Table of Contents

As filed with the Securities and Exchange Commission on June 24, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE

SECURITIES ACT OF 1933

Lantheus Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

2834 (Primary Standard Industrial Classification Code Number) |

35-2318913 (IRS Employer Identification No.) |

331 Treble Cove Road

North Billerica, Massachusetts 01862

(978) 671-8001

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Michael P. Duffy

Vice President, General Counsel and Secretary

331 Treble Cove Road, Building 600-2

North Billerica, Massachusetts 01862

(978) 671-8408

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

| Heather L. Emmel, Esq. Weil, Gotshal & Manges LLP 767 Fifth Avenue New York, New York 10153 Telephone: (212) 310-8000 Facsimile: (212) 310-8007 |

Marc D. Jaffe, Esq. Ian D. Schuman, Esq. Latham & Watkins LLP 885 Third Avenue New York, New York 10022 Telephone: (212) 906-1200 Facsimile: (212) 751-4864 | |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, or the Securities Act, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ |

Accelerated filer ¨ | Non-accelerated filer x (Do not check if a smaller reporting company) |

Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Price(1) |

Amount of Registration Fee | ||

| Common Stock, par value $0.01 per share |

$125,000,000 | $16,100.00 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) promulgated under the Securities Act. Includes shares of common stock that may be purchased by the underwriters under their option to purchase additional shares of common stock, if any. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the Commission acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

Upon consummation of this offering, we will enter into a corporate reorganization, whereby our direct, wholly-owned subsidiary, Lantheus MI Intermediate, Inc. will merge with and into us. See “Prospectus Summary—Corporate Reorganization” in the accompanying prospectus.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 24, 2014

PRELIMINARY PROSPECTUS

Shares

Lantheus Holdings, Inc.

Common Stock

$ per share

This is the initial public offering of our common stock. We are selling shares of our common stock. We currently expect the initial public offering price to be between $ and $ per share of common stock. No public market currently exists for our common stock.

We have granted the underwriters an option to purchase up to additional shares of common stock solely to cover over-allotments.

We intend to apply to have our common stock listed on The NASDAQ Global Market under the symbol “LNTH.”

We are an “emerging growth company” as defined under the federal securities laws and, as such, will be subject to reduced public company reporting requirements. See “Prospectus Summary—Implications of Being an Emerging Growth Company.”

Investing in our common stock involves a high degree of risks. See “Risk Factors” beginning on page 16.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| PER SHARE | TOTAL | |||||||

| Public Offering Price |

$ | $ | ||||||

| Underwriting Discount |

$ | $ | ||||||

| Proceeds to Lantheus Holdings, Inc. (before expenses) |

$ | $ | ||||||

The underwriters expect to deliver the shares to purchasers on or about , 2014 through the book-entry facilities of The Depository Trust Company.

| Citigroup | Jefferies |

| RBC Capital Markets | Wells Fargo Securities | Baird |

, 2014

Table of Contents

| 1 | ||||

| 16 | ||||

| 47 | ||||

| 49 | ||||

| 50 | ||||

| 51 | ||||

| 52 | ||||

| 54 | ||||

| 55 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

57 | |||

| 93 | ||||

| 126 | ||||

| 133 | ||||

| 147 | ||||

| 150 | ||||

| 152 | ||||

| 157 | ||||

| 160 | ||||

| Material U.S. Federal Income Tax Considerations to Non-U.S. Holders |

162 | |||

| 166 | ||||

| 171 | ||||

| 171 | ||||

| 171 | ||||

| F-1 |

You should rely only on the information contained in this prospectus. We and the underwriters have not authorized any other person to provide you with any additional information or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We and the underwriters are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is only accurate as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

TRADEMARKS

We own or have the rights to various trademarks, service marks and trade names, including, among others, the following: DEFINITY®, TechneLite®, Cardiolite®, Neurolite®, Ablavar®, Vialmix®, Quadramet® (United States only) and Lantheus Medical Imaging® referred to in this prospectus. Solely for convenience, we refer to trademarks, service marks and trade names in this prospectus without the TM, SM and ® symbols. Those references are not intended to indicate, in any way, that we will not assert, to the fullest extent permitted under applicable law, our rights to our trademarks, service marks and trade names. Each trademark, trade name or service mark of any other company appearing in this prospectus, such as Myoview®, Optison® and SonoVue® are, to our knowledge, owned by that other company.

Table of Contents

MARKET AND INDUSTRY INFORMATION

Market data and industry information used throughout this prospectus is based on management’s knowledge of the industry and the good faith estimates of management. We also relied, to the extent available, upon management’s review of independent industry surveys and publications, including Global Industry Analysts, Inc. and Frost & Sullivan, and other publicly available information prepared by a number of sources, including American Heart Association. All of the market data and industry information used in this prospectus involves a number of assumptions and limitations, and you are cautioned not to give undue weight to these estimates. While we believe the estimated market position, market opportunity and market size information included in this prospectus is reliable, that information, which is derived in part from management’s estimates and beliefs, is inherently uncertain and imprecise. Projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements” and elsewhere in this prospectus. Those and other factors could cause results to differ materially from those expressed in our estimates and beliefs and in the estimates prepared by independent parties.

ii

Table of Contents

This summary provides an overview of selected key information contained elsewhere in this prospectus and is qualified in its entirety by the more detailed information and consolidated financial statements included elsewhere in this prospectus. You should carefully review the entire prospectus, including the risk factors, the consolidated financial statements and the notes thereto, and the other documents to which this prospectus refers before making an investment decision. Unless the context requires otherwise: references to “Lantheus,” “the Company,” “our company,” “we,” “us” and “our” refer to Lantheus Holdings, Inc. and, as the context requires, its direct and indirect subsidiaries, after giving effect to the corporate reorganization described below; references to “Lantheus Holdings” refer to Lantheus Holdings, Inc. (previously named Lantheus MI Holdings, Inc.), our predecessor; references to “Lantheus Intermediate” refer to Lantheus MI Intermediate, Inc.; and references to “LMI” refer to Lantheus Medical Imaging, Inc., our wholly-owned subsidiary.

Overview

We are a global leader in developing, manufacturing, selling and distributing innovative diagnostic medical imaging agents and products that assist clinicians in the diagnosis of cardiovascular and other diseases. Our agents are routinely used to diagnose coronary artery disease, congestive heart failure, stroke, peripheral vascular disease and other diseases. Clinicians use our imaging agents and products across a range of imaging modalities, including nuclear imaging, echocardiography and magnetic resonance imaging, or MRI. We believe that the resulting improved diagnostic information enables healthcare providers to better detect and characterize, or rule out, disease, potentially achieving improved patient outcomes, reducing patient risk and limiting overall costs for payers and the entire healthcare system.

Our commercial products are used by nuclear physicians, cardiologists, radiologists, internal medicine physicians, technologists and sonographers working in a variety of clinical settings. We sell our products to radiopharmacies, hospitals, clinics, group practices, integrated delivery networks, group purchasing organizations and, in certain circumstances, wholesalers. We sell our products globally and have operations in the United States, Puerto Rico, Canada and Australia and distribution relationships in Europe, Asia Pacific and Latin America.

For the three months ended March 31, 2014, we recorded revenues, net income (loss) and Adjusted EBITDA of $73.3 million, $(1.3) million and $16.0 million, respectively. For the year ended December 31, 2013, we recorded revenues, net income (loss) and Adjusted EBITDA of $283.7 million, $(61.6) million and $47.4 million, respectively. Our products are sold in 30 countries and we generated approximately 23% and 25% of our revenues outside of the United States for the three months ended March 31, 2014 and the year ended December 31, 2013, respectively. For an explanation of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to net income (loss) as calculated under generally accepted accounting principles, or GAAP, see footnote (1) of “—Summary Consolidated Financial and Other Data.”

Our portfolio of 10 commercial products is diversified across a range of imaging modalities. Our imaging agents include radiopharmaceuticals and contrast agents.

| • | Radiopharmaceuticals are radioactive pharmaceuticals used by clinicians to perform nuclear imaging procedures. |

| • | In certain circumstances, a radioactive element, or radioisotope, is attached to a chemical compound to form the radiopharmaceutical. This act of attaching the radioisotope to the chemical compound is called radiolabeling, or labeling. |

| • | In other circumstances, a radioisotope can be used as a radiopharmaceutical without attaching any additional chemical compound. |

Table of Contents

| • | Radioisotopes are most commonly manufactured in a nuclear research reactor, where a radioactive target is bombarded with subatomic particles, or on a cyclotron, which is a type of particle accelerator that also creates radioisotopes. |

| • | Two common forms of nuclear imaging procedures are single-photon emission computed tomography, or SPECT, which measures gamma rays emitted by a SPECT radiopharmaceutical, and positron emission tomography, or PET, which measures positrons emitted by a PET radiopharmaceutical. |

| • | Contrast agents are typically non-radiolabeled compounds that are used in diagnostic procedures such as cardiac ultrasounds, or echocardiograms, x-ray imaging or MRIs that are used by physicians to improve the clarity of the diagnostic image. |

As an example of the procedures in which our products may be used, in the diagnosis of coronary artery disease, a typical diagnostic progression could include an electrocardiogram, followed by an echocardiogram (possibly using our agent DEFINITY), and then a nuclear myocardial perfusion imaging, or MPI, study using either SPECT or PET imaging (possibly using our technetium generator or one of our MPI agents). An MPI study assesses blood flow distribution to the heart. MPI is also used for diagnosing the presence of coronary artery disease. See “—Diagnostic Medical Imaging Overview.”

Leading Products

Our leading commercial products are:

| • | DEFINITY—the leading ultrasound contrast imaging agent used by cardiologists and sonographers during echocardiography exams based on revenue and usage. DEFINITY is an injectable agent that is indicated in the United States for use in patients with suboptimal echocardiograms to assist in the visualization of the left ventricle, the main pumping chamber of the heart. The use of DEFINITY in echocardiography allows physicians to significantly improve their assessment of the function of the left ventricle. Since its launch in 2001, DEFINITY has been used to image approximately five million patients. |

Of the approximately 28 million echocardiograms performed each year in the United States, a third party source estimates that approximately 20%, or approximately six million echocardiograms, produce suboptimal images. We believe that in 2013, 3.1% of the total echocardiography procedures performed in the United States used a contrast agent (which translates to only approximately 15% of all echocardiograms considered suboptimal). We believe that through April 2014, the average contrast penetration rate increased to 3.5%. Contrast penetration rates in echocardiography procedures have increased over the past six years and we believe will continue to increase in the future as clinicians continue to adopt the use of contrast as an important tool to assist their clinical decision-making. Of the echocardiograms in which a contrast agent is used, we estimate that DEFINITY had an approximate 75% share of these procedures in the United States in December 2013.

We believe that DEFINITY has this leading position because of its preferred product functionality and composition derived from a synthetic rather than a blood-based product. As a result, we believe DEFINITY will be a key driver of the future growth of our business, both in the United States and in international markets as we continue to grow contrast penetration through sales and marketing efforts focused on the appropriate use of contrast and maintain our leading position. DEFINITY currently has patent or other exclusivity protection until 2021 in the United States and until 2019 outside of the United States.

| • | TechneLite—a self-contained system, or generator, of technetium (Tc99m), a radioisotope with a six hour half-life, used by radiopharmacists at radiopharmacies to prepare patient-specific radiolabeled imaging agents. Technetium results from the radioactive decay of Molybdenum-99, or Moly, itself a radioisotope |

2

Table of Contents

| with a 66-hour half-life produced in nuclear research reactors around the world from enriched uranium. Because of the short half-lives of Moly and technetium, radiopharmacies typically replace TechneLite generators on a weekly basis pursuant to standing orders made with us. In addition, the supply chain for Moly is global and, because of the 66-hour half-life, we utilize just-in-time inventory management. We believe that we have the most balanced and diversified supply chain in the industry, buying Moly from four out of the five major global Moly processors, which are supplied by seven of the eight major global Moly reactors. |

We are one of two principal technetium generator manufacturers in the United States and Canada. We are also the leading and most consistent U.S. manufacturer of low-enriched uranium, or LEU, technetium generators. Governments and policy-makers are encouraging the increased use of technetium generators made with Moly derived from LEU rather than highly-enriched uranium, or HEU, which may present greater proliferation and security risks. In the United States, nuclear imaging agent unit doses prepared with LEU technetium generators are reimbursed by Medicare in the hospital outpatient setting at a higher rate.

We believe that our substantial capital investments in our highly automated TechneLite production line and our extensive experience in complying with the stringent regulatory requirements for the handling of nuclear materials create significant and sustainable competitive advantages for us in generator manufacturing and distribution. We estimate that in 2013, we had an approximately 40% share of generator sales in the United States. Certain TechneLite generator components currently have U.S. patent protection until 2029.

Other Commercial Products

In addition to the products listed above, our portfolio of commercial products also includes important imaging agents in specific market segments, which provide a stable base of recurring revenue. Most of these products have a favorable industry position as a result of our substantial infrastructure investment, our specialized workforce, our technical know-how and our supplier and customer relationships.

| • | Xenon Xe 133 Gas is a radiopharmaceutical gas that is inhaled and used to assess pulmonary function and also to image blood flow. Our Xenon is manufactured by a third party as part of the Moly production process and packaged by us. We are currently the leading provider of Xenon in the United States. |

| • | Cardiolite is an injectable, technetium-labeled imaging agent, also known by its generic name sestamibi, used with SPECT technology in MPI procedures that assess blood flow to the muscle of the heart. Launched in 1991, Cardiolite has the highest cumulative revenue of any branded radiopharmaceutical in history. |

| • | Neurolite is an injectable, technetium-labeled imaging agent used with SPECT technology to identify the area within the brain where blood flow has been blocked or reduced due to stroke. |

| • | Thallium Tl 201 is an injectable radiopharmaceutical imaging agent used in MPI studies to detect coronary artery disease and is manufactured by us using cyclotron-based technology. |

| • | Gallium Ga67 is an injectable radiopharmaceutical imaging agent used to detect certain infections and cancerous tumors, especially lymphoma, and is manufactured by us using cyclotron technology. |

| • | Gludef is an injectable, fluorine-18-labeled imaging agent used with PET technology to identify and characterize tumors in patients undergoing oncologic diagnostic procedures. Gludef is our branded version of fludeoxyglucose F 18 injection, or FDG. |

| • | Quadramet, our only therapeutic product, is an injectable radiopharmaceutical used to treat severe bone pain associated with certain kinds of cancer, and is manufactured by us. |

3

Table of Contents

| • | Ablavar is an injectable, gadolinium-based contrast agent used with magnetic resonance angiography, or MRA, a type of MRI scan, to image the iliac arteries that start at the aorta and go through the pelvis into the legs, in order to diagnose narrowing or blockage of these arteries in known or suspected peripheral vascular disease. |

In the United States, we sell DEFINITY through our sales team of approximately 80 employees that call on healthcare providers in the echocardiography space, as well as group purchasing organizations and integrated delivery networks. Our radiopharmaceutical products are primarily distributed through over 350 radiopharmacies, the majority of which are controlled by or associated with Cardinal Health, or Cardinal, United Pharmacy Partners, or UPPI, GE Healthcare and Triad Isotopes, Inc., or Triad.

In Canada, Puerto Rico and Australia, we own nine radiopharmacies and sell our radiopharmaceuticals, as well as others, directly to end users. In Europe, Asia Pacific and Latin America, we utilize distributor relationships to market, sell and distribute our products. We have entered into a partnership with Double-Crane Pharmaceutical Company, or Double-Crane, to complete confirmatory clinical trials necessary for Chinese regulatory approval and to distribute DEFINITY in China. We believe that international markets, particularly China, represent significant growth opportunities for our products.

Our Agents in Development

We have established a portfolio of three internally-discovered imaging agents in clinical and preclinical development, each of which we believe could represent a large market opportunity and has the potential to significantly enhance current imaging modalities and fulfill unmet diagnostic medical imaging needs. We are currently seeking strategic partners to pursue the further development of each of these agents, which include:

| • | Flurpiridaz F 18—Myocardial Perfusion Imaging Agent. Flurpiridaz F 18 is a small molecule imaging agent radiolabeled with fluorine-18 and designed for use in PET MPI to assess blood flow to the muscle of the heart. We believe that in comparison to SPECT MPI, the current standard of care, PET MPI with flurpiridaz F 18 potentially provides higher image quality, increased diagnostic certainty, more accurate risk stratification and reduced patient radiation exposure. This agent could be particularly useful in difficult to image heart patients, including women and obese patients. In the first of two planned Phase 3 studies, flurpiridaz F 18 outperformed SPECT in a highly statistically significant manner in the co-primary endpoint of sensitivity (that is, its ability to identify disease) and in the secondary endpoints of image quality and diagnostic certainty. However, flurpiridaz F 18 did not meet its other co-primary endpoint of non-inferiority for specificity (that is, its ability to rule out disease). Consequently, we have initiated discussions about potential next steps in the flurpiridaz F 18 development process with the U.S. Food and Drug Administration, or FDA. At the same time, we are seeking strategic partners to further develop and, if approved, commercialize flurpiridaz F 18. This compound currently has U.S. patent protection until 2028 before taking into account any potential regulatory extensions. |

| • | 18F LMI 1195—Cardiac Neuronal Imaging Agent. 18F LMI 1195 is a small molecule imaging agent also radiolabeled with fluorine-18 and designed to assess cardiac sympathetic nerve function with PET imaging. We believe that PET imaging with 18F LMI 1195 could allow for better identification of patients at risk of heart failure progression and fatal arrhythmias, which would better inform pharmaceutical therapy or implantable device use. This compound has completed a Phase 1 study and currently has U.S. patent protection until 2030 before taking into account any potential regulatory extensions. |

| • | LMI 1174—Vascular Remodeling Imaging Agent. LMI 1174 is a gadolinium-based MRI agent designed to identify elastin in the arterial walls and atherosclerotic plaques. We believe that this agent could allow for the minimally-invasive assessment of plaque location, burden and composition and, |

4

Table of Contents

| accordingly, could be used to risk stratify patients for potential vascular events, including heart attack or stroke. This compound is in late-stage preclinical studies and currently has U.S. patent protection until 2031 before taking into account any potential regulatory extensions. |

Diagnostic Medical Imaging Agent Overview

Medical imaging is commonly employed as a critical aid in the diagnosis of numerous medical conditions, including heart disease and cancer. Selection of treatment options and monitoring of disease progression are also facilitated by the use of imaging procedures. Diagnostic medical imaging procedures often employ imaging agents to highlight specific tissues and organs, or physiological or pathological processes. Imaging agents can be used in a range of imaging modalities, including x-ray, computed tomography, or CT, ultrasound, SPECT, PET and MRI.

Nuclear Imaging

Nuclear imaging uses small amounts of radioactive materials, called radiopharmaceuticals, taken by injection, inhalation, or orally to diagnose and treat disease. Radiopharmaceutical imaging agents consist of a radioisotope (such as technetium) paired with a molecular agent designed to localize in specific organs and tissues (such as Cardiolite and Neurolite). Clinicians utilize specialized cameras, either SPECT or PET, designed to capture radiation emitted by the agent. Computers are then used to generate detailed images of the area of interest. The resulting images provide clinicians with important information on both the structure and function of the internal organ or tissue.

Echocardiography

Cardiac ultrasound, also known as echocardiography, is a non-invasive test that uses sound waves to create moving images of the heart. These images allow an assessment of the heart’s size, shape and function. For example, echocardiography can be used to detect areas of the heart that are not functioning properly due to poor blood supply, as seen in patients with coronary artery disease. Echocardiography is considered to be one of the safest, most reliable and cost-effective ways to diagnose certain cardiac abnormalities, and it is the most widely used technique for non-invasive imaging of the heart. Echocardiography may, however, yield images of limited diagnostic value in certain situations due to signal attenuation, such as in women and patients who are obese or have lung disease. It is estimated that suboptimal image quality occurs in approximately 20% of all patients undergoing echocardiography in the United States. Uninterpretable images may lead to misdiagnosis or the need for additional, often unnecessary and costly tests. Use of contrast agents in echocardiography increases sensitivity (the ability to identify the disease) and specificity (the ability to rule out the disease), particularly in hard to image patients, by improving the delineation of the edges of the heart wall. In 2013, according to a third party source, there were 28.3 million echocardiography procedures performed in the United States.

Imaging Agents Market

We believe that the demand for imaging agents in developed and developing markets will continue to be driven by an aging and increasingly obese population, and bolstered by long-term initiatives focused on improving healthcare and the supporting infrastructure, with a particular emphasis on expanding access to rural areas and small towns and cities. According to a research report dated February 2012 released by Global Industry Analysts, Inc., or GIA, the worldwide diagnostic imaging market is projected to reach $15.5 billion by 2015, reflecting a compound annual growth rate of 6.9% over the period from 2007 through 2015.

Heart disease is a key driver of growth in the market for diagnostic medical imaging procedures and agents. Heart disease is currently the leading cause of death for both women and men in the United States and worldwide. According to the American Heart Association, or AHA, an estimated 83.6 million American adults, greater than one in three, have one or more types of heart disease. Heart disease refers to a number of disease

5

Table of Contents

states including coronary artery disease and structural defects of the heart. Coronary artery disease is the most common form of heart disease, with an estimated prevalence of approximately 6% in the United States. Many of our imaging agents and products are used in connection with diagnostic imaging for heart disease.

Our Competitive Strengths

We believe that our business model provides us with a strong platform to reach our strategic goal of providing cost-effective, clinically-beneficial diagnostic medical imaging agents and products that enable clinicians either to identify and characterize, or rule out, disease and consequently improve patient care. We believe our competitive strengths include:

| • | Leading Position Across a Range of Imaging Modalities. We are a global leader in the diagnostic medical imaging industry with over 50 years of experience in developing and bringing to market differentiated products critical to healthcare decision making, including radiopharmaceutical imaging agents, contrast imaging agents and other products. Our key brands include: DEFINITY, the leading echocardiology contrast imaging agent based on revenue and usage; and TechneLite, our technetium-based generator used by radiopharmacies to radiolabel technetium-based imaging agents, such as our own SPECT products Cardiolite and Neurolite, that are used in combination with nuclear imaging technologies. We also sell a broad portfolio of other commercial agents and products, diversified across a range of imaging modalities. |

| • | DEFINITY is a Uniquely-Positioned Growth Opportunity in the United States and Globally. We believe that DEFINITY will be a key driver of the future growth of our business, both in the United States and globally. In echocardiography procedures in which a contrast agent is used, we estimate that DEFINITY had approximately 75% share of these procedures in the United States in December 2013. We are actively pursuing international growth opportunities, such as our partnership with Double-Crane in China. If the regulatory and required clinical trial processes in China are both timely and successful, we currently estimate the commercialization of DEFINITY in China could begin as soon as 2017. We are also pursuing additional product registrations internationally to maximize the global potential of DEFINITY. We also believe our intellectual property for DEFINITY currently gives us patent or other market exclusivity protection in the United States until 2021 and outside of the United States until 2019. |

| • | Significant Investment in Complex Manufacturing and Regulatory Capabilities. We believe that our expertise in the design, development and validation of complex manufacturing systems and processes that many of our radiopharmaceutical products require due to their limited half-lives, as well as our strong track record of on-time delivery and reputation as a high-quality, reliable provider, has enabled us to become a leader in the diagnostic medical imaging industry. We believe that our substantial capital investments in our highly automated generator production line, our cyclotrons and our extensive experience in complying with the stringent regulatory requirements for the handling of nuclear materials create significant and sustainable competitive advantages. |

| • | Diversified Supply Chain. We are establishing a strong and diversified supply chain for our key products. For TechneLite, we have a strong, reliable and durable position in the technetium generator market because of our balanced and diversified Moly supply and our favorable access to Moly derived from LEU. We believe we have the most balanced and diversified Moly supply chain in the industry. We receive finished Moly from four of the five main processing sites in the world. These processing sites are, in turn, supplied by seven of the eight main Moly-producing reactors in the world. We are also the leading and most consistent manufacturer of LEU generators in North America, and we believe that in 2014, up to 40% of our Moly supply will be derived from LEU. For DEFINITY, we have already successfully completed a technology transfer from Ben Venue Laboratories, or BVL, our former manufacturing partner, to Jubilant HollisterStier, or JHS. We are also now in the process of our technology transfer activities with Phamalucence Inc., or Phamalucence, an additional manufacturing partner for DEFINITY. |

6

Table of Contents

| • | Established Global Distribution Network and Experienced Direct Sales Force. We have an established global distribution network including long-term relationships with Cardinal and UPPI, who together distributed an estimated 71% of SPECT doses sold by radiopharmacies in the United States in 2013. In the United States, our radiopharmaceuticals (including technetium generators) are primarily distributed through radiopharmacies, the majority of which are controlled by or associated with Cardinal, UPPI, GE Healthcare and Triad. In the United States, we sell DEFINITY through our sales team of approximately 80 employees, which we believe is the largest dedicated sales force in the industry serving the echocardiography market. The majority of our sales team has over a decade of experience selling diagnostic imaging agents. In Canada, Puerto Rico and Australia, we own radiopharmacies and sell directly to end users. In Europe, Asia Pacific and Latin America, we utilize distributor relationships to market, sell and distribute our products. |

| • | Experienced Management Team. Our senior management team has an average of more than 25 years of healthcare industry experience and consists of industry leaders with significant expertise in product development, operations and commercialization. We believe that the depth and experience of our management team demonstrates our expertise within the diagnostic medical imaging industry and our ability to operate successfully in a highly regulated environment. |

Our Business Strategy

Our objective is to enhance our position as a global leader in developing, manufacturing, selling and distributing innovative diagnostic medical imaging agents and products. The key elements of this strategy are to:

| • | continue to grow U.S. sales of our existing commercial products, which are diversified across a range of imaging modalities; |

| • | enhance the position of our portfolio of commercial products in international markets, obtaining additional regulatory approvals where necessary; |

| • | create strategic partnerships to further advance our agents in development to maximize their value in potentially large domestic and international markets; and |

| • | pursue select strategic licenses or acquisitions to further strengthen and diversify our portfolios of commercial products while leveraging core competencies. |

Implications of Being an Emerging Growth Company

As a company with less than $1 billion in revenue during our last fiscal year, we qualify as an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012, as amended, or the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other regulatory requirements for up to five years that are otherwise applicable generally to public companies. These provisions include, among other matters:

| • | exemption from the auditor attestation requirement on the effectiveness of our system of internal control over financial reporting; |

| • | exemption from compliance with any new requirements adopted by the Public Company Accounting Oversight Board requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer; |

| • | exemption from the requirement to seek non-binding advisory votes on executive compensation and golden parachute arrangements; and |

7

Table of Contents

| • | reduced disclosure about executive compensation arrangements. |

We will remain an emerging growth company for five years unless, prior to that time, we have (i) more than $1 billion in annual revenue, (ii) have a market value for our common stock held by non-affiliates of more than $700 million as of the last day of our second fiscal quarter of the fiscal year when a determination is made that we are deemed to be a “large accelerated filer,” as defined in Rule 12b-2 promulgated under the Securities Exchange Act of 1934, as amended, or the Exchange Act, or (iii) issue more than $1 billion of non-convertible debt over a three-year period. We have availed ourselves of the reduced reporting obligations with respect to executive compensation disclosure in this prospectus, and expect to continue to avail ourselves of the reduced reporting obligations available to emerging growth companies in future filings.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, or the Securities Act, for complying with new and revised accounting standards. An emerging growth company can, therefore, delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. However, we are choosing to “opt out” of that extended transition period and, as a result, we plan to comply with new and revised accounting standards on the relevant dates on which adoption of those standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new and revised accounting standards is irrevocable.

As a result of our decision to avail ourselves of certain provisions of the JOBS Act, the information that we provide may be different than what you may receive from other public companies in which you hold an equity interest. In addition, it is possible that some investors will find our common stock less attractive as a result of our elections, which may cause a less active trading market for our common stock and more volatility in our stock price.

Risks Associated With Our Business

Our business is subject to numerous risks, as discussed more fully in the section entitled “Risk Factors” beginning on page 17 of this prospectus, which you should read in its entirety. In particular:

| • | our dependence upon third parties for the manufacture and supply of a substantial portion of our products could prevent us from delivering our products to our customers in the required quantities, within the required timeframes, or at all, which could result in order cancellations and decreased revenues; |

| • | the global supply of Moly is fragile and not stable and our dependence on a limited number of third party suppliers for Moly could prevent us from delivering some of our products to our customers in the required quantities, within the required timeframe, or at all, which could result in order cancellations and decreased revenues; |

| • | our just-in-time manufacturing of radiopharmaceutical products relies on the timely receipt of radioactive raw materials and the timely shipment of finished goods, and any disruption of our supply or distribution networks could have a negative effect on our business; |

| • | the growth of our business is substantially dependent on increased market penetration for the appropriate use of DEFINITY in suboptimal echocardiograms; |

| • | we face potential supply and demand challenges for Xenon; |

| • | in the United States, we are heavily dependent on a few large customers to generate a majority of our revenues for our nuclear imaging products and outside of the United States, we rely on distributors to generate a substantial portion of our revenue; |

8

Table of Contents

| • | our history of net losses and ability to achieve sustained profitability; |

| • | we face continued pricing pressures from our competitors, large customers and group purchasing organizations; |

| • | certain of our customers are highly dependent on payments from third party payors, including government sponsored programs, particularly Medicare, in the United States and other countries in which we operate, and reductions in third party coverage and reimbursement rates for our products could adversely affect our business and results of operations; and |

| • | we have a substantial amount of indebtedness that may limit our financial and operating activities and adversely affect our ability to incur additional debt to fund future needs, and we may not be able to generate sufficient cash flow to meet our debt service requirements. |

Corporate Reorganization

Prior to the consummation of this offering, we will effect a corporate reorganization, whereby our direct, wholly-owned subsidiary, Lantheus MI Intermediate, Inc. (the direct parent of LMI) will merge with and into us, and we will be the surviving entity of the merger, and each share of our common stock outstanding immediately prior to the merger will be converted into the right to receive share of our newly issued common stock, with any fractional shares rounded down. In addition, as part of our corporate reorganization, shares of our common stock underlying stock options outstanding immediately prior to the merger will be ratably adjusted. The corporate reorganization will not affect our operations, which we will continue to conduct through our operating subsidiaries, including LMI.

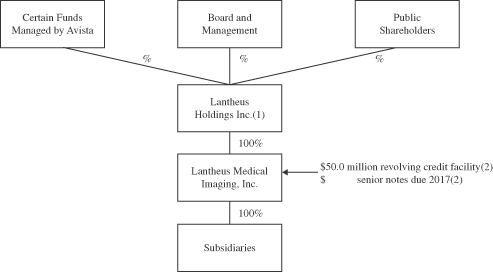

The diagram below reflects a simplified overview of our organizational structure following the corporate reorganization and this offering (including the application of the net proceeds therefrom):

| (1) | Guarantor of LMI’s $50.0 million revolving credit facility and $ million of LMI’s 9.750% senior notes due 2017, or the Notes. |

| (2) | For a description of our revolving credit facility and the Notes, see “Description of Material Indebtedness—Revolving Credit Facility” and “Description of Material Indebtedness—Senior Notes.” |

9

Table of Contents

History and Principal Stockholder

Founded in 1956 as New England Nuclear Corporation, our medical imaging business was purchased by E. I. du Pont de Nemours and Company, or DuPont, in 1981. Bristol-Myers Squibb Company, or BMS, subsequently acquired our medical imaging business from DuPont as part of its acquisition of DuPont Pharmaceuticals in 2001. In January 2008, Avista Capital Partners, L.P., Avista Capital Partners (Offshore), L.P. and ACP-Lantern Co-Invest, LLC, or collectively Avista, formed Lantheus Holdings and its subsidiary, Lantheus Intermediate, and, through Lantheus Intermediate, acquired our medical imaging business from BMS, or the Acquisition, in an entity which is now known as LMI. After this offering, Avista is expected to collectively own approximately % of our outstanding common stock.

Avista is a leading private equity firm with over $5 billion of assets under management and offices in New York, NY, Houston, TX and London, UK. Founded in 2005 as a spin-out from the former DLJ Merchant Banking Partners, or DLJMB, franchise, Avista makes controlling or influential minority investments primarily in growth-oriented healthcare, energy, communications and media, industrial and consumer businesses. Through its team of seasoned investment professionals and industry experts, Avista seeks to partner with exceptional management teams to invest in and add value to well-positioned businesses.

Corporate Information

Lantheus is a Delaware corporation, which was incorporated in 2007 and is headquartered in North Billerica, Massachusetts. LMI, our wholly-owned principal operating subsidiary, was founded in 1956 and incorporated as a Delaware corporation in 1999. Our principal executive offices are located at 331 Treble Cove Road, North Billerica, Massachusetts 01862, and our telephone number at that address is (978) 671-8001. Our web site is located at www.lantheus.com. The information on our web site is not part of, and is not incorporated by reference into, this prospectus.

10

Table of Contents

THE OFFERING

| Common stock offered by us |

shares ( shares, if the Underwriters exercise their option to purchase additional shares in full). |

| Common stock to be outstanding after this offering |

shares ( shares, if the Underwriters exercise their option to purchase additional shares in full). |

| Option to purchase additional shares of common stock |

The underwriters may also purchase up to additional shares of common stock from us, solely to cover over-allotments, at the public offering price, less the underwriting discount, within 30 days from the date of this prospectus. |

| Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and commissions and estimated expenses, will be approximately $ million, assuming the shares are offered at $ (the midpoint of the price range set forth on the cover of this prospectus). We intend to use these net proceeds to reduce our outstanding indebtedness and for working capital and other general corporate purposes. See “Use of Proceeds” for a more complete description of our intended use of the net proceeds from this offering. |

| Dividend policy |

We do not anticipate paying any dividends on our common stock; however, we may change this policy in the future. See “Dividend Policy.” |

| Proposed NASDAQ symbol |

“LNTH.” |

| Risk factors |

Investing in our common stock involves a high degree of risk. You should carefully read this entire prospectus, including the more detailed information set forth under the caption “Risk Factors” and the historical consolidated financial statements, and the related notes thereto, included elsewhere in this prospectus, before investing in our common stock. |

Unless otherwise indicated, the number of shares of common stock to be outstanding after this offering excludes:

| • | shares of our common stock issuable upon exercise of outstanding stock options as of March 31, 2014, with a weighted average exercise price of $ per share; |

| • | shares of our common stock reserved for the future issuance of grants under our 2014 Equity Incentive Plan. |

In addition, except where otherwise stated, the information in this prospectus:

| • | gives effect to our corporate reorganization (see “Prospectus Summary—Corporate Reorganization”); |

| • | gives effect to our amended and restated certificate of incorporation and our amended and restated bylaws, which will be in effect prior to the consummation of this offering; |

11

Table of Contents

| • | assumes no exercise of the underwriters’ over-allotment option to purchase up to additional shares from us. |

Unless otherwise indicated, this prospectus assumes an initial public offering price of $ per share, the midpoint of the price range set forth on the cover of this prospectus.

12

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following tables set forth our summary consolidated financial and other data for the periods ended and as of the dates indicated. The summary consolidated statements of operations data for each of the three fiscal years in the period ended December 31, 2013 have been derived from our audited consolidated financial statements and related notes included elsewhere in this prospectus. The summary consolidated balance sheet data as of March 31, 2014 and statements of operations data for the three months ended March 31, 2014 and 2013 have been derived from our unaudited consolidated financial statements and related notes included elsewhere in this prospectus. We have prepared the unaudited consolidated financial information set forth below on the same basis as our audited consolidated financial statements and have included all adjustments, consisting of only normal recurring adjustments, that we consider necessary for a fair presentation of our financial position and operating results for such periods. The results for any interim period are not necessarily indicative of the results that may be expected for a full year.

The summary consolidated financial data set forth below and elsewhere in this prospectus are not necessarily indicative of our future performance. You should read this information together with “Capitalization,” “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes thereto included elsewhere in this prospectus.

For a discussion on our quarterly results of operations for 2014 and 2013, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Quarterly Results of Operations.”

| Three Months ended March 31, |

Year ended December 31, | |||||||||||||||||||

| 2014 | 2013 | 2013 | 2012 | 2011 | ||||||||||||||||

|

(dollars in thousands except share and per share data) |

||||||||||||||||||||

| Revenues |

$ | 73,336 | $ | 71,018 | $ | 283,672 | $ | 288,105 | $ | 356,292 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Cost of goods sold |

43,275 | 48,206 | 206,311 | 211,049 | 255,466 | |||||||||||||||

| Loss on firm purchase commitment |

— | — | — | 1,859 | 5,610 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total cost of goods sold |

43,275 | 48,206 | 206,311 | 212,908 | 261,076 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross profit |

30,061 | 22,812 | 77,361 | 75,197 | 95,216 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating expenses |

||||||||||||||||||||

| Sales and marketing expenses |

9,498 | 9,797 | 35,227 | 37,437 | 38,689 | |||||||||||||||

| General and administrative expenses |

8,852 | 10,253 | 33,036 | 32,520 | 32,862 | |||||||||||||||

| Research and development expenses |

3,222 | 11,998 | 30,459 | 40,604 | 40,945 | |||||||||||||||

| Proceeds from manufacturer |

— | — | (8,876 | ) | (34,614 | ) | — | |||||||||||||

| Impairment on land |

— | — | 6,406 | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expenses |

21,572 | 32,048 | 96,252 | 75,947 | 112,496 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income (loss) |

8,489 | (9,236 | ) | (18,891 | ) | (750 | ) | (17,280 | ) | |||||||||||

| Interest expense |

(10,552 | ) | (10,669 | ) | (42,915 | ) | (42,014 | ) | (37,658 | ) | ||||||||||

| Interest income |

— | — | 104 | 252 | 333 | |||||||||||||||

| Other income (expense), net |

(414 | ) | 721 | 1,161 | (44 | ) | 1,429 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loss before income taxes |

(2,477 | ) | (19,184 | ) | (60,541 | ) | (42,556 | ) | (53,176 | ) | ||||||||||

| Provision (benefit) for income taxes |

(1,192 | ) | 628 | 1,014 | (555 | ) | 84,082 | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) |

$ | (1,285 | ) | $ | (19,812 | ) | $ | (61,555 | ) | $ | (42,001 | ) | $ | (137,258 | ) | |||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) per common share: |

||||||||||||||||||||

| Basic and diluted |

$ | (0.03) | $ | (0.39) | $ | (1.21 | ) | $ | (0.84 | ) | $ | (2.73 | ) | |||||||

| Common shares: |

||||||||||||||||||||

| Basic and diluted |

50,803,484 | 50,333,927 | 50,670,274 | 50,250,957 | 50,237,490 | |||||||||||||||

| Pro forma net income (loss) per common share (unaudited)(2): |

||||||||||||||||||||

| Basic |

||||||||||||||||||||

| Diluted |

||||||||||||||||||||

| Pro forma common shares (unaudited)(2): |

||||||||||||||||||||

| Basic |

||||||||||||||||||||

| Diluted |

||||||||||||||||||||

13

Table of Contents

| Three Months ended March 31, | Year ended December 31, | |||||||||||||||||||

| 2014 | 2013 | 2013 | 2012 | 2011 | ||||||||||||||||

| (dollars in thousands) |

||||||||||||||||||||

| Other Financial Data: |

||||||||||||||||||||

| Adjusted EBITDA (unaudited)(1) |

$ | 16,018 | $ | 4,750 | $ | 47,359 | $ | 56,212 | $ | 79,978 | ||||||||||

| As of March 31, 2014 | ||||||||||||

| Actual | Pro forma(3) | Pro forma as adjusted(4) |

||||||||||

| (dollars in thousands) |

||||||||||||

| Consolidated Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents |

$ | 17,010 | $ | $ | ||||||||

| Total assets |

260,960 | |||||||||||

| Total liabilities |

497,736 | |||||||||||

| Current portion of long-term debt |

— | |||||||||||

| Total long-term debt, net |

399,098 | |||||||||||

| Total stockholders’ deficit |

(236,776 | ) | ||||||||||

| (1) | Adjusted EBITDA is defined as EBITDA (GAAP net income (loss), plus interest expense, net, provision of income taxes, depreciation and amortization), further adjusted to exclude unusual items that management does not believe are indicative of its core operating performance. Adjusted EBITDA is used by management to measure operating performance and by investors to measure a company’s ability to service its debt and meet its other cash needs. Management believes that the inclusion of the adjustments to EBITDA applied in presenting Adjusted EBITDA is appropriate to provide additional information to investors about our performance across reporting periods on a consistent basis by excluding items that it does not believe are indicative of its core operating performance. See “Non-GAAP Financial Measures.” |

The following table provides a reconciliation of our net income (loss) to Adjusted EBITDA for the periods presented:

| Three Months ended March 31, | Year ended December 31, | |||||||||||||||||||

| 2014 | 2013 | 2013 | 2012 | 2011 | ||||||||||||||||

| (dollars in thousands) |

||||||||||||||||||||

| (unaudited) |

||||||||||||||||||||

| Net income (loss) |

$ | (1,285 | ) | $ | (19,812 | ) | $ | (61,555 | ) | $ | (42,001 | ) | $ | (137,258 | ) | |||||

| Interest expense, net |

10,552 | 10,669 | 42,811 | 41,762 | 37,325 | |||||||||||||||

| Provision for income taxes(a) |

(1,017 | ) | 189 | (127 | ) | (901 | ) | 82,702 | ||||||||||||

| Depreciation and amortization |

4,516 | 6,568 | 25,783 | 27,955 | 33,258 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| EBITDA |

12,766 | (2,386 | ) | 6,912 | 26,815 | 16,027 | ||||||||||||||

| Non-cash stock-based compensation |

284 | 257 | 578 | 1,240 | (969 | ) | ||||||||||||||

| Legal fees(b) |

234 | 268 | 660 | 1,455 | 2,017 | |||||||||||||||

| Loss on firm purchase commitment(c) |

— | — | — | 1,859 | 5,610 | |||||||||||||||

| Asset write-off(d) |

420 | 1,100 | 28,349 | 13,095 | 52,973 | |||||||||||||||

| Severance and recruiting costs(e) |

85 | 4,091 | 5,239 | 1,761 | 1,995 | |||||||||||||||

| Sponsor fee and other(f) |

251 | 257 | 1,457 | 1,042 | 1,719 | |||||||||||||||

| New manufacturer costs(g) |

1,978 | 1,163 | 4,164 | 8,945 | 606 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA(h) |

$ | 16,018 | $ | 4,750 | $ | 47,359 | $ | 56,212 | $ | 79,978 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (a) | Represents provision for income taxes, less tax indemnification associated with an agreement with BMS, and, in the year ended December 31, 2011, includes the establishment of a full valuation allowance against the U.S. deferred tax assets. |

14

Table of Contents

| (b) | Represents legal services expenses incurred in connection with our business interruption claim associated with the NRU reactor shutdown in 2009 to 2010. |

| (c) | Represents a loss associated with a portion of the committed purchases of Ablavar that we do not believe we will be able to sell prior to expiration. |

| (d) | Represents non-cash losses incurred associated with the write-down of land, intangible assets, inventory and write-off of long-lived assets. The March 31, 2014 and 2013 amounts consist primarily of non-cash losses incurred associated with the write-down of inventory. The December 31, 2013 amount consists primarily of a $6.4 million write-down of land, a $15.4 million impairment charge on the Cardiolite trademark intangible asset, a $1.7 million impairment charge on a customer relationship intangible asset and a $1.6 million inventory write-down related to Ablavar. The December 31, 2012 amount consists primarily of a $10.6 million inventory write-down related to Ablavar. The December 31, 2011 amount consists primarily of a $25.8 million inventory write-down related to Ablavar and a $23.5 million impairment charge to adjust the carrying value of the Ablavar patent portfolio asset to its fair value of zero. |

| (e) | Represents primarily severance and recruitment costs related to employees, executives and directors. |

| (f) | Represents annual sponsor monitoring fee and related expenses, non-recurring professional fees and certain non-recurring charges relating to a customer relationship. |

| (g) | Represents internal and external costs associated with establishing new manufacturing sources for our commercial products and agents in development. |

| (h) | Does not include run-rate cost savings, operating expense reductions and other expense and cost-savings of $14.4 million, $2.9 million and $6.6 million, which were realized for the years ended December 31, 2013 and 2012 and the three months ended March 31, 2013, respectively, primarily relating to our strategic shift from in-house research and development, or R&D, to an external partnering model of R&D. |

| (2) | Pro forma net income (loss) assumes $ million of the net offering proceeds are used to redeem a portion of our Notes based on an assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover of this prospectus) and assumes a reduction of interest expense, net of tax, of approximately $ million related to such redemption, assuming that the offering and the related application of net proceeds was completed on January 1, 2013. Pro forma net income (loss) per common share and number of common shares gives effect to our corporate reorganization immediately prior to the consummation of this offering and the sale of shares of our common stock in this offering at an assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover of this prospectus). |

| (3) | Pro forma information gives effect to our corporate reorganization described above, which had no impact on our historical results. |

| (4) | Pro forma as adjusted information gives effect to our corporate reorganization described above and our capitalization to reflect the sale of shares of our common stock in this offering by us at an assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover of this prospectus) after deducting underwriting discounts and commissions and estimated offering expenses payable by us, and the application of the net proceeds from this offering as described under “Use of Proceeds.” |

15

Table of Contents

An investment in our common stock involves a high degree of risk. You should carefully consider the following risks, as well as the other information contained in this prospectus, before making an investment decision. If any of the following risks, as well as other risks and uncertainties that are not identified or that we currently think are immaterial, actually occur, our business, results of operations or financial condition could be materially and adversely affected. In such an event, the trading price of our common stock could decline and you could lose part or all of your investment.

Risks Relating to our Business and Industry

Our dependence upon third parties for the manufacture and supply of a substantial portion of our products could prevent us from delivering our products to our customers in the required quantities, within the required timeframes, or at all, which could result in order cancellations and decreased revenues.

We obtain a substantial portion of our products from third party manufacturers and suppliers. Historically, we relied on BVL in Bedford, Ohio as our sole manufacturer of DEFINITY, Neurolite and evacuation vials, an ancillary component for our TechneLite generators, and as one of two manufacturers of Cardiolite. Our products were manufactured at BVL’s south complex facility, or the South Complex, where BVL also manufactured products for a number of other pharmaceutical customers. In July 2010, BVL temporarily shutdown the South Complex, in order to upgrade the facility to meet certain regulatory requirements. BVL had originally planned for the shutdown of the South Complex to run through March 2011 and to resume production of our products in April 2011. In anticipation of the shutdown, BVL manufactured for us additional inventory of these products to meet our expected needs during this period. A series of unexpected delays at BVL, however, resulted in a stockout for Neurolite from the third quarter 2011 until the third quarter 2013, product outages and shortages for DEFINITY in much of 2012 and product outages and shortages for Cardiolite in 2012 and 2013.

Although we entered into new agreements with BVL in March 2012, which provided, among other things, $35.0 million of cash payments to us, and BVL was able to resume some manufacturing under the new agreement, BVL continued to face regulatory issues and supply challenges. In October 2013, BVL announced that it would cease manufacturing further new batches of our products in its Bedford, Ohio facility and, in November 2013, BVL terminated our arrangement, and, among other things, paid us an additional $8.9 million.

Following extensive technology transfer activities, we now rely on JHS as our sole source manufacturer of DEFINITY and evacuation vials. We currently have additional ongoing technology transfer activities at JHS for our Neurolite product and at Pharmalucence for DEFINITY, but we can give no assurances as to when that technology transfer will be completed and when we will actually receive supply of Neurolite from JHS or DEFINITY from Pharmalucence. In the meantime, we have no other currently active manufacturer of Neurolite, and our DEFINITY, evacuation vial and Cardiolite product supply is currently manufactured by a single manufacturer. In addition, Mallinckrodt Pharmaceuticals, or Mallinckrodt, is our sole manufacturer for Ablavar.

Based on our current estimates, we believe that we will have sufficient supply of DEFINITY from JHS and remaining BVL inventory to meet expected demand, sufficient Cardiolite product supply from our current manufacturer to meet expected demand, sufficient supply of evacuation vials from JHS to meet expected demand and sufficient Ablavar product supply to meet expected demand. We also currently anticipate that we will have sufficient BVL-manufactured Neurolite supply for the U.S. market to last until Neurolite technology transfer and U.S. regulatory approval at JHS are completed. However, we can give no assurances that JHS or our other manufacturing partners will be able to manufacture and distribute our products in a high quality and timely manner and in sufficient quantities to allow us to avoid product stock-outs and shortfalls. Currently, the regulatory authorities in certain countries prohibit us from marketing products previously manufactured by BVL, and JHS has not yet obtained approval of some of those regulatory authorities that would permit us to market all of our products manufactured by JHS. Accordingly, until those regulatory approvals have been obtained, our international business, results of operations, financial condition and cash flows will continue to be adversely affected.

16

Table of Contents

Our manufacturing agreement for Ablavar runs until 2014, although we do not foresee the need to order any additional active pharmaceutical ingredients, or APIs, or finished drug product under this agreement, other than our outstanding purchase commitment. We do not have any current plans to initiate technology transfer activities for Ablavar. If we do not engage in Ablavar technology transfer activities in the future with a new manufacturing partner for Ablavar, then our existing Ablavar inventory will expire in 2016 and we will have no further Ablavar inventory that we will be able to sell.

In addition to the products described above, for reasons of quality assurance or cost-effectiveness, we purchase certain components and raw materials from sole suppliers (including, for example, the lead casing for our TechneLite generators and the evacuation vials for our TechneLite generators manufactured by JHS). Because we do not control the actual production of many of the products we sell and many of the raw materials and components that make up the products we sell, we may be subject to delays caused by interruption in production based on events and conditions outside of our control. At our North Billerica, Massachusetts facility, we manufacture TechneLite on a relatively new, highly automated production line, as well as Thallium and Gallium using our older cyclotron technology. If we or one of our manufacturing partners experiences an event, including a labor dispute, natural disaster, fire, power outage, security problem, failure to meet regulatory requirements, product quality issue, technology transfer issue or other issue, we may be unable to manufacture the relevant products at previous levels or on the forecasted schedule, if at all. Due to the stringent regulations and requirements of the governing regulatory authorities regarding the manufacture of our products, we may not be able to quickly restart manufacturing at a third party or our own facility or establish additional or replacement sources for certain products, components or materials.

In addition to our existing manufacturing relationships, we are also pursuing new manufacturing relationships to establish and secure additional or alternative suppliers for our commercial products. For example, on November 12, 2013, we entered into a Manufacturing and Supply Agreement with Pharmalucence to manufacture and supply DEFINITY. We cannot assure you, however, that these supply diversification activities will be successful, or that before those alternate manufacturers or sources of product are fully functional and qualified, that we will be able to avoid or mitigate interim supply shortages. In addition, we cannot assure you that our existing manufacturers or suppliers or any new manufacturers or suppliers can adequately maintain either their financial health or regulatory compliance to allow continued production and supply. A reduction or interruption in manufacturing, or an inability to secure alternative sources of raw materials or components, could eventually have a material adverse effect on our business, results of operations, financial condition and cash flows.

Challenges with product quality or product performance, including defects, caused by us or our suppliers could result in a decrease in customers and sales, unexpected expenses and loss of market share.

The manufacture of our products is highly exacting and complex and must meet stringent quality requirements, due in part to strict regulatory requirements, including the FDA’s current Good Manufacturing Practices, or cGMPs. Problems may be identified or arise during manufacturing quality review, packaging or shipment for a variety of reasons including equipment malfunction, failure to follow specific protocols and procedures, defective raw materials and environmental factors. Additionally, manufacturing flaws, component failures, design defects, off-label uses or inadequate disclosure of product-related information could result in an unsafe condition or the injury or death of a patient. Those events could lead to a recall of, or issuance of a safety alert relating to, our products. We also may undertake voluntarily to recall products or temporarily shutdown production lines based on internal safety and quality monitoring and testing data.

Quality, regulatory and recall challenges could cause us to incur significant costs, including costs to replace products, lost revenue, damage to customer relationships, time and expense spent investigating the cause and costs of any possible settlements or judgments related thereto and potentially cause similar losses with respect to other products. These challenges could also divert the attention of our management and employees from operational, commercial or other business efforts. If we deliver products with defects, or if there is a perception that our products or the processes related to our products contain errors or defects, we could incur additional recall and product liability costs, and our credibility and the market acceptance and sales of our products could be

17

Table of Contents

materially adversely affected. Due to the strong name recognition of our brands, an adverse event involving one of our products could result in reduced market acceptance and demand for all products within that brand, and could harm our reputation and our ability to market our products in the future. In some circumstances, adverse events arising from or associated with the design, manufacture or marketing of our products could result in the suspension or delay of regulatory reviews of our applications for new product approvals. These challenges could have a material adverse effect on our business, results of operations, financial condition and cash flows.

The global supply of Moly is fragile and not stable. Our dependence on a limited number of third party suppliers for Moly could prevent us from delivering some of our products to our customers in the required quantities, within the required timeframe, or at all, which could result in order cancellations and decreased revenues.

A critical ingredient of TechneLite, historically our largest product by annual revenues, is Moly. We currently purchase finished Moly from four of the five main processing sites in the world, namely Nordion, formerly known as MDS Nordion, in Canada; NTP Radioisotopes, or NTP, in South Africa; Institute for Radioelements, or IRE, in Belgium; and ANSTO in Australia. These processing sites are, in turn, supplied by seven of the eight main Moly-producing reactors in the world, namely, NRU in Canada, SAFARI in South Africa, OPAL in Australia, BR2 in Belgium, OSIRIS in France, LVR-10 in the Czech Republic and HFR in The Netherlands.

Historically, our largest supplier of Moly has been Nordion, which has relied on the NRU reactor owned and operated by Atomic Energy of Canada Limited, or AECL, a Crown corporation of the Government of Canada, located in Chalk River, Ontario. This reactor was off-line from May 2009 until August 2010 due to a heavy water leak in the reactor vessel. The inability of the NRU reactor to produce Moly and of Nordion to finish Moly during the shutdown period had a detrimental effect on our business, results of operations and cash flows. As a result of the NRU reactor shutdown, we experienced business interruption losses. We estimate the quantity of those losses to be, in the aggregate, more than $70 million, including increases in the cost of obtaining limited amounts of Moly from alternate, more distant, suppliers and substantial decreases in revenue as a result of significantly curtailed manufacturing of TechneLite generators and our decreased ability to sell other Moly-based medical imaging products, including Cardiolite, in comparison to our forecasted results. The Government of Canada has stated publicly its intent to exit the medical isotope business when the NRU reactor’s current license expires in October 2016.

As part of the conditions for the relicensing of the NRU reactor through October 2016, the Canadian government has asked AECL to shut down the reactor for at least four weeks at least once a year for inspection and maintenance. The most recent shutdown period ran from April 13, 2014 until May 13, 2014, and we were able to source sufficient Moly to satisfy all of our standing-order customer demand for our TechneLite generators during this time period from our other suppliers. During this shutdown period, however, because Xenon is a by-product of the Moly production process and is currently captured only by NRU, we were not able to supply all of our standing-order customer demand for Xenon. There can be no assurance that in the future these off-line periods will last for the stated time or that the NRU will not experience other unscheduled shutdowns. Further prolonged scheduled or unscheduled shutdowns would limit the amount of Moly and Xenon available to us and limit the quantity of TechneLite that we could manufacture, sell and distribute and the amount of Xenon that we could sell and distribute, resulting in a further substantial negative effect on our business, results of operations, financial condition and cash flows.

In the face of the NRU reactor operating challenges and licensure risks, we entered into Moly supply agreements with NTP, ANSTO and IRE to augment our supply of Moly. While we believe this additional Moly supply now gives us the most balanced and diversified Moly supply chain in the industry, a prolonged disruption of service from only one of our significant Moly suppliers could have a material adverse effect on our business, results of operations, financial condition and cash flows. We are also pursuing additional sources of Moly from potential new producers around the world to further augment our current supply, but we cannot assure you that these possible additional sources of Moly will result in commercial quantities of Moly for our business, or that these new suppliers together with our current suppliers will be able to deliver a sufficient quantity of Moly to meet our needs.

18

Table of Contents

Although our agreements with NTP, ANSTO and IRE run until December 31, 2017, our agreement with Nordion runs only until December 31, 2015 and can be terminated by Nordion upon the occurrence of certain events, including if we fail to purchase a minimum percentage of Moly or if Nordion incurs certain cost increases, and in the latter case, as soon as October 1, 2014.

U.S., Canadian and international governments have encouraged the development of a number of alternative Moly production projects with existing reactors and technologies as well as new technologies. However, the Moly produced from these projects will likely not become available until 2016 or later. As a result, there is a limited amount of Moly available which could limit the quantity of TechneLite that we could manufacture, sell and distribute, resulting in a further substantial negative effect on our business, results of operations, financial condition and cash flows.