UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| £ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011 |

| OR | |

| £ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to | |

| OR | |

| £ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission File Number: 001-34754

| China New Borun Corporation |

| (Exact name of Registrant as specified in its charter) |

| Not applicable |

| (Translation of Registrant’s name into English) |

| Cayman Islands |

| (Jurisdiction of incorporation or organization) |

| Bohai Industrial Park, Yangkou Town, Shouguang, Shandong, People’s Republic of China 262715 |

| (Address of principal executive offices) |

|

Mr. Yuanqin (Terence) Chen Chief Financial Officer Telephone: +86 536 545 1199 E-mail: terence.chen@chinanewborun.com Bohai Industrial Park, Yangkou Town Shouguang, Shandong People’s Republic of China 262715 |

| (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| American Depositary Shares, | New York Stock Exchange | |

| each representing one ordinary shares, par value $0.001 per share |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

| None |

| (Title of Class) |

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

| None |

| (Title of Class) |

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

| 25,725,000 Ordinary Shares, par value $0.001 per share, as of | |

| December 31, 2011 |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of the Securities Exchange Act 1934.

Yes o No x

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer x |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S.GAAP x | International Financial Reporting Standards as issued by the International Accounting Standards Board o |

Other o |

If “Other” has been checked in response to the previous question, indicated by check mark which financial statement item the registrant has elected to follow.

Item 17 o Item 18 o

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

CHINA NEW BORUN CORPORATION

TABLE OF CONTENTS

| INTRODUCTION | 4 | |

| FORWARD-LOOKING STATEMENTS | 5 | |

| PART I. | ||

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 7 |

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE | 7 |

| ITEM 3. | KEY INFORMATION | 7 |

| A. Selected Financial Data | 7 | |

| B. Capitalization and Indebtedness | 8 | |

| C. Reasons for the Offer and Use of Proceeds | 8 | |

| D. Risk Factors | 9 | |

| ITEM 4. | INFORMATION ON THE COMPANY | 35 |

| A. History and Development of the Company | 35 | |

| B. Business Overview | 42 | |

| C. Organizational Structure | 65 | |

| D. Property, Plant and Equipment | 65 | |

| ITEM 4A. | UNRESOLVED STAFF COMMENTS | 65 |

| ITEM 5. | OPERATING AND FINANCIAL REVIEW AND PROSPECTS | 66 |

| A. Operating Results | 66 | |

| B. Liquidity and Capital Resources | 78 | |

| C. Research and Development | 80 | |

| D. Trend Information | 80 | |

| E. Off-Balance Sheet Commitments and Arrangements | 80 | |

| F. Tabular Disclosure of Contractual Obligations | 80 | |

| ITEM 6. | DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES | 81 |

| A. Directors and Senior Management | 81 | |

| B. Compensation | 84 | |

| C. Board Practices | 84 | |

| D. Employees | 87 | |

| E. Share Ownership | 88 | |

| ITEM 7. | MAJOR SHAREHOLDERS AND RELATED PARTY TRANSACTIONS | 89 |

| A. Major Shareholders | 89 | |

| B. Related Party Transactions | 89 | |

| C. Interests of Experts and Counsel | 92 | |

| ITEM 8. | FINANCIAL INFORMATION | 92 |

| A. Consolidated Statements and Other Financial Information | 92 | |

| B. Significant Changes | 93 | |

| ITEM 9. | THE OFFER AND LISTING | 94 |

| A. Offering and listing details | 94 | |

| B. Plan of Distribution | 94 | |

| C. Markets | 94 | |

| D. Selling Shareholders | 94 | |

| E. Dilution | 94 | |

| F. Expenses of the Issue | 94 | |

| ITEM 10. | ADDITIONAL INFORMATION | 94 |

| A. Share capital | 94 | |

| B. Memorandum and Articles of Association | 95 | |

| C. Material Contracts | 95 | |

| D. Exchange Controls | 95 | |

| E. Taxation | 95 | |

| F. Dividends and Paying Agents | 102 | |

| 1 |

| G. Statement by Experts | 102 | |

| H. Documents on Display | 102 | |

| I. Subsidiaries Information | 103 | |

| ITEM 11. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 103 |

| ITEM 12. | DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 104 |

| PART II. | ||

| ITEM 13. | DEFAULTS, DIVIDEND ARREARAGES AND DELINQUENCIES | 106 |

| ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 106 |

| ITEM 15. | CONTROLS AND PROCEDURES | 106 |

| ITEM 16A. | AUDIT COMMITTEE FINANCIAL EXPERT | 106 |

| ITEM 16B. | CODE OF ETHICS | 106 |

| ITEM 16C. | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 107 |

| ITEM 16D. | EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 107 |

| ITEM 16E. | PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 107 |

| ITEM 16F. | CHANGE IN REGISTRANT’S CERTIFYING ACCOUNTANT | 107 |

| ITEM 16G. | CORPORATE GOVERNANCE | 107 |

| PART III. | ||

| ITEM 17. | FINANCIAL STATEMENTS | 108 |

| ITEM 18. | FINANCIAL STATEMENTS | 108 |

| ITEM 19. | EXHIBITS | 108 |

| INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | ||

| EX-1.1 | AMENDED AND RESTATED ARTICLES OF ASSOCIATION OF THE REGISTRANT | |

| EX-1.2 | CERTIFICATE OF INCORPORATION OF CHINA NEW BORUN CORPORATION | |

| EX-2.1 | FORM OF AMERICAN DEPOSITARY RECEIPT | |

| EX-2.2 | SPECIMEN CERTIFICATE FOR ORDINARY SHARES | |

| EX-2.3 | DEPOSIT AGREEMENT AMONG CHINA NEW BORUN CORPORATION, THE DEPOSITARY AND OWNERS AND HOLDERS OF AMERICAN DEPOSITARY SHARES ISSUED THEREUNDER, DATED JUNE 10, 2010 | |

| EX-2.4 | SHAREHOLDERS AGREEMENT, DATED MARCH 31, 2010, BY AND AMONG CHINA NEW BORUN CORPORATION, KING RIVER HOLDING LIMITED, STAR ELITE, EARNSTAR AND TDR ADVISORS | |

| EX-2.5 | AMENDMENT TO SHAREHOLDERS AGREEMENT, DATED JUNE 8, 2010, BY AND AMONG CHINA NEW BORUN CORPORATION, KING RIVER HOLDING LIMITED, EARNSTAR HOLDING LIMITED AND TDR ADVISORS, INC. | |

| EX-4.1 | SHARE EXCHANGE AGREEMENT, DATED FEBRUARY 28, 2010, BY AND AMONG CHINA NEW BORUN CORPORATION, GOLDEN DIRECTION LIMITED, STAR ELITE, EARNSTAR, TDR ADVISORS AND CHINA HIGH ENTERPRISES LIMITED | |

| EX-4.2 | SHARE EXCHANGE AGREEMENT, DATED MARCH 15, 2010, BY AND AMONG CHINA NEW BORUN CORPORATION, MRS. SHAN JUNQIN, GOLDEN DIRECTION LIMITED AND CHINA HIGH ENTERPRISES LIMITED | |

| EX-4.3 | MORTGAGE CONTRACT, DATED ON OR ABOUT NOVEMBER 4, 2011, BY AND BETWEEN DAQING BORUN BIOTECHNOLOGY CO., LTD. AND THE AGRICULTURAL DEVELOPMENT BANK OF CHINA | |

| EX-4.4 | FORM OF INDEPENDENT DIRECTOR AGREEMENT | |

| EX-4.5 | FORM OF INDEMNIFICATION AGREEMENT | |

| EX-4.6 | COUNTER SECURITY PLEDGE AGREEMENT, DATED JULY 1, 2011, BY AND BETWEEN DAQING BORUN BIOTECHNOLOGY CO., LTD. AND THE ZHONG LV CREDIT GUARANTEE CO., LTD. | |

| EX-4-7 | COUTNER-GUARANTEE (MORTGAGE) AGREEMENTS, DATED JULY 1, 2011, BY AND BETWEEN DAQING BORUN BIOTECHNOLOGY CO., LTD. AND THE ZHONG LV CREDIT GUARANTEE CO., LTD. | |

| EX-4-8 | COMMODITY FINANCING PLEDGE SUPERVISION AGREEMENT, DATED APRIL 15, 2011, BY AND AMONG INDUSTRIAL AND COMMERCIAL BANK OF CHINA CO., LTD. DAQING BRANCH, DAQING BORUN BIOTECHNOLOGY CO., LTD. AND CHINA NATIONAL FOREIGN TRADE TRANSPORTATION (GROUP) HEILONGJIANG CO., LTD. | |

| 2 |

| EX-8.1 | SUBSIDIARIES OF REGISTRANT | |

| EX-12.1 | CERTIFICATION BY PRINCIPAL EXECUTIVE OFFICER PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002 | |

| EX-12.2 | CERTIFICATION BY PRINCIPAL FINANCIAL OFFICER PURSUANT TO SECTION 302 OF THE SARBANES-OXLEY ACT OF 2002 | |

| EX-13.1 | CERTIFICATION BY PRINCIPAL EXECUTIVE OFFICER PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002 | |

| EX-13.2 | CERTIFICATION BY PRINCIPAL FINANCIAL OFFICER PURSUANT TO SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002 | |

| EX-15.1 | CONSENT OF BDO CHINA SHU LUN PAN CERTIFIED PUBLIC ACCOUNTANTS LLP | |

| EX-15.2 | CONSENT OF BDO CHINA DAHUA CPA CO., LTD. |

| 3 |

INTRODUCTION

Unless the context otherwise requires, references in this annual report on Form 20-F to:

| · | “ADRs” are to the American depositary receipts, which, if issued, evidence our ADSs; |

| · | “ADSs” are to our American depositary shares, each of which represents one ordinary share; |

| · | “BDO” is to our independent auditor BDO China Shu Lun Pan Certified Public Accountants LLP; |

| · | “CAGR” is to compound annual growth rate; |

| · | “China” or the “PRC” are to the People’s Republic of China, excluding, for the purposes of this annual report only, Taiwan and the special administrative regions of Hong Kong and Macau; |

| · | “NYSE” is to the New York Stock Exchange; |

| · | “ordinary shares” are to our ordinary shares, par value $0.001 per share; |

| · | “RMB” and “Renminbi” are to the legal currency of China; |

| · | “$” and “U.S. dollars” are to the legal currency of the United States; and |

| · | “we,” “us,” “our Company,” “our” and “New Borun” are to China New Borun Corporation and its consolidated subsidiaries. |

Discrepancies in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

We completed our initial public offering of 5,725,000 ADSs on June 16, 2010. Our ADSs are listed on the NYSE, under the symbol “BORN.”

Unless otherwise noted, all translations from RMB to U.S. dollars were made at a rate of RMB 6.3009 to $1.00 as published by the People’s Bank of China on December 31, 2011. We make no representation that the RMB amounts referred to in this annual report could have been or could be converted into U.S. dollars at any particular rate or at all. See also Item 3.A, “Key Information - Selected Financial Data - Exchange Rate Information.”

| 4 |

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F, including in particular Item 3.D, “Key information — Risk Factors,” Item 4, “Information on the Company” and Item 5, “Operating and Financial Review and Prospects,” contains statements that relate to future events, including our future operating results and conditions, our prospects and our future financial performance and condition. These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements.

In some cases, these forward-looking statements can be identified by words or phrases such as “anticipates,” “believes,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “possible,” “potential,” “predicts,” “projects,” “seeks,” “should,” “will,” “would,” negatives of such terms or other expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, without limitation, statements relating to:

| · | the significant risks, challenges and uncertainties in the edible alcohol manufacturing industry and for our business generally, including our beliefs regarding the cost advantages and scalability provided by our manufacturing methods and processes; |

| · | supply and demand in the edible alcohol industry in China; |

| · | our ability to offset anticipated increases in raw material and other costs that could compress or decrease our gross margins; |

| · | our current expansion strategy, including our ability to expand production capacity and outputs; |

| · | market and industry demand, including demand for our products by our customers that incorporate our products into other products in the food and beverage, medical and health and chemical industries; |

| · | the global economic downturn and its effect on our business and operations; |

| · | our beliefs regarding our strengths and strategies; |

| · | our ability to maintain strong relationships with suppliers or customers; |

| · | our beliefs as to the regulatory environment in China and in other jurisdictions in which we sell our products; |

| · | our ability to comply with all relevant environmental, health and safety laws and regulations; |

| · | our beliefs regarding the competitiveness of our products; |

| · | market acceptance of our products and our ability to attract new customers; |

| · | our ability to effectively protect our intellectual property and trade secrets and not infringe on the intellectual property and trade secrets of others; |

| · | our ability to obtain or maintain permits and licenses to carry on our business; |

| 5 |

| · | our success in the acquisition of new production facilities; and |

| · | our future prospects, business development, results of operations and financial condition. |

The forward-looking statements contained in this annual report speak only as of the date of this annual report or, if obtained from third-party studies or reports, the date of the corresponding study or report, and are expressly qualified in their entirety by the cautionary statements in this annual report. Since we operate in an emerging and evolving environment and new risk factors emerge from time to time, you should not rely upon forward-looking statements as predictions of future events. Except as otherwise required by the securities laws of the United States, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, to reflect events or circumstances after the date of this annual report or to reflect the occurrence of unanticipated events. All forward-looking statements contained in this annual report are qualified by reference to this cautionary statement.

| 6 |

PART I.

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

A. Selected Financial Data

The following audited consolidated statements of operations data for each of the years ended December 31, 2009, 2010 and 2011, and the audited balance sheet data as of December 31, 2010 and 2011 are derived from our audited consolidated financial statements, which are included elsewhere in this annual report. The selected historical consolidated statement of operations data for the years ended December 31, 2007 and 2008 and the selected historical consolidated balance sheet data as of December 31, 2007, 2008 and 2009 set forth below are derived from our audited historical consolidated financial statements, which are not included in this annual report. Historical results are not necessarily indicative of the results of operations for future periods. The following data is qualified in its entirety by and should be read in conjunction with Item 5, “Operating and Financial Review and Prospects” and our consolidated financial statements and related notes included elsewhere in this annual report. Our audited consolidated financial statements are prepared in accordance with U.S. Generally Accepted Accounting Principles (U.S. GAAP), and have been audited by BDO China Shu Lun Pan Certified Public Accountants LLP, an independent registered public accounting firm. Our historical results for any period are not necessarily indicative of results to be expected in any future period.

Selected Consolidated Statement of Operations Data:

| Year ended December 31, | ||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | 2011 | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | $ | |||||||||||||||||||

| Revenues | 487,305,927 | 615,881,195 | 1,060,493,812 | 1,713,924,878 | 2,685,223,409 | 426,165,057 | ||||||||||||||||||

| Cost of goods sold | 387,729,613 | 493,847,780 | 811,865,247 | 1,308,303,166 | 2,175,060,342 | 345,198,359 | ||||||||||||||||||

| Gross profit | 99,576,314 | 122,033,415 | 248,628,565 | 405,621,712 | 510,163,067 | 80,966,698 | ||||||||||||||||||

| Selling, general and administrative expenses | 10,057,899 | 12,928,345 | 22,547,881 | 45,716,043 | 59,061,056 | 9,373,432 | ||||||||||||||||||

| Operating income | 89,518,415 | 109,105,070 | 226,080,684 | 359,905,669 | 451,102,011 | 71,593,266 | ||||||||||||||||||

| Other expenses | 2,237,334 | 5,333,952 | 3,408,024 | 12,216,600 | 32,912,857 | 5,223,517 | ||||||||||||||||||

| Income before income taxes | 87,281,081 | 103,771,118 | 222,672,660 | 347,689,069 | 418,189,154 | 66,369,749 | ||||||||||||||||||

| Income tax expense | 28,557,072 | 26,640,990 | 56,262,029 | 88,264,738 | 105,194,680 | 16,695,183 | ||||||||||||||||||

| Net income | 58,724,009 | 77,130,128 | 166,410,631 | 259,424,331 | 312,994,474 | 49,674,566 | ||||||||||||||||||

| Amortization of preference share discount | — | (42,000,000 | ) | — | — | — | — | |||||||||||||||||

| Participation in undistributed earnings by preference shareholders | — | (7,026,026 | ) | (42,868,951 | ) | (27,744,622 | ) | — | — | |||||||||||||||

| Net income attributable to ordinary shareholders | 58,724,009 | 28,104,102 | 123,541,680 | 231,679,709 | 312,994,474 | 49,674,566 | ||||||||||||||||||

Earnings per share(1) | ||||||||||||||||||||||||

| Basic and diluted | 3.96 | 1.89 | 8.32 | 11.07 | 12.17 | 1.93 | ||||||||||||||||||

| Weighted average ordinary shares outstanding: | ||||||||||||||||||||||||

| Basic and diluted | 14,847,811 | 14,847,811 | 14,847,811 | 20,927,117 | 25,725,000 | 25,725,000 | ||||||||||||||||||

| (1) | All share and per share data have been presented to give retrospective effect to our reorganization as described in Item 4.A., “Information on the Company — History and Development of the Company.” For the purpose of calculating basic and diluted earnings per ordinary share, the number of ordinary shares used in the calculation reflects the issuance of ordinary shares as if the reorganization took place as of the beginning of the earliest period presented and assumes that all issued and outstanding Class A, Class B and Class C convertible preference shares have been fully converted into ordinary shares. | |

| 7 |

Selected Consolidated Balance Sheet Data:

| December 31, | ||||||||||||||||||||||||

| 2007 | 2008 | 2009 | 2010 | 2011 | 2011 | |||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | $ | |||||||||||||||||||

| Total current assets | 127,129,510 | 104,986,070 | 251,807,507 | 647,739,510 | 770,487,271 | 122,282,098 | ||||||||||||||||||

| Total assets | 265,622,975 | 476,114,001 | 765,860,621 | 1,762,905,212 | 1,972,753,262 | 313,090,711 | ||||||||||||||||||

| Total liabilities | 126,784,933 | 180,134,221 | 249,651,232 | 746,377,285 | 643,321,591 | 102,099,953 | ||||||||||||||||||

| Total shareholders’ equity | 138,838,042 | 295,979,780 | 516,209,389 | 1,016,527,927 | 1,329,431,671 | 210,990,758 | ||||||||||||||||||

Exchange Rate Information

Our business is conducted in China and all of our revenue and the majority of our expenses are denominated in Renminbi. This annual report contains translations of Renminbi amounts into U.S. dollars at specified rates. Unless otherwise noted, all translations from Renminbi to U.S. dollar amounts were made at a rate of RMB 6.3009 to USD 1.00 as published by the People’s Bank of China on December 31, 2011. We make no representation that the Renminbi or U.S. dollar amounts referred to in this annual report could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all.

The following table sets forth information concerning exchange rates between the Renminbi and the U.S. dollars for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this annual report or will use in the preparation of our periodic reports or any other information to be provided to you. The exchange rate of Renminbi per U.S. dollar as published by the People’s Bank of China was RMB6.3035 to $1.00 as of April 5, 2012.

| Exchange Rate | |||||||||||||||||

| Period | Period End |

Average(1) |

Low | High | |||||||||||||

| (RMB per $1.00) | |||||||||||||||||

| Year ended December 31, | |||||||||||||||||

| 2007 | 7.3046 | 7.5969 | 7.8074 | 7.3046 | |||||||||||||

| 2008 | 6.8346 | 6.9267 | 7.1853 | 6.8183 | |||||||||||||

| 2009 | 6.8282 | 6.8317 | 6.8420 | 6.8272 | |||||||||||||

| 2010 | 6.6227 | 6.7668 | 6.8280 | 6.6227 | |||||||||||||

| 2011 | 6.3009 | 6.4445 | 6.5891 | 6.3009 | |||||||||||||

| Most recent six months | |||||||||||||||||

| October 2011 | 6.3233 | 6.3566 | 6.3762 | 6.3233 | |||||||||||||

| November 2011 | 6.3482 | 6.3408 | 6.3587 | 6.3165 | |||||||||||||

| December 2011 | 6.3009 | 6.3281 | 6.3421 | 6.3009 | |||||||||||||

| January 2012 | 6.3115 | 6.3168 | 6.3306 | 6.3001 | |||||||||||||

| February 2012 | 6.2919 | 6.3000 | 6.3116 | 6.2919 | |||||||||||||

| March 2012 | 6.2932 | 6.3072 | 6.3359 | 6.2840 | |||||||||||||

| April 2012 (through April 5) | 6.3035 | 6.3035 | 6.3035 | 6.3035 | |||||||||||||

| (1) | Annual averages are calculated from month-end rates. Monthly averages are calculated using the average of the daily rates during the relevant period. |

Source: the People’s Bank of China Statistical Release

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

| 8 |

D. Risk Factors

An investment in the ADSs involves significant risks. You should consider carefully the material risks described below and all of the information contained in this annual report before deciding whether to purchase any ADSs. Our business, financial condition or results of operations could be materially adversely affected by these risks if any of them actually occur. The trading price of the ADSs could decline due to any of these risks, and an investor may lose all or part of his investment. This filing also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks described below and elsewhere in this annual report.

RISKS RELATED TO OUR COMPANY

If we fail to accurately project demand for our products, we may encounter problems of over capacity, which would materially and adversely affect our business, financial condition and results of operations, as well as damage our reputation and brand.

Historically, edible alcohol production capacity has exceeded actual market demand. Due to the rapid growth of market demand, we believe market demand for edible alcohol is likely to exceed production capacity in the PRC in the next few years. We have planned our expansion assuming a reduction in market supply based on the national industry policies to close “backward” smaller manufacturers with a production capacity of less than 30,000 tons per year (see Item 4.B, “Information on the Company — Business Overview — Regulation”), the halt in approvals for new corn deep-processing production capacities in principle, and the growth in demand for edible alcohol driven by the PRC Chinese baijiu industry. If supply of edible alcohol in the PRC is not in fact reduced or if the PRC government began to approve new production capacities or there is no, or little, growth in demand for edible alcohol as we have expected, we may encounter difficulties in selling our increased production capacity, which would materially and adversely affect our business, financial condition and results of operations.

Our Shouguang and Daqing facilities have signed pre-sales contracts and letters of intent with major customers worth a total of approximately 90% of our total edible alcohol production capacity for the year ending December 31, 2012 that provide for minimum purchases equal to an aggregate of 340,000 tons of edible alcohol. However, these sales are made through monthly purchase orders similar to those placed by our other customers (see Item 4.B, “Information on the Company — Business Overview — Our Customers and Methods of Distribution of Our Products”). Purchase orders are typically placed on a monthly basis, and we take such orders into account when we formulate our overall operation plans. We project demand for our products based on rolling projections from our customers and customer inventory levels. The varying sales and purchasing cycles of our customers, however, make it difficult for us to accurately forecast future demand for our products. Our inability to accurately predict and to timely meet demand, or the failure of our 2012 contract purchasers to take up their contracted volume of our products, could materially and adversely affect our business, financial condition and results of operations.

Our inability to expand or to manage the expansion of our production capacity and growth could materially adversely affect our business, financial condition and results of operations, and result in a loss of business opportunities.

We plan to continue to expand our production capacity at our Daqing facility. However, we may be unsuccessful in the timely or cost-efficient expansion of our production capacity. This project and others may not be constructed on the anticipated timetable or within budget. Any material delay in completing these projects, or any substantial increase in costs or quality issues in connection with these projects, could materially and adversely affect our business, financial condition and results of operations, and result in a loss of business opportunities.

| 9 |

Furthermore, we have limited operational, administrative and financial resources, which may be inadequate to sustain the growth we want to achieve. We have experienced a period of rapid growth and expansion that has placed, and will continue to place, strain on our management personnel, systems and resources. To accommodate our growth pursuant to our strategies, we anticipate that we will need to implement a variety of new and upgraded operational and financial systems, procedures and controls, and improve our accounting and other internal management systems, all of which require substantial management efforts and financial resources. We will also need to continue to expand, train, manage and motivate our workforce, and effectively manage our relationships with our customers and suppliers. All of these endeavors will require substantial management effort and skills and the incurrence of additional expenditures. We cannot assure you that we will be able to efficiently or effectively implement our growth strategies and manage the growth of our operations, and any failure to do so may limit our future growth and hamper our business strategy.

In addition, in Daqing, we rely on the use of a government-owned rail station in close proximity to our Daqing facility to transport our products, including our planned expanded production, to our customers. Although we have not previously been restricted from its use, the government may prohibit our use of such station at anytime. If this were to occur, or if we were to lose access to the station for any reason, we would be required to transport our products to the next closest rail station by truck, which would increase our costs of transportation, have an adverse effect on our profit margin and inhibit our expansion and growth.

Rising prices of our raw materials could yield lower margins for our products if we are unable to pass such rising prices on to our customers, which could reduce our profitability and have a material adverse effect on our business.

The key raw materials used in the production of our products are corn and coal. Changes in the prices for these raw materials would significantly affect our cost of goods sold. In general, rising prices of corn and coal will produce lower profit margins for us if we are unable to pass such rising costs on to our customers. Whether we can pass such rising costs on to our customers depends on a variety of factors, including but not limited to corn and coal pricing and consumer market conditions. The price of corn is influenced by weather conditions and other factors affecting crop yields, farmer planting decisions and general economic, market and regulatory factors. These factors include government policies and subsidies with respect to agriculture and international trade, and global and local demand and supply. The price of coal is influenced by a variety of factors, including market conditions, mine operating costs, coal quality, transportation costs, fluctuations in demand by other industry sectors, such as power plants, and the cost of alternative fuels. The significance and relative effect of these factors on the price of corn and coal is difficult to predict. In addition, although our supply contracts provide us access to corn at prices which we believe have historically been below the spot market price in the off season and times of high price volatility (due to crop failure and other factors), we have no contracts or derivative instruments in place that effectively hedge against the fluctuations in the price of our raw materials as our corn purchase and edible alcohol sales contracts are priced based on market conditions. Any event that tends to negatively affect the supply of these raw materials could increase prices and potentially harm our business. To the extent that we cannot fully pass on the price increases in raw materials to our customers, or at all, our business and profitability would be materially and adversely affected.

If we are unable to access corn of the quality required to meet our production standards, or if we are unable to obtain a sufficient supply of raw materials from our suppliers, or at all, our business, financial condition and results of operations may suffer.

From time to time we may be unable to access corn of the quality and type that meets our production standards, which could adversely affect our financial performance. For example, if the corn is too wet or if the starch content of the corn is too low, we would be required to purchase and then process larger quantities of such lower-quality corn in order to maintain the same quality in the production of our edible alcohol, and such increased raw material cost, as well as increased energy costs of burning more coal in order to process the increased amount of corn, would reduce our profit margins. Furthermore, our extended inability to obtain and process corn of the required quality would also reduce our annual production.

| 10 |

If we experience a shortage in the supply of corn in the future, irrespective of quality, our production capacities and results of operations would be materially and adversely affected. We intend to source corn for at least five months’ demand in the non-harvest season of 2012 through framework agreements with local granaries in Heilongjiang Province (where we believe corn prices are the lowest in Northeastern China). According to such framework agreements, we engage the granaries to purchase corn from local farmers in order to satisfy corn requirements of our Shouguang and Daqing facilities during the non-harvest season in 2012. The granaries also store the corn for us and obtain loans from the Agricultural Development Bank(“ADB”), to carry out the purchase of corn on our behalf (see Item 4.B, “Information on the Company — Business Overview — Our Competitive Strengths - Corn Sourcing Arrangements”). If we lose any of these significant sources of corn through crop failure or through the failure by the granaries or the ADB to abide by the material terms of our sourcing arrangements, we would be required to purchase corn at less favorable prices which could adversely affect our profit margins. Also, there is no guarantee that we will realize savings through our sourcing arrangements since we are liable for the interest payments on the bank loans between the granaries and ADB and other charges by the granaries like transportation costs and storage costs. We may also have difficulty finding alternative sources of corn on satisfactory terms in a timely manner, or at all, which could cause us not to operate at full capacity. Identifying and accessing alternative sources may increase our costs and extended lack of raw materials will reduce production capacity which would have a materially adverse effect on our financial performance.

We rely on a steady supply of coal to power our production facilities. If we experience a shortage of coal, our business could be adversely affected. We currently have relationships with nine suppliers of coal, however we do not have any long-term supply agreements in place with these suppliers and we cannot guarantee that such suppliers will continue to do business with us. In the event that our coal suppliers stop doing business with us, we would be forced to find replacement coal suppliers, or increase our coal uptake from existing suppliers, which could take time to locate and secure. If we experience any extended period of time without coal, we would need to obtain power from the local electricity grid, if available, which would have a material adverse effect on our business, financial condition and results of operations. See “Risk Factors - Risks Related To Our Company -Interruptions with our coal-fired power-generating systems, whether planned or unexpected, may have an adverse effect on our business, financial condition and results of operations.”

If we experience problems with our product quality, customer satisfaction with respect to pricing of our products or the timely delivery of our products, we could lose our customers and market acceptance, which would negatively affect our sales and have an adverse effect on our business, financial condition and results of operations.

Our growth and sales primarily depend on our maintenance of quality control, customer satisfaction with respect to pricing and the punctual availability and delivery of our products. If we fail to deliver the same quality of our products with the same punctuality and pricing which our customers have grown accustomed to, or in accordance with the terms of our sales agreements, we could damage our customer relations and market acceptance which will affect sales and our business in general. For example, as we advance and improve our methods of producing higher quality products such as Grade A and Grade B edible alcohol, it may become more difficult to maintain our quality standards at all times. Additionally, if we are ever forced to down-grade our edible alcohol, this could also affect the future improvement of our profit margins. If we experience deterioration in the performance or quality of any of our products, whether due to problems internally or externally, it could result in delays in delivery, cancellations of orders or customer complaints, loss of goodwill, diversion of the attention of our senior personnel and harm to our brand and reputation. Any and all of these results would have an adverse effect on our business, financial condition and results of operations.

| 11 |

Governmental authorities within the PRC periodically set corn prices and enact general industry policies that limit production capacity and use of raw materials. A significant increase in the market price of corn as a result of such governmental efforts would increase our cost of sales, and we may not be able to pass those increased costs on to our customers. Such increased costs and other policy initiatives could limit our growth and have a material adverse effect on our business, financial condition and results of operations.

The PRC government has the power to intervene in the price of important types of grain (including corn) under certain circumstances, such as when a material change occurs to the market supply and demand and/or the grain price fluctuates significantly, in order to protect the interests of farmers. In practice, the PRC government will periodically purchase a large amount of corn from farmers and set the price for the corn purchased by the government, resulting in effective guidance of the market price by the PRC government. This has a significant impact on the market price of corn for the following year, but does not constitute a legally mandated price for corn. A significant increase in the market price of corn as a result of such governmental efforts would increase our cost of sales, and we may not be able to pass those increased costs on to our customers. Such increased costs could have a material adverse effect on our business, financial condition and results of operations.

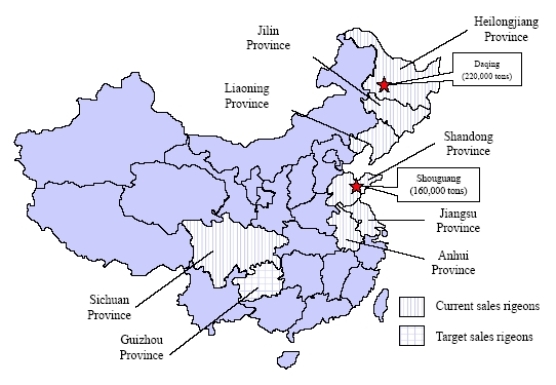

The PRC government requires all producers of edible alcohol to obtain production permits which set forth limitations on how much edible alcohol we can produce per annum. Our Shouguang facility has a government permit to produce 160,000 tons of edible alcohol per year and our Daqing facility has a government permit to process up to 1,000,000 tons of corn, which can produce approximately 330,000 tons of edible alcohol. If our permits are revoked for whatever reason, or if the PRC decides to revise its industry policies to our detriment, we could be forced to curtail or cease our operations.

Furthermore, in order to secure the supply of food and feed, PRC governmental entities set limitations on the use of certain raw materials. For instance, according to the 11th Five-Year Plan (2006-2010), the amount of corn used for deep-processing cannot exceed 26% of the total corn consumption as stated in the Guidance Opinion on Promoting of the Healthy Development of Corn Deep-Processing Industry announced by the PRC government. According to the 12th Five-Year Plan, the Chinese government will continue to impose strict control on the amount of corn used for deep-processing. Any further downward limitation may adversely affect our ability to obtain an adequate level of corn at favorable prices.

In addition, the Chinese government has ceased in principle approving applications for building new corn deep-processing capacity. Our growth could be limited if we fail to obtain government approval for new capacity or to expand through acquisitions in other geographical areas. In addition, we could face penalties and other enforcement actions if our production levels exceed our approved production levels. The realization of any of the foregoing risks could have a material adverse effect on our business, financial condition and results of operations.

Any interruption in our manufacturing operations or production and distribution processes could impair our financial performance and negatively affect our brand.

Our production operations involve the coordination of raw materials, internal production processes and external distribution processes. We may experience difficulties in coordinating the various aspects of our production processes, thereby causing downtime and delays. We produce and store almost all of our products, as well as conduct some of our development activities, at our Shouguang and Daqing facilities. We do not maintain back-up facilities, so we depend on these facilities for the continued operation of our business.

| 12 |

A delay or stoppage of production caused by adverse weather, natural disaster or other unanticipated catastrophic event, including, without limitation, power interruptions, water shortage, storms, fires, earthquakes, terrorist attacks and wars, could significantly impair our ability to produce our products and operate our business, as well as delay our research and development activities. Our facilities and certain equipment located in these facilities would be difficult to replace and could require substantial replacement lead-time. Catastrophic events may also destroy any inventory located in our facilities. The occurrence of such an event could materially and adversely affect our business. Any stoppage in production, even if temporary, or delay in delivery to our customers could severely affect our business or reputation. We currently do not have business interruption insurance to offset these potential losses and any interruption in our production operations or production and distribution processes could impair our financial performance and negatively affect our brand.

We have not obtained power generation permits for our coal-fired power-generating systems, which could result in the forfeiture of income and the imposition of fines.

A new permit system was established in 2005 requires all existing and new power-generating, dispatching and supplying companies to obtain permits from the State Electricity Regulatory Commission. The State Electricity Regulatory Commission has been in the process of implementing the new permit system. By the end of 2008, the State Electricity Regulatory Commission had issued 6,170 power-generating permits. We believe we are to date in compliance with the relevant permit regulations, which required all of our plants to apply for power generation permits no later than August 31, 2008. We have submitted applications for power generation permits for all our existing coal-fired power projects, but have not yet received the permits. The granting of a power generation permit for an existing power generation project is a time-consuming and complicated process, which may in some instances require retroactive application of existing laws and regulations to existing projects that were constructed many years ago. As a result, we may not be able to successfully obtain power generation permits for our coal-fired power-generating systems. A failure to obtain a power generation permit may have a material adverse effect on our business operations, including the forfeiture of income and the imposition of fines.

Interruptions with our coal-fired power-generating systems, whether planned or unexpected, may have an adverse effect on our business, financial condition and results of operations.

Our production facilities require a significant amount of electricity in order to operate at full capacity. Both our Shouguang and Daqing facilities were designed and built to be self-sufficient in power supply through the construction of their own coal-fired power-generating systems. We are also connected to the national power grid at both facilities as a backup measure in the event we experience unanticipated interruptions to our electricity generation and for when we carry out our annual full-scale inspection and maintenance program for our electricity supply systems (see “Business Overview - Our Supply of Electricity”). In addition, we are in the process of undertaking construction project approval procedures, environmental impact assessments and completion acceptance procedures for our Shouguang and Daqing power-generating systems. In the event that we fail to obtain approvals from competent government agencies for the construction of our power-generating systems, we may be required to shut down our power-generating systems and be subject to punishment. If the power-generating systems at our Shouguang facility or our Daqing facility experience unexpected stoppage due to mechanical failure or regulatory action, or when we schedule our annual inspection of our supply systems, we must negotiate with the government for the purchase of electricity to be supplied through the relevant grid until our power-generating systems become operational. During such negotiations, we could be forced to accept pricing terms which are not favorable to us. Furthermore, such negotiations could be time-consuming which could cause a diversion of resources and time of our senior management personnel. Furthermore, we cannot assure you that there will be no interruptions or shortages in the national or local grid electricity supply or that there will be sufficient electricity available to us to meet our needs. There have been shortages in electricity supply in various regions across China, especially during periods of severe winter weather and during the summer peak season. Therefore, if either of our production facilities were to experience any significant downtime, we would be unable to meet our production targets and our business would suffer. Any disruption at our facilities would have a material adverse effect on our business, financial condition and results of operations.

| 13 |

Transportation delays, including as a result of disruptions to infrastructure, could adversely affect our business, results of operations and financial condition.

Our business depends on the availability of rail, road and boat distribution infrastructure for the delivery of raw materials and for the delivery of our products to our customers. Any disruptions in this infrastructure network, whether caused by earthquakes, storms, other natural disasters or human error or malfeasance, could materially impact our business. Therefore, any unexpected delay in transportation of our raw materials or in the delivery of our products to our customers could result in significant disruption to our operations, including the closure of our facilities. Specifically, we do not have contractual rights or any other license to use the railways and rail station that transport our products from our Daqing facility. If for any reason we should lose the use of these facilities, we may not be able to find sufficient alternative methods of transport for products from our Daqing facility in a timely manner, or at all. We will also rely upon others to maintain rail lines and roads from our production facilities to national rail, road and shipping networks, and any failure on their part to maintain such transportation systems could impede the delivery of our raw materials to us and our products to our customers, impose additional costs on us or otherwise cause our business, results of operations and financial condition to suffer.

If we fail to continue to develop and introduce new products and technologies, our business, results of operations and financial condition could be materially adversely affected.

We intend to continue to develop new products and technologies to broaden our product line. The planned timing or introduction of new products and technologies is subject to risks and uncertainties. Actual timing may differ materially from original plans. Unexpected technical, operational, distribution or other problems could delay or prevent the introduction of one or more of our new products or technologies. Moreover, we cannot be sure that any of our new products or technologies will achieve widespread market acceptance or generate incremental revenue. If our efforts to develop, market and sell new products to the market and apply new technologies are not successful, our business, financial condition and results of operations could be materially adversely affected.

Our operations are subject to various risks associated with our use, handling, storage and disposal of hazardous materials, some of which are toxic and flammable. If we are found liable for contamination, injury to employees or others, or other harms related to our use, handling, storage and disposal of hazardous materials, our business, reputation, financial condition and results of operations may be adversely affected.

We use, handle, store and dispose of hazardous materials in our operations. Our wastewater may contain toxins and our edible alcohol and methane produced in our operations is flammable. See Item 4.B, “Information on the Company — Business Overview — Environmental Protection.” We cannot completely eliminate the risks of contamination, injury to employees or others, or other harms related to our use, handling, storage and disposal of hazardous material. Although we have not experienced incidents in the past, there can be no assurance that we will not experience fires, leakages and other accidents. In the event of future incidents, we could be liable for any damages that may result, including potentially significant monetary damages for any civil litigation or government proceedings related to a personal injury claim, as well as other fines, penalties and other consequences, including suspension or revocation of our licenses or permits or suspending production or ceasing operations at our manufacturing facilities, all of which would have a material adverse effect on our business, reputation, financial condition and results of operations. Furthermore, we currently do not carry any insurance coverage for potential liabilities relating to the release of hazardous materials.

Our use, production and disposal of hazardous materials subjects us to stringent environmental, health and safety regulations. Any actual or alleged violation of these regulations could result in significant regulatory actions, fines and other penalties, including suspending production or ceasing operations, substantial civil or criminal claims resulting in potentially significant monetary damages, adverse publicity and other negative consequences to our business.

| 14 |

Because we use, produce and dispose of hazardous materials and our production processes generate noise, wastewater, gaseous and other industrial wastes, we are required to comply with national and local environmental, health and safety regulations applicable to us. Except as disclosed in this annual report, we believe we have complied with all applicable environmental, health and safety procedures and measures. However, we cannot completely eliminate the environmental, health and safety risks associated with our use, production and disposal of hazardous materials and we may experience environmental, health and safety incidents at our facilities, including fires, leakages and other accidents, which could result in regulatory actions requiring us to take corrective actions and subject us to fines and other penalties. In some cases, we could be required to temporarily suspend production or cease operations while we perform corrective actions.

Our operations are subject to various risks associated with our use, handling, storage and disposal of hazardous materials, some of which are toxic and flammable. If we are found liable for contamination, injury to employees or others, or other harms related to our use, handling storage and disposal of hazardous materials, our business, reputation, financial condition and results of operations may be adversely affected. Except as described in this annual report, we believe we are currently in compliance with applicable environmental, health and safety regulations in all material aspects and have all necessary environmental, health and safety permits to operate our business as it is presently conducted. However, if more stringent regulations are adopted in the future, the costs of compliance with these new regulations could be substantial. If we fail to comply with present or future environmental, health and safety regulations, we may be subject to significant regulatory actions, fines and other penalties, including suspending production or ceasing operations, substantial civil or criminal claims resulting in potentially significant monetary damages, adverse publicity, and other negative consequences to our business, all of which could have a material adverse effect on our business, reputation, financial condition and results of operations.

Environmental compliance and remediation could result in substantially increased capital requirements and operating costs, which could adversely affect our business and results of operations.

We are subject to the PRC laws and regulations relating to the protection of the environment. These laws continue to evolve and are becoming increasingly stringent. The ultimate impact of complying with such laws and regulations is not always clearly known or determinable because regulations under some of these laws have not yet been promulgated or are undergoing revision. Our business and operating results could be materially and adversely affected if we were required to increase expenditures to comply with any new environmental regulations affecting our operations.

Our operations are subject to various risks associated with our use, handling, storage and disposal of edible alcohol, which is flammable. If we are found liable for contamination, injury to employees or others, or other harms related to our use, handling, storage and disposal of edible alcohol, our business, reputation, financial condition and results of operations may be adversely affected and our permits and licenses may be suspended or revoked by Chinese regulatory authorities.

| 15 |

Although we have designed and implemented procedures and measures to promote occupational health and safety, we cannot completely eliminate the risks of contamination, injury to employees or others, or other harms related to our use, handling, storage and disposal of edible alcohol. In the event of future incidents, we could be liable for any damages that may result, including potentially significant monetary damages for any civil litigation or government proceedings related to a personal injury claim, as well as other fines, penalties and other consequences, including suspension or revocation of our licenses or permits or suspending production or ceasing operations at our research and manufacturing facilities, all of which could have a material adverse effect on our business, reputation, financial condition and results of operations.

The expansion of our sales and marketing and distribution efforts in new provinces and regions may not be successful.

We plan to expand our sales and marketing and distribution efforts into provinces and regions beyond Shandong and Heilongjiang provinces in China, and have already commenced sales and marketing operations in Sichuan Province, Anhui Province, Jiangsu Province, Hebei Province, Jilin Province and Liaoning Province. However, our experience in the sales and marketing and distribution of our products in Shandong and Heilongjiang Provinces may not be applicable in other parts of China. We cannot assure you that we will be able to leverage such experience to expand into other provinces and regions. When we enter new markets, we may face intense competition from edible alcohol producers with established experience or presence in the geographical areas in which we plan to enter and from other edible alcohol producers with similar target customers. In addition, expansion of sales into new markets in new provinces will require the recruiting and training of a new sales force to market and sell our products in that region, the assimilation with the local business cultures of new regions which may be very different from the business cultures of Shandong and Heilongjiang provinces, and require a diversion of resources and time of our senior management personnel. If we fail to integrate effectively in new markets, our operating efficiency may be affected. Furthermore, because customers in new provinces may be far away from our production facilities, our profit margins may be lower because of increased costs in the transportation of our products. Demand for edible alcohol and government regulation may also be different in other provinces. Our failure to manage our planned expansion of sales into new provinces may have a material adverse effect on our business, financial condition and results of operations and we may not have the same degree of success in other provinces that we have had so far to date, or at all.

Our production activities are conducted and will continue to be conducted in concentrated locations. Damage to or disruptions at our production facilities could materially and adversely affect our business, financial condition and results of operations, especially since we do not have any business interruption insurance.

Our two operating production facilities are located in Shandong and Heilongjiang provinces, making our operations particularly vulnerable to natural and other disasters that may occur in those provinces. Operating hazards, natural disasters or other unanticipated or catastrophic events, including power interruptions, water shortages, storms, typhoons, fires, explosions, earthquakes, terrorist attacks, wars and labor disputes in and around these provinces could cause damage to or destroy our facilities or equipment therein. Any of these or similar events could significantly impair our ability to operate our business, as well as delay our research and development activities and commercial production. Our facilities and equipment are expensive and potentially difficult and time-consuming to repair or replace. Catastrophic events may also result in damage to or the destruction of inventory located in our production facilities. In addition, we do not carry any business interruption or other insurance that would compensate us in the event of a loss of this type. The occurrence of such an event could result in substantial costs and diversion of resources, and our business, financial condition and results of operations may be materially and adversely affected.

| 16 |

We rely on our relationships with customers with whom we have sale contracts, the termination of which could cause us to experience short-term or permanent losses that would have an adverse effect on our financial condition, results of operations and prospects.

Although during the years ended December 31, 2009, 2010 and 2011, there was no single customer from which we generated more than 10% of total sales for any of our products, we do rely on our relationships with certain customers, mainly baijiu distilleries, with which we have entered into 12- to 36-month sales contracts for the sale of an aggregate 340,000 tons, or pre-sales contracts, worth a total of approximately 90% of our total edible alcohol production capacity of 380,000 tons in 2012. Additionally, during the years ended December 31, 2009, 2010 and 2011, aggregate sales to our five largest customers represented 23.4%, 16.6% and 17.4% of our sales, respectively. If our relationships with our top customers terminate, or if our relationships with those customers with which we entered into sales contracts terminate, or if such customers decide not to abide by the sales agreements and fail to purchase our products thereunder, or if we are unable to renew our agreements to supply our products with such customers in the future in a satisfactory manner, if at all, then we would be forced to identify and negotiate with new customers in order to replace the lost volume of sales. If we find ourselves having to replace these customers, this may require a diversion of resources and time of our senior management personnel as well as a short-term reduction in our revenues, or we may not be successful in identifying and negotiating with new customers at all, all of which would have a material adverse effect on our financial condition, our results of operations and prospects.

Our business is capital intensive and our growth strategy may require additional capital, which may not be available on favorable terms or at all.

We may require additional cash resources due to changed business conditions, implementation of our strategy to expand our manufacturing capacity or potential investments or acquisitions we may pursue. We may need to sell debt securities or additional equity securities, or obtain additional credit facilities from banks in the PRC in order to implement our growth strategy or to otherwise meet our capital needs. The sale of additional equity securities could result in dilution of your holdings. The incurrence of indebtedness would result in increased debt service obligations and could require us to agree to operating and financial covenants that would restrict our operations. Financing may not be available in amounts or on terms acceptable to us, if at all. Any failure by us to raise additional funds on terms favorable to us, or at all, could limit our ability to expand our business operations and could harm our overall business prospects.

We may undertake acquisitions, which may distract our management, may not result in the benefits we had anticipated and may have unknown risks and liabilities associated with them.

Our growth strategy may involve the acquisition of new businesses or the creation of strategic alliances in the edible alcohol production business. These acquisitions could require that our management manage new business relationships, manage new facilities and attract new customers. Furthermore, acquisitions may require significant attention from our management, and the diversion of our management’s attention and resources could have a material adverse effect on our ability to manage our business. Future acquisitions may also expose us to potential risks, including risks associated with (1) the integration of new operations, services and personnel, (2) unforeseen or hidden liabilities, (3) the diversion of resources from our existing businesses, (4) our inability to generate sufficient revenue to offset the costs of acquisitions and (5) potential loss of, or harm to, relationships with employees or customers, any of which may have a material adverse effect on our ability to manage our business. We may also experience some or all of these risks with respect to our recently acquired Weifang Great Chemical Inc., or WGC, and Daqing Borun businesses. For example, we cannot ensure that WGC and Daqing Borun have obtained the necessary construction project permits, fully completed environmental impact assessment procedures and obtained all the licenses required for their conduct of business before we acquired them. Failure of Daqing Borun or WGC to comply with the aforementioned requirements may cause us to bear the liabilities provided by relevant laws and regulations.

| 17 |

We will continue to incur increased costs as a result of being a public company, which will adversely impact our results of operations.

We became a public company following the completion of our initial public offering in June 2010 and have incurred, and expect to continue to incur, significant legal, accounting and other expenses that we did not incur as a private company. Moreover, the Sarbanes-Oxley Act of 2002, the Dodd-Frank Wall Street Reform and Consumer Protection Act enacted in July 2010, as well as rules subsequently implemented by the U.S. Securities and Exchange Commission, or the SEC, and the New York Stock Exchange, or the NYSE, have imposed additional requirements on corporate governance practices of public companies. We expect these rules and regulations to increase our legal and financial compliance costs and to make some corporate activities more time-consuming and costly. For example, as a result of becoming a public company, we have added independent directors to our board and adopted policies regarding internal controls and disclosure controls and procedures. See also the risk factor entitled, “As a company incorporated in the Cayman Islands, we may adopt certain home country practices in relation to corporate governance matters. These practices may afford less protection to shareholders than they would enjoy if we complied fully with the NYSE corporate governance listing standards.”

In addition, we incur costs associated with our public company reporting requirements. It may also be difficult for us to attract and retain qualified persons to serve on our board of directors due to increased risks of liability to our directors under the rules and regulations. We are currently evaluating and monitoring developments with respect to these rules and regulations, and we cannot predict or estimate with any degree of certainty the amount or timing of additional costs we may incur.

Although our results of operations, cash flows and financial condition reflected in our consolidated financial statements include all of the expenses allocable to our business, because of the additional administrative and financial obligations associated with operating as a publicly traded company, they may not be indicative of the results of operations that we would have achieved had we operated as a public entity for all periods presented or of future results that we may achieve as a publicly traded company with our current holding company structure. Such variations may be material to our business.

We may have difficulty establishing adequate management, legal and financial controls in the PRC, and the failure to establish such controls could have a material adverse effect on our business and the price of our ADSs.

The PRC has only recently begun to adopt the management, legal and financial reporting concepts and practices with which investors in the United States are familiar. We may have difficulty in hiring and retaining employees in China who have the experience necessary to implement the kind of management, legal and financial controls that are expected of a United States public company. If we cannot establish such controls, or if such deficiencies persist, we may experience difficulty in collecting financial data and preparing financial statements, books of account and corporate records and instituting business practices that meet U.S. standards. The failure to establish such controls could also result in significant deficiencies or material weaknesses in our internal controls, which could impact the reliability of our financial statements. Any such deficiencies, weaknesses or lack of compliance could have a materially adverse effect on our business and the public announcement of such deficiencies could adversely impact the price of our ADSs.

| 18 |

We may be exposed to potential risks relating to our internal control over financial reporting.

We are subject to the Sarbanes-Oxley Act of 2002. As directed by Section 404 of the Sarbanes-Oxley Act of 2002, the SEC adopted rules requiring public companies to include a report of management on our internal controls over financial reporting in their annual reports. In addition, if we become an accelerated filer or a large accelerated filer for purposes of a future annual report, we will be required to include in such annual report a report of our independent registered public accounting firm that attests to and reports on management’s assessment of the effectiveness of our internal controls over financial reporting as well as the operating effectiveness of our internal controls. Our management may conclude that our internal controls over our financial reporting are not effective. Even if our management concludes that our internal controls over financial reporting are effective, our independent registered public accounting firm may, if we are required to include an attestation report from them, still decline to attest to our management’s assessment or may issue a report that is qualified if it is not satisfied with our controls or the level at which our controls are documented, designed, operated or reviewed, or if it interprets the relevant requirements differently from us.

In connection with the audit of our financial statements as of and for the years ended December 31 2007, 2008 and 2009 our auditors identified four “reportable conditions” as that term is defined under standards established by the Public Company Accounting Oversight Board (“PCAOB”), in our internal accounting controls. These reportable conditions, which do not qualify as material weakness, related to our lack of a computerized financial accounting information system to record and process our financial transactions, a need to improve the timely recording and processing of our business transactions, lack of formal documentation to document and validate that management has performed periodic financial analysis and failure to set up and carry out the budget and management control in the overall operation systematically. We have made improvements in light of the above reportable conditions by deploying a computerized financial accounting system to do the book-keeping, recording and processing business transactions in a timely manner, setting up procedures to make annual and monthly budget and perform periodic financial analysis.

We can provide no assurance that we will continue to be in compliance with all of the requirements imposed by Section 404 or that we will, if required, receive a positive attestation from our independent auditors. In the event we identify significant deficiencies or material weaknesses in our internal controls that we cannot remediate in a timely manner or we are unable, if required, to receive a positive attestation from our independent auditors with respect to our internal controls, investors and others may lose confidence in the reliability of our financial statements. Any of these possible outcomes could result in an adverse reaction in the financial marketplace due to a loss of investor confidence in the reliability of our reporting processes, which could adversely affect the trading price of the ADSs.

Unauthorized use of our Borun wet process patent of invention by third parties and the expenses incurred in protecting such patent may adversely affect our business.

We regard our Borun wet process patent of invention and our “Borun” trademark as important to our business. In January 2012 the State Intellectual Property Office awarded a patent to us for the Borun wet process, our proprietary manufacturing method. We believe we are the only corn-based edible alcohol producer in China using the Borun wet process and the market recognizes our brand name products. Infringements of relevant intellectual property rights may reduce our revenues and harm our reputation. We rely on intellectual property laws and contractual arrangements with our key employees and certain of our customers and others to protect our intellectual property rights. Policing unauthorized use of intellectual property is difficult and expensive, as are the steps necessary to prevent the misappropriation or infringement of our technology or trademark. Despite our precautions, it may be possible for third parties to obtain and use our Borun wet process method without authorization or sell their products under our “Borun” trademark. The validity, enforceability and scope of protection of intellectual property in many industries in China are uncertain and still evolving and may not protect intellectual property rights to the same extent as do the laws and enforcement procedures in the United States. Moreover, we may not prevail in any litigation that we undertake to enforce our intellectual property rights, and such litigation could result in substantial costs and diversion of our management resources. Our failure to adequately maintain and protect our intellectual property rights could lead to the loss of a competitive advantage or otherwise impair our ability to operate our business.

| 19 |

Our business, financial condition and results of operations, as well as our ability to obtain financing, may be adversely affected by a downturn in the global or Chinese economy.

The global financial markets have experienced significant disruptions since 2008 and the effect of the crisis has persisted through 2009 and 2010, and to a lesser extent in 2011. China’s economy has also faced challenges. To the extent that there have been improvements in some areas, it is uncertain whether such recovery is sustainable. The corn-based edible alcohol industry may be sensitive to economic downturns, and the macroeconomic environment in China may affect our business and prospects. A prolonged slowdown in China’s economy may lead to a reduced level of corn-based edible alcohol purchases which could materially and adversely affect our business, financial condition and results of operations.

Moreover, a slowdown in the global or China’s economy or the recurrence of any financial disruptions may have a material and adverse impact on financing available to us. The weakness in the economy could erode investors’ confidence, which constitutes the basis of the credit markets. The recent financial turmoil affecting the financial markets and banking system may significantly restrict our ability to obtain financing in the capital markets or from financial institutions on commercially reasonable terms, or at all. Although we are uncertain about the extent to which the recent global financial and economic crisis and slowdown of China’s economy may impact our business in the short term and long term, there is a risk that our business, results of operations and prospects will be materially and adversely affected by any ongoing global economic downturn or slowdown in China’s economy.

We are dependent upon our existing management, and our business may be severely disrupted if we lose their services.

Our future performance depends substantially on the continued services of our executive officers, most notably our Chief Executive Officer, Mr. Jinmiao Wang. If one or more of our executive officers are unable or unwilling to continue in their present positions, we might not be able to replace them easily or at all. In addition, we do not have any key person insurance on the lives of such individuals and the loss of any of their services could materially and adversely affect us.

If any of our executive officers joins a competitor or forms a competing company, we may lose know-how, key professionals and staff members as well as customers. These executive officers could develop products that could compete with and take market share away from us. Each of our executive officers has entered into an employment agreement with us, each of which contain non-competition provisions. However, if any dispute arises between our executive officers and us, these non-competition provisions may not be enforceable in China. If any of the foregoing were to happen, our competitive position and business prospects may be materially and adversely affected.

One of our shareholders has significant control over the outcome of our shareholder votes.

One shareholder, King River Holding Limited, or King River, beneficially owns 56.4% of our outstanding equity interests as of the date of this annual report. Accordingly, King River has significant control over the outcome of any corporate transaction or other matter submitted to our shareholders for approval, including the election of directors, mergers, consolidations and the sale of all or substantially all of our assets. This concentration of ownership in our ordinary shares by King River will limit your ability to influence corporate matters and may have the effect of delaying or preventing a third party from acquiring control over us.

Covenants in certain PRC loan agreements entered into by Shandong Borun Industrial Co., Ltd, or Shandong Borun, and Daqing Borun restrict our ability to engage in or enter into a variety of transactions, which may cause disruption in our business operations and have a material adverse effect on our business operations.

Shandong Borun and Daqing Borun have entered into PRC loan agreements with banks in the PRC which contain various covenants that may limit our discretion in operating the business of our operating subsidiaries.

Our lenders have rights that include the following:

| · | restricting us from using the loan for a purpose other than the one stated in the agreement; |

| · | restricting us during the term of the loan from undertaking any shareholding change or restructuring without obtaining prior approval of the lender; |