|

|

FINANCIAL STATEMENTS

FEG Absolute Access Fund I LLC |

FEG Absolute Access Fund I LLC

Financial Statements

Year Ended March 31, 2017

Contents

|

Report of Independent Registered Public Accounting Firm |

1 |

|

Statement of Assets and Liabilities |

2 |

|

Statement of Operations |

3 |

|

Statements of Changes in Net Assets |

4 |

|

Statement of Cash Flows |

5 |

|

Financial Highlights |

6 |

|

Notes to Financial Statements |

7 |

|

Other Information (Unaudited) |

|

|

Company Management |

13 |

|

Other Information |

15 |

|

Privacy Policy |

17 |

Financial Statements of FEG Absolute Access Fund LLC

FEG Absolute Access Fund I LLC

Report of Independent Registered Public Accounting Firm

March 31, 2017

|

1

FEG Absolute Access Fund I LLC

Statement of Assets and Liabilities

March 31, 2017

|

Assets |

||||

|

Cash |

$ |

3,553,449 |

||

|

Investment in FEG Absolute Access Fund LLC, at fair value (cost $295,919,872) |

334,976,685 |

|||

|

Prepaid expenses and other assets |

61,250 |

|||

|

Total assets |

338,591,384 |

|||

|

Liabilities |

||||

|

Capital redemptions payable |

3,016,449 |

|||

|

Capital subscriptions received in advance |

537,000 |

|||

|

Professional fees payable |

70,539 |

|||

|

Accounting and administration fees payable |

38,957 |

|||

|

Directors fees payable |

6,000 |

|||

|

Other liabilities |

2,628 |

|||

|

Total liabilities |

3,671,573 |

|||

|

Net assets |

$ |

334,919,811 |

||

|

Net assets consist of: |

||||

|

Paid-in capital |

$ |

337,676,771 |

||

|

Accumulated net investment loss |

(13,170,139 |

) |

||

|

Accumulated net realized gain on investments |

6,041,732 |

|||

|

Accumulated net unrealized appreciation on investments |

4,371,447 |

|||

|

Net assets |

$ |

334,919,811 |

||

|

Units issued and outstanding (unlimited units authorized) |

284,141 |

|||

|

Net Asset Value per unit |

$ |

1,178.71 |

||

See accompanying notes.

2

FEG Absolute Access Fund I LLC

Statement of Operations

Year Ended March 31, 2017

|

Investment income/(loss) allocated from FEG Absolute Access Fund LLC |

||||

|

Dividend income |

$ |

41,173 |

||

|

Expenses |

(3,526,504 |

) |

||

|

Net investment loss allocated from FEG Absolute Access Fund LLC |

(3,485,331 |

) |

||

|

Fund investment income |

||||

|

Withholding tax rebate |

22,677 |

|||

|

Fund expenses |

||||

|

Professional fees |

189,155 |

|||

|

Accounting and administration fees |

120,505 |

|||

|

Compliance monitoring fees |

102,083 |

|||

|

Custodian fees |

31,199 |

|||

|

Directors fees |

24,000 |

|||

|

Tender offer fees |

17,615 |

|||

|

Printing fees |

12,744 |

|||

|

Registration fees |

12,000 |

|||

|

Other expenses |

36,357 |

|||

|

Total Fund expenses |

545,658 |

|||

|

Net investment loss |

(4,008,312 |

) |

||

|

Realized and unrealized gain on investments allocated from FEG Absolute Access Fund LLC |

||||

|

Net realized gain on investments |

5,304,716 |

|||

|

Net change in unrealized appreciation/depreciation on investments |

14,115,620 |

|||

|

Net realized and unrealized gain on investments allocated from FEG Absolute Access Fund LLC |

19,420,336 |

|||

|

Net increase in net assets resulting from operations |

$ |

15,412,024 |

||

See accompanying notes.

3

FEG Absolute Access Fund I LLC

Statements of Changes in Net Assets

|

Year Ended |

Year Ended |

|||||||

|

Operations |

||||||||

|

Net investment loss |

$ |

(4,008,312 |

) |

$ |

(4,261,985 |

) |

||

|

Net realized gain (loss) on investments |

5,304,716 |

(1,261,567 |

) |

|||||

|

Net change in unrealized appreciation/depreciation on investments |

14,115,620 |

(9,744,173 |

) |

|||||

|

Net change in net assets resulting from operations |

15,412,024 |

(15,267,725 |

) |

|||||

|

Distributions |

||||||||

|

From net investment income |

(2,509,060 |

) |

(698,680 |

) |

||||

|

From net realized gains |

— |

(677,868 |

) |

|||||

|

Change in net assets from distributions |

(2,509,060 |

) |

(1,376,548 |

) |

||||

|

Capital transactions |

||||||||

|

Capital subscriptions |

25,457,110 |

(1) |

57,077,510 |

|||||

|

Capital reinvestments of distributions |

2,345,654 |

1,309,866 |

||||||

|

Capital redemptions(2) |

(39,301,470 |

) |

(29,552,143 |

) |

||||

|

Net change in net assets resulting from capital transactions |

(11,498,706 |

) |

28,835,233 |

|||||

|

Net change in net assets |

1,404,258 |

12,190,960 |

||||||

|

Net assets at beginning of year |

333,515,553 |

321,324,593 |

||||||

|

Net assets at end of year |

$ |

334,919,811 |

$ |

333,515,553 |

||||

|

Accumulated net investment loss |

$ |

(13,170,139 |

) |

$ |

(3,261,320 |

) |

||

|

Units transactions |

||||||||

|

Units sold |

21,750 |

48,236 |

||||||

|

Units reinvested |

2,004 |

1,150 |

||||||

|

Units redeemed |

(33,903 |

) |

(25,283 |

) |

||||

|

Net change in units |

(10,149 |

) |

24,103 |

|||||

|

(1) |

Includes a $10 subscription from FEG Investors, LLC (the Investment Manager) for Class II Units, which was the only activity for Class II Units during the year ended March 31, 2017. |

|

(2) |

Net of early repurchase fees in the amount of $1,433 and $0, respectively. |

See accompanying notes.

4

FEG Absolute Access Fund I LLC

Statement of Cash Flows

Year Ended March 31, 2017

|

Operating activities |

||||

|

Net increase in net assets resulting from operations |

$ |

15,412,024 |

||

|

Adjustments to reconcile net increase in net assets resulting from operations to net cash provided by operating activities: |

||||

|

Purchases of investments |

(25,459,846 |

) |

||

|

Proceeds from sales of investments |

40,002,746 |

|||

|

Net investment loss allocated from FEG Absolute Access Fund LLC |

3,485,331 |

|||

|

Net realized gain on investments allocated from FEG Absolute Access Fund LLC |

(5,304,716 |

) |

||

|

Net change in unrealized appreciation/depreciation on investments allocated from FEG Absolute Access Fund LLC |

(14,115,620 |

) |

||

|

Changes in operating assets and liabilities: |

||||

|

Prepaid expenses and other assets |

(30,917 |

) |

||

|

Professional fees payable |

38,451 |

|||

|

Accounting and administration fees payable |

(2,349 |

) |

||

|

Other liabilities |

(17,486 |

) |

||

|

Net cash provided by operating activities |

14,007,618 |

|||

|

Financing activities |

||||

|

Proceeds from capital subscriptions |

25,994,110 |

|||

|

Dividends paid to shareholders, net of reinvestments |

(163,406 |

) |

||

|

Payments for capital redemptions |

(37,770,358 |

) |

||

|

Net cash used in financing activities |

(11,939,654 |

) |

||

|

Net change in cash |

2,067,964 |

|||

|

Cash at beginning of year |

1,485,485 |

|||

|

Cash at end of year |

$ |

3,553,449 |

||

|

Supplemental disclosure of cash flow information |

||||

|

Non-cash distribution fully reinvested |

$ |

2,345,654 |

||

See accompanying notes.

5

FEG Absolute Access Fund I LLC

Financial Highlights

|

Year Ended March 31, |

||||||||||||||||

|

2017 |

2016 |

2015 |

2014 |

|||||||||||||

|

Per unit operating performances:(1)(2) |

||||||||||||||||

|

Net asset value per unit, beginning of year |

$ |

1,133.29 |

$ |

1,189.27 |

$ |

1,135.93 |

$ |

1,062.22 |

||||||||

|

Income (loss) from investment operations: |

||||||||||||||||

|

Net investment loss |

(14.62 |

) |

(13.72 |

) |

(6.07 |

) |

(5.98 |

) |

||||||||

|

Net realized and unrealized gain (loss) on investments |

68.75 |

(37.63 |

) |

59.41 |

79.69 |

|||||||||||

|

Total change in per unit value from investment operations |

54.13 |

(51.35 |

) |

53.34 |

73.71 |

|||||||||||

|

Distributions paid from: |

||||||||||||||||

|

Net investment income |

(8.71 |

) |

(2.35 |

) |

— |

— |

||||||||||

|

Net realized gains |

— |

(2.28 |

) |

— |

— |

|||||||||||

|

Total distributions to shareholders |

(8.71 |

) |

(4.63 |

) |

— |

— |

||||||||||

|

Net asset value per unit, end of year |

$ |

1,178.71 |

$ |

1,133.29 |

$ |

1,189.27 |

$ |

1,135.93 |

||||||||

|

Year Ended March 31, |

||||||||||||||||||||

|

2017 |

2016 |

2015 |

2014 |

2013 |

||||||||||||||||

|

Ratios to average net assets:(3) |

||||||||||||||||||||

|

Total expenses |

1.23 |

% |

1.27 |

% |

1.34 |

% |

1.56 |

% |

1.39 |

% |

||||||||||

|

Net investment loss |

(1.22 |

)% |

(1.27 |

)% |

(1.34 |

)% |

(1.56 |

)% |

(1.39 |

)% |

||||||||||

|

Total return |

4.78 |

% |

(4.32 |

)% |

4.70 |

% |

6.94 |

% |

8.24 |

% |

||||||||||

|

Portfolio turnover |

6.43 |

% |

12.33 |

% |

28.75 |

% |

17.93 |

% |

7.96 |

% |

||||||||||

|

Net assets end of year (000's) |

$ |

334,920 |

$ |

333,516 |

$ |

321,325 |

$ |

239,771 |

$ |

159,565 |

||||||||||

|

(1) |

Selected data is for a single unit outstanding throughout the year. |

|

(2) |

Effective April 1, 2013, the Fund was unitized. |

|

(3) |

The ratios include the Fund’s proportionate share of income and expenses allocated from FEG Absolute Access Fund LLC. |

See accompanying notes.

6

FEG Absolute Access Fund I LLC

Notes to Financial Statements

Year Ended March 31, 2017

1. Organization

FEG Absolute Access Fund I LLC (the “Fund”) was organized as a limited liability company under the laws of the State of Delaware on January 20, 2011 and commenced operations on April 1, 2011. Prior to December 31, 2015 the Fund was known as FEG Absolute Access TEI Fund LLC. The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified, closed-end management investment company. The business and operations of the Fund are managed and supervised under the direction of the Board of Directors (the “Board”). The objective of the Fund is to achieve capital appreciation in both rising and falling markets, although there can be no assurance that the Fund will achieve this objective. Effective January 1, 2015, the Fund attempts to achieve its investment objective by investing all or substantially all of its assets directly in FEG Absolute Access Fund LLC (“FEG Absolute Access Fund”), a limited liability company organized under the laws of the State of Delaware and registered under the 1940 Act. The Fund and FEG Absolute Access Fund are managed by FEG Investors, LLC (the “Investment Manager”), an investment manager registered under the Investment Advisers Act of 1940, as amended. FEG Absolute Access Fund’s Board of Directors (the “FEG Absolute Access Fund Board”) has overall responsibility for the management and supervision of FEG Absolute Access Fund’s operations. To the extent permitted by applicable law, the FEG Absolute Access Fund Board may delegate any of its respective rights, powers and authority to, among others, the officers of FEG Absolute Access Fund, any committee of the FEG Absolute Access Fund Board, or the Investment Manager.

Units of limited liability company interest (“Units”) of the Fund are offered only to investors (“Members”) that represent that they are an “accredited investor” within the meaning of Rule 501 under the Securities Act of 1933, as amended (the “1933 Act”).

The Second Amended and Restated Limited Liability Company Operating Agreement (as it may be further amended, the “Operating Agreement”) for the Fund was approved by the Board at a meeting held on August 18, 2014, and by Members at a meeting held on December 12, 2014. The Operating Agreement: (a) allows the Fund to elect to be classified, for purposes of U.S. federal income tax, as a corporation that intends to elect to be treated as a regulated investment company (“RIC”) under Subchapter M of Subtitle A, Chapter 1, of the Internal Revenue Code of 1986, as amended (the “Code”); and (b) permits the creation of multiple classes of Units of the Fund. The SEC granted the Fund an Exemptive Order on September 9, 2015 permitting the Fund to offer multiple classes of Units. The Fund’s registration statement permits it to offer two additional classes of Units. During the year ended March 31, 2017, the Fund received a $10 subscription from the Investment Manager as the initial investment for an additional class of units, Class II Units. There have been no other transactions involving Class II Units during the year ended March 31, 2017. Class II Units are expected to commence operations at an appropriate time in the future when additional subscriptions are available. When Class II Units commence operations, it is expected that the existing units of the Fund will be designated as Class I Units. As of March 31, 2017, no additional classes of units had commenced operations.

UMB Fund Services, Inc., a subsidiary of UMB Financial Corporation, serves as the Fund’s administrator (the “Administrator”). The Fund has entered into an agreement with the Administrator to perform general administrative tasks for the Fund, including but not limited to maintenance of the books and records of the Fund and the capital accounts of the Members of the Fund.

2. Significant Accounting Policies

The Fund is an investment company, and as such, these financial statements have applied the guidance set forth in Accounting Standards Codification (“ASC”) 946, Financial Services—Investment Companies. The following is a summary of significant accounting and reporting policies used in preparing the financial statements.

7

FEG Absolute Access Fund I LLC

Notes to Financial Statements (continued)

2. Significant Accounting Policies (continued)

Use of Estimates

The financial statements have been prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”). The preparation of these financial statements requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results could differ from such estimates.

Calculation of Net Assets and Net Asset Value per Unit

The Fund calculates its net assets as of the close of business on the last business day of each calendar month and the last day of each fiscal period. In determining its net assets, the Fund values its investments as of such month-end or as of the end of such fiscal period, as applicable. The net assets of the Fund equals the value of the total assets of the Fund less liabilities, including accrued fees and expenses, each determined as of the date the Fund’s net assets is calculated. The Net Asset Value per Unit equals net assets divided by Units outstanding.

Investment in FEG Absolute Access Fund LLC

The Fund records its investment in FEG Absolute Access Fund at fair value which is represented by the Fund’s units held in FEG Absolute Access Fund valued at their per unit net asset value. Valuation of investment funds and other investments held by FEG Absolute Access Fund is discussed in the notes to FEG Absolute Access Fund’s financial statements. The performance of the Fund is directly affected by the performance of FEG Absolute Access Fund. The financial statements of FEG Absolute Access Fund, which accompany this report, are an integral part of these financial statements. Refer to the accounting policies disclosed in the financial statements of FEG Absolute Access Fund for additional information regarding significant accounting policies that affect the Fund. As of March 31, 2017, the Fund owned 88.02% of the units of FEG Absolute Access Fund.

Taxation and Distributions to Members

For periods prior to January 1, 2015, the Fund, as a limited liability company, was classified as a partnership for federal tax purposes. Accordingly, no provision for federal income taxes was required. Components of net assets reflected in the Statement of Assets and Liabilities are reported on a tax basis, removing historical information prior to January 1, 2015.

Effective January 1, 2015, the Fund elected to be treated as a corporation for federal income tax purposes, and it further intends to elect to be treated, and expects each year to qualify, as a RIC under Subchapter M of the Code. For each taxable year that the Fund so qualifies, the Fund will not be subject to federal income tax on that part of its taxable income that it distributes to its investors. Taxable income consists generally of net investment income and net capital gains. The Fund intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains, resulting in no provision requirements for federal income or excise taxes.

Management has analyzed the Fund’s tax positions for all open tax years, which include the years ended December 31, 2013 through December 31, 2016, and has concluded that as of March 31, 2017, no provision for income taxes is required in the financial statements. Therefore, no additional tax expense, including any interest and penalties, was recorded in the current year and no adjustments were made to prior periods. To the extent the Fund recognizes interest and penalties, they are included in interest expense and other expenses, respectively, in the Statement of Operations.

The character of distributions made during the year from net investment income or net realized gain may differ from the characterization for federal income tax purposes due to differences in the recognition of income, expense, and gain/(loss) items for financial statement and tax purposes. Where appropriate, reclassifications between net asset accounts are made for such differences that are permanent in nature.

8

FEG Absolute Access Fund I LLC

Notes to Financial Statements (continued)

2. Significant Accounting Policies (continued)

Additionally, U.S. GAAP requires certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. Permanent differences between book and tax basis are attributable to partnerships and passive foreign investment companies adjustments. These reclassifications have no effect on net assets or Net Asset Value per Unit. For the tax year ended December 31, 2016, the following amounts were reclassified:

|

Paid-in capital |

$ |

1,392,864 |

||

|

Accumulated net investment loss |

(3,391,447 |

) |

||

|

Accumulated net realized gain on investments |

1,998,583 |

As of March 31, 2017, the federal tax cost of investments and unrealized appreciation/(depreciation) were as follows:

|

Gross unrealized appreciation |

$ |

38,094,618 |

||

|

Gross unrealized depreciation |

— |

|||

|

Net unrealized appreciation |

$ |

38,094,618 |

||

|

Cost of investments |

$ |

296,882,067 |

The difference between cost amounts for financial statement and federal income tax purposes is due primarily to timing differences in recognizing certain gains and losses in investment transactions.

As of December 31, 2016, the Fund had net capital loss carryforwards which are available to offset future net capital gains, if any:

|

Short-Term |

Long-Term |

|||||||

|

Non-Expiring |

$ |

2,426,779 |

$ |

806,070 |

||||

The tax character of distributions paid during the tax years ended December 31, 2016 and December 31, 2015 were as follows:

|

2016 |

2015 |

|||||||

|

Distributions paid from: |

||||||||

|

Ordinary income |

$ |

2,509,060 |

$ |

924,636 |

||||

|

Net long term capital gains |

— |

451,912 |

||||||

|

Total taxable distributions |

2,509,060 |

1,376,548 |

||||||

|

Total distributions paid |

$ |

2,509,060 |

$ |

1,376,548 |

||||

Capital Subscriptions Received in Advance and Capital Redemptions Payable

Capital subscriptions received in advance are comprised of cash received on or prior to fiscal year-end for which Units are issued on the the first day of the following fiscal year. Capital contributions received in advance do not participate in the earnings of the Fund until such Units are issued. Capital redemptions payable are comprised of requests for redemptions that were effective at fiscal-year end but were paid subsequent to fiscal year-end.

9

FEG Absolute Access Fund I LLC

Notes to Financial Statements (continued)

3. Related Party Transactions

The Investment Manager receives from FEG Absolute Access Fund a monthly management fee (the “Management Fee”) equal to 1/12 of 0.85% of the FEG Absolute Access Fund’s month-end members’ capital balances. The Fund indirectly incurs the Management Fee as a member of FEG Absolute Access Fund.

Each member of the Board who is not an “interested person” of the Fund (the “Independent Directors”), as defined by the 1940 Act, receives a quarterly retainer of $3,000. In addition, all Independent Directors are reimbursed by the Fund for all reasonable out-of-pocket expenses incurred by them in performing their duties. The Independent Directors’ fees totaled $24,000 for the year ended March 31, 2017, of which $6,000 was payable as of March 31, 2017.

4. Capital

Members may be admitted when permitted by the Board. Generally, Members will only be admitted as of the beginning of a calendar month but may be admitted at any other time in the discretion of the Board. The minimum initial investment is $50,000, and additional contributions from existing Members may be made in a minimum amount of $25,000, although the Board may waive such minimums in certain cases.

No Member will have the right to require the Fund to redeem its Units. Rather, the Board may, from time to time and in its complete and absolute discretion, cause the Fund to offer to repurchase Units from Members pursuant to written requests by Members on such terms and conditions as it may determine. However, because all or substantially all of the Fund’s assets will be invested in FEG Absolute Access Fund, the Fund generally will find it necessary to liquidate a portion of its FEG Absolute Access Fund units in order to satisfy repurchase requests. Because FEG Absolute Access Fund’s units may not be transferred, the Fund may withdraw a portion of its FEG Absolute Access Fund units only pursuant to repurchase offers by FEG Absolute Access Fund. Therefore, the Fund does not expect to conduct a repurchase offer for Units unless FEG Absolute Access Fund contemporaneously conducts a repurchase offer for FEG Absolute Access Fund units.

In determining whether the Fund should offer to repurchase Units from Members pursuant to written requests, the Board will consider, among other things, the recommendation of the Investment Manager. The Investment Manager expects that it will recommend to the FEG Absolute Access Fund Board that FEG Absolute Access Fund repurchases FEG Absolute Access Fund units from members twice a year, effective as of June 30th and December 31st each year. The repurchase amount will be determined by the FEG Absolute Access Fund Board in its complete and absolute discretion, but is expected to be no more than approximately 25% of FEG Absolute Access Fund’s outstanding units.

FEG Absolute Access Fund will make repurchase offers, if any, to all holders of FEG Absolute Access Fund units, including the Fund. The Fund does not expect to make a repurchase offer that is larger than the portion of FEG Absolute Access Fund’s corresponding repurchase offer expected to be available for acceptance by the Fund. Consequently, the Fund will conduct repurchase offers on a schedule and in amounts that will depend on FEG Absolute Access Fund’s repurchase offers.

Subject to the considerations described above, the aggregate value of Units to be repurchased at any time will be determined by the Board in its sole discretion, and such amount may be stated as a percentage of the value of the Fund’s outstanding Units. Therefore, the Fund may determine not to conduct a repurchase offer at a time that FEG Absolute Access Fund conducts a repurchase offer.

10

FEG Absolute Access Fund I LLC

Notes to Financial Statements (continued)

4. Capital (continued)

The Board also will consider the following factors, among others, in making such determination: (i) whether FEG Absolute Access Fund is making a contemporaneous repurchase offer for FEG Absolute Access Fund units, and the aggregate value of FEG Absolute Access Fund units that FEG Absolute Access Fund is offering to repurchase; (ii) the liquidity of the assets of the applicable fund; (iii) the investment plans and working capital requirements of the applicable fund; (iv) the relative economies of scale with respect to the size of the applicable fund; (v) the history of the applicable fund in repurchasing Units; (vi) the conditions in the securities markets and economic conditions generally; and (vii) the anticipated tax consequences of any proposed repurchases of Units.

The Operating Agreement and the FEG Absolute Access Fund operating agreement each provides that the respective entity will be dissolved if any Member that has submitted a written request, in accordance with the terms of the applicable Operating Agreement, to tender all of such Member’s Units or FEG Absolute Access Fund’s units, as applicable, for repurchase by the applicable fund has not been given the opportunity to so tender within a period of two (2) years after the request (whether in a single repurchase offer or multiple consecutive offers within the two-year period). Such a dissolution of the FEG Absolute Access Fund would likely result in a determination to dissolve the Fund.

When the Board determines that the Fund will offer to repurchase Units (or portions of Units), written notice will be provided to Members that describes the commencement date of the repurchase offer, and specifies the date on which repurchase requests must be received by the Fund (the “Repurchase Request Deadline”).

For Members tendering all of their Units in the Fund, Units will be valued for purposes of determining their repurchase price as of a date approximately 95 days after the Repurchase Request Deadline (the “Full Repurchase Valuation Date”). The amount that a Member who is tendering all of its Units in the Fund may expect to receive on the repurchase of such Member’s Units will be the value of the Member’s capital account determined on the Full Repurchase Valuation Date, and the Fund will generally not make any adjustments for final valuations based on adjustments received from FEG Absolute Access Fund, and the withdrawing Member (if such valuations are adjusted upwards) or the remaining Members (if such valuations are adjusted downwards) will bear the risk of change of any such valuations.

Members who tender a portion of their Units in the Fund (defined as a specific dollar value in their repurchase request), and which portion is accepted for repurchase by the Fund, will receive such specified dollar amount. Within five days of the Repurchase Request Deadline, each Member whose Units have been accepted for repurchase will be given a non-interest bearing, non-transferable promissory note by the Fund entitling the Member to be paid an amount equal to 100% of the unaudited net asset value of such Member’s capital account (or portion thereof) being repurchased, determined as of the Full Repurchase Valuation Date (after giving effect to all allocations to be made as of that date to such Member’s capital account). The note will entitle the Member to be paid within 30 days after the Full Repurchase Valuation Date, or ten business days after the Fund has received at least 90% of the aggregate amount withdrawn by the Fund from its investment in FEG Absolute Access Fund), whichever is later (either such date, a “Payment Date”). Notwithstanding the foregoing, if a Member has requested the repurchase of 90% or more of the Units held by such Member, such Member shall receive (i) a non-interest bearing, non-transferable promissory note, in an amount equal to 90% of the estimated unaudited net asset value of such Member’s capital account (or portion thereof) being repurchased, determined as of the Full Repurchase Valuation Date (after giving effect to all allocations to be made as of that date to such Member’s capital account) (the “Initial Payment”), which will be paid on or prior to the Payment Date; and (ii) a promissory note entitling the holder thereof to the balance of the proceeds, to be paid within 30 days following the completion of the Fund’s next annual audit, which is expected to be completed within 60 days after the end of the Fund’s fiscal year. The note will be held by the Administrator on the Member’s behalf. Upon written request by a Member to the Administrator, the Administrator will mail the note to the Member at the address of the Member as maintained in the books and records of the Fund.

11

FEG Absolute Access Fund I LLC

Notes to Financial Statements (continued)

4. Capital (continued)

In the event that a Member requests a repurchase of a capital account amount that had been contributed to the Fund within 18 months of the date of the most recent repurchase offer, the Board may require payment of a repurchase fee payable to the Fund in an amount equal to 2.00% of the repurchase price. The repurchase fee is intended to compensate the Fund for expenses related to such repurchase. Subscriptions shall be treated on a “first-in, first-out basis.” Otherwise, the Fund does not intend to impose any charges on the repurchase of Units.

If Members request that the Fund repurchase a greater number of Units than the repurchase offer amount as of the Repurchase Request Deadline, as determined by the Board in its complete and absolute discretion, the Fund shall repurchase the Units pursuant to repurchase requests on a pro rata basis, disregarding fractions, according to the portion of the Units requested by each Member to be repurchased as of the Repurchase Request Deadline.

A Member who tenders some but not all of the Member’s Units for repurchase will be required to maintain a minimum capital account balance of $50,000. The Fund reserves the right to reduce the amount to be repurchased from a Member so that the required capital account balance is maintained.

5. Indemnifications

The Fund enters into contracts that contain a variety of indemnifications. The Fund’s maximum exposure under these arrangements is not known. However, the Fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

6. Subsequent Events

The Investment Manager evaluated subsequent events through the date the financial statements were issued, and concluded that, there were no recognized or unrecognized subsequent events that required disclosure in or adjustment to the Fund’s financial statements.

12

FEG Absolute Access Fund I LLC

Company Management

(unaudited)

The identity of the Board Members and brief biographical information as of March 31, 2017 is set forth below. The Company’s Statement of Additional Information includes additional information about the Board Members and is available, without charge, by calling 1-888-268-0333.

|

INDEPENDENT DIRECTORS |

||||

|

Name, Date Of Birth, And Address |

Position(s) Held With The Company |

Term Of Office And Length Of Time Served |

Principal Occupation(s) |

Number Of Portfolios In Fund Complex Overseen By Director |

|

David Clark Hyland |

Director; Chairman of Audit Committee |

Indefinite; Since Inception |

Associate Professor of Finance, Xavier University since 2008; Board of Advisors, Sterling Valuation Group, 2006-present. |

4 |

|

Gregory James Hahn |

Director; Audit Committee Member |

Indefinite; Since Inception |

Chief Investment Officer, Portfolio Manager, Investment Strategy, Winthrop Capital Management, LLC since 2007. |

4 |

|

INTERESTED DIRECTORS AND OFFICERS |

||||

|

Name, Date Of Birth, And Address |

Position(s) Held With The Company |

Term Of Office And Length Of Time Served |

Principal Occupation(s) Other Directorships Held By Director or Officer |

Number Of Portfolios In Fund Complex Overseen By Director Or Officer |

|

Ryan S.Wheeler |

President; Secretary |

Indefinite; Since February 2017 (President) and Inception (Secretary) |

Director of Fund Operations since 2012 and Research Analyst from 2008-2012, Fund Evaluation Group, LLC. |

4 |

|

Mary T. Bascom |

Treasurer |

Indefinite; Since Inception |

Chief Financial Officer since 1999, Fund Evaluation Group, LLC. |

4 |

13

FEG Absolute Access Fund I LLC

Company Management (continued)

(unaudited)

|

INTERESTED DIRECTORS AND OFFICERS (continued) |

||||

|

Name, Date Of Birth, And Address |

Position(s) Held With The Company |

Term Of Office And Length Of Time Served |

Principal Occupation(s) Other Directorships Held By Director or Officer |

Number Of Portfolios In Fund Complex Overseen By Director Or Officer |

|

Julie T. Thomas |

Chief Compliance Officer |

Indefinite; Since December 2016 |

Chief Compliance Officer, Fund Evaluation Group, LLC, since November 2015; Vice President, Deputy Chief Compliance Officer, The Ohio National Life Insurance Company, January 2015-November 2015; Chief Compliance Officer, 2013-2015, Director, Fund Compliance, 2012-2013, Fund Compliance Officer, 2011-2012; Suffolk Capital Management LLC, Fiduciary Capital Management, LLC, Ohio National Investments, Inc., and Ohio National Fund. |

4 |

|

Kevin J. Conroy |

Vice President |

Indefinite; Since August 2016 |

Vice President of Hedged Strategies and Assistant Portfolio Manager since 2014, Senior Analyst of Hedged Strategies, 2012-2014, Analyst of Hedged Strategies, 2011-2012, Fund Evaluation Group, LLC. |

4 |

14

FEG Absolute Access Fund I LLC

Other Information

(unaudited)

Information on Proxy Voting

A description of the policies and procedures that the Company uses to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-888-268-0333. It is also available on the SEC’s website at http://www.sec.gov.

Information regarding how the Company voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge, upon request, by calling 1-888-268-0333, and on the SEC’s website at http://www.sec.gov.

Availability of Quarterly Report Schedule

The Company files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Company’s Forms N-Q are available on the SEC’s website at http://www.sec.gov. The Company’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

Approval of Investment Management and Sub-Advisory Agreements

At a meeting of the Board of the Fund and the FEG Absolute Access Fund Board (together, the “Board”) held on February 21, 2017, by a unanimous vote, the FEG Absolute Access Fund Board, including a majority of the Directors who are not “interested persons” within the meaning of Section 2(a)(19) of the 1940 Act (the “Independent Directors”), approved the continuation of the investment management agreement (the “Investment Management Agreement”) between the Investment Manager and FEG Absolute Access Fund and the sub-advisory agreement among the Investment Manager, Sub-Adviser and FEG Absolute Access Fund (the “Sub-Advisory Agreement”, and together with the Investment Management Agreement, the “Advisory Agreements”).

In advance of the meeting, the Directors requested and received extensive materials from the Investment Manager and Sub-Adviser to assist them in considering the approval of the Advisory Agreements. The materials provided by the Investment Manager and Sub-Adviser contained information including detailed comparative information relating to the performance, advisory fees and other expenses of the FEG Absolute Access Fund and the Fund (together, the “Funds”).

The Board engaged in a detailed discussion of the materials with management of the Investment Manager and Sub-Adviser. The Board then met in executive session with the counsel to the Independent Directors for a full review of the materials. Following this session, the meeting reconvened and after further discussion the Board determined that the information presented provided a sufficient basis upon which to approve the Advisory Agreements.

Discussion of Factors Considered

The Board considered, among other things: (1) the nature and quality of the advisory services rendered, including, the complexity of the services provided; (2) the experience and qualifications of the personnel providing such services; (3) the fee structure and the expense ratios in relation to those of other investment companies having comparable investment policies and limitations; (4) the direct and indirect costs that may be incurred by the Investment Manager, the Sub-Adviser and their affiliates in performing advisory services for the Funds, the basis of determining and allocating these costs, and the estimated profitability to the Investment Manager and its affiliates in performing such services; (5) possible economies of scale arising from any anticipated growth of the Funds and the extent to which these would be passed on to the Funds; (6) other compensation or possible benefits to the Investment Manager, the Sub-Adviser and their affiliates arising from their advisory and other relationships with the Funds; (7) possible alternative fee structures or bases for determining fees; (8) the fees charged by the Investment Manager and other investment managers to similar clients and in comparison to industry fees for similar services; (9) the allocation of total fees between the Investment

15

FEG Absolute Access Fund I LLC

Other Information (continued)

(unaudited)

Manager and the Sub-Adviser with respect to FEG Absolute Access Fund; and (10) possible conflicts of interest that the Investment Manager and the Sub-Adviser may have with respect to the Funds. It was noted that the Sub-Adviser does not perform similar services for other clients.

The Board concluded that the nature, extent and quality of the services to be provided by the Investment Manager and the Sub-Adviser to the Funds are appropriate and consistent with the terms of the Funds’ Amended and Restated Limited Liability Company Operating Agreements, that the quality of those services are anticipated to be consistent with industry norms and that the Funds are likely to benefit from the Investment Manager’s and the Sub-Adviser’s management of the Funds’ investment program.

The Board noted FEG Absolute Access Fund’s outperformance when compared against its benchmark for the 1-, 3-, 5- and 7-year time periods.

The Board also concluded that the Investment Manager and the Sub-Adviser had sufficient personnel, with the appropriate education and experience, to serve the Funds effectively and have demonstrated their continuing ability to attract and retain qualified personnel.

The Board considered the anticipated costs of the services provided by the Investment Manager, and the compensation and benefits received by the Investment Manager in providing services to the Funds. The Board reviewed the financial statements of the Investment Manager. In addition, the Board considered any direct or indirect revenues which may be received by the Investment Manager, the Sub-Adviser and their affiliates. The Board concluded that the Investment Manager’s anticipated fees and profits to be derived from its relationship with the Funds in light of the Funds’ expenses, were reasonable in relation to the nature and quality of the services provided, taking into account the fees charged by other investment managers for managing comparable funds. The Board also considered that the subadvisory fee received by InterOcean reflected the overall value of services provided to the Funds and to the Investment Manager, generally. The Board also concluded that the overall expense ratios of the Funds were reasonable, taking into account the projected size of the Funds and the quality of services provided by the Investment Manager.

The Board considered the extent to which economies of scale were expected to be realized relative to fee levels as the Funds’ assets grow.

The Board considered all factors and no one factor alone was deemed dispositive. After further discussion the Board determined that the information presented provided a sufficient basis upon which to approve the Management Agreement and Sub-Advisory Agreement.

Conclusion

After receiving full disclosure of relevant information of the type described above, the Board concluded that the compensation and other terms of the Advisory Agreements were in the best interests of the Funds’ Members.

16

FEG Absolute Access Fund I LLC

Privacy Policy

(unaudited)

In the course of doing business with shareholders, FEG Absolute Access Fund LLC (the “Fund”) collects nonpublic personal information about shareholders. “Nonpublic personal information” is personally identifiable financial information about shareholders. For example, it includes shareholders’ social security number, account balance, bank account information, and purchase and redemption history.

The Fund collects this information from the following sources:

|

● |

Information it receives from shareholders on applications or other forms; |

|

● |

Information about shareholder transactions with the Fund and its service providers, or others; |

|

● |

Information it receives from consumer reporting agencies (including credit bureaus). |

What information does the Fund disclose and to whom does the Fund disclose information?

The Fund only discloses nonpublic personal information collected about shareholders as permitted by law. For example, the Fund may disclose nonpublic personal information about shareholders:

|

● |

To government entities, in response to subpoenas or to comply with laws or regulations. |

|

● |

When shareholders direct the Fund to do so or consent to the disclosure. |

|

● |

To companies that perform necessary services for the Fund, such as data processing companies that the Fund uses to process shareholders transactions or maintain shareholder accounts. |

|

● |

To protect against fraud, or to collect unpaid debts. |

|

● |

Information about former shareholders. |

If a shareholder closes its account, the Fund will adhere to the privacy policies and practices described in this notice.

How the Fund safeguards information

Within the Fund, access to nonpublic personal information about shareholders is limited to employees and in some cases to third parties (for example, the service providers described above), as permitted by law. The Fund and its service providers maintain physical, electronic, and procedural safeguards that comply with federal standards to guard shareholder nonpublic personal information.

17

|

|

FINANCIAL STATEMENTS

|

|

|

FEG Absolute Access Fund LLC

Year Ended March 31, 2017 With Report of Independent Registered Public Accounting Firm |

|

Report of Independent Registered Public Accounting Firm

|

1

|

|

Statement of Assets, Liabilities and Members’ Capital

|

2

|

|

Schedule of Investments

|

3

|

|

Statement of Operations

|

6

|

|

Statements of Changes in Members’ Capital

|

7

|

|

Statement of Cash Flows

|

8

|

|

Financial Highlights

|

9

|

|

Notes to Financial Statements

|

10

|

|

Other Information (Unaudited)

|

|

|

Company Management

|

17

|

|

Other Information

|

19

|

|

Privacy Policy

|

21

|

|

|

|

|

Assets

|

||||

|

Cash

|

$

|

1,231,821

|

||

|

Short-term investments (cost $7,757,870)

|

7,757,870

|

|||

|

Investments in Portfolio Funds, at fair value (cost $325,980,150)

|

370,096,868

|

|||

|

Receivable for Portfolio Funds sold

|

3,233,781

|

|||

|

Prepaid expenses and other assets

|

12,726

|

|||

|

Total assets

|

$

|

382,333,066

|

||

|

Liabilities and members’ capital

|

||||

|

Capital withdrawals payable

|

$

|

957,700

|

||

|

Management fee payable

|

540,292

|

|||

|

Professional fees payable

|

140,395

|

|||

|

Accounting and administration fees payable

|

90,141

|

|||

|

Directors fees payable

|

6,000

|

|||

|

Line of credit fees payable

|

4,444

|

|||

|

Other liabilities

|

38,053

|

|||

|

Total liabilities

|

1,777,025

|

|||

|

Members’ capital

|

380,556,041

|

|||

|

Total liabilities and members’ capital

|

$

|

382,333,066

|

||

|

Components of members’ capital

|

||||

|

Paid-in capital

|

$

|

314,479,005

|

||

|

Accumulated net investment loss

|

(22,016,596

|

)

|

||

|

Accumulated net realized gain on investments

|

43,976,914

|

|||

|

Accumulated net unrealized appreciation on investments

|

44,116,718

|

|||

|

Members’ capital

|

$

|

380,556,041

|

||

|

Units issued and outstanding (unlimited units authorized)

|

293,807

|

|||

|

Net Asset Value per unit

|

$

|

1,295.26

|

||

|

Investment Name

|

Cost

|

Fair

Value |

Percentage of

Members’ Capital

|

Withdrawals

Permitted (1)

|

Notice

Period (1) |

||||||||||

|

Investments in Portfolio Funds: (2)

|

|||||||||||||||

|

United States:

|

|||||||||||||||

|

Multi-Strategy: (3)

|

|||||||||||||||

|

AG Super Fund, L.P.

|

$

|

577,426

|

$

|

799,121

|

0.2

|

%

|

Annually (5)

|

60 days

|

|||||||

|

Canyon Balanced Fund, L.P.

|

19,642,801

|

20,462,294

|

5.4

|

Quarterly (6)

|

90 days

|

||||||||||

|

Claren Road Credit Partners, L.P.

|

1,704,952

|

1,545,220

|

0.4

|

Quarterly (5)

|

45 days

|

||||||||||

|

CVI Global Value Fund A, L.P., Class H(4)

|

466,718

|

1,396,444

|

0.4

|

Quarterly (7)

|

120 days

|

||||||||||

|

Eton Park Fund, L.P., Class B(4)

|

19,227,946

|

22,117,933

|

5.8

|

Quarterly

|

65 days

|

||||||||||

|

Farallon Capital Partners, L.P.(4)

|

18,060,570

|

23,640,000

|

6.2

|

Annually (5)

|

45 days

|

||||||||||

|

Fir Tree Capital Opportunity Fund, L.P.

|

17,850,400

|

23,673,004

|

6.2

|

Annually (5)

|

90 days

|

||||||||||

|

Governors Lane Onshore Fund L.P.

|

14,000,000

|

14,984,589

|

3.9

|

Annually (5)

|

65 days

|

||||||||||

|

GSO Special Situations Fund, L.P.

|

166,240

|

314,844

|

0.1

|

Semi-Annually (5)

|

90 days

|

||||||||||

|

HBK Multi-Strategy Fund, L.P., Class A

|

13,497,263

|

18,895,556

|

5.0

|

Quarterly

|

90 days

|

||||||||||

|

Highfields Capital II, L.P.

|

115,532

|

113,992

|

0.0

|

Annually (7)

|

60 days

|

||||||||||

|

Kepos Alpha Fund, L.P., Class A

|

18,550,000

|

17,417,683

|

4.6

|

Quarterly (8)

|

65 days

|

||||||||||

|

LibreMax SL Fund, L.P.

|

1,486,988

|

1,820,635

|

0.5

|

Not Permitted

|

N/A

|

||||||||||

|

MKP Enhanced Opportunity Partners, L.P.

|

13,500,000

|

14,442,490

|

3.8

|

Monthly

|

60 days

|

||||||||||

|

OZ Asia Domestic Partners, L.P.

|

17,250,000

|

21,650,617

|

5.7

|

Quarterly (9)

|

45 days

|

||||||||||

|

Rimrock High Income PLUS (QP) Fund, L.P.

|

20,000,000

|

21,984,140

|

5.8

|

Annually (7)

|

120 days

|

||||||||||

|

Stark Investments, L.P. (4)

|

2,883

|

796

|

0.0

|

Quarterly

|

N/A

|

||||||||||

|

Stark Investments, L.P., Class A (4)(10)

|

132,816

|

137,128

|

0.0

|

Quarterly

|

N/A

|

||||||||||

|

Stark Investments, L.P., Class B (4)(11)

|

4,746

|

5,532

|

0.0

|

Quarterly

|

N/A

|

||||||||||

|

Strategic Value Restructuring Fund, L.P., Class C

|

12,530,860

|

15,614,839

|

4.1

|

Annually (5)

|

95 days

|

||||||||||

|

Taconic Opportunity Fund, L.P.

|

4,187,617

|

5,179,765

|

1.3

|

Quarterly

|

60 days

|

||||||||||

|

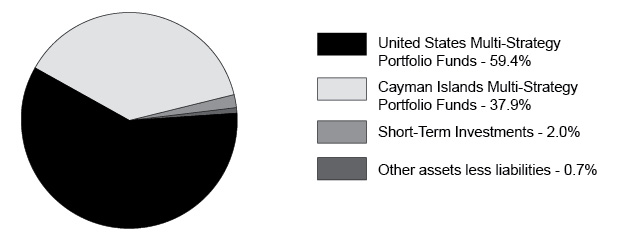

Total United States

|

192,955,758

|

226,196,622

|

59.4

|

||||||||||||

|

Cayman Islands:

|

|||||||||||||||

|

Multi-Strategy: (3)

|

|||||||||||||||

|

Caxton Global Investments Limited, Class T Unrestricted

|

18,800,000

|

18,922,885

|

5.0

|

Quarterly

|

45 days

|

||||||||||

|

Coastland Relative Value Fund, LLC - Series B

|

16,000,000

|

14,713,497

|

3.8

|

Quarterly

|

60 days

|

||||||||||

|

Elliott International Limited

|

25,928,845

|

30,720,155

|

8.1

|

Semi-Annually (7)

|

60 days

|

||||||||||

|

Eton Park Overseas Fund, Ltd.(4)

|

1,960,350

|

2,408,723

|

0.6

|

Annually (5)

|

65 days

|

||||||||||

|

Graham Global Investment Fund II SPC, Ltd.

|

13,640,529

|

11,702,206

|

3.1

|

Monthly

|

3 days

|

||||||||||

|

Highfields Capital, Ltd.(4)

|

19,194,668

|

22,713,108

|

6.0

|

Annually (7)(12)

|

60 days

|

||||||||||

|

Indaba Capital Partners (Cayman), LP

|

23,000,000

|

26,131,141

|

6.9

|

Quarterly

|

90 days

|

||||||||||

|

Systematica Alternative Markets Fund Limited

|

14,500,000

|

16,588,531

|

4.4

|

Monthly (5)

|

30 days

|

||||||||||

|

Total Cayman Islands

|

133,024,392

|

143,900,246

|

37.9

|

||||||||||||

|

Total investments in Portfolio Funds

|

325,980,150

|

370,096,868

|

97.3

|

||||||||||||

|

Investment Name

|

Cost

|

Fair

Value |

Percentage of

Members’ Capital

|

|||||||||

|

Short-term investments:

|

||||||||||||

|

United States:

|

||||||||||||

|

Money market fund:

|

||||||||||||

|

Federated Goverment Obligations Fund #5, 0.58% (13)

|

$

|

5,472,009

|

$

|

5,472,009

|

1.4

|

%

|

||||||

|

Fidelity Investments Money Market Government Portfolio - Institutional Class, 0.60% (13)

|

2,285,861

|

2,285,861

|

0.6

|

|||||||||

|

Total short-term investments

|

7,757,870

|

7,757,870

|

2.0

|

|||||||||

|

Total investments in Portfolio Funds and short-term investments

|

$

|

333,738,020

|

377,854,738

|

99.3

|

||||||||

|

Other assets less liabilities

|

2,701,303

|

0.7

|

||||||||||

|

Members’ capital

|

$

|

380,556,041

|

100.0

|

%

|

||||||||

|

(1)

|

Redemption frequency and redemption notice period reflect general redemption terms, and exclude liquidity restrictions.

|

|

(2)

|

Non-income producing.

|

|

(3)

|

Absolute return managers, while often investing in the same asset classes as traditional investment managers, do so in a market neutral framework that attempts to arbitrage pricing discrepancies or other anomalies that are unrelated to general market moves. Absolute return strategies are designed to reduce exposure to the market risks that define the broad asset classes and therefore should be viewed as a separate absolute return or diversifying strategy category for asset allocation purposes. An allocation to absolute return strategies can add a potentially valuable element of diversification to a portfolio of traditional investments and can be used by investors as a way to manage the total market risk of their portfolios. Examples of individual strategies that generally fall into this absolute return category include merger arbitrage, fixed income arbitrage, equity market neutral, convertible arbitrage, relative value arbitrage, and other event-driven strategies.

|

|

(4)

|

All or a portion of these investments are held in side-pockets. Such investments generally cannot be withdrawn until removed from the side-pocket, the timing of which cannot be determined. See Note 2 for a discussion of the Fund's investments in side pockets.

|

|

(5)

|

Withdrawals from these Portfolio Funds are permitted after a one-year lockup period from the date of the initial investment.

|

|

(6)

|

Withdrawals from this Portfolio Fund are permitted on a quarterly basis, with 25%, 33 ⅓E%, 50%, and 100% of the total investment becoming eligible for redemption each successive quarter.

|

|

(7)

|

Withdrawals from these Portfolio Funds are permitted after a two-year lockup period from the date of the initial investment.

|

|

(8)

|

In addition to quarterly withdrawals, monthly withdrawals are also permitted from this Portfolio Fund at a limited amount of 33% of the net asset value held by a shareholder subject to a 0.20% redemption fee on the proceeds.

|

|

(9)

|

Withdrawals from this Portfolio Fund are permitted after a one-year and a quarter lockup period from the date of the initial investment.

|

|

(10)

|

Does not include holdback at cost of $147,718, included in receivable for Portfolio Funds sold in the Statement of Assets, Liabilities and Members' Capital.

|

|

(11)

|

Does not include holdback at cost of $3,197, included in receivable for Portfolio Funds sold in the Statement of Assets, Liabilities and Members' Capital.

|

|

(12)

|

In addition to annual withdrawals, semi-annual withdrawals are also permitted from this Portfolio Fund at a limited amount of 25% of the net asset value held by a shareholder.

|

|

(13)

|

The rate shown is the annualized 7-day yield as of March 31, 2017.

|

|

Investment income

|

||||

|

Dividend income

|

$

|

47,410

|

||

|

Expenses

|

||||

|

Management fees

|

3,273,299

|

|||

|

Accounting and administration fees

|

347,196

|

|||

|

Professional fees

|

183,827

|

|||

|

Line of credit fees

|

102,241

|

|||

|

Custodian fees

|

40,296

|

|||

|

Directors fees

|

24,000

|

|||

|

Insurance expenses

|

10,710

|

|||

|

Line of credit interest expense

|

5,590

|

|||

|

Other expenses

|

81,621

|

|||

|

Total expenses

|

4,068,780

|

|||

|

Net investment loss

|

(4,021,370

|

)

|

||

|

Realized and unrealized gain on investments

|

||||

|

Net realized gain on investments

|

6,129,817

|

|||

|

Net change in unrealized appreciation/depreciation on investments

|

16,311,181

|

|||

|

Net realized and unrealized gain on investments

|

22,440,998

|

|||

|

Net increase in members' capital resulting from operations

|

$

|

18,419,628

|

||

|

Year Ended

March 31, 2017 |

Year Ended

March 31, 2016 |

|||||||

|

Operations

|

||||||||

|

Net investment loss

|

$

|

(4,021,370

|

)

|

$

|

(4,183,378

|

)

|

||

|

Net realized gain (loss) on investments

|

6,129,817

|

(1,505,465

|

)

|

|||||

|

Net change in unrealized appreciation/depreciation on investments

|

16,311,181

|

(11,589,153

|

)

|

|||||

|

Net change in members' capital resulting from operations

|

18,419,628

|

(17,277,996

|

)

|

|||||

|

Capital transactions

|

||||||||

|

Capital contributions

|

27,289,847

|

59,737,509

|

||||||

|

Capital withdrawals

|

(50,629,729

|

)

|

(55,190,017

|

)

|

||||

|

Net change in members' capital resulting from capital transactions

|

(23,339,882

|

)

|

4,547,492

|

|||||

|

Net change in members' capital

|

(4,920,254

|

)

|

(12,730,504

|

)

|

||||

|

Members' capital at beginning of year

|

385,476,295

|

398,206,799

|

||||||

|

Members' capital at end of year

|

$

|

380,556,041

|

$

|

385,476,295

|

||||

|

Accumulated net investment loss

|

$

|

(22,016,596

|

)

|

$

|

(17,995,226

|

)

|

||

|

Units transactions

|

||||||||

|

Units sold

|

21,313

|

46,606

|

||||||

|

Units redeemed

|

(39,829

|

)

|

(43,674

|

)

|

||||

|

Net change in units

|

(18,516

|

)

|

2,932

|

|||||

|

Operating activities

|

||||

|

Net increase in members’ capital resulting from operations

|

$

|

18,419,628

|

||

|

Adjustments to reconcile net increase in members’ capital resulting from operations to net cash provided by operating activities:

|

||||

|

Purchases of investments in Portfolio Funds

|

(24,000,000

|

)

|

||

|

Proceeds from sales of investments in Portfolio Funds

|

56,003,457

|

|||

|

Net realized gain on investments

|

(6,129,817

|

)

|

||

|

Net change in unrealized appreciation/depreciation on investments

|

(16,311,181

|

)

|

||

|

Purchases of short-term investments, net

|

(4,666,842

|

)

|

||

|

Changes in operating assets and liabilities:

|

||||

|

Prepaid expenses and other assets

|

(11,937

|

)

|

||

|

Management fee payable

|

(5,991

|

)

|

||

|

Professional fees payable

|

31,994

|

|||

|

Accounting and administration fees payable

|

(1,123

|

)

|

||

|

Other liabilities

|

2,900

|

|||

|

Net cash provided by operating activities

|

23,331,088

|

|||

|

Financing activities

|

||||

|

Proceeds from line of credit

|

5,000,000

|

|||

|

Payments for line of credit

|

(5,000,000

|

)

|

||

|

Line of credit fees payable

|

1,880

|

|||

|

Proceeds from capital contributions

|

26,539,847

|

|||

|

Payments for capital withdrawals

|

(51,320,145

|

)

|

||

|

Net cash used in financing activities

|

(24,778,418

|

)

|

||

|

Net change in cash

|

(1,447,330

|

)

|

||

|

Cash at beginning of year

|

2,679,151

|

|||

|

Cash at end of year

|

$

|

1,231,821

|

||

|

Supplemental disclosure of interest paid

|

$

|

5,590

|

||

|

Year Ended March 31,

|

||||||||||||||||

|

2017

|

2016

|

2015

|

2014

|

|||||||||||||

|

Per unit operating performances: (1)(2)

|

||||||||||||||||

|

Net asset value per unit, beginning of year

|

$

|

1,234.22

|

$

|

1,287.07

|

$

|

1,225.97

|

$

|

1,141.52

|

||||||||

|

Income (loss) from investment operations:

|

||||||||||||||||

|

Net investment loss

|

(17.32

|

)

|

(12.98

|

)

|

(4.81

|

)

|

(3.84

|

)

|

||||||||

|

Net realized and unrealized gain (loss) on investments

|

78.36

|

(39.87

|

)

|

65.91

|

88.29

|

|||||||||||

|

Total change in per unit value from investment operations

|

61.04

|

(52.85

|

)

|

61.10

|

84.45

|

|||||||||||

|

Net asset value per unit, end of year

|

$

|

1,295.26

|

$

|

1,234.22

|

$

|

1,287.07

|

$

|

1,225.97

|

||||||||

|

Year Ended March 31,

|

||||||||||||||||||||

|

2017

|

2016

|

2015

|

2014

|

2013

|

||||||||||||||||

|

Ratios to average members' capital: (3)

|

||||||||||||||||||||

|

Total expenses

|

1.07

|

%

|

1.06

|

%

|

1.06

|

%

|

1.12

|

%

|

1.21

|

%

|

||||||||||

|

Net investment loss

|

(1.05

|

)%

|

(1.04

|

)%

|

(1.06

|

)%

|

(1.12

|

)%

|

(1.21

|

)%

|

||||||||||

|

Total return

|

4.95

|

%

|

(4.11

|

)%

|

4.98

|

%

|

7.40

|

%

|

8.26

|

%

|

||||||||||

|

Portfolio turnover

|

6.43

|

%

|

12.33

|

%

|

28.75

|

%

|

17.93

|

%

|

7.96

|

%

|

||||||||||

|

Members’ capital end of year (000's)

|

$

|

380,556

|

$

|

385,476

|

$

|

398,207

|

$

|

314,170

|

$

|

232,230

|

||||||||||

|

(1)

|

Selected data is for a single unit outstanding throughout the year.

|

|

(2)

|

Effective April 1, 2013, the Company was unitized.

|

|

(3)

|

The ratios do not include investment income or expenses of the Portfolio Funds in which the Company invests.

|

|

Investments

|

Level 1

|

Level 2

|

Level 3

|

Total

|

||||||||||||

|

Short-term investments

|

$

|

7,757,870

|

$

|

—

|

$

|

—

|

$

|

7,757,870

|

||||||||

|

Total

|

$

|

7,757,870

|

$

|

—

|

$

|

—

|

$

|

7,757,870

|

||||||||

(unaudited)

|

INDEPENDENT DIRECTORS

|

||||

|

Name, Date Of Birth,

And Address

|

Position(s) Held

With The Company

|

Term Of Office

And Length Of

Time Served

|

Principal Occupation(s)

During Past 5 Years And Other

Directorships Held By Director

|

Number Of Portfolios

In Fund Complex

Overseen By

Director

|

|

David Clark Hyland

August 13, 1963 6596 Madeira Hills Drive, Cincinnati, OH 45243 |

Director; Chairman of Audit Committee

|

Indefinite; Since Inception

|

Associate Professor of Finance, Xavier University since 2008; Board of Advisors, Sterling Valuation Group, 2006-present.

|

4

|

|

Gregory James Hahn

January 23, 1961 2565 Durbin Drive, Carmel, IN 46032 |

Director; Audit Committee Member

|

Indefinite; Since Inception

|

Chief Investment Officer, Portfolio Manager, Investment Strategy, Winthrop Capital Management, LLC since 2007.

|

4

|

|

INTERESTED DIRECTORS AND OFFICERS

|

||||

|

Name, Date Of Birth,

And Address

|

Position(s) Held

With The Company

|

Term Of Office

And Length Of

Time Served

|

Principal Occupation(s)

During Past 5 Years And Other

Directorships Held By Director Or Officer

|

Number Of Portfolios

In Fund Complex

Overseen By

Director Or Officer

|

|

Ryan S. Wheeler

February 6, 1979 c/o Fund Evaluation Group, LLC 201 E. Fifth St., Suite 1600, Cincinnati, OH 45202 |

President; Secretary

|

Indefinite; Since February 2017 (President) and Inception (Secretary)

|

Director of Fund Operations since 2012 and Research Analyst from 2008-2012, Fund Evaluation Group, LLC.

|

4

|

|

Mary T. Bascom

April 24, 1958 c/o Fund Evaluation Group, LLC 201 E. Fifth St., Suite 1600, Cincinnati, OH 45202 |

Treasurer

|

Indefinite; Since Inception

|

Chief Financial Officer, since 1999, Fund Evaluation Group, LLC.

|

4

|

(unaudited)

|

INTERESTED DIRECTORS AND OFFICERS (continued)

|

||||

|

Name, Date Of Birth, And Address

|

Position(s) Held With The Company

|

Term Of Office And Length Of Time Served

|

Principal Occupation(s) During Past 5 Years And Other Directorships Held By Director Or Officer

|

Number Of Portfolios

In Fund Complex

Overseen By

Director Or Officer

|

|

Julie T. Thomas

July 10, 1962 c/o Fund Evaluation Group, LLC 201 E. Fifth St., Suite 1600, Cincinnati, OH 45202 |

Chief Compliance Officer

|

Indefinite; Since December 2016

|

Chief Compliance Officer, Fund Evaluation Group, LLC, since November 2015; Vice President, Deputy Chief Compliance Officer, The Ohio National Life Insurance Company, January 2015-November 2015; Chief Compliance Officer, 2013-2015, Director, Fund Compliance, 2012-2013, Fund Compliance Officer, 2011-2012; Suffolk Capital Management LLC, Fiduciary Capital Management, LLC, Ohio National Investments, Inc., and Ohio National Fund.

|

4

|

|

Kevin J. Conroy

December 14, 1977 c/o Fund Evaluation Group, LLC 201 E. Fifth St., Suite 1600, Cincinnati, OH 45202 |

Vice President

|

Indefinite; Since August 2016

|

Vice President of Hedged Strategies and Assistant Portfolio Manager since 2014, Senior Analyst of Hedged Strategies, 2012-2014, Analyst of Hedged Strategies, 2011-2012, Fund Evaluation Group, LLC.

|

4

|

(unaudited)

(unaudited)

(unaudited)

|

●

|

Information it receives from shareholders on applications or other forms;

|

|

●

|

Information about shareholder transactions with the Fund and its service providers, or others;

|

|

●

|

Information it receives from consumer reporting agencies (including credit bureaus).

|

|

●

|

To government entities, in response to subpoenas or to comply with laws or regulations.

|

|

●

|

When shareholders direct the Fund to do so or consent to the disclosure.

|

|

●

|

To companies that perform necessary services for the Fund, such as data processing companies that the Fund uses to process shareholders transactions or maintain shareholder accounts.

|

|

●

|

To protect against fraud, or to collect unpaid debts.

|

|

●

|

Information about former shareholders.

|

| (a) |

Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the report to shareholders filed under Item 1 of this form.

|

| 1. |

Records of proxy statements received regarding client securities;

|

| 2. |

Records of each vote cast by the Firm on behalf of a client;

|

| 3. |

Copies of any document created by the Firm that was material to making a decision on voting clients’ securities;

|

| 4. |

Records of all communications received and internal documents created that were material to the voting decision; and

|

| 5. |

Each written client request for proxy voting information and the Firm’s written response to such client request (written or oral) for proxy voting information.

|

| 6. |

Documentation noting the rationale behind each proxy vote decision made.

|

| · |

The Firm receives increased compensation as a result of the proxy vote due to increased or additional fees or other charges to be paid by the client.

|