UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________

Commission File Number: 000-55576

YANGTZE RIVER DEVELOPMENT LIMITED

(Exact name of registrant as specified in its charter)

| Nevada | 27-1636887 | |

State

or other jurisdiction |

(I.R.S.

Employer Identification No.) | |

183 Broadway, Suite 5 New York, NY United States |

10007 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: 646-861-3315

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange on which registered: | |

| None | None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.0001 per share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☒ No ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Accelerated filer | ☐ | Large accelerated filer | ☐ |

| Non-accelerated filer | ☐ (Do not check if a smaller reporting company) | Smaller reporting company | ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, as of the last business day of the registrant’s most recently completed second fiscal quarter: $5,343,998.

Number of the issuer’s common stock outstanding as of February 1, 2016: 172,254,446.

Documents incorporate by reference: None.

TABLE OF CONTENTS

| 2 |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Report”) contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements discuss matters that are not historical facts. Because they discuss future events or conditions, forward-looking statements may include words such as “anticipate,” “believe,” “estimate,” “intend,” “could,” “should,” “would,” “may,” “seek,” “plan,” “might,” “will,” “expect,” “predict,” “project,” “forecast,” “potential,” “continue” negatives thereof or similar expressions. These forward-looking statements are found at various places throughout this Report and include information concerning possible or assumed future results of our operations; business strategies; future cash flows; financing plans; plans and objectives of management; any other statements regarding future operations, future cash needs, business plans and future financial results, and any other statements that are not historical facts.

From time to time, forward-looking statements also are included in our other periodic reports on Forms 10-Q and 8-K, in our press releases, in our presentations, on our website and in other materials released to the public. Any or all of the forward-looking statements included in this Report and in any other reports or public statements made by us are not guarantees of future performance and may turn out to be inaccurate. These forward-looking statements represent our intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors. Many of those factors are outside of our control and could cause actual results to differ materially from the results expressed or implied by those forward-looking statements. In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than we have described. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Report. All subsequent written and oral forward-looking statements concerning other matters addressed in this Report and attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this Report.

Except to the extent required by law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, a change in events, conditions, circumstances or assumptions underlying such statements, or otherwise.

USE OF CERTAIN DEFINED TERMS

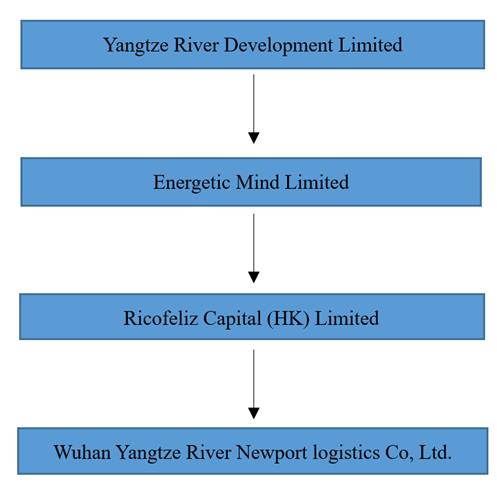

In this Report, unless otherwise noted or as the context otherwise requires, “Yangtze River”, the “Company,” “YERR,” “we,” “us,” and “our” refers to the combined business of Yangtze River Development Limited, a corporate formed under the laws of the State of Nevada, Energetic Mind Limited (“Energetic Mind”), which is our wholly-owned subsidiary formed under the laws of the British Virgin Islands (“BVI”), Energetic Mind’s wholly-owned subsidiary Ricofeliz Capital (HK) Ltd (“Ricofliz Capital”), a company formed under the laws of Hong Kong, and Ricofelix Capital’s wholly-owned subsidiary, Wuhan Yangtze River Newport Logistics Co., Ltd (“Wuhan Newport”), a wholly foreign-owned enterprise formed under the laws of the People’s Republic of China (“China”).

| 3 |

PART I

| Item 1. | Business. |

Overview

Yangtze River Development Limited is a Nevada corporation that operates through its wholly-owned subsidiary Ricofelix Capital, which operates through its wholly-owned subsidiary Wuhan Newport, a wholly foreign-owned enterprise that primarily engages in the business of real estate and infrastructural development with a port logistics project located in Wuhan, Hubei Province of China. Situated in the middle reaches of the Yangtze River, Wuhan Newport is a large infrastructure development project implemented under China's latest "One Belt One Road" initiative and is believed to be strategically positioned in the anticipated "Free Trade Zone" of the Wuhan Port, a crucial trading window between China, the Middle East and Europe. To be fully developed upon completion of three phases, within the logistics center, there will be six operating zones, including port operation area, warehouse and distribution area, cold chain logistics area, rail cargo loading area, exhibition area and residential community. The logistics center is also expected to provide a number of shipping berths for cargo ships of various sizes. Wuhan Newport is expected to provide domestic and foreign businesses a direct access to the anticipated Free Trade Zone in Wuhan. The project will include commercial buildings, professional logistic supply chain centers, direct access to the Yangtze River, Wuhan-Xinjiang-Europe Railway and ground transportation, storage and processing centers, IT supporting services, among others.

Wuhan Yangtze River Newport Logistics Center

One of the main projects of our Company is the Wuhan Yangtze River Newport Logistics Center (the “Logistics Center”), which is an extensive complex that is located in Wuhan, the capital of Hubei Province of China, a major transportation hub with dozens of railways, roads and expressways passing through the city and connecting to major cities in Mainland China, with connections to international centers of commerce and business.

The Logistics Center is expected to approximately a total of 474 Acres, for which the construction and development are expected to be completed in five years in three phases. It is expected to be located in the Wuhan Newport Yangluo Port, on the upper stream of the Yangtze River, and close to the northern base of Wu Iron and Steel, China's first supergiant iron and steel complex. The Logistics Center is expected to include a port that will be located approximately 26.5km to Wuhan Guan and 5.5km from the Yangluo Yangtze River Bridge. The operation area of the port is expected to consist of a riverbank of 1,039 meters with eight 5,000 to 10,000-ton berths, two of which are multi-purpose berths and the other six to general cargo berths. It is also designed to be able to handle up to five million tons of cargo and containers areas up to 100,000 TEU a year (including two freezers areas of 10,000 TEU).

Within the Logistics Center, functional areas will be divided into six operating zones, including a port operation area, a warehouse and distribution area, a cold chain supply logistics area, a rail cargo loading area, an exhibition area and a mixed residential and commercial community. The Logistics Center will also be complemented with container storage areas, multi-functional areas, general storage areas, multi-functional warehouse and infrastructural development, including new roads, gas stations, parking areas, gas and water pipes, electricity lines and all other facilities and equipment to operate the Logistics Center.

| 4 |

Aside from being situated in the Wuhan Yangluo Comprehensive Bonded Zone, Yangluo development area is amongst the third group of China’s Free-Trade Zone (FTZ) applicants to submit FTZ applications to the State Council through the Wuhan municipal government for approval. Approvals have so far been granted to Shanghai, Tianjin, Guangdong and Fujian. Enterprises within the approved free-trade zones are typically entitled to a series of favorable regulations and policies that could help the businesses grow and succeed.

Wuhan Newport has signed an agreement to rent 1.2 million square meters of land on a long term basis for building logistics warehouses covering 400,000 square meters in support of the new port. The warehouses is expected to comprise of port terminal zones, warehouse logistics zones, cold chain supply zones and railroad loading and unloading zones. The warehouses, once constructed, will connect the port terminal along the Yangtze River and the railway leading to Europe, satisfying the requirement of China’s latest “One Belt, One Road” initiative. It will also be able to support large logistics companies in Wuhan and other nearby provinces that lease the warehouses, terminals and offices.

Logistics Center Highlights:

| ● | The shipping center of Wuhan Newport will be implemented under China’s latest “One Belt, One Road” initiative to promote the "Yangtze River Economic Belt" | |

| ● | Wuhan Newport is part of the Yangluo port, which is part of the area that is currently seeking approval for status as a "Free-Trade Zone" | |

| ● | Wuhan Newport is part of the "Yangluo Comprehensive Bonded Zone", which allows the enterprises in the zone to receive certain favorable tax treatments such as export tax rebates and less or free of value-added tax and consumption tax |

The “One Belt, One Road” Initiative.

China’s “one belt one road” transportation infrastructure development strategy aiming to link Asia with Africa and Europe has spurred the development of more international air routes from second-tier cities such as Wuhan, Changsha, Xiamen and Urumqi. The belt manifests the continental dimension of this geo-strategic realm. The “Belt” consists of a network of rail routes, overland highways, oil and gas pipelines and other infrastructural projects, stretching from Xian in Western China, through Central Asia and into Russia, with one artery crossing Kazakhstan and the other through Mongolia but both linking up with the trans-Siberian railway and going on to Rotterdam.

The “Road” is the maritime dimension and consists of a network of ports and other coastal infrastructure from China’s eastern seaboard stretching across South East Asia, South Asia, the Gulf, East Africa and the Mediterranean, forming a loop terminating at Greece, Italy and Netherlands in Europe and Kenya in Africa.

The Belt and the Road run through the continents of Asia, Europe and Africa, connecting the vibrant East Asia economic circle at one end and developed European economic circle at the other, and encompassing countries with huge potential for economic development.

Chinese President Xi Jinping put forward the strategic conception of building the "Silk Road Economic Belt" and "21st Century Maritime Silk Road", known shortly as the "One Belt and One Road" initiatives in September, 2013. The proposal garnered the interest of the global community, as soon as it was announced. Various countries along the proposed route have expressed broad support, while domestic cities and provinces, which were part of the ancient Silk Road, have welcomed the idea. Over the past year, China and relevant countries, together with regional organizations, have put in a lot of efforts to jointly build the 'One Belt and One Road'. They have devised innovative methods to strengthen bilateral ties and enhance regional cooperation and have made impressive progress.

This visionary conception that leverages on China's historical connections has created a new opportunity to rejuvenate the economic and cultural ties built via the ancient Silk Road. It presents a "win-win approach" to peaceful coexistence and mutual development. The idea carries forward the spirit of the ancient Silk Road that was based on mutual trust, equality and mutual benefits, inclusiveness and mutual learning, and win-win cooperation. It also conforms to the 21st century norms of promoting peace, development, cooperation and adopting a win-win strategy for all. The conception organically links the "Chinese dream" to the "Global Dream" and has far-reaching strategic significance with a global impact.

Office Complex Project

Taking into consideration the Comprehensive Bonded Zone and Free Trade Zone status of the Logistic Center, Wuhan Newport has obtained the land use rights to own approximately 500,000 square meters of commercial lands on which Wuhan Newport will build a mixed residential and office complex of approximately 700,000 square meters. As of the date of this Annual Report, mixed-use complex totaling approximately 100,000 square meters have been completed and there are outstanding 600,000 square meters to be constructed in three phases within the next five (5) years.

To support the office complex, a light railway from downtown Wuhan to the complex is undergoing construction, for which the complex will be accessible by two stations along the light railway line. In addition, an expressway along the north shore of the Yangtze River in Wuhan is currently under construction; the completion of the highway is also expected to provide direct ground access between Wuhan city center and the Logistics Center and cut down the commute time to only 20 minutes.

Upon completion of the construction of the office buildings, Wuhan Newport plans to sell half of the complex while leasing out the remaining half for long-term income. It is Company’s goal to recover the initial investment costs through sale of half of the complex and generate a stable return based on rent of the other half complex upon completion of the project.

| 5 |

Corporate History

On December 23, 2009, the Company was incorporated under the laws of the State of Nevada under the name of “Ciglarette International, Inc.”. Our operations at the time consisted of marketing and distributing a “smokeless” cigarette. During that time, we had no revenue and our operations were limited to capital formation, organization, and development of our business plan and target customer market.

On March 1, 2011, the Company completed a reverse acquisition transaction through a share exchange with Kirin China Holding, a British Virgin Islands company (“Kirin China”), whereby the Company acquired all of the issued and outstanding shares of Kirin China in exchange for 18,547,297 shares of common stock, which represented approximately 98.4% of the total shares outstanding immediately following the closing of this share exchange (the “First Share Exchange”). Upon consummation of the First Share Exchange, Company changes its name to “Kirin International Holding, Inc.” and traded under the symbol “KIRI” on OTC Markets. As a result of the First Share Exchange, Kirin China became a wholly-owned subsidiary. The Company ceased the smokeless cigarette business and became a holding company, through various controlled entities in the China, engaged in the development and operation of real estate in China. Through Kirin China, Company engaged in private real estate development focusing on residential and commercial real estate development in “tier-three” cities in China. Tier-three cities are provincial capital cities with ordinary economic development and prefecture cities with relatively strong economic development.

On December 19, 2015, Company entered into certain share exchange agreements with Energetic Mind and all the shareholders of Energetic Mind whereby the Company acquired 100% issued and outstanding ordinary shares of Energetic Mind (the “Second Share Exchange”). Pursuant to the terms of the agreements for the Second Share Exchange, in exchange for 100% issued and outstanding ordinary shares of Energetic Mind, the Company agreed to issue to (i) the shareholders of Energetic Mind an aggregate of one hundred fifty-one million (151,000,000) shares of Company’s common stock and (2) a certain related party an additional 8% convertible promissory note in the principal amount of one hundred fifty million dollars ($150,000,000), with a conversion price of $10.00 per share.

On December 31, 2015, the Company disposed all of its interests in i) Brookhollow Lake, LLC, ii) Newport Property Holding, LLC, iii) Kirin China, iv) Kirin Hopkins Real Estate Group LLC, v) Archway Development Group LLC, vi) Specturm International Enterprise, LLC and vii) wholly-owned subsidiary HHC-6055 Centre Drive LLC. The sale of Kirin China also effectively terminated Company’s contractual relationship with Hebei Zhongding Real Estate Development Co. Ltd and Xingtai Zhongding Jiye Real Estate Development Co., Ltd, both of which are companies formed under the laws of the People’s Republic of China and were deemed Company’s variable interest entities prior to this sale (“Subsidiaries Sale”).

As a result of the Second Share Exchange and the Subsidiaries Sale, the Company currently operates its business solely through its wholly-owned subsidiary Energetic Mind, which is the sole shareholder of Ricofliz, which engages its business through its wholly-owned subsidiary Wuhan Newport.

On January 13, 2016, Company filed a Certificate of Amendment to its Articles of Incorporation (the “Amendment”) with the Secretary of the State of the State of Nevada, changing its name from “Kirin International Holding, Inc.” to “Yangtze River Development Limited”. Effective January 22, 2016, Company changed its stock symbol from “KIRI” to “YERR”.

Organization & Subsidiaries

Upon completion of the Second Share Exchange described above in “Corporate History”, Yangtze River Development Limited holds 100% ordinary shares of its wholly owned subsidiary, Energetic Mind, which holds all of the share capital of Ricofeliz Capital. Ricofeliz Capital holds all of the share capital of Wuhan Newport, a wholly foreign-owned enterprise located in Wuhan of Hubei Province in China.

| 6 |

The following diagram illustrates our corporate structure as of the date of this Annual Report:

Transportation and Logistics Services

Taking the regional advantage of the highways, railways and waterways in Yangluo area, Company plans to develop a shipping hub with access to all types of cargo transportation and offer complementary services to businesses within this logistics center. The Company intends to create an efficient, reliable and comprehensive logistics service system by utilizing the third-party service providers with offices within the Logistics Center to provide professional logistics services.

Company is currently constructing the port terminal which will be the focal point of the Yangtze River Economic Belt. The Yangtze River riverbank within our properties measures 1,039 meters, where we plan to complete eight cargo berths handling ships ranging from 5,000 to 10,000 tons.

A cargo transportation railway invested by the government has been built next to the Logistic Center. The railway is known as the Wuhan-Xinjiang-Europe (“WXE”) Railway in the Silk Road Economic Zone as it is in the “One Belt, One Road” initiative introduced by the Chinese government. The WXE Freight Train sets out from Wuhan to Xinjiang and finally ends in Mainland Europe. Wuhan Newport’s terminal is therefore an important component of the “Silk Road Economic Belt” under the “One Belt, One Road” framework.

The customs facility at the Yangluo Comprehensive Bonded Area allow cargo vessels ranging from 5,000 to 10,000 tons to set out from Shanghai downstream via the Yangtze River in order to transport “Made in China” commodities to the Pacific Ocean and further to any other ports across the Indian Ocean. In return transporting commodities from other countries will be shipped directly back to Wuhan and then distributed throughout rest of the Mainland China. Aside from being situated in the Wuhan Yangluo Comprehensive Bonded Zone, Yangluo development area is amongst the third group of China’s Free-Trade Zone (FTZ) applicants to submit FTZ applications to the State Council through the Wuhan municipal government for approval. Approvals have so far been granted to Shanghai, Tianjin, Guangdong and Fujian. Enterprises within the approved free-trade zones are typically entitled to a series of favorable regulations and policies that could help the businesses grow and succeed.

| 7 |

Cold Chain Logistics Services

A cold chain is a temperature-controlled supply chain. An unbroken cold chain is an uninterrupted series of storage and distribution activities which maintain a given temperature range. It is used to help extend and ensure the shelf life of products such as fresh agricultural produce, seafood and frozen food.

Within the Logistics Center, Company will provide extensive storage and processing services to its customers. Meanwhile, a cold chain logistics service system will be established to better help Company’s clients’ processing needs for their frozen foods, meats and other products that need special processing and handling. In addition, Company will offer professional services with temperature control, sorting, processing, packaging and delivery to ensure the reliability and safety of the logistics process.

Information Platform

To adapt to the needs of modern logistics service and meet the standards of the industry worldwide, Company will establish comprehensive automated management systems, as well as develop an operation system, enquiry system and decision-making systems for all types of business information such as warehouse, storage, trade, distribution and transportation, movable assets supervision and freight forwarding. Company plans to launch an integrated and information-sharing platform geared towards the demand of its targeted markets and potential clients.

Company will establish a uniform information platform including an internet-based logistics information portal and an e-commerce platform to provide the Company’s clients with services such as logistics services tracking, service rating, online operation, electronic transaction, and etc. Company expects this information portal to be equally reliable for both service providers and their respective clients.

Company will also establish an e-commerce system based on the logistics information portal and it will provide clients with many updated services such as online transactions, online payments, online inquiries and business information communication. This will create a comprehensive service system and a business model with high integration of information flow, capital flow, trade flow and goods flow.

Portside Service

Company also plans to provide incentives for companies that specialize in IT, production of new material and high-end equipment and manufacturing companies to station nearby the Logistics Center so that these companies can grow with the Logistics Center, leveraging each other’s specialization to serve each other’s business needs.

Logistics Financing

Logistics financing is mainly based on using supplies as collateral to obtain financing for supply chains to improve its overall economic efficiency. Developing an innovative logistics financing is significant because traditionally mortgages or loans are concentrated in real estate and logistics financing provides a lower systematic risk for lenders.

| 8 |

Compared to developed countries, logistics financing is a rather new field in China with a huge market potential of about 7 trillion RMB. The driving force for logistics financial service in western countries is mainly attributable to financial institutions as opposed to third-party private logistics companies in China who would occasionally provide financing options.

Logistics financial services became a popular investment vehicle among these third-party lenders. However, the business of logistics financing has become more complex for these private lenders to handle as they will need professional service to guide them the process and thus safeguard their investments.

According to the data from China Federation of Logistics and Purchasing, the total nationwide logistics in 2011 amounted to RMB 158.4 trillion which year-on-year growth rate is 12.3%. It decreased 2.7% compared to that of last year. The growth trend of the total nationwide logistics is high in first half year while low in last half year—it is 14.2% in the first quarter, 13.7% in the first half year and 13.4% in the first three quarters. Total nationwide logistics fees are 8.4 trillion Yuan which year-on-year growth rate is 18.5% an increase of 1.8% compared to that of last year. Data from China Federation of Logistics and Purchasing also shows that the proportion of total logistics fees to GDP in 2011 is 17.8%, which is almost same as that of last year. This means the logistics cost of social economic operation is still high. As an important part of a productive service industry, the position of the logistics industry in the national economy is more and more significant. It promotes the development of the growth and the maturity of the economy and society. The huge market space of logistics industry also attracts banks to enter the market.

Even though the history of logistics financing has been relatively short in China, the appetite for this is expected to grow as the Free Trade Zones in Shanghai, Tianjin and soon-to-be Wuhan will likely attract more business and international financial institutions. Logistics financing not only provides the businesses with a new alternative to meet their capital needs, but also opens a new channel for commercial banks to reach small and midsize businesses. While interest income generated from logistics financing transaction is often an important source of income for many multinational logistics companies, companies who are able to provide financing are often the industry leaders. Because logistics financing can be an effective channel for the Company to reach its targeted market, our Company plans to capture this first-mover advantage when logistics financing is still in its development stage in China.

In light of this market opportunity, Company plans to establish and utilize e-commerce platforms to offer online booking, online dealing and online exhibiting services to provide professional transaction services for electronic products, commodity, foods and metals. Company also plans to provide comprehensive support services to complement logistics financing. Maritime insurance and training services will be offered within the Logistic Center. Company plans to help its clients to raise construction capital through Build-Transfer (BT), Build-Operate-Transfer (BOT), corporate debt and equity financing. Company also plans to collaborate and develop strategic alliances with other logistics or cargo shipping centers around the world.

Sales and Marketing

Company plans to enter the market by collaboration with two strategic partners – CMST Development (Hankou) Co. Ltd. (“CMST”) and Hubei Province Chamber of Commerce (“HPCC”).

CMST is a state-owned enterprise that is principally engaged in the logistics and trading business. The company and its subsidiaries are primarily involved in the storage, sale and distribution of merchandises, and freight forwarding. As part of the collaborate, CMST has agreed to transfer storage and processing, logistics and other existing services to Wuhan Newport, including a turnover of more than 5 million tons of steel per year. Because of the collaboration, Company plans to offer the warehouse processing zones and provide the partner companies with professional service and advice. While company is responsible for providing storage areas, railway access, port terminal and equipment installation, along with a commodities trading e-commerce platform to provide a comprehensive range of supply chain for financial support services, CMST is responsible for warehouse operations management and client sourcing. Both companies will work together to create Wuhan Newport as a national logistics center and establish a greater influence on the commodity professional market. Company is expected to receive fees based on their use of the warehouse and terminal, as well as other services within the Logistics Center.

| 9 |

Company has also been collaborating with Hubei-Jin Business Chamber of Commerce (“Hubei-Jin”) as Hubei-Jin intends to move its headquarter to the Logistics Center. Hubei -Jin works with approximately fifty companies in the iron and steel production and trading business. Optimistic about the geographic advantages and appreciation potential of the Logistics Center, Hubei-Jin has committed to a total of not less than 100,000 square meters of office space and is expected to move in occupying the office spaces. While their biggest needs will be the warehouse within the Logistics Center, Hubei-Jin is also expected to use company’s port terminal, waterways, railways and other logistics services, for all of which Company will charge Hubei-Jin a service fee.

PRC Logistics Industry Overview

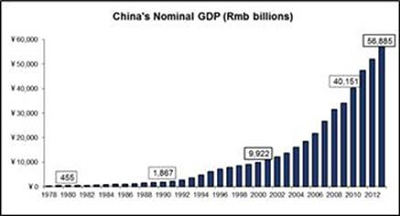

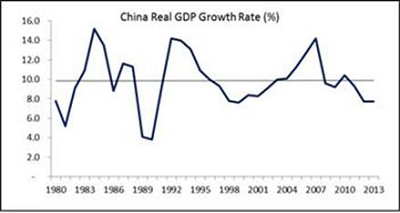

According to the National Bureau of Statistics of the PRC, China’s nominal GDP grew at a compound annual growth rate of 15.8% between 1980 and 2013 and reached RMB 56.9 trillion in 2013. Adjusted for inflation, China’s real GDP maintained an average annual growth rate of 9.9% between 1980 and 2013, significantly outpacing the world’s other major economies, such as the United States, Japan, India and Germany. Since 2010, China has been the world’s second largest economy behind the United States.

Source: National Bureau of Statistics of the PRC

| 10 |

Source: National Bureau of Statistics of the PRC

The logistics industry has become the new increasing point of China’s economy in the 21st century. In recent years, third party logistics indicated a tendency towards rapid increase, increasing from 40 billion in 2001 to 500 billion in 2013 with a 25% annual increase rate at average. Among these third party logistics companies, 70% of them had a 30% increase in their revenue annually and 20% of them had their revenue doubled each year.

The Rise of Logistics Finance

Logistics finance provides financial services such as financing, clearance and insurance to support the logistics industry. It evolves as the logistics industry develops. Not only can logistics finance services improve the service capability and increase the profitability of the third party logistics companies, it can also expand financing channels, decrease financing cost and increase the capital efficiency.

Compared with developed countries, logistics finance is a new field in China with huge market potential of about 7 trillion RMB. The driving force for logistics financial services in western countries are mainly financial institutes while it is the third party logistics corporations in China that provide such services. Logistics financial services appear along with modern third party logistics corporations. The business of logistic financial services for modern third party logistics corporations is more complex than before in that it not only includes modern logistics service but is part of finance services.

According to the data from China Federation of Logistics and Purchasing, total nationwide logistics amount in 2011 is 158.4 trillion Yuan which year-on-year growth rate is 12.3%. It decreases 2.7% comparing with that of last year. The growth trend of total nationwide logistics amounts is high in first half year while low in last half year—it is 14.2% in the first quarter, 13.7% in the first half year and 13.4% in the first three quarters. Total nationwide logistics fees are 8.4 trillion Yuan which have a year-on-year growth rate of 18.5% and increase to 1.8% compared that of last year. Data from the China Federation of Logistics and Purchasing also shows that proportion of total logistics fee to GDP in 2011 is 17.8% which is almost same to that of last year. It means the logistics cost of social economic operation is still high. As an important part of a productive service industry, the position of the logistics industry in national economy is more and more significant. It promotes the development of the economy. The huge market space of logistics industry also attracts banks to enter the market.

The major target client for logistics finance service are small or medium size companies, which are the main players in China’s economy and have a great weight in the market. One of the biggest hurdles in the life circle of these small or medium size companies is lack of cash flow, which always becomes the “bottle neck” of their development and prevents them from moving forward. The need for logistics financing is because of the lack of available credit financing facilities and incapability of financing on the capital markets.

| 11 |

Therefore, logistics finance services solve the financing problem by allowing these small and medium companies to use its raw materials and commodities as collateral to borrow money. Logistics financing increases the liquidity of cash flow, lowers the clearance risks and improves the efficiency of the economic operation. It is conservatively estimated that the logistics finance market in China is over 1,000 billion RMB. China’s logistics finance is a huge growing space.

Market Overview of Wuhan

Located in the middle reaches of the Yangtze River, Wuhan has been regarded as the gateway to nine provinces nearby. Beijing-Guangzhou Railway and the Yangtze River converge in Wuhan and also Beijing-Jiulong Railway and Beijing-Guangzhou Railway intersect in it, thus forming a railway network linking North China, Southwest China, Central South China and East China. Moreover, Beijing-Zhuhai Expressway and Shanghai-Chengdu Expressway converge in Wuhan and a high-speed railway along the Yangtze River will be completed here soon. Therefore, a “flexible multimodal transportation system” combining expressways, high-speed railways and water transportation on the Yangtze River will give greater prominence to Wuhan's position of strategic importance as a junction of water and land transportation in China.

Wuhan is the largest inland logistics and cargo distribution center in China, with its service covering approximately a 400 million populations in the five neighboring provinces including Hunan, Jiangxi, Anhui, Henan and Sichuan. At present, there are over 10,000 commercial organizations, 105,000 commodity networks, four commercial listed enterprises as well as eight comprehensive shopping centers on the list of China Top 100 Retail Shopping Centers.

China is thoroughly implementing the strategy of coordinated regional development, expanding domestic demand, innovation-driven development and new urbanization, and building a new economic support belt relying on the Yangtze River. As a central city in the central region and the middle reach of the Yangtze River, and the country’s major transportation hub and science and technology base, Wuhan faces multiple overlapping strategic opportunities. Location, transportation, science, education, market and other advantages will be further enhanced and fully released and more quickly transformed into development and competitive advantage.

| 12 |

Wuhan is a major transportation hub of China situated at the midstream of the Yangtze River. Going west alongside the Yangtze, upstream are the cities in Chongqing, Sichuan, Yunnan and Qinghai. Going east downstream are provinces of Hunan, Anhui and Jiangsu, as well as the cities of Nanjing and Shanghai, until finally arriving at the sea. The railway runs north bound to Harbin, westbound to Urumqi, east bound to Shanghai and south bound to the Shenzhen Highway and expressways that stretch in all directions ensuring easy and convenient transportation to all provinces in China. Likewise, Wuhan is largest economic city in central China with an annual GDP beyond 1,000 billion RMB. In 2015, the China State Council introduced and implemented the Midstream Yangtze River City Group Development Plan headed by Wuhan. In fact, the city was once called “The Oriental Chicago” by the US Harper’s Magazine back in 1918.

With the rapid development of inland water shipping in China, logistics and port management industry has grown significantly. Wuhan is one of the major inland water ports in China. In 2014, Wuhan government released an Opinion On Accelerating The Establishment Of Shipping Center In The Middle Reach Of Yangtze River, indicated that the government will help the Wuhan shipping center to be a well-equipped, surrounding industry developed internationally with a scaled and intelligent inland water shipping center with all port and shipping resources highly concentrated. In the Development Plan On Wuhan Logistics Space (2012-2020), Wuhan is strategically positioned as the critical joint of the global supply chain and the logistics transportation hub and information center of China.

Wuhan has supported many logistics companies, including, as of March 2014, 99 tier-one logistics companies, which are supported by the local government that aims to forming a multi-dimension logistics industry in Wuhan by providing meaningful support to promising logistics companies.

However, in Wuhan, logistics for domestic trade operated separately from that for international trade and all resources are scattered and not concentrated enough to form a well-organized and well-managed international supply chain. It becomes very difficult for Wuhan to realize the synergy of business, logistics, money and information. In addition, a majority of the current logistics companies in Wuhan focus on traditional cargo transportation and storage services. Therefore, there exists an opportunity for an efficient, comprehensive and modern logistics service center to facilitate the channel of both regional and global logistics.

Competitive Advantages

The following factors reflect Company’s advantages over the company’s competitors:

| ● | Experienced Logistics Management Team. Company has a professional team with significant experience in logistics management. Members of the company’s team have had work experience with well-known logistics management companies in different cities. In addition, the management members are well educated with degrees from top universities such as Huazhong University of Science and Technology, Wuhan University, University of British Columbia and Chinese Academy of Social Sciences. |

| 13 |

| ● | Encouraging Policy Environment. Under China’s latest “One Belt, One Road” initiative, Company is strategically positioned in the anticipated “Pilot Free Trade Zone” of the Wuhan Port, a crucial trading window between China, the Middle East and Europe. In May 2015, China State Council approved the nation’s economic strategic plan, the Vigorous Development Plan of Yangtze River Economic Belt. The Yangtze River Economic Belt has sharpened the focus on the Wuhan New Port Yangluo Terminal the port project that Company is developing. | |

| ● | Unique Transportation Network. Wuhan is located in the middle reaches of the Yangtze River, east facing south-eastern coastal economic developed area and west linking north-western Boda market and material base. The distance to metropolitan cities, such as Beijing, Shanghai, Hong Kong and Chongqing are within 1,200 kilometers. As a central city on mainland China, Wuhan is capable of reaching over 30 provinces like Yunnan Province, Henan Province, Sichuan Province, Shanxi Province, Jiangxi Province and Hunan Province and 600 cities and counties in China. |

| ● | Highway: Logistics Center is in close proximity to the Beijing-Zhuhai expressway, Shanghai-Chengdu Expressway, and Jiangbei Expressway. |

| ● | Waterway: the project adjacent to the Yangluo deep-water port, has eight 5,000-ton berths, directly leading to Jianghai. Yangluo port is the largest national shipping port in Central China and the largest container port in the upper reaches of the Yangtze River. Company will be is strategically located for international procurement, distribution and delivery. |

| ● | Railway: through Chinese commodity freight logistics Beijing-Guangzhou, Beijing-Kowloon Railway, close to Beijing-Guangzhou railway extension line, special railway lines offer direct access to the center of the Wuhan Yangtze River Newport logistics center, through Jiangbei railway- Xianglushan station connects all of the domestic railway freight station, and through the construction of the "Chinese new Europe" railway through the Continent. |

| ● | Airport: 30 kilometers from the Wuhan Tianhe airport. |

| ● | light-rail transit: by 2018 two light rail stations are expected to be completed next to the Logistics Center, cutting the commute to downtown Wuhan to only 20 minutes. |

| ● | Jiangbei Expressway: After the completion of Jiangbei Expressway, commute by car from downtown Wuhan to the Logistics Centers is expected to be only about a 20 minutes. |

| 14 |

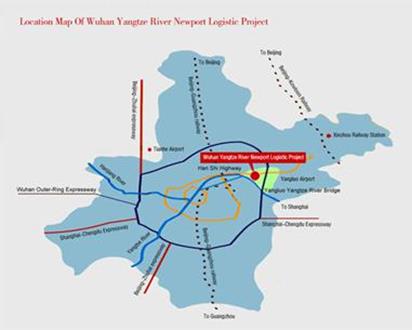

The following map shows the location of the Wuhan Newport Logistics Center and surrounding transportation network:

| 15 |

Employees

As of the date of this Report, we have a total of 87 employees, including our executive officers.

Our employees are not represented by any collective bargaining agreement, and we have never experienced a work stoppage. We believe we have good relations with our employees.

Legal Proceedings

Currently there are no legal proceedings pending or threatened against the Company. However, from time to time, we may become involved in various lawsuits and legal proceedings which arise in the ordinary course of business. Litigation is subject to inherent uncertainties, and an adverse result in these or other matters may arise.

| Item 1A. | Risk Factors. |

Smaller reporting companies are not required to provide the information required by this item.

| Item 1B. | Unresolved Staff Comments. |

Smaller reporting companies are not required to provide the information required by this item.

| Item 2. | Properties. |

The following chart illustrates the properties the Company currently has the land use rights to in Wuhan, Hubei Province, China.

| Certification Number of Land Use Right | Location | Purpose of Use | Area (㎡) | Termination Date |

| Wu

Xin Guo Yong (2008) Di Zhuang No. 029 |

South of Han Shi Road, Wuhan Yangluo Economic Development Zone, Hubei Province, PRC | Commercial | 9,802.67 | August 30, 2048 |

| Wu

Xin Guo Yong (2008) Di Zhuan No. 030 |

59,308.09 | |||

| Wu

Xin Guo Yong (2008) Di Zhuan No. 031 |

79,178.94 | |||

| Wu

Xin Guo Yong (2008) Di Zhuan No. 032 |

87,108.30 | |||

| Wu

Xin Guo Yong (2009) Di Zhuan No. 005 |

176,853.70 | |||

| Wu

Xin Guo Yong (2009) Di Zhuan No. 006 |

103,304.49 |

| 16 |

The following chart illustrates the properties the Company currently leases in Wuhan, Hubei Province, PRC and New York, United States.

| Name of the Property | Location | Purpose of Use | Area (㎡) | Duration Date |

| Land Lease No. HZ20150427 | Chunfeng Village, Yangluo Neighborhood, Wuhan, Hubei Province, PRC | Commercial | 1,214,654.52 | April 26, 2025 |

| New York Office Premise | 183 Broadway, New York, NY 10007 | Commercial | Suite 5 | April 15, 2017 |

| Item 3. | Legal Proceedings. |

We are currently not involved in any litigation that we believe could have a material adverse effect on our financial condition or results of operations. There is no action, suit, proceeding, inquiry or investigation before or by any court, public board, government agency, self-regulatory organization or body pending or, to the knowledge of the executive officers of our company or any of our subsidiaries, threatened against or affecting our company, our common stock, any of our subsidiaries or of our companies or our subsidiaries’ officers or directors in their capacities as such, in which an adverse decision could have a material adverse effect.

| Item 4. | Mine Safety Disclosures |

Not Applicable.

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases Of Equity Securities. |

Market Information

Our common stock trades on the OTC Markets under the symbol “YERR”. The OTC Markets is a quotation service that displays real-time quotes, last-sale prices, and volume information in over-the-counter (“OTC”) equity securities. An OTC Markets equity security generally is any equity that is not listed or traded on a national securities exchange.

| 17 |

Price Range of Common Stock

The following table shows, for the periods indicated, the high and low bid prices per share of our common stock as reported by the OTC Markets’ quotation service. These bid prices represent prices quoted by broker-dealers on the OTC Markets quotation service. The quotations reflect inter-dealer prices, without retail mark-up, mark-down or commissions, and may not represent actual transactions.

| Fiscal Year 2015 | ||||||||

| High | Low | |||||||

| First Quarter (January 1 - March 31) | $ | 0.45 | $ | 0.07 | ||||

| Second Quarter (April 1 - June 30) | $ | 1.90 | $ | 0.25 | ||||

| Third Quarter (July 1 - September 30) | $ | 3.20 | $ | 1.12 | ||||

| Fourth Quarter (October 1 - December 31) | $ | 8.40 | $ | 1.84 | ||||

| Fiscal Year 2014 | ||||||||

| High | Low | |||||||

| First Quarter (January 1 - March 31) | $ | 0.11 | $ | 0.10 | ||||

| Second Quarter (April 1 - June 30) | $ | 1.83 | $ | 0.10 | ||||

| Third Quarter (July 1 - September 30) | $ | 0.52 | $ | 0.16 | ||||

| Fourth Quarter (October 1 - December 31) | $ | 0.24 | $ | 0.06 | ||||

Holders

As of January 31, 2016, there were 59 holders of record of our common stock. This number does not include shares held by brokerage clearing houses, depositories or others in unregistered form.

Dividends

We have never declared or paid a cash dividend. Any future decisions regarding dividends will be made by our Board of Directors. We currently intend to retain and use any future earnings for the development and expansion of our business and do not anticipate paying any cash dividends in the foreseeable future. Our Board of Directors has complete discretion on whether to pay dividends. Even if our Board of Directors decides to pay dividends, the form, frequency and amount will depend upon our future operations and earnings, capital requirements and surplus, general financial condition, contractual restrictions and other factors that the Board of Directors may deem relevant.

Recent Sales of Unregistered Securities

None.

| Item 6. | Selected Financial Data. |

We are not required to provide the information required by this Item because we are a smaller reporting company.

| Item 7. | Management’s Discussion and Analysis of Financial Conditions and Results of Operations. |

The following discussion and analysis of the results of operations and financial condition for the year ended December 31, 2015 and 2014 should be read in conjunction with our financial statements and the notes to those financial statements that are included elsewhere in this Report. Our discussion includes forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors. See “Forward-Looking Statements.”

| 18 |

Overview

Yangtze River Development Limited is a Nevada corporation that operates through its wholly-owned subsidiary Ricofelix Capital, which operates through its wholly-owned subsidiary Wuhan Newport, a wholly foreign-owned enterprise that primarily engages in the business of real estate and infrastructural development with a port logistics project located in Wuhan, Hubei Province of China. Situated in the middle reaches of the Yangtze River, Wuhan Newport is a large infrastructure development project implemented under China's latest "One Belt One Road" initiative and is believed to be strategically positioned in the anticipated "Free Trade Zone" of the Wuhan Port, a crucial trading window between China, the Middle East and Europe. To be fully developed upon completion of three phases, within the logistics center, there will be six operating zones, including port operation area, warehouse and distribution area, cold chain logistics area, rail cargo loading area, exhibition area and residential community. The logistics center is also expected to provide a number of shipping berths for cargo ships of various sizes. Wuhan Newport is expected to provide domestic and foreign businesses a direct access to the anticipated Free Trade Zone in Wuhan. The project will include commercial buildings, professional logistic supply chain centers, direct access to the Yangtze River, Wuhan-Xinjiang-Europe Railway and ground transportation, storage and processing centers, IT supporting services, among others.

One of the main projects of our Company is the Wuhan Yangtze River Newport Logistics Center (the “Logistics Center”), which is an extensive complex that is located in Wuhan, the capital of Hubei Province of China, a major transportation hub with dozens of railways, roads and expressways passing through the city and connecting to major cities in Mainland China, with connections to international centers of commerce and business.

The Logistics Center is expected to approximately a total of 474 Acres, for which the construction and development are expected to be completed in five years in three phases. It is expected to be located in the Wuhan Newport Yangluo Port, on the upper stream of the Yangtze River, and close to the northern base of Wu Iron and Steel, China's first supergiant iron and steel complex. The Logistics Center is expected to include a port that will be located approximately 26.5km to Wuhan Guan and 5.5km from the Yangluo Yangtze River Bridge. The operation area of the port is expected to consist of a riverbank of 1,039 meters with eight 5,000 to 10,000-ton berths, two of which are multi-purpose berths and the other six to general cargo berths. It is also designed to be able to handle up to five million tons of cargo and containers areas up to 100,000 TEU a year (including two freezers areas of 10,000 TEU).

Within the Logistics Center, functional areas will be divided into six operating zones, including a port operation area, a warehouse and distribution area, a cold chain supply logistics area, a rail cargo loading area, an exhibition area and a mixed residential and commercial community. The Logistics Center will also be complemented with container storage areas, multi-functional areas, general storage areas, multi-functional warehouse and infrastructural development, including new roads, gas stations, parking areas, gas and water pipes, electricity lines and all other facilities and equipment to operate the Logistics Center.

Aside from being situated in the Wuhan Yangluo Comprehensive Bonded Zone, Yangluo development area is amongst the third group of China’s Free-Trade Zone (FTZ) applicants to submit FTZ applications to the State Council through the Wuhan municipal government for approval. Approvals have so far been granted to Shanghai, Tianjin, Guangdong and Fujian. Enterprises within the approved free-trade zones are typically entitled to a series of favorable regulations and policies that could help the businesses grow and succeed.

Wuhan Newport has signed an agreement to rent 1.2 million square meters of land on a long term basis for building logistics warehouses covering 400,000 square meters in support of the new port. The warehouses is expected to comprise of port terminal zones, warehouse logistics zones, cold chain supply zones and railroad loading and unloading zones. The warehouses, once constructed, will connect the port terminal along the Yangtze River and the railway leading to Europe, satisfying the requirement of China’s latest “One Belt, One Road” initiative. It will also be able to support large logistics companies in Wuhan and other nearby provinces that lease the warehouses, terminals and offices.

| 19 |

Factors Affecting our Operating Results

Growth of China’s Economy. We operate and derive all of our revenue from operations in China. Economic conditions in China, therefore, affect our operations, including the demand for our properties and services and the availability and prices of land maintenance among other expenses. China has experienced significant economic growth with recorded Gross Domestic Product growth rates at 7.7% in 2013, 7.4% in 2014 and 6.9% in 2015. China is expected to experience continued growth in all areas of investment and consumption. However, if the Chinese economy were to become significantly affected by a negative stimulus, China’s growth rate would likely to fall and our revenue could correspondingly decline.

Government Regulations. Our business and results of operations are subject to PRC government policies and regulations regarding the following:

| ● | Land Use Right — According to the Land Administration Law of the PRC and Interim Regulations of the People’s Republic of China Concerning the Assignment and Transfer of the Right to the Use of the State-owned Land in the Urban Areas, individuals and companies are permitted to acquire rights to use urban land or land use rights for specific purposes, including residential, industrial and commercial purposes. We acquire land use rights from local governments and/or other entities for development of residential and commercial real estate projects. | |

| ● | Land Development — According to the Urban Real Estate Development and Operation Administration Regulation, the Urban Real Estate Development and Operation Administration Rules of Hebei Province promulgated by the government of the Hebei Province, and the Real Estate Development Enterprise Qualification Administration Regulation, a real estate development enterprise shall obtain a Real Estate Development Enterprise Qualification Certificate. We obtained the related certificates and seek to ensure that each phase of our projects complies with our certificates. | |

| ● | Project Financing — According to the Land Administration Law and the Property Law of the PRC, the land use rights, residential housing and other buildings still in process of construction may be pledged and mortgaged. From time to time, we pledge and mortgage our land use rights and real properties to lenders in order to obtain project financing. |

Interest Rate and Inflation Challenges. We are subject to market risks due to fluctuations in interest rates and refinancing of mid-term debt. Higher interest rates may also affect our revenues, gross profits and our ability to raise and service debt and to finance our developments. Inflation could result in increases in the price of raw materials and labor costs. We do not believe that inflation or deflation has affected our business materially.

Acquisitions of Land Use Rights and Associated Costs. We acquire land use rights for development through the governmental auction process and by obtaining land use rights permits from third parties through negotiation, acquisition of entities, co-development or other joint venture arrangements. Our ability to secure sufficient financing for land use rights acquisitions and property development depends on internal cash flows in addition to lenders’ perceptions of our credit reliability, market conditions in the capital markets, investors’ perception of our securities, the PRC economy and the PRC government regulations that affect the availability and cost of financing real estate companies or property purchasers.

| 20 |

Significant Accounting Policies

Use of Estimates

The preparation of consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the consolidated financial statements, and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates. On an ongoing basis, management reviews these estimates using the currently available information. Changes in facts and circumstances may cause the Company to revise its estimates. Significant accounting estimates reflected in the consolidated financial statements include: (i) the allowance for doubtful debts; (ii) accrual of estimated liabilities; and (iii) contingencies; (iv) deferred tax assets; (v) impairment of long-lived assets; (vi) useful lives of property plant and equipment; and (vii) real estate property refunds and compensation payables.

Fair Value of Financial Instruments

ASC Topic 825, Financial Instruments (“Topic 825”) requires disclosure of fair value information of financial instruments, whether or not recognized in the balance sheets, for which it is practicable to estimate that value. In cases where quoted market prices are not available, fair values are based on estimates using present value or other valuation techniques. Those techniques are significantly affected by the assumptions used, including the discount rate and estimates of future cash flows. In that regard, the derived fair value estimates cannot be substantiated by comparison to independent markets and, in many cases, could not be realized in immediate settlement of the instruments. Topic 825 excludes certain financial instruments and all nonfinancial assets and liabilities from its disclosure requirements. Accordingly, the aggregate fair value amounts do not represent the underlying value of the Company.

Level 1 inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets.

Level 2 inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the assets or liability, either directly or indirectly, for substantially the full term of the financial instruments.

Level 3 inputs to the valuation methodology are unobservable and significant to the fair value.

As of December 31, 2015 and 2014, financial instruments of the Company primarily comprise of cash, accrued interest receivables, other receivables, short-term bank loans, deposits payables and accrued expenses, which were carried at cost on the balance sheets, and carrying amounts approximated their fair values because of their generally short maturities.

Reporting Currency and Foreign Currency Translation

The Company’s consolidated financial statements are presented in the U.S. dollar (US$), which is the Company’s reporting currency. Yangtze River, Energetic Mind, and Ricofeliz Capital uses US$ as its functional currency. Wuhan Newport uses Renminbi Yuan(“RMB”) as its functional currency. Transactions in foreign currencies are initially recorded at the functional currency rate ruling at the date of transaction. Any differences between the initially recorded amount and the settlement amount are recorded as a gain or loss on foreign currency transaction in the statements of operations.

In accordance with ASC 830, Foreign Currency Matters, the Company translated the assets and liabilities into US$ using the rate of exchange prevailing at the applicable balance sheet date and the statements of operations and cash flows are translated at an average rate during the reporting period. Adjustments resulting from the translation are recorded in owners’ equity as part of accumulated other comprehensive income.

| December 31, | ||||||||

| 2015 | 2014 | |||||||

| Balance sheet items, except for equity accounts | 6.4917 | 6.1460 | ||||||

| 21 |

| For the Years Ended December 31, | ||||||||

| 2015 | 2014 | |||||||

| Items in the statements of operations and comprehensive income, and statements of cash flows | 6.2288 | 6.1457 | ||||||

Revenue Recognition

The Company recognizes revenue from steel trading when persuasive evidence of an arrangement exists, delivery has occurred, the price is fixed or determinable and collection is reasonably assured.

Real estate sales are reported in accordance with the provisions of ASC 360-20, Property, Plant and Equipment, Real Estate Sales.

Revenue from the sales of completed properties and properties where the construction period is twelve months or less is recognized by the full accrual method when (a) sale is consummated; (b) the buyer’s initial and continuing involvements are adequate to demonstrate a commitment to pay for the property; (c) the receivable is not subject to future subordination; (d) the Company has transferred to the buyer the usual risks and rewards of ownership in a transaction that is in substance a sale and does not have a substantial continuing involvement with the property. A sale is not considered consummated until (a) the parties are bound by the terms of a contract or agreement, (b) all consideration has been exchanged, (c) any permanent financing for which the seller is responsible has been arranged, (d) all conditions precedent to closing have been performed. Fair value of buyer’s payments to be received in future periods pursuant to sales contract is classified under accounts receivable. Sales transactions not meeting all the conditions of the full accrual method are accounted for using the deposit method of accounting. Under the deposit method, all costs are capitalized as incurred, and payments received from the buyer are recorded as a deposit liability.

Revenue and profit from the sale of development properties where the construction period is more than twelve months is recognized by the percentage-of-completion method on the sale of individual units when the following conditions are met: (a)construction is beyond a preliminary stage; (b) the buyer is committed to the extent of being unable to require a refund except for non-delivery of the unit; (c) sufficient units have already been sold to assure that the entire property will not revert to rental property; (d) sales prices are collectible and (e) aggregate sales proceeds and costs can be reasonably estimated. If any of these criteria are not met, proceeds are accounted for as deposits until the criteria are met and/or the sale consummated.

The Company has not generated any revenue from the sales of real estate property for the years ended December 31, 2015 and 2014.

Real Estate Capitalization and Cost Allocation

Real estate property completed and real estate properties and land lots under development consist of commercial units under construction and units completed. Properties under development or completed are stated at cost or estimated net realizable value, whichever is lower. Costs include costs of land use rights, direct development costs, interest on indebtedness, construction overhead and indirect project costs. The Company acquires land use rights with lease terms of40years through government sale transaction. Land use rights are divided and transferred to customers after the Company delivers properties. The Company capitalizes payments for obtaining the land use rights, and allocates to specific units within a project based on units’ gross floor area. Costs of land use rights for the purpose of property development are not amortized. Other costs are allocated to units within a project based on the ratio of the sales value of units to the estimated total sales value.

| 22 |

Capitalization of Interest

In accordance with ASC 360, Property, Plant and Equipment, interest incurred during construction is capitalized to properties under development. For the years ended December 31, 2015 and 2014, nil and nil were capitalized as properties under development, respectively.

Cash and Cash Equivalents

Cash and cash equivalents consist of cash and bank deposits with original maturities of three months or less, which are unrestricted as to withdrawal and use the Company maintains accounts at banks and has not experienced any losses from such concentrations.

Property and Equipment, Net

The property and equipment are stated at cost less accumulated depreciation. The depreciation is computed on a straight-line method over the estimated useful lives of the assets with 5% salvage value.

The Company eliminates the cost and related accumulated depreciation of assets sold or otherwise retired from the accounts and includes any gain or loss in the statement of income. The Company charges maintenance, repairs and minor renewals directly to expenses as incurred; major additions and betterment to equipment are capitalized.

Income Taxes

Current income taxes are provided for in accordance with the laws of the relevant taxing authorities. As part of the process of preparing consolidated financial statements, the Company is required to estimate its income taxes in each of the jurisdictions in which it operates. The Company accounts for income taxes using the liability method. Under this method, deferred income taxes are recognized for tax consequences in future years of differences between the tax bases of assets and liabilities and their reported amounts in the consolidated financial statements at each year-end and tax loss carry forwards. Deferred tax assets and liabilities are measured using enacted tax rates applicable for the differences that are expected to affect taxable income.

The Company adopts a more likely than not threshold and a two-step approach for the tax position measurement and financial statement recognition. Under the two-step approach, the first step is to evaluate the tax position for recognition by determining if the weight of available evidence indicates that it is more likely than not that the position will be sustained, including resolution of related appeals or litigation process, if any. The second step is to measure the tax benefit as the largest amount that is more than 50% likely of being realized upon settlement. As of December 31, 2015 and 2014, the Company did not have any uncertain tax position.

Land Appreciation Tax (“LAT”)

In accordance with the relevant taxation laws in the PRC, the Company is subject to LAT based on progressive rates ranging from 30% to 60% on the appreciation of land value, which is calculated as the proceeds of sales of properties less deductible expenditures, including borrowing costs and all property development expenditures. LAT is prepaid at 1% to 2% of the pre-sales proceeds each year as required by the local tax authorities, and is settled generally after the construction of the real estate project is completed and majority of the units are sold. The Company provides LAT as expensed when the related revenue is recognized based on estimate of the full amount of applicable LAT for the real estate projects in accordance with the requirements set forth in the relevant PRC laws and regulations. LAT would be included in income tax expense in the statements of operations and comprehensive income (loss).

Earnings per Share

Basic earnings (loss) per share is computed using the weighted average number of common shares outstanding during the year. Diluted earnings per share is computed using the weighted average number of common shares and potential common shares outstanding during the period for convertible notes under if-convertible method, if dilutive. Potential common shares are not included in the denominator of the diluted earnings per share calculation when inclusion of such shares would be anti-dilutive, such as in a period in which a net loss is recorded.

| 23 |

Advertising Expenses

Advertising costs are expensed as incurred, or the first time the advertising takes place, in accordance with ASC 720-35, Advertising Costs. For the years ended December 31, 2015 and 2014, the Company recorded advertising expenses of $7,724 and $47,187, respectively.

Impairment of long-lived assets

The Company applies the provisions of ASC No. 360 Sub topic 10, "Impairment or Disposal of Long-Lived Assets"(ASC 360- 10) issued by the Financial Accounting Standards Board ("FASB"). ASC 360-10 requires that long-lived assets be reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable through the estimated undiscounted cash flows expected to result from the use and eventual disposition of the assets. Whenever any such impairment exists, an impairment loss will be recognized for the amount by which the carrying value exceeds the fair value.

The Company tests long-lived assets, including property and equipment and finite lived intangible assets, for impairment at least annually or more frequently upon the occurrence of an event or when circumstances indicate that the net carrying amount is greater than its fair value. Assets are grouped and evaluated at the lowest level for their identifiable cash flows that are largely independent of the cash flows of other groups of assets. The Company considers historical performance and future estimated results in its evaluation of potential impairment and then compares the carrying amount of the asset to the future estimated cash flows expected to result from the use of the asset. If the carrying amount of the asset exceeds estimated expected undiscounted future cash flows, the Company measures the amount of impairment by comparing the carrying amount of the asset to its fair value. The estimation of fair value is generally measured by discounting expected future cash flows as the rate the Company utilizes to evaluate potential investments. The Company estimates fair value based on the information available in making whatever estimates, judgments and projections are considered necessary. There were no impairment losses in the years ended December 31, 2015 and 2014.

Stock-Based Compensation

The Company adopted ASC 718 Stock Compensation. Stock-based compensation cost is measured at the grant date based on the fair value of the award and is recognized as expense over the requisite service period, which is generally the vesting period. The fair value estimate is based on the share price and other pertinent factors. The Company estimates forfeitures at the time of grant and to revise those estimates in subsequent periods if actual forfeitures differ from those estimates. The Company used a mix of historical data and future assumptions to estimate pre-vesting forfeitures and to record stock-based compensation expense only for those awards that are expected to vest.

Recently Issued Accounting Pronouncements

The Company does not believe recently issued but not yet effective accounting standards from ASU 2014-01 to ASU 2015-01, if currently adopted, would have a material effect of the consolidated financial position, results of operation and cash flows.

| 24 |

Results of Operations

Comparison of Fiscal Years Ended December 31, 2015 and 2014

| For the Years Ended December 31, | ||||||||

| 2015 | 2014 | |||||||

| Revenue | $ | - | $ | 3,458,295 | ||||

| Cost of revenue | - | 3,693,783 | ||||||

| Gross loss | - | (235,488 | ) | |||||

| Operating expenses | ||||||||

| Selling expenses | 11,577 | 87,866 | ||||||

| General and administrative expenses | 4,547,646 | 2,090,499 | ||||||

| Total operating expenses | 4,559,223 | 2,178,365 | ||||||

| Loss from operations | (4,559,223 | ) | (2,413,853 | ) | ||||

| Other income (expenses) | ||||||||

| Gain on disposal of subsidiaries | 11,687,098 | - | ||||||

| Other income | 868 | - | ||||||

| Other expenses | (3,231 | ) | - | |||||

| Interest income | 55 | 10,996 | ||||||

| Interest expenses | (3,199,031 | ) | (3,256,660 | ) | ||||

| Total other income (expenses) | 8,485,759 | (3,245,664 | ) | |||||

| Income (loss) before income taxes | 3,926,536 | (5,659,517 | ) | |||||

| Income taxes benefit | 1,378,700 | 1,402,421 | ||||||

| Net income (loss) | $ | 5,305,236 | $ | (4,257,096 | ) | |||

| Other comprehensive loss | ||||||||

| Foreign currency translation adjustments | (6,649,917 | ) | (147,341 | ) | ||||

| Comprehensive loss | $ | (1,344,681 | ) | $ | (4,404,437 | ) | ||

| Earnings (loss) per share - basic and diluted | $ | 0.03 | $ | (0.03 | ) | |||

| Weighted average shares outstanding - basic and diluted | 151,682,554 | 151,000,000 | ||||||

The following table sets forth the results of our operations for the periods indicated in U.S. dollars and as a percentage of net sales:

Revenue.

During the fiscal year ended December 31, 2015, we did not generate any revenue, compared to revenue of $3,458,295 for the fiscal year ended December 31, 2014, a decrease of $3,458,295 or approximately 100.0%. The significant decrease was mainly because we did not sell engage in any steel trading during the fiscal year ended 2015.

We also did not generate any revenue from the sales of real estate property for the years ended December 31, 2015 and 2014.

Cost of Revenue.

Our cost of revenue sold consists of the cost of purchased goods. During the year ended December 31, 2015, our cost of goods sold was $nil, compared to $3,693,783 for the cost of goods sold for the year ended December 31, 2014, a decrease of $3,693,783 or approximately 100.0%. The decrease in the cost of revenue was mainly due to the lack of steel trading during the fiscal year ended 2015.

Gross loss.

Our gross margin increased from a loss of $235,488 for the fiscal year ended December 31, 2014 to $nil for the fiscal year ended December 31, 2015. The increase of the gross margin is mainly due to the lack of steel trading during the fiscal year ended December 31, 2015 and we sold steel for less than the cost of goods during the fiscal year ended December 31, 2014.

| 25 |

Operating expenses.

Operating expenses totaled $4,559,223 for the year ended December 31, 2015, compared to $2,178,365 for the year ended December 31, 2014, an increase of $2,380,860, or approximately 209%. The significant increase is mainly because of significant increase of general and administrative expenses offset by decrease in selling expenses.

Selling, general and administrative expenses.

Selling expenses decrease from $87,866 for the fiscal year ended December 31, 2014 to $11,577 for the fiscal year ended December 31, 2015, a decrease of $76,289, or approximately 86.83%. The decrease is mainly attributable to decrease in steel trading during the fiscal year ended December 31, 2015.

Our general and administrative expenses consist of salaries, office expenses, utilities, business travel, amortization expenses (including legal expenses, accounting expenses and other professional service expenses) and stock compensation. General and administrative expenses were $4,547,646 for the fiscal year ended December 31, 2015, compared to $2,090,499 for the fiscal year ended December 31, 2014, an increase of $2,457,147 or 218 %. The significant increase is mainly because of the increase of expenses related to professional fees.

Loss from operations.

As a result of the factors described above, operating loss was $4,559,223 for the fiscal year ended December 31, 2015, compared to operating loss of $2,413,853 for the fiscal year ended December 31, 2014, an increase of operating loss of $2,145,370, or approximately 209%.

Other income and expenses.