Exhibit 99.1

1

CrossFirst Bankshares, Inc. Reports Fourth Quarter and Full Year 2022

Results

LEAWOOD, Kan., January 23, 2023 (GLOBE NEWSWIRE) -- CrossFirst Bankshares, Inc. (Nasdaq: CFB), the bank holding company for

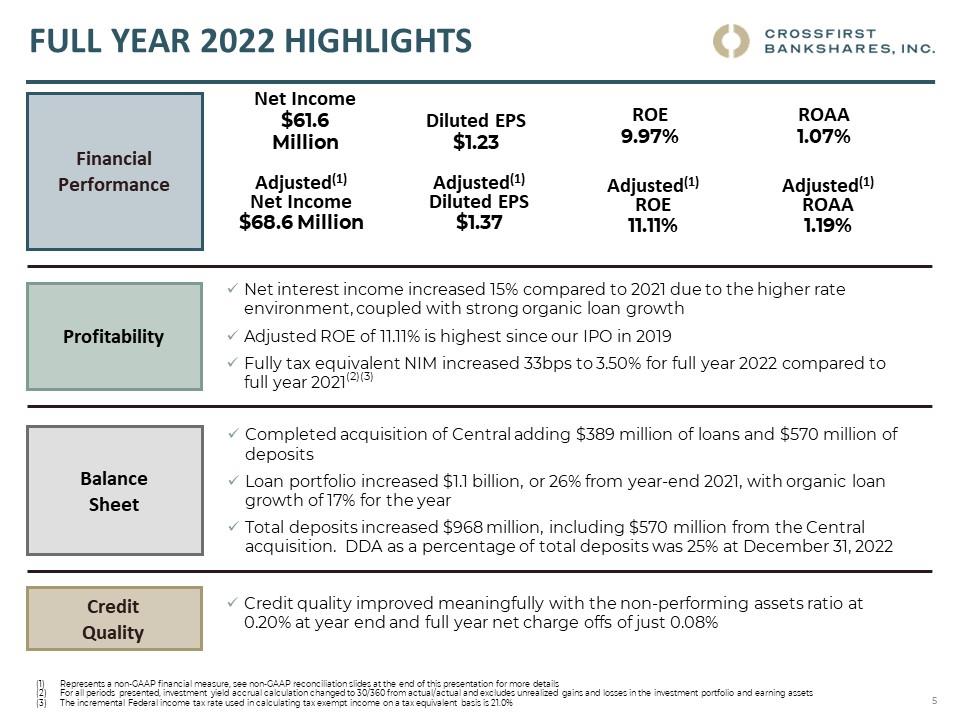

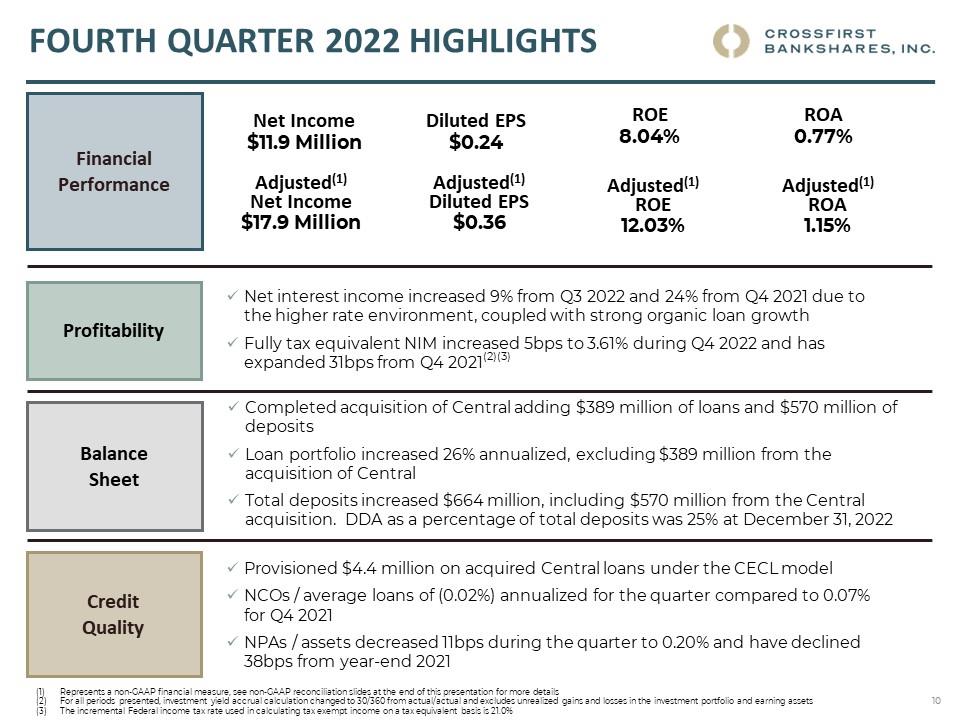

CrossFirst Bank, today reported fourth quarter net income of $11.9 million, or $0.24 per diluted share, and full year net income of $61.6

million, or $1.23 per diluted share. Adjusted net income was $17.9 million, or $0.36 per diluted share for the fourth quarter and $68.6

million, or $1.37 per diluted share for the full year.

Fourth Quarter 2022 Key Financial Performance Metrics

Net Income

ROAA

(1)

Net Interest Margin –

Fully Tax Equivalent

(“FTE”)

(1)

Diluted EPS

ROE

(1)

$11.9 million

0.77%

3.61%

$0.24

8.04%

Adjusted Fourth Quarter 2022 Key Financial Performance Metrics

(2)

Adjusted Net Income

Adjusted ROAA

(1)

Net Interest Margin -

(FTE)

(1)

Adjusted Diluted

EPS

Adjusted ROE

(1)

$17.9 million

1.15%

3.61%

$0.36

12.03%

(1)

Ratios are annualized.

(2)

With the exception of Net Interest Margin - (FTE), represents a non-GAAP financial measure. See “Table 5. Non-GAAP Financial

Measures” for a reconciliation of these measures.

CEO Commentary:

“CrossFirst had a very successful quarter with the closing of our acquisition of Central, launching our new digital banking platform, and

incredibly strong organic balance sheet growth,” said CrossFirst’s CEO and President, Mike Maddox. “2022 was our best year on record

by a number of different measures, and strategic investments we made last year supported our entry into dynamic markets including

Phoenix and Denver, which we believe will drive significant future growth.”

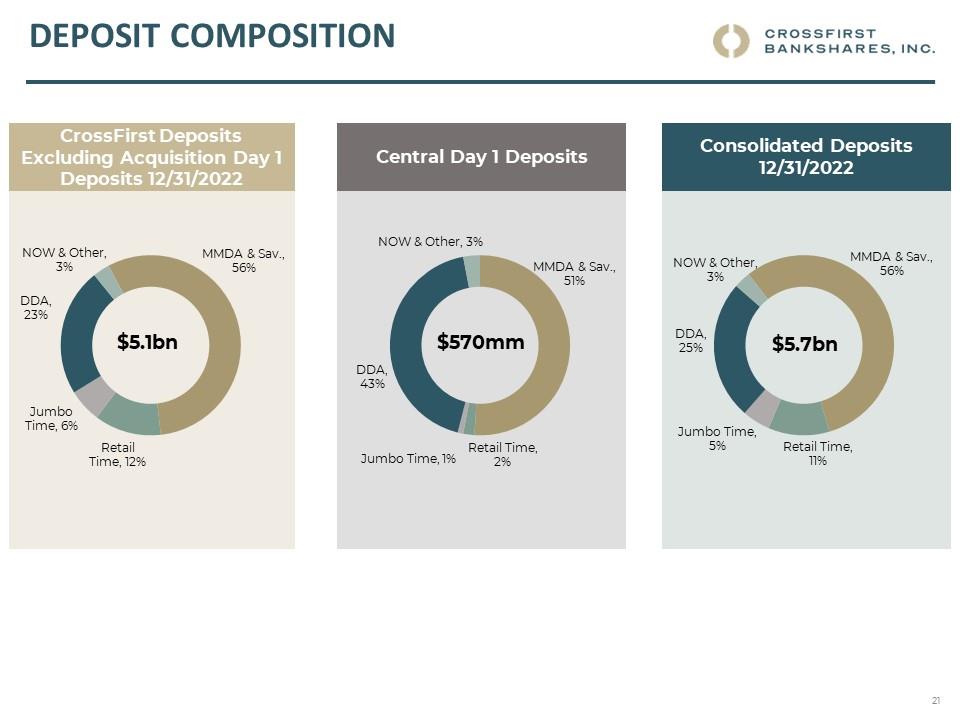

2022 Fourth Quarter and Full Year Highlights:

•

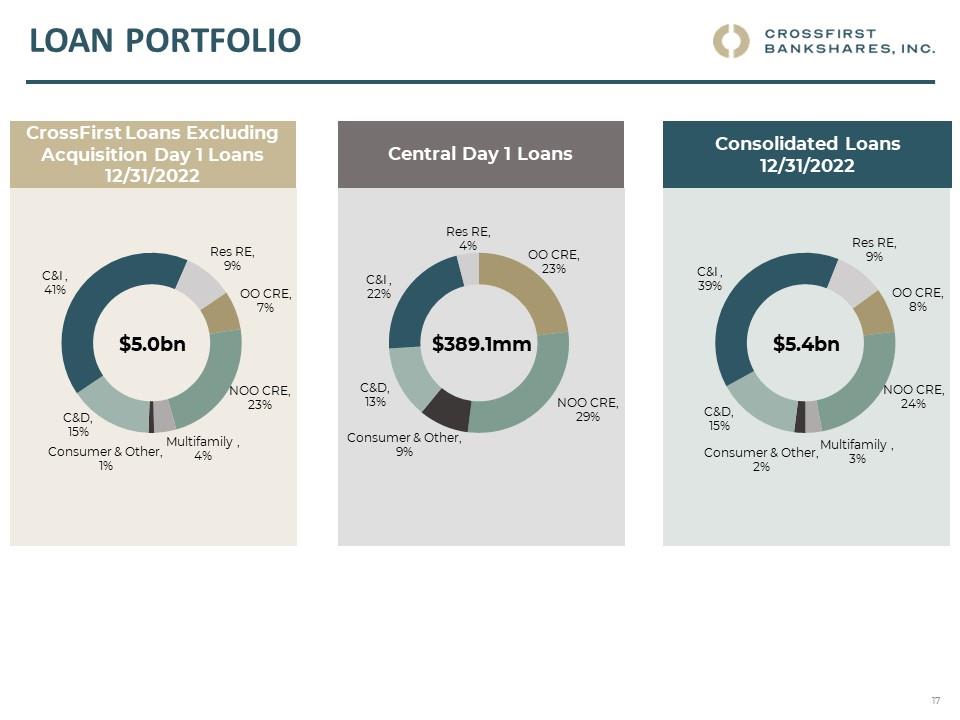

Completed the acquisition of Farmers & Stockmens Bank (“Central”) adding liquidity, new production talent, and expanding

into attractive and growing markets

◦

Added $389 million of loans and $570 million of deposits

•

Loans grew $1.1 billion for the year or 26%; loans grew $695 million for the quarter or 59% on an annualized basis

◦

Excluding the Central acquisition, loans grew 17% for the year and 26% on an annualized basis for the quarter

•

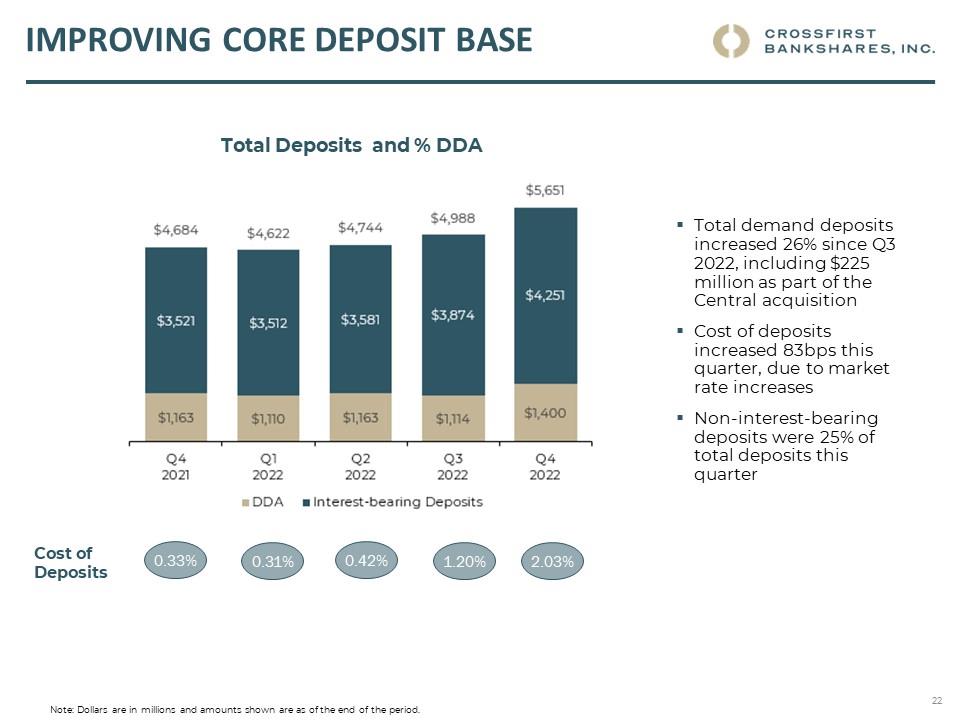

Deposits grew $968 million for the year or 21%; deposits grew $664 million for the quarter or 53% on an annualized basis

◦

Excluding the Central acquisition, deposits grew 9% for the year and 7% on an annualized basis for the quarter

◦

Non-interest-bearing deposit accounts grew to 25% of total deposits

•

Credit quality improved meaningfully with the non-performing assets ratio at 0.20% at year end and full year net charge offs

of just 0.08%

•

Launched a new digital banking platform, providing enhanced online tools and resources for clients

Exhibit 99.1

2

Quarter-to-Date

Full Year

December 31,

December 31,

(Dollars in millions except per share data)

2022

2021

2022

2021

Operating revenue

(1)

$

58.4

$

48.2

$

210.8

$

182.4

Net income

$

11.9

$

20.8

$

61.6

$

69.4

Diluted earnings per share

$

0.24

$

0.40

$

1.23

$

1.33

Return on average assets

0.77

%

1.50

%

1.07

%

1.24

%

Adjusted return on average assets

(2)

1.15

%

1.50

%

1.19

%

1.31

%

Return on average common equity

8.04

%

12.57

%

9.97

%

10.84

%

Adjusted return on average common equity

(2)

12.03

%

12.57

%

11.11

%

11.40

%

Net interest margin

3.56

%

3.24

%

3.44

%

3.11

%

Net interest margin -FTE

(3)(4)

3.61

%

3.30

%

3.50

%

3.17

%

Efficiency ratio

62.40

%

55.38

%

57.75

%

54.50

%

Adjusted efficiency ratio - FTE

(2)(4)

55.01

%

54.52

%

54.43

%

52.02

%

(1)

Net interest income plus non-interest income.

(2)

Represents a non-GAAP financial measure. See "Table 5. Non-GAAP Financial Measures" for a reconciliation of these measures.

(3)

The Company changed the annualization method on the available-for-sale securities portfolio from Actual/Actual to 30/360 and moved the unrealized

gain(loss) on available-for-sale securities from an interest-earning asset to a non-interest-earning asset. All periods presented reflect this change.

(4)

Tax exempt income is calculated on a tax-equivalent basis. Tax-free municipal securities are exempt from federal income taxes. The incremental federal

income tax rate used is 21.0%.

Income from Operations

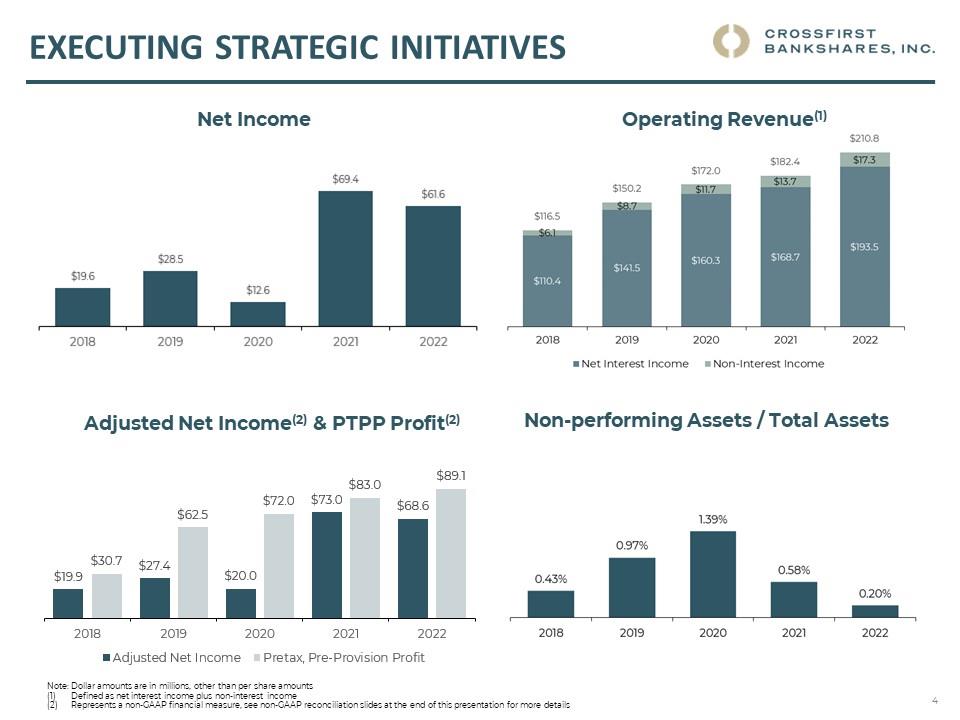

Net income totaled $11.9 million or $0.24 per diluted share for the fourth quarter of 2022, compared to $17.3 million or $0.35 per diluted

share during the third quarter of 2022. The quarter’s results were impacted by an increase in net interest income offset by higher non-

interest expenses. The quarter included acquisition-related non-interest expense of $3.6 million and a $4.4 million acquisition-related Day

1 CECL provision expense, discussed in detail below. Full year net income of $61.6 million was lower than 2021 net income of $69.4

million as better net interest income and non-interest income were more than offset by higher provision expense and non-interest expense.

Adjusted net income for 2022 totaled $68.6 million or $1.37 per diluted share compared to $73.0 million or $1.40 per diluted share for

2021. Full year adjusted net income was lower by $4.4 million as increases in net interest income were offset by higher CECL provision

and higher non-interest expense compared to 2021.

Net Interest Income

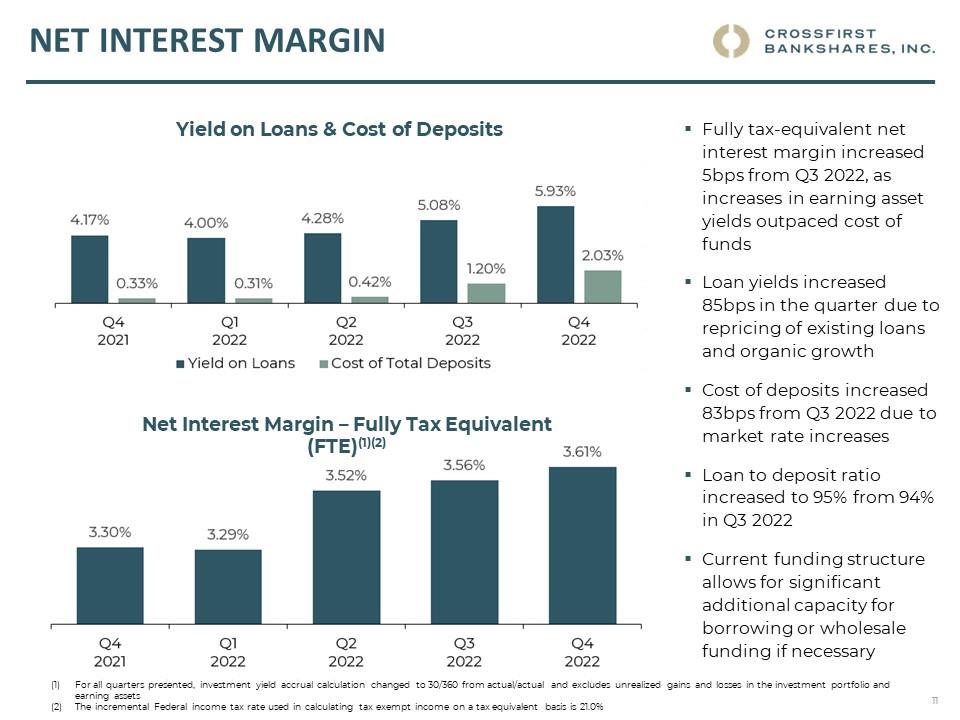

Fully taxable equivalent (“FTE”) net interest income totaled $54.8 million for the fourth quarter of 2022, which was 9% higher than the

third quarter and 24% higher than the fourth quarter of 2021. Net interest margin - FTE increased to 3.61% in the current quarter from

3.56% in the previous quarter and 3.30% in the fourth quarter of 2021 as increases in earning asset yields outpaced the cost of funds

increase. Full year 2022 net interest income - FTE grew $25.1 million, an increase of 15% compared to 2021, while the net interest

margin - FTE increased to 3.50% from 3.17% in the prior year due to the higher interest rate environment as well as the mix shift from

cash into higher earning assets.

Interest income was $82.4 million for the fourth quarter of 2022, an increase of 26% from the prior quarter and an increase of 67% from

the fourth quarter of 2021. Higher yields on earning assets - FTE was the primary driver of the increase and improved 80 basis points and

1.76% compared to the prior quarter and the prior year fourth quarter, respectively. Average earning assets increased $394 million, or 7%,

compared to the third quarter and increased $700 million, or 13%, compared to the same period in 2021. The increase in average earning

assets for the quarter was due to organic loan growth as well as the addition of $389 million of Central loans. Compared to the fourth

quarter of 2021, the earning asset increase was entirely driven by loan growth and higher average investment balances, partially offset by

lower cash balances. For the full year 2022, interest income increased $55.4 million primarily due to the higher interest rate environment,

loan growth, and a mix shift from cash into higher earning assets.

CROSSFIRST BANKSHARES, INC.

3

Interest expense for the fourth quarter of 2022 was $28.3 million, which increased 79% from the prior quarter and 392% from the same

quarter in 2021 due to significant changes in market rates in 2022 and higher average interest-bearing deposits. Average interest-bearing

deposits increased to $4.1 billion in the fourth quarter of 2022, a 9% increase from the third quarter and a 19% increase from the prior year

fourth quarter, respectively. For both comparative periods the increase in average interest-bearing deposits was due to organic growth of

savings and money market deposits, increased time deposits and the impact of the acquisition of Central. The cost of funds increased to

2.05% compared to 1.23% for the third quarter and 0.48% for the fourth quarter of 2021, driven by the higher interest rate environment.

For the full year 2022, interest expense increased $30.5 million due to higher market rates and increased competition for deposits.

Non-Interest Income

Non-interest income increased $0.6 million compared to the third quarter of 2022 and decreased by $0.4 million compared to the same

quarter in 2021. The increase in non-interest income compared to the previous quarter was due to gains on securities and increases in

service charges and fees. The decrease compared to the prior year was primarily the result of a decrease in credit card fees, partially offset

by increases in service charges and fees, as well as gains on securities. Full year 2022 non-interest income was up $3.6 million compared

to 2021 as the prior year included losses on securities net of bank-owned life insurance income totaling a net $4.4 million that did not

occur in the current year.

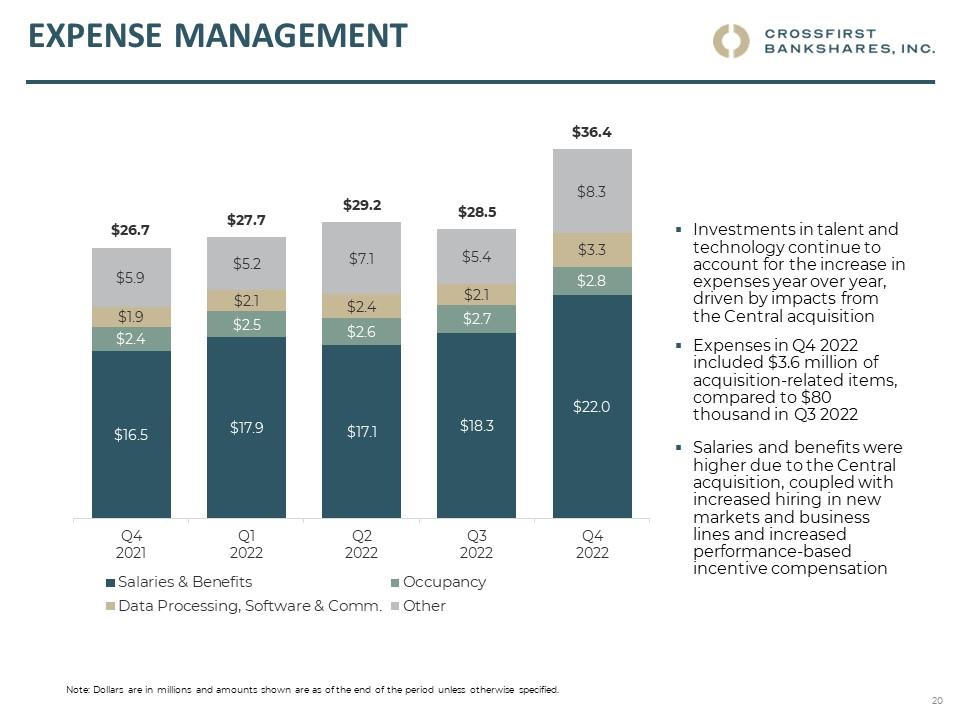

Non-Interest Expense

Non-interest expense increased $8.0 million from the third quarter of 2022. Included in the quarter were $3.6 million of acquisition-

related expenses with $1.2 million included in professional fees, $1.0 million in salaries and benefits, $1.1 million in data processing, and

$0.2 million in other non-interest expense. Excluding these acquisition-related expenses, non-interest expense increased $4.4 million

compared to the third quarter and $6.1 million compared to the fourth quarter of 2021. For both comparative periods salaries and benefit

costs were higher due to hiring in new markets, the addition of employees as part of the Central acquisition and increased performance-

based incentive compensation. Additionally, professional fees increased for both comparative periods primarily due to increases in legal

fees related to lending activity. Full year 2022 non-interest expense increased $22.4 million compared to 2021 due to a $14.2 million

increase in salaries due to hiring activity, the addition of Central, merit increases and increased incentive compensation. In addition,

occupancy expenses increased $1.0 million related to new market expansion, professional fees increased $1.8 million due to the Central

acquisition as well as lending related legal fees, and data processing increased $1.9 million due to the Central acquisition, account growth

and costs related to our digital banking conversion. Advertising as well as other non-interest expenses were up $1.1 million and $2.6

million, respectively, due to increased post-pandemic activities. Other non-interest expense also included an employee separation expense

of $1.1 million in 2022.

The Company’s effective tax rate for the fourth quarter of 2022 was 21.9%, as compared to 20.3% in the third quarter and 21.6% for the

fourth quarter of 2021. The increase compared to the third quarter was due to a $0.3 million charge related to certain non-deductible

acquisition costs.

Balance Sheet Performance & Analysis

During the fourth quarter of 2022, total assets increased by $0.8 billion or 13% compared to the end of the prior quarter, and increased $1.0

billion or 17% compared to December 31, 2021. Total assets increased on a linked quarter basis primarily due to a $0.7 billion increase in

loans. The year-over-year increase was primarily due to an increase in loans of $1.1 billion. For both comparative periods, the increases in

loans included a $0.4 billion increase from the Central acquisition. Deposits increased $0.7 billion compared to September 30, 2022, and

increased $1.0 billion from December 31, 2021. For both periods, $0.6 billion of the increase is due to the acquisition of Central.

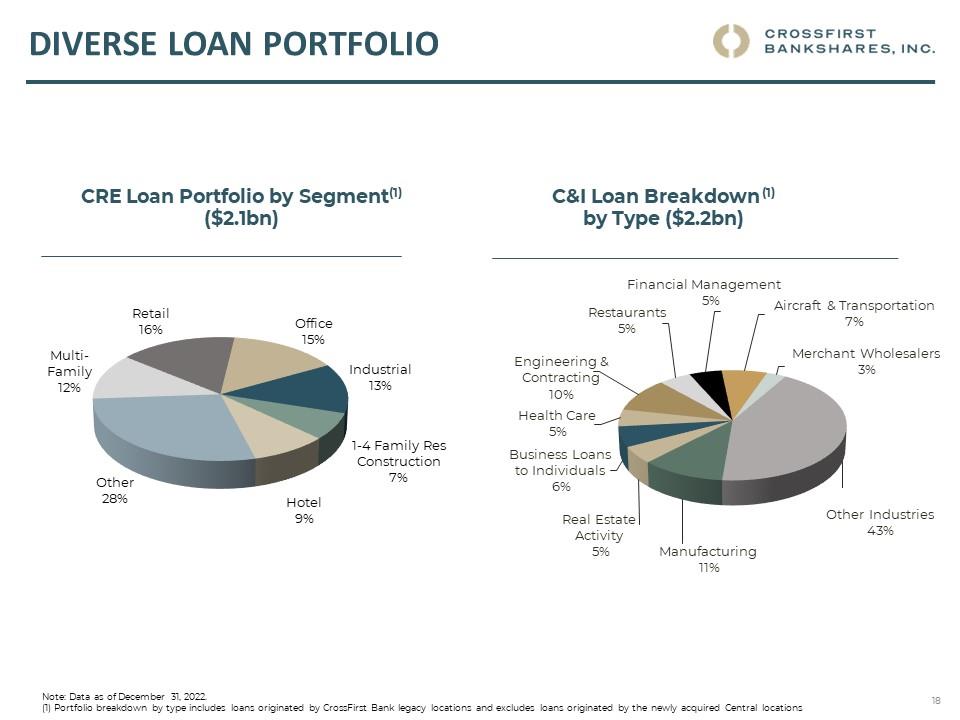

Loan Results

During the fourth quarter of 2022, the Company produced an increase in average loans of $383 million compared to the third quarter, and

an increase of $789 million or 19% compared to the fourth quarter of 2021. The linked quarter increase in average loans was primarily a

result of growth in the commercial and commercial real estate portfolios and the acquisition of Central.

CROSSFIRST BANKSHARES, INC.

4

4Q22

3Q22

2Q22

1Q22

4Q21

% of

Total

QoQ

Growth

($)

QoQ

Growth

(%)

(1)

YoY

Growth

($)

YoY

Growth

(%)

(1)

(Dollars in millions)

Average loans (gross)

Commercial

$

1,909

$

1,630

$

1,532

$

1,434

$

1,328

38

%

$

279

17

%

$

581

44

%

Energy

183

211

241

274

290

4

(28)

(13)

(107)

(37)

Commercial real estate

1,461

1,439

1,399

1,327

1,272

29

22

2

189

15

Construction and land development

734

633

581

593

579

15

101

16

155

27

Residential and multifamily real estate

645

644

609

604

612

13

1

0

33

5

Paycheck Protection Program

5

6

20

42

84

0

(1)

(17)

(79)

(94)

Consumer

73

64

56

59

56

1

9

14

17

30

Total

$

5,010

$

4,627

$

4,438

$

4,333

$

4,221

100

%

$

383

8

%

$

789

19

%

(1)

Actual unrounded values are used to calculate the reported percent disclosed. Accordingly, recalculations using the amounts in millions as disclosed in this release may not

produce the same amounts.

Deposit & Other Borrowing Results

During the fourth quarter of 2022, the Company produced an increase in average deposits of 7% compared to the previous quarter, and an

increase of 16% in average deposits compared to the fourth quarter of 2021. The average deposit increases for both comparative periods

was primarily due to increases in savings and money market deposits, and time deposits, including amounts related to the Central

acquisition.

4Q22

3Q22

2Q22

1Q22

4Q21

QoQ

Growth

($)

QoQ

Growth

(%)

(1)

YoY

Growth

($)

YoY

Growth

(%)

(1)

(Dollars in millions)

Average deposits

Non-interest-bearing deposits

$

1,142

$

1,138

$

1,150

$

1,157

$

1,058

$

4

0

%

$

84

8

%

Transaction deposits

529

531

507

586

543

(2)

0

(14)

(3)

Savings and money market deposits

2,742

2,520

2,334

2,303

2,272

222

9

470

21

Time deposits

868

734

560

587

662

134

18

206

31

Total

$

5,281

$

4,923

$

4,551

$

4,633

$

4,535

$

358

7

%

$

746

16

%

(1)

Actual unrounded values are used to calculate the reported percent disclosed. Accordingly, recalculations using the amounts in millions as disclosed in this release may

not produce the same amounts.

At December 31, 2022, other borrowings totaled $254 million, as compared to $206 million at September 30, 2022, and $238 million at

December 31, 2021, and increased due to short-term liquidity needs.

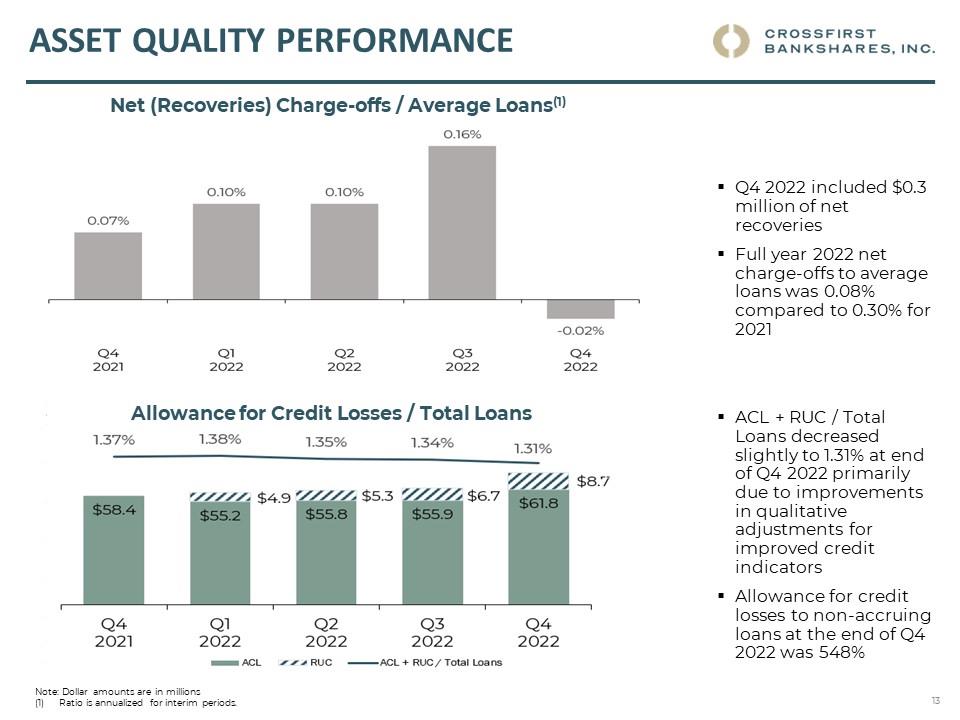

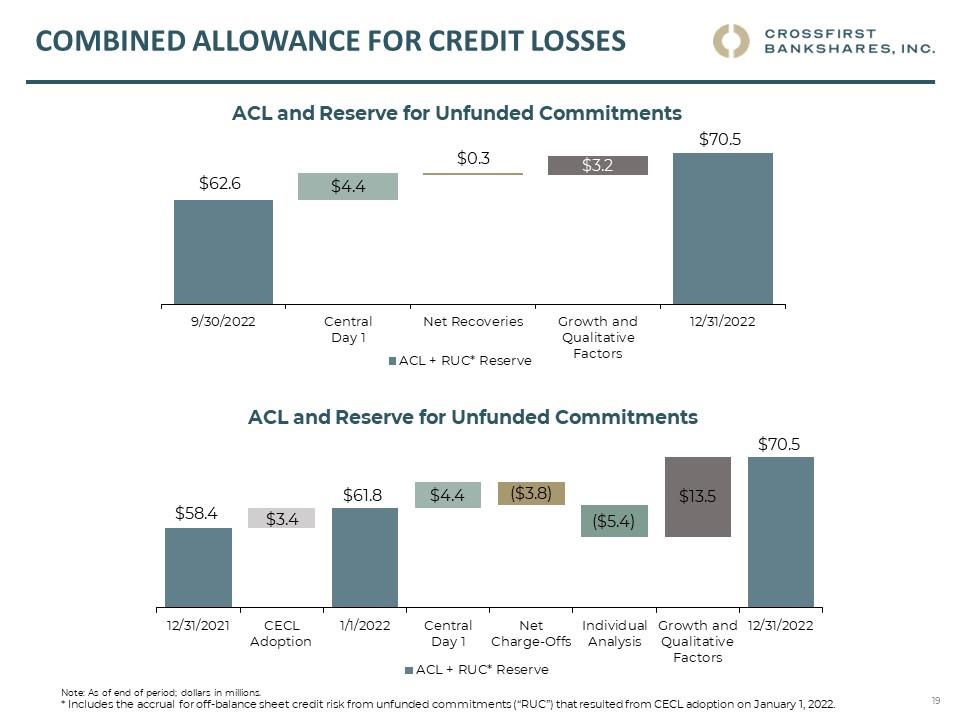

Asset Quality and Provision for Credit Losses

The Company recorded $6.7 million of provision expense, compared to $3.3 million last quarter and a ($5.0) million release of provision

in the prior year fourth quarter. The quarter’s provision included $4.4 million of acquisition-related Day 1 CECL provision expense for the

Central loan portfolio. The remainder of the quarter’s provision expense was driven by loan growth, partially offset by lower reserve

requirements from changes in the CECL model’s qualitative factors due to improvement in credit quality indicators.

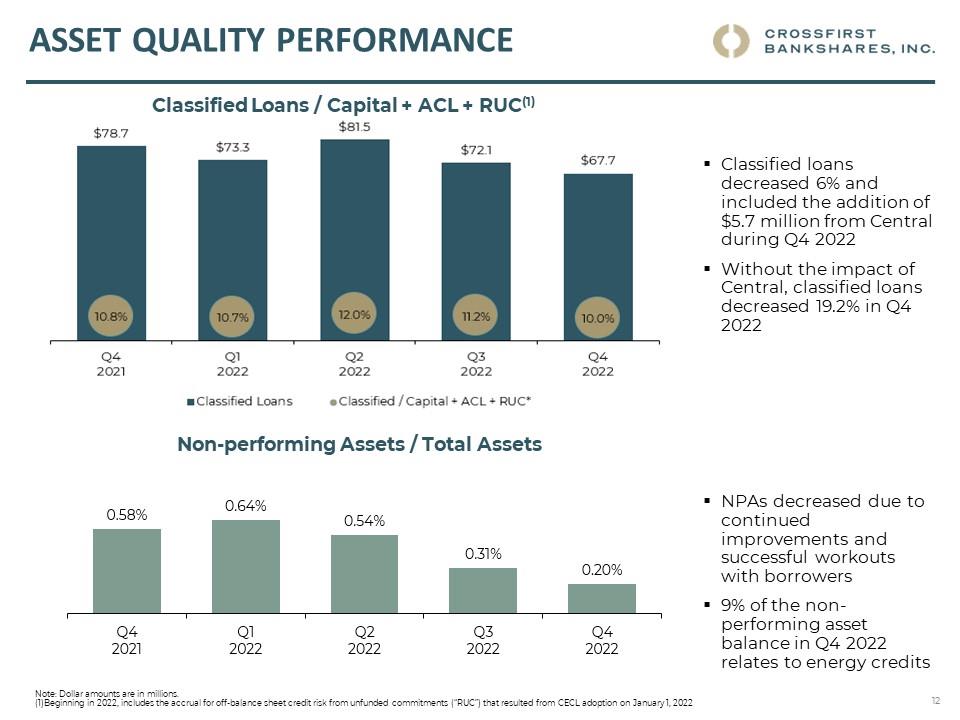

Non-performing assets decreased to $13.2 million at December 31, 2022 primarily due to a $5.6 million decrease in non-accrual loans. The

decline is attributable primarily to payments and payoffs on non-accrual energy, commercial and commercial real estate loans. The non-

performing assets to total assets ratio decreased from 0.58% at December 31, 2021 to 0.20% at December 31, 2022. Classified loans

decreased $4.4 million during the fourth quarter but included the addition of $5.7 million from Central. Without Central, classified assets

decreased $10.1 million due to reductions in classified energy and commercial loans. Net recoveries were ($0.3) million for the fourth

quarter of 2022 compared to $1.9 million of net charge-offs from the prior quarter and $0.8 million in the prior year fourth quarter.

The allowance for credit losses was $61.8 million or 1.15% of outstanding loans at December 31, 2022. The combined allowance for credit

losses and accrual for off-balance sheet credit risk from unfunded commitments (“RUC”) was $70.5 million or 1.31% of outstanding

loans. The allowance for credit losses and RUC to total loans decreased from 1.34% at September 30, 2022 due to the mix of funded

outstanding balances and unfunded commitments between the two periods and the aforementioned qualitative changes in the CECL model.

The allowance for credit losses and RUC to total loans ratio is not comparable to the prior year fourth quarter due to the adoption of CECL

on January 1, 2022.

CROSSFIRST BANKSHARES, INC.

5

The following table provides information regarding asset quality.

Asset quality

4Q22

3Q22

2Q22

1Q22

4Q21

Non-accrual loans

$

11.3

$

16.9

$

27.7

$

33.1

$

31.4

Other real estate owned

1.1

1.0

1.0

1.0

1.1

Loans 90+ days past due and still accruing

0.8

0.3

2.2

1.5

0.1

Total non-performing assets

$

13.2

$

18.2

$

30.8

$

35.6

$

32.7

Loans 30 - 89 days past due

$

19.6

$

21.4

$

16.6

$

15.9

$

3.5

Net charge-offs (recoveries)

(0.3)

1.9

1.1

1.1

0.8

Asset quality metrics

(%)

4Q22

3Q22

2Q22

1Q22

4Q21

Non-performing assets to total assets

0.20

%

0.31

%

0.54

%

0.64

%

0.58

%

Allowance for credit losses to total loans

1.15

1.19

1.23

1.27

1.37

Allowance for credit losses + RUC to total loans

(2)

1.31

1.34

1.35

1.38

Allowance for credit losses to non-performing loans

514

324

187

160

185

Net charge-offs (recoveries) to average loans

(1)

(0.02)

0.16

0.10

0.10

0.07

Provision to average loans

(1)

0.53

0.29

0.19

(0.06)

(0.47)

Classified Loans / (Capital + ACL)

10.1

11.3

12.1

10.8

10.8

Classified Loans / (Capital + ACL + RUC)

(2)

10.0

11.2

12.0

10.7

N/A

(1)

Interim periods annualized.

(2)

Includes the accrual for off-balance sheet credit risk from unfunded commitments that resulted from CECL adoption on January 1, 2022.

Capital Position

At December 31, 2022, stockholders' equity totaled $609 million, or $12.56 per share, compared to $668 million, or $13.23 per share, at

December 31, 2021. The decrease was due to the acquisition of Central and share repurchases, partially offset by earnings. During the

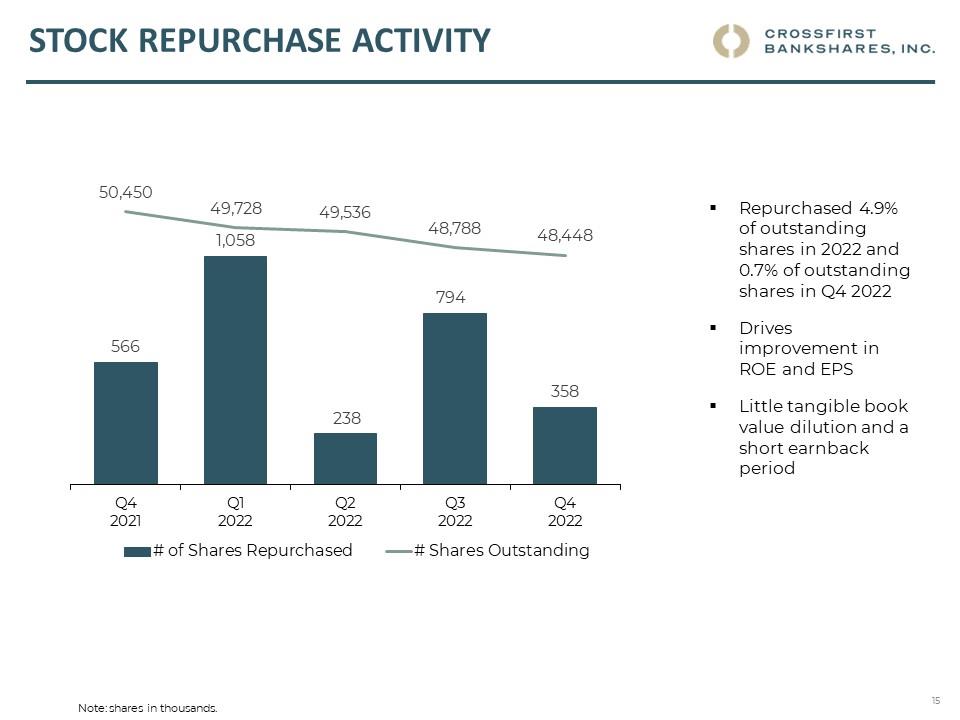

fourth quarter of 2022, the Company continued its share repurchase program by purchasing 357,646 shares of common stock outstanding

at a weighted average price of $13.42. In addition, accumulated other comprehensive loss declined by $86 million between December 31,

2021 and December 31, 2022; driven by a decrease in the unrealized loss on available-for-sale securities, net of tax.

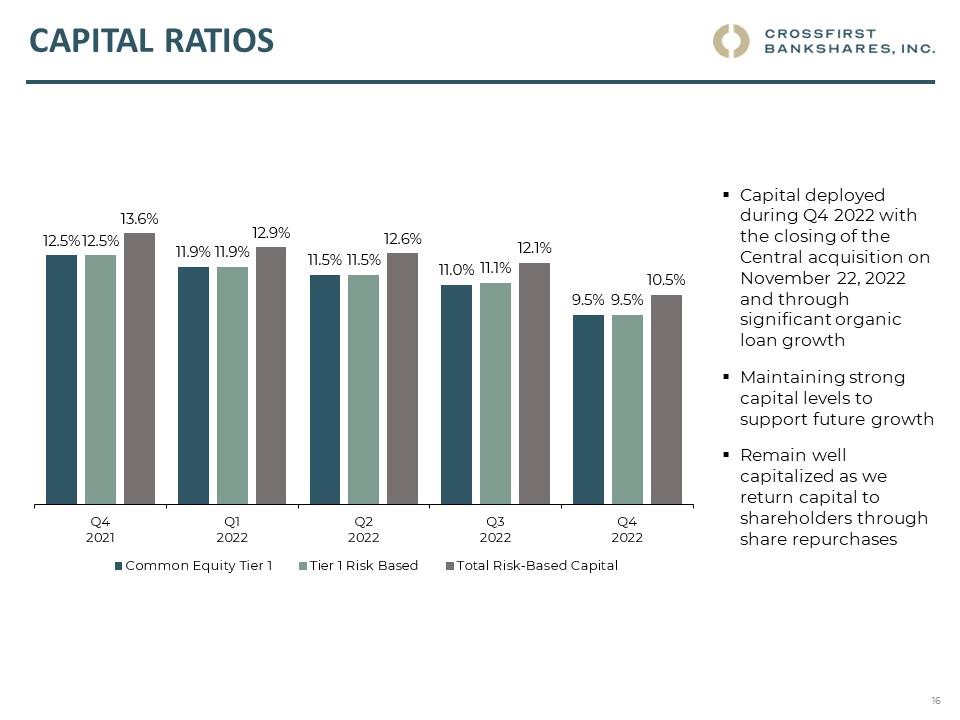

Tangible book value per share was $11.96 at December 31, 2022. The ratio of common equity Tier 1 capital to risk-weighted assets was

approximately 9.5%, and the ratio of total capital to risk-weighted assets was approximately 10.5% at December 31, 2022.

CROSSFIRST BANKSHARES, INC.

6

Conference Call and Webcast

Management will host a conference call to review fourth quarter and full year financial results on Tuesday, January 24, 2023, at 10 a.m.

CT / 11 a.m. ET. The conference call and webcast may also include discussion of Company developments, forward-looking statements and

other material information about business and financial matters. To access the event by telephone, please dial

(

833) 630-1956 at least

fifteen minutes prior to the start of the call and request access to the CrossFirst Bankshares call. International callers should dial

+1

(412)

317-1837 and request access as directed above. The call will also be broadcast live over the internet and can be accessed via the following

link: https://edge.media-server.com/mmc/p/jmnnrip7. Please visit the site at least 15 minutes prior to the call to allow time for registration.

For those unable to join the presentation, a replay of the call will be available two hours after the conclusion of the live call. To access the

replay, dial (877) 344-7529 and enter the replay access code 6033374. International callers should dial +1 (412) 317-0088 and enter the

same access code. A replay of the webcast will also be available for 90 days on the Company’s website

https://investors.crossfirstbankshares.com/.

Cautionary Notice about Forward-Looking Statements

The financial results in this press release reflect preliminary, unaudited results, which are not final until the Company’s Annual Report on

Form 10-K is filed. This earnings release contains forward-looking statements regarding, among other things, our business plans, and

future financial performance. Any statements about management’s expectations, beliefs, plans, predictions, forecasts, objectives,

assumptions or future events or performance are not historical facts and may be forward-looking. These statements are often, but not

always, made through the use of words or phrases such as “positioned,” “growth,” “approximately,” “believe,” “plan,” “future,”

“opportunities,” “feel,” “anticipate,” “target,” “expectations,” “expect,” “will,” and similar words or phrases. The inclusion of forward-

looking information in this earnings release should not be regarded as a representation by us or any other person that the future plans,

estimates or expectations contemplated by us will be achieved. The Company has based these forward-looking statements largely on its

current expectations and projections about future events and financial trends that it believes may affect its financial condition, results of

operations, business strategy and financial needs. Our actual results could differ materially from those anticipated in such forward-looking

statements.

Accordingly, the Company cautions you that any such forward-looking statements are not a guarantee of future performance and that

actual results may prove to be materially different from the results expressed or implied by the forward-looking statements due to a

number of factors. Such factors include, without limitation, economic and market conditions in the United States or internationally, interest

rates, business and growth strategy execution, the transition away from the London Interbank Offered Rate (LIBOR), fluctuations in fair

value of our investments, credit quality and risk, economic impact on our commercial real estate and commercial-based loan portfolios,

accounting estimates, allowance estimate and risk management processes, hiring and retention of key personnel, funding availability,

competition, industry and technological changes, cyber incidents or other failures, disruptions or security breaches, commercial and

residential real estate values, mortgage markets, fraud committed against the Company, reputation risk, environmental liability, severe

weather, natural disasters, acts of war or terrorism or other external events, ongoing impact of the COVID-19 pandemic, and legislative

and regulatory changes. These and other factors that could cause results to differ materially from those described in the forward-looking

statements, as well as a discussion of the risks and uncertainties that may affect our business, can be found in our Annual Report on Form

10-K, our Quarterly Reports on Form 10-Q and in other filings we make with the Securities and Exchange Commission. These forward-

looking statements are made as of the date of this communication, and we disclaim any obligation to update any forward-looking

statement or to publicly announce the results of any revisions to any of the forward-looking statements included herein, except as required

by law.

About CrossFirst Bankshares, Inc.

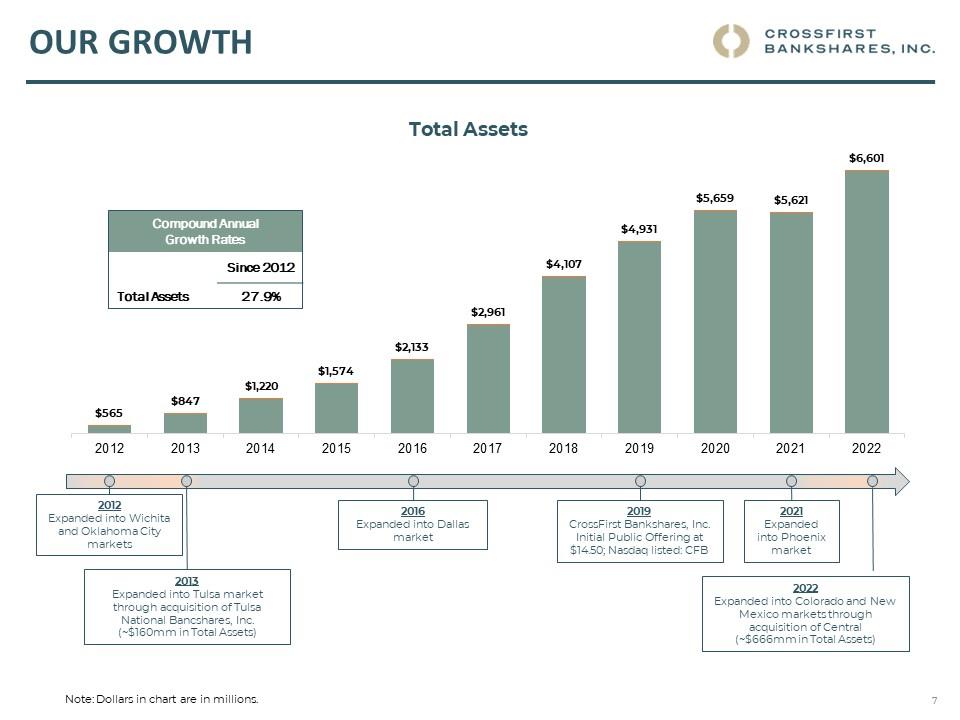

CrossFirst Bankshares, Inc. (Nasdaq: CFB) is a Kansas corporation and a registered bank holding company for its wholly owned

subsidiary CrossFirst Bank, a full-service financial institution that offers product and services to businesses, professionals, individuals, and

families. CrossFirst Bank, headquartered in Leawood, Kansas, has locations in Kansas, Missouri, Oklahoma, Texas, Arizona, Colorado,

and New Mexico.

INVESTOR CONTACT

Heather Worley

Heather@crossfirst.com

(214)676-4666

https://investors.crossfirstbankshares.com

CROSSFIRST BANKSHARES, INC.

7

TABLE 1. CONSOLIDATED BALANCE SHEETS (UNAUDITED)

December 31, 2022

December 31, 2021

(Dollars in thousands)

Assets

Cash and cash equivalents

$

300,138

$

482,727

Available-for-sale securities - taxable

198,808

192,146

Available-for-sale securities - tax-exempt

488,093

553,823

Loans, net of unearned fees

5,372,729

4,256,213

Allowance for credit losses on loans

61,775

58,375

Loans, net of the allowance for credit losses on loans

5,310,954

4,197,838

Premises and equipment, net

65,984

66,069

Restricted equity securities

12,536

11,927

Interest receivable

29,507

16,023

Foreclosed assets held for sale

1,130

1,148

Goodwill and other intangible assets, net

29,081

130

Bank-owned life insurance

69,101

67,498

Other

95,754

32,128

Total assets

$

6,601,086

$

5,621,457

Liabilities and stockholders’ equity

Deposits

Non-interest-bearing

$

1,400,260

$

1,163,224

Savings, NOW and money market

3,305,481

2,895,986

Time

945,567

624,387

Total deposits

5,651,308

4,683,597

Federal Home Loan Bank advances

218,111

236,600

Other borrowings

35,457

1,009

Interest payable and other liabilities

87,611

32,678

Total liabilities

5,992,487

4,953,884

Stockholders’ equity

Common Stock, $0.01 par value: Authorized - 200,000,000 shares, issued -

53,036,613 and 52,590,015 shares at December 31, 2022 and December 31, 2021,

respectively

530

526

Treasury stock, at cost: 4,588,398 and 2,139,970 shares held at December 31,

2022 and December 31, 2021, respectively

(64,127)

(28,347)

Additional paid-in capital

530,658

526,806

Retained earnings

206,095

147,099

Accumulated other comprehensive (loss) income

(64,557)

21,489

Total stockholders’ equity

608,599

667,573

Total liabilities and stockholders’ equity

$

6,601,086

$

5,621,457

CROSSFIRST BANKSHARES, INC.

8

Three Months Ended

Twelve Months Ended

December 31,

December 31,

2022

2021

2022

2021

(Dollars in thousands except per share data)

Interest Income

Loans, including fees

$

74,872

$

44,392

$

224,138

$

174,660

Available-for-sale securities - taxable

1,327

850

4,577

3,273

Available-for-sale securities - tax-exempt

3,896

3,623

15,338

14,033

Deposits with financial institutions

2,037

143

3,751

502

Dividends on bank stocks

231

194

709

682

Total interest income

82,363

49,202

248,513

193,150

Interest Expense

Deposits

26,830

3,734

49,982

18,523

Fed funds purchased and repurchase agreements

13

-

96

3

Federal Home Loan Bank Advances

1,457

1,999

4,759

5,837

Other borrowings

48

24

142

96

Total interest expense

28,348

5,757

54,979

24,459

Net Interest Income

54,015

43,445

193,534

168,691

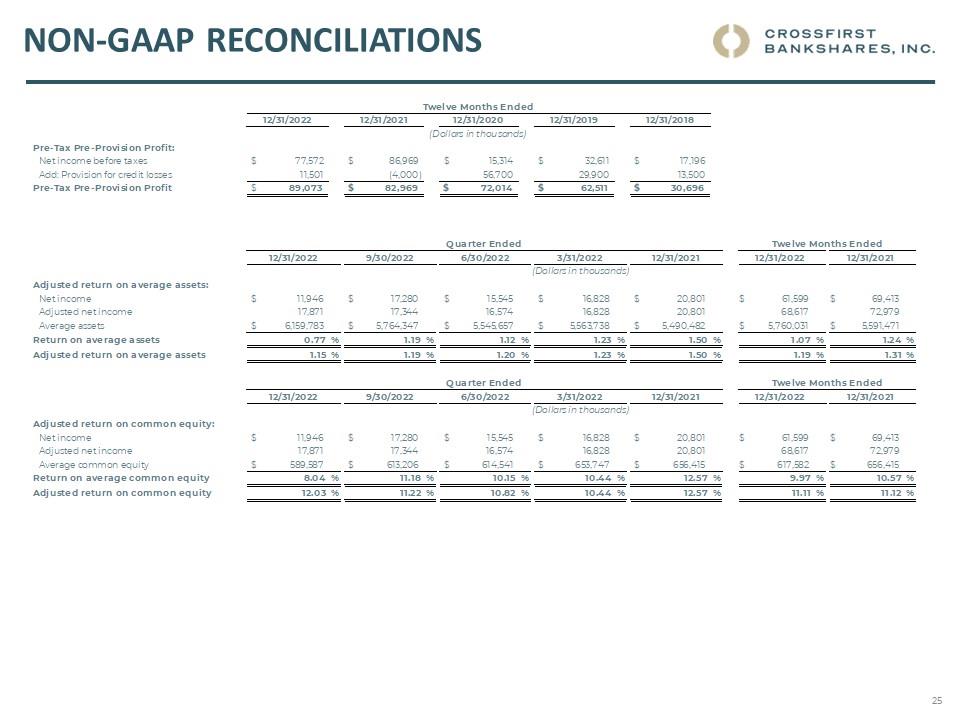

Provision for Credit Losses

6,657

(5,000)

11,501

(4,000)

Net Interest Income after Provision for Credit Losses

47,358

48,445

182,033

172,691

Non-Interest Income

Service charges and fees on customer accounts

1,708

1,250

6,228

4,580

Realized gains (losses) on available-for-sale securities

139

(20)

96

1,023

Gain on sale of loans

47

-

47

-

Gains (losses) on equity securities, net

80

(82)

(181)

(6,325)

Income from bank-owned life insurance

402

395

1,602

3,483

Swap fees and credit valuation adjustments, net

65

119

188

275

ATM and credit card interchange income

1,010

2,427

6,523

7,996

Other non-interest income

908

707

2,778

2,628

Total non-interest income

4,359

4,796

17,281

13,660

Non-Interest Expense

Salaries and employee benefits

22,000

16,468

75,288

61,080

Occupancy

2,812

2,381

10,663

9,688

Professional fees

2,822

981

5,275

3,519

Deposit insurance premiums

999

710

3,354

3,705

Data processing

1,901

742

4,750

2,878

Advertising

954

756

3,201

2,090

Software and communication

1,404

1,136

5,093

4,234

Foreclosed assets, net

13

17

(17)

697

Other non-interest expense

3,518

3,524

14,135

11,491

Total non-interest expense

36,423

26,715

121,742

99,382

Net Income Before Taxes

15,294

26,526

77,572

86,969

Income tax expense

3,348

5,725

15,973

17,556

Net Income

$

11,946

$

20,801

$

61,599

$

69,413

Basic Earnings Per Share

$

0.25

$

0.41

$

1.24

$

1.35

Diluted Earnings Per Share

$

0.24

$

0.40

$

1.23

$

1.33

CROSSFIRST BANKSHARES, INC.

9

TABLE 3. YEAR-TO-DATE ANALYSIS OF CHANGES IN NET INTEREST

INCOME - FTE

(UNAUDITED)

Twelve Months Ended

December 31,

2022

2021

Average

Balance

Interest

Income /

Expense

Average

Yield /

Rate

(4)

Average

Balance

Interest

Income /

Expense

Average

Yield /

Rate

(4)

(Dollars in thousands)

Interest-earning assets:

Securities - taxable

(1)

$

220,760

$

5,286

2.39

%

$

201,419

$

3,955

1.96

%

Securities - tax-exempt - FTE

(1)(2)

551,734

18,559

3.36

488,544

16,981

3.48

Federal funds sold

3,139

49

-

-

-

-

Interest-bearing deposits in other banks

239,240

3,702

1.55

389,893

502

0.13

Gross loans, net of unearned income

(3)

4,603,697

224,138

4.87

4,340,791

174,660

4.02

Total interest-earning assets - FTE

(1)(2)

5,618,570

$

251,734

4.48

%

5,420,647

$

196,098

3.62

%

Allowance for loan losses

(57,388)

(73,544)

Other non-interest-earning assets

198,849

244,368

Total assets

$

5,760,031

$

5,591,471

Interest-bearing liabilities

Transaction deposits

$

538,604

$

4,951

0.92

%

$

608,063

$

1,152

0.19

%

Savings and money market deposits

2,475,891

33,599

1.36

2,338,315

8,225

0.35

Time deposits

688,095

11,432

1.66

812,774

9,146

1.13

Total interest-bearing deposits

3,702,590

49,982

1.35

3,759,152

18,523

0.49

FHLB and short-term borrowings

232,018

4,855

2.09

279,379

5,840

2.09

Trust preferred securities, net of fair value

adjustments

1,072

142

13.25

982

96

9.76

Non-interest-bearing deposits

1,146,594

-

-

876,309

-

-

Cost of funds

5,082,274

$

54,979

1.08

%

4,915,822

$

24,459

0.50

%

Other liabilities

60,175

35,447

Stockholders’ equity

617,582

640,202

Total liabilities and stockholders' equity

$

5,760,031

$

5,591,471

Net interest income - FTE

(2)

$

196,755

$

171,639

Net interest spread - FTE

(1)(2)

3.40

%

3.12

%

Net interest margin - FTE

(1)(2)

3.50

%

3.17

%

(1)

(loss) on available-for-sale securities from an interest-earning asset to a non-interest-earning asset. All periods presented reflect this change.

(2)

rate used is 21.0%.

(3)

Average gross loan balances include non-accrual loans.

(4)

Actual unrounded values are used to calculate the reported yield or rate disclosed. Accordingly, recalculations using the amounts in thousands as disclosed

in this release may not produce the same amounts.

CROSSFIRST BANKSHARES, INC.

10

TABLE 4. 2021 - 2022 QUARTERLY ANALYSIS OF CHANGES IN NET INTEREST INCOME – FTE

(UNAUDITED)

Three Months Ended

December 31,

2022

2021

Average

Balance

Interest

Income /

Expense

Average

Yield /

Rate

(4)

Average

Balance

Interest

Income /

Expense

Average

Yield /

Rate

(4)

(Dollars in thousands)

Interest-earning assets:

Securities - taxable

(1)

$

227,701

$

1,558

2.74

%

$

194,850

$

1,044

2.14

%

Securities - tax-exempt - FTE

(1)(2)

558,393

4,714

3.38

522,860

4,385

3.35

Federal funds sold

12,453

50

-

-

-

-

Interest-bearing deposits in other banks

218,549

1,987

3.61

387,828

143

0.15

Gross loans, net of unearned income

(3)

5,009,667

74,872

5.93

4,220,842

44,392

4.17

Total interest-earning assets - FTE

(1)(2)

6,026,763

$

83,181

5.48

%

5,326,380

$

49,964

3.72

%

Allowance for loan losses

(57,909)

(64,102)

Other non-interest-earning assets

190,929

228,204

Total assets

$

6,159,783

$

5,490,482

Interest-bearing liabilities

Transaction deposits

$

528,725

$

2,772

2.08

%

$

543,088

$

216

0.16

%

Savings and money market deposits

2,742,026

18,359

2.66

2,272,307

1,824

0.32

Time deposits

868,029

5,699

2.60

661,978

1,694

1.02

Total interest-bearing deposits

4,138,780

26,830

2.57

3,477,373

3,734

0.43

FHLB and short-term borrowings

202,705

1,470

2.88

261,600

1,999

3.03

Trust preferred securities, net of fair value

adjustments

1,213

48

15.70

1,000

24

9.67

Non-interest-bearing deposits

1,141,977

-

-

1,058,462

-

-

Cost of funds

5,484,675

$

28,348

2.05

%

4,798,435

$

5,757

0.48

%

Other liabilities

85,521

35,632

Stockholders’ equity

589,587

656,415

Total liabilities and stockholders' equity

$

6,159,783

$

5,490,482

Net interest income - FTE

(2)

$

54,833

$

44,207

Net interest spread - FTE

(1)(2)

3.43

%

3.24

%

Net interest margin - FTE

(1)(2)

3.61

%

3.30

%

(1)

(loss) on available-for-sale securities from an interest-earning asset to a non-interest-earning asset. All periods presented reflect this change.

(2)

rate used is 21.0%.

(3)

Average loan balances include non-accrual loans.

(4)

Actual unrounded values are used to calculate the reported yield or rate disclosed. Accordingly, recalculations using the amounts in thousands as disclosed

in this release may not produce the same amounts.

CROSSFIRST BANKSHARES, INC.

11

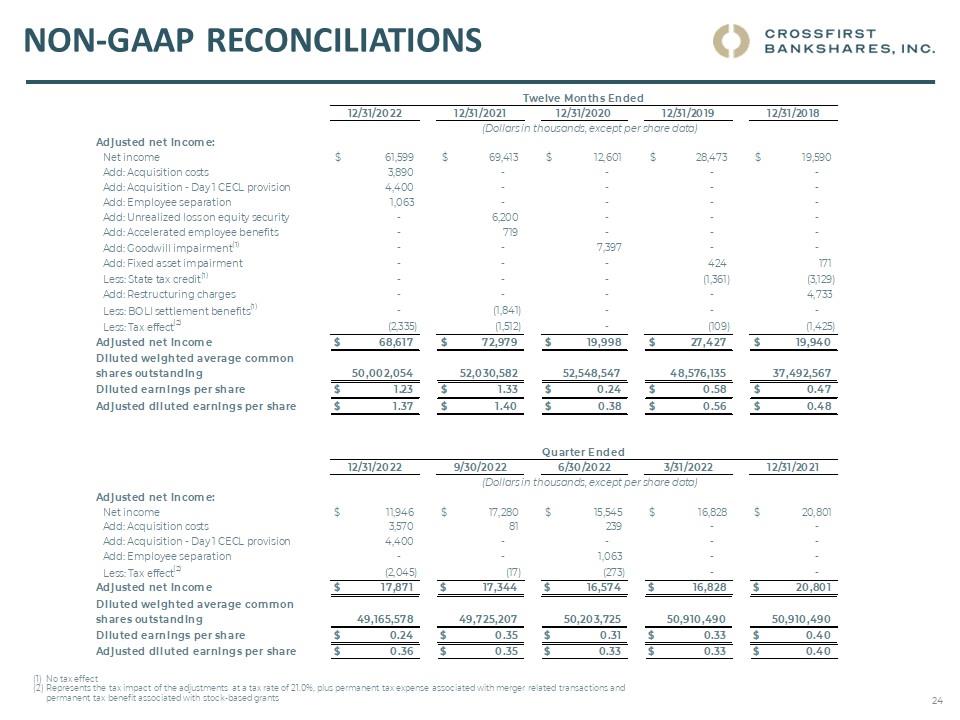

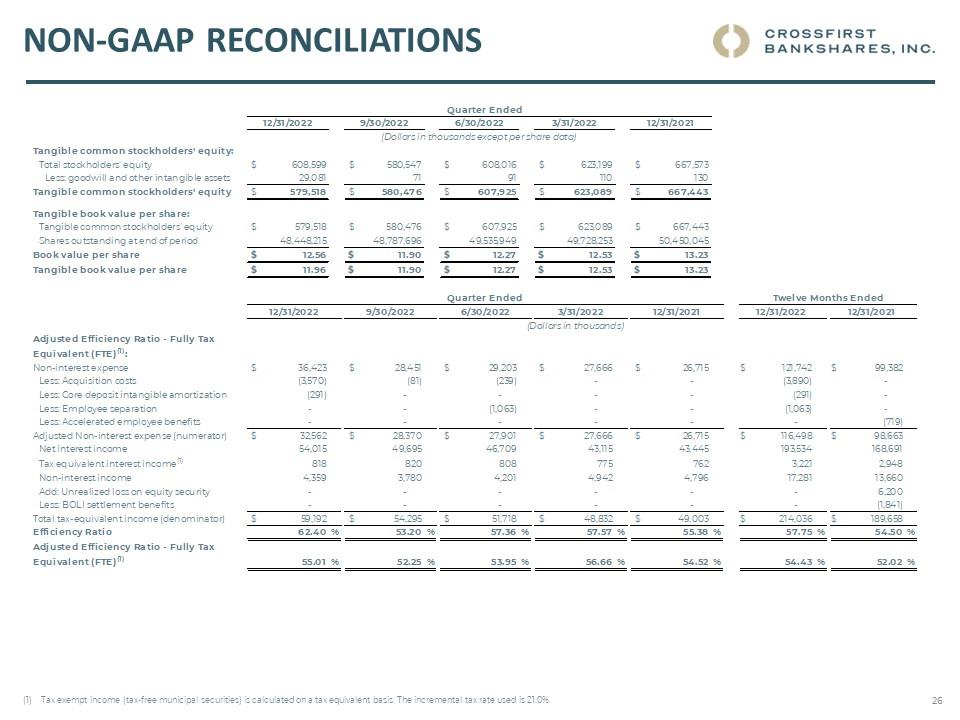

TABLE 5. NON-GAAP FINANCIAL MEASURES

Non-GAAP Financial Measures

In addition to disclosing financial measures determined in accordance with U.S. generally accepted accounting principles (GAAP), the

Company discloses non-GAAP financial measures in this release including “tangible common stockholders’ equity,” “tangible book value

per share,” “adjusted efficiency ratio – fully tax equivalent (FTE),” “adjusted net income,” “adjusted diluted earnings per share,” “adjusted

return on average assets (ROAA),” and “adjusted return on common equity (ROE).” We consider the use of select non-GAAP financial

measures and ratios to be useful for financial and operational decision making and useful in evaluating period-to-period comparisons. We

believe that these non-GAAP financial measures provide meaningful supplemental information regarding our performance by excluding

certain expenditures or gains that we believe are not indicative of our primary business operating results. We believe that management and

investors benefit from referring to these non-GAAP financial measures in assessing our performance and when planning, forecasting,

analyzing and comparing past, present and future periods.

These non-GAAP financial measures should not be considered a substitute for financial information presented in accordance with GAAP

and you should not rely on non-GAAP financial measures alone as measures of our performance. The non-GAAP financial measures we

present may differ from non-GAAP financial measures used by our peers or other companies. We compensate for these limitations by

providing the equivalent GAAP measures whenever we present the non-GAAP financial measures and by including a reconciliation of the

impact of the components adjusted for in the non-GAAP financial measure so that both measures and the individual components may be

considered when analyzing our performance.

A reconciliation of non-GAAP financial measures to the comparable GAAP financial measures follows.

CROSSFIRST BANKSHARES, INC.

12

Quarter Ended

Twelve Months Ended

12/31/2022

9/30/2022

6/30/2022

3/31/2022

12/31/2021

12/31/2022

12/31/2021

(Dollars in thousands, except per share data)

Adjusted net income:

Net income

$

11,946

$

17,280

$

15,545

$

16,828

$

20,801

$

61,599

$

69,413

Add: Acquisition costs

3,570

81

239

-

-

3,890

-

Add: Acquisition - Day 1 CECL provision

4,400

-

-

-

-

4,400

-

Add: Employee separation

-

-

1,063

-

-

1,063

-

Add: Unrealized loss on equity security

-

-

-

-

-

-

6,200

Add: Accelerated employee benefits

-

-

-

-

-

-

719

Less: BOLI settlement benefits

(1)

-

-

-

-

-

-

(1,841)

Less: Tax effect

(2)

(2,045)

(17)

(273)

-

-

(2,335)

(1,512)

Adjusted net income

$

17,871

$

17,344

$

16,574

$

16,828

$

20,801

$

68,617

$

72,979

Diluted weighted average common shares outstanding

49,165,578

49,725,207

50,203,725

50,910,490

51,660,723

50,002,054

52,030,582

Diluted earnings per share

$

0.24

$

0.35

$

0.31

$

0.33

$

0.40

$

1.23

$

1.33

Adjusted diluted earnings per share

$

0.36

$

0.35

$

0.33

$

0.33

$

0.40

$

1.37

$

1.40

(1)

No tax effect.

(2)

Represents the tax impact of the adjustments at a tax rate of 21.0%, plus permanent tax expense associated with merger related transactions and permanent tax benefit associated with stock-based grants

Quarter Ended

Twelve Months Ended

12/31/2022

9/30/2022

6/30/2022

3/31/2022

12/31/2021

12/31/2022

12/31/2021

(Dollars in thousands)

Adjusted return on average assets:

Net income

$

11,946

$

17,280

$

15,545

$

16,828

$

20,801

$

61,599

$

69,413

Adjusted net income

17,871

17,344

16,574

16,828

20,801

68,617

72,979

Average assets

$

6,159,783

$

5,764,347

$

5,545,657

$

5,563,738

$

5,490,482

$

5,760,031

$

5,591,471

Return on average assets

0.77

%

1.19

%

1.12

%

1.23

%

1.50

%

1.07

%

1.24

%

Adjusted return on average assets

1.15

%

1.19

%

1.20

%

1.23

%

1.50

%

1.19

%

1.31

%

Quarter Ended

Twelve Months Ended

12/31/2022

9/30/2022

6/30/2022

3/31/2022

12/31/2021

12/31/2022

12/31/2021

(Dollars in thousands)

Adjusted return on common equity:

Net income

$

11,946

$

17,280

$

15,545

$

16,828

$

20,801

$

61,599

$

69,413

Adjusted net income

17,871

17,344

16,574

16,828

20,801

68,617

72,979

Average common equity

$

589,587

$

613,206

$

614,541

$

653,747

$

656,415

$

617,582

$

640,202

Return on average common equity

8.04

%

11.18

%

10.15

%

10.44

%

12.57

%

9.97

%

10.84

%

Adjusted return on common equity

12.03

%

11.22

%

10.82

%

10.44

%

12.57

%

11.11

%

11.40

%

CROSSFIRST BANKSHARES, INC.

13

Quarter Ended

12/31/2022

9/30/2022

6/30/2022

3/31/2022

12/31/2021

(Dollars in thousands, except per share data)

Tangible common stockholders' equity:

Total stockholders' equity

$

608,599

$

580,547

$

608,016

$

623,199

$

667,573

Less: goodwill and other intangible assets

29,081

71

91

110

130

Tangible common stockholders' equity

$

579,518

$

580,476

$

607,925

$

623,089

$

667,443

Tangible book value per share:

Tangible common stockholders' equity

$

579,518

$

580,476

$

607,925

$

623,089

$

667,443

Shares outstanding at end of period

48,448,215

48,787,696

49,535,949

49,728,253

50,450,045

Book value per share

$

12.56

$

11.90

$

12.27

$

12.53

$

13.23

Tangible book value per share

$

11.96

$

11.90

$

12.27

$

12.53

$

13.23

Quarter Ended

Twelve Months Ended

12/31/2022

9/30/2022

6/30/2022

3/31/2022

12/31/2021

12/31/2022

12/31/2021

(Dollars in thousands)

Adjusted Efficiency Ratio - Fully Tax Equivalent

(FTE)

(1)

Non-interest expense

$

36,423

$

28,451

$

29,203

$

27,666

$

26,715

$

121,742

$

99,382

Less: Acquisition costs

(3,570)

(81)

(239)

-

-

(3,890)

-

Less: Core deposit intangible amortization

(291)

-

-

-

-

(291)

-

Less: Employee separation

-

-

(1,063)

-

-

(1,063)

-

Less: Accelerated employee benefits

-

-

-

-

-

-

(719)

Adjusted Non-interest expense (numerator)

$

32,562

$

28,370

$

27,901

$

27,666

$

26,715

$

116,498

$

98,663

Net interest income

54,015

49,695

46,709

43,115

43,445

193,534

168,691

Tax equivalent interest income

(1)

818

820

808

775

762

3,221

2,948

Non-interest income

4,359

3,780

4,201

4,942

4,796

17,281

13,660

Add: Unrealized loss on equity security

-

-

-

-

-

-

6,200

Less: BOLI settlement benefits

-

-

-

-

-

-

(1,841)

Total tax-equivalent income (denominator)

$

59,192

$

54,295

$

51,718

$

48,832

$

49,003

$

214,036

$

189,658

Efficiency Ratio

62.40

%

53.20

%

57.36

%

57.57

%

55.38

%

57.75

%

54.50

%

Adjusted Efficiency Ratio - Fully Tax Equivalent

(FTE)

(1)

55.01

%

52.25

%

53.95

%

56.66

%

54.52

%

54.43

%

52.02

%

(1)

Tax exempt income (tax-free municipal securities) is calculated on a tax equivalent basis. The incremental tax rate used is 21.0%.