UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

| x | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended December 31, 2015 |

OR

| o | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the transition period from to |

Commission File Number 001-36216

IDEAL POWER INC.

(Exact name of registrant as specified in its charter)

| DELAWARE | 14-1999058 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

4120 Freidrich Lane,

Suite 100

Austin, Texas 78744

(Address of principal executive offices)

(Zip Code)

(512) 264-1542

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which each is registered | |

| Common Stock, par value $0.001 | NASDAQ Capital Market |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

| Large accelerated filer o | Accelerated filer o | |

| Non-accelerated filer o | Smaller reporting company x | |

| (Do not check if a smaller reporting company) | ||

Indicate by check mark whether the issuer is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter.

As of June 30, 2015, the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the last sale price of the common equity was $51,870,059.

As of March 23, 2016 the issuer has 9,557,747 shares of common stock, par value $0.001, issued and outstanding.

TABLE OF CONTENTS

2

SPECIAL NOTE REGARDING

FORWARD-LOOKING STATEMENTS AND

OTHER INFORMATION CONTAINED IN THIS REPORT

This report contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and the provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements give our current expectations or forecasts of future events. You can identify these statements by the fact that they do not relate strictly to historical or current facts. You can find many (but not all) of these statements by looking for words such as “approximates,” “believes,” “hopes,” “expects,” “anticipates,” “estimates,” “projects,” “intends,” “plans,” “would,” “should,” “could,” “may,” or other similar expressions in this report. In particular, these include statements relating to future actions, prospective products, applications, customers, technologies, future performance or results of anticipated products, expenses, and financial results. These forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our historical experience and our present expectations or projections. Factors that could cause actual results to differ from those discussed in the forward-looking statements include, but are not limited to:

| • | our history of losses; |

| • | our ability to achieve profitability; |

| • | our limited operating history; |

| • | emerging competition and rapidly advancing technology in our industry that may outpace our technology; |

| • | customer demand for the products and services we develop; |

| • | the impact of competitive or alternative products, technologies and pricing; | |

| • | The timing of growth, and the growth rate of, the less mature markets we have entered or may enter in the future; |

| • | our ability to have any products we develop manufactured; | |

| • | the adequacy of protections afforded to us by the patents that we own and the cost to us of maintaining, enforcing and defending those patents; | |

| • | our ability to obtain, expand and maintain patent protection in the future, and to protect our non-patented intellectual property; | |

| • | our exposure to and ability to defend third-party claims and challenges to our patents and other intellectual property rights; |

| • | general economic conditions and events and the impact they may have on us and our potential customers; |

| • | our ability to obtain adequate financing in the future, as and when we need it; |

| • | our success at managing the risks involved in the foregoing items; and |

| • | other factors discussed in this report. |

The forward-looking statements are based upon management’s beliefs and assumptions and are made as of the date of this report. We undertake no obligation to publicly update or revise any forward-looking statements included in this report. You should not place undue reliance on these forward-looking statements.

3

| ITEM 1: | BUSINESS |

Our Company

Ideal Power Inc. was formed in Texas on May 17, 2007 and converted to a Delaware corporation on July 15, 2013. Unless otherwise stated or the context otherwise requires, the terms “Ideal Power,” “we,” “us,” “our” and the “Company” refer to Ideal Power Inc.

We design, market and sell electrical power conversion products using our proprietary technology called Power Packet Switching Architecture (“PPSA”). PPSA is a power conversion technology that improves upon existing power conversion technologies in key product metrics, such as size, weight, cost, and efficiency. PPSA utilizes standardized hardware with application specific embedded software. Our advanced technology is important to our business and we make significant investments in research and development and protection of our intellectual property. At December 31, 2015, we have been granted 36 United States, three European, one Chinese and two other foreign patents.

We sell our products primarily to systems integrators for integration into their larger turn-key system which enable end users to manage their electricity consumption by reducing demand charges or fossil fuel consumption, integrating renewable energy sources and/or form their own microgrid. Our products are made by contract manufacturers to our specifications, enabling us to scale production to meet demand on a cost-effective basis without requiring significant expenditures on manufacturing facilities and equipment. As our products gain broader acceptance in the power conversion market, we intend to license our proprietary PPSA-based product designs to OEMs within our target markets, as well as license our technologies for other markets which we do not plan to enter directly.

Industry Background

Utility power grids are built using AC generation, transmission, and distribution resources. This method of power transmission and distribution has been proven over time to be reliable and safe. The outlets in a typical home or business are AC but many electrical devices, such as computers, televisions, and other appliances operate on DC power. Batteries and PV solar panels produce DC power as well. In order to connect DC devices to an AC power grid, a power conversion device is necessary.

We believe that significant changes in the supply of and demand for electrical power are driving demand for new energy infrastructure products and supporting technologies. In a traditional utility model, electrical power is generated from central stations and transmitted over long distance high-voltage transmission lines to substations where the voltage is reduced for distribution to consumers. Utility power grids are built to manage the flow of power in one direction, from generation to use, where sophisticated tools have been developed to match the amount of power being generated with the amount being consumed. Utilities ramp power plants up or down to closely match generation with load.

The rapid growth in worldwide renewable energy generation, such as wind and solar power, has added a new level of complexity to the task of matching power generation with consumption. These intermittent resources cannot be dispatched at will or relied upon to meet the peak power demands of the grid. Renewable energy sources tend to ramp up and down quickly. For example, a single cloud over a photovoltaic, or PV, farm can cause electrical output to change dramatically in a matter of seconds. These new challenges make it increasingly difficult for utilities to accurately forecast and meet peak power demands.

Increased peak demand for power also has exposed weaknesses in the existing power grid. In high-cost, high-demand states, such as California, public utilities have instituted peak demand charges as a way to ration power during periods of peak demand and to incentivize customers to shift their power consumption to off-peak times. At the same time, both the Federal and certain state governments have created incentive programs to encourage the development and implementation of alternative energy sources, such as solar and wind power, which has the perverse consequence of making peak demand more difficult to forecast and satisfy. Strains on the electric grid have resulted in significant brown-outs and black-outs that have heightened awareness of the vulnerabilities of the existing system. As a result, power consumers are turning to new technologies to manage their energy consumption, lower costs and assure a reliable source of supply. We believe that distributed generation with advanced power conversion systems, such as our PPSA products, has become an increasingly important element of this new infrastructure.

In response to these changes in the market for electrical power, a number of technologies have been developed to enable users to more effectively manage their consumption and, one of these technologies, energy storage systems, has emerged as the best way to mitigate the instabilities and market inefficiencies caused by these emerging power grid realities. For example, a commercial business can shift energy usage from peak to non-peak times by installing a battery energy storage system, or BESS. The commercial business can use electricity generated during off-peak hours to charge the BESS and then use the stored power to satisfy all or part of its demand during peak hours. Similarly, a commercial business can install a solar power system to generate power for use either immediately upon generation or for storage in a BESS for later use.

Battery energy storage systems and many alternative energy sources provide power on a direct current, or DC, basis. However, the electric power grid and most electrical equipment operates on an alternating current, or AC, basis. Consequently, power conversion systems are required to convert power from DC to AC or from AC or DC as necessary to make the various components of the system function together. In addition to converting power, power conversion systems enable customers to regulate current, voltage and frequency while optimizing system resources such as batteries, PV and the utility power grid to reduce energy costs. Systems incorporating advanced power converters may also manage distributed grid energy storage and be used to create stand-alone microgrids to bring power to a business or residence if the main electrical grid, if one is present, is unavailable.

4

BESS and alternative energy sources, such as solar or wind power, can only be connected to the existing power grid if they are electrically isolated to prevent power from flowing back into the grid and potentially damaging components of the power system or creating potential safety hazards. Traditionally, power conversion systems have been paired with heavy, wire-wound transformers to provide this isolation and thereby protect the grid. Additionally, power conversion systems based on traditional power conversion technologies use many other passive components which make them big, heavy, expensive and inefficient due to the large quantity of copper and magnetic material and hard-switching topologies. Transformer-less power conversion systems in battery applications on the other hand still require bulky transformers if connected from the grid and thus have many of the same drawbacks as transformer-based systems. Consequently, power conversion systems with transformers are relatively large, expensive to manufacture, ship and install and require larger spaces for installation and heat dissipation.

Our Technology

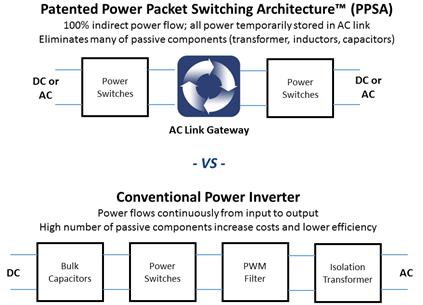

We believe PPSA is the only power conversion technology on the market that provides electrical isolation without the need for the transformer that conventional power conversion systems require to connect electrical devices such as energy storage systems to the grid. Electrical isolation is at the core of PPSA.

PPSA uses indirect power flow in which power flows through input switches and is temporarily stored in our proprietary AC link inductor. Our proprietary fast switching algorithms enable the transfer of quantum packets of power between ports in our system. As the AC link becomes charged, it disconnects from its input switches, resonates without being connected to either the input or output switches, and then reconnects to its output switches when it reaches the correct voltage and frequency for the application, providing true electrical isolation without the need for a transformer.

Figure 1: Schematic of PPSA Process

Transformer-based power conversion systems use continuous power flow that relies on relatively heavy and expensive magnetic components and bulk capacitors. Many of these traditional systems have custom hardware for specific applications and are not readily adaptable or customizable. Because they are relatively inefficient, these systems generate excess heat that causes electrical and thermal stresses resulting in drive component failures and losses. By contrast, our conversion technology eliminates the majority of the passive components of traditional power conversion systems, including transformers, inductors and bulk capacitors.

We believe PPSA offers several key advantages over traditional technologies, such as:

| • |

Size and Weight: PPSA architecture reduces size and weight by eliminating passive components such as transformers, inductors and bulk capacitors. Our 30kW power conversion system weighs 97 pounds. By contrast, similar transformer-based 30kW power conversion systems typically weigh over 600 pounds. | |

| • |

Efficiency: Efficiency is the measure of power out of the power conversion system as a percentage of the power into the system. Thus, high efficiency systems use less power in the conversion process and supply more power for use. Our 30kW power conversion system efficient rating was 96.5% based on the California Energy Commission (“CEC”) weighted efficiency test. Our efficiency advantage is more pronounced when operating the system at relatively low rated power, which is more common in battery systems. |

5

Figure 2: PPSA Size, Weight and Efficiency Comparison

| • | Cost: Reduced weight results in lower material and manufacturing, transportation and installation costs. |

| • | Safety: Since PPSA provides isolation, it allows the systems in which it is used to be grounded. Non-grounded systems require additional safeguards to pass U.S. safety regulations, which increase system cost and reduce efficiency. |

| • | Scalability/Flexibility: PPSA is made from standard industry components, is battery agnostic and software driven, thus providing more scalability that enables rapid development cycles for new products and new applications. This same functionality provides ultimate flexibility for customers globally as it is capable of power conversion in both 50Hz and 60Hz AC current environments. |

| • | Reliability: PPSA enables a simplified product that eliminates many components, thereby eliminating potential sources of failure, and several common failure modes. These design features are likely to increase overall system reliability. |

Products

We have developed products commercializing PPSA and make these products available for sale both directly to customers and through distributors. We currently sell five power conversion products utilizing our patented PPSA technology. These products are described as follows:

| • | 30kW Battery Converter, which is certified for UL1741 conformance and is intended to be used for the commercial and industrial grid-tied distributed energy storage market. This battery converter is bi-directional, which means power can flow to or from batteries. This product is more efficient and approximately 1/4th to 1/8th the size and weight of similar transformer-based products. |

| • | 30kW Grid-Resilient AC-DC Power Conversion System (“PCS”), which is certified for UL1741 conformance. This product is capable of power conversion in both 50Hz and 60Hz AC current environments and has the ability to form and manage a microgrid. This product is intended for customers who need a 30kW battery converter for use overseas or who need the additional capability to form a microgrid. This product is not a replacement for our 30kW battery converter but complements the existing product with additional features. |

| • | 30kW Grid-Resilient AC-DC-DC Multi-Port PCS with two DC ports enabling two DC inputs, such as PV and batteries, with one power converter. This product is certified for UL1741 conformance. This product is capable of power conversion in both 50Hz and 60Hz AC current environments, and also has the ability to form and manage a microgrid. The key feature of this multi-port PCS is that it effectively pairs energy storage with a distributed generation resource to support critical loads or allow a building to disconnect from the utility power grid. This product received the “Electrical Energy Storage Award” for product innovation in 2014 at InterSolar Germany, the world’s largest solar exhibition, and was recognized as one of the 2015 top inverter products by Solar Power World Magazine. |

| • | 125kW Grid-Resilient AC-DC PCS, which is certified for UL1741 conformance. This 125kW system has over four times the power of the 30kW product and is also able to convert in both 50Hz and 60Hz AC current environments and form and manage a microgrid. This product is a larger version of our 30kW grid-resilient AC-DC PCS for use in higher power applications. |

| • | 125kW Grid-Resilient AC-DC-DC Multi-Port PCS for higher power applications with multi-port capabilities. This product has over four times the power of the 30kW multi-port PCS and is also able to convert in both 50Hz and 60Hz AC current environments as well as form and manage a microgrid. The product is primarily for off-grid and microgrid management applications currently, as we have not yet sought certification for UL1741 conformance, required for connection to the utilize grid in the United States, for this product. This product is currently in prototype production only. We intend to certify this product for UL1741 conformance in late 2016 or early 2017 for grid tied operation. |

6

Future Innovations

Variable Frequency Drives

We are developing a PCS for variable frequency drives (“VFD”) based on our core PPSA technology. We believe that this product, once commercialized, can be offered as a high-efficiency alternative to traditional VFDs which suffer from similar size, weight, and heat loss inefficiencies as those of traditional power conversion systems. A PPSA-based VFD may offer medium to large low-voltage motors a high quality drive that improves efficiency, costs less to manufacture and install, and reduces electrical noise and harmonics over traditional VFDs. Such a product could also open up new markets for VFDs where they may not be commercially viable today due to their size, efficiency, or power quality.

Bi-Directional Switches

Our existing products incorporate multiple insulated gate bipolar transistors (“IGBTs”), which are power switches used in the process to convert power from one current form to another. IGBTs switch power in only one direction (DC to AC or AC to DC) and require the use of a blocking diode to prevent power from flowing back through the system. To enable our existing products to perform bi-directional power conversion, for each IGBT and diode used in our products, we must include a second IGBT and diode. These additional components have slight voltage drops that affect the electrical efficiency of our products and generate excess heat that must be dissipated. We have patented and are developing a new, highly efficient silicon switch called a bi-directional bipolar transistor (“B-TRAN”) that we believe will allow us to substitute one B-TRAN for two pairs of IGBTs and diodes used in our current products. Based on our software simulations, we believe that the B-TRANs can improve electrical efficiency in our power converters from approximately 96.5% to at or greater than 99.0%. The higher efficiency would substantially reduce the heat generated by the operation of our products. As a result, products incorporating B-TRANs will require less space for heat dissipation which would allow us to increase power density, or power per pound, and reduce material costs. We believe that these development efforts, if successful, will enhance the competitive position of our products. In addition, we believe the B-TRAN may potentially provide significant benefits for uses outside of our power converters as a potential replacement for IGBTs.

We received an award of $2.5 million from ARPA-E for the development of our bi-directional switch technology. Funds under the award have been spent and continuing development work is self-funded. The funding from ARPA-E was sufficient to develop and demonstrate advanced power switches in third party simulations and start the initial process development for fabrication of the devices. We expect to develop, manufacture and test initial prototypes of these switches in 2016.

Business Strategy

Our business strategy is to promote and expand the uses of PPSA initially through product development and product sales. To bring our products to market, we will seek out best-in-class partners who will distribute, white-label our products or integrate our innovative products into higher value systems resulting in multiple strategic sales channels for our PPSA based products and product designs. Although our primary market is the United States, we will increasingly target markets outside the United States. As our products gain broader acceptance in the power conversion market, we intend to license our proprietary PPSA-based product designs to OEMs within our target markets, as well as license our technologies for other markets which we do not plan to enter directly. The basis for this approach is the belief that OEMs may achieve higher product margins and gain more market share by providing PPSA-based products, which are differentiated from the traditional product offerings in the industry, to their customers. We believe such strategic relationships with key OEM licensees would enable us to reap the benefits of PPSA and gain market share more quickly than by strictly manufacturing and distributing our products.

Target Markets

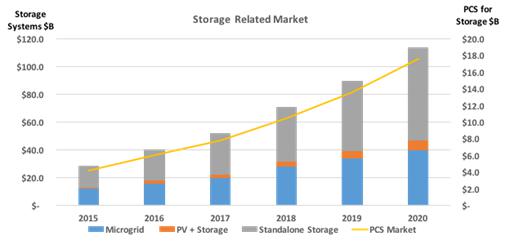

Currently, our three primary markets are standalone storage, which represented a majority of our sales in 2015, PV + storage, and microgrids. Based on market studies and forecasts by Navigant Research and Zpryme Research & Consulting, these three markets combined are forecasted to grow to over $100 Billion by 2020. Assuming that power conversion systems represent approximately 17.5% of the system cost, a Company estimate, power conversion systems such as those made by Ideal Power are forecasted to account for nearly $18 billion of this market.

7

Figure 3: Target Market Forecasts

Discussion of our Target Power Conversion Markets

Stand-Alone Storage Market

The stand-alone storage market is served by BESS. BESS are racks of batteries coupled with a power conversion system, such as those manufactured by us, to enable electric power to be captured, stored, and used in conjunction with electric power grids. These systems can be large, megawatt-scale systems operated by utilities to better manage their system resources, or smaller kilowatt-scale systems used by businesses and designed to enable these businesses to manage their power use and mitigate utility imposed “peak demand charges”, which are charges utilities levy on their business customers for delivery of power at peak usage times of the day, such as mid-afternoons in the summer. The growth of peak demand charges has been substantial over the past decade and now can make up 50% or more of a commercial utility bill in certain markets. This is a trend that is likely to continue as more intermittent resources are added to the utility power grid causing grid instability. Utilities and aggregators of distributed generation resources are also expected to adopt BESS due to the proliferation of renewables and to take advantage of additional value streams such as energy arbitrage, frequency regulation and ancillary services, infrastructure upgrade deferral and locational capacity.

There are strong economic incentives available to commercial and industrial consumers in major US markets such as California and New York in the form of reduced demand charges for installing a BESS and reducing peak consumption. There is also strong regulatory support for such systems. For example, California has issued a mandate for over 1,000 megawatts of new energy storage to be installed by 2020. Our 30kW and 125kW power conversion systems enable these BESS to connect to the utility power grid and, when paired with batteries, offer these customers a substantial cost saving opportunity on their monthly electric bill. This market is still in its early years, but we have established a strong brand and position in this market with our customers having many systems installed and operating today. Based on market studies and forecasts by Navigant Research and Zpryme Research & Consulting, this market is forecasted to grow 40% annually over the next five years and we believe it offers the highest value proposition today for our products.

We believe this market is beginning to grow beyond pilot installations to higher volume installations driven by the underlying economics of BESS to commercial and industrial customers. A good indicator of this is the availability of third party financing for BESS. Several of our customers have recently signed or announced financing deals for their BESS products, including Gexpro whose PowerIQ product is being commercially financed by a subsidiary of NextEra Energy Resources (NYSE: NEE).

We expect the cost of commercial and industrial BESS to continue to decline due primarily to lower battery costs and, as a result, expect significant expansion in the addressable market for these systems. We also believe the combination of lower BESS costs, third-party financing, increases in utility demand charges, and the continued entrance of large, established companies to the BESS space will all contribute to accelerating market growth for stand-alone storage.

PV + Storage Market

PV has one of the lowest levelized costs of energy for new electrical generation capacity and this is expected to remain true in the near term. We expect distributed PV to continue to be a high growth business as system costs have fallen dramatically over the past several years. As such, the economics of generating PV for local consumption is expected to remain strong for several more years, especially given the investment tax credit (“ITC”) extension passed by Congress in 2015 for solar energy production. One shortcoming of these distributed, behind-the-meter PV systems is that they require connection to the utility power grid in order to operate. For example, a business with PV on its roof will not, in most cases, benefit from the ability to generate power should the utility power grid go down. Another shortcoming of distributed PV systems is the instability they cause on the local power lines. Utility power grids were not designed to manage power inflow from the end of the lines. As such, distributed generation sources can lead to wide swings in line voltages when clouds pass and power output falls off, requiring the utility to ramp up its central power stations to make up for the shortfall in solar.

8

Our grid-resilient PCS help resolve these shortcomings. For example, when a distributed PV system is connected to a BESS that includes one of our multi-port PCS, the business will benefit from the ability to form and manage a local microgrid powered by the PV system and BESS even when the utility power grid is down. This capability is attractive to electricity consumers who need to power critical loads even in a blackout. Our grid-resilient PCS are also equipped to meet evolving utility requirements for low voltage ride through and other key operating parameters, enabling the PV and BESS it connects to the grid to help stabilize the utility power grid when voltage or frequency fluctuates due to imbalances in load and supply.

Commercial and industrial BESS are able to generate value far beyond peak demand reduction. We believe our products will become increasingly attractive to co-locate BESS with distributed PV. IHS, a global research firm with a strong renewable industry focus, forecasts that global installations of grid-tied commercial BESS coupled with PV will grow 111% annually from near obscurity in 2014 to over 600 MW PV + storage systems by 2018.

According to their research, IHS believes that systems will be deployed in two principle configurations. The present configuration is to have separate BESS and PV systems tied together through the AC wiring, which is supported by all of our current products. A second, emerging configuration will be to place the BESS and the PV system behind a single PCS with two DC inputs. This configuration is forecast to improve efficiency, reduce costs, and allow PV harvesting when operating without a utility power grid present in microgrid mode. Our grid-resilient 30kW and 125kW multi-port PCS were designed specifically to enable this lower cost and more efficient second configuration.

Also according to IHS, the global PV industry is projected to grow from 45GW of annual installations in 2014 to 71GW in 2018. Providing a new generation of solutions with integrated energy storage will enable the PV industry to address new markets with high growth potential. These new PV + storage markets include providing backup power during blackouts, improving grid stability in high penetration PV areas and reducing fossil fuel consumption in remote and off-grid microgrids. In the event of a grid failure, grid-tied PV installations are not capable of operating independently. For example, during Superstorm Sandy many PV system owners were displeased to learn that their grid-tied PV installations would not power their home or business. Systems incorporating our multi-port PCS along with PV and a BESS will be capable of providing backup power during grid blackouts. We expect our multi-port PCS products to be attractive to existing customers as a low-cost system upgrade to improve integration of PV. We further expect our products to provide competitive solutions for these market requirements.

Microgrid Market

Over the next decade the greatest demand for new power generation capacity is likely to occur in regions such as Southeast Asia, Africa, the Middle East, and Central and South America. Remote communities and infrastructure in these regions are more likely to depend on expensive and polluting fossil fuel generation for their primary fuel supply and may not have a utility power grid in place to access high quality, reliable power.

In contrast to grid-tied BESS and PV applications that are likely to be North American installations, we believe off-grid BESS and PV opportunities will develop rapidly across these regions with the greatest demand for new power generation. IHS recently forecasted the off-grid and microgrid BESS installations with PV market to reach 400MW by 2018 with the majority of this growth coming from regions with less developed electricity infrastructure. We believe that our grid-resilient 30kW and 125kW multi-port PCSs offer superior solutions for these applications.

We believe that our award-winning multi-port power conversion architecture is a highly attractive solution for integrating BESS and renewables for both grid-tied and off-grid markets. Customer and industry forecasts indicate that these markets will grow dramatically in the coming years, and we expect to benefit from this growth. The benefits of our multi-port PCS in microgrid application is not limited to PV or renewable energy systems. Our products have been integrated into systems to manage a diesel generator and, in combination with batteries, to form and operate a microgrid using far less fuel, emitting far fewer pollutants, and providing better power quality than a diesel generator alone.

Other Markets

Although our technology may be suitable for other vertical markets within the global power conversion market landscape, we do not currently offer products for sale directly to other power conversion markets such as the VFD, uninterruptible power supply, rail, wind, or EV traction drive markets. Our products are suitable for use as PV inverters, and our first products were sold into this market, but this market is saturated with incumbents offering inverters that convert power in a single direction and are thus suitable solely for PV applications. As such, while we do have a number of PV inverters in field service today, the stand-alone PV inverter market is not a primary target market for us. As discussed above, we are instead focused on PV integrated BESS applications for our multi-port PCS products where the fullest potential of our technology can be realized.

In addition to the markets discussed above, we also have opportunities for market expansion into fast electric vehicle chargers in certain applications where our products’ compact size and multi-port capabilities can unlock value for the system integrator particularly in locations where battery storage is coupled with the charging system to eliminate demand charges or expand the charging systems response capabilities. We have provided PCS to multiple EV charging system integrators who have deployed initial projects using our products coupled with batteries at EV charging stations to prove out these concepts. As these initial installations begin to operate, the value propositions of these new opportunities will become clearer.

We plan to continue to monitor all power conversion markets for opportunities to create solutions for customers and unlock the broader value of our patented technology.

9

Intellectual Property

We rely on a combination of patents, laws that protect intellectual property, confidentiality procedures, and contractual restrictions with our employees and others, to establish and protect our intellectual property rights. In addition, the software that is shipped with our products is encrypted. At December 31, 2015, we had 36 issued U.S. patents and six issued foreign patents. We also had over 100 additional pending U.S., foreign and international patent applications. We expect to continue to build our patent estate for both our core power conversion technology, our bi-directional switch technology and other technological developments that broaden the scope of our technology platform.

Customers

Although we are expanding our customer base and channels to market, we have historically been reliant on a small number of customers. For the year ended December 31, 2015, Sharp, Gexpro, GreenCharge Networks, and Coda Energy, accounted for 66% of net revenues. For the year ended December 31, 2014, Sharp, GreenCharge Networks and Coda Energy, accounted for 44% of product revenue. In addition, the Department of Energy, from which we received $579,079 in grant revenues, accounted for 32% of net revenue for the year ended December 31, 2014.

Sales and Marketing

We sell our products primarily to systems integrators for installation as part of a larger turn-key system providing the end user with a complete solution for managing their energy consumption. Our products are also sold through distribution channel partners. Before a system integrator agrees to specify our products in their systems, the integrator engages in a lengthy and time-consuming process of testing and evaluating our equipment for use, which typically may take from a few months to as long as a year.

For certain geographic markets and applications, we may seek to enter into licensing agreements that would enable licensees to build our products for sale in local markets or we may license product designs to global brands for specific applications.

Manufacturing and Supply

We use a contract manufacturer to manufacture our products to our specifications. We have an agreement with our contract manufacturer pursuant to which we provide them with a rolling forecast of our expected demand. Finished products are produced based on upon our forecast, and we have the ability to delay shipments for up to 18 months from the date of the purchase order. The initial three-year term of the agreement expires in October of 2017 and renews annually thereafter unless terminated. We believe there are many contract manufacturers that are qualified to manufacture our products to our specifications and we expect to add a second contract manufacturer in 2016.

Typically, our contract manufacturer is responsible for the sourcing of components and materials. We qualify sources for our components and materials. Our strategy is to have multiple suppliers for all of our components and materials. Currently, we have multiple sources for most of our components. A very limited number of components are singled sourced and the process of identifying and qualifying alternative sources for these components is underway.

Backlog

Our backlog was approximately $5.2 million at December 31, 2015, a 160% increase from our backlog of $2 million at December 31, 2014. The Company defines backlog as consisting of accepted orders from customers for which a product delivery schedule has been specified. The purchased orders comprising backlog are not cancellable in most cases and such orders do not provide price protection. Nevertheless, deliveries against received purchase orders may be rescheduled within negotiated parameters and our backlog may therefore not be indicative of the level of future sales.

Competition

We will compete against well-established incumbent power conversion technology providers as these competitors enter the commercial and industrial markets. For our target markets, we believe that PPSA provides significant competitive advantages compared to the traditional power conversion solutions sold by well-established power conversion technology providers.

Transformer Based: Transformer-based power conversion systems are the conservative choice, as they are proven and have been commercially available longer than any other type of power conversion system. They provide isolation, but are big, heavy, and relatively inefficient. There have been improvements in the efficiency of transformer-based power conversion systems over the years, but we believe further improvements are limited due to the physical characteristics of transformers themselves. Major suppliers in this market include ABB, Eaton, and Schneider Electric.

Transformerless PV Inverters: Transformerless photovoltaic (PV) solar inverters are a special class of power conversion system applicable only to PV arrays. They have become a popular choice in the market for distributed PV applications, as they are lighter and more efficient than transformer based inverters. These transformerless inverters are one-way (DC to AC) inverters, and provide no electrical isolation. PV systems are not required to be electrically isolated in most electrical code jurisdictions. These PV inverters have no applicability to markets that require electrical isolation, which includes every application in the electrical power conversion industry in which we compete. Key providers of transformerless PV inverters include companies such as SMA and SolarEdge.

10

Research and Development Costs

Grant research and development are costs incurred solely related to grant revenues, and are classified as a line item under cost of revenues. Other research and development costs are presented as a line item under operating expenses and are expensed as incurred. Total research and development costs incurred during the year ended December 31, 2015 amounted to $5,521,390, none of which was included in cost of revenues. Total research and development costs incurred during the year ended December 31, 2014 amounted to $2,983,648, inclusive of $643,421 related to grant research which was included in cost of revenues.

Employees

As of February 29, 2016, we have 28 full-time employees. None of these employees are covered by a collective bargaining agreement, and we believe our relationship with our employees is good.

Industry Certifications

Industry certifications are generally required for our products. The main certification requirement is conformance to UL1741, which specifies standards for grid and product safety for grid-connected generation equipment, including the power conversion systems made by us. A National Recognized Testing Laboratory (“NRTL”) must certify our products for conformance to UL1741 before our customers may install and use our products in grid-tied applications in the United States.

We have chosen Intertek, an NRTL, for our certification requirements and have completed testing and received authorization to use their ETL mark on our products. While we have been able to complete these certifications timely, we may not be as successful in completing certification in a timely manner on future products, which could limit our ability to bring such products to market in a timely manner.

Europe, Japan and other major countries have different certification test procedures, but generally test for similar safety and performance capabilities. Local certifications are likely to be required to sell our products outside of the United States for many applications. To date, we have not received any international certifications on our products but have deployed products in a few instances in foreign countries as demonstrations, test projects in laboratories or microgrid applications which may be exempt from the certification requirements. We expect to start the certification process in one or more international markets in 2016.

Government Regulation

Government approval is not required for us to sell our products. However, government support for renewable energy, grid storage, electric vehicle charging infrastructure and improved grid resiliency may impact the size and growth rate of our target markets. Utility regulations and support may also impact these end markets. In the near term, government and utility support for these markets is generally required for these markets to grow and therefore changes in policy by governments or utilities may limit the near term market opportunities for our products.

Available Information

Our Internet address is www.idealpower.com and our investor relations website is located at ir.idealpower.com. We make available free of charge on our investor relations website under the heading “SEC Filings” our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports as soon as reasonably practicable after such materials are electronically filed with (or furnished to) the SEC. We also make available on our website, our corporate governance documents, including our code of conduct and ethics. Information contained on our website is not incorporated by reference into this Annual Report on Form 10-K. In addition, the public may read and copy materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site, www.sec.gov, that includes filings of and information about issuers that file electronically with the SEC.

| ITEM 1A: | RISK FACTORS |

We are subject to various risks that may materially harm our business, prospects, financial condition and results of operations. An investment in our common stock is speculative and involves a high degree of risk. In evaluating an investment in shares of our common stock, you should carefully consider the risks described below, together with the other information included in this report.

The risks described below are not the only risks we face. If any of the events described in the following risk factors actually occurs, or if additional risks and uncertainties later materialize, that are not presently known to us or that we currently deem immaterial, then our business, prospects, results of operations and financial condition could be materially adversely affected. In that event, the trading price of our common stock could decline, and you may lose all or part of your investment in our shares. The risks discussed below include forward-looking statements, and our actual results may differ substantially from those discussed in these forward-looking statements.

Risks Related to Our Business

We lack an established operating history on which to evaluate our business and determine if we will be able to execute our business plan. We have also incurred losses in prior periods, expect to incur losses in the future and we can give no assurance that our operations will result in profits.

We were formed in Texas on May 17, 2007 and converted to a Delaware corporation on July 15, 2013. We have a limited operating history that makes it difficult to evaluate our business. Historical sales of our products have been in low volume, and we cannot say with certainty when we will begin to achieve profitability.

11

Since inception, we have sustained $34,093,074 in net losses and we had a net loss for the year ended December 31, 2015 of $10,440,643. We expect to have operating losses at least until such time as we have developed a substantial and stable revenue base. We cannot assure you that we can develop a substantial and stable revenue base or achieve or sustain profitability on a quarterly or annual basis in the future.

As sales of our products have generated limited operating revenues, we have been funding operations primarily through the sale of common stock and, prior to our initial public offering, the issuance of convertible debt. If we are unable to execute our business plan, generate sustainable revenue and achieve profitable operations with our existing capital we would need to raise funds through equity or debt offerings and there can be no assurance that we will be able to do so.

Our future success is difficult to predict because we operate in emerging and evolving markets, and the industries in which we compete are subject to volatile and unpredictable cycles.

The grid energy storage, solar combined with storage, microgrid and related industries are emerging and evolving markets which may make it difficult to evaluate our future prospects and which may lead to period to period variability in our operating results. Our products are based on unique technology which we believe offers significant advantages to our customers, but the markets we serve are in a relatively early stage of development and it is uncertain how rapidly they will develop. It is also uncertain whether our products will achieve high levels of demand and acceptance as these markets grow. If companies in the industries we serve do not perceive or value the benefits of our technologies and products, or if they are unwilling to adopt our products as alternatives to traditional power conversion solutions, the market for our products may not develop or may develop more slowly than we expect, which could significantly and adversely impact our operating results.

As a supplier to the grid energy storage, solar combined with storage, microgrid and related industries, we may be subject to business cycles. The timing, length, and volatility of these business cycles may be difficult to predict. These industries may be cyclical due to sudden changes in customers’ manufacturing capacity requirements and spending, which depend in part on capacity utilization, demand for customers’ products, inventory levels relative to demand, and access to affordable capital. These changes may affect the timing and amounts of customers’ purchases and investments in technology, and affect our orders, net sales, operating expenses, and net income. In addition, we may not be able to respond adequately or quickly to the declines in demand by reducing our costs. We may be required to record significant reserves for excess and obsolete inventory as demand for our products changes.

To meet rapidly changing demand in each of the industries we serve, we must effectively manage our resources and production capacity. During periods of decreasing demand for our products, we must be able to appropriately align our cost structure with prevailing market conditions, effectively manage our supply chain, and motivate and retain key employees. During periods of increasing demand, we must have sufficient manufacturing capacity and inventory to fulfill customer orders, effectively manage our supply chain, and attract, retain, and motivate a sufficient number of qualified individuals. If we are not able to timely and appropriately adapt to changes in our business environment or to accurately assess where we are positioned within a business cycle, our business, financial condition, or results of operations may be materially and adversely affected.

To date we have had a limited number of customers. We cannot assure you that our customer base will increase.

We had revenue from four customers which accounted for 66% of net revenue for the year ended December 31, 2015. One of these customers, Coda Energy, which accounted for 10% of net revenue, declared bankruptcy in December 2015. We had receivable balances from three customers that accounted for 66% of trade receivables at December 31, 2015. As we sell our products to a limited number of customers, we cannot assure you that our customer base will expand or that any decline in net revenue attributable to customer losses will be replaced in a timely manner.

Product development is an inherently uncertain process, and we may encounter unanticipated development challenges and may not be able to meet our product development and commercialization milestones.

Product development and testing may be subject to unanticipated and significant delays, expenses and technical or other problems. We cannot guarantee that we will successfully achieve our milestones within our planned timeframe or ever. We commonly develop prototypes of planned products prior to the full commercialization of these products. We cannot predict whether prototypes of future products will achieve results consistent with our expectations. A prototype could cost significantly more than expected or the prototype design and construction process could uncover problems that are not consistent with our expectations. Prototypes of emerging products are a material part of our business plan, and if they are not proven to be successful, our business and prospects could be harmed.

More generally, the commercialization of our products may also be adversely affected by many factors not within our control, including:

| • | the willingness of market participants to try a new product and the perceptions of these market participants of the safety, reliability, functionality and cost effectiveness of our products; |

| • | the emergence of newer, possibly more effective technologies; |

| • | the future cost and availability of the raw materials and components needed to manufacture and use our products; and |

| • | the adoption of new regulatory or industry standards that may adversely affect the use or cost of our products. |

12

Accordingly, we cannot predict that our products will be accepted on a scale sufficient to support development of mass markets for them.

We must achieve design wins to retain our existing customers and to obtain new customers, although design wins achieved do not necessarily result in substantial sales.

The constantly changing nature of technology in the markets we serve causes equipment manufacturers to continually design new systems. We must work with these manufacturers early in their design cycles to modify our equipment or design new equipment to meet the requirements of their new systems. Manufacturers typically choose one or two vendors to provide the components for use with early system shipments. Selection as one of these vendors is called a design win. It is critical that we achieve these design wins in order to retain existing customers and to obtain new customers.

We believe that equipment manufacturers often select their suppliers based on factors including long-term relationships and end user demand. Accordingly, we may have difficulty achieving design wins from equipment manufacturers who are not currently our customers. In addition, we must compete for design wins for new systems and products of our existing customers, including those with whom we have had long-term relationships. Our efforts to achieve design wins are time consuming, expensive, and may not be successful. If we are not successful in achieving design wins, or if we do achieve design wins but our customers’ systems that utilize our products are not successful, our business, financial condition, and results of operations could be materially and adversely impacted.

Once a manufacturer chooses a component for use in a particular product, it is likely to retain that component for the life of that product. Our sales and growth could experience material and prolonged adverse effects if we fail to achieve design wins. However, design wins do not always result in substantial sales, as sales of our products are dependent upon our customers’ sales of their products.

We have received grant funds from the United States for the development of a bi-directional switch. In certain instances, the United States may obtain title to inventions related to this effort. If we were to lose title to those inventions, we may have to pay to license them from the United States in order to manufacture the inventions. If we were unable to license those inventions from the United States, it could slow down our product development.

In conjunction with the Advanced Research Projects Agency-Energy, or ARPA-E, grant we received from the Department of Energy, we granted to the United States a non-exclusive, nontransferable, irrevocable, paid-up license to practice or have practiced for or on behalf of the United States inventions related to the bi-directional switch and made within the scope of the grant. If we fail to disclose to the Department of Energy an invention made with grant funds that we disclose to patent counsel or for publication, or if we elect not to retain title to the invention, the United States may request that title to the subject invention be transferred to it.

We also granted “march-in-rights” to the United States in connection with any bi-directional switch inventions in which we choose not to retain title, if those inventions are made under the ARPA-E grant. Pursuant to the march-in-rights, the United States has the right to require us, any person to whom we have assigned our rights, or any exclusive licensee to grant a non-exclusive, partially exclusive, or exclusive license in any field of use to a responsible applicant upon terms that are reasonable. If the license is not granted as requested, the United States has the right to grant the license if it determines that we have not achieved practical application of the invention in the field of use, the action is necessary to alleviate health or safety needs, the action is necessary to meet requirements for public use specified by Federal regulations and such requirements have not been satisfied, or the action is necessary because an agreement to manufacture the invention in the United States has not been obtained or waived or because any such agreement has been breached.

If we lost title to the United States as a result of any of these events, we would have to pay to license the inventions, if needed, to manufacture the bi-directional switch from the United States. If we were unable to license those inventions from the United States, it could slow down our product development.

As we continue to grow and to develop our intellectual property, we could attract threats from patent monetization firms or competitors alleging infringement. We may incur substantial costs as a result of litigation or other proceedings relating to patent and other intellectual property rights.

As we continue to grow and to develop our intellectual property, we could attract threats from patent monetization firms or competitors alleging infringement of intellectual property rights.

In addition, some of our competitors may be able to sustain the costs of complex patent litigation more effectively than we can because they have substantially greater resources. If we do not prevail in this type of litigation, we may be required to: pay monetary damages; stop commercial activities relating to our product; obtain one or more licenses in order to secure the rights to continue manufacturing or marketing certain products; or attempt to compete in the market with substantially similar products. Uncertainties resulting from the initiation and continuation of any litigation could limit our ability to continue some of our operations.

For instance, on October 4, 2013 we received a letter from a competitor alleging that the system architecture described on our website appeared to infringe on patents licensed to or held by the competitor. The letter asked that we explain why we believe that our technology does not represent an infringement. This competitor sent a subsequent letter on February 3, 2014 directly alleging our PPSA technology infringed upon one of the competitor’s patent. Following receipt of the first letter, we investigated the competitor’s claims and determined that their allegations were without merit. In early 2014, following our receipt of the February 3, 2014 letter, we met with the competitor to discuss their claims. No subsequent discussions have been held with, and no further correspondence has been received from, this competitor.

13

We expect to license our technology in the future; however the terms of these agreements may not prove to be advantageous to us. If the license agreements we enter into do not prove to be advantageous to us, our business and results of operations will be adversely affected.

We expect to license the manufacture of our product designs for certain markets as well as license our technology for certain potential applications which we choose not to pursue directly through the sale of products. However, we may not be able to secure license agreements with customers on terms that are advantageous to us. Furthermore, the timing and volume of revenue earned from license agreements will be outside of our control. If the license agreements we enter into do not prove to be advantageous to us, our business and results of operations will be adversely affected.

Until recently, we have not devoted significant resources towards the marketing and sale of our products and we continue to rely on the marketing and sales efforts of third parties whom we do not control.

We expect that the marketing and sale of our battery converter and PCS products to end user customers will continue to be conducted primarily by a combination of system integrators, third-party strategic partners, distributors, and original equipment manufacturers, or OEMs. Consequently, commercial success of our products will depend, to a great extent, on the efforts of others. We may not be able to identify, maintain or establish additional and/or appropriate relationships in the future. We can give no assurance that these third parties will focus adequate resources on selling our products or will be successful in selling them. In addition, these third-parties have or may require us to provide volume price discounts and other allowances, customize our products or provide other concessions that could reduce the potential profitability of these relationships. Failure to develop sufficient customer, distribution and marketing relationships in our target markets will adversely affect our commercialization schedule and to the extent we have entered or enter into such relationships, the failure of our distributors and other third parties to assist us with the marketing and distribution of our products, or to meet their monetary obligations to us, may adversely affect our financial condition and results of operations.

A material part of our success depends on our ability to manage our suppliers and contract manufacturers. Our failure to manage our suppliers and contract manufacturers could materially and adversely affect our results of operations and relations with our customers.

We rely upon suppliers to provide the components necessary to build our products and on contract manufacturers to procure components and assemble our products. There can be no assurance that key suppliers and contract manufacturers will provide components or products in a timely and cost efficient manner or otherwise meet our needs and expectations. Our ability to manage such relationships and timely replace suppliers and contract manufacturers, if necessary, is critical to our success. Our failure to timely replace our contract manufacturers and suppliers, should that become necessary, could materially and adversely affect our results of operations and relations with our customers.

Our business may be dependent upon our ability to obtain financing. If we do not obtain such financing, we may have to cease our activities.

There is no assurance that we will operate profitably or generate positive cash flows in the future. In the future, we may require additional financing in order to sell our then current products and to continue the research and development required to develop our next generation of products. At that time, we may not be able to obtain financing on commercially reasonable terms or at all. If we do not obtain such financing when needed, our business could fail.

The macro-economic environment in the United States and abroad has adversely affected, and may in the future adversely affect, our ability to raise capital, which may potentially impact our ability to continue our operations.

As a company with limited revenues to date, we may need to rely on raising funds from investors to support our future research and development activities and our operations. Macro-economic conditions in the United States and abroad may result in a tightening of the credit markets and/or less capital available for small public companies, which may make it more difficult to raise capital. If we are unable to raise funds as and when we need them, we may be forced to curtail our operations or even cease operating altogether.

We are subject to credit risks.

Some of our customers may experience financial difficulties and/or may fail to meet their financial obligations to us. As a result, we may incur charges for bad debt provisions related to some trade receivables. In addition, in connection with the growth of the renewable energy market and other markets for our products, we are gaining new customers, some of which have relatively short histories of operations or are newly formed companies. As a result, it is difficult to ascertain financial information in order to appropriately extend credit to these customers. Further, the volatility in the renewable energy market may put additional pressure on our customers’ financial positions, as they may be required to respond to large swings in revenue. The renewable energy industry has also, from time to time, seen an increasing amount of bankruptcies and reorganizations as the availability of financing has diminished. In 2015, two of our customers filed for bankruptcy. Although we have limited credit losses related to these bankruptcies, our December 31, 2015 backlog and near term future revenue were impacted by the bankruptcy of Coda Energy, one of these two customers.

14

If customers fail to meet their financial obligations to us, or if the assumptions underlying our recorded bad debt provisions with respect to receivables obligations do not accurately reflect our customers’ financial condition and payment levels, we could incur write-offs of receivables in excess of our provisions, which could have a material adverse effect on our cash flow and operating results.

We may not be able to control our warranty exposure, which could increase our expenses.

We currently offer and expect to continue to offer a warranty with respect to our products and we expect to offer a design warranty under future licensing agreements, if any. Due to our limited long-term history of operating data, our reserve is estimated based on engineering judgment and third party assessments of our product reliability. If the cost of warranty claims exceeds any reserves we may establish for such claims, our results of operations and financial condition could be adversely affected.

We may be exposed to lawsuits and other claims if our products malfunction, which could increase our expenses, harm our reputation and prevent us from growing our business.

Any liability for damages resulting from malfunctions of our products could be substantial, increase our expenses and prevent us from growing or continuing our business. Potential customers may rely on our products for critical needs and a malfunction of our products could result in warranty claims or other product liability. In addition, a well-publicized actual or perceived problem could adversely affect the market’s perception of our products. This could result in a decline in demand for our products, which would reduce revenue and harm our business. Further, since our products are used in systems that are made by other manufacturers, we may be subject to product liability claims even if our products do not malfunction.

We are highly dependent on the services of R. Daniel Brdar and William Alexander, as well as other key members of our executive management team. Our inability to retain these individuals could impede our business plan and growth strategies, which could have a negative impact on our business and the value of your investment.

Our ability to implement our business plan depends, to a critical extent, on the continued efforts and services of R. Daniel Brdar, our Chief Executive Officer and President, William Alexander, our founder and Chief Technology Officer, and other members of our executive management team. If we lose the services of any of these persons during this important time in our development, the loss may result in a delay in the implementation of our business plan and plan of operations. We can give no assurance that we could find satisfactory replacements for these individuals on terms that would not be unduly expensive or burdensome to us. We do not currently carry a key-man life insurance policy that would assist us in recouping our costs in the event of the death or disability of any of these persons.

Any failure by management to properly manage our expected rapid growth could have a material adverse effect on our business, operating results and financial condition.

If our business develops as expected, we anticipate that we will grow rapidly in the near future. Our failure to properly manage our expected rapid growth could have a material adverse effect on our ability to retain key personnel. Our expansion could also place significant demands on our management, operations, systems, accounting, internal controls and financial resources. If we experience difficulties in any of these areas, we may not be able to expand our business successfully or effectively manage our growth. Any failure by management to manage growth and to respond to changes in our business could have a material adverse effect on our business, financial condition and results of operations.

Backlog may not result in revenue.

Our backlog was approximately $5.2 million at December 31, 2015. We define backlog as consisting of accepted orders from customers for which an expected product delivery schedule has been specified. The purchase orders comprising backlog are not cancellable in most cases and such orders generally do not provide price protection. Nevertheless, deliveries against received purchase orders may be rescheduled within negotiated parameters and our backlog may, therefore, not be indicative of revenues in any given period.

Risks Relating to the Industry

The electric power conversion industry is competitive, has a number of well-financed incumbents and may see a significant number of new market entrants. We cannot guarantee that we can compete successfully.

We may compete against providers of PCS that are well established and have substantially greater assets, including manufacturing, marketing, and financial assets. These incumbents also have strong market share and name brand recognition in the industry. Potential competitors include ABB, Ltd., Eaton Corporation plc, SMA Solar Technology AG, and Schneider Electric SE. Pricing and servicing, as well as the general quality, efficiency and reliability of products, are significant competitive criteria in this industry. New market entrants may offer competitive new technologies and products, and may also contribute to significant price competition.

Our ability to successfully compete on each of these criteria is material to the acceptance of our products and their future profitability. In addition, the industry may resist new technology and products from suppliers that are not well capitalized with long track records of performance. Our competitors use their balance sheet and brand recognition to their competitive advantage. Should our products become commercially successful, competitors may seek to drive their own innovation and adopt or copy ideas, designs and features to regain their competitive positions. Incumbent or new competitors may develop or offer technologies and products that may be more effective or popular than our products and these competitors may be more successful in marketing their products than we are in marketing our products. Additionally, price competition may result in lower than expected margins for our products.

15

We expect to compete on the basis of our products’ lower cost, smaller footprint, higher efficiency, and technological innovation, flexibility and features. Unrelated technological advances in alternative energy products or other power conversion technologies may negatively impact the development of our products or make our products uncompetitive or obsolete at any time. We cannot guarantee that we will be able to compete successfully in the electric power conversion industry.

Our business is substantially dependent on utility rate structures and government incentive programs that encourage the use of alternative energy sources. The reduction or elimination of government subsidies and economic incentives for energy-related technologies would harm our business.

We believe that near-term growth of energy-related technologies, including power conversion technology, relies partly on the availability and size of government and economic incentives and grants (including, but not limited to, the U.S. Investment Tax Credit and various state and local incentive programs). These incentive programs could be challenged by utility companies, or for other reasons found to be unconstitutional, and/or could be reduced or discontinued for other reasons. The reduction, elimination, or expiration of government subsidies and economic incentives could harm our business.

A combination of utility rate structures and government subsidies that encourage the use of alternative energy sources is a primary driver of demand for our products. For example, public utilities are often allowed to collect demand charges on commercial and industrial customers in addition to traditional usage charges. In addition, the federal government and many states encourage the use of alternative energy sources through a combination of direct subsidies and tariff incentives such as net metering for users that use alternative energy sources such as solar power. California also encourages alternative energy technology through its Self-Generation Incentive Program, or SGIP, which offers rebates for businesses and consumers who adopt certain new technologies. As a result of these incentives, we believe that a substantial portion of the products we have sold have been for use by end customers in California. Other states have similar incentives and mandates which encourage the adoption of alternative energy sources. Notwithstanding the adoption of other incentive programs, we expect that California will be the most significant market for the sale of our products in the near term for stand-alone storage applications. Should California or another state in which we derive a substantial portion of our product revenues in the future change its utility rate structure or eliminate or significantly reduce its incentive programs, demand for our products could be substantially affected, which would adversely affect our business prospects, financial condition and operating results.

Changes to the National Electrical Codes could adversely affect our technology and products.

Our products are installed by system integrators that must meet the National Electrical Codes, or NEC, standards, including using equipment that meets industry standards such as UL1741. The NEC standards address the safety of these systems. The NEC standards, along with the UL1741 and IEEE1547 requirements, continue to evolve and are subject to change. If we respond to these changing standards and requirements more slowly than our competitors, or if we are unable to meet new standards and requirements, our products will be less competitive.

New technologies in the alternative energy industry may supplant our current products and technology in this market, which would harm our business and operations.

The alternative energy industry is subject to rapid technological change. Our future success will depend on the cutting edge relevance of our technology, and thereafter on our ability to appropriately respond to changing technologies and changes in function of products and quality. If new technologies supplant our power conversion technology, our business would be adversely affected and we will have to revise our plan of operation.

Businesses, consumers, and utilities might not adopt alternative energy solutions as a means for providing or obtaining their electricity and power needs.

On-site distributed power generation solutions that utilize our products provide an alternative means for obtaining electricity and are relatively new methods of obtaining electrical power. There is a risk that businesses, consumers, and utilities may not adopt these new methods at levels sufficient to grow our business. Traditional electricity distribution is based on the regulated industry model whereby businesses and consumers obtain their electricity from a government regulated utility. For alternative methods of distributed power to succeed, businesses, consumers and utilities must adopt new purchasing practices and must be willing to rely upon less traditional means of providing and purchasing electricity. As larger solar projects come online, utilities are becoming increasingly concerned with grid stability, power management and the predictable loading of such power onto the grid.

We cannot be certain that businesses, consumers, and utilities will choose to utilize on-site distributed power at levels sufficient to sustain our business. The development of a mass market for our products may be impacted by many factors which are out of our control, including:

| • | market acceptance of systems that incorporate our products; |

| • | the cost competitiveness of these systems; |

| • | regulatory requirements; and |

| • | the emergence of newer, more competitive technologies and products. |