Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | Registration statement pursuant to Section 12(b) or 12(g) of the Securities Exchange Act of 1934 |

or

| x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2014

or

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

or

| ¨ | Shell company report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Date of event requiring this shell company report

Commission file number 001-34563

Concord Medical Services Holdings Limited

(Exact Name of Registrant as Specified in Its Charter)

Cayman Islands

(Jurisdiction of Incorporation or Organization)

18/F, Tower A, Global Trade Center

36 North Third Ring Road, Dongcheng District

Beijing 100013

People’s Republic of China

(Address of Principal Executive Offices)

Mr. Adam Jigang Sun

Telephone: (86 10) 5957-5266

Facsimile: (86 10) 5957-5252

18/F, Tower A, Global Trade Center

36 North Third Ring Road, Dongcheng District

Beijing 100013

People’s Republic of China

(Name, Telephone, E-mail and/or Facsimile Number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Ordinary shares, par value US$0.0001 per share* | New York Stock Exchange* |

| * | Not for trading, but only in connection with the listing of the American depositary shares, or ADSs, on the New York Stock Exchange. Each ADS represents the right to receive three ordinary shares. The ADSs are registered under the Securities Act of 1933, as amended, pursuant to a registration statement on Form F-6. Accordingly, the ADSs are exempt from registration under Section 12(b) of the Securities Exchange Act of 1934, as amended, pursuant to Rule 12a-8 thereunder. |

Table of Contents

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

134,836,300 Class A Ordinary Shares Issued and Outstanding

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer x | Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP x | International Financial Reporting Standards as issued by the International Accounting Standards Board ¨ |

Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which consolidated financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes ¨ No x

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ¨ No ¨

Table of Contents

i

Table of Contents

CONVENTIONS THAT APPLY TO THIS ANNUAL REPORT ON FORM 20-F

Unless otherwise indicated, references in this annual report on Form 20-F to:

| • | “ADRs” are to the American depositary receipts, which, if issued, evidence our ADSs; |

| • | “ADSs” are to our American depositary shares, each of which represents three ordinary shares; |

| • | “China” and the “PRC” are to the People’s Republic of China, excluding, for the purposes of this annual report only, Taiwan and the special administrative regions of Hong Kong and Macau; |

| • | “Concord Medical,” “we,” “us,” “our company” and “our” are to Concord Medical Services Holdings Limited, its predecessor entities and its consolidated subsidiaries; |

| • | “ordinary shares” are to our ordinary shares, par value US$0.0001 per share; |

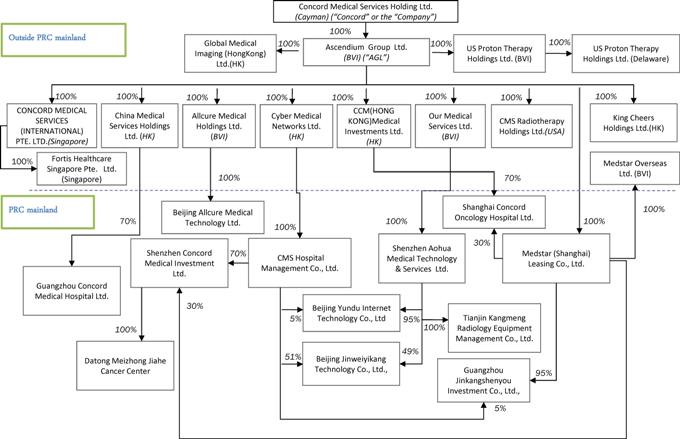

| • | “PRC subsidiaries” are to our subsidiaries incorporated in the People’s Republic of China, including CMS Hospital Management Co., Ltd., Beijing Yundu Internet Technology Co., Ltd., Shenzhen Aohua Medical Technology & Services Ltd., Tianjin Kangmeng Radiology Equipment Management Co., Ltd., Medstar (Shanghai) Leasing Co., Ltd., Guangzhou Concord Medical Cancer Hospital Co., Ltd., Beijing Jinweiyikang Technology Co., Ltd., Guangzhou Jinkangshenyou Investment Co., Ltd. Shanghai Concord Oncology Hospital Limited, Shenzhen Concord Medical Investment Ltd., Beijing Allcure Medical Technology Ltd., and Datong Meizhong Jiahe Cancer Center. |

| • | “RMB” and “Renminbi” are to the legal currency of China; |

| • | “US$” and “U.S. dollars” are to the legal currency of the United States; and |

| • | “£” is to the legal currency of the United Kingdom of Great Britain and Northern Ireland. |

1

Table of Contents

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not Applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not Applicable.

| ITEM 3. | KEY INFORMATION |

| A. | Selected Financial Data |

The following selected consolidated statements of comprehensive income and other consolidated financial data for the years ended December 31, 2012, December 31, 2013 and December 31, 2014 (other than the income (loss) per ADS data) and the selected consolidated balance sheets data as of December 31, 2013 and 2014 have been derived from our audited consolidated financial statements, which is included elsewhere in this annual report on Form 20-F. The selected consolidated statements of comprehensive income data for the years ended December 31, 2010 and 2011 and the selected consolidated balance sheets data as of December 31, 2010, 2011 and 2012 have been derived from our audited consolidated financial statements, which are not included in this annual report on Form 20-F. You should read the selected consolidated financial data in conjunction with those financial statements and the related notes and “Item 5. Operating and Financial Review and Prospects” included elsewhere in this annual report on Form 20-F. Our consolidated financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States, or U.S. GAAP. Our historical results are not necessarily indicative of our results expected for any future periods.

2

Table of Contents

| Concord Medical | ||||||||||||||||||||||||

| Year Ended December, 31 | ||||||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in thousands, except share, per share and per ADS data) | ||||||||||||||||||||||||

| Selected Consolidated Statements of Comprehensive Income Data |

||||||||||||||||||||||||

| Revenues, net of business tax, value-added tax and related surcharges |

389,524 | 450,125 | 455,651 | 563,124 | 606,883 | 97,813 | ||||||||||||||||||

| Cost of revenues |

(122,700 | ) | (159,416 | ) | (164,523 | ) | (217,655 | ) | (274,562 | ) | (44,251 | ) | ||||||||||||

| Gross profit |

266,824 | 290,709 | 291,128 | 345,469 | 332,321 | 53,562 | ||||||||||||||||||

| Operating expenses: |

||||||||||||||||||||||||

| Selling expenses(1) |

(17,150 | ) | (37,453 | ) | (53,911 | ) | (104,667 | ) | (95,096 | ) | (15,327 | ) | ||||||||||||

| General and administrative expenses(2) |

(66,789 | ) | (80,628 | ) | (61,106 | ) | (84,506 | ) | (53,576 | ) | (8,635 | ) | ||||||||||||

| Asset impairment |

(3,219 | ) | (333,934 | ) | (3,360 | ) | — | — | — | |||||||||||||||

| Other operating income |

— | — | 9,185 | — | — | — | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income |

179,666 | 161,306 | 181,936 | 156,296 | 183,649 | 29,600 | ||||||||||||||||||

| Interest expense |

(7,448 | ) | (6,454 | ) | (12,452 | ) | (36,884 | ) | (53,470 | ) | (8,618 | ) | ||||||||||||

| Foreign exchange (losses) gains, net |

(5,436 | ) | (10,975 | ) | (117 | ) | 784 | 9,585 | 1,545 | |||||||||||||||

| Gain (loss) from disposal of property, plant and equipment |

543 | — | 4,432 | (1,235 | ) | (3,955 | ) | (637 | ) | |||||||||||||||

| Interest income |

7,865 | 13,357 | 5,853 | 9,828 | 21,208 | 3,418 | ||||||||||||||||||

| Changes in fair value of derivatives |

— | — | — | — | 2,605 | 420 | ||||||||||||||||||

| Equity pick up of equity investee |

— | — | 1,790 | 13,470 | 13,911 | 2,242 | ||||||||||||||||||

| Other (expense) income, net |

(399 | ) | 346 | (307 | ) | 2,010 | 2,113 | 341 | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income from continuing operations before income taxes |

174,791 | (165,032 | ) | 181,135 | 144,269 | 175,646 | 28,311 | |||||||||||||||||

| Income tax expenses |

(43,873 | ) | (46,320 | ) | (54,249 | ) | (63,838 | ) | (80,850 | ) | (13,032 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) from continuing operations |

130,918 | (211,352 | ) | 126,886 | 80,431 | 94,796 | 15,279 | |||||||||||||||||

| Net income from discontinued operations |

— | — | 7,594 | 10,765 | 25,476 | 4,106 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income |

— | — | 134,480 | 91,196 | 120,272 | 19,385 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) attributable to non-controlling interests |

1,518 | 3,651 | 3,649 | 5,303 | (4,437 | ) | (715 | ) | ||||||||||||||||

| Net income (loss) attributable to ordinary shareholders |

129,400 | (215,003 | ) | 130,831 | 85,893 | 124,709 | 20,100 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Earning (loss) per share – basic / diluted |

0.89 | (1.51 | ) | 0.95 | 0.64 | 0.92 | 0.15 | |||||||||||||||||

| Earning (loss) per ADS – basic / diluted |

2.66 | (4.53 | ) | 2.84 | 1.92 | 2.76 | 0.45 | |||||||||||||||||

| (1) | Our selling expenses included share-based compensation of RMB2.5 million in 2010, RMB2.4 million in 2011, RMB2.3 million in 2012, RMB2.3 million in 2013 and RMB0.7 million (US$0.1 million) in 2014. |

| (2) | Our general and administrative expenses included share-based compensation expenses related to certain share options granted in 2010, 2011, 2012, 2013 and 2014 of RMB7.0 million, RMB6.9 million, RMB6.8 million, RMB6.5 million and RMB6.6 million (US$1.1 million), respectively. |

3

Table of Contents

| Concord Medical | ||||||||||||||||||||||||

| As of December 31, | ||||||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||

| Selected Consolidated Balance Sheets Data |

||||||||||||||||||||||||

| Cash |

535,783 | 219,078 | 75,382 | 283,033 | 478,682 | 77,150 | ||||||||||||||||||

| Total current assets |

904,416 | 733,657 | 853,133 | 1,300,010 | 1,463,682 | 235,903 | ||||||||||||||||||

| Property, plant and equipment, net |

907,336 | 1,068,703 | 1,522,920 | 1,492,573 | 749,683 | 120,827 | ||||||||||||||||||

| Goodwill |

300,163 | — | 292,885 | 292,885 | — | — | ||||||||||||||||||

| Intangible assets, net |

146,113 | 129,018 | 146,512 | 116,843 | 61,243 | 9,871 | ||||||||||||||||||

| Total assets |

2,663,044 | 2,393,446 | 3,665,220 | 4,093,557 | 2,959,332 | 476,959 | ||||||||||||||||||

| Long-term bank borrowings, current portion |

60,906 | 77,479 | 191,473 | 273,310 | 246,233 | 39,686 | ||||||||||||||||||

| Total equity |

2,301,835 | 2,038,096 | 2,339,910 | 2,433,717 | 1,800,058 | 290,119 | ||||||||||||||||||

| Total liabilities and equity |

2,663,044 | 2,393,446 | 3,665,220 | 4,093,557 | 2,959,332 | 476,959 | ||||||||||||||||||

| Concord Medical | ||||||||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||

| Selected Consolidated Statements of Cash Flow Data |

||||||||||||||||||||||||

| Net cash generated from operating activities |

190,972 | 137,102 | 259,515 | 259,033 | 490,381 | 79,036 | ||||||||||||||||||

| Net cash (used in) generated from investing activities (1) |

(529,468 | ) | (494,867 | ) | (659,290 | ) | (133,540 | ) | 287,055 | 46,265 | ||||||||||||||

| Net cash (used in) generated from financing activities |

(154,933 | ) | 41,785 | 255,932 | 77,722 | (579,144 | ) | (93,341 | ) | |||||||||||||||

| Exchange rate effect on cash |

(8,027 | ) | (725 | ) | 147 | 4,436 | (2,643 | ) | (427 | ) | ||||||||||||||

| Net (decrease) increase in cash |

(501,456 | ) | (316,705 | ) | (143,696 | ) | 207,651 | |

195,649 |

|

31,533 | |||||||||||||

| (1) | Net cash used in investing activities in 2010, 2011, 2012 and 2013 includes acquisitions, net of cash acquired, of RMB45.0 million, RMB20.3 million, RMB223.4 million, and nil respectively. Net cash generated from investing activities in 2014 includes disposal, net of cash disposal, of RMB280.1 million. |

| Concord Medical | ||||||||||||||||||||||||

| Year Ended December 31, | ||||||||||||||||||||||||

| 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||||||||||

| RMB | RMB | RMB | RMB | RMB | US$ | |||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||

| Total net revenues generated by our primary medical equipment under lease and management services arrangements: |

||||||||||||||||||||||||

| Linear accelerators |

108,974 | 114,250 | 115,009 | 135,268 | 144,694 | 23,320 | ||||||||||||||||||

| Head gamma knife systems |

80,909 | 77,035 | 76,239 | 68,553 | 58,509 | 9,430 | ||||||||||||||||||

| Body gamma knife systems |

38,599 | 42,512 | 31,365 | 42,016 | 31,478 | 5,073 | ||||||||||||||||||

| PET-CT scanners |

41,036 | 59,054 | 71,895 | 107,536 | 116,078 | 18,708 | ||||||||||||||||||

| MRI scanners |

51,738 | 65,031 | 79,220 | 83,619 | 103,197 | 16,632 | ||||||||||||||||||

| Others (1) |

27,992 | 22,576 | 38,602 | 61,564 | 57,635 | 9,290 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total net revenues — lease and management services |

349,248 | 380,457 | 412,330 | 498,556 | 511,591 | 82,453 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (1) | Other primary medical equipment used includes CT scanners and ECT scanners for diagnostic imaging, electroencephalography for the diagnosis of epilepsy, thermotherapy to increase the efficacy of and for pain relief after radiotherapy and chemotherapy, high intensity focused ultrasound therapy for the treatment of cancer, stereotactic radiofrequency ablation for the treatment of Parkinson’s Disease and refraction and tonometry for the diagnosis of ophthalmic conditions. |

4

Table of Contents

Exchange Rate Information

Our business is primarily conducted in China and all of our revenues are denominated in Renminbi. Periodic reports made to shareholders will be expressed in Renminbi with translations of Renminbi amounts into U.S. dollars at the then current exchange rate solely for the convenience of the reader. Conversions of Renminbi into U.S. dollars in this annual report are based on the noon buying rate as set forth in the H.10 statistical release of the Federal Reserve Board. Unless otherwise noted, all translations from Renminbi to U.S. dollars and from U.S. dollars to Renminbi in this annual report were made at a rate of RMB6.2046 to US$1.00, the noon buying rate in effect as of December 31, 2014. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, the rates stated below, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange and through restrictions on foreign trade. On April 17, 2015, the noon buying rate was RMB6.1976 to US$1.00.

The following table sets forth information concerning exchange rates between the Renminbi and the U.S. dollar for the periods indicated.

| Exchange Rate (Renminbi per US Dollar)(1) | ||||||||||||||||

| Period End | Average(2) | High | Low | |||||||||||||

| Period |

(RMB per US$1.00) | |||||||||||||||

| 2010 |

6.6000 | 6.7603 | 6.8330 | 6.6000 | ||||||||||||

| 2011 |

6.2939 | 6.4475 | 6.6364 | 6.2939 | ||||||||||||

| 2012 |

6.2301 | 6.2990 | 6.3879 | 6.2221 | ||||||||||||

| 2013 |

6.0537 | 6.1412 | 6.2438 | 6.0537 | ||||||||||||

| 2014 |

6.2046 | 6.1620 | 6.2591 | 6.0402 | ||||||||||||

| November |

6.1429 | 6.1249 | 6.1429 | 6.1117 | ||||||||||||

| December |

6.2046 | 6.1886 | 6.2256 | 6.1490 | ||||||||||||

| 2015 |

||||||||||||||||

| January |

6.2495 | 6.2181 | 6.2535 | 6.1870 | ||||||||||||

| February |

6.2695 | 6.2518 | 6.2695 | 6.2399 | ||||||||||||

| March |

6.1990 | 6.2386 | 6.2741 | 6.1955 | ||||||||||||

| April (through April 17) |

6.1976 | 6.2010 | 6.2152 | 6.1930 | ||||||||||||

| (1) | The source of the exchange rate is the H.10 statistical release of the Federal Reserve Board. |

| (2) | Annual averages are calculated from month-end rates. Monthly averages are calculated using the average of the daily rates during the relevant period. |

| B. | Capitalization and Indebtedness |

Not Applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not Applicable.

5

Table of Contents

| D. | Risk Factors |

Risks Related to Our Company

We plan to establish and operate additional specialty cancer hospitals that will be majority owned by us and are subject to significant risks.

As part of our growth strategy we plan to establish specialty cancer hospitals that will focus on providing radiotherapy services as well as diagnostic imaging services, chemotherapy and surgery. For example, at the Beijing Proton Medical Center, one of our planned specialty cancer hospitals, we plan to offer proton beam therapy treatment services with which we have had no prior experience. Since we have limited experience in operating our own specialty cancer hospital, or in providing many of the services that we plan to offer in our specialty cancer hospitals, such as chemotherapy treatments, surgical procedures or proton beam therapy, we may not be able to provide as high a level of service quality for those treatment options as compared to the other treatments that are currently offered at our network of centers, which may result in damage to our reputation and our future growth prospects. In addition, we may not be successful in recruiting qualified medical professionals to effectively provide the services that we intend to offer in our specialty cancer hospitals. Furthermore, although our brand name is well known among referring doctors, patients are not currently familiar with our brand as we do not carry our own brand name in our network of centers under our existing agreements with our hospital partners. Therefore, when we establish our own specialty cancer hospitals under our brand name, we may not be able to immediately gain wide acceptance among patients and, thus, may be unable to attract a sufficient number of patients to our new hospitals.

We plan to carry out a number of large-scale hospital construction projects in the near future, which requires substantial increase in capital expenditures. Our operation and financial conditions and results will be adversely affected if we could not effectively manage capital expenditures.

We plan to build three premium cancer hospitals in major cities in China, namely Beijing, Shanghai and Guangzhou. All these cities are considered top-tier cities in China, with large and nationally-renowned government hospitals. To attract patients, our planned premium hospitals need to train our staff members properly, provide services and treatment environment superior to local hospitals as well as install high-end equipment, including CyberKnife, IMRT (Intensity-Modulated Radiation Therapy) and proton beam therapy. The required capital expenditure will be substantial. The process of capital expenditure planning, designing and construction of the premium hospitals will be time consuming and complex which requires a dedicated team in our company. We do not have prior experience and existing team in managing projects of the planned size. If we cannot manage the process properly, our operating and financial results will be affected adversely.

Our growth plan includes the construction of premium cancer hospitals, free-standing radiotherapy and diagnostic centers. If we cannot identify and seize the growth opportunities in the fast-changing market, our future growth will face uncertainties.

We plan to apply for approvals to build free-standing radiotherapy and diagnostic centers in multiple regions in China. These free-standing centers will not be affiliated with local government hospitals like our current centers. While the current healthcare reform policies encourage the establishment of private medical institutions, the implementation process will be complex and time-consuming and subject to uncertainty. We are in the process of identifying suitable regions for such free-standing centers by taking into consideration a number of factors including the regional market size, existing competition and potential strategic partners. There are uncertainties about how successful we can identify the suitable market, acquire the required government approvals timely and control the planned investments. In addition, we may face competition from the existing centers.

We may encounter difficulties in successfully opening new centers or renewing agreements for existing centers due to the limited number of suitable hospital partners and their potential ability to finance the purchase of medical equipment directly.

Our growth was driven by our ability to expand our network of radiotherapy and diagnostic imaging centers by primarily entering into new agreements with top-tier hospitals in China, which are 3A hospitals, the highest ranked hospitals by quality and size in China as determined in accordance with the standards of the Ministry of Health. The agreements that hospitals enter into with us and our competitors are typically long-term in nature with terms of up to 20 years. As a result, in any locality or at any given time, there may only be a limited number of top-tier hospitals that have not yet entered into long-term agreements with us or our competitors and with which we are able to enter into new agreements. In addition, quotas imposed by government authorities as to the number and type of certain medical equipment that can be purchased, such as head gamma knife systems or PET-CT scanners, will further limit the number of top-tier hospitals that we or our competitors can enter into agreements within a given period. See “—Risks Related to Our Industry—Healthcare administrative authorities in China currently set procurement quotas for certain types of medical equipment.” Due to the limited supply of suitable top-tier hospitals and increasing competition, we may not be able to enter into agreements with new hospital partners or renew agreements with existing hospital partners on terms as favorable as those that we have been able to obtain in the past, or at all. Some of our competitors may have greater financial resources than us, which may provide them with an advantage in negotiating new agreements with hospitals, including our existing hospital partners. In addition, if

6

Table of Contents

adequate funding becomes available for hospitals to purchase medical equipment directly, hospitals may choose to purchase and manage radiotherapy and diagnostic imaging equipment on their own instead of entering into or renewing agreements with us or our competitors. If we are unable to compete effectively in entering into agreements with new hospital partners or to renew existing agreements on favorable terms, or at all, or if hospitals choose to purchase and manage their own medical equipment, our growth prospects could be materially and adversely affected. Finally, the development of new centers generally involves a ramp-up period during which time the operating efficiency of such centers may be lower than our established centers, which may negatively affect our profitability.

We have historically derived a significant portion of our revenues from centers located at a limited number of our hospital partners and regions in which we operate and our accounts receivable are also concentrated with a few hospital partners.

We have historically derived a large portion of our total net revenues from a limited number of our partner hospitals. In 2012, 2013 and 2014, net revenues derived from our top five hospital partners amounted to approximately 22.9%, 24.2% and 22.5% of our total net revenues, respectively. Our largest hospital partner accounted for 6.9%, 5.6% and 6.4% of our total net revenues during those periods, respectively. In addition, centers located in Beijing, Henan province and Shandong province accounted for 18.3%, 10.0% and 8.1% of our total net revenues in 2012, respectively, centers located in Beijing, Henan province and Sichuan Province accounted for 17.1%, 9.4% and 8.5% of our total net revenues in 2013, respectively, and centers located in Beijing, Shandong and Jiangsu accounted for 15.0%, 8.9% and 7.7% of our total net revenue in 2014, respectively. We may continue to experience such revenue concentration in the future. Due to the concentration of our revenues and dependence on a limited number of hospital partners, any one or more of the following events, among others, may cause material fluctuations or declines in our revenues and could have a material adverse effect on our financial condition, results of operations and prospects:

| • | reduction in the number of patient cases at the centers located at these partner hospitals; |

| • | loss of key experienced medical professionals; |

| • | decrease in the profitability of such centers; |

| • | failure to maintain or renew our agreements with these hospital partners; |

| • | any failure of these hospital partners to pay us our contracted percentage of any such center’s revenue net of specified operating expenses; |

| • | any regulatory changes in the geographic areas where our hospital partners are located; or |

| • | any other disputes with these hospital partners. |

In addition, the top ten of our hospital partners in terms of revenue contribution, accounted for 38.7% of our total network accounts receivable as of December 31, 2014. Any significant delay in the payment of such accounts receivable could have a material impact on our financial condition and results of operations.

We conduct our business in a heavily regulated industry.

The operation of our network of centers is subject to various laws and regulations issued by a number of government agencies at the national and local levels. Such rules and regulations relate mainly to the procurement of large medical equipment, the pricing of medical services, the operation of radiotherapy and diagnostic imaging equipment, the licensing and operation of medical institutions, the licensing of medical staff and the prohibition on non-profit civilian medical institutions from entering into cooperation agreements with third parties to set up for-profit centers that are not independent legal entities. Our growth prospects may be constrained by such rules and regulations, particularly those relating to the procurement of large medical equipment. If we or our hospital partners fail to comply with such applicable laws and regulations, we could be required to make significant changes to our business and operations or suffer fines or penalties, including the potential loss of our business licenses, the suspension from use of our medical equipment, and the suspension or cessation of operations at centers in our network. In addition, many of the agreements we have entered into with our hospital partners provide for termination in the event of major government policy changes that cause the agreements to become inexecutable. Our hospital partners may invoke such termination right to our disadvantage.

We depend on our hospital partners to recruit and retain qualified doctors and other medical professionals to ensure the high quality of treatment services provided in our network of centers.

Our success is dependent in part upon our hospital partners’ ability to recruit and retain doctors and other medical professionals and on our and our hospital partners’ ability to train and manage these medical professionals. Although we may help our hospital partners to identify and recruit suitable, qualified doctors and other medical professionals, almost all of these medical professionals

7

Table of Contents

are employed by our partner hospitals rather than by us. As a result, we may have little control over whether such medical professionals will continue to work in the centers in our network. In addition, there is a limited pool of qualified medical professionals with expertise and experience in radiotherapy and diagnostic imaging in China, and our hospital partners face competition for such qualified medical professionals from other public hospitals, private healthcare providers, research and academic institutions and other organizations. In the event that our hospital partners fail to recruit and retain a sufficient number of these medical professionals, the resulting shortage could adversely affect the operation of centers in our network and our growth prospects.

Any failure by our hospital partners to make contracted payments to us or any disputes over, or significant delays in receiving, such payments could have a material adverse effect on our business and financial condition.

Most of the centers in our network are established through long-term lease and management services arrangements entered into with our hospital partners. We also provide management services to certain radiotherapy and diagnostic imaging centers through service-only agreements. Payments for treatment and diagnostic imaging services provided in the centers in our network are typically collected by our hospital partners who then pass on to us our contracted percentage of such revenue net of specific operating expenses on a periodic basis. Our total outstanding accounts receivable from our hospital partners were RMB210.3 million, RMB272.3 million and RMB265.0 million (US$42.7 million) as of December 31, 2012, 2013 and 2014, respectively. As of December 31, 2014, approximately 9.7% of our network accounts receivable reported on our consolidated balance sheets as of December 31, 2013 were still outstanding. The average turnover days of our network accounts receivable in 2014 were 159 days. Any failure by our hospital partners to pay us our contracted percentage, or any disputes over or significant delays in receiving such payments from our hospital partners, for any reason, could negatively impact our financial condition. Accordingly, any failure by us to maintain good working relationships with our hospital partners, or any dissatisfaction on the part of our hospital partners with our services, could negatively affect the operation of the centers and our ability to collect revenue, reduce the likelihood that our agreements with hospital partners will be renewed, damage our reputation and otherwise have a material adverse effect on our business, financial condition and results of operation.

We may not be able to effectively manage the expansion of our operations through new acquisitions or joint ventures or to successfully realize the anticipated benefits of any such acquisition or joint venture.

We have historically complemented our organic development of new centers through the selective acquisition of complementary businesses or assets or the formation of joint ventures, and we may continue to do so in the future. For example, in June 2012, we acquired 52% of the equity interest in Chang’an Hospital, a licensed full-service private hospital. In December 2012, we acquired 19.98% of equity interest in The University of Texas MD Anderson Cancer Center Proton Therapy Center, a leading proton treatment center in the world. In April 2015, we acquired 100% of the equity interest in Fortis Surgical Hospital. The identification of suitable acquisition targets or joint venture candidates can be difficult, time consuming and costly, and we may not be able to successfully capitalize on identified opportunities. We may not be able to continue to grow our business as anticipated if we are unable to successfully identify and complete potential acquisitions in the future. Even if we successfully complete an acquisition or establish a joint venture, we may not be able to successfully integrate the acquired businesses or assets or cooperate successfully with the joint venture partner. For example, in December 2014 we disposed equity interest in Chang’an Hospital which we acquired in 2012, in order to fully concentrate on building a nationwide network of diagnosis and treatment centers and specialized cancer hospitals. Integration of the acquired business or assets or cooperation with the joint venture partners can be expensive, time consuming and may strain our resources. Such integration or cooperation could also require significant attention from our management team, which may prevent key members of our management from focusing on other important aspects of our business.

In addition, we may be unable to successfully integrate or retain employees or management of the acquired businesses or assets or retain the acquired entity’s patients, suppliers or other partners. Consequently, we may not achieve the anticipated benefits of any acquisitions or joint ventures. We cannot assure any transformation and integration would be implemented successfully, or without incurring significant cost. Furthermore, future acquisitions or joint ventures could result in potentially dilutive issuances of equity or equity-linked securities or the incurrence of debt, contingent liabilities or expenses, or other charges, any of which could have a material adverse effect on our business, financial condition and results of operations.

We had net current liabilities as of December 31, 2012 and we cannot assure you that we will not experience net current liabilities in the future.

We had net current liabilities of RMB6.4 million as of December 31, 2012 primarily due to cost incurred in connection with the acquisition of equity interests in Chang’an Hospital and Texas MD Anderson Cancer Center Proton Therapy Center in 2012. The total consideration we paid for the acquisition was RMB248.8 million for Chang’an Hospital and US$32.3 million for Texas MD Anderson Cancer Center Proton Therapy Center, respectively. We had net current assets of RMB693.9 million (US$111.8 million) as of December 31, 2014. We believe that our current cash and anticipated cash flow from operations will be sufficient to meet our anticipated cash needs, including our cash needs for working capital and capital expenditures, for at least the next 12 months.

8

Table of Contents

However, we cannot assure you that we will not have net current liabilities in the future. If we fail to generate current assets to the extent that the aggregate amount of our current assets on any given day exceeds the aggregate current liabilities on the same day, we will continue to record net current liabilities. If we have significant net current liabilities for an extended period of time, our working capital for purposes of our operations may be subject to constraints, which may have a material adverse effect on our business, financial condition and results of operations.

We may not be successful in negotiating the conversion of a few of our cooperation agreements with our partner hospitals into lease and management agreements due to regulatory changes.

Since the effectiveness in September 2000 of the Implementation Opinions on the Classified Management of Urban Medical Institutions, which was promulgated by the Ministry of Health, the State Administration of Traditional Chinese Medicine, the Ministry of Finance and the National Development Reform Committee, or NDRC, non-profit civilian medical institutions are no longer permitted to enter into cooperation agreements or to continue to operate under existing cooperation agreements with third parties pursuant to which the parties jointly invest in or cooperate to set up for-profit centers or units that are not independent legal entities. However, according to the Opinions on Certain Issues Regarding Classified Management of Urban Medical Institutions issued in July 2001 by the same authorities, a non-profit civilian medical institution may, if lacking sufficient funds to purchase medical equipment outright, enter into a leasing agreement pursuant to which the medical institution leases medical equipment from its partner at market rates. To comply with these regulatory changes, we have transitioned most of our cooperation agreements with non-profit civilian hospitals to lease and management agreements. Although neither we nor any of our hospital partners have incurred any penalties to date for continuing to operate under cooperation agreements at these centers, there can be no assurance that we will not incur penalties in the future or that we will be able to successfully negotiate the conversion of these agreements. If we are unable to successfully negotiate the conversion of our cooperation agreements with these hospitals or if government authorities decide to assess penalties against either us or our hospital partners or to suspend the operation of these centers before we are able to complete the transition, our business, financial condition and results of operation could be materially and adversely affected.

We are not aware of any similar restriction imposed by military healthcare administrative authorities on the cooperation agreements that we have entered into with military hospitals, which are hospitals regulated by the military but most of which are otherwise the same as other government-owned civilian hospitals open to the public. Accordingly, we have maintained our cooperation agreements with 34 military hospitals as of December 31, 2014. However, as military hospitals are also government-owned, if military hospitals are required by military healthcare administrative authorities to transition away from cooperation agreements in the future, we will have to negotiate a similar conversion of the agreements with our military hospital partners. If we are unable to successfully negotiate lease and management or other alternative agreements with our existing military hospital partners on terms not less favorable than those under our cooperation agreements, our business, financial condition and results of operation may be adversely affected.

We cannot assure you that government authorities will not interpret regulations differently from us to find that our lease and management agreements are still not in compliance with relevant regulations.

We believe that our lease and management agreements with civilian public hospital partners, which terms continue to provide that our revenues from hospital-based centers are to be calculated based on contracted percentages of each center’s revenue net of specified operating expenses, are in compliance with the Implementation Opinions on the Classified Management of Urban Medical Institutions and the Opinions on Certain Issues Regarding Classified Management of Urban Medical Institutions. However, we cannot assure you that the Ministry of Health or other competent authorities will not interpret these regulations differently to find that our lease and management agreements are still not in compliance with such regulations, in which instance, such authorities could, among other things, declare our lease and management agreements to be void, order our civilian hospital partners to terminate such agreements with us, order our civilian hospitals partners to suspend or cease operation of the centers governed by such agreements, suspend the use of our medical equipment, or confiscate revenues generated under the noncompliant agreements. Furthermore, we may have to change our business model which may not be successful. If any of the above were to occur, our business, financial condition and results of operation could be materially and adversely affected.

There may be corrupt practices in the healthcare industry in China, which may place us at a competitive disadvantage if our competitors engage in such practices and may harm our reputation if our hospital partners and the medical personnel who work in our centers, over whom we have limited control, engage in such practices.

There may be corrupt practices in the healthcare industry in China. For example, in order to secure agreements with hospital partners or to increase direct sales of medical equipment or patient referrals, our competitors, other service providers or their personnel or equipment manufacturers may engage in corrupt practices in order to influence hospital personnel or other decision-makers in violation of the anti-corruption laws of China and the U.S. Foreign Corrupt Practices Act, or the FCPA. We have adopted a policy regarding compliance with the anti-corruption laws of China and the FCPA to prevent, detect and correct such corrupt practice.

9

Table of Contents

However, as competition persists and intensifies in our industry, we may lose potential hospital partners, patient referrals and other opportunities to the extent that our competitors engage in such practices or other illegal activities. In addition, our partner hospitals or the doctors or other medical personnel who work in our network of centers may engage in corrupt practices without our knowledge to procure the referral of patients to centers in our network. Although our policies prohibit such practices, we have limited control over the actions of our hospital partners or over the actions of the doctors and other medical personnel who work in our network of centers since they are not employed by us. If any of them were to engage in such illegal practices with respect to patient referrals or other matters, we or the centers in our network may be subject to sanctions or fines and our reputation could be adversely affected by any negative publicity stemming from such incidents.

We could also face increased exposure to liability claims at our specialty cancer hospitals, including claims for medical malpractice. We may need to obtain medical malpractice insurance and other types of insurance that we do not currently carry, each of which could increase our expenses and decrease our profitability. In addition, there can be no assurance that such insurance will be available at a reasonable price or that we will be able to maintain adequate levels of liability insurance coverage, if at all. In addition, our specialty cancer hospitals will also be required to obtain various quotas, permits and authorizations, which are currently the responsibility of our hospital partners under our existing agreements. See “—Risks Related to Our Industry—Healthcare administrative authorities in China currently set procurement quotas for certain types of medical equipment” and “—Risks Related to Our Industry—We or our hospital partners may be unable to obtain various permits and authorizations from regulatory authorities in China relating to our medical equipment, which could delay the installation or interrupt the operation of our equipment.”

Finally, if our plans change for any reason or the anticipated timetable or costs of development change for our specialty cancer hospitals, our business and future prospects may be negatively impacted. There can be no assurance that the planned specialty cancer hospitals will be completed or that, if completed, they will achieve sufficient patient cases to generate positive operating margins. In addition, as our currently planned specialty cancer hospitals are to be established through joint ventures with other parties, we also may not be successful in cooperating with such joint venture partners in operating our specialty cancer hospitals. See “—Risk Factors Related to Our Business —We may not be able to effectively manage the expansion of our operations through any new acquisitions or joint ventures, which we may not be able to successfully execute.”

We rely on the doctors and other medical professionals providing services in our network of centers to make proper clinical decisions and we rely on our hospital partners to maintain proper control over the clinical aspects of the operation of our network of centers.

We rely on the doctors and other medical professionals who work in our network to make proper clinical decisions regarding the diagnosis and treatment of their patients. Although we develop treatment protocols for doctors, provide periodic training for medical professionals in our network of centers on proper treatment procedures and techniques and host seminars and conferences to facilitate consultation among doctors providing services in our network of centers, we ultimately rely on our hospital partners to maintain proper control over the clinical activities of each center and over the doctors and other medical professionals who work in such centers. Any incorrect clinical decisions on the part of doctors and other medical professionals or any failure by our hospital partners to properly manage the clinical activities of each center may result in unsatisfactory treatment outcomes, patient injury or possibly death. Although part of the liability for any such incidents may rest with our partner hospitals and the doctors and other medical professionals they employ, we may be made a party to any such liability claim which, regardless of its merit or eventual outcome, could result in significant legal defense costs for us, harm our reputation, and otherwise have a material adverse effect on our business, financial condition and results of operations. The centers in our network have experienced claims as to a limited number of medical disputes since they commenced operations. Any expenses resulting from such liability claims are generally required to be accounted for as expenses of the relevant center, which could reduce our revenue derived from such center. We do not carry malpractice or other liability insurance at many of the centers in our network, and at those centers that do carry such insurance, it may not be sufficient to cover any potential liability that may result from such claims. For our specialty cancer hospitals that are currently under development, we will likely face direct liability claims for any such incidents.

Any failures or defects of the medical equipment in our network of centers or any failure of the medical personnel who work at the centers in our network to properly operate our medical equipment could subject us to liability claims and we may not have sufficient insurance to cover any potential liability.

Our business exposes us to liability risks that are inherent in the operation of complex medical equipment, which may contain defects or experience failures. We rely to a large degree on equipment manufacturers to provide technical training to the medical technicians who work in our network of centers on the proper operation of our complex medical systems. If such medical technicians are not properly and adequately trained by the equipment manufacturers or by us, they may misuse or ineffectively use the complex medical equipment in our network of centers. These medical technicians may also make errors in the operation of the complex medical equipment even if they are properly trained. Any medical equipment defects or failures or any failure of the medical personnel who work in the centers to properly operate the medical equipment could result in unsatisfactory treatment outcomes,

10

Table of Contents

patient injury or possibly death. Although the liability for any such incidents rests with the equipment manufacturers or the medical technicians, we may be made a party to any such liability claim which, regardless of its merit or eventual outcome, could result in significant legal defense costs for us, harm our reputation, and otherwise have a material adverse effect on our business, financial condition and results of operations. In addition, any expenses resulting from such liability claims may be accounted for as expenses of the center, which could reduce our revenue derived from such center. We do not carry product liability insurance at any of the centers in our network.

Any downtime for maintenance and repair of our medical equipment could lead to business interruptions that could be expensive and harmful to our reputation and to our business.

Significant downtime associated with the maintenance and repair of medical equipment used in our network of centers would result in the inability of the centers to provide radiotherapy treatment or diagnostic imaging services to patients in a timely manner. We primarily rely on equipment manufacturers or third party service companies for maintenance and repair services. The failure of manufacturers or third party service companies to provide timely repairs on our equipment could interrupt the operation of centers in our network for extended periods of time. Such extended downtime could result in lost revenues for us and our partner hospitals, dissatisfaction on the part of patients and our partner hospitals and damage to the reputation of the centers in our network, our partner hospitals and our company.

We rely on a limited number of equipment manufacturers.

Much of the medical equipment used in our network of centers is highly complex and is produced by a limited number of equipment manufacturers. These equipment manufacturers provide training on the proper operation of our medical equipment to the medical personnel who work in the centers in our network as well as maintenance and repair services for such equipment. Any disruption in the supply of the medical equipment or services from these manufacturers, including as a result of failure by any such manufacturers to obtain the requisite third-party consents and licenses for the intellectual property used in the equipment they manufacture, may delay the development of new centers or negatively affect the operation of existing centers and could have a material adverse effect on our business, financial condition and results of operations.

We may fail to protect our intellectual property rights or we may be exposed to misappropriation and infringement claims by third parties, either of which may have a material adverse effect as to our business.

We have applied for and obtained the registration of our trademark “Medstar” and nine other trademarks including “Concord Medical” in China to protect our corporate name. As of December 31, 2014, we also owned the rights to 178 domain names that we use in connection with the operation of our business. We believe that such domain names provide us with the opportunity to enhance our marketing efforts for the treatments and services provided in our network and enhance patients’ knowledge as to cancers, the benefits of radiotherapy and the various treatment options that are available. Our failure to protect our trademark or such domain names may undermine our marketing efforts and result in harm to our reputation and the growth of our business.

Furthermore, we cannot be certain that the equipment manufacturers from whom we purchase equipment have all requisite third-party consents and licenses for the intellectual property used in the equipment they manufacture. As a result, those equipment manufacturers may be exposed to risks associated with intellectual property infringement and misappropriation claims by third parties which, in turn, may subject us to claims that the equipment we have purchased infringes the intellectual property rights of third parties. We have in the past been subject to, and may in the future continue to be subject to, such claims by third parties. As a result, we may be named as a defendant in, or joined as a party to, any intellectual property infringement proceedings against equipment manufacturers relating to any equipment we have purchased. If a court determines that any equipment we have purchased from our equipment manufacturers infringes the intellectual property rights of any third party, we may be required to pay damages to such third party and the centers in our network may be prohibited from using such equipment, either of which could damage our reputation and have a material adverse effect on our business prospects, financial condition and results of operations. In addition, any such proceeding may also be costly to defend and may divert our management’s attention and other resources away from our business. Furthermore, the standard equipment purchase agreements that we enter into with our equipment manufacturers typically do not contain indemnification provisions for intellectual property claims. Although we have obtained specific indemnity from one equipment manufacturer for a patent infringement claim, there can be no assurance that we would be able to recover any damages, lost profits or litigation costs resulting from any intellectual property infringement claims or proceedings in which we are named as a party.

11

Table of Contents

We do not have insurance coverage for some of our medical equipment and do not carry any business interruption insurance.

Damage to, or the loss of, such uninsured equipment due to natural disasters, such as fires, floods or earthquakes, could have an adverse effect on our financial condition and results of operation. In addition, the operations in our network of centers may be particularly vulnerable to natural disasters that disrupt transportation since many patients travel long distances to reach such centers. Also, we do not have any business interruption insurance. Any business disruption could result in substantial expenses and diversion of resources and could have a material adverse effect on our business, financial condition and results of operations. For example, the strong earthquake that struck Sichuan Province in May 2008 resulted in the suspension of operations at three of our centers in Chengdu, the provincial capital of Sichuan Province, for approximately one month due to the diversion of hospital resources toward the treatment of earthquake victims.

Most of our radiotherapy and diagnostic imaging equipment contains radioactive materials or emits radiation during operation.

Most of the radiotherapy and diagnostic imaging equipment in our network of centers, including gamma knife systems, proton beam therapy systems, linear accelerators and PET-CT systems, contain radioactive materials or emit radiation during operation. Radiation and radioactive materials are extremely hazardous unless properly managed and contained. Any accident or malfunction that results in radiation contamination could cause significant harm to human beings and could subject us to significant legal expenses and result in harm to our reputation. Although equipment manufacturers and our hospital partners and their staff may bear some or all of the liability and costs associated with any accidents or malfunctions, if we are found to be liable in any way we may also face severe fines, legal reparations and possible suspension of our operating permits, all of which could have a material and adverse effect on our business, results of operations and financial condition. Also, certain of our medical equipment require the periodic replacement of their radioactive source materials. We do not directly oversee the handling of radioactive materials during the replacement or reloading process or during the disposal process, and any failure on the part of our hospital partners to handle or dispose of such radioactive materials in accordance with PRC laws and regulations may have an adverse effect on the operation of such centers.

12

Table of Contents

Any change in the regulations governing the use of medical data in China, which are still in development, could adversely affect our ability to use our medical data and could potentially subject us to liability for our past use of such medical data.

The centers in our network collect and store medical data from radiotherapy treatments for purposes of analysis, use in training doctors providing services in our network and improving the effectiveness of the treatments provided in our network of centers. In addition, doctors in our network utilize such medical data to conduct clinical research. We do not make any such medical data public and only keep such medical data for our internal use and for research purposes by doctors upon the approval of our medical affairs department and our hospital partners. Chinese regulations governing the use of such medical data are still in development but currently do not impose any restrictions on the internal use of such data by us as long as we have the permission of our hospital partners who have ownership of such data. Any change in the regulations governing the use of such medical data could adversely affect our ability to use such medical data and could subject us to liability for past use of such data, either of which could have a material adverse effect on our business, operations and financial results.

Our future high-end cancer hospitals will provide patients high-end medical services and medicines that are not covered by the national basic medical insurance, and as a result we may need to cooperate with commercial insurance companies and face risks in respect of charge fees and patients’ ability of payment.

Currently, the majority of patients in our network centers are covered under the national basic medical insurance. We settle the payment with the local medical insurance agencies on regular basis. However, our planned premium cancer hospitals will offer high-end radiotherapy and other services that will not be covered under the national basic medical insurance program. Our patients will be self-pay or covered under various commercial insurances. We need to negotiate with various insurance companies, both domestic and international, which would enroll our hospitals into their coverage. We cannot assure you that we can establish and manage the business relationship with insurance companies properly and effectively. Without the insurance coverage, our future revenue may not meet our forecasts and profitability will be adversely affected. We may also face collection risks as insurance companies may decide not to pay for certain clinical procedures or refuse to pay accordingly to our requests.

13

Table of Contents

With the rising conflicts between doctors and patients, if we cannot properly handle disputes in a timely manner with the patients, we will face the increasing risk of litigation.

Recently, there were more incidents of patient / doctor conflicts and litigations in China. Patients in China are demanding more higher-service quality of the medical services and treatments they receive from the hospitals. In our network centers, we also deal with patient disputes and litigations due to real or perceived medical incidents and practices. While we offer periodic training to all medical staff in our centers and hospitals, our patients may still raise issues with the treatment procedures, especially with cancer patients who experience higher than expected side-effects, sometimes resulting in unexpected deaths. While all of our centers are covered by medical malpractice insurance and we also purchased body-injury insurance for our medical staff, the process to reach a settlement, usually financial settlement under the medical malpractice insurance, is time-consuming and our management team needs to divert their attention from the normal operation of the centers and hospital. If we cannot properly handle the medical disputes in our centers, we may face increasing risks of litigation and our reputation among patients may be affected adversely.

The proper implementation of our strategy requires that we recruit, train and retain the doctors, specialists and other medical staff. If we cannot achieve the proper level of doctor recruitment and retention, our current and future hospitals’ business may be affected adversely.

The financial and operational performance of our planned premium cancer hospitals depend significantly on our ability to attract and retain quality doctors, nurses, hospital administrators and managers. Under the current regulatory environment of China, doctors and nurses are affiliated with various hospitals, whose professional registration and accreditation need the approval of hospitals they serve. The government policy is relaxing on the mobility of doctors and other medical professionals, such as the policy to allow “multiple-location practice” for doctors. However, the full enactment and implementation may take time and vary from region to region. In order to attract, train and retain a qualified team of doctors, nurses and hospital managers, we may need to offer compensation packages superior to those of government hospitals, provide more professional training opportunities, including overseas training and exchange, and include the medical team into our ESOP. All these measures may result in higher compensation and administrative expenses and therefore have an adverse effect on our financial and operational results.

Our business is subject to seasonality.

During a fiscal year, the first quarter usually sees fewest patient visits, both inpatient and outpatient, mainly due to the Chinese New Year. The fourth quarter is usually the busiest quarter during the year, as most patients, especially patients from the rural areas, will have more free time to visit hospitals. Since our network centers are located within the government hospitals, they are subjected to seasonality of the patient traffic as well. Our planned premium cancer hospitals will also be affected by seasonality, although to a lesser degree, as cancer patients need to receive treatment and diagnosis immediately. If we cannot manage and mitigate the seasonality effectively, our financial and operational results will be adversely affected.

14

Table of Contents

Our business depends substantially on the continuing efforts of our executive officers and other key personnel, and our business may be severely disrupted if we lose their services.

We depend on key members of our management team, which includes Dr. Jianyu Yang, chairman and our chief executive officer, Dr. Zheng Cheng, a director and our president, Mr. Adam Jigang Sun, our chief investment officer, Mr. Jing Zhang, our chief operating officer, Mr. Yaw Kong Yap, chief financial officer, as well as other key personnel for the continued growth of our business. The loss of any of these members of our management team or other key employees could delay the implementation of our business strategy and adversely affect our operations. Our future success will also depend in large part on our continued ability to attract and retain highly qualified management personnel. The process of hiring suitable, qualified personnel is often lengthy and such talented and highly qualified management personnel is often in short supply in China. If our recruitment and retention efforts are unsuccessful in the future, it may be more difficult for us to execute our business strategy. We cannot assure we can always make similar smooth transition if any executive officers or key personnel were to leave our company in the future. Although none of the key members of our management team is nearing retirement age in the near future and we are not aware of any current key members of our management team or other key personnel planning to retire or leave us, if one or more of such personnel are unable or unwilling to continue in their present positions, we may not be able to replace them readily, if at all. Consequently, our business may be severely disrupted, and we may incur additional expenses to recruit and retain new officers. In addition, we do not maintain key employee insurance. We have entered into employment agreements and confidentiality agreements with all of the key members of our management team and other key personnel. However, if any disputes arise between any of our key members of our management team or other key personnel and us, we cannot assure you, in light of uncertainties associated with the PRC legal system, the extent to which any of these agreements could be enforced in China, where all key members of our management team and other key personnel reside and hold some of their assets. See “—Risks Related to Doing Business in China—Uncertainties with respect to the PRC legal system could have a material adverse effect on us.”

Our articles of association contain anti-takeover provisions that could adversely affect the rights of holders of our ordinary shares and ADSs.

Our fourth amended and restated articles of association limit the ability of others to acquire control of our company or cause us to engage in change-of-control transactions. These provisions could have the effect of depriving our shareholders of an opportunity to sell their shares at a premium over prevailing market prices by discouraging third parties from seeking to obtain control of our company in a tender offer or similar transaction. For example, our board of directors has the authority, without further action by our shareholders, to issue preferred shares in one or more series and to fix their designations, powers, preferences, privileges, and relative participating, optional or special rights and the qualifications, limitations or restrictions, including dividend rights, conversion rights, voting rights, terms of redemption and liquidation preferences, any or all of which may be greater than the rights associated with our ordinary shares, in the form of ADS or otherwise. Preferred shares could be issued quickly with terms calculated to delay or prevent a change in control of our company or to make removal of management more difficult. If our board of directors issues preferred shares, the price of our ADSs may fall and the voting and other rights of the holders of our ordinary shares and ADSs may be adversely affected.

We may require additional funding to finance our operations, which financing may not be available on terms acceptable to us or at all, and if we are able to raise funds, the value of your investment in us may be negatively impacted.

Our business operations may require expenditures that exceed our available capital resources. To the extent that our funding requirements exceed our financial resources, we will be required to seek additional financing or to defer planned expenditures. There can be no assurance that we can obtain these bank loans or additional funds on terms acceptable to us, or at all. In addition, our ability to raise additional funds in the future is subject to a variety of uncertainties, including, but not limited to:

| • | our future financial condition, results of operations and cash flows; |

| • | general market conditions for capital raising and debt financing activities; and |

| • | economic, political and other conditions in China and elsewhere. |

15

Table of Contents

Furthermore, if we raise additional funds through equity or equity-linked financings, your equity interest in our company may be diluted. Alternatively, if we raise additional funds by incurring debt obligations, we may be subject to various covenants under the relevant debt instruments that may, among other things, restrict our ability to pay dividends or obtain additional financing. Servicing such debt obligations could also be burdensome to our operations. If we fail to service such debt obligations or are unable to comply with any of these covenants, we could be in default under such debt obligations and our liquidity and financial condition could be materially and adversely affected.

If we fail to comply with financial covenants under our loan agreements, our financial condition, results of operations and business prospects may be materially and adversely affected.

We have entered into and may in the future enter into loan agreements containing financial covenants that require us to maintain certain financial ratios. We may not be able to comply with some of those financial covenants from time to time. However, if we need to obtain waivers from lenders again in the future with respect to prepayment or to amend financial covenants or other relevant provisions under such loan agreements to address potential breaches, we cannot assure you that we would be able to reach agreements with the lenders to avoid a breach. If we are required to repay a significant portion or all of our existing indebtedness prior to their maturity, we may lack sufficient financial resources to do so. Furthermore, a breach of those financial covenants will also restrict our ability to pay dividends. Any of those events could have a material adverse effect on our financial condition, results of operations and business prospects.

We have granted security interests over certain of our medical equipment in order to secure bank borrowings. Any failure to satisfy our obligations under such borrowings could lead to the forced sale of such equipment.

In order to secure bank loans in an aggregate amount of RMB875.5 million, RMB1,086.2 million and RMB903.8 million (US$145.7 million) as of December 31, 2012, 2013 and 2014, respectively, we have granted security interests in equipment with a net carrying value of RMB205.3 million, RMB502.6 million and RMB164.9 million (US$26.6 million), respectively, representing 13.5%. 33.7% and 22.0% of the net value of our net property, plant and equipment of RMB1,522.9 million, RMB1,492.6 million and RMB749.7 million (US$120.8 million) as of December 31, 2012, 2013 and 2014, respectively. Any failure on our part to satisfy our obligations under these loans could lead to the forced sale of our medical equipment that secure these loans, the suspension of the operation of the centers in which such medical equipment is used, or otherwise damage our relationship with our hospital partners and our reputation in the medical community, all of which could have a material adverse effect on our business, financial condition and results of operation. We may grant additional security interests in our equipment in order to secure future bank borrowings.

If we fail to maintain an effective system of internal controls over our financial reporting, we may be unable to accurately report our financial results or prevent fraud, and investor confidence and the market price of our ADSs may, therefore, be adversely impacted.

We have successfully completed our Section 404 assessment for the year ended December 31, 2014 and received the auditor’s attestation. However, in the future, if we fail to maintain effective internal controls over financial reporting or to obtain an “unqualified” auditors’ attestation, our ability to accurately report our financial results may be impaired, which could adversely impact investor confidence and the market price of our ADSs.

Our business may be adversely affected by fluctuations in the value of the Renminbi as a significant portion of our capital expenditures relates to the purchase of medical equipment priced in U.S. dollars.

A significant portion of our capital expenditures relates to the purchase of radiotherapy and diagnostic imaging equipment from manufacturers outside of China. As the price of such equipment is denominated almost exclusively in U.S. dollars, any depreciation in the value of the Renminbi against the U.S. dollar could cause a significant increase our capital expenditures, reduce the profitability of our network of centers and have a material and adverse effect on our business, results of operations and financial condition.

16

Table of Contents

If we grant employee share options, restricted shares or other equity incentives in the future, our net income could be adversely affected.

We adopted our 2008 share incentive plan on October 16, 2008, which was subsequently amended on November 17, 2009. We are required to account for share-based compensation in accordance with ASC 718, Compensation-Stock Compensation, which requires a company to recognize, as an expense, the fair value of share options and other equity incentives to employees based on the fair value of equity awards on the date of the grant, with the compensation expense recognized over the period in which the recipient is required to provide service in exchange for the equity award. On November 27, 2009 and September 30, 2011, we granted options to purchase 4,765,800 ordinary shares at an exercise price of US$3.67 and US$2.17 per share, respectively, under our 2008 share incentive plan to our directors and employees. We did not grant any option under our 2008 share incentive plan in 2012 and 2013. On February 18, 2014, we granted option to purchase 3,479,604 ordinary shares at an exercise price of US$2.037 per share. We also granted 1,370,250 restricted shares, 21,132 restricted shares and 69,564 restricted shares, respectively, on February 18, 2014, July 1, 2014 and August 1, 2014 to certain directors, officers and employees. We granted share options in 2007, before adopting our 2008 share incentive plan, to certain executive officers that were subsequently exercised in 2008. As a result, we have incurred share-based compensation expenses of RMB9.1 million in 2012, RMB8.8 million in 2013 and RMB7.4 million (US$1.2 million) in 2014 related to such options. If we grant more options, restricted shares or other equity incentives in the future, we could incur significant compensation charges and our results of operations could be adversely affected.

We are a Cayman Islands company and, because judicial precedent regarding the rights of shareholders is more limited under Cayman Islands law than that under U.S. law, you may have less protection for your shareholder rights than you would under U.S. law.

Our corporate affairs are governed by our memorandum and articles of association, as amended and restated from time to time, the Companies Law (as amended) of the Cayman Islands and the common law of the Cayman Islands. The rights of shareholders to take action against the directors, actions by minority shareholders and the fiduciary responsibilities of our directors to us under Cayman Islands law are to a large extent governed by the common law of the Cayman Islands. The common law of the Cayman Islands is derived in part from comparatively limited judicial precedent in the Cayman Islands as well as from English common law, which has persuasive, but not binding, authority on a court in the Cayman Islands. The rights of our shareholders and the fiduciary responsibilities of our directors under Cayman Islands law are not as clearly established as they would be under statutes or judicial precedent in some jurisdictions in the United States. In particular, the Cayman Islands has a less developed body of securities laws than the United States. In addition, some U.S. states, such as Delaware, have more fully developed and judicially interpreted bodies of corporate law than the Cayman Islands.