We have one class of ordinary shares, and each holder of our ordinary shares is entitled to one vote per share. However, in matters related to change of control, pursuant to our amended and restated memorandum and articles of association, Wincore Holdings Limited, Clinet Investments Limited and Vitz Holdings Limited were entitled to three votes per share for each ordinary share registered in their names in the register of members of the Company, and each other holder is entitled to one vote per share. Such change of control events include: (a) a merger, amalgamation, consolidation or similar transaction involving our company, (b) the filing of a petition for a scheme of arrangement involving our company, or the giving of consent to such a filing or the co-operation by our company in the making of such filing, and (c) a sale, transfer or other disposition of all or substantially all of the assets of our company. Subsequently on December 31, 2020, Vitz Holdings Limited gave up the three votes per share and is now entitled to one vote per share in matters related to change of control, pursuant to our amended and restated memorandum and articles of association. Client Investments Limited sold all the shares with entitlement to three votes per share in such matters related to a change of control. And Wincore Holdings Limited converted the shares with entitlement to three votes per share in such matters.

As of March 31, 2022, 226,120,381 of our ordinary shares were issued and outstanding, being the total ordinary shares issued and outstanding based on our register of members maintained by our Cayman Islands share registrar, excluding (1) ordinary shares represented by the ADSs repurchased by the Company; (2) ordinary shares issued to the depositary that are issuable upon the exercise of share options outstanding and vesting of restricted shares issued to employees, or reserved for future award grants under our 2008 Plan and 2019 Plan; and (3) ordinary shares underlying restricted shares issued to the grantees under the Plans that are in the process of being cancelled. Based on a review of our register of members, we believe that as of March 31, 2022, 116,558,948 ordinary shares, representing approximately 47.58% of our total outstanding shares, were held by three record shareholders, which includes 116,558,948 ordinary shares held of record by The Bank of New York Mellon, the depositary of our ADS program. The number of beneficial owners of our ADSs in the United States is likely to be much larger than the number of record holders of our ordinary shares in the United States. We are not aware of any arrangement that may at a subsequent date, result in a change of control of our company.

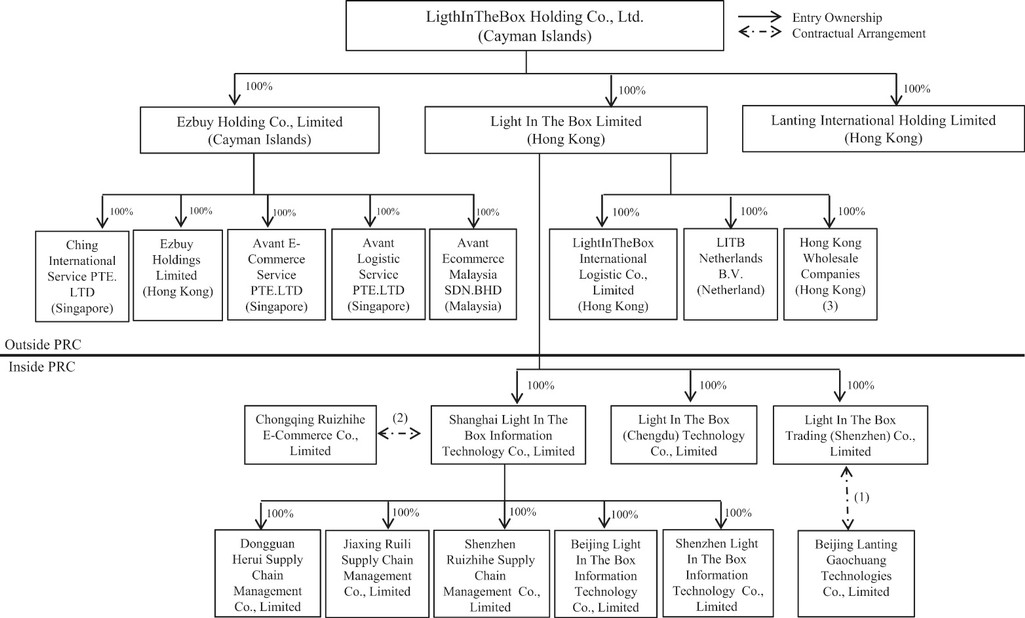

B. Related Party Transactions

We signed a share transfer agreement with Wuhan Zall Internet Technology Co., Ltd, a subsidiary of Zall, in 2019. The total purchase price was $4,223 thousand for a 30% equity interest in a long-term investment. As of December 31, 2020 and 2021, $2,820 thousand and $2,730 thousand has not been settled, respectively. Subsequently, $2,730 thousand has been settled in April 2022. See Note 8 for details of the share transfer.

We entered into a GPS project technical services contract with Hankou North Import and Export Service Co., Ltd, a subsidiary of Zall, in 2019. The total technical services fee received from Hankou North was $123 thousand in 2019, which was settled in full during 2019.

We entered into a technical development services contract with Demon Network Technology (Hong Kong) Co., Ltd. (“Demon Hong Kong”), a subsidiary of Zall, in 2019. The total technical services fee received from Demon Hong Kong in 2019 was $749 thousand and all received as of December 31, 2020.

We signed a share transfer agreement with Yew Tee Global Investment Pte. Ltd., a company controlled by our managements, in 2021, to acquire the remaining 20% of the issued share capital of Avant Logistic Service PTE.LTD. Upon the share transfer, Avant Logistic Service PTE.LTD became a wholly-owned subsidiary of Ezbuy. The total purchase price was $1,544 thousand and the transaction was fully settled as of December 31, 2021.

Employment Agreements

See “Item. 6 Directors, Senior Management and Employees—B. Compensation—Employment Agreements.”

Share Options

See “Item. 6 Directors, Senior Management and Employees—B. Compensation—Share Incentive Plan.”

C. Interests of Experts and Counsel

Not applicable.