SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

☑ |

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended June 30, 2021

or

|

|

☐ |

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Transition Period From ________ to ________. |

Commission File number 001-34839

|

Electromed, Inc. |

|

(Exact Name of Registrant as Specified in its Charter) |

|

Minnesota |

41-1732920 |

|

(State or other jurisdiction of |

(IRS Employer |

|

incorporation or organization) |

Identification No.) |

500 Sixth Avenue NW, New Prague, MN 56071

(Address of principal executive offices, including zip code)

|

(952) 758-9299 |

|

(Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

Common Stock, par value |

|

ELMD |

|

NYSE American |

Securities registered pursuant to Section 12(g) of the Act: None

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☑ |

|

|

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑ |

|

|

|

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐ |

|

|

|

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐ |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer ☐ |

Accelerated filer ☐ |

|

|

|

|

Non-accelerated filer ☐ |

Smaller reporting company ☑

Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Ac t (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

The aggregate market value of the common stock held by non-affiliates of the registrant as of December 31, 2020 was approximately $70,780,000 based upon the closing price of the registrant’s common stock, as reported on the NYSE American, on such date.

There were 8,559,109 shares of the registrant’s common stock outstanding as of August 20, 2021.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Definitive Proxy Statement for the registrant’s Fiscal 2021 Annual Meeting of Shareholders, to be filed within 120 days of June 30, 2021, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Electromed, Inc.

Index to Annual Report on Form 10-K

i

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

Statements contained in this Annual Report on Form 10-K that are not statements of historical fact should be considered forward-looking statements within the meaning of the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements include, but are not limited to, statements regarding: the expected impact of the COVID-19 pandemic on our business; our business strategy, including our intended level of investment in research and development (“R&D”) and marketing activities; our expectations with respect to earnings, gross margins and sales growth, industry relationships, marketing strategies and international sales; estimated sizes of markets into which our products are or may be sold; our business strengths and competitive advantages; our ability to grow additional sales distribution channels; our intent to retain any earnings for use in operations rather than paying dividends; our expectation that our products will continue to qualify for reimbursement and payment under government and private insurance programs; our intellectual property plans and practices; the expected impact of applicable regulations on our business; our beliefs about our manufacturing processes; our expectations and beliefs with respect to our employees and our relationships with them; our belief that our current facilities are adequate to support our growth plans; our expectations with respect to ongoing compliance with the terms of our credit facility; our expectations regarding the ongoing availability of credit and our ability to renew our line of credit; enhancements to our products and services; expected excise tax exemption for the SmartVest Airway Clearance System; and our anticipated revenues, expenses, capital requirements and liquidity. Words such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “goal,” “intend,” “may,” “ongoing,” “plan,” “potential,” “project,” “should,” “target,” “will,” “would,” and similar expressions, including the negative of these terms, are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. Although we believe these forward-looking statements are reasonable, they involve risks and uncertainties that may cause actual results to differ materially from those projected by such statements. Such statements involve known and unknown risks, uncertainties and other factors that may cause our actual results or our industry’s actual results, levels of activity, performance or achievements to be materially different from the information expressed or implied by the forward-looking statements.

Factors that could cause actual results to differ from those discussed in the forward-looking statements include, but are not limited to:

|

|

● |

the duration, extent and severity of the COVID-19 pandemic, including its effects on our business, operations and employees as well as its impact on our customers and distribution channels and on economies and markets more generally; |

|

|

● |

component or raw material shortages or changes to lead times; |

|

|

● |

the competitive nature of our market; |

|

|

● |

changes to Medicare, Medicaid or private insurance reimbursement policies; |

|

|

● |

changes to state and federal health care laws; |

|

|

● |

changes affecting the medical device industry; |

|

|

● |

our ability to develop new sales channels for our products such as the home care distributor channel; |

|

|

● |

our need to maintain regulatory compliance and to gain future regulatory approvals and clearances; |

|

|

● |

new drug or pharmaceutical discoveries; |

|

|

● |

general economic and business conditions; |

|

|

● |

our ability to renew our line of credit or obtain additional credit as necessary; |

|

|

● |

our ability to protect and expand our intellectual property portfolio; |

|

|

● |

the risks associated with cyberattacks, data breaches, computer viruses and other similar security threats; and |

|

|

● |

the risks associated with expansion into international markets. |

ii

This list of factors is not exhaustive, however, and these or other factors, many of which are outside of our control, could have a material adverse effect on us and our results of operations. Therefore, you should consider these risk factors with caution and form your own critical and independent conclusions about the likely effects of these risk factors on our future performance. Forward-looking statements speak only as of the date on which the statements are made, and we undertake no obligation to update any forward-looking statement for any reason, even if new information becomes available or other events occur in the future. You should carefully review the disclosures in this and other documents we file from time to time with the Securities and Exchange Commission (the “SEC”), including our Quarterly Reports on Form 10-Q and Current Reports on Form 8-K. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements set forth herein.

iii

Overview

Electromed, Inc. (“we,” “our,” “us,” “Electromed” or the “Company”) develops, manufactures, markets and sells innovative products that provide airway clearance therapy, including the SmartVest® Airway Clearance System (“SmartVest System”) and related products, to patients with compromised pulmonary function with a commitment to excellence and compassionate service. Our goal is to make High Frequency Chest Wall Oscillation (“HFCWO”) treatments as effective, convenient, and comfortable as possible, so our patients can breathe easier and live better with improved respiratory function and fewer exacerbations.

We employ a direct-to-patient and provider model, through which we obtain patient referrals from clinicians, manage insurance claims on behalf of our patients, and deliver the SmartVest System to patients, training them on proper use in their homes. This model allows us to directly approach patients and clinicians, whereby we disintermediate the traditional durable medical equipment (“DME”) channel and capture both the manufacturer and distributor margins. We also sell our products in the acute care setting for patients in a post-surgical or intensive care unit, or who were admitted for a lung infection brought on by compromised airway clearance. Electromed was incorporated in Minnesota in 1992. Our common stock is listed on the NYSE American under the ticker symbol “ELMD.”

The SmartVest System features a programmable air pulse generator, a therapy garment worn over the upper body and a connecting hose, which together provide safe, comfortable, and effective airway clearance therapy. The SmartVest System generates HFCWO, an airway clearance therapy. One factor of respiratory health is the ability to clear secretions from airways. Impaired airway clearance, when mucus cannot be expectorated, may result in labored breathing and/or inflammatory and immune systems boosting mucus production that invites bacteria trapped in stagnant secretions to cause infections. Studies show that HFCWO therapy is as effective an airway clearance method for patients who have compromised pulmonary function as traditional chest physical therapy (“CPT”) administered by a respiratory therapist.1 However, HFCWO can be self-administered, relieving a caregiver of participation in the therapy, and eliminating the attendant cost of an in-home care provider. We believe that HFCWO treatments are cost-effective primarily because they reduce a patient’s risk of respiratory infections and other secondary complications that are associated with impaired airway clearance and often result in costly hospital visits and repeated antibiotic use.

The SmartVest System is designed for patient comfort and ease of use which promotes adherence to prescribed treatment schedules, leading to improved airway clearance, patient outcomes and quality of life, and a reduction in healthcare utilization. We offer a broad range of garments, referred to as vests and wraps, in sizes for children and adults that allow for tailored fit. User-friendly controls allow patients to administer their daily therapy with minimal or no assistance. Our direct product support services provide patient and clinician education, training, and follow-up to ensure that the product is integrated into each patient’s daily treatment regimen. Additionally, our reimbursement department assures we are working on behalf of the patient by processing their physician paperwork, providing clinical support and billing the applicable insurance provider. We believe that the advantages of the SmartVest System and the Company’s customer services to the patient include:

|

|

● |

improved quality of life; |

|

|

● |

reduction in healthcare utilization; |

|

|

● |

independence from a dedicated caregiver; |

|

|

● |

consistent treatments at home; |

|

|

● |

improved comfort during therapy; and |

|

|

● |

eligibility for reimbursement by private insurance, federal or state government programs or combinations of the foregoing. |

1Nicolini A, et al. Effectiveness of treatment with high-frequency chest wall oscillation in patients with bronchiectasis. BMC Pulmonary Medicine. 2013;13(21).

1

Our Products

Since 2000, we have marketed the SmartVest System and its predecessor products to patients suffering from bronchiectasis, cystic fibrosis, and neuromuscular conditions such as cerebral palsy and amyotrophic lateral sclerosis (“ALS”). Our products are sold into the home health care market and the acute care setting for patients in a post-surgical or intensive care unit, or who were admitted for a lung infection brought on by compromised airway clearance. Accordingly, our sales points of contact include adult pulmonology clinics, cystic fibrosis centers, neuromuscular clinics and hospitals.

We have received clearance from the U.S. Food and Drug Administration (“FDA”) to market the SmartVest System to promote airway clearance and improve bronchial drainage. In addition, Electromed is certified to apply the Conformité Européenne (“European Conformity” or “CE”) marking for HFCWO device sales in all European Union member countries and approved for HFCWO device sales in other, select international countries. The SmartVest System is available only with a physician’s prescription.

The SmartVest System is currently available in one model – SQL® – which is sold into home care and hospital markets. As previously announced, we discontinued new patient and hospital market shipments of the SmartVest SV2100 model of the SmartVest System on July 1, 2021. We will continue to support and service the SmartVest SV2100 model pursuant to the applicable product warranty.

As part of our growth strategies, we periodically evaluate opportunities involving products and services, especially those that may provide value to the respiratory homecare and institutional market. To that end, we made meaningful progress in the development for our next generation SmartVest System during our fiscal year ended June 30, 2021 (“fiscal 2021”) and estimate launching such device and completing the corresponding FDA 510(k) clearance process in the first half of our fiscal year ending June 30, 2023 (“fiscal 2023”).

The SmartVest SQL System

The SmartVest SQL System consists of an inflatable therapy garment, a programmable air pulse generator and a patented single-hose that delivers air pulses from the generator to the garment. The SmartVest SQL is designed for maximum comfort and lifestyle convenience, so patients can readily fit therapy into their daily routines. The SmartVest SQL was designed to be significantly smaller, quieter, and lighter than its predecessor, and offers features that make it easier to use and enable greater patient freedom.

|

|

● |

Patented single-hose design: A single-hose delivers oscillations to the SmartVest garment, which we believe provides therapy in a more comfortable and unobtrusive manner than a two-hose system. Oscillations are delivered evenly from the base of the SmartVest garment, extending the forces upward and inward in strong but smooth cycles surrounding the chest. |

|

|

● |

Open system design with active inflate – active deflate: The active inflate – active deflate mechanism of the SmartVest System provides patients a more comfortable treatment experience by allowing them to take deep breaths and breathe more easily without feeling restricted. |

|

|

● |

Soft-fabric garment is lightweight and comfortable: The SmartVest garment is lightweight and designed to resemble an article of clothing. Quick fit Velcro®-like closures allow for a secure, comfortable fit without bulky straps and buckles. The simple design creates a broad size adjustment range to ensure a properly tailored fit to accommodate pediatric and adult patients. |

|

|

● |

Patented Soft Start® and 360° garment oscillation coverage:Soft Start gently fills the garment to acclimate the patient to therapy. All SmartVest garments provide 360° oscillation coverage, which delivers simultaneous treatment to all lobes of the lungs. |

|

|

● |

Smaller, quieter and lighter:The SmartVest SQL System is 25% smaller, 5db quieter and 30% lighter than the SmartVest SV2100 System. The SmartVest SQL is the lightest and overall quietest HFCWO generator on the market, weighing less than 16 pounds, making it easier for patients to use and integrate HFCWO therapy into their daily lives. |

2

|

|

● |

Programmable generator with user-friendly device operation: The SmartVest SQL features multiple operating modes, including ramp, and options for saving, locking and restoring protocols. Further, an enhanced pause feature allows the physician to program dedicated times for the patient to clear secretions. |

SmartVest Connect

In June 2017, we launched the SmartVest SQL with SmartVest Connect® wireless technology, a personalized HFCWO therapy management portal for patients with compromised pulmonary function. In March 2020, we launched the SmartVest Connect app for both the iOS and Android operating systems. The SmartVest Connect app securely connects to the SmartVest SQL System through Bluetooth™ technology. This interface allows patients and healthcare teams to track therapy in real-time and collaborate on care decisions to improve therapy adherence and patient outcomes. SmartVest Connect is available to pediatric and cystic fibrosis patients, and targeted adult pulmonary clinics using a Bluetooth-enabled SmartVest SQL System.

Other Products

We market the Single Patient Use (“SPU”) SmartVest and SmartVest Wrap® to health care providers in the acute care setting. Hospitals issue the SPU SmartVest or SmartVest Wrap to an individual patient for managing airway clearance. Both SPU products provide full coverage oscillation and facilitate continuity of care because they introduce the patient to our product and may encourage use of the SmartVest System for home care, which can be provided to patients with a chronic condition upon discharge.

Our Market

We estimate the total served U.S. market for HFCWO in 2019 was between approximately $220 million to $240 million, based on independent third-party market research. We believe the market for HFCWO is continuing to expand due to an aging population, higher incidence of chronic lung disease, and growing awareness by physicians of diseases and conditions for which patients can benefit from using HFCWO therapy, and treatments moving to lower cost home care settings. Indications for when HFCWO may be prescribed are not specific to any one disease. A physician may elect to prescribe HFCWO when he or she believes the patient will benefit from improved airway clearance and external chest manipulation is the treatment of choice to enhance mucus transport and improve bronchial drainage.

The SmartVest System is primarily prescribed for patients with bronchiectasis, cystic fibrosis, and neuromuscular conditions such as cerebral palsy and ALS. We believe that bronchiectasis represents the fastest growing diagnostic category and greatest potential for HFCWO growth in the United States. Bronchiectasis is an irreversible, chronic lung condition characterized by enlarged and permanently damaged bronchi. The condition is associated with recurrent lower respiratory infections, inflammation, reduction in pulmonary function, impaired respiratory secretion clearance, increased hospitalizations and medication use, and increased morbidity and mortality.

We are driven to make life’s important moments possible, one breath at a time, by leading the HFCWO therapy market in clinical evidence that supports the therapeutic imperative of clearing excess mucus from the lungs. Electromed is the only HFCWO therapy company with multiple published clinical outcome studies demonstrating a significant improvement in quality of life and reduction in exacerbation rates, hospitalizations, emergency department visits, and antibiotic prescriptions in bronchiectasis patients using the SmartVest System.2-5 Leading in clinical evidence to support the SmartVest System as a treatment for bronchiectasis patients will remain a focus for us in our fiscal year ending June 30, 2022 (“fiscal 2022”), with two clinical studies currently enrolling. The first such clinical study is a prospective, multi-center bronchiectasis outcomes study utilizing SmartVest therapy, and the second is a post surveillance study with chronic obstructive pulmonary disease (“COPD”) and bronchiectasis patients prescribed SmartVest utilizing quality of life questionnaires to measure outcomes prior to therapy and at two intervals following initiation of the therapy.

We believe that bronchiectasis is under recognized and underdiagnosed but is experiencing a surge in clinical interest and awareness, including the relationship to COPD, commonly referred to as bronchiectasis COPD overlap syndrome. The overlap of bronchiectasis and COPD increases exacerbations and hospitalizations, reduces pulmonary function, and increases mortality. Several recent studies have estimated prevalence of bronchiectasis, which we believe are helpful for estimating a range of the overall market size.

3

|

|

● |

Aksamit (2017) found 20% (n=350) of patients with bronchiectasis enrolled in the U.S. Bronchiectasis Research Registry (“BRR”) between 2008 and 2014 also had COPD and 29% (n=515) also had asthma.6 Other studies have found that the overlap between bronchiectasis and COPD is observed in 27% to 57% of patients with COPD. 7–9 |

|

|

● |

Chalmers (2017) found that prevalence of bronchiectasis in patients with COPD ranged from a low of 4% to as high as 69% with mean prevalence of 54%. In many studies in patients with COPD, the presence of bronchiectasis was associated with reduced lung function, greater sputum production, more frequent exacerbations and increased mortality versus those with COPD alone.10 |

|

|

● |

Henkle (2018) confirmed a high prevalence of bronchiectasis in the United States, identifying over 600,000 unique patients with at least one bronchiectasis claim (ICD-9 claims 494.0 or 494.1). The study also observed that patients with dual diagnosis of bronchiectasis and COPD were in poorer health, with more office visits, more inpatient admissions and more acute respiratory infections.11 |

|

|

● |

Seitz (2012) estimated that 190,000 unique cases of bronchiectasis were diagnosed in Medicare patients in 2007 and bronchiectasis prevalence increased 8.7% annually between 2000 and 2007.12 Based on historic growth in prevalence and assuming a constant growth rate, the estimated number of bronchiectasis diagnoses in Medicare patients in 2019 exceeded 515,000. |

|

|

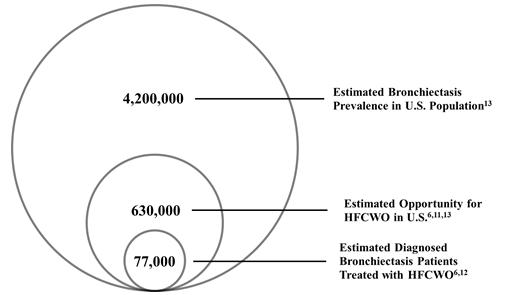

● |

Weycker (2017) projected 4.2 million adults in the United States over the age of 40 may have bronchiectasis, suggesting there is a large pool of patients with undiagnosed disease.13 |

These studies indicate a wide range of potential prevalence of bronchiectasis patients in the United States. We also believe that it is difficult to estimate from these studies which patients will need or benefit from HFCWO. The U.S. BRR indicated 15% of the patients included in the registry were prescribed HFCWO as part of their treatment plan. Using that study data, we estimate that, within the diagnosed Medicare population of 515,000, approximately 15% or 77,000 have been prescribed HFCWO. We believe that bronchiectasis is underdiagnosed in the U.S. based on clinical study evidence. We also believe that HFCWO is under prescribed for bronchiectasis patients. By applying approximately 15% HFCWO penetration of diagnosed Medicare patients to the Weycker clinical study cited above to the estimated 4.2 million prevalence of bronchiectasis in the U.S., we derived that the HFCWO opportunity may be 630,000 forecasted units (see Figure 1 below).

Estimated HFCWO Market Opportunity - Bronchiectasis Patients (U.S.) – Figure 1

The heightened awareness of bronchiectasis speaks to the growing body of clinical evidence supporting treatments to improve symptoms and manage disease progression. In 2019, an observational comparative retrospective cohort study published in BMC Pulmonary Medicine evaluated the efficacy of a treatment algorithm in 65 patients with radiographic and symptom confirmed bronchiectasis, centered on initiation of HFCWO therapy with the SmartVest System.5 Patients were treated per the algorithm if they reported greater than two exacerbations in the previous year and symptoms, including chronic cough, sputum production, or dyspnea. Results show that at one-year: exacerbations requiring hospitalization and antibiotic use were significantly reduced and mean-forced expiratory volume 1 remained stable post enrollment, suggesting early initiation of HFCWO therapy may slow the otherwise normal progression of the disease.

2Sievert C, et al. Using High Frequency Chest Wall Oscillation in a Bronchiectasis Patient Population: An Outcomes-Based Case Review. Respiratory Therapy Journal. 2016;11(4): 34–38.

3Sievert C, et al. Cost-Effective Analysis of Using High Frequency Chest Wall Oscillation (HFCWO) in Patients with Non-Cystic Fibrosis Bronchiectasis. Respiratory Therapy Journal. 2017;12(1): 45–49.

4Sievert C, et al. Incidence of Bronchiectasis-Related Exacerbation Rates After High Frequency Chest Wall Oscillation (HFCWO) Treatment — A Longitudinal Outcome-Based Study. Respiratory Therapy Journal. 2018;13(2): 38–41.

5Powner J, et al. Employment of an algorithm of care including chest physiotherapy results in reduced hospitalizations and stability of lung function in bronchiectasis. BMC Pulmonary Medicine. 2019;19(82).

6Aksamit T, et al. Bronchiectasis Research Registry C. Adult Patients With Bronchiectasis: A First Look at the US Bronchiectasis Research Registry. Chest. 2017;151:982-92.

7Patel I.S., et al. Bronchiectasis, exacerbation indices, and inflammation in chronic obstructive pulmonary disease. Am J Respir Crit Care Med. 2004;170:400-7.

8O’Brien C, et al. Physiological and radiological characterization of patients diagnosed with chronic obstructive pulmonary disease in primary care. Thorax. 2000;55:635-42.

9Bafadhel M, et al. The role of CT scanning in multidimensional phenotyping of COPD. Chest. 2011;140:634-42.

10Chalmers J. and Sethi S. Raising awareness of bronchiectasis in primary care: overview of diagnosis and management strategies in adults. NPJ Prim Care Respir Med. 2017;27:18.

11Henkle E, et al. Characteristics and Health-care Utilization History of Patients with Bronchiectasis in US Medicare Enrollees With Prescription Drug Plans, 2006 to 2014. Chest. 2018;154(6), 1311–1320.

12Seitz A, et al. Trends in Bronchiectasis Among Medicare Beneficiaries in the United States, 2000 to 2007. Chest. 2012;142(2), 432–439.

13Weycker D, Hansen G, Seifer F. Prevalence and incidence of noncystic fibrosis bronchiectasis among US adults in 2013. Chronic Respiratory Disease. 2017; 14(4):377-384.

4

Marketing, Sales and Distribution

Our sales and marketing efforts are focused on building market awareness and acceptance of our products and services with physicians, clinicians, patients, and third-party payers. Because the sale of the SmartVest System requires a physician’s prescription, we market to physicians and health care providers as well as directly to patients. The majority of our revenue comes from domestic home care sales through a physician referral model. We have established our own domestic sales force, which we believe is able to provide superior education, support and training to our customers. Our direct U.S. sales force works with physicians and clinicians, primarily pulmonologists, in defined territories to help them understand our products and services and the value they provide to their respective patients. As of June 30, 2021, we had 46 field sales employees, including five regional sales managers, 37 clinical area managers (“CAMs”) and two clinical educators. We also have developed a network of approximately 250 respiratory therapists and health care professionals across the U.S. to assist with in-home SmartVest System patient training on a non-exclusive, independent contractor basis. Virtual patient trainings are also available upon patient request. These independent contractors are credentialed by the National Board for Respiratory Care as either Certified Respiratory Therapists or Registered Respiratory Therapists.

|

|

● |

Of the $35.1 million of our revenue derived from the U.S. in fiscal 2021, approximately 94% represented home care and 4% represented hospital sales. Due to readmission penalties associated with the Patient Protection and Affordable Care Act, as reconciled by the Health Care and Education Reconciliation Act of 2010 (collectively the “PPACA”), for certain diseases and conditions including COPD and pneumonia, we believe opportunities for further growth exist for HFCWO therapy because the device used by a patient in a hospital may influence the choice of device prescribed at discharge. We expect to achieve future sales, earnings, and overall market share growth with increasing home care referrals by educating and building awareness of diseases and conditions that may benefit from HFCWO, like bronchiectasis, with physicians and patients and the value of the SmartVest System’s differentiated features and benefits. We believe that service to our providers and patients is an additional key component of achieving future sales. Providers seek companies that are easy to work with, are responsive and care for their patients as an extension of their practices. |

We generate sales leads through multiple channels that include visits to pulmonology clinics and medical centers, participation in medical conferences, maintenance of industry contacts to increase the visibility and acceptance of our products by physicians and health care professionals, participation with patient organizations such as the Cystic Fibrosis Foundation, as well as through patients by word of mouth and traffic to our website and social media channels. We continue to evaluate opportunities to offer the SmartVest System through selected Home Medical Equipment (“HME”) distributors. We entered into agreements with four HME distributors, one national and three regional, to distribute and sell the SmartVest System in the United States home care market. We expect to continue our direct sales channel as our primary homecare revenue source. Sale of the SmartVest System through HME distributors began in targeted geographies in first quarter of our fiscal year ended June 30, 2020 (“fiscal 2020”), and we had approximately $563,000 of revenue generated through these channels during fiscal 2021.

5

We believe that the addition of our HME distribution network expands our access to physicians and hospitals in certain areas of the United States and supports our other growth strategies. In addition, we place advertisements in leading medical magazines and journals.

Additionally, because the availability of reimbursement is an important consideration for health care professionals and patients, we must also demonstrate the effectiveness of our products to public and private insurance providers. The availability of reimbursement exists primarily due to an established Healthcare Common Procedure Coding System (“HCPCS”) code for HFCWO. A HCPCS code is assigned to services and products by the Centers for Medicare and Medicaid Services (“CMS”). Because our product has an assigned HCPCS code, a claim can be billed for reimbursement using that code.

International Marketing

Approximately 1.8% and 2.2% of our net revenues were from sales outside of the U.S. in our fiscal 2021 and fiscal 2020, respectively. We sell our products outside of the U.S. primarily through independent distributors specializing in respiratory products. Through June 30, 2021, the majority of our distributors operated in exclusive territories. Our principal distributors are located in Europe, the Arab states of the Persian Gulf, Southeast Asia, South America and Central America. Units are sold at a fixed contract price with payments made directly from the distributor, rather than being tied to reimbursement rates of a patient’s insurance provider as is the case for domestic sales. Our sales strategy outside of the U.S. is to maintain our current distributors with less emphasis on contracting with new distributors.

Third-Party Reimbursement

In the U.S., individuals who use the SmartVest System generally rely on third-party payers, including private payers and governmental payers such as Medicare and Medicaid, to cover and reimburse all or part of the cost of using the SmartVest System. Our home care revenue comes from reimbursement from commercial payors, Medicare, Medicaid, Veterans Affairs and direct patient payments. Reimbursement for HFCWO therapy and the SmartVest System varies among public and private insurance providers.

A key strategy to grow sales is achieving world class customer service and support for our patients and clinicians and increasing the number of covered lives across a broad payer market. We do this with an established and effective reimbursement department working on behalf of the patient by processing physician paperwork, seeking insurance authorization and processing claims. The skill and knowledge gained and offered by our reimbursement department is an important factor in building our revenue and serving patients’ financial interests. Our payment terms generally allow patients to acquire the SmartVest System over a period of one to 15 months, which is consistent with reimbursement procedures followed by Medicare and other third parties. The payment amount we receive for any single referral may vary based on a number of factors, including Medicare and third-party reimbursement processes and policies. The patient retains the risk of reimbursement to the Company in the event of non-payment by third-party payers. The reimbursement department includes the payer relations function working directly with all payer types to increase the covered lives for the SmartVest System with national and regional private insurers and applicable state and federal government entities as well as to maintain all of the current licenses with state and federal government and payer contracts.

Our SmartVest System is reimbursed under HCPCS code E0483. Currently, the Medicare total allowable amount of reimbursement for this billing code is approximately $13,000. The allowed amount for state Medicaid programs ranges from approximately $8,000 to $13,000, which is similar to commercial payers. Actual reimbursement from third-party payers can vary and can be significantly less than the full allowable amount. Deductions from the allowable amount, such as co-payments, deductibles and/or maximums on durable medical equipment, decrease the reimbursement received from the third-party payer. Collecting a full allowable amount depends on our ability to obtain reimbursement from the patient’s secondary and/or supplemental insurance if the patient has additional coverage, or our ability to collect amounts from individual patients.

6

Most patients are able to qualify for reimbursement and payment from Medicare, Medicaid, private insurance or combinations of the foregoing. We expect that subsequent generations of HFCWO products also will qualify for reimbursement under Medicare Plan B and most major health plans. However, some third-party payers must also approve coverage for new or innovative devices or therapies before they will reimburse health care providers who use the medical devices or therapies. In addition, we face the risk that new or modified products could have a lower reimbursement rate, or that the levels of reimbursement currently available for our existing products could decrease, which would hamper our ability to market and sell that product. Consequently, our sales will continue to depend in part on the availability of coverage and reimbursement from third-party payers, even though our devices may have been cleared for marketing by the FDA. The manner in which reimbursement is sought and obtained varies based upon the type of payer involved and the setting in which the procedure is furnished.

In response to the COVID-19 pandemic and the U.S. federal government’s declaration of a public health emergency in March 2020, CMS implemented a number of temporary rule changes and waivers to allow prescribers to best treat patients during the period of the public health emergency. These waivers are retroactively effective to March 1, 2020. Clinical indications and documentation typically required will not be enforced for respiratory related products including the SmartVest System (solely with respect to Medicare patients). The minimum documentation now requires a valid order and documentation of a respiratory-related diagnosis. Face-to-face and in-person requirements for respiratory devices are being waived during such period, which is currently scheduled to expire in October 2021.

Research and Development

Our R&D capabilities consist of full-time engineering staff and several consultants. We periodically engage consultants and contract engineering employees to supplement our development initiatives. Our team has a demonstrated record of developing new products that receive the appropriate product approvals and regulatory clearances around the world.

During fiscal 2021 and 2020, we incurred R&D expenses of approximately $1,722,000 and $1,050,000, or 4.8% and 3.2% of our net revenues, respectively. As a percentage of sales, we expect spending on R&D expenses to decrease slightly during fiscal 2022 as compared with fiscal 2021, as we conclude the design and testing of our next generation device in preparation for an anticipated fiscal 2023 product launch. Product enhancements were driven by voice of customer survey and in-person information focused on patient useability and device portability. We also estimate that the next generation product will be a lower cost bill of material compared to the SmartVest SQL.

Intellectual Property

As of June 30, 2021, we held 15 United States and 44 foreign issued patents covering the SmartVest System and its underlying technology and had 64 pending United States and foreign patent applications. These patents and patent applications offer coverage in the field of air pressure pulse delivery to a human in support of airway clearance.

We generally pursue patent protection for patentable subject matter in our proprietary devices in foreign countries that we have identified as key markets for our products. These markets include the European Union, Japan, and other countries.

We also have received ten U.S. trademark and service mark registrations, and one SmartVest registration in each of Canada, Peru, Japan, and India.

Manufacturing

Our headquarters in New Prague, Minnesota includes a dedicated manufacturing and engineering facility of more than 14,000 square feet and we are certified on an annual basis to be compliant with International Organization for Standardization (“ISO”) 13485 quality system standards. Our site has been audited regularly by the FDA and ISO, in accordance with their practices, and we maintain our operations in a manner consistent with their requirements for a medical device manufacturer. While components are outsourced to meet our detailed specifications, each SmartVest System is assembled, tested, and approved for final shipment at our manufacturing site in New Prague, consistent with FDA, Underwriters Laboratory, and ISO standards. Many of our strategic suppliers are located within 100 miles of our headquarters, which enables us to closely monitor our component supply chain. We maintain established inventory levels for critical components and finished goods to assure continuity of supply. During fiscal 2021 we experienced longer lead times for critical electronic components, certain plastic raw materials and packaging material related to worldwide shortages due to COVID-19 and the related U.S. economic recovery. We did not experience any material disruptions to customer shipments in fiscal 2021.

7

Product Warranties

We provide a warranty on the SmartVest System that covers the cost of replacement parts and labor, or a new SmartVest System in the event we determine a full replacement is necessary. For each home care SmartVest Systems initially purchased and currently located in the U.S. and Canada, we provide a lifetime warranty to the individual patient for whom the SmartVest System is prescribed. For sales to institutions and HME distributors within the U.S., and for all international sales, except Canadian home care, we provide a three-year warranty.

Competition

The original HFCWO technology was licensed to American Biosystems, Inc. (now part of Hill-Rom Holdings, Inc.) (“Hillrom”), which, until the introduction of our original MedPulse Respiratory Vest System® in 2000, was the only manufacturer of a product with HFCWO technology cleared for market by the FDA (Hillrom’s The Vest® Airway Clearance System). Hillrom has also received FDA 510(k) clearance for the Monarch®™ Airway Clearance System, a mobile device that uses pulmonary oscillating discs. Respiratory Technologies, Inc. (now RespirTech, part of Koninklijke Phillips N.V.) received FDA clearance to market their HFCWO product, the inCourage® Airway Clearance Therapy in 2005. Both Hillrom and RespirTech employ a direct-to-patient model, and recently Royal Phillips announced plans to offer its HFCWO device through selected HME distributors.

The AffloVest® from International Biophysics Corporation (“IBC”) also participates in the same market as our SmartVest System. IBC received FDA 510(k) clearance for its device in 2013. IBC primarily sells its device through DME companies who distribute home care medical devices and supplies. Clinical and cost-effective evidence, technology innovations, including wireless connectivity, and HFCWO product features and benefits, such as size, weight of the generator, reputation for patient and reimbursement services, and sales effectiveness of field personnel, have become the key drivers of HFCWO product sales.

Based on annual revenue, we estimate that Hillrom maintains the highest market share in HFCWO followed by RespirTech with Electromed in the third position followed by IBC.

Alternative products for administering pulmonary therapy include: Positive Expiratory Pressure; Intrapulmonary Percussive Ventilation; CPT and breathing techniques. Physicians may prescribe some or all of these devices and techniques, depending upon each patient’s health status, severity of disease, compliance, or personal preference.

We believe our primary competitive advantages over alternative treatments are patient comfort, ease of use, and the effectiveness of HFCWO treatment. Because HFCWO is not “technique dependent,” as compared to most other pulmonary therapy products, therapy begins automatically once power is provided and remains consistent and controlled for the duration of treatment.

Governmental Regulation

Medicare and Medicaid

Recent government and private sector initiatives in the U.S. and foreign countries aim at limiting the growth of health care costs, including price regulation, competitive pricing, coverage and payment policies, comparative effectiveness of therapies, technology assessments, and managed-care arrangements, and are causing the marketplace to put increased emphasis on the delivery of more cost-effective medical devices that result in better clinical outcomes. Government programs, including Medicare and Medicaid, have attempted to control costs by limiting the amount of reimbursement the program will pay for particular procedures or treatments, restricting coverage for certain products or services, and implementing other mechanisms designed to constrain utilization and contain costs. Many private insurance programs look to Medicare as a guide in setting coverage policies and payment amounts. These initiatives have created an increasing level of price sensitivity among our customers.

8

Home Medical Equipment Licensing

Although we do not fall under competitive bidding for Medicare, we often must satisfy the same licensing requirements as other DME providers that qualify for competitive bidding. In response to out-of-state businesses winning the competitive bidding process, which had a significant impact on small local DME businesses, many states have enacted regulations that require a DME provider to have an in-state business presence, specifically through state HME licensing boards or through state Medicaid programs. In order to do business with any patients in the state or to be a provider for the state Medicaid program, a DME provider must have an in-state presence. In addition to Minnesota, the location of our corporate headquarters, we have a licensed in-state presence in three other states. We also maintain an in-state presence in California in order to meet their state Medicaid requirements. In-state presence requirements vary from state to state, but generally require a physical location that is staffed and open during regular business hours. We are licensed to do business in all states except for Hawaii.

Product Regulations

Our medical devices are subject to regulation by numerous government agencies, including the FDA and comparable foreign regulatory agencies. To varying degrees, each of these agencies requires us to comply with laws and regulations governing the development, testing, manufacturing, labeling, marketing, and distribution of our medical devices, and compliance with these laws and regulations entails significant costs for us. Our regulatory and quality assurance departments provide detailed oversight in their areas of responsibility to support required clearances and approvals to market our products.

In addition to the clearances and approvals discussed below, we obtained ISO 13485 certification in January 2005 and receive annual certification of our compliance to the current ISO quality standards.

FDA Requirements

We have received clearance from the FDA to market our products, including the SmartVest System. We may be required to obtain additional FDA clearance before marketing a new or modified product in the U.S., either through the 510(k) clearance process or the more complex premarket approval process. The process may be time consuming and expensive, particularly if human clinical trials are required. Failure to obtain such clearances or approvals could adversely affect our ability to grow our business.

Continuing Product Regulation

In addition to its approval processes for new products, the FDA may require testing and post-market surveillance programs to monitor the safety and effectiveness of previously cleared products that have been commercialized and may prevent or limit further marketing of products based on the results of post-mark surveillance results. At any time after marketing clearance of a product, the FDA may conduct periodic inspections to determine compliance with both the FDA’s Quality System Regulation (“QSR”) requirements and current medical device reporting regulations. Product approvals by the FDA can be withdrawn due to failure to comply with regulatory standards or the occurrence of unforeseen problems following initial market clearance. The failure to comply with regulatory standards or the discovery of previously unknown problems with a product or manufacturer could result in fines, delays or suspensions of regulatory clearances, seizures or recalls of products (with the attendant expenses), the banning of a particular device, an order to replace or refund the cost of any device previously manufactured or distributed, operating restrictions and criminal prosecution, as well as decreased sales as a result of negative publicity and product liability claims.

We must register annually with the FDA as a device manufacturer and, as a result, are subject to periodic FDA inspection for compliance with the FDA’s QSR requirements that require us to adhere to certain extensive regulations. In addition, the federal Medical Device Reporting regulations require us to provide information to the FDA whenever there is evidence that reasonably suggests that a device may have caused or contributed to a death or serious injury or, if a malfunction were to occur, could cause or contribute to a death or serious injury. We also must maintain certain certifications to sell products internationally, and we undergo periodic inspections by notified bodies to obtain and maintain these certifications.

9

Advertising and marketing of medical devices, in addition to being regulated by the FDA, are also regulated by the Federal Trade Commission and by state regulatory and enforcement authorities. Recently, promotional activities for FDA-regulated products of other companies have been the subject of enforcement action brought under health care reimbursement laws and consumer protection statutes. Competitors and others also can initiate litigation relating to advertising and/or marketing claims. If the FDA were to determine our promotional or training materials constitute promotion of an unapproved or uncleared claim of use, it is possible we would need to modify our training or promotional materials or be subject to regulatory or enforcement actions that could result in civil fines or criminal penalties. Other federal, state or foreign enforcement authorities could also take similar action if they were to determine that our promotional or training materials constitute promotion of an unapproved use, which could result in significant fines or penalties.

European Union and Other Regions

European Union rules require that medical products receive the right to affix the CE marking, demonstrating adherence to quality standards and compliance with relevant European Union Medical Device Directives (“MDD”). Products that bear CE marking can be imported to, sold or distributed within the European Union. We obtained clearance to use CE marking on our products in April 2005. Renewal of CE marking is required every five years, and our notified body performs an annual audit to ensure that we are in compliance with all applicable regulations. We have maintained our CE marking in good standing since originally receiving it and most recently renewed it in January 2020. The renewal of our MDD certificate will allow us to continue to CE mark and sell our SmartVest SQL device, with no substantial changes, in the European Union until the certificate expires in May 2024. We are currently working on finalizing updates to the quality system to achieve full compliance with Regulation (EU) 2017/745 (EU MDR) which came into effect in May 2021. We also require all of our distributors in the European Union and other regions to comply with their home country regulations in our distributor agreements.

Federal Physician Payments Sunshine Act

The Federal Physician Payments Sunshine Act (Section 6002 of the PPACA) (the “Sunshine Act”) was adopted on February 1, 2013, to create transparency for the financial relationship between medical device companies and physicians and/or teaching hospitals. In January 2021, the Sunshine Act was expanded to cover payments made to physician assistants, nurse practitioners, clinical nurse specialists, certified nurse anesthetists, and certified nurse midwives. The Sunshine Act requires all manufacturers of drugs and medical devices to annually report to CMS any payments or any other “transfers of value” made to physicians and teaching hospitals, including but not limited to consulting fees, grants, clinical research support, royalties, honoraria, and meals. This information is then posted on a public website so that consumers can learn how much was paid to their physician by drug and medical device companies. The Sunshine Act requires ongoing data collection and annual management and reporting by us and imposes civil penalties for manufacturers that fail to report timely, accurately, or completely to CMS.

Fraud and Abuse Laws

Federal health care laws apply to the marketing of our products and when we or our customers submit claims for items or services that are reimbursed under Medicare, Medicaid or other federally-funded health care programs. The principal applicable federal laws include:

|

|

● |

the False Claims Act, which prohibits the submission of false or otherwise improper claims for payment to a federally-funded health care program; |

|

|

● |

the Anti-Kickback Statute, which prohibits offers to pay or receive remuneration of any kind for the purpose of inducing or rewarding referrals of items or services reimbursable by a federal health care program; and |

|

|

● |

the Stark Law, which prohibits physicians from profiting (actually or potentially) from their own referrals. |

10

There are often similar state false claims, anti-kickback, and anti-self-referral and insurance laws that apply to state-funded Medicaid and other health care programs and private third-party payers. In addition, the U.S. Foreign Corrupt Practices Act can be used to prosecute companies in the U.S. for arrangements with physicians, or other parties outside the U.S. if the physician or party is a government official of another country and the arrangement violates the law of that country. Enforcement of all of these regulations has become increasingly stringent, particularly due to more prevalent use of the whistleblower provisions under the False Claims Act, which allow a private individual to bring actions on behalf of the federal government alleging that the defendant has submitted a false claim to the federal government and to share in any monetary recovery. If a governmental authority were to conclude that we are not in compliance with applicable laws and regulations, we and our officers and employees could be subject to severe criminal and civil penalties and disbarment from participation as a supplier of product to beneficiaries covered by Medicare or Medicaid.

HIPAA, HITECH and Other Privacy Regulations

Federal and state laws protect the confidentiality of certain patient health information, including patient records, and restrict the use and disclosure of such information. The Health Insurance Portability and Accountability Act of 1996 and its implementing regulations (“HIPAA”) and the Health Information Technology for Economic and Clinical Health Act (“HITECH”) set forth privacy and security standards that govern the use and disclosure of protected electronic health information by “covered entities,” which include healthcare providers, health plans and healthcare clearinghouses. Because we provide our products directly to patients and bill third-party payers such as Medicare, Medicaid, and insurance companies, we are a “covered entity” and must comply with these standards. Failure to comply with HIPAA and HITECH or any state or foreign laws regarding personal data protection may result in significant fines or penalties and/or negative publicity. In addition to federal regulations issued under HIPAA and HITECH, some states have enacted privacy and security statutes or regulations that, in some cases, are more stringent than those issued under HIPAA and HITECH. In those cases, it may be necessary to modify our planned operations and procedures to comply with the more stringent state laws. If we fail to comply with applicable state laws and regulations, we could be subject to additional sanctions.

The HIPAA and HITECH health care fraud and false statement statutes also prohibit, among other things, knowingly and willfully executing, or attempting to execute, a scheme to defraud any health care benefit program, including private payers, and knowingly and willfully falsifying, concealing or covering up a material fact or making any materially false, fictitious or fraudulent statement or representation in connection with the delivery of or payment for health care benefits, items or services.

Environmental Laws

We are subject to various environmental laws and regulations both within and outside the U.S. Like other medical device companies, our operations involve the use of substances regulated under environmental laws, primarily manufacturing, sterilization, and disposal processes. We do not expect that compliance with environmental protection laws will have a material impact on our results of operations, financial position, or cash flows.

Cybersecurity and Data Privacy

Protecting the privacy of customer and personnel information is important to us, and we maintain security protocols and processes, including training and education for all personnel, designed to combat the risk of unauthorized access or inadvertent disclosure. Our business operations involve confidential information, including patient health information subject to regulation as discussed under “HIPAA, HITECH and Other Privacy Regulations” above. Our information technology infrastructure is designed to offer reliability, scalability, performance, security and privacy for our personnel, clients and third-party contractors.

We maintain comprehensive compliance and security programs designed to help safeguard and ensure the integrity of the confidential information we possess, which includes both organizational and technical control measures. We also have programs in place to monitor the safety of confidential information as well as plans for immediate, coordinated action in the event of a potential security incident. We routinely conduct employee trainings on important information security procedures and engage with independent third-party firms to test and measure compliance on these security measures. In addition, we have maintained appropriate cyber insurance policies that limit the financial risk of any potential incident. Our cyber insurance policies include dedicated support for remediating a specific cybersecurity or data privacy incident and limit the potential financial risk associated with an actual incident.

11

Even though we have implemented administrative, physical and technical safeguards designed to help protect the confidential data we possess and the integrity of our information systems and infrastructure, these safeguards may not be effective in preventing future cybersecurity incidents or data breaches.

Data Privacy Incident

In June 2021, we determined that an unauthorized third party gained access to a limited number of our files. Upon discovery, we immediately initiated an investigation and engaged third-party advisors to assist in investigating the source and scope of the unauthorized activity, and to further secure our information systems. From the investigation, we determined that certain files containing certain information of customers, employees, and some third-party contractors were accessed. There has been no indication that any of this information has been used inappropriately and we are working to mitigate any impact on the Company. Individuals whose information may have been involved in the data privacy incident were specifically contacted by the Company. The Company has a cyber insurance policy which we believe will cover most of the costs associated with this specific data incident. To help prevent a similar incident from occurring in the future, we further enhanced the security of our systems, and will continue to review and, where appropriate enhance, our security protocols and processes, and training and education.

Human Capital

We believe that our dedicated, talented employees are our most valuable resource and a key strength in accomplishing our collective mission and goals. As of June 30, 2021, we had 132 employees, an increase of 8.2% from fiscal 2020, who are located in 24 states throughout the United States. 10 of our employees were respiratory therapists licensed by appropriate state professional organizations, including all the employees in our Patient Services Department. We also had approximately 250 respiratory therapists and health care professionals retained on a non-exclusive, independent contractor basis to provide training to our customers in the U.S. None of our employees are covered by a collective bargaining agreement. We believe our relations with our employees are good.

We are committed to attracting, retaining, and developing diverse and high-performing talent that includes a strong focus on performance and development, total rewards, diversity, inclusion and equity, and employee safety. These serve as the pillars to our human capital management framework.

We understand that our success and growth depends on attracting, retaining, and developing talent across all levels of the organization. Our recruitment strategies are continuously reviewed with leadership and partners to ensure our practices align with our mission, purpose, and values.

We believe in ensuring that employees understand our mission, purpose, and goals as well as their impact on our success. We use an annual performance review process to support development and performance discussions with employees. In addition, every employee is eligible to participate in our incentive plan, which allows for us to share the rewards of the company with the people who significantly contribute to our success.

To cultivate a learning culture that provides enhancement and growth for our people, we offer educational assistance, online training, seminars, specific skill training, and participation in business and industry organizations. We are also committed to contributing our talents and resources to serve the communities in which we live and work through various charitable campaigns, employee programs and volunteerism. We believe that this commitment assists in our efforts to attract and retain employees.

We believe that sharing rewards is essential to increasing employee engagement and improving morale and creating a positive culture. We also offer our employees a competitive salary and benefits package and are committed to continuous review of these programs. These benefits include but are not limited to retirement savings, a variety of health insurance options and other benefits programs, including dental and vision, disability insurance, contributions to health savings accounts, paid maternity/paternity leave, and wellness resources. In addition, we offer opportunities for remote work and flexible schedules and location, depending on business needs and the specific role.

We are committed to ensuring a diverse workforce in a safe environment by maintaining compliance with applicable employment laws and governmental regulations. Treating employees with dignity and equality is of utmost importance in everything we do. We take pride in the fact that women represent 52% of our total managerial roles and comprise 37.5% of our executive leadership team. We pride ourselves on accepting, hearing, and celebrating multiple approaches and points of view and building on an inclusive and diverse culture.

12

Safety is a vital aspect to the success of our people and business. We are proud of our employees’ collective commitment to secure and maintain safe work practices that have resulted in zero lost time injuries within our manufacturing operations. We also provide wellbeing services to support each employee’s physical and mental health and will continue to emphasize the importance of the safety and health of our employees in all we do.

Available Information

Our Internet address is www.smartvest.com. We have made available on our website, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and, if applicable, amendments to those reports, as soon as reasonably practicable after we electronically file these materials with, or furnish them to, the SEC. Reports of beneficial ownership filed by our directors and executive officers pursuant to Section 16(a) of the Exchange Act are also available on our website. We are not including the information contained on our website as part of, or incorporating it by reference into, this Annual Report on Form 10-K. The SEC also maintains an Internet site that contains our reports, proxy and information statements, and other information we file or furnish with the SEC, available at www.sec.gov.

As a smaller reporting company, we are not required to provide disclosure pursuant to this item.

Item 1B. Unresolved Staff Comments.

As a smaller reporting company, we are not required to provide disclosure pursuant to this item.

We own our principal headquarters and manufacturing facilities, consisting of approximately 37,000 square feet, which are located on an approximately 2.3-acre parcel in New Prague, Minnesota. We believe that our facilities are satisfactory for our long-term growth plans.

We may be party to legal actions, proceedings, or claims in the ordinary course of business. We are not aware of any actual or threatened litigation that would have a material adverse effect on our financial condition or results of operations.

Item 4. Mine Safety Disclosures.

None.

Item 5. Market For Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market Information

Our common stock is listed on the NYSE American under the symbol “ELMD”.

As of August 20, 2021, there were 65 registered holders of our common stock.

13

Dividends

We have never paid cash dividends on any of our shares of common stock. We currently intend to retain any earnings for use in operations and do not anticipate paying cash dividends to our shareholders in the foreseeable future. The agreement governing our credit facility restricts our ability to pay dividends.

Recent Sales of Unregistered Equity Securities

None.

Purchases of Equity Securities by the Company and Affiliated Purchasers

On May 26, 2021, our Board of Directors approved a stock repurchase authorization. Under the authorization, we may repurchase up to $3.0 million of outstanding shares of our common stock through May 26, 2022. The shares of our common stock may be repurchased on the open market or in privately negotiated transactions subject to applicable securities laws and regulations. The following table sets forth information concerning purchases of shares of our common stock for three months ended June 30, 2021:

| Period | Total

Number of Shares Purchased | Average Price Paid per Share | Total

Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate

Dollar Value of Shares that May Yet be Purchased Under the Plans or Programs | |||||||||||||

| April 1 to April 30, 2021 | — | $ | — | — | $ | — | |||||||||||

| May 1 to May 30, 2021 | — | $ | — | — | $ | — | |||||||||||

June 1 to June 30, 2021 | 104,211 | $ | 10.79 | 104,211 | $ | 1,876,000 | |||||||||||

Total | 104,211 | $ | 10.79 | 104,211 | $ | 1,876,000 | |||||||||||

Item 6. Selected Financial Data.

As a smaller reporting company, we are not required to provide disclosure pursuant to this item.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our financial statements and the accompanying notes included elsewhere in this Annual Report on Form 10-K. The forward-looking statements include statements that reflect management’s good faith beliefs, plans, objectives, goals, expectations, anticipations and intentions with respect to our future development plans, capital resources and requirements, results of operations, and future business performance. Our actual results could differ materially from those anticipated in the forward-looking statements included in this discussion as a result of certain factors, including, but not limited to, those discussed in the section entitled “Information Regarding Forward-Looking Statements” immediately preceding Part I of this Annual Report on Form 10-K.

Overview

Electromed develops and provides innovative airway clearance products applying HFCWO technologies in pulmonary care for patients of all ages.

14

We manufacture, market and sell products that provide HFCWO, including the SmartVest System and related products, to patients with compromised pulmonary function. The SmartVest SQL is smaller, quieter and lighter than our previous product (the SmartVest SV2100), with enhanced programmability, ease of use, wireless technology, and a personalized HFCWO therapy management portal for patients with compromised pulmonary function. Our products are sold in both the home health care market and the institutional market for use by patients in hospitals, which we refer to as “institutional sales.” The SmartVest SQL has been sold in the domestic home care market since 2014. In 2017, we launched the SmartVest SQL with SmartVest Connect wireless technology.

The SmartVest System is often eligible for reimbursement from major private insurance providers, health maintenance organizations (“HMOs”), state Medicaid systems, and the federal Medicare system, which is an important consideration for patients considering an HFCWO course of therapy. For domestic sales, the SmartVest System may be reimbursed under the Medicare-assigned billing code for HFCWO devices if the patient has cystic fibrosis, bronchiectasis (including chronic bronchitis or chronic obstructive pulmonary disease that has resulted in a diagnosis of bronchiectasis), or any one of certain enumerated neuromuscular diseases, and can demonstrate that another less expensive physical or mechanical treatment did not adequately mobilize retained secretions. Private payers consider a variety of sources, including Medicare, as guidelines in setting their coverage policies and payment amounts.

We employ a direct-to-patient and provider model, through which we obtain patient referrals from clinicians, manage insurance claims on behalf of our patients and their clinicians, deliver our solutions to patients and train them on proper use in their homes. This model allows us to directly approach patients and clinicians, whereby we disintermediate the traditional durable medical equipment channel and capture both the manufacturer and distributor margins. We have engaged a limited number of regional durable medical equipment distributors focused on respiratory therapies as an alternate sales channel. Revenue through this channel was less than 2% of our total revenues in fiscal 2021.

Our key growth strategies for fiscal 2022 include the following:

Grow faster than the overall home care HFCWO market by taking market share and expanding the pool of physicians who prescribe the SmartVest System in the largest and fastest growing segments of the market: adult pulmonology/bronchiectasis;

|

|

● |

Expand our sales force in geographies with high incidence of bronchiectasis diagnosing physicians; |

|

|

● |

Increase revenue from direct-to-consumer marketing by expanding Electromed brand awareness; |

|

|

● |

Provide best-in-class customer care and support; |

|

|

● |

Develop and promulgate the body of bronchiectasis clinical evidence to increase physician adoption of the SmartVest System for patients; and |

| ● | Develop innovative device features in our next generation device that appeal to patients. |

Critical Accounting Policies and Estimates

During the preparation of our financial statements, we are required to make estimates, assumptions and judgments that affect reported amounts. Those estimates and assumptions affect our reported amounts of assets and liabilities, our disclosure of contingent assets and liabilities, and our reported revenues and expenses. We update these estimates, assumptions and judgments as appropriate, which in most cases is at least quarterly. We use our technical accounting knowledge, cumulative business experience, judgment and other factors in the selection and application of our accounting policies. While we believe the estimates, assumptions and judgments we use in preparing our financial statements are appropriate, they are subject to factors and uncertainties regarding their outcome and therefore, actual results may materially differ from these estimates. The following is a summary of our primary critical accounting policies and estimates. See also Note 1 to the Financial Statements, included in Part II, Item 8, of this Annual Report on Form 10-K.

COVID-19 Pandemic and CARES Act Funding

In March 2020, the World Health Organization designated COVID-19 as a global pandemic. The COVID-19 pandemic created significant volatility, uncertainty and economic disruption that negatively impacted business in our industry starting in March 2020 and continuing to varying degrees throughout fiscal 2021.

15

We consider our business to be essential under applicable governmental orders due primarily to our role in manufacturing and supplying needed medical devices to patients with respiratory related issues and remained fully operational for the duration of fiscal 2021.

We also took measures to ensure the safety of our employees and to comply with applicable governmental orders, including transitioning employees to remote work where possible, adhering to Centers for Disease Control (“CDC”) guidelines for mask wearing and social distancing, and implementing enhanced cleaning practices in the office. During the fourth quarter of fiscal 2021, as COVID-19 vaccines became more widely available in the United States, we reviewed our guidelines for corporate offices and manufacturing and adjusted our safety guidelines to align with CDC guidelines for mask wearing and social distancing. Additionally, we provided direction to employees on their work schedules, balancing business productivity and flexibility for employees and maintaining the highest level of safety in the workplace.

The home care market was impacted by COVID-19 primarily due to certain healthcare facilities and clinics restricting access to their clinicians, and patients reducing in-person visits to clinics for consultations and treatments. The degree of clinic access limitations and in-person patient visit reductions varied throughout fiscal 2021 based on multiple variables, including the number of daily COVID-19 cases occurring in key geographies, the degree of state and local government restrictions, and the availability and deployment of vaccines. During fiscal 2021, our sales team developed and utilized a hybrid selling approach that combined virtual and face-to-face clinician interactions, which helped mitigate the market disruption caused by COVID-19.

Our institutional business was negatively impacted by COVID-19 through fiscal 2021 as hospitals and long-term care facilities adjusted their operating protocols and procurement management in response to the pandemic. Limiting the spread of airborne particles was a priority in institutional settings during fiscal 2021, and airway clearance therapies usage, including HFCWO, induces coughing in patients.

In response to the negative impacts of the COVID-19 pandemic on our business, in April 2020 we initiated cost-containment measures, which included reducing discretionary and variable spend, such as travel, and the use of contractors, consultants, temporary help and employee furloughs in our manufacturing and general and administrative functions due to lower near-term demand for our products. As our referral volumes returned to near pre-pandemic levels in July 2020, all furloughed employees returned to work by August 2020, and we continued to make all planned strategic investments in our business throughout fiscal 2021 in both selling, general and administrative (“SG&A”) and R&D.

We did not receive any direct financial assistance from any government program during fiscal 2021. We received a one-time $913,000 payment under the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) in the fourth quarter of fiscal 2020, which partially offset lower profitability related to the revenue decline caused by the COVID-19 pandemic during the period. The amount received from the CARES Act is subject to compliance with certain terms and conditions and reporting requirements, and such report may be audited by a federal agency for compliance with the program’s terms and conditions.