As filed with the U.S. Securities and Exchange Commission on February 22, 2019

File Nos. 333-179904 and 811-22649

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 | ☒ | |||

| Post-Effective Amendment No. 466 | ☒ |

and/or

| REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 |

☒ | |||

| Amendment No. 466 | ☒ |

(Check appropriate box or boxes)

iShares U.S. ETF Trust

(Exact Name of Registrant as Specified in Charter)

c/o State Street Bank and Trust Company

1 Lincoln Street

Mail Stop SUM0703

Boston, MA 02111

(Address of Principal Executive Office)(Zip Code)

Registrant’s Telephone Number, including Area Code: (415) 670-2000

The Corporation Trust Company

1209 Orange Street

Wilmington, DE 19801

(Name and Address of Agent for Service)

With Copies to:

| MARGERY K. NEALE, ESQ. | DEEPA DAMRE, ESQ. | |

| WILLKIE FARR & GALLAGHER LLP |

BLACKROCK FUND ADVISORS | |

| 787 SEVENTH AVENUE | 400 HOWARD STREET | |

| NEW YORK, NY 10019-6099 | SAN FRANCISCO, CA 94105 |

It is proposed that this filing will become effective (check appropriate box):

| ☐ | Immediately upon filing pursuant to paragraph (b) |

| ☒ | On March 1, 2019 pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | On (date) pursuant to paragraph (a)(1) |

| ☐ | 75 days after filing pursuant to paragraph (a)(2) |

| ☐ | On (date) pursuant to paragraph (a)(2) |

If appropriate, check the following box:

| ☐ | The post-effective amendment designates a new effective date for a previously filed post-effective amendment |

| 2019 Prospectus |

|

| ► | iShares Bloomberg Roll Select Commodity Strategy ETF | CMDY | NYSE ARCA |

| Ticker: CMDY | Stock Exchange: NYSE Arca |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments)1 | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.28% | None | None | 0.01% | 0.29% | (0.01)% | 0.28% | ||||||

| 1 |

The expense information in the table has been restated to reflect current fees. |

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $29 | $90 | $157 | $362 |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $2,345,000 | 50,000 | $225 | 7% | 2% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout the period)

| iShares Bloomberg Roll Select Commodity Strategy ETF | |

| Period

From 04/03/18(a) to 10/31/18 | |

| Net asset value, beginning of period | $ 50.00 |

| Net investment income(b) | 0.58 |

| Net realized and unrealized loss(c) | (2.81) |

| Net decrease from investment operations | (2.23) |

| Net asset value, end of period | $ 47.77 |

| Total Return | |

| Based on net asset value | (4.46)% (d) |

| Ratios to Average Net Assets | |

| Total expenses | 0.28% (e) |

| Total expenses after fees waived | 0.10% (e) |

| Net investment income | 2.01% (e) |

| Supplemental Data | |

| Net assets, end of period (000) | $40,607 |

| Portfolio turnover rate | 0% (d) |

|

(a) Commencement of operations. | |

| (b) Based on average shares outstanding. | |

| (c) The amount reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |

| (d) Not annualized. | |

| (e) Annualized. | |

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 6.0% | 1 | 0.53% | ||

| Greater than 0.5% and Less than 1.0% | 5 | 2.67 | ||

| Greater than 0.0% and Less than 0.5% | 137 | 73.27 | ||

| At NAV | 4 | 2.14 | ||

| Less than 0.0% and Greater than -0.5% | 40 | 21.39 | ||

| 187 | 100.00% |

| Cumulative Total Returns | ||

| Since

Inception | ||

| Fund NAV | (4.46)% | |

| Fund Market | (4.30) | |

| Bloomberg Roll Select Commodity Index | (4.36) |

| Total returns for the period since inception are calculated from the inception date of the Fund (4/3/18). The first day of secondary market trading in shares of the Fund was 4/5/18. |

| The Bloomberg Roll Select Commodity Index is an unmanaged index that aims to reflect the performance of a diversified group of commodities, while also seeking to minimize the effect of contango and maximize the effect of backwardation in connection with periodically switching or “rolling” into new futures contracts. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Commodities Select Strategy ETF | COMT | NASDAQ |

|

|

S-1 |

|

|

1 |

|

|

1 |

|

|

15 |

|

|

18 |

|

|

18 |

|

|

22 |

|

|

31 |

|

|

32 |

|

|

33 |

|

|

34 |

| Ticker: COMT | Stock Exchange: NASDAQ |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses1 |

Acquired

Fund Fees and Expenses1 |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.48% | None | None | 0.00% | 0.48% | (0.00)% | 0.48% | ||||||

| 1 | For the most recently completed fiscal year, the amount rounded to 0.00%. |

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $49 | $154 | $269 | $604 |

| One Year | Since

Fund Inception | ||

| (Inception Date: 10/15/2014) | |||

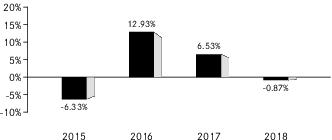

| Return Before Taxes | -6.60% | -7.17% | |

| Return After Taxes on Distributions1 | -10.34% | -8.67% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | -3.68% | -5.81% | |

| S&P GSCI™ Commodity Total Return Index2,3 (Index returns do not reflect deductions for fees, expenses, or taxes) | -13.82% | -13.99% | |

| S&P GSCI™ Dynamic Roll Reduced Energy 70/30 Futures/Equity Blend3 (Index returns do not reflect deductions for fees, expenses, or taxes) | -4.91% | -11.96% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

| 2 | The S&P GSCITM Commodity Total Return Index, the Fund's performance benchmark, is an unmanaged index that measures the performance of general commodity price movements and inflation in the world economy. |

| 3 | The S&P GSCITM Dynamic Roll Reduced Energy 70/30 Futures/Equity Blend is an unmanaged index that is designed to measure the performance of a multi-asset allocation strategy that consists of a futures-based commodities index and an equity-based index that is based on various commodity-related GICS subsectors. |

| ■ | Lower levels of liquidity and market efficiency; |

| ■ | Greater securities price volatility; |

| ■ | Exchange rate fluctuations and exchange controls; |

| ■ | Less availability of public information about issuers; |

| ■ | Limitations on foreign ownership of securities; |

| ■ | Imposition of withholding or other taxes; |

| ■ | Imposition of restrictions on the expatriation of the funds or other assets of the Fund; |

| ■ | Higher transaction and custody costs and delays in settlement procedures; |

| ■ | Difficulties in enforcing contractual obligations; |

| ■ | Lower levels of regulation of the securities markets; |

| ■ | Weaker accounting, disclosure and reporting requirements; and |

| ■ | Legal principles relating to corporate governance, directors’ fiduciary duties and liabilities and stockholders’ rights in markets in which the Fund invests may differ and/or may not be as extensive or protective as those that apply in the U.S. |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $3,518,000 | 100,000 | $700 | 7.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout each period)

| iShares Commodities Select Strategy ETF | |||||||||

| Year

Ended 10/31/18 |

Year

Ended 10/31/17 |

Year

Ended 10/31/16 |

Year

Ended 10/31/15 |

Period

From 10/15/14(a) to 10/31/14 | |||||

| Net asset value, beginning of period | $ 35.97 | $ 32.41 | $ 32.97 | $ 50.68 | $ 50.04 | ||||

| Net investment income (loss)(b) | 0.63 | 0.31 | 0.16 | 0.26 | (0.01) | ||||

| Net realized and unrealized gain (loss)(c) | 2.62 | 3.58 | (0.57) | (17.35) | 0.65 | ||||

| Net increase (decrease) from investment operations | 3.25 | 3.89 | (0.41) | (17.09) | 0.64 | ||||

| Distributions (d) | |||||||||

| From net investment income | (2.04) | (0.33) | (0.15) | (0.61) | — | ||||

| Return of capital | — | — | — | (0.01) | — | ||||

| Total distributions | (2.04) | (0.33) | (0.15) | (0.62) | — | ||||

| Net asset value, end of period | $ 37.18 | $ 35.97 | $ 32.41 | $ 32.97 | $ 50.68 | ||||

| Total Return | |||||||||

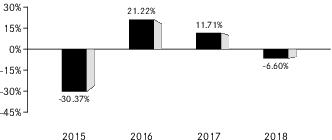

| Based on net asset value | 9.29% (e) | 12.08% | (1.23)% | (33.88)% | 1.28% (f) | ||||

| Ratios to Average Net Assets | |||||||||

| Total expenses | 0.48% | 0.48% | 0.48% | 0.48% | 0.48% (g) | ||||

| Total expenses after fees waived | 0.48% | 0.48% | 0.48% | 0.48% | 0.48% (g) | ||||

| Net investment income (loss) | 1.66% | 0.93% | 0.51% | 0.68% | (0.23)% (g) | ||||

| Supplemental Data | |||||||||

| Net assets, end of period (000) | $728,739 | $258,956 | $320,820 | $253,857 | $20,273 | ||||

| Portfolio turnover rate(h) | 167% | 44% | 43% | 76% | 0% (f) | ||||

|

(a) Commencement of operations. | |||||||||

| (b) Based on average shares outstanding. | |||||||||

| (c) The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |||||||||

| (d) Distributions for annual periods determined in accordance with U.S. federal income tax regulations. | |||||||||

| (e) Includes payment received from an affiliate, which impacted the Fund’s total return. Excluding the payment from an affiliate, the Fund’s total return would have been 9.06%. | |||||||||

| (f) Not annualized. | |||||||||

| (g) Annualized. | |||||||||

| (h) Portfolio turnover rate excludes in-kind transactions. | |||||||||

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 0.5% and Less than 1.0% | 2 | 0.80% | ||

| Greater than 0.0% and Less than 0.5% | 127 | 50.59 | ||

| At NAV | 12 | 4.78 | ||

| Less than 0.0% and Greater than -0.5% | 109 | 43.43 | ||

| Less than -0.5% and Greater than -1.0% | 1 | 0.40 | ||

| 251 | 100.00% |

| Average Annual Total Returns | Cumulative Total Returns | ||||

| 1 Year | Since

Inception |

1 Year | Since

Inception | ||

| Fund NAV | 9.06% (a) | (5.07)% | 9.06% (a) | (18.98)% | |

| Fund Market | 8.91 | (5.16) | 8.91 | (19.29) | |

| S&P GSCITM Commodity Total Return Index | 11.47 | (10.18) | 11.47 | (35.20) | |

| S&P GSCITM Dynamic Roll Reduced Energy 70/30 Futures/Equity Blend | 5.68 | N/A | 5.68 | N/A | |

| Total returns for the period since inception are calculated from the inception date of the Fund (10/15/14). The first day of secondary market trading in shares of the Fund was 10/16/14. | |

| The S&P GSCI™ Commodity Total Return Index, the Fund’s performance benchmark, is an unmanaged index that measures the performance of general commodity price movements and inflation in the world economy. | |

| The S&P GSCI™ Dynamic Roll Reduced Energy 70/30 Futures/Equity Blend is an unmanaged index that is designed to measure the performance of a multi-asset allocation strategy that consists of a futures-based commodities index and an equity-based index that is based on various commodity-related GICS subsectors. The inception date of this index was April 17, 2017. The average annual and cumulative total returns for the period April 17, 2017 through October 31, 2018 were 7.16% and 11.20%, respectively. | |

| (a) | The NAV total return presented in the table for the one-year period differs from the same period return disclosed in the financial highlights. The total return in the financial highlights is calculated in the same manner but differs due to certain adjustments made for financial reporting purposes in accordance with U.S. generally accepted accounting principles. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Gold Strategy ETF | IAUF | CBOE BZX |

| Ticker: IAUF | Stock Exchange: Cboe BZX |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses1 |

Total

Annual Fund Operating Expenses |

Fee Waiver1 | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.25% | None | None | 0.07% | 0.32% | (0.07)% | 0.25% | ||||||

| 1 | The expense information in the table has been restated to reflect current fees. |

| 1 Year | 3 Years | |||

| $26 | $80 |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $2,349,000 | 50,000 | $225 | 7.0%** | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

| ** | The maximum additional charge for creations is as of March 1, 2019. |

(For a share outstanding throughout the period)

| iShares Gold Strategy ETF | |

| Period

From 06/06/18(a) to 10/31/18 | |

| Net asset value, beginning of period | $50.00 |

| Net investment income(b) | 0.27 |

| Net realized and unrealized loss(c) | (3.51) |

| Net decrease from investment operations | (3.24) |

| Net asset value, end of period | $ 46.76 |

| Total Return | |

| Based on net asset value | (6.48)% (d) |

| Ratios to Average Net Assets | |

| Total expenses | 0.25% (e) |

| Total expenses after fees waived | 0.19% (e) |

| Net investment income | 1.45% (e) |

| Supplemental Data | |

| Net assets, end of period (000) | $ 4,676 |

| Portfolio turnover rate(f) | 13% (d) |

|

(a) Commencement of operations. | |

| (b) Based on average shares outstanding. | |

| (c) The amount reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |

| (d) Not annualized. | |

| (e) Annualized. | |

| (f) Portfolio turnover rate excludes in-kind transactions. | |

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 0.0% and Less than 0.5% | 90 | 63.39% | ||

| At NAV | 1 | 0.70 | ||

| Less than 0.0% and Greater than -0.5% | 50 | 35.21 | ||

| Less than -2.0% and Greater than -2.5% | 1 | 0.70 | ||

| 142 | 100.00% |

| Cumulative Total Returns | ||

| Since

Inception | ||

| Fund NAV | (6.48)% | |

| Fund Market | (6.30) | |

| Bloomberg Composite Gold Index | (7.89) |

| Total returns for the period since inception are calculated from the inception date of the Fund (6/6/18). The first day of secondary market trading in shares of the Fund was 6/8/18. |

| The Bloomberg Composite Gold Index is an unmanaged index comprised of exchange -traded gold futures contracts and one or more exchange-traded products backed by or linked to physical gold. The index is designed to track the price performance of gold. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Inflation Hedged Corporate Bond ETF | LQDI | CBOE BZX |

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

14 |

|

|

19 |

|

|

19 |

|

|

20 |

|

|

24 |

|

|

33 |

|

|

34 |

|

|

35 |

|

|

36 |

| Ticker: LQDI | Stock Exchange: Cboe BZX |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.20% | None | None | 0.14% | 0.34% | (0.15)% | 0.19% | ||||||

| 1 Year | 3 Years | |||

| $19 | $61 |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $1,200,000 | 50,000 | $100 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout the period)

| iShares Inflation Hedged Corporate Bond ETF | |

| Period

From 05/08/18(a) to 10/31/18 | |

| Net asset value, beginning of period | $25.00 |

| Net investment income(b) | 0.37 |

| Net realized and unrealized loss(c) | (0.70) |

| Net decrease from investment operations | (0.33) |

| Distributions (d) | |

| From net investment income | (0.36) |

| Total distributions | (0.36) |

| Net asset value, end of period | $ 24.31 |

| Total Return | |

| Based on net asset value | (1.34)% (e) |

| Ratios to Average Net Assets | |

| Total expenses(f) | 0.20% (g) |

| Total expenses after fees waived(f) | 0.05% (g) |

| Net investment income | 3.04% (g) |

| Supplemental Data | |

| Net assets, end of period (000) | $ 9,725 |

| Portfolio turnover rate(h)(i) | 0% (e)(j) |

|

(a) Commencement of operations. | |

| (b) Based on average shares outstanding. | |

| (c) The amount reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |

| (d) Distributions for annual periods determined in accordance with U.S. federal income tax regulations. | |

| (e) Not annualized. | |

| (f) The Fund indirectly bears its proportionate share of fees and expenses incurred by the underlying fund in which the Fund is invested. This ratio does not include these indirect fees and expenses. | |

| (g) Annualized. | |

| (h) Portfolio turnover rate excludes in-kind transactions. | |

| (i) Portfolio turnover rate excludes the portfolio activity of the underlying fund in which the Fund is invested. See the underlying fund's financial highlights for its respective portfolio turnover rates. | |

| (j) Rounds to less than 1%. | |

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 0.5% and Less than 1.0% | 8 | 4.94% | ||

| Greater than 0.0% and Less than 0.5% | 89 | 54.93 | ||

| At NAV | 1 | 0.62 | ||

| Less than 0.0% and Greater than -0.5% | 63 | 38.89 | ||

| Less than -0.5% and Greater than -1.0% | 1 | 0.62 | ||

| 162 | 100.00% |

| Cumulative Total Returns | ||

| Since

Inception | ||

| Fund NAV | (1.34)% | |

| Fund Market | (1.26) | |

| Markit iBoxx® USD Liquid Investment Grade Inflation Hedged Index | (1.25) |

| Total returns for the period since inception are calculated from the inception date of the Fund (5/8/18). The first day of secondary market trading in shares of the Fund was 5/10/18. |

| The Markit iBoxx® USD Liquid Investment Grade Inflation Hedged Index is an unmanaged index that is designed to reflect the inflation hedged performance of U.S. dollar-denominated investment-grade corporate debt. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Interest Rate Hedged Corporate Bond ETF | LQDH | NYSE ARCA |

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

14 |

|

|

17 |

|

|

17 |

|

|

18 |

|

|

21 |

|

|

30 |

|

|

31 |

|

|

32 |

|

|

33 |

| Ticker: LQDH | Stock Exchange: NYSE Arca |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.30% | None | None | 0.15% | 0.45% | (0.20)% | 0.25% | ||||||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $26 | $80 | $189 | $505 |

| One Year | Since

Fund Inception | ||

| (Inception Date: 5/27/2014) | |||

| Return Before Taxes | -1.79% | 1.05% | |

| Return After Taxes on Distributions1 | -3.43% | -0.23% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | -0.75% | 0.27% | |

| Markit iBoxx USD Liquid Investment Grade Interest Rate Hedged Swaps Index2 (Index returns do not reflect deductions for fees, expenses, or taxes) | -1.47% | 1.84% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

| 2 | The Markit iBoxx USD Liquid Investment Grade Interest Rate Hedged Swaps Index is an unmanaged index that is designed to reflect the duration hedged performance of U.S. dollar-denominated investment-grade corporate debt. |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $4,696,000 | 50,000 | $150 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout each period)

| iShares Interest Rate Hedged Corporate Bond ETF | |||||||||

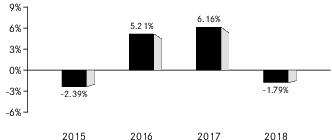

| Year

Ended 10/31/18 |

Year

Ended 10/31/17 |

Year

Ended 10/31/16 |

Year

Ended 10/31/15 |

Period

From 05/27/14(a) to 10/31/14 | |||||

| Net asset value, beginning of period | $ 96.62 | $ 92.49 | $ 92.13 | $ 97.95 | $100.32 | ||||

| Net investment income(b) | 3.16 | 2.76 | 2.74 | 2.95 | 1.32 | ||||

| Net realized and unrealized gain (loss)(c) | (1.16) | 3.73 | (0.29) | (5.82) | (2.36) | ||||

| Net increase (decrease) from investment operations | 2.00 | 6.49 | 2.45 | (2.87) | (1.04) | ||||

| Distributions (d) | |||||||||

| From net investment income | (2.83) | (2.36) | (2.09) | (2.81) | (1.32) | ||||

| Return of capital | — | — | — | (0.14) | (0.01) | ||||

| Total distributions | (2.83) | (2.36) | (2.09) | (2.95) | (1.33) | ||||

| Net asset value, end of period | $ 95.79 | $ 96.62 | $ 92.49 | $ 92.13 | $ 97.95 | ||||

| Total Return | |||||||||

| Based on net asset value | 2.08% | 7.11% | 2.70% | (2.97)% | (1.05)% (e) | ||||

| Ratios to Average Net Assets | |||||||||

| Total expenses(f) | 0.30% | 0.30% | 0.30% | 0.30% | 0.30% (g) | ||||

| Total expenses after fees waived(f) | 0.10% | 0.10% | 0.10% | 0.11% | 0.11% (g) | ||||

| Net investment income | 3.27% | 2.91% | 3.01% | 3.12% | 3.09% (g) | ||||

| Supplemental Data | |||||||||

| Net assets, end of period (000) | $215,530 | $77,295 | $32,372 | $18,427 | $ 9,795 | ||||

| Portfolio turnover rate(h)(i) | 2% | 0% (j) | 2% | 8% | 4% (e) | ||||

|

(a) Commencement of operations. | |||||||||

| (b) Based on average shares outstanding. | |||||||||

| (c) The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |||||||||

| (d) Distributions for annual periods determined in accordance with U.S. federal income tax regulations. | |||||||||

| (e) Not annualized. | |||||||||

| (f) The Fund indirectly bears its proportionate share of fees and expenses incurred by the underlying fund in which the Fund is invested. This ratio does not include these indirect fees and expenses. | |||||||||

| (g) Annualized. | |||||||||

| (h) Portfolio turnover rate excludes in-kind transactions. | |||||||||

| (i) Portfolio turnover rate excludes the portfolio activity of the underlying fund in which the Fund is invested. See the underlying fund's financial highlights for its respective portfolio turnover rates. | |||||||||

| (j) Rounds to less than 1%. | |||||||||

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 0.5% and Less than 1.0% | 1 | 0.40% | ||

| Greater than 0.0% and Less than 0.5% | 148 | 58.97 | ||

| At NAV | 11 | 4.38 | ||

| Less than 0.0% and Greater than -0.5% | 91 | 36.25 | ||

| 251 | 100.00% |

| Average Annual Total Returns | Cumulative Total Returns | ||||

| 1 Year | Since

Inception |

1 Year | Since

Inception | ||

| Fund NAV | 2.08% | 1.71% | 2.08% | 7.80% | |

| Fund Market | 1.94 | 1.70 | 1.94 | 7.74 | |

| Markit iBoxx® USD Liquid Investment Grade Interest Rate Hedged Swaps Index | 2.43 | 2.56 | 2.43 | 11.83 | |

| Total returns for the period since inception are calculated from the inception date of the Fund (5/27/14). The first day of secondary market trading in shares of the Fund was 5/28/14. |

| The Markit iBoxx USD Liquid Investment Grade Interest Rate Hedged Swaps Index is an unmanaged index that is designed to reflect the duration hedged performance of U.S. dollar-denominated investment-grade corporate debt. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Interest Rate Hedged Emerging Markets Bond ETF | EMBH | NYSE ARCA |

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

21 |

|

|

22 |

|

|

22 |

|

|

24 |

|

|

27 |

|

|

36 |

|

|

37 |

|

|

38 |

|

|

39 |

| Ticker: EMBH | Stock Exchange: NYSE Arca |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.75% | None | None | 0.38% | 1.13% | (0.65)% | 0.48% | ||||||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $49 | $154 | $422 | $1189 |

| One Year | Since

Fund Inception | ||

| (Inception Date: 7/22/2015) | |||

| Return Before Taxes | -3.77% | 3.29% | |

| Return After Taxes on Distributions1 | -5.68% | 1.50% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | -2.21% | 1.72% | |

| J.P. Morgan EMBI Global Core Swap Hedged Index (Index returns do not reflect deductions for fees, expenses, or taxes) | -3.61% | 3.57% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in certain Eastern European countries; |

| ■ | Risks in connection with the maintenance of the Fund's portfolio securities and cash with foreign sub-custodians and securities depositories, including the risk that appropriate sub-custody arrangements will not be available to the Fund; |

| ■ | The risk that the Fund's ownership rights in portfolio securities could be lost through fraud or negligence as a result of the fact that ownership in shares of certain Eastern European companies is recorded by the companies themselves and by registrars, rather than a central registration system; |

| ■ | The risk that the Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because certain Eastern European banking institutions and registrars are not guaranteed by their respective governments; and |

| ■ | Risks in connection with Eastern European countries' dependence on the economic health of Western European countries and the EU as a whole. |

| ■ | High yield securities may be issued by less creditworthy issuers. Issuers of high yield securities may have a larger amount of outstanding debt relative to their assets than issuers of investment-grade bonds. In the event of an issuer’s bankruptcy, claims of other creditors may have priority over the claims of high yield securities holders, leaving few or no assets available to repay high yield securities holders. |

| ■ | Prices of high yield securities are subject to extreme price fluctuations. Adverse changes in an issuer’s industry and general economic conditions may have a greater impact on the prices of high yield securities than on other higher rated fixed-income securities. The credit rating of a high yield security does not necessarily address its market value risk. Ratings and market value may change from time to time, positively or negatively, to reflect new developments regarding the issuer. |

| ■ | Issuers of high yield securities may be unable to meet their interest or principal payment obligations because of an economic downturn, specific issuer developments, or the unavailability of additional financing. |

| ■ | High yield securities frequently have redemption features that permit an issuer to repurchase the security from the Fund or the Underlying Fund before it matures. If the issuer redeems high yield securities held by the Fund or the Underlying Fund, the Fund or the Underlying Fund may have to invest the proceeds in bonds with lower yields and may lose income. |

| ■ | High yield securities may be less liquid than higher rated fixed-income securities, even under normal economic conditions. There are fewer dealers in the high yield securities market, and there may be significant differences in the prices quoted for high yield securities by the dealers. Because high yield securities are less liquid, judgment may play a greater role in valuing certain of the Fund’s or Underlying Fund's securities than is the case with securities trading in a more liquid market. |

| ■ | The Fund or the Underlying Fund may incur expenses to the extent necessary to seek recovery upon default or to negotiate new terms with a defaulting issuer. |

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in Russia; |

| ■ | Risks in connection with the maintenance of the Fund’s or the Underlying Fund's portfolio securities and cash with foreign sub-custodians and securities depositories, including the risk that appropriate sub-custody arrangements will not be available to the Fund or the Underlying Fund; |

| ■ | The risk that the Fund’s or the Underlying Fund's ownership rights in portfolio securities could be lost through fraud or negligence because ownership in shares of Russian companies is recorded by the companies themselves and by registrars, rather than by a central registration system; and |

| ■ | The risk that the Fund or the Underlying Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, |

| and because Russian banking institutions and registrars are not guaranteed by the Russian government. |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $1,238,000 | 50,000 | $300 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout each period)

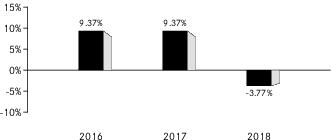

| iShares Interest Rate Hedged Emerging Markets Bond ETF | |||||||

| Year

Ended 10/31/18 |

Year

Ended 10/31/17 |

Year

Ended 10/31/16 |

Period

From 07/22/15(a) to 10/31/15 | ||||

| Net asset value, beginning of period | $ 26.44 | $25.06 | $24.20 | $25.05 | |||

| Net investment income(b) | 1.06 | 1.11 | 1.17 | 0.33 | |||

| Net realized and unrealized gain (loss)(c) | (1.19) | 1.24 | 0.61 | (0.95) | |||

| Net increase (decrease) from investment operations | (0.13) | 2.35 | 1.78 | (0.62) | |||

| Distributions (d) | |||||||

| From net investment income | (1.03) | (0.97) | (0.89) | (0.23) | |||

| Return of capital | — | — | (0.03) | (0.00) (e) | |||

| Total distributions | (1.03) | (0.97) | (0.92) | (0.23) | |||

| Net asset value, end of period | $ 25.28 | $26.44 | $ 25.06 | $24.20 | |||

| Total Return | |||||||

| Based on net asset value | (0.51)% | 9.57% | 7.49% | (2.43)% (f) | |||

| Ratios to Average Net Assets | |||||||

| Total expenses(g) | 0.75% | 0.75% | 0.75% | 0.75% (h) | |||

| Total expenses after fees waived(g) | 0.10% | 0.10% | 0.10% | 0.12% (h) | |||

| Net investment income | 4.07% | 4.32% | 4.82% | 4.86% (h) | |||

| Supplemental Data | |||||||

| Net assets, end of period (000) | $13,902 | $ 2,644 | $ 2,506 | $ 2,420 | |||

| Portfolio turnover rate(i)(j) | 0% (k) | 2% | 3% | 0% (f) | |||

|

(a) Commencement of operations. | |||||||

| (b) Based on average shares outstanding. | |||||||

| (c) The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |||||||

| (d) Distributions for annual periods determined in accordance with U.S. federal income tax regulations. | |||||||

| (e) Rounds to less than $0.01. | |||||||

| (f) Not annualized. | |||||||

| (g) The Fund indirectly bears its proportionate share of fees and expenses incurred by the underlying fund in which the Fund is invested. This ratio does not include these indirect fees and expenses. | |||||||

| (h) Annualized. | |||||||

| (i) Portfolio turnover rate excludes in-kind transactions. | |||||||

| (j) Portfolio turnover rate excludes the portfolio activity of the underlying fund in which the Fund is invested. See the underlying fund's financial highlights for its respective portfolio turnover rates. | |||||||

| (k) Rounds to less than 1%. | |||||||

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 0.0% and Less than 0.5% | 106 | 42.23% | ||

| At NAV | 9 | 3.59 | ||

| Less than 0.0% and Greater than -0.5% | 136 | 54.18 | ||

| 251 | 100.00% |

| Average Annual Total Returns | Cumulative Total Returns | ||||

| 1 Year | Since

Inception |

1 Year | Since

Inception | ||

| Fund NAV | (0.51)% | 4.17% | (0.51)% | 14.33% | |

| Fund Market | (0.58) | 4.15 | (0.58) | 14.28 | |

| J.P. Morgan EMBI Global Core Swap Hedged Index | 0.34 | 4.67 | 0.34 | 16.13 | |

| Total returns for the period since inception are calculated from the inception date of the Fund (7/22/15). The first day of secondary market trading in shares of the Fund was 7/23/15. |

| The J.P. Morgan EMBI Global Core Swap Hedged Index is an unmanaged index that consists of the J.P. Morgan EMBI® Global Core Index plus interest rate swaps that intend to hedge the interest rate exposure of the J.P. Morgan EMBI® Global Core Index. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Interest Rate Hedged High Yield Bond ETF | HYGH | NYSE ARCA |

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

14 |

|

|

19 |

|

|

19 |

|

|

20 |

|

|

23 |

|

|

32 |

|

|

33 |

|

|

34 |

|

|

35 |

| Ticker: HYGH | Stock Exchange: NYSE Arca |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.65% | None | None | 0.48% | 1.13% | (0.60)% | 0.53% | ||||||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $54 | $170 | $438 | $1203 |

| One Year | Since

Fund Inception | ||

| (Inception Date: 5/27/2014) | |||

| Return Before Taxes | -0.87% | 1.73% | |

| Return After Taxes on Distributions1 | -3.29% | -0.55% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | -0.47% | 0.29% | |

| Markit iBoxx USD Liquid High Yield Interest Rate Hedged Swaps Index2 (Index returns do not reflect deductions for fees, expenses, or taxes) | -1.02% | 2.25% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

| 2 | The Markit iBoxx USD Liquid High Yield Interest Rate Hedged Swaps Index is an unmanaged index that reflects the duration hedged performance of U.S. dollar-denominated high yield corporate debt. |

| ■ | High yield securities may be issued by less creditworthy issuers. Issuers of high yield securities may have a larger amount of outstanding debt relative to their assets than issuers of investment-grade bonds. In the event of an issuer’s bankruptcy, claims of other creditors may have priority over the claims of high yield securities holders, leaving few or no assets available to repay high yield securities holders. |

| ■ | Prices of high yield securities are subject to extreme price fluctuations. Adverse changes in an issuer’s industry and general economic conditions may have a greater impact on the prices of high yield securities than on other higher rated fixed-income securities. The credit rating of a high yield security does not necessarily address its market value risk. Ratings and market value may change from time to time, positively or negatively, to reflect new developments regarding the issuer. |

| ■ | Issuers of high yield securities may be unable to meet their interest or principal payment obligations because of an economic downturn, specific issuer developments, or the unavailability of additional financing. |

| ■ | High yield securities frequently have redemption features that permit an issuer to repurchase the security from the Fund or the Underlying Fund before it matures. If the issuer redeems high yield securities held by the Fund or the Underlying Fund, the Fund or the Underlying Fund may have to invest the proceeds in bonds with lower yields and may lose income. |

| ■ | High yield securities may be less liquid than higher rated fixed-income securities, even under normal economic conditions. There are fewer dealers in the high yield securities market, and there may be significant differences in the prices quoted for high yield securities by the dealers. Because high yield securities are less liquid, judgment may play a greater role in valuing certain of the Fund’s or Underlying Fund's securities than is the case with securities trading in a more liquid market. |

| ■ | The Fund or the Underlying Fund may incur expenses to the extent necessary to seek recovery upon default or to negotiate new terms with a defaulting issuer. |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $4,456,000 | 50,000 | $150 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout each period)

| iShares Interest Rate Hedged High Yield Bond ETF | |||||||||

| Year

Ended 10/31/18 |

Year

Ended 10/31/17 |

Year

Ended 10/31/16 |

Year

Ended 10/31/15 |

Period

From 05/27/14(a) to 10/31/14 | |||||

| Net asset value, beginning of period | $ 91.78 | $ 87.42 | $ 87.66 | $ 96.93 | $100.10 | ||||

| Net investment income(b) | 4.98 | 4.57 | 4.86 | 4.80 | 1.86 | ||||

| Net realized and unrealized gain (loss)(c) | (1.46) | 4.21 | (0.94) | (9.29) | (2.87) | ||||

| Net increase (decrease) from investment operations | 3.52 | 8.78 | 3.92 | (4.49) | (1.01) | ||||

| Distributions (d) | |||||||||

| From net investment income | (4.83) | (4.42) | (4.16) | (4.74) | (2.15) | ||||

| Return of capital | — | — | — | (0.04) | (0.01) | ||||

| Total distributions | (4.83) | (4.42) | (4.16) | (4.78) | (2.16) | ||||

| Net asset value, end of period | $ 90.47 | $ 91.78 | $ 87.42 | $ 87.66 | $ 96.93 | ||||

| Total Return | |||||||||

| Based on net asset value | 3.93% | 10.26% | 4.73% | (4.77)% | (1.03)% (e) | ||||

| Ratios to Average Net Assets | |||||||||

| Total expenses(f) | 0.65% | 0.65% | 0.65% | 0.65% | 0.65% (g) | ||||

| Total expenses after fees waived(f) | 0.05% | 0.05% | 0.05% | 0.06% | 0.06% (g) | ||||

| Net investment income | 5.46% | 5.04% | 5.78% | 5.21% | 4.41% (g) | ||||

| Supplemental Data | |||||||||

| Net assets, end of period (000) | $416,178 | $137,670 | $30,596 | $48,215 | $ 43,619 | ||||

| Portfolio turnover rate(h)(i) | 0% (j) | 0% | 0% (j) | 3% | 3% (e) | ||||

|

(a) Commencement of operations. | |||||||||

| (b) Based on average shares outstanding. | |||||||||

| (c) The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |||||||||

| (d) Distributions for annual periods determined in accordance with U.S. federal income tax regulations. | |||||||||

| (e) Not annualized. | |||||||||

| (f) The Fund indirectly bears its proportionate share of fees and expenses incurred by the underlying fund in which the Fund is invested. This ratio does not include these indirect fees and expenses. | |||||||||

| (g) Annualized. | |||||||||

| (h) Portfolio turnover rate excludes in-kind transactions. | |||||||||

| (i) Portfolio turnover rate excludes the portfolio activity of the underlying fund in which the Fund is invested. See the underlying fund's financial highlights for its respective portfolio turnover rates. | |||||||||

| (j) Rounds to less than 1%. | |||||||||

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 1.0% and Less than 1.5% | 1 | 0.40% | ||

| Greater than 0.5% and Less than 1.0% | 9 | 3.59 | ||

| Greater than 0.0% and Less than 0.5% | 103 | 41.04 | ||

| At NAV | 10 | 3.98 | ||

| Less than 0.0% and Greater than -0.5% | 128 | 50.99 | ||

| 251 | 100.00% |

| Average Annual Total Returns | Cumulative Total Returns | ||||

| 1 Year | Since

Inception |

1 Year | Since

Inception | ||

| Fund NAV | 3.93% | 2.82% | 3.93% | 13.11% | |

| Fund Market | 3.98 | 2.83 | 3.98 | 13.19 | |

| Markit iBoxx® USD Liquid High Yield Interest Rate Hedged Swaps Index | 4.01 | 3.44 | 4.01 | 16.12 | |

| Total returns for the period since inception are calculated from the inception date of the Fund (5/27/14). The first day of secondary market trading in shares of the Fund was 5/28/14. |

| The Markit iBoxx USD Liquid High Yield Interest Rate Hedged Swaps Index is an unmanaged index that reflects the duration hedged performance of U.S. dollar-denominated high yield corporate debt. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Short Maturity Bond ETF | NEAR | CBOE BZX |

BOND ETF

| Ticker: NEAR | Stock Exchange: Cboe BZX |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Total

Annual Fund Operating Expenses | |||

| 0.25% | None | None | 0.25% | |||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $26 | $80 | $141 | $318 |

| One Year | Five Years | Since

Fund Inception | |||

| (Inception Date: 9/25/2013) | |||||

| Return Before Taxes | 1.71% | 1.22% | 1.22% | ||

| Return After Taxes on Distributions1 | 0.79% | 0.66% | 0.68% | ||

| Return After Taxes on Distributions and Sale of Fund Shares1 | 1.01% | 0.69% | 0.69% | ||

| Bloomberg Barclays Short-Term Government/Corporate Index2 (Index returns do not reflect deductions for fees, expenses or taxes) | 1.99% | 0.84% | 0.81% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

| 2 | The Bloomberg Barclays Short-Term Government/Corporate Index is an unmanaged index that measures the performance of government and corporate securities with less than one year remaining to maturity. |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $2,501,000 | 50,000 | $600 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout each period)

| iShares Short Maturity Bond ETF | |||||||||

| Year

Ended 10/31/18 |

Year

Ended 10/31/17 |

Year

Ended 10/31/16 |

Year

Ended 10/31/15 |

Year

Ended 10/31/14 | |||||

| Net asset value, beginning of year | $ 50.25 | $ 50.17 | $ 50.04 | $ 50.15 | $ 50.07 | ||||

| Net investment income(a) | 1.11 | 0.74 | 0.50 | 0.44 | 0.44 | ||||

| Net realized and unrealized gain (loss)(b) | (0.23) | 0.04 | 0.14 | (0.13) | 0.04 | ||||

| Net increase from investment operations | 0.88 | 0.78 | 0.64 | 0.31 | 0.48 | ||||

| Distributions (c) | |||||||||

| From net investment income | (1.01) | (0.70) | (0.51) | (0.42) | (0.40) | ||||

| Total distributions | (1.01) | (0.70) | (0.51) | (0.42) | (0.40) | ||||

| Net asset value, end of year | $ 50.12 | $ 50.25 | $ 50.17 | $ 50.04 | $ 50.15 | ||||

| Total Return | |||||||||

| Based on net asset value | 1.78% | 1.57% | 1.28% | 0.62% | 0.96% | ||||

| Ratios to Average Net Assets | |||||||||

| Total expenses | 0.25% | 0.25% | 0.25% | 0.25% | 0.25% | ||||

| Net investment income | 2.21% | 1.47% | 1.01% | 0.87% | 0.87% | ||||

| Supplemental Data | |||||||||

| Net assets, end of year (000) | $4,981,818 | $2,909,738 | $2,021,893 | $1,781,306 | $418,732 | ||||

| Portfolio turnover rate(d) | 48% | 56% | 79% | 23% | 35% | ||||

|

(a) Based on average shares outstanding. | |||||||||

| (b) The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |||||||||

| (c) Distributions for annual periods determined in accordance with U.S. federal income tax regulations. | |||||||||

| (d) Portfolio turnover rate excludes in-kind transactions. | |||||||||

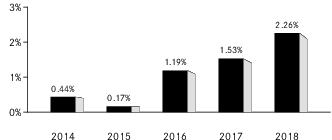

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 0.0% and Less than 0.5% | 203 | 80.87% | ||

| At NAV | 14 | 5.58 | ||

| Less than 0.0% and Greater than -0.5% | 34 | 13.55 | ||

| 251 | 100.00% |

| Average Annual Total Returns | Cumulative Total Returns | ||||||

| 1 Year | 5 Years | Since

Inception |

1 Year | 5 Years | Since

Inception | ||

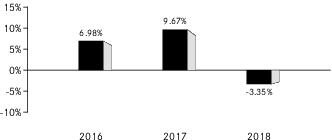

| Fund NAV | 1.78% | 1.24% | 1.24% | 1.78% | 6.36% | 6.51% | |

| Fund Market | 1.78 | 1.24 | 1.25 | 1.78 | 6.36 | 6.53 | |

| Bloomberg Barclays Short-Term Government/Corporate Index | 1.68 | 0.76 | 0.74 | 1.68 | 3.84 | 3.85 | |

| Total returns for the period since inception are calculated from the inception date of the Fund (9/25/13). The first day of secondary market trading in shares of the Fund was 9/26/13. |

| The Bloomberg Barclays Short-Term Government/Corporate Index is an unmanaged index that measures the performance of government and corporate securities with less than one year remaining to maturity. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Short Maturity Municipal Bond ETF | MEAR | CBOE BZX |

MUNICIPAL BOND ETF

| Ticker: MEAR | Stock Exchange: Cboe BZX |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Total

Annual Fund Operating Expenses | |||

| 0.25% | None | None | 0.25% | |||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $26 | $80 | $141 | $318 |

| One Year | Since

Fund Inception | ||

| (Inception Date: 3/3/2015) | |||

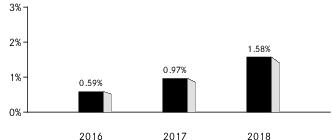

| Return Before Taxes | 1.58% | 0.91% | |

| Return After Taxes on Distributions1 | 1.58% | 0.91% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | 1.50% | 0.93% | |

| Bloomberg Barclays Municipal Bond: 1 Year (1-2) Index2 (Index returns do not reflect deductions for fees, expenses, or taxes) | 1.74% | 0.87% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

| 2 | The Bloomberg Barclays Municipal Bond: 1 Year (1-2) Index is an unmanaged index comprised of national municipal bond issues having a maturity of at least one year and less than two years. |

| ■ | Credit Quality of Issuers — based on bond ratings and other factors, including economic and financial conditions. |

| ■ | Yield Analysis — takes into account factors such as the different yields available on different types of obligations and the shape of the yield curve (longer-term obligations typically have higher yields). |

| ■ | Maturity Analysis — the weighted average maturity of the portfolio will be maintained within a desirable range as determined from time to time. Factors considered include portfolio activity, maturity of the supply of available bonds and the shape of the yield curve. Maturity of a debt security refers to the date upon which debt securities are due to be repaid, that is, the date when the issuer generally must pay back the face amount of the security. The securities to be selected will have remaining maturities of up to five years, calculated off the put dates. |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $2,494,500 | 50,000 | $300 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout each period)

| iShares Short Maturity Municipal Bond ETF | |||||||

| Year

Ended 10/31/18 |

Year

Ended 10/31/17 |

Year

Ended 10/31/16 |

Period

From 03/03/15(a) to 10/31/15 | ||||

| Net asset value, beginning of period | $ 50.01 | $ 50.02 | $ 50.07 | $ 50.00 | |||

| Net investment income(b) | 0.68 | 0.49 | 0.39 | 0.20 | |||

| Net realized and unrealized gain (loss)(c) | (0.21) | (0.03) | (0.04) | 0.04 | |||

| Net increase from investment operations | 0.47 | 0.46 | 0.35 | 0.24 | |||

| Distributions (d) | |||||||

| From net investment income | (0.63) | (0.47) | (0.40) | (0.17) | |||

| Total distributions | (0.63) | (0.47) | (0.40) | (0.17) | |||

| Net asset value, end of period | $ 49.85 | $ 50.01 | $ 50.02 | $ 50.07 | |||

| Total Return | |||||||

| Based on net asset value | 0.95% | 0.93% | 0.69% | 0.48% (e) | |||

| Ratios to Average Net Assets | |||||||

| Total expenses | 0.25% | 0.25% | 0.25% | 0.25% (f) | |||

| Total expenses after fees waived | 0.25% | 0.25% | 0.25% | 0.25% (f) | |||

| Net investment income | 1.35% | 0.99% | 0.79% | 0.59% (f) | |||

| Supplemental Data | |||||||

| Net assets, end of period (000) | $127,111 | $52,507 | $35,012 | $35,049 | |||

| Portfolio turnover rate(g) | 221% | 163% | 100% | 184% (e) | |||

|

(a) Commencement of operations. | |||||||

| (b) Based on average shares outstanding. | |||||||

| (c) The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |||||||

| (d) Distributions for annual periods determined in accordance with U.S. federal income tax regulations. | |||||||

| (e) Not annualized. | |||||||

| (f) Annualized. | |||||||

| (g) Portfolio turnover rate excludes in-kind transactions. | |||||||

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 0.0% and Less than 0.5% | 154 | 61.35% | ||

| At NAV | 8 | 3.19 | ||

| Less than 0.0% and Greater than -0.5% | 89 | 35.46 | ||

| 251 | 100.00% |

| Average Annual Total Returns | Cumulative Total Returns | ||||

| 1 Year | Since

Inception |

1 Year | Since

Inception | ||

| Fund NAV | 0.95% | 0.84% | 0.95% | 3.10% | |

| Fund Market | 1.01 | 0.86 | 1.01 | 3.20 | |

| Bloomberg Barclays Municipal Bond: 1 Year (1-2) Index | 0.65 | 0.72 | 0.65 | 2.67 | |

| Total returns for the period since inception are calculated from the inception date of the Fund (3/3/15). The first day of secondary market trading in shares of the Fund was 3/5/15. |

| The Bloomberg Barclays Municipal Bond: 1 Year (1-2) Index is an unmanaged index comprised of national municipal bond issues having a maturity of at least one year and less than two years. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Ultra Short-Term Bond ETF | ICSH | CBOE BZX |

| Ticker: ICSH | Stock Exchange: Cboe BZX |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Total

Annual Fund Operating Expenses | |||

| 0.08% | None | None | 0.08% | |||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $8 | $26 | $45 | $103 |

| One Year | Five Years | Since

Fund Inception | |||

| (Inception Date: 12/11/2013) | |||||

| Return Before Taxes | 2.26% | 1.12% | 1.10% | ||

| Return After Taxes on Distributions1 | 1.35% | 0.65% | 0.65% | ||

| Return After Taxes on Distributions and Sale of Fund Shares1 | 1.33% | 0.65% | 0.64% | ||

| ICE BofAML 6-Month US Treasury Bill Index2 (Index returns do not reflect deductions for fees, expenses or taxes) | 1.92% | 0.78% | 0.77% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

| 2 | The ICE BofAML 6-Month US Treasury Bill Index is an unmanaged index that measures the performance of government securities with less than six months remaining to maturity. |

securities, instruments of non-U.S. issuers, privately-issued securities, ABS and MBS, structured securities, municipal bonds, repurchase agreements, money market instruments and investment companies. The Fund invests a significant portion of its assets in securities issued by financial institutions, such as banks, broker-dealers and insurance companies. BFA or its affiliates may advise the money market funds and investment companies in which the Fund may invest.

investment strategy meetings, market outlook meetings where investment professionals present their views on the various market sectors, and portfolio strategy meetings where lead portfolio managers discuss asset allocation, portfolio risk, and investment themes. The macro, firm-level view is a consideration in setting the investment strategy.

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $2,507,000 | 50,000 | $500 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout each period)

| iShares Ultra Short-Term Bond ETF | |||||||||

| Year

Ended 10/31/18 |

Year

Ended 10/31/17 |

Year

Ended 10/31/16 |

Year

Ended 10/31/15 |

Period

From 12/11/13(a) to 10/31/14 | |||||

| Net asset value, beginning of period | $ 50.12 | $ 50.04 | $ 49.97 | $ 50.08 | $ 49.99 | ||||

| Net investment income(b) | 1.16 | 0.71 | 0.47 | 0.24 | 0.16 | ||||

| Net realized and unrealized gain (loss)(c) | (0.16) | 0.02 | (0.02) | (0.07) | 0.06 | ||||

| Net increase from investment operations | 1.00 | 0.73 | 0.45 | 0.17 | 0.22 | ||||

| Distributions (d) | |||||||||

| From net investment income | (0.97) | (0.65) | (0.38) | (0.24) | (0.13) | ||||

| From net realized gain | — | — | — | (0.04) | — | ||||

| Total distributions | (0.97) | (0.65) | (0.38) | (0.28) | (0.13) | ||||

| Net asset value, end of period | $ 50.15 | $ 50.12 | $ 50.04 | $ 49.97 | $ 50.08 | ||||

| Total Return | |||||||||

| Based on net asset value | 2.02% | 1.47% | 0.90% | 0.32% | 0.45% (e) | ||||

| Ratios to Average Net Assets | |||||||||

| Total expenses | 0.08% | 0.09% | 0.18% | 0.18% | 0.18% (f) | ||||

| Net investment income | 2.33% | 1.43% | 0.93% | 0.47% | 0.35% (f) | ||||

| Supplemental Data | |||||||||

| Net assets, end of period (000) | $601,794 | $187,932 | $25,018 | $12,493 | $15,024 | ||||

| Portfolio turnover rate(g) | 32% | 11% | 139% | 41% | 71% (e) | ||||

|

(a) Commencement of operations. | |||||||||

| (b) Based on average shares outstanding. | |||||||||

| (c) The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund’s underlying securities. | |||||||||

| (d) Distributions for annual periods determined in accordance with U.S. federal income tax regulations. | |||||||||

| (e) Not annualized. | |||||||||

| (f) Annualized. | |||||||||

| (g) Portfolio turnover rate excludes in-kind transactions. | |||||||||

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 2.0% and Less than 2.5% | 1 | 0.40% | ||

| Greater than 0.0% and Less than 0.5% | 242 | 96.41 | ||

| At NAV | 5 | 1.99 | ||

| Less than 0.0% and Greater than -0.5% | 3 | 1.20 | ||

| 251 | 100.00% |

| Average Annual Total Returns | Cumulative Total Returns | ||||

| 1 Year | Since

Inception |

1 Year | Since

Inception | ||

| Fund NAV | 2.02% | 1.06% | 2.02% | 5.27% | |

| Fund Market | 2.08 | 1.07 | 2.08 | 5.33 | |

| ICE BofAML 6-Month US Treasury Bill Index | 1.68 | 0.71 | 1.68 | 3.52 | |

| Total returns for the period since inception are calculated from the inception date of the Fund (12/11/13). The first day of secondary market trading in shares of the Fund was 12/13/13. |

| The ICE BofAML 6-Month US Treasury Bill Index is an unmanaged index that measures the performance of government securities with less than six months remaining to maturity. |

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

| 2019 Prospectus |

|

| ► | iShares Interest Rate

Hedged Long-Term Corporate Bond ETF | IGBH | NYSE ARCA |

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

16 |

|

|

22 |

|

|

22 |

|

|

23 |

|

|

26 |

|

|

35 |

|

|

36 |

|

|

37 |

|

|

38 |

| Ticker: IGBH | Stock Exchange: NYSE Arca |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.35% | None | None | 0.06% | 0.41% | (0.25)% | 0.16% | ||||||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $16 | $52 | $150 | $440 |

| One Year | Since

Fund Inception | ||

| (Inception Date: 7/22/2015) | |||

| Return Before Taxes | -3.35% | 2.47% | |

| Return After Taxes on Distributions1 | -5.28% | 1.00% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | -1.65% | 1.30% | |

| Bloomberg Barclays U.S. Long Credit Interest Rate Swaps Hedged Index2 (Index returns do not reflect deductions for fees, expenses, or taxes) | -3.32% | 3.09% | |

| ICE Q70A Custom Index2 (Index returns do not reflect deductions for fees, expenses, or taxes) | -3.82% | N/A 3 |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

| 2 | The Bloomberg Barclays U.S. Long Credit Interest Rate Swaps Hedged Index is an unmanaged index that consists of the Bloomberg Barclays U.S. Long Credit Index plus interest rate swaps that intend to hedge the interest rate exposure of the Bloomberg Barclays U.S. Long Credit Index. On August 1, 2018, the Fund's performance benchmark changed from the Bloomberg Barclays U.S. Long Credit Interest Rate Swaps Hedged Index to the ICE Q70A Custom Index. The ICE Q70A Custom Index is an index that consists of the ICE BofAML 10+ Year US Corporate Index plus interest rate swaps that intend to hedge the interest rate exposure of the ICE BofAML 10+ Year US Corporate Index. The ICE Q70A Custom Index more accurately reflects the investment strategy of the Fund because the Underlying Fund tracks the ICE BofAML 10+ Year US Corporate Index as of August 1, 2018. Prior to August 1, 2018, the Underlying Fund tracked the Bloomberg Barclays U.S. Long Credit Index. |

| 3 | The inception date of the ICE Q70A Custom Index was December 31, 2017. The average annual total return of this index for the period December 31, 2017 through December 31, 2018 was -3.82%. |

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in Russia; |

| ■ | Risks in connection with the maintenance of the Fund’s or the Underlying Fund's portfolio securities and cash with foreign sub-custodians and securities depositories, including the risk that appropriate sub-custody arrangements will not be available to the Fund or the Underlying Fund; |

| ■ | The risk that the Fund’s or the Underlying Fund's ownership rights in portfolio securities could be lost through fraud or negligence because ownership in shares of Russian companies is recorded by the companies themselves and by registrars, rather than by a central registration system; and |

| ■ | The risk that the Fund or the Underlying Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because Russian banking institutions and registrars are not guaranteed by the Russian government. |

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $1,249,000 | 50,000 | $300 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

(For a share outstanding throughout each period)

| iShares Interest Rate Hedged Long-Term Corporate Bond ETF | |||||||

| Year

Ended 10/31/18 |

Year

Ended 10/31/17 |

Year

Ended 10/31/16 |

Period

From 07/22/15(a) to 10/31/15 | ||||

| Net asset value, beginning of period | $ 25.98 | $ 24.07 | $24.08 | $ 25.10 | |||

| Net investment income(b) | 1.01 | 0.91 | 0.89 | 0.26 | |||

| Net realized and unrealized gain (loss)(c) | (0.32) | 1.78 | (0.28) | (1.09) | |||

| Net increase (decrease) from investment operations | 0.69 | 2.69 | 0.61 | (0.83) | |||

| Distributions (d) | |||||||

| From net investment income | (0.91) | (0.76) | (0.60) | (0.13) | |||

| Return of capital | — | (0.02) | (0.02) | (0.06) | |||

| Total distributions | (0.91) | (0.78) | (0.62) | (0.19) | |||

| Net asset value, end of period | $ 25.76 | $ 25.98 | $24.07 | $24.08 | |||

| Total Return | |||||||

| Based on net asset value | 2.66% | 11.36% | 2.49% (e) | (3.19)% (e)(f) | |||

| Ratios to Average Net Assets | |||||||

| Total expenses(g) | 0.35% | 0.35% | 0.35% | 0.35% (h) | |||

| Total expenses after fees waived(g) | 0.10% | 0.10% | 0.10% | 0.12% (h) | |||

| Net investment income | 3.86% | 3.62% | 3.78% | 3.80% (h) | |||

| Supplemental Data | |||||||