Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(B) OR (G) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended March 31, 2015

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number 001-34837

MakeMyTrip Limited

(Exact Name of Registrant as specified in its charter)

| Not Applicable | Mauritius | |

| (Translation of Registrant’s Name Into English) | (Jurisdiction of Incorporation or Organization) |

Tower A, SP Infocity, 243,

Udyog Vihar, Phase 1

Gurgaon, Haryana 122016, India

(Address of Principal Executive Offices)

Mohit Kabra

Group Chief Financial Officer

Tower A, SP Infocity, 243,

Udyog Vihar, Phase 1

Gurgaon, Haryana 122016, India

(91-124) 439-5000

mohit.kabra@makemytrip.com

(Name, Telephone, E-mail and/or facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Ordinary Shares, par value $0.0005 per share | Nasdaq Global Market | |

| (Title of Class) | (Name of Exchange On Which Registered) |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report.

As of March 31, 2015, 41,986,966 ordinary shares, par value $0.0005 per share, were issued and outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ¨ No x

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See the definitions of “large accelerated filer” and “accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| US GAAP ¨ |

International Financial Reporting Standards as issued | Other ¨ | ||

| by the International Accounting Standards Board x |

If “Other” has been checked in the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 ¨

If this is an Annual Report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).

Yes ¨ No x

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court:

Yes ¨ No ¨

Table of Contents

| PAGE | ||||

| PART I |

||||

| ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

4 | |||

| 4 | ||||

| 4 | ||||

| 30 | ||||

| 53 | ||||

| 53 | ||||

| 76 | ||||

| 92 | ||||

| 95 | ||||

| 99 | ||||

| 101 | ||||

| ITEM 11. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK |

121 | |||

| ITEM 12. DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES |

122 | |||

| PART II |

||||

| 123 | ||||

| ITEM 14. MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

123 | |||

| 123 | ||||

| 126 | ||||

| 126 | ||||

| 126 | ||||

| ITEM 16D. EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES |

127 | |||

| ITEM 16E. PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

127 | |||

| 127 | ||||

| 128 | ||||

| 128 | ||||

| PART III |

||||

| 129 | ||||

| 129 | ||||

| 129 | ||||

| 133 | ||||

| F-1 | ||||

Table of Contents

CONVENTIONS USED IN THIS ANNUAL REPORT

In this Annual Report, we refer to information regarding the travel service industry and our competitors from market research reports, analyst reports and other publicly available sources, including from PhoCusWright Inc., or PhoCusWright, an independent travel industry research company founded and previously controlled by Mr. Philip C. Wolf, one of our directors. See “Item 7. Major Shareholders and Related Party Transactions — Transactions with PhoCusWright” for details of our transactions with PhoCusWright. We also refer to data from the United States Central Intelligence Agency “World Factbook”, or CIA World Factbook, the Directorate General of Civil Aviation, the Indian governmental regulatory body for civil aviation, or DGCA and the Internet and Mobile Association of India, or IAMAI.

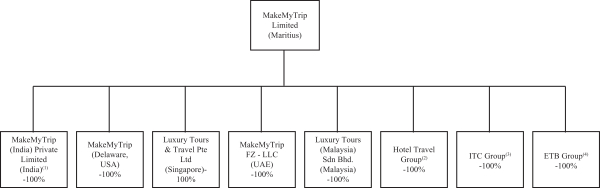

We conduct our business principally through our Indian subsidiary, MakeMyTrip (India) Private Limited, or MMT India. Our other principal operating subsidiaries include Hotel Travel Limited, Malaysia and HTN Co., Ltd., Thailand, the two main operating entities of the group of companies known as the Hotel Travel Group; ITC Bangkok Co., Ltd., Thailand, the main operating entity of the group of companies known as the ITC Group; Luxury Tours & Travel Pte Ltd, Singapore, or Luxury Tours; Luxury Tours (Malaysia) Sdn. Bhd. or Luxury Tours (Malaysia); MakeMyTrip Inc., or MMT USA; and Easy To Book Service B.V., the main operating entity of the group of companies known as the Easytobook.com group, or the ETB Group. In this Annual Report, unless otherwise stated or unless the context otherwise requires, references to “we,” “us,” “our,” “our company” or “our group” are to MakeMyTrip Limited and its subsidiaries collectively, and references to “our holding company” are to MakeMyTrip Limited on a standalone basis.

In this Annual Report, references to “US,” the “United States” or “USA” are to the United States of America, its territories and its possessions, references to “India” are to the Republic of India, references to “Mauritius” are to the Republic of Mauritius, references to “the Netherlands” are to the Kingdom of the Netherlands, references to “Singapore” are to the Republic of Singapore, references to “Malaysia” are to the Federation of Malaysia and references to “Thailand” are to the Kingdom of Thailand. References to “$,” “dollars” or “US dollars” are to the legal currency of the United States, references to “Rs.,” “Rupees” or “Indian Rupees” are to the legal currency of India and references to “Euro” are to the legal currency of the European Union.

Solely for the convenience of the reader, this Annual Report contains translations of certain Indian Rupee amounts into US dollars at specified rates. Except as otherwise stated in this Annual Report, all translations from Indian Rupees to US dollars are based on the noon buying rate of Rs. 63.71 per $1.00 in the City of New York for cable transfers of Indian Rupees, as certified for customs purposes by the Federal Reserve Bank of New York on May 29, 2015. No representation is made that the Indian Rupee amounts referred to in this Annual Report could have been or could be converted into US dollars at such rates or any other rates. Any discrepancies in any table between totals and sums of the amounts listed are due to rounding.

Unless otherwise indicated, the consolidated statement of profit or loss and other comprehensive income (loss) and related notes for fiscal years 2013, 2014 and 2015 and consolidated statement of financial position of March 31, 2014 and 2015 included elsewhere in this Annual Report have been prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. References to a particular “fiscal year” are to our fiscal year ended March 31 of that year. Our fiscal quarters end on June 30, September 30, December 31 and March 31. References to a year other than a “fiscal” year are to the calendar year ended December 31.

We also refer in various places within this Annual Report to “adjusted operating profit (loss),” “adjusted net profit (loss)” and “revenue less service cost,” which are non-IFRS measures. “Revenue less service cost” is calculated as revenue less costs for the acquisition of relevant services and products for sale to customers. The IFRS measures most directly comparable to “adjusted operating profit (loss)” and “adjusted net profit (loss)” are results from operating activities and profit (loss) for the year, respectively. Each item is more fully explained in

2

Table of Contents

“Item 5. Operating and Financial Review and Prospects”. The presentation of these non-IFRS measures is not meant to be considered in isolation or as a substitute for our consolidated financial results prepared in accordance with IFRS as issued by the IASB.

On June 1, 2015, we designated five officers as additional executive officers including Chief Marketing Officer, Chief Human Resource Officer, Chief Technology Officer – International & platforms, Chief Technology Officer – India and Chief Business Officer – Holidays. Since this occurred after the end of fiscal year 2015, this Annual Report only reflects the foregoing in “Item 6.A. Directors and Senior Management” and “Item 6.E. Share Ownership”.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements that relate to our current expectations and views of future events. These forward-looking statements are contained principally in the sections entitled “Item 3. Key Information,” “Item 4. Information on the Company” and “Item 5. Operating and Financial Review and Prospects.” These statements relate to events that involve known and unknown risks, uncertainties and other factors, including those listed under “Item 3. Key Information — D. Risk Factors,” which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, these forward-looking statements can be identified by words or phrases such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “potential,” “continue,” “is/are likely to” or other similar expressions.

These forward-looking statements are subject to risks, uncertainties and assumptions, some of which are beyond our control. In addition, these forward-looking statements reflect our current views with respect to future events and are not a guarantee of future performance. Actual outcomes may differ materially from the information contained in the forward-looking statements as a result of a number of factors, including, without limitation, the risk factors set forth in “Item 3. Key Information — D. Risk Factors,” and the following:

| • | our ability to maintain and expand our supplier relationships; |

| • | our reliance on technology; |

| • | our ability to expand our business, implement our strategy and effectively manage our growth; |

| • | political and economic stability in and around India, Thailand and other key travel destinations; |

| • | our ability to successfully implement our growth strategy; |

| • | our ability to attract, train and retain executives and other qualified employees; |

| • | increasing competition in the Indian travel industry; and |

| • | risks associated with online commerce security. |

The forward-looking statements made in this Annual Report relate only to events or information as of the date on which the statements are made in this Annual Report. Our actual results, performance, or achievement may differ from those expressed in, or implied by, these forward-looking statements. Accordingly, we can give no assurances that any of the events anticipated by these forward-looking statements will transpire or occur or, if any of the foregoing factors or other risks and uncertainties described elsewhere in this Annual Report were to occur, what impact they would have on these forward-looking statements, including our results of operations or financial condition. In view of these uncertainties, you are cautioned not to place undue reliance on these forward-looking statements.

Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

3

Table of Contents

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable

A. Selected Consolidated Financial Data

The following selected consolidated statement of profit or loss and other comprehensive income (loss) data for fiscal years 2013, 2014 and 2015 and the selected consolidated statement of financial position data as of March 31, 2014 and 2015 have been derived from our audited consolidated financial statements included elsewhere in this Annual Report. The selected consolidated statement of profit or loss and other comprehensive income (loss) data for fiscal years 2011 and 2012 and the selected consolidated statement of financial position data as of March 31, 2011, 2012 and 2013 have been derived from our audited consolidated financial statements not included in this Annual Report. The financial data set forth below should be read in conjunction with, and is qualified by reference to, “Item 5. Operating and Financial Review and Prospects” and the consolidated financial statements and notes thereto included elsewhere in this Annual Report. Our consolidated financial statements are prepared and presented in accordance with IFRS as issued by the IASB. Our historical results do not necessarily indicate results expected for any future period.

4

Table of Contents

The following information should be read in conjunction with, and is qualified in its entirety by reference to, “Item 5. Operating and Financial Review and Prospects” and the audited consolidated financial statements and the notes thereto included elsewhere in this Annual Report.

| Fiscal Year Ended March 31 | ||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | ||||||||||||||||

| (in thousands, except percentages) | ||||||||||||||||||||

| Consolidated Statement of Profit or Loss and Other Comprehensive Income (Loss) Data: |

||||||||||||||||||||

| Revenue: |

||||||||||||||||||||

| Air ticketing |

$ | 47,622.7 | $ | 76,190.3 | $ | 60,888.8 | $ | 66,523.2 | $ | 74,324.9 | ||||||||||

| Hotels and packages |

74,558.0 | 116,701.1 | 164,129.3 | 184,500.7 | 220,511.9 | |||||||||||||||

| Other revenue |

2,540.7 | 3,707.8 | 3,803.8 | 4,350.7 | 4,824.9 | |||||||||||||||

| Total revenue |

124,721.4 | 196,599.3 | 228,821.9 | 255,374.6 | 299,661.7 | |||||||||||||||

| Other Income |

— | — | — | 1,312.3 | 853.4 | |||||||||||||||

| Service cost: |

||||||||||||||||||||

| Procurement cost of hotels and packages services |

(63,650.9 | ) | (98,474.8 | ) | (136,537.1 | ) | (144,507.8 | ) | (157,897.2 | ) | ||||||||||

| Cost of air ticket coupons |

— | (9,939.6 | ) | (4,119.6 | ) | (4,471.7 | ) | (2,815.7 | ) | |||||||||||

| Personnel expenses |

(14,399.0 | ) | (26,520.7 | ) | (34,520.5 | ) | (37,220.8 | ) | (44,317.5 | ) | ||||||||||

| Other operating expenses |

(40,698.9 | ) | (54,868.7 | ) | (67,954.0 | ) | (80,116.0 | ) | (102,069.0 | ) | ||||||||||

| Depreciation and amortization |

(1,910.6 | ) | (2,790.2 | ) | (3,752.7 | ) | (5,692.1 | ) | (7,954.6 | ) | ||||||||||

| Results from operating activities |

4,061.9 | 4,005.4 | (18,062.0 | ) | (15,321.6 | ) | (14,540.0 | ) | ||||||||||||

| Net finance income (costs) |

(1,923.9 | ) | (2,969.2 | ) | (741.9 | ) | (5,334.0 | ) | (3,543.5 | ) | ||||||||||

| Share of loss of equity-accounted investees |

— | (66.0 | ) | (186.1 | ) | (171.5 | ) | (139.2 | ) | |||||||||||

| Profit (Loss) before tax |

2,138.0 | 970.2 | (18,990.1 | ) | (20,827.0 | ) | (18,223.0 | ) | ||||||||||||

| Income tax benefit (expense) |

2,691.7 | 6,078.1 | (8,599.0 | ) | (78.5 | ) | (134.6 | ) | ||||||||||||

| Profit (Loss) for the year |

$ | 4,829.7 | $ | 7,048.4 | $ | (27,589.1 | ) | $ | (20,905.6 | ) | $ | (18,358.0 | ) | |||||||

| Earnings (Loss) per ordinary share: |

||||||||||||||||||||

| Basic |

$ | 0.17 | $ | 0.20 | $ | (0.74 | ) | $ | (0.55 | ) | $ | (0.44 | ) | |||||||

| Diluted |

$ | 0.15 | $ | 0.19 | $ | (0.74 | ) | $ | (0.55 | ) | $ | (0.44 | ) | |||||||

| Weighted average number of ordinary shares outstanding: |

||||||||||||||||||||

| Basic |

28,320,901 | 36,682,240 | 37,315,434 | 37,832,246 | 41,808,897 | |||||||||||||||

| Diluted |

34,950,246 | 38,234,070 | 37,315,434 | 37,832,246 | 41,808,897 | |||||||||||||||

| Proforma earnings (loss) per ordinary share(1) |

||||||||||||||||||||

| Basic |

$ | 0.16 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Diluted |

$ | 0.15 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Proforma weighted average number of ordinary shares outstanding(1) |

||||||||||||||||||||

| Basic |

32,993,361 | — | — | — | — | |||||||||||||||

| Diluted |

34,929,282 | — | — | — | — | |||||||||||||||

Note:

| (1) | In December 2006, August 2007 and May 2008, we issued Series A, Series B and Series C preferred shares, respectively, that were converted into ordinary shares effective upon the completion of our initial public offering on August 17, 2010. Our proforma earnings (loss) per ordinary share (basic and diluted) and proforma weighted average number of ordinary shares outstanding (basic and diluted) have been calculated and presented for fiscal year 2011 assuming that the conversion of all our outstanding preferred shares occurred on a “hypothetical basis” on April 1, 2007 for our Series A and Series B preferred shares and |

5

Table of Contents

| April 1, 2008 for our Series C preferred shares. As no preferred shares were outstanding during fiscal years 2012, 2013, 2014 and 2015, proforma earnings (loss) per ordinary share (basic and diluted) and proforma weighted average number of ordinary shares outstanding (basic and diluted) have not been presented for fiscal years 2012, 2013, 2014 and 2015. |

The following table sets forth a summary of our consolidated statement of financial position as of March 31, 2011, 2012, 2013, 2014 and 2015:

| As of March 31 | ||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Consolidated Statement of Financial Position Data: |

||||||||||||||||||||

| Trade and other receivables |

$ | 12,857.2 | $ | 21,382.4 | $ | 26,111.4 | $ | 29,355.7 | $ | 29,852.4 | ||||||||||

| Term deposits |

16,941.9 | 44,325.1 | 48,115.0 | 105,169.8 | 93,491.7 | |||||||||||||||

| Cash and cash equivalents |

51,730.3 | 43,798.2 | 36,501.5 | 38,011.8 | 49,857.2 | |||||||||||||||

| Net current assets |

66,585.5 | 89,469.2 | 57,758.1 | 37,264.6 | 97,384.7 | |||||||||||||||

| Total assets |

112,939.6 | 170,191.4 | 194,620.1 | 269,837.0 | 280,405.0 | |||||||||||||||

| Total equity (deficit) |

76,275.9 | 118,791.8 | 101,994.0 | 162,299.5 | 157,854.0 | |||||||||||||||

| Loans and borrowings |

209.6 | 259.4 | 419.9 | 318.1 | 499.5 | |||||||||||||||

| Trade and other payables |

29,694.7 | 46,697.6 | 80,592.2 | 86,213.5 | 103,655.1 | |||||||||||||||

| Total liabilities |

36,663.8 | 51,399.6 | 92,626.2 | 107,537.5 | 122,550.8 | |||||||||||||||

| Total equity (deficit) and liabilities |

$ | 112,939.6 | $ | 170,191.4 | $ | 194,620.1 | $ | 269,837.0 | $ | 280,405.0 | ||||||||||

Other Data:

The following table sets forth for the periods indicated, certain selected consolidated financial and other data:

| Fiscal Year Ended March 31 | ||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | ||||||||||||||||

| (in thousands, except percentages) | ||||||||||||||||||||

| Number of transactions: |

||||||||||||||||||||

| Air ticketing |

2,824.6 | 3,715.4 | 3,794.1 | 3,999.2 | 5,432.8 | |||||||||||||||

| Hotels and packages |

175.9 | 343.1 | 568.1 | 869.8 | 1,385.5 | |||||||||||||||

| Revenue less service cost(1): |

||||||||||||||||||||

| Air ticketing |

$ | 47,622.7 | $ | 66,250.7 | $ | 56,769.2 | $ | 62,051.5 | $ | 71,509.2 | ||||||||||

| Hotels and packages |

10,907.1 | 18,226.3 | 27,592.2 | 39,992.9 | 62,614.7 | |||||||||||||||

| Other revenue |

2,540.7 | 3,707.8 | 3,803.8 | 4,350.7 | 4,824.9 | |||||||||||||||

| $ | 61,070.5 | $ | 88,184.9 | $ | 88,165.2 | $ | 106,395.1 | $ | 138,948.8 | |||||||||||

| Gross bookings(2): |

||||||||||||||||||||

| Air ticketing |

$ | 647,846.9 | $ | 839,234.3 | $ | 939,637.5 | $ | 943,699.1 | $ | 1,175,379.2 | ||||||||||

| Hotels and packages |

94,608.2 | 153,723.2 | 229,921.0 | 317,518.4 | 472,997.6 | |||||||||||||||

| Net revenue margins(3): |

||||||||||||||||||||

| Air ticketing |

7.4 | % | 7.9 | % | 6.0 | % | 6.6 | % | 6.1 | % | ||||||||||

| Hotels and packages |

11.5 | % | 11.9 | % | 12.0 | % | 12.6 | % | 13.2 | % | ||||||||||

Notes:

| (1) | As certain parts of our revenue are recognized on a “net” basis and other parts of our revenue are recognized on a “gross” basis, we evaluate our financial performance based on revenue less service cost, which is a non-IFRS measure, as we believe that revenue less service cost reflects more accurately the value addition of the travel services that we provide to our customers. The presentation of this non-IFRS information is not meant to be considered in isolation or as a substitute for our consolidated financial results prepared in |

6

Table of Contents

| accordance with IFRS as issued by the IASB. Our revenue less service cost may not be comparable to similarly titled measures reported by other companies due to potential differences in the method of calculation. The following table reconciles our revenue (an IFRS measure) to revenue less service cost (a non-IFRS measure): |

| Air Ticketing | Hotels and Packages | Other Revenue | Total | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fiscal Year Ended March 31 | Fiscal Year Ended March 31 | Fiscal Year Ended March 31 | Fiscal Year Ended March 31 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2011 | 2012 | 2013 | 2014 | 2015 | 2011 | 2012 | 2013 | 2014 | 2015 | 2011 | 2012 | 2013 | 2014 | 2015 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Revenue |

$ | 47,622.7 | $ | 76,190.3 | $ | 60,888.8 | $ | 66,523.2 | $ | 74,324.9 | $ | 74,558.0 | $ | 116,701.1 | $ | 164,129.3 | $ | 184,500.7 | $ | 220,511.9 | $ | 2,540.7 | $ | 3,707.8 | $ | 3,803.8 | $ | 4,350.7 | $ | 4,824.9 | $ | 124,721.4 | $ | 196,599.3 | $ | 228,821.9 | $ | 255,374.6 | $ | 299,661.7 | ||||||||||||||||||||||||||||||||||||||||

| Less: |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Service Cost |

— | 9,939.6 | 4,119.6 | 4,471.7 | 2,815.7 | 63,650.9 | 98,474.8 | 136,537.1 | 144,507.8 | 157,897.2 | — | — | — | — | — | 63,650.9 | 108,414.3 | 140,656.7 | 148,979.6 | 160,712.9 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Revenue less service cost |

$ | 47,622.7 | $ | 66,250.7 | $ | 56,769.2 | $ | 62,051.5 | $ | 71,509.2 | $ | 10,907.1 | $ | 18,226.3 | $ | 27,592.2 | $ | 39,992.9 | $ | 62,614.7 | $ | 2,540.7 | $ | 3,707.8 | $ | 3,803.8 | $ | 4,350.7 | $ | 4,824.9 | $ | 61,070.5 | $ | 88,184.9 | $ | 88,165.2 | $ | 106,395.1 | $ | 138,948.8 | ||||||||||||||||||||||||||||||||||||||||

| (2) | Gross bookings represent the total amount paid by our customers for the travel services and products booked through us, including taxes, fees and other charges, and are net of cancellations and refunds. |

| (3) | Net revenue margins is defined as revenue less service cost as a percentage of gross bookings. |

B. Capitalization and Indebtedness

Not applicable

C. Reasons for the Offer and Use of Proceeds

Not applicable

7

Table of Contents

D. Risk Factors

This Annual Report contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of a number of factors, including those described in the following risk factors and elsewhere in this Annual Report. If any of the following risks actually occur, our business, financial condition and results of operations could suffer.

Risks Related to Us and Our Industry

Declines or Disruptions in the Travel Industry Could Adversely Affect Our Business and Financial Performance.

Our business and financial performance is affected by the health of the travel industry in India and worldwide, including changes in supply and pricing. Events specific to the travel industry that could negatively affect our business include continued fare increases, travel-related strikes or labor unrest, general civil unrest, fuel price volatility and bankruptcies or liquidations of our suppliers. For example, events in the Middle East over the past several years have resulted in an adverse impact on travel to that region. Such events also impact crude oil prices which may have an adverse impact on the travel industry globally, including our business. Similarly, political unrest in Bangkok, Thailand, has negatively impacted travel to those locations. In addition, the drop in the average value of the Indian Rupee as compared to the US dollar in fiscal year 2014 adversely impacted the Indian travel industry as it made travel for Indian consumers outside of India more expensive.

Additionally, our business is sensitive to safety concerns, and thus our business has in the past declined and may in the future decline after incidents of actual or threatened terrorism, during periods of political instability or conflict or during other periods in which travelers become concerned about safety issues, including as a result of natural disasters such as tsunamis or earthquakes or when travel might involve health-related risks, such as the influenza A virus (H1N1), avian flu (H5N1 and H7N9) and Severe Acute Respiratory Syndrome, or other epidemics or pandemics. For example, the eruption of the Icelandic volcano in spring 2010, social unrest, such as in the West Indies in 2010 and in Tunisia, Egypt and Syria in recent years, among others, had or may in the future have a negative impact on our tourism business. In addition, there may be work stoppages or labor unrest at airlines or airports. Furthermore, hotels, airlines and cruises have in recent years been the subject of terrorist attacks, notably cruise ship piracy in the Gulf of Aden, India, Spain, Egypt, Russia, Turkey and Sri Lanka. Such events are outside our control and could result in a significant decrease in demand for our travel services. Any such decrease in demand, depending on its scope and duration, together with any other issues affecting travel safety, could significantly and adversely affect our business and financial performance over the short and long term. The occurrence of such events could result in disruptions to our customers’ travel plans and we may incur additional costs and constrained liquidity if we provide relief to affected customers by not charging cancellation fees or by refunding the cost of airline tickets, hotel reservations and other travel services and products. If there is a prolonged substantial decrease in travel volumes, particularly air travel and hotels, for these or any other reasons, our business, financial condition and results of operations would be adversely affected.

Our Business and Results of Operations Could Be Adversely Affected by Global Economic Conditions.

Consumer purchases of discretionary items generally decline during periods of recession and other periods in which disposable income is adversely affected. As a substantial portion of travel expenditure, for both business and leisure, is discretionary, the travel industry tends to experience weak or reduced demand during economic downturns.

Unfavorable changes in the above factors or in other business and economic conditions affecting our customers could result in fewer reservations made through our websites and/or lower our net revenue margins, and have a material adverse effect on our financial condition and results of operations.

Since the beginning of the global financial crisis in the third quarter of 2008, adverse developments in the international financial markets have created challenging economic conditions for businesses and governments

8

Table of Contents

around the world. These adverse developments have included increased market volatility, tightened liquidity in credit markets, diminished expectations for economic growth and a reduction in consumer and business spending. While the global economy has recovered to some extent since 2010, the recovery remains fragile and slow-paced as high-income countries continue to suffer from volatility and slow growth, and it could be adversely impacted by several factors, including the deterioration of general economic conditions or political unrest in Europe as fiscal austerity continues, negative media coverage about the economic crisis in Greece, unemployment rates remain elevated and the potential for conflict in eastern Europe, restrained monetary policy in the form of tapering and other debt and fiscal issues in the United States and a slowdown in economic growth in China as its new leadership attempts to rebalance its economy from investment and exports to increased domestic consumption and restrain lending practices. The weakness and uncertainty in the global economy have negatively impacted both corporate and consumer spending patterns and demand for travel services, globally and in India, and may continue to do so in the future.

As an intermediary in the travel industry, a significant portion of our revenue is affected by fares and tariffs charged by our suppliers as well as volumes of sales made by us. During periods of poor economic conditions, airlines and hotels tend to reduce rates or offer discounted sales to stimulate demand, thereby reducing our commission-based income. A slowdown in economic conditions may also result in a decrease in transaction volumes and adversely affect our revenue. It is difficult to predict the effects of the uncertainty in global economic conditions. If economic conditions worsen globally or in India, our growth plans, business, financial condition and results of operations could be adversely impacted.

If We Are Unable to Maintain Existing, and Establish New, Arrangements with Our Travel Suppliers, Our Business May Be Adversely Affected.

Our business is dependent on our ability to maintain our relationships and arrangements with existing suppliers, such as airlines which supply air tickets to us directly, Amadeus IT Group, SA, or Amadeus, our global distribution system, or GDS, service provider, Indian Railways, hotels, hotel suppliers and destination management companies, bus operators and car hire companies, as well as our ability to establish and maintain relationships with new travel suppliers. A substantial portion of our revenue less service cost is derived from fees and commissions negotiated with travel suppliers for bookings made through our websites or via our other distribution channels. Adverse changes in existing arrangements, including an inability by any travel supplier to fulfill their payment obligation to us in a timely manner, increasing industry consolidation or our inability to enter into or renew arrangements with these parties on favorable terms, if at all, could reduce the amount, quality, pricing and breadth of the travel services and products that we are able to offer, which could adversely affect our business and financial performance. For example, we have experienced short-term disruptions in the supply of tickets from domestic airlines in the past.

In addition, adverse economic developments affecting the travel industry could also adversely impact our ability to maintain our existing relationships and arrangements with one or more of our suppliers. In particular, adverse changes to the overall business and financial climate for the airline industry in India due to various factors including, but not limited to, rising fuel costs, high taxes, significant depreciation of the Indian Rupee as compared to the US dollar making travel for Indian consumers outside India more expensive, and increased liquidity constraints, could affect the ability of one or more of our airline suppliers to continue to operate or otherwise meet our demand for tickets, which, in turn, could materially and adversely affect our financial results. For example, during fiscal year 2013, Kingfisher Airlines, one of the major airlines in India and one of our airline suppliers, shut down its operations, which resulted in a decline in the total capacity in the airline industry in India. In addition, adverse changes to the overall business and financial climate for the airline industry in India due to various factors including, but not limited to, rising fuel costs, high taxes, significant depreciation of the Indian Rupee as compared to the US dollar making travel for Indian consumers outside India more expensive, and increased liquidity constraints, resulted in airlines in India reducing the base commissions paid to travel agencies. These factors were primarily responsible for causing us to record a net loss of $(27.6) million in fiscal year 2013. Adverse economic developments continued to negatively affect the travel industry in fiscal year 2014,

9

Table of Contents

which was a significant reason for our net loss of $(20.9) million in fiscal year 2014. During fiscal year 2015, the domestic airlines in India continued to reduce the base commissions paid to travel agencies and we spent significantly on marketing expenses to promote transactions on our mobile platforms in India and to promote our international hotels. These factors were mainly responsible for our net loss of $(18.4) million in fiscal year 2015. Any consolidation in the airline industry involving our suppliers may also adversely affect our existing relationships and arrangements with such suppliers.

No assurance can be given that our agreements or arrangements with our travel suppliers or GDS service provider will continue or that our travel suppliers or GDS service provider will not further reduce or eliminate fees or commissions or attempt to charge us for content, terminate our contracts, make their products or services unavailable to us as part of exclusive arrangements with our competitors or default on or dispute their payment or other obligations towards us, any of which could reduce our revenue and net revenue margins or may require us to initiate legal or arbitral proceedings to enforce their contractual payment obligations, which may adversely affect our business and financial performance. See also “— Some of Our Airline Suppliers (Including Our GDS Service Provider) May Reduce or Eliminate the Commission and Other Fees They Pay to Us for the Sale of Air Tickets and This Could Adversely Affect Our Business and Results of Operations.”

We Do Not Have Formal Agreements with Many of Our Travel Suppliers.

We rely on various travel suppliers to facilitate the sale of our travel services. We do not have formal agreements with many of our travel suppliers, including low-cost airlines and many hotels, whose booking systems or central reservations systems are relied upon by us for bookings and confirmation as well as certain payment gateway arrangements, and there can be no assurance that these third parties will not terminate these arrangements with us at short notice or without notice. Further, where we have entered into formal agreements, many of these agreements are short-term contracts, requiring periodic renewal and providing our counterparties with a right to terminate at short notice or without notice. Some of these agreements are scheduled to expire in the near future and we are in the process of renewing those agreements. Many of our suppliers with whom we have formal agreements, including airlines, are also able to alter the terms of their contracts with us at will or at short notice. For example, our agreement with Indian Railways Catering and Tourism Corporation Limited, or IRCTC, which allows us to transact with Indian Railways’ passenger reservation system through the Internet, can be terminated or temporarily suspended by IRCTC without prior notice and at its sole discretion. Termination, non-renewal or suspension or an adverse amendment of any of the abovementioned agreements and/or arrangements could have a material adverse effect on our business, financial condition and results of operations.

We Have Sustained Operating Losses in the Past and May Continue to Experience Operating Losses in the Future.

We sustained operating losses in fiscal years 2013, 2014 and 2015 and in all our fiscal years prior to and including fiscal year 2010. While we generated operating profits in fiscal years 2011 and 2012, there can be no assurance that we will be able to return to profitability or that we can avoid operating losses in the future. We expect that our advertisement and business promotion expenses going forward will increase as a result of our continued investment in the hotels and packages business. The degree of increase in these expenses will be largely based on anticipated organizational growth and revenue trends. As a result, any decrease or delay in generating additional sales volumes and revenue could result in substantial operating losses.

We Rely on Third-Party Systems and Service Providers, and Any Disruption or Adverse Change in Their Businesses Could Have a Material Adverse Effect on Our Business.

We currently rely on certain third-party computer systems, service providers and software companies, including the GDS used by full service airlines, and the electronic central reservation systems used by low-cost airlines, certain hotels and hotel suppliers which are directly connected to us, Indian Railways and bus operators. In particular, we rely on third parties to:

| • | assist in conducting searches for airfares and process air ticket bookings; |

10

Table of Contents

| • | process hotel reservations; |

| • | process credit card, debit card and net banking payments; |

| • | provide computer infrastructure critical to our business; and |

| • | provide customer relationship management, or CRM, software services. |

Any interruption or deterioration in performance of these third-party systems and services could have a material adverse effect on our business. Further, the information provided to us by certain of these third-party systems, such as the central reservations systems of certain of our hotel suppliers, may not always be accurate due to either technical glitches or human error, and we may incur monetary and/or reputational loss as a result.

Our success is also dependent on our ability to maintain our relationships with these third-party systems and service providers, including our technology partners. In the event our arrangements with any of these third parties are impaired or terminated, we may not be able to find an alternative source of systems support on a timely basis or on commercially reasonable terms, which could result in significant additional costs or disruptions to our business.

Our Results of Operations Are Subject to Fluctuations in Currency Exchange Rates.

Our presentation currency is the US dollar. However, the functional currency of MMT India, our key operating subsidiary, is the Indian Rupee. We receive a substantial portion of our revenue in Indian Rupees and most of our costs are incurred in Indian Rupees. Any fluctuation in the value of the Indian Rupee against the US dollar, such as the approximately 1.1% drop in the average value of the Indian Rupee as compared to the US dollar in fiscal year 2015 as compared to the average value of the Indian Rupee against the US dollar in fiscal year 2014, will affect our results of operations. For example, our loss on account of foreign exchange fluctuations in fiscal year 2015 was $5.2 million as compared to $2.7 million in fiscal year 2014. We expect to be adversely affected by any further depreciation of the Indian Rupee and Euro against the US dollar. The drop in the average value of the Indian Rupee as compared to the US dollar in fiscal year 2015 adversely impacted the Indian travel industry as it made outbound travel for Indian consumers more expensive. In addition, our exposure to foreign currency risk also arises in respect of our non-Indian Rupee-denominated trade and other receivables, trade and other payables, and cash and cash equivalents. Similarly, the drop in the average value of the Euro as compared to the US dollar in fiscal year 2015 has also adversely impacted the European travel industry.

Based on our operations in fiscal year 2015, a 10.0% appreciation of the US dollar against the Indian Rupee as of March 31, 2015, assuming all other variables remained constant, would have increased our loss for fiscal year 2015 by $1.9 million. Similarly, a 10.0% depreciation of the US dollar against the Indian Rupee as of March 31, 2015, assuming all other variables remained constant, would have decreased our loss for fiscal year 2014 by $1.9 million.

Further, we are also exposed to movements in currency exchange rates between the US dollar and the Euro. As the functional currency of the Hotel Travel Group is the US dollar, our exposure to foreign currency risk primarily arises in respect of our non-US dollar denominated trade and other receivables, trade and other payables and cash and cash equivalents, which were $0.4 million, $3.0 million and $1.7 million, respectively, as of March 31, 2015. Based on our operations in fiscal year 2015, a 10.0% appreciation of the Euro against the US dollar as of March 31, 2015, assuming all other variables remained constant, would have increased our loss for the year by $0.1 million. Similarly, a 10.0% depreciation of the Euro against the US dollar as of March 31, 2014, assuming all other variables remained constant, would have decreased our loss for the year by $0.1 million.

Similarly, as the functional currency of the ETB Group is the Euro, our exposure to foreign currency risk primarily arises in respect of our non-Euro denominated trade and other receivables, trade and other payables and cash and cash equivalents, which were $0.4 million, $6.7 million and $1.7 million, respectively, as of March 31, 2015. Based on our operations in fiscal year 2015, a 10.0% appreciation of the US dollar against the Euro as of

11

Table of Contents

March 31, 2015, assuming all other variables remained constant, would have increased our loss for the year by $0.4 million. Similarly, a 10.0% depreciation of the US dollar against the Euro as of March 31, 2015, assuming all other variables remained constant, would have decreased our loss for the year by $0.4 million.

We are also exposed to movements between the US dollar and the Indian Rupee in our operations, as 3.9%, 2.9% and 1.8% of our revenue for fiscal years 2013, 2014 and 2015, respectively, was generated by MMT India from its air ticketing business and received in US dollars although our expenses are generally incurred in Indian Rupees. Additionally, we receive revenue from our hotels and packages business in Indian Rupees, but a portion of our expenses in this segment (those relating to outbound packages from India in particular) could be incurred in a non-Indian currency. We currently do not have any hedging agreements or similar arrangements with any counter-party to cover our exposure to any fluctuations in foreign exchange rates. Fluctuation in the Indian Rupee-US dollar exchange rate could have a material adverse effect on our business and our financial condition and results of operations as these are reported in US dollars.

We Outsource a Significant Portion of Our Call Center Services and If Our Outsourcing Service Providers Fail to Meet Our Requirements or Face Operational or System Disruptions, Our Business May Be Adversely Affected.

We outsource our call center service for sales for all international flights and most of our hotel reservations and packages. We also outsource our call center service for post-sales customer service support for all flights (domestic and international), hotel reservations and packages, and rail and bus ticketing, as well as back office fulfillment and ticketing services, to various third parties in India. If our outsourcing service providers experience difficulty meeting our requirements for quality and customer service standards, our reputation could suffer and our business and prospects could be adversely affected. Our operations and business could also be materially and adversely affected if our outsourcing service providers face any operational or system interruptions.

Further, many of our contracts with outsourcing service providers are short-term or have short notice periods. For example, our agreement with Serco BPO Private Limited (formerly Intelenet Global Services Private Limited), or Serco, which provides call center services for our hotels and packages business is for a renewable term of three years but may be terminated by either party on two months’ notice. The agreements with some of our outsourcing service providers, including iEnergizer IT Services Private Limited, or iEnergizer IT Services, and Motif India Infotech Private Limited, or Motif India Infotech, may be terminated by either party on 90 days’ notice after the first year in the case of Motif India Infotech Private Limited and post the initial two year term for iEnergizer IT Services Private Limited. In the event one or more of our contracts with our outsourcing service providers is terminated on short notice, we may be unable to find alternative outsourcing service providers on commercially reasonable terms, or at all. Further, the quality of the service provided by a new or replacement outsourcing service provider may not meet our requirements, including during the transition and training phase. Hence, termination of any of our contracts with our outsourcing service providers could cause a decline in the quality of our services and disrupt and adversely affect our business, results of operations and financial condition.

We Rely on Information Technology to Operate Our Business and Maintain Our Competitiveness, and Any Failure to Adapt to Technological Developments or Industry Trends Could Harm Our Business.

We depend on the use of sophisticated information technology and systems, which we have customized in-house for search and reservation for flights and hotels, as well as payments, refunds, customer relationship management, communications and administration. As our operations grow in both size and scope, we must continuously improve and upgrade our systems and infrastructure to offer our customers enhanced services, features and functionality, while maintaining the reliability and integrity of our systems and infrastructure in a cost-effective manner. Our future success also depends on our ability to upgrade our services and infrastructure ahead of rapidly evolving consumer demands while continuing to improve the performance, features and reliability of our service in response to competitive offerings.

12

Table of Contents

We may not be able to maintain or replace our existing systems or introduce new technologies and systems as quickly as our competitors, in a cost-effective manner or at all. We may also be unable to devote adequate financial resources to develop or acquire new technologies and systems in the future.

We may not be able to use new technologies effectively, or we may fail to adapt our websites, mobile applications, transaction processing systems and network infrastructure to consumer requirements or emerging industry standards. If we face material delays in introducing new or enhanced solutions, our customers may forego the use of our services in favor of those of our competitors. Any of these events could have a material adverse effect on our operations.

We currently license from third-parties some of the technologies incorporated into our websites. As we continue to introduce new services that incorporate new technologies, we may be required to license additional technology. We cannot be sure that such technology licenses will be available on commercially reasonable terms, if at all.

The Travel Industry in India and Worldwide is Intensely Competitive, and We May Not Be Able to Effectively Compete in the Future.

The travel market is intensely competitive. Factors affecting our competitive success include, among other things, price, availability and breadth of choice of travel services and products, brand recognition, customer service, fees charged to travelers, ease of use, accessibility and reliability. We currently compete with both established and emerging providers of travel services and products, including other online travel agencies both in India and abroad, such as cleartrip.com, expedia.co.in, travelocity.co.in, yatra.com, goibibo.com, booking.com and agoda.com, as well as traditional travel agencies, tour operators, travel suppliers and operators of travel industry reservation databases. Large, established Internet search engines have also launched applications offering travel itineraries in destinations around the world, and meta-search companies who can aggregate travel search results also compete against us for customers. Certain of our competitors have launched brand marketing campaigns to increase their visibility with customers. For example, trivago.com had commenced a television advertising campaign in India. Some of our competitors have significantly greater financial, marketing, personnel and other resources than us and certain of our competitors have a longer history of established businesses and reputations in the Indian travel market (particularly in the hotels and packages business) as compared with us. From time to time we may be required to reduce service fees and net revenue margins in order to compete effectively and maintain or gain market share.

Further, we may also face increased competition from new entrants in our industry. We cannot assure you that we will be able to successfully compete against existing or new competitors in our existing lines of business as well as new lines of business into which we may venture. If we are not able to compete effectively, our business and results of operations may be adversely affected.

Some travel suppliers are seeking to decrease their reliance on distribution intermediaries such as us, by promoting direct distribution channels. Many airlines, hotels, car rental companies and tour operators have call centers and have established their own travel distribution websites and mobile applications. From time to time, travel suppliers offer advantages, such as bonus loyalty awards and lower transaction fees or discounted prices, when their services and products are purchased from supplier-related channels. We also compete with competitors who may offer less content, functionality and marketing reach but at a relatively lower cost to suppliers. If our access to supplier-provided content or features were to be diminished either relative to our competitors or in absolute terms or if we are unable to compete effectively with travel supplier-related channels or other competitors, our business could be materially and adversely affected.

13

Table of Contents

Some of Our Airline Suppliers (Including Our GDS Service Provider) May Reduce or Eliminate the Commission and Other Fees They Pay to Us for the Sale of Air Tickets, and This Could Adversely Affect Our Business and Results of Operations.

In our air ticketing business, we generate revenue through commissions and incentive payments from airline suppliers, service fees charged to our customers and fees from our GDS service provider. Our airline suppliers may reduce or eliminate the commissions and incentive payments they pay to us. For example, few airlines in India have reduced the base commissions paid to travel agencies during fiscal year 2015. To the extent any of our airline suppliers further reduce or eliminate the commissions or incentive payments they pay to us in the future, our revenue may be further reduced unless we are able to adequately mitigate such reduction by increasing the service fees we charge to our customers in a sustainable manner. Any increase in service fees, to mitigate reductions in or elimination of commissions or otherwise, may also result in a loss of potential customers. Further, our arrangements with the airlines that supply air tickets to us may limit the amount of service fees that we are able to charge our customers. Our business would also be negatively impacted if competition or regulation in the travel industry causes us to reduce or eliminate our service fees.

We Depend on and Expect to Continue to Depend on a Small Number of Airline Suppliers in India for a Significant Percentage of our Air Ticketing Revenue.

The domestic air travel industry in India is dominated by five airlines. As a substantial portion of our air ticketing revenue is represented by base commissions and incentive payments paid to us by these domestic airlines, our dependence on a limited number of domestic airlines means that a reduction or elimination in base commissions and incentive payments by any one or all of these airlines could have a material adverse effect on our revenue.

In addition, our reliance on a small number of airline suppliers in India gives those airline suppliers additional bargaining power in negotiating agreements with us. A reduction or elimination of base commissions and incentive payments by any of these domestic airline suppliers, the loss of any of these domestic airline suppliers or a domestic airline supplier exerting significant price and margin pressure on us could materially and adversely affect our business, financial condition and results of operations.

We Rely on the Value of Our Brands, and Any Failure to Maintain or Enhance Consumer Awareness of Our Brands Could Have a Material Adverse Effect on Our Business, Financial Condition and Results of Operations.

We believe continued investment in our brand, “MakeMyTrip,” is critical to retain and expand our business. We believe that our brand is well respected and recognized in the Indian travel market. We have invested in developing and promoting our brand since our inception and expect to continue to spend on maintaining our brand’s value to enable us to compete against increased spending by our competitors, as well as against emerging competitors, including search engines and meta-search engines, and to allow us to expand into new geographies and products where our brand is not well known. With the acquisition of the Hotel Travel Group and the ITC Group in November 2012, we acquired the brands “HotelTravel” and “ITC,” which we believe are well-known brands globally, especially in Southeast Asia. We also acquired the “Easytobook” brand, which we believe is a well-known brand in Europe, through our acquisition of the ETB Group in February 2014. We have invested and intend to continue to invest in developing and promoting these brands. There is no assurance that we will be able to successfully maintain or enhance consumer awareness of our brands. Even if we are successful in our branding efforts, such efforts may not be cost-effective. Our marketing costs may also increase as a result of inflation in media pricing (including search engine keywords). If we are unable to maintain or enhance consumer awareness of our brands and generate demand in a cost-effective manner, it would negatively impact our ability to compete in the travel industry and would have a material adverse effect on our business. See also “— We Cannot Be Sure That Our Intellectual Property Is Protected from Copying or Use by Others, Including Current or Potential Competitors.”

14

Table of Contents

We May Not Be Successful in Implementing Our Growth Strategies.

Our growth strategies involve expanding our hotels and packages business (including through our travel agents’ network), expanding our service and product offerings, enhancing our service platforms by investing in technology, expanding into new geographic markets and pursuing strategic partnerships and acquisitions.

Our success in implementing our growth strategies is affected by:

| • | our ability to increase the number of suppliers, especially hotel suppliers, that are directly connected to us, which is dependent on the willingness of such suppliers to invest in new technology; |

| • | our ability to continue to expand our distribution channels, and market and cross-sell our travel services and products to facilitate the expansion of our business; |

| • | our ability to build or acquire required technology; |

| • | our ability to expand our businesses through strategic acquisitions and successfully integrate such acquisitions; |

| • | the general condition of the global economy (particularly in India and markets with close proximity to India) and continued growth in demand for travel services, particularly online; |

| • | our ability to compete effectively with existing and new entrants to the Indian travel industry, including online travel companies as well as traditional offline travel agents and tour providers; |

| • | the growth of the Internet and mobile technology as a medium for commerce in India; and |

| • | changes in our regulatory environment. |

Many of these factors are beyond our control and there can be no assurance that we will succeed in implementing our strategies.

Even if we are successful in executing our growth strategies, our different businesses may not grow at the same rate or with a uniform effect on our revenues and profitability. For example, the rate of growth in our hotels and packages business, which has generally outpaced our air tickets business and is a relatively higher margin business, may not grow at a pace to affect our overall growth in the short term as it is currently smaller than our air tickets business. In addition, the relatively higher margins of our hotels and packages business may be adversely affected by our recent acquisitions, due to the additional expenses associated with such acquisitions.

We are also subject to additional risks involved in our strategies of expanding into new geographic markets and pursuing strategic partnerships and acquisitions. See “— Our International Operations, Some of Which Are New to Us, Involve Additional Risks” and “— We May Not Be Successful in Pursuing Strategic Partnerships and Acquisitions, and Future Partnerships and Acquisitions May Not Bring Us Anticipated Benefits.”

We May Not Be Successful in Pursuing Strategic Partnerships and Acquisitions, and Future Partnerships and Acquisitions May Not Bring Us Anticipated Benefits.

Part of our growth strategy is the pursuit of strategic partnerships and acquisitions. There can be no assurance that we will succeed in implementing this strategy as it is subject to many factors which are beyond our control, including our ability to identify, attract and successfully execute suitable acquisition opportunities and partnerships. This strategy may also subject us to uncertainties and risks, including acquisition and financing costs, potential ongoing and unforeseen or hidden liabilities, diversion of management resources and cost of integrating acquired businesses. We could face difficulties integrating the technology of acquired businesses with our existing technology, and employees of the acquired business into various departments and ranks in our company, and it could take substantial time and effort to integrate the business processes being used in the acquired businesses with our existing business processes. Moreover, there is no assurance that such partnerships or acquisitions will achieve our intended objectives or enhance our revenue.

15

Table of Contents

We have made a number of acquisitions since March 2010, including the acquisition of certain assets of Travis Internet Private Limited, an online bus ticketing company, 100% of Luxury Tours, a Singapore-based travel agency, 19.9% of Le Travenues Technology Private Limited, which owns and operates www.ixigo.com, an online travel meta search engine, approximately 38% stake in My Guest House Accommodations Private Limited, or My Guest House, which is engaged in the business of aggregation, sales and distribution of hotel room inventory with a special focus on budget lodging accommodations and serviced apartments, a 100% stake in the companies comprising the Hotel Travel Group, a group of companies which operate through their website HotelTravel.com and offers its customers online hotel reservations in South East Asia and other key global travel destinations, and a 100% stake in the ITC Group, a well-established hotel aggregator and tour operator in Thailand.

In February 2014, we acquired a 100% equity interest in the group of companies comprising the ETB Group. Established in 2004, the ETB Group primarily operates through its website www.easytobook.com and offers its customers online hotel reservations in Europe, North America and other key global travel destinations.

In September 2014, we announced the establishment of our innovation fund (“Innovation Fund”), through which we will consider investing up to $3.0 million in each start-up or early-stage companies in the travel technology space. Through the Innovation Fund, in December 2014, we acquired a minority equity stake in Simplotel Technologies Private Limited (“Simplotel”) and have committed to make a further investment by June 2015, which will increase our total equity shareholding in Simplotel to approximately 25%. Simplotel aims to provide hotels with responsive and optimized websites along with booking engines. We believe our investment in Simplotel will help to promote the online distribution of accommodation inventory in India. Further, in April 2015, we acquired certain assets of the online travel-planning service, Mygola.com, and the entire Mygola team joined our Company to focus on innovation in online travel. In April 2015, we acquired approximately 18% of the equity shares of Inspirock, Inc., which owns and operates www.inspirock.com, an online planning tool for developing custom-made itineraries. We believe that this investment will help us to further enhance our capabilities in the online tour planning space.

We believe these acquisitions serve to strengthen our presence in key geographic markets and expand the travel products and services that we can offer our customers. However, there is no assurance that any of these investments or acquisitions will be successful or bring about their intended results. Any such failure could negatively impact our ability to compete in the travel industry and have a material adverse effect on our business.

For further details on these investments and acquisitions, see “Item 4. Business — Recent Acquisitions” and “Information On the Company — History and Development of our Company — Investments and Acquisitions” in this Annual Report.

Our Arrangements with Some of Our Suppliers May Subject Us to Additional Monetary Risks.

We generally do not assume inventory risk in our air ticketing business as we typically act as an agent. However, on a few occasions, we pre-purchase air ticket inventory in order to enjoy special negotiated rates and we assume inventory risk on such tickets. When we sell pre-purchased tickets to our customers, revenue is accounted for on a “gross” basis (representing the price of the tickets paid by our customers) and the amount spent to pre-purchase the ticket is classified as a service cost. We obtain inventory for most hotels outside India through contracts with online travel agents and aggregators outside India. In some instances, in order to enjoy special negotiated rates for these hotels, we pre-purchase hotel room nights and assume inventory risk on them. If we are unable to sell pre-purchased tickets or hotel room nights inventory as anticipated either at all or at expected rates, our revenue and business may be adversely affected.

Our International Operations, Some of Which Are New to Us, Involve Additional Risks.

We have been operating in the United States since 2000, servicing mainly the air ticketing needs of non-resident Indians in the United States traveling inbound to India. We launched our website in the United Arab

16

Table of Contents

Emirates in December 2009 and in Canada in July 2010. We further expanded our presence in the United Arab Emirates through the incorporation of a new wholly owned subsidiary in fiscal year 2013. We need to continue to tailor our services and business model to the unique circumstances of such markets to succeed, including building new supplier relationships and customer preferences. We have also expanded, and intend to continue to expand, our business in other new markets, particularly those with a significant non-resident Indian population as well as those with proximity to India or favored by Indian travelers. We have entered into new geographies in Southeast Asia and in Europe through our acquisitions of Luxury Tours, the Hotel Travel Group, the ITC Group and the ETB Group. Adapting our practices and models effectively to the supplier and customer preferences in these, or other, new markets could be difficult and costly and could divert management and personnel resources. We could also face additional regulatory requirements in these, or other, new markets which could be onerous. We cannot assure you that we will be able to efficiently or effectively manage the growth of our operations in these, or other, new markets.

In addition, we are subject to risks in our international operations that may not exist in our Indian operations, including:

| • | differences and unexpected changes in regulatory requirements and exposure to local economic conditions; |

| • | differences in consumer preferences in such markets; |

| • | increased risk to and limits on our ability to enforce our intellectual property rights; |

| • | competition from providers of travel services in such foreign countries; |

| • | restrictions on the repatriation of earnings from such foreign countries, including withholding taxes imposed by certain foreign jurisdictions; and |

| • | currency exchange rate fluctuations. |

If we are not able to effectively mitigate or eliminate these risks, our results of operations could be adversely affected.

For example, since our acquisition of the Hotel Travel Group, a portion of our business and some of our employees are located in Thailand, and we intend to continue to develop and expand our business in Thailand. Consequently, our financial performance and the market price of our ordinary shares will be affected by social and civil unrest and other political, social and economic developments in or affecting Thailand, such as the military coup in May 2014 and continuing political unrest in Thailand, as well as any changes in exchange rates and controls, interest rates and changes in government policies, including taxation policies.

Our Business Could Be Negatively Affected by Changes in Search Engine Logic.

We utilize Internet search engines such as Google™ and Yahoo!™ India, including through the purchase of travel-related keywords, to drive traffic to our websites. These search engines frequently update and change the logic that determines the placement and display of results of a user’s search, such that the purchased or optimal placement of links to our websites may be negatively affected. In addition, a significant amount of our business is directed to our websites through pay-per-click and display advertising campaigns on the Internet and search engines whose pricing and operating dynamics can rapidly change, both technically and competitively. If major search engines such as Google™ or Yahoo!™ India, which we utilize for a significant amount of our search engine traffic, change the logic used on their websites for search results in a manner that negatively affects the search engine ranking, paid or unpaid, of our websites or those of our third-party distribution partners, we may experience a decline in traffic on our websites and our business may be adversely affected.

System Interruption in Our Information Systems and Infrastructure May Harm Our Business.

We rely significantly on computer systems to facilitate and process transactions. We may in the future experience system interruptions that make some or all of these systems unavailable or prevent us from efficiently

17

Table of Contents

fulfilling bookings or providing services to our customers. Any interruptions, outages or delays in our systems, or deterioration in their performance, could impair our ability to process transactions and decrease the quality of our service to our customers. If we were to experience frequent or persistent system failures, our reputation and brand could be harmed.

While we have backup systems and contingency plans for critical aspects of our operations or business processes, certain other non-critical systems are not fully redundant and our disaster recovery or business continuity planning may not be sufficient. Fires, floods, power outages, telecommunications failures, earthquakes, acts of war or terrorism, acts of God, computer viruses, sabotage, break-ins and electronic intrusion attempts from both external and internal sources and similar events or disruptions may damage, impact or interrupt our computer or communications systems, business processes or infrastructure at any time. Although we have put measures in place to protect certain portions of our facilities and assets, any of these events could cause system interruptions, delays and loss of critical data, and could prevent us from providing services to our customers and/or suppliers for a significant period of time. We do not carry business interruption insurance for such eventualities. Remediation may be costly and we may not have adequate insurance to cover such costs. Moreover, the costs of enhancing infrastructure to attain improved stability and redundancy may be time consuming and expensive and may require resources and expertise that are difficult to obtain.

We Are Exposed to Risks Associated with Online Security and Credit Card Fraud.

The secure transmission of confidential information over the Internet is essential in maintaining customer and supplier confidence in us. Security breaches, whether instigated internally or externally on our system or other Internet-based systems, could significantly harm our business. We currently require customers to guarantee their transactions with their credit cards online. We rely on licensed encryption and authentication technology to effect secure transmission of confidential customer information, including credit card numbers, over the Internet. However, advances in technology or other developments could result in a compromise or breach of the technology that we use to protect customer and transaction data. We incur substantial expense to protect against and remedy security breaches and their consequences. However, our security measures may not prevent security breaches and we may be unsuccessful in or incur additional costs by implementing our remediation plan to address these potential exposures. In fiscal year 2015, our key operating subsidiaries in India and Malaysia incurred losses of $0.2 million and $0.7 million, respectively, on unauthorized credit card transactions. These losses pertained to credit card or digital commerce fraud committed by third parties on our websites through the purchase of air tickets and hotels and packages products using fraudulent credit cards.

We also have agreements with banks and certain companies that process customer credit card transactions for the facilitation of customer bookings of travel services from our travel suppliers. The online payment gateway for certain of our sales made through our mobile platform and through international credit and debit cards is not secured by “Verified by VISA”, “MasterSecure” or “American Express SafeKey” and we may be liable for accepting fraudulent credit cards on our websites. We may also be subject to other payment disputes with our customers for such sales. If we are unable to combat the use of fraudulent credit cards, our revenue from such sales would be susceptible to demands from the relevant banks and credit card processing companies, and our results of operations and financial condition could be adversely affected.

Our Processing, Storage, Use and Disclosure of Customer Data of Our Customers or Visitors to Our Website Could Give Rise to Liabilities As a Result of Governmental Regulation, Conflicting Legal Requirements, Differing Views of Personal Privacy Rights or Data Security Breaches.

In the processing of our customer transactions, we receive and store a large volume of customer information. Such information is increasingly subject to legislation and regulations in various jurisdictions and governments are increasingly acting to protect the privacy and security of personal information that is collected, processed and transmitted in or from the governing jurisdiction. We could be adversely affected if legislation or regulations are expanded or amended to require changes in our business practices or if governing jurisdictions

18

Table of Contents

interpret or implement their legislation or regulations in ways that negatively affect our business, financial condition and results of operations. As privacy and data protection become more sensitive issues in India, we may also become exposed to potential liabilities. For example, under the Indian Information Technology Act, 2000, as amended, we are subject to civil liability for wrongful loss or gain arising from any negligence by us in implementing and maintaining reasonable security practices and procedures with respect to sensitive personal data or information on our computer systems, networks, databases and software. India has also implemented privacy laws, including the Information Technology (Reasonable Security Practices and Procedures and Sensitive Personal Data or Information) Rules, 2011, which impose limitations and restrictions on the collection, use and disclosure of personal information. Any liability we may incur for violation of such laws and regulations and related costs of compliance and other burdens may adversely affect our business and profitability.

We cannot guarantee that our security measures will prevent data breaches. Companies that handle such information have also been subject to investigations, lawsuits and adverse publicity due to allegedly improper disclosure of personally identifiable information. Security breaches could damage our reputation, cause interruptions in our operations, expose us to a risk of loss or litigation and possible liability, and could also cause customers and potential customers to lose confidence in the security of our transactions, which would have a negative effect on the demand for our services and products. Moreover, public perception concerning security and privacy on the Internet could adversely affect customers’ willingness to use our websites. A publicized breach of security in India or in other countries in which we have operations, even if it only affects other companies conducting business over the Internet, could inhibit the growth of the Internet as a means of conducting commercial transactions, and, therefore, the prospects of our business.