UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the fiscal year ended December 31, 2015 | ||||

or | ||||

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||

For the transition period from to

Commission file number: 1-35229

Xylem Inc.

(Exact name of registrant as specified in its charter)

Indiana | 45-2080495 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

1 International Drive, Rye Brook, NY 10573 | ||

(address of principal executive offices and zip code) | ||

(914) 323-5700 | ||

(Registrant's telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of each class | Name of each exchange on which registered | |

Common Stock, par value $0.01 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer þ Accelerated Filer ¨ Non-Accelerated Filer ¨ Smaller reporting company ¨

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of the common stock of the registrant held by non-affiliates of the registrant as of June 30, 2015 was approximately $6.7 billion. As of January 29, 2016, there were 178,485,808 outstanding shares of the registrant’s common stock, par value $0.01 per share.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2016 Annual Meeting of Shareowners, to be held in May 2016, are incorporated by reference into Part II and Part III of this Report.

Xylem Inc.

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended December 31, 2015

Table of Contents

ITEM | PAGE | |

PART I | ||

1 | ||

1A. | ||

1B. | ||

2 | ||

3 | ||

4 | ||

* | ||

PART II | ||

5 | ||

6 | ||

7 | ||

7A. | ||

8 | ||

9 | ||

9A. | ||

9B. | ||

PART III | ||

10 | ||

11 | ||

12 | ||

13 | ||

14 | ||

PART IV | ||

15 | ||

* | Included pursuant to Instruction 3 of Item 401(b) of Regulation S-K. |

2

PART I

The following discussion should be read in conjunction with the consolidated financial statements, including the notes thereto, included in this Annual Report on Form 10-K (this "Report"). Xylem Inc. was incorporated in Indiana on May 4, 2011. Except as otherwise indicated or unless the context otherwise requires, “Xylem,” “we,” “us,” “our” and “the Company” refer to Xylem Inc. and its subsidiaries. References in the consolidated financial statements to "ITT" or the "former parent" refer to ITT Corporation and its consolidated subsidiaries (other than Xylem Inc.).

Forward-Looking Statements

This Report contains information that may constitute “forward-looking statements" within the meaning of the Private Securities Litigation Act of 1995. Forward-looking statements by their nature address matters that are, to different degrees, uncertain. Generally, the words “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “forecast,” “believe,” “target,” “will,” “could,” “would,” “should” and similar expressions identify forward-looking statements. However, the absence of these words or similar expressions does not mean that a statement is not forward-looking. These forward-looking statements include any statements that are not historical in nature, including any such statements about the capitalization of the Company, the Company’s restructuring and realignment, future strategic plans and other statements that describe the Company’s business strategy, outlook, objectives, plans, intentions or goals. All statements that address operating or financial performance, events or developments that we expect or anticipate will occur in the future including statements relating to orders, revenue, operating margins and earnings per share growth, and statements expressing general views about future operating results are forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause actual results to differ materially from those expressed or implied in, or reasonably inferred from, such forward-looking statements.

Factors that could cause results to differ materially from those anticipated include: overall economic and business conditions, political and other risks associated with our international operations, including military actions, economic sanctions or trade embargoes that could affect customer markets, and non-compliance with laws, including foreign corrupt practice laws, export and import laws and competition laws; potential for unexpected cancellations or delays of customer orders in our reported backlog; our exposure to fluctuations in foreign currency exchange rates; competition and pricing pressures in the markets we serve; the strength of housing and related markets; weather conditions; ability to retain and attract key members of management; our relationship with and the performance of our channel partners; our ability to successfully identify, complete and integrate acquisitions; our ability to borrow or to refinance our existing indebtedness and availability of liquidity sufficient to meet our needs; changes in the value of goodwill or intangible assets; risks relating to product defects, product liability and recalls; governmental investigations; security breaches or other disruptions of our information technology systems; litigation and contingent liabilities; and other factors set forth below under “Item 1A. Risk Factors” and those described from time to time in subsequent reports filed with the Securities and Exchange Commission (“SEC”).

All forward-looking statements made herein are based on information available to the Company as of the date of this Report. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

ITEM 1. BUSINESS

Business Overview

Xylem, with 2015 revenue of $3.7 billion and approximately 12,700 employees, is a world leader in the design, manufacturing, and application of highly engineered technologies for the water industry. We are a leading equipment and service provider for water and wastewater applications with a broad portfolio of products and services addressing the full cycle of water, from collection, distribution and use to the return of water to the environment. We have leading market positions among equipment and service providers in the core application areas of the water equipment industry: transport, treatment, test, building services, industrial processing and irrigation. Our Company’s brands, such as Bell & Gossett and Flygt, are well known throughout the industry and have served the water market for many years.

We serve a global customer base across diverse end markets while offering localized expertise. We sell our products in approximately 150 countries through a balanced distribution network consisting of our direct sales force and independent channel partners. In 2015, 59% of our revenue was generated outside the United States, with 21% of revenue generated in emerging markets.

3

Our Industry

Our planet faces a serious water challenge. Less than 1% of the total water available on earth is fresh water, and this percentage is declining due to factors such as the draining of aquifers, increased pollution and climate change. In addition, demand for fresh water is rising rapidly due to population growth, industrial expansion, and increased agricultural development, with consumption estimated to double every 20 years. By 2025, more than 30% of the world’s population is expected to live in areas without adequate water supply. Even in developed countries with sufficient clean water supply, existing infrastructure for water supply is aging and inadequately funded. In the United States, degrading pipe systems leak one out of every six gallons of water, on average, on its way from a treatment plant to the customer. These challenges are driving opportunities for growth in the global water industry, which we estimate to have a total market size of approximately $550 billion. We estimate our total served market size to be approximately $37 billion.

We view these challenges through the lens of water productivity, water quality and resilience. Water productivity refers to the more efficient delivery and use of clean water. Water quality refers to the efficient and effective management of wastewater. Resilience refers to the management of water-related risks and the resilience of water infrastructure. The Company’s customers often face all three of these challenges, ranging from inefficient aging water distribution networks (which require increases in “water productivity”); energy-intensive or unreliable wastewater management systems (which require increases in “water quality”); or exposure to natural disasters such as floods or droughts (which require increases in “resilience”). Delivering value in these areas creates significant opportunity for the Company.

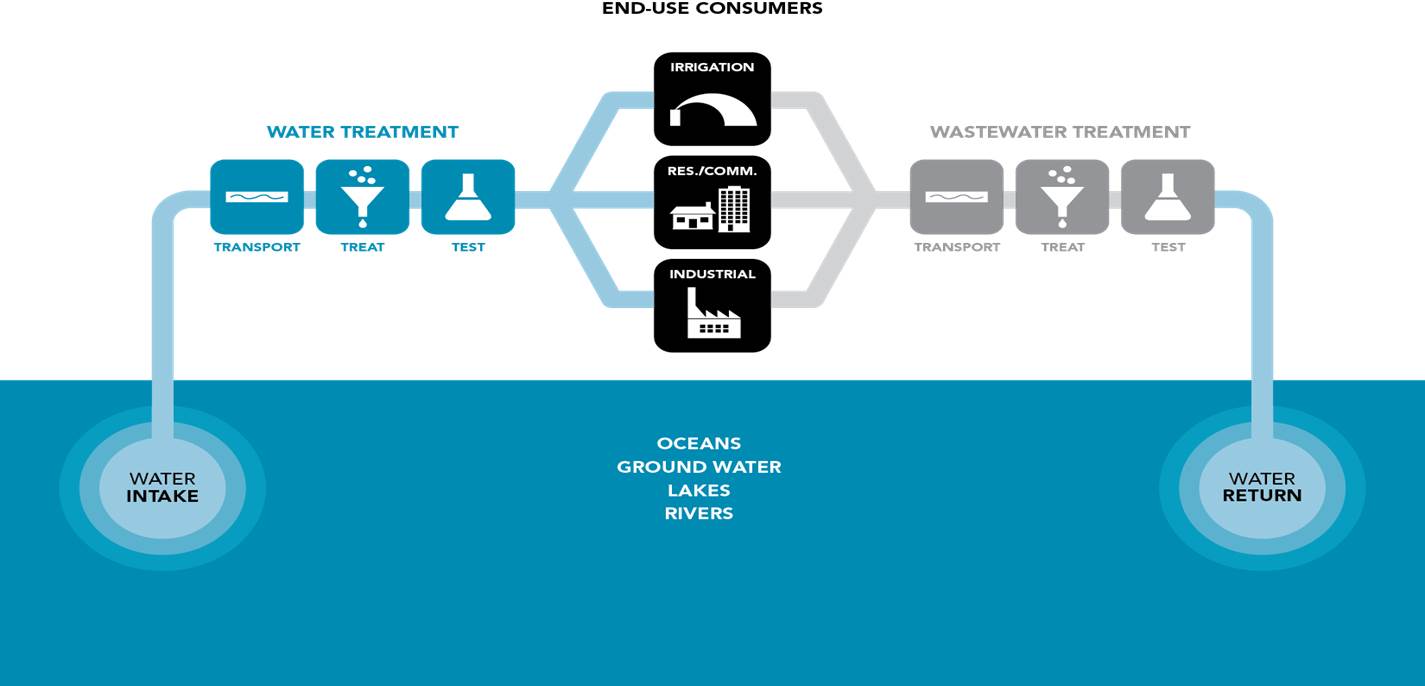

The water industry supply chain is comprised of Equipment and Services companies, Design and Build service providers, and Utilities. Equipment and Service providers serve distinct customer types. The Utilities supply water through an infrastructure network. Supply chain companies provide single, or sometimes combined, functions from equipment manufacturing and services to facility design (engineering, procurement and construction, or “EPC” firms) to plant operations (Utilities), as depicted below in Figure 1. The Utilities and EPC customers are looking for technology and application expertise from their Equipment and Services providers to address trends such as rising pollution, stricter regulations, and the increased outsourcing of process knowledge. The end users of water consist of a wide array of entities, including farms, mines, power plants, industrial facilities and residential homes. These customers are predominately served through specialized distributors and original equipment manufacturers (“OEMs”).

Figure 1: Water Industry Supply Chain

Our business focuses on the beginning of the supply chain by providing technology-intensive equipment and services. We sell our equipment and services via direct and indirect channels that serve the needs of each customer type. On the utility side, we provide the majority of our sales direct to customers with strong application expertise, with the remaining amount going through distribution partners. To end users of water, we provide the majority of our sales through long-standing relationships with the world’s leading distributors, with the remainder going direct to customers.

4

The Equipment and Services market addresses the key processes of the water industry, which are best illustrated through the cycle of water, as depicted in Figure 2, below. We believe this industry has two distinct sectors within the cycle of water: Water Infrastructure and Usage Applications. The key processes of this cycle begin when raw water is extracted by pumps, which provide the necessary pressure and flow, to move or transport, this water from natural sources, such as oceans, groundwater, lakes and rivers, through pipes to treatment facilities. Treatment facilities can provide many forms of treatment, such as filtration, disinfection and desalination, to remove solids, bacteria, and salt, respectively. Throughout each of these stages, analytical instruments test the water to ensure regulatory requirements are met so that it can be utilized by end-use customers. A network of pipes and pumps again transports this clean water to where it is needed, such as to crops for irrigation, to power plants to provide cooling in industrial water, or to an apartment building as drinking water in residential and commercial buildings. After usage, the wastewater is collected by a separate network of pipes and pumps and transported to a wastewater treatment facility, where processes such as digestion deactivate and reduce the volume of solids, and disinfection purifies effluent water. Once treated, analytical instruments test the water to ensure regulatory requirements are met so that it can be discharged back to the environment, thereby completing the cycle.

Figure 2: Cycle of Water

In the Water Infrastructure sector, two primary end markets exist: public utility and industrial. The public utility market comprises public, private and public-private institutions that handle water and wastewater for mostly residential and commercial purposes. The industrial market involves the supply of water and removal of wastewater for industrial facilities. We view the main macro drivers of this sector to be water quality, the desire for energy-efficient products, water scarcity, regulatory requirements and infrastructure needs, for both the repair of aging systems in developed countries as well as new installations in emerging markets.

In the Usage Applications sector, end-use customers fall into four main markets: residential, commercial, industrial and agricultural. Homeowners represent the end users in the residential market. Owners and managers of properties such as apartment buildings, retail stores, institutional buildings, restaurants, schools, hospitals and hotels are examples of end users in the commercial market. The industrial market is wide ranging, involving OEMs, exploration and production firms, and developers and managers of facilities operated by electrical power generators, chemical manufacturers, machine shops, clothing manufacturers, beverage dispensing and food processing firms, and car washes. The agricultural market end users are owners and operators of businesses such as crop and livestock farms, aquaculture, golf courses, and other turf applications. We believe population growth, urbanization and regulatory requirements are the primary macro drivers of these markets, as these trends drive the need for housing, food, community services and retail goods within growing city centers. Water reuse and conservation are driving the need for new technologies.

5

Business Strategy

Our strategy is to enhance shareholder value by providing distinctive solutions for our customers' most important water productivity, quality and resilience challenges, enabling us to grow revenue, organically and through strategic acquisitions, as we streamline our cost structure. Key elements of our strategy are summarized below:

• | Accelerate Profitable Growth. To achieve our goal of accelerating growth, we have identified the following five priorities: |

• | Emerging Markets - We seek to accelerate our growth in priority emerging markets through increased focus on product localization and channel development. |

▪ | Innovation & Technology - We seek to enhance the Company’s innovation efforts with increased focus on technologies and innovation that can significantly improve customers’ water productivity, quality and resilience. |

• | Commercial Leadership - We are strengthening our capabilities by focusing on simplifying our commercial processes along with the supporting backend information technology systems. |

• | Mergers and acquisitions - We continue to evaluate and, where appropriate, will act upon attractive acquisition candidates to accelerate our growth, including into new markets. |

• | Drive Continuous Improvement. We seek to embed continuous improvement into our culture and simplify our organizational structure to make the Company more agile, more profitable, and create room to re-invest in growth. To accomplish this, we will continue to strengthen our lean six sigma and global procurement capabilities, and continue to optimize our cost structure through business simplification by eliminating structural, process and product complexity. |

• | Leadership and Talent Development. We seek to continue to invest in attracting, developing and retaining world-class talent with an increased focus on leadership and talent development programs. We will continue to align individual performance to the objectives of the Company and its shareholders. |

• | Focus on Execution and Accountability. We seek to ensure the impact of these strategic focus areas by holding our people accountable and streamlining our performance management and goal deployment systems. |

6

Business Segments

We have two reportable business segments that are aligned with the cycle of water and the key strategic market applications they provide: Water Infrastructure (collection, distribution, return) and Applied Water (usage). See Note 20, “Segment and Geographic Data,” in our consolidated financial statements for financial information about segments and geographic areas.

The table and descriptions below provide an overview of our business segments.

Market Applications | 2015 Revenue (in millions) | % Revenue | Major Products | Primary Brands | |||||||||

Water Infrastructure | Transport | $ | 1,624 | 73 | % | • Water and wastewater pumps • Filtration, disinfection and biological treatment equipment • Test equipment • Controls | • Flygt • Wedeco • Godwin • WTW • Sanitaire • YSI • Leopold | ||||||

Treatment | 316 | 14 | % | ||||||||||

Test | 291 | 13 | % | ||||||||||

$ | 2,231 | 100 | % | ||||||||||

Applied Water | Building Services | $ | 774 | 54 | % | • Pumps • Valves • Heat exchangers • Controls • Dispensing equipment systems | • Goulds Water Technology • Bell & Gossett • A-C Fire Pump • Standard Xchange • Lowara • Jabsco • Flojet • Flowtronex | ||||||

Industrial Water | 562 | 40 | % | ||||||||||

Irrigation | 86 | 6 | % | ||||||||||

$ | 1,422 | 100 | % | ||||||||||

Water Infrastructure

Water Infrastructure involves the process that collects water from a source and distributes it to users, and then returns the wastewater responsibly to the environment. Within the Water Infrastructure segment, our pump systems transport water from oceans, groundwater, aquifers, lakes, rivers and seas. From there, our filtration, ultraviolet ("UV") and ozone systems provide treatment, making the water fit for use. After consumption, our pump lift stations move the wastewater to treatment facilities where our mixers, biological treatment, monitoring, and control systems provide the primary functions in the treatment process. Throughout each of these stages, our analytical systems test the quality of water for consumption as well as for its return to nature. Water Infrastructure serves its customers, public utilities and industrial applications, through three closely linked applications: Transport, Treatment and Test of water and wastewater. We estimate our served market size in this sector to be approximately $21 billion.

Transport

The Transport application includes all of the equipment and services involved in the safe and efficient movement of water from sources such as oceans, groundwater, aquifers, lakes, rivers and seas to treatment facilities, and then to users. It also includes the movement of wastewater from the point of use to a treatment facility and then back into the environment. Finally, the Transport application also includes dewatering pumps, equipment and services which provide the safe removal or draining of groundwater and surface water from a riverbed, construction site or mine shaft and bypass pumping for the repair of aging public utility infrastructure, as well as emergency water removal during severe weather events. We offer a wide range of highly engineered products such as water and wastewater submersible pumps, monitoring controls, and application solutions; we do not serve the market for lower-value equipment such as pipes and fittings. We primarily employ configure-to-order capabilities to maximize manufacturing and logistics efficiencies by producing high volumes of basic product configurations. When we provide a configure-to-order solution, we configure a standard product to our customers’ specifications. To a lesser extent, we provide engineer-to-order products to meet the customization requirements of our customers. This process requires that we apply our technical expertise and production capabilities to provide a non-standard solution to the customer. We believe our business is one of the largest players in this served market based on management estimates. With operations on six continents, we also have one of the world’s largest dewatering rental fleets. Our key brands for this application are Flygt and Godwin. Transport accounted for approximately 73% of our Water Infrastructure segment revenue in both 2015 and 2014, and 74% in 2013.

7

Treatment

The Treatment application includes equipment and services that treat both water for consumption and wastewater to be returned responsibly to the environment or reused. Primary served markets include public utilities and industrial operations. While there are several treatment solutions in the market today, we focus on three basic treatment types: (i) filtration systems, (ii) disinfection systems, (iii) biological treatment systems, including mixers. Our key brands for this application are Leopold, Wedeco, Sanitaire and Flygt. Filtration uses gravity-based media filters and clarifiers to clean both water and wastewater. Leopold, has been a worldwide leader in filtration for over 90 years. Wedeco offers chemical-free and environmentally friendly disinfection systems, both UV and ozone oxidation, to treat public utility drinking water, wastewater and industrial process water. Biological treatment systems are key to the treatment and mixing of solids in wastewater plants, which are provided through our Sanitaire and Flygt brands. We believe our business is one of the largest players in this served market based on management estimates. Treatment accounted for approximately 14% of our Water Infrastructure segment revenue in 2015, 2014 and 2013.

Test

Analytical instrumentation is used across most industries to ensure regulatory requirements are met. Growth in this market is primarily driven by increasing regulation of water and wastewater in North America, Europe and Asia. Our served market is predominately focused on water and the environment for quality levels throughout the water infrastructure loop. Analytical systems are applied in three primary ways: in the field, in a facility laboratory, or real time, online monitoring in a treatment facility process. We believe we have a leading position in this served market based on management estimates. Our key brands for this application are WTW and YSI. Test accounted for approximately 13% of our Water Infrastructure segment revenue in both 2015 and 2014, and 12% in 2013.

Applied Water

Applied Water encompasses the uses of water. Since water is used to some degree in almost every aspect of human, economic and environmental activity, this segment has a significant number of applications and we participate in all major areas of water demand. Residential and Commercial Building Services account for human and building consumption, where we deliver water boosting systems for drinking, heating, ventilation and air conditioning ("HVAC") and fire protection systems. Industrial Water applications account for water consumption activities that use pumps, heat exchangers, valves and controls to provide cooling to power plants and manufacturing facilities, as well as circulation for food and beverage processing. The remaining portion of global water use resides in irrigation applications. Examples of what we provide include: boosting systems for farming irrigation, pumps for dairy operations, and rainwater reuse systems for small scale crop and turf irrigation.We estimate our served market size in this sector to be approximately $16 billion.

Residential & Commercial Building Services

This business is defined by four primary uses of water in building services applications, such as in residential homes and commercial buildings, including offices, hotels, hospitals, schools, restaurants and malls. The first application is in HVAC, where Bell & Gossett and Lowara specialize in pumps and valves that are used in water-driven heating and cooling systems, along with heat exchangers, valves, and monitoring and control products that augment the system. The second is the supply of potable water for consumption, including drinking water and for hygienic purposes . The Goulds Water Technology, Lowara and Bell & Gossett brands provide pumps and boosting systems utilized within buildings, sourcing water from distribution networks or from wells. The third application is wastewater removal with sump and sewage pumps, provided by Bell & Gossett, Goulds Water Technology and Lowara. The fourth water-related building service area is fire protection, where our A-C Fire Pump brand supplies full pump systems for emergency fire suppression. Bell & Gossett, Goulds Water Technology and Lowara have continued to innovate, focusing on providing industry-leading energy-efficient and intelligent pumps for the building services market; many of these products are more efficient than competitive devices. We believe our business is one of the largest players in this served market based on management estimates. Building Services accounted for approximately 54% of our Applied Water segment revenue in 2015, 53% in 2014 and 50% in 2013.

Industrial Water

Water is used in most industrial facilities to provide processing steps such as cooling, heating, cleaning and mixing. Our Goulds Water Technology and Lowara brands supply vertical multistage pumps to bring in source water or to boost pressure for purposes, including water circulation through a manufacturing facility to cool machine tools. Our Standard Xchange brand delivers heat exchangers for combined heat and power applications within power generation plants. We also service niche applications such as wine processing with Jabsco brand flexible impeller pumps, and water-based detergent dispensing and water circulation for car washes served by Flojet air-operated

8

diaphragm and Goulds Water Technology end suction pumps. Our boosting pumps are also increasingly being used in hydraulic fracturing applications. We can support mines throughout exploration, development and operation. Our wide range of durable pumps ensures reliability that minimizes risks, maximizes uptime and delivers superior total cost of ownership. Across all these various end applications, we believe our business is the second largest player in this served market based on management estimates. Industrial Water accounted for approximately 40% of our Applied Water segment revenue in 2015 and 2014, and 43% in 2013.

Irrigation

The irrigation business consists of irrigation-related equipment and services associated with bringing water from a source to a production plant or livestock facility, including hoses, sprinklers, center pivot and drip irrigation systems. We focus on the pumps and boosting systems that supply this ancillary equipment with water. Our Goulds Water Technology brand brings mixed flow pumps, and our Flowtronex group specializes in equipment "packaged solutions" incorporating monitoring and controls to optimize energy efficiency in irrigation delivery. Our Lowara brand also produces pumps for agricultural applications and irrigation for gardens and parks. We believe we have a leading position in this served market based on management estimates. Irrigation accounted for approximately 6% of our Applied Water segment revenue in 2015, and 7% in 2014 and 2013.

Geographic Profile

The table below illustrates the annual revenue and percentage of revenue by geographic area for each of the three years ended December 31.

Revenue | ||||||||||||||||||||

(in millions) | 2015 | 2014 | 2013 | |||||||||||||||||

$ Amount | % of Total | $ Amount | % of Total | $ Amount | % of Total | |||||||||||||||

United States | $ | 1,490 | 41 | % | $ | 1,477 | 38 | % | $ | 1,434 | 38 | % | ||||||||

Europe | 1,179 | 32 | % | 1,379 | 35 | % | 1,387 | 36 | % | |||||||||||

Asia Pacific | 482 | 13 | % | 478 | 12 | % | 467 | 12 | % | |||||||||||

Other | 502 | 14 | % | 582 | 15 | % | 549 | 14 | % | |||||||||||

Total | $ | 3,653 | $ | 3,916 | $ | 3,837 | ||||||||||||||

In addition to the traditional markets of the United States and Europe, opportunities in emerging markets within Asia Pacific, Eastern Europe, Latin America and other countries are growing. Revenue derived from emerging markets comprised 21%, 21% and 19% of our revenue in 2015, 2014 and 2013, respectively.

The table below illustrates the property, plant & equipment and percentage of property, plant & equipment by geographic area for each of the three years ended December 31.

Property, Plant & Equipment | ||||||||||||||||||||

(in millions) | 2015 | 2014 | 2013 | |||||||||||||||||

$ Amount | % of Total | $ Amount | % of Total | $ Amount | % of Total | |||||||||||||||

United States | $ | 168 | 38 | % | $ | 180 | 39 | % | $ | 186 | 38 | % | ||||||||

Europe | 189 | 43 | % | 206 | 45 | % | 225 | 46 | % | |||||||||||

Asia Pacific | 56 | 13 | % | 53 | 11 | % | 45 | 9 | % | |||||||||||

Other | 26 | 6 | % | 22 | 5 | % | 32 | 7 | % | |||||||||||

Total | $ | 439 | $ | 461 | $ | 488 | ||||||||||||||

Distribution, Training and End Use

Water Infrastructure provides the majority of its sales through direct channels with remaining sales through indirect channels and service capabilities. Both public utility and industrial facility customers increasingly require our teams’ global but locally proficient expertise to use our equipment in their specific applications. Several trends are increasing the need for this application expertise: (i) the increase in type and amount of contaminants in water supply, (ii) increasing environmental regulations, (iii) the need to increase system efficiencies to optimize energy costs, (iv) the retirement of a largely aging water industry workforce not systematically replaced at utilities and other end user customers, and (v) the build-out of water infrastructure in the emerging markets.

In the Applied Water segment, many end-use areas are widely different, so specialized distribution partners are often preferred. Our commercial teams have built long-standing relationships around our brands in many of these industries through which we can continue to leverage new product and service applications. Revenue opportunities are balanced between OEMs and after-market customers. Our products in the Applied Water segment are sold

9

through our global direct sales and strong indirect channels with the majority of revenue going through indirect channels. We have long-standing relationships with many of the leading independent distributors in the markets we serve, and we provide incentives to distributors, such as specialized loyalty and training programs.

Aftermarket Parts and Service

During their lifecycle, installed products require maintenance, repair services and parts due to the harsh environments in which they operate. We have many service centers around the world, which employ service employees to provide aftermarket parts and services to our large installed base of customers. Service centers offer an array of integrated service solutions for the industry including: preventive monitoring, contract maintenance, emergency field service, engineered upgrades, inventory management, and overhauls for pumps and other rotating equipment.

Depending on the type of product, median lifecycles range from five years to over 50 years, at which time they must be replaced. Many of our products are precisely selected and applied within a larger network of equipment driving a strong preference by customers and installers to replace them with the same exact brand and model when they reach the end of their lifecycle. This dynamic establishes a large recurring revenue stream for our business.

Supply and Seasonality

We have a global manufacturing footprint, with production facilities in Europe, North America, Latin America, and Asia. Our inventory management and distribution practices seek to minimize inventory holding periods by striving to take delivery of the inventory and manufacturing as close as possible to the sale or distribution of products to our customers. All of our businesses require various parts and raw materials, of which the availability and prices may fluctuate. Parts and raw materials commonly used in our products include motors, fabricated parts, castings, bearings, seals, nickel, copper, aluminum, and plastics. While we may recover some cost increases through operational improvements, we are still exposed to some pricing risk. We attempt to control costs through fixed-priced contracts with suppliers and various other programs, such as our global procurement initiative.

Our business relies on third-party suppliers, contract manufacturing and commodity markets to secure raw materials, parts and components used in our products. We typically acquire materials and components through a combination of blanket and scheduled purchase orders to support our materials requirements. For most of our products, we have existing alternate sources of supply, or such sources are readily available.

We may experience price volatility or supply constraints for materials that are not available from multiple sources. From time to time, we acquire certain inventory in anticipation of supply constraints or enter into longer-term pricing commitments with vendors to improve the priority, price and availability of supply. There have been no raw material shortages that have had a significant adverse impact on our business as a whole.

Our Water Infrastructure and Applied Water segments experience some modest level of seasonality in its business. This seasonality is dependent on factors such as capital spending of customers as well as weather conditions, including heavy flooding, droughts, and fluctuations in temperatures, which can positively or negatively impact portions of our business.

Customers

Our business is not dependent on any single customer or a few customers, the loss of which would have a material adverse effect on our Water Infrastructure or Applied Water segments or on the Company as a whole. No individual customer accounted for more than 10% of our consolidated 2015, 2014 or 2013 revenue.

Backlog

Delivery schedules vary from customer to customer based upon their requirements. Typically, large projects require longer lead production cycles and delays can occur from time to time. Total backlog was $716 million at December 31, 2015 and $740 million at December 31, 2014. We anticipate that more than 81% of the backlog at December 31, 2015 will be recognized as revenue during 2016.

Competition

Given the highly fragmented nature of the water industry, the Water Infrastructure segment competes with a large number of businesses. Competition in the water transport and treatment technologies markets focuses on product performance, reliability and innovation, application expertise, brand reputation, energy efficiency, product life cycle cost, timeliness of delivery, proximity of service centers, effectiveness of our distribution channels and price. In the sale of products and services, we benefit from our large installed base of pumps and complementary products, which require maintenance, repair and replacement parts due to the nature of the products and the conditions under which they operate. Timeliness of delivery, quality and the proximity of service centers are important

10

customer considerations when selecting a provider for after-market products and services as well as equipment rentals. In geographic regions where we are locally positioned to provide a quick response, customers have historically relied on us, rather than our competitors, for after-market products relating to our highly engineered and customized solutions. Our key competitors within the Water Infrastructure segment include KSB Inc., Sulzer Ltd., Evoqua Water Technologies and Danaher Corporation.

Competition in the Applied Water segment focuses on brand equity, application expertise, product delivery and performance, quality, and price. We compete by offering a wide variety of innovative and high-quality products, coupled with world-class application expertise. We believe our distribution through well-established channels and our reputation for quality significantly enhance our market position. Our ability to deliver innovative product offerings has allowed us to compete effectively, to cultivate and maintain customer relationships and to serve and expand into many niche and new markets. Our key competitors within the Applied Water segment include Grundfos, Wilo SE, Pentair Ltd. and Franklin Electric Co., Inc.

Research and Development

Research and development (“R&D”) is a key foundation of our growth strategy and we focus on the design and development of products and application know-how that anticipate customer needs and emerging trends. Our engineers are involved in new product development as well as improvement of existing products to increase customer value. Our businesses invest substantial resources for R&D. We anticipate we will continue to develop and invest in our R&D capabilities to promote a steady flow of innovative, high-quality and reliable products and applications to further strengthen our position in the markets we serve. We invested $95 million, $104 million, and $104 million in R&D in 2015, 2014 and 2013, respectively.

We have R&D and product development capabilities around the world. R&D activities are initially conducted in our technology centers, located in conjunction with some of our major manufacturing facilities to ensure an efficient and robust development process. We have several global technical centers and local development teams around the world where we are supporting global needs and accelerating the customization of our application expertise to local needs. In some cases, our R&D activities are conducted at our piloting and testing facilities and at strategic customer sites. These piloting and testing facilities enable us to serve our strategic markets in each region of the world.

Intellectual Property

We generally seek patent protection for those inventions and improvements that we believe will improve our competitive position. We believe that our patents and applications are important for maintaining the competitive differentiation of our products and improving our return on research and development investments. While we own, control or license a significant number of patents, trade secrets, proprietary information, trademarks, trade names, copyrights, and other intellectual property rights which, in the aggregate, are of material importance to our business, management believes that our business, as a whole, as well as each of our core business segments, is not materially dependent on any one intellectual property right or related group of such rights.

Patents, patent applications, and license agreements expire or terminate over time by operation of law, in accordance with their terms or otherwise. As the portfolio of our patents, patent applications, and license agreements has evolved over time, we do not expect the expiration of any specific patent to have a material adverse effect on our financial position or results of operations.

Environmental Matters and Regulation

Our manufacturing operations worldwide are subject to many requirements under environmental laws. In the United States, the Environmental Protection Agency and similar state agencies administer laws and regulations concerning air emissions, water discharges, waste disposal, environmental remediation, and other aspects of environmental protection. Such environmental laws and regulations in the United States include, for example, the Federal Clean Air Act, the Clean Water Act, the Resource, Conservation and Recovery Act, and the Comprehensive Environmental Response, Compensation and Liability Act. Environmental requirements significantly affect our operations. We have established an internal program to address compliance with applicable environmental requirements and, as a result, management believes that we are in substantial compliance with current environmental regulations.

While environmental laws and regulations are subject to change, such changes can be difficult to predict reliably and the timing of potential changes is uncertain. Management does not believe, based on current circumstances, that compliance costs pursuant to such regulations will have a material adverse effect on our financial position or results of operations. However, the effect of future legislative or regulatory changes could be material to our financial condition or results of operations.

11

Accruals for environmental matters are recorded on a site-by-site basis when it is probable that a liability has been incurred and the amount of the liability can be reasonably estimated, based on current law and existing technologies. It can be difficult to estimate reliably the final costs of investigation and remediation due to various factors. Our accrued liabilities for these environmental matters represent the best estimates related to the investigation and remediation of environmental media such as water, soil, soil vapor, air and structures, as well as related legal fees based upon the facts and circumstances as currently known to us. These estimates, and related accruals, are reviewed quarterly and updated for progress of investigation and remediation efforts and changes in facts and legal circumstances. Liabilities for these environmental expenditures are recorded on an undiscounted basis. We do not anticipate these liabilities will have a material adverse effect on our consolidated financial position or results of operations. We cannot make assurances that other sites, or new details about sites known to us, that could give rise to environmental liabilities with such material adverse effects on us will not be identified in the future. At December 31, 2015, we had estimated and accrued $4 million related to environmental matters.

Employees

As of December 31, 2015, Xylem had approximately 12,700 employees worldwide. We have more than 3,700 employees in the United States, of whom approximately 17% are represented by labor unions, and in certain foreign countries, some of our employees are represented by work councils. We believe that our facilities are in favorable labor markets with ready access to adequate numbers of workers and believe our relations with our employees are good.

Company History and Certain Relationships

On October 31, 2011 (the "Distribution Date"), ITT completed the Spin-off (the “Spin-off”) of Xylem, formerly ITT’s water equipment and services businesses ("WaterCo"). The Spin-off was completed pursuant to the Distribution Agreement, dated as of October 25, 2011 (the “Distribution Agreement”), among ITT, Exelis Inc., acquired by Harris Inc. on May 29, 2015, (“Exelis”) and Xylem.

Available Information

We are required to file annual, quarterly and current reports, proxy statements and other information with the SEC. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and amendments to those reports are available free of charge on our website www.xyleminc.com as soon as reasonably practicable after such reports are electronically filed with or furnished to the SEC. The information on our website is not, and shall not be deemed to be, a part hereof or incorporated into this or any of our other filings with the SEC.

In addition, the public may read or copy any materials filed with the SEC at the SEC’s Public Reference Room located at 100 F Street NE, Washington, D.C. 20549. The public may also obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. These reports and other information are also available, free of charge, at www.sec.gov.

12

ITEM 1A. RISK FACTORS

In evaluating our business, each of the following risks should be carefully considered, along with all of the other information in this Report and in our other filings with the SEC. Should any of these risks and uncertainties develop into actual events, our business, financial condition or results of operations could be materially and adversely affected.

Risks Related to Operational and External Factors

Failure to compete successfully in our markets could adversely affect our business.

We offer our products and services in competitive markets. We believe the principal points of competition in our markets are product performance, reliability and innovation, application expertise, brand reputation, energy efficiency, product life cycle cost, timeliness of delivery, proximity of service centers, effectiveness of our distribution channels and price. Maintaining and improving our competitive position will require successful management of these factors, including continued investment by us in manufacturing, research and development, engineering, marketing, customer service and support, and our distribution networks. We may not be successful in maintaining our competitive position. Our competitors may develop products that are superior to our products, or may develop more efficient or effective methods of providing products and services or may adapt more quickly than we do to new technologies or evolving customer requirements. Pricing pressures also could cause us to adjust the prices of certain products to stay competitive, which could adversely affect our financial performance. Failure to continue competing successfully or to win large contracts could adversely affect our business, financial condition or results of operations.

Our results of operations and financial condition may be adversely affected by global economic and financial market conditions.

We compete around the world in various geographic and product markets. In 2015, 41%, 32% and 21% of our total revenue was from customers located in the United States, Europe and emerging markets, respectively. We expect revenue from these markets to be significant for the foreseeable future. Important factors impacting our businesses include the overall strength of these economies and our customers’ confidence in both local and global macro-economic conditions; industrial and federal, state, local and municipal governmental spending; the strength of the residential and commercial real estate markets; interest rates; availability of commercial financing for our customers and end-users; and unemployment rates. A slowdown or prolonged downturn in financial or macro-economic conditions in these areas or in the United States could have a material adverse effect on our business, financial condition and results of operations.

Economic and other risks associated with international sales and operations could adversely affect our business.

In 2015, 59% of our total revenue was from customers outside the United States, with 21% of total revenue generated in emerging markets. We expect our international operations sales and export sales to continue to be a significant portion of our revenue. We have placed a particular emphasis on increasing our growth and presence in emerging markets. Both our sales from international operations and export sales are subject, in varying degrees, to risks inherent to doing business outside the United States. These risks include the following:

• | possibility of unfavorable circumstances arising from host country laws or regulations; |

• | currency exchange rate fluctuations and restrictions on currency repatriation; |

• | potential negative consequences from changes to taxation policies; |

• | disruption of operations from labor and political disturbances; |

• | changes in tariff and trade barriers and import and export licensing requirements; |

• | increased costs and risks of developing, staffing and simultaneously managing a number of global operations as a result of distance as well as language and cultural differences; and |

• | insurrection, armed conflict, terrorism or war. |

Any payment of distributions, loans or advances to us by our foreign subsidiaries could be subject to restrictions on, or taxation of, dividends on repatriation of earnings under applicable local law, monetary transfer restrictions and foreign currency exchange regulations in the jurisdictions in which our subsidiaries operate. In addition to the general risks that we face outside the United States, we now conduct more of our operations in emerging markets than we have in the past, which could involve additional uncertainties for us, including risks that governments may impose limitations on our ability to repatriate funds; governments may impose withholding or other taxes on

13

remittances and other payments to us, or the amount of any such taxes may increase; an outbreak or escalation of any insurrection or armed conflict may occur; governments may seek to nationalize our assets; or governments may impose or increase investment barriers or other restrictions affecting our business. In addition, emerging markets pose other uncertainties, including the difficulty of enforcing agreements, challenges collecting receivables, protection of our intellectual property and other assets, pressure on the pricing of our products, higher business conduct risks, less qualified talent and risks of political instability. We cannot predict the impact such future, largely unforeseeable events might have on our business, financial condition and results of operations.

Failure to comply with laws, regulations and policies, including the U.S. Foreign Corrupt Practices Act or other applicable anti-corruption legislation could result in fines, criminal penalties and an adverse effect on our business.

We are subject to regulation under a wide variety of U.S. federal and state and non-U.S. laws, regulations and policies, including laws related to anti-corruption, export and import compliance, anti-trust and money laundering, due to our global operations. The U.S. Foreign Corrupt Practices Act (the "FCPA"), the U.K. Bribery Act of 2010 and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments to government officials or other persons for the purpose of obtaining or retaining business. There has been an increase in anti-bribery law enforcement activity in recent years, with more frequent and aggressive investigations and enforcement proceedings by both the Department of Justice ("DOJ") and the SEC, increased enforcement activity by non-U.S. regulators, and increases in criminal and civil proceedings brought against companies and individuals. Our policies mandate compliance with these anti-bribery laws. We operate in many parts of the world that are recognized as having governmental and commercial corruption and in certain circumstances, strict compliance with anti-bribery laws may conflict with local customs and practices. We cannot assure you that our internal control policies and procedures will always protect us from improper conduct of our employees or business partners. In the event that we believe or have reason to believe that our employees or agents have or may have violated applicable laws, including anti-corruption laws, we may be required to investigate or have outside counsel investigate the relevant facts and circumstances, which can be expensive and require significant time and attention from senior management. Any such violation could result in substantial fines, sanctions, civil and/or criminal penalties, and curtailment of operations in certain jurisdictions, and might materially and adversely affect our business, results of operations or financial condition. In addition, actual or alleged violations could damage our reputation and ability to do business. Furthermore, detecting, investigating, and resolving actual or alleged violations is expensive and can consume significant time and attention of our senior management.

Our business could be adversely affected by the inability of suppliers to meet delivery requirements.

Our business relies on third-party suppliers, contract manufacturing and commodity markets to secure raw materials, parts and components used in our products. Parts and raw materials commonly used in our products include motors, fabricated parts, castings, bearings, seals, nickel, copper, aluminum, and plastics. We are exposed to the availability of these materials, which may be subject to curtailment or change due to, among other things, interruptions in production by suppliers, labor disputes, the impaired financial condition of a particular supplier, suppliers’ allocations to other purchasers, changes in exchange rates and prevailing price levels, ability to meet regulatory requirements, weather emergencies or acts of war or terrorism. Any delay in our suppliers’ abilities to provide us with necessary materials could impair our ability to deliver products to our customers and, accordingly, could have a material adverse effect on our business, financial condition or results of operations.

Our business could be adversely affected by significant movements in foreign currency exchange rates.

We conduct approximately 59% of our business in various locations outside the United States. We are exposed to fluctuations in foreign currency transaction exchange rates, particularly with respect to the Euro, Swedish Krona, Canadian Dollar, British Pound, Polish Zloty and Australian Dollar. Any significant change in the value of currencies of the countries in which we do business relative to the value of the U.S. Dollar or Euro could affect our ability to sell products competitively and control our cost structure, which could have a material adverse effect on our business, financial condition and results of operations. Additionally, we are subject to foreign exchange translation risk due to changes in the value of foreign currencies in relation to our reporting currency, the U.S. dollar. The translation risk is primarily concentrated in the exchange rate between the U.S. Dollar and the Euro, British Pound, Chinese Yuan, Swedish Krona, Canadian Dollar and Australian Dollar. As the U.S. Dollar fluctuates against other currencies in which we transact business, revenue and income can be impacted. For instance, our 2015 revenue decreased by 8.0% due to unfavorable foreign currency impacts. Continued strengthening of the U.S. Dollar relative to the Euro and the currencies of the other countries in which we do business, could materially and adversely affect our revenue growth in future periods. Refer to Item 7A "Quantitative and Qualitative Disclosures about Market Risk" for additional information on foreign exchange risk.

14

Weather conditions and climate changes may adversely affect, or cause volatility to/in, our financial results.

Weather conditions, including heavy flooding, droughts and fluctuations in temperatures or shifting conditions as a result of climate change, can positively or negatively impact portions of our business. Within the dewatering space, our pumps provided through our Godwin and Flygt brands are used to remove excess or unwanted water. Heavy flooding due to weather conditions drives increased demand for these applications. On the other hand, drought conditions drive higher demand for pumps used in agricultural and turf irrigation applications, such as those provided by our Goulds Water Technology, Flowtronex and Lowara brands. Fluctuations to warmer and cooler temperatures result in varying levels of demand for products used in residential and commercial applications where homes and buildings are heated and cooled with HVAC units such as those provided by our B&G brand. Given the unpredictable nature of weather conditions and climate change, this may result in volatility for certain portions of our business, as well as the operations of certain of our customers and suppliers.

Our financial results can be difficult to predict.

Our business is impacted by an increasing amount of short cycle, and book-and-bill business, which we have limited insight into, particularly for the business that we transact through our distributors. We are also impacted by large projects, whose timing can change based upon customer requirements due to a number of factors affecting the project, such as funding, readiness of the project and regulatory approvals. Accordingly, our financial results for any given period can be difficult to predict.

Our strategy includes acquisitions, and we may not be able to make acquisitions of suitable candidates or integrate acquisitions successfully.

Our historical growth has included acquisitions. As part of our growth strategy, we plan to pursue the acquisition of other companies, assets and product lines that either complement or expand our existing business. We cannot make assurances, however, that we will be able to identify suitable candidates successfully, negotiate appropriate acquisition terms, obtain financing that may be needed to consummate those acquisitions, complete proposed acquisitions, successfully integrate acquired businesses into our existing operations or expand into new markets. In addition, we cannot make assurances that any acquisition, once successfully integrated, will perform as planned, be accretive to earnings, or prove to be beneficial to our operations or cash flow.

Acquisitions involve a number of risks and present financial, managerial and operational challenges, including: diversion of management attention from existing businesses and operations; integration of technology, operations personnel, and financial and other systems; potentially insufficient internal controls over financial activities or financial reporting at an acquired entity that could impact us on a combined basis; the failure to realize expected synergies; the possibility that we become exposed to substantial undisclosed liabilities or new material risks associated with the acquired businesses; and the loss of key employees of the acquired businesses.

We may incur impairment charges for our goodwill and other indefinite-lived intangible assets which would negatively impact our operating results.

We have a significant amount of goodwill and purchased intangible assets on our balance sheet as a result of acquisitions we have completed. As of December 31, 2015, the net carrying value of our goodwill and other indefinite-lived intangible assets totaled approximately $2 billion. The carrying value of goodwill represents the fair value of an acquired business in excess of identifiable assets and liabilities as of the acquisition date. The carrying value of indefinite-lived intangible assets represents the fair value of trademarks and trade names as of the acquisition date. We do not amortize goodwill and indefinite-lived intangible assets that we expect to contribute indefinitely to our cash flows, but instead we evaluate these assets for impairment at least annually, or more frequently if interim indicators suggest that a potential impairment could exist. In testing for impairment, we will make a qualitative assessment, and if we believe that it is more likely than not that the fair value of a reporting unit is less than its carrying amount, the quantitative two-step goodwill impairment test is required. Significant negative industry or economic trends, disruptions to our business, inability to effectively integrate acquired businesses, unexpected significant changes or planned changes in use of the assets, divestitures and market capitalization declines may impair our goodwill and other indefinite-lived intangible assets. Any charges relating to such impairments could adversely affect our results of operations and financial condition in the periods recognized.

We may not achieve some or all of the expected benefits of our restructuring plans and our restructuring may adversely affect our business.

We have announced restructuring plans in an effort to reposition our European and North American businesses to optimize our cost structure and improve our operational efficiency and effectiveness. We may not be able to obtain the cost savings and benefits that were initially anticipated in connection with our restructuring. Additionally, as a

15

result of our restructuring, we may experience a loss of continuity, loss of accumulated knowledge or inefficiency during transitional periods. Reorganization and restructuring can require a significant amount of management and other employees' time and focus, which may divert attention from operating and growing our business.

The successful implementation and execution of our restructuring and realignment actions is critical to achieving our expected cost savings as well as effectively competing in the marketplace. Factors that may impede a successful implementation is retention of key employees, the impact of regulatory matters, and adverse economic market conditions. If the restructuring and realignment actions are not executed successfully, it could have a material adverse effect on our competitive position, business, financial condition and results of operations.

Changes in our effective tax rates may adversely affect our financial results.

We sell our products in more than 150 countries and 59% of our revenue was generated outside the United States in 2015. Given the global nature of our business, a number of factors may increase our future effective tax rates, including:

• | our decision to repatriate non-U.S. earnings for which we have not previously provided for U.S. taxes; |

• | the jurisdictions in which profits are determined to be earned and taxed; |

• | sustainability of historical income tax rates in the jurisdictions in which we conduct business; |

• | the resolution of issues arising from tax audits with various tax authorities; and |

• | changes in the valuation of our deferred tax assets and liabilities, and changes in deferred tax valuation allowances. |

Any significant increase in our future effective tax rates could reduce net income for future periods.

Our business could be adversely affected by inflation and other manufacturing and operating cost increases.

Our operating costs are subject to fluctuations, particularly due to changes in commodity prices, raw materials, energy and related utilities, freight, and cost of labor. In order to remain competitive, we may not be able to recuperate all or a portion of these higher costs from our customers through product price increases. Further, in a declining price environment, our operating margins may contract because we account for inventory using the first-in, first- out method. Actions we take to mitigate volatility in manufacturing and operating costs may not be successful and, as a result, our business, financial condition and results of operation could be materially and adversely affected.

Product defects and unanticipated use or inadequate disclosure with respect to our products could adversely affect our business, reputation and financial statements.

Manufacturing or design defects in (including in products or components that we source from third parties), unanticipated use of, or inadequate disclosure of risks relating to the use of products there can be no assurance that we or our customers or other third parties will not experience operational process failures or other problems that could result in potential product safety, regulatory or environmental risk which can lead to personal injury, death or property damage. These events could lead to recalls or safety alerts relating to our products, result in the removal of a product from the market and result in product liability claims being brought against us. Although we have liability insurance, we cannot be certain that this insurance coverage will continue to be available to us at a reasonable cost or will be adequate to cover any product liability claims. Recalls, removals and product liability claims can result in significant costs, as well as negative publicity and damage to our reputation that could reduce demand for our products.

Our indebtedness may affect our business and may restrict our operational flexibility.

As of December 31, 2015, our total outstanding indebtedness was $1,274 million, including our 3.55% Senior Notes of $600 million aggregate principal amount due September 2016 and 4.875% Senior Notes of $600 million aggregate principal amount due October 2021. We have an existing Five-Year Competitive Advance and Revolving Credit Facility (the “Credit Facility”), which provides for an aggregate principal amount of up to $600 million. We have a Risk Sharing Finance Facility Agreement (the "R&D Facility Agreement") with The European Investment Bank ("EIB") in an aggregate principal amount of up to €120 million (approximately $132 million).

Our indebtedness could:

• | increase our vulnerability to general adverse economic and industry conditions; |

• | limit our ability to obtain additional financing or borrow additional funds; |

16

• | limit our ability to pay future dividends; |

• | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

• | require that a substantial portion of our cash flow from operations be used for the payment of interest on our indebtedness instead of funding working capital, capital expenditures, acquisitions or other general corporate purposes; and |

• | increase the amount of interest expense that we must pay because some of our borrowings are at variable interest rates, which, as interest rates increase, would result in higher interest expense. |

In addition, there can be no assurance that future borrowings or equity financing will be available to us on favorable terms or at all for the payment or refinancing of our indebtedness. If we incur additional debt or raise equity through the issuance of preferred stock, the terms of the debt or preferred stock issued may give the holders rights, preferences and privileges senior to those of holders of our common stock, particularly in the event of liquidation. The terms of the debt may also impose additional and more stringent restrictions on our operations than we currently have.

Our ability to make scheduled principal payments of, to pay interest on, or to refinance our indebtedness and to satisfy our other debt obligations will depend on our future operating performance, which may be affected by factors beyond our control. If we are unable to service our indebtedness, our business, financial condition and results of operations would be materially adversely affected.

We may be negatively impacted by litigation and regulatory proceedings.

We are subject to laws, regulations and potential liability relating to claims, complaints and proceedings, including those related to antitrust, environmental, product, and other matters.

We are subject to various laws, ordinances, regulations and other requirements of government authorities in foreign countries and in the United States, any violation of which could potentially create substantial liability for us and also damage to our reputation. Changes in laws, ordinances, regulations or other government policies, the nature, timing, and effect of which are uncertain, may significantly increase our expenses and liabilities.

From time to time, we are involved in legal proceedings that are incidental to the operation of our businesses, including acquisitions and divestitures. Some of these proceedings seek remedies relating to environmental matters, intellectual property matters, product liability and personal injury claims, employment, labor and pension matters, and government and commercial or contract issues, sometimes related to acquisitions or divestitures. We may become subject to significant claims of which we are currently unaware, or the claims of which we are aware may result in our incurring a significantly greater liability than we anticipate or can estimate. Additionally, we may receive fines or penalties or be required to change or cease operations at one or more facilities if a regulatory agency determines that we have failed to comply with laws, regulations or orders applicable to our business.

Our business could be adversely affected by interruptions in information technology, communications networks and operations or cybersecurity threats.

Our business operations rely on information technology and communications networks, and operations that are vulnerable to damage or disturbance from a variety of sources. Regardless of protection measures, essentially all systems are susceptible to disruption due to failure, vandalism, computer viruses, security breaches, natural disasters, power outages and other events. In addition, we, and some of our third party vendors, have experienced cybersecurity attacks in the past and may experience them in the future, potentially with more frequency. To date, none have resulted in any material adverse impact to our business or operations. We have adopted measures to mitigate potential risks associated with information technology disruptions and cybersecurity threats, however, given the unpredictability of the timing, nature and scope of such disruptions, we could potentially be subject to production downtimes, operational delays, other detrimental impacts on our operations or ability to provide products and services to our customers, the compromising of confidential or otherwise protected information, destruction or corruption of data, security breaches, other manipulation or improper use of our systems or networks, financial losses from remedial actions, loss of business or potential liability, regulatory enforcement actions, and/or damage to our reputation, any of which could have a material adverse effect on our competitive position, results of operations, cash flows or financial condition. We also have a concentration of operations on certain sites, e.g. production and shared services centers, where business interruptions could cause material damage and costs. Transport of goods from suppliers, and to customers, could also be hampered for the reasons stated above. Although we continue to assess these risks, implement controls, and perform business continuity planning, we cannot be sure that interruptions with material adverse effects will not occur.

17

Failure to retain our existing senior management, engineering, sales and other key personnel or the inability to attract and retain new qualified personnel could negatively impact our ability to operate or grow our business.

Our success will continue to depend to a significant extent on our ability to retain or attract a significant number of employees in senior management, engineering, sales and other key personnel. The ability to attract or retain employees will depend on our ability to offer competitive compensation, training and cultural benefits. We will need to continue to develop a roster of qualified talent to support business growth and replace departing employees. Effective succession planning is also important to our long-term success. Failure to ensure effective transfer of knowledge and smooth transitions involving key employees could hinder our strategic planning and execution. A failure to retain or attract highly skilled personnel could adversely affect our operating results or ability to operate or grow our business.

If we do not or cannot adequately protect our intellectual property, if third parties infringe our intellectual property rights, or if third parties claim that we are infringing or misappropriating their intellectual property rights, we may suffer competitive injury, expend significant resources enforcing our rights or defending against such claims, or be prevented from selling products or services.

We own numerous patents, trademarks, copyrights, trade secrets and other intellectual property and licenses to intellectual property owned by others, which in aggregate are important to our business. The intellectual property rights that we obtain, however, may not provide us with a significant competitive advantage because they may not be sufficiently broad or may be challenged, invalidated, circumvented, independently developed, or designed-around, particularly in countries where intellectual property rights laws are not highly developed, protected or enforced. Our failure to obtain or maintain intellectual property rights that convey competitive advantage, adequately protect our intellectual property or detect or prevent circumvention or unauthorized use of such property and the cost of enforcing our intellectual property rights could adversely impact our business, financial condition and results of operations.

From time to time, we receive notices from third parties alleging intellectual property infringement or misappropriation. Any dispute or litigation regarding intellectual property could be costly and time-consuming due to the complexity and the uncertainty of intellectual property litigation. Our intellectual property portfolio may not be useful in asserting a counterclaim, or negotiating a license, in response to a claim of infringement or misappropriation. In addition, as a result of such claims of infringement or misappropriation, we could lose our rights to critical technology, be unable to license critical technology or sell critical products and services, be required to pay substantial damages or license fees with respect to the infringed rights or be required to redesign our products at substantial cost, any of which could adversely impact our competitive position, financial condition and results of operations. Even if we successfully defend against claims of infringement or misappropriation, we may incur significant costs and diversion of management attention and resources, which could adversely affect our business, financial condition and results of operations.

We cannot make assurances that we will pay dividends on our common stock or continue to repurchase our common stock under Board approved share repurchase plans, and likewise our indebtedness could limit our ability to pay dividends or make share repurchases.

The timing, declaration, amount and payment of future dividends to our shareholders fall within the discretion of our Board of Directors and will depend on many factors, including our financial condition, results of operations and capital requirements, as well as applicable law, regulatory constraints, industry practice and other business considerations that our Board of Directors considers relevant. There can be no assurance that we will pay a dividend in the future or continue to pay dividends.

Further, the timing and amount of the repurchase of our common stock under Board approved share repurchase plans has similar dependencies as the payment of dividends and accordingly, there can be no assurances that we will continue to repurchase our common stock.

Additionally, if we cannot generate sufficient cash flow from operations to meet our debt payment obligations, then our ability to pay dividends, if so determined by the Board of Directors, or make share repurchases will be impaired and we may be required to attempt to restructure or refinance our debt, raise additional capital or take other actions such as selling assets, reducing or delaying capital expenditures, reducing our dividend or delaying or curtailing share repurchases. There can be no assurance, however, that any such actions could be effected on satisfactory terms, if at all, or would be permitted by the terms of our debt or our other credit and contractual arrangements.

18

The level of returns on postretirement benefit plan assets, changes in interest rates and other factors could affect our earnings and cash flows in future periods.