UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| (Mark One) | |||||

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED | |||||

| OR | |||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| FOR THE TRANSITION PERIOD FROM TO | |||||

Commission file number: 001-35826

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of principal executive offices) | (Zip Code) | ||||

(414 ) 390-6100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| (Title of each class) | (Trading Symbol) | (Name of each exchange on which registered) | ||||||

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Accelerated filer o | |||||||||||

Non-accelerated filer o | Smaller reporting company | ||||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

The aggregate market value of common equity held by non-affiliates of the registrant at June 30, 2022, which was the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $2.3 billion based on the closing price of $35.57 for the Class A common stock, as reported on the New York Stock Exchange on that date.

For purposes of this calculation only, it is assumed that the affiliates of the registrant include only directors and executive officers of the registrant.

The number of outstanding shares of the registrant’s Class A common stock, par value $0.01 per share, Class B common stock, par value $0.01 per share, and Class C common stock, par value $0.01 per share, as of February 23, 2023 were 67,948,122 , 2,491,147 and 9,025,147 , respectively.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant’s definitive proxy statement for its annual meeting of stockholders, to be filed with the Securities and Exchange Commission within 120 days after December 31, 2022, are incorporated by reference into Part III of this Form 10-K.

TABLE OF CONTENTS

| Page | ||||||||

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

Except where the context requires otherwise, in this report:

•“Artisan Funds” refers to each series of Artisan Partners Funds, Inc., an open-ended management investment company, registered with the Securities and Exchange Commission.

•“Artisan Global Funds” refers to each sub-fund of Artisan Partners Global Funds plc, an open-ended investment company registered with the Central Bank of Ireland pursuant to the European UCITS Directive.

•“Artisan Private Funds” refers to private investment funds sponsored by Artisan.

•“Client” and “clients” refer to investors who access our investment management services by investing in funds, including Artisan Funds, Artisan Global Funds, Artisan Private Funds, or other pooled investment vehicles (including collective investment trusts) for which we serve as investment adviser, or by engaging us to manage a separate account in one or more of our investment strategies.

•“Company”, “Artisan”, “we”, “us” or “our” refer to Artisan Partners Asset Management Inc. (“APAM”) and its direct and indirect subsidiaries, including Artisan Partners Holdings LP (“Artisan Partners Holdings” or “Holdings”), and, for periods prior to our IPO, “Artisan,” the “company,” “we,” “us” and “our” refer to Artisan Partners Holdings and, unless the context otherwise requires, its direct and indirect subsidiaries. On March 12, 2013, APAM closed its IPO and related IPO Reorganization. Prior to that date, APAM was a subsidiary of Artisan Partners Holdings. The IPO Reorganization and IPO are described in the notes to our consolidated financial statements included in Part II of this Form 10-K.

•“IPO” means the initial public offering of 12,712,279 shares of Class A common stock of Artisan Partners Asset Management Inc. completed on March 12, 2013.

•“IPO Reorganization” means the series of transactions Artisan Partners Asset Management Inc. and Artisan Partners Holdings completed on March 12, 2013, immediately prior to the IPO, in order to reorganize their capital structures in preparation for the IPO.

•“2020 Follow-On Offering” means the registered offering of 1,802,326 shares of Class A common stock of Artisan Partners Asset Management Inc. completed on February 24, 2020.

i

•“2021 Follow-On Offering” means the registered offering of 963,614 shares of Class A common stock of Artisan Partners Asset Management Inc. completed on March 1, 2021.

Forward-Looking Statements

This report contains, and from time to time our management may make, forward-looking statements within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. Statements regarding future events and our future performance, as well as management’s current expectations, beliefs, plans, estimates or projections relating to the future, are forward-looking statements within the meaning of these laws. In some cases, you can identify these statements by forward-looking words such as “may”, “might”, “will”, “should”, “expects”, “intends”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue”, the negative of these terms and other comparable terminology. Forward-looking statements are only predictions based on current expectations and projections about future events. Forward-looking statements are subject to a number of risks and uncertainties, and there are important factors that could cause actual results, level of activity, performance, actions or achievements to differ materially from the results, level of activity, performance, actions or achievements expressed or implied by the forward-looking statements. These factors include: the loss of key investment professionals or senior management, adverse market or economic conditions, poor performance of our investment strategies, change in the legislative and regulatory environment in which we operate, operational or technical errors or other damage to our reputation and other factors disclosed in the Company’s filings with the Securities and Exchange Commission, including those factors listed under the caption entitled “Risk Factors” in Item 1A of this Form 10-K, as may be amended from time to time. We undertake no obligation to publicly update any forward-looking statements in order to reflect events or circumstances that may arise after the date of this report, except as required by law.

Forward-looking statements include, but are not limited to, statements about:

•our anticipated future results of operations;

•our potential operating performance and efficiency, including our ability to operate under different and unique circumstances;

•our expectations with respect to future business initiatives;

•our expectations with respect to the performance of our investment strategies;

•our expectations with respect to future levels of assets under management, including the capacity of our strategies and client cash inflows and outflows;

•our expectations with respect to industry trends and how those trends may impact our business;

•our financing plans, cash needs and liquidity position;

•our intention to pay dividends and our expectations about the amount of those dividends;

•our expected levels of compensation of our employees, including equity- and cash-based long-term incentive compensation;

•our expectations with respect to future expenses and the level of future expenses;

•our expected tax rate, and our expectations with respect to deferred tax assets; and

•our estimates of future amounts payable pursuant to our tax receivable agreements.

ii

Performance and Assets Under Management Information Used in this Report

We manage investments primarily through pooled investment funds and separate accounts. We serve as investment adviser to Artisan Funds, Artisan Global Funds and Artisan Private Funds. We refer to funds and other accounts that are managed by us with a broadly common investment objective and substantially in accordance with a single model account as being part of the same investment “strategy”.

We measure investment performance based upon the results of our “composites”, which represent the aggregate performance of all discretionary client accounts, including pooled investment vehicles, invested in the same strategy, except those accounts with respect to which we believe client-imposed investment restrictions may have a material impact on portfolio construction and those accounts managed in a currency other than U.S. dollars. The results of these excluded accounts, which represented approximately 13% of our assets under management at December 31, 2022, are maintained in separate composites the results of which are not presented in this report.

The performance of accounts with investment restrictions differs from the performance of accounts included in our principal composite for the applicable strategy because one or more securities may be omitted from the portfolio in order to comply with client restrictions and the weightings in the portfolio of other securities are typically correspondingly altered. The performance of non-U.S. dollar accounts differs from the performance of the principal composite for the applicable strategy because of the fluctuations in currency exchange rates between the currencies in which portfolio securities are traded and the currency in which the account is managed or U.S. dollars, respectively. Results for any investment strategy described herein, and for different investment vehicles within a strategy, are affected by numerous factors, including: different material market or economic conditions; different investment management fee rates, brokerage commissions and other expenses; and the reinvestment of dividends or other earnings. The returns for any strategy may be positive or negative, and past performance does not guarantee future results. In this report, we refer to the date on which we began tracking the performance of an investment strategy as the “inception date”.

Unless otherwise noted, we present the average annual returns of our composites on a “gross” basis, which represent average annual returns before payment of fees payable to us by any portfolio in the composite and net of commissions and transaction costs. An investor’s return in a portfolio would be lower than the gross results presented due to the deduction of applicable fees and expenses. We also present the average annual returns of certain market indices or “benchmarks” for the comparable period. The indices are unmanaged and have differing volatility, credit and other characteristics. You should not assume that there is any material overlap between the securities included in the portfolios of our investment strategies during these periods and those that comprise any of the strategy’s comparator index in this report. At times, this causes material differences in relative performance. It is not possible to invest directly in any of the indices. The returns of these indices, as presented in this report, have not been reduced by fees and expenses associated with investing in securities, but do include the reinvestment of dividends.

In these materials, we present Value Added, which is the difference, in basis points, between an Artisan strategy’s average annual return and the return of its respective benchmark. The benchmark used for purposes of presenting a strategy’s performance and calculating Value Added is generally the market index most commonly used by our clients to compare the performance of the relevant strategy or, if none, the market index used by management to evaluate the performance of the strategy. Composites / Indexes used for the Value Added calculations described are: Non-U.S. Growth Strategy / International Value Strategy-MSCI EAFE Index; Global Discovery / Global Equity Strategy / Global Opportunities Strategy / Global Value Strategy-MSCI ACWI Index; Non-U.S. Small-Mid Growth Strategy-MSCI ACWI ex-USA Small Mid Index; U.S. Mid-Cap Growth Strategy-Russell Midcap Growth® Index; U.S. Mid-Cap Value Strategy-Russell Midcap Value® Index; U.S. Small-Cap Growth Strategy-Russell 2000 Growth® Index; Value Equity Strategy-Russell 1000 Value® Index; Developing World Strategy / Sustainable Emerging Markets Strategy-MSCI Emerging Markets Index; High Income Strategy-ICE BofA U.S. High Yield Master II Total Return Index; Credit Opportunities Strategy-ICE BofA US Dollar LIBOR 3-month Constant Maturity Index; Antero Peak Strategy / Antero Peak Hedge Strategy / Select Equity Strategy / Value Income Strategy-S&P 500® Index; China Post-Venture Strategy-MSCI China SMID Cap Index (Net); International Explorer Strategy-MSCI All Country World Ex USA Small Cap Index; Floating Rate Strategy-Credit Suisse Leveraged Loan Index; Global Unconstrained Strategy-ICE BofA 3-month U.S. Treasury Bill Index; Emerging Markets Debt Opportunities Strategy-J.P. Morgan EMB Hard Currency / Local Currency 50-50 Index; Emerging Markets Local Opportunities Strategy-J.P. Morgan GBI-EM Global Diversified Index.

The MSCI EAFE Index, the MSCI EAFE Growth Index, the MSCI EAFE Value Index, the MSCI ACWI Index, the MSCI ACWI ex-USA Index, the MSCI ACWI ex-USA SMID Index, the MSCI ACWI ex-USA Small Cap, the MSCI Emerging Markets Index and MSCI China SMID Cap Index are trademarks of MSCI Inc. MSCI Inc. is the owner of all copyrights relating to these indices and is the source of the performance statistics of these indices that are referred to in this report. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used to create indices or financial products. This document is not approved or produced by MSCI.

The Russell 2000® Index, the Russell 2000® Value Index, the Russell Midcap® Index, the Russell Midcap® Value Index, the Russell 1000® Index, the Russell 1000® Value Index, the Russell Midcap® Growth Index, the Russell 1000® Growth Index and the Russell 2000® Growth Index are trademarks of Russell Investment Group. Russell Investment Group is the source and owner of the Russell Index data contained or reflected in this report and all trademarks and copyrights related thereto.

The S&P 500 Index is a product of S&P Dow Jones Indices LLC (S&P DJI) and/or its affiliates and has been licensed for use. Copyright© 2023 S&P Dow Jones Indices LLC, a division of S&P Global, Inc. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. S&P® is a registered trademark of S&P Global and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones). None of S&P DJI, Dow Jones, their affiliates or third party licensors makes any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and none shall have any liability for any errors, omissions, or interruptions of any index or the data included therein.

iii

The ICE BofA U.S. High Yield Master II Total Return Index, ICE BofA US Dollar LIBOR 3-month Constant Maturity Index and the ICE BofA 3-Month U.S. Treasury Bill Index are owned by ICE Data Indices, LLC, used with permission. ICE Data Indices, LLC permits use of the ICE BofA indices and related data on an "as is" basis, makes no warranties regarding same, does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the ICE BofA indices or any data included in, related to, or derived therefrom, assumes no liability in connection with the use of the foregoing, and does not sponsor, endorse, or recommend Artisan Partners or any of its products or services.

J.P. Morgan EMB Hard Currency / Local Currency 50/50 Index and the J.P. Morgan GBI-EM Global Diversified Index are trademarks of J.P. Morgan. Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. Indices are used with permission and may not be copied, used, or distributed without J.P. Morgan's prior written approval. Copyright 2023, J.P. Morgan Chase & Co. All rights reserved.

In this report, we present ratings from Morningstar, Inc., for the series of Artisan Funds. The Morningstar RatingTM for funds, or “star rating” is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods. The ratings which form the basis for the information reflected in this report, and the fund categories in which they are rated, relating to each Fund's Investor Share Class are: Artisan Developing World Fund—Diversified Emerging Markets; Artisan Focus Fund—Large Growth; Artisan Global Discovery—Global Small/Mid Stock; Artisan Global Equity Fund—Global Large-Stock Growth; Artisan Global Opportunities Fund—Global Large-Stock Growth; Artisan Global Value Fund—Global Large-Stock Value; Artisan High Income Fund—High Yield Bond; Artisan International Fund—Foreign Large Growth; Artisan International Small-Mid Fund—Foreign Small/Mid Growth; Artisan International Value Fund—Foreign Large Blend; Artisan Mid Cap Fund—Mid-Cap Growth; Artisan Mid Cap Value Fund—Mid-Cap Value; Artisan Small Cap Fund—Small Growth; Artisan Sustainable Emerging Markets Fund—Diversified Emerging Markets; Artisan Value Fund—Large Value; Artisan Select Equity Fund—Large Blend; Artisan International Explorer Fund—Foreign Small/Mid Blend; Artisan Floating Rate Fund—Bank Loan; Artisan Value Income Fund—Large Value; Artisan Global Unconstrained Fund—Nontraditional Bond; Artisan Emerging Markets Debt Opportunities Fund—Emerging Markets Bond. Morningstar ratings are initially given on a fund's three year track record and change monthly.

Throughout this report, we present historical information about our assets under management, including information about changes in our assets under management due to client cash flows, investment returns and transfers between investment vehicles (e.g., pooled investment vehicles and separate accounts). Client cash flows represent client fundings, terminations and client initiated contributions and withdrawals (which could be in cash or in securities), but generally exclude Artisan Funds’ income and capital gain distributions that are not reinvested by fund shareholders. Investment returns and other represents realized gains and losses, the change in unrealized gains and losses, net income and certain miscellaneous items, immaterial in the aggregate, which may include payment of Artisan’s management fees or payment of custody expenses to the extent a client causes these fees to be paid from the account we manage. The effect of translating into U.S. dollars the value of portfolio securities denominated in currencies other than the U.S. dollar is also included in investment returns and other.

We use our information management systems to track our assets under management, the components of investment returns, and client cash flows, and we believe the information set forth in this report regarding our assets under management, investment returns, and client cash flows is accurate in all material respects. We also present information regarding the amount of our assets under management and client cash flows sourced through particular investment vehicles and distribution channels. The allocation of assets under management and client cash flows sourced through particular distribution channels involves estimates because precise information on the sourcing of assets invested in Artisan Funds or Artisan Global Funds through intermediaries is not available on a complete or timely basis and involves the exercise of judgment because the same assets, in some cases, might fairly be said to have been sourced from more than one distribution channel. We have presented the information on our assets under management and client cash flows sourced by distribution channel in the way in which we prepare and use that information in the management of our business. Non-financial data, including information about our investment performance, client cash flows, and assets under management sourced by distribution channel are not subject to our internal controls over financial reporting.

None of the information in this report constitutes either an offer or a solicitation to buy or sell any fund securities, nor is any such information a recommendation for any fund security or investment service.

iv

PART I

Item 1. Business

Overview

Founded in 1994, Artisan is an investment management firm focused on providing high valued added, active investment strategies in asset classes for sophisticated clients around the world.

Since our founding, we have maintained a business model that is designed to maximize our ability to produce attractive investment results for our clients, and we believe this model has contributed to our success in doing so. We focus on attracting, retaining and developing talented investment professionals by creating an environment in which each investment team is provided ample resources and support, transparent and direct financial incentives, a high degree of investment autonomy, and a long-term time horizon. Each of our investment teams is led by one or more experienced portfolio managers and applies its own unique investment philosophy and process. We believe this autonomous investment team structure promotes independent analysis and accountability among our investment professionals, which we believe promotes superior investment results.

Each of our investment teams manages one or more investment strategies, each of which is designed to have a clearly articulated, consistent and replicable investment process that is well-understood by clients and managed to achieve long-term performance. Over our firm’s history, we have created new investment strategies that can use a broad array of securities, instruments and techniques (which we call degrees of freedom) to differentiate returns and manage risk.

We launch a new strategy when we believe it has the potential to achieve superior investment performance in an area that we believe will have sustained client demand at attractive fee rates over the long term. We strive to maintain the integrity of the investment process followed in each of our strategies by rigorous adherence to the investment parameters we have communicated to our clients. We also carefully monitor our investment capacity in each investment strategy. We believe that management of our investment capacity protects our ability to deliver strong investment returns, which protects the interests of our clients and, in the long term, protects our ability to retain client assets and maintain our profit margins. In order to better achieve our long-term goals, we are willing to close a strategy to new investors or otherwise take action to slow or restrict its growth, even though our short-term results may be impacted.

In addition to our investment teams, we have a management team with a fiduciary mindset that is focused on thoughtfully growing the business over the long term while preserving a stable environment for our talented investment professionals and associates. We believe that maintaining the firm’s talent-driven business model and investment-focused culture is critical to generating sustainable, long-term outcomes for clients, which in turn is critical to generating sustainable long-term outcomes for shareholders. To that end, our management team focuses on managing the alignment of, and resources for, the firm’s investment professionals, managing our operational infrastructure to provide a distraction-free investment environment, adhering to our transparent and predictable financial model, and promoting the sustainability of the firm.

We offer our investment management capabilities primarily to institutions and through intermediaries that operate with institutional-like decision-making processes by means of separate accounts and pooled vehicles. We access traditional institutional clients primarily through relationships with investment consultants. We access other institutional-like investors primarily through consultants, alliances with major defined contribution/401(k) platforms and relationships with financial advisors and broker-dealers.

We derive essentially all of our revenues from investment management fees, which primarily are based on a specified percentage of clients’ average assets under management. A small percentage of our clients and investors pay us performance fees or incentive allocations, in which a portion of the fee or allocation is based on the performance of clients’ accounts relative to a benchmark. These investment advisory fees are determined by the investment advisory and sub-advisory agreements between us and our clients. Investment advisory and sub-advisory agreements between us and our clients are generally terminable by our clients upon short or no notice.

Investment Teams

We offer clients a broad range of actively managed investment strategies diversified by asset class, market cap and investment style. Each strategy is managed by one of the investment teams described below. The following table sets forth total assets under management and certain performance information for our investment teams and strategies as of December 31, 2022.

1

| Investment Team and Strategy | AUM as of December 31, 2022 | Composite Inception Date | Value-Added Since Inception Date (1) as of December 31, 2022 | Fund Rating(2) as of December 31, 2022 | |||||||||||||

| (in millions) | |||||||||||||||||

| Growth Team | |||||||||||||||||

| Global Opportunities | 18,676 | February 1, 2007 | 473 | «««« | |||||||||||||

| Global Discovery | 1,392 | September 1, 2017 | 491 | ««««« | |||||||||||||

| U.S. Mid-Cap Growth | 10,624 | April 1, 1997 | 494 | ««« | |||||||||||||

| U.S. Small-Cap Growth | 3,285 | April 1, 1995 | 321 | ««« | |||||||||||||

| Global Equity Team | |||||||||||||||||

| Global Equity | 413 | April 1, 2010 | 342 | ««« | |||||||||||||

| Non-U.S. Growth | 13,285 | January 1, 1996 | 462 | ««« | |||||||||||||

| Non-U.S. Small-Mid Growth | 6,752 | January 1, 2019 | 596 | «««« | |||||||||||||

| China Post-Venture | 173 | April 1, 2021 | (32) | Not Applicable | |||||||||||||

| U.S. Value Team | |||||||||||||||||

| Value Equity | 3,252 | July 1, 2005 | 111 | «« | |||||||||||||

| U.S. Mid-Cap Value | 2,826 | April 1, 1999 | 255 | «« | |||||||||||||

| Value Income | 10 | March 1, 2022 | 324 | Not yet rated | |||||||||||||

| International Value Team | |||||||||||||||||

| International Value | 30,152 | July 1, 2002 | 568 | ««««« | |||||||||||||

| International Explorer | 58 | October 1, 2020 | 812 | Not yet rated | |||||||||||||

| Global Value Team | |||||||||||||||||

| Global Value | 21,432 | July 1, 2007 | 282 | ««« | |||||||||||||

| Select Equity | 335 | March 1, 2020 | (467) | Not yet rated | |||||||||||||

| Sustainable Emerging Markets Team | |||||||||||||||||

| Sustainable Emerging Markets | 873 | July 1, 2006 | 39 | ««« | |||||||||||||

| Credit Team | |||||||||||||||||

| High Income | 6,957 | April 1, 2014 | 251 | ««««« | |||||||||||||

| Credit Opportunities | 136 | July 1, 2017 | 951 | Not Applicable | |||||||||||||

| Floating Rate | 47 | January 1, 2022 | 26 | Not yet rated | |||||||||||||

| Developing World Team | |||||||||||||||||

| Developing World | 3,466 | July 1, 2015 | 486 | «««« | |||||||||||||

| Antero Peak Group | |||||||||||||||||

| Antero Peak | 2,948 | May 1, 2017 | 584 | «««« | |||||||||||||

| Antero Peak Hedge | 728 | November 1, 2017 | 29 | Not Applicable | |||||||||||||

| EMsights Capital Group | |||||||||||||||||

| Global Unconstrained | 16 | April 1, 2022 | 698 | Not yet rated | |||||||||||||

| Emerging Markets Debt Opportunities | 45 | May 1, 2022 | 927 | Not yet rated | |||||||||||||

| Emerging Markets Local Opportunities | 11 | August 1, 2022 | 69 | Not yet rated | |||||||||||||

Total AUM as of December 31, 2022 | 127,892 | ||||||||||||||||

2

(1) Value-added is the amount, in basis points, by which the average annual gross composite return of each of our strategies has outperformed or underperformed its respective benchmark. See “Performance and Assets Under Management Information Used in this Report” for information regarding the benchmarks used. Value-added for periods less than one year is not annualized. The High Income strategy holds loans and other security types that are not included in its benchmark, which, at times, causes material differences in relative performance. The Credit Opportunities strategy is benchmark agnostic and has been compared to the 3-month LIBOR for reference purposes only. The Antero Peak and Antero Peak Hedge strategies' investments in initial public offerings (IPOs) made a material contribution to performance. IPO investments may contribute significantly to a small portfolio’s return, an effect that will generally decrease as assets grow. IPO investments may be unavailable in the future. | |||||||||||||||||

(2) The Overall Morningstar RatingTM applicable to the Artisan Fund managed to each investment strategy is derived from a weighted average of the performance figures associated with its three-year, five-year, and ten-year (if applicable) Morningstar Ratings metrics. | |||||||||||||||||

Growth Team

Our Growth team manages four investment strategies: Global Opportunities, Global Discovery, U.S. Mid-Cap Growth and U.S. Small-Cap Growth. James D. Hamel, Matthew H. Kamm, Craigh A. Cepukenas, Jason L. White and Jay C. Warner are the portfolio managers of all four strategies. Mr. Hamel is the lead portfolio manager of the Global Opportunities strategy; Mr. White is the lead portfolio manager of the Global Discovery strategy; Mr. Kamm is the lead portfolio manager of the U.S. Mid-Cap Growth strategy; and Mr. Cepukenas is the lead portfolio manager of the U.S. Small-Cap Growth strategy.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Global Opportunities (February 1, 2007) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (29.53) | % | 4.71 | % | 7.69 | % | 11.22 | % | 9.95 | % | |||||||||||||||||||

MSCI ACWI® Index | (18.36) | % | 4.00 | % | 5.22 | % | 7.97 | % | 5.22 | % | |||||||||||||||||||

| Global Discovery (September 1, 2017) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (30.08) | % | 5.65 | % | 10.78 | % | — | % | 11.28 | % | |||||||||||||||||||

MSCI ACWI® Index | (18.36) | % | 4.00 | % | 5.22 | % | — | % | 6.37 | % | |||||||||||||||||||

| U.S. Mid-Cap Growth (April 1, 1997) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (36.04) | % | 4.51 | % | 9.18 | % | 11.30 | % | 13.90 | % | |||||||||||||||||||

Russell Midcap® Index | (17.32) | % | 5.87 | % | 7.10 | % | 10.95 | % | 9.86 | % | |||||||||||||||||||

Russell Midcap® Growth Index | (26.72) | % | 3.85 | % | 7.64 | % | 11.40 | % | 8.96 | % | |||||||||||||||||||

| U.S. Small-Cap Growth (April 1, 1995) | |||||||||||||||||||||||||||||

Average Annual Gross Returns | (28.67) | % | 2.35 | % | 9.51 | % | 12.29 | % | 10.37 | % | |||||||||||||||||||

Russell 2000® Index | (20.44) | % | 3.10 | % | 4.12 | % | 9.01 | % | 8.56 | % | |||||||||||||||||||

Russell 2000® Growth Index | (26.36) | % | 0.65 | % | 3.50 | % | 9.20 | % | 7.16 | % | |||||||||||||||||||

Global Equity Team

Our Global Equity team currently manages four investment strategies: Global Equity, Non-U.S. Growth, Non-U.S. Small-Mid Growth and China Post-Venture.

Mark L. Yockey serves as portfolio manager of the Global Equity and Non-U.S. Growth strategies. Charles-Henri Hamker and Andrew J. Euretig are also portfolio managers of the Global Equity strategy and associate portfolio managers of the Non-U.S. Growth strategy. Rezo Kanovich serves as the sole portfolio manager of the Non-U.S. Small-Mid Growth strategy. Tiffany Hsiao serves as portfolio manager and Yuanyuan Ji serves as associate portfolio manager of the China Post-Venture strategy.

3

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Global Equity (April 1, 2010) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (19.79) | % | 3.60 | % | 7.69 | % | 10.41 | % | 10.97 | % | |||||||||||||||||||

MSCI ACWI® Index | (18.36) | % | 4.00 | % | 5.22 | % | 7.97 | % | 7.55 | % | |||||||||||||||||||

| Non-U.S. Growth (January 1, 1996) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (18.44) | % | (0.84) | % | 2.83 | % | 5.66 | % | 9.07 | % | |||||||||||||||||||

MSCI EAFE® Index | (14.45) | % | 0.87 | % | 1.54 | % | 4.67 | % | 4.45 | % | |||||||||||||||||||

| Non-U.S. Small-Mid Growth (January 1, 2019) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (23.02) | % | 3.10 | % | — | % | — | % | 10.96 | % | |||||||||||||||||||

| MSCI All Country World Index Ex USA Small Mid Cap (Net) | (19.49) | % | (0.22) | % | — | % | — | % | 5.00 | % | |||||||||||||||||||

| China Post-Venture (April 1, 2021) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (27.30) | % | — | % | — | % | — | % | (21.02) | % | |||||||||||||||||||

| MSCI China SMID Cap Index | (22.17) | % | — | % | — | % | — | % | (20.70) | % | |||||||||||||||||||

U.S. Value Team

Our U.S. Value team manages three investment strategies: Value Equity, U.S. Mid-Cap Value and Value Income. Thomas A. Reynolds, Daniel L. Kane and Craig Inman are the portfolio managers for the strategies.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Value Equity (July 1, 2005) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (8.21) | % | 8.18 | % | 7.49 | % | 10.41 | % | 8.56 | % | |||||||||||||||||||

Russell 1000® Index | (19.13) | % | 7.34 | % | 9.13 | % | 12.37 | % | 9.07 | % | |||||||||||||||||||

Russell 1000® Value Index | (7.54) | % | 5.95 | % | 6.66 | % | 10.29 | % | 7.45 | % | |||||||||||||||||||

| U.S. Mid-Cap Value (April 1, 1999) | |||||||||||||||||||||||||||||

Average Annual Gross Returns | (12.11) | % | 6.27 | % | 5.55 | % | 9.03 | % | 11.79 | % | |||||||||||||||||||

Russell Midcap® Index | (17.32) | % | 5.87 | % | 7.10 | % | 10.95 | % | 9.09 | % | |||||||||||||||||||

Russell Midcap® Value Index | (12.03) | % | 5.82 | % | 5.72 | % | 10.10 | % | 9.24 | % | |||||||||||||||||||

Value Income (March 1, 2022) 1 | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | — | % | — | % | — | % | — | % | (7.74) | % | |||||||||||||||||||

| S&P 500 Market Index | — | % | — | % | — | % | — | % | (10.98) | % | |||||||||||||||||||

1 Periods less than one year are not annualized. | |||||||||||||||||||||||||||||

4

International Value Team

Our International Value team, led by N. David Samra manages two investment strategies: International Value and International Explorer (formerly known as International Small Cap Value). N. David Samra serves as lead portfolio manager of the International Value strategy and managing director of the International Explorer strategy. Ian P. McGonigle serves as co-portfolio manager of the International Value strategy. Beini Zhou and Anand Vasagiri serve as co-portfolio managers of the International Explorer strategy.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| International Value (July 1, 2002) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (6.12) | % | 6.76 | % | 5.45 | % | 8.74 | % | 11.13 | % | |||||||||||||||||||

MSCI EAFE® Index | (14.45) | % | 0.87 | % | 1.54 | % | 4.67 | % | 5.45 | % | |||||||||||||||||||

| International Explorer (October 1, 2020) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (13.21) | % | — | % | — | % | — | % | 12.65 | % | |||||||||||||||||||

| MSCI All Country World Index Ex USA Small Cap (Net) | (19.97) | % | — | % | — | % | — | % | 4.53 | % | |||||||||||||||||||

Global Value Team

Our Global Value team, led by Daniel J. O’Keefe manages two investment strategies. Mr. O’Keefe serves as lead portfolio manager and Michael J. McKinnon serves as portfolio manager of the team’s Global Value and Select Equity strategies.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Global Value (July 1, 2007) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (12.69) | % | 3.22 | % | 3.95 | % | 8.80 | % | 7.61 | % | |||||||||||||||||||

MSCI ACWI® Index | (18.36) | % | 4.00 | % | 5.22 | % | 7.97 | % | 4.79 | % | |||||||||||||||||||

| Select Equity (March 1, 2020) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (15.92) | % | — | % | — | % | — | % | 6.78 | % | |||||||||||||||||||

S&P 500 Index | (18.11) | % | — | % | — | % | — | % | 11.45 | % | |||||||||||||||||||

Sustainable Emerging Markets Team

Our Sustainable Emerging Markets team manages one investment strategy. Maria Negrete-Gruson is the portfolio manager of the Sustainable Emerging Markets strategy.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Sustainable Emerging Markets (July 1, 2006) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (27.21) | % | (3.69) | % | (1.33) | % | 2.67 | % | 4.33 | % | |||||||||||||||||||

MSCI Emerging Markets Index | (20.09) | % | (2.69) | % | (1.40) | % | 1.44 | % | 3.94 | % | |||||||||||||||||||

5

Credit Team

Our Credit team manages three investment strategies: High Income, Credit Opportunities and Floating Rate. Bryan C. Krug serves as portfolio manager of the High Income and Credit Opportunities strategies and lead portfolio manager of the Floating Rate strategy. Seth B. Yeager also serves as portfolio manager of the Floating Rate strategy.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| High Income (April 1, 2014) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (9.15) | % | 2.62 | % | 4.31 | % | — | % | 5.83 | % | |||||||||||||||||||

| ICE BofA U.S. High Yield Master II Total Return Index | (11.22) | % | (0.23) | % | 2.12 | % | — | % | 3.32 | % | |||||||||||||||||||

| Credit Opportunities (July 1, 2017) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (3.64) | % | 12.17 | % | 10.48 | % | — | % | 10.92 | % | |||||||||||||||||||

| ICE BofA U.S. High Yield Master II Total Return Index | 1.21 | % | 0.82 | % | 1.42 | % | — | % | 1.41 | % | |||||||||||||||||||

| Floating Rate (January 1, 2022) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (0.80) | % | — | % | — | % | — | % | (0.80) | % | |||||||||||||||||||

| Credit Suisse Leveraged Loan Total Return Index | (1.06) | % | — | % | — | % | — | % | (1.06) | % | |||||||||||||||||||

Developing World Team

Our Developing World team manages one investment strategy. Lewis S. Kaufman is the portfolio manager of the Developing World strategy.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Developing World (July 1, 2015) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (40.56) | % | (0.15) | % | 4.06 | % | — | % | 7.04 | % | |||||||||||||||||||

| MSCI Emerging Markets Index | (20.09) | % | (2.69) | % | (1.40) | % | — | % | 2.18 | % | |||||||||||||||||||

Antero Peak Group

Antero Peak Group manages two investment strategies: Antero Peak and Antero Peak Hedge. Christopher P. Smith is the portfolio manager of both strategies.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Antero Peak (May 1, 2017) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (24.90) | % | 7.13 | % | 12.96 | % | — | % | 16.58 | % | |||||||||||||||||||

| S&P 500 Index | (18.11) | % | 7.65 | % | 9.42 | % | — | % | 10.74 | % | |||||||||||||||||||

| Antero Peak Hedge (November 1, 2017) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (22.96) | % | 4.24 | % | 9.92 | % | — | % | 10.27 | % | |||||||||||||||||||

| S&P 500 Index | (18.11) | % | 7.65 | % | 9.42 | % | — | % | 9.98 | % | |||||||||||||||||||

6

EMsights Capital Group

EMsights Capital Group manages three investment strategies: Emerging Markets Debt Opportunities, Global Unconstrained and Emerging Markets Local Opportunities. Michael A. Cirami and Sarah C. Orvin serve as the portfolio managers of each strategy.

| As of December 31, 2022 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

Global Unconstrained (April 4, 2022)1 | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | — | % | — | % | — | % | — | % | 8.40 | % | |||||||||||||||||||

| ICE BofA 3-month Treasury Bill Index | — | % | — | % | — | % | — | % | 1.42 | % | |||||||||||||||||||

Emerging Markets Debt Opportunities (May 1, 2022)1 | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | — | % | — | % | — | % | — | % | 8.28 | % | |||||||||||||||||||

| J.P. Morgan EMB Hard Currency/Local currency 50-50 | — | % | — | % | — | % | — | % | (0.99) | % | |||||||||||||||||||

Emerging Markets Local Opportunities (August 1, 2022)1 | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | — | % | — | % | — | % | — | % | 3.72 | % | |||||||||||||||||||

| J.P. Morgan GBI-EM Global Diversified | — | % | — | % | — | % | — | % | 3.03 | % | |||||||||||||||||||

1 Periods less than one year are not annualized. | |||||||||||||||||||||||||||||

Distribution, Investment Products and Client Relationships

The goal of our marketing, distribution and client service efforts is to grow and maintain a client base that is diversified by investment strategy, client type, distribution channel and geographic region. We focus our distribution and marketing efforts on sophisticated investors and asset allocators, including institutions and intermediaries that operate with institutional-like, centralized decision-making processes and longer-term investment horizons. We have designed our distribution strategies and structured our distribution teams to use knowledgeable, seasoned marketing and client service professionals in a way intended to limit the time our investment professionals spend on marketing and client service activities. We believe that minimizing other demands allows our portfolio managers and other investment professionals to focus their energies and attention on the investment decision-making process, which we believe enhances the opportunity to achieve superior investment returns. Our distribution efforts are centrally managed by our Head of Global Distribution, who oversees and coordinates the efforts of our marketing and client service professionals.

Institutional Channel

Our institutional distribution channel includes institutional clients, such as U.S.-registered mutual funds, non-U.S. funds and collective investment trusts we sub-advise; state and local governments; employee benefit plans including Taft-Hartley plans; foundations; and endowments. Our institutional channel also includes assets under management sourced from defined contribution plans. We offer our investment products to institutional clients directly and by marketing our services to the investment consultants and advisors that advise them. As of December 31, 2022, approximately 37% of our assets under management were attributed to clients represented by investment consultants.

As of December 31, 2022, 65% of our assets under management were sourced through our institutional channel.

Intermediary Channel

We maintain relationships with a number of major brokerage firms and larger private banks and trust companies at which the process for identifying which funds to offer has been centralized to a relatively limited number of key decision-makers that exhibit institutional-like decision-making behavior. We also maintain relationships with a number of financial advisory firms and broker-dealer advisors that offer our investment products to their clients. These advisors range from relatively small firms to large organizations.

As of December 31, 2022, approximately 31% of our assets under management were sourced through our intermediary channel.

Retail Channel

We primarily access retail investors indirectly through mutual fund supermarkets through which investors have the ability to purchase and redeem fund shares. U.S. investors can also invest directly in Artisan Funds. Our subsidiary, Artisan Partners Distributors LLC, a registered broker-dealer, distributes shares of Artisan Funds. Publicity and ratings and rankings from Morningstar, Lipper and others are essential to building the Artisan Partners brand, which is important for attracting retail investors. As a result, we publicize the ratings and rankings received by Artisan Funds and work to ensure that potential retail investors have appropriate information to evaluate a potential investment in Artisan Funds. We do not generally use direct marketing campaigns as we believe that their cost outweighs their potential benefits.

7

As of December 31, 2022, approximately 4% of our assets under management were sourced from investors we categorize as retail investors.

Access Through a Range of Investment Vehicles

Our clients access our investment strategies through a range of investment vehicles, including separate accounts and pooled vehicles. As of December 31, 2022, Artisan Funds and Artisan Global Funds accounted for approximately 48% of our total assets under management, and approximately 52% of our assets under management were managed in separate accounts and other pooled vehicles.

Separate Accounts and Other

We manage traditional separate accounts within most of our investment strategies. As of December 31, 2022, we managed 226 traditional separate accounts spanning 133 client relationships with our largest separate account relationship representing approximately 10% of our assets under management. These separate account clients include both institutional and intermediary channel relationships, such as pension and profit sharing plans, corporations, trusts, endowments, foundations, charitable organizations, high net worth individuals, governmental entities, insurance companies, commingled investment vehicles, investment advisers and other financial institutions, trustees of collective investment trusts and investment companies and similar pooled investment vehicles. The fees we charge on separate accounts vary by client, investment strategy and the size of the account. Fees are accrued monthly, but generally are paid quarterly in arrears.

A number of our investment strategies are accessible to certain types of employee benefit plans through Artisan-branded collective investment trusts, or CITs. We act as investment adviser to the CITs and earn a management fee for providing this service. As of December 31, 2022, CITs represented approximately 5% of our assets under management.

Certain of our investment strategies are primarily offered through Artisan-sponsored unregistered pooled investment vehicles, referred to as Artisan Private Funds. For serving as investment adviser to Artisan Private Funds, we earn a management fee and, for certain funds, are entitled to receive either an allocation of profits or a performance-based fee. As of December 31, 2022, Artisan Private Funds comprised approximately 1% of our assets under management.

In our reporting materials, unless otherwise stated, our “separate accounts and other” AUM includes assets we manage in traditional separate accounts, Artisan-branded CITs and Artisan Private Funds, as well as assets under advisement representing less than 1% of our assets under management, related to clients for whom we provide investment models but do not have discretionary investment authority.

Artisan Funds and Artisan Global Funds

U.S. investors that do not meet our minimum account size for a separate account, or who otherwise prefer to invest through a mutual fund, can invest in our strategies through Artisan Funds. We serve as the investment adviser to each series of Artisan Funds, SEC-registered mutual funds that offer no-load, no 12b-1 share classes designed to meet the needs of a range of investors. Each series of Artisan Funds corresponds to an investment strategy we offer to clients. We earn management fees, which are based on the average daily net assets of each Artisan Fund and are paid monthly, for serving as investment adviser to these funds. As of December 31, 2022, Artisan Funds represented approximately 45% of our assets under management.

We also serve as investment manager of Artisan Global Funds, a family of Ireland-based UCITS funds. Artisan Global Funds provides non-U.S. investors with access to a number of our investment strategies in a pooled vehicle structure. We earn investment management fees, which are based on the average daily net assets of each sub-fund and are generally paid monthly, for serving as investment adviser to these funds. As of December 31, 2022, Artisan Global Funds represented approximately 3% of our assets under management.

Regulatory Environment and Compliance

Our business is subject to extensive regulation in the United States at the federal level and, to a lesser extent, the state level, as well as by self-regulatory organizations and regulators located outside the United States. Under these laws and regulations, agencies that regulate investment advisers, investment funds and other related entities have broad administrative powers, including the power to limit, restrict or prohibit the regulated entity from conducting business in the event that it fails to comply with such laws and regulations. Breaches of these laws and regulations could result in regulatory enforcement actions, civil liability, criminal liability and/or the imposition of sanctions, including monetary damages, injunctions, disgorgements, fines, censures, and the revocation, cancellation, suspension or restriction of licenses, registration status or approvals held by us or our employees in a jurisdiction or market. In addition, a regulatory proceeding, regardless of whether it results in a sanction, can require substantial expenditures and can have an adverse effect on our reputation or business.

The domestic, international and extra-territorial laws and regulations that apply to our business relate to a broad range of subjects, including securities, compliance, corporate governance, financial reporting and disclosure, tax, privacy and data protection, sustainability, information security, anti-bribery and anti-corruption, anti-money laundering and anti-terrorist financing. These laws and regulations are complex and continue to change and evolve over time. As a result, there is a level of uncertainty associated with the regulatory environments in which we operate. Accordingly, the discussion below is general in nature, does not purport to be complete and is current only as of the date of this report.

8

U.S. Regulation

As a publicly traded company, we are subject to U.S. federal securities laws, state securities and corporate laws, and the rules and regulations of U.S. regulatory and self-regulatory organizations. In particular, we are subject to the Securities Act of 1933, the Securities Exchange Act of 1934 (the “Exchange Act”), the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the Sarbanes-Oxley Act of 2002 and, because we are listed on the New York Stock Exchange, the NYSE listing rules.

Artisan Partners Limited Partnership and Artisan Partners UK LLP are registered with the SEC as investment advisers under the Investment Advisers Act of 1940 (the “Advisers Act”), and Artisan Funds and several of the investment companies we sub-advise are registered under the Investment Company Act of 1940 (the “1940 Act”). The Advisers Act and the 1940 Act, together with other applicable securities laws and the SEC’s regulations and interpretations thereunder, impose substantive and material restrictions and requirements on the operations of investment advisers and mutual funds. The SEC is authorized to institute proceedings and impose sanctions for violations, ranging from fines and censures to, in the case of investment advisers, the termination of an adviser’s registration.

Artisan Partners Limited Partnership is registered with the Commodity Futures Trading Commission (“CFTC”) as a commodity pool operator, and is a member of the National Futures Association (“NFA”), with respect to its management of certain Artisan Funds. The CFTC and NFA each administer a comparable regulatory system covering futures, swaps and other derivative instruments. As the commodity pool operator of these Funds, Artisan Partners claims relief under the Commodity Exchange Act from certain reporting and recordkeeping requirements. Artisan Partners Distributors LLC, our SEC-registered limited purpose broker-dealer subsidiary, is subject to the Exchange Act, the SEC’s rules promulgated thereunder and the rules and regulations of the Financial Industry Regulatory Authority (“FINRA”), which generally relate to sales practices, registration of personnel, compliance and supervision, and compensation and disclosure. FINRA has the authority to conduct periodic examinations of member broker-dealers, and may initiate administrative proceedings. Artisan Partners Distributors LLC is also subject to the SEC’s Uniform Net Capital Rule and the National Securities Clearing Corporation’s excess net capital requirement, which require that at least a minimum part of a registered broker-dealer’s assets be kept in relatively liquid form.

Artisan Partners Limited Partnership is a fiduciary under the Employee Retirement Income Security Act of 1974, as amended, (“ERISA”) with respect to assets that we manage for certain benefit plan clients. ERISA imposes duties on persons who are ERISA fiduciaries, and prohibits certain transactions between related parties to a retirement plan. The U.S. Department of Labor administers ERISA and regulates plan fiduciaries, including investment advisers who service retirement plan clients.

The legislative and regulatory environment in the U.S. is subject to continual change. Political and electoral changes and developments have in the past introduced, and may in the future introduce, additional uncertainty. New legal or regulatory requirements often add further complexity to our business and operations, and addressing such new requirements may require substantial expenditures of time and capital. Certain regulatory reforms in the U.S. that have impacted, or may in the future impact, our business include the following items:

•The SEC has recently proposed and/or adopted a number of new rules impacting registered investment advisers (e.g. private fund advisor rules, ESG disclosure rules, cybersecurity risk management and disclosure rules, beneficial ownership rules, service provider oversight requirements, amendments to Form PF and amended advertising rule) and registered investment companies (e.g. ESG disclosure rules, amendments to the names rule, liquidity risk management, reporting modernization, valuation). In addition, the SEC has proposed and/or adopted a number of rules impacting public companies (e.g. new disclosure requirements on topics such as climate change, human capital management, cybersecurity risk governance, and executive compensation). These rules impact us and the mutual funds we manage to varying degrees.

•In recent years there has been an increased focus on the protection of customer privacy and data, and the need to secure sensitive information. We are subject to the California Consumer Privacy Act, which took effect in January 2020, and provides for enhanced consumer protections for California residents. Since then, California has also adopted the California Privacy Rights Act and several additional states have proposed and/or adopted data privacy laws with which we are or may be required to comply.

Non-U.S. Regulation

In addition to the extensive regulation we are subject to in the United States, a number of our subsidiaries and certain of our non-U.S. operations are subject to regulation in non-U.S. jurisdictions. Some laws in non-U.S. jurisdictions are also extra-territorial and may apply to our business.

Artisan Partners UK LLP is authorized and regulated by the U.K. Financial Conduct Authority, which is responsible for the conduct of business and supervision of financial firms in the United Kingdom. The FCA imposes a comprehensive system of regulation that is primarily principles-based (compared to the primarily rules-based U.S. regulatory system).

Artisan Partners Europe is authorized and regulated by the Central Bank of Ireland, which regulates our Irish business activities, including our management of Artisan Global Funds, a family of Ireland-domiciled UCITS funds. Artisan Global Funds are registered for sale in many countries around the world, both in the EU and beyond, and thus are also subject to the laws of, and supervision by, the governmental authorities of those countries.

9

Artisan Partners Hong Kong Limited, our Hong Kong subsidiary, is licensed and regulated by the Hong Kong Securities and Futures Commission (the “SFC”). Artisan Partners Hong Kong Limited and its employees conducting regulated activities under the Securities and Futures Ordinance are subject to the rules, codes and guidelines issued by the SFC from time to time.

We have historically operated in Australia on the basis of a “sufficient equivalence relief” exemption from local licensing with the Australian Securities and Investments Commission. This relief is expiring for foreign financial service providers like us and, as a result, Artisan Partners Limited Partnership or one of its affiliates may need to apply for and obtain a securities license or a new exemption by April 2024.

Certain Artisan Private Funds are regulated as mutual funds under the Mutual Funds Law (as amended) of the Cayman Islands, and the Cayman Islands Monetary Authority has supervisory and enforcement powers to ensure the funds’ compliance with the Mutual Funds Law.

Our business is also subject to the rules and regulations of the countries in which we conduct distribution or investment management activities. We have relationships with clients located outside of the United States, which may be subject to laws and regulations of the jurisdictions in which the client is domiciled. In addition, 47% of our assets under management were invested in securities denominated in currencies other than the U.S. dollar as of December 31, 2022. Our investments in these non-U.S. securities may subject us to certain laws and regulations of the jurisdictions in which the issuer resides or is traded. We may also be subject to U.S. laws and regulations with respect to our distribution or investment management activities in non-U.S. markets, including in jurisdictions that may be considered higher risk.

Regulatory reforms in jurisdictions in which we currently operate or invest and expansion of our business into new international jurisdictions, further complicate our compliance efforts. Addressing these legal and regulatory matters may require substantial time and expense. Certain non-U.S. regulatory reforms or guidance regarding such regulations that have impacted, or may in the future impact, our business include the following items:

•Under the Sustainability-Related Finance Disclosure Regulation (“SFDR”) and the EU Taxonomy Regulation, financial services companies operating in the European Union are required to disclose information on the impact of environmental, social and governance (ESG) effects on their portfolios. Asset managers are required to categorize their products and show their own processes of ESG integration and the extent to which ESG risks are expected to affect the returns on products sold. In addition, asset managers are required to annually report certain detailed information depending on the categorization of the product.

•The EU’s Markets in Financial Instruments Directive II regulates the use of soft dollars to pay for research and other soft dollar services. MiFID II’s soft dollar rules do not directly apply to our business because we currently conduct our investment management activities in the United States. However, in response to MiFID II and the industry-wide changes prompted by it, we have in the past experienced requests from clients to bear research expenses that are currently paid for using soft dollars. In response to such requests or as a result of changes in our operations, we may eventually bear a significant portion or all of the costs of research that are currently paid for using soft dollars, which would increase our operating expenses materially.

We may become subject to additional regulatory demands in the future to the extent we expand our business in existing and new jurisdictions. See “Risk Factors—Risks Related to our Industry—We are subject to extensive, complex and sometimes overlapping rules, regulations and legal interpretations.” and “Risk Factors—Risks Related to our Industry—The regulatory environment in which we operate is subject to continual change, and regulatory developments may adversely affect our business.”

Competition

The investment management industry is highly competitive. In order to be successful and grow our business, we must be able to compete effectively for assets under management. We compete to attract clients and investors principally on the basis of:

•the performance of our investment strategies

•the continuity of our investment and distribution professionals

•the quality of the service we provide to our clients

•the range of investment strategies and vehicles we offer

•our brand recognition and reputation within the investing community

•the fees we charge for the investment management services we provide

We compete in all aspects of our business with a large number of investment management firms, commercial banks, broker-dealers, insurance companies and other financial institutions. For additional information concerning the competitive risks that we face, see “Risks Factors—Risks Related to Our Industry—The investment management industry is intensely competitive.”

10

Human Capital Resources

Since Artisan Partners was founded in 1994, our success as an investment management firm has been predicated on having talented associates throughout the organization in every role, at every level. We understand that attracting, developing and retaining talented professionals is an essential component of our business strategy. As a result, we are committed to providing an environment that is attractive to our current and prospective associates and that allows our talented associates to thrive throughout the course of their careers at Artisan.

As of December 31, 2022, we employed 549 associates. Approximately 29% of our associates work within our investment teams, 25% within our distribution teams and 46% within our business management and operations teams. Approximately 94% of our associates operate from our U.S. offices and 6% operate from our offices outside of the U.S. As of December 31, 2022, 43% of our U.S. associates were female and 22% of our U.S. associates self-identified as ethnically diverse.

We invest significant energy in the recruitment of our associates as they are critical to ensuring the long-term success of our firm. We strive to recruit and hire outstanding associates who thrive in broad roles and want the freedom to grow their talents and careers. We are committed to seeking professionals from different backgrounds, experiences and locations to foster creative thinking and differentiated perspectives that remain a pillar of the firm’s culture. We have built relationships with a variety of recruitment partners and community organizations to broaden our candidate pools and increase our access to diverse talent.

We actively support associate engagement and development, both formally and informally, and encourage advancement from within the firm. Our tuition reimbursement program is available to associates who are pursuing applicable undergraduate and graduate degrees or certifications or licenses relevant to the business. Our diversity, equity and inclusion committee champions our DEI initiatives by bringing together a group of individuals with broad representation across the firm, as well as diverse social, regional and cultural identities. We also actively support a number of associate-led groups including the Pride Alliance, Multicultural Exchange, diffAbilities and the Women’s Networking Initiative. These groups create supportive and collaborative networks, encourage engagement and a sense of belonging, and enhance professional and personal growth. Our support of these and other associate-led programs are part of our ongoing commitment to providing an environment that allows our talented associates to thrive.

We believe in order to attract and retain talent, it is critical that we continue to foster an engaging environment and provide attractive compensation and benefits programs. We regularly review compensation paid to associates to ensure it is competitive, equitable and fair for the role, experience, location and individual contribution. We provide equity or equity-linked incentives to all of our associates in order to align their economic interests with those of our clients and stockholders. We encourage our associates to save for retirement. In the U.S., we match 100% of associate 401(k) contributions dollar for dollar (fully vested), up to the IRS limit. We also maintain competitive retirement programs or benefits for all non-U.S. associates. In addition, we offer a comprehensive benefits program that is available to all associates regardless of title, role, or responsibility.

Sustainability

Artisan Partners' purpose is to generate and compound wealth over the long-term for our clients. The wealth we generate improves retirement outcomes, pays for education, funds charitable purposes and in general improves people's lives. In addition to generating successful investment outcomes for our clients, we strive to promote success across a diverse group of associates and generate sustainable financial outcomes for our shareholders.

To achieve our purpose, we must continue to thoughtfully grow our business over the long term while preserving a consistent environment in which our talented investment professionals and associates can thrive. Maintaining our talent-driven business model and investment-focused culture is critical to providing a stable environment for our associates, generating sustainable, long-term investment outcomes for clients, and creating long-term successful financial outcomes for shareholders.

To us, sustainability means the following:

•Building relationships with the right clients, on the right terms and with the right long-term investment horizons. We foster client relationships by prioritizing investment returns. Prioritizing clients’ investment returns may, at times, require us to limit client cash flows and overall assets managed in a strategy—a practice we refer to as capacity management.

•Using a deliberate process to bring on new investment talent, launch new strategies and build sustainable franchises. We are patient in developing our talent, teams and strategies. We are comfortable with evolving—and sometimes even disrupting—our firm to increase the probability of long-term successful investment outcomes through market cycles.

•Compelling work in a tailored environment, with long-term opportunities for associates across our firm. Our culture promotes associates’ success—ideally over their entire careers—with economic alignment in the form of variable compensation and long-duration incentive awards.

•Growing our business value while maintaining financial discipline and continuing to generate and distribute significant cash to our shareholders. By taking care of our people and fulfilling our fiduciary duty to our clients, we create a waterfall effect that helps generate sustainable financial outcomes for our shareholders over the long term.

11

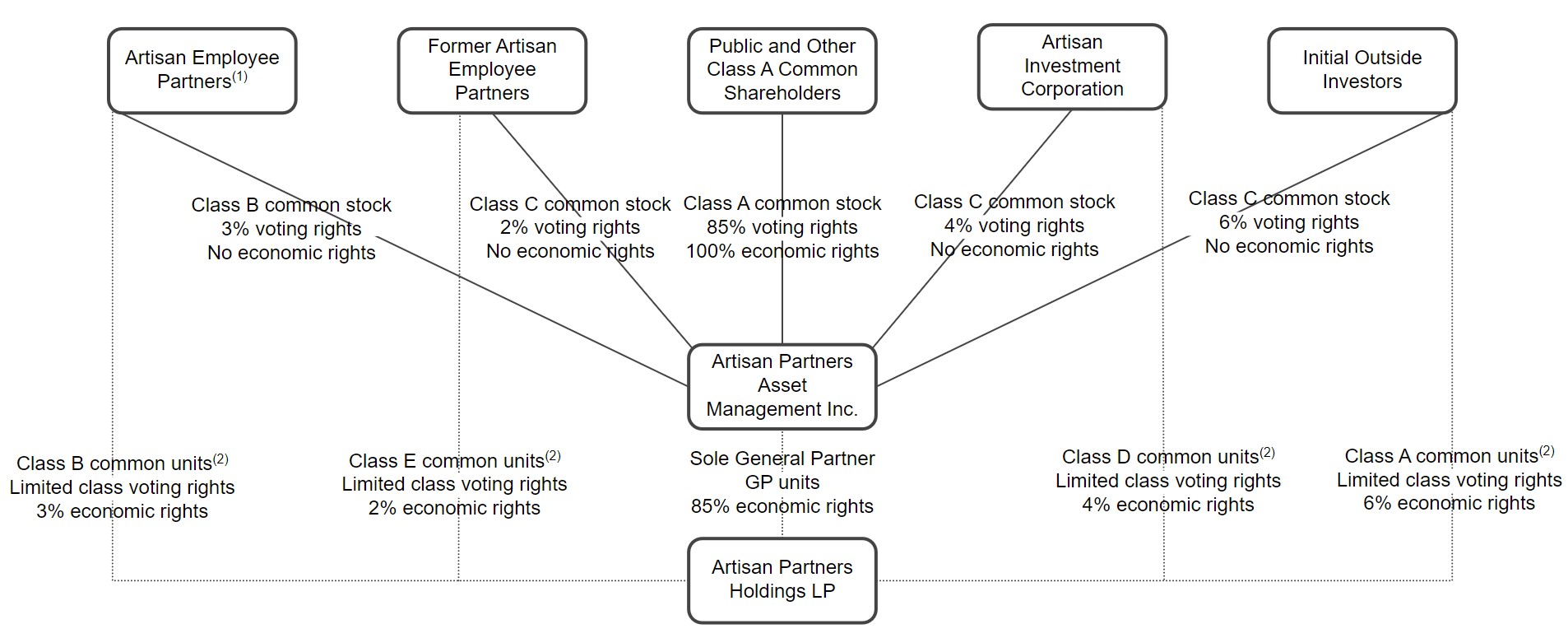

Our Structure

Holding Company Structure

We are a holding company and our assets principally consist of our ownership of partnership units of Artisan Partners Holdings, deferred tax assets and cash. As the sole general partner of Artisan Partners Holdings, we operate and control all of its business and affairs, subject to certain voting rights of its limited partners. We conduct all of our business activities through operating subsidiaries of Artisan Partners Holdings. Net profits and net losses are allocated based on the ownership of partnership units of Artisan Partners Holdings. As of December 31, 2022, we owned approximately 85% of Artisan Partners Holdings, and the other 15% was owned by the limited partners of Artisan Partners Holdings.

Our holding company structure is predominantly a result of our IPO, which we completed in March 2013. In connection with the IPO, we and Artisan Partners Holdings completed a series of reorganization transactions, which we refer to as the IPO Reorganization, in order to reorganize our capital structures in preparation for the IPO. The IPO Reorganization included, among other changes, the following:

•Our appointment as the sole general partner of Artisan Partners Holdings.

•The modification of our capital structure into three classes of common stock and a series of convertible preferred stock. We issued shares of our Class B common stock and Class C common stock and convertible preferred stock to pre-IPO partners of Artisan Partners Holdings. Each share of Class B common stock corresponds to a Class B common unit of Artisan Partners Holdings. Each share of Class C common stock corresponds to either a Class A, Class D or Class E common unit of Artisan Partners Holdings. Subject to certain restrictions, each common unit of Artisan Partners Holdings (together with the corresponding share of Class B or Class C common stock) is exchangeable for a share of our Class A common stock.

•A corporation (“H&F Corp”) merged with and into Artisan Partners Asset Management, which we refer to in this document as the H&F Corp Merger.

•We entered into two tax receivable agreements (“TRAs”), one with a private equity fund (the “Pre-H&F Corp Merger Shareholder”) and the other with each limited partner of Artisan Partners Holdings. Pursuant to the first TRA, APAM pays to the assignees of the Pre-H&F Corp Merger Shareholder a portion of certain tax benefits APAM realizes as a result of the H&F Corp Merger. Pursuant to the second TRA, APAM pays to current or former limited partners of Artisan Partners Holdings (or their assignees) a portion of certain tax benefits APAM realizes as a result of the purchase or exchange of their limited partnership units of Artisan Partners Holdings.

The diagram below depicts our organizational structure as of December 31, 2022:

(1) | Our employees to whom we have granted equity have entered into a stockholders agreement with respect to all shares of our common stock they have acquired from us and any shares they may acquire from us in the future, pursuant to which they granted an irrevocable voting proxy to a stockholders committee currently consisting of Eric R. Colson (Chief Executive Officer), Charles J. Daley, Jr. (Chief Financial Officer) and Gregory K. Ramirez (Executive Vice President). The stockholders committee, by vote of a majority of its members, will determine the vote of all of the shares subject to the stockholders agreement. In addition to owning all of the shares of our Class B common stock, our employee-partners, together with our other employees, owned unvested restricted shares of our Class A common stock representing approximately 8% of our outstanding Class A common stock as of December 31, 2022. | ||||

(2) | Each class of common units generally entitles its holders to the same economic and voting rights in Artisan Partners Holdings as each other class of common units, except that the Class E common units have no voting rights except as required by law. | ||||

12

Available Information