UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2015 | |

| Or | |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ______________ to _____________ | |

Commission File Number 000-54010

B. RILEY FINANCIAL, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 27-0223495 |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

| 21860 Burbank Boulevard, Suite 300 South Woodland Hills, CA |

91367 |

| (Address of Principal Executive Offices) | (Zip Code) |

(818) 884-3737

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.0001 per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes: ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes: x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or such shorter period that the registrant was required to submit and post such files). Yes: x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes: ¨ No x

The aggregate market value of the registrant’s common stock held by non-affiliates, based on the closing price of the registrant’s common stock as reported on the OTC Bulletin Board on June 30, 2015, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $61.0 million. For purposes of this calculation, it has been assumed that all shares of the registrant's common stock held by directors, executive officers and stockholders beneficially owning ten percent or more of the registrant's common stock are held by affiliates. The treatment of these persons as affiliates for purposes of this calculation is not conclusive as to whether such persons are, in fact, affiliates of the registrant.

The number of shares outstanding of the registrant’s common stock as of March 21, 2016 was 16,614,786.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement relating to the registrant’s 2016 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report.

B. RILEY FINANCIAL, INC.

INDEX TO ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2015

| 2 |

This Annual Report on Form 10-K (this “Annual Report”) contains forward-looking statements regarding our business, financial condition, results of operations and prospects. Words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “may,” “will,” “predict,” “potential,” “continue,” “estimate” and similar expressions are generally intended to identify forward-looking statements, but are not exclusive means of identifying forward-looking statements in this Annual Report. You should not place undue reliance on such forward-looking statements, which are based on the information currently available to us and speak only as of the date on which this Annual Report was filed with the Securities and Exchange Commission (the “SEC”). Because these forward-looking statements involve known and unknown risks and uncertainties, there are important factors that could cause actual results, events or developments to differ materially from those expressed or implied by these forward-looking statements, including our plans, objectives, expectations and intentions and other factors discussed in “Part I—Item 1A. Risk Factors” contained in this Annual Report. Risk factors that could cause actual results to differ from those contained in the forward-looking statements include but are not limited to risks related to: volatility in our revenues and results of operations; changing conditions in the financial markets; our ability to generate sufficient revenues to achieve and maintain profitability; the short term nature of our engagements; the accuracy of our estimates and valuations of inventory or assets in “guarantee” based engagements; competition in the asset management business; potential losses related to our auction or liquidation engagements; our dependence on communications, information and other systems and third parties; potential losses related to purchase transactions in our auction and liquidations business; the potential loss of financial institution clients; potential losses from or illiquidity of our proprietary investments; changing economic and market conditions; potential liability and harm to our reputation if we were to provide an inaccurate appraisal or valuation; potential mark-downs in inventory in connection with purchase transactions; failure to successfully compete in any of our segments; loss of key personnel; our ability to borrow under our credit facilities as necessary; failure to comply with the terms of our credit agreements; and our ability to meet future capital requirements. We undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Except as otherwise required by the context, references in this Annual Report to “the Company,” “B. Riley,”“we,” “us” or “our” refer to the combined business of B. Riley Financial, Inc. and all of its subsidiaries.

| Item 1. | BUSINESS |

General

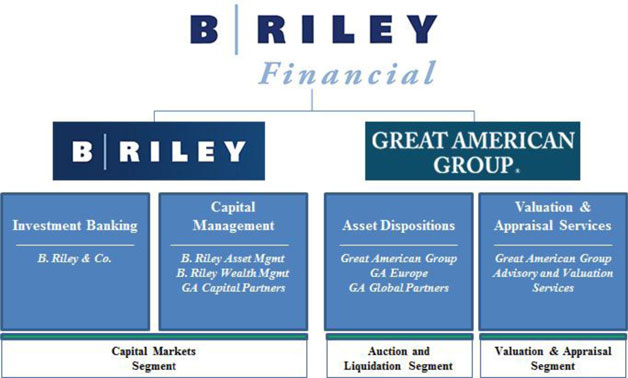

B. Riley Financial, Inc. and its subsidiaries provide collaborative financial services and solutions through several subsidiaries, including:

| § | B. Riley & Co., LLC (“BRC”), a mid-sized, full service investment bank providing financial advisory, corporate finance, research, and sales & trading services to corporate, institutional and high net worth individual clients; |

| § | B. Riley Capital Management, LLC, an Securities and Exchange Commission (“SEC”) registered investment advisor, which includes: |

| o | B. Riley Asset Management, an advisor to certain public and private funds and to institutional and high net worth investors; |

| o | B. Riley Wealth Management (formerly MK Capital Advisors), a multi-family office practice and wealth management firm focused on the needs of ultra-high net worth individuals and families; and |

| o | Great American Capital Partners, LLC (“GACP”), the general partner of a private fund, GACP I, L.P. a direct lending fund that provides senior secured loans and second lien secured loan facilities to middle market public and private U.S. companies |

| § | Great American Group, LLC, a leading provider of asset disposition and auction solutions to a wide range of retail and industrial clients; and |

| § | Great American Group Advisory and Valuation Services, LLC, a leading provider of appraisal and valuation services for asset based lenders, private equity firms and corporate clients. |

We are headquartered in Los Angeles with offices in major financial markets throughout the United States and Europe.

| 3 |

For financial reporting purposes we classify our businesses into three segments: (i) capital markets, (ii) auction and liquidation and (iii) valuation and appraisal.

Capital Markets Segment. Our capital markets segment provides a full array of investment banking, corporate finance, research, wealth management, sales and trading services to corporate, institutional and high net worth clients. Our corporate finance and investment banking services include merger and acquisitions advisory services to public and private companies, initial and secondary public offerings, and institutional private placements. In addition, we trade equity securities as a principal for the Company’s account, including investments in funds managed by our subsidiaries. Our capital markets segment also includes our asset management businesses that manage various private and public funds for institutional and individual investors.

Auction and Liquidation Segment. Our auction and liquidation segment utilizes our significant industry experience, a scalable network of independent contractors and industry-specific advisors to tailor our services to the specific needs of a multitude of clients, logistical challenges and distressed circumstances. Furthermore, our scale and pool of resources allow us to offer our services across North American as well as parts of Europe, Asia and Australia. Our auction and liquidation segment operates through two main divisions, retail store liquidations and wholesale and industrial assets dispositions. Our wholesale and industrial assets disposition division operates through limited liability companies that are controlled by us.

Valuation and Appraisal Segment. Our valuation and appraisal segment provides valuation and appraisal services to financial institutions, lenders, private equity firms and other providers of capital. These services primarily include the valuation of assets (i) for purposes of determining and monitoring the value of collateral securing financial transactions and loan arrangements and (ii) in connection with potential business combinations. Our valuation and appraisal segment operates through limited liability companies that are majority owned by us.

Private Placement and Strategic Combination

On June 5, 2014, we completed a private placement of 10,289,300 shares of our common stock at a purchase price of $5.00 per share (the “Private Placement”). Fifty-three accredited investors (the “Investors”) participated in the Private Placement pursuant to the terms and provisions of a securities purchase agreement entered into among us and the Investors on May 19, 2014. At the closing of the Private Placement on June 5, 2014, we received net proceeds of approximately $51.2 million. On June 5, 2014, we used $30.2 million of the net proceeds from the Private Placement to repay long-term debt payable to Andrew Gumaer and Harvey Yellen, both of whom were executive officers and directors of the Company at the time of such repayment. The $30.0 million principal payment and then outstanding accrued interest of $0.2 million retired the entire $48.8 million face amount of the long-term debt at a discount of $18.8 million. The discount of $18.8 million has been recorded as a capital contribution to additional paid in capital in our consolidated financial statements.

| 4 |

On June 18, 2014, we completed the acquisition of B. Riley and Co. Inc. (“BRC Inc.”) pursuant to the terms of the Acquisition Agreement (the Acquisition Agreement”), dated as of May 19, 2014, by and among the Company, Darwin Merger Sub I, Inc., a wholly owned subsidiary of the Company, B. Riley Capital Markets, LLC, a wholly owned subsidiary of the Company (“BCM”), BRC Inc., B. Riley & Co. Holdings, LLC (“BRH”), Riley Investment Management LLC (“RIM”), and collectively with BRC Inc. and BRH, the (“B. Riley Entities”) and Bryant Riley, a director of the Company and principal owner of each of the B. Riley Entities. In connection with the Company’s acquisition of BRC Inc., Darwin Merger Sub I, Inc. merged with and into BRC Inc., and BRC Inc. subsequently merged with and into BCM, with BCM surviving as a wholly owned subsidiary of the Company. We completed the acquisitions of BRH, whose operations include asset management and financial advisory services, and RIM, which provides services to certain pooled investment vehicles, on August 1, 2014.

The total purchase price for the B. Riley Entities was $26.4 million, which was paid at closing on June 18, 2014, or through post-closing adjustments and arrangements, in the form of 4,182,637 newly issued shares of our common stock. The fair value of the newly issued shares of the Company’s common stock for accounting purposes was determined based on the closing market price of the Company’s shares of common stock on the acquisition date, less a 25% discount for lack of marketability as the shares issued are subject to certain restrictions that limit their trade or transfer in the open market.

Effective upon the closing of the acquisition on June 18, 2014, Bryant Riley, the principal owner of BRC Inc., was appointed as our Chief Executive Officer and Chairman. As a result of the acquisition of BRC Inc., Bryant Riley owns approximately 24.1% of our outstanding common stock.

Recent Developments

On January 2, 2015, we entered into a purchase agreement to acquire all of the membership interests of MK Capital Advisors, LLC (“MK Capital”), a wealth management business with operations primarily in New York. On February 2, 2015, the pre-closing conditions were satisfied and we completed the purchase of MK Capital. Upon closing, we paid the members of MK Capital $2.5 million in cash and issued 333,333 shares of our common stock to such members. The purchase agreement also requires the payment of contingent consideration of $1.25 million in cash and 166,667 shares of our common stock on the first anniversary date of the closing (February 2, 2016) and a final payment of $1.25 million in cash and 166,666 of our common stock on the second anniversary date of the closing (February 2, 2017). Such contingent consideration is contingent on MK Capital generating a minimum amount of gross revenues as defined in the purchase agreement for the twelve months ending on the first and second anniversary dates of the closing. MK Capital achieved the minimum amount of revenues for the first anniversary period and the contingent cash consideration and contingent stock consideration for such first anniversary period was paid and issued on February 2, 2016. The acquisition of MK Capital allows the Company to expand into the wealth management business..

In April 2015, we announced the formation of GACP, a wholly owned subsidiary of the Company, and GACP I, L.P., a private direct lending fund of which GACP is the general partner, together with an anchor investment from a business development company advised by a large financial services company. GACP I, L.P. provides asset-based loans to middle market companies. GACP leverages the knowledge and expertise of Great American Group’s liquidation and appraisal business to provide insight into asset collateral values that support the asset-based loans. We believe that this internal expertise in assessing collateral values provides GACP with a competitive advantage over other middle market direct lenders. In connection with the formation of GACP I, L.P., we committed to invest $5.0 million in exchange for an ownership interest of approximately 5% of GACP I, L.P. As of December 31, 2015, we funded $1.7 million of the $5.0 million commitment to invest in GACP I, L.P.

In February 2016, we announced the hiring of a senior managing director to form and head our corporate restructuring practice group. Our new senior managing director brings extensive experience in the retail, healthcare, real estate, energy, and communications sectors and has advised municipalities and other governmental entities. He was named the 2014 "Turnaround Consultant of the Year" by The M&A Advisor and a Top 100 Global Restructuring and Turnaround Professional by Global M&A Network.

| 5 |

B. Riley

Investment Banking and Corporate Finance

B. Riley investment banking professionals provide equity and debt capital raising, merger and acquisition and financial advisory services to both private and publicly traded companies. Those services include: follow-on public offerings, debt and equity private placements, debt refinancings, corporate debt and equity security repurchases, and buy-side and sell-side representation, divestitures/carveouts, leveraged buyouts, management buyouts, strategic alternatives reviews, fairness opinions, valuations, return-of-capital advisory, hostile/activist advisory, and options trading programs.

Sales, Trading and Corporate Services

Our sales and trading professionals distribute B. Riley proprietary research products to our institutional investor clients and high net worth individuals. B. Riley sales and trading also sells the securities of companies in which B. Riley acts as an underwriter and executes equity trades on behalf of clients. We maintain active trading relationships with substantially all major institutional money managers. Our equity and fixed income traders make markets in approximately 150 securities. Our corporate services include retail orders, block trades, Rule 144 transactions, cashless exercise of options, and corporate equity repurchase programs.

Equity Research

Our equity research is focused on fundamentals-based research. Our research focuses on an in-depth analysis of earnings, cash flow trends, balance sheet strength, industry outlook, and strength of management that involves extensive meetings with key management, competitors, channel partners and customers. We provide research on all sizes of firms; however, our research primarily focuses on small and mid-cap stocks that are under-followed by Wall Street. Our analysts regularly communicate their findings through Research Updates and daily Morning Notes.

Our research department includes research analysts maintaining coverage on a variety of companies in a variety of industry sectors. Our research department annually organizes non-deal road shows for issuers in our targeted industries. To provide our institutional clients access to management teams of companies in our coverage universe and others, our research department has held 16 consecutive annual institutional investor conferences.

Capital Management

We provide investment management services under our subsidiary, B. Riley Capital Management, LLC, an SEC registered investment advisor. The registered investment advisor manages one mutual fund and certain other private investment funds, including a fund of funds. All of the funds managed typically invest in both public and private equity and debt. Investors for the various funds include institutional, high net worth, and individual investors. GACP is the general partner of GACP I, L.P., a direct lending fund that provides asset based loans to middle market companies.

Wealth Management

In February 2015, we acquired MK Capital, a wealth management business with operations primarily in New York, and subsequently changed the name to “B. Riley Wealth Management”. Our wealth management business provides comprehensive investment advisory services to ultrahigh net worth families and individuals. We provide traditional asset management, alternative asset management and trust and estate planning to our clients. B. Riley Wealth Management is a division of B. Riley Capital Management, LLC, an SEC registered investment advisor.

Proprietary Trading

We engage in trading activities for strategic investment purposes (i.e proprietary trading) utilizing the firm’s capital. Proprietary trading activities include investments in public and private stock and debt securities. In 2010, the federal government passed the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”). Dodd-Frank significantly restructures and intensifies regulation in the financial services industry and includes a section referred to as the “Volcker Rule”. The Volcker Rule provides for a limitation on proprietary trading and investments by certain bank holding companies. We are not a bank holding company and, as a result, the limitations applicable to bank holding companies regarding proprietary trading and investment in the Volcker Rule do not apply to us.

The business described above for B. Riley is reported in our capital markets segment for financial reporting purposes.

| 6 |

Great American Group

Retail Store Liquidations

We enable our clients to quickly and efficiently dispose of under-performing assets and generate cash from excess inventory by conducting or assisting in retail store closings, going out of business sales, bankruptcy sales and fixture sales. With the goal of providing a single-source solution to our retail clients, we also provide merger and acquisition due diligence through our auction and liquidation segment and reverse logistics and appraisal services through our valuation and appraisal segment. Financial institution and other capital providers rely on us to maximize recovery rates in distressed asset sales and in retail bankruptcy situations. Additionally, healthy, mature retailers utilize our proven inventory management and strategic disposition solutions, relying on our extensive network of retail professionals, to close unproductive stores and dispose of surplus inventory and fixtures as existing stores are updated. For example, in a potential bankruptcy engagement, the debtor provides potential disposition firms with a snapshot of inventory and other assets available for sale. The disposition firms must analyze the inventory data and generate an estimate of potential recovery based on their valuation expertise and past liquidation experience. The disposition firms then submit bids that guarantee a minimum recovery based on a percentage of retail value or cost. The successful bidder assumes management of the debtor’s stores on a contract basis and conducts the orderly disposition of the inventory and assets in these stores. Profits are generated by efficiently merchandizing inventory, managing the orderly closing of store locations and pricing remaining products to balance margin with speed of sale and liquidation expenses. Unlike merchandisers who employ a “top down” approach by focusing only on driving total sales (because overhead costs are fixed), disposition firms take a “bottom up” approach by focusing on balancing cost savings with maximizing proceeds. A typical retail disposition process spans eight to twelve weeks from the bankruptcy court’s approval of the successful bid to the final store closure.

We often conduct large retail liquidations that entail significant capital requirements through collaborative arrangements with other liquidators. By entering into an agreement with one or more collaborators, we are able to bid on larger engagements that we couldn’t conduct on our own due to the significant capital outlay involved, number of independent contractors required or financial risk associated with the particular engagement. We act as the lead partner in many of the collaborative arrangements that we enter into, meaning that we have primary responsibility for the due diligence, contract negotiation and execution of the engagement.

Wholesale and Industrial Asset Dispositions

We design and implement customized disposition programs for our clients seeking to convert excess wholesale and industrial inventory and operational assets into capital. We dispose of a wide array of assets including, among others, equipment related to transportation, heavy mobile construction, energy exploration and services, metal fabrication, food processing, semiconductor fabrication, and distribution services. We manage projects of all sizes and scopes across a variety of asset categories. We believe that our databases of information regarding potential buyers that we have collected from past transactions and engagements, our nationwide name recognition and experience with alternative distribution channels allow us to provide superior wholesale and industrial disposition services.

We offer clients various wholesale and industrial disposition strategies including, among others, live auctions, webcast auctions, and online auctions. The live public auction is the most traditional sales technique for wholesale and industrial asset dispositions and one of our most frequently utilized services. In live auctions, bidders gather at a specified date and time to competitively bid against one another, with each item selling to the highest bidder. We believe that our auctioneers are recognized throughout the industry for their auctioneering skills, project experience, engaging personalities and ability to extract top prices. Our live auctions can cover single sites or multiple locations, and we utilize point-of-sale software to generate customized sales reports and invoices and to track assets. Increasingly, we have been webcasting our live auctions over the Internet. This auction format allows online bidders to compete in real time against bidders at the live auction. Bidders can log onto the auction from personal computers, view and bid on lots as they come up for sale, hear the auctioneers as the sale is being conducted and, in some cases, view live streaming video of the auctioneer calling the bids on-site. We believe that this auction format maximizes proceeds by providing access to otherwise unavailable potential bidders, including international participants, thereby increasing competition. In some cases, particularly when assets are located in remote areas that are not easily accessible to bidders, we may determine, in consultation with the client, that a webcast only auction is the most appropriate format. In the online auction format, the sale of assets takes place exclusively online, without a live auctioneer calling the sale. Similar to the timed auctions popularized by online auction sites such as eBay, assets are posted for sale online and buyers can bid on lots and items for a set period of time, usually one week. The online auction format is optimal for clients that have idle assets in quantities insufficient to justify the cost of a live auction. We conduct our wholesale and industrial disposition business throughout parts of North America, Europe, Asia and Australia. Our business is primarily conducted through GA Global Partners, LLC, a 50% owned subsidiary that is controlled by us.

| 7 |

Great American Group provides the foregoing services to clients on a guarantee, fee or outright purchase basis.

Guarantee. When providing services on a guarantee basis, we guarantee the client a specific recovery often expressed as a percentage of retail inventory value or wholesale inventory cost or, in the case of machinery or equipment, a set dollar amount. This guarantee is often required to be supported by a letter of credit, a cash deposit or a combination thereof. Cash deposits are typically funded in part with available cash together with short term borrowings under our credit facilities. Often when we provide auction or liquidation services on a guarantee basis, we do so through a collaborative arrangement with other service providers. In this situation, each collaborator agrees to provide a certain percentage of the guaranteed amount to the client through a combination of letters of credit, cash and financing. If we are engaged individually, we receive 100% of the net profit, less debt financing fees, sale related expenses (if any) and any share of the profits due to the client as a result of any profit sharing arrangement entered into based on a pre-negotiated formula. If the engagement was conducted through a collaborative arrangement, the profits or losses are divided among us and our partner or partners as set forth in the agreement governing the collaborative arrangement. If the net sales proceeds after expenses are less than the guarantee, we, together with our partners if the engagement was conducted through a collaborative arrangement, are responsible for the shortfall and will recognize a loss on the engagement.

Fee. When we provide services on a fee basis, clients pay a pre-negotiated flat fee for the services provided, a percentage of asset sales generated or a combination of both.

Outright Purchase. When providing services on an outright purchase basis, we purchase the assets from the client and typically sell them at auction, orderly liquidation, through a third-party broker or, less frequently, as augmented inventory in conjunction with another liquidation that we are conducting. In an outright purchase, we take, together with any collaboration partners, title to the assets and absorb the profit or loss associated with the asset disposition.

The retail store liquidations and wholesale and industrial asset dispositions business of Great American Group described above is reported in our auction and liquidation segment for financial reporting purposes.

Valuation and Appraisal

Our valuation and appraisal teams provide independent appraisals to financial institutions, lenders, private equity firms and other providers of capital for estimated liquidation values of assets. These teams include experts specializing in particular industry niches and asset classes. We provide valuation and appraisal services across five general categories:

Consumer and Retail Inventory. Representative types of appraisals and valuations include inventory of specialty apparel retailers, department stores, jewelry retailers, sporting goods retailers, mass and discount merchants, home furnishing retailers and footwear retailers.

Wholesale and Industrial Inventory. Representative types of appraisals and valuations include inventory held by manufacturers or distributors of automotive parts, chemicals, food and beverage products, wine and spirits, building and construction products, industrial products, metals, paper and packaging.

Machinery and Equipment. Representative types of asset appraisals and valuations include a broad range of equipment utilized in manufacturing, construction, transportation and healthcare.

Intangible Assets. Representative types of asset appraisals and valuations include intellectual property, goodwill, brands, logos, trademarks and customer lists.

Real Estate. Representative types of asset appraisals and valuations include owned and leased manufacturing and distribution facilities, retail locations and corporate offices. We do not perform appraisals of residential properties.

We provide valuation and appraisal services on a pre-negotiated flat fee basis.

The valuation and appraisal services business of Great American Group described above is reported in our valuation and appraisal segment for financial reporting purposes.

| 8 |

UK Retail Stores

We previously had an additional operating segment relating to UK retail stores. Our UK retail stores segment included the operations of ten retail footwear stores in the United Kingdom as a result of our investment in Shoon Trading Limited (“Shoon”) on May 4, 2012. We ceased to consider this a separate operating segment in August 2013 following the amendment and restatement of a shareholders agreement for Shoon which eliminated our control rights. As a result of this amendment, Shoon’s operating results are not consolidated with the Company’s for any periods after July 31, 2013. Notwithstanding the deconsolidation, our operating results for periods from July 31, 2013 to January 2014 include the income (loss) from our 44.4% equity investment in the common stock of Shoon. In January 2014, Shoon was sold to a third party, and we no longer have a financial interest in the operations of Shoon.

Customers

We serve retail, corporate, capital provider and individual customers across our services lines. Revenues from liquidation service contracts to one retailer represented 12.4% of our total revenues during the year ended December 31, 2015. Revenues from one liquidation service contract and the sale of four oil rigs to one customer represented 10.7% and 12.2% of total revenues during the year ended December 31, 2013. The services provided to these customers were under short-term liquidation contracts that generally do not exceed a period of six months. There were no recurring revenues from year-to-year in connection with the services we performed under these contracts.

B. Riley

We are engaged by corporate customers, including publicly held and privately owned companies, to provide investment banking, corporate finance, research and sales and trading services. We also provide corporate finance, research, wealth management, and sales and trading services to high net worth individuals. We maintain client relationships with companies in the consumer goods, consumer services, defense, industrials and technology industries.

Great American Group

Our retail auction and liquidation clients include financially healthy retailers as well as distressed retailers, bankruptcy professionals, financial institution workout groups and a wide range of professional service providers. Some retail segments in which we specialize include apparel, arts and crafts, department stores, discount stores, drug / health and beauty, electronics, footwear, grocery stores, hardware / home improvement, home goods and linens, jewelry, office / party supplies, specialty stores, and sporting goods. Previous clients include Target, Cache, Orchard Supply Stores, Blockbuster Video, Borders Group, Circuit City, Friedman’s Jewelers, Fortunoff, Office Depot, TJ Hughes, Hancock Fabrics, Movie Gallery, Linens N Things, and Kmart.

We provide wholesale and industrial auction services and customized disposition programs to a wide range of clients. Specifically, we have experience in providing auction and liquidation solutions to the following industries: aircraft / aerospace, casino / hospitality, construction / mining / earthmoving, food and beverage processing, hospital / medical, machine tools / metalworking, material handling, packaging / bottling, plastics and rubber processing, printing / bindery, pulp processing / paper converting, restaurant / bar / bakery, retail / trade fixtures, stadium / arena, textile / apparel, transportation / rolling stock, warehouse / distribution centers, and woodworking / lumber. Representative recent clients include Boeing, Hollywood Park, Stardust Hotel & Casino, Midas International, James River Coal Company, Lillian Vernon, and Saint Vincent Medical Center of New York.

We are engaged by financial institutions, lenders, private equity firms and other capital providers, as well as professional service providers, to provide valuation and advisory services. We have extensive experience in the appraisal and valuation of retail and consumer inventories, wholesale and industrial inventories, machinery and equipment, intellectual property and real estate. We maintain ongoing client relationships with major asset based lenders including Bank of America, Credit Suisse, GE Capital, JPMorgan Chase, Union Bank of California, and Wells Fargo. Our clients also include private equity firms such as Apollo Management, Goldman Sachs Capital Partners, and Sun Capital Partners.

Competition

B. Riley

We face intense competition for our capital markets services. Since the mid-1990s, there has been substantial consolidation among U.S. and global financial institutions. In particular, a number of large commercial banks, insurance companies and other diversified financial services firms have merged with other financial institutions or have established or acquired broker-dealers. During 2008, the failure or near-collapse of a number of very large financial institutions led to the acquisition of several of the most sizeable U.S. investment banking firms, consolidating the financial industry to an even greater extent. Currently, our competitors are other investment banks, bank holding companies, brokerage firms, merchant banks and financial advisory firms. Our focus on our target industries also subjects us to direct competition from a number of specialty securities firms and smaller investment banking boutiques that specialize in providing services to these industries.

| 9 |

The industry trend toward consolidation has significantly increased the capital base and geographic reach of many of our competitors. Our larger and better-capitalized competitors may be better able than we are to respond to changes in the investment banking industry, to recruit and retain skilled professionals, to finance acquisitions, to fund internal growth and to compete for market share generally. Many of these firms have the ability to offer a wider range of products than we do, including loans, deposit-taking and insurance, in addition to brokerage, asset management and investment banking services, all of which may enhance their competitive position relative to us. These firms also have the ability to support investment banking and securities products with commercial banking, insurance and other financial services revenues in an effort to gain market share, which could result in downward pricing pressure in our businesses. In particular, the trend in the equity underwriting business toward multiple book runners and co-managers has increased the competitive pressure in the investment banking industry and has placed downward pressure on average transaction fees.

As we seek to expand our asset management business, we face competition in the pursuit of investors for our investment funds, in the identification and completion of investments in attractive portfolio companies or securities, and in the recruitment and retention of skilled asset management professionals.

Great American Group

We also face intense competition in our other service areas. While some competitors are unique to specific service offerings, some competitors cross multiple service offerings. A number of companies provide services or products to the auction and liquidation and valuation and appraisal markets, and existing and potential clients can, or will be able to, choose from a variety of qualified service providers. Some of our competitors may even be able to offer discounts or other preferred pricing arrangements. In a cost-sensitive environment, such arrangements may prevent us from acquiring new clients or new engagements with existing clients. Some of our competitors may be able to negotiate secure alliances with clients and affiliates on more favorable terms, devote greater resources to marketing and promotional campaigns or to the development of technology systems than us. In addition, new technologies and the expansion of existing technologies with respect to the online auction business may increase the competitive pressures on us. We must also compete for the services of skilled professionals. There can be no assurance that we will be able to compete successfully against current or future competitors, and competitive pressures we face could harm our business, operating results and financial condition.

We face competition for our retail services from traditional liquidators as well as Internet-based liquidators such as overstock.com and eBay. Our wholesale and industrial services competitors include traditional auctioneers and fixed site auction houses that may specialize in particular industries or geographic regions as well as other large, prestigious or well-recognized auctioneers. We also face competition and pricing pressure from the internal remarketing groups of our clients and potential clients and from companies that may choose to liquidate or auction assets and/or excess inventory without assistance from service providers like us. We face competition for our valuation and appraisal services from large accounting, consulting and other professional service firms as well as other valuation, appraisal and advisory firms.

Regulation

We are subject to federal and state consumer protection laws, including regulations prohibiting unfair and deceptive trade practices. In addition, numerous states and municipalities regulate the conduct of auctions and the liability of auctioneers. We and/or our auctioneers are licensed or bonded in the following states where we conduct, or have conducted, retail, wholesale or industrial asset auctions: California, Florida, Georgia, Illinois, Massachusetts, Ohio, South Carolina, Texas, Virginia and Washington. In addition, we are licensed or obtain permits in cities and/or counties where we conduct auctions, as required. If we conduct an auction in a state where we are not licensed or where reciprocity laws do not exist, we will work with an auctioneer of record in such state.

As a participant in the financial services industry, we are subject to complex and extensive regulation of most aspects of our business by U.S. federal and state regulatory agencies, self-regulatory organizations and securities exchanges. The laws, rules and regulations comprising the regulatory framework are constantly changing, as are the interpretation and enforcement of existing laws, rules and regulations. The effect of any such changes cannot be predicted and may direct the manner of our operations and affect our profitability.

BRC, our broker-dealer subsidiary, is subject to regulations governing every aspect of the securities business, including the execution of securities transactions; capital requirements; record-keeping and reporting procedures; relationships with customers, including the handling of cash and margin accounts; the experience of and training requirements for certain employees; and business interactions with firms that are not members of regulatory bodies.

BRC is registered as a securities broker-dealer with the SEC and is a member of FINRA. FINRA is a self-regulatory body composed of members such as our broker-dealer subsidiary that have agreed to abide by the rules and regulations of FINRA. FINRA may expel, fine and otherwise discipline member firms and their employees. BRC is also licensed as a broker-dealer in 18 states in the U.S., requiring us to comply with the laws, rules and regulations of each such state. Each state may revoke the license to conduct securities business, fine and otherwise discipline broker-dealers and their employees. We are also registered with NASDAQ and must comply with its applicable rules.

| 10 |

BRC is also subject to the SEC’s Uniform Net Capital Rule, Rule 15c3-1, which may limit our ability to make withdrawals of capital from our broker-dealer subsidiary. The Uniform Net Capital Rule sets the minimum level of net capital a broker-dealer must maintain and also requires that a portion of its assets be relatively liquid. In addition, BRC is subject to certain notification requirements related to withdrawals of excess net capital.

We are also subject to the USA PATRIOT Act of 2001 (the Patriot Act), which imposes obligations regarding the prevention and detection of money-laundering activities, including the establishment of customer due diligence and customer verification, and other compliance policies and procedures. The conduct of research analysts is also the subject of rule-making by the SEC, FINRA and the federal government through the Sarbanes-Oxley Act. These regulations require certain disclosures by, and restrict the activities of, research analysts and broker-dealers, among others. Failure to comply with these requirements may result in monetary, regulatory and, in the case of the USA Patriot Act, criminal penalties.

Our asset management subsidiary, B. Riley Capital Management, LLC is an SEC-registered investment adviser, and accordingly subject to regulation by the SEC. Requirements under the Investment Advisors Act of 1940 include record-keeping, advertising and operating requirements, and prohibitions on fraudulent activities.

Various regulators, including the SEC, FINRA and state securities regulators and attorneys general, are conducting both targeted and industry-wide investigations of certain practices relating to the financial services industry, including marketing, sales practices, valuation practices, asset managers, and market and compensation arrangements. These investigations, which have been highly publicized, have involved mutual fund companies, broker-dealers, hedge funds, investors and others.

In addition, the SEC staff has conducted studies with respect to soft dollar practices in the brokerage and asset management industries and proposed interpretive guidance regarding the scope of permitted brokerage and research services in connection with soft dollar practices.

In July 2010, Congress enacted Dodd-Frank. Dodd-Frank institutes a wide range of reforms that will impact financial services firms and requires significant rule-making. In addition, the legislation mandates multiple studies, which could result in additional legislative or regulatory action. Many of the provisions of Dodd-Frank are subject to further rulemaking procedures and studies and will take effect over several years. As a result, we cannot assess the impact of these new legislative and regulatory changes on our business at the present time.

Employees

As of December 31, 2015, we had 217 full time employees and three part time employees. We are not a party to any collective bargaining agreements. We have never experienced a work stoppage or strike and believe that relations with our employees are good.

We rely significantly on the expertise of independent contractors whom we engage in connection with specific transactions. As of December 31, 2015, we maintained a network of approximately 160 independent contractors who we engage from time to time to provide services pursuant to the terms of independent contractor agreements.

Other

We were incorporated in Delaware in May 2009 as a subsidiary of Alternative Asset Management Acquisition Corp. (“AAMAC”). On July 31, 2009, we closed a transaction pursuant to which (i) the members of Great American Group, LLC contributed to the Company of all of their membership interests in Great American Group, LLC, and (ii) AAMAC merged with and into our wholly-owned subsidiary. As a result of such transactions, Great American Group, LLC and AAMAC became our wholly-owned subsidiaries. Following the acquisition of BRC Inc., we changed the Company’s name from Great American Group, Inc. to B. Riley Financial, Inc. in November 2014.

Available Information

We maintain a website at www.brileyfin.com. We file reports with the SEC, and make available, free of charge, on or through our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy and information statements and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information on our website is not a part of, or incorporated in, this Annual Report.

| 11 |

| Item 1A. | RISK FACTORS |

Given the nature of our operations and services we provide, a wide range of factors could materially affect our operations and profitability. Changes in competitive, market and economic conditions also affect our operations. The risks and uncertainties described below are not the only risks and uncertainties facing us. Additional risks and uncertainties not presently known or that are currently considered to be immaterial may also materially and adversely affect our business operations or stock price. If any of the following risks or uncertainties occurs, our business, financial condition or operating results could materially suffer.

Our revenues and results of operations are volatile and difficult to predict.

Our revenues and results of operations fluctuate significantly from quarter to quarter, due to a number of factors. These factors include, but are not limited to, the following:

| • | Our ability to attract new clients and obtain additional business from our existing client base; |

| • | The number, size and timing of mergers and acquisition transactions, capital raising transactions and other strategic advisory services where we act as an adviser on our auction and liquidation and investment banking engagements; |

| • | The extent to which we acquire assets for resale, or guarantee a minimum return thereon, and our ability to resell those assets at favorable prices; |

| • | Variability in the mix of revenues from the auction and liquidation and valuation and appraisal businesses; |

| • | The rate of growth of new service areas; |

| • | The types of fees we charge clients, or other financial arrangements we enter into with clients; and |

| • | Changes in general economic and market conditions. |

We have limited or no control over some of the factors set forth above and, as a result, may be unable to forecast our revenues accurately. For example, our investment banking revenues are typically earned upon the successful completion of a transaction, the timing of which is uncertain and beyond our control. A client’s acquisition transaction may be delayed or terminated because of a failure to agree upon final terms with the counterparty, failure to obtain necessary regulatory consents or board or stockholder approvals, failure to secure necessary financing, adverse market conditions or unexpected financial or other problems in the business of a client or a counterparty. If the parties fail to complete a transaction on which we are advising or an offering in which we are participating, we will earn little or no revenue from the contemplated transaction.

We rely on projections of revenues in developing our operating plans for the future and will base our expectations regarding expenses on these projections and plans. If we inaccurately forecast revenues and/or earnings, or fail to accurately project expenses, we may be unable to adjust our spending in a timely manner to compensate for these inaccuracies and, as a result, may suffer operating losses and such losses could have a negative impact on our financial condition and results of operations. If, for any reason, we fail to meet company, investor or analyst projections of revenue, growth or earnings, the market price of the common stock could decline and you may lose all or part of your investment.

Conditions in the financial markets and general economic conditions have impacted and may continue to impact our ability to generate business and revenues, which may cause significant fluctuations in our stock price.

Our business has in the past, and may in the future, be materially affected by conditions in the financial market and general economic conditions, such as the level and volatility of interest rates, investor sentiment, the availability and the cost of credit, the U.S. mortgage market, the U.S. real estate market, volatile energy prices, consumer confidence, unemployment, and geopolitical issues. Further, certain aspects of our business are cyclical in nature and changes in the current economic environment may require us to adjust our sales and marketing practices and react to different business opportunities and modes of competition. If we are not successful in reacting to changing economic conditions, we may lose business opportunities which could harm our financial condition. For example, we are more likely to conduct auctions and liquidations in connection with insolvencies and store closures during periods of economic downturn relative to periods of economic expansion. Conversely, during an economic downturn, financial institutions that provide asset-based loans typically reduce the number of loans made, which reduces their need for our valuation and appraisal services.

In addition, weakness or disruption in equity markets and diminished trading volume of securities could adversely impact our sales and trading business in the future. Any industry-wide declines in the size and number of underwritings and mergers and acquisitions transactions could also have an adverse effect on our investment banking revenues. Reductions in the trading prices for equity securities tend to reduce the transaction value of investment banking transactions, such as underwriting and mergers and acquisitions transactions, which in turn may reduce the fees we earn from these transactions. Market conditions may also affect the level and volatility of securities prices and the liquidity and value of investments in our funds and proprietary inventory, and we may not be able to manage our business’s exposure to these market conditions. In addition to these factors, deterioration in the financial markets or economic conditions could materially affect our investment banking business in other ways, including the following:

| 12 |

| • | Our opportunity to act as underwriter or placement agent could be adversely affected by a reduction in the number and size of capital raising transactions or by competing government sources of equity. |

| • | The number and size of mergers and acquisitions transactions or other strategic advisory services where we act as adviser could be adversely affected by continued uncertainties in valuations related to asset quality and creditworthiness, volatility in the equity markets, and diminished access to financing. |

| • | Market volatility could lead to a decline in the volume of transactions that we execute for our customers and, therefore, to a decline in the revenue we receive from commissions and spreads. |

| • | We may experience losses in securities trading activities, or as a result of write-downs in the value of securities that we own, as a result of deteriorations in the businesses or creditworthiness of the issuers of such securities. |

| • | We may experience losses or write downs in the realizable value of our proprietary investments due to the inability of companies we invest in to repay their borrowings. |

| • | Our access to liquidity and the capital markets could be limited, preventing us from making proprietary investments and restricting our sales and trading businesses. |

| • | We may incur unexpected costs or losses as a result of the bankruptcy or other failure of companies for which we have performed investment banking services to honor ongoing obligations such as indemnification or expense reimbursement agreements. |

| • | Sudden sharp declines in market values of securities can result in illiquid markets and the failure of counterparties to perform their obligations, which could make it difficult for us to sell securities, hedge securities positions, and invest funds under management. |

| • | As an introducing broker to clearing firms, we are responsible to the clearing firm and could be held liable for the defaults of our customers, including losses incurred as the result of a customer’s failure to meet a margin call. When we allow customers to purchase securities on margin, we are subject to risks inherent in extending credit. This risk increases when a market is rapidly declining and the value of the collateral held falls below the amount of a customer’s indebtedness. If a customer’s account is liquidated as the result of a margin call, we are liable to our clearing firm for any deficiency. |

| • | Competition in our investment banking, sales, and trading businesses could intensify as a result of the increasing pressures on financial services companies and larger firms competing for transactions and business that historically would have been too small for them to consider. |

| • | Market volatility could result in lower prices for securities, which may result in reduced management fees calculated as a percentage of assets under management. |

| • | Market declines could increase claims and litigation, including arbitration claims from customers. |

| • | Our industry could face increased regulation as a result of legislative or regulatory initiatives. Compliance with such regulation may increase our costs and limit our ability to pursue business opportunities. |

| • | Government intervention may not succeed in improving the financial and credit markets and may have negative consequences for our business. |

It is difficult to predict how long current financial market and economic conditions will continue, whether they will deteriorate and if they do, which of our business lines will be adversely affected. If one or more of the foregoing risks occurs, our revenues are likely to decline and, if we were unable to reduce expenses at the same pace, our profit margins could erode.

| 13 |

We focus principally on specific sectors of the economy in our investment banking operations, and deterioration in the business environment in these sectors or a decline in the market for securities of companies within these sectors could harm our business.

We focus principally on five target industries in our investment banking operations: consumer goods, consumer services, defense, industrials and technology. Volatility in the business environment in these industries or in the market for securities of companies within these industries could adversely affect our financial results and the market value of our common stock. The business environment for companies in some of these industries has been subject to high levels of volatility in recent years, and our financial results have consequently been subject to significant variations from year to year. The market for securities in each of our target industries may also be subject to industry-specific risks. For example, we have research, investment banking and principal investments focused in the areas of defense. This sector has been subject to U.S. Department of Defense budget cuts as well as by disruptions in the financial markets and downturns in the general economy. The consumer goods and services sectors are subject to consumer spending trends, which have been volatile, to mall traffic trends, which have been down, to the availability of credit, and to broader trends such as the rise of Internet retailers. Emerging markets have driven the growth of certain consumer companies but emerging market economies are fragile, subject to wide swings in GDP, and subject to changes in foreign currencies. The technology industry has been volatile, driven by evolving technology trends, by technological obsolescence, by enterprise spending, and by changes in the capital spending trends of major corporations and government agencies around the world.

Our investment banking operations focus on various sectors of the economy, and we also depend significantly on private company transactions for sources of revenues and potential business opportunities. Most of these private company clients are initially funded and controlled by private equity firms. To the extent that the pace of these private company transactions slows or the average transaction size declines due to a decrease in private equity financings, difficult market conditions in our target industries or other factors, our business and results of operations may be harmed.

Underwriting and other corporate finance transactions, strategic advisory engagements and related sales and trading activities in our target industries represent a significant portion of our investment banking business. This concentration of activity in our target industries exposes us to the risk of declines in revenues in the event of downturns in these industries.

Our corporate finance and strategic advisory engagements are singular in nature and do not generally provide for subsequent engagements.

Our investment banking clients generally retain us on a short-term, engagement-by-engagement basis in connection with specific corporate finance, merger and acquisition transactions (often as an advisor in company sale transactions) and other strategic advisory services, rather than on a recurring basis under long-term contracts. As these transactions are typically singular in nature and our engagements with these clients may not recur, we must seek new engagements when our current engagements are successfully completed or are terminated. As a result, high activity levels in any period are not necessarily indicative of continued high levels of activity in any subsequent period. If we are unable to generate a substantial number of new engagements that generate fees from new or existing clients, our business, results of operations and financial condition could be adversely affected.

The asset management business is intensely competitive.

Over the past several years, the size and number of asset management funds, including hedge funds and mutual funds, has continued to increase. If this trend continues, it is possible that it will become increasingly difficult for our funds to raise capital. More significantly, the allocation of increasing amounts of capital to alternative investment strategies by institutional and individual investors leads to a reduction in the size and duration of pricing inefficiencies. Many alternative investment strategies seek to exploit these inefficiencies and, in certain industries, this drives prices for investments higher, in either case increasing the difficulty of achieving targeted returns. In addition, if interest rates were to rise or there were to be a prolonged bull market in equities, the attractiveness of our funds relative to investments in other investment products could decrease. Competition is based on a variety of factors, including:

| • | investment performance; |

| • | investor perception of the drive, focus and alignment of interest of an investment manager; |

| • | quality of service provided to and duration of relationship with investors; |

| • | business reputation; and |

| • | level of fees and expenses charged for services. |

| 14 |

We compete in the asset management business with a large number of investment management firms, private equity fund sponsors, hedge fund sponsors and other financial institutions. A number of factors serve to increase our competitive risks, as follows:

| • | investors may develop concerns that we will allow a fund to grow to the detriment of its performance; |

| • | some of our competitors have greater capital, lower targeted returns or greater sector or investment strategy specific expertise than we do, which creates competitive disadvantages with respect to investment opportunities; |

| • | some of our competitors may perceive risk differently than we do which could allow them either to outbid us for investments in particular sectors or, generally, to consider a wider variety of investments; |

| • | there are relatively few barriers to entry impeding new asset management firms, and the successful efforts of new entrants into our various lines of business, including former “star” portfolio managers at large diversified financial institutions as well as such institutions themselves, will continue to result in increased competition; and |

| • | other industry participants in the asset management business continuously seek to recruit our best and brightest investment professionals away from us. |

These and other factors could reduce our earnings and revenues and adversely affect our business. In addition, if we are forced to compete with other alternative asset managers on the basis of price, we may not be able to maintain our current base management and incentive fee structures. We have historically competed primarily on the performance of our funds, and not on the level of our fees relative to those of our competitors. However, there is a risk that fees in the alternative investment management industry will decline, without regard to the historical performance of a manager, including our managers. Fee reductions on our existing or future funds, without corresponding decreases in our cost structure, would adversely affect our revenues and distributable earnings.

Poor investment performance may decrease assets under management and reduce revenues from and the profitability of our asset management business.

Revenues from our asset management business are primarily derived from asset management fees. Asset management fees are generally comprised of management and incentive fees. Management fees are typically based on assets under management, and incentive fees are earned on a quarterly or annual basis only if the return on our managed accounts exceeds a certain threshold return, or “highwater mark,” for each investor. We will not earn incentive fee income during a particular period, even when a fund had positive returns in that period, if we do not generate cumulative performance that surpasses a highwater mark. If a fund experiences losses, we will not earn incentive fees with regard to investors in that fund until its returns exceed the relevant highwater mark.

In addition, investment performance is one of the most important factors in retaining existing investors and competing for new asset management business. Investment performance may be poor as a result of the current or future difficult market or economic conditions, including changes in interest rates or inflation, terrorism or political uncertainty, our investment style, the particular investments that we make, and other factors. Poor investment performance may result in a decline in our revenues and income by causing (i) the net asset value of the assets under our management to decrease, which would result in lower management fees to us, (ii) lower investment returns, resulting in a reduction of incentive fee income to us, and (iii) investor redemptions, which would result in lower fees to us because we would have fewer assets under management.

To the extent our future investment performance is perceived to be poor in either relative or absolute terms, the revenues and profitability of our asset management business will likely be reduced and our ability to grow existing funds and raise new funds in the future will likely be impaired.

The historical returns of our funds may not be indicative of the future results of our funds.

The historical returns of our funds should not be considered indicative of the future results that should be expected from such funds or from any future funds we may raise. Our rates of returns reflect unrealized gains, as of the applicable measurement date, which may never be realized due to changes in market and other conditions not in our control that may adversely affect the ultimate value realized from the investments in a fund. The returns of our funds may have also benefited from investment opportunities and general market conditions that may not repeat themselves, and there can be no assurance that our current or future funds will be able to avail themselves of profitable investment opportunities. Furthermore, the historical and potential future returns of the funds we manage also may not necessarily bear any relationship to potential returns on our common stock.

| 15 |

Our asset management clients may generally redeem their investments, which could reduce our asset management fee revenues.

Our asset management fund agreements generally permit investors to redeem their investments with us after an initial “lockup” period during which redemptions are restricted or penalized. However, any such restrictions may be waived by us. Thereafter, redemptions are permitted at specified intervals. If the return on the assets under our management does not meet investors’ expectations, investors may elect to redeem their investments and invest their assets elsewhere, including with our competitors. Our management fee revenues correlate directly to the amount of assets under our management; therefore, redemptions may cause our fee revenues to decrease. Investors may decide to reallocate their capital away from us and to other asset managers for a number of reasons, including poor relative investment performance, changes in prevailing interest rates which make other investments more attractive, changes in investor perception regarding our focus or alignment of interest, dissatisfaction with changes in or a broadening of a fund’s investment strategy, changes in our reputation, and departures or changes in responsibilities of key investment professionals. For these and other reasons, the pace of redemptions and corresponding reduction in our assets under management could accelerate. In the future, redemptions could require us to liquidate assets under unfavorable circumstances, which would further harm our reputation and results of operations.

We are subject to risks in using custodians.

Our asset management subsidiary and its managed funds depend on the services of custodians to settle and report securities transactions. In the event of the insolvency of a custodian, our funds might not be able to recover equivalent assets in whole or in part as they will rank among the custodian’s unsecured creditors in relation to assets which the custodian borrows, lends or otherwise uses. In addition, cash held by our funds with the custodian will not be segregated from the custodian’s own cash, and the funds will therefore rank as unsecured creditors in relation thereto.

We may suffer losses if our reputation is harmed.

Our ability to attract and retain customers and employees may be diminished to the extent our reputation is damaged. If we fail, or are perceived to fail, to address various issues that may give rise to reputational risk, we could harm our business prospects. These issues include, but are not limited to, appropriately dealing with market dynamics, potential conflicts of interest, legal and regulatory requirements, ethical issues, customer privacy, record-keeping, sales and trading practices, and the proper identification of the legal, reputational, credit, liquidity and market risks inherent in our products and services. Failure to appropriately address these issues could give rise to loss of existing or future business, financial loss, and legal or regulatory liability, including complaints, claims and enforcement proceedings against us, which could, in turn, subject us to fines, judgments and other penalties. In addition, our capital markets operations depend to a large extent on our relationships with our clients and reputation for integrity and high-caliber professional services to attract and retain clients. As a result, if a client is not satisfied with our services, it may be more damaging in our business than in other businesses.

Our capital markets operations are highly dependent on communications, information and other systems and third parties, and any systems failures could significantly disrupt our capital markets business.

Our data and transaction processing, custody, financial, accounting and other technology and operating systems are essential to our capital markets operations. A system malfunction (due to hardware failure, capacity overload, security incident, data corruption, etc.) or mistake made relating to the processing of transactions could result in financial loss, liability to clients, regulatory intervention, reputational damage and constraints on our ability to grow. We outsource a substantial portion of our critical data processing activities, including trade processing and back office data processing. We also contract with third parties for market data and other services. In the event that any of these service providers fails to adequately perform such services or the relationship between that service provider and us is terminated, we may experience a significant disruption in our operations, including our ability to timely and accurately process transactions or maintain complete and accurate records of those transactions.

Adapting or developing our technology systems to meet new regulatory requirements, client needs, expansion and industry demands also is critical for our business. Introduction of new technologies present new challenges on a regular basis. We have an ongoing need to upgrade and improve our various technology systems, including our data and transaction processing, financial, accounting, risk management and trading systems. This need could present operational issues or require significant capital spending. It also may require us to make additional investments in technology systems and may require us to reevaluate the current value and/or expected useful lives of our technology systems, which could negatively impact our results of operations.

Secure processing, storage and transmission of confidential and other information in our internal and outsourced computer systems and networks also is critically important to our business. We take protective measures and endeavor to modify them as circumstances warrant. However, our computer systems, software and networks may be vulnerable to unauthorized access, computer viruses or other malicious code, inadvertent, erroneous or intercepted transmission of information (including by e-mail), and other events that could have an information security impact. If one or more of such events occur, this potentially could jeopardize our or our clients' or counterparties' confidential and other information processed and stored in, and transmitted through, our computer systems and networks, or otherwise cause interruptions or malfunctions in our, our clients', our counterparties' or third parties' operations. We may be required to expend significant additional resources to modify our protective measures or to investigate and remediate vulnerabilities or other exposures, and we may be subject to litigation and financial losses that are either not insured against or not fully covered through any insurance maintained by us.

| 16 |

A disruption in the infrastructure that supports our business due to fire, natural disaster, health emergency (for example, a disease pandemic), power or communication failure, act of terrorism or war may affect our ability to service and interact with our clients. If we are not able to implement contingency plans effectively, any such disruption could harm our results of operations.

The growth of electronic trading and the introduction of new technology in the markets in which our market-making business operates may adversely affect this business and may increase competition.

The continued growth of electronic trading and the introduction of new technologies is changing our market-making business and presenting new challenges. Securities, futures and options transactions are increasingly occurring electronically, through alternative trading systems. It appears that the trend toward alternative trading systems will continue to accelerate. This acceleration could further increase program trading, increase the speed of transactions and decrease our ability to participate in transactions as principal, which would reduce the profitability of our market-making business. Some of these alternative trading systems compete with our market-making business and with our algorithmic trading platform, and we may experience continued competitive pressures in these and other areas. Significant resources have been invested in the development of our electronic trading systems, which includes our ATM business, but there is no assurance that the revenues generated by these systems will yield an adequate return on the investment, particularly given the increased program trading and increased percentage of stocks trading off of the historically manual trading markets.

Pricing and other competitive pressures may impair the revenues of our sales and trading business.

We derive a significant portion of our revenues for our investment banking operations from our sales and trading business. There has been intense price competition and trading volume reduction in this business in recent years. In particular, the ability to execute trades electronically and through alternative trading systems has increased the downward pressure on per share trading commissions and spreads. We expect these trends toward alternative trading systems and downward pricing pressure in the business to continue. We believe we may experience competitive pressures in these and other areas in the future as some of our competitors seek to obtain market share by competing on the basis of price or by using their own capital to facilitate client trading activities. In addition, we face pressure from our larger competitors, which may be better able to offer a broader range of complementary products and services to clients in order to win their trading business. These larger competitors may also be better able to respond to changes in the research, brokerage and investment banking industries, to compete for skilled professionals, to finance acquisitions, to fund internal growth and to compete for market share generally. As we are committed to maintaining and improving our comprehensive research coverage in our target sectors to support our sales and trading business, we may be required to make substantial investments in our research capabilities to remain competitive. If we are unable to compete effectively in these areas, the revenues of our sales and trading business may decline, and our business, results of operations and financial condition may be harmed.