As filed with the Securities and Exchange Commission on February 5, 2018

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22727

The Cushing MLP Infrastructure Fund I

(Exact name of registrant as specified in charter)

(Exact name of registrant as specified in charter)

8117 Preston Road, Suite 440, Dallas, TX 75225

(Address of principal executive offices) (Zip code)

(Address of principal executive offices) (Zip code)

Jerry V. Swank

8117 Preston Road, Suite 440, Dallas, TX 75225

(Name and address of agent for service)

(Name and address of agent for service)

214-692-6334

(Registrant’s telephone number, including area code)

Date of fiscal year end: November 30, 2017

Date of reporting period: November 30, 2017

Item 1. Reports to Stockholders.

|

The Cushing® MLP Infrastructure Fund I

|

|||

|

MASTER INDEX

|

|||

|

Section

|

|||

|

The Cushing® MLP Infrastructure Fund I

|

I

|

||

|

Financial Statements and Report of the Independent Registered Public Accounting

|

|||

|

Firm as of November 30, 2017 and for the fiscal year then ended

|

|||

|

The Cushing® MLP Infrastructure Master Fund

|

II

|

||

|

Financial Statements and Report of the Independent Registered Public Accounting

|

|||

|

Firm as of November 30, 2017 and for the fiscal year then ended

|

|||

|

The Cushing® MLP Infrastructure Fund I

|

||

|

TABLE OF CONTENTS

|

||

|

Unitholder Letter (Unaudited)

|

1

|

|

|

Statement of Assets and Liabilities

|

5

|

|

|

Statement of Operations

|

6

|

|

|

Statements of Changes in Net Assets

|

7

|

|

|

Statement of Cash Flows

|

8

|

|

|

Financial Highlights

|

9

|

|

|

Notes to Financial Statements

|

10

|

|

|

Report of the Independent Registered Public Accounting Firm

|

14

|

|

|

Additional Information (Unaudited)

|

15

|

|

|

Trustees and Executive Officers (Unaudited)

|

17

|

The Cushing® MLP Infrastructure Fund I

UNITHOLDER LETTER (Unaudited)

Dear Fellow Unitholder,

For the twelve month fiscal period ended November 30, 2017 (the “period”), the Cushing® MLP Infrastructure Fund I delivered a -5.94% total return, versus total returns of +22.84% and -6.83% for the S&P 500 Index (Total Return) and the Alerian MLP Index (Total Return) (“AMZ”), respectively.

Industry Overview and Themes

Energy commodity prices and the equities of midstream master limited partnerships (“MLPs”) initially benefited early in the period from favorable production curtailments agreed to by certain OPEC and non-OPEC nations (the “OPEC Agreement”) as well as indications that the newly-elected U.S. President would increase infrastructure spending and reduce federal regulations. However, investor sentiment in energy-related equities (including those held by the Fund) progressively worsened during the period driving lackluster sector performance. Despite the subsequent recovery in crude oil prices beginning in June 2017, the midstream MLP sector, as measured by performance of the AMZ, continued to slide to new lows in November. While the space recovered somewhat towards the end of the fiscal period, we remain frustrated and perplexed by the midstream MLP sector’s performance given the improving macro backdrop and attractive sector valuations. Frustratingly, MLPs traded below relative low levels experienced by the sector in February 2016, when crude oil prices fell to $26 per barrel.

To be sure, fundamentals for the midstream energy sector continued to improve during the period with increasing energy commodity prices driving higher rig counts, improving volume projections and new capital project announcements. However, several factors weighed on investor sentiment and created headwinds for performance including: 1) concerns over capital discipline and project returns in the energy sector and MLPs specifically; 2) related fears of increasing competitive forces (particularly in the Permian Basin) driven by significant new project proposals and competition from private equity; 3) another round of distribution reductions by several midstream companies; 4) concerns over corporate governance and limited partner unitholder rights following a number of adverse corporate actions; 5) the cost of capital burden imposed by incentive distribution rights (IDRs) given lower sector growth; and 6) MLP equity issuance in the face of anemic MLP-focused product fund flows. Other factors that contributed to negative sentiment at various times during the period but the impacts of which were subsequently abated or mitigated: 1) continued crude oil price volatility; 2) uncertainty regarding the exit strategy related to the OPEC Agreement; 3) continued elevated domestic crude oil inventories weighing on crude oil prices; 4) ongoing regulatory and environmental pressure; and 5) lack of conviction in the U.S. federal government’s ability to execute on the aforementioned pro-business and pro-energy company agenda.

Having said that, we believe the sector is actively addressing the concerns around corporate structure noted above and thus our outlook for midstream MLPs remains constructive, especially given the improving fundamental backdrop for energy. Several drivers of our positive outlook include: 1) improving fundamentals as U.S. shale producers have increased drilling activity (higher rig counts) and production which should lead to growing midstream system volumes; 2) record export volumes of U.S. produced hydrocarbons; 3) midstream company valuations that currently screen attractive relative to historical levels and compared to other energy subsectors and yield products, in our opinion; 4) crude oil macro supply and demand fundamentals appear more constructive globally; and 5) in general, midstream company balance sheets, leverage and coverage ratios appear to be improving.

1

Fund Performance and Strategy

Turning to the Fund’s performance and positioning for the period, during the Fund’s fiscal fourth quarter, we began the process of repositioning the Fund to qualify for treatment as a Regulated Investment Company (RIC) for U.S. federal tax purposes. While these changes will limit the Fund’s holdings of MLPs structured as qualified publicly traded partnerships to no more than 25% of the Fund’s assets, we see ample opportunity in the broader midstream sector (including midstream businesses organized as traditional C-Corporations) to continue executing the Fund’s strategy. Notably, several of these new additions contributed positive performance to the Fund during the period, as discussed below.

At the subsector level, the Fund benefited from overweight exposure to holdings in the Shipping General Partners (GPs) and newly added Electric Utility subsectors. The latter Electric Utility subsector continued to benefit from investor demand for stable and regulated cash flows compared to some MLPs with more variability. The Natural Gas Transportation and Storage subsector also contributed positive absolute and relative performance with security selection offsetting a lower average weight compared to the AMZ.

The Fund was negatively impacted by the performance of holdings in the Large Cap Diversified, Crude Oil & Refined Products and General Partners (GPs) subsectors. Performance in these subsectors was negatively impacted during the period by crude oil price volatility in addition to several negatively perceived company-specific corporate actions and guidance forecasts.

The top three contributors to the Fund’s absolute performance during the reporting period were all Large Cap Diversified MLPs, despite the fact that the subsector detracted from the Fund’s overall performance. The top contributors in order of greatest contribution to least were: 1) ONEOK Partners, LP (NYSE: OKS); MPLX, LP (NYSE: MPLX); and 3) Williams Partners, LP (NYSE: WPZ). ONEOK Partners’ performance benefited from the announced merger with its parent, ONEOK Inc., and Williams Partners benefited from corporate restructuring steps taken with its parent, The Williams Companies, Inc. (NYSE: WMB). MPLX enjoyed momentum from a series of strong earnings reports and the announcement of a planned buy-out of its IDRs. All three of these holdings had positive absolute performance for the period.

Cutting both ways, two of the bottom three contributors to performance during the reporting period were also Large Cap Diversified MLPs. In order of the most negative to least negative performance, were: 1) Plains All American Pipeline, LP (NYSE: PAA) and 2) Energy Transfer Partners, LP (NYSE: ETP), both Large Cap Diversified MLPs; and 3) SemGroup Corp. (NYSE: SEMG). Plains All American Pipeline was negatively impacted by persistently weaker than expected earnings results and the eventual reduction of its distribution for the second time in two years. Energy Transfer suffered from a number of external and self-inflicted factors including project and regulatory challenges along with a large equity offering in August of 2017. A similar self-inflicted wound hurt SemGroup when it failed to pre-fund the equity portion of a large acquisition. Each of these holdings had negative returns for the period.

During the reporting period, the Fund increased exposure to subsectors dominated by the stocks of C-Corporations including General Partners and Diversified GPs, and reduced exposure to the Crude Oil & Refined Products subsector. As mentioned above, the Fund also added new subsector exposure to Electric Utilities and YieldCos, both of which are increasingly important providers of energy infrastructure in the U.S. At the end of the reporting period, the three largest subsector exposures, in order of size, were: 1) Large Cap Diversified MLPs; 2) Diversified General Partners; and 3) General Partners.

For the period, the Fund’s largest purchases consisted mostly of energy infrastructure C-Corporations, including: TransCanada Corp. (NYSE: TRP) and Enbridge, Inc. (NYSE: ENB), both Diversified GPs; and Cheniere Energy, Inc. (NYSE: LNG), a Shipping GP.

2

For the period, the Fund’s largest sales included: EQT Midstream Partners. LP (NYSE: EQM) and Dominion Energy Midstream Partners. LP (NYSE: DM), both Natural Gas Transportation and Storage MLPs; and Western Gas Partners. LP (NYSE: WES), a Natural Gas Gatherer & Processor MLP.

In conclusion, even though midstream energy sector performance and sentiment remained challenged during the period, we maintain a positive outlook given our expectation for improving hydrocarbon volumes, relatively attractive sector valuations and recovering global crude oil supply / demand fundamentals. We remain confident that North American shale basins will be developed over time and that midstream infrastructure will be well utilized given the need to move production to market.

We truly appreciate your support and look forward to continuing to help you achieve your investment goals.

Sincerely,

Jerry V. Swank

Chairman, Chief Executive Officer and President

The information provided herein represents the opinion of the Fund’s portfolio managers and is not intended to be a forecast of future events, a guarantee of future results, nor investment advice. The opinions expressed are as of the date of this report and are subject to change. The information in this report is not a complete analysis of every aspect of any market, sector, industry, security or the Fund itself. Statements of fact are from sources considered reliable, but the Fund makes no representation or warranty as to their completeness or accuracy. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. Please refer to the Schedule of Investments for a complete list of Fund holdings.

Past performance does not guarantee future results. An investment in the Fund involves risks. The Fund operates as a “feeder” fund within a “master-feeder” structure and pursues its investment objective by investing all or substantially all of its investable assets in The Cushing MLP Infrastructure Master Fund (the “Master Fund”), which has the same investment objectives as the Fund. The Master Fund is nondiversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Master Fund is more exposed to individual stock volatility than a diversified fund.

The Master Fund will invest in energy companies, including Master Limited Partnerships (MLPs), which concentrate investments in the natural resources sector. Energy companies are subject to certain risks, including, but not limited to the following: fluctuations in the prices of commodities; the highly cyclical nature of the natural resources sector may adversely affect the earnings or operating cash flows of the companies in which the Master Fund will invest; a significant decrease in the production of energy commodities could reduce the revenue, operating income, operating cash flows of MLPs and other natural resources sector companies and, therefore, their ability to make distributions or pay dividends and a sustained decline in demand for energy commodities could adversely affect the revenues and cash flows of energy companies. Holders of MLP units are subject to certain risks inherent in the structure of MLPs, including tax risks; the limited ability to elect or remove management or the general partner or managing member; limited voting rights and conflicts of interest between the general partner or managing member and its affiliates, on the one hand, and the limited partners or members, on the other hand. Damage to facilities and infrastructure of MLPs may significantly affect the value of an investment and may incur environmental costs and liabilities due to the nature of their business. Investors in MLP funds incur management fees from underlying MLP investments. Small- and mid-cap stocks are often more volatile and less liquid than large-cap stocks. Smaller companies generally face higher risks due to their limited product lines, markets, and financial resources. Funds that invest in bonds are subject to interest-rate risk and can lose principal value when interest rates rise. Bonds are also subject to credit risk, in which the bond issuer may fail to pay interest and principal in a timely manner. High yield securities have speculative characteristics and present a greater risk of loss than higher quality debt securities. These securities can also be subject to greater price volatility. An investment in the Fund will involve tax risks, including, but not limited to: The portion, if any, of a distribution received by the Fund as the holder of an MLP equity security that is offset by the MLP’s tax deductions or losses generally will be treated as a return of capital to the extent of the Fund’s tax basis in the MLP equity security, which will cause income or gain to be higher, or losses to be lower, upon the sale of the MLP security by the Fund. Changes in tax laws, regulations or interpretations of those laws or regulations in the future could adversely affect the Fund or the energy companies in which the Fund will invest.

3

This performance update, which has been furnished on a confidential basis to the recipient, does not constitute an offer of any security, which may be made only by means of a private placement memorandum which contains a description of material terms and risks.

The Fund incurs operating expenses, including advisory fees. Investment returns for the Fund are shown net of fees and expenses

The S&P 500 Index is an unmanaged index of common stocks that is frequently used as a general measure of stock market performance. The Alerian MLP Index is a capitalization-weighted index of prominent energy master limited partnerships. Neither index includes fees or expenses. It is not possible to invest directly in an index.

|

The Cushing® MLP Infrastructure Fund I

|

||||

|

STATEMENT OF ASSETS & LIABILITIES

|

||||

|

November 30, 2017

|

||||

|

Assets

|

||||

|

Investment in The Cushing MLP Infrastructure Master Fund

|

$

|

36,672,854

|

||

|

Short-term investments

|

7,505

|

|||

|

Receivable from Adviser, net of waiver

|

21,061

|

|||

|

Total assets

|

36,701,420

|

|||

|

Liabilities

|

||||

|

Accrued expenses

|

41,560

|

|||

|

Total liabilities

|

41,560

|

|||

|

Preferred Shares

|

||||

|

Net assets

|

$

|

36,659,860

|

||

|

Net Asset Value, 52,479.55 units outstanding

|

$

|

698.56

|

||

5

|

The Cushing® MLP Infrastructure Fund I

|

||||

|

STATEMENT OF OPERATIONS

|

||||

|

Year Ended

November 30, 2017

|

||||

|

Investment Income and Expenses Allocated from The Cushing MLP Infrastructure Master Fund

|

||||

|

Distributions and dividends

|

$

|

2,342,976

|

||

|

Less: return of capital on distributions

|

(2,028,791

|

)

|

||

|

Distribution and dividend income

|

314,185

|

|||

|

Interest income

|

10,683

|

|||

|

Management fees

|

(394,841

|

)

|

||

|

Professional fees

|

(74,424

|

)

|

||

|

Administrator fees

|

(58,315

|

)

|

||

|

Fund accounting fees

|

(36,239

|

)

|

||

|

Trustees’ fees

|

(23,949

|

)

|

||

|

Custodian fees and expenses

|

(11,897

|

)

|

||

|

Insurance expense

|

(7,639

|

)

|

||

|

Other expenses

|

(9,338

|

)

|

||

|

Expense reimbursement by Adviser

|

27,261

|

|||

|

Total Net Investment Loss Allocated from The Cushing MLP Infrastructure Master Fund

|

(264,513

|

)

|

||

|

Fund Investment Income

|

||||

|

Interest income

|

3,405

|

|||

|

Fund Expenses

|

||||

|

Administrator fees

|

35,668

|

|||

|

Professional fees

|

34,857

|

|||

|

Transfer agent fees

|

11,975

|

|||

|

Registration fees

|

1,170

|

|||

|

Other expenses

|

3,757

|

|||

|

Total Fund Expenses

|

87,427

|

|||

|

Less: expense reimbursement by Adviser

|

(88,293

|

)

|

||

|

Net Fund Expenses

|

(866

|

)

|

||

|

Net Investment Loss

|

(260,242

|

)

|

||

|

Realized and Unrealized Gain (Loss) on Investments

|

||||

|

Net realized gain allocated from The Cushing MLP Infrastructure Master Fund

|

2,292,262

|

|||

|

Change in unrealized appreciation/depreciation on investments allocated from

|

||||

|

The Cushing MLP Infrastructure Master Fund

|

(4,620,678

|

)

|

||

|

Net Realized and Unrealized Loss on Investments

|

(2,328,416

|

)

|

||

|

Decrease in Net Assets Resulting from Operations

|

$

|

(2,588,658

|

)

|

|

6

7

|

The Cushing® MLP Infrastructure Fund I

|

||||

|

STATEMENT OF CASH FLOWS

|

||||

|

Year Ended

November 30, 2017

|

||||

|

OPERATING ACTIVITIES

|

||||

|

Decrease in Net Assets Resulting from Operations

|

$

|

(2,588,658

|

)

|

|

|

Adjustments to reconcile decrease in net assets resulting from operations

|

||||

|

to net cash provided by operating activities

|

||||

|

Net realized gain allocated from

|

||||

|

The Cushing MLP Infrastructure Master Fund

|

(2,292,262

|

)

|

||

|

Change in unrealized appreciation/depreciation on investments allocated from

|

||||

|

The Cushing MLP Infrastructure Master Fund

|

4,620,678

|

|||

|

Net investment loss allocated from The Cushing MLP Infrastructure Master Fund

|

264,513

|

|||

|

Net purchases of investment in The Cushing MLP Infrastructure Master Fund

|

289,960

|

|||

|

Net sales of short-term investments

|

133,158

|

|||

|

Changes in operating assets and liabilities

|

||||

|

Receivable from Adviser, net of waiver

|

(14,296

|

)

|

||

|

Accrued expenses

|

8,668

|

|||

|

Net cash provided by operating activities

|

421,761

|

|||

|

FINANCING ACTIVITIES

|

||||

|

Proceeds from issuance of units including the change in subscriptions

|

||||

|

received in advance

|

4,866,871

|

|||

|

Payments for redemptions of units

|

(3,803,673

|

)

|

||

|

Distributions paid

|

(1,484,959

|

)

|

||

|

Net cash used in financing activities

|

(421,761

|

)

|

||

|

INCREASE IN CASH

|

-

|

|||

|

CASH:

|

||||

|

Beginning of fiscal year

|

-

|

|||

|

End of fiscal year

|

$

|

-

|

||

|

SUPPLEMENTAL DISCLOSURE OF CASH FLOW AND NON-CASH INFORMATION

|

||||

|

Distribution reinvestment

|

$

|

1,030,824

|

||

8

|

The Cushing® MLP Infrastructure Fund I

|

|||||||||||||||||||||||

|

FINANCIAL HIGHLIGHTS

|

|||||||||||||||||||||||

|

Year Ended

November

30,

2017

|

Year Ended

November

30,

2016

|

Year Ended

November

30,

2015

|

Year Ended

November 30,

2014

|

Year Ended

November 30,

2013

|

|||||||||||||||||||

|

Per Unit Data (1)

|

|||||||||||||||||||||||

|

Net Asset Value,

|

|||||||||||||||||||||||

|

beginning of fiscal year

|

$

|

795.46

|

$

|

746.50

|

$

|

1,132.69

|

$

|

927.42

|

$

|

723.54

|

|||||||||||||

|

Income from Investment Operations:

|

|||||||||||||||||||||||

|

Net investment income (loss) (2)

|

(5.11

|

)

|

(8.64

|

)

|

(11.20

|

)

|

29.82

|

28.01

|

|||||||||||||||

|

Net realized and unrealized

|

|||||||||||||||||||||||

|

gain (loss) on investments

|

(42.12

|

)

|

109.09

|

(325.83

|

)

|

219.07

|

214.92

|

||||||||||||||||

|

Total increase (decrease) from investment operations

|

(47.23

|

)

|

100.45

|

(337.03

|

)

|

248.89

|

242.93

|

||||||||||||||||

|

Less Distributions and Dividends to Unitholders:

|

|||||||||||||||||||||||

|

Net investment income

|

-

|

-

|

-

|

-

|

-

|

||||||||||||||||||

|

Return of capital

|

(49.67

|

)

|

(51.49

|

)

|

(49.16

|

)

|

(43.62

|

)

|

(39.05

|

)

|

|||||||||||||

|

Total distributions and dividends to unitholders

|

(49.67

|

)

|

(51.49

|

)

|

(49.16

|

)

|

(43.62

|

)

|

(39.05

|

)

|

|||||||||||||

|

Net Asset Value,

|

|||||||||||||||||||||||

|

end of fiscal year

|

$

|

698.56

|

$

|

795.46

|

$

|

746.50

|

$

|

1,132.69

|

$

|

927.42

|

|||||||||||||

|

Total Investment Return (3)

|

(5.94

|

)%

|

13.46

|

%

|

(29.75

|

)

|

%

|

26.84

|

%

|

33.58

|

%

|

||||||||||||

|

Supplemental Data and Ratios

|

|||||||||||||||||||||||

|

Net assets, end

|

|||||||||||||||||||||||

|

of fiscal year

|

$

|

36,659,860

|

$

|

39,620,279

|

$

|

31,395,468

|

$

|

35,832,300

|

$

|

28,006,462

|

|||||||||||||

|

Ratio of expenses to average net

|

|||||||||||||||||||||||

|

assets before waiver

|

1.79

|

%

|

1.92

|

%

|

2.20

|

%

|

1.53

|

%

|

1.93

|

%

|

|||||||||||||

|

Ratio of expenses to average net

|

|||||||||||||||||||||||

|

assets after waiver

|

1.50

|

%

|

1.50

|

%

|

1.50

|

%

|

1.50

|

%

|

1.50

|

%

|

|||||||||||||

|

Ratio of net investment

|

|||||||||||||||||||||||

|

income (loss) to average net

|

|||||||||||||||||||||||

|

assets after waiver

|

(0.66

|

)%

|

(1.17

|

)%

|

(1.17

|

)

|

%

|

2.73

|

%

|

3.26

|

%

|

||||||||||||

|

Portfolio turnover rate

|

N/A

|

N/A

|

11.76

|

%

|

(4)

|

26.02

|

%

|

36.69

|

%

|

||||||||||||||

|

Portfolio turnover rate of

|

|||||||||||||||||||||||

|

Master Fund

|

85.91

|

%

|

54.68

|

%

|

12.63

|

%

|

(5)

|

N/A

|

N/A

|

||||||||||||||

|

(1) Information presented relates to a unit outstanding for the period presented.

|

|||||||||||||||||||||||

|

(2) Calculated using average shares outstanding method.

|

|||||||||||||||||||||||

|

(3) Individual returns and ratios may vary based on the timing of capital transactions.

|

|||||||||||||||||||||||

|

(4) Covers the period from December 1, 2014 through June 30, 2015, prior to the transfer of securities

|

|||||||||||||||||||||||

|

to The Cushing MLP Infrastructure Master Fund.

|

|||||||||||||||||||||||

|

(5) Covers the period July 1, 2015 through November 30, 2015.

|

|||||||||||||||||||||||

9

The Cushing® MLP Infrastructure Fund I

NOTES TO FINANCIAL STATEMENTS

November 30, 2017

|

1.

|

Organization

|

The Cushing® MLP Infrastructure Fund I (the “Fund”), was organized as a Delaware statutory trust pursuant to an agreement and declaration of trust dated January 15, 2010. The Fund commenced operations on March 1, 2010. Effective August 1, 2012, the Fund registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940. The Fund’s investment objective is to seek a high level of after-tax total return, with an emphasis on current distributions paid to its unitholders.

Effective as of July 1, 2015, the Fund converted to a “master/feeder” structure by contributing substantially all of its investable assets less cash retained by the Fund (the “Transferred Assets”) to The Cushing® MLP Infrastructure Master Fund (the “Master Fund”) in exchange for Master Fund units with an aggregate net asset value equal to the aggregate value of the Transferred Assets. The Fund pursues its investment objective by investing all or substantially all of its investable assets in the Master Fund. The Master Fund is registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940 and has the same investment objective as the Fund. The Fund and Master Fund are managed by Cushing® Asset Management, LP (the “Adviser”).

The financial statements of the Master Fund, including the Schedule of Investments, are attached to this report and should be read in conjunction with the Fund’s financial statements. The Fund owns 100% of the Master Fund as of November 30, 2017.

|

2.

|

Significant Accounting Policies

|

A. Basis of Presentation

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”) as detailed in the Financial Accounting Standards Board’s Accounting Standards Codification. The Fund is an investment company and follows the investment company accounting and reporting guidance under FASB ASC Topic 946, “Financial Services-Investment Companies.”

B. Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities, recognition of distribution income and disclosure of contingent assets and liabilities at the date of the financial statements. Actual results could differ from those estimates.

C. Investment Valuation

The Fund uses the following valuation methods to determine fair value as either fair value for investments for which market quotations are available, or if not available, the fair value, as determined in good faith pursuant to such policies and procedures as may be approved by the Fund’s Board of Trustees (“Board of Trustees” or “Trustees”) from time to time. The valuation of the portfolio securities of the Fund currently includes the following processes:

(i) The market value of each security listed or traded on any recognized securities exchange or automated quotation system will be the last reported sale price at the relevant valuation date on the composite tape or on the principal exchange on which such security is traded except those listed on the NASDAQ Global Market®, NASDAQ Global Select Market® and the NASDAQ Capital Market® exchanges (collectively, “NASDAQ”). Securities traded on NASDAQ will be valued at the NASDAQ official closing price. If no sale is reported on that date, the closing price from the prior trading day may be used. Short-term investments are generally priced at the ending net asset value provided by the service agent of the funds.

(ii) The Fund’s non-marketable investments will generally be valued in such manner as the Adviser determines in good faith to reflect their fair values under procedures established by, and under the general supervision and responsibility of, the Board of Trustees. The pricing of all assets that are fair valued in this manner will be subsequently reported to and ratified by the Board of Trustees.

The Fund records its investment in the Master Fund at fair value which is represented by the Fund’s proportionate indirect interest in the net assets of the Master Fund as of November 30, 2017. Valuation of securities and other investments held by the Master Fund is discussed in the notes to the Master Fund’s financial statements. The Fund records its pro rata share of the Master Fund’s income, expenses and realized and unrealized gains and losses. The performance of the Fund is directly affected by the performance of the Master Fund. The financial statements of the Master Fund, which are attached, are an integral part of these financial statements. Please refer to the accounting policies disclosed in the financial statements of the Master Fund for additional information regarding significant accounting policies that affect the Fund.

10

D. Security Transactions, Investment Income and Expenses

The Master Fund’s security transactions are accounted for on the date the securities are purchased or sold (trade date). Realized gains and losses are reported on a first in, first out cost basis. Interest income is recognized on an accrual basis. Distributions and dividends (collectively referred to as “Distributions”) are recorded on the ex-dividend date. Distributions received from the Master Fund’s investments in master limited partnerships (“MLPs”) generally are comprised of ordinary income, capital gains and return of capital. For financial statement purposes, the Master Fund uses return of capital and income estimates to determine the dividend income received from MLP Distributions. Such estimates are based on historical information available from each MLP and other industry sources. These estimates may subsequently be revised based on information received from the MLPs after their tax reporting periods are concluded, as the actual character of these Distributions is not known until after the fiscal year end of the Master Fund.

The Master Fund estimates the allocation of investment income and return of capital for the Distributions received from its portfolio investments within the Master Fund’s Statement of Operations.

Expenses are recorded on an accrual basis. The Fund records its proportionate share of the Master Fund’s income, expenses, and realized and unrealized gains and losses. In addition, the Fund incurs and accrues its own expenses.

E. Distributions to Unitholders

Distributions to unitholders are recorded on the ex-dividend date. The character of Distributions to unitholders are comprised of 100% return of capital.

F. Federal Income Taxation

The Fund is treated as a partnership for Federal income tax purposes. Accordingly, no provision for Federal income taxes is reflected in the accompanying financial statements. The Fund does not record a provision for U.S. federal, state, or local income taxes because the unitholders report their share of the Fund’s income or loss on their income tax returns. The Fund files an income tax return in the U.S. federal jurisdiction, and may file income tax returns in various U.S. states. Generally, the Fund is subject to income tax examinations by major taxing authorities during the three year period prior to the period covered by these financial statements.

In accordance with GAAP, the Fund is required to determine whether its tax positions are more likely than not to be sustained upon examination by the applicable taxing authority, based on the technical merits of the position. The tax benefit recognized is measured as the largest amount of benefit that has a greater than fifty percent likelihood of being realized upon ultimate settlement with the relevant taxing authorities. Based on its analysis, the Fund has determined that it has not incurred any liability for unrecognized tax benefits as of November 30, 2017. The Fund does not expect that its assessment regarding unrecognized tax benefits will materially change over the next twelve months. However, the Fund’s conclusions may be subject to review and adjustment at a later date based on factors including, but not limited to, questioning the timing and amount of deductions, the nexus of income among various tax jurisdictions, compliance with U.S. federal and U.S. state and foreign tax laws, and changes in the administrative practices and precedents of the relevant taxing authorities.

G. Cash Flow Information

The Fund makes Distributions from investments, which include the amount received as cash Distributions from the Master Fund. These activities are reported in the Statement of Changes in Net Assets, and additional information on cash receipts and payments is presented in the Statement of Cash Flows.

H. Indemnification

Under the Fund’s organization documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Fund may enter into contracts that provide general indemnification to other parties. The Fund’s maximum exposure under such indemnification arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred, and may not occur.

11

|

3.

|

Concentrations of Risk

|

The Fund’s investment objective is to seek a high level of after-tax total return, with an emphasis on current distributions paid to its unitholders. The Fund seeks to achieve its investment objective by investing, under normal market conditions, in the Master Fund, which invests in MLPs.

In the normal course of business, substantially all of the Fund’s and Master Fund’s securities transactions, money balances, and security positions are transacted with the Fund’s custodian, U.S. Bank, N.A. The Fund and Master Fund are subject to credit risk to the extent any broker with whom it conducts business is unable to fulfill contractual obligations on its behalf. The Adviser monitors the financial condition of such brokers.

|

4.

|

Agreements and Related Party Transactions

|

Each of the Fund and the Master Fund has entered into an Investment Management Agreement (the “Agreement”) with the Adviser. Under the terms of the Agreement, the Master Fund pays the Adviser a management fee, payable monthly in arrears, equal to 1.0% per annum of the Managed Assets of the Master Fund for services and facilities provided by the Adviser to the Fund and the Master Fund. “Managed Assets” means the total assets of the Master Fund, minus all accrued expenses incurred in the normal course of operations other than liabilities or obligations attributable to financial leverage, including, without limitation, financial leverage obtained through (i) indebtedness of any type (including, without limitation, borrowing through credit facility or the issuance of debt securities), (ii) the issuance of preferred securities, (iii) the reinvestment of collateral received for securities loaned in accordance with the Master Fund’s investment objective and policies, and/or (iv) an other means. Due to its investment in the Master Fund, the Fund bears its proportionate percentage of the management fee paid to the Adviser by the Master Fund.

The Adviser agreed to waive a portion of its management fee and reimburse the Fund and the Master Fund expenses such that the annual operating expenses (exclusive of any taxes, brokerage commissions, expenses incurred in connection with any merger or reorganization (other than conversion of the Fund to a master/feeder structure), acquired fund fees and expenses, extraordinary expenses such as litigation, or any distribution and/or service fees payable by the Fund) would not exceed 1.50% of the respective fund’s net assets through November 30, 2017. For the fiscal year ended November 30, 2017, the Adviser waived fees and reimbursed Fund expenses in the amount of $88,293. As of November 30, 2017, the Adviser owed the Fund $21,061 for expense reimbursements. For the fiscal year ended November 30, 2017, the Adviser earned $395,600 in management fees from the Master Fund and waived fees and reimbursed the Master Fund expenses in the amount of $27,259.

Amounts waived or reimbursed by the Adviser are subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years after such waiver or reimbursement) if such recoupment can be achieved without exceeding the expense limitation; provided, however that amounts waived or reimbursed by the Adviser with respect to the Master Fund are not subject to recoupment. The Adviser’s waived fees and reimbursed expenses that are subject to potential recoupment are as follows:

|

Fiscal Year Incurred

|

Amount

Waived/Reimbursed

|

Amount

Recouped

|

Amount Subject

to Potential

Recoupment

|

Expiration Date

|

|||||||||

|

November 30, 2014

|

$

|

21,221

|

$

|

-

|

$

|

21,221

|

November 30, 2017

|

||||||

|

November 30, 2015

|

101,935

|

-

|

101,935

|

November 30, 2018

|

|||||||||

|

November 30, 2016

|

82,793

|

-

|

82,793

|

November 30, 2019

|

|||||||||

|

November 30, 2017

|

88,293

|

-

|

88,293

|

November 30, 2020

|

|||||||||

|

$

|

294,242

|

$

|

-

|

$

|

294,242

|

||||||||

Jerry V. Swank, the founder and managing partner of the Adviser, is Chairman of the Fund’s Board of Trustees and President of the Fund.

U.S. Bancorp Fund Services, LLC serves as the Fund’s administrator and transfer agent. In addition to the fees it charges the Master Fund, the Fund pays the administrator a monthly fee computed at an annual rate of 0.035% of the first $50 million of the Fund’s net assets, 0.020% on the next $100 million of net assets and 0.010% on the balance of the Fund’s net assets above $150 million, with a minimum annual fee of $30,000.

U.S. Bank, N.A. serves as the Fund’s custodian. There is no fee directly attributable to the Fund other than its allocated portion of the Master Fund’s expenses.

Quasar Distributors, LLC, an affiliate of U.S. Bancorp Fund Services, LLC and U.S. Bank, N.A., serves as the Fund’s distributor.

12

Certain unitholders are affiliated with the Fund. The aggregate value of the affiliated unitholders’ share of net assets as of November 30, 2017 was approximately $474,695.

|

5.

|

Fair Value Measurements

|

Various inputs that are used in determining the fair value of the Fund’s investments are summarized in the three broad levels listed below:

|

·

|

Level 1 — quoted prices in active markets for identical securities

|

|

·

|

Level 2 — other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.)

|

|

·

|

Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments)

|

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

As of November 30, 2017, short-term investments valued at $7,505 were classified as Level 1 in the fair value hierarchy. The individual securities are listed in the table below. The Fund invests substantially all of its assets in the Master Fund.

|

Shares

|

Fair Value

|

|||

|

Morgan Stanley Institutional Liquidity Funds - Institutional Class

|

1,877

|

$ |

1,877

|

|

|

Fidelity Money Market Portfolio - Institutional Class

|

1,876

|

1,876

|

||

|

First American Government Obligations Fund - Class Z

|

1,876

|

1,876

|

||

|

Invesco STIC Prime Portfolio

|

1,876

|

1,876

|

||

| $ |

7,505

|

The Fund discloses transfers between levels based on valuations at the end of the reporting period. For the fiscal year ended November 30, 2017, the Fund did not have any transfers between any of the levels of the fair value hierarchy.

|

6.

|

Unit Transactions

|

Units of beneficial interest (“Units”) of the Fund may be offered or sold in a private placement to persons who satisfy the suitability standards set forth in the Fund’s confidential offering memorandum. The Fund is authorized to issue an unlimited number of Units. The Units are not registered under the Securities Act of 1933 or the securities laws of any state of the United States. The Fund generally offers Units on the first business day of each month. For the fiscal year ended November 30, 2017, the Fund sold 6,229.70 units. As of November 30, 2017, the Fund had 52,479.55 Units outstanding.

The Fund generally intends to pay Distributions quarterly, in such amounts as may be determined from time to time by the Fund’s Board of Trustees. Unless a unitholder elects otherwise, Distributions, if any, will be automatically reinvested in additional Units in the Fund. For the fiscal year ended November 30, 2017, the Fund issued 1,369.96 units through its dividend reinvestment plan. The Fund may, from time to time, conduct tender offers to repurchase Units from Unitholders in those amounts and on such terms as the Board of Trustees may determine. The amount of shares in each tender offer is determined quarterly by the Board of Trustees. For the fiscal year ended November 30, 2017, the Fund repurchased 4,928.36 shares from Unitholders.

|

7.

|

Subsequent Events

|

On December 15, 2017, the Fund was converted into an open-end investment company through a reorganization (the “Reorganization”) of the Fund with and into Cushing® MLP Infrastructure Fund (the “Successor Fund”), a newly formed series of Cushing® Mutual Funds Trust, an open-end management investment company. Immediately prior to the closing of the Reorganization, the Master Fund liquidated and distributed all of its assets to the Fund.

13

The Adviser’s right to recoup amounts waived or reimbursed with respect to the Fund did not survive the Reorganization. Therefore, amounts waived or reimbursed with respect to the Fund prior to the closing of the Reorganization may not be recouped from the Successor Fund.

The Fund has evaluated the need for additional disclosures and/or adjustments resulting from subsequent events through the date the financial statements were issued. Based on this evaluation, no additional adjustments were required to the financial statements as of November 30, 2017.

14

Report of Independent Registered Public Accounting Firm

The Unitholders and Board of Trustees

The Cushing MLP Infrastructure Fund I:

We have audited the accompanying statement of assets and liabilities of The Cushing MLP Infrastructure Fund I (the “Fund”) as of November 30, 2017, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of November 30, 2017, by correspondence with the custodian or by other appropriate auditing procedures. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the Fund as of November 30, 2017, the results of its operations and cash flows for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended in conformity with U.S. generally accepted accounting principles.

/s/ KPMG LLP

Columbus, Ohio

January 25, 2018

January 25, 2018

15

The Cushing® MLP Infrastructure Fund I

ADDITIONAL INFORMATION (Unaudited)

November 30, 2017

Trustee and Officer Compensation

The Fund does not currently compensate any of its trustees who are interested persons nor any of its officers. The Master Fund is responsible for compensation of the Trustees. The Fund, through its investment in the Master Fund, bears its proportionate percentage of the Trustee fees paid by the Master Fund. The Fund did not pay any special compensation to any of its trustees or officers. The Fund continuously monitors standard industry practices and this policy is subject to change. The Fund’s Statement of Additional Information includes additional information about the Trustees and is available, without charge, upon request by calling the Fund toll-free at (877) 653-1415 and on the SEC’s Web site at www.sec.gov.

Cautionary Note Regarding Forward-Looking Statements

This report contains “forward-looking statements” as defined under the U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to materially differ from the Fund’s historical experience and its present expectations or projections indicated in any forward-looking statements. These risks include, but are not limited to, changes in economic and political conditions; regulatory and legal changes; MLP industry risk; leverage risk; valuation risk; interest rate risk; tax risk; and other risks discussed in the Fund’s filings with the SEC. You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. The Fund undertakes no obligation to update or revise any forward-looking statements made herein. There is no assurance that the Fund’s investment objectives will be attained.

Proxy Voting Policies

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities owned by the Fund and information regarding how the Fund voted proxies relating to the portfolio of securities during the 12-month period ended June 30 is available to stockholders (i) without charge, upon request by calling the Fund toll-free at (877) 653-1415; and (ii) on the SEC’s Web site at www.sec.gov. The Fund was not registered with the SEC until August 1, 2012, therefore proxy voting information is only made available from this date forward.

Form N-Q

The Fund files its complete schedule of portfolio holdings for the first and third quarters of each fiscal year with the SEC on Form N-Q. The Fund’s Form N-Q and statement of additional information are available without charge by visiting the SEC’s Web site at www.sec.gov from August 1, 2012 forward. In addition, you may review and copy the Fund’s Form N-Q at the SEC’s Public Reference Room in Washington D.C. You may obtain information on the operation of the Public Reference Room by calling (800) SEC-0330.

Privacy Policy

In order to conduct its business, the Fund collects and maintains certain nonpublic personal information about its stockholders of record with respect to their transactions in shares of the Fund’s securities. This information includes the stockholder’s address, tax identification or Social Security number, share balances, and dividend elections. We do not collect or maintain personal information about stockholders whose share balances of our securities are held in “street name” by a financial institution such as a bank or broker.

We do not disclose any nonpublic personal information about you, the Fund’s other stockholders or the Fund’s former stockholders to third parties unless necessary to process a transaction, service an account, or as otherwise permitted by law.

To protect your personal information internally, we restrict access to nonpublic personal information about the Fund’s stockholders to those employees who need to know that information to provide services to our stockholders. We also maintain certain other safeguards to protect your nonpublic personal information.

Householding

In an effort to decrease costs, the Fund intends to reduce the number of duplicate annual and semi-annual reports, proxy statements and other similar documents you receive by sending only one copy of each to those addresses shared by two or more accounts and to shareholders the Transfer Agent reasonably believes are from the same family or household. Once implemented, if you would like to discontinue householding for your accounts, please contact investor services at investorservices@usbank.com to request individual copies of these documents. Once the Transfer Agent receives notice to stop householding, the Transfer Agent will begin sending individual copies thirty days after receiving your request. This policy does not apply to account statements.

16

The Cushing® MLP Infrastructure Fund I

TRUSTEES AND EXECUTIVE OFFICERS (Unaudited)

November 30, 2017

Set forth below is information with respect to each of the Trustees and executive officers of the Fund and Master Fund, including their principal occupations during the past five years. The business address of the Fund and Master Fund, its Trustees and executive officers is 8117 Preston Road, Suite 440, Dallas, Texas 75225.

|

Name and

Year of Birth

|

Position(s) Held

with the Trust

|

Term of

Office and

Length of

Time

Served (1)

|

Principal

Occupations

During Past

Five Years

|

Number of

Portfolios in

Fund

Complex (2)

Overseen

by Trustee

|

Other

Directorships

Held by Trustee

During the Past

Five Years

|

|

|

Independent Trustees

|

||||||

|

Brian R. Bruce

(1955)

|

Lead Independent Trustee

|

Trustee

since 2010

|

Chief Executive Officer, Hillcrest Asset Management, LLC (2008 to present) (registered investment adviser). Previously, Director of Southern Methodist University’s Encap Investment and LCM Group Alternative Asset Management Center (2006 to 2011). Chief Investment Officer of Panagora Asset Management, Inc. (1999 to 2007) (investment management company).

|

6

|

CM Advisers Family of Funds (2 series) (2003 to present) and Dreman Contrarian Funds (2 series) (2007 to present).

|

|

|

Brenda A. Cline

(1960)

|

Trustee and Chair of Audit Committee

|

Trustee

since 2017

|

Executive Vice President, Chief Financial Officer, Secretary and Treasurer of Kimbell Art Foundation (1993-present).

|

6

|

American Beacon Funds (32 series) (2004-present); Tyler Technologies, Inc. (2014-present) (software); Range Resources Corporation (2015-present) (natural gas and oil exploration and production).

|

|

|

Ronald P. Trout

(1939)

|

Trustee and Chairman of the Nominating, and Corporate Governance Committee

|

Trustee

since 2010

|

Retired. Previously, founding partner and Senior Vice President of Hourglass Capital Management, Inc. (1989 to 2002) (investment management company).

|

6

|

Dorchester Minerals LP (2008 - present) (acquisition, ownership and administration of natural gas and crude oil royalty, net profits and leasehold interests in the U.S.)

|

|

|

Interested Trustees

|

||||||

|

Jerry V. Swank

(1951) (3)

|

Trustee, Chairman of the Board, Chief Executive Officer and President

|

Trustee

since 2010

|

Managing Partner of the Adviser and founder Swank Capital, LLC of (2000 - present).

|

6

|

E-T Energy Ltd. (2008 - 2014) (developing, operating, producing and selling recoverable bitumen); Central Energy Partners, LP (2010-2013) (storage and transportation of refined petroleum products and petrochemicals).

|

|

|

(1)

|

Each Trustee serves an indefinite term until his or her successor is elected and qualified, or his or her earlier resignation or removal.

|

|||||

|

(2)

|

The “Fund Complex” includes the Fund, Master Fund and each other registered investment company for which the Adviser serves as investment adviser. As of November 30, 2017, there were six funds, including the Fund and Master Fund, in the Fund Complex.

|

|||||

|

(3)

|

Mr. Swank is an “interested person” of the Fund and Master Fund, as defined under the Investment Company Act of 1940, as amended, by virtue of his position as Managing Partner of the Investment Adviser.

|

|||||

17

|

Executive Officers (Unaudited)

|

||||||

|

The following provides information regarding the executive officers of the Fund and Master Fund who are not Trustees. Officers serve at the pleasure of the Board of Trustees and until his or her successor is appointed and qualified or until his or her earlier resignation or removal.

|

||||||

18

THE CUSHING®MLP INFRASTRUCTURE MASTER FUND

ANNUAL REPORT

November 30, 2017

|

The Cushing® MLP Infrastructure Master Fund

|

||||||

|

TABLE OF CONTENTS

|

||||||

|

Allocation of Portfolio Assets (Unaudited)

|

1

|

|||||

|

Schedule of Investments

|

2

|

|||||

|

Statement of Assets and Liabilities

|

4

|

|||||

|

Statement of Operations

|

5

|

|||||

|

Statements of Changes in Net Assets

|

6

|

|||||

|

Financial Highlights

|

7

|

|||||

|

Notes to Financial Statements

|

8

|

|||||

|

Report of the Independent Registered Public Accounting Firm

|

13

|

|||||

|

Additional Information (Unaudited)

|

14

|

|||||

|

Trustees and Executive Officers (Unaudited)

|

16

|

|||||

|

The Cushing® MLP Infrastructure Master Fund

|

|

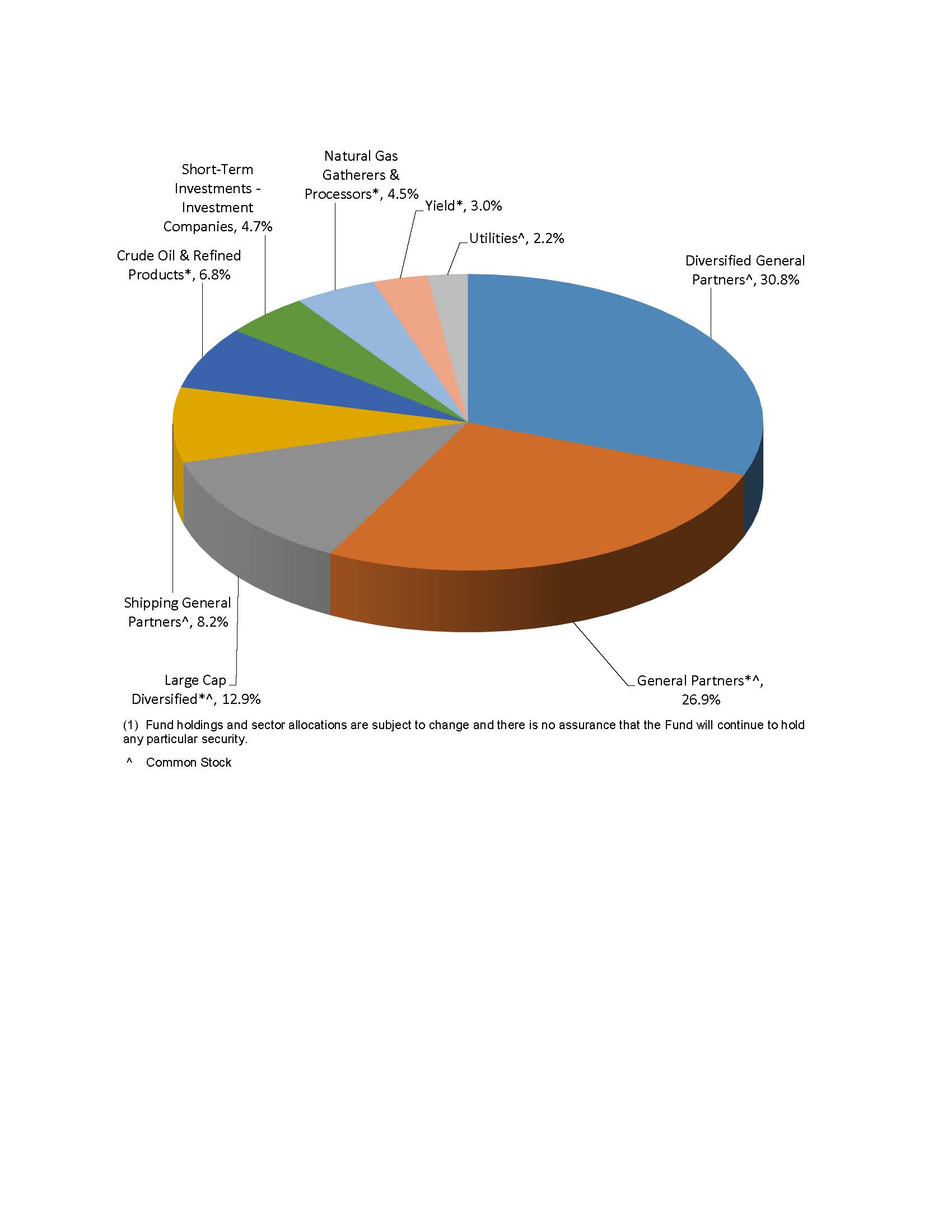

ALLOCATION OF PORTFOLIO ASSETS (Unaudited) (1)

|

|

November 30, 2017

|

|

(Expressed as a Percentage of Total Investments)

|

|

1

|

The Cushing® MLP Infrastructure Master Fund

|

||||||||

|

SCHEDULE OF INVESTMENTS

|

||||||||

|

November 30, 2017

|

||||||||

|

Shares

|

Fair Value

|

|||||||

|

Common Stock - 59.7%

|

||||||||

|

Diversified General Partners - 30.8%

|

||||||||

|

United States - 30.8%

|

||||||||

|

Dominion Energy, Inc.

|

9,900

|

$

|

832,887

|

|||||

|

Enbridge, Inc.

|

46,500

|

1,753,515

|

||||||

|

Marathon Petroleum Corporation

|

14,200

|

889,346

|

||||||

|

Nextera Energy, Inc.

|

5,200

|

821,808

|

||||||

|

Phillips 66

|

9,000

|

878,040

|

||||||

|

SemGroup Corporation

|

74,700

|

1,792,800

|

||||||

|

Transcanada Corporation

|

44,400

|

2,132,532

|

||||||

|

Williams Companies, Inc.

|

75,800

|

2,201,990

|

||||||

|

11,302,918

|

||||||||

|

General Partners - 14.0%

|

||||||||

|

United States - 14.0%

|

||||||||

|

EnLink Midstream LLC

|

68,500

|

1,143,950

|

||||||

|

ONEOK, Inc.

|

41,400

|

2,148,660

|

||||||

|

Targa Resources Corporation

|

42,500

|

1,844,500

|

||||||

|

5,137,110

|

||||||||

|

Large Cap Diversified - 4.6%

|

||||||||

|

United States - 4.6%

|

||||||||

|

Kinder Morgan, Inc.

|

97,600

|

1,681,648

|

||||||

|

Shipping General Partners - 8.1%

|

||||||||

|

United States - 8.1%

|

||||||||

|

Cheniere Energy, Inc.

|

43,800

|

2,116,416

|

||||||

|

Golar LNG Ltd.

|

35,300

|

872,263

|

||||||

|

2,988,679

|

||||||||

|

Utilities - 2.2%

|

||||||||

|

United States - 2.2%

|

||||||||

|

Sempra Energy

|

6,600

|

798,534

|

||||||

|

Total Common Stock (Cost $20,375,345)

|

$

|

21,908,889

|

||||||

|

Master Limited Partnerships and Related Companies - 35.5%

|

||||||||

|

Crude Oil & Refined Products - 6.8%

|

||||||||

|

United States - 6.8%

|

||||||||

|

MPLX, L.P.

|

49,200

|

$

|

1,764,312

|

|||||

|

Phillips 66 Partners, L.P.

|

15,800

|

740,388

|

||||||

|

2,504,700

|

||||||||

|

General Partners - 12.9%

|

||||||||

|

United States - 12.9%

|

||||||||

|

Antero Midstream GP, L.P.

|

61,100

|

1,084,525

|

||||||

|

Energy Transfer Equity, L.P.

|

96,400

|

1,561,680

|

||||||

|

Plains GP Holdings, L.P.

|

101,000

|

2,079,590

|

||||||

|

4,725,795

|

||||||||

|

Large Cap Diversified - 8.3%

|

||||||||

|

United States - 8.3%

|

||||||||

|

Energy Transfer Partners, L.P.

|

88,300

|

1,466,663

|

||||||

|

Enterprise Products Partners, L.P.

|

64,600

|

1,591,098

|

||||||

|

3,057,761

|

||||||||

2

|

The Cushing® MLP Infrastructure Master Fund

|

||||||||

|

SCHEDULE OF INVESTMENTS (Continued)

|

||||||||

|

November 30, 2017

|

||||||||

|

Shares

|

Fair Value

|

|||||||

|

Natural Gas Gatherers & Processors - 4.5%

|

||||||||

|

United States - 4.5%

|

||||||||

|

DCP Midstream, L.P.

|

23,600

|

829,304

|

||||||

|

EnLink Midstream Partners, L.P.

|

50,307

|

804,409

|

||||||

|

1,633,713

|

||||||||

|

Yield - 3.0%

|

||||||||

|

United States - 3.0%

|

||||||||

|

Nextera Energy Partners, L.P.

|

28,100

|

1,096,743

|

||||||

|

Total Master Limited Partnerships and Related Companies (Cost $12,482,769)

|

$

|

13,018,712

|

||||||

|

Short-Term Investments - Investment Companies - 4.8%

|

||||||||

|

United States - 4.8%

|

||||||||

|

Fidelity Government Portfolio Fund - Institutional Class, 0.97%(1)

|

434,678

|

$

|

434,678

|

|||||

|

First American Prime Obligations Fund - Class Z, 0.95%(1)

|

434,677

|

434,677

|

||||||

|

Invesco Short-Term Government & Agency Portfolio - Institutional Class, 0.98%(1)

|

434,677

|

434,677

|

||||||

|

Morgan Stanley Institutional Liquidity Funds - Government Portfolio - Institutional Class, 0.97%(1)

|

434,677

|

434,677

|

||||||

|

Total Short-Term Investments (Cost $1,738,709)

|

$

|

1,738,709

|

||||||

|

Total Investments - 100.00% (Cost $34,596,823)

|

$

|

36,666,310

|

||||||

|

Other Assets in Excess of Liabilities - (0.0)%

|

6,542

|

|||||||

|

Total Net Assets Applicable to Unitholders - 100.0%

|

$

|

36,672,852

|

||||||

|

(1) Rate reported is the current yield as of November 30, 2017.

|

|

|||||||

3

|

The Cushing® MLP Infrastructure Master Fund

|

||||

|

STATEMENT OF ASSETS & LIABILITIES

|

||||

|

|

November 30, 2017 | |||

|

Assets

|

||||

|

Investments at fair value (cost $34,596,823)

|

$

|

36,666,310

|

||

|

Prepaid expenses

|

4,051

|

|||

|

Dividends receivable

|

80,630

|

|||

|

Total assets

|

36,750,991

|

|||

|

Liabilities

|

||||

|

Payable to Adviser, net of waiver

|

6,966

|

|||

|

Accrued expenses

|

71,173

|

|||

|

Total liabilities

|

78,139

|

|||

|

Net assets

|

$

|

36,672,852

|

||

|

Net Asset Value, 52,607.94 units outstanding

|

$

|

697.10

|

||

4

|

The Cushing® MLP Infrastructure Master Fund

|

||||

|

STATEMENT OF OPERATIONS

|

||||

|

Year Ended

November 30, 2017

|

||||

|

Investment Income

|

||||

|

Distributions and dividends

|

$

|

2,347,397

|

||

|

Less: return of capital on distributions

|

(2,032,608

|

)

|

||

|

Distribution and dividend income

|

314,789

|

|||

|

Interest income

|

10,705

|

|||

|

Total Investment Income

|

325,494

|

|||

|

Expenses

|

||||

|

Management fees

|

395,600

|

|||

|

Professional fees

|

74,517

|

|||

|

Administrator fees

|

58,425

|

|||

|

Fund accounting fees

|

36,307

|

|||

|

Trustees’ fees

|

24,000

|

|||

|

Custodian fees and expenses

|

11,918

|

|||

|

Insurance expense

|

7,654

|

|||

|

Other expenses

|

9,351

|

|||

|

Total Expenses

|

617,772

|

|||

|

Less: expense reimbursement by Adviser

|

(27,259

|

)

|

||

|

Net Expenses

|

590,513

|

|||

|

Net Investment Loss

|

(265,019

|

)

|

||

|

Realized and Unrealized Gain (Loss) on Investments

|

||||

|

Net realized gain on investments

|

2,296,413

|

|||

|

Change in unrealized appreciation/depreciation on investments

|

(4,626,806

|

)

|

||

|

Net Realized and Unrealized Loss on Investments

|

(2,330,393

|

)

|

||

|

Decrease in Net Assets Resulting from Operations

|

$

|

(2,595,412

|

)

|

|

5

|

The Cushing® MLP Infrastructure Master Fund

|

||||||||

|

STATEMENTS OF CHANGES IN NET ASSETS

|

||||||||

|

Year Ended

November 30, 2017

|

Year Ended

November 30, 2016

|

|||||||

|

Operations

|

||||||||

|

Net investment loss

|

$

|

(265,019

|

)

|

$

|

(414,025

|

)

|

||

|

Net realized gain (loss) on investments

|

2,296,413

|

(2,206,923

|

)

|

|||||

|

Change in unrealized appreciation/depreciation

|

||||||||

|

on investments

|

(4,626,806

|

)

|

8,138,101

|

|||||

|

Net increase (decrease) in net assets

|

||||||||

|

resulting from operations

|

(2,595,412

|

)

|

5,517,153

|

|||||

|

Distributions and Dividends to Common Unitholders

|

||||||||

|

Net investment income

|

-

|

-

|

||||||

|

Return of capital

|

(2,521,460

|

)

|

(2,390,879

|

)

|

||||

|

Total distributions and dividends

|

||||||||

|

to common unitholders

|

(2,521,460

|

)

|

(2,390,879

|

)

|

||||

|

Capital Share Transactions (Note 7)

|

||||||||

|

Proceeds from unitholder subscriptions

|

3,050,000

|

4,357,803

|

||||||

|

Distribution reinvestments

|

1,103,700

|

870,067

|

||||||

|

Payments for redemptions

|

(2,008,495

|

)

|

-

|

|||||

|

Net increase in net assets from

|

||||||||

|

capital share transactions

|

2,145,205

|

5,227,870

|

||||||

|

Total increase (decrease) in net assets

|

(2,971,667

|

)

|

8,354,144

|

|||||

|

Net Assets

|

||||||||

|

Beginning of fiscal year

|

39,644,519

|

31,290,375

|

||||||

|

End of fiscal year

|

$

|

36,672,852

|

$

|

39,644,519

|

||||

6

|

The Cushing® MLP Infrastructure Master Fund

|

||||||||||||||||

|

FINANCIAL HIGHLIGHTS

|

||||||||||||||||

|

Year Ended

November 30, 2017

|

Year Ended

November 30, 2016

|

Period From

July 1, 2015 (1)

through

November 30,

2015

|

||||||||||||||

|

Per Unit Data (2)

|

||||||||||||||||

|

Net Asset Value, beginning of period

|

$

|

793.52

|

$

|

744.39

|

$

|

1,000.00

|

||||||||||

|

Income from Investment Operations:

|

||||||||||||||||

|

Net investment loss (3)

|

(5.18

|

)

|

(8.63

|

)

|

(3.38

|

)

|

||||||||||

|

Net realized and unrealized

|

||||||||||||||||

|

gain (loss) on investments

|

(41.67

|

)

|

109.36

|

(240.06

|

)

|

|||||||||||

|

Total increase (decrease) from

investment operations

|

(46.85

|

)

|

100.73

|

(243.44

|

)

|

|||||||||||

|

Less Distributions and Dividends to Unitholders:

|

||||||||||||||||

|

Net investment income

|

-

|

-

|

-

|

|||||||||||||

|

Return of capital

|

(49.57

|

)

|

(51.60

|

)

|

(12.17

|

)

|

||||||||||

|

Total distributions and dividends to

unitholders

|

(49.57

|

)

|

(51.60

|

)

|

(12.17

|

)

|

||||||||||

|

Net Asset Value, end of period

|

$

|

697.10

|

$

|

793.52

|

$

|

744.39

|

||||||||||

|

Total Investment Return (4)

|

(5.90

|

)%

|

13.53

|

%

|

(24.34

|

)

|

%(5) | |||||||||

|

Supplemental Data and Ratios

|

||||||||||||||||

|

Net assets, end of period

|

$ | 36,672,852 | $ | 39,644,519 | $ | 31,290,375 | ||||||||||

|

Ratio of expenses to average

|

||||||||||||||||

|

net assets before waiver (6)

|

1.57

|

%

|

1.68

|

%

|

2.54

|

% | ||||||||||

|

Ratio of expenses to average

|

||||||||||||||||

|

net assets after waiver (6)

|

1.50

|

%

|

1.50

|

%

|

1.50

|

% | ||||||||||

|

Ratio of net investment

|

||||||||||||||||

|

loss to average net

|

||||||||||||||||

|

assets after waiver (6)

|

(0.67

|

)%

|

(1.17

|

)%

|

(0.99

|

)

|

%

|

|||||||||

|

Portfolio turnover rate

|

85.91

|

%

|

54.68

|

%

|

12.63

|

%(5) | ||||||||||

|

(1) Commencement of operations.

|

||||||||||||||||

|

(2) Information presented relates to a unit outstanding for the period presented.

|

||||||||||||||||

|

(3) Calculated using average shares outstanding method.

|

||||||||||||||||

|