FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

December 5, 2022

VIA EDGAR

U.S. Securities and Exchange Commission

Division of Corporation Finance

Office of Technology

United States Securities and Exchange Commission

100 F Street NE

Washington, D.C. 20549

Attn: Kathleen Collins

Chen Chen

Re: Brunswick Corporation

Form 10-K for Fiscal Year Ended December 31, 2021

Filed February 22, 2018

File No. 001-01043

Dear Ms. Collins:

This letter is Brunswick Corporation’s response to the comment letter from the staff (the “Staff”) of the Division of Corporation Finance of the Securities and Exchange Commission (the “Commission”) dated November 18, 2022. We have reproduced below the Staff’s comments together with Brunswick’s responses.

Due to the commercially sensitive nature of certain information contained herein, this response letter is also a request for confidential treatment of the portions of this letter bracketed below (designated by “[***]”) pursuant to the Commission’s confidential treatment procedure under Rule 83 (17 C.F.R. § 200.83).

Form 10-K for Fiscal Year Ended December 31, 2021

Management’s Discussion and Analysis of Financial Condition and Results of Operations

Results of Operations, page 32

1.We note your disclosure for the “summary of Adjusted operating earnings and Adjusted diluted earnings per common share.” Please revise to clarify that this is a “reconciliation” of your non-GAAP measures and consider clearly labeling each measure, both here and in the Form 8-K earnings releases as non-GAAP rather than “adjusted” so that the intent of this disclosures is clear.

Response:

In response to the Staff’s comment, the Company will revise its table to “Reconciliation of Non-GAAP Measures” in future filings.

FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

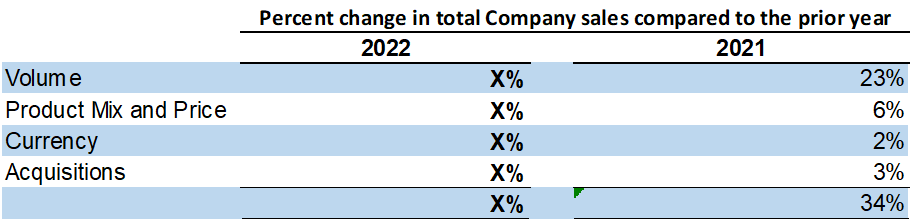

2. You state that net sales increased during fiscal 2021 compared to 2020 due to increased volume from strong global demand for marine products, market share gains and higher pricing. You refer to the segment discussion for further details on the drivers of net sales changes, however, such disclosure refers to the “factors affecting all of [y]our segments as previously mentioned.” Please revise to include both a quantitative and qualitative discussion of the various factors, including any offsetting factors, that impacted each of your consolidated and segment revenues. For example, include a quantified discussion regarding the impact of price versus volume on your net sales, and if specific products had a significant impact, either positively or negatively on the segment net sales growth, revise to disclose as such. Refer to Item 303(b) of Regulation S-K.

Response:

The Company acknowledges the Staff’s comment regarding revisions to include both quantitative and qualitative discussions of the various factors, including any offsetting factors, impacting consolidated and segment revenues. Beginning with our Annual Report on Form 10-K for fiscal year end December 31, 2022 (“Form 10-K”), we will provide additional disclosures describing and, to the extent possible, quantifying the material factors impacting revenue. An example of revised quantitative disclosures representing factors impacting consolidated revenues is presented below. Similar disclosures will be made for each segment.

With respect to qualitative discussions, the Company believes it has adequately disclosed the material qualitative factors in the following disclosure on page 32 of its 2021 Form 10-K:

“Sales in each segment benefited from increased volume due to strong global demand for marine products, market share gains, and higher pricing.”

We will continue to disclose material qualitative factors in future filings as well.

3. We note your disclosures that “excluding certain one-time items presented above,” selling general and administrative expense (SG&A) as a percentage of sales was lower in fiscal 2021. Please tell us what the one-time items is referring to and to the extent you are adjusting for non-GAAP items, revise to include a discussion of your GAAP SG&A with greater prominence. Refer to Question 102.10 of the non-GAAP C&DIs. In addition, you cite several factors that impacted your SG&A expenses such as increased spending on sales and marketing, ACES programs, growth initiatives, and variable compensation costs. Where a material change from period-to-period is due to two or more factors, including any offsetting factors, revise to describe the underlying reasons for such changes in both quantitative and qualitative terms. Similar revisions should be made to your gross margin discussion.

Response:

FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

In response to the Staff’s comment, the “one time” items refer to the summary of one-time items included on page 32 within the summary of Adjusted operating earnings. In future filings, we plan to eliminate this disclosure. An example of our revised disclosure can be found on page 29 of our Quarterly Report on Form 10-Q for the third quarter of 2022, which discloses the following:

“Selling, general and administrative expense (SG &A) increased during the third quarter and nine months ended October 1, 2022 when compared with the same prior year period, primarily due to the businesses acquired during 2021. SG&A as a percentage of sales was lower in the third quarter of 2022 and higher in the nine months ended October 1, 2022 compared with the same prior year period. The decrease in the third quarter of 2022 was driven by increased net sales and the benefit from cost-containment measures. The increase in the nine months ended October 1, 2022 reflects the impact of 2021 acquisitions, increased spending on sales and marketing, ACES ("Autonomy, Connectivity, Electrification and Shared access") programs, and other growth initiatives, partially offset by increased net sales. Research and development expense increased in 2022 versus 2021, reflecting continued investment in new products in all segments.”

Regarding gross margin, beginning with our 2022 Form 10-K, we will provide additional disclosures describing and, to the extent possible, quantifying the material factors impacting gross margin. An example of revised disclosures is presented as follows:

“Gross margin percentage increased 60 basis points in 2021 when compared to 2020, driven by increased sales (100 bps), acquisitions (10 bps), and favorable changes in foreign exchange rates (10 bps), partially offset by increased manufacturing costs, including material and labor inflation (60 bps).”

Regarding SG&A expenses, we currently disclose the factors impacting these line items in the order of relative significance, including consideration of offsetting impacts. The Company’s disclosures have included quantitative and qualitative information and the underlying reason for material changes, to the extent such information has been deemed material to investors’ understanding of business trends. For the periods presented, there were no such individual items deemed material. We will continue to disclose material factors in future filings.

4. We note that during each of the last three fiscal years and to date in fiscal 2022 you implemented various strategic initiatives to improve your cost structure, general operating efficiencies and utilization of production capacity. Your discussion of restructuring activities on page 33 provides a cross reference to Note 4. Please tell us how your current disclosures address the disclosure guidance in SAB Topic 5.P.4, or revise as necessary.

Response:

The Company acknowledges the Staff’s comment regarding the disclosure requirements in SAB Topic 5.P.4. We concluded the restructuring charges of $0.8 million, $4.1 million, and $18.8 million in 2021, 2020, and 2019, respectively, were immaterial to the consolidated financial statements as they represented 0.1%, 0.8%, and 4.0% of operating earnings in 2021, 2020, and 2019, respectively. We also concluded the likely effects the related actions would have on our financial position, future operating results, and liquidity were not material. Activities executed in prior periods were complete and the benefits realized prior to the year ended December 31, 2021. As such, we concluded the disclosures in SAB Topic 5.P.4 were not material or meaningful. In the event material restructuring activities occur in future periods, we will include the disclosures required by SAB Topic 5.P.4.

FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

Liquidity and Capital Resources, page 41

5. We note your disclosure regarding the dollar amount of future contractual cash obligations as of December 31, 2021. Please revise to also include a quantified discussion of the cash requirements related to the credit facility fee as discussed in Note 16. To the extent that such amounts are already reflected in the amounts disclosed, please revise and clarify accordingly. Refer to Item 303(b)(1) of Regulation S-K.

Response:

The Company acknowledges the Staff’s comment regarding our future contractual cash obligations disclosure and the cash requirements related to our credit facility fee. The credit facility fee per annum is 15 basis points of the total facility or $0.75 million. The maximum potential facility fee is $1.8 million using the 35 basis point maximum rate. We concluded the credit facility fees are not material future cash requirements as they represented .05% and 0.4%, using the maximum fee of $1.8 million, of total future contractual cash obligations and obligations coming due within one year, respectively. In the event the credit facility fees become material, we will include disclosure consistent with the requirements in Item 303(b)(1) of Regulation S-K.

Critical Accounting Estimates, page 42

6. Your Critical Accounting Estimates appear to repeat your accounting policy disclosures in the notes to the consolidated financial statements. Please revise to explain why each critical accounting estimate is subject to uncertainty and, to the extent the information is material and reasonably available, how much each estimate and/or assumption has changed over a relevant period, and the sensitivity of the reported amounts to the material methods, assumptions and estimates underlying its calculation. Refer to Item 303(b)(3) of Regulation S-K.

Response:

The Company acknowledges the Staff’s comment. We will revise the description of our critical accounting estimates beginning with our 2022 Form 10-K as requested by the Staff. The change during the fiscal year ended December 31, 2021, and the associated sensitivity of the reported amounts relating to each estimate, was not material. We will continue to evaluate any reasonably likely changes that could impact our critical accounting estimates and provide disclosure as needed in future filings. An example of our revised disclosures is presented as follows:

Warranty Reserves

We record an estimated liability for product warranties at the time revenue is recognized. The liability is estimated using historical warranty experience, projected claim rates and expected costs per claim. We exercise judgment when determining the appropriate historical periods to projected claim rates and expected costs per claim. Further, these estimates are subject to uncertainty as historical warranty experience may not be consistent with future warranty claims. We adjust our liability for specific warranty matters when they become known and the exposure can be estimated. Our warranty liabilities are affected by product failure rates as well as material usage and labor costs incurred in correcting a product failure. If actual costs differ from estimated costs, we must make a revision to the warranty liability, which could have an adverse impact on our results of operations and cash flows.

FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

Notes to Consolidated Financial Statements

Note 6. Segment Information, page 73

7. We note that the Engine Parts and Accessories and Advanced Systems Group operating segments have been aggregated into a single reportable segment, Parts & Accessories. Please provide us with an analysis of each of the criteria in ASC 280-10-50-11 to support such aggregation. Also, tell us how the acquisitions and integrations of Navico and RELiON impacted your evaluation, if at all.

Response:

We regularly reassess our segment presentation and document our conclusions based on the considerations outlined in ASC 280. In response to the request from the Staff, we have summarized our operating segment aggregation analysis for the year-ended December 31, 2021 below. The Company’s contemporaneous documentation and accounting analysis is also available.

•Criterion 1 – Aggregation is consistent with the objectives and basic principles of ASC 280

The Engine Parts & Accessories (“Engine P&A”) operating segment sells and distributes a wide range of marine parts and accessories to both original equipment manufacturers (“OEM”) and aftermarket channels. The Advanced Systems Group (“ASG”) operating segment sells and distributes many similar products within its portfolio of brands and also sells to both OEM and aftermarket customers.

Given that both operating segments have similar customers, similar products, and operate within the same industry subject to the same macro-economic environment and external factors, we have concluded that aggregating the Engine P&A and ASG operating segments is appropriate and consistent with the guidance in ASC 280. Further, the Company does not believe that providing disaggregated information would materially impact an investor’s view or understanding of our financial performance.

We also considered that Engine P&A and ASG have separate segment managers. The chief operating decision maker (“CODM”) believes that having separate individuals responsible for the Engine P&A and ASG segments will provide additional focus on each operating segment from an operational perspective. However, the CODM also believes it is important that the two operating segments work together to drive synergies and growth given their inter-dependence on one another. This is the reason the segment managers’ compensation is partially based on the combined segment results. Given that the CODM’s rationale for having separate segment managers for these operating segments is to increase focus within each of the operating segments as opposed to fundamental differences in the businesses that need to be evaluated separately, the Company does not believe that the fact that each operating segment has a segment manager (rather than one segment manager over both operating segments) is a reason that precludes aggregation.

•Criterion 2 – The segments have similar economic characteristics

The Engine P&A and ASG operating segments have similar economic characteristics. Overall, both segments operate within the same industry and are impacted by similar macroeconomic factors. Both operating segments are impacted heavily by the recreational boating market, OEM and aftermarket retail customer behavior, as well as seasonal weather conditions. The assembled workforce is also similar between both segments whereby no particular segment has a more or less unique labor force highly specialized in manufacturing and production.

FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

While ASC 280-10-50-11 specifies that segments with similar economic characteristics would be expected to have similar long-term average gross margins, it does not describe other factors an entity may use to evaluate economic characteristics. The Company has concluded that the primary metric to be assessed is operating margin as this is the primary measure of profitability used by the CODM for allocating resources and assessing performance.

The operating results reviewed by the CODM each period exclude unique, one-time nonrecurring items, restructuring, and purchase accounting amortization, and these are the results used by the CODM in making decisions and allocating resources. Purchase accounting amortization, approximately [***] per year, relates primarily to the timing of the acquisition of Power Products (2018), which is the largest business unit within the ASG operating segment. We note that that the purchase accounting intangible amortization is finite in nature based on the useful life of the intangible asset and not representative of the operating performance of the business and is a non-cash item. It should also be noted that management believes that the Company’s analysts and investors rely primarily on the adjusted operating metrics (vs. GAAP metrics). Finally, our bonus plan is based on adjusted operating metrics. Because the CODM, management, analysts, and investors all use adjusted operating metrics in evaluating the Company’s performance, we concluded it is appropriate to utilize the adjusted metrics within the economic similarity analysis.

In performing our assessment, we took into account historical, current, and projected performance of each operating segment. We also considered the fact that the Company’s current strategic outlook is not more or less directionally focused towards one particular operating segment vs. the other, as such, the Company would not expect a divergence in future prospects or margins to occur going forward. Furthermore, overall operating margins by product group and product types are generally consistent within each of the individual operating segments. Finally, overall product mix is also expected to remain generally consistent over time.

The Company’s historical, current, and projected quantitative assessment supporting its ability to aggregate the Engine P&A and ASG operating segments is presented below.

Actual operating margins for both operating segments range from [***] during the historical, current and forecasted periods from 2019 - 2025, which indicates that the businesses have similar overall operating performance. We also considered that the operating margin for ASG in 2018 was lower than 2019, 2020 and the forecasted periods as a result of the Power Products acquisition in 2018. As we don’t expect this disparity to exist going forward, we determined that the 2018 margins do not preclude aggregation of the businesses.

We also noticed that operating margins are expected to diverge slightly for FY2022, resulting in a projected [***] actual difference or a [***] relative difference, due primarily to one-time investments within ASG. However, it should be noted that the relative margins continue to converge during the strategic period for fiscal years 2023, 2024, and 2025, resulting in an actual difference of [***] or a relative difference of [***] expected for 2025.

ASC 280 does not prescribe a specific threshold for economic similarity, and, therefore, there is no bright line or definitive test when determining if economic characteristics are sufficiently similar. We note that the Deloitte and KPMG segment financial reporting guides do not refer to any specific percentage threshold, and the E&Y segment financial reporting guide references a 10% relative difference as a datapoint to consider, but also stresses the importance of management judgment. We believe that an investor would consider these businesses to be economically similar given the operating margins are within [***] basis points for 2019, 2020 and 2021, and separate reporting would not add to an investor’s

FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

understanding. As such, we conclude that the two operating segments have similar economic characteristics.

Although less utilized by the CODM for evaluating operating performance, the Company also evaluated the historical, current and projected gross margins for both the Engine P&A and ASG operating segments presented as follows:

The Company notes that the difference in gross margins is not representative of any difference in future prospects when comparing the Engine P&A operating segment to the ASG operating segment. While the relative difference of gross margin is greater than that of operating earnings, we considered that both businesses have gross margin in the [***] range, the CODM does not utilize gross margin as a primary metric when evaluating business performance and allocating resources, and investors/analysts are less focused on gross margin than operating margin. This is evidenced by discussions with the CODM and that the reporting packages described above focus on revenues and operating margins. We also noted that ASC 280 does not prescribe specific thresholds or bright line guidance regarding economic similarity. While we do not believe gross margin is the primary metric to consider when evaluating economic similarity based on how our business performance is managed and evaluated, we note that this data point supports aggregation of the Engine P&A and ASG operating segments

•Criterion 3 – The segments are similar with respect to the five qualitative characteristics specified in ASC 280-10-50-11(a)-(e).

The nature of the products and services

Both segments manufacture, assemble, and distribute marine parts and accessories to the global boating and marine industry. In addition, a small portion of each segment has a targeted focus on selling to and serving the RV industry.

The Engine P&A operating segment, comprised of Mercury P&A, Land and Sea Distributing Inc, Lankhorst Taselaar, Paynes Marine Group, and Boating Lifestyle Adventure businesses sell and distribute a wide range of marine parts and accessories, as well as a small product offering catalog to the RV industry. The ASG operating segment sells and distributes many similar products within its Attwood, RELiON, and Power Products businesses. The Power Products businesses also are a leading supplier of electrical and surge protection equipment to the RV industry.

Overall, both operating segments provide a full suite of parts and accessories, which complement our other key business of selling boats and selling marine engines. It should be further noted that both the products and service offerings within these segments are subject to the same cyclical and seasonal market trends. Demand in most instances is typically driven primarily by boat use.

Finally, as previously mentioned, both segments serve predominately the marine industry, however both segments also have a small portion of the business dedicated the RV industry, (both segments sales account for approximately [***] marine and [***] RV). The Company notes that this relative market breakout between operating segments is also expected to remain consistent over time.

As such, we have concluded that both operating segments essentially have similar products and services which are sold into the same industry.

The nature of the production processes

FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

Both operating segments include core manufacturing processes and some light assembly. In addition, both segments also include some fully dedicated distribution businesses. For example, the Engine P&A operating segment is approximately [***] distribution, which is mainly comprised of the Land ‘N’ Sea business. The ASG operating segment is approximately [***] distribution, which is sold through both Attwood and Power Products. The remaining is manufacturing. The Company also plans on integrating some of the manufacturing locations and distribution networks across both segments (see further discussion in the “methods used to distribute products” criteria). As such, we conclude that the nature of the production processes for Engine P&A and ASG is similar.

The type or class of customer for their products and services

The Engine P&A and ASG operating segments serve a similar class of customer and, in most instances, the same customers. In addition, the segments also have several of the same future prospective customers. Sales are driven through domestic and international markets through large, big box retail channels, and through the Company’s Mercury Marine Dealer networks and OEM networks. All businesses within each of the segments also sell directly to all boat brands comprising Brunswick Boat Group (“BBG”), which is one of the Company’s other operating segments, and many other boat manufacturers.

Both operating segments are primarily domestic based (approximately [***] domestic) with the remaining portion serving international customers.

Both segments have several large, similar customers and, in many instances, the same customers. In addition, there were no, large, material customers within the Engine P&A customer base that have substantially different risk profiles that are not also served by ASG.

Furthermore, all brands and businesses comprising the Engine P&A and ASG operating segments offer similar retail incentive promotions and volume discounts. Both operating segments also offer to its customers the Mercury Marine Power of Choice incentive program, which is effectively a rebate program based on cumulative purchase activity.

In addition, for inclusion under the terms of the programs, each OEM, retailer, or distributor must purchase a minimum threshold of Brunswick P&A products over the course of a year. Qualifying purchases can be made from either the Engine P&A or ASG operating segment.

Given these considerations, we conclude that the type and class of customer for the Engine P&A and ASG operating segments are similar.

The methods used to distribute their products or provide their services

Both segments sell and distribute their products through dedicated distributors, authorized dealers, or sell direct to large retail customers. In connection with the recent acquisition of Power Products in 2018, the Company has also made it a strategic initiative to integrate the two operating segments in attempt to take advantage of opportunistic synergies across the two businesses; the largest of which is leveraging the existing footprints for each of the businesses in order to better reach and serve customers. For example, the Land ‘N’ Sea business, (within the Engine P&A segment) has warehouse and distribution locations located throughout the United States, Latin America, and Canada regions. Currently the Attwood business (ASG segment) has a portion of its revenue generated through selling direct to Land ‘N’ Sea to take advantage of its larger network.

In addition, a similar initiative exists for channel optimization relating to the Mercury P&A business (Engine P&A segment), and the Power Products business (ASG segment). As previously mentioned, both segments effectively sell to and serve the same customers (both boat OEMs and retail customers).

FOIA Confidential Treatment Request by

Brunswick Corporation Pursuant to Rule 83 (17 C.F.R. 200.83)

Depending on customer location relative to the existing footprint across all businesses comprising both segments, there are significant opportunities to better serve customers and reduce costs given the same customers and product types.

Given the interdependence of and similarities between both businesses (similar products, similar customers, etc.), this further illustrates the Company’s strategic goals of leveraging synergies across both businesses given the similar offerings, product portfolio, and distribution methods.

As such, we conclude that the methods used to distribute Engine P&A and ASG products are similar.

If applicable, the nature of the regulatory environment, for example, banking, insurance, or public utilities

Both segments operate in and are subject to the global marine regulatory environment.

Aggregation Conclusion:

The Company has concluded that its Engine P&A and ASG operating segments are economically similar and meet the criteria for aggregation. As such, we have aggregated both operating segments into a single “P&A” Reportable Segment for external disclosure purposes under ASC 280.

As it relates to the acquisition of Navico and Relion, total 2021 Navico forecasted revenues and operating earnings were [***] and [***] respectively, which represented [***] and [***] of consolidated net sales and operating earnings. Total 2021 Relion forecasted revenues and operating earnings were [***] and [***] respectively, which represented less than [***] of consolidated net sales and operating earnings. These results did not materially impact our evaluation of the aggregation criteria under ASC 280.

Please do not hesitate to contact me at (847)735-4926 if you have any questions or would like to discuss any of the information addressed in this letter.

Sincerely,

/s/ Ryan M. Gwillim

Ryan M. Gwillim, Executive Vice President and Chief Financial Officer

cc: Sonia Barros, Sidley Austin LLP