UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| [X] | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended March 31, 2012 | |

| [ ] | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT |

| For the transition period from _________ to ________ | |

|

Commission file number: 333-173699

|

| Nepia, Inc. |

| (Exact name of registrant as specified in its charter) |

| Nevada | 27-4588540 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

|

Tian Bei W. Rd. Yung Guang Tian Di Ming Xing Ge, Unit 1503, Shenzhen, China |

________ |

| (Address of principal executive offices) | (Zip Code) |

|

Registrant’s telephone number: 86-075525601615

|

|

Securities registered under Section 12(b) of the Exchange Act:

| ||

| Title of each class | Name of each exchange on which registered | |

| None | Not applicable | |

|

Securities registered under Section 12(g) of the Exchange Act:

| ||

| Title of each class | ||

| None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X]

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the proceeding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [X]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [X]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [X] No [ ]

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter. Not available

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. 2,625,000 common shares as of June 26, 2012.

| 2 |

PART I

Company Overview

We were incorporated as “Nepia, Inc.” in the State of Nevada on August 9, 2010, for the purpose of developing, manufacturing, and selling small boilers aimed at farmers primarily in Southeast Asia. We are currently in the development stage and have nominal operations and minimal assets, which makes us a “shell company” as defined in Rule 12b-2 of the Exchange Act, as amended.

Business of Company

We are engaged in the business of developing, manufacturing, and selling straw burning boilers specifically for use as energy-efficient heating systems, as well as for cooking. Our product consists of three main components: a straw-burning boiler, pipes for distributing hot water for heating, and a stove-top “burner” for cooking. The boiler uses straw from fields as fuel, generating thermal energy; the pipes with hot water can be used to heat a home, barn, or grain storage unit; and the burner is used to cook food. We are currently in the process of designing and developing our straw-burning boiler prototype at our operations office in China. Our product is not yet ready for commercial sale. We are at the latter stages of the design process on our prototype, but we have designing and testing to accomplish before the final product is ready for commercial sale. We intent to conduct testing at our facility and not through a third party testing company. When we are satisfied that our product will compete effectively in the Chinese Boiler Industry by being the most efficient in terms of heating capability, efficiency, and alternative uses, we intend to begin the manufacture and distribution of our product to home improvement merchants throughout China.

Boilers

The information in this section is generally accepted mechanical information on the nature and uses of boilers. The specific sources of this information are two books: High Pressure Boilers by Frederick Steingress, Harold J. Frost and Daryl R. Walker; and Low Pressure Boilers by Frederick Steingress and Daryl R. Walker. The books were published in 2009 and 2008, respectively, and represent a comprehensive representation of the current state of the science behind boilers, as well as their mechanical functioning.

A boiler is a closed vessel in which water or other fluid is heated under pressure. The heated or vaporized fluid exits the boiler for use in various processes or heating applications. Construction of boilers is mainly limited to carbon steel, stainless steel, and cast iron. The source of heat for a boiler is usually combustion of any of several fuels, such as wood, coal, oil, or natural gas. Electric boilers use resistance or immersion type heating elements to heat the water to a useful temperature.

The goal of a boiler is to make the heat flow as completely as possible from the heat source to the water. Most boilers heat water until it boils, and then the steam is used at saturation temperature (i.e., saturated steam). Superheated steam boilers boil the water and then further heat the steam in a superheater. Some superheaters are radiant type (absorb heat by radiation), others are convection type (absorb heat via a fluid or gas) and some are a combination of the two. Whether by convection or radiation, the extreme heat in the boiler furnace/flue gas path will also heat the superheater steam piping and the steam within as well. It is important to note that while the temperature of the steam in the superheater is raised, the pressure of the steam is not. The process of superheating steam is most importantly designed to remove all moisture content from the steam to prevent damage to the turbine blading and/or associated piping.

| 3 |

Hydronic boilers (according to the Wikipedia.com article on boilers) are typically used in generating heat for residential uses. They are the typical power plant for central heating systems fitted to houses in northern Europe (where they are commonly combined with domestic water heating), as opposed to the forced-air furnaces or wood burning stoves more common in North America. The hydronic boiler operates by way of heating water/fluid to a preset temperature (or sometimes in the case of single pipe systems, until it boils and turns to steam) and circulating that fluid or steam throughout the home by way of radiators, baseboard heaters or through the floors. The fluid can be heated by any means, but in built-up areas where piped gas is available, natural gas is currently the most economical and therefore the common choice. The fluid is in an enclosed system and circulated throughout by means of a motorized pump. Most modern systems are fitted with condensing boilers for greater efficiency.

Most boilers now depend on mechanical draft equipment rather than natural draft. This is because natural draft is subject to outside air conditions and temperature of flue gases leaving the furnace, as well as the chimney height. All these factors make proper draft hard to attain and therefore make mechanical draft equipment much more economical.

There are three types of mechanical draft:

Induced draft: This is obtained one of three ways, the first being the "stack effect" of a heated chimney, in which the flue gas is less dense than the ambient air surrounding the boiler. The more dense column of ambient air forces combustion air into and through the boiler. The second method is through use of a steam jet. The steam jet oriented in the direction of flue gas flow induces flue gasses into the stack and allows for a greater flue gas velocity increasing the overall draft in the furnace. This method was common on steam driven locomotives which could not have tall chimneys. The third method is by simply using an induced draft fan (ID fan) which sucks flue gases out of the furnace and up the stack. Almost all induced draft furnaces have a negative pressure.

Forced draft: Draft is obtained by forcing air into the furnace by means of a fan (FD fan) and ductwork. Air is often passed through an air heater; which, as the name suggests, heats the air going into the furnace in order to increase the overall efficiency of the boiler. Dampers are used to control the quantity of air admitted to the furnace. Forced draft furnaces usually have a positive pressure.

Combination: The use of both induced and forced draft allows for the greatest level of draft control. This is more common with larger boilers where the flue gases have to travel a long distance through many boiler passes. The induced draft fan works in conjunction with the forced draft fan allowing the furnace pressure to be maintained slightly below atmospheric.

Straw Burning Boilers

The information in this section is generally accepted industry information, which was reported specifically in The Research Update printed in July, 1995 by the Alberta Farm Machinery Research Centre and the Prairie Agricultural Machinery Institute, and reviewed/revised on January 6, 2010 by the Agricultural Technology Centre of the Government of Alberta, Canada. This report, as well as information on the revision date, can be accessed at http://www1.agric.gov.ab.ca/$department/deptdocs.nsf/all/eng3127.

The use of straw as a heating fuel on the farm is growing in popularity because it helps to reduce the farm's dependency and related expenditures on fossil fuels and electricity, and it provides a practical and environmentally acceptable alternative to stubble burning. An inexpensive supply of fuel is usually close at hand. Most grain farms produce enough straw each year to supply a straw burning system. However, even if straw for fuel must be purchased, it is usually a worthwhile venture.

| 4 |

Burning straw for recovery of heat energy is a viable alternative use using excess straw produced on prairie farms. Large, whole bale burners are currently in general use on large British and Danish farms. A growing number of farmers are burning straw to heat their houses and workshops, and even to help dry their grain. Most farmers who heat with straw burners burn flax straw. Flax straw is advantageous due to its low ash content, and significant flamability. Most straw is burned as whole bales in large boilers. These furnaces produce heat with overall efficiencies of 30 - 60%.

The most common system for burning straw is an outdoor boiler used to heat water which is then piped to buildings. Economic feasibility of burning straw on large farms increases as system output increases. Using a large volume of water to store heat may significantly increase the efficiency of the system by causing it to operate at maximum capacity while straw is being burned. Therefore, a large straw burning system is most economical if a large heat load, usually for multiple buildings or grain drying, needs to be met.

There are four basic types of straw burners currently available:

- those that accept shredded, loose straw

- burners that use sifted straw products such as pellets, briquettes or cubes and straw logs

- square bale burners

- round bale burners.

Current loose straw burners are designed to operate on a large scale and require automatic stoking systems. They are built anticipating that operators will shred baled hay into loose straw. The capital investment and increased operating cost for energy to chop and feed the straw is beyond the practical capabilities of most farms.

Pellets, cubes and briquettes are very efficient forms of fuel but can be costly. Straw logs are generally more expensive, and therefore even less economical. Therefore, whole bale burners have separated themselves as the most practical straw burning systems for large boilers. Most such bale burners heat water which is in turn used to heat a home, workshop or similar building. Some, however, are set up as hot air systems.

The combustion chamber fuel capacity of a square bale burner can range from a single, standard square bale size to as many as six bales at a time. Although the fuel-to-heat conversion efficiencies of square bale burners are generally the lowest of all straw burners, averaging 30% to 40%, output is still more than adequate to heat a home or workshop.

A round bale burner has a more efficient output, and is generally larger, therefore, they are more practical when more than one building, or a very large building such as a greenhouse or hog barn, is being heated. A square bale burner will not likely be adequate for these purposes, or at least be too inconvenient because of the frequent need for re-stoking.

Lower Heat Value (“LHV”)

The information in this section is generally accepted scientific information, which was reported specifically in The Research Update printed in July, 1995 by the Alberta Farm Machinery Research Centre and the Prairie Agricultural Machinery Institute, and reviewed/revised on January 6, 2010 by the Agricultural Technology Centre of the Government of Alberta, Canada. This report, as well as information on the revision date, can be accessed at http://www1.agric.gov.ab.ca/$department/deptdocs.nsf/all/eng3127.

The energy content of a material is expressed in British Thermal Units per pound (BTU/lb) or megajoules per kilogram (MJ/kg). One MJ/kg is approximately equivalent to 430 BTU/lb. The maximum amount of energy available for use in a fuel is called the Lower Heat Value (LHV). The amount of moisture in the fuel affects the LHV because approximately 1170 BTU of energy is consumed by heating and evaporating each pound of water (2.72 MJ/kg). This energy would otherwise be used to create heat.

| 5 |

For example, the LHV of flax straw with a moisture content of 20% is 6635 BTU/lb (15.43 MJ/kg) while dry flax straw has a LHV of 8586 BTU/lb (19.97 MJ/kg). More than 22% of the potential heat production is consumed in drying the straw. This demonstrates the importance of drying straw before burning it in a boiler to maximize boiler fuel efficiency.

The table below gives a comparison of LHV for some common boiler fuels:

| Fuel | LHV | |||||||

| BTU/lb | MJ/kg | |||||||

| Propane | 19940 | 46.37 | ||||||

| #1 Fuel Oil | 15910 | 37.00 | ||||||

| Flax straw (dry) | 8587 | 19.97 | ||||||

| Wheat straw (dry) | 7680 | 17.86 | ||||||

| Flax straw (20% m.c.) | 6635 | 15.43 | ||||||

| Coal (lignite) | 6583 | 15.31 | ||||||

| Wood (15% m.c.) | 6450 | 15.00 | ||||||

| Wheat straw (20% m.c.) | 5908 | 13.74 | ||||||

Our Product

China’s rising demand for renewable and environmentally friendly energy sources in the face of the rising cost of electricity combined has resulted in what we anticipate will be a receptive potential market for our product. We are currently early in the process of designing and developing our straw-burning boiler prototype at our operations office in China. All of the raw materials related to the straw-burning boiler are available through the public marketplace. Our product is being designed to be installed in individual farm homes, initially only in China, and then later in other Asian countries.

As stated earlier, a large straw burning system is most economical if a large heat load, usually for multiple buildings or grain drying, needs to be met. However, we feel that smaller systems will be more efficient if heat load needs are much smaller, such as on individual family farms in China and elsewhere. China has millions of farmers who cultivate small plots of land. During the winter months, many of these farmers struggle to find the resources to heat their homes.

Following harvest, straw, stalks from grain, and other agricultural remnants litter fields and thrashing houses alike. These are combustible materials that can be used in straw-burning stoves described above. However, in order to be economical and feasible for rural farmers, the stoves must be smaller and serve a dual purpose. With this widespread need in mind, we have begun to develop a straw-burning boiler, which will also serve as a stove for food preparation.

| 6 |

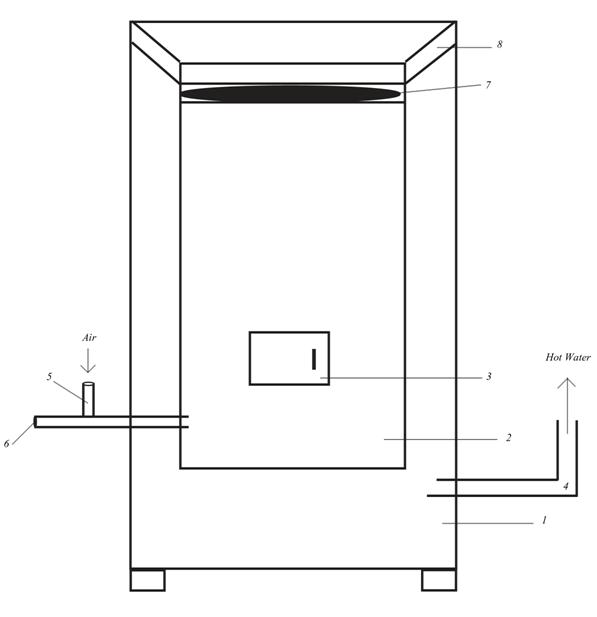

The diagram below shows how our product will work to generate heat and hot water for a house or other residential building, as well as provide a cooking surface:

Our product is a self-contained straw-burning boiler with a stove on top. The product is composed of a water tank (1) or water jacket, which encloses a metal combustion chamber (2) designed to contain a straw fire. There is a small door (3) to access the combustion chamber for adding straw. The fire heats the water, which is then circulated throughout the building in pipes (4). The heat from the hot water can be transferred to most existing heating systems (or simply transferred from the pipes into rooms as radiant heat) and the building's hot water supply.

A damper (5) and fan (6) on the boiler can be manually controlled in order to increase or decrease the heat output by the boiler. If more heat is needed, the damper can be opened to allow more air into the boiler, which will cause the fire to burn more intensely and increase the heat output. More air can be forced in and more heat generated by turning on the fan as well. The fire will then raise the temperature of the water which increases the heat supplied to the home.

| 7 |

In order to use the stove top (7) as a heat source for cooking, the insulating panel (8) on top of the boiler is simply removed and set aside. As it is constructed from highly insulating material, it should absorb little heat from the combustion chamber when in place, and also hold little residual heat when removed (reducing safety concerns).

Competition

We face substantial competition in the boiler market. We compete with a number of established manufacturers, importers and distributors who sell boilers in China. These companies enjoy brand recognition which exceeds that of our brand name. We compete with several manufacturers, importers and distributors who have significantly greater financial, distribution, advertising, and marketing resources than we do. We compete primarily on the basis of quality, brand name recognition, and price.

| § | Linhai Shengtian Wash Machinery Co., Ltd (“Linhai”) has been manufacturing boilers for home heating in China since 1992. They have nearly 200 employees, and a manufacturing plant over 8,200 square feet in size. They manufacture and supply a wide variety of boilers to wholesale and retail customers both in China and internationally. |

| § | Zhengzhou Brother Furnace Co., Ltd has been developing and manufacturing solutions to heating problems in China for 15 years. Using cutting edge technology, they supply boilers, furnaces, and other heating solutions to a wide variety of customers. While they produce a number of electric and oil based boilers, they do not currently have any straw burning boilers in their product line. Nor do they have any products directed specifically at rural farmers. |

| § | Guangzhou Devotion Thermal Facility Co., Ltd, a core member of Devotion group, also manufactures boilers in China. It is located in economic & technological development district of Guangzhou China. It is a national high-tech enterprise and stock company listed in the Singapore Stock Market (stock code 1523). Covering a manufacturing facility of 50,000 square meters, Guangzhou Devotion boasts a work force of 500 employees, including 100 engineers and technicians. They produce Gas/oil-fired Hot-water Boilers, Gas/oil-fired Thermal Oil Heaters, Gas/oil-fired Steam Boiler, Electric Hot-water/Steam Boiler, Coal-fired Steam/Hot Water Boilers, and Wall-Mounted Boilers for customers throughout China and Southeast Asia. |

Intellectual Property

We intend to aggressively assert our rights under trade secret, unfair competition, trademark and copyright laws to protect our intellectual property, including proprietary manufacturing processes and technologies, product research and concepts, and recognized trademarks. These rights are protected through the acquisition of patents and trademark registrations, the maintenance of trade secrets, the development of trade dress, and, where appropriate, litigation against those who are, in our opinion, infringing these rights.

We are currently consulting with law firms to protect our brand name and product design. While there can be no assurance that registered trademarks will protect our proprietary information, we intend to assert our intellectual property rights against any infringer. Although any assertion of our rights can result in a substantial cost to, and diversion of effort by, our company, management believes that the protection of our intellectual property rights is a key component of our operating strategy.

Regulatory Matters

We are subject to the laws and regulations of those jurisdictions in which we plan to sell our product, which are generally applicable to business operations, such as business licensing requirements, income taxes, and payroll taxes. In general, the sale of our product in China is not subject to special regulatory and/or supervisory requirements.

| 8 |

Employees

We have no other employees other than our sole officer and director. Our President is the only employee of the company. He oversees all responsibilities in the areas of corporate administration, business development and research. If finances permit, however, we intend to expand our current management to retain skilled directors, officers and employees with experience relevant to our business focus. Our current management team is highly skilled in technical areas such as researching and developing our product, but not skilled in areas such as marketing our product and business management. Obtaining the assistance of individuals with an in-depth knowledge of operations and marketing will allow us to build market share more effectively.

A smaller reporting company is not required to provide the information required by this Item.

Item 1B. Unresolved Staff Comments

A smaller reporting company is not required to provide the information required by this Item.

We do not lease or own any real property. We maintain our offices at Tian Bei W. Rd., Yung Guang Tian Di Ming Xing Ge, Unit 1503, Shenzhen, China. This office space is being provided free of charge by our officer and director, Li Deng Ke.

We are not a party to any pending legal proceeding. We are not aware of any pending legal proceeding to which any of our officers, directors, or any beneficial holders of 5% or more of our voting securities are adverse to us or have a material interest adverse to us.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity and Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

There is presently no public market for our common stock. We have made an application through a market maker for quotation of our common stock on the FINRA over the counter bulletin board. We can provide no assurance that our shares will be quoted on the bulletin board, or if quoted, that a public market will materialize.

| 9 |

Penny Stock

The Securities Exchange Commission has adopted rules that regulate broker-dealer practices in connection with transactions in penny stocks. Penny stocks are generally equity securities with a price of less than $5.00, other than securities registered on certain national securities exchanges or quoted on the NASDAQ system, provided that current price and volume information with respect to transactions in such securities is provided by the exchange or system. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock, to deliver a standardized risk disclosure document prepared by the Commission, that: (a) contains a description of the nature and level of risk in the market for penny stocks in both public offerings and secondary trading;(b) contains a description of the broker's or dealer's duties to the customer and of the rights and remedies available to the customer with respect to a violation to such duties or other requirements of Securities' laws; (c) contains a brief, clear, narrative description of a dealer market, including bid and ask prices for penny stocks and the significance of the spread between the bid and ask price;(d) contains a toll-free telephone number for inquiries on disciplinary actions;(e) defines significant terms in the disclosure document or in the conduct of trading in penny stocks; and;(f) contains such other information and is in such form, including language, type, size and format, as the Commission shall require by rule or regulation.

The broker-dealer also must provide, prior to effecting any transaction in a penny stock, the customer with; (a) bid and offer quotations for the penny stock;(b) the compensation of the broker-dealer and its salesperson in the transaction;(c) the number of shares to which such bid and ask prices apply, or other comparable information relating to the depth and liquidity of the market for such stock; and (d) a monthly account statements showing the market value of each penny stock held in the customer's account.

In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from those rules; the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser's written acknowledgment of the receipt of a risk disclosure statement, a written agreement to transactions involving penny stocks, and a signed and dated copy of a written suitability statement.

These disclosure requirements may have the effect of reducing the trading activity in the secondary market for our stock if it becomes subject to these penny stock rules. Therefore, because our common stock is subject to the penny stock rules, stockholders may have difficulty selling those securities.

Holders of Our Common Stock

Currently, we have thirty-eight (38) holders of record of our common stock.

Stock Option Grants

To date, we have not granted any stock options.

Dividends

There are no restrictions in our articles of incorporation or bylaws that prevent us from declaring dividends. The Nevada Revised Statutes, however, do prohibit us from declaring dividends where after giving effect to the distribution of the dividend:

| 1. | we would not be able to pay our debts as they become due in the usual course of business, or; |

| 2. | our total assets would be less than the sum of our total liabilities plus the amount that would be needed to satisfy the rights of shareholders who have preferential rights superior to those receiving the distribution. |

We have not declared any dividends and we do not plan to declare any dividends in the foreseeable future.

| 10 |

Recent Sales of Unregistered Securities

On August 31, 2010, we issued 637,500 shares of common stock to Li Deng Ke, our President and Director. These shares were issued pursuant to Regulation S of the Securities Act of 1933 (the “Securities Act”) at a price of $0.02 per share, for total proceeds of $12,750. The 637,500 shares of common stock are restricted shares as defined in the Securities Act.

On August 31, 2010, we issued 637,500 shares of common stock to Xiong Chao Jun, our director. These shares were issued pursuant to Regulation S of the Securities Act at a price of $0.02 per share, for total proceeds of $12,750. The 637,500 shares of common stock are restricted shares as defined in the Securities Act.

On December 15, 2010, we completed a private placement of 1,350,000 shares of our common stock pursuant to Regulation S of the 1933 Act. All shares were issued at a price of $0.02 per share. We received proceeds of $27,000 from the offering. Each purchaser represented to us that the purchaser was a Non-US Person as defined in Regulation S. We did not engage in a distribution of this offering in the United States. Each purchaser represented their intention to acquire the securities for investment only and not with a view toward distribution. All purchasers were given adequate access to sufficient information about us to make an informed investment decision. None of the securities were sold through an underwriter and accordingly, there were no underwriting discounts or commissions involved. The selling stockholders named in this prospectus include all of the purchasers who purchased shares pursuant to this Regulation S offering.

Securities Authorized for Issuance under Equity Compensation Plans

We did not issue any securities under any equity compensation plan as of March 31, 2012.

Item 6. Selected Financial Data

A smaller reporting company is not required to provide the information required by this Item.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

Certain statements, other than purely historical information, including estimates, projections, statements relating to our business plans, objectives, and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements generally are identified by the words “believes,” “project,” “expects,” “anticipates,” “estimates,” “intends,” “strategy,” “plan,” “may,” “will,” “would,” “will be,” “will continue,” “will likely result,” and similar expressions. We intend such forward-looking statements to be covered by the safe-harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, and are including this statement for purposes of complying with those safe-harbor provisions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties which may cause actual results to differ materially from the forward-looking statements. Our ability to predict results or the actual effect of future plans or strategies is inherently uncertain. Factors which could have a material adverse affect on our operations and future prospects on a consolidated basis include, but are not limited to: changes in economic conditions, legislative/regulatory changes, availability of capital, interest rates, competition, and generally accepted accounting principles. These risks and uncertainties should also be considered in evaluating forward-looking statements and undue reliance should not be placed on such statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise. Further information concerning our business, including additional factors that could materially affect our financial results, is included herein and in our other filings with the SEC.

| 11 |

Results of Operations for the Year Ended March 31, 2012 and Period from Inception (August 9, 2010) through March 31, 2012 and 2011

We generated no revenue for the period from August 9, 2010 (Date of Inception) until March 31, 2012. We had operating expenses of $31,891 for the year ended March 31, 2012, and operating expenses of $50,580 from August 9, 2010 (Date of Inception) until March 31, 2012. Our operating expenses consisting entirely of organizational expenses and professional fees. We, therefore, recorded a net loss of $31,891 for the year ended March 31, 2012, and $50,580 for the period from August 9, 2010 (Date of Inception) until March 31, 2012.

We anticipate our operating expenses will increase as we implement our business plan. The increase will be attributable to expenses

to implement our business plan, and the professional fees to be incurred in connection with our ongoing filing requirements as

a reporting company under the Securities Exchange Act of 1934.

Liquidity and Capital Resources

As of March 31, 2012, we had total current assets of $12,500 and current liabilities of $10,580. Thus, we have working capital of $1,920 as of March 31, 2012.

Operating activities used $44,000 in cash for the period from August 9, 2010 (Date of Inception) until March 31, 2012. Our net loss of $50,580 represented all of our negative operating cash flow offset by an increase in accrued expenses of $6,580. Financing activities during the period from August 9, 2010 (Date of Inception) to March 31, 2012 generated $56,500 in cash during the period.

As of March 31, 2012, we have insufficient cash to operate our business at the current level for the next twelve months and insufficient cash to achieve our business goals. The success of our business plan beyond the next 12 months is contingent upon us obtaining additional financing. We intend to fund operations through debt and/or equity financing arrangements, which may be insufficient to fund our capital expenditures, working capital, or other cash requirements. We do not have any formal commitments or arrangements for the sales of stock or the advancement or loan of funds at this time. There can be no assurance that such additional financing will be available to us on acceptable terms, or at all.

Going Concern

The accompanying financial statements have been prepared in conformity with generally accepted accounting principle, which contemplate continuation of us as a going concern. However, we have accumulated deficit of $50,580 as of March 31, 2012. We currently have limited liquidity, and have not completed our efforts to establish a stabilized source of revenues sufficient to cover operating costs over an extended period of time.

Management anticipates that we will be dependent, for the near future, on additional investment capital to fund operating expenses. We intend to position the company so that it may be able to raise additional funds through the capital markets. In light of management’s efforts, there are no assurances that we will be successful in this or any of our endeavors or become financially viable and continue as a going concern.

Off Balance Sheet Arrangements

As of March 31, 2012, there were no off balance sheet arrangements.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

A smaller reporting company is not required to provide the information required by this Item.

| 12 |

Item 8. Financial Statements and Supplementary Data

Index to Financial Statements Required by Article 8 of Regulation S-X:

Audited Financial Statements:

| 13 |

Silberstein Ungar, PLLC CPAs and Business Advisors

Phone (248) 203-0080

Fax (248) 281-0940

30600 Telegraph Road, Suite 2175

Bingham Farms, MI 48025-4586

www.sucpas.com

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Boards of Directors

Nepia, Inc.

Shenzhen, China

We have audited the accompanying balance sheets of Nepia, Inc., as of March 31, 2012 and 2011, and the related statements of operations, stockholders’ equity, and cash flows for the periods then ended and the period from August 9, 2010 (date of inception) to March 31, 2012. These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement. The Company has determined that it is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Nepia, Inc., as of March 31, 2012 and 2011 and the results of its operations and cash flows for the periods then ended and the period from August 9, 2010 (date of inception) to March 31, 2012, in conformity with accounting principles generally accepted in the United States of America.

The accompanying financial statements have been prepared assuming that the Nepia, Inc. will continue as a going concern. As discussed in Note 8 to the financial statements, the Company has not received revenue from sales of products or services, and has incurred losses from operations since inception. These factors raise substantial doubt about the Company’s ability to continue as a going concern. Management’s plans with regard to these matters are described in Note 8. The accompanying financial statements do not include any adjustments that might result from the outcome of this uncertainty.

/s/ Silberstein Ungar, PLLC

Silberstein Ungar, PLLC

Bingham Farms, Michigan

June 22, 2012

| F-1 |

NEPIA, INC.

(A DEVELOPMENT STAGE COMPANY)

AS OF MARCH 31, 2012 AND 2011

| 2012 | 2011 | |||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and equivalents | $ | 12,500 | $ | 29,811 | ||||

| Prepaid expenses | 0 | 4,000 | ||||||

| TOTAL ASSETS | $ | 12,500 | $ | 33,811 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Accrued expenses | $ | 6,580 | $ | 0 | ||||

| Due to officer | 4,000 | 0 | ||||||

| Total Liabilities | $ | 10,580 | 0 | |||||

| Stockholders’ Equity | ||||||||

| Common Stock, $.001 par value, 90,000,000 shares authorized, 2,625,000 shares issued and outstanding | 2,625 | 2,625 | ||||||

| Preferred Stock, $.001 par value, 10,000,000 shares authorized, -0- shares issued and outstanding | 0 | 0 | ||||||

| Additional paid-in capital | 49,875 | 49,875 | ||||||

| Deficit accumulated during the development stage | (50,580 | ) | (18,689 | ) | ||||

| Total stockholders’ equity | 1,920 | 33,811 | ||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 12,500 | $ | 33,811 | ||||

See accompanying notes to financial statements.

| F-2 |

NEPIA, INC.

(A DEVELOPMENT STAGE COMPANY)

FOR THE PERIODS ENDED MARCH 31, 2012 AND 2011

FOR THE PERIOD FROM AUGUST 9, 2010 (INCEPTION) TO MARCH 31, 2012

| Year ended March 31, 2012 | Period from August 9, 2010 (Inception) to March 31, 2011 | Period from August 9, 2010 (Inception) to March 31, 2012 | ||||||||||

| REVENUES | $ | 0 | $ | 0 | $ | 0 | ||||||

| OPERATING EXPENSES | ||||||||||||

| Organization costs | 0 | 320 | 320 | |||||||||

| Professional fees | 31,891 | 18,369 | 50,260 | |||||||||

| TOTAL OPERATING EXPENSES | 31,891 | 18,689 | 50,580 | |||||||||

| LOSS FROM OPERATIONS | (31,891 | ) | (18,689 | ) | (50,580 | ) | ||||||

| PROVISION FOR INCOME TAXES | 0 | 0 | 0 | |||||||||

| NET LOSS | $ | (31,891 | ) | $ | (18,689 | ) | $ | (50,580 | ) | |||

| NET LOSS PER SHARE: BASIC AND DILUTED | $ | (0.01 | ) | $ | (0.01 | ) | ||||||

| WEIGHTED AVERAGE NUMBER OF SHARES OUTSTANDING: BASIC AND DILUTED | 2,625,000 | 2,625,000 | ||||||||||

See accompanying notes to financial statements.

| F-3 |

NEPIA, INC.

(A DEVELOPMENT STAGE COMPANY)

STATEMENT OF STOCKHOLDERS’ EQUITY

FOR THE PERIOD FROM AUGUST 9, 2010 (INCEPTION) TO MARCH 31, 2012

| Common Stock | Additional Paid in | Deficit Accumulated During the Development | Total Stockholders’ | |||||||||||||||||

| Shares | Amount | Capital | Stage | Equity | ||||||||||||||||

| Inception, August 9, 2010 | — | $ | — | $ | — | $ | — | $ | — | |||||||||||

| Issuance of common stock for cash at $0.02 per share | 2,625,000 | 2,625 | 49,875 | — | 52,500 | |||||||||||||||

| Net loss for the period ended March 31, 2011 | — | — | — | (18,689 | ) | (18,689 | ) | |||||||||||||

| Balance, March 31, 2011 | 2,625,000 | 2,625 | 49,875 | (18,689 | ) | 33,811 | ||||||||||||||

| Net loss for the year ended March 31, 2012 | — | — | — | (31,891 | ) | (31,891 | ) | |||||||||||||

| Balance, March 31, 2012 | 2,625,000 | $ | 2,625 | $ | 49,875 | $ | (50,580 | ) | $ | 1,920 | ||||||||||

See accompanying notes to financial statements.

| F-4 |

NEPIA, INC.

(A DEVELOPMENT STAGE COMPANY)

FOR THE PERIODS ENDED MARCH 31, 2012 AND 2011

FOR THE PERIOD FROM AUGUST 9, 2010 (INCEPTION) TO MARCH 31, 2012

| Year ended March 31, 2012 | Period from August 9, 2010 (Inception) to March 31, 2011 | Period from August 9, 2010 (Inception) to March 31, 2012 | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | ||||||||||||

| Net loss for the period | $ | (31,891 | ) | $ | (18,689 | ) | $ | (50,580 | ) | |||

| Adjustments To Reconcile Net Loss To Net Cash Used In Operating Activities | ||||||||||||

| Changes in operating assets and liabilities: | ||||||||||||

| (Increase) decrease in prepaid expenses | 4,000 | (4,000 | ) | 0 | ||||||||

| Increase in accrued expenses | 6,580 | 0 | 6,580 | |||||||||

| Net Cash Used by Operating Activities | (21,311 | ) | (22,689 | ) | (44,000 | ) | ||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | ||||||||||||

| Increase in due to officer | 4,000 | 0 | 4,000 | |||||||||

| Proceeds from sale of common stock | 0 | 52,500 | 52,500 | |||||||||

| Net Cash Provided by Financing Activities | 4,000 | 52,500 | 56,500 | |||||||||

| Net Increase (Decrease) in Cash and Cash Equivalents | (17,311 | ) | 29,811 | 12,500 | ||||||||

| Cash and cash equivalents, beginning of period | 29,811 | 0 | 0 | |||||||||

| Cash and cash equivalents, end of period | $ | 12,500 | $ | 29,811 | $ | 12,500 | ||||||

| SUPPLEMENTAL CASH FLOW INFORMATION: | ||||||||||||

| Interest paid | $ | 0 | $ | 0 | ||||||||

| Income taxes paid | $ | 0 | $ | 0 | ||||||||

See accompanying notes to financial statements.

| F-5 |

NEPIA, INC.

(A DEVELOPMENT STAGE COMPANY)

NOTES TO THE FINANCIAL STATEMENTS

MARCH 31, 2012

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Business

Nepia, Inc. (“Nepia” and the “Company”) is a development stage company and was incorporated in Nevada on August 9, 2010. The Company plans to develop, manufacture, and sell small boilers aimed at farmers primarily in Southeast Asia.

Development Stage Company

The accompanying financial statements have been prepared in accordance with generally accepted accounting principles related to development-stage companies. A development-stage company is one in which planned principal operations have not commenced or if its operations have commenced, and there has been no significant revenues there from.

Basis of Presentation

The financial statements of the Company have been prepared using the accrual basis of accounting in accordance with generally accepted accounting principles in the United States of America and are presented in U.S. dollars. The Company has adopted a March 31 fiscal year end.

Cash and Cash Equivalents

Nepia considers all highly liquid investments with maturities of three months or less to be cash equivalents. At March 31, 2012 and 2011 the Company had $12,500 and $29,811, respectively, of unrestricted cash that was being held in an escrow account by its outside attorneys, to be used for future business operations.

Fair Value of Financial Instruments

Nepia’s financial instruments consist of cash and cash equivalents, prepaid expenses, accrued expenses and an amount due to an officer. The carrying amount of these financial instruments approximates fair value due either to length of maturity or interest rates that approximate prevailing market rates unless otherwise disclosed in these financial statements.

Income Taxes

Income taxes are computed using the asset and liability method. Under the asset and liability method, deferred income tax assets and liabilities are determined based on the differences between the financial reporting and tax bases of assets and liabilities and are measured using the currently enacted tax rates and laws. A valuation allowance is provided for the amount of deferred tax assets that, based on available evidence, are not expected to be realized.

Stock-Based Compensation

Stock-based compensation is accounted for at fair value in accordance with ASC Topic 718. To date, the Company has not adopted a stock option plan and has not granted any stock options.

Basic loss per share

The basic earnings (loss) per share is calculated by dividing the Company’s net income available to common shareholders by the weighted average number of common shares during the year. The diluted earnings (loss) per share is calculated by dividing the Company’s net income (loss) available to common shareholders by the diluted weighted average number of shares outstanding during the year. The diluted weighted average number of shares outstanding is the basic weighted number of shares adjusted as of the first of the year for any potentially dilutive debt or equity. The Company has not issued any options or warrants or similar securities since inception.

| F-6 |

NEPIA, INC.

(A DEVELOPMENT STAGE COMPANY)

NOTES TO THE FINANCIAL STATEMENTS

MARCH 31, 2012

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Revenue Recognition

The Company will recognize revenue when products are fully delivered or services have been provided and collection is reasonably assured.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

Recent Accounting Pronouncements

The Company does not expect the adoption of recently issued accounting pronouncements to have a significant impact on the Company’s results of operations, financial position or cash flow.

NOTE 2 – PREPAID EXPENSES

Prepaid expenses of $4,000 at March 31, 2011 consisted of an advance retainer paid to the Company’s outside auditors for services to be rendered for periods after March 31, 2011. The amount was expensed during the year ended March 31, 2012. Prepaid expenses were $0 as of March 31, 2012.

NOTE 3 – ACCRUED EXPENSES

Accrued expenses consisted of the following as of March 31, 2012 and 2011:

| 2012 | 2011 | |||||||

| Audit fees | $ | 2,500 | $ | 0 | ||||

| Legal fees | 2,150 | 0 | ||||||

| Transfer agent fees | 1,930 | 0 | ||||||

| Total Accrued Expenses | $ | 6,580 | $ | 0 | ||||

NOTE 4 – DUE TO OFFICER

An officer has loaned the company funds to help support operations. The amount is unsecured, non-interest bearing and due on demand. The total due to the officer was $4,000 and $0 as of March 31, 2012 and 2011, respectively.

NOTE 5 – COMMITMENTS AND CONTINGENCIES

Nepia neither owns nor leases any real or personal property. An officer has provided office services without charge. There is no obligation for the officer to continue this arrangement. Such costs are immaterial to the financial statements and accordingly are not reflected herein. The officers and directors are involved in other business activities and most likely will become involved in other business activities in the future.

| F-7 |

NEPIA, INC.

(A DEVELOPMENT STAGE COMPANY)

NOTES TO THE FINANCIAL STATEMENTS

MARCH 31, 2012

NOTE 6 – CAPITAL STOCK

The Company has 90,000,000 common shares authorized with a par value of $ 0.001 per share.

The Company has 10,000,000 preferred shares authorized with a par value of $ 0.001 per share.

At inception, the Company issued 2,625,000 shares of common stock at $0.02 per share for total cash proceeds of $52,500.

There were 2,625,000 shares of common stock issued and outstanding as of March 31, 2012 and 2011.

There were 0 shares of preferred stock issued and outstanding as of March 31, 2012 and 2011.

NOTE 7 – INCOME TAXES

As of March 31, 2012, the Company had net operating loss carry forwards of approximately $51,000 that may be available to reduce future years’ taxable income in varying amounts through 2032. Future tax benefits which may arise as a result of these losses have not been recognized in these financial statements, as their realization is determined not likely to occur and accordingly, the Company has recorded a valuation allowance for the deferred tax asset relating to these tax loss carry-forwards.

The provision for Federal income tax consists of the following for the periods ended March 31, 2012 and 2011:

| 2012 | 2011 | |||||||

| Federal income tax benefit attributable to: | ||||||||

| Current operations | $ | 10,843 | $ | 6,354 | ||||

| Less: valuation allowance | (10,843 | ) | (6,354 | ) | ||||

| Net provision for Federal income taxes | $ | 0 | $ | 0 | ||||

The cumulative tax effect at the expected rate of 34% of significant items comprising our net deferred tax amount is as follows as of March 31, 2012 and 2011:

| 2012 | 2011 | |||||||

| Deferred tax asset attributable to: | ||||||||

| Net operating loss carryover | $ | 17,197 | $ | 6,354 | ||||

| Less: valuation allowance | (17,197 | ) | (6,354 | ) | ||||

| Net deferred tax asset | $ | 0 | $ | 0 | ||||

Due to the change in ownership provisions of the Tax Reform Act of 1986, net operating loss carry forwards of approximately $51,000 for Federal income tax reporting purposes are subject to annual limitations. Should a change in ownership occur net operating loss carry forwards may be limited as to use in future years.

| F-8 |

NEPIA, INC.

(A DEVELOPMENT STAGE COMPANY)

NOTES TO THE FINANCIAL STATEMENTS

MARCH 31, 2012

NOTE 8 – LIQUIDITY AND GOING CONCERN

Nepia has limited working capital and has not yet received revenues from sales of products or services. These factors create substantial doubt about the Company’s ability to continue as a going concern. The financial statements do not include any adjustment that might be necessary if the Company is unable to continue as a going concern.

The ability of Nepia to continue as a going concern is dependent on the Company generating cash from the sale of its common stock and/or obtaining debt financing and attaining future profitable operations. Management’s plans include selling its equity securities and obtaining debt financing to fund its capital requirement and ongoing operations; however, there can be no assurance the Company will be successful in these efforts.

NOTE 9 – SUBSEQUENT EVENTS

In accordance with ASC 855-10, the Company has analyzed its operations subsequent to March 31, 2012 to the date these financial statements were issued, and has determined that it does not have any material subsequent events to disclose in these financial statements.

| F-9 |

Item 9. Changes In and Disagreements with Accountants on Accounting and Financial Disclosure

None

Item 9A. Controls and Procedures

Disclosure Controls and Procedures

As required by Rule 13a-15 under the Securities Exchange Act of 1934, we have carried out an evaluation of the effectiveness of our disclosure controls and procedures as of the end of the period covered by this annual report, being March 31, 2012. This evaluation was carried out under the supervision and with the participation of our management, including our Chief Executive Officer and Chief Financial Officer.

Disclosure controls and procedures are controls and other procedures that are designed to ensure that information required to be disclosed in our reports filed or submitted under the Securities Exchange Act of 1934 is recorded, processed, summarized and reported, within the time periods specified in the Securities and Exchange Commission’s rules and forms. Disclosure controls and procedures include controls and procedures designed to ensure that information required to be disclosed in our company’s reports filed under the Securities Exchange Act of 1934 is accumulated and communicated to management, including our Chief Executive Officer and Chief Financial Officer, to allow timely decisions regarding required disclosure.

Based upon that evaluation, including our Chief Executive Officer and Chief Financial Officer, we have concluded that our disclosure controls and procedures were ineffective as of the end of the period covered by this annual report.

Management’s Report on Internal Control over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting (as defined in Rule 13a-15(f) under the Securities Exchange Act of 1934). Management has assessed the effectiveness of our internal control over financial reporting as of March 31, 2012 based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. As a result of this assessment, management concluded that, as of March 31, 2012, our internal control over financial reporting was not effective. Our management identified the following material weaknesses in our internal control over financial reporting, which are indicative of many small companies with small staff: (i) inadequate segregation of duties and effective risk assessment; and (ii) insufficient written policies and procedures for accounting and financial reporting with respect to the requirements and application of both US GAAP and SEC guidelines.

We plan to take steps to enhance and improve the design of our internal control over financial reporting. During the period covered by this annual report on Form 10-K, we have not been able to remediate the material weaknesses identified above. To remediate such weaknesses, we hope to implement the following changes during our fiscal year ending March 31, 2013: (i) appoint additional qualified personnel to address inadequate segregation of duties and ineffective risk management; and (ii) adopt sufficient written policies and procedures for accounting and financial reporting. The remediation efforts set out in (i) and (ii) are largely dependent upon our securing additional financing to cover the costs of implementing the changes required. If we are unsuccessful in securing such funds, remediation efforts may be adversely affected in a material manner.

This annual report does not include an attestation report of our registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by our registered public accounting firm pursuant to an exemption for non-accelerated filers set forth in Section 989G of the Dodd-Frank Wall Street Reform and Consumer Protection Act.

| 14 |

Remediation of Material Weakness

We are unable to remedy our controls related to the inadequate segregation of duties and ineffective risk management until we receive financing to hire additional employees. We are currently in the process of hiring an outsourced controller to improve the controls for accounting and financial reporting.

Limitations on the Effectiveness of Internal Controls

Our management, including our Chief Executive Officer and our Chief Financial Officer, does not expect that our disclosure controls and procedures or our internal control over financial reporting are or will be capable of preventing or detecting all errors or all fraud. Any control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the control system’s objectives will be met. The design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Further, because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that misstatements, due to error or fraud will not occur or that all control issues and instances of fraud, if any, within the company have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty and that breakdowns may occur because of simple error or mistake. Controls can also be circumvented by the individual acts of some persons, by collusion of two or more people, or by management override of controls. The design of any system of controls is based in part on certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Projections of any evaluation of controls effectiveness to future periods are subject to risk.

None

PART III

Item 10. Directors, Executive Officers and Corporate Governance

We have two executive officers and one director. As of March 31, 2012, these persons are as follows:

| Name | Age | Position Held with the Company | ||||

| Li Deng Ke Tian Bei W. Rd. Yung Guang Tian Di Ming Xing Ge, Unit 1503, Shenzhen, China | 26 | President, Chief Executive Officer, Principal Executive Officer, Chief Financial Officer, Principal Financial Officer, Principal Accounting Officer, and Director | ||||

| Xiong Chao Jun Tian Bei W. Rd. Yung Guang Tian Di Ming Xing Ge, Unit 1503, Shenzhen, China | 37 | Director |

Set forth below is a brief description of the background and business experience of our executive officers and directors.

| 15 |

Li Deng Ke is our President, Chief Executive Officer, Principal Executive Officer, Chief Financial Officer, Principal Financial Officer, Principal Accounting President and Director. In 2006, Mr. Ke received his Bachelor of Science degree from Sichuan Normal University in Chengdu, Sichuan, China. In addition to being our sole executive officer, since 2006 Mr. Ke has been employed as a technician for KTV Ltd.

Xiong Chao Jun is our Director. In 1996, Mr. Jun received his Bachelor of Science degree from Hunan Industrial University in Changsha, Hunan. Since 1999 he has been employed as a sale manager for KTV Ltd.

Term of Office

Our directors are appointed for a one-year term to hold office until the next annual general meeting of our shareholders or until removed from office in accordance with our bylaws. Our officers are appointed by our board of directors and hold office until removed by the board.

Family Relationships

There are no family relationships between or among the directors, executive officers or persons nominated or chosen by us to become directors or executive officers.

Involvement in Certain Legal Proceedings

To the best of our knowledge, during the past ten years, none of the following occurred with respect to a present or former director, executive officer, or employee: (1) any bankruptcy petition filed by or against any business of which such person was a general partner or executive officer either at the time of the bankruptcy or within two years prior to that time; (2) any conviction in a criminal proceeding or being subject to a pending criminal proceeding (excluding traffic violations and other minor offenses); (3) being subject to any order, judgment or decree, not subsequently reversed, suspended or vacated, of any court of competent jurisdiction, permanently or temporarily enjoining, barring, suspending or otherwise limiting his or her involvement in any type of business, securities or banking activities; and (4) being found by a court of competent jurisdiction (in a civil action), the SEC or the Commodities Futures Trading Commission to have violated a federal or state securities or commodities law, and the judgment has not been reversed, suspended or vacated.

Committees of the Board

Our company currently does not have nominating, compensation or audit committees or committees performing similar functions nor does our company have a written nominating, compensation or audit committee charter. Our directors believe that it is not necessary to have such committees, at this time, because the functions of such committees can be adequately performed by the board of directors.

Our company does not have any defined policy or procedural requirements for shareholders to submit recommendations or nominations for directors. The board of directors believes that, given the stage of our development, a specific nominating policy would be premature and of little assistance until our business operations develop to a more advanced level. Our company does not currently have any specific or minimum criteria for the election of nominees to the board of directors and we do not have any specific process or procedure for evaluating such nominees. The board of directors will assess all candidates, whether submitted by management or shareholders, and make recommendations for election or appointment.

A shareholder who wishes to communicate with our board of directors may do so by directing a written request addressed to our CEO and director, Li Deng Ke, at the address appearing on the first page of this annual report.

| 16 |

Code of Ethics

We have not adopted a Code of Ethics that applies our principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions.

Item 11. Executive Compensation

The table below summarizes all compensation awarded to, earned by, or paid to our executive officer for all services rendered in

all capacities to us for the periods ended March 31, 2012 and 2011.

| SUMMARY COMPENSATION TABLE | |||||||||

|

Name and principal position |

Year | Salary ($) |

Bonus ($) |

Stock Awards ($) |

Option Awards ($) |

Non-Equity Incentive Plan Compensation ($) |

Nonqualified Deferred Compensation Earnings ($) |

All Other Compensation ($) |

Total ($) |

| Li Deng Ke, President, Chief Executive Officer, Principal Executive Officer, Chief Financial Officer, Principal Financial Officer,Principal Accounting Officer, and Director |

2012 2011 |

0 0 |

0 0 |

0 0 |

0 0 |

0 0 |

0 0 |

0 0 |

0 0 |

Narrative Disclosure to Summary Compensation Table

Although we do not currently compensate our officers, we reserve the right to provide compensation at some time in the future. Our decision to compensate officers depends on the availability of our cash resources with respect to the need for cash to further business purposes.

Outstanding Equity Awards at Fiscal Year-End

The table below summarizes all unexercised options, stock that has not vested, and equity incentive plan awards for each named executive officer as of March 31, 2012.

| OUTSTANDING EQUITY AWARDS AT FISCAL YEAR-END | |||||||||

| OPTION AWARDS | STOCK AWARDS | ||||||||

| Name | Number of Securities Underlying Unexercised Options (#) Exercisable | Number of Securities Underlying Unexercised Options (#) Unexercisable | Equity Incentive Plan Awards: Number of Securities Underlying Unexercised Unearned Options (#) | Option Exercise Price ($) | Option Expiration Date | Number of Shares or Units of Stock That Have Not Vested (#) |

Market Value of Shares or Units of Stock That Have Not Vested ($) |

Equity Incentive Plan Awards: Number of Unearned Shares, Units or Other Rights That Have Not Vested (#) |

Equity Incentive Plan Awards: Market or Payout Value of Unearned Shares, Units or Other Rights That Have Not Vested (#) |

| Li Deng Ke | - | - | - | - | - | - | - | - | - |

| 17 |

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

The following table sets forth, as of June 7, 2012 , certain information as to shares of our common stock owned by (i) each person known by us to beneficially own more than 5% of our outstanding common stock, (ii) each of our directors, and (iii) all of our executive officers and directors as a group:

| Name and Address of Beneficial Owners of Common Stock |

Title of Class | Amount and Nature of Beneficial Ownership 1 |

% of Common Stock 2 |

|

Li Deng Ke Tian Bei W. Rd. Yung Guang Tian Di Ming Xing Ge, Unit 1503, Shenzhen, China |

Common Stock | 637,500 Shares | 24% |

|

Xiong Chao Jun Tian Bei W. Rd. Yung Guang Tian Di Ming Xing Ge, Unit 1503, Shenzhen, China

|

Common Stock | 637,500 Shares | 24% |

| DIRECTORS AND OFFICERS – TOTAL (One Officer and Two Directors) | 1,275,000 Shares | 48% | |

| 5% SHAREHOLDERS | |||

| NONE | Common Stock |

| 1. | As used in this table, "beneficial ownership" means the sole or shared power to vote, or to direct the voting of, a security, or the sole or shared investment power with respect to a security (i.e., the power to dispose of, or to direct the disposition of, a security). In addition, for purposes of this table, a person is deemed, as of any date, to have "beneficial ownership" of any security that such person has the right to acquire within 60 days after such date. |

| 2. | The percentage shown is based on denominator of 2,625,000 shares of common stock issued and outstanding for the company as of June 26, 2012. |

Item 13. Certain Relationships and Related Transactions, and Director Independence

Since March 1, 2011 there have not been, and there is not currently proposed, any transaction or series of similar transactions to which we were or will be a participant in which the amount involved exceeded or will exceed the lesser of $120,000 or one percent of the average of our total assets at year-end for the last two completed fiscal years, and in which any director, executive officer, holder of 5% or more of any class of our capital stock or any member of the immediate family of any of the foregoing persons had or will have a direct or indirect material interest.

| 18 |

Item 14. Principal Accounting Fees and Services

Below is the table of Audit Fees billed by our auditors in connection with the audits of the Company’s annual financial statements for the years ended:

| Financial Statements for the Year Ended March 31 | Audit Services | Audit Related Fees | Tax Fees | Other Fees | ||||||||||||

| 2012 | $8,000 | $ | 0 | $ | 0 | $ | 0 | |||||||||

| 2011 | $8,750 | $ | 0 | $ | 0 | $ | 0 | |||||||||

PART IV

Item 15. Exhibits, Financial Statements Schedules

| (a) | Financial Statements and Schedules |

The following financial statements and schedules listed below are included in this Form 10-K.

Financial Statements (See Item 8)

| (b) | Exhibits |

| 1 | Incorporated by reference to the Registration Statement on Form S-1 filed on April 25, 2011. |

| 19 |

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Nepia, Inc.

By: /s/ Li Deng Ke

Li Deng Ke

President, Chief Executive Officer, Principal Executive Officer,

Chief Financial Officer, Principal Financial Officer,

Principal Accounting Officer, and Director

July 11, 2012

Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

By: /s/ Li Deng Ke

Li Deng Ke

President, Chief Executive Officer, Principal Executive Officer,

Chief Financial Officer, Principal Financial Officer,

Principal Accounting Officer, and Director

July 11, 2012

By: /s/ Xiong Chao Jun

Xiong Chao Jun

Director

July 11, 2012

| 20 |