on and in the human body. The Company’s non-invasive bioelectric medical devices are designed to target inflammation, cardiovascular diseases, chronic kidney disease, and central nervous system disorders (“CNS” disorders).

Endonovo’s core mission is to transform the field of medicine by developing safe, wearable, non-invasive bioelectric medical devices that deliver the Company’s Electroceutical® Therapy. Endonovo’s bioelectric Electroceutical® devices harnesses bioelectricity to restore key electrochemical processes that initiate anti-inflammatory processes and growth factors in the body necessary for healing to rapidly occur.

Corporate History

Our predecessor company, Hanover Asset Management, Inc. was incorporated in November 2008 in California. For the purpose of reincorporating in Delaware, we merged with a newly incorporated successor company, Hanover Portfolio Acquisitions, Inc., in July 2011 under which we continue to operate.

IP Resources International, Inc. began operations on September 1, 2011 and was formally incorporated on October 17, 2011.

Reverse Acquisition

On March 14, 2012, we entered into a Share Exchange Agreement (“Agreement”) with IPR and certain of its shareholders. Under the Agreement, each participating IPR shareholder exchanged all of their issued and outstanding IPR common shares totaling 33,234,294, free and clear of all liens, and $155,000 for Company common shares equal to 1.2342 times the number of IPR shares being transferred to the Company for a total of 410 of our shares (410,177 pre-reverse split). The $155,000 was not paid at closing. The Company recorded the $155,000 as acquisition payable. IPR agreed to make payments of up to 25% of the proceeds from any private placement or gross profits earned by IPR until the obligation is satisfied. The percentage of the proceeds to be paid is at the sole discretion of IPR’s Chief Executive Officer and the ex-Chief Executive Officer of the Company based on the liquidity of the Company.

As a result of the Agreement, the former shareholders of IPR, immediately post acquisition owned approximately 89% of the Company and its officers and directors constituted the majority of the officers and directors of the Company. Since the shareholders, officers and directors of IPR have control of the Company, the acquisitions constitutes a reverse acquisition, so IPR was the accounting acquirer and we were the accounting acquiree. For legal purposes, we are the legal parent and IPR is the legal subsidiary.

Acquisition of Aviva Companies Corporation

On April 2, 2013, the Company entered into an Acquisition Agreement (the “Acquisition Agreement”) with (i) The Aviva Companies Corporation (“Aviva”) and (ii) all of the shareholders of Aviva (the “Shareholders”) pursuant to which the Company acquired all of the outstanding shares of Aviva in exchange for the issuance of 60 shares of our common stock (60,000 pre-reverse split), par value $0.0001 per share to the Shareholders (the “Share Exchange”). As a result of the Share Exchange, Aviva became a wholly-owned subsidiary of the Company.

Other than in respect to the transaction, there is no material relationship among Aviva’s stockholders and any of the Company’s affiliates, directors or officers. We are not currently actively pursuing the development of the Aviva Companies Corporation.

Acquisition of WeHealAnimals, Inc.

On November 16, 2013, the Company entered into an Acquisition Agreement (the “Acquisition Agreement”) with (i) WeHealAnimals, Inc. (“WHA”) and (ii) the sole shareholder of WHA (the “Shareholder”) pursuant to which the Company acquired all of the outstanding shares of WHA in exchange for the issuance of 3 shares of our common stock (3,000 shares pre- reverse split), par value $0.0001 per share and $96,000 to the Shareholder (the “Share Exchange”). As a result of the Share Exchange, WHA became a wholly-owned subsidiary of the Company and all of the equity of WHA including its and its sole shareholder’s intellectual property became the property of the Company. This obligation was fully paid on December 15, 2015 through the issuance of 350 shares of stock (350,000 pre-reverse split) to Shareholder. WHA is a Nevada corporation with intellectual property in the fields of bio-technology including its biologics and time-varying electromagnetic frequencies with potential applications on people and animals that management believes can be developed to the benefit of the Company and its shareholders. WHA’s sole shareholder was formerly Chairman and Chief Scientist of Regenetech, Inc. Regenetech was acquired by a company that wanted its technology, biomolecules grown in microgravity, for use in cosmetics. WHA’s sole shareholder left Regenetech with exclusive rights to this proprietary square wave form technology and stem cell technologies, including the patents and patent applications relating thereto.

Other than in respect to the transaction, there is no material relationship between WHA’s sole stockholder and any of the Company’s affiliates, directors or officers.

| 4 |

Acquisition of Rio Grande Assets

On December 22, 2017, we acquired intellectual property and other assets (the “RGN Assets”) from Rio Grande Neurosciences, Inc. (RGN). The price was $4,500,000 of which we paid $3,000,000 in cash and delivered a $1,500,000 secured promissory note due November 30, 2018 and security agreement. Before such note was due, the note was assigned to Eagle Equities, LLC (“Eagle”) its due date was extended to November 30, 2019, and it was made convertible into our common stock at a price related to our common stock’s market price at the time of conversion. The maturity date was then extended to December 31, 2020. The RGN Assets relate to RGN’s PEMF portfolio of intellectual property, including 27 issued patents with foreign patent protection covering the therapeutic use of PEMF as well as the treatment of various central nervous system disorders. We intend to initiate and fund future clinical trials to evaluate the further use of PEMF in the treatment of central nervous system disorders, including traumatic brain injury, post-concussion syndrome, stroke and multiple sclerosis. However, no assurance can be given that we will be successful in these endeavors or that the results of any tests will indicate further development of the RGN Assets.

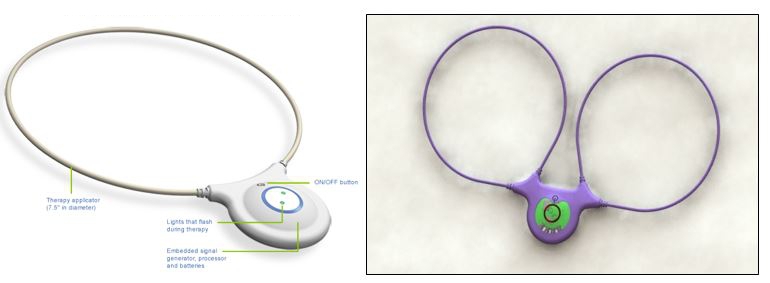

The PEMF assets acquired include SofPulse®, a portable, disposable PEMF device with a CE Mark and an FDA 510(k) clearance for the treatment of post-surgical pain and edema in addition to medical reimbursement for the treatment of chronic wounds. Endonovo Therapeutics has begun the commercialization of the PEMF assets through marketing and the creation of various sales channels and distribution agreements.

Present Development Plans

We now are a biotechnology company developing bioelectronic devices and cell therapies for regenerative medicine. And a commercial-stage developer of non-invasive wearable Electroceuticals™ therapeutic devices.

The Company’s current portfolio of commercial and clinical-stage wearable Electroceuticals™ therapeutic devices addresses wound healing, pain, post-surgical pain and edema, cardiovascular disease, chronic kidney disease, and Central Nervous System (CNS) Disorders, including traumatic brain injury (TBI), acute concussions, post- concussion syndrome and multiple sclerosis. The Company’s non-invasive Electroceutical™ therapeutic device, SofPulse®, using pulsed short-wave radiofrequency at 27.12 MHz has been FDA-Cleared and CE Marked for the palliative treatment of soft tissue injuries and post-operative pain and edema, and has CMS National Coverage for the treatment of chronic wounds. The Company’s current portfolio of pre-clinical stage Electroceuticals™ therapeutic devices address chronic kidney disease, liver disease non-alcoholic steatohepatitis (NASH), cardiovascular and peripheral artery disease (PAD), and ischemic stroke. The Company’s non-invasive, wearable Electroceuticals™ therapeutic devices work by restoring key electrochemical processes that initiate anti-inflammatory and growth factor cascades necessary for healing to occur.

These bioelectronics devices are also commonly referred to as “electroceuticals.” These products are part of an emerging field termed “Bioelectronic Medicine,” that seeks to harness electrical signals in nerves and cells to alter the course of diseases and conditions. Whereas our competitors are primarily using implantable electrical nerve stimulators, we are developing devices that are not implantable and use electromagnetic pulses to deliver electrical stimulation to cells and tissues. We are developing these bioelectronic devices for the treatment of inflammatory conditions in tissues and vital organs with a concentration on vascular diseases and ischemia/reperfusion injuries.

Intellectual Property:

SofPulse: We have 29 issued patents with foreign patent protection covering the therapeutic use of tPEMF as well as the treatment of various central nervous system disorders. Additionally to date, we have filed seven patent applications in the U.S. through the U.S. Patent and Trademark Office (USPTO) and four international patent applications in the E.U., China, South Korea and Japan covering our Time-Varying Electromagnetic Field (TVEMF) technology, the production of biomolecules, the creation of an allogeneic mesenchymal stem cell product a treatment for chemical and radiation injuries, production of stem cell secretome and a method of treating tissues and organs using our TVEMF technology. To date, we have been granted one U.S. Patent (U.S. Patent No. 9,410,143) issued on August 9, 2017 covering the production of human biomolecules using our TVEMF technology. We will continue to seek to strengthen our portfolio of intellectual property by filing additional patents around uses of our core technologies.

Our business strategy is aimed at building value by positioning each of our technologies and therapies to treat specific diseases that lack effective treatment, post-operative pain and edema, or whose current standard of treatment involves invasive procedures and/or potentially harmful side effects. We anticipate updating and refining the business strategy as new medical and/or clinical advancements are made as a result of extensive research and development. In general, the component functions of the business model are to:

| ● | Commercialize our FDA cleared technology through direct sales, distributors and licensees; | |

| ● | License our technologies; |

| 5 |

| ● | Develop additional medical indications for our medical devices; | |

| ● | Develop additional non-invasive, medical technologies; | |

| ● | Conduct pre-clinical and clinical human studies for FDA Approval of our medical devices and cell therapies; | |

| ● | Acquire subsidiaries under the parent company, Endonovo Therapeutics, to assist in the development and distribution of medical technologies; | |

| ● | Incrementally invest, market, and refine acquired and developed medical technologies and therapies. |

Industry Overview

Bioelectrical Medicine within the Healthcare Industry

The healthcare industry is one of the world’s largest and fastest-growing industries. Consuming over 10 percent of Gross Domestic Product (GDP) of most developed nations, health care can form an enormous part of a country’s economy.

As of 2016, 91.1% of residents had health protection in the United States, either through their employer or bought individually. During 2016, healthcare costs reached $3.3 trillion, or $10,348 per person. The share of U.S. GDP devoted to healthcare was 17.9% of U.S. Gross Domestic Product (GDP), the largest of any country in the world. Specifically, the cost of pharmaceuticals in the United States is the highest on the planet. It is expected that Healthcare’s share of U.S. GDP will continue its upward trend, reaching 20 percent of U.S. GDP by 2025. Globally, by 2040, Healthcare spending is expected to exceed $18 Trillion annually.

Bio-Electrical Medicine is a $17.2 Billion sector of the Healthcare Industry growing at more than a 11% CAGR estimated to exceed $35.5 Billion by 2025, according to Grand View Research. Get me a copy of this Bioelectric medicine is at the forefront of technological revolution in medical sciences. As opposed to the pharmaceutical industry, bioelectric medicine has a different treatment therapy that is based on electrical pulses instead of drugs to trigger the body’s recovery capabilities. Bioelectric medicine develops nerve stimulating and sensors activation technologies to regulate biological functions and treat diseases by combining bioengineering, neuroscience, molecular medicines and electronics. These technologies may change the future of therapies for wide range of diseases.

On the basis of type of device, the global Electroceuticals®/Bioelectrical Medicine Market is classified into two major classes:

| Ø | Implantable Electroceuticals® Devices, and, | |

| Ø | Non-Invasive Electroceuticals® Devices. |

| 6 |

BioElectric Medicine vs. Drug Therapies

Over the past 15 years, long-acting and extended-release opioids have been used to treat open wounds, post-operative wounds and chronic pain. These opioids are normally administered at high doses and over long treatment durations particularly in the United States, resulting in a drastic increase in the number opioid-tolerant individuals and a prescription opioid abuse epidemic. Endonovo offers an alternative, non-opioid treatment through its Electroceuticals® systems: The Company’s SofPulse® system is a medical device/designed to rapidly reduce post-operative swelling/edema, pain and to treat and accelerate the recovery of chronic wounds through the use of tPEMF. Chronic pain therapy via tPEMF works by relieving the underlying cause of pain – inflammation.

Drug therapies remain the standard of care for a broad range of medical conditions, including high blood pressure, chronic pain, autoimmune diseases, and psychiatric disorders. Management believes that bioelectronic medicine has developed as a viable alternative for the treatment of many disorders.

Normally, our nervous systems send signals to our tissues and organs to suppress inflammation, a phenomenon known as the inflammatory reflex. But sometimes, this system does not work properly, with malfunctions resulting in diseases like rheumatoid arthritis and inflammatory bowel disease. Traditionally, doctors have treated these diseases using drugs designed to suppress inflammation, such as infliximab (trade name Remicade) or adalimumab (Humira). But these drugs are expensive. Plus, they don’t work for everyone, often come with nasty side effects, and in some rare cases, they can even kill.

Current Product Being Sold – SofPulse®

| 7 |

In clinical trials, the SofPulse® device has proven to reduce mean pain scores by nearly 300% and inflammation by 275% thereby improving and reducing recovery time. Additionally, active patients have experienced a 2.2 fold reduction in narcotic use. The SofPulse® delivers tPEMF to enhance post-surgical recovery, naturally. Since the SofPulse® is non-invasive and non-pharmacologic, there are no known side effects and no potential for overdose or dependency AND no effects on healthy tissue.

How the SofPulse® Works

SofPulse® delivers low intensity microcurrents of energy directly to the procedure site, to enhance recovery, by increasing the amount of naturally occurring Vascular Endothelial Growth Factor (VEGF), thereby increasing the physiological process through which new blood vessels form from pre-existing vessels (Angiogenesis). Within hours/days, the Fibroblast Growth Factor (FGF) enhances, thereby increasing the production of Collagen/Granulation (within days) and Transforming Growth Factor (TGF-β) accelerating Remodeling in the body within days/weeks. This device reduces inflammation and speeds/improves the healing process. The natural healing process allows patients to get back to life faster with lowered use of narcotics. A surgeon places and activates SofPulse® immediately after a procedure. The SofPulse® can be placed over a surgical dressing or clothing and can easily be applied and/or removed in many cases by the patient themselves. The length of time the device is used will vary depending on the type of procedure.

The SofPulse® allows patients to get back to an active life faster with less use of narcotics.

| Ø | Immediately Usable and Effective - Single use patient device applied immediately after surgery. | |

| Ø | Easy to Use - SofPulse® can easily be applied and or removed, including in many cases by the patient themselves. | |

| Ø | Automated Dosing - Device is activated automatically or can be used as needed. | |

| Ø | Versatile - The product comes as a single device or dual device to accommodate different surgical procedures. |

| 8 |

Manufacturing

Our SofPulse® device is manufactured for us by ADM Tronics, Inc. in an FDA approved facility in Northvale, New Jersey.

Sales & Marketing

Endonovo’s strategy is to establish relationships with third parties (such as well-established sales organizations, distributors and marketing coordinators) that assist us in developing, marketing, selling and implementing our products.

We believe that strategic and technology-based relationships with medical facilities are fundamental to our success. We have forged numerous relationships with medical device distributors to enhance our combined capabilities. This approach enhances our ability to accelerate market penetration, accelerate the pace of our sales growth and solidify relationships.

We have a variety of marketing programs designed to create brand awareness and market recognition for our product offerings and for sales lead generation. Our marketing efforts include attending and presenting at healthcare related conferences, advertising, content development and distribution, public relations, social media publication of technical and informative articles in industry journals and sales training.

In addition, our strategic partners augment our marketing and sales campaigns through seminars, trade shows and joint public relations and advertising campaigns. Our customers and strategic partners provide references and recommendations that we often feature in external marketing activities.

Endonovo also is utilizing Key Opinion Leaders (KOLs) and Scientific Advisory Board Members (SABs) within the medical community to develop a sales channel recommendations to other physicians/surgeons.

Competition

The pain management market is intensely competitive, highly fragmented and characterized by rapidly changing technology and drugs. We currently compete with other medical device manufacturers as well as pharmaceutical companies that have developed drugs many which are considered addictive.

Employees

The Company has one employee with the recent hiring of the Company’s Chief Medical Officer. However, we have retained approximately 10 individuals as independent contractors that are involved in business development and sales, research & development and administrative functions.

Not applicable because we are a smaller reporting company.

Item 1B. Unresolved Staff Comments.

Not applicable because we are a smaller reporting company.

| 9 |

We have two office locations; Woodland Hills, CA and San Jose CA, in serviced office suite on a month to month basis. We believe such offices are adequate for our present needs.

We are not party to any material legal proceeding. Due to the nature of our business, we may become active in litigation relating to the defense or assertion of our patent rights or other corporate matters.

Item 4. Mine Safety Disclosures.

Not applicable.

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

Our common stock trades on the OTCQB under the symbol “ENDV”. The OTCQB is a quotation service that displays real-time quotes, last-sale prices, and volume information in over-the-counter (“OTC”) equity securities. An OTCQB equity security generally is any equity that is not listed or traded on a national securities exchange. Our stock is thinly traded, and a robust, active trading market may never develop. The market for the Company’s common stock has been limited, volatile, and sporadic.

Price Range of Common Stock

The following table shows, for the periods indicated, the high and low closing prices per share of our common stock as reported by the OTCQB quotation service.

| Closing Price | ||||||||

| High | Low | |||||||

| Year Ended December, 2018 | ||||||||

| First Quarter | $ | 61.50 | $ | 32.00 | ||||

| Second Quarter | $ | 55.00 | $ | 30.70 | ||||

| Third Quarter | $ | 62.00 | $ | 20.00 | ||||

| Fourth Quarter | $ | 64.00 | $ | 18.92 | ||||

| Year Ended December, 2019 | ||||||||

| First Quarter | $ | 39.50 | $ | 16.50 | ||||

| Second Quarter | $ | 21.70 | $ | 10.00 | ||||

| Third Quarter | $ | 18.66 | $ | 6.20 | ||||

| Fourth Quarter | $ | 10.70 | $ | 1.30 | ||||

| 10 |

Approximate Number of Equity Security Holders

As of May 1, 2020, there were approximately 391 stockholders of record. Because shares of our common stock are held by depositaries, brokers and other nominees, the number of beneficial holders of our shares is substantially larger than the number of stockholders of record.

Dividends

Holders of our common stock are entitled to receive dividends if, as and when declared by the Board of Directors out of funds legally available therefore. We have never declared or paid any dividends on our common stock. We intend to retain any future earnings for use in the operation and expansion of our business. Consequently, we do not anticipate paying any cash dividends on our common stock to our stockholders for the foreseeable future.

Item 6. Selected Financial Data.

Not applicable because we are a smaller reporting company.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The information and financial data discussed below is derived from the audited financial statements of the Company for its fiscal year ended December 31, 2019. The audited financial statements were prepared and presented in accordance with generally accepted accounting principles in the United States. The information and financial data discussed below is only a summary and should be read in conjunction with the historical financial statements and related notes contained elsewhere in this 10-K. The financial statements contained elsewhere in this 10-K fully represent the Company’s financial condition and operations; however, they are not indicative of the Company’s future performance. Although management believes that the assumptions made and expectations reflected in the forward-looking statements are reasonable, there is no assurance that the underlying assumptions will, in fact, prove to be correct or that actual results will not be different from expectations expressed in this 10-K.

Cautionary Notice Regarding Forward Looking Statements

The information contained in Item 2 contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Actual results may materially differ from those projected in the forward-looking statements as a result of certain risks and uncertainties set forth in this report. Although management believes that the assumptions made and expectations reflected in the forward-looking statements are reasonable, there is no assurance that the underlying assumptions will, in fact, prove to be correct or that actual results will not be different from expectations expressed in this report.

This filing contains a number of forward-looking statements which reflect management’s current views and expectations with respect to our business, strategies, products, future results and events, and financial performance. All statements made in this filing other than statements of historical fact, including statements addressing operating performance, events, or developments which management expects or anticipates will or may occur in the future, including statements related to distributor channels, volume growth, revenues, profitability, new products, adequacy of funds from operations, statements expressing general optimism about future operating results, and non-historical information, are forward looking statements. In particular, the words “believe,” “expect,” “intend,” “anticipate,” “estimate,” “may,” variations of such words, and similar expressions identify forward-looking statements, but are not the exclusive means of identifying such statements, and their absence does not mean that the statement is not forward-looking. These forward-looking statements are subject to certain risks and uncertainties, including those discussed below. Our actual results, performance or achievements could differ materially from historical results as well as those expressed in, anticipated, or implied by these forward-looking statements. We do not undertake any obligation to revise these forward-looking statements to reflect any future events or circumstances.

| 11 |

Readers should not place undue reliance on these forward-looking statements, which are based on management’s current expectations and projections about future events, are not guarantees of future performance, are subject to risks, uncertainties and assumptions (including those described below), and apply only as of the date of this filing. Our actual results, performance or achievements could differ materially from the results expressed in, or implied by, these forward-looking statements. Factors which could cause or contribute to such differences include, but are not limited to, the risks discussed in this Annual Report on Form 10K, in press releases and in other communications to shareholders issued by us from time to time which attempt to advise interested parties of the risks and factors which may affect our business. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise.

Critical Accounting Policies and Estimates

We prepare our consolidated financial statements in accordance with accounting principles generally accepted in the U.S. (U.S. GAAP). In doing so, we have to make estimates and assumptions that affect our reported amounts of assets, liabilities, revenues, and expenses, as well as related disclosure of contingent assets and liabilities. In some cases, we could reasonably have used different accounting policies and estimates. In some cases, changes in the accounting estimates are reasonably likely to occur from period to period. Accordingly, actual results could differ materially from our estimates. To the extent that there are material differences between these estimates and actual results, our financial condition or results of operations will be affected. We base our estimates on past experience and other assumptions that we believe are reasonable under the circumstances, and we evaluate these estimates on an ongoing basis. We refer to accounting estimates of this type as critical accounting policies and estimates, which we discuss further below.

Use of estimates

Preparing financial statements requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenue, and expenses. The significant estimates were made for the fair value of common stock issued for services, with notes payable arrangements, in connection with note extension agreements, and as repayment for outstanding debt, in estimating the useful life used for depreciation and amortization of our long-lived assets, in the valuation of the derivative liability, and the valuation of deferred income tax assets. Actual results and outcomes may differ from management’s estimates and assumptions.

Net Loss per Share

Basic net loss per share is calculated based on the net loss attributable to common shareholders divided by the weighted average number of shares outstanding for the period excluding any dilutive effects of options, warrants, unvested share awards and convertible securities. Diluted net loss per common share assumes the conversion of all dilutive securities using the if-converted method and assumes the exercise or vesting of other dilutive securities, such as options, common shares issuable under convertible debt, warrants and restricted stock using the treasury stock method when dilutive.

Accounts Receivable

The Company uses the specific identification method for recording the provision for doubtful accounts, which was $0 at December 31, 2019 and 2018. Accounts receivable are written off when all collection attempts have failed.

| 12 |

Research and Development

Costs relating to the development of new products are expensed as research and development as incurred in accordance with FASB Accounting Standards Codification (“ASC”) 730-10, Research and Development. Research and development costs amounted to $153,126 and $274,271 for the years ended December 31, 2019 and 2018, respectively, and are included in operating expenses in the consolidated statements of operations.

Recently Issued Accounting Pronouncements

In February 2016, the FASB issued ASU 2016-02, Leases (Topic 842), which supersedes existing guidance on accounting for leases in “Leases (Topic 840)” and generally requires all leases to be recognized in the consolidated balance sheet. ASU 2016-02 is effective for annual and interim reporting periods beginning after December 15, 2018; early adoption is permitted. The provisions of ASU 2016-02 are to be applied using a modified retrospective approach. The Company has adopted ASU 2016-02 on January 1, 2019. The adoption of ASU 2016-02 did not have a significant impact on the Company’s consolidated results of operations, financial position and cash flows.

In June 2018, the FASB issued ASU No. 2018-07, Compensation—Stock Compensation (Topic 718): Improvements to Nonemployee Share-Based Payment Accounting, which simplifies several aspects of the accounting for nonemployee share-based payment transactions resulting from expanding the scope of Topic 718, Compensation—Stock Compensation, to include share-based payment transactions for acquiring goods and services from nonemployees. This ASU is effective for public business entities for fiscal years beginning after December 15, 2018, including interim periods within that fiscal year. For all other entities, the amendments are effective for fiscal years beginning after December 15, 2019, and interim periods within fiscal years beginning after December 15, 2020. Early adoption is permitted, but no earlier than an entity’s adoption date of Topic 606. The Company has early adopted ASU 2018-07 and the adoption did not have a significant impact on the Company’s consolidated financial statements.

In August 2018, the FASB issued ASU No. 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework- Changes to the Disclosure Requirements for Fair Value Measurement. The amendments in this Update modify the disclosure requirements on fair value measurements in Topic 820, Fair Value Measurement, based on the concepts in the Concepts Statement, including the consideration of costs and benefits. Effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2019. The amendments on changes in unrealized gains and losses, the range and weighted average of significant unobservable inputs used to develop Level 3 fair value measurements, and the narrative description of measurement uncertainty should be applied prospectively for only the most recent interim or annual period presented in the initial fiscal year of adoption. All other amendments should be applied retrospectively to all periods presented upon their effective date. Early adoption is permitted upon issuance of this Update. Any entity is permitted to early adopt any removed or modified disclosures upon issuance of this Update and delay adoption of the additional disclosures until their effective date. The Company has not yet selected a transition method nor has it determined the effect of the standard on its ongoing financial reporting.

The Company has evaluated all the recent accounting pronouncements and determined that there are no other accounting pronouncements that will have a material effect on the Company’s financial statements.

| 13 |

Results of Operations

Results of Operations Year Ended December 31, 2019 vs. Year Ended December 31, 2018

| Year Ended December 31, | Favorable | |||||||||||||||

| 2019 | 2018 | (Unfavorable) | % | |||||||||||||

| Revenue | $ | 310,164 | $ | 83,263 | 226,901 | 272.5 | ||||||||||

| Cost of revenue | 93,385 | 12,930 | (80,455 | ) | (622.2 | ) | ||||||||||

| Gross profit | 216,779 | 70,333 | 146,446 | 208.2 | ||||||||||||

| Operating expenses | 4,025,851 | 4,229,595 | 203,744 | 4.8 | ||||||||||||

| Loss from operations | (3,809,072 | ) | (4,159,262 | ) | 350,190 | 8.4 | ||||||||||

| Other expense | (13,505,432 | ) | (2,276,577 | ) | (11,228,855 | ) | (493.2 | ) | ||||||||

| Net loss | $ | (17,314,504 | ) | $ | (6,435,839 | ) | $ | (10,878,665 | ) | (169.0 | ) | |||||

Revenue

Revenue of the Company’s SofPulse® product during the current year increased by $226,901 compared to the previous year.

Revenues for our SofPulse® product is typically recognized at the time the product is shipped, at which time the title passes to the customer, and there are no further performance obligations.

In connection with offering products and services provided to the end user by third-party vendors, we review the relationship between us, the vendor and the end user to assess whether revenue should be reported on a gross or net basis. In asserting whether revenue should be reported on a gross or net basis, we consider whether we act as a principal in the transaction and control the goods and services used to fulfill the performance obligation(s) associated with the transaction.

We anticipate that revenue will continue to increase in future periods as the roll out of the SofPulse® product continues.

Cost of Revenue

Cost of revenue increased by $80,455 or 622.2% from the previous year to $93,385 during the current year compared to $12,930 during the previous year. Cost of revenue is recognized on those sales recorded as gross for which we are the principal in the transaction as opposed to net sales which reflect no cost of revenue.

It is anticipated that cost of revenue will increase in future periods as the roll out of the SofPulse® product continues.

Operating Expenses

Our operating expenses for 2019 were $4,025,851 compared to $4,229,595 for 2018. The operating expenses were comprised primarily of consulting and professional fees for the development of our intellectual property, research and development, expenses related to being a public company and depreciation and amortization expenses.

Depreciation and Amortization

We incur depreciation and amortization expense for costs related to our assets, including our patents, information technology and software. Our depreciation and amortization was $650,315 in 2019 compared to $650,216 in 2018. There were no significant equipment purchases or sales during 2019.

Other Expense

Other Expense were $13,505,432 in 2019 compared to $2,276,577 in 2018. The increase in other expense during our fiscal year 2019 was primarily the result of changes in our financings and re-valuations to reflect liability accounting for convertible notes issued with variable conversion rates.

| 14 |

Liquidity and Capital Resources

| As of December 31, | Increase | |||||||||||

| 2019 | 2018 | (Decrease) | ||||||||||

| Working Capital | ||||||||||||

| Current assets | $ | 62,555 | $ | 382,496 | $ | (319,941 | ) | |||||

| Current liabilities | 23,623,470 | 15,479,151 | 8,144,319 | |||||||||

| Working capital deficit | $ | (23,560,915 | ) | $ | (15,096,655 | ) | $ | (8,464,260 | ) | |||

| Long-term debt | $ | 155,000 | $ | 155,000 | $ | - | ||||||

| Stockholders’ deficit | $ | (20,503,820 | ) | $ | (11,391,838 | ) | $ | (9,111,982 | ) | |||

| For Year Ended December 31, | Increase | |||||||||||

| 2019 | 2018 | (Decrease) | ||||||||||

| Statements of Cash Flows Select Information | ||||||||||||

| Net cash provided (used) by: | ||||||||||||

| Operating activities | $ | (2,541,007 | ) | $ | (2,878,834 | ) | $ | 337,827 | ||||

| Investing activities | $ | (2,594 | ) | $ | (8,969 | ) | $ | 6,375 | ||||

| Financing activities | $ | 2,183,343 | $ | 3,176,781 | $ | (993,438 | ) | |||||

| As of December 31, | Increase | |||||||||||

| 2019 | 2018 | (Decrease) | ||||||||||

| Balance Sheet Select Information | ||||||||||||

| Cash | $ | 18,893 | $ | 379,151 | $ | (360,258 | ) | |||||

| Accounts payable and accrued expenses | $ | 4,348,219 | $ | 3,189,243 | $ | (1,158,976 | ) | |||||

Since inception and through December 31, 2019, the Company has raised approximately $16.1 million in equity and debt transactions. These funds have been used to advance the operations of the Company, build its bio-medical platform, patent work and general corporate development. Our accompanying consolidated financial statements have been prepared assuming the Company will continue as a going concern, which contemplates realization of assets and the satisfaction of liabilities in the normal course of business for the twelve-month period following the date of these consolidated financial statements. However, the Company has incurred substantial losses. Our current liabilities exceed our current assets and available cash is not sufficient to fund the expected future operation. The Company is raising additional capital through debt and equity securities in order to continue the funding of its operations. However, there is no assurance that the Company can raise enough funds or generate sufficient revenues to pay its obligations as they become due, which raises substantial doubt about our ability to continue as a going concern. To reduce the risk of not being able to continue as a going concern, management has implemented its business plan to materialize revenues from sales and future license agreements and has also initiated an equity line of credit offering to raise capital through the sale of its common stock and has engaged an Investment Banker to raise additional capital. Although, uncertainty exists as to whether the Company will be able generate enough cash from operations to fund the Company’s working capital needs or raise sufficient capital to meet the Company’s obligations as they become due, no adjustments have been made to the carrying value of assets or liabilities as a result of this uncertainty. Our cash on hand at December 31, 2019 was $18,893. This will not be sufficient to fund operations if additional capital is not raised. The Company raised an aggregate of $1.3 million through the sale of equity and debt securities since December 31, 2019 through the date of this report.

| 15 |

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements, as defined in Item 303(a)(4)(ii) of Regulation S-K, obligations under any guarantee contracts or contingent obligations. We also have no other commitments, other than the costs of being a public company that will increase our operating costs or cash requirements in the future.

Seasonality

Management does not believe that our current business segment is seasonal to any material extent.

Securities Authorized for Issuance under Equity Compensation Plans

We do not have in effect any compensation plans under which our equity securities are authorized for issuance.

Unregistered Sales of Equity Securities

During the year ended December 31, 2019, we issued the following unregistered equity securities:

| Number of | ||||||||

| Common Shares | Source of | |||||||

| Issued | Payment | Amount | ||||||

| 10,340 | Services | $ | 159,850 | |||||

| 728,057 | Conversion of notes | $ | 7,533,318 | |||||

| 753 | Lock-up agreements/Note extension | $ | 12,121 | |||||

| 17,900 | Cash | $ | 168,343 | |||||

| 1,091 | Issued with notes | $ | 26,545 | |||||

The above issuances of were exempt from registration pursuant to Section 4(2), and/or Regulation D promulgated under the Securities Act. These securities qualified for exemption under Section 4(2) of the Securities Act since the issuance securities by us did not involve a public offering. The offering was not a “public offering” as defined in Section 4(2) due to the insubstantial number of persons involved in the deal, size of the offering, manner of the offering and number of securities offered. We did not undertake an offering in which we sold a high number of securities to a high number of investors. In addition, these stockholders had the necessary investment intent as required by Section 4(2) since they agreed to and received share certificates bearing a legend stating that such securities are restricted pursuant to Rule 144 of the Securities Act. This restriction ensures that these securities would not be immediately redistributed into the market and therefore not be part of a “public offering.” Based on an analysis of the above factors, we have met the requirements to qualify for exemption under Section 4(2) of the Securities Act for this transaction.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

We are a Smaller Reporting Company and are not required to provide the information under this item.

| 16 |

Item 8. Financial Statements and Supplementary Data.

EDONOVO THERAPEUTICS, INC.

AND SUBSIDIARIES

INDEX TO FINANCIAL STATEMENTS

| 17 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders

Endonovo Therapeutics, Inc. and Subsidiaries

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheets of Endonovo Therapeutics, Inc. and Subsidiaries (the Company) as of December 31, 2019 and 2018, and the related statements of operations, stockholders’ deficit, and cash flows for each of the years in the two-year period ended December 31, 2019, and the related notes to the consolidated financial statements (collectively referred to as the consolidated financial statements). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2019 and 2018, and the results of its operations and its cash flows for each of the years in the two-year period ended December 31, 2019, in conformity with accounting principles generally accepted in the United States of America.

Explanatory Paragraph – Going Concern

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the consolidated financial statements, the Company has continued to incur significant operating losses and negative cash flows from operations, during the year ended December 31, 2019 and has negative working capital at December 31, 2019. These conditions raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans in regard to these matters are also described in Note 1. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s consolidated financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that our audits provide a reasonable basis for our opinion.

/s/ Rose, Snyder & Jacobs LLP

We have served as the Company’s auditor since 2008.

Encino, California

May 1, 2020

| 18 |

Endonovo Therapeutics, Inc. and Subsidiaries

Consolidated Balance Sheets

As of December 31,

| 2019 | 2018(*) | |||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash | $ | 18,893 | $ | 379,151 | ||||

| Accounts receivable, net of allowance for doubtful accounts of $0 | 22,742 | 3,345 | ||||||

| Prepaid expenses and other current assets | 20,920 | - | ||||||

| Total current assets | 62,555 | 382,496 | ||||||

| Property Plant and Equipment, net | 5,915 | 6,727 | ||||||

| Patents, net | 3,206,180 | 3,853,090 | ||||||

| Total assets | $ | 3,274,650 | $ | 4,242,313 | ||||

| LIABILITIES AND SHAREHOLDERS’ DEFICIT | ||||||||

| Current Liabilities | ||||||||

| Accounts payable | $ | 599,470 | $ | 157,388 | ||||

| Accrued interest | 1,317,376 | 786,098 | ||||||

| Deferred compensation | 2,431,373 | 2,245,757 | ||||||

| Notes payable, net of discounts of $ 12,649 as of December 31, 2019 and $1,833,795 as of December 31, 2018 | 6,697,146 | 6,054,403 | ||||||

| Notes payable - related party | 165,000 | 270,000 | ||||||

| Derivative liability | 10,599,690 | 4,426,026 | ||||||

| Series C preferred stock liability, net of discounts of $766 and $180,712 at December 31, 2019 and December 31, 2018, respectively | 1,813,415 | 1,539,479 | ||||||

| Total current liabilities | 23,623,470 | 15,479,151 | ||||||

| Acquisition payable | 155,000 | 155,000 | ||||||

| Total liabilities | 23,778,470 | 15,634,151 | ||||||

| COMMITMENTS AND CONTINGENCIES, note 9 | ||||||||

| Shareholders’ deficit | ||||||||

| Super AA super voting preferred stock, $0.001 par value; 1,000,000 authorized and 25,000 issued and outstanding at December 31, 2019 and December 31, 2018 | 25 | 25 | ||||||

| Series B convertible preferred stock, $0.0001 par value; 50,000 shares authorized and 600 issued and outstanding at December 31, 2019 and December 31, 2018 | 1 | 1 | ||||||

| Series D convertible preferred stock, $0.0001 par value; 20,000 shares authorized and 255 and 0 issued and outstanding at December 31, 2019 and December 31, 2018, respectively | - | - | ||||||

| Common stock, $0.0001 par value; 2,500,000,000 shares authorized; and 1,189,204 and 431,063 shares issued and outstanding as of December 31, 2019 and December 31, 2018, respectively | 118 | 43 | ||||||

| Additional paid-in capital | 32,432,392 | 24,229,945 | ||||||

| Stock subscriptions | (1,570 | ) | (1,570 | ) | ||||

| Accumulated deficit | (52,934,786 | ) | (35,620,282 | ) | ||||

| Total shareholders’ deficit | (20,503,820 | ) | (11,391,838 | ) | ||||

| Total liabilities and shareholders’ deficit | $ | 3,274,650 | $ | 4,242,313 |

See accompanying summary of accounting policies and notes to consolidated financial statements.

(*) The consolidated financial statements have been retroactively restated to reflect the 1,000-for-1-reverse stock split that occurred in December 20, 2019.

| 19 |

Endonovo Therapeutics, Inc. and Subsidiaries

Consolidated Statements of Operations

For the Years Ended December 31,

| 2019 | 2018(*) | |||||||

| Revenue | $ | 310,164 | $ | 83,263 | ||||

| Cost of revenue | 93,385 | 12,930 | ||||||

| Gross profit | 216,779 | 70,333 | ||||||

| Operating expenses | 4,025,851 | 4,229,595 | ||||||

| Loss from operations | (3,809,072 | ) | (4,159,262 | ) | ||||

| Other income (expense) | ||||||||

| Change in fair value of derivative liability | (7,488,690 | ) | 2,603,983 | |||||

| Gain (loss) on extinguishment of debt | 73,503 | 316,560 | ||||||

| Interest expense, net | (6,090,245 | ) | (5,197,120 | ) | ||||

| Total other expense | (13,505,432 | ) | (2,276,577 | ) | ||||

| Loss before income taxes | (17,314,504 | ) | (6,435,839 | ) | ||||

| Provision for income taxes | - | - | ||||||

| Net loss | $ | (17,314,504 | ) | $ | (6,435,839 | ) | ||

| Basic and diluted loss per share | $ | (24.83 | ) | $ | (17.76 | ) | ||

| Weighted average common share outstanding: | ||||||||

| Basic and diluted | 697,305 | 362,466 |

See accompanying summary of accounting policies and notes to consolidated financial statements.

(*) The consolidated financial statements have been retroactively restated to reflect the 1,000-for-1-reverse stock split that occurred in December 20, 2019.

| 20 |

Endonovo Therapeutics, Inc. and Subsidiaries

Consolidated Statement of Stockholders Deficit

For the Years Ended December 31, 2019 and 2018

| Series AA | Series B Convertible | Series D Convertible | Additional | Total | ||||||||||||||||||||||||||||||||||||||||||||

| Preferred Stock | Preferred Stock | Preferred Stock | Common Stock | Paid-in | Subscription | Retained | Shareholder’s | |||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | Shares | Amount | Capital | Receivable | Earnings | Deficit | |||||||||||||||||||||||||||||||||||||

| Balance December 31, 2017(*) | 5,000 | $ | 5 | - | $ | - | - | $ | - | 316,952 | $ | 32 | $ | 19,635,675 | $ | (1,570 | ) | $ | (29,184,443 | ) | $ | (9,550,300 | ) | |||||||||||||||||||||||||

| Private placement units issued for cash (*) | - | - | - | - | - | - | 1,562 | 0 | 60,000 | - | - | 60,000 | ||||||||||||||||||||||||||||||||||||

| Preferred stock issued for cash | 20,000 | 20 | 1,350 | 1 | - | - | - | - | 134,981 | - | - | 135,002 | ||||||||||||||||||||||||||||||||||||

| Shares issued for cash (*) | - | - | - | - | - | - | 2,000 | 0 | 25,000 | - | - | 25,000 | ||||||||||||||||||||||||||||||||||||

| Shares issued for services (*) | - | - | - | - | - | - | 7,175 | 1 | 224,784 | - | - | 224,785 | ||||||||||||||||||||||||||||||||||||

| Shares issued for conversion of Preferred Series B (*) | - | - | (750 | ) | - | - | - | 2,941 | 0 | - | - | - | - | |||||||||||||||||||||||||||||||||||

| -Shares issued with lock-up agreements (*) | - | - | - | - | - | - | 477 | - | 17,194 | - | - | 17,194 | ||||||||||||||||||||||||||||||||||||

| Shares issued for conversion of notes payable and accrued interest (*) | - | - | - | - | - | - | 92,773 | 9 | 3,440,716 | - | - | 3,440,725 | ||||||||||||||||||||||||||||||||||||

| Valuation of warrants issued with Preferred Series C | - | - | - | - | - | - | - | - | 175,538 | - | - | 175,538 | ||||||||||||||||||||||||||||||||||||

| Valuation of warrant and stock options issued for services | - | - | - | - | - | - | - | - | 402,919 | - | - | 402,919 | ||||||||||||||||||||||||||||||||||||

| Valuation of warrant issued with note payable | - | - | - | - | - | - | - | - | 71,521 | - | - | 71,521 | ||||||||||||||||||||||||||||||||||||

| Valuation of warrants issued for extension of notes | - | - | - | - | - | - | - | - | 19,417 | - | - | 19,417 | ||||||||||||||||||||||||||||||||||||

| Valuation of stock issued with notes payable (*) | - | - | - | - | - | - | 1,000 | 0 | 22,200 | - | - | 22,200 | ||||||||||||||||||||||||||||||||||||

| Exercise of cashless warrants (*) | - | - | - | - | - | - | 6,183 | 1 | - | - | - | - | ||||||||||||||||||||||||||||||||||||

| Net loss for the year ended December 31, 2017 | - | - | - | - | - | - | - | - | - | (6,435,839 | ) | (6,435,839 | ) | |||||||||||||||||||||||||||||||||||

| Balance December 31, 2018 (*) | 25,000 | 25 | 600 | 1 | - | - | 431,063 | 43 | 24,229,945 | (1,570 | ) | (35,620,282 | ) | (11,391,838 | ) | |||||||||||||||||||||||||||||||||

| Shares issued for cash | - | - | - | - | - | - | 17,900 | 1 | 168,342 | - | - | 168,343 | ||||||||||||||||||||||||||||||||||||

| Shares issued for services | - | - | - | - | - | - | 10,340 | 1 | 159,849 | - | - | 159,850 | ||||||||||||||||||||||||||||||||||||

| Shares issued with lock-up agreements | - | - | - | - | - | - | 310 | - | 3,788 | - | - | 3,788 | ||||||||||||||||||||||||||||||||||||

| Shares issued for conversion of notes payable and accrued interest | - | - | - | - | - | - | 728,057 | 73 | 7,533,245 | - | - | 7,533,318 | ||||||||||||||||||||||||||||||||||||

| Shares issued for Preferred Series D | - | - | - | - | 255 | 255,000 | - | - | 255,000- | - | - | 255,000 | ||||||||||||||||||||||||||||||||||||

| Valuation of stock issued with notes payable | - | - | - | - | - | - | 1,091 | - | 26,545 | - | - | 26,545 | ||||||||||||||||||||||||||||||||||||

| Valuation of warrants issued with Preferred Series C | - | - | - | - | - | - | - | - | 16,333 | - | - | 16,333 | ||||||||||||||||||||||||||||||||||||

| Valuation of warrant and stock options issued for services | - | - | - | - | - | - | - | - | 31,012 | - | - | 31,012 | ||||||||||||||||||||||||||||||||||||

| Valuation of common stock issued for extension of notes | - | - | - | - | - | - | 443 | - | 8,333 | - | - | 8,333 | ||||||||||||||||||||||||||||||||||||

| Net loss for the year ended December 31, 2019 | - | - | - | - | - | - | - | - | - | - | (17,314,504 | ) | (17,314,504 | ) | ||||||||||||||||||||||||||||||||||

| Balance December 31, 2019 | 25,000 | $ | 25 | 600 | $ | 1 | 255 | $ | 255,000 | 1,189,204 | $ | 118 | $ | 32,432,392 | $ | (1,570 | ) | $ | (52,934,786 | ) | $ | (20,503,820 | ) | |||||||||||||||||||||||||

See accompanying summary of accounting policies and notes to consolidated financial statements.

(*) The consolidated financial statements have been retroactively restated to reflect the 1,000-for-1-reverse stock split that occurred in December 20, 2019.

| 21 |

Endonovo Therapeutics, Inc. and Subsidiaries

Consolidated Statements of Cash Flows

For the Years Ended December 31,

| 2019 | 2018(*) | |||||||

| Operating activities: | ||||||||

| Net loss | $ | (17,314,504 | ) | $ | (6,435,839 | ) | ||

| Adjustments to reconcile net loss to cash used in operating activities: | ||||||||

| Depreciation and amortization expense | 650,315 | 650,216 | ||||||

| Fair value of equity issued for services | 159,850 | 627,704 | ||||||

| Amortization of discount on Series C Preferred stock liability | 196,269 | 96,635 | ||||||

| Non-cash interest and fees | 2,654,071 | 759,949 | ||||||

| Non-cash value of stock, options and warrants issued for services | 34,802 | - | ||||||

| Amortization of note discount and original issue discount | 2,044,940 | 3,464,096 | ||||||

| Change in fair value of derivative liability | 7,488,690 | (2,603,983 | ) | |||||

| (Gain) loss on extinguishment of debt | (73,503 | ) | (316,559 | ) | ||||

| Changes in assets and liabilities: | ||||||||

| Accounts receivable | (19,397 | ) | (3,345 | ) | ||||

| Prepaid expenses and other current assets | (20,920 | ) | 21,000 | |||||

| Accounts payable | 442,082 | 63,232 | ||||||

| Accrued interest | 1,030,682 | 623,885 | ||||||

| Deferred compensation | 185,616 | 174,175 | ||||||

| Net cash used in operating activities | (2,541,007 | ) | (2,878,834 | ) | ||||

| Investing activities: | ||||||||

| Acquisition of property and equipment | (2,594 | ) | (8,969 | ) | ||||

| Net cash used in investing activities | (2,594 | ) | (8,969 | ) | ||||

| Financing activities: | ||||||||

| Proceeds from the issuance of notes payable | 1,995,000 | 2,836,000 | ||||||

| Proceeds from short term advances | - | 65,000 | ||||||

| Proceeds from issuance of preferred stock | - | 135,002 | ||||||

| Repayments on related party short term advances | (105,000 | ) | (87,000 | ) | ||||

| Proceeds from issuance of common stock | 168,343 | 85,000 | ||||||

| Payment on notes payable | (130,000 | ) | (555,500 | ) | ||||

| Proceeds from issuance of redeemable shares | 255,000 | 702,500 | ||||||

| Payment against long term loan | - | (4,221 | ) | |||||

| Net cash provided by financing activities | 2,183,343 | 3,176,781 | ||||||

| Net increase in cash | (360,258 | ) | 288,978 | |||||

| Cash, beginning of year | 379,151 | 90,173 | ||||||

| Cash, end of year | $ | 18,893 | $ | 379,151 | ||||

| Supplemental disclosure of cash flow information: | ||||||||

| Cash paid for interest | $ | 17,000 | $ | 248,730 | ||||

| Cash paid for income taxes | $ | - | $ | - | ||||

| Cash paid for Preferred C dividends | $ | 115,115 | $ | 64,300 | ||||

| Non-Cash Investing and Financing Activities: | ||||||||

| Conversion of notes payable and accrued interest to common stock | $ | 3,645,956 | $ | 1,852,415 | ||||

| Value of derivative liability from transfer to equity upon conversion of notes payable and accrued interest | $ | 3,960,864 | $ | 1,712,307 | ||||

| Reduction in note payable and accrued interest as result of settlement | $ | - | $ | 82,000 | ||||

| Conversion of notes payable to redeemable preferred stock | $ | 94,000 | $ | 317,691 | ||||

See accompanying summary of accounting policies and notes to consolidated financial statements.

(*) The consolidated financial statements have been retroactively restated to reflect the 1,000-for-1-reverse stock split that occurred in December 20, 2019.

| 22 |

Endonovo Therapeutics, Inc. and Subsidiary

Notes to Consolidated Financial Statements

For the Years Ended December 31, 2019 and 2018

Note 1 - Nature of Business and Summary of Significant Accounting Policies

Endonovo Therapeutics, Inc. (Endonovo or the “Company”) is an innovative biotechnology company that has developed a bio-electronic approach to regenerative medicine. Endonovo is a growth stage company whose stock is publicly traded (OTCQB: ENDV).

The Company develops, manufactures and distributes evolutionary medical devices focused on the rapid healing of wounds and reduction of inflammation on and in the human body. The Company’s non-invasive bioelectric medical devices are designed to target inflammation, cardiovascular diseases, chronic kidney disease, and central nervous system disorders (“CNS” disorders).

Endonovo’s core mission is to transform the field of medicine by developing safe, wearable, non-invasive bioelectric medical devices that deliver the Company’s Electroceutical® Therapy. Endonovo’s bioelectric Electroceutical® devices harnesses bioelectricity to restore key electrochemical processes that initiate anti-inflammatory processes and growth factors in the body necessary for healing to rapidly occur.

On January 22, 2014, Hanover Portfolio Acquisitions, Inc. (the “Company”) received written consents in lieu of a meeting of stockholders from holders of a majority of the shares of Common Stock representing in excess of 50% of the total issued and outstanding voting power of the Company approving an amendment to the Company’s Certificate of Incorporation to change the name of the Company from “Hanover Portfolio Acquisitions, Inc.” to “Endonovo Therapeutics, Inc.” The name change was affected pursuant to a Certificate of Amendment (the “Certificate of Amendment”), filed with the Secretary of State of Delaware on January 24, 2014.

Basis of Presentation and Principles of Consolidation

The consolidated financial statements of the Company include the accounts of ETI, IP Resources International, Inc., Aviva Companies Corporation, and WeHealAnimals, Inc. All significant intercompany accounts and transactions are eliminated in consolidation.

Going Concern

These accompanying consolidated financial statements have been prepared assuming the Company will continue as a going concern, which contemplates realization of assets and the satisfaction of liabilities in the normal course of business for a period following the date of these consolidated financial statements. The Company has recurring net losses, negative cash flows from operations and working capital deficits. The Company has raised approximately $ 2.4 million in debt and equity financing for the year ended December 31, 2019. The Company is raising additional capital through debt and equity securities in order to continue the funding of its operations. However, there is no assurance that the Company can raise enough funds or generate sufficient revenues to pay its obligations as they become due, which raises substantial doubt about our ability to continue as a going concern. No adjustments have been made to the carrying value of assets or liabilities as a result of this uncertainty. To reduce the risk of not being able to continue as a going concern, management has implemented its business plan to materialize revenues from potential, future, license agreements, has initiated an equity line of credit offering to raise capital through the sale of its common stock, has engaged a broker/dealer to raise additional capital.

| 23 |

Endonovo Therapeutics, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (continued)

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Critical estimates include the value of shares issued for services, in connection with notes payable agreements, in connection with note extension agreements, and as repayment for outstanding debt, the useful lives of property and equipment, the valuation of the derivative liability, and the valuation of deferred income tax assets. Management uses its historical records and knowledge of its business in making these estimates. Actual results could differ from these estimates.

Cash and cash equivalents

The Company considers all highly liquid investments with an original maturity of three months or less to be cash equivalents. Financial instruments that potentially subject us to a concentration of credit risk consist of cash and cash equivalents. Cash is deposited with what we believe are highly credited, quality institutions. The deposited cash may exceed Federal Deposit Insurance Corporation (“FDIC”) insured limits. At December 31, 2019, the Company does not hold any cash in excess of FDIC limits.

Accounts Receivable

The Company uses the specific identification method for recording the provision for doubtful accounts, which was $0 at December 31, 2019 and 2018. Accounts receivable are written off when all collection attempts have failed.

Property, plant and equipment

Property, plant and equipment are stated at cost. Depreciation is computed using the straight-line method over the estimated useful lives of the assets, which range between five and seven years. Repairs and maintenance are charged to expense as incurred while improvements are capitalized. Upon the sale, retirement or disposal of fixed assets, the accounts are relieved of the cost and the related accumulated depreciation with any gain or loss recorded to the consolidated statements of operations.

Impairment of Long-lived Assets

The Company reviews its long-lived assets for impairment whenever events or changes in business circumstances indicate that the carrying amount of assets may not be fully recoverable or that the useful lives of these assets are no longer appropriate. Each impairment test is based on a comparison of the undiscounted future cash flows generated from the asset group to the recorded value of the asset group. If impairment is indicated, the asset is written down to its estimated fair value.

Equity-Based Compensation

The Company measures equity-based compensation cost at the grant date based on the fair value of the award and recognizes it as expense, net of forfeitures which are recognized as they occur, over the vesting or service period, as applicable, of the stock award using the straight-line method.

| 24 |

Endonovo Therapeutics, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (continued)

The Company measured equity-based compensation using the Black-Scholes option valuation model using the following assumptions:

| For Year Ending December 31, | ||||||||

| 2019 | 2018 | |||||||

| Expected term | 4 years | 2 - 3 years | ||||||

| Exercise price | $11.60 | $29.80 - $47.00 | ||||||

| Expected volatility | 349.60% | 226.00% - 261.00% | ||||||

| Expected dividends | None | None | ||||||

| Risk-free interest rate | 2.28% | 1.58% - 2.06% | ||||||

| Forfeitures | None | None | ||||||

Income Taxes

The Company records a tax provision for the anticipated tax consequences of its reported results of operations. The provision for income taxes is computed using the asset and liability method, under which deferred tax assets and liabilities are recognized for the expected future tax consequences of temporary differences between the financial reporting and tax bases of assets and liabilities, and for operating losses and income tax credit carryforwards. Deferred tax assets and liabilities are measured using the currently enacted tax rates that apply to taxable income in effect for the years in which those tax assets are expected to be realized or settled. The Company records a valuation allowance to reduce deferred tax assets to the amount that is more likely than not to be realized.

The Company has adopted ASC Topic 740, which clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s financial statements. ASC Topic 740 prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return, and also provides guidance on derecognition of tax benefits, classification on the balance sheet, interest and penalties, accounting in interim periods, disclosure and transition. The Company has determined that the adoption did not result in the recognition of any liability for unrecognized tax benefits and that there are no unrecognized tax benefits that would, if recognized, affect the Company’s effective tax rate.

Net Loss per Share

Basic net loss per share is calculated based on the net loss attributable to common shareholders divided by the weighted average number of shares outstanding for the period excluding any dilutive effects of options, warrants, unvested share awards and convertible securities. Diluted net loss per common share assumes the conversion of all dilutive securities using the if-converted method and assumes the exercise or vesting of other dilutive securities, such as options, common shares issuable under convertible debt, warrants and restricted stock using the treasury stock method when dilutive.

Research and Development

Costs relating to the development of new products are expensed as research and development as incurred in accordance with FASB Accounting Standards Codification (“ASC”) 730-10, Research and Development. Research and development costs amounted to $153,126 and $274,265 for the years ended December 31, 2019 and 2018, respectively, and are included in operating expenses in the consolidated statements of operations.

| 25 |

Endonovo Therapeutics, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (continued)

Fair Value of Financial Instruments

Accounting guidance on fair value measurements and disclosures defines fair value, establishes a framework for measuring the fair value of assets and liabilities using a hierarchy system, and defines required disclosures. It clarifies that fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants in the market in which the reporting entity transacts business.

The Company’s balance sheet contains derivative liability that is recorded at fair value on a recurring basis. The three-level valuation hierarchy for disclosure of fair value is as follows:

Level 1: uses quoted market prices in active markets for identical assets or liabilities.

Level 2: uses observable market-based inputs or unobservable inputs that are corroborated by market data.

Level 3: uses unobservable inputs that are not corroborated by market data.

The fair value of the Company’s recorded derivative liability is determined based on unobservable inputs that are not corroborated by market data, which require a Level 3 classification. A Black-Sholes option valuation model was used to determine the fair value. The Company records derivative liability on the condensed consolidated balance sheets at fair value with changes in fair value recorded in the condensed consolidated statements of operation.

The following table presents changes in the liabilities with significant unobservable inputs (Level 3) for the years ended December 31, 2019 and 2018:

| Fair Value Measurements at December 31, 2019 Using | ||||||||||||||||

| Quoted Prices in Active Markets for | Significant Other Observable | Significant Unobservable | ||||||||||||||

| Identical Assets | Inputs | Inputs | ||||||||||||||

| (Level 1) | (Level 2) | (Level 3) | Total | |||||||||||||

| Derivative liability | $ | - | $ | - | $ | 10,599,690 | $ | 10,599,690 | ||||||||

| Total | $ | - | $ | - | $ | 10,599,690 | $ | 10,599,690 | ||||||||

| Fair Value Measurements at December 31, 2018 Using | ||||||||||||||||

| Quoted Prices in Active Markets for | Significant Other Observable | Significant Unobservable | ||||||||||||||

| Identical Assets | Inputs | Inputs | ||||||||||||||

| (Level 1) | (Level 2) | (Level 3) | Total | |||||||||||||

| Derivative liability | $ | - | $ | - | $ | 4,426,026 | $ | 4,426,026 | ||||||||

| Total | $ | - | $ | - | $ | 4,426,026 | $ | 4,426,026 | ||||||||

| 26 |

Endonovo Therapeutics, Inc. and Subsidiaries

Notes to Consolidated Financial Statements (continued)

The following table presents changes in the liabilities with significant unobservable inputs (Level 3) for the years ended December 31, 2019 and 2018:

| Derivative | ||||

| Liability | ||||

| Balance December 31, 2017 | 5,939,600 | |||

| Increase in Derivative Liability resulting from Issuance of convertible debt | 2,864,161 | |||

| Decrease in Derivative Liability resulting from Settlements by debt extinguishment | (1,773,752 | ) | ||

| Increase in Derivative Liability resulting from Change in estimated fair value | (2,603,983 | |||

| Balance December 31, 2018 | 4,426,026 | |||