UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2019

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________ to ___________

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report _________________________

Commission file number: 001-34661

LIANLUO SMART LIMITED

(Exact Name of Registrant as Specified in Its Charter)

Not Applicable

(Translation of Registrant’s Name Into English)

British Virgin Islands

(Jurisdiction of Incorporation or Organization)

Room 611, 6th Floor, BeiKong Technology Building

No. 10 Baifuquan Road, Changping District

Beijing 102200, People’s Republic of China

(Address of Principal Executive Offices)

Mr. Zhitao He, Chief Executive Officer

Room 611, 6th Floor, BeiKong Technology Building

No. 10 Baifuquan Road, Changping District

Beijing 102200, People’s

Republic of China

Tel: +86-10-89788107

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange On Which Registered | ||

| Class A Common Shares, par value $0.002731 per share | LLIT | NASDAQ Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report (December 31, 2019): There were 17,806,586 shares of the registrant’s Common Shares outstanding, including 6,695,475 Class A Common Shares, par value $0.002731 per share and 11,111,111 Class B Common Shares, par value $0.002731 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ☐ | Accelerated Filer ☐ | Non-Accelerated Filer ☒ | Emerging growth company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Annual Report on Form 20-F

Year Ended December 31, 2019

TABLE OF CONTENTS

i

ii

EXPLANATORY NOTE

As previously disclosed on Lianluo Smart Limited’s (the “Company”) Form 6-K furnished on April 28, 2020, the filing of this annual report on Form 20-F for the period ended December 31, 2019 was delayed due to circumstances related to COVID-19 and its impact on the Company’s operations. Substantially all of the Company’s operating subsidiaries, employees and facilities are located in China which has been affected by the outbreak of COVID-19 since early 2020. During the first quarter of 2020, COVID-19 caused businesses and government agencies throughout China to suspend operations or operate with reduced workforce in shifts for limited periods of time. The COVID-19 pandemic has caused disruptions in the Company’s daily activities and impaired the Company’s ability to file the annual report by the original deadline of April 30, 2020. The Company relied on the SEC’s Order Under Section 36 of the Securities Exchange Act of 1934 Modifying Exemptions from the Reporting and Proxy Delivery Requirements for Public Companies, dated March 25, 2020 (Release No. 34-88465), to delay the filing of this annual report.

INTRODUCTORY NOTES

Use of Certain Defined Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to:

| ● | “LLIT,” “we,” “us,” “our” and the “Company” are to the combined business of Lianluo Smart Limited and its subsidiaries; |

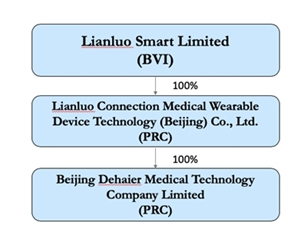

| ● | “Lianluo Smart” are to Lianluo Smart Limited, a BVI company; |

| ● | “Lianluo Connection” are to Lianluo Connection Medical Wearable Device Technology (Beijing) Co., Ltd., a PRC company; |

| ● | “Beijing Dehaier” are to Beijing Dehaier Medical Technology Company Limited, a PRC company; |

| ● | “Hangzhou Lianluo” are to Hangzhou Lianluo Interactive Information Technology Co., Ltd.; |

| ● | “BTL” are to Beijing Dehaier Technology Company Limited, a PRC company; |

| ● | “BVI” are to the British Virgin Islands; |

| ● | “Hong Kong” are to the Hong Kong Special Administrative Region of the People’s Republic of China; |

| ● | “PRC” and “China” are to the People’s Republic of China; |

| ● | “SEC” are to the Securities and Exchange Commission; |

| ● | “Exchange Act” are to the Securities Exchange Act of 1934, as amended; |

| ● | “Securities Act” are to the Securities Act of 1933, as amended; |

| ● | “Renminbi” and “RMB” are to the legal currency of China; and |

| ● | “U.S. dollars,” “dollars” and “$” are to the legal currency of the United States. |

Forward-Looking Information

In addition to historical information, this annual report contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. We use words such as “believe,” “expect,” “anticipate,” “project,” “target,” “plan,” “optimistic,” “intend,” “aim,” “will” or similar expressions which are intended to identify forward-looking statements. Such statements include, among others, those concerning market and industry segment growth and demand and acceptance of new and existing products; any projections of sales, earnings, revenue, margins or other financial items; any statements of the plans, strategies and objectives of management for future operations; and any statements regarding future economic conditions or performance, as well as all assumptions, expectations, predictions, intentions or beliefs about future events. You are cautioned that any such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, as well as assumptions, which, if they were to ever materialize or prove incorrect, could cause the results of the Company to differ materially from those expressed or implied by such forward-looking statements. Potential risks and uncertainties include, among other things, the possibility that third parties hold proprietary rights that preclude us from marketing our products, the emergence of additional competing technologies, changes in domestic and foreign laws, regulations and taxes, changes in economic conditions, uncertainties related to legal system and economic, political and social events in China, a general economic downturn, a downturn in the securities markets, and other risks and uncertainties which are generally set forth under Item 3 “Key information—D. Risk Factors” and elsewhere in this annual report.

Readers are urged to carefully review and consider the various disclosures made by us in this report and our other filings with the SEC. These reports attempt to advise interested parties of the risks and factors that may affect our business, financial condition and results of operations and prospects. The forward-looking statements made in this report speak only as of the date hereof and we disclaim any obligation, except as required by law, to provide updates, revisions or amendments to any forward-looking statements to reflect changes in our expectations or future events.

iii

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

The following table presents selected financial data regarding our business. It should be read in conjunction with our consolidated financial statements and related notes contained elsewhere in this annual report and the information under Item 5 “Operating and Financial Review and Prospects.” The selected consolidated statement of income (loss) data for the fiscal years ended December 31, 2019, 2018, and 2017, and the selected consolidated balance sheet data as of December 31, 2019 and 2018 have been derived from our audited consolidated financial statements that are included in this annual report beginning on page F-1. The selected consolidated statement of income (loss) data for the fiscal years ended December 31, 2016 and 2015, and the selected consolidated balance sheet data as of December 31, 2017, 2016 and 2015 have been derived from our audited consolidated financial statements that are not included in this annual report.

Our consolidated financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States, or U.S. GAAP. The selected financial data information is only a summary and should be read in conjunction with the historical consolidated financial statements and related notes contained elsewhere herein. The financial statements contained elsewhere fully represent our financial condition and operations; however, they are not indicative of our future performance.

| For the Years Ended December 31, | ||||||||||||||||||||

| 2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| Revenues | $ | 383,458 | $ | 559,386 | $ | 882,011 | $ | 13,062,373 | $ | 738,301 | ||||||||||

| Costs of revenue | (743,744 | ) | (757,901 | ) | (1,655,970 | ) | (17,179,060 | ) | (1,094,124 | ) | ||||||||||

| Gross loss | (360,286 | ) | (198,515 | ) | (773,959 | ) | (4,116,687 | ) | (355,823 | ) | ||||||||||

| Service income | - | - | 56,030 | 14,587 | 1,600,012 | |||||||||||||||

| Service expenses | - | - | (1,289 | ) | (21,130 | ) | (1,234,257 | ) | ||||||||||||

| Selling expenses | (835,270 | ) | (2,082,829 | ) | (1,170,378 | ) | (927,243 | ) | (2,815,609 | ) | ||||||||||

| General and administrative expenses | (2,593,808 | ) | (3,675,465 | ) | (3,192,030 | ) | (4,183,775 | ) | (4,089,592 | ) | ||||||||||

| (Provision for) recovery from doubtful accounts | (13,011 | ) | (22,229 | ) | 23,608 | 150,280 | (8,544 | ) | ||||||||||||

| Impairment loss for intangible assets | - | (3,281,779 | ) | - | - | - | ||||||||||||||

| Operating loss | (3,802,375 | ) | (9,260,817 | ) | (5,058,018 | ) | (9,083,968 | ) | (6,903,813 | ) | ||||||||||

| Loss before provision for income tax and non-controlling interest | (4,450,994 | ) | (8,910,002 | ) | (5,136,434 | ) | (9,704,761 | ) | (6,710,848 | ) | ||||||||||

| Income tax benefit | - | - | - | 95,026 | 11,978 | |||||||||||||||

| Net loss from continuing operations | (4,450,994 | ) | (8,910,002 | ) | (5,136,434 | ) | (9,609,735 | ) | (6,698,870 | ) | ||||||||||

| Discontinued operations: | ||||||||||||||||||||

| Loss from operations of discontinued operations, net of taxes | - | - | - | (168,574 | ) | (3,663,465 | ) | |||||||||||||

| Loss from disposal of discontinued operations, net of taxes | - | - | - | (82,579 | ) | - | ||||||||||||||

| Net loss | (4,450,994 | ) | (8,910,002 | ) | (5,136,434 | ) | (9,860,888 | ) | (10,362,335 | ) | ||||||||||

| Less: net loss attributable to non-controlling interest | - | - | - | (129,020 | ) | (139,205 | ) | |||||||||||||

| Net loss attributable to Lianluo Smart Limited | $ | (4,450,994 | ) | $ | (8,910,002 | ) | $ | (5,136,434 | ) | $ | (9,731,868 | ) | $ | (10,223,130 | ) | |||||

| Other comprehensive (loss) income: | ||||||||||||||||||||

| Foreign currency translation (loss) gain | (166,892 | ) | (515,477 | ) | 380,077 | (567,162 | ) | (461,548 | ) | |||||||||||

| Comprehensive loss | (4,617,886 | ) | (9,425,479 | ) | (4,756,357 | ) | (10,428,050 | ) | (10,823,883 | ) | ||||||||||

| -less comprehensive loss attributable to non-controlling interest | - | - | - | (230,838 | ) | (189,670 | ) | |||||||||||||

| Comprehensive loss attributable to Lianluo Smart Limited | $ | (4,617,886 | ) | $ | (9,425,479 | ) | $ | (4,756,357 | ) | $ | (10,197,212 | ) | $ | (10,634,213 | ) | |||||

| Weighted average number of common shares used in computation | ||||||||||||||||||||

| -Basic and Diluted | 17,806,586 | 17,617,416 | 17,312,586 | 10,422,765 | 5,990,552 | |||||||||||||||

| Net loss per share of common stock | ||||||||||||||||||||

| -Basic and Diluted | $ | (0.25 | ) | $ | (0.51 | ) | $ | (0.30 | ) | $ | (0.93 | ) | $ | (1.71 | ) | |||||

1

| December 31, | ||||||||||||||||||||

| 2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 22,834 | $ | 477,309 | $ | 6,809,485 | $ | 10,792,823 | $ | 615,517 | ||||||||||

| Working (deficiency) capital | (1,555,999 | ) | 1,260,558 | 7,152,147 | 10,221,074 | 462,687 | ||||||||||||||

| Total current assets | 1,677,113 | 2,713,362 | 9,833,029 | 11,336,148 | 6,868,333 | |||||||||||||||

| Total assets | 2,333,953 | 5,698,670 | 15,563,108 | 16,552,137 | 13,875,247 | |||||||||||||||

| Total current liabilities | 3,233,112 | 1,452,804 | 2,680,882 | 1,115,074 | 6,405,646 | |||||||||||||||

| Non-controlling interest | - | - | - | - | 867,826 | |||||||||||||||

| Total Lianluo Smart Limited shareholders’ (deficit) equity | (1,288,789 | ) | 3,116,620 | 11,153,115 | 13,937,701 | 6,439,039 | ||||||||||||||

| Common shares | 48,630 | 48,630 | 47,281 | 47,281 | 16,918 | |||||||||||||||

| Total (deficit) equity | (1,288,789 | ) | 3,116,620 | 11,153,115 | 13,937,701 | 7,306,865 | ||||||||||||||

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

An investment in our capital stock involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this annual report, before making an investment decision. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, the trading price of our Class A Common Shares could decline, and you may lose all or part of your investment.

2

Risks Relating to Our Business

The outbreak of the coronavirus may have a material adverse effect on our business and the trading price of our Class A Common Shares.

Our business has been adversely affected by the outbreak of coronavirus. The World Health Organization labelled the coronavirus outbreak a pandemic on March 11, 2020, after the disease spread globally. Given the high public health risks associated with the disease, governments around the world have imposed various degrees of travel and gathering restrictions and other quarantine measures. Businesses in China have scaled back or suspended operations since the outbreak in December 2019. The coronavirus outbreak is currently having an indeterminable adverse impact on the global economy.

All of our operating subsidiaries are located in China. Substantially all of our employees and all of our customers and suppliers are located in China. From January to February 2020, our service revenue plunged, as the number of patient users decreased sharply; and our revenue from the sale of products also dropped, because our distributors and sales personnel were trapped at home and our contract manufacturers shut down production during this period. Constrained by the epidemic, management and employees have been working from home to mitigate the impacts of operation disruptions caused by the coronavirus. As of the date of this annual report, we have resumed operations but at below normal levels. Medical check-up centers and hospitals in China that we have business relationships with have partially resumed operations since March 2020, including the medical check-up centers in Wuhan that focus on physical examinations. In addition, while our supply chains currently are not affected, it is unknown whether or how they may be affected if the pandemic persists for an extended period. We estimate that the coronavirus has made a material adverse impact on our operating results for the first quarter of 2020 and may adversely impact our revenue and results of operations for the fiscal year ending December 31, 2020.

In addition, fears of the economic impacts of the coronavirus have sparked share prices to fluctuate significantly recently. The volatility of share prices and across-the-market selloff may depress our share price, and moreover, adversely affect our ability to obtain equity or debt financings from the financial market.

Given the uncertainty of the outbreak, the spread of the coronavirus may be prolonged and worsened, and we may be forced to further scale back or even suspend our operations. As the coronavirus epidemic spreads outside China, the global economy is suffering a noticeable slowdown. If this outbreak persists, commercial activities throughout the world could be curtailed with decreased consumer spending, business operation disruptions, interrupted supply chain, difficulties in travel, and reduced workforces. The duration and intensity of disruptions resulting from the coronavirus outbreak is uncertain. It is unclear as to when the outbreak will be contained, and we also cannot predict if the impact will be short-lived or long-lasting. The extent to which the coronavirus impacts our financial results will depend on its future developments. If the outbreak of the coronavirus is not effectively controlled in a short period of time, our business operation and financial condition may be materially and adversely affected as a result of any slowdown in economic growth, operation disruptions or other factors that we cannot predict.

Our business is seasonal and revenues and operating results could fall below investor expectations during certain periods, which could cause the trading price of our Class A Common Shares to decline.

Our revenues and operating results have fluctuated in the past and may continue to fluctuate significantly depending upon numerous factors. In particular, we generally experience an increase in revenues in the period from March through May, and September through December. The increase in the fourth quarter is associated with hospital purchasing designed to extinguish governmental budgets prior to the fiscal year end. We believe that our first quarter performance will generally decline as a result of the lack of business conducted during the Chinese Lunar New Year holiday. To the extent our financial performance fluctuates significantly, investors may lose confidence in our business and the price of our Class A Common Shares could decrease.

We may fail to effectively develop and commercialize new products and services, which could materially and adversely affect our business, financial condition, results of operations and prospects.

The sleep respiratory market is developing rapidly, and related technology trends are constantly evolving. This results in the frequent introduction of new products and services, short product life cycles and significant price competition. Consequently, our future success depends on our ability to anticipate technology development trends and identify, develop and commercialize in a timely and cost-effective manner the new and advanced products that our customers demand. Moreover, it may take an extended period of time for our new products to gain market acceptance, if at all. Furthermore, as the life cycle for a product matures, the average selling price generally decreases. In the future, we may be unable to offset the effect of declining average sales prices through increased sales volume and controlling product costs. Lastly, during a product’s life cycle, problems may arise regarding regulatory, intellectual property, product liability or other issues that may affect the product’s continued commercial viability.

3

New sleep respiratory disorder related technology and relevant regulation could materially affect provision of our Obstructive Sleep Apnea Syndrome (“OSAS”) service to hospitals and medical centers. Development of our OSAS service business depends on our ability to decrease OSAS service-related device production cost and the relationship with hospital and medical center. It may take an extended period of time for us to decrease the cost of our new devices and to market our new devices. We may be unable to provide service to sufficient hospitals and medical centers, which could adversely affect our financial condition and results of operations and prospects.

We sell our products primarily to distributors, and our technical services are provided to hospitals and check-up centers; our ability to add distributors, hospitals and check-up centers will impact our revenue growth. Failure to maintain or expand our distribution network and network of hospitals and check-up centers would materially and adversely affect our business.

We depend on sales to distributors for a significant majority of our product revenues. Our distributors purchase all products ordered regardless of whether the products are ultimately sold. Products are not purchased by distributors on consignment, and distributors have no right to return unsold products. As our existing distributor agreements expire, we may be unable to renew such agreements on favorable terms or at all, and we do not own, employ or control these independent distributors. Furthermore, we actively manage our distribution network and regularly review the performance of each distributor. We may terminate agreements with distributors, without penalty, if we are not satisfied with their performance for any reason. We periodically terminate relationships with underperforming exclusive distributors. Our distributors may also terminate their relationship with us without penalty. When an exclusive distributor in a particular geographic area fails to meet our expectations, then we are economically incentivized to replace that distributor with a new distributor so that area can be served as well as possible. We occasionally terminate a relationship with a non-exclusive distributor and are more likely to simply appoint another one; however, we have found that in some instances we are better served to replace an underperforming non-exclusive distributor with an exclusive distributor. Additionally, we have found that even in cases where there may not be an economic incentive to terminate a non-exclusive distributor, having the ability to replace a distributor often motivates distributors to increase their efforts to meet our expectations. This policy may make us less attractive to some distributors. In addition, we compete for distributors with other medical device companies who may enter into long-term distribution agreements, effectively preventing many distributors from selling our products. As a result, a significant amount of time and resources must be devoted to maintaining and growing our distribution network.

In the OSAS sector, starting from fiscal 2018 we provide technical services in relation to detection and analysis of OSAS. We focused on the promotion of sleep respiratory solutions and service in public hospitals. Our wearable sleep diagnostic products and cloud-based services are also available in the medical centers of private preventive healthcare companies. We sign service agreements with public hospitals usually for a period of 1 to 3 years, and check-up centers usually for a period of one year or less, with the aim of provision of wearable sleep diagnostic products and cloud-based services and we charge a fixed technical service fee on a per user basis when our OSAS diagnostic services are provided to the user at medical centers and public hospitals. Our service revenue is dependent on the number of OSAS tests performed by each hospital/check-up center. The provision of these OSAS diagnosis services is still in its early stage and we may be required to invest more marketing efforts in order to build up and consolidate our partnership with hospitals and physical examination centers in China. We may terminate relationships with underperforming hospital/check-up center. The hospital/check-up may also terminate their relationship with us without penalty, and they may not renew their service agreement with us upon expiration.

Impacted by the COVID-19, from January to February 2020, our service revenue plunged, as the number of patient users decreased sharply; and our revenue from the sale of products also dropped, because our distributors and sales personnel were trapped at home and our contract manufacturers shut down production during this period. As of the date of this annual report, we have resumed operations but at below normal levels. Medical check-up centers and hospitals in China that we have business relationships with have partially resumed operations since March 2020, including the medical check-up centers in Wuhan that focus on physical examinations. As a result, we estimate that the coronavirus has made a material adverse impact on our operating results for the first quarter of 2020. Any disruption in our distribution network and network of hospitals and check-up centers could have negative effects on our ability to market our products and services, which would in turn materially and adversely affect our business, financial condition and results of operations.

4

Although we do not own or control our distributors, the actions of these distributors may affect our business operations or our reputation in the marketplace.

Our distributors are independent from us, and as such, our ability to effectively manage their activities is limited. Distributors could take any number of actions that could have material adverse effects on our business. If we fail to adequately manage our distribution network or if distributors do not comply with our distribution agreements, our corporate image could be tarnished among end users, disrupting our sales. Furthermore, we could be liable for actions taken by our distributors, including any violations of applicable law in connection with the marketing or sale of our products, including China’s anti-corruption laws. The PRC government has increased its anti-bribery efforts in the healthcare sector in recent years to reduce improper payments received by hospital administrators and doctors in connection with the purchase of pharmaceutical products and medical devices. Our distributors may violate these laws or otherwise engage in illegal practices with respect to their sales or marketing of our products. If our distributors violate these laws, we could be required to pay damages or fines, which could materially and adversely affect our financial condition and results of operations. In addition, our brand and reputation, our sales activities or the price of our shares could be adversely affected if our company becomes the target of any negative publicity as a result of actions taken by our distributors.

We are highly dependent on our key personnel such as key executives.

We are highly dependent on the continued service of our key executives, including our chief executive officer, Mr. Zhitao He, and other key personnel such as Mr. Ping Chen, our founder and former chief executive officer. We have entered into standard three-year employment contracts, or where required by law, open-term employment contracts, with all of our officers and managers and other key personnel, and three-year employment contracts, or where required by law, open-term employment contracts with our other employees. These contracts prohibit our employees from engaging in any conduct or activity that would be competitive with our business during the term of their employment. Loss of any of our key personnel could severely disrupt our business. We may not be able to find suitable or qualified replacements and will likely incur additional expenses in order to recruit and train any new personnel.

In 2019, our PRC subsidiaries, namely Lianluo Connection and Beijing Dehaier, laid off a total of over fifty employees, due to a business downturn and the need of business restructuring. Notwithstanding, our future success depends on our ability to attract and retain skilled personnel and failure to do so could result in disruptions to our business and growth.

Our business is subject to intense competition, which may reduce demand for our products and materially and adversely affect our business, financial condition, results of operations and prospects.

The medical device and health wearables markets are highly competitive, and we expect competition to intensify. Given the huge stimulus initiative in China and its impact on healthcare, we expect the availability of healthcare to increase, as more hospitals and clinics are developed rurally.

We face direct competition from both domestic and international competitors across all product lines and price points. Our competitors also vary by product. Currently, in China our competitors include publicly traded and privately held multinational companies. As we expand into international markets, we expect that our competitors will primarily be publicly traded and privately held multinational companies. We also expect to face competition in international sales from companies that have local operations in the markets in which we sell our products. Some of our larger competitors may have:

| ● | greater financial and other resources; |

| ● | larger variety of products; |

| ● | more products that have received regulatory approvals; |

| ● | greater pricing flexibility; |

| ● | more extensive research and development and technical capabilities; |

| ● | patent portfolios that may present an obstacle to our conduct of business; |

| ● | greater knowledge of local market conditions where we seek to make our international sales; |

| ● | stronger brand recognition; and |

| ● | larger sales and distribution networks. |

5

As a result, we may be unable to offer products similar to, or more desirable than, those offered by our competitors, market our products as effectively as our competitors or otherwise respond successfully to competitive pressures. In addition, our competitors may be able to offer discounts on competing products as part of a “bundle” of non-competing products, systems and services that they sell to our customers, and we may not be able to profitably match those discounts. Our competitors may develop technologies and products that are more effective than those we currently offer or that render our products obsolete or uncompetitive. The timing of the introduction of competing products into the market could affect the market acceptance and market share of our products. As we expect demand for our products to increase along with the availability of healthcare, we must continue to focus on competitive pricing and innovation by being at the forefront of market trends and improving our product and service offerings. Our failure to compete successfully could materially and adversely affect our business, financial condition, results of operations and prospects.

Some of our internationally based competitors may establish production or research and development facilities in China, while others may enter into cooperative business arrangements with Chinese manufacturers. If we are unable to develop competitive branded products, obtain regulatory approval or clearance and supply sufficient quantities to the market as quickly and effectively as our competitors, market acceptance of our branded products may be limited, which could result in decreased sales. In addition, we may not be able to maintain our branded products’ cost advantages.

We believe that corrupt practices in the medical device industry in China still occur. To increase sales, certain manufacturers or distributors of medical devices may pay kickbacks or provide other benefits to hospital personnel who make procurement decisions. Our company policy prohibits these practices by our direct sales personnel and our distribution agreements require our distributors to comply with applicable law. As competition intensifies in the medical device industry in China, we may lose sales, customers or contracts to competitors.

If we fail to accurately project demand for our products, we may encounter problems of inadequate supply or oversupply, which would materially and adversely affect our financial condition and results of operations, as well as damage our reputation and brand.

Our distributors typically order our products on a purchase order basis. We project demand for our products based on rolling projections from our distributors, our understanding of anticipated hospital procurement spending, and distributor inventory levels. The varying sales and purchasing cycles of our distributors and other customers, however, makes it difficult for us to forecast future demand accurately.

If we overestimate demand, we may purchase more unassembled parts or components for our branded products than we require. If we underestimate demand, our third-party suppliers may have inadequate supply of parts or product component inventories, which would delay shipments of our branded products, and could result in lost sales. In particular, we are seeking to reduce our procurement and inventory costs by matching our inventory closely with our projected product needs and by, from time to time, deferring our purchase of components in anticipation of supplier price reductions. As we seek to balance reduced inventory costs, we may fail to accurately forecast demand and coordinate our procurement to meet demand on a timely basis. Our inability to accurately predict our demand and to timely meet our demand could materially and adversely affect our financial conditions and results of operations as well as damage our reputation and corporate brand.

Failure to effectively restructure our business could materially and adversely affect our business and prospects.

We experienced a business downturn in 2019 and terminated over fifty employees’ employment. Currently, we are making efforts to overcome such downturn by restructuring our business. Our business restructuring strategy includes strengthening our brand, increasing market penetration of our existing products, developing new products, increasing our targeting of the sleep respiratory market in China, and embarking on exports. Pursuing these strategies requires, among other things:

| ● | continued enhancement of our research and development capabilities; |

| ● | information technology system enhancement; |

| ● | stringent cost controls and sufficient liquidity; |

| ● | strengthening of financial and management controls and information technology systems; and |

| ● | increased marketing, sales and support activities. |

6

If we are not able to restructure our business successfully, we may not be able to overcome our business downturn, and our prospects would be materially and adversely affected.

If we fail to obtain or maintain applicable regulatory clearances or approvals for our products, or if such clearances or approvals are delayed, we will be unable to commercially distribute and market our products at all or in a timely manner, which could significantly disrupt our business and materially and adversely affect our sales and profitability.

The sale and marketing of our products are subject to regulation in China. For a significant portion of our sales, we need to obtain and renew licenses and registrations with the China Food and Drug Administration (CFDA). The processes for obtaining regulatory clearances or approvals can be lengthy and expensive, and the results are unpredictable. In addition, the relevant regulatory authorities may introduce additional requirements or procedures that have the effect of delaying or prolonging the regulatory clearance or approval for our existing or new products. If we are unable to obtain clearances or approvals needed to market existing or new branded products, or obtain such clearances or approvals in a timely fashion, our business would be significantly disrupted, and our sales and profitability could be materially and adversely affected.

We generate a significant portion of our revenues from a small number of products, and a reduction in demand for any of these products could materially and adversely affect our financial condition and results of operations.

We derive a substantial percentage of our revenues from a small number of products. We expect that a small number of our key products will continue to account for a significant portion of our net revenues for the foreseeable future. As a result, continued market acceptance and popularity of these products is critical to our success, and a reduction in demand due to, among other factors, the introduction of competing products by our competitors, the entry of new competitors, or end-users’ dissatisfaction with the quality of these products could materially and adversely affect our financial condition and results of operations.

If we fail to protect our intellectual property rights, it could harm our business and competitive position.

We rely on a combination of patent, copyright, trademark and trade secret laws and non-disclosure agreements and other methods to protect our intellectual property rights. The process of seeking patent protection can be lengthy and expensive, our patent applications may fail to result in patents being issued, and our existing and future patents may be insufficient to provide us with meaningful protection or commercial advantage. Our patents and patent applications may also be challenged, invalidated or circumvented.

We also rely on trade secret rights to protect our business through non-disclosure provisions in employment agreements with employees. If our employees breach their non-disclosure obligations, we may not have adequate remedies in China, and our trade secrets may become known to our competitors.

Intellectual property rights and confidentiality protections in China may not be as effective as in the United States or other western countries. Furthermore, policing unauthorized use of proprietary technology is difficult and expensive, and we may need to resort to litigation to enforce or defend patents issued to us or to determine the enforceability, scope and validity of our proprietary rights or those of others. Such litigation and an adverse determination in any such litigation, if any, could result in substantial costs and diversion of resources and management attention, which could harm our business and competitive position.

We may be exposed to intellectual property infringement and other claims by third parties which, if successful, could disrupt our business and have a material adverse effect on our financial condition and results of operations.

Our success depends, in large part, on our ability to use and develop our technology and know-how without infringing third party intellectual property rights. If we sell our branded products internationally, and as litigation becomes more common in China, we face a higher risk of being the subject of claims for intellectual property infringement, invalidity or indemnification relating to other parties’ proprietary rights. Our current or potential competitors, many of which have substantial resources and have made substantial investments in competing technologies, may have or may obtain patents that will prevent, limit or interfere with our ability to make, use or sell our branded products in either China or other countries, including the United States and other countries in Asia. The validity and scope of claims relating to medical device technology patents involve complex scientific, legal and factual questions and analysis and, as a result, may be highly uncertain. In addition, the defense of intellectual property suits, including patent infringement suits, and related legal and administrative proceedings can be both costly and time consuming and may significantly divert the efforts and resources of our technical and management

personnel. Furthermore, an adverse determination in any such litigation or proceedings to which we may become a party could cause us to:

| ● | pay damage awards; |

7

| ● | seek licenses from third parties; |

| ● | pay ongoing royalties; |

| ● | redesign our branded products; or |

| ● | be restricted by injunctions. |

Each of the foregoing could effectively prevent us from pursuing some or all of our business and result in our customers or potential customers deferring or limiting their purchase or use of our branded products, which could have a material adverse effect on our financial condition and results of operations.

We are subject to product liability exposure and currently do not have insurance coverage for product-related liabilities. Any product liability claims or potential safety-related regulatory actions could damage our reputation and materially and adversely affect our business, financial condition and results of operations.

The medical devices we assemble and sell can expose us to potential product liability claims if the use of these products causes or is alleged to have caused personal injuries or other adverse effects. Any product liability claim or regulatory action could be costly and time-consuming to defend. If successful, product liability claims may require us to pay substantial damages. We do not maintain product liability insurance to cover potential product liability arising from the use of our branded products because product liability insurance available in China offers only limited coverage compared to coverage offered in many other countries. As we expand our sales internationally and increase our exposure to these risks in many countries, we may be unable to obtain sufficient product liability insurance coverage on commercially reasonable terms, or at all. A product liability claim or potential safety-related regulatory action, with or without merit, could result in significant negative publicity and could materially and adversely affect the marketability of our branded products and our reputation, as well as our business, financial condition and results of operations.

Moreover, a material design, manufacturing or quality failure or defect in our branded products, other safety issues or heightened regulatory scrutiny could each warrant a product recall by us and result in increased product liability claims. Also, if these products are deemed by the authorities in China where we currently sell our branded products to fail to conform to product quality and safety requirements, we could be subject to regulatory action. In China, violation of PRC product quality and safety requirements may subject us to confiscation of related earnings, penalties, an order to cease sales of the violating product, or to cease operations pending rectification. Furthermore, if the violation is determined to be serious, our business license to assemble or sell violating and other products could be suspended or revoked.

We may undertake acquisitions, which may have a material adverse effect on our ability to manage our business, and may end up being unsuccessful.

Our growth strategy may involve the acquisition of new technologies, businesses, products or services or the creation of strategic alliances in areas in which we do not currently operate. We do not have any commitment or agreement in place with regard to any such acquisitions at this time. These acquisitions could require that our management develop expertise in new areas, manage new business relationships and attract new types of customers. Furthermore, acquisitions may require significant attention from our management, and the diversion of our management’s attention and resources could have a material adverse effect on our ability to manage our business. We may also experience difficulties integrating acquisitions into our business and operations. Future acquisitions may also expose us to potential risks, including risks associated with:

| ● | the integration of new operations, services and personnel; |

| ● | unforeseen or hidden liabilities; |

| ● | the diversion of resources from our existing businesses and technologies; |

8

| ● | our inability to generate sufficient revenue to offset the costs of acquisitions; and |

| ● | potential loss of, or harm to, relationships with employees or customers, any of which could significantly disrupt our ability to manage our business and materially and adversely affect our business, financial condition and results of operations. |

We may need additional capital in the future, and we may be unable to obtain such capital in a timely manner or on acceptable terms, if at all.

In order for us to grow, remain competitive, develop new products, and expand our distribution network, we may require additional capital in the future. Our ability to obtain additional capital in the future is subject to a variety of uncertainties, including:

| ● | our future financial condition, results of operations and cash flows; |

| ● | general market conditions for capital raising activities by medical device manufacturers and other related companies; and |

| ● | economic, political and other conditions in China and elsewhere. |

We may be unable to obtain additional capital in a timely manner or on acceptable terms or at all. Furthermore, the terms and amount of any additional capital raised through issuances of equity securities may result in significant shareholder dilution.

If we experience a significant number of warranty claims, our costs could substantially increase and our reputation and brand could suffer.

We typically sell our branded products with standard warranty terms covering 12 months after purchase. Our branded product warranty requires us to repair all mechanical malfunctions and, if necessary, replace defective components. We accrue liability for potential warranty claims at the time of sale. If we experience an increase in warranty claims or if our repair and replacement costs associated with warranty claims increase significantly, we may have to accrue a greater liability for potential warranty claims. Moreover, an increase in the frequency of warranty claims could substantially increase our costs and harm our reputation and brand. Our business, financial condition, results of operations and prospects may suffer materially if we experience a significant increase in warranty claims on our branded products.

If our security measures are breached or fail, and unauthorized access to a client’s data is obtained, our services may be perceived as not being secure, clients may curtail or stop using our services, and we may incur significant liabilities.

Our products and services involve the web-based storage and transmission of clients’ proprietary information and protected health information of patients. Because of the sensitivity of this information, security features of our software are very important. From time to time we may detect vulnerabilities in our systems, which, even if they do not result in a security breach, may reduce customer confidence and require substantial resources to address. If our security measures are breached or fail as a result of third-party action, employee error, malfeasance, insufficiency, defective design, or otherwise, someone may be able to obtain unauthorized access to client or patient data. As a result, our reputation could be damaged, our business may suffer, and we could face damages for contract breach, penalties for violation of applicable laws or regulations, and significant costs for remediation and efforts to prevent future occurrences. We rely upon our clients as users of our system for key activities to promote security of the system and the data within it, such as administration of client-side access credentialing and control of client-side display of data. On occasion, our clients have failed to perform these activities. Failure of clients to perform these activities may result in claims against us that this reliance was misplaced, which could expose us to significant expense and harm to our reputation. Because techniques used to obtain unauthorized access or to sabotage systems change frequently and generally are not recognized until launched against a target, we may be unable to anticipate these techniques or to implement adequate preventive measures. If an actual or perceived breach of our security occurs, the market perception of the effectiveness of our security measures could be harmed and we could lose sales and clients. In addition, our clients may authorize or enable third parties to access their client data or the data of their patients on our systems. Because we do not control such access, we cannot ensure the complete propriety of that access or integrity or security of such data in our systems.

9

If our services fail to provide accurate and timely information, or if our content or any other element of any of our services is associated with faulty clinical decisions or treatment, we could have liability to clients, clinicians, or patients, which could adversely affect our results of operations.

Our products, software, content, and services are used to assist clinical decision-making and provide information about treatment plans. If our products, software, content, or services fail to provide accurate and timely information or are associated with faulty clinical decisions or treatment, then clients, clinicians, or their patients could assert claims against us that could result in substantial costs to us, harm our reputation in the industry, and cause demand for our services to decline.

The assertion of such claims and ensuing litigation, regardless of its outcome, could result in substantial cost to us, divert management’s attention from operations, damage our reputation, and decrease market acceptance of our products and services. We attempt to limit by contract our liability for damages and to require that our clients assume responsibility for medical care and approve key system rules, protocols, and data. Despite these precautions, the allocations of responsibility and limitations of liability set forth in our contracts may not be enforceable, be binding upon patients, or otherwise protect us from liability for damages.

Our proprietary software may contain errors or failures that are not detected until after the software is introduced or updates and new versions are released. It is challenging for us to test our software for all potential problems because it is difficult to simulate the wide variety of computing environments or treatment methodologies that our clients may deploy or rely upon. From time to time we have discovered defects or errors in our software, and such defects or errors can be expected to appear in the future. Defects and errors that are not timely detected and remedied could expose us to risk of liability to clients, clinicians, and patients and cause delays in introduction of new services, result in increased costs and diversion of development resources, require design modifications, or decrease market acceptance or client satisfaction with our services.

We rely on Internet infrastructure, bandwidth providers, other third parties, and our own systems for providing services to our users, and any failure or interruption in the services provided by these third parties or our own systems could expose us to litigation and negatively impact our relationships with users, adversely affecting our brand and our business.

Our ability to deliver our Internet and telecommunications-based services is dependent on the development and maintenance of the infrastructure of the Internet and other telecommunications services by third parties. This includes maintenance of a reliable network backbone with the necessary speed, data capacity, and security for providing reliable Internet access and services. Our services are designed to operate without interruption in accordance with our service level commitments. However, we have experienced and expect that we will experience interruptions and delays in services and availability from time to time. We rely on internal systems as well as third-party vendors, including data center, bandwidth, and telecommunications equipment providers, to provide our services. We do not maintain redundant systems or facilities for some of these services. In the event of a catastrophic event with respect to one or more of these systems or facilities, we may experience an extended period of system unavailability, which could negatively impact our relationship with users. Any disruption in the network access, telecommunications, or co- location services provided by these third-party providers or any failure of or by these third-party providers or our own systems to handle current or higher volume of use could significantly harm our business. We exercise limited control over these third-party vendors, which increases our vulnerability to problems with services they provide.

Any errors, failures, interruptions, or delays experienced in connection with these third-party technologies and information services or our own systems could negatively impact our relationships with users and adversely affect our business and could expose us to third-party liabilities. The reliability and performance of the Internet may be harmed by increased usage or by denial-of-service attacks. The Internet has experienced a variety of outages and other delays as a result of damages to portions of its infrastructure, and it could face outages and delays in the future. These outages and delays could reduce the level of Internet usage as well as the availability of the Internet to us for delivery of our Internet-based services.

If we are unable to keep up with the rapid technological changes of the internet industry, our business may suffer.

The internet industry is experiencing rapid technological changes. The future success of our cloud-based services will depend on our ability to anticipate, adapt and support new technologies and industry standards. If we fail to anticipate and adapt to these and other technological changes, our market share, profitability and share price could suffer.

10

Our internal control over financial reporting is not effective and has material weaknesses.

We are subject to the reporting obligations under the U.S. securities laws. The Securities and Exchange Commission, or the SEC, as required under Section 404 of the Sarbanes-Oxley Act of 2002 (“Section 404”), has adopted rules requiring public companies to include a report of management on the effectiveness of such companies’ internal control over financial reporting in their respective annual reports. This annual report does not include an attestation report of our registered public accounting firm regarding internal control over financial reporting because we are currently a non-accelerated filer and therefore not required to obtain such report.

Our management has concluded that under the rules of Section 404, our internal control over financial reporting was not effective as of December 31, 2019. A material weakness is a deficiency, or a combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of our company’s financial statements will not be prevented or detected and corrected on a timely basis. The material weakness we identified is insufficient qualified accounting personnel with appropriate understanding of U.S. GAAP and SEC reporting requirements commensurate with our financial reporting requirements. Also, as a small company, we do not have sufficient internal control personnel to set up adequate review functions at each reporting level.

We are in the process of implementing measures to resolve the material weakness and improve our internal and disclosure controls. However, we may not be able to successfully implement the remedial measures. The implementation of our remedial initiatives may not fully address the material weakness in our internal control over financial reporting. In addition, the process of designing and implementing an effective financial reporting system is a continuous effort that requires us to anticipate and react to changes in our business and economic and regulatory environments and to expend significant resources to maintain a financial reporting system that is adequate in satisfying our reporting obligations.

As a result, our business and financial condition, results of operations and prospects, as well as the trading price of our Class A Common Shares may be materially and adversely affected. Ineffective internal control over financial reporting could also expose us to increased risk of fraud or misuse of corporate assets, which in turn, could subject us to potential delisting from the Nasdaq Capital Market on which our Class A Common Shares are listed, regulatory investigations or civil or criminal sanctions.

Risks Relating to Doing Business in China

Adverse changes in economic and political policies of the PRC government could have a material adverse effect on the overall economic growth of China, which could adversely affect our business.

Substantially all of our business operations are conducted in China. Accordingly, our results of operations, financial condition and prospects are subject to economic, political and legal developments in China. China’s economy differs from the economies of most developed countries in many respects, with respect to the amount of government involvement, level of development, growth rate, control of foreign exchange, and allocation of resources.

While the PRC economy has grown more rapidly in the past 30 years than the world economy as a whole, growth has been uneven across different regions and among various economic sectors of China. The PRC government has implemented various measures to encourage economic development and guide the allocation of resources. Some of these measures benefit the overall PRC economy, but may also have a negative effect on us. For example, our financial condition and results of operations may be adversely affected by government control over capital investments or changes in tax regulations that are applicable to us. Stimulus measures designed to boost the Chinese economy may contribute to higher inflation, which could adversely affect our results of operations and financial condition. In addition, since 2012, growth of the Chinese economy has slowed down. We cannot assure you that Chinese economy will continue to grow, or that if there is growth, such growth will be steady and uniform, or that if there is a slowdown, such slowdown will not have a negative effect on our business and results of operations.

We do not have business interruption, litigation or natural disaster insurance.

The insurance industry in China is still at an early stage of development. In particular, PRC insurance companies offer limited insurance products. As a result, we do not have any business liability or disruption insurance coverage for our operations in China. Any business interruption, litigation or natural disaster may result in our business incurring substantial costs and the diversion of resources.

11

Currently, there are no specific laws or regulations applicable to wearable medical products in China, which are instead subject to general laws applicable to medical products. If there are applicable government regulations in the future, it may create risks and challenges with respect to our compliance efforts and our business strategies.

The health care industry is highly regulated and is subject to changing political, legislative, regulatory, and other influences. Existing and new laws and regulations affecting the health care industry could create unexpected liabilities for us, cause us to incur additional costs, and restrict our operations. Many health care laws are complex, and their application to specific services and relationships may not be clear. In particular, many existing health care laws and regulations, when enacted, did not anticipate the wearable medical products and services that we provide, and these laws and regulations may be applied to our business in ways that we do not anticipate. Our failure to accurately anticipate the application of these laws and regulations, or our other failure to comply, could create liability for us, result in adverse publicity, and negatively affect our business.

Restrictions on currency exchange may limit our ability to receive and use our income effectively.

Lianluo Connection, our directly wholly-owned PRC subsidiary, is a foreign invested enterprise (FIE) under PRC laws, and substantially all of our sales are settled in RMB. Any future restrictions on currency exchanges may limit our ability to use revenue generated in RMB to fund any future business activities outside of China or to make dividend or other payments in U.S. dollars. Although the conversion of RMB into foreign currency for current account transactions, such as interest payments, profit distributions, and trade or service related transactions, can be made without prior governmental approval, significant restrictions still remain, including primarily the restriction that FIEs may only buy, sell, or remit foreign currencies after providing valid commercial documents to certain banks in China authorized to conduct foreign exchange business. In addition, conversion of RMB for capital account items, including direct investment and loans, are subject to governmental approval in China, and requires companies to open and maintain separate foreign exchange accounts for capital account items. We cannot be certain that the Chinese regulatory authorities will not impose more stringent restrictions on the convertibility of the RMB.

Uncertainties with respect to the PRC legal system could limit the legal protections available to you and us.

We conduct substantially all of our business through our operating subsidiaries in the PRC. Our operating subsidiaries are generally subject to laws and regulations applicable to foreign investments in China and, in particular, laws applicable to foreign invested entities established in the PRC, or FIEs. The PRC legal system is based on written statutes, and prior court decisions may be cited for reference but have limited precedential value. Since 1979, a series of new PRC laws and regulations have significantly enhanced the protections afforded to various forms of foreign investments in China. However, since the PRC legal system continues to evolve rapidly, the interpretations of many laws, regulations, and rules are not always uniform, and enforcement of these laws, regulations, and rules involve uncertainties, which may limit legal protections available to you and us. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention. Furthermore, all of our executive officers and most of our directors are residents of China and not of the United States, and substantially all the assets of these persons are located outside the United States. As a result, it could be difficult for investors to effect service of process in the United States or to enforce a judgment obtained in the United States against our Chinese operations and subsidiaries.

You may have difficulty enforcing judgments against us.

Most of our assets are located outside of the United States and most of our current operations are conducted in the PRC. In addition, most of our directors and officers are nationals and residents of countries other than the United States. A substantial portion of the assets of these persons is located outside the United States. As a result, it may be difficult for you to effect service of process within the United States upon these persons. It may also be difficult for you to enforce U.S. courts’ judgments entered pursuant to the civil liability provisions of the U.S. federal securities laws against us, or our officers and directors most of whom are not residents of the United States and the substantial majority of whose assets are located outside of the United States. In addition, there is uncertainty as to whether the courts of the PRC would recognize or enforce judgments of U.S. courts. The recognition and enforcement of foreign judgments are provided for in the PRC Civil Procedures Law. Courts in China may recognize and enforce foreign judgments in accordance with the requirements of the PRC Civil Procedures Law based on treaties between China and the country where the judgment is made or on reciprocity between jurisdictions. China does not have any treaties or other arrangements with the United States or British Virgin Islands that provide for the reciprocal recognition and enforcement of judgments. In addition, according to the PRC Civil Procedures Law, courts in the PRC will not enforce a foreign judgment, if they decide that the judgment violates basic principles of PRC law, sovereignty, national security, or public interest. It is uncertain whether a PRC court would enforce a judgment rendered by a court in the United States against us or our officers and directors.

12

The PRC government exerts substantial influence over the manner in which business activities are conducted.

The PRC government has exercised and continues to exercise substantial control over virtually every sector of the Chinese economy through regulations and state ownership. Our ability to operate in China may be harmed by changes in Chinese laws and regulations, including those relating to taxation, product liability, healthcare, labor, property, privacy and other matters. We believe that our operations in China comply with, in material aspects, with all applicable legal and regulatory requirements. However, the central or local governments of China may impose new, stricter regulations or interpretations of existing regulations that would require additional expenditures and efforts on our part to ensure our compliance with such regulations or interpretations.

Fluctuations in exchange rates could adversely affect our business and the value of our securities.

The value of our Class A Common Shares will be indirectly affected by the foreign exchange rate between the U.S. dollar and RMB. Appreciation or depreciation in the value of RMB relative to the U.S. dollar would affect our financial results reported in U.S. dollar without giving effect to any underlying change in our business or results of operations. Fluctuations in the exchange rate will also affect the relative value of any dividend we issue that will be exchanged into U.S. dollars, as well as earnings from any U.S. dollar-denominated investments we make in the future.

Since July 2005, the RMB has no longer been pegged to the U.S. dollar. Although the People’s Bank of China regularly intervenes in the foreign exchange market to prevent significant short-term fluctuations in the exchange rate, RMB may appreciate or depreciate significantly in value against the U.S. dollar in the medium to long term. Moreover, it is possible that in the future PRC authorities may lift restrictions on fluctuations in the RMB exchange rate and lessen intervention in the foreign exchange market.

Very limited hedging transactions are available in China to reduce our exposure to the exchange rate fluctuations. To date, we have not entered into any hedging transactions. While we may enter into hedging transactions in the future, the availability and effectiveness of these transactions may be limited. We may not be able to successfully hedge our exposure at all. In addition, our foreign currency exchange losses may be magnified by PRC exchange control regulations that restrict our ability to convert RMB into foreign currencies.

Restrictions under PRC law on our PRC subsidiaries’ ability to make dividends and other distributions could materially and adversely affect our ability to grow, make investments or acquisitions that could benefit our business, pay dividends to you, and otherwise fund and conduct our business.

Substantially all of our revenues are earned by our PRC subsidiaries. However, PRC regulations restrict the ability of our PRC subsidiaries to make dividends and other payments to their offshore parent companies. PRC legal restrictions permit payments of dividends by our PRC subsidiaries only out of their accumulated after-tax profits, if any, determined in accordance with PRC accounting standards and regulations. Our PRC subsidiaries are also required under PRC laws and regulations to allocate at least 10% of their annual after-tax profits determined in accordance with PRC GAAP to a statutory general reserve fund until the amounts in said reserve fund reach 50% of the company’s registered capital. Allocations to these statutory reserve funds can only be used for specific purposes and are not transferable to us in the form of loans, advances, or cash dividends. Any limitations on the ability of our PRC subsidiaries to transfer funds to us could materially and adversely limit our ability to grow, make investments or acquisitions that could be beneficial to our business, pay dividends and otherwise fund and conduct our business.

13

PRC regulations relating to investments in offshore companies by PRC residents may subject our PRC-resident beneficial owners or our PRC subsidiaries to liability or penalties, limit our ability to inject capital into our PRC subsidiaries or limit our PRC subsidiaries’ ability to increase their registered capital or distribute profits.

The State Administration of Foreign Exchange (SAFE) promulgated the Circular on Relevant Issues Concerning Foreign Exchange Control on Domestic Residents’ Offshore Investment and Financing and Roundtrip Investment through Special Purpose Vehicles, or SAFE Circular 37, on July 4, 2014, which replaced the former circular commonly known as “SAFE Circular 75” promulgated by SAFE on October 21, 2005. SAFE Circular 37 requires PRC residents to register with local branches of the SAFE in connection with their direct establishment or indirect control of an offshore entity, for the purpose of overseas investment and financing, with such PRC residents’ legally owned assets or equity interests in domestic enterprises or offshore assets or interests, referred to in SAFE Circular 37 as a “special purpose vehicle.” SAFE Circular 37 further requires amendment to the registration in the event of any significant changes with respect to the special purpose vehicle, such as increase or decrease of capital contributed by PRC individuals, share transfer or exchange, merger, division or other material event. In the event that a PRC shareholder holding interests in a special purpose vehicle fails to fulfill the required SAFE registration, the PRC subsidiaries of that special purpose vehicle may be prohibited from making profit distributions to the offshore parent and from carrying out subsequent cross-border foreign exchange activities, and the special purpose vehicle may be restricted in its ability to contribute additional capital into its PRC subsidiaries. Moreover, failure to comply with the various SAFE registration requirements described above could result in liability under PRC law for evasion of foreign exchange controls. According to the Notice on Further Simplifying and Improving Policies for the Foreign Exchange Administration of Direct Investment released on February 13, 2015 by SAFE, local banks will examine and handle foreign exchange registration for overseas direct investment, including the initial foreign exchange registration and amendment registration, under SAFE Circular 37 from June 1, 2015.

According to SAFE Circular 37, our shareholders or beneficial owners, who are PRC residents, are subject to SAFE Circular 37 or other foreign exchange administrative regulations in respect of their investment in our company. We have notified substantial beneficial owners of our Common Shares who we know are PRC residents of their filing obligations. Nevertheless, we may not be aware of the identities of all of our beneficial owners who are PRC residents. We do not have control over our beneficial owners and there can be no assurance that all of our PRC-resident beneficial owners will comply with SAFE Circular 37 and subsequent implementation rules, and there is no assurance that the registration under SAFE Circular 37 and any amendment will be completed in a timely manner, or will be completed at all. The failure of our beneficial owners who are PRC residents to register or amend their foreign exchange registrations in a timely manner pursuant to SAFE Circular 37 and subsequent implementation rules, or the failure of future beneficial owners of our company who are PRC residents to comply with the registration procedures set forth in SAFE Circular 37 and subsequent implementation rules, may subject such beneficial owners or our PRC subsidiaries to fines and legal sanctions. Such failure to register or comply with relevant requirements may also limit our ability to contribute additional capital to our PRC subsidiaries and limit our PRC subsidiaries’ ability to distribute dividends to us. These risks may have a material adverse effect on our business, financial condition and results of operations.

Furthermore, it is uncertain how SAFE Circular 37, and any future regulation concerning offshore or cross-border transactions, will be interpreted, amended and implemented by the relevant PRC government authorities, and we cannot predict how these regulations will affect our business operations or future strategy. Failure to register or comply with relevant requirements may also limit our ability to contribute additional capital to our PRC subsidiaries and limit our PRC subsidiaries’ ability to distribute dividends to us. These risks could in the future have a material adverse effect on our business, financial condition and results of operations.

We may be unable to complete a business combination transaction efficiently or on favorable terms due to complicated merger and acquisition regulations which first became effective on September 8, 2006.

On August 9, 2006, six PRC regulatory agencies, including the China Securities Regulatory Commission, promulgated the Regulation on Mergers and Acquisitions of Domestic Companies by Foreign Investors, which became effective on September 8, 2006, and was subsequently amended in 2009. This regulation, among other regulations and rules, governs the approval process of a PRC company’s participation in an acquisition of assets or equity interests. Depending on the structure of the transaction, the regulation requires the PRC parties to make a series of applications and supplemental applications to the government agencies for approval of acquisition of assets or equity interests of another entity. In some instances, the application process may require a presentation of economic data concerning the transaction, including appraisals of the target business and evaluations of the acquirer, which are designed to allow the government to assess viability of the transaction. Government approvals will have expiration dates, by which a transaction must be completed and reported to the government agencies. Compliance with the regulation is likely to be more time consuming and expensive than it was in the past, and provides the government more controls over business combination of two enterprises.