UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________

FORM 10-K

______________________

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2021

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ________ to ________

Commission File Number 001-37622

______________________

(Exact name of registrant as specified in its charter)

______________________

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||||||

Address Not Applicable1

(Address of principal executive offices, including zip code)

(415 ) 375-3176

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non‑accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b‑2 of the Exchange Act.

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, based on the closing price of a share of the registrant’s Class A common stock on June 30, 2021 as reported by the New York Stock Exchange on such date was approximately $95.2 billion. Shares of the registrant’s Class A common stock and Class B common stock held by each executive officer, director and holder of 5% or more of the outstanding Class A common stock and Class B common stock have been excluded in that such persons may be deemed to be affiliates. This calculation does not reflect a determination that certain persons are affiliates of the registrant for any other purpose.

As of February 18, 2022, the number of shares of the registrant’s Class A common stock outstanding was 518,361,474 and the number of shares of the registrant's Class B common stock outstanding was 61,696,578 .

1 As of 2021, we do not designate a headquarters location as we have adopted a distributed work model.

TABLE OF CONTENTS

| Page No | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, that involve substantial risks and uncertainties. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “may,” “will,” “appears,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential,” or “continue,” or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans, or intentions. Forward-looking statements contained in this Annual Report on Form 10-K include, but are not limited to, statements about our future financial performance, the impact of the COVID-19 pandemic and related public health measures on our business, customers, and employees, our expectations regarding transaction and loan losses, the adequacy of our allowance for loan losses on loans held for investment, or increased delinquencies, and the impact of inaccurate estimates or inadequate reserves, our potential exposure as a participant in the Paycheck Protection Program ("PPP"), our anticipated growth and growth strategies and our ability to effectively manage that growth, our ability to invest in and develop our products and services to operate with changing technology, the expected benefits of our products to our customers and the impact of our products on our business, and our expectations regarding Gross Payment Volume (GPV) and revenue, including our expectations regarding the Cash App and Square ecosystems, our expectations regarding product launches, the expected impact of our recent acquisitions, the integration of Afterpay with our business, our plans with respect to patents and other intellectual property, our expectations regarding litigation and regulatory matters and the adequacy of reserves for such matters, our expectations regarding share-based compensation, our expectations regarding the impacts of accounting guidance and the timing of our compliance therewith, our expectations regarding restricted cash, and the sufficiency of our cash and cash equivalents and cash generated from operations to meet our working capital and capital expenditure requirements.

We have based the forward-looking statements on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations, prospects, business strategy, and financial needs. The outcome of the events described in these forward-looking statements is subject to known and unknown risks, uncertainties, and other factors described in the section titled “Risk Factors” and elsewhere in this Annual Report on Form 10-K. We operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report on Form 10-K. We cannot assure you that the results, events, and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events, or circumstances could differ materially from those described in the forward-looking statements.

All forward-looking statements are based on information and estimates available to the Company at the time of this Annual Report on Form 10-K and are not guarantees of future performance. We undertake no obligation to update any forward-looking statements made in this Annual Report on Form 10-K to reflect events or circumstances after the date of this Annual Report on Form 10-K or to reflect new information or the occurrence of unanticipated events, except as required by law.

3

PART I

Item 1. BUSINESS

Our Business

We started Block with the Square ecosystem in February 2009 to enable businesses ("sellers") to accept card payments, an important capability that was previously inaccessible to many businesses. As our company grew, we recognized that sellers need a variety of solutions to thrive and saw how we could apply our strength in technology and innovation to help sellers. We have since expanded our Square ecosystem to provide more than 30 distinct products and services to sellers that help them manage and grow their business. Similarly, with Cash App, we have built an ecosystem of financial services to help individuals manage their money. Our purpose of economic empowerment drives the development of all our products and services. Effective June 30, 2020, we changed the way we reported our results from one operating and reportable segment to two. Our two reportable segments are Square, formerly referred to as Seller, and Cash App, reflecting our two primary ecosystems and the way management and our chief operating decision maker (“CODM”) review and assess the performance of our business.

On December 1, 2021, we changed our name from Square to Block. Block is the name for the company as a corporate entity. The Square name has become synonymous with our Seller business, and this move allowed the Seller business to own the Square brand it was built for. The change to Block acknowledges our growth. Since our start in 2009, we have added Cash App, TIDAL, and TBD as businesses, and the name change creates room for further growth. Block is an overarching ecosystem of many businesses united by their purpose of economic empowerment, and serves many people—individuals, artists, fans, developers, and sellers.

Square Ecosystem: Square offers a cohesive commerce ecosystem that helps our sellers start, run, and grow their businesses. We combine software, hardware, and financial services to create products and services that are cohesive, fast, self-serve, and elegant. These attributes differentiate Square in a fragmented industry that traditionally forces sellers to stitch together products and services from multiple vendors, and more often than not, rely on inefficient non-digital processes and tools. Our ability to add new sellers efficiently, help them grow their business, and cross-sell products and services has historically led to continued and sustained long-term growth. In the year ended December 31, 2021, we processed $152.8 billion of Square Gross Payment Volume ("GPV"), which was generated by more than 3 billion card payments from 526 million payment cards. At the end of 2021, our Square ecosystem had over 261 million buyer profiles and approximately 366 million items were listed on Square by sellers.

Cash App Ecosystem: Cash App provides an ecosystem of financial products and services to help individuals manage their money. Cash App’s goal is to redefine the world’s relationship with money by making it more relatable, instantly available, and universally accessible. While Cash App started with the single ability to send and receive money, it now provides an ecosystem of financial services that allows individuals to store, send, receive, spend, and invest their money.

TIDAL: In the second quarter of 2021, we completed the acquisition of a majority ownership interest in TIDAL, a global music and entertainment platform that expands our purpose of economic empowerment to artists. TIDAL offers an extensive catalog of more than 80 million songs and 350,000 high-quality videos. TIDAL focuses on putting both the artist experience and fan experience at the center of decisions, providing artists direct access to their audience and allowing fans deeper connections to their favorite artists through original, exclusive, and curated content and events. TIDAL has a global presence with listeners in more than 60 countries and relationships with more than 200 labels and distributors.

TBD: In the third quarter of 2021, we launched TBD with a mission to build an open developer platform to make it easier for individuals and businesses to access bitcoin and other blockchain technologies without having to go through an institution.

Spiral: In 2019, we launched Spiral, an independent team solely focused on contributing to bitcoin open source work.

Afterpay: On January 31, 2022, we completed the acquisition of Afterpay Limited ("Afterpay"). Afterpay is a global ‘buy now, pay later’ ("BNPL") platform that facilitates commerce between retail merchants and end-customers by allowing its retail merchant clients to offer their customers the ability to buy goods and services on a BNPL basis. Through the use of Afterpay’s BNPL products, end-customers can split their purchases across four installments, generally due in two-

4

week increments, without paying fees (if payments are made on time). Afterpay provides end-customers the ability to get desired items now but pay for them later while simultaneously helping merchants increase sales and order values. Afterpay pays its retail merchant customers the full order value upfront (less a percentage fee) and assumes the risk of non-payment from the end-customer. Apart from capped late payment fees, end-customers do not incur additional fees. Afterpay operates an online shop directory, which allows consumers to search by product category for stores that offer Afterpay as a payment option, and offers an Afterpay in-store card for in-person transactions at a merchant’s point of sale. We intend to integrate the Afterpay BNPL platform into the Cash App and Square ecosystems, strengthening the connection between these ecosystems, expanding access to more sellers and customers, and helping drive more commerce between our sellers and customers. Afterpay will be integrated into Square’s online and in-person checkout solutions, strengthening Square’s omnichannel platform. Customers will be able to manage their installments and repayments directly within Cash App, potentially driving increased engagement, while the commerce discovery from the Afterpay App will be integrated with Cash App to help drive lead generation for merchants and customer engagement.

Response to COVID-19

In 2020 and 2021, we made certain focused investments in each of our Square and Cash App ecosystems to help our customers adapt to COVID-19.

For our Square sellers, we provided resources with information and advice. We eliminated fees for our software products for the months of March and April 2020, as well as certain other months in 2020 and 2021 for markets outside the U.S., and introduced options for sellers to pause subscriptions temporarily based on their circumstances. We prioritized omnichannel product launches to help sellers transition to serving more of their customers online and through contactless commerce, including curbside pickup and delivery for Square Online and a website for customers to purchase eGift Cards from sellers. We also temporarily offered our sellers free marketing campaigns to update their buyers on recent changes and to promote their businesses. As a participant in the Paycheck Protection Program (PPP), we distributed loans to Square sellers. As of December 31, 2021, we had facilitated approximately $1.5 billion of PPP loans, excluding canceled loans, providing more than 150,000 loans to small businesses. As of December 31, 2021, approximately $725.9 million in the aggregate of PPP loans had been forgiven by the Small Business Administration, of which, $679.6 million was forgiven in 2021. We approved and funded the last remaining PPP applications on May 21, 2021 upon exhaustion of the funds in the program.

For our Cash App customers, we published educational materials to help them understand the Coronavirus Aid, Relief, and Economic Security Act ("CARES Act") stimulus programs. We expanded direct deposit access to many of our Cash App customers, allowing customers to direct deposit government funds into their Cash App accounts. Customers could spend their funds using Cash Card and we adapted certain Boost rewards to pandemic-relevant merchants and categories (e.g. grocery stores) to benefit our customers.

Our Customers

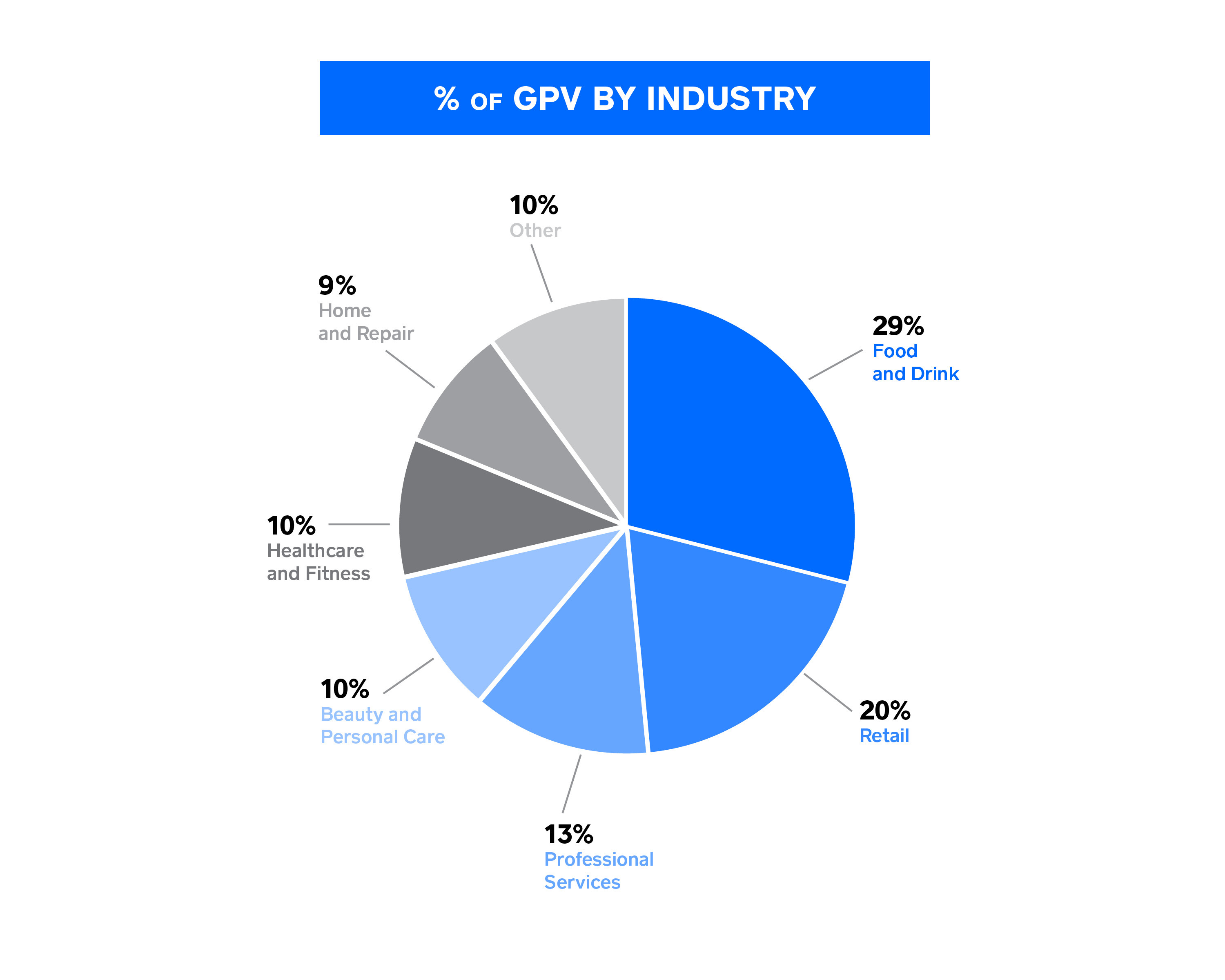

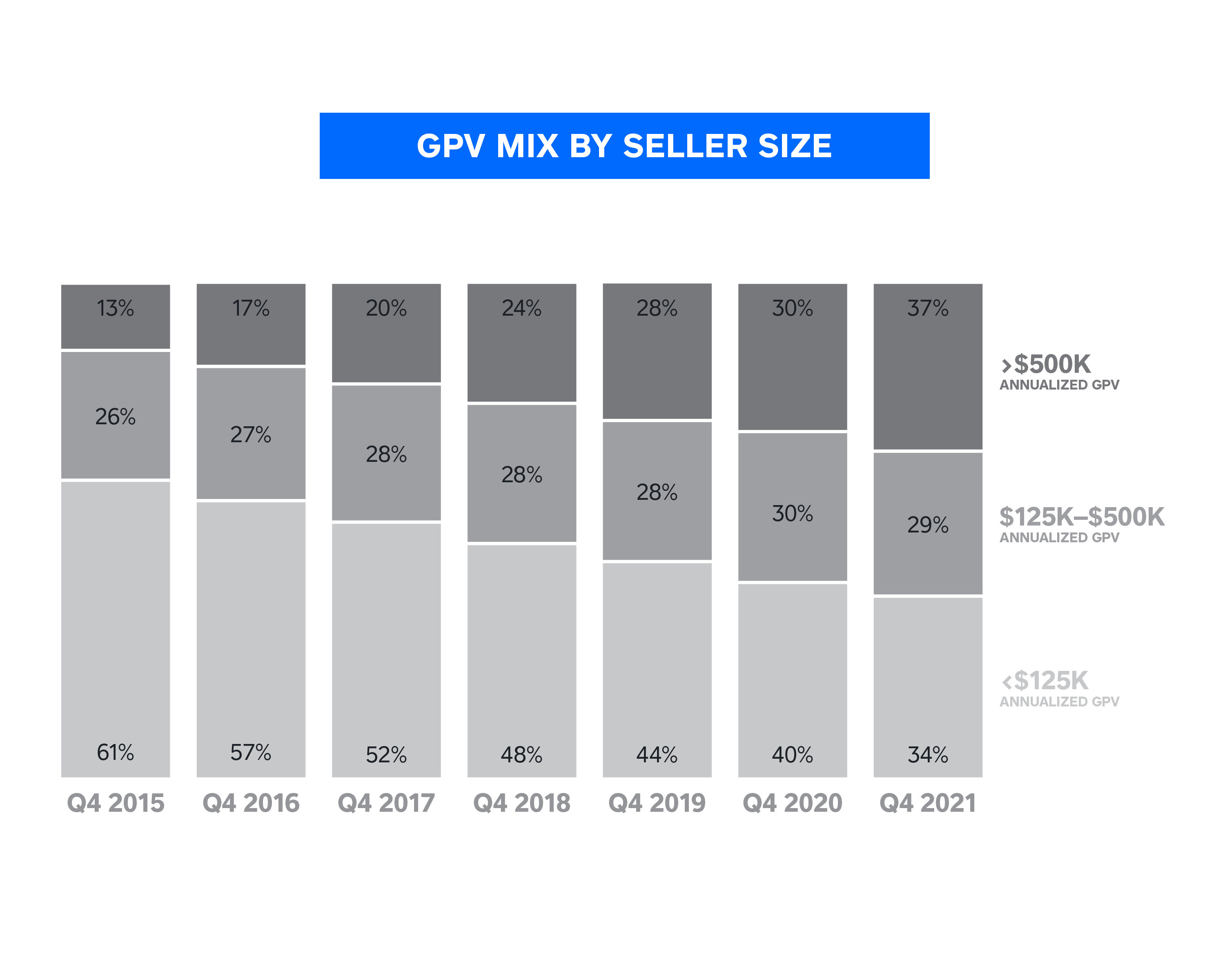

Our Square sellers: Square sellers represent a diverse range of industries (including services, food-related, and retail businesses) and sizes, ranging from sole proprietors to multi-national businesses. Square sellers span geographies, including the United States, Canada, Japan, Australia, the United Kingdom, Ireland, France, and Spain. We believe the diversity of our sellers underscores the accessibility and flexibility of our offerings. We are also increasingly serving mid-market sellers, which we define as sellers that generate more than $500,000 in annualized GPV. Our ability to service mid-market sellers is due to our ability to offer more flexible and complex solutions as well as a growing product suite. GPV from mid-market sellers represented 37% of Square GPV in the fourth quarter of 2021, up from 30% in the fourth quarter of 2020 and 28% in the fourth quarter of 2019. For the years ended December 31, 2021, 2020 and 2019, we had no customer who accounted for greater than 5% of our GPV or our total net revenue.

The charts below show the percentage mix of our Square GPV by seller industry and seller size, excluding Cash App for the year ended December 31, 2021:

5

6

Our Cash App Customers: As of December 2021, Cash App had more than 44 million monthly transacting actives across the United States and Europe which had at least one financial transaction using any Cash App product or service. In 2021, across the iOS App Store and Google Play, Cash App was the number one finance app and the number four app overall, based on downloads in the United States. Cash App has a diverse mix of customers. In the United States, Cash App had monthly transacting actives in each of the 50 states and nearly every county as of December 2021.

Our Products and Services

Square Ecosystem:

Our Square ecosystem consists of more than 30 distinct software, hardware, and financial services products. We monetize these products through a combination of transaction, subscription, and service fees.

Software

We offer a growing suite of cloud-based software solutions to help Square sellers more effectively operate and manage their businesses. Our software is designed to be self-serve and intuitive to make initial setup and new employee training fast and easy. Our products are integrated to create a seamless experience and enable a holistic view of sales, customers, employees, and locations. Sellers get frequent software updates and upgrades automatically. Square's software offerings include our Online, Point of Sale, Developer Platform, Customer Relationship Management, and Team Management products.

Square's point of sale products help sellers make sales and track sales, inventory, customers’ purchase histories, and tips. All point of sale products have a free software tier without a subscription fee, which we monetize only through payments transaction fees. Among Square's point of sale products, Square Appointments, Square for Retail, and Square for Restaurants also have premium tiers with additional functionality, which we monetize through subscription fees in addition to transaction fees on payments.

•Square Point of Sale is a general purpose point-of-sale software solution for businesses that need an easy to use, customizable point of sale solution that adapts to any business type and stage. It is available for both iOS and Android and is pre-installed on Square Register and Square Terminal hardware devices.

•Square Appointments is for appointment-based businesses that need a point-of-sale software solution with integrated booking capabilities. It can be used on iOS, Android, or via a web browser. Appointments includes a free online booking site so buyers can easily schedule appointments and select their preferred time, service, and staff member. It is also integrated with Square Assistant, an artificial intelligence enabled automated messaging tool that responds to buyers efficiently and professionally, saving sellers' time and helping prevent no-shows.

•Square for Retail is tailored for sellers in the retail industry and includes advanced inventory management, cost of goods sold reporting, purchase orders, vendor management, and barcode scanning.

•Square for Restaurants is tailored for both quick service and full-service restaurants. It includes table, order and course management, a kitchen display system, and revenue and cost reporting.

Square's online products make it easy to sell online and via social media. When used in conjunction with Square's point of sale products, sellers can offer omnichannel experiences for their customers such as buy online, pickup in store or curbside, and buy online, return in store. All online products have a free tier without a subscription fee, which we monetize only through transaction fees on payments. Square Online and Square Invoices also have premium tiers with additional functionality that is monetized via software fees in addition to transaction fees on payments.

•Square Online helps sellers across a range of verticals reach customers in more ways. It makes it easy to build a website and online store as well as sell on Instagram and Facebook. The online store is mobile responsive, delivering an app-like ordering experience on a buyer’s phone. With integrated support for QR code ordering, sellers can also streamline their in-store operations by posting the QR code and having their buyers order from their own phones. Fulfillment options include pickup, delivery managed by our sellers, and partner delivery platforms. Orders, items, inventory, and customer data stay in sync when selling both online and in-person.

7

•Square Online Checkout makes it easy to sell online without a website by allowing sellers to create a checkout link with only a name and price for their good or service.

•Square Invoices is a customizable digital invoicing solution with integrated and secure online payment acceptance. This eliminates the need to print and mail statements to customers and wait for checks to arrive. Sellers use Square Invoices for upcoming, recurring, or previously-delivered goods and services, such as catering orders, contractor services, lessons, and retail orders. Square Invoices also lets sellers send estimates and collect partial payments for goods and services.

•Square Virtual Terminal allows sellers to use a computer as a card terminal. Sellers can take a payment, set up recurring billing, record sales, and send digital receipts for payments, including those made by check and bank transfer.

Square's business and customer relationship management products give sellers digital tools to streamline their operations. These tools seamlessly integrate with other Square products eliminating the latent, time-consuming, and error prone processes typically used to copy and sync data between disparate systems. We monetize these products via software fees with the exception of Square Contracts, Feedback, and Dashboard which we do not directly monetize.

•Square Team Management makes it easy to schedule staff, view team performance and sales analytics in real time, and pay employees in minutes when used together with Square Payroll. It also enables limiting access to Square software features per employee or role. The Square Team App enables team members to clock in and out, view and adjust their schedules, see timecards, hours worked, and estimated pay from their mobile phone. Team members paid via Square Payroll can also view their pay stubs in the Square Team App.

•Square Contracts helps sellers protect themselves by creating custom and template-based digital contracts with e-signature support for uses such as service agreements and liability waivers. These contracts can be used on their own or easily added to Square Invoices or Square Appointments.

•Square Loyalty, Messages, Marketing, Gift Cards, and Feedback help sellers engage with their buyers in-store and online to grow their business. By linking customer data and feedback with point-of-sale and online commerce data, Square can offer sellers integrated omnichannel loyalty, marketing and feedback. Square's closed-loop system allows sellers to easily assess performance and return on investment.

•Square Dashboard provides sellers with real-time data and insights about orders, items, inventory, customers, employees, payments, marketing, and loyalty performance. It can be used via the web or the Dashboard iOS app. This reporting enables sellers to stay informed and make timely decisions about their business from anywhere.

Finally, Square offers a developer platform including APIs (application programming interfaces) and SDKs (software development kits) that enable external developers to integrate with the Square ecosystem.

•Payment APIs support in-person, online, and mobile payments. Square Reader SDK enables developers to seamlessly integrate Square hardware with a seller’s custom point of sale, allowing them to build unique checkout experiences such as self-ordering kiosks powered by Square’s managed payments service. With Square's online payments APIs, developers can integrate Square payments into a seller’s e-commerce website or online store. Square's In-App Payments SDK enables developers to build consumer mobile apps that use Square to process payments. These products are primarily monetized through transaction fees on payment volumes.

•Commerce APIs include more than 30 commerce APIs, through which developers can create and manage orders, subscriptions, product catalogs, inventory, customer profiles, employees, loyalty programs, gift cards and more in order to build applications that enrich and integrate with Square's ecosystem of products. In addition, these APIs enable developers to build integrations with their existing business systems such as accounting, CRM (customer relationship management), employee management, and ERP (enterprise resource planning) software.

Hardware

Square custom-designs hardware that can process all major card payment forms, including magnetic stripe, EMV chip, and NFC (contactless). Sellers are able to accept cards issued by Visa, MasterCard, American Express, Discover, JCB,

8

Interac Flash (in Canada), e-Money (in Japan), and eftpos (in Australia). Square hardware can be integrated with additional accessories such as cash drawers, receipt printers, scales, and barcode scanners to provide sellers with a comprehensive point-of-sale solution. Square's hardware portfolio includes the following:

•Magstripe reader enables swiped transactions of magnetic stripe cards by connecting with an iOS or Android smartphone or tablet via the headphone jack or lightning connector.

•Contactless and chip reader accepts EMV chip cards and NFC payments, enabling acceptance via Apple Pay, Google Pay, and other mobile wallets.

•Square Stand enables an iPad to be used as a payment terminal or full point of sale solution. It features an integrated magnetic stripe reader, provides power to a connected iPad, and can connect to the contactless and chip reader wirelessly or via USB.

•Square Register is an all-in-one offering that combines our hardware, point-of-sale software, and payments technology. The dedicated hardware consists of two screens: a seller display and a customer display with a built-in card reader that accepts tap, dip, and swipe payments.

•Square Terminal is a portable, all-in-one payments device and receipt printer to replace traditional keypad terminals. It accepts tap, dip, and swipe payments and has a battery that lasts all day, enabling payments anywhere in the store.

Financial Services

Square acts as both the merchant of record for the transaction as well as the payment service provider (PSP). As the merchant of record, Square is the party responsible for settling funds with the seller and helps manage transaction risk loss on behalf of the merchant. Square's position as the merchant of record helps Square better serve its sellers. For example, as the merchant of record, we can more efficiently onboard new sellers through our website, leveraging our risk assessment models, and we have insights into transaction-level data that we use to inform our sellers and launch new products. Square has negotiated terms and entered into contractual arrangements directly with the other service providers of transaction processing services, including the acquiring processors and card networks, and indirectly with the issuing banks. These contracts include negotiated terms, such as more favorable pricing, that are generally not available to sellers if they were to contract directly with these sub-service providers.

We offer a growing number of accessible financial services that make it easier for sellers to manage cash flow and get faster access to funds. Financial Services includes our Managed Payments, Business Banking, and Payroll products.

•Managed Payments includes next-day settlements, payment dispute management, data security, and PCI compliance. Sellers can onboard in minutes and, once onboarded, accept payments in person via swipe, dip, or tap of a card or online via a stored card on file or payment entry form. Sellers pay a transparent transaction fee for our managed payment offering.

•Risk Manager gives sellers insight into online payment fraud patterns and enables them to set custom rules and alerts to manage risk. Machine learning algorithms automatically identify fraud patterns and adapt to fit a seller's operations.

•Instant Transfer enables sellers to receive funds from their payments instantly or later that same day. Instant Transfer is an important tool for sellers that need faster access to their funds in order to better manage their cash flow or working capital.

•Square Savings is a high-yield business savings account, with no monthly fees or minimums, designed to make cash flow management easier for sellers. With Square Savings, sellers can easily and automatically put aside a portion of their sales into their savings account while also organizing their money within folders, streamlining the process of saving funds for specific goals and priorities, such as quarterly tax obligations.

9

•Square Checking provides sellers with a FDIC-insured account that gives them instant access to their sales and the ability to immediately use those funds via a debit card (Square Debit Card), withdrawn from an ATM, or transferred via ACH.

•Square Loans (formerly Square Capital) facilitates loans to qualified Square sellers through our subsidiary Square Financial Services (“SFS”), which is an industrial loan corporation (“ILC"). SFS began its operations in March 2021. Square Loans eliminates the lengthy (and often unsuccessful) loan application process. We are able to approve sellers for these loans while facilitating prudent risk management by using our unique data set of a seller’s Square transactions to help facilitate loan underwriting and collections. The terms are straightforward for sellers, and once approved, they get their funds quickly, often the next business day. Generally, for loans to Square sellers, loan repayment occurs automatically through a fixed percentage of every card transaction a seller takes. Loans are sized to be less than 20% of a seller's expected annual GPV and, by simply running their business, sellers historically have repaid their loan in less than nine months on average. We currently fund a majority of these loans from arrangements with institutional third-party investors who purchase these loans on a forward-flow basis. This funding allows us to mitigate our balance sheet and liquidity risk. Since its public launch in May 2014, Square Loans has facilitated more than 1.6 million loans and advances, representing more than $11.3 billion in principal amount loaned. This includes approximately $1.5 billion of Paycheck Protection Program (PPP) loans, excluding canceled loans, providing more than 150,000 loans to small businesses.

•Square Payroll allows sellers to pay wages and associated employee taxes, and offer employee benefits (e.g. 401(k) accounts). The Square ecosystem drives competitive differentiation for our Payroll product with the ability to use Payroll in conjunction with our point of sale products, Team Management, and Cash App.

Cash App Ecosystem:

With Cash App, we are building an ecosystem of financial products and services that helps individuals manage their money by making it more relatable, instantly available, and universally accessible. Cash App has a diverse set of customers across demographics and domestic regions. Cash App primarily serves customers in the United States with its breadth of products, and also provides certain services to customers in Europe, primarily with Cash App in the United Kingdom and with Verse in Spain.

Storing, Sending, and Receiving Funds

Customers can use Cash App to inflow funds in a variety of ways, including by receiving money from another Cash App customer through the app’s core peer-to-peer transfer service, by transferring money from a bank account, depositing mobile-checks, or by adding physical cash at participating retailers. We have enhanced the efficiency of peer-to-peer transfers by streamlining the onboarding process for new Cash App customers. Many Cash App accounts also have a routing number and a unique account number, which allows customers to deposit funds directly from their paychecks. These funds can then be sent to another customer through the app, spent anywhere that accepts cards or withdrawn from an ATM using the Cash Card, invested in stocks or ETFs, used to buy bitcoin, or transferred to a bank account (either instantly for a fee or for free in 1-3 days). Additionally, Cash App has made it easier for people to manage a business by enabling payments to their Cashtag, allowing higher weekly limits, and providing relevant tax reporting forms.

We are expanding Cash App’s ecosystem by reaching more customers globally. We offer cross-border payments between the United States and the United Kingdom, allowing customers to instantly transfer funds between these countries using real-time exchange rates with no fees.

Spending

Cash Card is a debit card that is linked directly to a customer’s Cash App balance. Customers can order a Cash Card for free and use their Cash Card anywhere that accepts cards to make purchases, drawing down from the funds stored in their Cash App balance. Square earns interchange fees when individuals make purchases with Cash Card. Customers can select new or promotional Cash Card designs for a fee.

Cash Card also offers customers discounts at certain businesses through the Cash Boost program. Cash Boost is a free and instant rewards program for Cash App customers, which offers a discount at a specific business (e.g. 10% off a purchase on DoorDash) or a discount at certain business types (e.g. grocery stores). Customers can select the Cash Boost they

10

want to apply to their Cash Card through the Cash App, and the discount is instantly applied to their Cash App balance when customers make eligible transactions. Some Cash Boosts are selected and funded by Cash App, while others are funded by our partners. Costs related to the Cash Boost rewards program that are funded by Cash App are recognized as reductions to revenue.

Investing

Customers can also use Cash App to invest their funds in U.S. listed stocks and exchange-traded funds ("ETFs") or buy and sell bitcoin.

Cash App makes investing more accessible by giving customers access to hundreds of listed stocks and ETFs, as well as the ability to buy and sell bitcoin. Stocks, ETFs, or bitcoin can be purchased using the funds in a customer’s Cash App balance or from a linked debit card and once the order is filled, all investments are viewable through the Investing tab on the Cash App home screen. We offer Cash App customers the ability to buy fractional amounts of a stock, ETF, or bitcoin starting at as little as $1, which expands access to investing to more people. For bitcoin buying and selling, we recognize revenue when customers purchase bitcoin and it is transferred to the customer's account.

Commerce

Cash App is focused on driving greater commerce between customers and merchants.

Launched in the third quarter of 2021, Cash App Pay is a simple, mobile-friendly way for Cash App customers to pay at merchants across online and in-person channels. As of December 2021, Cash App Pay is enabled for a subset of Square sellers that are using certain Square hardware and software products. With Cash App Pay, Cash App customers can pay at Square sellers by simply scanning a QR code or tapping a button on their mobile device at checkout.

Cash for Business allows business accounts to use Cash App to collect payments for their business by accepting peer-to-peer transactions for a fee.

Tax Preparation

In the fourth quarter of 2020, we acquired Credit Karma Tax, which added a tax filing product for individuals to Cash App's ecosystem. In the first quarter of 2021, we launched Cash App Taxes, which provides a seamless, mobile-first solution for individuals to file their taxes for free.

Sales and Marketing

Square Ecosystem

Square's seller ecosystem has a strong brand and continues to increase awareness of Square and our Square ecosystem of products among sellers by enhancing our services and fostering rapid adoption through brand affinity, direct marketing, public relations, direct sales, and partnerships. Our Net Promoter Score (NPS) has averaged nearly 63 over the past four quarters, which is approximately double the average score for banking providers. Our high NPS means Square sellers recommend our services to others, which we believe strengthens the Square brand and helps drive efficient customer acquisition.

Direct marketing, online and offline, has also been an effective customer acquisition channel. These tactics include online search engine optimization and marketing, online display advertising, direct mail campaigns, direct response television advertising, mobile advertising, and affiliate and seller referral programs. Our direct sales and account management teams also contribute to the acquisition and support of larger sellers.

Our direct, ongoing interactions with our sellers help us tailor offerings to them, at scale, and in the context of their usage. We use various scalable communication channels such as email marketing, in-product notifications and messaging, and Square Communities, our online forum for sellers, to increase the awareness and usage of our products and services with little incremental sales and marketing expense. Our customer support team also helps increase awareness and usage of our products as part of helping sellers address inquiries and issues.

11

In addition to direct channels, we work with third-party developers and partners who offer our solutions to their customers. Partners expand our addressable market to sellers with individualized or industry-specific needs. Through the Square App Marketplace, Square partners are able to expand their own addressable market by reaching the millions of sellers using Square. As of December 31, 2021, Square had more than 800 managed partners connected to its platform.

Cash App Ecosystem

Cash App has also developed a strong brand, which can be traced back to our compelling features, self-serve experience, unique design, and engaging marketing.

Peer-to-peer transactions serve as the primary acquisition channel for Cash App. Peer-to-peer transactions have powerful network effects as every time a customer sends or requests money, Cash App can acquire a new customer or reengage an existing customer. We have enhanced the efficiency of peer-to-peer transfers by streamlining the onboarding process for Cash App, enabling customers to sign up in minutes. We offer the peer-to-peer service to our Cash App customers for free, and we consider it to be a marketing tool to encourage the usage of Cash App. We do not generate revenue on the majority of peer-to-peer transactions and for these transactions we characterize card issuance costs, peer-to-peer costs and risk loss as a sales and marketing expense.

Cash App also uses paid marketing, including referrals, advertising spend, partnerships, and social media campaigns, to expand its network by enhancing its brand, reaching new customers, and improving retention among existing customers.

Additionally, we see the launch and advertising of new Cash App features as an important way to attract new customers. Features such as Cash Card and Boost rewards, bitcoin buying and selling, investing in stocks and ETFs, cross-border payments, Cash App Pay, and a tax preparation service enhance Cash App’s utility for customers and provide reasons for individuals to try Cash App.

Product Development and Technology

We design both our Square and Cash App products and services to be cohesive, fast, self-serve, and elegant, and we organize our product teams accordingly, combining individuals from product management, engineering, data science, analytics, design, and product marketing. Our products and services are platform-agnostic with most supporting iOS, Android, and web. We frequently update our software products and have a rapid software release schedule with improvements deployed regularly. Our services are built on a scalable technology platform, and we place a strong emphasis on data analytics and machine learning to maximize the efficacy, efficiency, and scalability of our services.

In our Square ecosystem, this enables us to capture and analyze billions of transactions per year and automate risk assessment for more than 99.95% of all transactions. Our hardware is designed and developed in-house, and we contract with third-party manufacturers for production.

Our Competition

Square Ecosystem

The markets in which our Square ecosystem operates are competitive and evolving. Our competitors range from large, well-established vendors to smaller, earlier-stage companies.

We seek to differentiate ourselves from competitors primarily on the basis of our extensive commerce ecosystem and our focus on building remarkable products and services that are cohesive, fast, self-serve, and elegant. In addition, we differentiate ourselves by offering transparent pricing, no long-term contracts, and our ability to innovate and reshape the industries we operate in to expand access to traditionally unserved or underserved sellers. With respect to each of these factors, we believe that we compare favorably to our competitors. Competitors that overlap with certain functions and features that we provide include:

•Pen and paper, manual processes, and paper currency

12

•Business software providers such as those that provide point of sale, website building, inventory management, employee management, customer relationship management invoicing, and appointment booking solutions

•Payment terminal vendors

•Merchant acquirers

•Banks that provide payment processing, checking, savings, loans, and payroll

•Payroll processors

•Established or new alternative lenders

Cash App Ecosystem

Cash App is our ecosystem of financial services for individuals and competes with other companies in the peer-to-peer payments, debit and prepaid cards, credit card rewards, stock trading, tax filing, digital wallet, and bitcoin exchange spaces. Our competitors include money transfer apps, prepaid debit card offerings, brokerage firms, tax firms and crypto trading services.

We primarily compete based on our brand and the simplicity and quality of our customer experience. We invest in brand, design, and technology to keep our products fast and simple, while also improving and expanding our features.

Human Capital

Our employees are the driving force behind our purpose of economic empowerment. Attracting, developing, and retaining top talent remain a focus in the development of our human capital programs. As of December 31, 2021, we had 8,521 full-time employees worldwide with 1,353 full-time employees outside the US. We also engage temporary employees and consultants as needed to support our operations.

We have a purpose-driven culture, with a focus on employee input and well-being, which we believe enables us to attract and retain exceptional talent. We offer learning and development programs for all employees, as well as a robust manager training program. Employees are able to actively voice their questions and thoughts through many internal channels, including our company townhall meetings and bi-annual employee engagement surveys. While we have been in support of a distributed work model for years, due to the COVID-19 pandemic we were able to increase our focus on this model more quickly. For Block, the distributed work model means that we no longer have a designated headquarters location and that for the vast majority of roles, our employees have the option to work from home or from a Block office space. Whether it be from home, in an office, or a combination of the two, we are focused on providing our employees with more flexibility. This policy has unlocked opportunities to hire and retain talent in more locations, as many employees can continue to work for us if they need or want to relocate.

A key focus of our human capital management approach is our commitment to improving inclusion and diversity. In 2021, our focus was on building sustainable systems to champion inclusion and diversity via three critical channels — growing our Communities program (employee resource groups), equipping our managers to build and lead inclusive teams, and making diversity a central component of our recruiting strategy. Each year, we publish our workforce demographics on our inclusion and diversity blog to show how far we have come, where there is room to grow, and how our workforce is evolving from multiple perspectives. The 2021 report is available at: https://squareup.com/us/en/about/diversity/workforce-data-2021. The contents of the report and our websites are not incorporated by reference into this Annual Report on Form 10-K.

From a total rewards perspective, Block offers a competitive compensation and benefits package, which we review and update each year. Our annual compensation planning coincides with our feedback cycle where employees and managers have performance conversations to facilitate learning and career development. As part of our compensation review program, we conduct pay equity analyses annually.

Intellectual Property

We seek to protect our intellectual property rights by relying on a combination of federal, state, and common law rights in the United States and other countries, as well as on contractual measures. It is our practice to enter into confidentiality, non-disclosure, and invention assignment agreements with our employees and contractors, and into confidentiality and non-disclosure agreements with other third parties, in order to limit access to, and disclosure and use of, our confidential information and proprietary technology. In addition to these contractual measures, we also rely on a

13

combination of trademarks, trade dress, copyrights, registered domain names, trade secrets, and patent rights to help protect our brand and our other intellectual property.

We have developed a patent program and strategy to identify, apply for, and secure patents for innovative aspects of our products, services, and technologies where appropriate. In addition to our existing patents, we intend to file additional patent applications as we continue to innovate through our research and development efforts and to pursue additional patent protection to the extent we deem it beneficial and cost-effective.

We actively pursue registration of our trademarks, logos, service marks, trade dress, and domain names in the United States and in other jurisdictions. We are the registered holder of a variety of U.S. and international trademarks and domain names that include the terms “Block,” “Square,” “Cash App," “Afterpay,” “Weebly," “TIDAL,” “Spiral,” “TBD,” and variations thereof.

From time to time, we also incorporate certain intellectual property licensed from third parties, including under certain open source licenses. Even if any such third-party technology did not continue to be available to us on commercially reasonable terms, we believe that alternative technologies would be available as needed in every case.

Government Regulation

Foreign and domestic laws and regulations apply to many key aspects of our business. Any actual or perceived failure to comply with these requirements may result in, among other things, revocation of required licenses or registrations, loss of approved status, private litigation, regulatory or governmental investigations, administrative enforcement actions, sanctions, civil and criminal liability, and constraints on our ability to continue to operate. It is also possible that current or future laws or regulations could be interpreted or applied in a manner that would prohibit, alter, or impair our existing or planned products and services, or that could require costly, time-consuming, or otherwise burdensome compliance measures from us.

Payments Regulation

Various laws and regulations govern the payments industry in the United States and globally. For example, certain jurisdictions in the United States require a license to offer money transmission services, such as Cash App’s peer-to-peer payments, and we maintain a license in each of those jurisdictions and comply with new license requirements as they arise. We are also registered as a “Money Services Business” with the U.S. Department of Treasury’s Financial Crimes Enforcement Network. These licenses and registrations subject us, among other things, to record-keeping requirements, reporting requirements, bonding requirements, limitations on the investment of customer funds, and inspection by state and federal regulatory agencies.

Outside the United States, we provide localized versions of some of our services to customers, including through various foreign subsidiaries. The activities of those non-U.S. entities are, or may be, supervised by regulatory authorities in the jurisdictions in which they operate. For instance, we hold an Australian Financial Services License issued by the Australian Securities and Investments Commission to provide non-cash payments in Australia, and we are licensed as an Electronic Money Institution to provide payments services and electronic money in the United Kingdom by the Financial Conduct Authority and in the European Union by the Central Bank of Ireland and the Bank of Lithuania.

Our payments services may be or become subject to regulation by other authorities, and the laws and regulations applicable to the payments industry in any given jurisdiction are always subject to interpretation and change.

Consumer Protection

The Consumer Financial Protection Bureau and other federal, local, state, and foreign regulatory and law enforcement agencies regulate financial products and enforce consumer protection laws, including those applicable to credit, deposit, and payments services, and other similar services. These agencies have broad consumer protection mandates, and they promulgate, interpret, and enforce rules and regulations that affect our business.

Anti-Money Laundering

14

We are subject to anti-money laundering ("AML") laws and regulations in the United States and other jurisdictions. We have implemented an AML program designed to prevent our payments network from being used to facilitate money laundering, terrorist financing, and other illicit activity. Our program is also designed to prevent our network from being used to facilitate business in countries, or with persons or entities, included on designated lists promulgated by the U.S. Department of the Treasury’s Office of Foreign Assets Controls and equivalent applicable foreign authorities. Our AML compliance program includes policies, procedures, reporting protocols, and internal controls, including the designation of an AML compliance officer, and is designed to address these legal and regulatory requirements and to assist in managing risk associated with money laundering and terrorist financing.

Bank Regulation

We obtained approval from the Federal Deposit Insurance Corporation ("FDIC") and the Utah Department of Financial Institutions to open an industrial loan corporation ("ILC") in 2021. The opening of Square Financial Services, our ILC, in March 2021 subjects us to direct state and federal regulatory supervision and requires compliance with applicable banking regulations and requirements.

Broker-Dealer Regulation

Our subsidiary, Cash App Investing LLC ("Cash App Investing"), operates as a broker-dealer and is therefore registered with the Securities and Exchange Commission ("SEC") and a member of the Financial Industry Regulatory Authority ("FINRA"). As a broker-dealer, Cash App Investing is subject to SEC and FINRA laws and regulations including, without limitation, how it markets its services, handles customer assets, keeps records, and reports to the SEC and FINRA. Cash App Investing is also registered in each state where we conduct business, and subject to those states’ securities laws and regulations.

Virtual Currency Regulation

We are subject to certain licensing and supervisory frameworks as a result of our Cash App offering, through which customers can use their stored funds to buy, hold and sell bitcoin, and transfer bitcoin to and from Cash App. We currently hold a New York State BitLicense. The laws and regulations applicable to virtual currency are evolving and subject to interpretation and change. Therefore, our current and future virtual currency services may be or become subject to additional licensing and regulatory requirements by other state and federal authorities.

Protection and Use of Information

We collect and use a wide variety of information for various purposes in our business, including to help ensure the integrity of our services and to provide features and functionality to our customers. This aspect of our business, including the collection, use, disclosure, and protection of the information we acquire from our own services as well as from third-party sources, is subject to laws and regulations in the United States, the European Union, and elsewhere. Accordingly, we publish our privacy policies and terms of service, which describe our practices concerning the use, transmission, and disclosure of information. As our business continues to expand in the United States and worldwide, and as laws and regulations continue to be passed and their interpretations continue to evolve in numerous jurisdictions, additional laws and regulations may become relevant to us.

Communications Regulation

We send texts, emails, and other communications in a variety of contexts, such as when providing digital receipts and marketing. Communications laws and regulations, including those promulgated by the Federal Communications Commission, apply to certain aspects of this activity in the United States and elsewhere.

Additional Developments

Various regulatory agencies in the United States and elsewhere in our international markets continue to examine a wide variety of issues that could impact our business, including products liability, import and export compliance, accessibility for the disabled, insurance, marketing, privacy, data protection, information security, and labor and employment matters. As our business continues to develop and expand, additional rules and regulations may become relevant. For example, if we choose to offer Square Payroll in more jurisdictions, additional regulations, including tax rules, will apply.

15

Seasonality

Historically, for our Square ecosystem transaction-based revenue has been strongest in our fourth quarter and weakest in our first quarter, as our sellers typically generate additional GPV during the holiday season. Subscription and services-based revenue generally demonstrates less seasonality than transaction-based revenue. Hardware revenue generally demonstrates less seasonality than transaction-based revenue, with most fluctuations tied to periodic product launches, promotions, or other arrangements with our retail partners. We have not historically experienced meaningful seasonality with respect to total net revenue as this effect has been offset by our revenue growth. In 2020 and 2021, typical seasonality trends for the Square ecosystem were impacted as a result of the COVID-19 pandemic and subsequent shelter in-place restrictions.

Historically, our Cash App ecosystem experiences improvements in revenue and gross profit related to the distribution of government funds as customers have pulled more funds into Cash App, including during the first quarter when tax refunds are distributed. During the year ended December 31, 2021, we saw a significant increase in total Cash App revenue, primarily from bitcoin revenue which contributed 57% of total consolidated net revenue in 2021, and 48% of the total increase in consolidated net revenues in 2021. The primary drivers of bitcoin revenue are customer demand and the current market price of bitcoin, and as such, may not be indicative of future performance and skew typical seasonality trends in the Cash App ecosystem.

Corporate Information

Block was incorporated in Delaware in June 2009. In 2020, we started adopting a distributed work model. As of 2021, although our real estate footprint remains intact, we no longer have a designated headquarters location. Our telephone number is (415) 375-3176. Our website is located at www.block.xyz, and our investor relations website is located at investors.block.xyz. The information contained in, or accessible through, our website is not part of, and is not incorporated into, this Annual Report on Form 10-K.

We use various trademarks and trade names in our business, including “Block,” “Square,” “Cash App” and “Afterpay,” which we have registered in the United States and in various other countries. This Annual Report on Form 10-K also contains trademarks and trade names of other businesses that are the property of their respective holders. We have omitted the ® and ™ designations, as applicable, for the trademarks we name in this Annual Report on Form 10-K.

Available Information

Copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (Exchange Act), are available, free of charge, on our investor relations website as soon as reasonably practicable after we file such material electronically with or furnish it to the Securities and Exchange Commission (SEC). The SEC also maintains a website that contains our SEC filings. The address of the site is www.sec.gov.

We webcast our earnings calls and certain events we participate in or host with members of the investment community on our investor relations website. Additionally, we provide notifications of news or announcements regarding our financial performance, including SEC filings, investor events, press and earnings releases, and blogs as part of our investor relations website. We have used, and intend to continue to use, our investor relations website, as well as the Twitter accounts @Blocks and @BlockIR, as means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD. Further corporate governance information, including our board committee charters, code of business conduct and ethics, and corporate governance guidelines, is also available on our investor relations website under the heading “Governance Documents.” The contents of our websites are not intended to be incorporated by reference into this Annual Report on Form 10-K or in any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

Item 1A. RISK FACTORS

Investing in our securities involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this Annual Report on Form 10-K, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes, before making any investment decision with respect to our securities. The risks and

16

uncertainties described below may not be the only ones we face. If any of the risks actually occur, our business could be materially and adversely affected. In that event, the market price of our Class A common stock could decline, and you could lose part or all of your investment.

Risk Factors Summary

Our business operations are subject to numerous risks and uncertainties, including those outside of our control, that could cause our actual results to be harmed, including risks regarding the following:

Risks related to our business and our industry:

•our ability to maintain, protect, and enhance our brands;

•our participation in government relief programs set up in response to the COVID-19 pandemic;

•our ability to retain existing sellers and customers, attract new sellers and customers, and increase sales to both new and existing sellers and customers;

•our investments in our business and ability to maintain profitability;

•our efforts to expand our product portfolio and market reach;

•our ability to develop products and services to address the rapidly evolving market for payments and financial services;

•competition in our industry;

•any acquisitions, strategic investments, entries into new businesses, joint ventures, divestitures and other transactions that we may undertake;

•liabilities that may exist at Afterpay;

•the successful integration of our business with Afterpay;

•additional risks of our majority interest in TIDAL;

•expanding our business globally;

•additional risks of BNPL lending;

•additional risks of Square Banking relating to the structure of bank partnerships, and FDIC and other regulatory obligations; and

•additional risks of Square Loans related to the availability of capital, seller payments, interest rate, deposit insurance premiums, and general macroeconomic conditions.

Operational risks:

•real or perceived improper or unauthorized use of, disclosure of, or access to sensitive data;

•real or perceived security breaches or incidents or human error in administering our software, hardware, and systems;

•systems failures, interruptions, delays in service, catastrophic events, and resulting interruptions in the availability of our products or services or those of our sellers;

•any inability to access our private keys required to access our bitcoins or any hack or other data loss relating to the bitcoins we hold;

•our risk management efforts;

•our dependence on payment card networks and acquiring processors;

•our reliance on third parties and their systems for a variety of services, including the processing of transaction data and settlement of funds;

•our dependence on key management and any failure to attract, motivate, and retain our employees;

•our operational, financial, and other internal controls and systems;

•any shortage, price increases, tariffs, changes, delay or discontinuation of our key components;

•our ability to accurately forecast demand for our products and adequately manage our product inventory;

•the integration of our services with a variety of operating systems and the interoperation of our hardware that enables merchants to accept payment cards with third-party mobile devices utilizing such operating systems; and

•difficulties estimating the amount payable under TIDAL's license agreements.

Economic, financial, and tax risks:

•the ongoing COVID-19 pandemic and measures intended to prevent its spread;

•a deterioration of general macroeconomic conditions;

•any inability to secure financing on favorable terms, or at all, or covenants in our existing credit agreement, the indentures, or future agreements;

17

•our ability to service our convertible notes and our senior notes;

•counterparty risk with respect to our convertible note hedge transactions;

•our bitcoin investments being subject to volatile market prices, impairment, and other risks of loss;

•foreign exchange rates risks; and

•any greater-than-anticipated tax liabilities or significant valuation allowances on our deferred tax assets.

Legal, regulatory, and compliance risks:

•extensive regulation and oversight in a variety of areas of our business;

•complex and evolving regulations and oversight related to privacy and data protection;

•litigation, including intellectual property claims, government investigations or inquiries, and regulatory matters or disputes;

•obligations and restrictions as a licensed money transmitter;

•regulatory scrutiny or changes in the BNPL space;

•regulation and scrutiny of our subsidiary Cash App Investing, which is a broker-dealer registered with the SEC and a member of FINRA, including net capital and other regulatory capital requirements;

•changes to our business practices imposed by FINRA based on our ownership of Cash App Investing;

•regulation and scrutiny of our subsidiary Square Financial Services, which is a Utah state-chartered industrial bank, including the requirement that we serve as a source of financial strength to it;

•supervision and regulation of Square Financial Services, including the Dodd-Frank Act and its related regulations'

•any inability to protect our intellectual property rights; and

•assertions by third parties of infringement of intellectual property rights by TIDAL.

Risks related to ownership of our common stock:

•the dual class structure of our common stock;

•volatility of the market price of our Class A common stock;

•the dual-listing of our Class A common stock on the NYSE and our CDIs on the Australian Securities Exchange;

•our convertible note hedge and warrant transactions;

•anti-takeover provisions contained in our amended and restated certificate of incorporation, our second amended and restated bylaws, and provisions of Delaware law; and

•exclusive forum provisions in our bylaws.

Risks Related to Our Business and Our Industry

Our business depends on our ability to maintain, protect, and enhance our brands.

Having a strong and trusted brand has contributed significantly to the success of our business. We believe that maintaining, promoting, and enhancing the Square brand, the Cash App brand, the TIDAL brand, and our other brands, in a cost-effective manner is critical to achieving widespread acceptance of our products and services and expanding our base of customers. Maintaining and promoting our brands will depend largely on our ability to continue to provide useful, reliable, secure, and innovative products and services, as well as our ability to maintain trust and be a technology leader. We may introduce, or make changes to, features, products, services, privacy practices, or terms of service that customers do not like, which may materially and adversely affect our brands. Our brand promotion activities may not generate customer awareness or increase revenue, and even if they do, any increase in revenue may not offset the expenses we incur in building our brands. If we fail to successfully promote and maintain our brands or if we incur excessive expenses in this effort, our business could be materially and adversely affected.

The introduction and promotion of new products and services, as well as the promotion of existing products and services, may be partly dependent on our visibility on third-party advertising platforms, such as Google, Twitter, or Facebook. Changes in the way these platforms operate or changes in their advertising prices, data use practices or other terms could make the maintenance and promotion of our products and services and our brands more expensive or more difficult. If we are unable to market and promote our brands on third-party platforms effectively, our ability to acquire new customers would be materially harmed. We also use retail partners to sell hardware and acquire sellers for Square. Our ability to acquire new sellers could be materially harmed if we are unable to enter into or maintain these partnerships on terms that are commercially reasonable to us, or at all.

Harm to our brands can arise from many sources, including failure by us or our partners and service providers to satisfy expectations of service and quality; inadequate protection or misuse of sensitive information; fraud committed by third

18

parties using our products or applications; compliance failures and claims; litigation and other claims; and misconduct by our partners, service providers, or other counterparties. We have also been from time to time in the past, and may in the future be, the target of incomplete, inaccurate, and misleading or false statements about our company and our business that could damage our brands and deter customers from adopting our services or our products. Any negative publicity about the industries we operate in or our company, the quality and reliability of our products and services, our risk management processes, changes to our products and services, our ability to effectively manage and resolve customer complaints, our privacy, data protection, and information security practices, litigation, regulatory activity, policy positions, and the experience of our customers with our products or services could adversely affect our reputation and the confidence in and use of our products and services. If we do not successfully maintain, protect or enhance our brands, our business could be materially and adversely affected.

Our participation in government relief programs set up in response to the COVID-19 pandemic, such as facilitating loans to businesses under the Paycheck Protection Program or unemployment benefits, stimulus, and child tax credit payments to individuals through Cash App, may subject us to new risks and uncertainties.

The Coronavirus Aid, Relief, and Economic Security Act ("CARES Act"), the Consolidated Appropriations Act, 2021, and the American Rescue Plan Act provided for stimulus funds, called economic impact payments, to individuals, expanded eligibility for unemployment benefits, increased the amount of and extended the period for unemployment insurance benefits, and provided child tax credit payments to qualifying households. Cash App has been facilitating the payment of such stimulus funds, unemployment benefits, and child tax credit payments by offering account and routing numbers that customers can use to deposit such payments directly into their Cash App accounts and accepting cash-in deposits from prepaid cards issued by state governments. Cash App has also worked with partner banks to expand direct deposit eligibility for its customers. The federal programs were set up quickly and under difficult and unprecedented circumstances and the implementation of these programs at the federal, state, and local levels has been complex and difficult, causing them to be more susceptible to fraud, data breaches, technical difficulties, and other new and uncertain risks. Cash App’s facilitation of unemployment, stimulus, and child tax credit payments exposes us to operational, compliance, reputational, and legal risks, which could result in governmental action, litigation, or other forms of material and adverse loss. Moreover, as such stimulus measures have ended, growth in new Cash App customers may slow.

As a participant in the Paycheck Protection Program (“PPP”) administered by the Small Business Administration (“SBA”) and enacted in March 2020 under the CARES Act in response to the COVID-19 pandemic, Square Capital provided small businesses two-year or five-year PPP loans. Square Capital approved and funded the last remaining PPP loan applications in May 2021 upon exhaustion of the funds in the program. In the event that it is determined that a borrower does not qualify for loan forgiveness or if a borrower defaults on its PPP loan, Square Capital is at risk to the extent the SBA may decline to honor its guarantee or to forgive the loan due to documentation or verification errors, failure to follow regulatory requirements, or lack of adherence to underwriting standards. As a result, Square Capital’s documentation, review, underwriting, and servicing processes will be subject to scrutiny, and we could incur losses if we fail to comply with the SBA documentation and other requirements. We also may become subject to litigation arising as a result of our participation in the PPP, which could result in significant financial liability or could adversely affect our reputation. There can be no assurance that Square Capital will be successful in mitigating all of the risks associated with the PPP loans or that this lending will not have a negative impact on our business and results of operations.

As our revenue has increased, our growth rate has slowed at times in the past and may slow or decline in the future, and our growth rates in each of our reporting segments may vary. Future revenue growth depends on our ability to retain existing sellers and customers, attract new sellers and customers, and increase sales to both new and existing sellers and customers.

Our rate of revenue growth has slowed at times in the past and may decline in the future, and it may slow or decline more quickly than we expect for a variety of reasons, including the risks described in this Annual Report on Form 10-K. Additionally, our rate of revenue growth may vary between our reporting segments. For example, in recent periods our Cash App segment revenue has grown at a high rate, which has varied and may continue to vary from the growth rate of our Square segment. Our sellers and customers have no obligation to continue to use our services, and we cannot assure you that they will. We generally do not have long-term contracts with our sellers and customers, and the difficulty and costs associated with switching to a competitor may not be significant for many of the services we offer. Our sellers’ activity with us may decrease for a variety of reasons, including sellers’ level of satisfaction with our products and services, our pricing and the pricing and quality of competing products or services, the effects of global economic conditions, or reductions in the aggregate spending of our sellers’ customers. Growth in monthly transacting actives on Cash App and customers’ level of

19

engagement with our products and services on Cash App are essential to our success and long-term financial performance. However, the growth rate of monthly transacting actives has fluctuated over time, and it may slow or decline in the future. A number of factors have affected and could potentially negatively affect Cash App customer growth and engagement, including our ability to introduce new products and services that are compelling to our customers, the network effects of other customers choosing whether to use Cash App, technical or other problems that affect customer experience, failure to provide sufficient customer support, fraud and scams targeting Cash App customers, and harm to our reputation and brand. Further, certain events or programs, such as government stimulus programs may correlate with periods of significant growth, but such growth may not be sustainable. Additionally, the growth rate of Cash App revenue may be distorted by the prices of bitcoin, as bitcoin revenue may increase or decrease due to the price of bitcoin and may not correlate to customer or engagement growth rates.

The growth of our business depends in part on our existing sellers and customers expanding their use of our products and services. If we are unable to encourage broader use of our services within each ecosystem by our existing sellers and customers, our growth may slow or stop, and our business may be materially and adversely affected. The growth of our business also depends on our ability to attract new sellers and customers, to encourage sellers and customers to use our products and services, and to introduce successful new products and services. We have invested and will continue to invest in our business in order to offer better or new features, products, and services and to adjust our product offerings to changing economic conditions, but if those features, products, services, and changes fail to be successful on the expected timeline or at all, our growth may slow or decline.

We have generated significant net losses in the past, and we intend to continue to invest substantially in our business. Thus, we may not be able to maintain profitability.

While we generated net income of $166.3 million, $213.1 million, and $375.4 million for the years ended December 31, 2021, 2020 and 2019, respectively, we have generated significant net losses in the past. As of December 31, 2021, we had an accumulated deficit of $28.0 million.