As filed with the Securities and Exchange Commission on September 23, 2013

Registration No. 333-189977

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1 TO FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

LONE STAR GOLD, INC.

(Exact name of registrant in its charter)

|

Nevada

|

1000

|

45-2578051

|

|

(State or other jurisdiction of

|

(Primary Standard Industrial Classification

|

(I.R.S. Employer Identification Number)

|

|

incorporation or organization)

|

Code Number)

|

6565 Americas Parkway NE, Suite 200

Albuquerque, NM 87110

(505) 563-5828

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Capitol Corporate Services, Inc.

202 South Minnesota Street

Carson City, NV 89703

(800) 899-0490

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of communications to:

Gregg E. Jaclin, Esq.

Anslow & Jaclin, LLP

195 Route 9 South, Suite 204

Manalapan, NJ 07726

Tel. No.: (732) 409-1212

Fax No.: (732) 577-1188

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective. If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act of 1933, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer

|

¨

|

Accelerated filer

|

¨

|

|

Non-accelerated filer

|

¨

|

Smaller reporting company

|

x

|

|

(Do not check if a smaller reporting company)

|

|||

CALCULATION OF REGISTRATION FEE

|

Proposed

|

Proposed

|

|||||||||||||||

|

Maximum

|

Maximum

|

Amount of

|

||||||||||||||

|

Title of Each Class of Securities

|

Amount to be

|

Offering Price

|

Aggregate

|

Registration

|

||||||||||||

|

to be Registered

|

Registered (1)

|

Per Share (2)

|

Offering Price

|

Fee (3)

|

||||||||||||

|

Common Stock, par value $0.001 per share,

issuable pursuant to the KVM Investment Agreement

|

26,100,000

|

$

|

0.034 |

$

|

887,400 |

$

|

121.04 | |||||||||

|

Total

|

$

|

$

|

||||||||||||||

|

(1)

|

We are registering 26,100,000 shares of our common stock that we will put to KVM Capital Partners LLC pursuant to that certain investment agreement (the “KVM Investment Agreement”). The KVM Investment Agreement was entered into on June 27. 2013. In the event of stock splits, stock dividends or similar transactions involving the common stock, the number of common shares registered shall, unless otherwise expressly provided, automatically be deemed to cover the additional securities to be offered or issued pursuant to Rule 416 promulgated under the Securities Act of 1933, as amended (the “Securities Act”). In the event that the adjustment provisions of the KVM Investment Agreement require the registrant to issue more shares than are being registered in this registration statement, for reasons other than those stated in Rule 416 of the Securities Act, the registrant will file a new registration statement to register those additional shares.

|

|

|

(2)

|

The offering price has been estimated solely for the purpose of computing the amount of the registration fee in accordance with Rule 457(o) of the Securities Act on the basis of the closing bid price of the common stock of the registrant as reported on the OTCBB on June 28, 2013.

|

|

| (3) |

Offset pursuant to Rule 457(p) under the Securities Act by the registration fee of $132.99 paid on July 16, 2013 pursuant to the Registrant’s S-1 Registration Statement, File No. 333-189977.

|

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the commission, acting pursuant to said section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

|

PRELIMINARY PROSPECTUS

|

SUBJECT TO COMPLETION, DATED SEPTEMBER 23, 2013

|

26,100,000 Shares of Common Stock

2

LONE STAR GOLD, INC.

This prospectus relates to the resale of up to 26,100,000 shares of common stock of Lone Star Gold, Inc. (“we” or the “Company”), par value $0.001 per share, issuable to KVM pursuant to that certain investment agreement. The investment agreement permits us to “put” up to $5,000,000 in shares of our common stock to KVM over a period of up to thirty-six (36) months. We will not receive any proceeds from the resale of these shares of common stock. However, we will receive proceeds from the sale of securities pursuant to our exercise of the put right offered by KVM. KVM is deemed an underwriter for our common stock.

The selling stockholder may offer all or part of the shares for resale from time to time through public or private transactions, at either prevailing market prices or at privately negotiated prices. KVM is paying all of the registration expenses incurred in connection with the registration of the shares except for accounting fees and expenses and we will not pay any of the selling commissions, brokerage fees and related expenses.

Our common stock is quoted on the Over-the-Counter Bulletin Board (“OTCBB”) under the ticker symbol “LSTG.” On August 14, 2013 , the closing price of our common stock was $0.0334 per share.

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 5 to read about factors you should consider before investing in shares of our common stock.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The Date of This Prospectus Is: _____________, 2013

TABLE OF CONTENTS

|

Page

|

|

|

Prospectus Summary

|

4 |

|

The Offering

|

5 |

|

Risk Factors

|

5 |

|

Special Note Regarding Forward-Looking Statements

|

13 |

|

Use of Proceeds

|

13 |

|

Market For Common Equity and Related Stockholder Matters

|

14 |

|

Management’s Discussion and Analysis of Financial Condition and Results Of Operations

|

15 |

|

Description of Business

|

21 |

|

Directors and Executive Officers

|

33 |

|

Executive Compensation

|

35 |

|

Security Ownership of Certain Beneficial Owners and Management

|

36 |

|

Certain Relationships and Related Transactions

|

37 |

|

Changes In and Disagreement With Accountants On Accounting and Financial Disclosure

|

38 |

|

Selling Stockholders

|

38 |

|

Plan of Distribution

|

39 |

|

Description of Securities To Be Registered

|

41 |

|

Legal Matters

|

42 |

|

Experts

|

42 |

|

Available Information

|

42 |

|

Index To Consolidated Financial Statements

|

F-1

|

3

PROSPECTUS SUMMARY

This summary highlights selected information contained elsewhere in this Prospectus. This summary does not contain all the information that you should consider before investing in the common stock of Lone Star Gold, Inc. (referred to herein as the “Company,” “we,” “our,” and “us”). You should carefully read the entire Prospectus, including “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the accompanying financial statements and notes before making an investment decision.

Business Overview

We are currently a start-up exploration stage company in the business of gold and mineral exploration, acquisition and development. We were incorporated in the State of Nevada under the name Keyser Resources, Inc. on November 26, 2007. Our business was initially operated to acquire an option to purchase a mining interest in Canada. After a change in control in November 2010, we explored a merger with another company in order to obtain an option to purchase several oil and gas leases in Nevada. A merger agreement was signed in January 2011. The then-current management decided not to pursue the merger, and the merger agreement was terminated by mutual agreement of the parties as of March 18, 2011.

On March 29, 2011, we underwent another change in management. On March 29, 2011, Daniel M. Ferris was elected to serve as the sole director. Mr. Ferris subsequently appointed himself President, Secretary and Treasurer. Following the appointment of Daniel M. Ferris as our sole director and officer, we changed our focus to engage in the acquisition, exploration and development of gold and silver mining properties. To further reflect this change in business focus, we changed our name to “Lone Star Gold, Inc.” on June 14, 2011. In addition, to create a more flexible capital structure, we increased the number of authorized shares of our common stock from 75,000,000 to 150,000,000 on June 14, 2011. A 20:1 forward stock split was declared to stockholders of record as of June 17, 2011.

On August 29, 2011, we entered into an investment agreement with North American Gold Corp. (“North American”) pursuant to which North American agreed to invest up to $15,000,000 to purchase our common stock in increments of $100,000 or an integral multiple thereof, at our option at any time through August 31, 2013 (the “North American Investment Agreement”).

Investment Agreement with KVM

On June 27, 2013, we entered into an investment agreement with KVM Capital Partners LLC, a New York limited liability company (“KVM”). Pursuant to the terms of the KVM Investment Agreement, KVM committed to purchase up to $5,000,000 of our common stock over a period of up to thirty-six (36) months. From time to time during the thirty-six (36) months period commencing from the effectiveness of the registration statement, we may deliver a put notice to KVM which states the dollar amount that we intend to sell to KVM on a date specified in the put notice. The maximum investment amount per notice shall be no more than two hundred percent (200%) of the average daily volume of the common stock for the ten consecutive trading days immediately prior to date of the applicable put notice. The purchase price per share to be paid by KVM shall be calculated at a twenty percent (20%) discount to the lowest volume weighted average price of the common stock as reported by Bloomberg, L.P. during the ten (10) consecutive trading days immediately prior to the receipt by KVM of the put notice. We initially reserved 30,000,000 shares of our common stock for issuance under the KVM Investment Agreement based upon the registration statement filed with the Securities and Exchange Commission (the “SEC”) on July 16, 2013. We have more shares reserved than are covered in this registration statement.

In connection with the KVM Investment Agreement, we also entered into a registration rights agreement with KVM, pursuant to which we are obligated to file a registration statement with the SEC covering 26,100,000 shares of our common stock underlying the KVM Investment Agreement within 21 days after the closing of the transaction. In addition, we are obligated to use all commercially reasonable efforts to have the registration statement declared effective by the SEC within 120 days after the closing of the transaction and maintain the effectiveness of such registration statement until termination of the KVM Investment Agreement.

The 26,100,000 shares to be registered herein represent 25.89% of the shares issued and outstanding, assuming that the selling stockholder will sell all of the shares offered for sale.

4

At an assumed purchase price of $0.0272 (equal to 80% of the closing price of our common stock of $0.034 on August 14, 2013), we will be able to receive up to $709,920 in gross proceeds, assuming the sale of the entire 26,100,000 shares being registered hereunder pursuant to the KVM Investment Agreement. Accordingly, we would be required to register additional 157,723,530 shares to obtain the balance of $4,290,080 under the KVM Investment Agreement. We are currently authorized to issue 150,000,000 shares of our common stock. We may be required to increase our authorized shares in order to receive the entire purchase price. KVM has agreed to refrain from holding an amount of shares which would result in KVM owning more than 4.99% of the then-outstanding shares of our common stock at any one time.

There are substantial risks to investors as a result of the issuance of shares of our common stock under the KVM Investment Agreement. These risks include dilution of stockholders’ percentage ownership, significant decline in our stock price and our inability to draw sufficient funds when needed.

KVM will periodically purchase our common stock under the KVM Investment Agreement and will, in turn, sell such shares to investors in the market at the market price. This may cause our stock price to decline, which will require us to issue increasing numbers of common shares to KVM to raise the same amount of funds, as our stock price declines.

The aggregate investment amount of $5 million was determined based on numerous factors, including the following: Our current running costs are approximately $1 – 2 million per annum, and thus we need a portion of the investment amount to pay general operating expenses. We believe we need the remaining funds for capital expenditures related to the Tailings Property and the Candelaria project, including the construction of a nitrogen leach plant on the Tailings property. While it is difficult to estimate the likelihood that the Company will need the full investment amount, we believe that the Company may need the full amount of $5 million funding under the KVM Investment Agreement.

Where You Can Find Us

Our principal office is located at 6565 Americas Parkway NE, Suite 200, Albuquerque, New Mexico 87110. Our telephone number is (505) 563-5828.

THE OFFERING

|

Common stock outstanding before the offering

|

100,804,663 shares of common stock as of June 28, 2013.

|

|

Common stock outstanding after the offering

|

126,904,663 shares of common stock.

|

|

Use of proceeds

|

We will not receive any proceeds from the sale of shares by the selling stockholder. However, we will receive proceeds from the sale of securities pursuant to the KVM Investment Agreement. The proceeds received under the KVM Investment Agreement will be used for general corporate and working capital purposes and acquisitions or assets, businesses or operations or for other purposes that the Board of Directors, in its good faith deem to be in the best interest of the Company.

|

|

OTCBB Trading Symbol

|

LSTG.OB

|

|

Risk Factors

|

The common stock offered hereby involves a high degree of risk and should not be purchased by investors who cannot afford the loss of their entire investment. See “Risk Factors”.

|

RISK FACTORS

You should carefully consider the risks described below together with all of the other information included in this Prospectus before making an investment decision with regard to our securities. The statements contained in or incorporated into this Prospectus that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

5

Risks Related to Our Business

We are an exploration stage company with a history of operating losses and expect to continue to realize losses in the near future. We currently have no operations that are producing revenue, and currently rely on investments by third parties to fund our business. Even when we begin to generate revenues from operations, we may not become profitable or be able to sustain profitability.

We are an exploration stage company, and since inception, we have incurred significant net losses and have not realized any revenue from our operations. We have reported a net loss of $4,542,053 from the date of inception through June 30, 2013 . We expect to continue to incur net losses and negative cash flow from operations in the near future, and we will continue to experience losses for at least as long as it takes our company to generate revenue by selling Extracted Minerals from the Tailings, or through our mining operations. The size of these losses will depend, in large part, on whether we find gold or other minerals in our properties and are able to extract and sell the minerals in a profitable manner. To date, we have not had any operating revenues, nor have we found any minerals or developed any mineral deposits. Because we do not yet have a revenue stream resulting from sales or other operations, there can be no assurance that we will achieve material revenues in the future. Should we achieve a level of revenues that make us profitable, there is no assurance that we can maintain or increase profitability levels in the future.

There is substantial doubt as to whether we will continue operations. If we discontinue operations, you could lose your investment.

The following factors raise substantial doubt regarding the ability of our business to continue as a going concern: (i) the losses we incurred since our inception; (ii) our lack of operating revenues since inception through the date of this Report; and (iii) our dependence on the sale of equity securities to continue in operation. We have signed certain investment agreements with North American, for up to $15,000,000 through sales of our Common Stock, and KVM for up to $5,000,000 through sales of our Common Stock. However, North American has the option to refuse to fund any request for investment if market conditions are not favorable. We anticipate that we will incur increased expenses without realizing enough revenues from operations. We therefore expect to incur significant losses in the foreseeable future. The financial statements do not include any adjustments that might result from the uncertainty about our ability to continue our business. If we are unable to obtain additional financing from outside sources and eventually produce enough revenues, we may be forced to curtail or cease our operations. If this happens, you could lose all or part of your investment.

Our lack of any operating history makes it difficult for us to evaluate our future business prospects and make decisions based on those estimates of our future performance.

We do not have any material operating history, which makes it impossible to evaluate our business on the basis of historical operations. Furthermore, we have pursued the business of mineral exploration and development for a short time, and thus our business carries both known and unknown risks. As a consequence, our past results may not be indicative of future results. Although this is true for any business, it is particularly true for us because of our lacking any material operating history.

We recently underwent two separate changes in management, and the current management had no experience in mining or mineral exploration prior to joining the Company.

We underwent a change in management in November 2010 and again in March 2011. The new director and sole executive officer of the Company was not previously an employee of or otherwise involved in the management of the Company. While Mr. Ferris has prior business experience, he had no prior experience in mining or mineral exploration or development before joining the Company.

6

Together, two of our stockholders have the ability to significantly influence any matters to be decided by the stockholders, which may prevent or delay a change in control of our company.

Mr. Ferris and Mr. John Rhoden currently own approximately 22.32% of our Common Stock on a fully diluted basis, as a group. As a result, they could exert considerable influence over the outcome of any corporate matter submitted to our stockholders for approval, including the election of directors and any transaction that might cause a change in control, such as a merger or acquisition. Any stockholders in favor of a matter that is opposed by these two stockholders would have to obtain a significant number of votes to overrule the collective votes of Mr. Ferris and the other principal stockholder.

Mr. Ferris is our sole director and officer and the loss of Mr. Ferris could adversely affect our business.

Since Mr. Ferris is currently our sole director and officer, if he were to die, become disabled, or leave our company, we would be forced to retain individuals to replace him. There is no assurance that we can find suitable persons to replace him if that becomes necessary. We have no “Key Man” life insurance at this time.

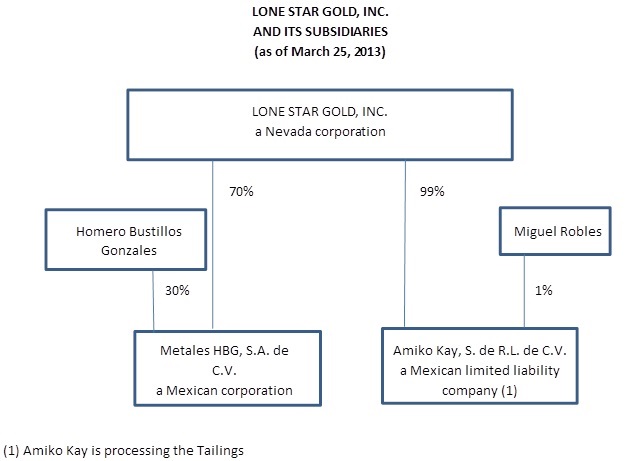

We hold the Concessions through a Mexican subsidiary, Metales, in which we own a 70% interest. Therefore, our ability to realize revenues from the La Candelaria project will depend in part upon the payment of dividends by Metales and thus is dependent on Mexican corporate and other law.

As a U.S. company, we cannot hold the Concessions (as defined in Description of Business) directly. Instead, Mexican law requires a company formed in Mexico to own the Concessions. We have invested in Metales in order to comply with the Mexican law. Therefore, Metales must comply with Mexican laws regarding the declaration and payment of dividends in order to distribute profits to its stockholders, including the Company. If it fails to do so, we could fail to realize revenues from the project.

Risks Relating to Mining Activities

We have no known mineral reserves and we may not find any gold or, if we find gold, it may not be in economic quantities. If we fail to find any gold or if we are unable to find gold in economic quantities, we will have to suspend operations.

The chance of finding gold, silver or other mineral reserves on any individual parcel of land is almost infinitesimal. It is not uncommon to spend millions of dollars on a potential project, complete many phases of exploration and still not obtain reserves that can be economically exploited. Therefore, our chances finding economically viable mineral reserves are remote.

We have no known mineral reserves. Even if we find gold or silver deposits, we may not be of sufficient quantity to warrant recovery. Additionally, even if we find gold or silver deposits in sufficient quantity to warrant recovery, we ultimately may find that those deposits are not recoverable. Finally, even if any gold or silver is recoverable, we may be unable to recover at a profit. Failure to locate deposits in economically recoverable quantities will cause us to cease operations.

We face a high risk of business failure because of the unique difficulties and uncertainties inherent in mineral exploration ventures.

Potential investors should be aware of the difficulties generally encountered by new mineral exploration companies and their high rate of failure. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays that we may encounter in our mining activities. These potential problems may lead to additional costs and expenses that exceed current estimates. Problems such as unusual or unexpected formations and other adverse conditions often result in unsuccessful exploration efforts. If the results of our exploration do not reveal viable commercial mineralization, we may decide to abandon the Concessions and acquire new properties for exploration. The acquisition of additional properties will depend on whether we possess sufficient capital resources at the time. If no funding is available, we may be forced to abandon our mining operations.

The Tailings may fail to yield Extracted Minerals in amounts or grades that are sufficient to produce a steady source of revenue to Amiko Kay. If the Tailings operation fails to produce sufficient revenue to offset the substantial costs incurred in exploration and development of the site, we may lose all amounts invested under the JV Agreement.

7

Because of the inherent dangers involved in mineral exploration, there is a risk that we may incur liability or damages as we conduct our business.

The search for valuable minerals involves numerous hazards. As a result, we may become subject to liability for such hazards, including pollution, cave-ins and other hazards against which we cannot insure or against which we may elect not to insure. The payment of such liabilities may have a material adverse effect on our financial position.

We may not have access to all of the supplies and materials we need to explore our properties, which could delay or suspend our operations.

Competition and unforeseen limited sources of supplies in the industry or in the region in which we operate could result in occasional spot shortages of supplies, such as explosives, and certain equipment such as bulldozers and excavators. If we cannot find the products and equipment we need, we will have to suspend our exploration plans until we do find the products and equipment we need.

We face intense competition in the mining industry. We will have to compete for financing and for qualified managerial and technical employees.

The mining industry is intensely competitive. Competition includes large established mining companies with substantial capabilities and with greater financial and technical resources than we have. As a result of this competition, we may be unable to acquire additional attractive mining claims or financing on terms we consider acceptable. We also compete with other mining companies in the recruitment and retention of qualified managerial and technical employees. If we are unable to successfully compete for financing or for qualified employees, our exploration and development programs may be slowed down or suspended.

Our properties are located in Mexico and are subject to changes in Mexican political conditions and government regulations.

The Concessions and Tailings are located in Mexico. In the past, Mexico has been subject to political and social instability. Change and uncertainty in Mexico could lead to changes in existing government regulations affecting mineral exploration and mining. Our business activities in Mexico may be adversely affected by changing governmental regulations relating to the mining industry. More generally, shifts in political conditions may increase the cost of conducting our business or maintaining our properties. Finally, Mexico’s status as a developing country may make it more difficult to obtain required financing for our projects.

Our business operations may be adversely affected by social and political unrest in Chihuahua, or by violence and crime in Mexico.

Both La Candelaria and the Mine Tailings Project are located in the state of Chihuahua, Mexico. Our business operations could be negatively impacted if Chihuahua or other areas of Mexico experiences a period of social and political unrest. Various areas in Mexico are affected by persistent violence and crime, which has been well-publicized in the US. Our exploration and construction program in La Candelaria, or the processing of the Tailings, could be interrupted if we are unable to hire qualified personnel or if we are denied access to our properties. We may be required to make additional expenditures to provide increased security in order to protect our property or personnel located at our sites. Significant delays in exploration or increases in expenditures will likely have a material adverse effect on our financial condition and results of operations.

Our operations in Mexico may be adversely affected by factors outside our control, such as changing political, local and economic conditions, any of which could materially adversely affect our financial position or results of operations.

The La Candelaria Concessions are mineral concessions granted by the Mexican government. We hold the Mine Tailings Project under a contractual arrangement with a Mexican national.

8

Both of these projects are subject to the laws of Mexico. Exploration and potential development activities are potentially subject to political and economic risks, including:

|

·

|

Cancellation or renegotiation of contracts;

|

|

|

·

|

Competition from companies not subject to US laws and regulations, such as the Foreign Corrupt Practices Act;

|

|

·

|

Changes in Mexican laws and regulations;

|

|

|

·

|

Changes in tax laws;

|

|

·

|

Royalty and tax increases or claims by Mexican governmental authorities;

|

|

|

·

|

Expropriation or nationalization of property;

|

|

·

|

Foreign exchange controls;

|

|

|

·

|

Import and export regulations;

|

|

·

|

Environmental controls;

|

|

|

·

|

Risks of loss due to civil strife, war, guerilla activity, insurrection and terrorism; and

|

|

·

|

Other risks arising out of foreign sovereignty over the areas in which our business is operated.

|

Our business in Mexico is dependent on our consultants.

We are almost entirely dependent on the services of consultants in Mexico to operate our business in Mexico and to advise the Company on matters vital to its continued viability and success. For example, Adam Whyte is responsible for overseeing the day to day operation of the La Candelaria property, while Miguel Jaramillo (“Jaramillo”) operates the Mine Tailings Project. We rely on such persons for advice on matters such as permitting and environmental compliance, as well as mining operations. In addition, we rely on legal counsel in Mexico to maintain the registration of our properties, to form our subsidiaries and to advise us on other matters involving Mexican law. The loss of these persons or our inability to attract and train additional skilled employees may adversely affect our business, future operations and financial condition.

We require substantial funds merely to determine if mineral reserves exist on our Concessions.

Any potential development and production of minerals on our Concessions depends upon the results of exploration programs, feasibility studies and the recommendations of qualified engineers and geologists. Such activities require substantial funding. Before deciding to explore for, and then produce or develop, mineral reserves, we must consider several significant factors, including, but not limited to:

|

•

|

Costs of bringing the property into production;

|

|

|

•

|

Availability and costs of financing;

|

|

•

|

Ongoing costs of production;

|

|

|

•

|

Market prices for the products to be produced;

|

|

•

|

Environmental compliance regulations and restraints; and

|

|

|

•

|

Political climate and/or governmental regulation and control.

|

There is no assurance that Extracted Minerals from the Tailings will be produced in amounts that will make the Tailings project commercially viable.

The 1.2 million tons of Tailings must be processed at a plant operated by a third party to determine whether any gold, silver or other minerals may be extracted. There is no assurance that any valuable minerals will be extracted after processing. Even if valuable minerals are extracted from the Tailings, there is no assurance that they will be in sufficient quantities, or of sufficient grades, to allow the processing to be commercially viable for the Company. If we cannot make a profit by processing the Tailings, the Tailings project may fail, and we may lose our investment in the Tailings project. The failure of the Tailing project to provide a source of current revenue to the Company may also force us to abandon or curtail our other operations.

9

The Assignment Agreement and the Option Agreement obligate the Company to fund certain exploration costs under the Work Plan. If we fail to satisfy those obligations, Gonzalez could demand a return of the Concessions.

Under the terms of that certain assignment agreement (the “Assignment Agreement”) and the option agreement between American Gold Holdings, Ltd. and Homero Bustillos Gonzalez (“Gonzalez”) dated January 11, 2011 (the “Option Agreement”), if we fail to comply with our obligations to make expenditures under the Work Plan (as defined in the Description of Business) before January 11, 2014, the Option Agreement will terminate and we will be obligated to return the Concessions to Gonzalez. If this occurs, we would lose all our investment in the Concessions.

Since most of our expenses are paid in Mexican pesos, and our outside investors fund the Company in United States dollars, we are subject to adverse changes in currency values that may adversely affect our results of operations.

Our operations in the future could be affected by changes in the value of the Mexican peso against the United States dollar. The appreciation of non-U.S. dollar currencies such as the peso against the U.S. dollar increases expenses and the cost of purchasing capital assets in U.S. dollar terms in Mexico, which can adversely impact our operating results and cash flows. Conversely, depreciation of the non-U.S. dollar currencies usually decreases operating costs and capital asset purchases in U.S. dollar terms. The value of cash and cash equivalents denominated in foreign currencies also fluctuates with changes in currency exchange rates.

Title to some of our properties may be defective or challenged.

While we believe that we have satisfactory title to our properties, some titles may be defective or subject to challenge. In addition, certain of our Mexican properties could be subject to rights of the Ejido, as discussed below.

Our ability to develop our property in Mexico is subject to the rights of the Ejido (local inhabitants) to use the surface for agricultural purposes.

Our ability to mine minerals is subject to maintaining satisfactory arrangements with the Ejido for access and surface disturbances. Ejidos are groups of local inhabitants who were granted rights to conduct agricultural activities on the property. We must negotiate and maintain a satisfactory arrangement with these residents in order to disturb or discontinue their rights to farm. While Jaramillo and our consultants we have successfully negotiated and signed such agreements related to the Tailing project, our ability to maintain these agreements or consummate similar agreements for new projects could impair or impede our ability to successfully mine the properties.

In the event of a dispute regarding title or any other matter related to our operations in Mexico, we might be subject to Mexican courts or dispute resolution entities, where we would be faced with unfamiliar laws and procedures.

The resolution of disputes in foreign countries can be costly and time consuming. In a foreign country we would be faced with the additional burden of understanding unfamiliar laws and procedures. We would also be faced with the necessity of hiring lawyers and other professionals who are familiar with the foreign laws. For these reasons, we may incur unforeseen losses if we are forced to resolve a dispute in Mexico or any other foreign country.

Risks Related to Our Common Stock

We may conduct further offerings in the future in which case investors' shareholdings will be diluted.

Since our inception, we have relied on sales of our Common Stock and warrants to fund our operations. We have signed certain investment agreements with North American, for up to $15,000,000 through sales of our Common Stock, with Deer Valley, for up to $15,000,000 through sales of our Common Stock, and with KVM, for up to $5,000,000. Such investment agreements grant the investors the ability to buy a substantial number of shares of Common Stock in a series of private placement transactions at a price that is at a discount to the market price. In addition, under the Option Agreement, we must allow Gonzalez the opportunity to maintain his percentage stock ownership in the Company until the date on which we have complied fully with our obligations under the Option Agreement or January 11, 2014, whichever comes first, so any issuance of Common Stock or equivalents will result in even greater dilution because of the shares or share equivalents that will have to be issued to Jaramillo as a result. Finally, Jaramillo is entitled to 600,000 shares of Common Stock as partial consideration under the Joint Venture Agreement (the “JV Agreement”) with Jaramillo. We may conduct further equity offerings in the future to finance our current projects or to finance subsequent projects that we decide to undertake. If Common Stock is issued in return for additional funds, the price per share could be lower than that paid by our current stockholders. We anticipate continuing to rely on equity sales of our Common Stock in order to fund our business operations. If we issue additional stock, investors' percentage interests in us will be diluted. The result of this could reduce the value of current investors' stock.

10

We are subject to penny stock regulations and restrictions and you may have difficulty selling shares of our common stock.

Our Common Stock is subject to the provisions of Section 15(g) and Rule 15g-9 of the Securities Exchange Act of 1934 (the “Exchange Act”), commonly referred to as the “penny stock rule.” Section 15(g) sets forth certain requirements for transactions in penny stock, and Rule 15g-9(d) incorporates the definition of “penny stock” that is found in Rule 3a51-1 of the Exchange Act. The SEC generally defines a penny stock to be any equity security that has a market price less than $5.00 per share, subject to certain exceptions. We are subject to the SEC’s penny stock rules.

Since our Common Stock is deemed to be penny stock, trading in the shares of our Common Stock is subject to additional sales practice requirements on broker-dealers who sell penny stock to persons other than established customers and accredited investors. “Accredited investors” are persons with assets in excess of $1,000,000 (excluding the value of such person’s primary residence) or annual income exceeding $200,000 or $300,000 together with their spouse. For transactions covered by these rules, broker-dealers must make a special suitability determination for the purchase of such security and must have the purchaser’s written consent to the transaction prior to the purchase. Additionally, for any transaction involving a penny stock, unless exempt the rules require the delivery, prior to the first transaction of a risk disclosure document, prepared by the SEC, relating to the penny stock market. A broker-dealer also must disclose the commissions payable to both the broker-dealer and the registered representative and current quotations for the securities. Finally, monthly statements must be sent disclosing recent price information for the penny stocks held in an account and information to the limited market in penny stocks. Consequently, these rules may restrict the ability of broker-dealer to trade and/or maintain a market in our Common Stock and may affect the ability of our stockholders to sell their shares of Common Stock.

There can be no assurance that our shares of Common Stock will qualify for exemption from the Penny Stock Rule. In any event, even if our Common Stock was exempt from the Penny Stock Rule, we would remain subject to Section 15(b)(6) of the Exchange Act, which gives the SEC the authority to restrict any person from participating in a distribution of penny stock if the SEC finds that such a restriction would be in the public interest.

We do not expect to pay dividends in the foreseeable future.

We do not intend to declare dividends for the foreseeable future, as we anticipate that we will reinvest any future earnings in the development and growth of our business. Therefore, our stockholders will not receive any funds unless they sell their Common Stock, and stockholders may be unable to sell their shares on favorable terms or at all.

Our common stock is subject to price volatility unrelated to our operations.

The market price of our Common Stock could fluctuate substantially due to a variety of factors, including market perception of our ability to achieve our planned growth, quarterly operating results of other companies in the same industry, trading volume in our Common Stock, changes in general conditions in the economy and the financial markets or other developments affecting our competitors or ourselves. In addition, the OTCBB is subject to extreme price and volume fluctuations in general. This volatility has had a significant effect on the market price of securities issued by many companies for reasons unrelated to their operating performance and could have the same effect on our Common Stock.

11

Trading in our common stock on the OTC Bulletin Board is limited and sporadic making it difficult for our shareholders to sell their shares or liquidate their investments.

Our Common Stock is currently listed for public trading on the OTC Bulletin Board. The trading price of our Common Stock has been subject to wide fluctuations. Trading prices of our Common Stock may fluctuate in response to a number of factors, many of which will be beyond our control. The stock market has generally experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of companies with no current business operation. There can be no assurance that trading prices and price earnings ratios previously experienced by our Common Stock will be matched or maintained. These broad market and industry factors may adversely affect the market price of our Common Stock, regardless of our operating performance. In the past, following periods of volatility in the market price of a company's securities, securities class-action litigation has often been instituted. Such litigation, if instituted, could result in substantial costs for us and a diversion of management's attention and resources.

KVM will pay less than the then-prevailing market price for our common stock.

The Common Stock to be issued to KVM pursuant to the KVM Investment Agreement will be purchased at a 20% discount to the lowest trading price of our Common Stock during the ten (10) consecutive trading days immediately before KVM receives our notice of sale. KVM has a financial incentive to sell our Common Stock immediately upon receiving the shares to realize the profit equal to the difference between the discounted price and the market price. If KVM sells the shares, the price of our Common Stock could decrease. If our stock price decreases, KVM may have a further incentive to sell the shares of our Common Stock that it holds. These sales may have a further impact on our stock price.

Your ownership interest may be diluted and the value of our common stock may decline by exercising the put right pursuant to the KVM Investment Agreement.

Pursuant to the KVM Investment Agreement, when we deem it necessary, we may raise capital through the private sale of our Common Stock to KVM at a price equal to a discount to the lowest volume weighted average price of the common stock for the ten (10) consecutive trading days before KVM receives our notice of sale. Because the put price is lower than the prevailing market price of our Common Stock, to the extent that the put right is exercised, your ownership interest may be diluted.

We are registering an aggregate of 26,100,000 shares of common stock to be issued under the KVM Investment Agreement. The sales of such shares could depress the market price of our common stock.

We are registering an aggregate of 26,100,000 shares of Common Stock under the registration statement of which this prospectus is a part, pursuant to the KVM Investment Agreement. Notwithstanding KVM’s ownership limitation, the 26,100,000 shares would represent approximately 25.89% of our shares of Common Stock outstanding immediately after our exercise of the put right under the Investment Agreement. The sale of these shares into the public market by KVM could depress the market price of our Common Stock.

We may not have access to the full amount available under the KVM Investment Agreement.

Our ability to draw down funds and sell shares under the KVM Investment Agreement requires that this resale registration statement be declared effective and continue to be effective. This registration statement registers the resale of 26,100,000 shares issuable under the KVM Investment Agreement, and our ability to sell any remaining shares issuable under the KVM Investment Agreement is subject to our ability to prepare and file one or more additional registration statements registering the resale of these shares. These registration statements may be subject to review and comment by the staff of the SEC, and will require the consent of our independent registered public accounting firm. Therefore, the timing of effectiveness of these registration statements cannot be assured. The effectiveness of these registration statements is a condition precedent to our ability to sell all of the shares of Common Stock to KVM under the KVM Investment Agreement. Even if we are successful in causing one or more registration statements registering the resale of some or all of the shares issuable under the KVM Investment Agreement to be declared effective by the SEC in a timely manner, we may not be able to sell the shares unless certain other conditions are met. For example, we might have to increase the number of our authorized shares in order to issue the shares to KVM. Accordingly, because our ability to draw down any amounts under the KVM Investment Agreement is subject to a number of conditions, there is no guarantee that we will be able to draw down any portion or all of the proceeds of $5,000,000 under the KVM Investment Agreement.

12

Certain restrictions on the extent of puts and the delivery of advance notices may have little, if any, effect on the adverse impact of our issuance of shares in connection with the KVM Investment Agreement, and as such, KVM may sell a large number of shares, resulting in substantial dilution to the value of shares held by existing shareholders.

KVM has agreed, subject to certain exceptions listed in the KVM Investment Agreement, to refrain from holding an amount of shares which would result in KVM or its affiliates owning more than 4.99% of the then-outstanding shares of our Common Stock at any one time. These restrictions, however, do not prevent KVM from selling shares of Common Stock received in connection with a put, and then receiving additional shares of Common Stock in connection with a subsequent put. In this way, KVM could sell more than 4.99% of the outstanding Common Stock in a relatively short time frame while never holding more than 4.99% at one time.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Prospectus contains certain forward-looking statements. When used in this Prospectus or in any other presentation, statements which are not historical in nature, including the words “anticipate,” “estimate,” “should,” “expect,” “believe,” “intend,” “may,” “project,” “plan” or “continue,” and similar expressions are intended to identify forward-looking statements. They also include statements containing a projection of revenues, earnings or losses, capital expenditures, dividends, capital structure or other financial terms.

The forward-looking statements in this Prospectus are based upon our management’s beliefs, assumptions and expectations of our future operations and economic performance, taking into account the information currently available to them. These statements are not statements of historical fact. Forward-looking statements involve risks and uncertainties, some of which are not currently known to us that may cause our actual results, performance or financial condition to be materially different from the expectations of future results, performance or financial condition we express or imply in any forward-looking statements. These forward-looking statements are based on our current plans and expectations and are subject to a number of uncertainties and risks that could significantly affect current plans and expectations and our future financial condition and results.

We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. In light of these risks, uncertainties and assumptions, the forward-looking events discussed in this Prospectus might not occur. We qualify any and all of our forward-looking statements entirely by these cautionary factors. As a consequence, current plans, anticipated actions and future financial conditions and results may differ from those expressed in any forward-looking statements made by or on our behalf. You are cautioned not to unduly rely on such forward-looking statements when evaluating the information presented herein.

USE OF PROCEEDS

We will not receive any proceeds from the sale of shares by the selling stockholder. However, we will receive proceeds from the sale of securities pursuant to the KVM Investment Agreement. The proceeds received from any “Puts” tendered to KVM under the KVM Investment Agreement will be used for general corporate and working capital purposes and acquisitions or assets, businesses or operations or for other purposes that the Board of Directors, in its good faith deem to be in the best interest of the Company.

DILUTION

The following information is based upon the Company’s unaudited balance sheet as filed in the Company’s Form 10-Q on August 19, 2013 , for the period ended June 30, 2013 , the net tangible book value of the Company’s assets as of June 30, 2013 is $(0.00077).

“Dilution” as used herein represents the difference between the offering price per share of shares offered hereby and the net tangible book value per share of the Company’s common stock after completion of the offering. Dilution in the offering is primarily due to the losses previously recognized by the Company.

13

The net book value of the Company at June 30, 2013 was $(73,149) or $(0.001) per share. Net tangible book value represents the amount of total tangible assets less total liabilities. Assuming that 26,100,000 of the shares offered hereby were purchased by investors (a fact of which there can be no assurance) as of June 30, 2013 , the then outstanding 126,904,663 shares of common stock, which would constitute all of the issued and outstanding equity capital of the Company, would have a net tangible book value $636,771 (after deducting commissions and offering expenses) or approximately $0.005 per share.

At an assumed purchase price of $0.0272 (equal to 80% of the closing price of our common stock of $0.034 on August14, 2013 ), we will be required to issue an aggregate of 183,823,529 shares of common stock, if the full amount of $5,000,000 is exercised pursuant to the KVM Investment Agreement.

Assuming a 50% decrease to the purchase price of $0.0272 (equal to 80% of the closing price of our common stock of $0.034 on August14, 2013 ), we will be required to issue an aggregate of 367,647,058 shares of common stock, if the full amount of $5,000,000 is exercised pursuant to the KVM Investment Agreement.

Assuming a 75% decrease to the purchase price of $0.0272 (equal to 80% of the closing price of our common stock of $0.034 on August14, 2013 ), we will be required to issue an aggregate of 735 , 294 , 117 shares of common stock, if the full amount of $5,000,000 is exercised pursuant to the KVM Investment Agreement.

The dilution associated with the offering and each of the above scenarios is as follows:

|

Offering

|

183,823,529

shares issued

|

367,647,058

shares issued

|

725,294,117

shares issued

|

|||||||||||||

|

Offering price

|

$

|

0.02720

|

$

|

0.02720

|

$

|

0.01360

|

$

|

0.00680

|

||||||||

|

Net Tangible Book Value Before Offering (per share)

|

$

|

(0.001)

|

$

|

(0.001)

|

$

|

(0.001)

|

$

|

(0.001)

|

||||||||

|

Net Tangible Book Value After Offering (per share)

|

$

|

0.00498

|

$

|

0.00222

|

$

|

0.00059

|

$

|

0.00012

|

||||||||

|

Dilution per share to Investors

|

$

|

0.02222

|

$

|

0.02498

|

$

|

0.01301

|

$

|

0.006682

|

||||||||

|

Dilution percentage to Investors

|

81.69%

|

91.84%

|

95.66%

|

98.24%

|

||||||||||||

MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Public Market for Common Stock

Since June 20, 2011, shares of our common stock have been quoted on the OTCBB under the symbol “LSTG”, following the change of our corporate name to “Lone Star Gold, Inc.” From October 27, 2010 to June 20, 2011, our shares of common stock were quoted on the OTCBB under the symbol “KYSR”. Our stock began trading on October 27, 2010 at $0.155 and the stock price did not change until the July 2011. Accordingly, there are no high and low bids for the common stock before the third quarter 2011.

The following table summarizes the high and low historical closing prices reported by the OTCBB Historical Data Service for the periods indicated. OTCBB quotations reflect inter-dealer prices, without retail mark-up, mark down or commissions, so those quotes may not represent actual transactions.

|

High

|

Low

|

|||||||

|

2011

|

||||||||

|

Third Quarter 2011

|

$

|

1.40

|

$

|

0.80

|

||||

|

Fourth Quarter 2011

|

$

|

1.21

|

$

|

0.60

|

||||

|

2012

|

||||||||

|

First Quarter 2012

|

$

|

0.66

|

$

|

0.28

|

||||

|

Second Quarter 2012

|

$

|

0.23

|

$

|

0.14

|

||||

|

Third Quarter 2012

|

$

|

0.19

|

$

|

0.075

|

||||

|

Fourth Quarter 2012

|

$

|

0.09

|

$ |

0.03

|

||||

|

2013

|

||||||||

|

First Quarter 2013

|

$

|

0.158

|

$

|

0.031

|

||||

|

Second Quarter 2013

|

$

|

0.059

|

$

|

0.0306

|

||||

|

Third Quarter 2013 (Through September 19, 2013)

|

$ | 0.035 | $ | 0.021 | ||||

14

Holders

We had approximately 17 record holders of our common stock as of August 14, 2013 , according to the books of our transfer agent. The number of our stockholders of record excludes any estimate by us of the number of beneficial owners of shares held in street name, the accuracy of which cannot be guaranteed.

Dividends

There are no restrictions in our articles of incorporation or bylaws that restrict us from declaring dividends. The Nevada Revised Statutes, however, do prohibit us from declaring dividends where, after giving effect to the distribution of the dividend:

|

1.

|

we would not be able to pay our debts as they become due in the usual course of business; or

|

|

|

2.

|

our total assets would be less than the sum of our total liabilities, plus the amount that would be needed to satisfy the rights of shareholders who have preferential rights superior to those receiving the distribution.

|

We have not declared any dividends. We do not plan to declare any dividends in the foreseeable future.

Equity Compensation Plans

Other than the shares of common stock to be issued to Mr. Ferris under his Employment Agreement, as described more fully in “Executive Compensation” below, we have no equity compensation program, including no stock option plan, and none are planned for the foreseeable future.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Our discussion includes forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors, including those set forth under the Risk Factors, Cautionary Notice Regarding Forward-Looking Statements and Business sections in this Prospectus. We use words such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “could,” and similar expressions to identify forward-looking statements.

Business Overview

We are currently a start-up exploration stage company in the business of gold and mineral exploration, acquisition and development. We were incorporated in the State of Nevada under the name Keyser Resources, Inc. on November 26, 2007. Our business was initially operated to acquire an option to purchase a mining interest in Canada. After a change in control in November 2010, we explored a merger with another company in order to obtain an option to purchase several oil and gas leases in Nevada. A merger agreement was signed in January 2011. The then-current management decided not to pursue the merger, and the merger agreement was terminated by mutual agreement of the parties as of March 18, 2011.

On March 29, 2011, we underwent another change in management. On March 29, 2011, Daniel M. Ferris was elected to serve as the sole director. Mr. Ferris subsequently appointed himself President, Secretary and Treasurer. Following the appointment of Daniel M. Ferris as our sole director and officer, we changed our focus to engage in the acquisition, exploration and development of gold and silver mining properties. To further reflect this change in business focus, we changed our name to “Lone Star Gold, Inc.” on June 14, 2011. In addition, to create a more flexible capital structure, we increased the number of authorized shares of our common stock from 75,000,000 to 150,000,000 on June 14, 2011. A 20:1 forward stock split was declared to stockholders of record as of June 17, 2011.

15

Agreements

La Candelaria Project

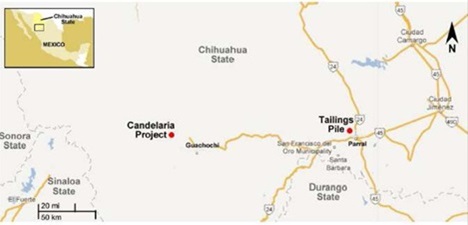

In May 2011, Metales HBG, S.A. de C.V., a company organized under the laws of Mexico (“Metales”) was formed, with the Company owning 70% of the issued and outstanding shares of capital stock. Metales owns certain gold and silver mining Concessions covering 800 hectares, or 1,976 acres, near Guachochi, Chihuahua, Mexico. The Concessions are sometimes referred to as the “La Candelaria Project”. See Note 5 to the Financial Statements.

The Company has granted anti-dilution rights to Gonzalez, such that the Company must allow Gonzalez the opportunity to maintain his percentage stock ownership in the Company until the date on which the Company has complied fully with its obligations under the Option Agreement or January 11, 2014, whichever comes first. Gonzalez has waived the exercise of his anti-dilution rights with respect to issuances of Common Stock to North American under the Investment Agreement, but has not waived those rights as to the Fairhills Investment Agreement discussed below.

If the Company fails to comply with all its obligations under the Option Agreement before January 11, 2014, the Option Agreement will terminate and the Company will be obligated to return the Concessions to Gonzalez. The Company and Gonzalez have verbally agreed that any further Work Plan payments have been put on hold until such time as the Company has sufficient capital to continue the project.

The Concessions are without known proven (measured) or probable (indicated) reserves, as defined under SEC Industry Guide 7, and the exploration program described in this Quarterly Report is exploratory in nature. See “No Proven or Probable Reserves” below.

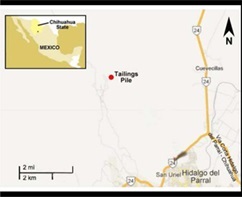

Tailings Project

On January 26, 2012, the Company, acting through a newly-formed subsidiary, Amiko Kay entered into the Joint Venture Agreement with Jaramillo to process mine tailings located in the city of Hidalgo Del Parral in the state of Chihuahua, Mexico, and, after processing, to use, market and sell any minerals extracted from the Tailings. See Note 6 to the Financial Statements for a description of the JV Agreement.

The Company is obligated to fund $250,000 for the benefit of the processing operation before January 26, 2013, under the work commitment established for the Tailings Project. For the year ended December 31, 2012, the Company made payments totaling $250,000 pursuant to the Work Commitment. For the period ended June 30, 2013 , the Company made payments totaling $10,000 towards the second year Work Commitment. See “Results of Operations” below.

On the Tailings property, two out of three on-site washing jigs are now complete and operational. The jigs separate the heavy mineral-rich material from the lighter worthless material in the Tailings. The Company has been pre-washing material for approximately three months to maximize the silver and gold content per ton of material to be shipped to nearby floatation and leaching plants in Parral, Mexico. The cost of the wash plant and jig circuit was $60,000 to date. Washing has been halted until the local plant in Parral is operational, as discussed below.

Approximately 6,000 tons of the Tailings material has been sent to the processing plant in Parral, Mexico (the "Parral Plant"). As of the date of this Quarterly Report, this shipment has not been fully processed. The Parral Plant closed unexpectedly during the third quarter of 2012 and reopened in March 2013. It has operated sporadically since March 2013 and has not been able to operate on a consistent basis. Accordingly, the Company estimates that the Parral Plant has accumulated a one year backlog of tailings to process, and the Company does not believe that it can rely on the Parral Plant to process a significant amount of the tailings in the foreseeable future. The Company has developed plans to build its own plant capable of processing 150 tons of tailings per day. The cost to build such a plant is estimated to be $1M. The Company is actively seeking investors to fund the construction of a plant. Accordingly, the Company has no revenues from the Tailings as of the date of filing.

No Proven or Probable Reserves

16

We are a start-up, exploration-stage company engaged in the search for gold and related minerals. No proven (measured) or probable (indicated) reserves have been established with respect to the La Candelaria project or the Tailings project, and the proposed program of exploration and development for the La Candelaria project and the Tailings project is exploratory in nature. There is no assurance that a commercially viable mineral deposit, or reserve, exists on the property covered by the Concessions or the Tailings project or can be shown to exist until sufficient and appropriate exploration is done, and a comprehensive evaluation of such work concludes that the extraction of such a mineral deposit, if found, can be economically and legally feasible.

Recent Development

KVM Investment Agreement

On June 27, 2013, we entered into the KVM Investment Agreement with KVM Capital Partners pursuant to which KVM agreed to purchase shares of our common stock for an aggregate purchase price of up to $5,000,000.

The KVM Investment Agreement provides that we may, from time to time during the thirty-six (36) months period commencing from the effectiveness of the registration statement, in our sole discretion, deliver a put notice to KVM which states the dollar amount that we intend to sell to KVM on a date specified in the put notice. The maximum investment amount per notice shall be no more than two hundred percent (200%) of the average daily volume of the common stock for the ten consecutive trading days immediately prior to date of the applicable put notice. The purchase price per share to be paid by KVM shall be calculated at a twenty percent (20%) discount to the lowest volume weighted average price of the common stock as reported by Bloomberg, L.P. during the ten (10) consecutive trading days immediately prior to the receipt by KVM of the put notice. We have reserved 30,000,000 shares of our common stock for issuance under the KVM Investment Agreement.

We plan to use the proceeds from the sale of the common stock under the KVM Investment Agreement for general corporate and working capital purposes and acquisitions or assets, businesses or operations or for other purposes that the Board of Directors, in its good faith deem to be in the best interest of the Company.

Results of Operations

We have not generated any revenue since our inception. We do not anticipate earning revenues until we have begun to commercially produce minerals from the Concessions, the Tailings, or other mineral properties that we may own in the future.

Three months ended June 30, 2013 and 2012

For the periods below, we had the following expenses:

|

For the Three months Ended June 30,

|

||||||||

|

2013

|

2012

|

|||||||

|

General and administrative

|

$

|

100,768

|

$

|

63,852

|

||||

|

Exploration

|

-

|

108,500

|

||||||

|

Management fees

|

303,699

|

279,999

|

||||||

|

Total operating expenses

|

$

|

404,467

|

$

|

452,351

|

||||

For the three months ended June 30, 2013 , we incurred general and administrative expenses totaling $100,768. This was an increase of $36,916 compared to the second quarter of 2012.

For the three months ended June 30, 2012, we incurred general and administrative expenses totaling $63,852. In 2012, our expenses consisted, primarily, of general and administrative expenses and office supplies of $35,764, legal fees of $17,258, accounting and auditing fees of $2,575, depreciation expense of $2,340 and rent expense of $1,297.

There we no exploration expenses for the three months ended June 30, 2013.

For the three months ended June 30, 2012, we incurred aggregate Exploration costs of $108,500 are costs of $3,500 related to the La Candelaria Project and costs of $90,000 related to the Tailings Project. With respect to the La Candelaria Project, we paid a total of $3,500 under the Work Plan for La Candelaria. With respect to the Tailings Project, the Company made payments of $90,000 to the Joint Venture, which includes approximately $40,000 for construction of the wash plant, $40,000 for equipment and trucks and $10,000 for repairs, fuel, taxes, insurance, office and management costs.

During the three months ended June 30, 2013, the Company paid management fees totaling $53,700 to our sole officer and director and recognized $249,999 in expenses related to the stock grant under Mr. Ferris’ Employment Agreement.

17

Six months ended June 30, 2013 and 2012

For the periods below, we had the following expenses:

|

For the Six months Ended June 30,

|

||||||||

|

2013

|

2012

|

|||||||

|

General and administrative

|

$

|

205,986

|

$

|

215,916

|

||||

|

Exploration

|

24,500

|

465,196

|

||||||

|

Management fees

|

583,698

|

559,998

|

||||||

|

Total operating expenses

|

$

|

814,184

|

$

|

1,241,110

|

||||

For the six months ended June 30, 2013, we incurred operating expenses totaling $814,184. This was a decrease of $426,926 compared to the six months ended June 30, 2012. In 2013, our expenses consisted, primarily, of accounting and auditing fees of $87,271, legal and other professional fees of $98,608, depreciation expense of $4,680 and travel expenses of $15,427.

For the six months ended June 30, 2012, we incurred general and administrative expenses totaling $215,916. In 2012, our expenses consisted, primarily, of professional fees of $59,095, accounting and auditing fees of $40,362, legal fees of $37,237, telephone expense of $5,301, travel of $2,229, depreciation expense of $2,340 and rent expense of $2,696.

Included in Exploration expenses of $24,500 for the six months ended June 30, 2013 are costs of $24,500 related to the Tailings and La Candelaria Projects. With respect to the Tailings Project, the Company made a payment of $10,000 for services from a mining consultant. For La Candelaria, the Company made a payment of $14,500 to Mining Capital Advisors for services.

For the six months ended June 30, 2012, we incurred aggregate Exploration costs of $465,196. Costs related to the La Candelaria Project totaled $185,195 and funding of the Tailings Project totaled $250,000. With respect to the La Candelaria Project, we paid a total of $60,195 under the Work Plan for La Candelaria, and made $125,000 in payments to Homero Gonzalez under the Option Agreement. With respect to the Tailings Project, the Company made payments of $250,000 to the Joint Venture, which includes approximately $60,000 for construction of the wash plant, $122,500 for equipment and trucks and $67,500 for repairs, fuel, taxes, insurance, office and management costs.

During the six months ended June 30, 2013, the Company paid management fees totaling $83,700 to our sole officer and director and recognized $499,998 in expenses related to the stock grant under Mr. Ferris’ Employment Agreement.

Results of Operations for the Year Ended December 31, 2012 as Compared to the Year Ended December 31, 2011

We have not generated any revenue since our inception. For the years ended December 31, 2012 and 2011, we had the following expenses:

|

For the year

ended

December 31,

2012

|

For the year

ended

December 31,

2011

|

|||||

|

General and administrative

|

$

|

350,447

|

$

|

486,741

|

||

|

Exploration cost

|

495,195

|

530,925

|

||||

|

Management fees

|

1,119,996

|

543,974

|

||||

|

$

|

1,965,638

|

$

|

1,561,640

|

|||

For the year ended December 31, 2012, we incurred $350,447 in general and administrative expenses, $495,195 in exploration costs and $1,119,996 in management fees. Our general and administrative fees were primarily for legal costs and accounting and auditing fees. Management fees include cash compensation and the value ($999,996) of the equity compensation paid to Mr. Ferris. Exploration costs include direct costs associated with La Candelaria of $213,500 and the Tailings Project of $280,000.

For the year ended December 31, 2011, we incurred $486,741 in general and administrative expenses, $530,925 in exploration costs and $543,974 in management fees. Our general and administrative fees were primarily for legal costs and accounting and auditing fees. Management fees include cash compensation and the value ($473,974) of the equity compensation paid to Mr. Ferris. Exploration costs include direct costs associated with La Candelaria of $201,925 and the value of stock issued to Gonzalez of $303,000.

The following is a summary of our balance sheets as of June 30 , 2013 and December 31, 2012:

|

|

June 30 , 2013

|

December 31, 2012

|

||||||

|

Cash

|

$ | - | $ | - | ||||

|

Current Liabilities

|

290,301 | 320,053 | ||||||

|

Working Capital Deficit

|

(286,122 | ) | (319,901 | ) | ||||

|

Shareholders’ Equity (Deficit)

|

(73,149 | ) | (102,248 | ) | ||||

18

We have committed to fund $450,000 over three years under the La Candelaria Work Plan, and $1,000,000 over two years under the work commitment for the Tailings Project. Because the Company has no revenues from operations, we are dependent upon obtaining additional financing in order to fund our obligations under the Work Plan, and also to fund our obligations under the Tailings Project. The Company has funded its exploratory program to date primarily through sales of its restricted common stock.

During the six months ended June 30, 2013, we received $375,000 from the sale of 10,810,000 shares of common stock under the Fairhills Investment Agreement, which we used to make certain payments relating to the Company’s Tailings Project, and for general operating expenses. Additionally, we received $42,500 in net proceeds from a loan from KVM (See Note 3 - Debt).

In June 2013, the Company entered into the KVM Investment Agreement with KVM whereby KVM agreed to purchase up to $5 million of the Company’s common stock over a period of up to 36 months.