UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22405

ClearBridge MLP and Midstream Fund Inc.

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 47th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

George P. Hoyt

Financial Templeton

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-888-777-0102

Date of fiscal year end: November 30

Date of reporting period: May 31, 2023

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Semi-Annual Report to Stockholders is filed herewith.

![]()

| Semi-Annual Report | May 31, 2023 |

CLEARBRIDGE

MLP AND MIDSTREAM FUND INC. (CEM)

| INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE |

Fund objective

The Fund’s investment objective is to provide a high level of total return with an emphasis on cash distributions.

The Fund seeks to achieve its objective by investing primarily in energy master limited partnerships (“MLPs”) and energy midstream entities.

Dear Shareholder,

We are pleased to provide the semi-annual report of ClearBridge MLP and Midstream Fund Inc. for the six-month reporting period ended May 31, 2023. Please read on for Fund performance information during the Fund’s reporting period.

As always, we remain committed to providing you with excellent service and a full spectrum of investment choices. We also remain committed to supplementing the support you receive from your financial advisor. One way we accomplish this is through our website, www.franklintempleton.com. Here you can gain immediate access to market and investment information, including:

| • | Fund prices and performance, |

| • | Market insights and commentaries from our portfolio managers, and |

| • | A host of educational resources. |

We look forward to helping you meet your financial goals.

Sincerely,

Jane Trust, CFA

Chairman, President and Chief Executive Officer

June 30, 2023

| II | ClearBridge MLP and Midstream Fund Inc. |

For the six months ended May 31, 2023, ClearBridge MLP and Midstream Fund Inc. returned -9.33% based on its net asset value (“NAV”)i and -9.01% based on its New York Stock Exchange (“NYSE”) market price per share. The Alerian MLP Indexii returned 0.39% over the same time frame.

The Fund has a practice of seeking to maintain a relatively stable level of distributions to shareholders. This practice has no impact on the Fund’s investment strategy and may reduce the Fund’s NAV. The Fund’s manager believes the practice helps maintain the Fund’s competitiveness and may benefit the Fund’s market price and premium/discount to the Fund’s NAV.

During this six-month period, the Fund made distributions to shareholders totaling $1.27 per share. As of May 31, 2023, the Fund estimates that all of the distributions during the period constituted a return of capital.* The performance table shows the Fund’s six-month total return based on its NAV and market price as of May 31, 2023. Past performance is no guarantee of future results.

| Performance Snapshot as of May 31, 2023 (unaudited) | ||||

| Price Per Share | 6-Month Total Return** |

|||

| $37.31 (NAV) | -9.33 | %† | ||

| $31.33 (Market Price) | -9.01 | %‡ | ||

All figures represent past performance and are not a guarantee of future results. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

** Total returns are based on changes in NAV or market price, respectively. Returns reflect the deduction of all Fund expenses, including management fees, operating expenses, and other Fund expenses. Returns do not reflect the deduction of brokerage commissions or taxes that investors may pay on distributions or the sale of shares.

† Total return assumes the reinvestment of all distributions, including returns of capital, if any, at NAV.

‡ Total return assumes the reinvestment of all distributions, including returns of capital, if any, in additional shares in accordance with the Fund’s Dividend Reinvestment Plan.

Looking for additional information?

The Fund is traded under the symbol “CEM” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available online under the symbol “XCEMX” on most financial websites. Barron’s and The Wall Street Journal’s Monday edition both carry closed-end fund tables that provide additional information. In addition,

| * | This estimate is not for tax purposes. The Fund will issue a Form 1099 with final composition of the distributions for tax purposes after year-end. A return of capital is not taxable and results in a reduction in the tax basis of a shareholder’s investment. For more information about a distribution’s composition, please refer to the Fund’s distribution press release or, if applicable, the Section 19 notice located in the press release section of our website, www.franklintempleton.com. |

| ClearBridge MLP and Midstream Fund Inc. | III |

Performance review (cont’d)

the Fund issues a monthly press release that can be found on most major financial websites as well as www.franklintempleton.com.

In a continuing effort to provide information concerning the Fund, shareholders may call 1-888-777-0102 (toll free), Monday through Friday from 8:00 a.m. to 5:30 p.m. Eastern Time, for the Fund’s current NAV, market price and other information.

Thank you for your investment in ClearBridge MLP and Midstream Fund Inc. As always, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

Jane Trust, CFA

Chairman, President and Chief Executive Officer

June 30, 2023

RISKS: The Fund is a non-diversified, closed-end management investment company designed primarily as a long-term investment and not as a trading vehicle. The Fund is not intended to be a complete investment program and, due to the uncertainty inherent in all investments, there can be no assurance that the Fund will achieve its investment objective. The Fund’s common stock is traded on the New York Stock Exchange. Similar to stocks, the Fund’s share price will fluctuate with market conditions and, at the time of sale, may be worth more or less than the original investment. Shares of closed-end funds often trade at a discount to their net asset value. Because the Fund is non-diversified, it may be more susceptible to economic, political or regulatory events than a diversified fund. The Fund’s investments are subject to a number of risks, including stock market risk, MLP and midstream entities risk, market events risk and portfolio management risk. MLP distributions are not guaranteed and there is no assurance that all distributions will be tax deferred. Investments in MLP securities and midstream entities are subject to unique risks. The Fund’s concentration of investments in energy related MLPs and midstream entities subjects it to the risks of MLPs, midstream entities and the energy sector, including the risks of declines in energy and commodity prices, decreases in energy demand, adverse weather conditions, natural or other disasters, changes in government regulation, and changes in tax laws. Leverage may result in greater volatility of NAV and the market price of common shares and increases a shareholder’s risk of loss. The Fund may make significant investments in derivative instruments. Derivative instruments can be illiquid, may disproportionately increase losses and have a potentially large impact on Fund performance. The Fund may invest in small capitalization or illiquid securities which can increase the risk and volatility of the Fund. The market values of securities or other assets will fluctuate, sometimes sharply and unpredictably, due to changes in general market conditions, overall economic trends or events, governmental actions or intervention, actions taken by the U.S. Federal Reserve or

| IV | ClearBridge MLP and Midstream Fund Inc. |

foreign central banks, market disruptions caused by trade disputes or other factors, political developments, armed conflicts, economic sanctions and countermeasures in response to sanctions, major cybersecurity events, investor sentiment, the global and domestic effects of a pandemic, and other factors that may or may not be related to the issuer of the security or other asset. The Fund may also invest in money market funds, including funds affiliated with the Fund’s manager and subadviser.

All investments are subject to risk including the possible loss of principal. Past performance is no guarantee of future results. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | Net asset value (“NAV”) is calculated by subtracting total liabilities, including liabilities associated with financial leverage (if any), from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is the Fund’s market price as determined by supply of and demand for the Fund’s shares. |

| ii | The Alerian MLP Index is a composite of the fifty most prominent energy master limited partnerships (“MLPs”) and is calculated using a float-adjusted, capitalization-weighted methodology. |

| ClearBridge MLP and Midstream Fund Inc. | V |

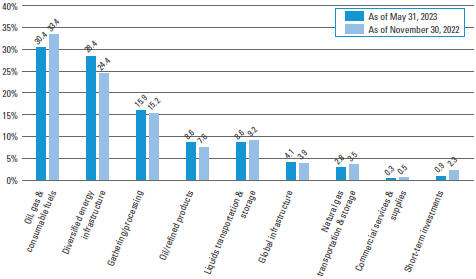

Investment breakdown (%) as a percent of total investments

| † | The bar graph above represents the composition of the Fund’s investments as of May 31, 2023 and November 30, 2022. The Fund is actively managed. As a result, the composition of the Fund’s investments is subject to change at any time. |

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 1 |

Schedule of investments (unaudited)

May 31, 2023

ClearBridge MLP and Midstream Fund Inc.

(Percentages shown based on Fund net assets)

| Security | Shares/Units | Value | ||||||

| Master Limited Partnerships — 102.6% | ||||||||

| Diversified Energy Infrastructure — 42.6% |

||||||||

| Energy Transfer LP |

5,018,027 | $62,223,535 | ||||||

| Enterprise Products Partners LP |

2,479,854 | 62,814,702 | ||||||

| Genesis Energy LP |

1,331,323 | 12,847,267 | ||||||

| Plains All American Pipeline LP |

2,854,586 | 36,881,251 | ||||||

| Plains GP Holdings LP, Class A Shares |

2,695,251 | 36,655,413 | * | |||||

| Total Diversified Energy Infrastructure |

211,422,168 | |||||||

| Gathering/Processing — 23.9% |

||||||||

| Crestwood Equity Partners LP |

1,225,775 | 31,453,387 | ||||||

| Hess Midstream LP, Class A Shares |

1,191,190 | 33,222,289 | ||||||

| Western Midstream Partners LP |

2,127,721 | 53,703,678 | ||||||

| Total Gathering/Processing |

118,379,354 | |||||||

| Global Infrastructure — 6.1% |

||||||||

| Brookfield Infrastructure Partners LP |

846,514 | 30,381,388 | ||||||

| Liquids Transportation & Storage — 12.9% |

||||||||

| Holly Energy Partners LP |

476,872 | 8,187,892 | ||||||

| Magellan Midstream Partners LP |

862,281 | 51,917,939 | ||||||

| NuStar Energy LP |

224,000 | 3,657,920 | ||||||

| Total Liquids Transportation & Storage |

63,763,751 | |||||||

| Natural Gas Transportation & Storage — 4.2% |

||||||||

| Cheniere Energy Partners LP |

474,498 | 21,091,436 | ||||||

| Oil/Refined Products — 12.9% |

||||||||

| MPLX LP |

1,919,271 | 63,988,495 | ||||||

| Total Master Limited Partnerships (Cost — $431,298,821) |

509,026,592 | |||||||

| Shares | ||||||||

| Common Stocks — 46.0% | ||||||||

| Energy — 45.5% | ||||||||

| Oil, Gas & Consumable Fuels — 45.5% |

||||||||

| Antero Midstream Corp. |

2,910,680 | 29,718,043 | ||||||

| DT Midstream Inc. |

115,000 | 5,227,900 | ||||||

| Enbridge Inc. |

832,840 | 29,315,968 | ||||||

| Equitrans Midstream Corp. |

517,125 | 4,411,076 | ||||||

| Kinder Morgan Inc. |

1,836,625 | 29,588,029 | ||||||

| ONEOK Inc. |

545,178 | 30,889,785 | ||||||

| Targa Resources Corp. |

583,182 | 39,685,535 | ||||||

| TC Energy Corp. |

529,780 | 20,629,633 | ||||||

| Williams Cos. Inc. |

1,270,021 | 36,398,802 | ||||||

| Total Energy |

225,864,771 | |||||||

See Notes to Financial Statements.

| 2 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

ClearBridge MLP and Midstream Fund Inc.

(Percentages shown based on Fund net assets)

| Security | Shares | Value | ||||||||||

| Industrials — 0.5% | ||||||||||||

| Commercial Services & Supplies — 0.5% |

||||||||||||

| Aris Water Solutions Inc., Class A Shares |

257,530 | $ | 2,366,701 | |||||||||

| Total Common Stocks (Cost — $260,459,368) |

228,231,472 | |||||||||||

| Total Investments before Short-Term Investments (Cost — $691,758,189) |

|

737,258,064 | ||||||||||

| Rate | ||||||||||||

| Short-Term Investments — 1.3% | ||||||||||||

| JPMorgan 100% U.S. Treasury Securities Money Market Fund, Institutional Class |

4.877 | % | 6,262,518 | 6,262,518 | (a) | |||||||

| Total Investments** — 149.9% (Cost — $698,020,707) |

|

743,520,582 | ||||||||||

| Mandatory Redeemable Preferred Stock, at Liquidation Value — (11.6)% |

|

(57,400,045 | ) | |||||||||

| Other Liabilities in Excess of Other Assets — (38.3)% |

(190,131,005 | ) | ||||||||||

| Total Net Assets Applicable to Common Shareholders — 100.0% |

|

$ | 495,989,532 | |||||||||

| * | Non-income producing security. |

| ** | The entire portfolio is subject to a lien, granted to the lender and Senior Note holders, to the extent of the borrowings outstanding and any additional expenses. |

| (a) | Rate shown is one-day yield as of the end of the reporting period. |

See Notes to Financial Statements.

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 3 |

Statement of assets and liabilities (unaudited)

May 31, 2023

| Assets: | ||||

| Investments, at value (Cost — $698,020,707) |

$ | 743,520,582 | ||

| Income tax receivable |

2,279,821 | |||

| Receivable for securities sold |

845,423 | |||

| Dividends and distributions receivable |

786,608 | |||

| Money market fund distributions receivable |

42,903 | |||

| Prepaid expenses |

27,156 | |||

| Total Assets |

747,502,493 | |||

| Liabilities: | ||||

| Loan payable (Note 5) |

138,000,000 | |||

| Mandatory Redeemable Preferred Stock ($100,000 and $35 liquidation value per share; 324 and 714,287 shares issued and outstanding, respectively) (net of deferred offering costs of $635,128) (Note 7) |

56,764,917 | |||

| Senior Secured Notes (net of deferred debt issuance and offering costs of $175,437) (Note 6) |

54,106,752 | |||

| Interest expense payable |

920,499 | |||

| Investment management fee payable |

617,569 | |||

| Distributions payable to Mandatory Redeemable Preferred Stockholders |

121,336 | |||

| Directors’ fees payable |

849 | |||

| Accrued expenses |

981,039 | |||

| Total Liabilities |

251,512,961 | |||

| Total Net Assets Applicable to Common Shareholders | $ | 495,989,532 | ||

| Net Assets Applicable to Common Shareholders: | ||||

| Common stock par value ($0.001 par value; 13,294,195 shares issued and outstanding; 99,285,389 common shares authorized) |

$ | 13,294 | ||

| Paid-in capital in excess of par value |

615,336,996 | |||

| Total distributable earnings (loss), net of income taxes |

(119,360,758) | |||

| Total Net Assets Applicable to Common Shareholders | $ | 495,989,532 | ||

| Common Shares Outstanding | 13,294,195 | |||

| Net Asset Value Per Common Share | $37.31 | |||

See Notes to Financial Statements.

| 4 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

Statement of operations (unaudited)

For the Six Months Ended May 31, 2023

| Investment Income: | ||||

| Dividends and distributions |

$ | 28,961,622 | ||

| Return of capital (Note 1(h)) |

(21,686,718) | |||

| Net Dividends and Distributions |

7,274,904 | |||

| Money market fund distributions |

213,657 | |||

| Less: Foreign taxes withheld |

(279,649) | |||

| Total Investment Income |

7,208,912 | |||

| Expenses: | ||||

| Interest expense (Notes 5 and 6) |

4,969,653 | |||

| Investment management fee (Note 2) |

3,880,125 | |||

| Distributions to Mandatory Redeemable Preferred Stockholders (Notes 1 and 7) |

1,599,931 | |||

| Transfer agent fees |

615,632 | |||

| Legal fees |

237,392 | |||

| Audit and tax fees |

135,451 | |||

| Directors’ fees |

109,984 | |||

| Commitment fees (Note 5) |

73,402 | |||

| Amortization of preferred stock offering costs (Note 7) |

63,464 | |||

| Amortization of debt issuance and offering costs (Note 6) |

47,770 | |||

| Fund accounting fees |

30,826 | |||

| Rating agency fees |

11,552 | |||

| Shareholder reports |

10,397 | |||

| Franchise taxes |

9,474 | |||

| Insurance |

2,264 | |||

| Custody fees |

1,428 | |||

| Stock exchange listing fees |

1,232 | |||

| Miscellaneous expenses |

104,513 | |||

| Total Expenses |

11,904,490 | |||

| Less: Fee waivers and/or expense reimbursements (Note 2) |

(194,006) | |||

| Net Expenses |

11,710,484 | |||

| Net Investment Loss, before income taxes | (4,501,572) | |||

| Current tax expense (Note 9) |

(3,794,600) | |||

| Net Investment Loss, net of income taxes | (8,296,172) | |||

| Realized and Unrealized Gain (Loss) on Investments and Foreign Currency Transactions (Notes 1, 3 and 9): | ||||

| Net Realized Gain (Loss) From: |

||||

| Investment transactions |

12,265,866 | |||

| Foreign currency transactions |

(10,070) | |||

| Net Realized Gain, before income taxes |

12,255,796 | |||

| Net Realized Gain, net of income taxes |

12,255,796 | |||

| Change in Net Unrealized Appreciation (Depreciation) From: |

||||

| Investments |

(57,190,752) | |||

| Foreign currencies |

2,751 | |||

| Change in Net Unrealized Appreciation (Depreciation), before income taxes |

(57,188,001) | |||

| Change in Net Unrealized Appreciation (Depreciation), net of income taxes |

(57,188,001) | |||

| Net Loss on Investments and Foreign Currency Transactions, net of income taxes | (44,932,205) | |||

| Decrease in Net Assets Applicable to Common Shareholders From Operations | $ | (53,228,377) | ||

See Notes to Financial Statements.

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 5 |

Statements of changes in net assets

| For the Six Months Ended May 31, 2023 (unaudited) and the Year Ended November 30, 2022 |

2023 | 2022 | ||||||

| Operations: | ||||||||

| Net investment loss, net of income taxes |

$ | (8,296,172) | $ | (5,761,395) | ||||

| Net realized gain, net of income taxes |

12,255,796 | 41,249,888 | ||||||

| Change in net unrealized appreciation (depreciation), net of income taxes |

(57,188,001) | 148,122,608 | ||||||

| Increase (Decrease) in Net Assets Applicable to Common Shareholders From Operations |

(53,228,377) | 183,611,101 | ||||||

| Distributions to Common Shareholders From (Note 1): | ||||||||

| Dividends |

— | (31,283,612) | ||||||

| Return of capital |

(16,900,008) | — | ||||||

| Decrease in Net Assets From Distributions to Common Shareholders |

(16,900,008) | (31,283,612) | ||||||

| Fund Share Transactions: | ||||||||

| Cost of shares repurchased (161,000 and 84,000 shares repurchased, respectively) (Note 8) |

(5,334,424) | (2,805,578) | ||||||

| Decrease in Net Assets From Fund Share Transactions |

(5,334,424) | (2,805,578) | ||||||

| Increase (Decrease) in Net Assets Applicable to Common Shareholders |

(75,462,809) | 149,521,911 | ||||||

| Net Assets Applicable to Common Shareholders: | ||||||||

| Beginning of period |

571,452,341 | 421,930,430 | ||||||

| End of period |

$ | 495,989,532 | $ | 571,452,341 | ||||

See Notes to Financial Statements.

| 6 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

Statement of cash flows (unaudited)

For the Six Months Ended May 31, 2023

| Increase (Decrease) in Cash: | ||||

| Cash Flows from Operating Activities: | ||||

| Net decrease in net assets applicable to common shareholders resulting from operations |

$ | (53,228,377) | ||

| Adjustments to reconcile net decrease in net assets resulting from operations to net cash provided (used) by operating activities: |

||||

| Purchases of portfolio securities |

(217,237,650) | |||

| Sales of portfolio securities |

210,022,266 | |||

| Net purchases, sales and maturities of short-term investments |

12,787,902 | |||

| Return of capital |

21,686,718 | |||

| Increase in dividends and distributions receivable |

(43,155) | |||

| Increase in receivable for securities sold |

(845,423) | |||

| Decrease in money market fund distributions receivable |

10,709 | |||

| Decrease in prepaid expenses |

13,602 | |||

| Decrease in income tax receivable |

3,832,151 | |||

| Decrease in payable for securities purchased |

(952,582) | |||

| Amortization of preferred stock offering costs |

63,464 | |||

| Amortization of debt issuance and offering costs |

47,770 | |||

| Decrease in investment management fee payable |

(5,828) | |||

| Decrease in Directors’ fees payable |

(23,280) | |||

| Increase in interest expense payable |

26,608 | |||

| Increase in accrued expenses |

603,080 | |||

| Decrease in distributions payable to Mandatory Redeemable Preferred Stockholders |

(15,476) | |||

| Net realized gain on investments |

(12,265,866) | |||

| Change in net unrealized appreciation (depreciation) of investments |

57,190,752 | |||

| Net Cash Provided in Operating Activities* |

21,667,385 | |||

| Cash Flows from Financing Activities: | ||||

| Distributions paid on common stock |

(16,900,008) | |||

| Proceeds from loan facility borrowings |

7,000,000 | |||

| Payment for Fund shares repurchased |

(5,334,424) | |||

| Redemption of Mandatory Redeemable Preferred Stock |

(6,400,000) | |||

| Preferred stock offering costs |

(32,953) | |||

| Net Cash Used by Financing Activities |

(21,667,385) | |||

| Cash and restricted cash at beginning of period | — | |||

| Cash and restricted cash at end of period | — | |||

| * | Included in operating expenses is $5,019,461 paid for interest and commitment fees on borrowings, $1,615,407 paid for distributions to Mandatory Redeemable Preferred Stockholders and $37,551 refunded for income taxes, net of income taxes paid. |

The following table provides a reconciliation of cash and restricted cash reported within the Statement of Assets and Liabilities that sums to the total of such amounts shown on the Statement of Cash Flows.

| May 31, 2023 | ||||

| Cash | — | |||

| Restricted cash | — | |||

| Total cash and restricted cash shown in the Statement of Cash Flows | — | |||

See Notes to Financial Statements.

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 7 |

| For a common share of capital stock outstanding throughout each year ended November 30, unless otherwise noted: |

||||||||||||||||||||||||

| 20231,2 | 20221 | 20211 | 20201,3 | 20191,3 | 20181,3 | |||||||||||||||||||

| Net asset value, beginning of period | $42.47 | $31.16 | $20.19 | $56.65 | $65.60 | $69.30 | ||||||||||||||||||

| Income (loss) from operations: | ||||||||||||||||||||||||

| Net investment income (loss) |

(0.62) | (0.43) | (0.07) | (0.85) | (0.50) | 1.40 | ||||||||||||||||||

| Net realized and unrealized gain (loss) |

(3.34) | 14.01 | 12.84 | (32.75) | (2.55) | 2.00 | ||||||||||||||||||

| Total income (loss) from operations |

(3.96) | 13.58 | 12.77 | (33.60) | (3.05) | 3.40 | ||||||||||||||||||

| Less distributions to common shareholders from: | ||||||||||||||||||||||||

| Dividends |

— | (2.32) | (1.49) | — | (2.05) | (1.40) | ||||||||||||||||||

| Return of capital |

(1.27) | 4 | — | (0.43) | (2.90) | (3.85) | (5.70) | |||||||||||||||||

| Total distributions to common shareholders |

(1.27) | (2.32) | (1.92) | (2.90) | (5.90) | (7.10) | ||||||||||||||||||

| Anti-dilutive impact of repurchase plan |

0.07 | 5 | 0.05 | 5 | 0.12 | 5 | 0.04 | 5 | — | — | ||||||||||||||

| Net asset value, end of period | $37.31 | $42.47 | $31.16 | $20.19 | $56.65 | $65.60 | ||||||||||||||||||

| Market price, end of period | $31.33 | $35.77 | $26.69 | $16.31 | $50.05 | $59.60 | ||||||||||||||||||

| Total return, based on NAV6,7 |

(9.33) | % | 44.33 | % | 64.74 | % | (60.86) | % | (5.27) | % | 4.08 | % | ||||||||||||

| Total return, based on Market Price8 |

(9.01) | % | 43.36 | % | 76.05 | % | (63.33) | % | (6.81) | % | 3.39 | % | ||||||||||||

| Net assets applicable to common shareholders, end of period (millions) | $496 | $571 | $422 | $281 | $798 | $924 | ||||||||||||||||||

| Ratios to average net assets: | ||||||||||||||||||||||||

| Management fees |

1.47 | %9 | 1.42 | % | 1.41 | % | 1.53 | % | 1.49 | % | 1.47 | % | ||||||||||||

| Other expenses |

3.05 | 9 | 1.61 | 1.66 | 3.87 | 10 | 2.08 | 1.94 | ||||||||||||||||

| Subtotal |

4.52 | 9 | 3.03 | 3.07 | 5.40 | 10 | 3.57 | 3.41 | ||||||||||||||||

| Income tax expenses |

0.72 | 11 | 0.35 | — | 12 | — | 12 | — | 12 | — | 12 | |||||||||||||

| Total gross expenses |

5.24 | 13,14 | 3.38 | 3.07 | 5.40 | 10 | 3.57 | 3.41 | ||||||||||||||||

| Total net expenses |

5.17 | 13,14,15 | 3.31 | 15 | 3.01 | 15 | 5.39 | 10,15 | 3.57 | 3.41 | ||||||||||||||

| Net investment income (loss), net of income taxes |

(2.43) | 13 | (1.11) | (0.24) | (2.89) | 10 | (0.80) | 1.88 | ||||||||||||||||

| Portfolio turnover rate | 27 | % | 53 | % | 48 | % | 16 | % | 33 | % | 14 | % | ||||||||||||

See Notes to Financial Statements.

| 8 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

| For a common share of capital stock outstanding throughout each year ended November 30, unless otherwise noted: |

||||||||||||||||||||||||

| 20231,2 | 20221 | 20211 | 20201,3 | 20191,3 | 20181,3 | |||||||||||||||||||

| Supplemental data: | ||||||||||||||||||||||||

| Loan and Debt Issuance Outstanding, End of Period (000s) |

$192,282 | $185,282 | $148,309 | $76,107 | $347,607 | $421,000 | ||||||||||||||||||

| Asset Coverage Ratio for Loan and Debt Issuance Outstanding16 |

388 | % | 443 | % | 411 | % | 542 | % | 345 | % | 332 | % | ||||||||||||

| Asset Coverage, per $1,000 Principal Amount of Loan and Debt Issuance Outstanding16 |

$3,878 | $4,429 | $4,107 | $5,421 | $3,454 | $3,324 | ||||||||||||||||||

| Weighted Average Loan and Debt Issuance (000s) |

$191,205 | $176,718 | $121,077 | $163,529 | $395,909 | $432,329 | ||||||||||||||||||

| Weighted Average Interest Rate on Loan and Debt Issuance |

5.14 | % | 2.95 | % | 2.75 | % | 6.58 | %17 | 3.77 | % | 3.67 | % | ||||||||||||

| Mandatory Redeemable Preferred Stock at Liquidation Value, End of Period (000s) |

$57,400 | $63,800 | $38,800 | $55,000 | $55,000 | $55,000 | ||||||||||||||||||

| Asset Coverage Ratio for Mandatory Redeemable Preferred Stock18 |

299 | % | 329 | % | 325 | % | 315 | % | 298 | % | 294 | % | ||||||||||||

| Asset Coverage, per $100,000 Liquidation Value per Share of Mandatory Redeemable Preferred Stock18 |

$298,648 | $329,423 | $325,500 | $314,709 | $298,242 | $294,013 | ||||||||||||||||||

| Asset Coverage, per $35 Liquidation Value per Share of Mandatory Redeemable Preferred Stock18 |

$105 | $115 | — | — | — | — | ||||||||||||||||||

See Notes to Financial Statements.

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 9 |

Financial highlights (cont’d)

| 1 | Per share amounts have been calculated using the average shares method. |

| 2 | For the six months ended May 31, 2023 (unaudited). |

| 3 | On July 28, 2020, the Fund completed a 1-for-5 reverse stock split. Prior year per share amounts have been restated to reflect the impact of the reverse stock split. |

| 4 | The actual source of the Fund’s current fiscal year distributions may be from dividends, return of capital or a combination of both. Shareholders will be informed of the tax characteristics of the distributions after the close of the fiscal year. |

| 5 | The repurchase plan was completed at an average repurchase price of $33.13 for 161,000 shares and $5,334,424 for the six months ended May 31, 2023, $33.40 for 84,000 shares and $2,805,578 for the year ended November 30, 2022, $23.78 for 402,851 shares and $9,578,283 for the year ended November 30, 2021 and $7.63 for 290,885 shares and $2,219,316 for the year ended November 30, 2020. |

| 6 | Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

| 7 | The total return calculation assumes that distributions are reinvested at NAV. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

| 8 | The total return calculation assumes that distributions are reinvested in accordance with the Fund’s dividend reinvestment plan. Past performance is no guarantee of future results. Total returns for periods of less than one year are not annualized. |

| 9 | Annualized. |

| 10 | Includes non-recurring prepayment penalties and the write-off of debt issuance and offering costs recognized during the period totaling 1.24% of average net assets. |

| 11 | Not annualized. |

| 12 | For the years ended November 30, 2021, 2020, 2019 and 2018, the net income tax benefit was 0.92%, 7.62%, 1.65% and 6.18%, respectively. The net income tax benefit is not reflected in the Fund’s expense ratios. |

| 13 | Annualized, except for income tax expenses. |

| 14 | Included in the expense ratios are certain non-recurring legal and transfer agent fees that were incurred by the Fund during the period. Without these fees, the gross and net expense ratios would have been 4.97% and 4.90%, respectively. |

| 15 | Reflects fee waivers and/or expense reimbursements. |

| 16 | Represents value of net assets plus the loan outstanding, debt issuance outstanding and mandatory redeemable preferred stock at the end of the period divided by the loan and debt issuance outstanding at the end of the period. |

| 17 | Includes prepayment penalties recognized during the period. |

| 18 | Represents value of net assets plus the loan outstanding, debt issuance outstanding and mandatory redeemable preferred stock at the end of the period divided by the loan, debt issuance and mandatory redeemable preferred stock outstanding at the end of the period. |

See Notes to Financial Statements.

| 10 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

Notes to financial statements (unaudited)

1. Organization and significant accounting policies

ClearBridge MLP and Midstream Fund Inc. (the “Fund”) was incorporated in Maryland on March 31, 2010 and is registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Board of Directors authorized 99,285,389 shares of $0.001 par value common stock. The Fund’s investment objective is to provide a high level of total return with an emphasis on cash distributions. The Fund seeks to achieve its objective by investing primarily in energy master limited partnerships (“MLPs”) and energy midstream entities. There can be no assurance that the Fund will achieve its investment objective.

Under normal market conditions, the Fund invests at least 80% of its Managed Assets in energy MLPs and energy midstream entities (the 80% policy). For purposes of the 80% policy, the Fund considers investments in MLPs to include investments that offer economic exposure to public and private MLPs in the form of MLP equity securities, securities of entities holding primarily general partner or managing member interests in MLPs, securities that are derivatives of interests in MLPs (including I-Shares), exchange-traded funds that primarily hold MLP interests and debt securities of MLPs. For purposes of the 80% policy, the Fund considers investments in midstream entities as direct or indirect investments in those entities that provide midstream services including the gathering, transporting, processing, fractionation, storing, refining, and distribution of oil, natural gas liquids, natural gas and refined petroleum products. The Fund considers an entity to be within the energy sector if it derives at least 50% of its revenues from the business of exploring, developing, producing, gathering, fractionating, transporting, processing, storing, refining, distributing, mining or marketing natural gas, natural gas liquids (including propane), crude oil, refined petroleum products or coal. The Fund may also invest up to 20% of its managed assets in other securities that are not MLPs or midstream entities. “Managed Assets” means net assets plus the amount of borrowings and assets attributable to any preferred stock of the Fund that may be outstanding.

The Fund follows the accounting and reporting guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946, Financial Services – Investment Companies (“ASC 946”). The following are significant accounting policies consistently followed by the Fund and are in conformity with U.S. generally accepted accounting principles (“GAAP”), including, but not limited to, ASC 946. Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ. Subsequent events have been evaluated through the date the financial statements were issued.

(a) Investment valuation. Equity securities for which market quotations are available are valued at the last reported sales price or official closing price on the primary market or exchange on which they trade. The valuations for fixed income securities (which may include, but are not limited to, corporate, government, municipal, mortgage-backed, collateralized mortgage obligations and asset-backed securities) and certain derivative

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 11 |

Notes to financial statements (unaudited) (cont’d)

instruments are typically the prices supplied by independent third party pricing services, which may use market prices or broker/dealer quotations or a variety of valuation techniques and methodologies. The independent third party pricing services typically use inputs that are observable such as issuer details, interest rates, yield curves, prepayment speeds, credit risks/spreads, default rates and quoted prices for similar securities. Investments in open-end funds are valued at the closing net asset value per share of each fund on the day of valuation. When the Fund holds securities or other assets that are denominated in a foreign currency, the Fund will normally use the currency exchange rates as of 4:00 p.m. (Eastern Time). If independent third party pricing services are unable to supply prices for a portfolio investment, or if the prices supplied are deemed by the manager to be unreliable, the market price may be determined by the manager using quotations from one or more broker/dealers or at the transaction price if the security has recently been purchased and no value has yet been obtained from a pricing service or pricing broker. When reliable prices are not readily available, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Fund calculates its net asset value, the Fund values these securities as determined in accordance with procedures approved by the Fund’s Board of Directors.

Pursuant to policies adopted by the Board of Directors, the Fund’s manager has been designated as the valuation designee and is responsible for the oversight of the daily valuation process. The Fund’s manager is assisted by the Global Fund Valuation Committee (the “Valuation Committee”). The Valuation Committee is responsible for making fair value determinations, evaluating the effectiveness of the Fund’s pricing policies, and reporting to the Fund’s manager and the Board of Directors. When determining the reliability of third party pricing information for investments owned by the Fund, the Valuation Committee, among other things, conducts due diligence reviews of pricing vendors, monitors the daily change in prices and reviews transactions among market participants.

The Valuation Committee will consider pricing methodologies it deems relevant and appropriate when making fair value determinations. Examples of possible methodologies include, but are not limited to, multiple of earnings; discount from market of a similar freely traded security; discounted cash-flow analysis; book value or a multiple thereof; risk premium/yield analysis; yield to maturity; and/or fundamental investment analysis. The Valuation Committee will also consider factors it deems relevant and appropriate in light of the facts and circumstances. Examples of possible factors include, but are not limited to, the type of security; the issuer’s financial statements; the purchase price of the security; the discount from market value of unrestricted securities of the same class at the time of purchase; analysts’ research and observations from financial institutions; information regarding any transactions or offers with respect to the security; the existence of merger proposals or tender offers affecting the security; the price and extent of public trading in similar securities of the issuer or comparable companies; and the existence of a shelf registration for restricted securities.

| 12 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

For each portfolio security that has been fair valued pursuant to the policies adopted by the Board of Directors, the fair value price is compared against the last available and next available market quotations. The Valuation Committee reviews the results of such back testing monthly and fair valuation occurrences are reported to the Board of Directors quarterly.

The Fund uses valuation techniques to measure fair value that are consistent with the market approach and/or income approach, depending on the type of security and the particular circumstance. The market approach uses prices and other relevant information generated by market transactions involving identical or comparable securities. The income approach uses valuation techniques to discount estimated future cash flows to present value.

GAAP establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

| • | Level 1 — unadjusted quoted prices in active markets for identical investments |

| • | Level 2 — other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| • | Level 3 — significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used in valuing the Fund’s assets carried at fair value:

| ASSETS | ||||||||||||||||

| Description | Quoted Prices (Level 1) |

Other Significant Observable Inputs (Level 2) |

Significant Unobservable Inputs (Level 3) |

Total | ||||||||||||

| Long-Term Investments†: | ||||||||||||||||

| Master Limited Partnerships |

$ | 509,026,592 | — | — | $ | 509,026,592 | ||||||||||

| Common Stocks |

228,231,472 | — | — | 228,231,472 | ||||||||||||

| Total Long-Term Investments | 737,258,064 | — | — | 737,258,064 | ||||||||||||

| Short-Term Investments† | 6,262,518 | — | — | 6,262,518 | ||||||||||||

| Total Investments | $ | 743,520,582 | — | — | $ | 743,520,582 | ||||||||||

| † | See Schedule of Investments for additional detailed categorizations. |

(b) Net asset value. The Fund determines the net asset value of its common stock on each day the NYSE is open for business, as of the close of the customary trading session (normally 4:00 p.m. Eastern Time), or any earlier closing time that day. The Fund determines the net asset value per share of common stock by dividing the value of the Fund’s securities,

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 13 |

Notes to financial statements (unaudited) (cont’d)

cash and other assets (including interest accrued but not collected) less all its liabilities (including accrued expenses, borrowings, interest payables and the aggregate liquidation value (i.e., $100,000 and $35 per outstanding share) of the Mandatory Redeemable Preferred Stock (“MRPS”)), net of income taxes, by the total number of shares of common stock outstanding.

(c) Master limited partnerships. Entities commonly referred to as “MLPs” are generally organized under state law as limited partnerships or limited liability companies. The Fund intends to primarily invest in MLPs receiving partnership taxation treatment under the Internal Revenue Code of 1986, as amended (the “Code”), and whose interests or “units” are traded on securities exchanges like shares of corporate stock. To be treated as a partnership for U.S. federal income tax purposes, an MLP whose units are traded on a securities exchange must receive at least 90% of its income from qualifying sources such as interest, dividends, real estate rents, gain from the sale or disposition of real property, income and gain from mineral or natural resources activities, income and gain from the transportation or storage of certain fuels, and, in certain circumstances, income and gain from commodities or futures, forwards and options with respect to commodities. Mineral or natural resources activities include exploration, development, production, processing, mining, refining, marketing and transportation (including pipelines) of oil and gas, minerals, geothermal energy, fertilizer, timber or industrial source carbon dioxide. An MLP consists of a general partner and limited partners (or in the case of MLPs organized as limited liability companies, a managing member and members). The general partner or managing member typically controls the operations and management of the MLP and has an ownership stake in the partnership. The limited partners or members, through their ownership of limited partner or member interests, provide capital to the entity, are intended to have no role in the operation and management of the entity and receive cash distributions. The MLPs themselves generally do not pay U.S. federal income taxes. Thus, unlike investors in corporate securities, direct MLP investors are generally not subject to double taxation (i.e., corporate level tax and tax on corporate dividends). Currently, most MLPs operate in the energy and/or natural resources sector.

(d) Foreign currency translation. Investment securities and other assets and liabilities denominated in foreign currencies are translated into U.S. dollar amounts based upon prevailing exchange rates on the date of valuation. Purchases and sales of investment securities and income and expense items denominated in foreign currencies are translated into U.S. dollar amounts based upon prevailing exchange rates on the respective dates of such transactions.

The Fund does not isolate that portion of the results of operations resulting from fluctuations in foreign exchange rates on investments from the fluctuations arising from changes in market prices of securities held. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

Net realized foreign exchange gains or losses arise from sales of foreign currencies, including gains and losses on forward foreign currency contracts, currency gains or losses

| 14 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

realized between the trade and settlement dates on securities transactions, and the difference between the amounts of dividends, interest, and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Net unrealized foreign exchange gains and losses arise from changes in the values of assets and liabilities, other than investments in securities, on the date of valuation, resulting from changes in exchange rates.

Foreign security and currency transactions may involve certain considerations and risks not typically associated with those of U.S. dollar denominated transactions as a result of, among other factors, the possibility of lower levels of governmental supervision and regulation of foreign securities markets and the possibility of political or economic instability.

(e) Foreign investment risks. The Fund’s investments in foreign securities may involve risks not present in domestic investments. Since securities may be denominated in foreign currencies, may require settlement in foreign currencies or may pay interest or dividends in foreign currencies, changes in the relationship of these foreign currencies to the U.S. dollar can significantly affect the value of the investments and earnings of the Fund. Foreign investments may also subject the Fund to foreign government exchange restrictions, expropriation, taxation or other political, social or economic developments, all of which affect the market and/or credit risk of the investments.

(f) Concentration risk. Concentration in the energy sector may present more risks than if the Fund were broadly diversified over numerous sectors of the economy. A downturn in the energy sector of the economy could have a larger impact on the Fund than on an investment company that does not concentrate in the sector. At times, the performance of securities of companies in the sector may lag the performance of other sectors or the broader market as a whole.

(g) Security transactions and investment income. Security transactions are accounted for on a trade date basis. Interest income (including interest income from payment-in-kind securities), adjusted for amortization of premium and accretion of discount, is recorded on the accrual basis. Dividend income is recorded on the ex-dividend date for dividends received in cash and/or securities. Foreign dividend income is recorded on the ex-dividend date or as soon as practicable after the Fund determines the existence of a dividend declaration after exercising reasonable due diligence. The cost of investments sold is determined by use of the specific identification method. To the extent any issuer defaults or a credit event occurs that impacts the issuer, the Fund may halt any additional interest income accruals and consider the realizability of interest accrued up to the date of default or credit event.

(h) Return of capital estimates. Distributions received from the Fund’s investments in MLPs generally are comprised of income and return of capital. The Fund records investment income and return of capital based on estimates made at the time such distributions are received. Such estimates are based on historical information available from each MLP and

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 15 |

Notes to financial statements (unaudited) (cont’d)

other industry sources. These estimates may subsequently be revised based on information received from the MLPs after their tax reporting periods are concluded.

For the six months ended May 31, 2023, the Fund estimated that approximately 76% of the MLP distributions received would be treated as a return of capital. The Fund recorded as return of capital the amount of $21,914,255 of dividends and distributions received from its investments.

Additionally, the Fund updated the return of capital estimates from the year ended November 30, 2022 based on actual amounts subsequently reported to the Fund. This resulted in an increase of $227,537 in net dividends and distributions received from investments.

(i) Partnership accounting policy. The Fund records its pro rata share of the income (loss) and capital gains (losses), to the extent of distributions it has received, allocated from the underlying partnerships and accordingly adjusts the cost basis of the underlying partnerships for return of capital. These amounts are included in the Fund’s Statement of Operations.

(j) Distributions to shareholders. Distributions to common shareholders are declared and paid on a quarterly basis and are recorded on the ex-dividend date. The estimated characterization of the distributions paid to common shareholders will be either a dividend (ordinary income), distribution (return of capital) or combination of both. This estimate is based on the Fund’s operating results during the period. The Fund anticipates that 100% of its current period distributions will be comprised of return of capital. The actual tax characterization of the common stock distributions made during the current year will not be determined until after the end of the fiscal year when the Fund can determine its earnings and profits and, therefore, may differ from the preliminary estimates.

Distributions to holders of MRPS are accrued on a daily basis as described in Note 7 and are treated as an operating expense as required by GAAP. For tax purposes, the payments made to the holders of the Fund’s MRPS are treated as a dividend (ordinary income) or distribution (return of capital) similar to the treatment of distributions made to common shareholders as described above. The Fund anticipates that 100% of its current period distributions to the MRPS shareholders will be treated as return of capital. The actual tax characterization of the MRPS distributions made during the current year will not be determined until after the end of the fiscal year when the Fund can determine its earnings and profits and, therefore, may differ from the preliminary estimates.

(k) Compensating balance arrangements. The Fund has an arrangement with its custodian bank whereby a portion of the custodian’s fees is paid indirectly by credits earned on the Fund’s cash on deposit with the bank.

(l) Federal and other taxes. The Fund, as a corporation, is obligated to pay federal and state income tax on its taxable income. The Fund invests its assets primarily in MLPs, which generally are treated as partnerships for federal income tax purposes. As a limited partner

| 16 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

in the MLPs, the Fund includes its allocable share of the MLP’s taxable income in computing its own taxable income. The Fund, and entities in which the Fund invests, may be subject to audit by the Internal Revenue Service or other applicable tax authorities. The Fund’s taxable income or tax liability for prior taxable years could be adjusted if there is an audit of the Fund, or of any entity that is treated as a partnership for tax purposes in which the Fund holds an equity interest. The Fund may be required to pay tax, as well as interest and penalties, in connection with such an adjustment.

Deferred income taxes reflect (i) taxes on unrealized gains (losses), which are attributable to the temporary difference between fair market value and book basis, (ii) the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes and, as applicable, (iii) the net tax benefit of accumulated net operating losses, capital losses and tax credit carryforwards. To the extent the Fund has a deferred tax asset, consideration is given as to whether or not a valuation allowance is required. The need to establish a valuation allowance for deferred tax assets is assessed periodically by management of the Fund based on Financial Accounting Standards Board (“FASB”), Accounting Standards Codification Topic 740, Income Taxes (“ASC 740”) that it is more likely than not that some portion or all of the deferred tax asset will not be realized. In the assessment for a valuation allowance, consideration is given to all positive and negative evidence related to the realization of the deferred tax asset. This assessment considers, among other matters, the nature, frequency and severity of current and cumulative losses, forecasts of future profitability (which are highly dependent on future allocations of taxable income and future cash distributions from the Fund’s MLP holdings), the duration of statutory carryforward periods and the associated risk that net operating losses, capital losses and tax credit carryforwards may expire unused.

For all open tax years and for all major jurisdictions, management of the Fund has concluded that there are no significant uncertain tax positions that would require recognition in the financial statements. Furthermore, management of the Fund is also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

The Fund may rely to some extent on information provided by the MLPs, which may not necessarily be timely, to estimate taxable income and gains allocable from the MLP units held in the portfolio and to estimate the associated deferred tax liability. Such estimates are made in good faith. From time to time, as new information becomes available, the Fund modifies its estimates or assumptions regarding the current and deferred tax liabilities.

The Fund’s policy is to classify interest and penalties associated with underpayment of federal and state income taxes, if any, as income tax expense on its Statement of Operations. The 2018 through 2022 tax years remain open and subject to examination by tax jurisdictions.

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 17 |

Notes to financial statements (unaudited) (cont’d)

(m) Reclassification. GAAP requires that certain components of net assets be reclassified to reflect permanent differences between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share. During the current period, the Fund had no reclassifications.

2. Investment management agreement and other transactions with affiliates

Legg Mason Partners Fund Advisor, LLC (“LMPFA”) is the Fund’s investment manager and ClearBridge Investments, LLC (“ClearBridge”) is the Fund’s subadviser. LMPFA and ClearBridge are indirect, wholly-owned subsidiaries of Franklin Resources, Inc. (“Franklin Resources”).

Under the investment management agreement, the Fund pays LMPFA an annual fee, paid monthly, in an amount equal to 1.00% of the Fund’s average daily Managed Assets.

LMPFA provides administrative and certain oversight services to the Fund. LMPFA delegates to the subadviser the day-to-day portfolio management of the Fund. For its services, LMPFA pays ClearBridge a fee monthly, at an annual rate equal to 70% of the net management fee it receives from the Fund.

During periods in which the Fund utilizes financial leverage, the fees paid to LMPFA will be higher than if the Fund did not utilize leverage because the fees are calculated as a percentage of the Fund’s assets, including those investments purchased with leverage.

Effective March 1, 2021, LMPFA implemented a voluntary investment management fee waiver of 0.05% that will continue until May 31, 2024.

During the six months ended May 31, 2023, fees waived and/or expenses reimbursed amounted to $194,006.

All officers and one Director of the Fund are employees of Franklin Resources or its affiliates and do not receive compensation from the Fund.

3. Investments

During the six months ended May 31, 2023, the aggregate cost of purchases and proceeds from sales of investments (excluding short-term investments) were as follows:

| Purchases | $ | 217,237,650 | ||

| Sales | 210,022,266 |

4. Derivative instruments and hedging activities

During the six months ended May 31, 2023, the Fund did not invest in derivative instruments.

5. Loan

The Fund has a revolving credit agreement with The Bank of Nova Scotia (“Credit Agreement”), which allows the Fund to borrow up to an aggregate amount of $195,000,000. The Credit Agreement is subject to a scheduled commitment termination date of

| 18 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

December 13, 2023. The Fund pays a commitment fee on the unutilized portion of the loan commitment amount at an annual rate of 0.25%, except that the commitment fee is 0.15% in the event that the aggregate outstanding principal balance of the loan is equal to or greater than 75% of the current commitment amount. The interest on the loan is calculated at a variable rate based on adjusted Term SOFR plus any applicable margin. Securities held by the Fund are subject to a lien, granted to The Bank of Nova Scotia, to the extent of the borrowing outstanding and any additional expenses. The Fund’s Credit Agreement contains customary covenants that, among other things, may limit the Fund’s ability to pay distributions in certain circumstances, incur additional debt, change its fundamental investment policies and engage in certain transactions, including mergers and consolidations and require asset coverage ratios in addition to those required by the 1940 Act. In addition, the Credit Agreement may be subject to early termination under certain conditions and may contain other provisions that could limit the Fund’s ability to utilize borrowing under the agreement. At May 31, 2023, the Fund had $138,000,000 of borrowings outstanding per this Credit Agreement. Interest expense related to this loan for the six months ended May 31, 2023 was $3,923,537. For the six months ended May 31, 2023, the Fund incurred commitment fees of $73,402. For the six months ended May 31, 2023, the average daily loan balance was $136,923,077 and the weighted average interest rate was 5.67%.

6. Senior secured notes

At May 31, 2023, the Fund had $54,282,189 aggregate principal amount of fixed-rate senior secured notes (“Senior Notes”) outstanding. Interest expense related to the Senior Notes for the six months ended May 31, 2023 was $1,046,116. Costs incurred by the Fund in connection with the Senior Notes are recorded as a deferred charge and are amortized over the life of the notes. Securities held by the Fund are subject to a lien, granted to the Senior Notes holders, to the extent of the borrowings outstanding and any additional expenses. The Senior Notes holders and the lender have equal access to the lien (See Note 5).

The table below summarizes the key terms of each series of Senior Notes at May 31, 2023.

| Security | Amount | Rate | Maturity | Estimated Fair Value |

||||||||||||

| Senior secured notes: | ||||||||||||||||

| Series D | $ | 16,788,306 | 4.21 | % | July 12, 2024 | $ | 16,286,232 | |||||||||

| Series A | 9,326,836 | 3.65 | % | June 6, 2023 | 9,004,255 | |||||||||||

| Series B | 9,326,836 | 3.78 | % | June 6, 2025 | 8,840,068 | |||||||||||

| Series A | 2,984,588 | 4.20 | % | April 30, 2026 | 2,818,246 | |||||||||||

| Series I | 4,663,419 | 3.46 | % | June 11, 2025 | 4,392,924 | |||||||||||

| Series J | 4,663,419 | 3.56 | % | June 11, 2027 | 4,238,671 | |||||||||||

| Series K | 6,528,785 | 3.76 | % | June 11, 2030 | 5,662,712 | |||||||||||

| $ | 54,282,189 | $ | 51,243,108 | |||||||||||||

The Senior Notes are not listed on any exchange or automated quotation system. The estimated fair value of the Senior Notes was calculated, for disclosure purposes, based on

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 19 |

Notes to financial statements (unaudited) (cont’d)

estimated market yields and credit spreads for comparable instruments with similar maturity, terms and structure. The Senior Notes are categorized as Level 3 within the fair value hierarchy.

7. Mandatory redeemable preferred stock

At May 31, 2023, the Fund had 714,611 shares of fixed rate MRPS outstanding with an aggregate liquidation value of $57,400,045. Offering costs incurred by the Fund in connection with the MRPS issuance are being amortized to expense over the respective life of each series of MRPS.

On January 8, 2023, which was the scheduled redemption date, the Fund redeemed 64 shares of Series H MRPS at a liquidation value of $6,400,000 plus any accumulated unpaid dividends.

The table below summarizes the key terms of each series of the MRPS at May 31, 2023.

| Series | Term Redemption Date |

Rate | Shares | Liquidation Preference Per Share |

Aggregate Liquidation Value |

Estimated Fair Value |

||||||||||||||||||

| Series I | 6/11/2025 | 4.16 | % | 160 | $ | 100,000 | $ | 16,000,000 | $ | 15,136,092 | ||||||||||||||

| Series J | 6/11/2025 | 4.16 | % | 82 | 100,000 | 8,200,000 | 7,757,247 | |||||||||||||||||

| Series K | 6/11/2027 | 4.26 | % | 82 | 100,000 | 8,200,000 | 7,517,513 | |||||||||||||||||

| Series L | 11/17/2029 | 7.12 | % | 428,572 | 35 | 15,000,020 | 15,393,525 | |||||||||||||||||

| Series M | 11/17/2032 | 7.28 | % | 285,715 | 35 | 10,000,025 | 10,408,951 | |||||||||||||||||

| $ | 57,400,045 | $ | 56,213,328 | |||||||||||||||||||||

The MRPS are not listed on any exchange or automated quotation system. The estimated fair value of the MRPS was calculated, for disclosure purposes, based on estimated market yields and credit spreads for comparable instruments with similar maturity, terms and structure. The MRPS are categorized as Level 3 within the fair value hierarchy.

Holders of MRPS are entitled to receive quarterly cumulative cash dividends payable on the first business day following each quarterly dividend date (February 15, May 15, August 15 and November 15). In the event of a rating downgrade of any series of the MRPS below “A” by a nationally recognized statistical ratings organization (“NRSRO”) then providing a rating, the applicable dividend rate will increase by 0.5% to 4.0% according to a predetermined schedule.

The MRPS rank senior to the Fund’s outstanding common stock and on parity with any other preferred stock. The Fund may, at its option, redeem the MRPS, in whole or in part, at the liquidation preference amount plus all accumulated but unpaid dividends plus the make whole amount equal to the discounted value of the remaining scheduled payments. If the Fund fails to maintain a total leverage (debt and preferred stock) asset coverage ratio of at least 225% or, if applicable, is in default of specified rating agency requirements, the MRPS are subject to mandatory redemption and penalties under certain provisions.

| 20 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

The Fund may not declare dividends or make other distributions on shares of its common stock unless the Fund has declared and paid full cumulative dividends on the MRPS, due on or prior to the date of the common stock dividend or distribution, and meets the MRPS asset coverage and, if applicable, rating agency requirements.

The holders of Series L and Series M MRPS have one vote per share and the holders of Series I, Series J and Series K MRPS have one vote for every $35.00 of liquidation preference held. Holders of MRPS vote together with the holders of common stock of the Fund as a single class, except on matters affecting only the holders of MRPS or the holders of common stock. Pursuant to the 1940 Act, holders of the MRPS have the right to elect two Directors of the Fund, voting separately as a class.

8. Stock repurchase program

On November 16, 2015, the Fund announced that the Fund’s Board of Directors (the “Board”) had authorized the Fund to repurchase in the open market up to approximately 10% of the Fund’s outstanding common stock when the Fund’s shares are trading at a discount to net asset value. On July 29, 2022, the Fund announced that the Board had authorized the amendment of the Fund’s repurchase program under which the Fund may continue to repurchase in the open market up to an additional 10% of the Fund’s outstanding common stock when the Fund’s shares are trading at a discount to net asset value. The Board has directed management of the Fund to continue to repurchase shares of common stock at such times and in such amounts as management reasonably believes may enhance stockholder value. The Fund is under no obligation to purchase shares at any specific discount levels or in any specific amounts.

During the six months ended May 31, 2023, the Fund repurchased and retired 1.14% of its common shares outstanding under the repurchase plan. The weighted average discount per share on these repurchases was 14.63% for the six months ended May 31, 2023. During the year ended November 30, 2022, the Fund repurchased and retired 0.60% of its common shares outstanding under the repurchase plan. The weighted average discount per share on these repurchases was 17.88% for the year ended November 30, 2022. Shares repurchased and the corresponding dollar amount are included in the Statements of Changes in Net Assets. The anti-dilutive impact of these share repurchases is included in the Financial Highlights.

Since the commencement of the stock repurchase program through May 31, 2023, the Fund repurchased 938,736 shares or 5.60% of its common shares outstanding for a total amount of $19,937,601.

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 21 |

Notes to financial statements (unaudited) (cont’d)

9. Income taxes

The Fund’s federal and state income tax provisions consist of the following:

| Federal | State | Total | ||||||||||

| Current tax expense (benefit) | $ | 3,533,461 | $ | 261,139 | $ | 3,794,600 | ||||||

| Deferred tax expense (benefit) | — | — | — | |||||||||

| Total tax expense (benefit) | $ | 3,533,461 | $ | 261,139 | $ | 3,794,600 | ||||||

Total income taxes have been computed by applying the U.S. federal statutory income tax rate of 21% plus a blended net state income tax rate of 1.2%. The Fund applied this rate to net investment income (loss) and realized and unrealized gains (losses) on investments before income taxes in computing its total income tax expense (benefit).

The provision for income taxes differs from the amount derived from applying the statutory income tax rate to net investment income (loss) and realized and unrealized gains (losses) before income taxes as follows:

| Provision at statutory rates | 21.00 | % | $ | (10,381,093) | ||||

| State taxes, net of federal tax benefit | 1.20 | % | (593,205) | |||||

| Non-deductible distributions on MRPS, dividends received deduction and other, net (federal and state) | (0.15) | % | 73,430 | |||||

| Change in valuation allowance | (29.73) | % | 14,695,468 | |||||

| Total tax expense (benefit) | (7.68) | % | $ | 3,794,600 |

Components of the Fund’s net deferred tax asset (liability) as of May 31, 2023 are as follows:

| Deferred tax assets | ||||

| Net operating loss carryforward | $ | 3,832,525 | ||

| Capital loss carryforward | 44,126,017 | |||

| Other deferred tax assets | 3,269,017 | |||

| Deferred tax liabilities | ||||

| Unrealized gains on investment securities | (10,100,217) | |||

| Basis reduction resulting from differences in the book vs. taxable income received from MLPs | (22,973,474) | |||

| Net deferred tax asset (liability) before valuation allowance | 18,153,868 | |||

| Less: Valuation allowance | (18,153,868) | |||

| Total net deferred tax asset (liability) | — | |||

At May 31, 2023, the Fund had federal and state net operating loss carryforwards of $17,016,897 and $5,802,441 (net of state apportionment), respectively (deferred tax asset of $3,832,525). Several states compute net operating losses before apportionment, therefore the value of the state net operating loss carryforward disclosed may fluctuate for changes in apportionment factors. Realization of the deferred tax asset related to the net operating loss carryforward is dependent, in part, on generating sufficient taxable income in each respective jurisdiction prior to expiration of the loss carryforward. If not utilized, the state

| 22 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

net operating loss carryforward either expires in tax years between 2029 and 2042 or has an indefinite carryforward. The federal net operating loss carryforward does not have an expiration.

Additionally, at May 31, 2023, the Fund had federal and state capital loss carryforwards of $198,765,844 (deferred tax asset of $44,126,017), which may be carried forward for 5 years. During the period ended May 31, 2023, the Fund utilized $6,540,792 of capital loss carryforward available from previous years. If not utilized, the capital loss carryforward expires in tax year 2024. For corporations, capital losses can only be used to offset capital gains and cannot be used to offset ordinary income. Therefore, the use of this capital loss carryforward is dependent upon the Fund generating sufficient net capital gains prior to the expiration of the loss carryforward.

The amount of net operating loss and capital loss carryforwards differed from the amounts disclosed in the prior year financial statements due to differences between the estimated and actual amounts of taxable income received from the MLPs for the prior year.

Cumulative net operating losses and capital losses incurred and expected to be incurred have resulted in the Fund having a net deferred tax asset as of May 31, 2023. Note 1(l) describes the assessment required under ASC 740 to determine whether a valuation allowance for deferred tax assets is necessary using a more likely than not standard of realizability. Based on that assessment, management has determined that the Fund is not expected to be able to generate significant future taxable income of the appropriate character in order to realize its deferred tax assets, and accordingly has determined that a full valuation allowance on its net deferred tax asset is appropriate at this time. The capital loss carryforward is a material component of the net deferred tax asset and also has a five-year expiration. If in the future, a valuation allowance is required to reserve against an individual deferred tax asset, such as the capital loss carryforward, it could have a material impact on the Fund’s net asset value and results of operations in the period it is recorded.

At May 31, 2023, the cost basis of investments for Federal income tax purposes was $600,812,663. At May 31, 2023, gross unrealized appreciation and depreciation of investments for Federal income tax purposes were as follows:

| Gross unrealized appreciation | $ | 180,724,033 | ||

| Gross unrealized depreciation | (38,016,114) | |||

| Net unrealized appreciation (depreciation) before tax | $ | 142,707,919 | ||

| Net unrealized appreciation (depreciation) after tax | $ | 111,026,761 |

10. Recent accounting pronouncement and regulatory update

On August 16, 2022, President Biden signed the Inflation Reduction Act of 2022 (the “Act”) into law. The Act, among other things, imposes a nondeductible 1 percent excise tax on public company stock buybacks. This excise tax is applicable to the fair market value of stock repurchased after December 31, 2022, and may include both common and preferred stock. The Act also imposes a 15 percent corporate alternative minimum tax on the adjusted financial statement income of large corporations for taxable years beginning after

| ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report | 23 |

Notes to financial statements (unaudited) (cont’d)

December 31, 2022. Management anticipates forthcoming proposed regulations from the Treasury Department to determine the impact of the Act, however based on interim guidance currently does not believe such potential impact to be material to the Fund.

* * *

In June 2022, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2022-03, Fair Value Measurement (Topic 820) – Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions. The amendments in the ASU clarify that a contractual restriction on the sale of an equity security is not considered part of the unit of account of the equity security and, therefore, should not be considered in measuring fair value. The ASU is effective for interim and annual reporting periods beginning after December 15, 2023, with the option of early adoption. Management has reviewed the requirements and believes that the adoption of the ASU will not have a material impact on the financial statements.

11. Subsequent event

On July 21, 2023, the Fund was served with a complaint by Saba Capital Master Fund, Ltd. and Saba Capital Management, L.P. dated June 29, 2023 (the “Complaint”). The Complaint, filed with the United States District Court, Southern District of New York, alleges that the control share provisions of the Maryland Control Share Acquisition Act (“MCSAA”) that apply to the Fund under Maryland law violate the 1940 Act. The Complaint also asks the court to rescind the application of the MCSAA provisions to the Fund and a declaration that the MCSAA provisions are void. Fifteen other closed-end investment companies registered under the 1940 Act were also named in the Complaint. As of the date these financial statements were issued, the court has not ruled on these allegations or the plaintiffs’ related requests for judgment. At this time no reasonable estimate can be made as to the potential outcome of the complaint nor any possible loss or damage to the Fund.

| 24 | ClearBridge MLP and Midstream Fund Inc. 2023 Semi-Annual Report |

Board approval of management and subadvisory agreements (unaudited)

Background

The Investment Company Act of 1940, as amended (the “1940 Act”), requires that the Board of Directors (the “Board”) of ClearBridge MLP and Midstream Fund Inc. (the “Fund”), including a majority of its members who are not considered to be “interested persons” under the 1940 Act (the “Independent Directors”) voting separately, approve on an annual basis the continuation of the investment management agreement (the “Management Agreement”) between the Fund and the Fund’s manager, Legg Mason Partners Fund Advisor, LLC (the “Manager”), and the sub-advisory agreement (the “Sub-Advisory Agreement”) between the Manager and ClearBridge Investments, LLC (the “Sub-Adviser”), an affiliate of the Manager, with respect to the Fund.

At an in-person meeting (the “Contract Renewal Meeting”) held on May 9-10, 2023, the Board, including the Independent Directors, considered and approved the continuation of each of the Management Agreement and the Sub-Advisory Agreement for an additional one-year period. To assist in its consideration of the renewal of each of the Management Agreement and the Sub-Advisory Agreement, the Board received and considered extensive information (together with the information provided at the Contract Renewal Meeting, the “Contract Renewal Information”) about the Manager and the Sub-Adviser, as well as the management and sub-advisory arrangements for the Fund and the other closed-end funds in the same complex under the Board’s purview (the “Franklin Templeton/Legg Mason Closed-end Funds”), certain portions of which are discussed below.