UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

For the quarterly period ended March 31, 2022

OR

FOR THE TRANSITION PERIOD FROM TO

Commission File Number 001-37880

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

(919 ) 485-8080

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | |||||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Sections 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||||||||

| ☒ | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of May 9, 2022, there were 19,172,585 shares of the registrant’s Common Stock outstanding.

Table of Contents

| Page | ||||||||

| Item 1. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

2

PART I—FINANCIAL INFORMATION

Item 1. Financial Statements

NOVAN, INC.

Condensed Consolidated Balance Sheets

(unaudited)

(in thousands, except share and per share amounts)

| March 31, 2022 | December 31, 2021 | ||||||||||

| ASSETS | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Accounts receivable, net | |||||||||||

| Inventory, net | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

| Restricted cash | |||||||||||

| Property and equipment, net | |||||||||||

| Intangible assets, net | |||||||||||

| Other assets | |||||||||||

| Right-of-use lease assets | |||||||||||

| Goodwill | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Deferred revenue, current portion | |||||||||||

| Research and development service obligation liability, current portion | |||||||||||

| Contingent consideration liability, current portion | |||||||||||

| Operating lease liabilities, current portion | |||||||||||

| Total current liabilities | |||||||||||

| Deferred revenue, net of current portion | |||||||||||

| Operating lease liabilities, net of current portion | |||||||||||

| Notes payable | |||||||||||

| Research and development service obligation liability, net of current portion | |||||||||||

| Research and development funding arrangement liability | |||||||||||

| Contingent consideration liability, net of current portion | |||||||||||

| Other long-term liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (Note 10) | |||||||||||

| Stockholders’ equity | |||||||||||

Common stock $ | |||||||||||

| Additional paid-in capital | |||||||||||

Treasury stock at cost, | ( | ( | |||||||||

| Accumulated deficit | ( | ( | |||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements

3

NOVAN, INC.

Condensed Consolidated Statements of Operations and Comprehensive Loss

(unaudited)

(in thousands, except share and per share amounts)

| Three Months Ended March 31, | |||||||||||

| 2022 | 2021 | ||||||||||

| Net product revenues | $ | $ | |||||||||

| License and collaboration revenues | |||||||||||

| Government research contracts and grants revenue | |||||||||||

| Total revenue | |||||||||||

| Operating expenses: | |||||||||||

| Product cost of goods sold | |||||||||||

| Research and development | |||||||||||

| Selling, general and administrative | |||||||||||

| Amortization of intangible assets | |||||||||||

| Total operating expenses | |||||||||||

| Operating loss | ( | ( | |||||||||

| Other income (expense), net: | |||||||||||

| Interest income | |||||||||||

| Interest expense | ( | ||||||||||

| Other expense | ( | ( | |||||||||

| Total other expense, net | ( | ( | |||||||||

| Net loss and comprehensive loss | $ | ( | $ | ( | |||||||

| Net loss per share, basic and diluted | $ | ( | $ | ( | |||||||

Weighted-average common shares outstanding, basic and diluted | |||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements

4

NOVAN, INC.

Condensed Consolidated Statements of Stockholders’ Equity

(unaudited)

(in thousands, except share amounts)

| Three Months Ended March 31, 2022 | |||||||||||||||||||||||||||||||||||

| Additional Paid-In Capital | Treasury Stock | ||||||||||||||||||||||||||||||||||

| Common Stock | Accumulated | ||||||||||||||||||||||||||||||||||

| Shares | Amount | Deficit | Total | ||||||||||||||||||||||||||||||||

| Balance as of December 31, 2021 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Common stock issued pursuant to equity distribution agreement (at-the-market facility) | — | — | — | ||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Balance as of March 31, 2022 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Three Months Ended March 31, 2021 | |||||||||||||||||||||||||||||||||||

| Additional Paid-In Capital | Treasury Stock | ||||||||||||||||||||||||||||||||||

| Common Stock | Accumulated | ||||||||||||||||||||||||||||||||||

| Shares | Amount | Deficit | Total | ||||||||||||||||||||||||||||||||

| Balance as of December 31, 2020 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Exercise of common stock warrants | — | — | — | ||||||||||||||||||||||||||||||||

| Exercise of stock options | — | — | — | ||||||||||||||||||||||||||||||||

| Common stock issued pursuant to common stock purchase agreements | — | — | |||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Balance as of March 31, 2021 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements

5

NOVAN, INC.

Condensed Consolidated Statements of Cash Flows

(unaudited)

(in thousands)

| Three Months Ended March 31, | |||||||||||

| 2022 | 2021 | ||||||||||

| Cash flow from operating activities: | |||||||||||

| Net loss | $ | ( | $ | ( | |||||||

| Adjustments to reconcile net loss to net cash used in operating activities: | |||||||||||

Depreciation and amortization of property and equipment | |||||||||||

| Amortization of intangible assets | |||||||||||

| Stock-based compensation | |||||||||||

| Foreign currency transaction loss | |||||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accounts receivable | ( | ||||||||||

| Inventory | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Accounts payable | ( | ||||||||||

| Accrued expenses | ( | ||||||||||

| Deferred revenue | ( | ||||||||||

| Research and development service obligation liabilities | ( | ( | |||||||||

| Other long-term assets and liabilities | ( | ||||||||||

| Net cash provided by (used in) operating activities | ( | ||||||||||

| Cash flow from investing activities: | |||||||||||

| Purchases of property and equipment | ( | ( | |||||||||

| Payment for EPI Health Acquisition | ( | ||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| Cash flow from financing activities: | |||||||||||

| Proceeds from exercise of common stock warrants | |||||||||||

| Proceeds from issuance of common stock under common stock purchase agreement | |||||||||||

Proceeds from common stock issued pursuant to equity distribution agreement (at-the-market facility) | |||||||||||

| Proceeds from exercise of stock options | |||||||||||

| Net cash provided by financing activities | |||||||||||

| Net decrease in cash, cash equivalents and restricted cash | ( | ( | |||||||||

| Cash, cash equivalents and restricted cash as of beginning of period | |||||||||||

| Cash, cash equivalents and restricted cash as of end of period | $ | $ | |||||||||

| Supplemental disclosure for cash flow information: | |||||||||||

| Interest paid | $ | $ | |||||||||

| Supplemental disclosure of non-cash investing and financing activities: | |||||||||||

| Purchases of property and equipment with accounts payable and accrued expenses | $ | $ | |||||||||

| Contingent consideration related to EPI Health Acquisition | |||||||||||

Note payable issued for EPI Health Acquisition | |||||||||||

| Reconciliation to condensed consolidated balance sheets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash included in noncurrent assets | |||||||||||

| Total cash, cash equivalents and restricted cash shown in the statement of cash flows | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements

6

NOVAN, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

(dollar values in thousands, except per share data)

Note 1: Organization and Significant Accounting Policies

Business Description

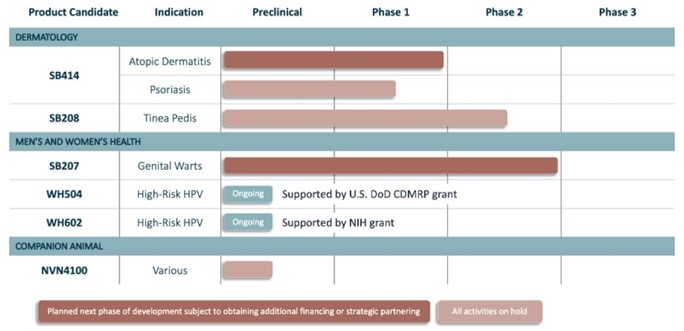

Novan, Inc. (“Novan” and together with its subsidiaries, the “Company”) is a medical dermatology company focused primarily on researching, developing and commercializing innovative therapeutic products for skin diseases. Its goal is to deliver safe and efficacious therapies to patients, including developing product candidates where there are unmet medical needs. The Company is developing SB206 (berdazimer gel, 10.3%) as a topical prescription gel for the treatment of viral skin infections, with a current focus on molluscum contagiosum. On March 11, 2022, the Company acquired EPI Health, LLC, a specialty pharmaceutical company focused on medical dermatology (“EPI Health”), from Evening Post Group, LLC, a South Carolina limited liability company (“EPG” or the “Seller”). The acquisition of EPI Health (the “EPI Health Acquisition”) has provided the Company with a commercial infrastructure to sell a marketed portfolio of therapeutic products for skin diseases. Subsequent to the acquisition, the Company sells various medical dermatology products for the treatments of plaque psoriasis, rosacea, acne and dermatoses.

Novan was incorporated in January 2006 under the state laws of Delaware. In 2015, Novan Therapeutics, LLC, was organized as a wholly owned subsidiary under the state laws of North Carolina; in March 2019, the Company completed registration of a wholly owned Ireland-based subsidiary, Novan Therapeutics, Limited; and in March 2022, the Company acquired its wholly owned subsidiary, EPI Health, a South Carolina limited liability company.

See Note 2—“Acquisition of EPI Health” for further information regarding the EPI Health Acquisition. The post-acquisition operating results of EPI Health are reflected within the Company’s condensed consolidated statement of operations and comprehensive loss for the three months ended March 31, 2022, specifically from March 11, 2022 through March 31, 2022.

Basis of Presentation

The accompanying condensed consolidated financial statements of the Company have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The December 31, 2021 year-end condensed consolidated balance sheet data was derived from audited financial statements but does not include all disclosures required by U.S. GAAP for annual financial statements. Additionally, the Company’s independent registered public accounting firm’s report on the December 31, 2021 financial statements included an explanatory paragraph indicating that there is substantial doubt about the Company’s ability to continue as a going concern.

Basis of Consolidation

The accompanying condensed consolidated financial statements reflect the operations of the Company and its wholly owned subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation.

7

Liquidity and Ability to Continue as a Going Concern

The Company’s condensed consolidated financial statements have been prepared assuming that the Company will continue as a going concern, which contemplates the realization of assets and the settlement of liabilities and commitments in the normal course of business. The accompanying condensed consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classification of liabilities that may result from uncertainty related to the Company’s ability to continue as a going concern.

The Company has evaluated principal conditions and events, in the aggregate, that may raise substantial doubt about its ability to continue as a going concern within one year from the date that these financial statements are issued. The Company identified the following conditions:

•The Company has reported a net loss in all fiscal periods since inception and, as of March 31, 2022, the Company had an accumulated deficit of $292,349 .

•As of March 31, 2022, the Company had a total cash and cash equivalents balance of $35,492 .

•The Company anticipates that it will continue to generate losses for the foreseeable future, and it expects the losses to increase as it continues the development of, and seeks regulatory approvals for, its product candidates and begins activities to prepare for potential commercialization of SB206, if approved.

•The Company has concluded that the prevailing conditions and ongoing liquidity risks faced by the Company, coupled with its current forecasts, including costs associated with implementing the SB206 prelaunch strategy and commercial preparation, raise substantial doubt about its ability to continue as a going concern.

This evaluation is also based on other relevant conditions that are known or reasonably knowable at the date that the financial statements are issued, including ongoing liquidity risks faced by the Company, the Company’s conditional and unconditional obligations due or anticipated within one year, the funds necessary to maintain the Company’s operations considering its current financial condition, obligations, and other expected cash flows, and other conditions and events that, when considered in conjunction with the above, may adversely affect the Company’s ability to meet its obligations. The Company will continue to evaluate this going concern assessment in connection with the preparation of its quarterly and annual financial statements based upon relevant facts and circumstances, including, but not limited to, its cash and cash equivalents balance and its operating forecast and related cash projection.

Based on the Company’s operating forecast, it believes that its existing cash and cash equivalents balance as of March 31, 2022, plus expected receipts associated with product sales from its commercial product portfolio, will provide it with adequate liquidity to fund its planned operating needs into the early fourth quarter of 2022, but not through the targeted submission of the SB206 new drug application (“NDA”), planned no later than the fourth quarter of 2022. This operating forecast and related cash projection includes (i) costs associated with preparing for and seeking U.S. regulatory approval of SB206 as a treatment for molluscum, including costs to prepare for pre-NDA meetings with the Food and Drug Administration (the “FDA”) and NDA-enabling drug stability studies for SB206, (ii) costs associated with the readiness of its new corporate headquarters and manufacturing capability necessary to support small-scale drug substance and drug product manufacturing, (iii) conducting drug manufacturing activities with external third-party contract manufacturing organizations (“CMOs”), (iv) ongoing commercial operations, including sales, marketing, inventory procurement and distribution, and supportive activities, related to its portfolio of therapeutic products for skin diseases acquired with the EPI Health transaction, and (v) initial efforts to support potential commercialization of SB206, but excludes (a) progression of the SB019 program subsequent to the pre-investigational new drug submission, including the execution of a Phase 1 study, (b) any potential costs associated with other late-stage clinical programs, including executing the potentially registrational Phase 3 study of SB204 for acne, and (c) additional operating costs that could occur between a potential NDA submission for SB206 through NDA approval, including, but not limited to, marketing and commercialization efforts to achieve potential launch of SB206. The Company may decide to revise its development, commercial and operating plans or the related timing, depending on information it learns through its research and development activities, including regulatory submission efforts related to SB206, commercialization strategies, ongoing commercial operations, the impact of outside factors such as the COVID-19 pandemic, the Company’s ability to enter into strategic arrangements or other transactions, its ability to access additional capital and its financial priorities. The Company does not currently have sufficient funds to complete commercialization of any of its product candidates that are under development, and its funding needs will largely be determined by its commercialization strategy for SB206, subject to the NDA submission timing and the regulatory approval process and outcome, and the operating performance of its commercial product portfolio.

The inability of the Company to obtain significant additional funding on acceptable terms, could have a material adverse effect on the Company’s business and cause the Company to alter or reduce its planned operating activities, including, but not limited to, delaying, reducing, terminating or eliminating planned product candidate development activities, to conserve its cash and

8

cash equivalents. The Company may pursue additional capital through equity or debt financings or from non-dilutive sources, including partnerships, collaborations, licensing, grants or other strategic relationships. The Company’s anticipated expenditure levels may change if it adjusts its current operating plan. Such actions could delay development timelines and have a material adverse effect on its business, results of operations, financial condition and market valuation.

The Company may also explore the potential for additional strategic transactions, such as strategic acquisitions or in-licenses, sales or divestitures of some of its assets, or other potential strategic transactions, which could include a sale of the Company. If the Company were to pursue such a transaction, it may not be able to complete the transaction on a timely basis or at all or on terms that are favorable to the Company. Alternatively, if the Company is unable to obtain significant additional funding on acceptable terms or progress with a strategic transaction, it could instead determine to dissolve and liquidate its assets or seek protection under the bankruptcy laws. If the Company decides to dissolve and liquidate its assets or to seek protection under the bankruptcy laws, it is unclear to what extent the Company would be able to pay its obligations, and, accordingly, it is further unclear whether and to what extent any resources would be available for distributions to stockholders.

Business Acquisitions

The Company accounts for business acquisitions using the acquisition method of accounting in accordance with Accounting Standards Codification (“ASC”) 805, Business Combinations. ASC 805 requires, among other things, that assets acquired and liabilities assumed be recognized at their fair values, as determined in accordance with ASC 820, Fair Value Measurements, as of the acquisition date. For certain assets and liabilities, book value approximates fair value. In addition, ASC 805 establishes that consideration transferred be measured at the closing date of the acquisition at the then-current market price. Under ASC 805, acquisition-related costs (i.e., advisory, legal, valuation and other professional fees) are expensed in the period in which the costs are incurred. The application of the acquisition method of accounting requires the Company to make estimates and assumptions related to the estimated fair values of net assets acquired.

COVID-19

In December 2019, the novel strain of a virus named SARS-CoV-2 (severe acute respiratory syndrome coronavirus 2), which causes novel coronavirus disease (“COVID-19”) was reported in China, and in March 2020, the World Health Organization declared it a pandemic. The extent to which COVID-19, and its variant strains, and domestic and global efforts to contain its spread will impact the Company’s business including its operations, preclinical studies, clinical trials, and financial condition will depend on future developments, which are highly uncertain and cannot be predicted at this time, and include the duration, severity and scope of the pandemic, the availability and effectiveness of vaccines in preventing the spread of COVID-19 (and its variants), and the actions taken by other parties, such as governmental authorities, to contain and treat COVID-19 and its variants.

During the pandemic, the timetable for development of the Company’s product candidates has been impacted and may face further disruption and the Company’s business could be further adversely affected by the outbreak of COVID-19 and its variants. In particular, COVID-19 impacted the timing of trial initiation of the Company’s B-SIMPLE4 Phase 3 study and is a factor influencing the Company’s adjustment of its targeted SB206 submission timing, planned no later than the fourth quarter of 2022.

In addition, certain factors from the COVID-19 pandemic may delay or otherwise adversely affect the Company’s generation of product revenues from its portfolio of therapeutic products for skin diseases, as well as adversely impact the Company’s business generally, including (i) changes in buying patterns caused by lack of normal access by patients to the healthcare system and concern about the supply of medications, (ii) adverse impacts on the Company’s manufacturing operations, supply chain and distribution processes, which may impact its ability to procure, produce and distribute its products or product candidates, (iii) the inability of third parties to fulfill their obligations to the Company due to staffing shortages, production slowdowns or stoppages and disruptions in delivery systems, (iv) the risk of shutdown in countries where the Company relies on CMOs to provide commercial manufacture of its products or clinical batch manufacturing of its product candidates, (v) the ability to procure raw materials needed for the production of the Company’s active pharmaceutical ingredient (“API”) and other manufacturing components for the Company’s product candidates, (vi) the possibility that third parties on which the Company may rely for certain functions and services, including CMOs, suppliers, distributors, logistics providers, and external business partners, may be adversely impacted by restrictions resulting from the COVID-19 pandemic, which could cause the Company to experience delays or the incurrence of additional costs, and (vii) the risk that the COVID-19 pandemic may intensify other risks inherent in the Company’s business.

Use of Estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amount of revenues and expenses during the reporting period. The Company reviews all significant estimates affecting the

9

condensed consolidated financial statements on a recurring basis and records the effects of any necessary adjustments prior to their issuance.

Significant estimates made by management include provisions for product returns, coupons, rebates, chargebacks, trade and cash discounts, allowances and distribution fees paid to certain wholesalers, inventory net realizable value, useful lives of amortizable intangible assets, stock-based compensation, accrued expenses, valuation of assets and liabilities in business combinations, developmental timelines related to licensed products, valuation of contingent consideration and contingencies. Actual results may differ materially and adversely from these estimates. To the extent there are material differences between the estimates and actual results, the Company’s future results of operations will be affected.

Unaudited Interim Condensed Consolidated Financial Statements

The accompanying interim condensed consolidated financial statements and the related footnote disclosures are unaudited. These unaudited condensed consolidated financial statements have been prepared in accordance with U.S. GAAP and applicable rules and regulations of the Securities and Exchange Commission’s (“SEC”) Rule 10-01 of Regulation S-X for interim financial information. The condensed consolidated financial statements were prepared on the same basis as the audited consolidated financial statements and in the opinion of management, reflect all adjustments of a normal, recurring nature that are necessary for the fair statement of the Company’s financial position and its results of operations and cash flows. The results of operations for interim periods are not necessarily indicative of the results expected for the full fiscal year or any future period. These interim financial statements should be read in conjunction with the consolidated financial statements and notes set forth in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021 filed with the SEC on February 18, 2022.

Reclassifications

Certain amounts in the Company’s consolidated balance sheet as of December 31, 2021 have been reclassified to conform to the current presentation. Prepaid insurance in the amount of $1,697 109 2,164

Net Loss Per Share

Basic net loss per share attributable to common stockholders is computed by dividing the net loss attributable to common stockholders by the weighted average number of shares of common stock outstanding for the period. Diluted net loss per share is calculated by adjusting weighted average shares outstanding for the dilutive effect of common stock equivalents outstanding for the period. Diluted net loss per share is the same as basic net loss per share, since the effects of potentially dilutive securities are anti-dilutive for all periods presented.

| March 31, | |||||||||||

| 2022 | 2021 | ||||||||||

| Warrants to purchase common stock (Note 11) | |||||||||||

| Stock options outstanding under the 2008 and 2016 Plans (Note 16) | |||||||||||

| Stock appreciation rights outstanding under the 2016 Plan (Note 16) | |||||||||||

| Inducement stock options outstanding (Note 16) | |||||||||||

10

Revenue Recognition

The Company accounts for revenue in accordance with ASC 606, Revenue from Contracts with Customers. To determine revenue recognition for arrangements that are within the scope of Topic 606, the Company (i) identifies the contract with a customer, (ii) identifies the performance obligations within the contract, (iii) determines the transaction price, (iv) allocates the transaction price to the performance obligations in the contract, and (v) recognizes revenue when (or as) the Company satisfies a performance obligation. The Company only applies the five-step model to contracts when it is probable that it will collect the consideration to which it is entitled in exchange for the goods or services it transfers to the customer.

At contract inception, once the contract is determined to be within the scope of Topic 606, the Company assesses the goods or services promised within the contract and determines those that are performance obligations and assesses whether each promised good or service is distinct. The Company then recognizes as revenue the amount of the transaction price that is allocated to the respective performance obligation when (or as) the performance obligation is satisfied.

Upon occurrence of a contract modification, the Company conducts an evaluation pursuant to the modification framework in Topic 606 to determine the appropriate revenue recognition. The framework centers around key questions, including (i) whether the modification adds additional goods and services, (ii) whether those goods and services are distinct, and (iii) whether the contract price increases by an amount that reflects the standalone selling price for the new goods or services. The resulting conclusions will determine whether the modification is treated as a separate, standalone contract or if it is combined with the original contract and accounted for in that manner. In addition, some modifications are accounted for on a prospective basis and others on a cumulative catch-up basis.

The Company currently has the following types of revenue generating arrangements:

Net Product Revenues

Net product revenues encompass sales recognized resulting from transferring control of products to the customer, excluding amounts collected on behalf of third parties and sales taxes. The amount of revenue recognized is the amount allocated to the satisfied performance obligation taking into account variable consideration. The estimated amount of variable consideration is included in the transaction price only to the extent that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved.

Product sales are recognized at the point in time when legal transfer of title has occurred, based on shipping terms. For product sales for which the Company owns rights to the products, the Company records a reduction to the transaction price for estimated chargebacks, rebates, coupons, trade and cash discounts and sales returns. A liability is recognized for expected sales returns, rebates, coupons, trade and cash discounts, chargebacks or other reimbursements to customers in relation to sales made in the reporting period. Payment terms can differ from contract to contract, but no element of financing is deemed present as the typical payment terms are less than one year. Therefore, the transaction price is not adjusted for the effects of a significant financing component. A receivable is recognized as soon as control over the products is transferred to the customer as this is the point in time that the consideration is unconditional because only the passage of time is required before the payment is due.

Variable consideration relates to sales returns, rebates, coupons, trade and cash discounts, and chargebacks granted to various direct and indirect customers. The Company recognizes provisions at the time of sale and adjusts them if the actual amounts differ from the estimated provisions. The following describes the nature of each deduction and how provisions are estimated:

Chargebacks – The Company has arrangements with various third-party wholesalers that require the Company to issue a credit to the wholesaler for the difference between the invoice price to the wholesaler and the customer’s contract price. Provisions for chargebacks involve estimates of the contract prices within multiple contracts with multiple wholesalers. The provisions for chargebacks vary in relation to changes in product mix, pricing and the level of inventory at the wholesalers and, in addition, fluctuate in proportion to an increase or decrease in sales. Provisions for estimated chargebacks are calculated using the historical chargeback experience and expected chargeback levels for new products and anticipated pricing changes. Chargeback provisions are compared to externally obtained distribution channel reports for reasonableness. The Company regularly monitors the provisions for chargebacks and makes adjustments when the Company believes that actual chargebacks may differ from estimated provisions.

11

Rebates – Rebates include managed care services, fee for service and Medicaid rebate programs. Rebates are primarily related to volume-based incentives and are offered to key customers to promote loyalty. Customers receive rebates upon the attainment of a pre-established volume or the attainment of revenue milestones for a specified period. Since rebates are contractually agreed upon, provisions are estimated based on the specific terms in each agreement based on historical trends and expected sales.

Returns – Returns primarily relate to customer returns of expired products that the customer has the right to return up to one year following the product’s expiration date. Such returned products are destroyed and credits and/or refunds are issued to the customer for the value of the returns. Accordingly, no returned assets are recorded in connection with those products. The returns provision is estimated by applying a historical return rate to the amounts of revenue estimated to be subject to returns. Revenue subject to returns is estimated based on the lag time from time of sale to date of return. The estimated lag time is developed by analyzing historical experience. Additionally, the Company considers specific factors, such as levels of inventory in the distribution channel, product dating and expiration, size and maturity of launch, entrance of new competitors, changes in formularies or packaging and any changes to customer terms, in determining the overall expected levels of returns.

Prompt pay discounts – Prompt pay discounts are offered to most customers to encourage timely payment. Discounts are estimated at the time of invoice based on historical discounts in relation to sales. Prompt pay discounts are almost always utilized by customers. As a result, the actual discounts typically do not vary significantly from the estimated amount.

Coupons – The Company offers coupons to market participants in order to stimulate product sales. The redemption cost of consumer coupons is based on historical redemption experience by product and value.

Sales and other taxes the Company collects concurrent with revenue-producing activities are excluded from revenue. Shipping and handling costs are accounted for as a fulfillment cost and are recorded as cost of revenue. Incidental items that are immaterial in the context of the contract are recognized as expense. Costs incurred to obtain a contract will be expensed as incurred when the amortization period is less than a year.

There can be a lag between the Company’s establishment of an estimate and the timing of the invoicing or claim. The Company believes it has made reasonable estimates for future rebates and claims, however, these estimates involve assumptions pertaining to contractual utilization and performance, and payor mix. If the performance or mix across third-party payors is different from the Company’s estimates, the Company may be required to pay higher or lower total price adjustments and/or chargebacks than it had estimated.

License and Collaboration Revenues

The Company has entered into various types of agreements that license the Company’s intellectual property. If the applicable license is determined to be distinct from the other performance obligations identified in the arrangement, the Company recognizes revenues from non-refundable, upfront fees allocated to the license when the license is transferred to the customer and the customer is able to use and benefit from the license. For licenses that are bundled with other promises, the Company’s management utilizes judgment to assess the nature of the combined performance obligation to determine whether the combined performance obligation is satisfied over time or at a point in time and, if over time, the estimated performance period and the appropriate method of measuring progress during the performance period for purposes of recognizing revenue. The Company re-evaluates the estimated performance period and measure of progress each reporting period and, if necessary, adjusts related revenue recognition accordingly.

The Company also enters into various types of collaborative arrangements to develop and commercialize products. The Company’s collaborative activities may include marketing, selling and distribution of the developed drugs, which may be bundled with a license for the Company’s intellectual property, as noted above. These arrangements often include milestone as well as royalty or profit-share payments, contingent upon the occurrence of certain future events linked to the success of the asset in development, as well as expense reimbursements from or payments to the collaboration partner. Because of the risk that products in development will not receive regulatory approval, the Company does not recognize any contingent payments until after regulatory approval has been achieved.

Royalty revenue from licenses provided to the Company’s collaboration partners, which is based on sales to third parties of licensed products and technology, is recorded when the third-party sale occurs and the performance obligation to which some or all of the royalty has been allocated has been satisfied. This royalty revenue is included in collaboration revenue in the accompanying condensed consolidated statements of operations and comprehensive loss.

Operating expenses for costs incurred pursuant to these arrangements are reported in their respective expense line item. Such contractually required reimbursements are recognized when amounts are known and determinable and are reported as a liability within the accompanying condensed consolidated balance sheets based upon the timing of cash receipt from the collaboration partner.

12

Advertising Costs

Promotion, marketing and advertising costs are expensed as incurred. Promotion, marketing and advertising costs for the three months ended March 31, 2022 and 2021 were approximately $113 and zero , respectively, and are included in selling, general and administrative expenses in the condensed consolidated statement of operations and comprehensive loss.

Income Taxes

Deferred tax assets and liabilities are determined based on the temporary differences between the financial statement carrying amounts and the tax bases of assets and liabilities using the enacted tax rates in effect in the years in which the differences are expected to reverse. In estimating future tax consequences, all expected future events are considered other than enactment of changes in the tax law or rates.

The Company did not record a federal or state income tax benefit for the three months ended March 31, 2022 or 2021 due to its conclusion that a full valuation allowance is required against the Company’s deferred tax assets.

The determination of recording or releasing a tax valuation allowance is made, in part, pursuant to an assessment performed by management regarding the likelihood that the Company will generate future taxable income against which benefits of its deferred tax assets may or may not be realized. This assessment requires management to exercise judgment and make estimates with respect to its ability to generate taxable income in future periods.

Accounts Receivable, net

Accounts receivable are carried at original invoice amount less an estimate made for doubtful receivables. An account receivable is considered to be past due if any portion of the receivable balance is outstanding beyond the agreed-upon due date.

The Company records an allowance for credit losses, which includes a provision for expected losses based on historical write-offs, adjusted for current conditions as deemed necessary, reasonable and supportable based on forecasts about future conditions that affect the expected collectability of the reported amount of the financial asset, as well as a specific reserve for accounts deemed at risk. The allowance is the Company’s estimate for accounts receivable as of the balance sheet date that ultimately will not be collected. Any changes in the allowance are reflected in the results of operations in the period in which the change occurs. The Company writes off accounts receivable and the related allowance recorded previously when it becomes probable, based upon customer facts and circumstances, that such amounts will not be collected. No

Account balances are written off against the allowance after all means of collection have been exhausted and the potential for recovery is considered remote. Recoveries of receivables previously written off are recorded when received. The Company does not charge interest on accounts receivable.

13

Inventory, net

The Company maintains inventory consisting of for-sale pharmaceuticals related to its marketed product portfolio. The Company measures inventory using the first-in, first-out method and values inventory at the lower of cost and net realizable value. Net realizable value represents the estimated selling price for inventories less all estimated costs to sell.

Property and Equipment, net

Property and equipment are recorded at cost and depreciated using the straight-line method over their estimated useful lives. Leasehold improvements are amortized over the shorter of the life of the lease or the useful life of the improvements. Expenditures for maintenance and repairs are expensed as incurred. Improvements and betterments that add new functionality or extend the useful life of an asset are capitalized. Leases for real estate often include tenant improvement allowances, which the Company assesses according to applicable accounting guidance to determine the appropriate owner, and capitalizes such tenant improvement assets accordingly.

Intangible Assets, net and Goodwill

Intangible assets represent certain identifiable intangible assets, including pharmaceutical product licenses and patents. Amortization for pharmaceutical products licenses is computed using the straight-line method based on the lesser of the term of the agreement and the useful life of the license. Amortization for pharmaceutical patents is computed using the straight-line method based on the useful life of the patent.

Definite-lived intangible assets are reviewed for impairment whenever events or circumstances indicate that carrying amounts may not be recoverable. In the event impairment indicators are present or if other circumstances indicate that an impairment might exist, then management compares the future undiscounted cash flows directly associated with the asset or asset group to the carrying amount of the asset group being determined for impairment. If those estimated cash flows are less than the carrying amount of the asset group, an impairment loss is recognized. An impairment loss is recognized to the extent that the carrying amount exceeds the asset’s fair value. Considerable judgment is necessary to estimate the fair value of these assets, accordingly, actual results may vary significantly from such estimates.

Indefinite-lived intangible assets, such as goodwill and the cost to obtain and register the Company’s internet domain, are not amortized. The Company tests the carrying amounts of goodwill for recoverability on an annual basis at September 30 or when events or changes in circumstances indicate evidence that a potential impairment exists, using a fair value based test.

A significant amount of judgment is involved in determining if an indicator of goodwill impairment has occurred. Such indicators may include, among others: a significant decline in expected future cash flows, a sustained, significant decline in the Company’s stock price and market capitalization, a significant adverse change in legal factors or in the business climate, adverse assessment or action by a regulator, and unanticipated competition. Key assumptions used in the annual goodwill impairment test are highly judgmental. Any change in these indicators or key assumptions could have a significant negative impact on the Company’s financial condition, impact the goodwill impairment analysis or cause the Company to perform a goodwill impairment analysis more frequently than once per year.

Related Parties

Members of the Company’s board of directors held 123,497 and 100,497 shares of the Company’s common stock as of March 31, 2022 and December 31, 2021, respectively.

14

Recently Issued Accounting Standards

Accounting Pronouncements Adopted

In June 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2016-13, Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which is designed to provide financial statement users with more information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity at each reporting date. When determining such expected credit losses, the guidance requires companies to apply a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. The adoption of this new accounting guidance, as of January 1, 2022, did not have a material impact on the Company’s condensed consolidated financial statements.

Note 2: Acquisition of EPI Health

On March 11, 2022, the Company completed the EPI Health Acquisition, in which the Company acquired all of the issued and outstanding units of membership interest of EPI Health from EPG for estimated purchase consideration of $36,335 . EPI Health is an integrated medical dermatology company providing the Company with a commercial infrastructure to support the commercialization of products. Subsequent to the EPI Health Acquisition, the Company sells various dermatological products for the treatments of plaque psoriasis, rosacea, acne and dermatoses.

The portion of the estimated purchase consideration at closing was $27,500 , as adjusted for cash, indebtedness, net working capital estimates and other contractually defined adjustments (the “Closing Purchase Price”). The Closing Purchase Price consisted of (i) $11,000 paid in cash, (ii) a secured promissory note issued to EPG in the principal amount of $16,500 (the “Seller Note”), and (iii) a $993 payment representing an adjustment for estimated net working capital. See Note 9—“Notes Payable” for additional detail regarding the Seller Note and its related terms.

The purchase agreement entered into in connection with the EPI Health Acquisition (the “EPI Heath Purchase Agreement”) included the potential payment of additional consideration totaling up to $23,500 upon achievement of certain milestones, as follows:

a.$1,000 , as a one-time cash payment, upon EPG’s performance of transition services and the successful completion of the transition provided under the transition services agreement between the Company and EPG;

b.$3,000 , as a one-time payment, payable in cash or the Company’s common stock, at the discretion of the Company, upon net sales of certain of EPI Health’s legacy products exceeding $30,000 during the period from April 1, 2022 through March 31, 2023;

c.up to $2,500 , paid in quarterly installments in cash or the Company’s common stock at the discretion of the Company, upon net sales of Wynzora Cream (“Wynzora”) exceeding certain quarterly thresholds or an annual threshold of $12,500 during the period from April 1, 2022 through March 31, 2023;

d.$5,000 , as a one-time payment, payable in cash or the Company’s common stock at the discretion of the Company, upon the first occurrence of post-closing net sales of certain of EPI Health’s legacy products exceeding $35,000 during any twelve-month period from April 1, 2023 through March 31, 2026; and

e.up to $12,000 based on receipt by EPI Health of regulatory and net sales milestones related to Sitavig from EPI Health’s OTC Switch License Agreement with Bayer.

Certain of the above milestone payments will accelerate and become immediately payable upon certain specified events during the applicable milestone periods, including a sale of all or substantially all of the assets with respect to certain of EPI Health’s legacy products. The EPI Health Purchase Agreement provides that payment of any additional consideration may be made in cash or in shares of the Company’s common stock, so long as the number of shares that may be issued pursuant to the EPI Health Purchase Agreement or otherwise in connection with the EPI Health Acquisition limited to no more than 19.99 % of the Company’s outstanding shares of common stock immediately prior to the closing, unless stockholder approval is obtained to issue more than 19.99 %.

The EPI Health Acquisition is being accounted for as a business combination using the acquisition method in accordance with ASC 805, Business Combinations. Under this method of accounting the fair value of the consideration transferred is allocated to the assets acquired and liabilities assumed based upon their estimated fair values on the date of the EPI Health Acquisition. Any excess of the purchase price over the fair value of identified assets acquired and liabilities assumed is recognized as goodwill.

For the three months ended March 31, 2022, the Company incurred costs related to the EPI Health Acquisition of $4,021 recognized in selling, general and administrative expenses within the condensed consolidated statements of operations and comprehensive loss.

15

From the EPI Health Acquisition date through March 31, 2022, $1,246 of total net revenue and a net loss of $726 associated with EPI Health’s operations are included in the condensed consolidated statements of operations and comprehensive loss for the three months ended March 31, 2022.

Purchase Consideration

The following table presents the allocation of the estimated purchase consideration to be allocated to the estimated fair values of the net assets acquired at the EPI Health Acquisition date.

| As of March 11, 2022 | ||||||||

| Initial cash consideration to Seller | $ | |||||||

Secured promissory note issued to Seller | ||||||||

| Fair value of contingent consideration liability | ||||||||

| Remaining working capital adjustment to be paid | ||||||||

| Working capital adjustment paid at close | ||||||||

| Total estimated purchase consideration | $ | |||||||

The estimated fair value of the contingent consideration as of March 31, 2022 is $3,773 , of which $443 and $3,330 is recognized as a current liability and long-term liability, respectively, in the condensed consolidated balance sheets.

Significant increases or decreases in any of the probabilities of success or changes in expected achievement of any of the milestones underlying the contingent consideration would result in a significantly higher or lower fair value of the contingent consideration liability. The contingent consideration is revalued at each reporting period and changes in fair value are recognized in the condensed consolidated statements of operations and comprehensive loss until settlement. See Note 17—“Fair Value” for additional information.

Provisional Allocation of Purchase Consideration to Estimated Fair Values of Net Assets Acquired

ASC 805 requires, among other things, that the assets acquired and liabilities assumed in a business combination be recognized at their fair values as of the acquisition date. Further, ASC 805 requires any consideration transferred or paid in a business combination in excess of the fair value of the assets acquired and liabilities assumed should be recognized as goodwill.

The total estimated purchase consideration was allocated to the estimated fair values of the assets acquired and liabilities assumed as of March 11, 2022 as follows:

| Assets acquired and liabilities assumed: | ||||||||

| Accounts receivable, net | $ | |||||||

| Inventory, net | ||||||||

| Prepaid expenses and other current assets | ||||||||

| Property and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Other assets | ||||||||

| Right-of-use lease assets | ||||||||

| Total assets | $ | |||||||

| Accounts payable | $ | |||||||

| Accrued expenses | ||||||||

| Operating lease liabilities, current portion | ||||||||

| Operating lease liabilities, net of current portion | ||||||||

| Other long-term liabilities | ||||||||

| Total liabilities | $ | |||||||

| Total identifiable net assets acquired | $ | |||||||

| Goodwill | ||||||||

| Total estimated purchase consideration | $ | |||||||

16

The Company determined the estimated fair value of the acquired intangible assets as of the closing date using the income approach. This is a valuation technique that is based on the market participant’s expectations of the cash flows that the intangible assets are forecasted to generate. The projected cash flows from these intangible assets were based on various assumptions, including estimates of revenues, expenses, and operating profit, and risks related to the viability of and commercial potential for alternative treatments. The cash flows were discounted at a rate commensurate with the level of risk associated with the projected cash flows. The Company believes the assumptions are representative of those a market participant would use in estimating fair value.

Goodwill was determined on the basis of the provisional fair values of the assets and liabilities identified at the time of the EPI Health Acquisition. The estimated provisional allocation of purchase consideration will be adjusted, within a period of no more than 12 months from the EPI Health Acquisition date, if these fair values change as a result of circumstances existing at the acquisition date. These measurement period adjustments may arise with regard to amounts recorded as assets and liabilities upon verification of such amounts or upon finalization of the required valuations of intangible assets identified. The amounts of reserves and provisions may also be adjusted as a result of ongoing procedures to identify and measure liabilities, including tax, environmental risks and litigation. The purchase consideration may also be adjusted in connection with finalizing the valuation procedures for the contingent consideration liability and finalizing the amount of the working capital adjustment to the purchase price. Any adjustments to amounts may impact the valuation of the consideration or the amounts recorded as goodwill.

Goodwill was calculated as the excess of the consideration paid consequent to completing the acquisition, compared to the net assets recognized. Goodwill represents the future economic benefits arising from the other acquired assets, which could not be individually identified and separately valued. Goodwill is primarily attributable to the acquired commercial platform and infrastructure, including personnel, and expected synergies related to the commercialization of product candidates. Goodwill is not expected to be deductible for tax purposes.

Pro forma Information

The following pro forma information presents the combined results of operations for the three months ended March 31, 2022 and 2021, as if the Company had completed the EPI Health Acquisition at the beginning of the periods presented. The pro forma financial information is provided for comparative purposes only and is not indicative of what actual results would have been had the EPI Health Acquisition occurred at the beginning of the periods presented, nor does it give effect to synergies, cost savings, fair market value adjustments, and other changes expected to result from the EPI Health Acquisition. Accordingly, the pro forma financial results do not purport to be indicative of consolidated results of operations as of the date hereof, for any period ended on the date hereof, or for any other future date or period. The pro forma financial information has been calculated after applying the Company’s accounting policies and includes adjustments for transaction-related costs.

| Three Months Ended | ||||||||||||||

| March 31, 2022 | March 31, 2021 | |||||||||||||

| Total revenue | $ | $ | ||||||||||||

| Net loss and comprehensive loss | ( | ( | ||||||||||||

| Net loss per share, basic and diluted | $ | ( | $ | ( | ||||||||||

Note 3: Inventory, net

The major components of inventory, net, were as follows:

| March 31, 2022 | ||||||||

| Finished goods available for sale | $ | |||||||

| Reserve for obsolescence | ||||||||

| Inventory, net | $ | |||||||

As part of the EPI Health Acquisition, inventory, net, were marked to fair value as part of the Company’s ASC 805 business combination accounting. See Note 2—“Acquisition of EPI Health” for additional detail.

Note 4: Prepaid Expenses and Other Current Assets

17

| March 31, 2022 | December 31, 2021 | |||||||||||||

| Inventory and raw material deposits | $ | $ | ||||||||||||

| Prepaid service contracts | ||||||||||||||

| Prepaid insurance | ||||||||||||||

Prepaid Prescription Drug User Fee Act (PDUFA) fees | ||||||||||||||

| Product samples | ||||||||||||||

| Other current assets related to leasing arrangement | ||||||||||||||

| Prepaid expenses and other current assets | ||||||||||||||

| Total prepaid expenses and other current assets | $ | $ | ||||||||||||

Note 5: Property and Equipment, net

Property and equipment consisted of the following:

| March 31, 2022 | December 31, 2021 | ||||||||||

| Computer equipment | $ | $ | |||||||||

| Furniture and fixtures | |||||||||||

| Laboratory equipment | |||||||||||

| Office equipment | |||||||||||

| Leasehold improvements | |||||||||||

| Property and equipment, gross | |||||||||||

| Less: Accumulated depreciation and amortization | ( | ( | |||||||||

| Total property and equipment, net | $ | $ | |||||||||

Depreciation and amortization expense was $97 for the three months ended March 31, 2022, and $57 for the three months ended March 31, 2021.

New Facility

As of March 31, 2022 and December 31, 2021, the Company had construction in progress amounts related to leasehold improvements of $8,392 and $7,485 , respectively.

See Note 6—“Leases” for details regarding the new facility and related lease.

Note 6: Leases

The Company leases office space and certain equipment under non-cancelable lease agreements.

In accordance with ASC 842, Leases, arrangements meeting the definition of a lease are classified as operating or financing leases and are recorded on the balance sheet as both a right-of-use asset and lease liability, calculated by discounting fixed lease payments over the lease term at the rate implicit in the lease, if available, otherwise at the Company’s incremental borrowing rate. For operating leases, interest on the lease liability and the amortization of the right-of-use asset result in straight-line rent expense over the lease term. Variable lease expenses, if any, are recorded when incurred.

In calculating the right-of-use asset and lease liability, the Company elected, and has in practice, historically combined lease and non-lease components. The Company excludes short-term leases having initial terms of 12 months or less from the guidance as an accounting policy election and recognizes rent expense on a straight-line basis over the lease term.

Office Lease at Triangle Business Center, Durham, North Carolina

On January 18, 2021, the Company entered into a lease with an initial term expiring in 2032, as amended for 19,265 rentable square feet, located in Durham, North Carolina. This lease dated as of January 18, 2021, as amended (the “TBC Lease”), is by and between the Company and Copper II 2020, LLC (the “TBC Landlord”), pursuant to which the Company is leasing space serving as its corporate headquarters and small-scale manufacturing site (the “Premises”) located within the Triangle Business Center. The lease executed on January 18, 2021, as amended, was further amended on November 23, 2021 to expand the Premises by approximately 3,642 additional rentable square feet from 15,623 rentable square feet.

18

The Premises serves as the Company’s corporate headquarters and has been and continues to be prepared to support various cGMP activities, including research and development and small-scale manufacturing capabilities. These capabilities include the infrastructure necessary to support small-scale drug substance manufacturing and the ability to act as a primary, or secondary backup, component of a potential future commercial supply chain.

The TBC Lease commenced on January 18, 2021 (the “Lease Commencement Date”). Rent under the TBC Lease commenced in October 2021 (the “Rent Commencement Date”). The term of the TBC Lease expires on the last day of the one hundred twenty-third calendar month after the Rent Commencement Date. The TBC Lease provides the Company with one option to extend the term of the TBC Lease for a period of five years , which would commence upon the expiration of the original term of the TBC Lease, with base rent of a market rate determined according to the TBC Lease; however, the renewal period was not included in the calculation of the lease obligation as the Company determined it was not reasonably certain to exercise the renewal option.

The monthly base rent for the Premises is approximately $40 for months 1-10 and approximately $49 for months 11-12, per the second amendment to the primary lease. Beginning with month 13 and annually thereafter, the monthly base rent will be increased by 3 %. Subject to certain terms, the TBC Lease provides that base rent will be abated for three months following the Rent Commencement Date. The Company is obligated to pay its pro-rata portion of taxes and operating expenses for the building as well as maintenance and insurance for the Premises, all as provided for in the TBC Lease.

The TBC Landlord has agreed to provide the Company with a tenant improvement allowance in an amount not to exceed $130 per rentable square foot, totaling approximately $2,450 , per the primary lease, inclusive of the first amendment, and $115 per rentable square foot, totaling $419 , per the second amendment to the TBC Lease. The tenant improvement allowance will be paid over four equal installments corresponding with work performed by the Company. Pursuant to the terms of the TBC Lease, the Company delivered to the TBC Landlord a letter of credit in the amount of $583 , as amended, as collateral for the full performance by the Company of all of its obligations under the TBC Lease and for all losses and damages the TBC Landlord may suffer as a result of any default by the Company under the TBC Lease. Cash funds maintained in a separate deposit account at the Company’s financial institution to fully secure the letter of credit are presented as restricted cash in non-current assets on the accompanying condensed consolidated balance sheets.

Office Lease at Meeting Street, Charleston, South Carolina

On March 3, 2022 EPI Health entered into a sublease agreement with EPG (the “Meeting Street Lease”) for office space at 174 Meeting Street in Charleston, South Carolina for approximately 6,000 rentable square feet.

The term of the Meeting Street Lease is through September 30, 2024, and EPI Health has the right to terminate the Meeting Street Lease with 60 days’ prior notice. The monthly base rent for the Meeting Street Lease is $20 for months 1-12, inclusive of taxes and operating expenses such as maintenance and insurance. Beginning with month 13 and annually thereafter, the monthly base rent will be increased by 3 %.

TBC Lease and Meeting Street Lease

Rent expense, including both short-term and variable lease components associated with the TBC Lease and the Meeting Street Lease, as applicable, was $137 for the three months ended March 31, 2022 and $145 for the three months ended March 31, 2021.

The remaining lease term for the TBC Lease and the Meeting Street Lease are 9.86 years and 2.42 years, respectively, as of March 31, 2022. The weighted average discount rate for both leases was 8.35

19

Future net minimum lease payments, net of amounts expected to be received related to the tenant improvement allowance, as of March 31, 2022 were as follows:

| Maturity of Lease Liabilities | Operating Lease | ||||

| 2022 | $ | ( | |||

| 2023 | |||||

| 2024 | |||||

| 2025 | |||||

| 2026 | |||||

| 2027 and beyond | |||||

| Total future undiscounted lease payments | $ | ||||

| Add: reclassification of discounted net cash inflows to other current assets | |||||

| Less: imputed interest | ( | ||||

| Total reported lease liability | $ | ||||

The table above reflects payments for an operating lease with a remaining term of one year or more, but does not include obligations for short-term leases. In addition, the net cash inflow related to the 2022 fiscal year presented above relates to the expected timing of the remaining balance of the total tenant improvement allowance of $2,450 being funded by the TBC Landlord, which the Company reasonably expects to receive within the next twelve months, partially offset by expected lease payments for the corresponding period.

Components of lease assets and liabilities as of March 31, 2022 were as follows:

| March 31, 2022 | |||||

| Assets | |||||

| Other current assets related to leasing arrangement | $ | ||||

| Right-of-use lease assets | |||||

| Total lease assets | $ | ||||

| Liabilities | |||||

| Operating lease liabilities, current portion | $ | ||||

| Operating lease liabilities, net of current portion | |||||

| Total lease liabilities | $ | ||||

During the year ended December 31, 2021, the Company received $1,523 related to payments as part of the total TBC Landlord funded tenant improvement allowance. The effective discounted value of the remaining tenant improvement allowance payments being funded by the TBC Landlord, of the total tenant improvement allowance of $2,450 , partially offset by the expected lease payments by the Company within the next twelve months, results in a net balance of $51 . This net amount is presented within the condensed consolidated balance sheets within prepaid expenses and other current assets as of March 31, 2022. Furthermore, this amount is also included in long-term lease liabilities within the condensed consolidated balance sheets as of March 31, 2022.

20

Note 7: Goodwill and Intangible Assets, net

Goodwill

The Company’s goodwill balance as of March 31, 2022 was $4,002 . The entire goodwill balance relates to the EPI Health Acquisition during the three months ended March 31, 2022. None of the goodwill is expected to be deductible for income tax purposes.

Intangible Assets

The following table presents both definite and indefinite lived intangible assets as of March 31, 2022, comprised primarily of acquired product rights related to the EPI Health Acquisition:

| Initial Carrying Value | Accumulated Amortization | Net Book Value | Useful Life (Years) | |||||||||||||||||||||||

| Rhofade | $ | $ | $ | |||||||||||||||||||||||

| Wynzora | ||||||||||||||||||||||||||

| Minolira | ||||||||||||||||||||||||||

| Cloderm | ||||||||||||||||||||||||||

| Nuvail | ||||||||||||||||||||||||||

| Sitavig | ||||||||||||||||||||||||||

| Website domain | — | — | ||||||||||||||||||||||||

| Total intangible assets | $ | $ | $ | |||||||||||||||||||||||

The Company amortizes the product rights related to its commercial product portfolio over their estimated useful lives. As part of the EPI Health Acquisition, product rights were recorded at fair value as part of the Company’s ASC 805 business combination accounting. See Note 2—“Acquisition of EPI Health” for additional detail.

The following table represents annual amortization of definite lived intangible assets for the next five fiscal years, and thereafter:

| 2022 | $ | |||||||

| 2023 | ||||||||

| 2024 | ||||||||

| 2025 | ||||||||

| 2026 | ||||||||

| Thereafter | ||||||||

| Total amortization | $ | |||||||

21

Note 8: Accrued Expenses

The following table represents the components of accrued expenses as of March 31, 2022 and December 31, 2021:

| March 31, 2022 | December 31, 2021 | |||||||||||||

| Accrued rebates, discounts and chargebacks | $ | $ | ||||||||||||

| Accrued returns | ||||||||||||||

| Accrued compensation | ||||||||||||||

| Accrued outside research and development services | ||||||||||||||

| Accrued royalties | ||||||||||||||

| Accrued working capital adjustment | ||||||||||||||

| Accrued construction in process | ||||||||||||||

| Accrued SB206 pre-commercial and marketing | ||||||||||||||

| Accrued collaboration reimbursement | ||||||||||||||

| Accrued other expenses | ||||||||||||||

| Total accrued expenses | $ | $ | ||||||||||||

Note 9: Notes Payable

Seller Note with Evening Post Group

On March 11, 2022, at the closing of the EPI Health Acquisition, the Company entered into a secured promissory note and security agreement with EPG. The Company entered into the Seller Note with EPG to finance a portion of the Closing Purchase Price related to the EPI Health Acquisition.

The Seller Note has a principal amount of $16,500 with interest-only payments due over the course of the 24-month term of the Seller Note. The Seller Note will bear interest at the rate of 5.0 % per annum for the first 90 days after the closing date, 15.0 % per annum for the following 12 months, and 18.0 % per annum for the remainder of the term. The non-amortizing principal of the Seller Note is to be paid in full at maturity and is secured by the membership interests of EPI Health held by the Company. EPI Health is a guarantor of the Seller Note. There is no penalty for repaying the Seller Note prior to the end of the term. Based on the escalating interest rate over the term of the Seller Note, the Company has recorded interest expense using the effective interest method.

During the three months ended March 31, 2022, the Company recorded interest expense of $132 related to the Seller Note. As of March 31, 2022, the Company had $87 of accrued interest included within accrued expenses on the condensed consolidated balance sheets.

The following table represents future maturities of the Seller Note obligation as of March 31, 2022:

| 2022 | $ | |||||||

| 2023 | ||||||||

| 2024 | ||||||||

| Total notes payable | $ | |||||||

Note 10: Commitments and Contingencies

Contingencies

From time to time, the Company may have certain contingent liabilities that arise in the ordinary course of business activities. The Company accrues a liability for such matters when it is probable that future expenditures will be made and such expenditures can be reasonably estimated. See Legal Proceedings below for further discussion of pending legal claims.

The Company has entered into, and expects to continue to enter into, contracts in the normal course of business with various third parties that support its clinical trials, preclinical research studies, development services, and commercial sales and marketing activities in addition to potential third-party manufacturers for both the manufacture of the Company’s product candidates and procurement of its commercial finished good products. The scope of the services under these agreements can generally be modified at any time, and these agreements can generally be terminated by either party after a period following written notice.

22

In connection with entering into the Equity Distribution Agreement with Oppenheimer discussed in Note 11—“Stockholders’ Equity,” the Company terminated its common stock purchase agreement with Aspire Capital on March 10, 2022. Other than such termination, there have been no material contract terminations as of March 31, 2022.

Also, see Note 11—“Stockholders’ Equity” regarding outstanding common stock warrants.

Contingent Payment Obligations Related to the Purchase of EPI Health

See Note 2—“Acquisition of EPI Health” for certain contingent payments related to consideration due to EPG upon achievement of certain milestones by EPI Health.

Contingent Payment Obligations from Historical Acquisitions by EPI Health

EPI Health has in the past acquired certain rights to pharmaceutical products and such arrangements have typically included requirements that EPI Health make certain contingent payments to the applicable seller as discussed below.

Rhofade. On October 10, 2019, EPI Health entered into an agreement whereby it acquired certain assets related to Rhofade (the “Rhofade Acquisition Agreement”). In connection with the Rhofade Acquisition Agreement, EPI Health is required to make the following milestone payments to the seller upon reaching the following net sales thresholds during any calendar year following the closing date, as defined in the Rhofade Acquisition Agreement:

| Calendar Year Net Sales Threshold | Milestone Payment | |||||||

| $ | $ | |||||||

| $ | $ | |||||||

| $ | $ | |||||||

Under the terms of the Rhofade Acquisition Agreement, EPI Health assumed certain liabilities of the prior licensees of the Rhofade product. In particular, EPI Health would also be required to pay certain earnout payments pursuant to historic acquisition agreements for Rhofade upon the achievement of net sales thresholds higher than those set forth above. However, the Company has not recognized a liability for such Rhofade milestones based on current and historical sales figures and management’s estimates of future sales.

Cloderm. On September 28, 2018, EPI Health entered into an agreement pursuant to which it acquired assets related to the product Cloderm. EPI Health is required to pay a low double-digit royalty once cumulative net sales of Cloderm reach $20,833 , until $6,500 of royalty payments have been made by EPI Health.

Minolira. On August 20, 2018, EPI Health entered into an agreement pursuant to which it acquired assets related to the product Minolira. In connection with the agreement, EPI Health is required to make the following milestone payments to the seller upon reaching cumulative net sales thresholds as defined in the acquisition agreement:

| Cumulative Net Sales Threshold | Milestone Payment | ||||||||||

| $ | $ | ||||||||||

| $ | $ | ||||||||||

| Each additional | $ | $ | |||||||||

See Note 12—“Licensing and Collaboration Arrangements” for certain obligations and contingent payments related to license agreements, including those related to the Company’s commercial product portfolio.

Also see Note 15—“Research and Development Agreements” for certain obligations regarding the Company’s research and development license agreements, including the Reedy Creek Purchase Agreement and the Ligand Funding Agreement.

For the three months ended March 31, 2022, the Company recorded $98 of expense related to royalties on net sales and accruals of certain cumulative sales-based milestones related to its commercial product portfolio, described above. As of March 31, 2022 the Company had accrued royalties of $1,040 and accrued milestones of $297 , presented within accrued expenses and other long-term liabilities, respectively, in its condensed consolidated balance sheets.

Development Services Agreement