UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

OR

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from_____________ to _____________.

Commission file number 000-54267

| FREEZE TAG, Inc. |

| (Exact name of registrant as specified in its charter) |

| Delaware |

| 20-4532392 |

| (State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

|

| 18062 Irvine Blvd., Suite 103 Tustin, California |

|

92780 |

| (Address of principal executive offices) |

| (Zip Code) |

Registrant’s telephone number, including area code: (714) 210-3850

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

| Trading Symbol |

| Name of each exchange on which registered |

| None |

| None |

| None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.00001

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

|

|

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

Aggregate market value of the voting stock held by non-affiliates as of June 30, 2020: $506,450 based on the closing price of $0.016 on June 30, 2020 of our common stock. The voting stock held by non-affiliates on that date consisted of 31,653,123 shares of common stock.

Applicable Only to Registrants Involved in Bankruptcy Proceedings During the Preceding Five Years:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date. As of March 31, 2021, there were 75,056,123 shares of common stock, par value $0.00001, issued and outstanding.

Documents Incorporated by Reference

List hereunder the following documents if incorporated by reference and the Part of the Form 10-K (e.g., Part I, Part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or information statement; and (3) Any prospectus filed pursuant to rule 424(b) or (c) of the Securities Act of 1933. The listed documents should be clearly described for identification purposes (e.g., annual report to security holders for fiscal year ended December 24, 1980). None.

Freeze Tag, Inc.

| 2 |

| Table of Contents |

Explanatory Note

This Annual Report includes forward‑looking statements within the meaning of the Securities Exchange Act of 1934 (the “Exchange Act”). These statements are based on management’s beliefs and assumptions, and on information currently available to management. Forward‑looking statements include the information concerning possible or assumed future results of operations of the Company set forth under the heading “Management's Discussion and Analysis of Financial Condition or Plan of Operation.” Forward‑looking statements also include statements in which words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” “consider” or similar expressions are used.

Forward‑looking statements are not guarantees of future performance. They involve risks, uncertainties and assumptions. The Company’s future results and shareholder values may differ materially from those expressed in these forward‑looking statements. Readers are cautioned not to put undue reliance on any forward‑looking statements.

Corporate History

We were incorporated as Freeze Tag, Inc. in February 2006 in the State of Delaware. In March 2006, Freeze Tag, LLC, our predecessor which was formed in October 2005, was merged with and into Freeze Tag, Inc. In October of 2017, we completed a merger transaction with Munzee Inc. in a transaction in which Freeze Tag, Inc. became the surviving entity and both companies merged their operations together (the “Merger”). Under U.S. generally accepted accounting principles, the Merger is treated as a “reverse merger” under the purchase method of accounting, with Munzee as the accounting acquirer. Accordingly, Munzee’s historical financial results of operations replace Freeze Tag’s historical financial results of operations for all periods prior to the Merger and, for all periods following the Merger, our financial statements include the financial results of operations of the combined company. Beginning in the quarter ended March 31, 2020, our wholly-owned subsidiary, Space Coast Geo Store, LLC, a Florida limited liability company, sells merchandise to the geocaching industry. The consolidated entity maintains offices in Tustin, California and McKinney, Texas. Other corporate actions that occurred as a result of the merger are that Robert Vardeman, Jr., former CEO of Munzee Inc. became President of Freeze Tag, Inc. and both Robert Vardeman, Jr. and Robert D. Vardeman were added to the Freeze Tag, Inc. Board of Directors. Our Board of Directors currently consists of Craig Holland, Mick Donahoo, Robert Vardeman, Jr., and Robert D. Vardeman.

Business Overview

Freeze Tag, Inc. is a creator of location-based, mobile social games that are fun and engaging for consumers and businesses. Based on a free-to-play business model that has propelled games built and marketed by some of our competitors to worldwide success, we employ state-of-the-art data analytics and proprietary technology to dynamically optimize the gaming experience for revenue generation. Players can download and enjoy our games for free, and, if they so choose, they can purchase virtual items and additional features within the game to increase the fun factor.

Founded by gaming industry veterans, Freeze Tag has launched several successful games over the course of its history. Our current portfolio includes hits such as Munzee®, a social platform with over 10 million locations worldwide and hundreds of thousands of players that blends gamification and geolocation into an experience that rewards players for going places in the physical world, Garfield Go, a Pokemon Go style augmented reality game based on the iconic cat Garfield, WallaBee®, an addictive collecting game with over 2,000 beautifully drawn digital cards, as well as many social mobile games that provide endless hours of family-friendly fun. We also offer our technology and services to third party businesses that want to leverage mobile gaming in their marketing and branding programs. For example, our Eventzee® solution allows businesses to create private scavenger hunts in physical places such as malls, tradeshows, company events or campuses to create immersive brand experiences.

| 3 |

| Table of Contents |

In Q4 of 2019, we embarked upon another major development project involving our Eventzee app. We have completely re-designed the Eventzee app, adding many features requested by our customers over the years.

In Q2 of 2020, we launched the revised Eventzee. The new and improved version of Eventzee offers more activity types (7 in total) than most of its competitors with Info, Text Entry, Photo, Video, Quiz, QR Code, and GPS challenges. The new Eventzee also allows event hosts to group challenges together by theme, type, or location providing a much-needed organizational tool.

In May of 2020, we also launched a private label version of Eventzee for our client Barnes Harley-Davidson based in British Columbia, Canada. The relationship with Barnes Harley-Davidson has continued to grow as we have expanded the number of Eventzee events offered to Barnes’ customers in 2021.

Throughout the second half of 2020, we were able to obtain a number of new types of customers for the Eventzee platform, including downtown marketing organizations who are members of the IDA (International Downtown Association) such as Downtown Evanston, Downtown Jacksonville, and Downtown Sacramento and many more. Through the new markets and rapid acceptance of a new and improved Eventzee app, Freeze Tag has realized increased revenue opportunities.

Growing the Eventzee customer base is part of a long-term plan to add additional sources of revenue to the Freeze Tag top line. The Eventzee platform expansion depends upon business-to-business sales, complimenting the consumer-based revenue model of Munzee and other Freeze Tag apps. Eventzee is usually free to play for Eventzee players. Clients pay Freeze Tag a per user licensing fee to use the Eventzee software to create custom-designed events for their participants. The market opportunity for Eventzee services is large with potential clients in a wide array of industries and applications, including cities, tourism centers, parks and zoos, educational institutions, brands and marketing organizations, companies looking for team building tools, and many more. For more information, we refer you to the Eventzee web site: www.eventzeeapp.com.

Our mission is to design, develop and deliver innovative digital entertainment that surprises and delights. Our products bring families together by providing fun to kids of all ages. We also strive to create a workplace environment where creativity and fun can thrive in a demanding industry.

Business Strategy

In recent years, we have shifted our business strategy to focus our efforts on creating free-to-play (FTP) social games for the mobile market. We’ve made this change because we believe that games that are social and mobile will provide the greatest revenue opportunities now and in the foreseeable future. This change in direction has not been an easy one as we’ve had to deploy resources differently, learn new techniques, and experiment with new game designs and marketing processes. As we realize success with profitable free-to-play games like Munzee and WallaBee, we are realizing dividends from the many hours invested in learning, experimenting and testing FTP game mechanics and marketing techniques.

We have also announced our intention to grow through acquisition. The merger with Munzee Inc. is evidence that we are making progress on our intention to grow the business through merging and/or acquiring other companies in our field. During 2018, we focused a great deal of management effort on building a successful multi-office and multi-state team, developing communications, reporting, and working relationships to integrate all of the Freeze Tag employees and contractors into a cohesive, thriving worldwide team.

| 4 |

| Table of Contents |

We still feel that the time is right to build an alliance of mobile game developers who can become stronger and more successful by working together to build a company that can leverage market intelligence, development expertise and cross-promotional opportunities to achieve great results for our customers and shareholders.

During 2021 and beyond, we will continue to look for acquisition candidates and propose transactions in cases where it makes sense for both parties and will enhance the value of the company.

In the event we do enter into any such transactions in the future, such transactions will likely be accomplished through the issuance of shares of our stock and/or in connection with a strategic financial investor, and not with cash directly from us unless and until our cash position improves.

Free-to-play Business Model

The free-to-play business model for games was pioneered on the PC platform and has exploded globally on the mobile platform. The free-to-play model allows users to download and play an enjoyable, but limited, portion of a game for free. If the user wants to access premium features or special virtual items to increase the fun factor, then the user is required to pay, usually $0.99 per feature or item or $0.99 for a bundle of virtual items. For example, if a player has run out of “lives” or “moves” in a game, the player is given two options: 1) Wait for the lives to re-charge which involves waiting but no expense of money or virtual currency; 2) Spend money or virtual currency to buy additional “lives” and keep playing immediately.

With the exception of the Eventzee platform, we adhere to the “free-to-play” business model in our currently live Freeze Tag games. In Munzee, players can purchase blast caps to capture virtual munzees deployed near them. WallaBee also offers players a chance to “forage” for honeycombs for free or they may be purchased as in-game items. In all cases, Munzee, WallaBee and Garfield Go are games that players can and do play for free, yet by spending money on additional items, the gameplay experience is enhanced.

Over the last several years, the free-to-play business model has proven to be a very successful model for mobile games. The revenue potential of a game largely depends on the fun-factor and popularity of the game and the game creator’s proprietary techniques for encouraging the player to make a purchase decision – without overly offending the player. The potential for rapidly spreading the game through social networks and small in-game purchases can add up to a very sizeable business opportunity, as evidenced by many mobile games generating millions and even billions of dollars based solely on an accumulation of players making many individual item purchases.

Going forward, we plan on the majority of Freeze Tag’s mobile games to be based on the free-to-play model. In addition, we believe that games are more fun with friends, so we connect our players with major social networks such as Facebook and Twitter to enhance the games’ addictiveness, enjoyment and world-of-mouth referrals. We also offer ways for players to communicate directly with each other in Munzee and WallaBee to enhance the feeling of community and comradery. In both Munzee and WallaBee mobile apps, there are certain aspects of gameplay that are more enjoyable when the experience is shared with other players.

Since mobile app development technology is constantly changing and evolving, we review and research platforms, tools, techniques, and third-party SDK’s on a routine basis to ensure we are in synch with the market. In executing our business model, we have derived the most benefit from employing proprietary game engine(s) built on commonly used technologies (like Cordova, HTML5, and others) because using our own tools and techniques allows us to be nimble and anticipate market changes.

In the future, we plan to continue to employ our game engine(s). This approach allows us to find the best development teams, engineering teams, and partners to help us quickly deploy our games.

| 5 |

| Table of Contents |

The Freeze Tag Strategy

In targeting the global market for mobile games, we are highly focused on developing mobile social games that are casual, fun and engaging for all ages and genders. The free-to-play business model combined with the use of best-in-class development environments and Analytics and Deployment tools, allows us to systematically launch, optimize and monetize our games. We design our games to be never ending entertainment that our users will enjoy playing and be willing to pay us $0.99 or more from time-to-time for special features and virtual items to keep having fun. We believe that the free-to-play model should not be run as a sprint but rather as a marathon. Over the span of several months, or even years, each game is continuously subject to this optimization process to increase user enjoyment and financial return to the company.

Distribution and Marketing

We market, sell and distribute our games primarily through direct-to-consumer digital storefronts, such as Apple’s App Store, the Google Play Store and Amazon’s App Store. We also sell to our players directly through our own web site http://www.freezetag.com and https://store.freezetag.com. We work with payment vendors like Shopify, Square and PayPal to process our online payments. In addition to publishing our smartphone games on direct-to-consumer digital storefronts, we also publish some of our titles on other platforms, such as the Facebook App Store, the Mac App Store and PC Download portals such as Big Fish Games and others.

User Acquisition

In the free-to-play business model, a constant stream of new players is necessary to be successful. So, we have partnered with advertising networks and lead generation companies such as Facebook and Google to help us reach the appropriate audience for our products. We also employ data analytics to determine which creative messages and which lead referral sources are bringing in the most players who spend money in our games.

To help reduce the cost of acquiring downloads, we have embedded social networking mechanisms into our games to enable our best customers to do the marketing for us. Every time a satisfied player invites her friend to play one of our games, we have been introduced to a new potential customer without incurring a cost to entice that player to download the game. We will continue to design methods to encourage our players to invite their friends and spread the word about our games. Each time a user downloads one of our games from a friend referral without a direct expense from us, our user acquisition cost is lower, and therefore our profitability is potentially higher.

Technology and Tools

Free-to-play Revenue Model

The game industry, like many other forms of entertainment (music, TV, books, etc.) has undergone a major shift. The free-to-play business model has increased in appeal to game players of every genre and platform. Nowhere has this been felt more deeply than the mobile market. Free is a very powerful marketing approach that is irresistible to game players. The top grossing charts on popular mobile app stores like Apple, Google, and Amazon continually show that “free” games earn the most revenue for their developers. So, with all this “free-ness,” how does a game creator make any money?

Optimizing Customer Lifetime Value

The key business metric of any free-to-play game is the Customer Lifetime Value (CLV). A free-to-play gamer starts out as a zero-revenue customer, but he or she may become a paying customer throughout the customer’s life of playing the game. The game creator’s business is an ongoing engagement with the game players to get them to buy things in the game, without ruining the fun. Optimizing this delicate balance is where the most revenue can be extracted.

| 6 |

| Table of Contents |

This combination allows us to optimize the features of our games to refresh and update the content so that players are happily engaged and invite their friends to play with them. When players invite their friends, they lower our user acquisition costs. The longer and more often players come back to play, the more likely they are to spend money on virtual goods (through in-game purchases). The net result is a customer with a greater lifetime value. The happier customers are, the more they share with their friends and the more often they come back to spend money. Everything we do is geared to our players having more fun because ultimately customer fun translates into revenue.

Data Analytics

By using commercial and proprietary data analytics tools, we analyze various aspects of the game across the entire pool of players to determine what modifications can be made to the game, which allows us to: (1) make it more fun, and (2) induce a purchase.

Some of the analysis we perform regularly are:

|

| · | Analyze the number of users that complete the tutorial process |

|

| · | Identify the Day 1, Day 7, and Day 30 retention metrics of how many players are returning to play |

|

| · | Quantify the ARPDAU (average revenue per daily active user) to determine the monetization effectiveness of each game |

|

| · | Determine the percentage of overall users that are converting to spenders |

|

| · | Quantify the ARPPDAU (average revenue per paying daily active user) |

|

| · | Determine what parts of the game users are playing most |

|

| · | Identify where in the game users are dropping out, and find out why |

|

| · | Average play time per day and per session |

|

| · | Importance of social networks, like Facebook and Twitter, to the game and how many players login to social networks |

|

| · | Frequency of users playing against friends |

|

| · | Identify what events most correlate with purchase events |

|

| · | Identify how many invites a user is sending out, how long it takes them to send the first invite out, and how many of those players are coming in. |

Dynamic Game Engine(s)

Over the years, we have developed proprietary dynamic game engine(s) (Freeze Tag Engine(s)) that allows us to make changes to game play and game economies on-the-fly, in most cases, without requiring the download of another update. We also integrate several business analytics packages, and other key game management tools into our games that provide us with real time data to measure detailed player behavior, and respond directly to that behavior. We continue to develop and enhance our own game engine(s) which use web-friendly technology that can be easily ported to the most popular mobile platforms, iOS and Android. As our games have become more sophisticated with the need for constant data connection and several points of data required to be associated with physical locations on a map, we have developed server-side tools to handle these requirements.

Over the years, the Freeze Tag Game Engine(s) have allowed us the ability to port across multiple platforms using a single codebase. We continue to look to contract with outside teams and outside contractors, allowing us to maintain a smaller internal team.

As we continue our development efforts, our approach is to review the technical requirements of the game we want to develop, then make a decision as to which Game Engine is the most appropriate to implement for that development effort, whether that be our own proprietary game engine based on web technologies or third-party platforms such as Unity 3D.

| 7 |

| Table of Contents |

As we make decisions about which Game Engine to employ, here are a few of the things that we look to have:

|

| · | A single codebase that can be easily ported to other platforms |

|

| · | Ability to “bolt on” other technologies and codes to easily integrate with other SDK’s, platforms and special needs |

|

| · | Interface easily with scalable backend databases and architecture |

|

| · | Easily localized into new languages |

|

| · | Updates can be pushed to the game allowing us to change things like: |

|

| ○ | adding new characters |

|

| ○ | changing the values in the economy |

|

| ○ | updating text |

|

| ○ | messaging users (in game) about new features |

|

| ○ | instigating a social network based contest |

Integrated Feedback Mechanisms

In addition, we aim to integrate feedback mechanisms into our games to provide incentive for our players to communicate their favorite features and any technical difficulties they may be experiencing. By combining dynamic gaming technology and data analytics into one integrated business process, we can optimize the “fun” factor for our players and maximize our revenue potential.

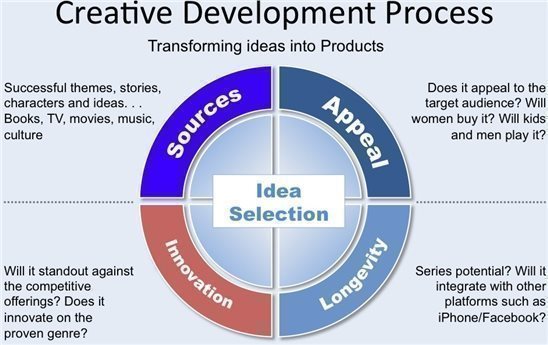

Product Development

We have learned that establishing and following a fairly rigid process is essential to producing commercially successful products, regardless of the platform. The process all begins with the creative development process. The chart below describes the approach we use to filter ideas and make final decisions on which games we will actually produce. After choosing the game that we will focus on, we write a detailed design document. A thorough design document ensures that all of those involved in the creation of the game have a common reference source throughout the production process. Also, critical to producing high quality games, a test plan accompanies every design document. Not only do we test for bugs, but also we test the game for usability. Since most casual gamers do not want to read instructions, it is critical that the finished game be easy to play by just tapping at objects on the screen.

| 8 |

| Table of Contents |

As a developer of mobile social games, we have developed expertise in three core aspects of game production. These core competencies help to give us a competitive advantage in the industry. They are listed below, with the resulting benefit also identified.

| 1. | Create High Quality Products (including art and sound assets). Benefit: Provides high value to distribution partners and consumers, resulting in increased downloads and purchases. |

|

|

|

| 2. | Maintain Flexible Engineering Tools and Processes. Benefit: Decreases time-to-market delivery of products. |

|

|

|

| 3. | Minimize Risk by doing the following: 1) selecting proven genres, 2) keeping development costs low, and 3) modifying designs “on the fly” based on consumer feedback. Benefit: Increases the number of games released per year and decreases reliance on any one title’s success, ultimately improving return on investment for each game. |

Competition

The business of mobile games is very competitive. New products are introduced frequently and the platforms and devices change rapidly. To be successful in this crowded marketplace, we have to entice consumers to play our games based on the quality and “fun” of the experience. Players evaluate our games based on the game play, graphics quality, the music and sound effects and the efficiency and clarity of our software engineering and user interface design.

We compete with a continually increasing number of successful location based mobile game companies, including Niantic (makers of Pokemon Go), Geocaching, Seek, and many others.

In addition, given the open nature of the development and distribution for mobile devices, we also compete or will compete with a vast number of small companies and individuals who are able to create and launch games and other content for these devices using relatively limited resources and with relatively limited start-up time or expertise.

Some of our competitors and our potential competitors have one or more advantages over us, either globally or in particular geographic markets, which include:

|

| · | significantly greater financial resources; |

|

| · | greater experience with the free-to-play games and games-as-a-service (GAAS) business models and more effective game monetization; |

|

| · | stronger brand and consumer recognition regionally or worldwide; |

|

| · | greater experience and effectiveness integrating community features into their games and increasing the revenues derived from their users; |

|

| · | larger installed customer bases from their existing mobile games; |

|

| · | the capacity to leverage their marketing expenditures across a broader portfolio of mobile and non-mobile products; |

|

| · | larger installed customer bases from related platforms, such as console gaming or social networking websites, to which they can market and sell mobile games; |

|

| · | more substantial intellectual property of their own from which they can develop games without having to pay royalties; |

|

| · | better overall economies of scale; |

|

| · | greater platform-specific focus, experience and expertise; and |

|

| · | broader global distribution and presence. |

| 9 |

| Table of Contents |

Intellectual Property

Our intellectual property is an essential element of our business. We use a combination of trademark, patent, copyright, trade secret and other intellectual property laws, confidentiality agreements and license agreements to protect our intellectual property. We have also registered a number of domain names, which we believe will be important to the branding and success of our games. Our employees and independent contractors are required to sign agreements acknowledging that all inventions, trade secrets, works of authorship, developments and other processes generated by them on our behalf are our property, and assigning to us any ownership that they may claim in those works. Despite our precautions, it may be possible for third parties to obtain and use without consent intellectual property that we own or license. Unauthorized use of our intellectual property by third parties, and the expenses incurred in protecting our intellectual property rights, may adversely affect our business.

We intend to register ownership of software copyrights in the United States as well as seek registration of various trademarks associated with the Company’s name and mobile social games that we will develop.

Wherever possible, we own registered trademark protection for properties we develop. As the digital markets evolve, there are and will continue to be many competitors who will imitate successful game properties. We are investing in trademark protection to create game brands and protect them. For example, we have received approval from the United States Patent and Trademark Office to register Unsolved Mystery®, Unsolved Mystery Club®, Ancient Astronauts®, Victorian Mysteries®, Grimm Reaper® and Rocket Weasel® for all gaming platforms. Munzee Inc. has previously received approval for the trademarks Munzee®, Eventzee®, and WallaBee®. These marks will assist us in defending against copycats who may try to incorporate these terms into their game titles.

From time to time, we may encounter disputes over rights and obligations concerning intellectual property. While we believe that our product and service offerings do not infringe the intellectual property rights of any third party, we cannot be assured that we will prevail in any intellectual property dispute. If we do not prevail in such disputes, we may lose some or all of our intellectual property protection, be enjoined from further sales of the applications determined to infringe the rights of others, and/or be forced to pay substantial royalties to a third party.

Business Acquisitions

In addition to our current operations, we propose to seek, investigate and, if warranted, acquire an interest in one or more businesses. The merger with Munzee Inc. is evidence of our pursuit of this strategy. We propose to investigate potential opportunities, particularly focusing upon existing privately held businesses whose owners are willing to consider merging their businesses into our company in order to establish a public trading market for their common stock, and whose managements are willing to operate the acquired businesses as divisions or subsidiaries of our company. The businesses we acquire may or may not need an injection of cash to facilitate their future operations. Presently, if we acquire any businesses, we envision such acquisition being completed either with our shares of our stock or with the assistance of a strategic funding partner. We currently do not have substantial funds, or a revenue stream, to make acquisitions utilizing cash.

We are primarily interested in other technology opportunities, but we currently do not intend to restrict our search for investment opportunities to any particular industry or geographical location and may, therefore, engage in essentially any business. Our executive officers will review material furnished to them by the proposed merger or acquisition candidates and will ultimately decide if a merger or acquisition is in our best interests and the interests of our shareholders. We intend to source business opportunities through our officers and directors and their contacts. Those contacts include professional advisors such as attorneys and accountants, securities broker dealers, venture capitalists, members of the financial community, other businesses and others who may present solicited and unsolicited proposals. Management believes that business opportunities and ventures may become available to it due to a number of factors, including, among others: (1) management’s willingness to consider a wide variety of businesses; (2) management’s contacts and acquaintances; and (3) our flexibility with respect to the manner in which we may be able to structure, finance, merge with or acquire any business opportunity.

| 10 |

| Table of Contents |

The analysis of new business opportunities will be undertaken by or under the supervision of our executive officers and directors. Inasmuch as we will have limited funds available to search for business opportunities and ventures, we will not be able to expend significant funds on a complete and exhaustive investigation of such business or opportunity. We will, however, investigate, to the extent believed reasonable by our management, such potential business opportunities or ventures by conducting a so-called “due diligence investigation”.

In a so-called “due diligence investigation,” we intend to obtain and review materials regarding the business opportunity. Typically, such materials will include information regarding a target business’ products, services, contracts, management, ownership, and financial information. In addition, we intend to cause our officers or agents to meet personally with management and key personnel of target businesses, ask questions regarding our prospects, tour facilities, and conduct other reasonable investigation of the target business to the extent of our limited financial resources and management and technical expertise.

Government Regulation

Because of our recent partnership with Paws Inc. (Garfield license), and our development of Augmented Reality / Geolocation games, and the types of data that we collect in those games, we must be more mindful of government regulations regarding the Children’s Online Privacy Protection Act or COPPA. To protect minors on the Internet (and now mobile devices), U.S. officials passed The Children’s Online Privacy Protection Act (COPPA). Essentially, COPPA governs online data collection of people aged 13 and younger. The COPPA rules define privacy policy requirements, data collection parameters, and the process of acquiring verifiable parental consent. In the past, we have disclosed the information that we collect in Privacy Policies, but now need to focus on getting parental approval for certain types of applications as they relate to children under the age of 13.

Our Employees

We have 13 employees, that work in our offices in Tustin, California, McKinney, Texas, and other remote locations throughout the world. Four of these are managers, one is administrative staff, and the remaining nine are artists, engineers, production staff, etc. We also work with several other artists, engineers, designers, and contractors on an as-needed basis.

Human Capital Resources

As noted above, we only have a small number of employees. The remainder of our workforce is consultants due to the nature of our business. As it relates to our employees and the consultants that work with us:

Oversight and Management

Our executive officers are tasked with leading our organization in managing employment-related matters, including recruiting and hiring, onboarding and training, compensation planning, talent management and development. We are committed to providing team members with the training and resources necessary to continually strengthen their skills. Our executive team is responsible for periodically reviewing team member programs and initiatives, including healthcare and other benefits, as well as our management development and succession planning practices. Management periodically reports to the Board regarding our human capital measures and results that guide how we attract, retain and develop a workforce to enable our business strategies.

| 11 |

| Table of Contents |

Diversity, Equity and Inclusion

We believe that a diverse workforce is critical to our success, and we continue to monitor and improve the application of our hiring, retention, compensation and advancement processes for women and underrepresented populations across our workforce, including persons of color, veterans and LGBTQ to enhance our inclusive and diverse culture. We continue to invest in recruiting diverse talent.

Workplace Safety and Health

A vital part of our business is providing our workforce with a safe, healthy and sustainable working environment. We focus on implementing change through workforce observation and feedback channels to recognize risk and continuously improve our processes.

Importantly during 2020, our focus on providing a positive work environment on workplace safety have enabled us to preserve business continuity without sacrificing our commitment to keeping our colleagues and workplace visitors safe during the COVID-19 pandemic. We took immediate action at the onset of the COVID-19 pandemic to enact safety protocols in our facilities by improving sanitation measures, implementing mandatory social distancing, use of face coverings, reducing on-site workforce through staggered shifts and schedules, remote working for most employees, and restricting visitor access to our locations. These actions helped minimize the impact of COVID-19 on our workforce.

Description of Property

Our executive offices are located in Tustin, California, at 18062 Irvine Blvd, Suite 103, Tustin, CA 92780 and are leased on a month-to-month basis at a cost of $1,173 per month. Our production office in Texas is located at 1441 Redbud Blvd., Suite 201, McKinney, TX 75069 and we are currently in the third year of a 3-year lease. Current monthly lease payment is $2,850 per month plus utilities.

Available Information

We are a fully reporting issuer, subject to the Securities Exchange Act of 1934. Our Quarterly Reports, Annual Reports, and other filings can be obtained from the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549, on official business days during the hours of 10 a.m. to 3 p.m. You may also obtain information on the operation of the Public Reference Room by calling the Commission at 1-800-SEC-0330. The Commission maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the Commission at http://www.sec.gov.

Our Internet website address is http://www.freezetag.com/.

| 12 |

| Table of Contents |

As a smaller reporting company, we are not required to provide a statement of risk factors. However, we believe this information may be valuable to our shareholders. We reserve the right to not provide risk factors in our future filings. We face risks in developing our games and products and eventually bringing them to market. The following risks are material risks that we face. If any of these risks occur, our business, our ability to achieve revenues, our operating results and our financial condition could be seriously harmed. Our primary risk factors and other considerations include:

Risk Factors Related to the Business of the Company

We have incurred losses from operations, and we may never generate substantial revenue or become profitable.

We incurred net losses of $269,582 for the year ended December 31, 2020. As of December 31, 2020, we had a working capital deficit of $668,493 and a total stockholders’ deficit of $673,797. The Company reported net cash used by operating activities of $84,741 for the year ended December 31, 2020. Management believes that by implementing cost reductions and realizing cost efficiencies from the Merger, operating cash flows will be sufficient to support our business plan. We will also continue to develop and launch new games to maximize revenues. There can be no assurance that we will be successful in these efforts.

Our ability to generate revenues from any of our games will depend on a number of factors, including our ability to satisfy consumer demand identify appropriate commercialization strategies, and successfully market and sell our games. Our ultimate success will depend on many factors, including factors outside of our control. We may never successfully commercialize or achieve and sustain market acceptance of any of our games, our game operations may not generate sufficient revenue to support our business, and we may never reach the level of sales and revenues necessary to achieve and sustain profitability.

If we are unable to meet our future capital needs, we may be required to reduce or curtail operations.

Since 2017, we have relied on cash flow from operations to fund operations. We have limited cash liquidity and capital resources. Our cash on hand as of December 31, 2020, was $491,639, and our projected monthly expenditures rate is approximately $165,000. For the year ended December 31, 2020, our revenues were $1,779,733.

Our future capital requirements will depend on many factors, including our ability to market our products successfully, cash flow from operations, and competing market developments. Based on our current financial situation we may have difficulty continuing our operations at their current level, or at all, if we do not receive additional financing in the near future. Consequently, although we currently have no specific plans or arrangements for financing, we intend to raise funds through private placements, public offerings or other financings. Any equity financings would result in dilution to our then-existing stockholders. Sources of debt financing may result in higher interest expense. Any financing, if available, may be on unfavorable terms. If adequate funds are not obtained, we may be required to reduce or curtail operations. We anticipate that our existing capital resources will not be adequate to satisfy our operating expenses and capital requirements for any length of time. However, this estimate of expenses and capital requirements may prove to be inaccurate.

Debt financing is difficult to obtain.

Debt financing is difficult to obtain in the current credit markets. This difficulty may make future acquisitions either unlikely, or too difficult and expensive. This could materially adversely affect our company and the trading price of our common stock.

| 13 |

| Table of Contents |

Raising capital by borrowing could be risky.

If we were to raise capital by borrowing to fund our operations or acquisitions, it could be risky. Borrowing through non-convertible instruments typically results in less dilution than in connection with equity financings, but it also would increase our risk, in that cash is required to service the debt, ongoing covenants are typically employed which can restrict the way in which we operate our business, and if the debt comes due either upon maturity or an event of default, we may lack the resources at that time to either pay off or refinance the debt, or if we are able to refinance, the refinancing may be on terms that are less favorable than those originally in place, and may require additional equity or quasi equity accommodations. These risks could materially adversely affect our company and the trading price of our common stock.

Our financing decisions may be made without stockholder approval.

Our financing decisions and related decisions regarding levels of debt, capitalization, distributions, acquisitions and other key operating parameters, are determined by our board of directors in its discretion, in many cases without any notice to or vote by our stockholders. This could materially adversely affect our company and the trading price of our common stock.

Our independent registered public accounting firm has expressed doubts about our ability to continue as a going concern.

As a result of our financial condition, we have received a report from our independent registered public accounting firm for our financial statements for the year ended December 31, 2020 that includes an explanatory paragraph describing the uncertainty as to our ability to continue as a going concern. In order to continue as a going concern, we must effectively balance many factors and increase our revenues to a point where we can better fund our operations from our sales and revenues. If we are not able to do this, we may not be able to continue as an operating company.

Because we face intense competition, we may not be able to operate profitably in our markets.

The market for casual games is highly competitive and is becoming more so, which could hinder our ability to successfully market our products. We may not have the resources, expertise or other competitive factors to compete successfully in the future. We expect to face additional competition from existing competitors and new market entrants in the future. Many of our competitors have greater name recognition and more established relationships in the industry than we do. As a result, these competitors may be able to:

|

| · | develop and expand their product offerings more rapidly; |

|

| · | adapt to new or emerging changes in customer requirements more quickly; |

|

| · | take advantage of acquisition and other opportunities more readily; and |

|

| · | devote greater resources to the marketing and sale of their products and adopt more aggressive pricing policies than we can. |

If we are unable to maintain brand image or product quality, our business may suffer.

Our success depends on our ability to maintain and build brand image for our existing products, new products and brand extensions. We have no assurance that our advertising, marketing and promotional programs will have the desired impact on our products’ brand image and on consumer preferences.

If we are unable to attract and retain key personnel, we may not be able to compete effectively in our market.

Our success will depend, in part, on our ability to attract and retain key management, including primarily Robert Vardeman, Jr., Craig Holland and Mick Donahoo, technical experts, and sales and marketing personnel. We attempt to enhance our management and technical expertise by recruiting qualified individuals who possess desired skills and experience in certain targeted areas. Our inability to retain employees and attract and retain sufficient additional employees, and information technology, engineering and technical support resources, could have a material adverse effect on our business, financial condition, results of operations and cash flows. The loss of key personnel could limit our ability to develop and market our products.

| 14 |

| Table of Contents |

Because our officers and directors control our common stock vote, they have the ability to influence matters affecting our shareholders.

As of December 31, 2020, there were 75,056,123 outstanding shares of Common Stock, no outstanding shares of Series A Preferred Stock (“Series A Preferred”), 2,480,482 shares of Series B Preferred Stock (“Series B Preferred”), and 4,355,000 shares of Series C Preferred Stock (“Series C Preferred”). Our officers and directors own a significant portion of our outstanding voting rights on any matters that may be brought before our shareholders for a vote. As a result, they have the ability to influence matters affecting our shareholders, including the election of our directors, the acquisition or disposition of our assets, and the future issuance of our shares. Because they control such shares, investors may find it difficult to replace our management if they disagree with the way our business is being operated. Because the influence by these insiders could result in management making decisions that are in the best interest of those insiders and not in the best interest of the investors, you may lose some or all of the value of your investment in our common stock.

Our business may be negatively impacted by a slowing economy or by unfavorable economic conditions or developments in the United States and/or in other countries in which we operate.

A general slowdown in the economy in the United States or unfavorable economic conditions or other developments may result in decreased consumer demand, business disruption, foreign currency devaluation, inflation or deflation. A slowdown in the economy or unstable economic conditions in the United States or in the countries in which we operate could have an adverse impact on our business results or financial condition.

Social distancing and “stay-at-home” orders caused by the coronavirus may adversely impact our geolocation games, which require users to be outdoors and visiting various locations.

Some of our most successful games are geolocation games, in which the user plays the game while exploring outdoors with certain aspects of the outdoors augmented with gameplay features. With many state and localities requiring or encouraging people to stay at home and/or apply social distancing due to the coronavirus, some of our users did not go outside as much, and, as a result, did not play our geolocation games as much. As a result, users did not purchase the in-game additions, which caused us to experience decreased revenue. Additionally, for some of our games, we host events for our users to attend and play the game together and receive certain promotional items. Many states and localities are limiting the number of people that be together in any one location to 10 or less people. As a result we have had to postpone certain events, and will likely have to postpone additional ones in the future, which may decrease both downloads of our games, as well in-game purchases.

We may not be able to effectively manage our growth and operations, which could materially and adversely affect our business.

We may experience rapid growth and development in a relatively short period of time by aggressively marketing our casual games. The management of this growth will require, among other things, continued development of our financial and management controls and management information systems, stringent control of costs, increased marketing activities, the ability to attract and retain qualified management personnel and the training of new personnel. We intend to hire additional personnel in order to manage our expected growth and expansion. Failure to successfully manage our possible growth and development could have a material adverse effect on our business and the value of our common stock.

| 15 |

| Table of Contents |

Failure to renew our existing licenses or to obtain additional licenses could harm our business.

Some of our game products are or will be based on or incorporate intellectual properties that we license from third parties. Our current licenses to use these properties do not extend beyond terms of two to three years. We may be unable to renew these licenses on terms favorable to us, or at all, and we may be unable to secure alternatives in a timely manner. We expect that licenses we obtain in the future may impose development, distribution and marketing obligations on us. If we breach our obligations, our licensors may have the right to terminate the license or change an exclusive license to a non-exclusive license.

Competition for licenses may also increase the advances, guarantees and royalties that we must pay to the licensor, which could significantly increase our costs. Failure to maintain our existing licenses or obtain additional licenses with significant commercial value could impair our ability to introduce new applications or continue our current game products and applications, which could materially harm our business.

If we fail to develop and introduce new casual games and other applications that achieve market acceptance, our sales could suffer.

Our business depends on providing casual games and applications that consumers initially want to download to their devices and then make subsequent in-game purchases. We must invest significant resources in research and development to enhance our offering of casual games and other applications and introduce new games and other applications. Our operating results would suffer if our games and other applications are not responsive to the preferences of our customers or are not effectively brought to market.

The planned timing or introduction of new casual games is subject to risks and uncertainties. Unexpected technical, operational, deployment, distribution or other problems could delay or prevent the introduction of new casual games, which could result in a loss of, or delay in, revenues or damage to our reputation and brand. If any of our applications is introduced with defects, errors or failures, we could experience decreased sales, loss of customers and damage to our reputation and brand. In addition, new applications may not achieve sufficient market acceptance to offset the costs of development. Our success depends, in part, on unpredictable and volatile factors beyond our control, including customer preferences, competing applications and the availability of other entertainment activities. A shift in Internet or mobile device usage or the entertainment preferences of our customers could cause a decline in our applications’ popularity that could materially reduce our revenues and harm our business.

We intend to continuously develop and introduce new games and other applications for use on next-generation Internet and mobile devices. We must make product development decisions and commit significant resources well in advance of the anticipated introduction of new mobile devices. New mobile devices for which we will develop applications may be delayed, may not be commercially successful, may have a shorter life cycle than anticipated or may not be adequately promoted by wireless carriers or the manufacturer. If the mobile devices for which we are developing games and other applications are not released when expected or do not achieve broad market penetration, our potential revenues will be limited and our business will suffer.

If our independent, third-party developers cease development of new applications for us and we are unable to find comparable replacements, our competitive position may be adversely impacted.

We rely on independent third-party developers to develop some of our game products which subjects us to the following risks:

|

| · | key developers who work for us may choose to work for or be acquired by our competitors; |

|

| · | developers currently under contract may try to renegotiate our agreements with them on terms less favorable to us; and |

|

| · | our developers may be unable or unwilling to allocate sufficient resources to complete our applications on a timely or satisfactory basis or at all. |

| 16 |

| Table of Contents |

If our developers terminate their relationships with us or negotiate agreements with terms less favorable to us, we may have to increase our internal development staff, which would be a time consuming and potentially costly process. If we are unable to increase our internal development staff in a cost-effective manner or if our current internal development staff fails to create successful applications, our earnings could be materially diminished.

In addition, although we require our third-party developers to sign agreements acknowledging that all inventions, trade secrets, works of authorship, development and other processes generated by them are our property and to assign to us any ownership they may have in those works, it may still be possible for third parties to obtain and use our intellectual properties without our consent.

Our industry is experiencing consolidation that may cause us to lose key relationships and intensify competition.

The Internet and media distribution industries are undergoing substantial change, which has resulted in increasing consolidation and formation of strategic relationships. We expect this consolidation and strategic partnering to continue. Acquisitions or other consolidating transactions could harm us in a number of ways, including:

|

| · | we could lose strategic relationships if our strategic partners are acquired by or enter into relationships with a competitor (which could cause us to lose access to distribution, content, technology and other resources); |

|

| · | we could lose customers if competitors or users of competing technologies consolidate with our current or potential customers; and |

|

| · | our current competitors could become stronger, or new competitors could form, from consolidations. |

Any of these events could put us at a competitive disadvantage, which could cause us to lose customers, revenue and market share. Consolidation could also force us to expend greater resources to meet new or additional competitive threats, which could also harm our operating results.

We rely on the continued reliable operation of third parties’ systems and networks and, if these systems and networks fail to operate or operate poorly, our business and operating results will be harmed.

Our operations are in part dependent upon the continued reliable operation of the information systems and networks of third parties. If these third parties do not provide reliable operation, our ability to service our customers will be impaired and our business, reputation and operating results could be harmed.

The Internet and our network are subject to security risks that could harm our business and reputation and expose us to litigation or liability.

Online commerce and communications depend on the ability to transmit confidential information and licensed intellectual property securely over private and public networks. Any compromise of our ability to transmit and store such information and data securely, and any costs associated with preventing or eliminating such problems, could damage our business, hurt our ability to distribute products and services and collect revenue, threaten the proprietary or confidential nature of our technology, harm our reputation, and expose us to litigation or liability. We also may be required to expend significant capital or other resources to protect against the threat of security breaches or hacker attacks or to alleviate problems caused by such breaches or attacks. Any successful attack or breach of our security could hurt consumer demand for our products and services, expose us to consumer class action lawsuits and harm our business.

| 17 |

| Table of Contents |

We may be unable to adequately protect our proprietary rights.

Our ability to compete partly depends on the superiority, uniqueness and value of our intellectual property and technology, including both internally developed technology and technology licensed from third parties. To the extent we are able to do so, in order to protect our proprietary rights, we will rely on a combination of trademark, copyright and trade secret laws, confidentiality agreements with our employees and third parties, and protective contractual provisions and licensing agreement. Despite these efforts, any of the following occurrences may reduce the value of our intellectual property:

|

| · | Our applications for trademarks and copyrights relating to our business may not be granted and, if granted, may be challenged or invalidated; |

|

| · | Issued trademarks and registered copyrights may not provide us with any competitive advantages; |

|

| · | Our efforts to protect our intellectual property rights may not be effective in preventing misappropriation of our technology; |

|

| · | Our efforts may not prevent the development and design by others of products or technologies similar to or competitive with, or superior to those we develop; |

|

| · | Another party may obtain a blocking patent and we would need to either obtain a license or design around the patent in order to continue to offer the contested feature or service in our products; or |

|

| · | We may not be able to afford to pay the costs associated with protecting our intellectual property rights. |

We may be forced to litigate to defend our intellectual property rights, or to defend against claims by third parties against us relating to intellectual property rights.

We may be forced to litigate to enforce or defend our intellectual property rights, to protect our trade secrets or to determine the validity and scope of other parties’ proprietary rights. Any such litigation could be very costly and could distract our management from focusing on operating our business. The existence and/or outcome of any such litigation could harm our business.

Interpretation of existing laws that did not originally contemplate the Internet could harm our business and operating results.

The application of existing laws governing issues such as property ownership, copyright and other intellectual property issues to the Internet is not clear. Many of these laws were adopted before the advent of the Internet and do not address the unique issues associated with the Internet and related technologies. In many cases, the relationship of these laws to the Internet has not yet been interpreted. New interpretations of existing laws may increase our costs, require us to change business practices or otherwise harm our business.

It is not yet clear how laws designed to protect children that use the Internet may be interpreted, and such laws may apply to our business in ways that may harm our business.

The Child Online Protection Act and the Child Online Privacy Protection Act impose civil and criminal penalties on persons distributing material harmful to minors (e.g., obscene material) over the Internet to persons under the age of 17, or collecting personal information from children under the age of 13. We do not knowingly distribute harmful materials to minors or collect personal information from children under the age of 13. The COPPA rules define privacy policy requirements, data collection parameters, and the process of acquiring verifiable parental consent. In the past, we have disclosed the information that we collect in Privacy Policies, but now need to focus on getting parental approval for certain types of applications as they relate to children under the age of 13. Although we have verification procedures in place to ensure we do not violate COPPA, in the event those safeguards fail, we could be subject to fines and/or lawsuits, and harm our business in other ways.

| 18 |

| Table of Contents |

We may be subject to market risk and legal liability in connection with the data collection capabilities of our products and services.

Many of our products are interactive Internet applications that by their very nature require communication between a client and server to operate. To provide better consumer experiences and to operate effectively, our products send information to our servers. Many of the services we provide also require that a user provide certain information to us. We post an extensive privacy policy concerning the collection, use and disclosure of user data involved in interactions between our client and server products.

Our planned venture into augmented reality and geolocation games could subject us to greater liability risks from our users and third parties.

As noted herein, we are currently planning to develop a number of augmented reality and geolocation games. Such games place characters on a user’s mobile device in real world surroundings and have the user interacting with the game while on the move in real life. Augmented reality games developed by some of our competitors have led users into situations that may not be ideal for the user, such as near roads, bodies of water and/or possibly on private property. Although we will use our best efforts to develop our games to minimize locations that could be dangerous for our users, there is a chance that they could wander into a dangerous situation or onto a third parties’ private property, potentially harming themselves or others. Although we will have appropriate disclaimers and disclosures on our games, any such harmful events could expose us to potential lawsuits and/or liability.

Risk Factors Relating to Future Acquisitions

We may not be able to identify, negotiate, finance or close future acquisitions.

A significant component of our growth strategy focuses on acquiring additional companies or assets. We may not, however, be able to identify, audit, or acquire companies or assets on acceptable terms, if at all. Additionally, we may need to finance all or a portion of the purchase price for an acquisition by incurring indebtedness. There can be no assurance that we will be able to obtain financing on terms that are favorable, if at all, which will limit our ability to acquire additional companies or assets in the future. Failure to acquire additional companies or assets on acceptable terms, if at all, would have a material adverse effect on our ability to increase assets, revenues and net income and on the trading price of our common Stock.

We may acquire businesses without any apparent synergies with our casual games related operations.

In an effort to diversify our sources of revenue and profits, we may decide to acquire businesses without any apparent synergies with our casual games related operations. For example, we believe that the acquisition of technologies unrelated to games and leisure may be an important way for us to enhance our stockholder value. Notwithstanding the critical importance of diversification, some members of the investment community and research analysts would prefer that micro-cap or small-cap companies restrict the scope of their activity to a single line of business, and may not be willing to make an investment in, or recommend an investment in, a micro-cap or small-cap company that undertakes multiple lines of business. This situation could materially adversely impact our company and the trading price of our stock.

We may not be able to properly manage multiple businesses.

We may not be able to properly manage multiple businesses. Managing multiple businesses would be more complicated than managing a single line of business, and would require that we hire and manage executives with experience and expertise in different fields. We can provide no assurance that we will be able to do so successfully. A failure to properly manage multiple businesses could materially adversely affect our company and the trading price of our stock.

| 19 |

| Table of Contents |

We may not be able to successfully integrate new acquisitions.

Even if we are able to acquire additional companies or assets, we may not be able to successfully integrate those companies or assets. For example, we may need to integrate widely dispersed operations with different corporate cultures, operating margins, competitive environments, computer systems, compensation schemes, business plans and growth potential requiring significant management time and attention. In addition, the successful integration of any companies we acquire will depend in large part on the retention of personnel critical to our combined business operations due to, for example, unique technical skills or management expertise. We may be unable to retain existing management, finance, engineering, sales, customer support, and operations personnel that are critical to the success of the integrated company, resulting in disruption of operations, loss of key information, expertise or know-how, unanticipated additional recruitment and training costs, and otherwise diminishing anticipated benefits of these acquisitions, including loss of revenue and profitability. Failure to successfully integrate acquired businesses could have a material adverse effect on our company and the trading price of our stock.

Our acquisitions of businesses may be extremely risky and we could lose all of our investments.

We may invest in software companies, other technology businesses, or other risky industries. An investment in these companies may be extremely risky because, among other things, the companies we are likely to focus on: (1) typically have limited operating histories, narrower product lines and smaller market shares than larger businesses, which tend to render them more vulnerable to competitors’ actions and market conditions, as well as general economic downturns; (2) tend to be privately-owned and generally have little publicly available information and, as a result, we may not learn all of the material information we need to know regarding these businesses; (3) are more likely to depend on the management talents and efforts of a small group of people; and, as a result, the death, disability, resignation or termination of one or more of these people could have an adverse impact on the operations of any business that we may acquire; (4) may have less predictable operating results; (5) may from time to time be parties to litigation; (6) may be engaged in rapidly changing businesses with products subject to a substantial risk of obsolescence; and (7) may require substantial additional capital to support their operations, finance expansion or maintain their competitive position. Our failure to make acquisitions efficiently and profitably could have a material adverse effect on our business, results of operations, financial condition and the trading price of our stock.

Future acquisitions may fail to perform as expected.

Future acquisitions may fail to perform as expected. We may overestimate cash flow, underestimate costs, or fail to understand risks. This could materially adversely affect our company and the trading price of our Stock.

Competition may result in overpaying for acquisitions.

Other investors with significant capital may compete with us for attractive investment opportunities. These competitors may include publicly traded companies, private equity firms, privately held buyers, individual investors, and other types of investors. Such competition may increase the price of acquisitions, or otherwise adversely affect the terms and conditions of acquisitions. This could materially adversely affect our company and the trading price of our stock.

We may have insufficient resources to cover our operating expenses and the expenses of raising money and consummating acquisitions.

We have limited cash to cover our operating expenses and to cover the expenses incurred in connection with money raising and a business combination. It is possible that we could incur substantial costs in connection with money raising or a business combination. If we do not have sufficient proceeds available to cover our expenses, we may be forced to obtain additional financing, either from our management or third parties. We may not be able to obtain additional financing on acceptable terms, if at all, and neither our management nor any third party is obligated to provide any financing. This could have a negative impact on our company and our stock price.

| 20 |

| Table of Contents |

The nature of our proposed future operations is speculative and will depend to a great extent on the businesses which we acquire.

While management typically intends to seek a merger or acquisition of privately held entities with established operating histories, there can be no assurance that we will be successful in locating an acquisition candidate meeting such criteria. In the event we complete a merger or acquisition transaction, of which there can be no assurance, our success if any will be dependent upon the operations, financial condition and management of the acquired company, and upon numerous other factors beyond our control. If the operations, financial condition or management of the acquired company were to be disrupted or otherwise negatively impacted following an acquisition, our company and our stock price would be negatively impacted.

We may make actions that will not require our stockholders’ approval.

The terms and conditions of any acquisition could require us to take actions that would not require stockholder approval. In order to acquire certain companies or assets, we may issue additional shares of common or preferred stock, borrow money or issue debt instruments including debt convertible into capital stock. Not all of these actions would require our stockholders’ approval even if these actions dilute our shareholders’ economic or voting interest.

Our investigation of potential acquisitions will be limited.

Our analysis of new business opportunities will be undertaken by or under the supervision of our executive officers and directors. Inasmuch as we will have limited funds available to search for business opportunities and ventures, we will not be able to expend significant funds on a complete and exhaustive investigation of such business or opportunity. We will, however, investigate, to the extent believed reasonable by our management, such potential business opportunities or ventures by conducting a so-called “due diligence investigation.” In a so-called “due diligence investigation,” we intend to obtain and review materials regarding the business opportunity. Typically such materials will include information regarding a target business’ products, services, contracts, management, ownership, and financial information. In addition, we intend to cause our officers or agents to meet personally with management and key personnel of target businesses, ask questions regarding the company’s prospects, tour facilities, and conduct other reasonable investigation of the target business to the extent of our limited financial resources and management and technical expertise. Any failure of our typical “due diligence investigation” to uncover issues and problems relating to potential acquisition candidates could materially adversely affect our company and the trading price of our stock.

We will have only a limited ability to evaluate the directors and management of potential acquisitions.

We may make a determination that our current directors and officers should not remain, or should reduce their roles, following money raising or a business combination, based on an assessment of the experience and skill sets of new directors and officers and the management of target businesses. We cannot assure you that our assessment of these individuals will prove to be correct. This could have a negative impact on our company and our stock price.

We will be dependent on outside advisors to assist us.

In order to supplement the business experience of management, we may employ accountants, technical experts, appraisers, attorneys or other consultants or advisors. The selection of any such advisors will be made by management and without any control from shareholders. Additionally, it is anticipated that such persons may be engaged by us on an independent basis without a continuing fiduciary or other obligation to us.

| 21 |

| Table of Contents |

We may be unable to protect or enforce the intellectual property rights of any target business that we acquire or the target business may become subject to claims of intellectual property infringement.