Filed pursuant to Rule 497

File No. 333-225462

| PROSPECTUS SUPPLEMENT | |

| (To Prospectus dated August 2, 2018 | May 8, 2019 |

| and Prospectus Supplements dated August 10, 2018, | |

| November 7, 2018 and February 13, 2019) |

Oxford Lane Capital Corp.

$500,000,000

Common Stock

IMPORTANT NOTICE REGARDING ELECTRONIC DELIVERY

Beginning in May 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of shareholder reports for Oxford Lane Capital Corp. (the “Company”) such as this report will no longer be sent by mail, unless you specifically request paper copies of the reports from the Company or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Company’s website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you do not need to take any action. For shareholder reports and other communications from the Company issued prior to May 2021, you may elect to receive such reports and other communications electronically. If you own shares of the Company through a financial intermediary, you may contact your financial intermediary to elect to receive materials electronically. This information is available free of charge by contacting us by mail at 8 Sound Shore Drive, Suite 255, Greenwich, CT 06830, by telephone at (203) 983-5275 or on our website at http://www.oxfordlanecapital.com.

You may elect to receive all future reports in paper, free of charge. If you own shares of the Company through a financial intermediary, you may contact your financial intermediary to elect to continue to receive paper copies of your shareholder reports after May 2021. This information is available free of charge by contacting us by mail at 8 Sound Shore Drive, Suite 255, Greenwich, CT 06830, by telephone at (203) 983-5275 or on our website at http://www.oxfordlanecapital.com. If you make such an election through your financial intermediary, your election to receive reports in paper may apply to all funds held through your financial intermediary.

This prospectus supplement supplements the prospectus supplement, dated August 10, 2018 (the “First Prospectus Supplement”), the prospectus supplement, dated November 7, 2018 (the “Second Prospectus Supplement”), the prospectus supplement, dated February 13, 2019 (the “Third Prospectus Supplement”) and the accompanying prospectus thereto, dated August 2, 2018 (the “Base Prospectus,” together with the First Prospectus Supplement, the Second Prospectus Supplement, the Third Prospectus Supplement and this prospectus supplement, the “Prospectus”), which relate to the sale of shares of common stock of Oxford Lane Capital Corp. in an “at-the-market” offering pursuant to an amended and restated equity distribution agreement, dated August 10, 2018, with Ladenburg Thalmann & Co. Inc., which was amended on May 8, 2019 to increase the maximum aggregate offering size of the “at-the-market” offering from $300,000,000 to $500,000,000 (collectively, the “Equity Distribution Agreement”).

You should carefully read the entire Prospectus before investing in our common stock. You should also review the information set forth under the “Risk Factors” section beginning on page 19 of the Base Prospectus before investing.

The terms “Oxford Lane,” the “Company,” the “Fund,” “OXLC,” “we,” “us” and “our” generally refer to Oxford Lane Capital Corp.

PRIOR SALES PURSUANT TO THE “AT THE MARKET” OFFERING

From March 7, 2016 to May 7, 2019, we sold a total of 24,822,697 shares of common stock pursuant to the “at-the-market” offering. Of the 24,822,697 shares of common stock sold, 13,813,244 shares were sold pursuant to our prior registration statement on Form N-2 (File No 333-205405) (the “Prior Registration Statement”). The total amount of capital raised as a result of these sales of common stock was approximately $262.2 million ($147.6 million pursuant to the Prior Registration Statement) and net proceeds were approximately $257.3 million ($144.5 million pursuant to the Prior Registration Statement) after deducting the sales agent’s commissions and offering expenses.

FEES AND EXPENSES

The following table is intended to assist you in understanding the costs and expenses that you will bear directly or indirectly. We caution you that some of the percentages indicated in the table below are estimates and may vary. Except where the context suggests otherwise, whenever the Prospectus contains a reference to fees or expenses paid by “us” or “Oxford Lane Capital,” or that “we” will pay fees or expenses, you will indirectly bear such fees or expenses as an investor in Oxford Lane Capital Corp.

| Stockholder transaction expenses: | ||||

| Sales load (as a percentage of offering price) | 2.00 | %(1) | ||

| Offering expenses borne by us (as a percentage of offering price) | 0.37 | %(2) | ||

| Distribution reinvestment plan expenses | None | (3) | ||

| Total stockholder transaction expenses (as a percentage of offering price) | 2.37 | % | ||

| Annual expenses (as a percentage of net assets attributable to common stock): | ||||

| Base management fee | 3.21 | %(4) | ||

| Incentive fees payable under our investment advisory agreement (20% of net investment income) | 3.36 | %(5) | ||

| Interest payments on borrowed funds | 0.63 | %(6) | ||

| Preferred stock dividend payment | 3.24 | %(7) | ||

| Other expenses (estimated) | 1.02 | %(8) | ||

| Total annual expenses (estimated) | 11.46 | %(9) | ||

Example

The following example demonstrates the projected dollar amount of total cumulative expenses that would be incurred over various periods with respect to a hypothetical investment in our common stock. In calculating the following expense amounts, we have assumed that our annual operating expenses would remain at the levels set forth in the table above, and that we pay the transaction expenses set forth in the table above, including a sales load of 2.00% paid by you (the commission to be paid by us with respect to common stock sold by us in this offering) and offering expenses of 0.37%. See Note 6 below for additional information regarding certain assumptions regarding our level of leverage.

| 1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

| You would pay the following expenses on a $1,000 investment, assuming a 5% annual return | $ | 153 | $ | 378 | $ | 565 | $ | 905 | ||||||||

The example and the expenses in the tables above should not be considered as a representation of our future expenses, and actual expenses may be greater or less than those shown. While the example assumes, as required by the SEC, a 5.0% annual return, our performance will vary and may result in a return greater or less than 5.0%. The incentive fee under the Investment Advisory Agreement, which, assuming a 5.0% annual return, would either not be payable or would have an insignificant impact on the expense amounts shown above, is included in the example. Also, while the example assumes reinvestment of all distributions at net asset value, participants in our distribution reinvestment plan will receive a number of shares of our common stock, determined by dividing the total dollar amount of the distribution payable to a participant by the market price per share of our common stock at the close of trading on the distribution payment date, which may be at, above or below net asset value. See “Distribution Reinvestment Plan” in the Prospectus for additional information regarding our distribution reinvestment plan.

| (1) | Represents the commission with respect to the shares of our common stock being sold in this offering, which we will pay to Ladenburg Thalmann & Co. Inc. in connection with sales of shares of our common stock effected by Ladenburg Thalmann & Co. Inc. under the Equity Distribution Agreement. There is no guaranty that there will be any sales of our common stock pursuant to this prospectus supplement and the Prospectus. |

| (2) | The offering expenses of this offering are estimated to be approximately $185,000. |

| (3) | The expenses of the distribution reinvestment plan are included in “other expenses.” The plan administrator’s fees will be paid by us. We will not charge any brokerage charges or other charges to stockholders who participate in the plan. However, your own broker may impose brokerage charges in connection with your participation in the plan. |

3

| (4) | Assumes gross assets of $648.4 million and $226.1 million of leverage (which reflects $90.4 million of Series 2023 Term Preferred Shares and $68.2 million of Series 2024 Term Preferred Shares issued and outstanding as of March 31, 2019, and as adjusted to reflect the issuance of an additional $25.0 million of new preferred stock, as well as $42.5 million due under a Master Repurchase Agreement with Nomura Securities International, Inc. (the “Repurchase Agreement”)), and assumes net assets of $403.8 million (which has been adjusted to reflect the issuance of an additional $50.0 million of common stock). The above calculation presents our base management fee as a percentage of our net assets. Our base management fee under the Investment Advisory Agreement, however, is based on our gross assets, which is defined as all the assets of Oxford Lane Capital, including those acquired using borrowings for investment purposes. As a result, to the extent we use additional leverage, it would have the effect of increasing our base management fee as a percentage of our net assets. See “Investment Advisory Agreement” in the Prospectus for additional information. |

| (5) | Amount reflects the estimated annual incentive fees payable to our investment adviser, Oxford Lane Management, during the fiscal year following this offering. The estimate assumes that the incentive fee earned will be proportional to the fee earned during the fiscal quarter ended March 31, 2019, annualized, and adjusted to include the estimated incentive fee based on the issuance of an additional $50.0 million of common stock and $25.0 million of preferred stock. Based on our current business plan, we anticipate that substantially all of the net proceeds of this offering will be invested within three months depending on the availability of investment opportunities that are consistent with our investment objective and other market conditions. We expect that it will take approximately one to three months to invest all of the proceeds of this offering, in part because equity and junior debt investments in CLO vehicles require substantial due diligence prior to investment. |

The incentive fee, which is payable quarterly in arrears, equals 20.0% of the excess, if any, of our “Pre-Incentive Fee Net Investment Income” that exceeds a 1.75% quarterly (7.0% annualized) hurdle rate, which we refer to as the Hurdle, subject to a “catch-up” provision measured at the end of each calendar quarter. The incentive fee is computed and paid on income that may include interest that is accrued but not yet received in cash. The operation of the incentive fee for each quarter is as follows:

| • | no incentive fee is payable to our investment adviser in any calendar quarter in which our Pre-Incentive Fee Net Investment Income does not exceed the Hurdle of 1.75%; |

| • | 100% of our Pre-Incentive Fee Net Investment Income with respect to that portion of such Pre-Incentive Fee Net Investment Income, if any, that exceeds the Hurdle but is less than 2.1875% in any calendar quarter (8.75% annualized) is payable to our investment adviser. We refer to this portion of our Pre-Incentive Fee Net Investment Income (which exceeds the Hurdle but is less than 2.1875%) as the “catch-up.” The “catch-up” is meant to provide our investment adviser with 20.0% of our Pre-Incentive Fee Net Investment Income, as if a Hurdle did not apply when our Pre-Incentive Fee Net Investment Income exceeds 2.1875% in any calendar quarter; and |

| • | 20.0% of the amount of our Pre-Incentive Fee Net Investment Income, if any, that exceeds 2.1875% in any calendar quarter (8.75% annualized) is payable to our investment adviser (once the Hurdle is reached and the catch-up is achieved, 20.0% of all Pre-Incentive Fee Investment Income thereafter is allocated to our investment adviser). |

No incentive fee is payable to our investment adviser on realized capital gains. For a more detailed discussion of the calculation of this fee, see “Investment Advisory Agreement” in the Prospectus.

| (6) | Assumes that we maintain our current level of outstanding borrowings as of March 31, 2019 under the Repurchase Agreement of $42.5 million with a funding cost of 5.947% per annum. |

| (7) | Assumes that we continue to have an aggregate of (a) $90.4 million of preferred stock with a preferred rate of 7.50% per annum and (b) $68.2 million of preferred stock with a preferred rate of 6.75% per annum, which were the amounts outstanding as of March 31, 2019, and (c) adjusted to reflect the issuance of an additional $25.0 million of preferred stock with a preferred rate of 6.75% per annum. We may issue additional shares of preferred stock pursuant to the registration statement of which this prospectus supplement forms a part. In the event we were to issue additional preferred stock, our borrowing costs, and correspondingly our total annual expenses, including our base management fee as a percentage of our net assets, would increase. |

4

| (8) | “Other expenses” ($4.1 million) are estimated for the current fiscal year, which considers the actual expenses for the quarter ended March 31, 2019, annualized, and adjusted for any new and non-recurring expenses, such as the offering costs on an assumed issuance of an additional $50.0 million of common stock and the amortization of debt offering costs on an assumed issuance of an additional $25.0 million of preferred stock. |

| (9) | “Total annual expenses” is presented as a percentage of net assets attributable to common stockholders, because the holders of shares of our common stock (and not the holders of our preferred stock or debt securities, if any) bear all of our fees and expenses, all of which are included in this fee table presentation. The indirect expenses associated with the Company’s CLO equity investments are not included in the fee table presentation, but if such expenses were included in the fee table presentation then the Company’s total annual expenses would have been 33.23%. |

5

SENIOR SECURITIES

Information about our senior securities is shown in the following table as of the end of each fiscal year since our formation. The information as of March 31, 2019, 2018, 2017, 2016, 2015, 2014 and 2013 has been derived from our financial statements that have been audited by an independent registered public accounting firm. The reports of our independent registered public accounting firm covering the total amount of senior securities outstanding as of March 31, 2019, 2018, 2017, 2016, 2015, 2014 and 2013 are attached as exhibits to the registration statement of which this prospectus supplement is a part.

Total Amount Outstanding Exclusive of Treasury Securities(1) | Asset Coverage Ratio Per Unit(2) | Involuntary Liquidation Preference Per Unit(3) | Average Market Value Per Unit(4) | |||||||||||||

| Fiscal Year | ||||||||||||||||

| 8.50% Series 2017 Term Preferred Shares(5) | ||||||||||||||||

| 2016 | $ | — | — | $ | — | $ | — | |||||||||

| 2015 | $ | 15,811,250 | 2.47 | $ | 25 | $ | 1.03 | |||||||||

| 2014 | $ | 15,811,250 | 3.99 | $ | 25 | $ | 1.05 | |||||||||

| 2013 | $ | 15,811,250 | 8.79 | $ | 25 | $ | 1.03 | |||||||||

| 7.50% Series 2023 Term Preferred Shares | ||||||||||||||||

| 2019 | $ | 90,400,025 | 2.73 | $ | 25 | $ | 1.01 | |||||||||

| 2018 | $ | 90,400,025 | 2.41 | $ | 25 | $ | 1.02 | |||||||||

| 2017 | $ | 90,400,025 | 2.59 | $ | 25 | $ | 1.01 | |||||||||

| 2016 | $ | 90,638,450 | 1.91 | $ | 25 | $ | 0.97 | |||||||||

| 2015 | $ | 73,869,250 | 2.47 | $ | 25 | $ | 0.98 | |||||||||

| 2014 | $ | 65,744,250 | 3.99 | $ | 25 | $ | 0.94 | |||||||||

| 8.125% Series 2024 Term Preferred Shares(6) | ||||||||||||||||

| 2018 | $ | — | — | $ | — | $ | — | |||||||||

| 2017 | $ | 50,504,475 | 2.59 | $ | 25 | $ | 1.02 | |||||||||

| 2016 | $ | 50,539,775 | 1.91 | $ | 25 | $ | 1.00 | |||||||||

| 2015 | $ | 60,687,500 | 2.47 | $ | 25 | $ | 1.01 | |||||||||

| 6.75% Series 2024 Term Preferred Shares(7) | ||||||||||||||||

| 2019 | $ | 68,235,375 | 2.73 | $ | 25 | $ | 1.02 | |||||||||

| 2018 | $ | 68,235,375 | 2.41 | $ | 25 | $ | 1.01 | |||||||||

| Repurchase Agreement (8) | ||||||||||||||||

| 2019 | $ | 42,493,500 | 2.73 | N/A | N/A | |||||||||||

| 2018 | $ | 42,493,500 | 2.41 | N/A | N/A | |||||||||||

| (1) | Total amount of each class of senior securities outstanding at the end of the period presented. |

| (2) | Asset coverage per unit is the ratio of the carrying value of our total consolidated assets, less all liabilities and indebtedness not represented by senior securities, to the aggregate amount of outstanding senior securities, as calculated separately for each of the Term Preferred Shares and the Repurchase Agreement in accordance with section 18(h) of the 1940 Act. With respect to the Term Preferred Shares, the asset coverage per unit is expressed in terms of a ratio per share of outstanding Term Preferred Shares (when expressing in terms of dollar amounts per share, the asset coverage ratio per unit is multiplied by the involuntary liquidation preference per unit of $25). With respect to the Repurchase Agreement, the asset coverage ratio per unit is expressed in terms of a ratio per unit of outstanding Repurchase Agreement (when expressing in terms of dollar amounts per share, the asset coverage per unit is multiplied by $1,000 per principal amount). |

| (3) | The amount to which such class of senior security would be entitled upon the voluntary liquidation of the issuer in preference to any security junior to it. |

| (4) | With respect to the Term Preferred Shares, the Average Market Value Per Unit is calculated by taking the daily average closing price of the security for the respective period and dividing it by $25 per share to determine a unit price per share consistent with Asset Coverage Per Unit. With respect to the Repurchase Agreement, the Average Market Value is not applicable as there are no senior securities thereunder which are registered for public trading. |

| (5) | On July 24, 2015, OXLC redeemed all issued and outstanding Series 2017 Term Shares at the term redemption price. |

| (6) | On July 14, 2017, we redeemed all issued and outstanding 8.125% Series 2024 Term Preferred Shares at the term redemption price. |

| (7) | On June 14, 2017, we issued 2,729,415 shares of our newly designated 6.75% Series 2024 Term Preferred Shares. |

| (8) | On January 2, 2018, the Fund entered into the Repurchase Agreement with Nomura Securities International, Inc. |

6

FOURTH QUARTER 2019 FINANCIAL HIGHLIGHTS

| · | Net asset value (“NAV”) per share as of March 31, 2019 stood at $8.32, compared with a NAV per share on December 31, 2018 of $7.56. |

| · | Net investment income (“NII”), calculated in accordance with generally accepted accounting principles (“GAAP”), was approximately $13.5 million, or $0.34 per share, for the quarter ended March 31, 2019. |

| · | Our core net investment income (“Core NII”) was approximately $20.8 million, or $0.53 per share, for the quarter ended March 31, 2019. |

| · | Core NII represents NII adjusted for additional cash distributions received, or entitled to be received (if any, in either case), on our collateralized loan obligation (“CLO”) equity investments while excluding any cash distributions believed to represent a return of capital. See additional information under “Supplemental Information Regarding Core Net Investment Income” below. |

| · | While, in our experience, cash flow distributions have historically represented useful indicators of our CLO equity investments’ annual taxable income during certain periods, we believe that current and future cash flow distributions may be less accurate indicators of taxable income with respect to our CLO equity investments than they have been in the past. Accordingly, our taxable income may materially differ from GAAP NII and/or Core NII. |

| · | Total GAAP investment income for the fourth fiscal quarter amounted to approximately $23.5 million, which represented an increase of $0.8 million from the third fiscal quarter. |

| · | For the quarter ended March 31, 2019 we recorded investment income from our portfolio as follows: |

| · | $22.0 million from our CLO equity investments, and |

| · | $1.5 million from our CLO debt investments and other income. |

| · | As of March 31, 2019 the following metrics applied (note that none of these values represented a total return to shareholders): |

| · | The weighted average yield of our CLO debt investments at current cost was 11.7%, compared with 11.2% as of December 31, 2018. |

| · | The weighted average GAAP effective yield of our CLO equity investments at current cost was 15.7%, compared with 15.8% as of December 31, 2018. |

| · | The weighted average cash yield of our CLO equity investments at current cost was 20.3%, compared with 19.8% as of December 31, 2018. |

| · | For the quarter ended March 31, 2019 we recorded a GAAP net increase in net assets resulting from operations of approximately $38.1 million, or $0.96 per share, including: |

| · | Net investment income of $13.5 million; |

| · | Net realized loss of $5.0 million; and |

| · | Net unrealized appreciation of $29.6 million. |

| · | During the quarter ended March 31, 2019 we made additional CLO investments of approximately $145.4 million, and received $89.3 million from sales and repayments of our CLO investments. |

7

| · | For the fourth fiscal quarter, we issued a total of 4,250,728 shares of common stock pursuant to an “at-the-market” offering. After deducting the sales agent’s commissions and offering expenses, this resulted in net proceeds of approximately $42.2 million. |

| · | On May 1, 2019 our Board of Directors declared the following distributions on our common stock: |

| Month Ending | Record Date | Payment Date | Amount Per Share | |||||

| July 31, 2019 | July 24, 2019 | July 31, 2019 | $ | 0.135 | ||||

| August 31, 2019 | August 23, 2019 | August 30, 2019 | $ | 0.135 | ||||

| September 30, 2019 | September 23, 2019 | September 30, 2019 | $ | 0.135 | ||||

Our Board of Directors also declared the required monthly dividends on our Series 2023 Term Preferred Shares and Series 2024 Term Preferred Shares (each, a “Share”) as follows:

| Preferred Shares Type | Per Share Dividend Amount Declared | Record Dates | Payment Dates | |||||

| Series 2023 | $ | 0.156250 | June 21, July 24, August 23 | June 28, July 31, August 30 | ||||

| Series 2024 | $ | 0.140625 | June 21, July 24, August 23 | June 28, July 31, August 30 | ||||

In accordance with their terms, each of the Series 2023 Term Preferred Shares and Series 2024 Term Preferred Shares will pay a monthly dividend at a fixed rate of 7.50% and 6.75%, respectively, of the $25.00 per share liquidation preference, or $1.875 and $1.6875 per share per year, respectively. This fixed annual dividend rate is subject to adjustment under certain circumstances, but will not, in any case, be lower than 7.50% and 6.75% per year, respectively, for each of the Series 2023 Term Preferred Shares and Series 2024 Term Preferred Shares.

Supplemental Information Regarding Core Net Investment Income

We provide information relating to Core NII (a non-GAAP measure) on a supplemental basis. This measure is not provided as a substitute for GAAP NII, but in addition to it. Our non-GAAP measures may differ from similar measures by other companies, even in the event of similar terms being utilized to identify such measures. Core NII represents GAAP NII adjusted for additional cash distributions received, or entitled to be received (if any, in either case), on our CLO equity investments.

Income from investments in the “equity” class securities of CLO vehicles, for GAAP purposes, is recorded using the effective interest method – this is based on an effective yield to the expected redemption utilizing estimated cash flows at current cost. The result is an effective yield for the investment in which the difference between the actual cash received, or distributions entitled to be received, and the effective yield calculation is adjusted from the cost. Accordingly, investment income recognized on CLO equity securities in the GAAP statement of operations differs from the cash distributions actually received by the Company during the period (referred to below as “CLO equity adjustments”).

Furthermore, in order for the Company to continue qualifying as a regulated investment company (“RIC”) for tax purposes, we are required, among other things, to distribute at least 90% of our investment company taxable income annually. Therefore, Core NII may provide a better indication of our estimated taxable income for a reporting period than GAAP NII; we can offer no assurance that will be the case, however, as the ultimate tax character of our earnings cannot be determined until after tax returns are prepared at the close of a fiscal year. We note that these non-GAAP measures may not serve as useful indicators of taxable earnings, particularly during periods of market disruption and volatility, and, as such, our taxable income may differ materially from our Core NII.

8

The following table provides a reconciliation of GAAP NII to Core NII for the three months ended March 31, 2019:

| Three Months Ended | ||||||||

| March 31, 2019 | ||||||||

| Amount | Per Share Amount | |||||||

| GAAP Net investment income | $ | 13,535,179 | $ | 0.343 | ||||

| CLO equity adjustments | 7,225,804 | 0.182 | ||||||

| Core Net investment income | $ | 20,760,983 | $ | 0.525 | ||||

9

Annual report to stockholders

On May 7, 2019, the Company filed its Annual Report to stockholders for the fiscal year ended March 31, 2019. The text of the Annual Report is attached hereto and is incorporated herein by reference.

Information contained on our website is not incorporated by reference into this prospectus supplement or the Prospectus, and you should not consider that information to be part of this prospectus supplement or the Prospectus.

10

Oxford Lane Capital Corp.

Annual Report

March 31, 2019

oxfordlanecapital.com

IMPORTANT NOTICE REGARDING ELECTRONIC DELIVERY

Beginning in May 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of shareholder reports for Oxford Lane Capital Corp. (the “Company”) such as this report will no longer be sent by mail, unless you specifically request paper copies of the reports from the Company or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on the Company’s website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you do not need to take any action. For shareholder reports and other communications from the Company issued prior to May 2021, you may elect to receive such reports and other communications electronically. If you own shares of the Company through a financial intermediary, you may contact your financial intermediary to elect to receive materials electronically. This information is available free of charge by contacting us by mail at 8 Sound Shore Drive, Suite 255, Greenwich, CT 06830, by telephone at (203) 983-5275 or on our website at http://www.oxfordlanecapital.com.

You may elect to receive all future reports in paper, free of charge. If you own shares of the Company through a financial intermediary, you may contact your financial intermediary to elect to continue to receive paper copies of your shareholder reports after May 2021. This information is available free of charge by contacting us by mail at 8 Sound Shore Drive, Suite 255, Greenwich, CT 06830, by telephone at (203) 983-5275 or on our website at http://www.oxfordlanecapital.com. If you make such an election through your financial intermediary, your election to receive reports in paper may apply to all funds held through your financial intermediary.

OXFORD LANE CAPITAL CORP.

TABLE OF CONTENTS

i

May 7, 2019

To Our Stockholders:

We are pleased to submit to you the report of Oxford Lane Capital Corp. (“we”, “us”, “our”, the “Fund” or “Oxford Lane”) for the fiscal year ended March 31, 2019. The net asset value of our shares at that date was $8.32 per common share. The Fund’s common stock is traded on the NASDAQ Global Select Market and its share price can differ from its net asset value. The Fund’s closing price at March 31, 2019 was $9.84, compared to $10.13 at March 31, 2018. The total return based on market value for Oxford Lane, for the year ended March 31, 2019, as reflected in the Fund’s financial highlights, was 13.47%. This return reflects the change in market price for the year ended March 31, 2019, as well as the impact of $1.62 per share in distributions declared and paid. The total return based on net asset value (“NAV”) for the year ended March 31, 2019, as reflected in the Fund’s financial highlights, was (1.39%). Please refer to “Note 12. Financial Highlights” for further details. On May 6, 2019, the last reported sale price of the Fund’s common stock was $10.94.

We note that there may be significant differences between Oxford Lane’s earnings prepared in accordance with generally accepted accounting principles (“GAAP”) in the United States of America and our taxable earnings, particularly related to collateralized loan obligation (“CLO”) equity investments where our taxable earnings are based upon the distributable share of earnings as determined under tax regulations for each CLO equity investment, while GAAP earnings are based upon an effective yield calculation. Additionally, as our taxable earnings are not generally known until after our distributions are made, those distributions may represent a return of capital on a tax basis. While reportable GAAP revenue from our CLO equity investments for the year ended March 31, 2019 was approximately $85.7 million, we received or were entitled to receive approximately $130.2 million in distributions from our CLO equity investments.

Investment Review

The Fund’s investment objective is to maximize its portfolio’s risk-adjusted total return over its investment horizon. Our current focus is to seek that return by investing in equity and junior tranches of CLO vehicles(1), which are collateralized primarily by a diverse portfolio of senior loans, and which generally have little to no exposure to real estate loans, mortgage loans or pools of consumer-based debt, such as credit card receivables or auto loans. Our investment strategy also includes investing in warehouse facilities, which are financing structures intended to aggregate senior loans that may be used to form the basis of a CLO vehicle. As of March 31, 2019, we held debt investments in four different CLO structures, and equity investments in approximately 100 different CLO structures.

Structurally, CLO vehicles are entities formed to originate and manage a portfolio of loans. The loans within a CLO vehicle are limited to those which, on an aggregated basis, meet established credit criteria and are subject to concentration limitations in order to limit a CLO vehicle’s exposure to a single credit or industry.

An investment in our Fund carries with it a significant number of meaningful risks, certain of which are discussed in the notes to our financial statements. Investors should read “Note 13. Risks and Uncertainties” carefully.

Investment Outlook

We believe that the market for CLO-related assets continues to provide us with opportunities to generate attractive risk-adjusted returns over the long term.

The long-term and relatively low-cost capital that many CLO vehicles have secured, compared with current asset spreads, have created opportunities to purchase certain CLO equity and junior debt instruments that may produce attractive risk-adjusted returns. Additionally, given that the CLO vehicles we invest in are cash flow-based vehicles, this term financing may be beneficial in periods of market volatility.

| 1. | A CLO vehicle is formed by issuing various classes or “tranches” of debt (with the most senior tranches being rated “AAA” to the most junior tranches typically being rated “BB” or “B”) and equity. The tranches of CLO vehicles rated “BB” or “B” may be referred to as “junk.” The equity of a CLO vehicle is generally structured to absorb the CLO’s losses before any of the CLO’s debt tranches, and it also has the lowest level of payment priority among the CLO’s tranches; therefore, the equity is typically the riskiest tranche of a CLO vehicle. |

1

We continue to review a large number of CLO investment opportunities in the current market environment, and we expect that the majority of our portfolio holdings, over the near to intermediate-term, will continue to be comprised of CLO debt and equity securities, with the more significant focus over the near-term likely to be on CLO equity securities.

Jonathan H. Cohen

Chief Executive Officer

This letter is intended to assist stockholders in understanding the Company’s performance during the twelve months ended March 31, 2019. The views and opinions in this letter were current as of May 7, 2019. Statements other than those of historical facts included herein may constitute forward-looking statements and are not guarantees of future performance or results and involve a number of risks and uncertainties. Actual results may differ materially from those in the forward-looking statements as a result of a number of factors. The Company undertakes no duty to update any forward-looking statement made herein. Information contained on our website is not incorporated by reference into this stockholder letter and you should not consider information contained on our website to be part of this stockholder letter or any other report we file with the Securities and Exchange Commission.

[Not Part of the Annual Report]

This report is transmitted to the stockholders of the Company and is furnished pursuant to certain regulatory requirements. This report and the information and views herein do not constitute investment advice, or a recommendation or an offer to enter into any transaction with the Company or any of its affiliates. This report is provided for informational purposes only, does not constitute an offer to sell securities of the Company and is not a prospectus. From time to time, the Company may have a registration statement relating to one or more of its securities on file with the U.S. Securities and Exchange Commission (“SEC”).

An investment in the Company is not appropriate for all investors. The investment program of the Company is speculative, entails substantial risk and includes investment techniques not employed by traditional mutual funds. An investment in the Company is not intended to be a complete investment program. Shares of closed-end investment companies, such as the Company, frequently trade at a discount from their net asset value (“NAV”), which may increase investors’ risk of loss. Past performance is not indicative of, or a guarantee of, future performance. The performance and certain other portfolio information quoted herein represents information as of March 31, 2019. Nothing herein should be relied upon as a representation as to the future performance or portfolio holdings of the Company. Investment return and principal value of an investment will fluctuate, and shares, when sold, may be worth more or less than their original cost. The Company’s performance is subject to change since the end of the period noted in this report and may be lower or higher than the performance data shown herein.

About Oxford Lane Capital Corp.

Oxford Lane Capital Corp. is a publicly-traded registered closed-end management investment company. It currently seeks to achieve its investment objective of maximizing risk-adjusted total return by investing in debt and equity tranches of collateralized loan obligation (“CLO”) vehicles. CLO investments may also include warehouse facilities, which are financing structures intended to aggregate loans that may be used to form the basis of a CLO vehicle.

Forward-Looking Statements

This report may contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Statements other than statements of historical facts included in this report may constitute forward-looking statements and are not guarantees of future performance or results and involve a number of risks and uncertainties. Actual results may differ materially from those in the forward-looking statements as a result of a number of factors, including those described in the Company’s filings with the SEC. The Company undertakes no duty to update any forward-looking statement made herein. All forward-looking statements speak only as of the date of this report.

2

OXFORD LANE CAPITAL CORP.

TOP TEN HOLDINGS

AS OF MARCH 31, 2019

| Investment | Maturity | Fair Value | % of Net Assets | ||||||||

| Octagon Investment Partners 40, Ltd. - CLO subordinated notes | April 20, 2031 | $ | 39,193,403 | 11.08 | % | ||||||

| Madison Park Fund XLI, Ltd. (fka: Atrium XII CLO) - CLO subordinated notes | April 22, 2027 | $ | 25,376,625 | 7.17 | % | ||||||

| Madison Park Funding XXX, Ltd. - CLO subordinated notes | April 15, 2029 | $ | 17,116,035 | 4.84 | % | ||||||

| Venture XXI CLO, Limited - CLO subordinated notes | July 15, 2027 | $ | 15,631,000 | 4.42 | % | ||||||

| Midocean Credit CLO VI - CLO income notes | January 20, 2029 | $ | 15,561,000 | 4.40 | % | ||||||

| Madison Park Funding XXIX, Ltd. - CLO subordinated notes | October 18, 2047 | $ | 15,300,000 | 4.32 | % | ||||||

| Shackleton 2013-IV-R CLO, Ltd. - CLO subordinated notes | April 13, 2031 | $ | 12,500,846 | 3.53 | % | ||||||

| Battalion CLO VII Ltd. - CLO subordinated notes | July 17, 2028 | $ | 11,836,000 | 3.35 | % | ||||||

| Ares XXXVII CLO Ltd. - CLO subordinated notes | October 15, 2030 | $ | 11,445,095 | 3.23 | % | ||||||

| Venture 33 CLO, Limited - CLO subordinated notes | July 15, 2031 | $ | 11,169,250 | 3.16 | % | ||||||

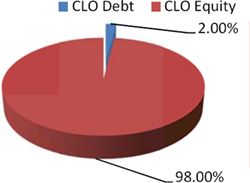

Portfolio Investment Breakdown as

of March 31, 2019

(Excludes cash and cash equivalents and other assets)

3

OXFORD LANE CAPITAL CORP.

STATEMENT OF ASSETS AND LIABILITIES

| March 31, 2019 | ||||

| ASSETS | ||||

| Investments, at fair value (cost: $619,716,034) | $ | 537,440,723 | ||

| Cash and cash equivalents | 21,473,934 | |||

| Distributions receivable | 8,354,379 | |||

| Securities sold not settled | 4,790,000 | |||

| Deferred offering costs on common stock | 304,633 | |||

| Interest receivable, including accrued interest purchased | 211,212 | |||

| Prepaid expenses and other assets | 717,576 | |||

| Fee receivable | 59,959 | |||

| Total assets | 573,352,416 | |||

| LIABILITIES | ||||

| Mandatorily redeemable preferred stock, net of discount and deferred issuance costs (10,000,000 shares authorized, 6,345,416 shares issued and outstanding) | 152,931,142 | |||

| Securities sold under agreement to repurchase | 42,493,500 | |||

| Securities purchased not settled | 17,404,918 | |||

| Incentive fees payable to affiliate | 3,383,795 | |||

| Investment advisory fee payable to affiliate | 2,255,436 | |||

| Interest payable | 624,752 | |||

| Accrued expenses | 348,860 | |||

| Directors’ fees payable | 70,000 | |||

| Accrued offering costs | 6,262 | |||

| Administrator expense payable | 1,661 | |||

| Total liabilities | 219,520,326 | |||

| COMMITMENTS AND CONTINGENCIES (Note 10) | ||||

| NET ASSETS applicable to common stock, $0.01 par value, 90,000,000 shares authorized, and 42,547,801 shares issued and outstanding | $ | 353,832,090 | ||

| NET ASSETS consist of: | ||||

| Paid in capital | $ | 473,516,331 | ||

| Total distributable earnings/(accumulated losses) | (119,684,241 | ) | ||

| Total net assets | $ | 353,832,090 | ||

| Net asset value per common share | $ | 8.32 | ||

| Market price per share | $ | 9.84 | ||

| Percentage of market price premium to net asset value per share | 18.27 | % | ||

See Accompanying Notes.

4

OXFORD LANE CAPITAL CORP.

SCHEDULE OF INVESTMENTS

MARCH 31, 2019

| COMPANY/INVESTMENT(1)(14) | PRINCIPAL

AMOUNT | COST | FAIR VALUE(2) | %

of Net Assets | ||||||||||||

| Collateralized Loan Obligation - Debt Investments | ||||||||||||||||

| Structured Finance - Debt Investments | ||||||||||||||||

| Ares XL CLO Ltd. | ||||||||||||||||

| CLO secured notes - Class ER(3)(4)(6), 10.79% (LIBOR + 8.00%, due January 15, 2029) | $ | 1,000,000 | $ | 873,844 | $ | 925,600 | ||||||||||

| Longfellow Place CLO, Ltd. | ||||||||||||||||

| CLO secured notes - Class FRR(3)(4)(6), 10.22% (LIBOR + 5.75%, due April 15, 2029) | 775,000 | 622,104 | 621,938 | |||||||||||||

| Mountain Hawk II CLO, Ltd. | ||||||||||||||||

| CLO secured notes - Class E(3)(4)(6), 7.56% (LIBOR + 4.80%, due July 20, 2024) | 8,000,000 | 7,008,702 | 6,880,000 | |||||||||||||

| OZLM XXII, Ltd. | ||||||||||||||||

| CLO secured notes - Class E(3)(4)(6), 10.16% (LIBOR + 7.39%, due January 17, 2031) | 2,670,000 | 2,584,542 | 2,321,031 | |||||||||||||

| Total Structured Finance - Debt Investments | $ | 11,089,192 | $ | 10,748,569 | 3.04 | % | ||||||||||

| Total Collateralized Loan Obligation - Debt Investments | $ | 11,089,192 | $ | 10,748,569 | 3.04 | % | ||||||||||

| Collateralized Loan Obligation - Equity Investments | ||||||||||||||||

| Structured Finance - Equity Investments | ||||||||||||||||

| ALM XVII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 26.57%, maturity January 15, 2028) | $ | 6,500,000 | $ | 3,794,756 | $ | 3,710,460 | ||||||||||

| AMMC CLO XI, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 17.85%, maturity April 30, 2031) | 2,100,000 | 1,256,114 | 1,113,000 | |||||||||||||

| AMMC CLO XII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 15.20%, maturity November 10, 2030) | 11,428,571 | 5,994,940 | 4,800,000 | |||||||||||||

| Anchorage Capital CLO 5-R, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 14.39%, maturity January 15, 2030) | 4,000,000 | 3,994,792 | 3,343,773 | |||||||||||||

| Anchorage Capital CLO 8, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 20.98%, maturity July 28, 2028) | 6,000,000 | 4,965,643 | 4,920,000 | |||||||||||||

| Apex Credit CLO 2018 Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 23.21%, maturity April 25, 2031) | 9,750,000 | 7,700,987 | 7,527,833 | |||||||||||||

| Apex Credit CLO 2015-II, Ltd. (fka: JFIN CLO 2015-II Ltd.) | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 16.50%, maturity October 17, 2026) | 5,750,000 | 4,764,295 | 3,794,630 | |||||||||||||

| Arch Street CLO, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 35.73%, maturity October 20, 2028) | 3,000,000 | 1,991,880 | 2,070,000 | |||||||||||||

| Ares XXVII CLO, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 25.69%, maturity July 28, 2029) | 17,000,000 | 7,737,935 | 7,659,760 | |||||||||||||

| Ares XXXVII CLO Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(9), (Estimated yield 24.58%, maturity October 15, 2030) | 15,000,000 | 10,532,626 | 11,445,095 | |||||||||||||

| Ares XL CLO Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 17.86%, maturity January 15, 2029) | 10,100,000 | 7,280,014 | 6,149,767 | |||||||||||||

| Ares XLIII CLO Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 28.82%, maturity October 15, 2029) | 3,320,000 | 1,697,146 | 1,965,610 | |||||||||||||

| Atlas Senior Loan Fund XII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(9), (Estimated yield 22.87%, maturity October 24, 2031) | 1,500,000 | 1,124,965 | 1,170,000 | |||||||||||||

| Battalion CLO VI Ltd. | ||||||||||||||||

| CLO preference shares (5)(7)(10), (Estimated yield 0.00%, maturity October 17, 2026) | 5,000,000 | 581,049 | 300,000 | |||||||||||||

| Battalion CLO VII Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 10.80%, maturity July 17, 2028) | 26,900,000 | 16,290,336 | 11,836,000 | |||||||||||||

| Benefit Street Partners CLO III Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 22.02%, maturity July 20, 2029) | 5,000,000 | 2,195,417 | 2,250,000 | |||||||||||||

| Benefit Street Partners CLO V Ltd. | ||||||||||||||||

| CLO preference shares (5)(7)(10), (Estimated yield 0.00%, maturity October 20, 2026) | 11,500,000 | 852,715 | 460,000 | |||||||||||||

| BlueMountain CLO 2013-2, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 25.90%, maturity October 22, 2030) | 4,746,000 | 1,970,536 | 1,993,320 | |||||||||||||

| B&M CLO 2014-1 LTD | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield -13.60%, maturity April 16, 2026) | 2,000,000 | 661,393 | 420,000 | |||||||||||||

(Continued on next page)

See Accompanying Notes.

5

OXFORD LANE CAPITAL CORP.

SCHEDULE OF INVESTMENTS - (continued)

MARCH 31, 2019

| COMPANY/INVESTMENT(1)(14) | PRINCIPAL

AMOUNT | COST | FAIR VALUE(2) | %

of Net Assets | ||||||||||||

| Collateralized Loan Obligation - Equity Investments - (continued) | ||||||||||||||||

| Structured Finance - Equity Investments (continued) | ||||||||||||||||

| Bristol Park CLO, Ltd. | ||||||||||||||||

| CLO income notes(5)(7), (Estimated yield 10.84%, maturity April 15, 2029) | $ | 10,000,000 | $ | 7,699,592 | $ | 5,500,000 | ||||||||||

| Canyon Capital CLO 2015-1, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 23.74%, maturity April 15, 2029) | 10,000,000 | 6,242,280 | 5,200,000 | |||||||||||||

| Carlyle Global Market Strategies CLO 2013-2, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 21.64%, maturity January 18, 2029) | 16,500,000 | 10,418,745 | 10,333,375 | |||||||||||||

| Carlyle Global Market Strategies CLO 2014-5, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 22.12%, maturity July 15, 2031) | 5,500,000 | 3,420,333 | 3,410,000 | |||||||||||||

| Cathedral Lake CLO 2013, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 19.66%, maturity October 15, 2029) | 6,350,000 | 2,923,060 | 2,603,500 | |||||||||||||

| Cathedral Lake II, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 23.56%, maturity July 15, 2029) | 8,112,200 | 5,150,534 | 4,745,637 | |||||||||||||

| CIFC Funding 2013-III-R, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 22.58%, maturity April 24, 2031) | 4,900,000 | 2,374,499 | 2,352,000 | |||||||||||||

| CIFC Funding 2014, Ltd. | ||||||||||||||||

| CLO income notes(5)(7), (Estimated yield 15.82%, maturity January 18, 2031) | 6,000,000 | 3,607,934 | 2,940,000 | |||||||||||||

| CIFC Funding 2014-III, Ltd. | ||||||||||||||||

| CLO income notes(5)(7)(12), (Estimated yield 18.89%, maturity October 22, 2031) | 13,500,000 | 8,197,556 | 7,560,000 | |||||||||||||

| Covenant Credit Partners CLO II, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 0.00%, maturity October 17, 2026) | 8,650,000 | — | — | |||||||||||||

| Dryden 49 Senior Loan Fund | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 14.50%, maturity July 18, 2030) | 6,425,000 | 5,260,019 | 4,176,250 | |||||||||||||

| Dryden 54 Senior Loan Fund | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 16.12%, maturity October 19, 2029) | 2,500,000 | 2,047,805 | 1,750,000 | |||||||||||||

| Ellington CLO II, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 20.32%, maturity February 15, 2029) | 4,000,000 | 3,588,441 | 3,200,000 | |||||||||||||

| Figueroa CLO 2013-2, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 14.78%, maturity June 20, 2027) | 8,500,000 | 4,247,811 | 3,995,000 | |||||||||||||

| Flatiron CLO 17 Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 23.99%, maturity May 15, 2030) | 2,337,500 | 1,558,908 | 1,566,125 | |||||||||||||

| GoldenTree Loan Opportunities XI, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 13.33%, maturity January 18, 2031) | 3,000,000 | 2,409,633 | 2,250,000 | |||||||||||||

| Golub Capital Partners CLO 35(B), Ltd., | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 17.64%, maturity July 20, 2029) | 14,200,000 | 10,546,826 | 8,378,000 | |||||||||||||

| Halcyon Loan Advisors Funding 2015-1 Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 1.66%, maturity April 20, 2027) | 7,000,000 | 3,357,798 | 2,100,000 | |||||||||||||

| Halcyon Loan Advisors Funding 2018-1 Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 17.52%, maturity July 20, 2031) | 11,250,000 | 10,323,510 | 9,675,000 | |||||||||||||

| Hull Street CLO Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield -11.98%, maturity October 18, 2026) | 15,000,000 | 4,806,094 | 1,950,000 | |||||||||||||

| ICG US CLO 2016-1, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 9.78%, maturity July 29, 2028) | 4,750,000 | 4,641,569 | 3,490,300 | |||||||||||||

| Ivy Hill Middle Market Credit VII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 9.54%, maturity October 20, 2029) | 5,400,000 | 4,524,254 | 3,213,869 | |||||||||||||

| Jamestown CLO III, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(10), (Estimated yield 0.00%, maturity January 15, 2026) | 15,575,000 | 984,321 | — | |||||||||||||

(Continued on next page)

See Accompanying Notes.

6

OXFORD LANE CAPITAL CORP.

SCHEDULE OF INVESTMENTS - (continued)

MARCH 31, 2019

| COMPANY/INVESTMENT(1)(14) | PRINCIPAL

AMOUNT | COST | FAIR VALUE(2) | %

of Net Assets | ||||||||||||

| Collateralized Loan Obligation - Equity Investments - (continued) | ||||||||||||||||

| Structured Finance - Equity Investments (continued) | ||||||||||||||||

| Jamestown CLO IV, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield -10.09%, maturity July 15, 2026) | 9,500,000 | 2,917,908 | 1,105,857 | |||||||||||||

| Jamestown CLO VII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield -6.38%, maturity July 25, 2027) | 3,500,000 | 2,273,294 | 1,540,000 | |||||||||||||

| Longfellow Place CLO, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 22.63%, maturity April 15, 2029) | 19,640,000 | 8,038,087 | 4,973,600 | |||||||||||||

| Madison Park Funding XI, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 8.74%, maturity July 23, 2047) | 1,236,843 | 850,408 | 606,053 | |||||||||||||

| Madison Park Funding XV, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 15.68%, maturity January 27, 2026) | 7,000,000 | 4,324,344 | 4,270,000 | |||||||||||||

| Madison Park Funding XXIV, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 18.95%, maturity January 20, 2028) | 3,568,750 | 2,628,480 | 2,623,031 | |||||||||||||

| Madison Park Funding XXV, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 12.03%, maturity April 25, 2029) | 1,300,000 | 1,187,291 | 1,053,000 | |||||||||||||

| Madison Park Funding XXIX, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 13.36%, maturity October 18, 2047) | 17,000,000 | 14,935,777 | 15,300,000 | |||||||||||||

| Madison Park Funding XXX, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(11)(12), (Estimated yield 20.14%, maturity April 15, 2029) | 17,550,000 | 16,091,913 | 17,116,035 | |||||||||||||

| Madison Park Fund XLI, Ltd. (fka: Atrium XII CLO) | ||||||||||||||||

| CLO subordinated notes(5)(7)(11)(15), (Estimated yield 24.27%, maturity April 22, 2027) | 34,762,500 | 24,171,426 | 25,376,625 | |||||||||||||

| Midocean Credit CLO VI | ||||||||||||||||

| CLO income notes(5)(7)(11), (Estimated yield 9.12%, maturity January 20, 2029) | 24,700,000 | 21,239,806 | 15,561,000 | |||||||||||||

| Mountain Hawk II CLO, Ltd. | ||||||||||||||||

| CLO secured notes (3)(4)(5), (Estimated yield -27.02%, maturity July 20, 2024) | 25,670,000 | 4,950,079 | 1,283,500 | |||||||||||||

| Mountain View CLO 2014-1 Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 2.43%, maturity October 15, 2026) | 15,000,000 | 3,596,519 | 1,885,075 | |||||||||||||

| Mountain View CLO 2017-2 Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 22.65%, maturity January 16, 2031) | 1,400,000 | 1,138,072 | 1,120,000 | |||||||||||||

| Ocean Trails CLO VI | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 20.91%, maturity July 15, 2028) | 4,000,000 | 3,260,811 | 2,518,438 | |||||||||||||

| Octagon Investment Partners XXII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 19.52%, maturity January 22, 2030) | 3,168,750 | 2,084,341 | 1,996,313 | |||||||||||||

| Octagon Investment Partners 27, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 19.85%, maturity July 15, 2030) | 5,000,000 | 3,354,424 | 3,182,172 | |||||||||||||

(Continued on next page)

See Accompanying Notes.

7

OXFORD LANE CAPITAL CORP.

SCHEDULE OF INVESTMENTS - (continued)

MARCH 31, 2019

| COMPANY/INVESTMENT(1)(14) | PRINCIPAL

AMOUNT | COST | FAIR VALUE(2) | %

of Net Assets | ||||||||||||

| Collateralized Loan Obligation - Equity Investments - (continued) | ||||||||||||||||

| Structured Finance - Equity Investments (continued) | ||||||||||||||||

| Octagon Investment Partners 33, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 16.41%, maturity January 20, 2031) | $ | 10,000,000 | $ | 9,111,226 | $ | 8,700,000 | ||||||||||

| Octagon Investment Partners 38, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 17.38%, maturity July 20, 2030) | 5,000,000 | 4,352,357 | 4,400,000 | |||||||||||||

| Octagon Investment Partners 39, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(9)(12), (Estimated yield 18.18%, maturity October 20, 2030) | 10,400,000 | 9,444,872 | 9,152,000 | |||||||||||||

| Octagon Investment Partners 40, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(9)(15), (Estimated yield 18.16%, maturity April 20, 2031) | 47,250,000 | 40,090,291 | 39,193,403 | |||||||||||||

| Octagon Loan Funding, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 19.45%, maturity November 18, 2031) | 1,774,526 | 1,010,677 | 1,046,970 | |||||||||||||

| OFSI Fund VII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield -5.11%, maturity October 18, 2026) | 28,840,000 | 18,561,124 | 10,670,800 | |||||||||||||

| OFSI BSL IX, LTD. | ||||||||||||||||

| CLO preferred shares(5)(7)(12), (Estimated yield 19.29%, maturity July 31, 2118) | 11,480,000 | 10,323,461 | 9,758,000 | |||||||||||||

| OZLM Funding III, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 12.20%, maturity January 22, 2029) | 12,000,000 | 7,426,847 | 5,640,000 | |||||||||||||

| OZLM VIII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 22.50%, maturity October 17, 2029) | 10,000,000 | 3,412,892 | 3,400,000 | |||||||||||||

| OZLM XIII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 12.14%, maturity July 30, 2027) | 7,000,000 | 5,005,662 | 3,360,000 | |||||||||||||

| OZLM XIV, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(11), (Estimated yield 11.38%, maturity January 15, 2029) | 10,000,000 | 8,242,555 | 5,830,609 | |||||||||||||

| Regatta III Funding Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(10)(16), (Estimated yield 0.00%, maturity April 15, 2026) | 3,750,000 | 38,367 | 112,500 | |||||||||||||

| Shackleton 2013-IV-R CLO, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 21.05%, maturity April 13, 2031) | 16,750,000 | 13,968,282 | 12,500,846 | |||||||||||||

| Shackleton 2015-VII CLO, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 20.05%, maturity July 15, 2031) | 12,500,000 | 9,339,127 | 7,674,657 | |||||||||||||

| Shackleton 2017-X CLO, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 10.82%, maturity April 20, 2029) | 10,000,000 | 8,931,584 | 6,400,000 | |||||||||||||

| Sound Point CLO VI-R, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(9), (Estimated yield 14.31%, maturity October 20, 2031) | 8,093,378 | 4,311,871 | 3,803,888 | |||||||||||||

| Steele Creek CLO 2016-1, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 18.90%, maturity June 15, 2031) | 4,000,000 | 3,592,952 | 3,320,000 | |||||||||||||

| Telos CLO 2013-3, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 11.15%, maturity July 17, 2026) | 14,332,210 | 8,843,427 | 5,302,918 | |||||||||||||

| Telos CLO 2013-4, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 19.07%, maturity January 17, 2030) | 11,350,000 | 7,283,045 | 5,914,465 | |||||||||||||

| Telos CLO 2014-6, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 12.92%, maturity January 17, 2027) | 21,400,000 | 9,441,544 | 8,673,254 | |||||||||||||

(Continued on next page)

See Accompanying Notes.

8

OXFORD LANE CAPITAL CORP.

SCHEDULE OF INVESTMENTS - (continued)

MARCH 31, 2019

| COMPANY/INVESTMENT(1)(14) | PRINCIPAL

AMOUNT | COST | FAIR VALUE(2) | %

of Net Assets | ||||||||||||

| Collateralized Loan Obligation - Equity Investments - (continued) | ||||||||||||||||

| Structured Finance - Equity Investments (continued) | ||||||||||||||||

| THL Credit Wind River 2017-1 CLO Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(11), (Estimated yield 10.76%, maturity April 18, 2029) | $ | 12,000,000 | $ | 10,232,086 | $ | 7,680,000 | ||||||||||

| THL Credit Wind River 2017-4 CLO Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 16.27%, maturity November 20, 2030) | 8,200,000 | 7,728,752 | 7,298,000 | |||||||||||||

| Tralee CLO II, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 27.10%, maturity July 20, 2029) | 6,300,000 | 2,495,876 | 2,142,000 | |||||||||||||

| Tralee CLO IV, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 18.56%, maturity January 20, 2030) | 13,270,000 | 11,852,556 | 10,350,600 | |||||||||||||

| Trinitas CLO VIII, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 19.89%, maturity July 20, 2117) | 750,000 | 634,971 | 630,000 | |||||||||||||

| Venture XIV CLO, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 18.04%, maturity August 28, 2029) | 8,250,000 | 4,716,747 | 3,547,500 | |||||||||||||

| Venture XV CLO, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 9.76%, maturity July 15, 2028) | 6,500,000 | 4,385,413 | 2,990,000 | |||||||||||||

| Venture XVII CLO, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 19.40%, maturity April 15, 2027) | 17,000,000 | 11,318,937 | 8,656,011 | |||||||||||||

| Venture XX CLO, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 14.45%, maturity April 15, 2027) | 6,000,000 | 4,296,647 | 3,420,000 | |||||||||||||

| Venture XXI CLO, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 14.96%, maturity July 15, 2027) | 26,950,000 | 17,631,648 | 15,631,000 | |||||||||||||

| Venture 32 CLO, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 19.61%, maturity July 18, 2031) | 3,500,000 | 3,204,292 | 3,167,500 | |||||||||||||

| Venture 33 CLO, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 19.32%, maturity July 15, 2031) | 12,987,500 | 11,151,087 | 11,169,250 | |||||||||||||

| Vibrant CLO III, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 23.37%, maturity October 20, 2031) | 5,000,000 | 3,612,920 | 3,650,000 | |||||||||||||

| Wellfleet 2016-2 CLO, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 20.96%, maturity October 20, 2028) | 10,000,000 | 8,482,286 | 7,200,000 | |||||||||||||

| West CLO 2014-1, Ltd. | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 15.85%, maturity July 18, 2026) | 3,000,000 | 1,567,758 | 1,380,000 | |||||||||||||

| Zais CLO 8, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7)(12), (Estimated yield 27.01%, maturity April 15, 2029) | 3,000,000 | 2,330,446 | 2,490,000 | |||||||||||||

| Zais CLO 9, Limited | ||||||||||||||||

| CLO subordinated notes(5)(7), (Estimated yield 21.53%, maturity July 20, 2031) | 10,700,000 | 9,490,216 | 9,095,000 | |||||||||||||

(Continued on next page)

See Accompanying Notes.

9

OXFORD LANE CAPITAL CORP.

SCHEDULE OF INVESTMENTS - (continued)

MARCH 31, 2019

| COMPANY/INVESTMENT(1)(14) | PRINCIPAL

AMOUNT | COST | FAIR VALUE(2) | %

of Net Assets | ||||||||||||

| Collateralized Loan Obligation - Equity Investments - (continued) | ||||||||||||||||

| Structured Finance - Equity Investments (continued) | ||||||||||||||||

| Other CLO equity related investments | ||||||||||||||||

| CLO other(8) | — | 2,511,980 | ||||||||||||||

| Total Structured Finance - Equity Investments | $ | 608,626,842 | $ | 526,692,154 | 148.88 | % | ||||||||||

| Total Collateralized Loan Obligation - Equity Investments | $ | 608,626,842 | $ | 526,692,154 | 148.88 | % | ||||||||||

| Total Investments | $ | 619,716,034 | $ | 537,440,723 | 151.92 | % | ||||||||||

| Cash and Cash Equivalents | ||||||||||||||||

| First American Government Obligations Fund(13) | $ | 21,473,934 | $ | 21,473,934 | ||||||||||||

| Total Cash and Cash Equivalents | $ | 21,473,934 | $ | 21,473,934 | 3.86 | % | ||||||||||

| Total Investments, Cash and Cash Equivalents | $ | 641,189,968 | $ | 558,914,657 | 155.78 | % | ||||||||||

| (1) | We do not “control” and are not an “affiliate” of any of our portfolio companies, each as defined in the Investment Company Act of 1940, as amended (the “1940 Act”). In general, under the 1940 Act, we would be presumed to “control” a portfolio company if we owned 25% or more of its voting securities and would be an “affiliate” of a portfolio company if we owned 5% or more of its voting securities. |

| (2) | Fair value is determined in good faith by the Board of Directors of the Fund. |

| (3) | Notes bear interest at variable rates. |

| (4) | Cost value reflects accretion of original issue discount or market discount. |

| (5) | Cost value reflects accretion of effective yield less any cash distributions received or entitled to be received from CLO equity investments. |

| (6) | The CLO secured notes generally bear interest at a rate determined by reference to three-month LIBOR which resets quarterly. For each CLO debt investment, the rate provided is as of March 31, 2019. |

| (7) | The CLO subordinated notes and income notes are considered equity positions in the CLO funds. Equity investments are entitled to recurring distributions which are generally equal to the remaining cash flow of the payments made by the underlying fund’s securities less contractual payments to debt holders and fund expenses. The estimated yield indicated is based upon a current projection of the amount and timing of these recurring distributions and the estimated amount of repayment of principal upon termination. Such projections are periodically reviewed and adjusted, and the estimated yield may not ultimately be realized. |

| (8) | Fair value represents discounted cash flows associated with fees earned from CLO equity investments. |

| (9) | Investment has not made inaugural distribution for relevant period end. See “Note 2. Summary of Significant Accounting Policies - Investment Income.” |

| (10) | The CLO equity investment was optionally redeemed. See “Note 2. Summary of Significant Accounting Policies - Securities Transactions.” |

| (11) | Securities held as collateral pursuant to repurchase agreement with Nomura Securities International, Inc. See “Note 8. Borrowings Related to Securities Sold Under Agreement to Repurchase.” |

| (12) | The CLO equity is co-invested with the Fund’s affiliates. See “Note 4. Related Party Transactions.” |

| (13) | Represents cash equivalents held in a money market account as of March 31, 2019. |

| (14) | The fair value of the investment was determined using significant unobservable inputs. See “Note 3. Fair Value.” |

| (15) | Aggregate investments represent greater than 5% of net assets. |

| (16) | This investment represents our percent ownership in certain equity securities transferred to OXLC upon the redemption of this investment on October 25, 2018. |

See Accompanying Notes.

10

OXFORD LANE CAPITAL CORP.

| Year Ended March 31, 2019 | ||||

| INVESTMENT INCOME | ||||

| Income from securitization vehicles and investments | $ | 85,656,178 | ||

| Interest income - debt investments | 1,398,612 | |||

| Other income | 2,344,189 | |||

| Total investment income | 89,398,979 | |||

| EXPENSES | ||||

| Interest expense | 15,051,475 | |||

| Investment advisory fees | 10,581,133 | |||

| Incentive fees | 12,271,355 | |||

| Professional fees | 721,390 | |||

| Administrator expense | 630,998 | |||

| General and administrative | 436,994 | |||

| Directors’ fees | 319,000 | |||

| Insurance expense | 160,548 | |||

| Transfer agent and custodian fees | 140,669 | |||

| Total expenses | 40,313,562 | |||

| Net investment income | 49,085,417 | |||

| Net change in unrealized depreciation on investments | (67,170,145 | ) | ||

| Net realized loss on investments | (2,897,270 | ) | ||

| Net realized loss and net change in unrealized depreciation | $ | (70,067,415 | ) | |

| Net decrease in net assets resulting from operations | $ | (20,981,998 | ) | |

See Accompanying Notes.

11

OXFORD LANE CAPITAL CORP.

STATEMENT OF CHANGES IN NET ASSETS

| Year Ended March 31, 2019 | Year Ended March 31, 2018 | |||||||

| Decrease in net assets from operations: | ||||||||

| Net investment income | $ | 49,085,417 | $ | 40,353,995 | ||||

| Net realized (loss) gain on investments | (2,897,270 | ) | 625,683 | |||||

| Net realized loss on the redemption of mandatorily redeemable preferred stock | — | (1,709,991 | ) | |||||

| Net change in unrealized depreciation on investments | (67,170,145 | ) | (1,264,099 | ) | ||||

| Net (decrease) increase in net assets resulting from operations | (20,981,998 | ) | 38,005,588 | |||||

| Distributions from net investment income | (47,264,503 | ) | (35,198,279 | ) | ||||

| Tax return of capital distributions | (9,750,228 | ) | (6,318,441 | ) | ||||

| Total distributions to shareholders | (57,014,731 | ) | (41,516,720 | ) | ||||

| Capital share transaction: | ||||||||

| Issuance of common stock (net of underwriting fees and offering costs of $2,535,898 and $1,090,419, respectively) | 139,119,170 | 61,392,800 | ||||||

| Reinvestment of dividends | 2,779,536 | — | ||||||

| Net increase in net assets from capital share transactions | 141,898,706 | 61,392,800 | ||||||

| Total increase in net assets | 63,901,977 | 57,881,668 | ||||||

| Net assets at beginning of period | 289,930,113 | 232,048,445 | ||||||

| Net assets at end of period | $ | 353,832,090 | $ | 289,930,113 | ||||

| Capital share activity: | ||||||||

| Shares issued | 13,496,082 | 6,017,467 | ||||||

| Shares issued from reinvestment of dividends | 282,820 | — | ||||||

| Net increase in capital share activity | 13,778,902 | 6,017,467 | ||||||

See Accompanying Notes.

12

OXFORD LANE CAPITAL CORP.

| Year Ended March 31, 2019 | ||||

| CASH FLOWS FROM OPERATING ACTIVITIES | ||||

| Net decrease in net assets resulting from operations | $ | (20,981,998 | ) | |

| Adjustments to reconcile net decrease in net assets resulting from operations to net cash used in operating activities: | ||||

| Amortization/accretion of discounts and premiums | (216,033 | ) | ||

| Amortization of deferred issuance costs on mandatorily redeemable preferred stock | 683,121 | |||

| Accretion of discount on mandatorily redeemable preferred stock | 565,592 | |||

| Amortization of deferred offering costs on common stock | 270,656 | |||

| Purchases of investments | (504,133,287 | ) | ||

| Sales of investments | 235,925,382 | |||

| Repayments of principal and reductions to investment cost value | 93,250,000 | |||

| Net change in unrealized depreciation on investments | 67,170,145 | |||

| Net realized loss on investments | 2,897,270 | |||

| Net reductions to CLO equity cost value | 44,484,167 | |||

| Increase in distributions receivable | (3,295,524 | ) | ||

| Decrease in fee receivable | 21,198 | |||

| Increase in interest receivable | (17,633 | ) | ||

| Increase in prepaid expenses and other assets | (601,752 | ) | ||

| Decrease in investment advisory fee payable | (172,785 | ) | ||

| Increase in incentive fee payable | 642,748 | |||

| Increase in interest payable | 94,794 | |||

| Increase in directors’ fees payable | 11,250 | |||

| Decrease in administrator expense payable | (29,403 | ) | ||

| Decrease in accrued offering costs | (11,012 | ) | ||

| Increase in accrued expenses | 44,967 | |||

| Net cash used in operating activities | (83,398,137 | ) | ||

| CASH FLOWS FROM FINANCING ACTIVITIES | ||||

| Distributions paid (net of dividend reinvestment plan of $2,779,536) | (54,235,195 | ) | ||

| Proceeds from the issuance of common stock | 141,655,068 | |||

| Underwriting fees and offering costs for the issuance of common stock | (2,535,898 | ) | ||

| Deferred offering costs | (346,126 | ) | ||

| Net cash provided by financing activities | 84,537,849 | |||

| Net increase in cash and cash equivalents | 1,139,712 | |||

| Cash and cash equivalents, beginning of period | 20,334,222 | |||

| Cash and cash equivalents, end of period | $ | 21,473,934 | ||

| SUPPLEMENTAL DISCLOSURES | ||||

| Cash paid for interest | $ | 13,592,102 | ||

| NON-CASH ACTIVITIES | ||||

| Value of shares issued in connection with dividend reinvestment plan | $ | 2,779,536 | ||

| Securities sold not settled | $ | 4,790,000 | ||

| Securities purchased not settled | $ | 17,404,918 | ||

| Receipt of distribution in-kind | $ | 1,233,900 | ||

See Accompanying Notes.

13

OXFORD LANE CAPITAL CORP.

NOTES TO FINANCIAL STATEMENTS

MARCH 31, 2019

NOTE 1. ORGANIZATION

Oxford Lane Capital Corp. (“OXLC,” “we,” “us,” “our,” or the “Fund”) was incorporated under the General Corporation Laws of the State of Maryland on June 9, 2010. The Fund is a non-diversified closed-end management investment company that has registered under the Investment Company Act of 1940, as amended (the “1940 Act”). In addition, the Fund has elected to be treated for tax purposes as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). The Fund’s investment objective is to maximize its portfolio’s risk adjusted total return, and it currently seeks to achieve its investment objective by investing in structured finance investments, specifically the equity and junior debt tranches of collateralized loan obligation (“CLO”) vehicles, which are collateralized primarily by a diverse portfolio of Senior Loans, and which generally have very little or no exposure to real estate loans, or mortgage loans or to pools of consumer-based debt, such as credit card receivables or auto loans.

OXLC’s investment activities are managed by Oxford Lane Management, LLC (“OXLC Management”), a registered investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act.”) Oxford Funds, LLC (“Oxford Funds”), is the managing member of OXLC Management and serves as the administrator of OXLC. Under the investment advisory agreement with OXLC Management (the “Investment Advisory Agreement”), OXLC has agreed to pay OXLC Management an annual base management fee based on gross assets as well as an incentive fee based on its performance. For further detail please refer to “Note 4. Related Party Transactions.”

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

BASIS OF PRESENTATION

The accompanying financial statements, which have been prepared in accordance with generally accepted accounting principles in the United States of America (“GAAP”), include the accounts of the Fund. The Fund follows the accounting and reporting guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services — Investment Companies. Certain prior period figures have been reclassified from those originally published on Form N-CSR to conform to the current period presentation for comparative purposes. The Fund maintains its accounting records in U.S. dollars.

USE OF ESTIMATES

The financial statements have been prepared in accordance with GAAP, which requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results may differ from those estimates and such differences could be material.

In the normal course of business, the Fund may enter into contracts that contain a variety of representations and provide indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. However, based upon experience, the Fund expects the risk of loss to be remote.

CASH AND CASH EQUIVALENTS

Cash and cash equivalents consist of demand deposits and cash held in a money market fund which contain investments with original maturities of three months or less. The Fund places its cash and cash equivalents with financial institutions and, at times, cash held in bank accounts may exceed the Federal Deposit Insurance Corporation (“FDIC”) insured limit. Cash equivalents are classified as Level 1 assets and are included on the Fund’s Schedule of Investments. Cash equivalents are carried at cost or amortized cost which approximates fair value.

14

OXFORD LANE CAPITAL CORP.

NOTES TO FINANCIAL STATEMENTS

March 31, 2019

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

INVESTMENT VALUATION

The Fund fair values its investment portfolio in accordance with the provisions of ASC 820, Fair Value Measurement and Disclosure. Estimates made in the preparation of OXLC’s financial statements include the valuation of investments and the related amounts of unrealized appreciation and depreciation of investments recorded. OXLC believes that there is no single definitive method for determining fair value in good faith. As a result, determining fair value requires that judgment be applied to the specific facts and circumstances of each portfolio investment while employing a consistently applied valuation process for the types of investments OXLC makes. OXLC is required to specifically fair value each individual investment on a quarterly basis.