UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 20-F

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2012

Commission File Number: 001- 34429

PAMPA ENERGíA S.A.

(Exact name of registrant as specified in its charter)

Pampa Energy Inc.

(Translation of registrant’s name into English)

Argentina

(Jurisdiction of incorporation or organization)

Ortiz de Ocampo 3302, Building #4

C1425DSR, City of Buenos Aires

Argentina

(Address of principal executive offices)

Romina Benvenuti

Ortiz de Ocampo 3302, Building #4

C1425DSR, City of Buenos Aires

Argentina

Tel.: + 54 11 4809 9500 / Fax: + 54 11 4809 9555

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Name of each exchange |

|

Common Stock American Depositary Shares, each representing 25 shares of common stock, par value Ps. 1.00 per share |

New York Stock Exchange* New York Stock Exchange |

|

* Not for trading, but only in connection with the registration of American Depositary Shares, pursuant to the requirements of the Securities and Exchange Commission. | |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

|

1,314,310,895 shares of common stock, par value Ps. 1.00 per share |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

¨Yes |

xNo |

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

|

¨Yes |

xNo |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

|

xYes |

¨No |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large Accelerated filer ¨ |

Accelerated filer x |

Non-accelerated filer ¨ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP ¨ |

International Financial Reporting Standards as issued by the International Accounting Standards Board x |

Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

|

¨Item 17 |

¨Item 18 |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

|

¨ Yes |

x No |

TABLE OF CONTENTS

| PART I | ||

| Item 1. | Identity of Directors, Senior Management and Advisors | 7 |

| Item 2. | Offer Statistics and Expected Timetable | 7 |

| Item 3. | Key Information | 7 |

| Selected Financial Data | 7 | |

| Exchange Rates | 11 | |

| Risk Factors | 12 | |

| Item 4. | Information on the Company | 38 |

| History and Development of the Company | 38 | |

| Our Business | 38 | |

| The Argentine Electricity Sector | 83 | |

| Item 4A. | Unresolved Staff Comments | 99 |

| Item 5. | Operating and Financial Review and Prospects | 99 |

| Item 6. | Directors, Senior Management and Employees | 175 |

| Item 7. | Major Shareholders and Related Party Transactions | 188 |

| Item 8. | Financial Information | 190 |

| Consolidated Financial Statements | 190 | |

| Legal Proceedings | 190 | |

| Dividends | 195 | |

| Item 9. | The Offer and Listing | 196 |

| Trading History | 196 | |

| The Argentine Securities Market | 198 | |

| Item 10. | Additional Information | 201 |

| Memorandum and Articles of Association | 201 | |

| Material Contracts | 201 | |

| Exchange Controls | 201 | |

| Taxation | 203 | |

| Dividends and Paying Agents | 207 | |

| Documents on Display | 208 | |

| Item 11. | Quantitative and Qualitative Disclosures about Market Risk | 209 |

| Item 12. | Description of Securities Other than Equity Securities | 212 |

| Description of American Depositary Shares | 212 | |

| PART II | ||

| Item 13. | Defaults, Dividend Arrearages and Delinquencies | 214 |

| Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | 214 |

| Item 15. | Controls and Procedures | 214 |

| Item 16A. | Audit Committee Financial Expert | 215 |

| Item 16B. | Code of Ethics | 215 |

| Item 16C. | Principal Accountant Fees and Services | 215 |

| Item 16D. | Exemptions from the Listing Standards for Audit Committees | 216 |

| Item 16E. | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 216 |

| Item 16F. | Change in Registrant’s Certifying Accountant | 217 |

| Item 16G. | Corporate Governance | 217 |

| Item 16 H. | Mine Safety Disclosure | 222 |

| PART III | ||

| Item 17. | Financial Statements | 223 |

| Item 18. | Financial Statements | 223 |

| Item 19. | Exhibits | 223 |

| Index to Financial Statements | F1 | |

|

i |

|

PRESENTATION OF INFORMATION

In this annual report, we use the terms “we,” “us,” “our,” the “registrant” and the “Company” to refer to Pampa Energía S.A.

Financial Information

This annual report contains our audited consolidated financial statements as of December 31, 2012, December 31, 2011 and January 1, 2011, and for the years ended December 31, 2012 and 2011, and the notes thereto (the “Consolidated Financial Statements”). The Consolidated Financial Statements have been audited by Price Waterhouse & Co. S.R.L., member firm of PricewaterhouseCoopers network, whose report is included in this annual report.

Our Consolidated Financial Statements are set forth in Item 18 beginning on page F-1 of this annual report. Our Consolidated Financial Statements are prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (the “IASB”) and have been approved by resolution of the Board of Directors’ meeting of the Company held on March 8, 2013.

Significant Acquisitions

We started acquiring our principal generation, transmission, distribution and other core assets in 2006. Before these acquisitions, we did not have any operations or engage in any activities, as our former business activities, which were limited to the ownership and operation of a cold storage warehouse building, were suspended in 2003. Accordingly, prior to the second half of 2006, we have had no relevant operating history, comparable financial statements or business track record that might constitute a basis for comparing or evaluating the performance of our operations or business prospects following our recent acquisitions.

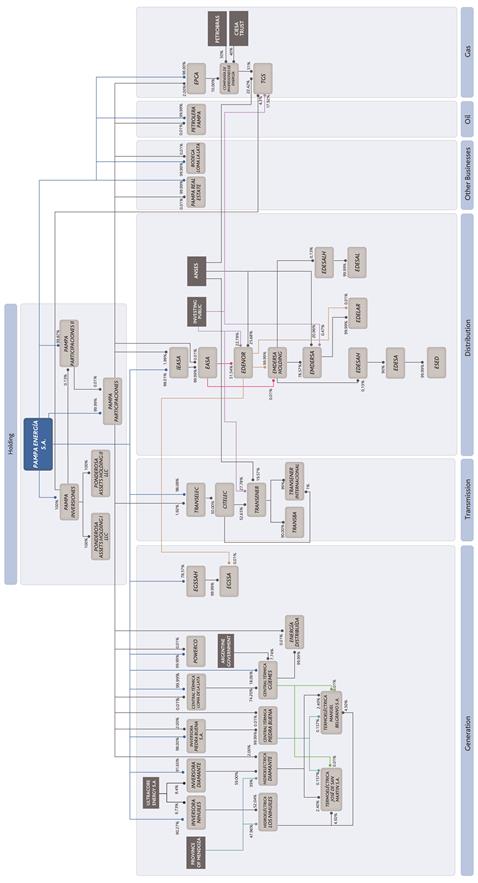

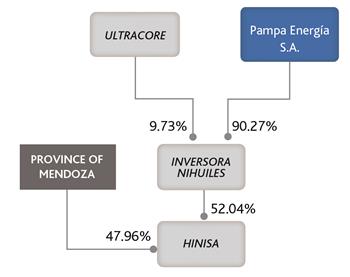

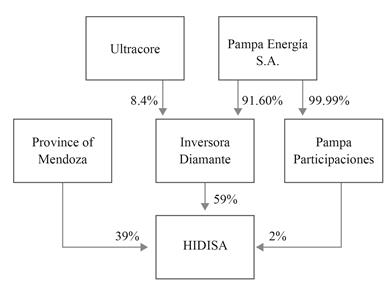

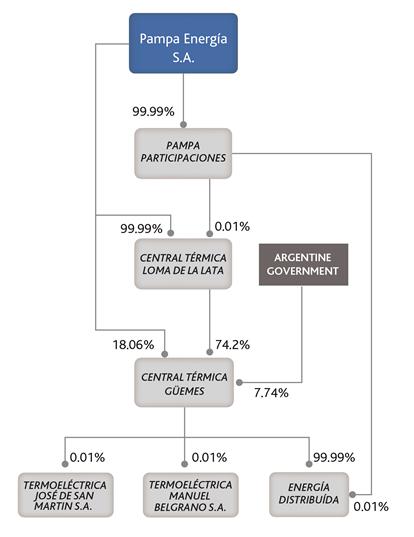

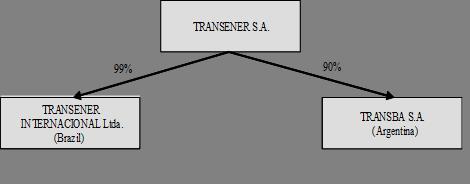

Our significant acquisitions include Electricidad Argentina S.A. (“EASA”) in September 2007, which owns a controlling stake in our distribution subsidiary, Empresa Distribuidora y Comercializadora Norte S.A. (“Edenor”); Corporación Independiente de Energía S.A. (“CIE”) in August 2007 (now known as Inversora Piedra Buena S.A. or “IPB”), which owns our subsidiary Central Piedra Buena S.A. (“Piedra Buena”) generation facilities; the assets comprising Central Térmica Loma de la Lata S.A. (“Loma de la Lata” or “CTLL”) in May 2007; Pampa Inversiones S.A. (“PISA”) in January 2007; a direct interest in Central Térmica Güemes S.A. (“Güemes”); a direct interest in Inversora Nihuiles S.A. (“Nihuiles”) and Inversora Diamante S.A. (“Diamante”) in October 2006, which in turn own our two hydroelectric generation plants Hidroeléctrica Nihuiles (“HINISA”) and Hidroeléctrica Diamante (“HIDISA”), respectively, a direct interest in Petrolera Pampa S.A. (“Petrolera Pampa”) in February 2009; and a co-controlling interest in Compañía Inversora en Transmisión Eléctrica Citelec S.A. (“Citelec”) in September 2006, which owns a controlling stake in Compañía de Transporte de Energía Eléctrica en Alta Tensión S.A. (“Transener”).

Recent Developments

Since 2011, Edenor has taken action to divest certain assets consisting of former subsidiaries of Empresa Distribuidora Eléctrica Regional S.A. (“EMDERSA”), a company engaged in the distribution of electricity in the Argentine provinces of San Luis, La Rioja and Salta, and AESEBA S.A. (“AESEBA”).

Spin-off Process – EMDERSA

In order to carry out the sale of certain of EMDERSA’s former subsidiaries, Edenor, the controlling company of EMDERSA, was required to cause EMDERSA to complete a partial spin-off process (the “Spin-off Process”), which resulted in the creation of three new investment companies, (i) EDESAL Holding S.A. (“EDESALH”), holder of 99.99% of the capital stock and votes of Empresa Distribuidora San Luis S.A. (“EDESAL”), (ii) EDESA Holding S.A. (“EDESAH”), holder of 90% of the capital stock and votes of Empresa Distribuidora de Electricidad de Salta S.A. (“EDESA”), and (iii) EGSSA Holding (“EGSSAH”), holder of 99.99% of EGGSA’s capital stock and votes. EMDERSA was to retain 99.99% of the capital stock and voting rights in EDELAR. On December 16, 2011, at EMDERSA’s Extraordinary General Shareholders’ Meeting, which was resumed on January 13, 2012 after a recess, the Spin-off Process was approved.

|

|

2 |

|

The Spin-off Process has also been approved by the Comisión Nacional de Valores (the National Securities Commission, or “CNV”) and registered with the Regulatory Agency of Corporations (the “IGJ”), together with the registration of the three new companies. On November 8, 2012, the new companies were authorized by the National Securities Commission to go public, and they obtained admission to listing on the Bolsa de Comercio de Buenos Aires (the Buenos Aires Stock Exchange).

Companies’ sale agreements

Edenor’s Board of Directors approved at different times the offer letters received for the carrying out of the following transactions:

· From Rovella Carranza S.A. (“Rovella”), for the acquisition of Edenor’s direct and indirect stake in EDESAL (the “EDESAL Sale”).

· From Salta Inversiones Eléctricas S.A. (“SIESA”), for the acquisition of Edenor’s direct and indirect stake in EDESA (the “EDESA Sale”)

· From the Company, for the acquisition of Edenor’s direct and indirect stake in EGSSA (the “EGSSA Acquisition”).

EDESAL Sale

On September 16, 2011, Edenor’s Board of Directors approved the offer for the acquisition of 78.44% of the capital stock and votes of EDESALH by Rovella for a total and final price of U.S.$ 26.7 million that was paid in two installments. The first of them, for U.S.$ 4.0 million, was paid three days after the acceptance of the offer, and the remaining balance was collected by Edenor on October 25, 2011.

Along with the payment of the balance in October 2011, EDESAL also repaid a financial loan granted by the Edenor to EDESAL for an amount of Ps. 37.5 million, plus interest accrued through the settlement date.

EDESA Sale

On April 23, 2012, Edenor’s Board of Directors accepted the offer made by Salta Inversiones Eléctricas S.A. (“SIESA”) to Edenor and its subsidiary EMDERSA Holding S.A. (“EMDERSAH”), for the acquisition of shares representing: (i) 78.44% of the capital stock and voting rights of EDESAH, holder of 90% of the capital stock and voting rights of EDESA, which in turn owns 99.99% of the capital stock and voting rights of Empresa de Sistemas Eléctricos Dispersos S.A. (ESED), and (ii) the remaining 0.01% of ESED.

The transaction was carried out on May 10, 2012 at the offered price payable through the delivery of Argentine sovereign debt bonds (Boden 2012) for a value equivalent to Ps. 100.5 million. Such price was partially cancelled through the payment of Ps. 83.8 million, and the remainder will be cancelled in five annual and consecutive installments in U.S. dollars, with the first of them falling due on May 5, 2013, at an interest rate of LIBOR plus a 2% margin.

As a part of this transaction, EDESA also cancelled in full a loan held with Edenor for an amount of Ps. 131.3 million plus accrued interest, and the purchaser released EMDERSA from any and all liability resulting from the surety granted by the latter to EDESA in connection with a syndicated loan held by that company with multiple banking entities.

As collateral for the payment of the price of the EDESA Sale, SIESA granted a second lien share pledge over 23.53% of the shares of EDESA in favor of Edenor.

EGSSA Acquisition

On October 3, 2011, the Company sent to Edenor an offer to buy 78.57% of the shares and votes of EGSSAH together with 0.01% of EGSSA’s capital stock held by Edenor. On October 11, 2011, Edenor’s Board of Directors approved such offer.

The total and final agreed-upon price for this transaction amounts to U.S.$ 10.8 million, to be paid in two installments. The first of them, for an amount of U.S.$ 2.2 million was made on October 31, 2011 as partial payment of the price, and the remaining balance will have to be paid in October 2013. The latter amount will accrue interest at an annual rate of 9.75%, payable semi-annually.

|

|

3 |

|

EDELAR Offer

An offer from Andes Energía Argentina S.A. (“Andes Energía”) was accepted by Edenor’s board of directors on September 16, 2011, pursuant to which a proposal was made for Andes Energía to acquire a purchase option for a price of U.S. $1.5 million to buy, if the Spin-off Process was completed within a term of two years, 78.44% of Edenor’s direct and indirect stake in EDELAR for U.S. $20.29 million, to be paid in two installments. The purchase option was paid for by the buyer on September 16, 2011.

Subsequently, Edenor’s board of directors approved proposals from Andes Energía to extend the term during which the buyer could exercise the option, with Edenor retaining the right to freely sell or assign to any third party or cause the sale or assignment of some or all the shares that are the object of the transaction and/or the rights over such shares. In the event that a sale to a third party is made, Andes Energía option may not be exercised, there being no outstanding payment or any responsibility of any kind for Edenor or Andes Energía.

On December 31, 2012, the Andes Energía purchase option had expired. As of the date of this annual report, Edenor is currently negotiating with Andes Energía new terms and conditions. At the same time, Edenor has received other expressions of interests in connection with such assets from third parties, which are currently being analyzed, although no specific offers have yet been received.

Taking into consideration that Edenor still intends to sell these assets and that it has received other expressions of interests in connection therewith, such assets continue to be classified as assets available for sale.

AESEBA and EDEN Sale

On February 27, 2013, Edenor’s Board of Directors unanimously approved an offer sent by Servicios Eléctricos Norte BA S.L. (the “Buyer”) for (i) the acquisition of the shares representing 100% of the capital stock and voting rights of AESEBA, an electric utility company, which owns 90% of the outstanding capital stock of Empresa Distribuidora de Energía Norte S.A. (“EDEN”), an electricity distribution company holding the concession area in the north region of the Province of Buenos Aires; and (ii) the assignment of certain credits that EASA (the controlling company of Edenor) had with EDEN. The price offered by the Buyer has been paid through the assignment to Edenor of certain rights under a trust established for purposes of the transaction to receive debt securities of Edenor, in an amount equivalent, as of the date of the acceptance of the offer, to U.S.$85 million face value, which are to be cancelled by Edenor as such bonds are released to it in accordance with the terms and conditions of the trust. As part of the transaction, and in order to guarantee the obtention of funds necessary to acquire the Edenor bonds to be received by such company, U.S.$8.5 million of Argentine sovereign debt bonds multiplied by a certain factor was to be deposited into the trust on or before April 30, 2013. As collateral for the portion of the price to be paid at that later date, the Buyer granted a pledge over 30% of the shares of AESEBA. On April 5, 2013 the transaction was settled in accordance with the terms described above.

Others

On January 27, 2011, we also acquired from AEI and through our subsidiary Pampa Inversiones S.A., all of the issued and outstanding capital stock of Inversiones Argentina I, a company incorporated in the Cayman Islands to which AEI had previously assigned all of its right, title and interest to U.S.$ 199.6 million nominal value of the floating rate notes due April 22, 2002, issued by Compañía de Inversiones de Energía S.A. (“CIESA”) on April 22, 1997 (the “CIESA Bonds”), other liabilities of CIESA arising from two derivatives transactions (together with the CIESA Bonds, the “CIESA Liabilities”) and the rights over certain lawsuits related to the CIESA Bonds. The CIESA Bonds have been in default since a missed principal repayment due on April 22, 2002. Pampa acquired the capital stock of Inversiones Argentina I for U.S.$ 136 million, while the assets of such company, including the CIESA Bonds and accrued and unpaid interest, had a total value of approximately U.S.$ 322 million. CIESA is the controlling company of Transportadora de Gas del Sur (“TGS”). TGS is a leading gas transportation company in Argentina. TGS is also one of the leading natural gas liquid producers and traders, and an important provider of midstream services, including business structuring, turnkey construction and operation and maintenance of facilities used for gas storage, conditioning and transportation. On April 8, 2011, we acquired, directly and indirectly, 100% of the capital stock of Enron Pipeline Company Argentina S.A. (now known as EPCA S.A. or “EPCA”), which owns 10% of the capital stock of CIESA, which in turn owns 55.3% of the share capital of TGS, for a total price of U.S.$ 29.0 million.

|

|

4 |

|

In connection with the acquisition of the CIESA Bonds and the other assets related to CIESA described above, on April 28, 2011, the Company and its subsidiaries Inversiones Argentina I, Pampa Inversiones S.A. and EPCA entered into an agreement (the “Acta Acuerdo”) with Petrobras Energía S.A., Petrobras Hispano S.A., and CIESA, pursuant to which the parties thereto agreed to (i) continue negotiating to reach an agreement to re-implement the restructuring of the CIESA Liabilities, (ii) cause CIESA to vote in favor of a dividend payment by TGS in an amount of approximately U.S.$ 239 million (the “TGS Dividend”), which was declared by the shareholders’ meeting of TGS on April 29, 2011 and (iii) set up a trust (the “MSA Trust”) to hold CIESA’s pro rata portion of the TGS Dividend which, to the extent the restructuring of the CIESA Liabilities is completed, will be distributed as follows: (x) an amount equal to 4.3% of the TGS Dividend will be distributed to the Company (or its designee) and (y) the remainder, net of CIESA operating expenses for fiscal year 2011, will be distributed to the shareholders of CIESA following the restructuring of the CIESA Liabilities pro rata to their respective holding in CIESA. To the extent the restructuring of the CIESA Liabilities is not achieved as agreed by the parties to the Acta Acuerdo, the pro rata portion of the TGS Dividend held in trust shall be distributed to CIESA.

On May 10, 2011, we entered into a Memorandum of Understanding (the “MOU”) with Inversiones Argentina I, Pampa Inversiones S.A., EPCA, Petrobras Energía S.A., Petrobras Hispano Argentina S.A. and CIESA, in which the parties to the MOU agreed: (i) to suspend (“standstill”) until May 10, 2012, the action captioned “Compañía de Inversiones de Energía S.A. v. AEI, AEI v. Compañía de Inversiones de Energía S.A., Petrobras Energía S.A., Petrobras Hispano Argentina S.A., Héctor Daniel Casal, Claudio Fontes Nunes and Rigoberto Mejía Aravena” (the “CIESA Action”), pending before the Supreme Court of the State of New York (Index No. 600245/09E), and to make best efforts to re-implement (x) the financial restructuring set forth in the Restructuring Agreement executed on September 1, 2005 among CIESA, Petrobras Energía S.A., Petrobras Hispano Argentina S.A., EPCA, ABN AMRO Bank N.V. Argentine branch (acting in its capacity as trustee) and the financial creditors of CIESA, as amended from time to time (the “Restructuring Agreement”), regarding the CIESA Bonds and (y) two derivatives transactions originally executed between CIESA and J. Aron & Company on August 3, 2000, and between CIESA and Morgan Guaranty Trust Company of New York on August 4, 2000, respectively. Following the execution of the MOU we have become a party to the Restructuring Agreement. The foregoing is subject to obtaining the necessary governmental approvals to (i) implement the Restructuring Agreement; and (ii) timely withdraw all the claims and actions relating to the CIESA Action.

As the Argentine antitrust approval required to implement the Restructuring Agreement had not been obtained and the parties did not agree to extend either the MOU that expired on May 11, 2012 or the CIESA Action, on July 13, 2012, the parties to the Restructuring Agreement, including the Company, entered into a Fifth Amendment to the Restructuring Agreement pursuant to which (i) in exchange for U.S.$ 46,033,917 principal amount of debt owed to Pampa Inversiones, CIESA irrevocably designated and appointed Pampa Inversiones as sole and exclusive beneficiary of the two hundred fifty five million, five hundred twenty seven thousand, four hundred seventy seven (255,527,477) CIESA shares and, accordingly, Pampa Inversiones became the sole “Beneficiario” and “Fideicomisario” under the MSA Trust; and (ii) CIESA assigned to Pampa Inversiones any rights it might otherwise retain for having been a “Beneficiario” and “Fideicomisario” under the MSA Trust to instruct the MSA trustee and to receive any proceeds of the Bienes Fideicomitidos. Also, all actions to be taken in case the governmental approvals are obtained were established under the above mentioned agreement.

Additionally, on July 13, 2012, Petrobras Argentina S.A., Petrobras Hispano Argentina S.A., the Company, Pampa Inversiones and Inversiones Argentina I entered into a Settlement Agreement (the “Settlement Agreement”) with the intention to terminate and extinguish to the fullest extent permitted by law the CIESA Action and to mutually release each other from all claims and actions in such CIESA Action. On October 25, 2012, the conditions to which the Settlement Agreement was subject were satisfied, thus terminating and extinguishing the CIESA Action.

Pursuant to the Settlement Agreement and as a condition thereto, the above mentioned parties totally cancelled all of CIESA’s debt due and outstanding since the year 2002. As compensation, PISA received from CIESA: (i) ownership of 34,133,200 ordinary Class B shares issued by TGS, representing 4.3% of the capital stock and voting rights in TGS; (ii) a payment of U.S.$ 86,997,232; and (iii) the appointment of PISA as beneficiary and trustee under the Trust Agreement dated August 29, 2005, pursuant to which The Royal Bank of Scotland, Argentine branch, holds in trust 40% of CIESA’s shares (the “Shares held in Trust”). Consequently, once the pending governmental approval has been obtained, the Shares held in Trust will be transferred to Pampa pursuant to the terms of the Restructuring Agreement executed by CIESA and its financial creditors, as amended.Pursuant to a Call Option Agreement (the “Call Option Agreement”) dated March 11, 2001,entered into by and among the Company, Inversiones Argentina II and GEB Corp. (parent company of Inversiones Argentina II), on such date, the Company purchased an option for U.S.$ 1.0 million, exercisable at any time during a period of 18 months thereafter, to acquire either (i) the rights over the lawsuit initiated by Ponderosa Assets L.P. and Enron Creditors Recovery Corp. (the “Arbitration”) against the Republic of Argentina before the International Centre for Settlement of Investment Disputes (the “ICSID”) of the World Bank (the “ICSID Claim”) for freezing and pesifing U.S. dollar-based gas transportation tariffs in violation of certain provisions of the bilateral investment treaty between the United States and Argentina (See “Item 3. Key Information -Risk Factors – Our Generation Business”) or, (ii) at the Company’s option, all of the issued and outstanding capital stock of Inversiones Argentina II. On October 7, 2011 the Company exercised the option and, therefore, in consideration of the amount of U.S.$ 25 million acquired the rights over the ICSID Claim (and therefore not the capital stock of Inversiones Argentina II) to control, suspend and waive the Arbitration proceedings against the Republic of Argentina pursuant to the Call Option Agreement.

|

|

5 |

|

On July 31, 2012, the ICSID Arbitration Court ordered, in accordance with the instructions timely given by the Company, the suspension of the arbitration proceeding brought by the Plaintiffs against the Republic of Argentina originally involving an amount in dispute which would currently amount to approximately U.S.$ 167 million.

Such suspension was requested pursuant to the commitment undertaken with the Argentine Antitrust Commission and the ENERGAS by CIESA, EPCA, Petrobras and the Company on August 29, 2011, in the filings submitted before both entities seeking the approval of CIESA’s Restructuring Agreement. In this respect, the corresponding governmental approvals have not yet been granted as of the date of this annual report.

In connection with the above mentioned claims, on November 20, 2012, Ponderosa Assets Holding I LLC and Ponderosa Assets Holding II LLC (two new subsidiaries of Pampa Inversiones specially created for this transaction) entered into an assignment agreement with Enron Creditors Recovery Corp., Citicorp North America, Inc., Atlantic Commercial Finance, Inc., Enron Global Power & Pipelines L.L.C., and Citibank N.A., pursuant to which (i) Enron Creditors Recovery Corp. transferred all of its right, title and interest in and to the general partnership interest in Ponderosa Assets LP to Ponderosa Assets Holding I LLC, and (ii) each of Citicorp North America, Inc., Atlantic Commercial Finance, Inc., Enron Global Power & Pipelines L.L.C. and any other relevant affiliate of Enron Creditors Recovery Corp. transferred all of its right, title and interest in and to the limited partnership interests in Ponderosa Assets LP to Ponderosa Assets Holding II LLC; therefore, Ponderosa Assets Holding I LLC and Ponderosa Assets Holding II LLC became the owners of Ponderosa Assets LP, which is the formal plaintiff under the ICSID Claim.

Furthermore, on December 30, 2011 the board directors of the Company, after entering into negotiations with Pampa Generación S.A., Inversora Ingentis S.A. and Powerco S.A. (“Powerco”) (in the case of Powerco the negotiations took place only in respect of the assets and liabilities related to its investment business) resolved that it would be beneficial for these companies if they were merged into a single company. The purpose of this merger is to optimize the resources of each of the companies by simplifying and consolidating their administrative and operational structure. On March 9, 2012, and in connection with the required procedures, the Company’s board of directors approved the special financial statements for merger purposes of the Company, the preliminary merger agreement executed among the Company, Pampa Generación S.A., Inversora Ingentis S.A. and Powerco, and the offering memorandum that describes the terms and conditions of the merger. On April 27, 2012, a shareholders meeting took place, where the merger as well as all of the documentation relating to it were approved. Finally, on July 13, 2012, the special financial statements for merger purposes were issued. On September 13, 2012, through Resolution No. 16,903, the CNV approved the corporate reorganization described above and referred the case to the IGJ for registration. As of the date of this annual report, such IGJ approval is still pending.

Functional and Presentation Currency

The Company and its subsidiaries maintain their accounting records and prepare their financial statements in Argentine Pesos, which is their functional currency. Our subsidiary PISA, however, maintains its accounting records and prepares its financial statements in Uruguayan Pesos. Our Consolidated Financial Statements include the results of this subsidiary translated into Argentine Pesos. Assets and liabilities are translated at year-end exchange rates, and revenue and expense accounts at average exchange rates for the year. Certain financial information contained in this annual report has been presented in U.S. dollars .

Rounding

Certain figures included in this annual report (including percentage amounts) have been subject to rounding adjustments. Accordingly, figures shown as totals may not sum.

|

|

6 |

|

Exchange Rate

In this annual report, except as otherwise specified, references to “U.S. $” and “Dollars” are to U.S. Dollars, and references to “Ps.” and “Pesos” are to Argentine Pesos. Solely for the convenience of the reader, we have converted certain amounts included in “Item 3. Key Information” and elsewhere in this annual report from Pesos into U.S. Dollars using, for the information provided as of December 31, 2012, the seller exchange rate reported by the Banco de la Nación Argentina, or Banco Nación, as of December 31, 2012 of U.S. $1.00 = Ps. 4.9180, unless otherwise indicated. These conversions should not be considered representations that any such amounts have been, could have been or could be converted into U.S. Dollars at that or at any other exchange rate. The Federal Reserve Bank of New York does not report a noon buying rate for Pesos. For more information regarding historical exchange rates, see “Item 3. Key Information-Exchange Rates.”

FORWARD-LOOKING STATEMENTS

This annual report contains estimates and forward-looking statements, principally in “Item 3. Key Information-Risk Factors,” “Item 4. Information on the Company—Our Business” and “Item 5. Operating and Financial Review and Prospects.” Some of the matters discussed concerning our business operations and financial performance include estimates and forward-looking statements within the meaning of the U.S. Securities Act of 1933, as amended (the “Securities Act”) and the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Our estimates and forward-looking statements are mainly based on our current expectations and estimates on future events and trends that affect or may affect our businesses and results of operations. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to several risks and uncertainties and are made in light of information currently available to us.

Our estimates and forward-looking statements may be influenced by the following factors, among others:

· our ability to arrange financing under reasonable terms;

· the outcome and timing of the tariff renegotiation process of our regulated businesses and uncertainties relating to future government approvals to increase or otherwise adjust such tariffs;

· changes in the laws and regulations applicable to energy and electricity and oil and gas sectors in Argentina;

· government interventions, resulting in changes in the economy, taxes, tariffs or regulatory framework, or in the delay or withholding of governmental approvals;

· general economic, social and political conditions in Argentina, and other regions where we or our subsidiaries operate, such as the rate of economic growth, fluctuations in exchange rates of the Peso or inflation;

· restrictions on the ability to exchange Pesos into foreign currencies or to transfer funds abroad;

· competition in the electricity, public utility services and related industries;

· the impact of high rates of inflation on our costs;

· deterioration in regional and national business and economic conditions in Argentina; and

· other risks factors discussed under “Item 3. Key Information—Risk Factors.”

|

|

7 |

|

The words “believe,” “may,” “will,” “aim,” “estimate,” “continue,” “anticipate,” “intend,” “expect” and similar words are intended to identify estimates and forward-looking statements. Estimates and forward-looking statements speak only as of the date they were made, and we undertake no obligation to update or to renew any estimates and/or forward-looking statements because of new information, future events or other factors. Estimates and forward-looking statements involve risks and uncertainties and are not guarantees of future performance. Our future results may differ materially from those expressed in these estimates and forward-looking statements. In light of the risks and uncertainties described above, the estimates and forward-looking statements discussed in this annual report might not occur and our future results and our performance may differ materially from those expressed in these forward-looking statements due to, factors including, but not limited to, those mentioned above.

|

|

8 |

|

PART I

Item 1. Identity of Directors, Senior Management and Advisors

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

SELECTED FINANCIAL DATA

The following table presents our summary financial data for each of the years in the two-year period ended December 31, 2012. The selected consolidated income statement data and cash flow data for the years ended December 31, 2012 and 2011 and the selected consolidated balance sheet data as of December 31, 2012, December 31 and January 1, 2011 have been prepared in accordance with IFRS as issued by the IASB and have been derived from our Consolidated Financial Statements included elsewhere in this annual report. Our audited consolidated financial statements as of December 31, 2011 and for the year then ended, which have been prepared for comparison purposes with our financial information as of December 31, 2012 and for the year then ended, are the first annual audited financial statements of the Company that are fully compliant with IFRS, as issued by the IASB. Our consolidated financial statements for periods before the year ended December 31, 2011 have only been prepared in accordance with accounting principles generally accepted in Argentina (“Argentine GAAP”).

The mandatory adoption of IFRS for public companies in Argentina became effective for fiscal years beginning January 1, 2012 You should read the information below in conjunction with our Consolidated Financial Statements, including the notes thereto, as well as the sections “Presentation of Financial Information” and “Item 5. Operating and Financial Review and Prospects”.

|

|

9 |

|

|

At December 31, |

At January, 1 | |||||||||||

|

2012 |

2012 |

|

2011 |

2011 | ||||||||

|

(U.S. Dollars) (1) |

(Pesos) |

|

(Pesos) |

| ||||||||

|

BALANCE SHEET DATA |

||||||||||||

|

Non-current assets: |

||||||||||||

|

Properties, plant and equipment |

U.S.$ |

1,229,870 |

Ps. |

6,023,903 |

Ps. |

5,847,072 |

>Ps. |

5,925,219 | ||||

|

Intangible assets |

369,235 |

|

1,808,511 |

|

1,791,802 |

977,741 | ||||||

|

Biological assets |

403 |

|

1,976 |

|

1,936 |

- | ||||||

|

Investments in joint ventures |

39,264 |

|

192,316 |

|

222,220 |

239,223 | ||||||

|

Investments in associates |

27,061 |

|

132,546 |

|

130,251 |

- | ||||||

|

Financial assets at fair value through profit and loss |

62,025 |

|

303,799 |

|

553,768 |

67 | ||||||

|

Deferred tax asset |

17,871 |

|

87,532 |

|

116,574 |

49,289 | ||||||

|

Trade and other receivables |

86,150 |

|

421,965 |

|

342,192 |

312,132 | ||||||

|

Inventories |

- |

|

- |

|

- |

639 | ||||||

|

Total non-current assets |

1,831,880 |

|

8,972,548 |

|

9,005,815 |

7,504,310 | ||||||

|

Current assets: |

||||||||||||

|

Inventories |

21,096 |

|

103,330 |

|

60,422 |

29,573 | ||||||

|

Biological assets |

101 |

|

497 |

|

99 |

- | ||||||

|

Infrastructure under construction |

17,245 |

|

84,466 |

|

45,504 |

- | ||||||

|

Derivatives financial instruments |

- |

|

- |

|

1,316 |

5,912 | ||||||

|

Financial assets at fair value through profit and loss |

23,153 |

|

113,405 |

|

72,699 |

520,772 | ||||||

|

Financial assets at amortized cost |

- |

|

- |

|

- |

69,144 | ||||||

|

Trade and other receivables |

314,729 |

|

1,541,543 |

|

1,373,557 |

1,048,428 | ||||||

|

Cash and cash equivalents |

57,142 |

|

279,882 |

|

345,119 |

425,460 | ||||||

|

Total current assets |

433,467 |

|

2,123,123 |

|

1,898,716 |

2,099,289 | ||||||

|

Assets classified as held for sale |

48,019 |

|

235,197 |

|

1,183,952 |

120,564 | ||||||

|

Total assets |

2,313,366 |

|

11,330,868 |

|

12,088,483 |

9,724,163 | ||||||

|

Shareholders´ equity |

||||||||||||

|

Share capital |

268,336 |

|

1,314,311 |

|

1,314,311 |

1,314,311 | ||||||

|

Additional paid-in capital |

207,912 |

|

1,018,352 |

|

1,536,759 |

1,535,823 | ||||||

|

Reserve for directors’ options |

51,124 |

|

250,406 |

|

241,460 |

232,515 | ||||||

|

Legal reserve |

- |

|

- |

|

27,397 |

27,397 | ||||||

|

(Accumulated losses) Retained earnings |

(157,574) |

|

(771,797) |

|

(667,906) |

73,489 | ||||||

|

Other comprehensive income (loss) |

(2,195) |

|

(10,753) |

|

(12,651) |

(8,313) | ||||||

|

Equity attributable to owners |

367,603 |

|

1,800,519 |

|

2,439,370 |

3,175,222 | ||||||

|

Non-controlling interest |

108,150 |

|

529,721 |

|

1,327,965 |

1,035,602 | ||||||

|

Total equity |

475,753 |

|

2,330,240 |

|

3,767,335 |

4,210,824 | ||||||

|

Non-current liabilities: |

||||||||||||

|

Trade and other payables |

455,526 |

|

2,231,164 |

|

1,568,887 |

1,036,585 | ||||||

|

Borrowings |

452,937 |

|

2,218,483 |

|

2,487,651 |

1,767,496 | ||||||

|

Deferred revenues |

53,987 |

|

264,427 |

|

174,796 |

- | ||||||

|

Salaries and social security payable |

3,565 |

|

17,460 |

|

23,585 |

19,277 | ||||||

|

Defined benefit plans |

24,684 |

|

120,903 |

|

103,634 |

74,235 | ||||||

|

Deferred tax liabilities |

129,842 |

|

635,968 |

|

821,124 |

832,428 | ||||||

|

Taxes payable |

9,555 |

|

46,802 |

|

45,676 |

46,664 | ||||||

|

Provisions |

17,462 |

|

85,528 |

|

69,974 |

11,327 | ||||||

|

Total non-current liabilities |

1,147,557 |

|

5,620,735 |

|

5,295,327 |

3,788,012 | ||||||

|

Current liabilities: |

||||||||||||

|

Trade and other payables |

344,622 |

|

1,687,959 |

|

1,082,963 |

663,304 | ||||||

|

Borrowings |

161,478 |

|

790,917 |

|

893,801 |

634,764 | ||||||

|

Salaries and social security payable |

91,440 |

|

447,871 |

|

324,900 |

201,190 | ||||||

|

Defined benefit plans |

4,460 |

|

21,847 |

|

14,889 |

2,790 | ||||||

|

Taxes payable |

53,860 |

|

263,804 |

|

196,282 |

158,049 | ||||||

|

Derivative financial instruments |

- |

|

- |

|

- |

7,253 | ||||||

|

Provisions |

2,380 |

|

11,659 |

|

11,399 |

57,977 | ||||||

|

Total current liabilities |

658,239 |

|

3,224,057 |

|

2,524,234 |

1,725,327 | ||||||

|

Liabilities associated with assets classified as held for sale |

31,816 |

|

155,836 |

|

501,587 |

- | ||||||

|

Total liabilities |

1,837,613 |

|

9,000,628 |

|

8,321,148 |

5,513,339 | ||||||

|

Total liabilities and equity |

2,313,366 |

|

11,330,868 |

|

12,088,483 |

9,724,163 | ||||||

(1) Solely for the convenience of the reader, Peso amounts as of December 31, 2012 have been translated into U.S. Dollars at the average buy/sell rate for U.S. Dollars quoted by Banco Nación on December 31, 2012 of Ps. 4.898 to U.S. $1.00. The U.S. Dollar equivalent information should not be construed to imply that the Peso amounts represent, or could have been or could be converted into, U.S. Dollars at such rates or any other rate.

(2) Figures in thousands

|

|

10 |

|

|

At December 31, | |||||||||

|

2012 |

2012 |

|

2011 | ||||||

|

(U.S. Dollars) (1)(4) |

(Pesos)(4) |

(Pesos)(4) | |||||||

|

STATEMENT OF OPERATION DATA |

|||||||||

|

Sales |

U.S.$ |

1,544,438 |

Ps. |

7,564,658 |

Ps. |

5,819,604 | |||

|

Cost of sales |

(1,425,476) |

|

(6,981,982) |

|

(5,122,723) | ||||

|

Gross profit |

118,962 |

|

582,676 |

|

696,881 | ||||

|

Selling expenses |

(100,340) |

|

(491,467) |

|

(330,941) | ||||

|

Administrative expenses |

(105,173) |

|

(515,138) |

|

(411,576) | ||||

|

Other operating income |

40,320 |

|

197,488 |

|

137,981 | ||||

|

Other operating expenses |

(30,557) |

|

(149,667) |

|

(81,101) | ||||

|

Loss of joint ventures |

(6,333) |

|

(31,020) |

|

(14,605) | ||||

|

Share profit of associates |

469 |

|

2,295 |

|

19,779 | ||||

|

Impairment of property, plant and equipment |

(22,108) |

|

(108,284) |

|

(557,669) | ||||

|

Impairment of intangible assets |

- |

|

- |

|

(90,056) | ||||

|

Profit of acquisition of subsidiaries |

- |

|

- |

|

505,936 | ||||

|

Operating income (loss) |

(104,761) |

|

(513,117) |

|

(125,371) | ||||

|

Financial results, net |

(131,867) |

|

(645,883) |

|

(551,205) | ||||

|

Loss before income tax |

(236,627) |

|

(1,159,000) |

|

(676,576) | ||||

|

Income tax |

20,784 |

|

101,798 |

|

(37,381) | ||||

|

Discontinued operations |

(4,567) |

|

(22,368) |

|

(105,974) | ||||

|

Loss for the year |

(220,410) |

|

(1,079,570) |

|

(819,931) | ||||

|

Total loss of the year attributable to: |

|||||||||

|

Owners of the company |

(132,645) |

(649,694) |

(741,395) | ||||||

|

Non - controlling interest |

(87,766) |

(429,876) |

(78,536) | ||||||

|

Basic and diluted loss per share from continuing operations |

(0.1000) |

(0.4898) |

|

(0.5242) | |||||

|

Basic and diluted loss per share from discontinued operations |

(0.0009) |

(0.0045) |

|

(0.0399) | |||||

|

Dividends per share (2) |

- |

|

- |

|

0.0138 | ||||

|

Basic and diluted loss per ADS (3) from continuing operations |

(0.0040) |

(0.0196) |

|

(0.0210) | |||||

|

Basic and diluted loss per ADS (3) from discontinued operations |

(0.0002) |

|

(0.0016) | ||||||

|

Dividends per ADS (3) |

- |

|

- |

|

0.0006 | ||||

|

Weighted average number of shares outstanding |

268,336 |

1,314,311 |

1,314,311 | ||||||

|

CASH FLOW DATA |

|||||||||

|

Net cash flow provided by operating activities |

U.S.$ 274,490 |

Ps. 1,344,454 |

Ps. 1,136,421 | ||||||

|

Net cash flow used in investing activities |

(162,209) |

(794,500) |

(1,715,216) | ||||||

|

Net cash flow provided by (used in) financing activities |

(141,314) |

(692,158) |

395,295 | ||||||

|

Financial results generated by cash and cash equivalents |

U.S.$ 15,714 |

Ps. 76,967 |

Ps. 103,156 | ||||||

|

(1) |

Solely for the convenience of the reader, Peso amounts for the year ended December 31, 2012 have been translated into U.S. Dollars at the average buy/sell rate for U.S. Dollars quoted by Banco Nación on December 31, 2012 of Ps. 4.898 to U.S. $1.00. The U.S. Dollar equivalent information should not be construed to imply that the Peso amounts represent, or could have been or could be converted into, U.S. Dollars at such rates or any other rate. |

|

(2) |

In the year 2010, we declared advance dividends of Ps. 18.1 million, an amount sufficient to cover the Argentine personal asset tax obligations of certain of our shareholders. In March 2011we paid those dividends and withheld the corresponding amount of personal asset tax from those shareholders who were subject to the personal asset tax. See “Item 8. Financial Information—Dividends” and “Item 10. Additional Information—Taxation.” |

|

(3) |

Each ADS represents 25 common shares. |

|

(4) |

Figures in thousands. |

|

|

11 |

|

EXCHANGE RATES

Exchange Rates

The following table sets forth the high, low, average and period-end exchange rates for the periods indicated, expressed in Pesos per U.S. Dollar and not adjusted for inflation. There can be no assurance that the Peso will not depreciate or appreciate again in the future. The Federal Reserve Bank of New York does not report a noon buying rate for Pesos.

___

__________________

__________________

Source: Banco Nación

(1) Represents the average of the exchange rates on the last day of each month during the period.

(2) Average of the lowest and highest daily rates in the month.

(3) Represents the average of the lowest and highest daily rates from April 1 through April 26, 2013.

In the future, any cash dividends we pay will be in Pesos, and exchange rate fluctuations affect the U.S. Dollar amounts received by holders of American Depositary Shares (“ADSs”), on conversion by us or by the depositary of cash dividends on the shares represented by such ADSs. Fluctuations in the exchange rate between the Peso and the U.S. Dollar will affect the U.S. Dollar equivalent of the Peso price of our shares on the Buenos Aires Stock Exchange and, as a result, can also affect the market price of the ADSs.

|

|

12 |

|

RISK FACTORS

Risks Related to Argentina

General

We are a stock corporation (sociedad anónima) incorporated under the laws of the Republic of Argentina and substantially all of our revenues are earned in Argentina and substantially all of our operations, facilities, and customers are located in Argentina. Accordingly, our financial condition and results of operations depend to a significant extent on macroeconomic, regulatory, political and financial conditions prevailing in Argentina, including growth, inflation rates, currency exchange rates, interest rates, and other local, regional and international events and conditions that may affect Argentina in any manner. For example, slower economic growth or economic recession could lead to a decreased demand for electricity in the service areas in which our subsidiaries operate or a decline in the purchasing power of our customers, which, in turn, could lead to a decrease in collection rates from our customers or increased energy losses due to illegal use of our services. Actions of the Argentine Government concerning the economy, including decisions with respect to inflation, interest rates, price controls, foreign exchange controls and taxes, have had and could continue to have a material adverse effect on private sector entities, including us. For example, during the Argentine economic crisis of 2001, the Argentine Government froze electricity distribution margins and caused the pesification of our tariffs, which had a materially adverse effect on our business and financial condition and led us to suspend payments on our financial debt at the time. We cannot assure you that the Argentine Government will not adopt other policies that could adversely affect the Argentine economy or our business, financial condition or results of operations. In addition, we cannot assure you that future economic, regulatory, social and political developments in Argentina will not impair our business, financial condition or results of operations, or cause the market value of our ADSs to decline.

A global financial crisis and unfavorable credit and market conditions may negatively affect our liquidity, customers, business, and results of operations

The effects of a global credit crisis and related turmoil in the global financial system may have a negative impact on our business, financial condition and results of operations, an impact that is likely to be more severe on an emerging market economy, such as Argentina. The effect of this economic crisis on our customers and on us cannot be predicted. Weak economic conditions could lead to reduced demand or lower prices for energy, which could have a negative effect on our revenues. Economic factors such as unemployment, inflation levels and the availability of credit could also have a material adverse effect on demand for energy and therefore on our financial condition and operating results. The financial and economic situation may also have a negative impact on third parties with whom we do, or may do, business. In addition, our ability to access credit or capital markets may be restricted at a time when we would need financing, which could have an impact on our flexibility to react to changing economic and business conditions (See “Argentina’s ability to obtain financing from international markets is limited, which may impair its ability to implement reforms and foster economic growth, and consequently, may affect our business, results of operations and prospects for growth”). For these reasons, any of the foregoing factors or a combination of these factors could have an adverse effect on our results of operations and financial condition and cause the market value of our ADSs to decline.

The Argentine economy remains fragile, and any significant decline could adversely affect our financial condition

Sustainable economic growth in Argentina is dependent on a variety of factors, including international demand for Argentine exports, the stability and competitiveness of the Argentine Peso against foreign currencies, confidence among consumers and foreign and domestic investors, and a stable rate of inflation.

The Argentine economy remains fragile, as reflected by the following economic conditions:

· GDP growth has declined and employment is beginning to show some signals of weakness;

· inflation has accelerated recently and threatens to continue at levels that risk economic stability;

|

|

13 |

|

· investment as a percentage of GDP remains too low to sustain the growth rate of recent years;

· the availability of long-term credit is scarce, while international financing remains limited;

· the regulatory environment continues to be uncertain, as the Argentine Government has been implementing market regulations and other interventionist measures at the microeconomic level in lieu of policies addressing inflation at a macroeconomic level;

· in the climate created by the above conditions, demand for foreign currency has grown, generating a capital flight effect to which the Argentine Government has responded with regulations and currency exchange and transfer restrictions, and it is widely reported that in other countries where the Peso is traded, the Peso/U.S. Dollar exchange rate differs substantially from the official exchange rate in Argentina; and

· previous GDP performance has depended to some extent on high commodity prices which, despite having a favorable long-term trend, are volatile in the short-term and beyond the control of the Argentine Government.

As in the recent past, Argentina’s economy may be adversely affected if political and social pressures inhibit the implementation by the Argentine Government of policies designed to control inflation, generate growth and enhance consumer and investor confidence, or if policies implemented by the Argentine Government that are designed to achieve these goals are not successful. This could, in turn, materially adversely affect our financial condition and results of operations, or cause the market value of our ADSs to decline.

As public finances became increasingly tight, the Argentine Government decided to revise its subsidy policies, particularly those related to energy, electricity and gas, water and public transportation. However, as economic growth has not reached the levels of previous years (on average, GDP grew close to 8.0% per year between 2003 and 2010) and inflation has continued to increase, the manner in which the Argentine Government has revised those policies has been affected. As ultimately implemented, the revised policies will not have an impact on companies’ revenues, but could affect the timing of the revision of the tariff process, and generate a strong negative impact on economic activity and an increase in prices, considering that they would be put into effect in a context of subpar growth, high inflation and capital flight.

We cannot assure you that a decline in economic growth, increased economic instability, or the expansion of economic policies and measures taken by the Argentine Government that affect private sector enterprises such as us, all developments over which we have no control, would not have an adverse effect on our business, financial condition or results of operations or would not have a negative impact on the market value of our ADSs.

The impact of inflation in Argentina on the costs of our subsidiaries could have a material adverse effect on our results of operations

Inflation has, in the past, materially undermined the Argentine economy and the Argentine Government’s ability to create conditions that permit growth. In recent years, Argentina has confronted inflationary pressure, evidenced by significantly higher fuel, energy and food prices, among other factors. According to data published by the Instituto Nacional de Estadística y Censos (National Statistics and Census Institute or INDEC), the rate of inflation reached 10.9% in 2010, 9.5% in 2011 and 10.8% in 2012. The Argentine Government has implemented programs to control inflation and monitor prices for essential goods and services, including freezing the prices of supermarket products, and price support arrangements agreed between the Argentine Government and private sector companies in several industries and markets.

A high inflation environment would undermine Argentina’s foreign competitiveness by diluting the effects of the Argentine Peso devaluation, negatively impact the level of economic activity and employment and undermine confidence in Argentina´s banking system, which could further limit the availability of domestic and international credit to businesses. In turn, a portion of the Argentine debt is adjusted by the Coeficiente de Estabilización de Referencia (Stabilization Coefficient, or “CER”), a currency index, that is strongly related to inflation. Therefore, any significant increase in inflation would cause an increase in the Argentine external debt and consequently in Argentina’s financial obligations, which could exacerbate the stress on the Argentine economy. A continuing high inflation environment could undermine our results of operations as a result of a delay in our ability to, or our inability to, adjust our tariffs accordingly and could adversely affect our ability to finance the working capital needs of our businesses on favorable terms, and adversely affect our results of operations and cause the market value of our ADSs to decline.

|

|

14 |

|

The credibility of several Argentine economic indexes has been called into question, which may lead to a lack of confidence in the Argentine economy and may in turn limit our ability to access the credit and capital markets

In January 2007, INDEC modified its methodology used to calculate the consumer price index (the “CPI”), which is calculated as the monthly average of a weighted basket of consumer goods and services that reflects the pattern of consumption of Argentine households. These events have affected the credibility of the CPI published by INDEC, as well as other indexes. As a result of this uncertainty relating to the accuracy of INDEC indexes, the inflation rate of Argentina and the other rates calculated by INDEC could be higher than as indicated in official reports.

Beginning November 23, 2010, the Argentine government consulted with the IMF for technical assistance in order to prepare a new national consumer price index with the aim of modernizing the current statistical system. During the first quarter of 2011, a team from the IMF started working in conjunction with the INDEC to create such new national consumer price index. Notwithstanding the foregoing, reports published by the IMF state that their staff also uses alternative measures of inflation for macroeconomic surveillance, including data produced by private sources, which have shown inflation rates considerably higher than those issued by the INDEC since 2007, and the IMF has called on Argentina to adopt remedial measures to address the quality of official data. In its meeting held on February 1, 2013, the Executive Board of the IMF found that Argentina’s progress in implementing remedial measures since September 2012 has not been sufficient, and as a result, the IMF issued a declaration of censure against Argentina in connection with its breach of its related obligations to the IMF under the Articles of Agreement, and called on Argentina to adopt remedial measures to address the inaccuracy of inflation and GDP data without further delay.

Any required correction or restatement of the INDEC indexes could result in a significant further decrease in confidence in Argentina’s economy, which could, in turn, have an adverse effect on our ability to access international capital markets to finance our operations and growth, which could, in turn, adversely affect our results of operations and financial condition and cause the market value of our ADSs to decline.

Argentina’s ability to obtain financing from international markets is limited, which may impair its ability to implement reforms and foster economic growth, and consequently, may affect our business, results of operations and prospects for growth

In 2005, Argentina restructured part of its sovereign debt that had been in default since the end of 2001. The Argentine Government announced that as a result of this restructuring, it had approximately U.S.$129.2 billion in total gross public debt as of December 31, 2005. Holdout creditors that declined to participate in the exchanges commenced numerous lawsuits against Argentina in several countries, including the United States, Italy, Germany, and Japan. These lawsuits generally assert that Argentina has failed to make timely payments of interest and/or principal on their bonds, and seek judgments for the face value of and/or accrued interest on those bonds. Judgments have been issued in several proceedings but to date judgment creditors have not succeeded in having those judgments enforced. In at least one case, plaintiffs have asserted that allowing Argentina to make payments under its newly issued bonds and remain in default on its pre-2002 bonds violates the pari passu clause in the original bonds and entitles the plaintiffs to enjoin such payments. The U.S. Court of Appeals for the Second Circuit has ruled in the case that the ranking clause in bonds issued by Argentina prevents Argentina from making such payments unless it makes pro rata payments in respect of defaulted debt that ranks pari passu with the performing

|

|

15 |

|

bonds. The judgment has been appealed, and we cannot predict when or in what form a final appellate decision will be granted.

In September 2008, Argentina announced its intention to cancel its external public debt to Paris Club creditor nations using reserves of the Banco Central de la República Argentina (the Argentine Central Bank, or the “Central Bank”) in an amount equal to approximately U.S. $6.5 billion. However, as of the date of this annual report, the Argentine Government has not yet cancelled such debt. Indeed, negotiations in this respect remain stagnant. If no agreement with the Paris Club creditor nations is reached, financing from multilateral financial institutions may be limited or not available, which could adversely affect economic growth in Argentina and Argentina’s public finances.

Certain groups of holders that did not participate in the 2005 restructuring have filed claims against Argentina and it is possible that new claims will be filed in the future. In addition, foreign shareholders of several Argentine companies have filed claims before the ICSID alleging that certain government measures adopted during the country’s 2001 crisis were inconsistent with the fair and equitable treatment standards set forth in various bilateral investment treaties to which Argentina is a party. Since May 2005, the ICSID tribunals have issued several awards against Argentina. Only the cases “CMS v. Argentina”, “Azurix v. Argentina” and “Vivendi v. Argentina” are currently final and unappealable, which decisions required that the Argentine Government pay U.S. $133.2 million, U.S. $165.2 million and U.S. $105 million, respectively. As of the date of this annual report, Argentina has not yet paid the amounts referred to above.

On April 30, 2010, Argentina launched a new debt exchange to holders of the securities issued in the 2005 debt exchange and to holders of the securities that were eligible to participate in the 2005 debt exchange (other than Brady bonds) to exchange such debt for new securities and, in certain cases, a cash payment. As a result of the 2005 and 2010 exchange offers, Argentina restructured over 91% of the defaulted debt eligible for the 2005 and 2010 exchange offers. The creditors who did not participate in the 2005 or 2010 exchange offers may continue with legal action against Argentina for the recovery of debt, which could adversely affect Argentina’s access to the international capital markets.

Argentina’s past default and its failure to restructure completely its remaining sovereign debt and fully negotiate with the holdout creditors may limit Argentina’s ability to reenter the international capital markets. Litigation initiated by holdout creditors as well as ICSID claims have resulted and may continue to result in judgments and awards against the Argentine Government which, if not paid, could prevent Argentina from obtaining credit from multilateral organizations. Judgment creditors have sought and may continue to seek to attach or enjoin assets of Argentina. A recent example of this is the Libertad Frigate case, in which a commercial court in Accra, Ghana, granted an order (which has been overturned) to detain an Argentine ship which had entered the Accra port on a routine trip. In addition, various creditors have organized themselves into associations to engage in lobbying and public relations concerning Argentina’s default on its public indebtedness. Such groups have over the years unsuccessfully urged passage of federal and New York state legislation directed at Argentina’s defaulted debt and aimed at limiting Argentina’s access to the U.S. capital markets. Although neither the United States Congress nor the New York state legislature has adopted such legislation, we can make no assurance that legislation or other political actions designed to limit Argentina’s access to capital markets will not take effect.

As a result of Argentina’s default and the events that have followed it, the government may not have the financial resources necessary to implement reforms and foster economic growth, which, in turn, could have a material adverse effect on the country’s economy and, consequently, our businesses and results of operations. Furthermore, Argentina’s inability to obtain credit in international markets could have a direct impact on our own ability to access international credit markets to finance our operations and growth, which could adversely affect our results of operations and financial condition and cause the market value of our ADSs and shares to decline.

Significant fluctuations in the value of the Argentine Peso could adversely affect the Argentine economy, which could, in turn adversely affect our results of operations

The devaluation of the Argentine Peso could have a negative impact on the financial condition of many Argentine businesses, including us. Such situation could negatively impact the ability of Argentine businesses to honor their foreign currency-denominated debt, lead to very high inflation and significantly reduce real wages, jeopardize the stability of businesses whose success is dependent on domestic market demand, including public utilities and the financial industry, and adversely affect the Argentine Government’s ability to honor its foreign debt obligations. If the Argentine Peso devalues significantly, the negative effects on the Argentine economy could have adverse consequences to our businesses, our results of operations and the market value of our ADSs, including as measured in U.S. Dollars.

|

|

16 |

|

On the other hand, a substantial increase in the value of the Argentine Peso against the U.S. Dollar also presents risks for the Argentine economy, including the possibility of a reduction in exports (as a consequence of the loss of external competitiveness). Any such increase could also have a negative effect on economic growth and employment, reduce the Argentine public sector’s revenues from tax collection in real terms, and have a material adverse effect on our business, our results of operations and the market value of our ADSs as a result of the weakening of the Argentine economy in general.

Certain measures that may be taken by the Argentine Government may adversely affect the Argentine economy and, as a result, our business and results of operations

In November 2008, the Argentine Government enacted Law No. 26,425 which provided for the nationalization of the Administradoras de Fondos de Jubilaciones y Pensiones (the “AFJPs”) (See “The nationalization of Argentina’s private pension funds caused an adverse effect in the Argentine capital markets and increased the Argentine Government’s interest in certain stock exchange listed companies, such that the Argentine Government became a significant shareholder of such companies”). More recently, beginning in April 2012, the Argentine Government provided for the nationalization of YPF S.A. and imposed major changes to the system under which oil companies operate, principally through the enactment of Law No. 26,741 and Decree No. 1277/2012. Additionally, on December 19, 2012, the Argentine Government issued Decree No. 2552/2012 which, in its article 2, ordered the expropriation of the “Predio Rural de Palermo”. However, on January 4, 2013, the Federal Civil and Commercial Chamber, granted an injunction that has temporarily blocked the application of Decree No. 2552/2012. We cannot assure you that these or other measures that may be adopted by the Argentine Government, such as expropriation, nationalization, forced renegotiation or modification of existing contracts, new taxation policies, changes in laws, regulations and policies affecting foreign trade, investment, etc, will not have a material adverse effect on the Argentine economy and, as a consequence, adversely affect our financial condition, our results of operations and the market value of our shares and ADSs.

|

|

17 |

|

Exchange controls and restrictions on capital inflows and outflows may continue to limit the availability of international credit and could threaten the financial system and lead to renewed political and social tensions, adversely affecting the Argentine economy, and, as a result, our business

In 2001 and 2002, Argentina imposed exchange controls and transfer restrictions, substantially limiting the ability of companies to retain foreign currency or make payments abroad. After 2002, these restrictions, including those requiring the Central Bank’s prior authorization for the transfer of funds abroad to pay principal and interest on debt obligations, were substantially eased through 2007. Since the last quarter of 2011, however, regulations were issued making foreign exchange transactions subject to the prior approval of the Argentine tax authorities. Through a combination of foreign exchange and tax regulations, the Argentine authorities have significantly curtailed access to foreign exchange by individuals and private sector entities.

Since the enhancement of exchange controls began in late 2011, and upon the introduction of measures that have practically closed the foreign exchange market to retail transactions, it is widely reported that the peso/U.S. dollar exchange rate in the unofficial market substantially differs from the official foreign exchange rate. See “Exchange Rates” and “Item 10. Exchange Controls.” In addition to the foreign exchange restrictions, in June 2005 the Argentine Government adopted various rules and regulations that established new restrictive controls on capital inflows into the country, including a requirement that for certain funds remitted into Argentina an amount equal to 30% of the funds must be deposited into an account with a local financial institution as a U.S. Dollar deposit for a one-year period without any accrual of interest, benefit or other use as collateral for any transaction.

The Argentine Government could impose further exchange controls, transfer restrictions or restrictions on the movement of capital, and/or take other measures in response to capital flight or a significant depreciation of the Peso. Such measures could limit our ability to access the international capital markets and impair our ability to make interest or principal payments abroad, and could also lead to renewed political and social tensions and undermine the Argentine Government’s public finances, which could adversely affect Argentina’s economy and prospects for economic growth. This, in turn, could adversely affect our business and results of operations and the market value of our shares and ADSs. In addition, the Argentine Government or the Central Bank may reenact certain restrictions on the transfers of funds abroad, impairing our ability to make dividend payments to holders of the ADSs, which may adversely affect the market value of our ADSs. As of the date of this annual report, however, the transfer of funds abroad to pay dividends is permitted to the extent such dividend payments are made in connection with audited financial statements approved by a shareholders’ meeting. Notwithstanding the foregoing, as of the date of this annual report, in light of applicable regulations, the financial situation of the Company does not permit the payment of dividends.

The nationalization of Argentina’s private pension funds caused an adverse effect in the Argentine capital markets and increased the Argentine Government’s interest in certain stock exchange listed companies, such that the Argentine Government became a significant shareholder of such companies

In recent years a significant portion of the local demand for securities of Argentine companies came from the Argentine private pension funds. In response to the global economic crisis, in December 2008, by means of Argentine Law No. 26,425, the Argentine Congress unified the Argentine pension and retirement system into a system publicly administered by the Administración Nacional de la Seguridad Social (the National Social Security Agency, or “ANSES”), eliminating the pension and retirement system previously administered by private managers. In accordance with the new law, private pension managers transferred all of the assets administered by them under the pension and retirement system to the ANSES. With the nationalization of Argentina’s private pension funds the Argentine Government became a significant shareholder in many of the country’s public companies. In April 2011, the Argentine Government lifted certain restrictions pursuant to which ANSES was prevented from exercising more than 5% of its voting rights in any stock exchange listed company (regardless of the equity interest held by ANSES in such companies). ANSES has publicly stated that it intends to exercise its voting rights in excess of such 5% limit in order to appoint directors in different stock exchange listed companies in which it holds an interest exceeding 5%. ANSES’ interests may differ from those of other investors, and consequently, those investors may understand that ANSES’ actions might have an adverse effect on such companies. As of the date of this annual report, ANSES owns shares representing 23.23% of the capital stock of the Company and also owns shares of the capital stock of our subsidiaries Edenor, Transener and Emdersa.

|

|

18 |

|

The Argentine Government has stated its intention to exert a stronger influence on the operation of stock exchange listed companies. We cannot assure you that these or other similar actions taken by the Argentine Government will not have an adverse effect on the Argentine economy and consequently on our financial condition and results of operations.

The Argentine economy could be adversely affected by economic developments in other markets and by more general “contagion” effects