UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2020

or

| [ ] | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _______________ to _______________

Force Protection Video Equipment Corp.

(Exact name of registrant as specified in its charter)

| Florida | 000-55519 | 45-1443512 | ||

| (State

or other jurisdiction of incorporation or organization) |

(Commission File Number) |

(IRS Employer Identification No.) |

2629 Townsgate Road, Suite 215

Westlake Village, CA 91361

(Address of principal executive offices)

(714) 312-6844

(Registrant’s telephone number, including area code)

Securities registered under Section 12(b) of the Act:

| Title of Class | Trading Symbol | Name of Each Exchange on Which Registered | ||

| N/A | N/A | N/A |

Securities registered under Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. [ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). [X] Yes [ ] No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] | |

| Non-accelerated filer [X] | Smaller reporting company [X] | |

| Emerging Growth Company [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). [ ] Yes [X] No

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was sold, or the average bid and asked prices of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. $2,018,842 based on the closing price of $0.002 on October 31, 2020.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. 158,244,935,162 shares of Class A common stock are outstanding as of April 14, 2021.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement relating to its 2021 annual meeting of shareholders (the “2021 Proxy Statement”) are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. The 2021 Proxy Statement will be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

TABLE OF CONTENTS

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Except for historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements involve risks and uncertainties, including, among other things, statements regarding our business strategy, future revenues and anticipated costs and expenses. Such forward-looking statements include, among others, those statements including the words “expects,” “anticipates,” “intends,” “believes” and similar language. Our actual results may differ significantly from those projected in the forward-looking statements. Factors that might cause or contribute to such differences include, but are not limited to, those discussed in the sections “Description of Business,” “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” You should carefully review the risks described in this Annual Report on Form 10-K and in other documents we file from time to time with the Securities and Exchange Commission including and our Quarterly Reports on Form 10-Q. You are cautioned not to place undue reliance on the forward-looking statements, which speak only as of the date of this report. We undertake no obligation to publicly release any revisions to the forward-looking statements or reflect events or circumstances after the date of this document.

Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, there are a number of risks and uncertainties that could cause actual results to differ materially from such forward-looking statements.

All references in this Annual to the “Company,” “we,” “us” or “our” refer to Force Protection Video Equipment Corporation and our wholly owned subsidiary BIG Token, Inc. on a consolidated basis. All references to “Common Stock” or “Common Shares” refers to the common stock, $0.00000001 par value (upon effectiveness of our amendment to the articles of incorporation filed on April 15, 2021), of Forced Protection Video Equipment. All references to “BIG Token”, “BIG Token Application” or “BIG Token business” refers to our wholly owned subsidiary and corresponding operations that consist of a consumer based platform, technologies offer and services used to identify and reach target consumers which we purchased from SRAX, Inc. (“SRAX”) on February 4, 2021.

As used herein, references to (i) “Exchange Agreement” refer to that certain share exchange agreement entered into by and between the Company, SRAX, and Paul Feldman (the Company’s prior CEO) on September 30, 2020, (ii) “Exchange Amendment” refer to the amendment to the Exchange Agreement entered into by between the Company, SRAX, and Paul Feldman on January 27, 2021, (iii) “TSA” refer to the transition services agreement entered into by and between SRAX and BIGtoken on January 27, 2021, (iv) “MSA” refer to the master separation agreement entered into by BIGtoken and SRAX on January 27, 2021, (v) “FPVD Warrants” refer to the common stock purchase warrants the Company issued as a result of SRAX’s June 30, 2020 convertible debt offering whereby we assumed the obligation to issue 25,568,064,462 Common Stock purchase warrants, and (vi) “Debt Exchange Agreement” refer to the debt exchange agreement the Company entered into with Red Diamond Partners, LLC pursuant to which Red Diamond exchanged an aggregate of $815,520 of principal plus accrued interest for (i) 7,000,000,000 shares of unrestricted Common Stock and (ii) 8,313 shares of Series C Convertible Preferred Stock, convertible into approximately 12,864,419,313 shares of common Stock.

| ITEM 1. | BUSINESS. |

Our Business

Prior to the completion of the Share Exchange, BIG Token was an operating segment of SRAX. On February 4, 2021 we completed the Share Exchange. As a result, BIG Token became our wholly owned subsidiary and we adopted BIG Token’s business plan. We anticipate formally changing our name to BIG Token in the future. In connection with the Share Exchange, we also entered into certain agreements with SRAX including but not limited to the TSA and MSA, as more fully described below. The terms of these agreements may be more or less favorable to us than if they had been negotiated with unaffiliated third parties.

We were initially incorporated as M Street Gallery, Inc. in March of 2011, in the state of Florida. On September 25, 2013, we changed our name to Enhance-Your-Reputation.com, Inc. On February 1, 2015, we changed our name to Force Protection Video Equipment Corporation. Our headquarters are located in Westlake Village, California, but we work as a virtually distributed organization. On February 4, 2021 we completed a share exchange with BIG Token, Inc., a wholly owned subsidiary of SRAX. As a result of the exchange, BIG Token became our wholly owned subsidiary. Additionally, simultaneous with the exchange, we adopted BIG Token’s business plan.

| 3 |

Company Overview

We are a data technology company offering a consumer based mobile application that allows consumers to own and earn from their digital data. We generate revenue by anonymizing the data, and using it to extract consumer insights that we sell to brand advertisers. Our consumer- based platform and technologies offer tools and services to identify and reach the target consumers of our brand advertisers. Our technologies assist our clients to identify their core consumers and such consumers’ characteristics across various channels in order to discover new and measurable opportunities that amplify the performance of marketing campaigns and maximize a return on marketing spend.

When consumers download our app, we ask them some questions, engage them with surveys, and ask them to connect their various online accounts including their bank accounts, credit card accounts, and social media accounts. Based on the amount of information they provide directly by answering questions or taking surveys, or passively, by connecting accounts, we’re able to track more than 4,000 attributes per consumer.

We derive our revenues from applying the data we collect, and deriving insights and audiences that we use to increase the efficiency of the online advertising of our clients. We then share the revenue generated with our consumers based on their activity and various other parameters.

To date, there have been more than 16 million accounts registered on BIG Token. The vast majority of our registrations have been driven by referrals from existing users who get rewards for driving new users. Of the 16 million, we’ve “verified” over 9 million through emails and bot detection techniques.

Our Market Opportunity – Data Economy

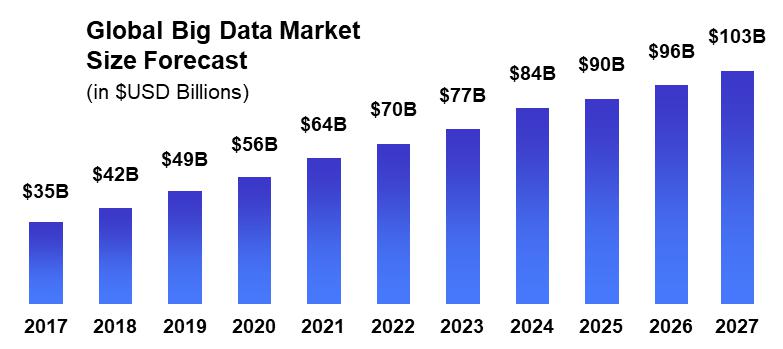

The global big data market is forecasted to grow to $103B by 2027, more than double its market size in 2018. A consumer’s digital footprint includes everything they search for, view, read, listen to, purchase, like or comment on.

Data spending keeps rising - The majority of survey respondents (69.2%) said their organizations increased spending on data and related services in 2018 (relative to 2017), while over three-fourths (78.2%) anticipate investing even more in the coming year.

Companies are prioritizing data-driven insights in order to develop marketing strategy and allocate marketing spend.

| 4 |

Government Regulation On Data Privacy Is Driving Major Tech Companies To Restrict Or Eliminate Traditional Data Collection Techniques

Regulation is changing the way businesses and tech can use data. In 2016, the European Union (EU) passed the General Data Protection Regulation (GDPR) to give individuals control over their personal data and to unify regulations within the EU. Other seminal regulatory events include the 2018 passage of the California Consumer Privacy Act (CCPA) intended to enhance privacy rights and consumer protection for Californians.

In response to the changing global regulatory environment around data privacy, major tech companies are changing how they allow their customers to collect user data. Notably, the major browsers, including Google’s Chrome and Apple’s Safari, are eliminating, or severely restricting, the use of 3rd party cookies. Those cookies have been a principal way that brands have been able to identify and market to consumers. In addition, in iOS 14, Apple is changing the Identifier For Advertiser (IDFA) tags used by mobile apps to identify users from opt out, to opt-in.

As a result of the intensifying regulatory landscape, and the tech industry’s response, first-party opt-in data, like that collected by BIGtoken, is becoming increasingly valuable. As we scale our compliant first party data set, BIGtoken will be strongly positioned to capitalize on the rapidly evolving data marketplace. We are currently focused on increasing registered users on the platform, increasing the engagement of our users, monetizing our data driven insights, and rewarding our users for sharing their data.

Given the massive tailwinds in data privacy, and our focus on first-party opt-in data, we believe BIGtoken is well positioned to accelerate growth as we play an increasingly larger role in ensuring data privacy is treated as a human right.

For additional information about government regulation applicable to our business, see Risk Factors in Part I, Item 1A.

Our Competitive Advantages — What Sets Us Apart

With the changing data privacy landscape, BIGtoken’s product offering is well positioned to provide marketing solutions compliant with these new and evolving regulations. BIGtoken’s product offering provides marketers with data solutions that traditional data providers cannot:

| ● | Data accuracy for research and ad targeting | |

| ● | Manage reach and frequency with greater accuracy across multiple media platforms | |

| ● | Access to consumers at scale for research, measurement, and attribution | |

| ● | Speed of execution for research and new targeting cohorts | |

| ● | Ability to target advertising to consumers based on identity without cookies |

Consumers are increasingly demanding data privacy, compensation for their data, and transparency and choice of how their data is used. The BIGtoken platform is focused on providing consumers with the tools and preferences they need to achieve their unique data requirements, including:

| ● | Compensation | |

| Consumers earn when they opt-in to sharing their data and when that data is purchased. | ||

| ● | Choice | |

| Consumers decide what data is shared & who can buy it. | ||

| ● | Transparency | |

| Consumers are fully aware of how their data is used. |

| 5 |

Our Growth Strategy

Our business is currently based on using our mobile app to aggregate users who opt-in to provide us their data via direct and passive actions, anonymizing that data, and using that data to provide unique consumer insights that enable marketers to advertise more efficiently. We believe that as the information gathered through the BIGtoken platform scales, we will be able to introduce new products, and monetize our growing user base at increasingly higher rates.

We are currently focused on increasing registered users on the platform, increasing the engagement of our users, monetizing our data driven insights, and rewarding our users for sharing their data. As part of this strategy, we continue to explore partnership opportunities that would allow us to leverage the capabilities of the BIGtoken platform to effectively grow the platform and increase and enhance our user experience and user rewards / compensation.

Examples of how we plan to use BIGtoken and the proprietary consumer data derived therefrom include:

| ● | The use of BIGtoken user surveys and the sale of such information received from surveys. | |

| ● | The creation and management of targeted rewards and loyalty programs based on information and buying trends ascertained by data captured on our BIGtoken platform. We offer this solution both on and off the BIGtoken app. | |

| ● | The ability to assist our customers in conducting market research based on analytics received from users of the BIGtoken platform. | |

| ● | The ability to identify specific audiences for our customers and to target questions, surveys and data analytics geared toward our customers’ products / industries. Additionally, if we are unable to scale the needed information for a customer’s target audience, we may utilize our proprietary analytics to gain insight to further focus and refine user segments that need to be targeted in order to optimize data and media spend. | |

| ● | The use of Lightning Insights that allow our customers to conduct research around specific audience groups through both long and short research studies. | |

| ● | The creation of customized loyalty programs that utilize rewards to drive consumer purchasing habits. | |

| ● | We plan to increasingly embrace crypto-currencies, including, but limited to, offering to reward our users with Bitcoin and other cryptocurrency, offering to pay our employees and vendors with such currency. offering our users digital wallets to store their crypto, enabling our users to store rewards in interest bearing stablecoins, holding cryptocurrency in our Treasury, developing our own Layer One Protocol optimized for users to own and monetize data, developing our own cryptocurrency to be used as rewards. |

Marketing and sales

We market our services through our in-house sales team, with a focus today on the largest brand advertisers with the biggest advertising budgets. Our customers include 8 of the 10 largest brand advertisers, each poised to dramatically increase their spend with BIGtoken in 2021. We believe that our focus on the largest brand advertisers will not only drive meaningful revenue growth but will help build the BIGtoken brand as the leader in privacy focused, opt in, first-party data, positioning us well when we expand our focus to mid-market agencies and brands.

On the client side, our in-house marketing is focused on positioning BIGtoken as a thought leader in data privacy, via social media, including Facebook, LinkedIn and Twitter, public relations (PR), industry events and the creation of white papers which assist in our marketing efforts and are used as lead generation tools for our sales team.

On the consumer side, we are focused on marrying our privacy leadership, with a reward system that provides meaningful value to our users who provide us with meaningful data.

| 6 |

Intellectual property

We currently rely on a combination of trade secret laws and restrictions on disclosure to protect our intellectual property rights. Our success depends on the protection of the proprietary aspects of our technology as well as our ability to operate without infringing on the proprietary rights of others. We also enter into proprietary information and confidentiality agreements with our employees, consultants and commercial partners and control access to, and distribution of, our software documentation and other proprietary information. We have one Trademark, “BIGtoken.”

Competition

We operate in a highly competitive digital media and ad tech environment. We compete based on our ability to: assist our customers in obtaining the best available prices, data, and analytics, our customer service and, the quality and accessibility of our innovative products and service offerings. We believe our platform provides for a competitive advantage. We expect an increasing number of other companies to provide similar services, leading to an increasingly competitive landscape.

Government Regulations

We are subject to a variety of laws and regulations in the United States and abroad that involve matters central to our business. Many of these laws and regulations are still evolving and being tested in courts and could be interpreted in ways that could harm our business. These may involve privacy, data protection and personal information, rights of publicity, content, intellectual property, advertising, marketing, distribution, data security, data retention and deletion, electronic contracts and other communications, competition, protection of minors, consumer protection, product liability, taxation, economic or other trade prohibitions or sanctions, anti-corruption law compliance, securities law compliance, and online payment services. In particular, we are subject to federal, state, and foreign laws regarding privacy and protection of people’s data. Foreign data protection, privacy, content, competition, and other laws and regulations can impose different obligations or be more restrictive than those in the United States. U.S. federal and state and foreign laws and regulations, which in some cases can be enforced by private parties in addition to government entities, are constantly evolving and can be subject to significant change. As a result, the application, interpretation, and enforcement of these laws and regulations are often uncertain, particularly in the new and rapidly evolving industry in which we operate, and may be interpreted and applied inconsistently from country to country and inconsistently with our current policies and practices.

Proposed or new legislation and regulations could also significantly affect our business. For example, the European General Data Protection Regulation (GDPR) took effect in May 2018 and applies to all of our products and services used by people in Europe. The GDPR includes operational requirements for companies that receive or process personal data of residents of the European Union that are different from those previously in place in the European Union and includes significant penalties for non-compliance. The California Consumer Privacy Act, which took effect in January 2020, also establishes certain transparency rules and creates new data privacy rights for users. Similarly, there are a number of legislative proposals in the European Union, the United States, at both the federal and state level, as well as other jurisdictions that could impose new obligations or limitations in areas affecting our business, such as liability for copyright infringement. In addition, some countries are considering or have passed legislation implementing data protection requirements or requiring local storage and processing of data or similar requirements that could increase the cost and complexity of delivering our services.

We may become the subject of investigations, inquiries, data requests, requests for information, actions, and audits by government authorities and regulators in the United States, Europe, and around the world, particularly in the areas of privacy, data protection, law enforcement, consumer protection, and competition, as we continue to grow and expand our operations. We are currently, and may in the future be, subject to regulatory orders or consent decrees, including the modified consent order we entered into in July 2019 with the U.S. Federal Trade Commission (FTC) which is pending federal court approval and which, among other matters, will require us to implement a comprehensive expansion of our privacy program. Orders issued by, or inquiries or enforcement actions initiated by, government or regulatory authorities could cause us to incur substantial costs, expose us to unanticipated civil and criminal liability or penalties (including substantial monetary remedies), interrupt or require us to change our business practices in a manner materially adverse to our business, divert resources and the attention of management from our business, or subject us to other remedies that adversely affect our business.

| 7 |

We anticipate embracing crypto and digital assets in the future. The regulatory regime governing blockchain technologies, cryptocurrencies, digital assets, utility tokens, security tokens and offerings of digital assets is uncertain, and new regulations or policies may materially adversely affect our development and the value. Regulation of digital assets, like cryptocurrencies, blockchain technologies and cryptocurrency exchanges, is currently undeveloped and likely to rapidly evolve as government agencies take greater interest in them. Regulation also varies significantly among international, federal, state and local jurisdictions and is subject to significant uncertainty. Various legislative and executive bodies in the United States and in other countries may in the future adopt laws, regulations, or guidance, or take other actions, which may severely impact the permissibility of tokens generally and the technology behind them or the means of transaction or in transferring them. Failure by us to comply with any laws, rules and regulations, some of which may not exist yet or are subject to interpretation and may be subject to change, could result in a variety of adverse consequences, including civil penalties and fines.

Employees and Human Capital Resources

As of March 26, 2021, we had 86 full-time employees. 7 are engaged in executive management such as our Chief Executive Officer, 57 in information technology including those participating in our research and development efforts, 7 in sales and marketing, 8 in integration and customer support and 7 in administration. All employees are employed “at will.” We believe our relations with our employees are generally positive and we have no collective bargaining agreements with any labor unions.

Our human capital resources objectives include, as applicable, identifying, recruiting, retaining, incentivizing and integrating our existing and new employees. The principal purposes of our equity and cash incentive plans are to attract, retain and reward personnel, whether existing employees or new hires, through the granting of stock-based and cash-based compensation awards. We believe that this increases value to our stockholders and the success of our company by motivating such individuals to perform to the best of their abilities and achieve our objectives.

As the success of our business is fundamentally connected to the well-being of our employees, we are committed to their health, safety and wellness. We provide our employees and their families with access to convenient health and wellness programs, including benefits that provide protection and security giving them peace of mind concerning events that may require time away from work or that impact their financial well-being; and that offer choice where possible so they can customize their benefits to meet their needs and the needs of their families. In response to the COVID-19 pandemic, we implemented significant changes that we determined were in the best interest of our employees, as well as the community in which we operate, and which comply with government regulations, including working in a remote environment where appropriate or required.

Relationship with SRAX

We have operated as an operating segment of SRAX since April 1, 2020. SRAX currently provides certain services to us, and costs associated with these functions are billed to us. These services relate to: executive management, information technology, legal, finance and accounting, human resources, tax, treasury, research and development, sales and marketing, shared facilities and other services.

On February 4, 2021, we completed the share exchange transaction (“Share Exchange”) as described in the share exchange agreement (“Exchange Agreement”). The Exchange Agreement and proposed Share Exchange was disclosed in our Current Report on Form 8-K that was filed with the Securities and Exchange Commission (the “Commission” or “SEC”)) on October 5, 2020.

Pursuant to the Share Exchange, we acquired all of the outstanding capital stock of BIG Token. As a result, we became a majority owned subsidiary of SRAX, BIG Token became our wholly owned subsidiary and Force Protection Video Equipment Corporation adopted BIG Token’s business plan. In connection with the Share Exchange, we entered into the following agreements:

| 8 |

Transition Services Agreement

On January 27, 2021, we entered into the Transition Services Agreement (“TSA”) with SRAX and BIG Token. Pursuant to the TSA, SRAX will provide us with certain transitional related services for such period of time as needed. Pursuant to the TSA, we pay SRAX, on a monthly basis, for certain services required to run the BIG Token business and platform, including but not limited to: (i) general and administrative services, (ii) finance and accounting services, (iii) technical operations, (iv) software services, (v) human resources services, (vi) use of facilities, (vii) and other services on an as needed basis if requested by the Company.

Master Separation Agreement

On January 27, 2021, we entered into a Master Separation Agreement (“MSA”) with SRAX. Pursuant to the MSA: (a) SRAX transferred all of the BIG Token assets required to run the BIG Token business including but not limited to (i) SRAXauto, SRAXcore, and SRAXshopper advertising tools and software, (ii) the BIG Token platform, (iii) associated BIG Token software and hardware; (iv) contracts associated with BIG Token, (v) intellectual property rights associated with BIG Token, (vi) bank accounts and certain inventory of BIG Token, and (vii) other assets required in the BIG Token business; and (b) certain liabilities and obligations related to the BIG Token business including but not limited to (v) liabilities related to the BIG Token business, (w) certain BIG Token accounts payable, (x) liabilities resulting from BIG Token contracts, (y) liabilities arising out of third-party claims against the BIG Token business and its assets, and (z) other liabilities that arise out of or result from the BIG Token business prior or subsequent to the closing of the Share Exchange. SRAX and the Company further agreed to take such steps necessary to facilitate the transfers, including continued efforts on each party if there is any delay in the assignment of any asset or liability.

The MSA also requires, for as long as SRAX is required to consolidate our results of operations and financial position, that we agree to: (i) prepare its annual and quarterly financial statements in accordance with the general accepted accounting principles (GAAP), (ii) undertake certain internal controls and procedures over financial reporting, (iii) provide our preliminary financial statements to SRAX for review, (iv) file all required quarterly and annual reports with the Commission on a timely basis, (v) provide SRAX with all annual budgets and periodic financial projections related to our operations on a consolidated basis, (vi) cooperate with SRAX on all public filings, press releases, and proxy statements filed or disseminated by SRAX as needed, and (vii) to use the same certified public accountant as SRAX.

Provided that SRAX owns at least fifty percent (50%) of the total voting power of our capital stock, without the prior consent of SRAX, we (i) will not restrict the ability of SRAX to sell, transfer or dispose of the Common Stock, (ii) will not breach certain contraction obligation to which SRAX is a party to and pursuant to which we receive a benefit pursuant to the TSA, and (iii) will not make any acquisitions or dispositions of businesses or assets in excess of $3,000,000 in the aggregate, or acquire shares, or interest in any company or partnership or loans in excess of $3,000,000 in the aggregate.

SRAX as our Controlling Stockholder

SRAX currently owns 149,562,566,584 shares of our Common Stock or approximately 95% of the voting power of the Company. For as long as SRAX continues to control more than 50% of our outstanding common stock, SRAX or its successor-in-interest will be able to direct the election of all the members of our board of directors. Similarly, SRAX will have the power to determine matters submitted to a vote of our stockholders without the consent of our other stockholders, will have the power to prevent a change in control of us and will have the power to take certain other actions that might be favorable to SRAX. In addition, the master separation agreement will provide that, as long as SRAX beneficially owns at least 50% of the total voting power of our outstanding capital stock entitled to vote in the election of our board of directors, we will not (without SRAX’s prior written consent) take certain actions, such as incurring additional indebtedness and acquiring businesses or assets or disposing of assets in excess of certain amounts. To preserve the tax-free treatment of the separation, the master separation agreement will include certain covenants and restrictions to ensure that, until immediately prior to the share exchange, SRAX will retain beneficial ownership of at least 80% of our carve-out voting power and 80% of each class of nonvoting capital stock, if any is outstanding. In addition, to preserve the tax-free treatment of the separation, we will agree in the tax matters agreement to restrictions, including restrictions that would be effective during the period following the distribution, that could limit our ability to pursue certain strategic transactions, equity issuances or repurchases or other transactions that we may believe to be in the best interests of our stockholders or that might increase the value of our business.

| 9 |

| ITEM 1A. | RISK FACTORS. |

Investing in our Common Stock involves substantial risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this Annual Report, including our financial statements and the related notes included elsewhere in this Annual Report, before deciding whether to invest in shares of our common stock. We describe below what we believe are currently the material risks and uncertainties we face, but they are not the only risks and uncertainties we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. If any of the following risks actually occur, our business, financial condition, results of operations and future prospects could be materially and adversely affected. In that event, the market price of our common stock could decline and you could lose part or all of your investment.

Risks Related to the COVID-19 Pandemic

The COVID-19 pandemic, or other epidemic and pandemic diseases or governmental or other actions taken in response to them, could significantly disrupt our business.

Outbreaks of epidemic, pandemic or contagious diseases, such as the recent SARS-CoV-2 virus, or coronavirus, which causes coronavirus disease 2019, or COVID-19, or, historically, the Ebola virus, Middle East Respiratory Syndrome, Severe Acute Respiratory Syndrome or the H1N1 virus, could significantly disrupt our business. These outbreaks pose the risk that we or our employees, contractors, and other partners may be prevented from conducting business activities for an indefinite period of time due to spread of the disease within these groups, or due to restrictions that may be requested or mandated by governmental authorities. Business disruptions could include disruptions or restrictions on our ability to travel, as well as temporary closures of all or part of our facilities and the facilities of our partners. As the COVID-19 pandemic rapidly evolves and spreads, both across the United States and through much of the world, we continue to actively monitor the impact that COVID-19 is having and may have on our business.

As a result of the COVID-19 pandemic, many states and counties have issued and may in the future issue orders for all residents to remain at home, except as needed for essential activities, and have placed restrictions on the scope and conduct of business activities. As a result, we have implemented work from home policies for a majority of our employees that may continue for an indefinite period. We have taken steps to ensure the safety of our patients and employees, while working to ensure the sustainability of our business operations as this unprecedented situation continues to evolve.

In addition, a significant outbreak of epidemic, pandemic or contagious diseases in the human population, such as the global COVID-19 pandemic, could result in a widespread health crisis and adversely affect the economies and financial markets of many countries, resulting in an economic downturn that could affect demand for our current or future products.

While the potential economic impact brought by, and the duration of, COVID-19 may be difficult to assess or predict, a continuing widespread pandemic could result in significant disruption of global financial markets, reducing our ability to access capital, which could in the future negatively affect our liquidity. In addition, a recession or market correction resulting from the spread of COVID-19 could materially affect the value of our common stock.

Risks Related to Our Business

We have a history of operating losses and there are no assurances we will report profitable operations in the foreseeable future.

We have losses from operations of $8,581,000 and $15,981,000 for the years ended December 31, 2020 and 2019, respectively. Our future success depends upon our ability to continue to grow our revenues, contain our operating expenses and generate profits. We do not have any long-term agreements with our customers. There are no assurances that we will be able to increase our revenues and cash flow to a level which supports profitable operations. We may continue to incur losses in future periods until such time, if ever, as we are successful in significantly increasing our revenues and cash flow beyond what is necessary to fund our ongoing operations and pay our obligations as they become due. If we are not able to grow, increase revenue and begin generating consistent profits, it is unlikely we will be able to generate sufficient cash from operations to pay our operating expenses and service our debt obligations, or report profitable operations in future periods.

| 10 |

We may not be able to continue as a going concern if we do not obtain additional financing.

We have incurred losses since our inception and have not demonstrated an ability to generate revenues from the sales of our proposed products. Our ability to continue as a going concern is dependent on raising capital from the sale of our common stock and/or obtaining debt financing. Our cash, cash equivalents and short-term investment balance as of December 31, 2020 was approximately $1,000. On March 12, 2021 we closed on the private placement of our Series B Preferred Stock. The offering resulted in gross proceeds of 4,724,827, not including an additional $1,050,000 that we closed on in October 2020. Based on our cash, cash equivalents and short term investments, as well as the proceeds from our offering, as well as our current expected level of operating expenditures, we expect to be able to fund our operations through the third quarter of 2021. Our ability to remain a going concern is wholly dependent upon our ability to continue to obtain sufficient capital to fund our operations. Accordingly, despite our ability to secure capital in the past, there can be no assurance that additional equity or debt financing will be available to us when needed or that we may be able to secure funding from any other sources. In the event that we are not able to secure funding, we may be forced to curtail operations, delay or stop ongoing clinical trials, cease operations altogether or file for bankruptcy.

We will need to raise additional capital to continue operations.

We have historically operated as a business unit of SRAX and accordingly, SRAX has funded our operations. As of December 31, 2020, we had minimal cash or cash equivalents or short-term investment. On March 12, 2021, we closed on a private placement of our Series B Preferred Stock resulting in gross proceeds of approximately $4.7 million. Based on our cash, cash equivalents and short term investments, as well as the proceeds from our offering, as well as our current expected level of operating expenditures, we expect to be able to fund our operations through the third quarter of 2021. We cannot assure you that we will be able to secure additional capital through financing transactions, including issuance of debt. Our inability to operate profitably, or secure additional financing will materially impact our ability to fund our current and planned operations.

We have spent and expect to continue spending substantial cash in the execution of our business plan and the development of the BIG Token platform. We cannot assure you that financing will be available if needed. If additional financing is not available, we may not be able to fund our operations, develop or enhance our product offerings, take advantage of business opportunities or respond to competitive market pressures. If we exhaust our cash reserves and are unable to secure additional financing, we may be unable to meet our obligations which could result in us initiating bankruptcy proceedings or delaying or eliminating some or all our research and product development programs.

Our failure to maintain an effective system of internal control over financial reporting may result in the need for us to restate previously issued financial statements. As a result, current and potential stockholders may lose confidence in our financial reporting, which could harm our business and value of our stock.

Or management has determined that, as of December 31, 2020, we did not maintain effective internal controls over financial reporting based on criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission in Internal Control-Integrated Framework as a result of identified material weaknesses in our internal control over financial reporting. A material weakness is a deficiency, or a combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of the company’s annual or interim financial statements will not be prevented or detected on a timely basis.

Our auditors have expressed substantial doubt about our ability to continue as a going concern.

Our auditors’ report on our December 31, 2020 consolidated financial statements expresses an opinion that our capital resources as of the date of their audit report were not sufficient to sustain operations or complete our planned activities for the upcoming year unless we raised additional funds. Our current cash level raises substantial doubt about our ability to continue as a going concern past the third quarter of 2021. If we do not obtain additional capital by such time, we may no longer be able to continue as a going concern and may cease operation or seek bankruptcy protection.

| 11 |

If we are unable to successfully retain and integrate a new management team, our business could be harmed.

We have historically operated as a business unit of SRAX. Our success depends largely on the development and execution of our business strategy by our senior management team. Effective February 16, 2021, Lou Kerner was appointed Chief Executive Officer. Our success depends largely on the development and execution of our business strategy by our senior management team. We currently have a limited executive team which may adversely affect our business. Additionally, the loss of any members or key personnel would likely harm our ability to implement our business strategy and respond to the rapidly changing market conditions in which we operate. There may be a limited number of persons with the requisite skills to serve in these positions, and we cannot assure you that we would be able to identify or employ such qualified personnel on acceptable terms, if at all. We cannot assure you that management will succeed in working together as a team. In the event we are unsuccessful, our business and prospects could be harmed.

We depend on the services of our executive officers and the loss of any of their services could harm our ability to operate our business in future periods.

Our success largely depends on the efforts and abilities of our or Chief Executive Officer, Lou Kerner. We are a party to an employment agreement with Mr. Kerner. Although we do not expect to lose his services in the foreseeable future, the loss of any of them could materially harm our business and operations in future periods until such time as we were able to engage a suitable replacement.

We have no operating history as a standalone entity or management team as presently configured which results in a high degree of uncertainty regarding our ability to effectively operate our business.

Our limited staff, operating history as well as our recently appointed management team means that there is a high degree of uncertainty regarding our ability to:

| ● | develop and commercialize our technologies and proposed products; | |

| ● | identify, hire and retain the needed personnel to implement our business plan; | |

| ● | manage growth; or | |

| ● | respond to competition. |

No assurances can be given as to exactly when, if at all, we will be able to develop our business or take the necessary steps to derive net income.

The employment contract of Lou Kerner contains anti-termination provisions which could make changes in management difficult or expensive.

We have entered into an employment agreement with Lou Kerner, our Chief Executive Officer. This agreement may require the payment of severance in the event he ceases to be employed. The provision makes the replacement of Mr. Kerner costly and could cause difficulty in effecting any required changes in management or a change in control.

We may be required to expend significant capital to redeem BIGtoken Points which will negatively impact our ability to fund our core operations.

Users of BIGtoken receive points for undertaking certain actions on the platform that may be redeemed directly for cash from us, with such value as determined by management. Accordingly, we are currently obligated to redeem users’ points which are earned on BIGtoken. We are currently redeeming each point for up to $0.01, subject to the user meeting certain conditions. As of December 31, 2020, we recorded a contingent liability for future point redemptions equal to approximately $445,000 and we have redeemed an aggregate amount of approximately $1,250,000. As of December 31, 2020, we had approximately 16 million application downloads. If our users continue to increase, we will be required to have enough cash reserves to redeem points held by our qualified users for cash. There can be no assurance that we will have enough cash reserves, or if we do have sufficient cash, if we will be able to continue to fund our other business obligations and operational expenses.

| 12 |

If our efforts to attract and retain BIGtoken users are not successful, our number of users and the amount of data collected could fail to reach critical mass, grow or decline and our potential for BIGtoken to earn revenues may be materially affected.

We will be dependent on advertisers to pay us for access to user data. We must attract users to grow the amount of accessible data and make it attractive to these third parties. If the public does not perceive our mission or our services to be reliable, valuable or of high quality, we may not be able to attract or retain users and create a critical mass of data which will impact our ability to earn revenues which could have a materially adversely affected us.

The regulatory regime governing blockchain technologies, cryptocurrencies, digital assets, utility tokens, security tokens and offerings of digital assets is evolving and uncertain, and new regulations or policies may materially adversely affect our development.

We anticipate embracing digital assets and cryptocurrencies in the future. Regulation of digital assets like, cryptocurrencies, blockchain technologies and cryptocurrency exchanges, is currently undeveloped and likely to rapidly evolve as government agencies take greater interest in them. Regulation also varies significantly among international, federal, state and local jurisdictions and is subject to significant uncertainty. Various legislative and executive bodies in the United States and in other countries may in the future adopt laws, regulations, or guidance, or take other actions, which may severely impact the permissibility of tokens generally and the technology behind them or the means of transaction or in transferring them. The regulatory regime governing blockchain technologies, cryptocurrencies, digital assets, utility tokens, security tokens and offerings of digital assets is uncertain, and new regulations or policies may materially adversely affect the development and the value of the Company if we materially embrace digital assets and cryptocurrencies in the future.

Natural disasters, epidemic or pandemic disease outbreaks, trade wars, political unrest or other events could disrupt our business or operations or those of our development partners, manufacturers, regulators or other third parties with whom we conduct business now or in the future.

A wide variety of events beyond our control, including natural disasters, epidemic or pandemic disease outbreaks (such as the recent novel coronavirus outbreak), trade wars, political unrest or other events could disrupt our business or operations or those of our manufacturers, regulatory authorities, or other third parties with whom we conduct business. These events may cause businesses and government agencies to be shut down, supply chains to be interrupted, slowed, or rendered inoperable, and individuals to become ill, quarantined, or otherwise unable to work and/or travel due to health reasons or governmental restrictions. For example, California recently ordered most businesses closed, mandating work-from-home arrangements, where feasible, in response to the coronavirus pandemic. These limitations could negatively affect our business operations and continuity and could negatively impact our ability to timely perform basic business functions, including making SEC filings and preparing financial reports. If our operations or those of third parties with whom we have business are impaired or curtailed as a result of these events, the development and commercialization of our products and product candidates could be impaired or halted, which could have a material adverse impact on our business.

Challenges in acquiring user data could adversely affect our ability to retain and expand BIGtoken, and therefore could materially affect our business, financial condition and results of operations.

In order to expand BIGtoken, we must continue to expend resources to make the submission of user data as user-friendly as possible. We, and our users, may face legal, logistical, cultural and commercial challenges in procuring user data. Additionally, once such data is obtained, if the process for validation and collection of rewards may be perceived as too cumbersome and discourage potential users from submission. We may need to expend significant resources on user interfaces for evolving platforms, such as mobile devices. Inconveniences to our users or potential users at any stage of the process may materially challenge our growth.

If we fail to ensure that the user data derived from BIGtoken is of high quality, our ability to attract customers or monetize the data may be materially impaired.

The reliability of our user data depends upon the integrity and the quality of the process of accepting user data into BIGtoken. We will take certain measures to validate user data submitted by our users and potential users to assure a high quality of data in BIGtoken and generally confirming that data is submitted in accordance with our terms for such data. We must continue to invest in our quality control measures relating to BIGtoken in order to provide a high-quality product to potential customers.

If BIGtoken experiences an excessive rate of user attrition, our ability to attract customers could fail.

Users may elect to have their data deleted from BIGtoken at any time. We must continually add new users both to replace users who choose to delete their data and to increase our user base. Users may choose to delete their data for many reasons. If users are concerned about privacy and security and do not perceive BIGtoken to be reliable, if we fail to keep users engaged and interested in our application, or if we simply lose our users’ attention, we could fail to gather sufficient user data and our ability to earn revenues may be materially affected.

| 13 |

If we are unable to manage our marketing and advertising expenses, it could materially harm our results of operations and growth.

We plan to rely in part on our marketing and advertising efforts to attract new members. Our future growth and profitability, as well as the maintenance and enhancement of our brand, will depend in large part on the effectiveness and efficiency of our marketing and advertising strategies and expenditures. If we are unable to maintain our marketing and advertising channels on cost-effective terms, our marketing and advertising expenses could increase substantially, and our business, financial condition and results of operations may suffer. In addition, we may be required to incur significantly higher marketing and advertising expenses than we currently anticipate if excessive numbers of members withdraw their member data from our database.

Failure to comply with federal, state and local laws and regulations or our contractual obligations relating to data privacy, protection and security of BIGtoken user data, and civil liabilities relating to breaches of privacy and security of user data, could damage our reputation and harm our business.

A variety of federal, state and local laws and regulations govern the collection, use, retention, sharing and security of user data. We will collect BIGtoken user data from and about our members when they redeem rewards and maintain that date in our BIGtoken Application. Claims or allegations that we have violated applicable laws or regulations related to privacy, data protection or data security could in the future result in negative publicity and a loss of confidence in us by our users and potential new users and may subject us to fines and penalties by regulatory authorities. In addition, we have privacy policies and practices concerning the collection, use and disclosure of user data as part of our agreements with our members, including ones posted on our website. Several Internet companies have incurred penalties for failing to abide by the representations made in their privacy policies and practices. In addition, our use and retention of user data could lead to civil liability exposure in the event of any disclosure of such information due to hacking, malware, phishing, inadvertent action or other unauthorized use or disclosure. Several companies have been subject to civil actions, including class actions, relating to this exposure.

We have incurred, and will continue to incur, expenses to comply with data privacy, protection and security standards and protocols for BIGtoken user data imposed by law, regulation, self-regulatory bodies, industry standards and contractual obligations. Such laws, standards and regulations, however, are evolving and subject to potentially differing interpretations, and federal, state and provincial legislative and regulatory bodies may expand current or enact new laws or regulations regarding privacy matters. Additionally, we accept user from foreign countries which subjects us to the personal and other data privacy, protection and security laws of those countries, We are unable to predict what additional legislation, standards or regulation in the area of privacy and security of personal information could be enacted or its effect on our operations and business.

If we are unable to satisfy data privacy, protection, security, and other government- and industry-specific requirements, our growth could be harmed.

We need or may in the future need to comply with a number of data protection, security, privacy and other government- and industry-specific requirements, including those that require companies to notify individuals of data security incidents involving certain types of personal data. Security compromises could harm our reputation, erode user confidence in the effectiveness of our security measures, negatively impact our ability to attract new members, or cause existing users to withdraw their data from BIGtoken.

| 14 |

Regulatory, legislative or self-regulatory developments regarding internet privacy matters could adversely affect our ability to conduct our business.

The United States and foreign governments have enacted, considered or are considering legislation or regulations that could significantly restrict our ability to collect, process, use, transfer and pool data collected from and about consumers and devices. Trade associations and industry self-regulatory groups have also promulgated best practices and other industry standards relating to targeted advertising. Various U.S. and foreign governments, self-regulatory bodies and public advocacy groups have called for new regulations specifically directed at the digital advertising industry, and we expect to see an increase in legislation, regulation and self-regulation in this area. The legal, regulatory and judicial environment we face around privacy and other matters is constantly evolving and can be subject to significant change. For example, the General Data Protection Regulation, or GDPR, which was agreed by E.U. institutions in 2016 and came into effect after a two-year transition period on May 25, 2018, updated and modernized the principles of the 1995 Data Protection Directive and significantly increases the level of sanctions for non-compliance. Data Protection Authorities will have the power to impose administrative fines of up to a maximum of €20 million or 4% of the data controller’s or data processor’s total worldwide turnover of the preceding financial year. Similarly, the E-Privacy Regulation, which was launched by the European Parliament in October 2016, could result in, once enacted, new rules and mechanisms for “cookie” consent. In addition, the interpretation and application of data protection laws in the U.S., Europe and elsewhere are often uncertain and in flux. Legislative and regulatory authorities around the world may decide to enact additional legislation or regulations, which could reduce the amount of data we can collect or process and, as a result, significantly impact our business. Similarly, clarifications of and changes to these existing and proposed laws, regulations, judicial interpretations and industry standards can be costly to comply with, and we may be unable to pass along those costs to our clients in the form of increased fees, which may negatively affect our operating results. Such changes can also delay or impede the development of new solutions, result in negative publicity and reputational harm, require significant incremental management time and attention, increase our risk of non-compliance and subject us to claims or other remedies, including fines or demands that we modify or cease existing business practices, including our ability to charge per click or the scope of clicks for which we charge. Additionally, any perception of our practices or solutions as an invasion of privacy, whether or not such practices or solutions are consistent with current or future regulations and industry practices, may subject us to public criticism, private class actions, reputational harm or claims by regulators, which could disrupt our business and expose us to increased liability. Finally, our legal and financial exposure often depends in part on our clients’ or other third parties’ adherence to privacy laws and regulations and their use of our services in ways consistent with visitors’ expectations. We rely on representations made to us by clients that they will comply with all applicable laws, including all relevant privacy and data protection regulations. We make reasonable efforts to enforce such representations and contractual requirements, but we do not fully audit our clients’ compliance with our recommended disclosures or their adherence to privacy laws and regulations. If our clients fail to adhere to our contracts in this regard, or a court or governmental agency determines that we have not adequately, accurately or completely described our own solutions, services and data collection, use and sharing practices in our own disclosures to consumers, then we and our clients may be subject to potentially adverse publicity, damages and related possible investigation or other regulatory activity in connection with our privacy practices or those of our clients.

Privacy concerns could damage our reputation and deter current and potential users from contributing additional data through our BIGtoken Application. If our security measures are breached resulting in the improper use and disclosure of user data, BIGtoken may be perceived as not being secure, users and customers may curtail or stop using BIGtoken, and we may incur significant legal and financial exposure.

Concerns about our practices with regard to the collection, use, disclosure, or security of user data or other privacy related matters, even if unfounded, could damage our reputation and adversely affect our operating results. Our services will involve the purchase, storage, transmission and sale of user data, and theft and security breaches expose us to a risk of loss of this information, improper use and disclosure of such information, litigation, and potential liability. Any systems failure or compromise of our security that results in the release of user data, or in our or our users’ ability to access such data, could seriously harm our reputation and brand and, therefore, our business, and impair our ability to attract and retain users. Additionally, if user data is somehow made public or made available through a security breach, it may be used to identify our users and people related thereto. We may experience cyber attacks of varying degrees. Our security measures may also be breached due to employee error, malfeasance, system errors or vulnerabilities, including vulnerabilities of our vendors, suppliers, their products, or otherwise. Such breach or unauthorized access, increased government surveillance, or attempts by outside parties to fraudulently induce employees, users, or customers to disclose sensitive information in order to gain access to user data could result in significant legal and financial exposure, damage to our reputation, and a loss of confidence in the security of BIGtoken that could potentially have an adverse effect on our business. Because the techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently, become more sophisticated, and often are not recognized until launched against a target, we may be unable to anticipate these techniques or to implement adequate preventative measures. Additionally, cyber attacks could also compromise trade secrets and other sensitive information and result in such information being disclosed to others and becoming less valuable, which could negatively affect our business. If an actual or perceived breach of our security occurs, the market perception of the effectiveness of our security measures could be harmed and we could lose members and customers.

| 15 |

Our business is subject to complex and evolving U.S. and foreign laws and regulations regarding privacy, data protection, content, competition, consumer protection, and other matters. Many of these laws and regulations are subject to change and uncertain interpretation, and could result in claims, changes to our business practices, monetary penalties, increased cost of operations, or declines in user growth or engagement, or otherwise harm our business.

We are subject to a variety of laws and regulations in the United States and abroad that involve matters central to our business, such as privacy, data protection and personal information, rights of publicity, content, intellectual property, advertising, marketing, distribution, data security, data retention and deletion, electronic contracts and other communications, competition, protection of minors, consumer protection, taxation and securities law compliance. Expansion of our activities in certain jurisdictions, or other actions that we may take, may subject us to additional laws, regulations, or other government scrutiny. In addition, foreign data protection, privacy, content, competition, and other laws and regulations can impose different obligations or be more restrictive than those in the United States.

Additionally, as we allow European users, we are subject to the European General Data Protection Regulation (GDPR), effective as of May 2018. The GDPR increases privacy rights for individuals in Europe, extends the scope of responsibilities for data controllers and data processors and imposes increased requirements and potential penalties on companies offering goods or services to individuals who are located in Europe or monitoring the behavior of such individuals (including by companies based outside of Europe). Noncompliance can result in penalties of up to the greater of €20 million, or 4% of global company revenues.

These U.S. federal and state and foreign laws and regulations, which in some cases can be enforced by private parties in addition to government authorities, are constantly evolving and can be subject to significant change. As a result, the application, interpretation, and enforcement of these laws and regulations are often uncertain, particularly in the newer industry in which we operate, and may be interpreted and applied inconsistently from country to country and inconsistently with our current policies and practices.

These laws and regulations, as well as any associated inquiries or investigations or any other government actions, may be costly to comply with and may delay or impede our international growth, result in negative publicity, increase our operating costs, require significant management time and attention, and subject us to remedies that may harm our business.

Security breaches and improper access to or disclosure of our data or user data, or other hacking and phishing attacks on our systems, could harm our reputation and adversely affect our business.

Our industry is prone to cyber-attacks by third parties seeking unauthorized access to our data or users’ data or to disrupt our ability to provide service. Any failure to prevent or mitigate security breaches and improper access to or disclosure of our data or user data, including personal information, content, or payment information from or to users, or information from marketers, could result in the loss or misuse of such data, which could harm our business and reputation and diminish our competitive position. In addition, computer malware, viruses, social engineering (predominantly spear phishing attacks), and general hacking have become more prevalent in our industry. Our BIGtoken platform has experienced an increase in the occurrence of such attempts and we cannot be assured that we will be able to prevent a successful attack on our systems in the future. We also regularly encounter attempts to create false or undesirable user accounts or take other actions on our BIGtoken platform for purposes such as spreading misinformation, attempting to have us improperly purchase user data or other objectionable ends. As a result of recent attention and growth of our BIGtoken platform, the size of our user base, and the types and volume of personal data on our systems, we believe that we are a particularly attractive target for such breaches and attacks. Our efforts to address undesirable activity may also increase the risk of retaliatory attacks. Such attacks may cause interruptions to the services we provide, degrade the user experience, cause users or marketers to lose confidence and trust in our products, impair our internal systems, or result in financial harm to us. Our efforts to protect our company data or the information we receive may also be unsuccessful due to software bugs or other technical malfunctions; employee, contractor, or vendor error or malfeasance; government surveillance; or other threats that evolve. In addition, third parties may attempt to fraudulently induce employees or users to disclose information in order to gain access to our data or our users’ data. Cyber-attacks continue to evolve in sophistication and volume, and inherently may be difficult to detect for long periods of time. Although we are currently in the process of developing systems and processes that are designed to protect our data and user data, to prevent data loss, to disable undesirable accounts and activities on our BIGtoken platform, and to prevent or detect security breaches, we cannot assure you that such measures will ultimately become operational or provide absolute security, and we may incur significant costs in protecting against or remediating cyber-attacks.

| 16 |

Affected users or government authorities could initiate legal or regulatory actions against us in connection with any actual or perceived security breaches or improper disclosure of data, which could cause us to incur significant expense and liability or result in orders or consent decrees forcing us to modify our business practices, especially with regard to the BIGtoken platform. Such incidents or our efforts to remediate such incidents may also result in a decline in our active user base or engagement levels. Any of these events could have a material and adverse effect on our business, reputation, or financial results.

Certain user data must be provided on a recurring basis in order to provide full value.

Certain types of user data will need to be contributed by users recurrently for such data to provide full value to our potential customers. If users fail to provide us with sufficient recurring data, the value of the user data may substantially decrease and our ability to earn revenues may be materially affected.

Unfavorable media coverage could negatively affect our business.

Unfavorable publicity regarding, for example, our privacy practices, terms of service, regulatory activity, the actions of third parties, the use of our products or services for illicit, objectionable, or illegal ends or the actions of other companies that provide similar services to us, could adversely affect our reputation. Such negative publicity also could have an adverse effect on the size, engagement, and loyalty of our user base and result in user attrition which could adversely affect our business and financial results.

Weak economic conditions may reduce consumer demand for products and services.

A weak economy in the United States could adversely affect demand for advertising products, and services. A substantial portion of our revenue is derived from businesses that are highly dependent on discretionary spending by individuals, which typically falls during times of economic instability. Accordingly, the ability of our advertisers to increase or maintain revenue and earnings could be adversely affected to the extent that relevant economic environments remain weak or decline further. We currently are unable to predict the extent of any of these potential adverse effects.

Because we store, process and use data, some of which contain personal information, we are subject to complex and evolving federal, state and foreign laws and regulations regarding privacy, data protection and other matters, which are subject to change.

We are subject to a variety of laws and regulations in the United States and other countries that involve matters central to our business, including with respect to user privacy, rights of publicity, data protection, content, protection of minors and consumer protection. These laws can be particularly restrictive in countries outside the United States. Both in the United States and abroad, these laws and regulations constantly evolve and remain subject to significant change. In addition, the application and interpretation of these laws and regulations are often uncertain, particularly in the new and rapidly evolving industry in which we operate. Because we store, process and use data, some of which contain personal information, we are subject to complex and evolving federal, state and foreign laws and regulations regarding privacy, data protection and other matters. Many of these laws and regulations are subject to change and uncertain interpretation and could result in investigations, claims, changes to our business practices, increased cost of operations and declines in user growth, retention or engagement, any of which could materially adversely affect our business, results of operations and financial condition.

Several proposals are pending before federal, state and foreign legislative and regulatory bodies that could significantly affect our business. For example, a revision to the 1995 European Union Data Protection Directive is currently being considered by European legislative bodies that may include more stringent operational requirements for data processors and significant penalties for non-compliance. In addition, the EU General Data Protection Regulation 2016/679 (“GDPR”), which came into effect on May 25, 2018, establishes new requirements applicable to the processing of personal data ( i.e. , data which identifies an individual or from which an individual is identifiable), affords new data protection rights to individuals ( e.g. , the right to erasure of personal data) and imposes penalties for serious data breaches. Individuals also have a right to compensation under GDPR for financial or non-financial losses. GDPR will impose additional responsibility and liability in relation to our processing of personal data. GDPR may require us to change our policies and procedures and, if we are not compliant, could materially adversely affect our business, results of operations and financial condition.

| 17 |

If advertising on the Internet loses its appeal, our revenue could decline.

Our business model may not continue to be effective in the future for a number of reasons, including:

| ● | a decline in the rates that we can charge for advertising and promotional activities; | |

| ● | our inability to create applications for our customers; | |

| ● | Internet advertisements and promotions are, by their nature, limited in content relative to other media; | |

| ● | companies may be reluctant or slow to adopt online advertising and promotional activities that replace, limit or compete with their existing direct marketing efforts; | |

| ● | companies may prefer other forms of Internet advertising and promotions that we do not offer; | |

| ● | the quality or placement of transactions, including the risk of non-screened, non-human inventory and traffic, could cause a loss in customers or revenue; and | |

| ● | regulatory actions may negatively impact our business practices. |

If the number of companies who purchase online advertising and promotional services from us does not grow, we may experience difficulty in attracting publishers, and our revenue could decline.

Our stock price may be volatile and your investment in our common stock could suffer a decline in value.

There has been significant volatility in the market price and trading volume of securities of technology and other companies, which may be unrelated to the financial performance of these companies. These broad market fluctuations may negatively affect the market price of our common stock.

Some specific factors that may have a significant effect on the market price of our common stock include:

| ● | actual or anticipated fluctuations in our results of operations or our competitors’ operating results; | |

| ● | actual or anticipated changes in the growth rate of the connected lifestyle market, our growth rates or our competitors’ growth rates; | |

| ● | conditions in the financial markets in general or changes in general economic conditions; | |

| ● | changes in governmental regulation, including taxation and tariff policies; | |

| ● | interest rate or currency rate fluctuations; | |

| ● | our ability to forecast accurate financial results; and | |

| ● | changes in stock market analyst recommendations regarding our common stock, other comparable companies or our industry generally |

| 18 |

We rely upon third parties for technology that is critical to our products, and if we are unable to continue to use this technology and future technology, our ability to develop, sell, maintain and support technologically innovative products would be limited.

We rely on third parties to obtain non-exclusive patented hardware and software license rights in technologies that are incorporated into and necessary for the operation and functionality of most of our products. In these cases, because the intellectual property we license is available from third parties, barriers to entry into certain markets may be lower for potential or existing competitors than if we owned exclusive rights to the technology that we license and use. Moreover, if a competitor or potential competitor enters into an exclusive arrangement with any of our key third-party technology providers, or if any of these providers unilaterally decides not to do business with us for any reason, our ability to develop and sell products and services containing that technology would be severely limited.