Consolidated Financial Statements

(Expressed in U.S. dollars)

BALLARD POWER SYSTEMS INC.

Years ended December 31, 2022 and 2021

MANAGEMENT’S REPORT

Management’s Responsibility for the Financial Statements and Report on Internal Control over Financial Reporting

The consolidated financial statements contained in this Annual Report have been prepared by management in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board. The integrity and objectivity of the data in these consolidated financial statements are management’s responsibility. Management is also responsible for all other information in the Annual Report and for ensuring that this information is consistent, where appropriate, with the information and data contained in the consolidated financial statements.

Management is responsible for establishing and maintaining adequate internal control over financial reporting. Internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of consolidated financial statements for external reporting purposes in accordance with IFRS. Internal control over financial reporting may not prevent or detect fraud or misstatements because of limitations inherent in any system of internal control. Management has assessed the effectiveness of the Corporation’s internal control over financial reporting based on the framework in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission, and concluded that the Corporation’s internal control over financial reporting was effective as of December 31, 2022. In addition, management maintains disclosure controls and procedures to provide reasonable assurance that material information is communicated to management and appropriately disclosed. Some of the assets and liabilities include amounts, which are based on estimates and judgments, as their final determination is dependent on future events.

The Board of Directors oversees management’s responsibilities for financial reporting through the Audit Committee, which consists of eight directors who are independent and not involved in the daily operations of the Corporation. The Audit Committee meets on a regular basis with management and the external and internal auditors to discuss internal controls over the financial reporting process, auditing matters and financial reporting issues. The Audit Committee is responsible for appointing the external auditors (subject to shareholder approval), and reviewing and approving all financial disclosure contained in our public documents and related party transactions.

The external auditors, KPMG LLP, have audited the financial statements and expressed an unqualified opinion thereon. KPMG has also expressed an unqualified opinion on the effective operation of the internal controls over financial reporting as of December 31, 2022. The external auditors have full access to management and the Audit Committee with respect to their findings concerning the fairness of financial reporting and the adequacy of internal controls.

| “RANDALL MACEWEN” | “PAUL DOBSON” | ||||

| RANDALL MACEWEN | PAUL DOBSON | ||||

| President and | Vice President and | ||||

| Chief Executive Officer | Chief Financial Officer | ||||

| March 16, 2023 | March 16, 2023 | ||||

| ||||||||

KPMG LLP Chartered Professional Accountants PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K23 Canada | Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca | |||||||

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors

Ballard Power Systems Inc.

Opinion on the Consolidated Financial Statements

We have audited the accompanying consolidated statements of financial position of Ballard Power Systems Inc. and subsidiaries (the Corporation) as of December 31, 2022 and 2021, the related consolidated statements of loss and comprehensive income (loss), changes in equity, and cash flows for each of the years then ended, and the related notes (collectively, the consolidated financial statements). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Corporation as of December 31, 2022 and 2021, and its operations and its cash flows for each of the years then ended, in conformity with International Financial Reporting Standards as issued by the International Accounting Standards Board.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the Corporation’s internal control over financial reporting as of December 31, 2022, based on criteria established in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission, and our report dated March 15, 2023 expressed “an unqualified opinion on the effectiveness of the Corporation’s internal control over financial reporting”.

Change in Accounting Principle

As discussed in Note 3 to the consolidated financial statements, the Corporation has changed its method of accounting for onerous contracts as of January 1, 2022 due to the adoption of Amendments to IAS 37.

Basis for Opinion

These consolidated financial statements are the responsibility of the Corporation’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Corporation in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the consolidated financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements. We believe that our audits provide a reasonable basis for our opinion.

KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. KPMG Canada provides services to KPMG LLP.

Critical Audit Matter

The critical audit matter communicated below is the matter arising from the current period audit of the consolidated financial statements that was communicated or required to be communicated to the audit committee and that: (1) relate to accounts or disclosures that are material to the consolidated financial statements and (2) involved our especially challenging, subjective, or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the consolidated financial statements, taken as a whole, and we are not, by communicating the critical audit matter below, providing a separate opinion on the critical audit matter or on the accounts or disclosures to which it relates.

Estimated costs to complete engineering and technology transfer services for long-term fixed-price contracts

As discussed in Notes 4(j) and 5(a) to the consolidated financial statements, the Corporation recognizes engineering and technology transfer service revenues from long-term fixed-price contracts over time by multiplying the expected consideration from the contract by the ratio of the cost incurred to date to estimated costs to complete the contract. Engineering and technology transfer service revenues from long-term fixed-price contracts are inherently uncertain in that total revenue from these contracts is fixed while the amount recognized to a period end requires estimates of costs to complete these contracts which estimates are subject to significant variability. As discussed in Note 23 to the consolidated financial statements, engineering and technology transfer service revenues from long-term fixed-price contracts totaled $31,037 thousand for the year ended December 31, 2022.

We identified the evaluation of the estimate of costs to complete engineering and technology transfer services for long-term fixed-price contracts as a critical audit matter. A higher degree of auditor judgment was required to evaluate the significant assumptions used to estimate costs to complete the contracts, including the estimated labour hours and cost of materials to complete the contracts.

The following are the primary procedures we performed to address this critical audit matter. We evaluated the design and tested the operating effectiveness of internal controls related to the Corporation’s determination of estimated costs to complete long-term fixed-price contracts, including the determination of significant assumptions. For a selection of long-term fixed-price contracts we compared the Corporation’s historical estimated costs to complete contracts to actual labour hours and cost of materials incurred to assess the Corporation’s ability to accurately forecast. We evaluated the estimated costs to completion for a selection of customer contracts, by (1) inspecting contractual documents with customers to understand the timing of services; (2) interviewing operational personnel of the Corporation to evaluate progress to date, the estimate of costs to complete contracts, and factors impacting the estimated labour hours and cost of material to complete the contracts; (3) evaluating contract progress by inspecting correspondence between the Corporation and the customer; (4) evaluating the cost to complete the contracts for consistency with the status of delivery and the underlying contractual terms; (5) comparing the Corporation’s current estimate of costs to complete the contracts to those estimated in prior periods and investigating changes during the period; and (6) comparing labour hours and cost of materials incurred subsequent to the Corporation’s year-end date to assess the consistency with the estimated costs for the period.

//s// KPMG LLP

We have served as the Corporation’s auditor since 1999.

Chartered Professional Accountants

Vancouver, Canada

March 16, 2023

KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. KPMG Canada provides services to KPMG LLP.

| ||||||||

KPMG LLP Chartered Professional Accountants PO Box 10426 777 Dunsmuir Street Vancouver BC V7Y 1K23 Canada | Telephone (604) 691-3000 Fax (604) 691-3031 Internet www.kpmg.ca | |||||||

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors

Ballard Power Systems Inc.:

Opinion on Internal Control Over Financial Reporting

We have audited Ballard Power Systems Inc.’s and subsidiaries’ (the Corporation) internal control over financial reporting as of December 31, 2022, based on criteria established in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission. In our opinion, the Corporation maintained, in all material respects, effective internal control over financial reporting as of December 31, 2022, based on criteria established in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the consolidated statements of financial position of the Corporation as of December 31, 2022 and 2021, the related consolidated statements of loss and comprehensive income (loss), changes in equity, and cash flows for each of the years then ended, and the related notes (collectively, the consolidated financial statements), and our report dated March 16, 2023 expressed “an unqualified opinion on those consolidated financial statements”.

Basis for Opinion

The Corporation’s management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting, included in the accompanying “Management’s Responsibility for the Financial Statements and Report on Internal Control over Financial Reporting” . Our responsibility is to express an opinion on the Corporation’s internal control over financial reporting based on our audit. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Corporation in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects. Our audit of internal control over financial reporting included obtaining an understanding of internal control over financial reporting, assessing the risk that a material weakness exists, and testing and evaluating the design and operating effectiveness of internal control based on the assessed risk. Our audit also included performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion.

KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. KPMG Canada provides services to KPMG LLP.

Definition and Limitations of Internal Control Over Financial Reporting

A company’s internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company’s internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could have a material effect on the financial statements.

Because of its inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

//s// KPMG LLP

March 16, 2023

KPMG LLP is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. KPMG Canada provides services to KPMG LLP.

BALLARD POWER SYSTEMS INC.

Consolidated Statements of Financial Position

(Expressed in thousands of U.S. dollars)

| Note | December 31, 2022 | December 31, 2021 | ||||||||||||||||||

| Assets | ||||||||||||||||||||

| Current assets: | ||||||||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||||||||

| Short-term investments | ||||||||||||||||||||

| Trade and other receivables | 9 | |||||||||||||||||||

| Inventories | 10 | |||||||||||||||||||

| Prepaid expenses and other current assets | ||||||||||||||||||||

| Total current assets | ||||||||||||||||||||

| Non-current assets: | ||||||||||||||||||||

| Property, plant and equipment | 11 | |||||||||||||||||||

| Intangible assets | 12 & 27 | |||||||||||||||||||

| Goodwill | 13 | |||||||||||||||||||

| Investments | 14 | |||||||||||||||||||

| Other long-term assets | ||||||||||||||||||||

| Total assets | $ | $ | ||||||||||||||||||

| Liabilities and Equity | ||||||||||||||||||||

| Current liabilities: | ||||||||||||||||||||

| Trade and other payables | 16 | $ | $ | |||||||||||||||||

| Deferred revenue | 17 | |||||||||||||||||||

| Provisions and other current liabilities | 18 | |||||||||||||||||||

| Current lease liabilities | 19 | |||||||||||||||||||

| Total current liabilities | ||||||||||||||||||||

| Non-current liabilities: | ||||||||||||||||||||

| Non-current lease liabilities | 19 | |||||||||||||||||||

| Deferred gain on finance lease liability | 19 | |||||||||||||||||||

| Provisions and other non-current liabilities | 18 | |||||||||||||||||||

| Employee future benefits | 20 | |||||||||||||||||||

| Deferred income tax liability | 29 | |||||||||||||||||||

| Total liabilities | ||||||||||||||||||||

| Equity: | ||||||||||||||||||||

| Share capital | 21 | |||||||||||||||||||

| Contributed surplus | 21 | |||||||||||||||||||

| Accumulated deficit | ( | ( | ||||||||||||||||||

| Foreign currency reserve | ( | |||||||||||||||||||

| Total equity | ||||||||||||||||||||

| Total liabilities and equity | $ | $ | ||||||||||||||||||

See accompanying notes to consolidated financial statements.

Approved on behalf of the Board:

| “Doug Hayhurst” | “Jim Roche” | ||||

| Director | Director | ||||

BALLARD POWER SYSTEMS INC.

Consolidated Statements of Loss and Comprehensive Income (Loss)

For the years ended December 31

(Expressed in thousands of U.S. dollars, except per share amounts and number of shares)

| Note | 2022 | 2021 | ||||||||||||||||||

| Revenues: | ||||||||||||||||||||

| Product and service revenues | 23 & 32 | $ | $ | |||||||||||||||||

| Cost of product and service revenues | ||||||||||||||||||||

| Gross margin | ( | |||||||||||||||||||

| Operating expenses: | ||||||||||||||||||||

| Research and product development | ||||||||||||||||||||

| General and administrative | ||||||||||||||||||||

| Sales and marketing | ||||||||||||||||||||

| Other expense | 25 | |||||||||||||||||||

| Total operating expenses | ||||||||||||||||||||

| Results from operating activities | ( | ( | ||||||||||||||||||

| Finance loss and other | 26 | ( | ( | |||||||||||||||||

| Finance expense | 26 | ( | ( | |||||||||||||||||

| Net finance loss | ( | ( | ||||||||||||||||||

| Equity in loss of investment in joint venture and associates | 14 & 30 | ( | ( | |||||||||||||||||

| Impairment charges on property, plant and equipment | 11 | ( | ( | |||||||||||||||||

| Impairment charges on intangible assets | 12 & 27 | ( | ||||||||||||||||||

| Recovery on settlement of contingent consideration | 28 | |||||||||||||||||||

| Loss before income taxes | ( | ( | ||||||||||||||||||

| Income tax recovery | 29 | |||||||||||||||||||

| Net loss from continued operations | ( | ( | ||||||||||||||||||

| Net income from discontinued operations | 8 | |||||||||||||||||||

| Net loss | $ | ( | $ | ( | ||||||||||||||||

| Other comprehensive income (loss): | ||||||||||||||||||||

| Items that will not be reclassified to profit or loss: | ||||||||||||||||||||

| Actuarial gain on defined benefit plans | 20 | |||||||||||||||||||

| Items that may be reclassified subsequently to profit or loss: | ||||||||||||||||||||

| Foreign currency translation differences | ( | |||||||||||||||||||

| ( | ||||||||||||||||||||

| Other comprehensive income (loss), net of tax | ( | |||||||||||||||||||

| Total comprehensive loss | $ | ( | $ | ( | ||||||||||||||||

| Basic and diluted loss per share | ||||||||||||||||||||

| Loss per share | $ | ( | $ | ( | ||||||||||||||||

| Weighted average number of common shares outstanding | ||||||||||||||||||||

See accompanying notes to consolidated financial statements.

BALLARD POWER SYSTEMS INC.

Consolidated Statements of Changes in Equity

(Expressed in thousands of U.S. dollars except number of shares)

| Number of shares | Share capital | Contributed surplus | Accumulated deficit | Foreign currency reserve | Total equity | |||||||||||||||||||||||||||||||||

| Balance, December 31, 2020 | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Deferred share consideration related to acquisition (notes 7 & 21) | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Equity offerings (note 21) | — | — | — | |||||||||||||||||||||||||||||||||||

| DSUs redeemed (note 21) | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| RSUs redeemed (note 21) | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Options exercised (note 21) | ( | — | — | |||||||||||||||||||||||||||||||||||

| Share-based compensation (note 21) | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Other comprehensive loss: | ||||||||||||||||||||||||||||||||||||||

| Defined benefit plan actuarial gain (note 20) | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Foreign currency translation for foreign operations | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Balance, December 31, 2021 | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||

| Onerous contracts provision (notes 4 & 18) | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Restated balance, January 1, 2022 | $ | $ | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Deferred share consideration related to acquisition (notes 7 & 21) | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| DSUs redeemed (note 21) | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| RSUs redeemed (note 21) | ( | — | — | ( | ||||||||||||||||||||||||||||||||||

| Options exercised (note 21) | ( | — | — | |||||||||||||||||||||||||||||||||||

| Share-based compensation (note 21) | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss): | ||||||||||||||||||||||||||||||||||||||

| Defined benefit plan actuarial gain (note 20) | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Foreign currency translation for foreign operations | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||

| Balance, December 31, 2022 | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||

See accompanying notes to consolidated financial statements.

BALLARD POWER SYSTEMS INC.

Consolidated Statements of Cash Flows

For the years ended December 31

(Expressed in thousands of U.S. dollars)

| Note | 2022 | 2021 | ||||||||||||||||||

| Cash provided by (used in): | ||||||||||||||||||||

| Operating activities: | ||||||||||||||||||||

| Net loss for the year | $ | ( | $ | ( | ||||||||||||||||

| Adjustments for: | ||||||||||||||||||||

| Depreciation and amortization | ||||||||||||||||||||

| Impairment loss on trade receivables | 25 | |||||||||||||||||||

| Unrealized loss on forward contracts | ||||||||||||||||||||

| Equity in loss of investment in joint venture and associates | 14 & 30 | |||||||||||||||||||

| Net decrease in fair value of investments | 14 & 33 | |||||||||||||||||||

| Impairment charges on property, plant and equipment | 11 | |||||||||||||||||||

| Impairment charges on intangible assets | 12 & 27 | |||||||||||||||||||

| Recovery on settlement of contingent consideration | 28 | ( | ||||||||||||||||||

| Accretion (dilution) on decommissioning liabilities | ( | |||||||||||||||||||

| Employee future benefits | 20 | |||||||||||||||||||

| Employee future benefits plan contributions | 20 | ( | ( | |||||||||||||||||

| Share-based compensation | 21 | |||||||||||||||||||

| Deferred income tax recovery | ( | ( | ||||||||||||||||||

| ( | ( | |||||||||||||||||||

| Changes in non-cash working capital: | ||||||||||||||||||||

| Trade and other receivables | ( | |||||||||||||||||||

| Inventories | ( | ( | ||||||||||||||||||

| Prepaid expenses and other current assets | ( | ( | ||||||||||||||||||

| Trade and other payables | ||||||||||||||||||||

| Deferred revenue | ( | |||||||||||||||||||

| Warranty provision | ( | |||||||||||||||||||

| ( | ( | |||||||||||||||||||

| Cash used in operating activities | ( | ( | ||||||||||||||||||

| Investing activities: | ||||||||||||||||||||

| Net decrease in short-term investments | 33 | |||||||||||||||||||

| Contributions to long-term investments | 14 | ( | ( | |||||||||||||||||

| Additions to property, plant and equipment | 11 | ( | ( | |||||||||||||||||

| Investment in intangible assets | 12 | ( | ( | |||||||||||||||||

| Investment in joint venture and associates | 14 | ( | ( | |||||||||||||||||

| Consideration paid related to acquisition | 7 & 28 | ( | ( | |||||||||||||||||

| Cash used in investing activities | ( | ( | ||||||||||||||||||

| Financing activities: | ||||||||||||||||||||

| Principal payments of lease liabilities | 19 | ( | ( | |||||||||||||||||

| Net proceeds on issuance of share capital from share option exercises | 21 | |||||||||||||||||||

| Net proceeds on issuance of share capital from equity offering | 21 | |||||||||||||||||||

| Cash provided by (used in) financing activities | ( | |||||||||||||||||||

| Effect of exchange rate fluctuations on cash and cash equivalents held | ( | ( | ||||||||||||||||||

| Increase (decrease) in cash and cash equivalents | ( | |||||||||||||||||||

| Cash and cash equivalents, beginning of year | ||||||||||||||||||||

| Cash and cash equivalents, end of year | $ | $ | ||||||||||||||||||

Supplemental disclosure of cash flow information (note 31). See accompanying notes to consolidated financial statements.

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

1. Reporting entity:

The principal business of Ballard Power Systems Inc. (the “Corporation”) is the design, development, manufacture, sale and service of proton exchange membrane ("PEM") fuel cell products for a variety of applications, focusing on the power product markets of Heavy-Duty Motive (consisting of bus, truck, rail and marine applications), Material Handling and Stationary Power Generation, as well as the delivery of Technology Solutions, including engineering services, technology transfer, and the license and sale of the Corporation's extensive intellectual property portfolio and fundamental knowledge for a variety of PEM fuel cell applications. A fuel cell is an environmentally clean electrochemical device that combines hydrogen fuel with oxygen (from the air) to produce electricity.

The Corporation is a company domiciled in Canada and its registered office is located at 9000 Glenlyon Parkway, Burnaby, British Columbia, Canada, V5J 5J8. The consolidated financial statements of the Corporation as at and for the years ended December 31, 2022 and 2021 comprise the Corporation and its subsidiaries (note 4(a)).

2. Basis of preparation:

(a) Statement of compliance:

These consolidated financial statements of the Corporation have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

The consolidated financial statements were authorized for issue by the Board of Directors on March 16, 2023.

Details of the Corporation's significant accounting policies are included in note 4.

(b) Basis of measurement:

The consolidated financial statements have been prepared on the historical cost basis except for the following material items in the statement of financial position:

•Financial assets classified as measured at fair value through profit or loss (FVTPL); and

•Employee future benefits liability is recognized as the net of the present value of the defined benefit obligation, less the fair value of plan assets.

(c) Functional and presentation currency:

These consolidated financial statements are presented in U.S. dollars, which is the Corporation’s functional currency.

(d) Use of estimates:

The preparation of the consolidated financial statements in conformity with IFRS requires the Corporation’s management to make estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected.

Significant areas having estimation uncertainty include revenue recognition, asset impairment, warranty provision, inventory provision, and employee future benefits. These estimates and judgments are discussed further in note 5.

11

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

2. Basis of preparation (cont'd):

(e) Future operations:

The Corporation is required to assess its ability to continue as a going concern or whether substantial doubt exists as to the Corporation’s ability to continue as a going concern into the foreseeable future. The Corporation has forecast its cash flows for the foreseeable future and despite the ongoing volatility and uncertainties inherent in the business, the Corporation believes it has adequate liquidity in cash and working capital to achieve its liquidity objective. The Corporation’s ability to continue as a going concern and realize its assets and discharge its liabilities and commitments in the normal course of business is dependent upon the Corporation having adequate liquidity and achieving profitable operations that are sustainable.

The Corporation’s strategy to mitigate this uncertainty is to continue its drive to attain profitable operations that are sustainable by executing a business plan that continues to focus on revenue growth, improving overall gross margins, maintaining discipline over cash operating expenses, managing working capital and capital expenditure requirements, and securing additional financing to fund operations as needed until the Corporation does achieve profitable operations that are sustainable. Failure to implement this plan could have a material adverse effect on the Corporation’s financial condition and or results of operations.

3. Changes in accounting policies:

The Corporation has consistently applied the accounting policies set out in note 4 to all periods presented in these consolidated financial statements.

The Corporation has initially adopted Onerous Contracts – Cost of Fulfilling a Contract (Amendments to IAS 37), effective January 1, 2022.

Onerous Contracts – Cost of Fulfilling a Contract (Amendments to IAS 37)

IAS 37 does not specify which costs are included as a cost of fulfilling a contract when determining whether a contract is onerous. The IASB’s amendments address this issue by clarifying that the "costs of fulfilling a contract" comprise both:

•the incremental costs – e.g. direct labour and materials; and

•an allocation of other direct costs – e.g. an allocation of the depreciation charge for an item of PPE used in fulfilling the contract.

The amendments are effective for annual periods beginning on or after January 1, 2022 and apply to contracts existing at the date when the amendments are first applied. At the date of initial application of the amendments to IAS 37, the cumulative effect of applying the amendments is recognized as an opening balance adjustment to retained earnings or other component of equity, as appropriate. The comparatives are not restated.

On completion of a review of the Corporation's "open" contracts as of December 31, 2021, it was determined that on adoption of the Amendments to IAS 37 on January 1, 2022, additional onerous contract costs of $1,200,000 were recognized as an opening balance adjustment to accumulated deficit. As of December 31, 2022, total onerous contract cost provisions of $4,400,000 have been accrued in provisions and other current liabilities.

A number of new standards and interpretations became effective from January 1, 2022 however, they did not have a material impact on the Corporation's consolidated financial statements.

12

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies:

The accounting policies set out below have been applied consistently to all periods presented in these consolidated financial statements, unless otherwise indicated.

(a) Basis of consolidation:

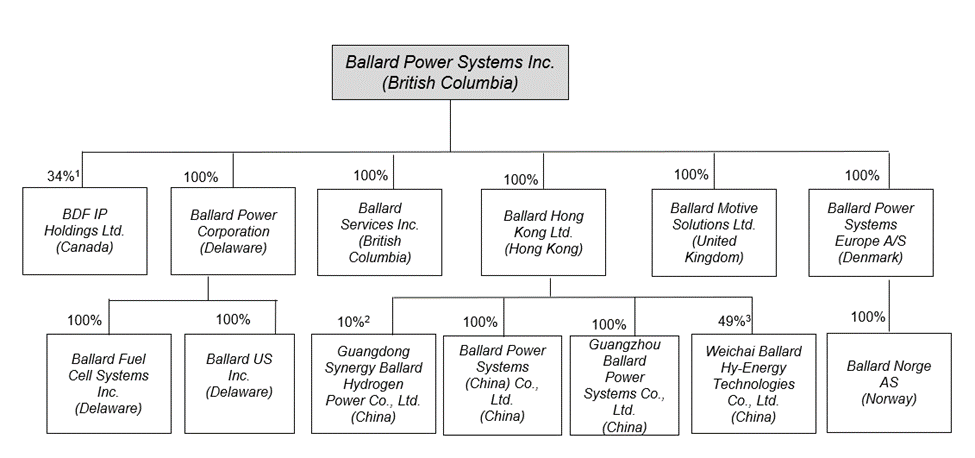

The consolidated financial statements include the accounts of the Corporation and its principal subsidiaries as follows:

| Percentage ownership | |||||||||||

| 2022 | 2021 | ||||||||||

| Ballard Motive Solutions | % | % | |||||||||

| Guangzhou Ballard Power Systems Co., Ltd. | % | % | |||||||||

| Ballard Power Systems Europe A/S | % | % | |||||||||

| Ballard Hong Kong Ltd. | % | % | |||||||||

| Ballard US Inc. | % | % | |||||||||

| Ballard Services Inc. | % | % | |||||||||

| Ballard Fuel Cell Systems Inc. | % | % | |||||||||

| Ballard Power Corporation | % | % | |||||||||

Subsidiary Entities

(i) Ballard Motive Solutions

On November 11, 2021, the Corporation acquired Ballard Motive Solutions (formerly Arcola Energy Limited), a UK-based systems engineering company specializing in hydrogen fuel cell systems and powertrain integration.

(ii) Guangzhou Ballard Power Systems

On January 10, 2017, the Corporation incorporated Guangzhou Ballard Power Systems Co., Ltd. ("GBPS"), a 100 % wholly foreign-owned enterprise ("WFOE") in China to serve as the Corporation's operations entity for all of China.

(iii) Ballard Power Systems Europe A/S

On January 18, 2010, the Corporation acquired a 45 % interest in its European subsidiary, Ballard Power Systems Europe A/S ("BPSE"). BPSE (formerly Dantherm Power A/S) has been consolidated since acquisition. In August 2010, the Corporation acquired an additional 7 % interest and a further 5 % interest in December 2012. On January 5, 2017, the Corporation purchased the remaining 43 % interest in its subsidiary, held by Dansk Industri Invest A/S, thus resulting in the Corporation now owning 100 % of BPSE. BPSE supports a growing market and customer base with sales, business development, engineering, manufacturing and service capabilities.

(iv) Ballard Hong Kong Ltd.

On July 19, 2016, the Corporation incorporated Ballard Hong Kong Ltd. (“BHKL”), a 100 % owned holding company in Hong Kong, China.

13

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(a) Basis of consolidation (cont'd):

(v) Ballard Unmanned Systems

On October 1, 2015, the Corporation acquired Ballard Unmanned Systems (formerly Protonex Technology Corporation), a designer and manufacturer of advanced power management products and portable fuel cell solutions. On October 14, 2020, the Corporation completed an agreement to sell the remaining business assets of this subsidiary (note 8). The entity will remain held by the Corporation and has been re-named Ballard US Inc.

Equity Investment Entities

The Corporation also has a non-controlling, 49 % interest (2021 - 49 %), in Weichai Ballard Hy-Energy Technologies Co., Ltd ("Weichai Ballard JV") and a non-controlling, 10 % interest (2021 - 10 %), in Guangdong Synergy Ballard Hydrogen Power Co., Ltd (“Synergy Ballard JVCo”). Both of these associated companies are accounted for using the equity method of accounting.

(i) Weichai Ballard JV

On November 13, 2018, the Corporation, through Ballard Hong Kong Ltd. ("BHKL"), established a joint venture company, Weichai Ballard Hy-Energy Technologies Co., Ltd. ("Weichai Ballard JV"), in Shandong province to support China's fuel cell electric vehicle market, with Weichai Power ("Weichai") holding a controlling ownership interest of 51 % and the Corporation holding a non-controlling 49 % ownership position. Weichai Ballard JV's business is to manufacture fuel cell products utilizing the Corporation's liquid-cooled fuel cell stack ("LCS") and LCS-based power modules for bus, commercial truck and forklift applications with certain exclusive rights in China.

During the years 2018 through 2022, Weichai has made all of its committed capital contributions totaling RMB 561,000,000 and the Corporation has made all of its committed capital contributions totaling RMB 539,000,000 ($79,369,000 ). Weichai holds three of five Weichai Ballard JV board seats and Ballard holds two , with Ballard having certain shareholder protection provisions. Weichai Ballard JV is not controlled by the Corporation and therefore is not consolidated. The Corporation's 49 % investment in Weichai Ballard JV is accounted for using the equity method of accounting.

(ii) Synergy Ballard JVCo

On September 26, 2016, the Corporation, through BHKL, established a joint venture company, Guangdong Synergy Hydrogen Power Co., Ltd (“Synergy Ballard JVCo”), located in Guangdong province in China. Synergy Ballard JVCo's business is to manufacture fuel cell products utilizing the Corporation's FCvelocity®-9SSL fuel cell stack technology for use primarily in fuel cell engines assembled and sold in China.

The Corporation holds a non-controlling 10 % interest in the joint venture, Synergy Ballard JVCo, together with Guangdong Nation Synergy Hydrogen Power Technology Co., Ltd. (a member of the “Synergy Group”) who holds a controlling 90 % interest. Synergy Ballard JVCo is not controlled by the Corporation and therefore is not consolidated. The Corporation’s 10 % investment in Synergy Ballard JVCo is accounted for using the equity method of accounting.

14

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(b) Foreign currency:

(i) Foreign currency transactions

Transactions in foreign currencies are translated to the respective functional currencies of the Corporation and its subsidiaries at the exchange rate in effect at the transaction date. Monetary assets and liabilities denominated in other than the functional currency are translated at the exchange rates in effect at the statement of financial position date. The resulting exchange gains and losses are recognized in earnings. Non-monetary assets and liabilities denominated in other than the functional currency that are measured at fair value are translated to the functional currency at the exchange rate at the date that the fair value was determined. Non-monetary items that are measured in terms of historical cost in other than the functional currency are translated using the exchange rate at the date of the transaction.

(ii) Foreign operations

The assets and liabilities of foreign operations are translated to the presentation currency using exchange rates at the reporting date. The income and expenses of foreign operations are translated to the presentation currency using exchange rates at the dates of the transactions. Foreign currency differences are recognized in other comprehensive income.

(c) Financial instruments:

(i) Financial assets

The Corporation initially recognizes loans and receivables and deposits on the date that they originated and all other financial assets on the trade date at which the Corporation becomes a party to the contractual provisions of the instrument. The Corporation de-recognizes a financial asset when the contractual rights to the cash flows from the asset expire, or when it transfers substantially all the risks and rewards of ownership of the financial asset.

Financial assets are classified as measured at: amortized cost; fair value through other comprehensive income ("FVOCI") or fair value through profit or loss ("FVTPL"). The classification of financial assets is generally based on the business model in which a financial asset is managed and its contractual cash flow characteristics. Derivatives embedded in contracts where the host is a financial asset in the scope of the standard are never separated. Instead, the hybrid financial instrument as a whole is assessed for classification. The Corporation's financial assets which consist primarily of cash and cash equivalents, short-term investments, trade and other receivables, and contract assets are classified at amortized cost.

The Corporation also periodically enters into foreign exchange forward contracts to limit its exposure to foreign currency rate fluctuations. These derivatives are recognized initially at fair value and are recorded as either assets or liabilities based on their fair value. Subsequent to initial recognition, these derivatives are measured at fair value and changes to their value are recorded through profit or loss.

(ii) Financial liabilities

15

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(c) Financial instruments (cont'd):

(iii) Share capital

(d) Inventories:

Inventories are recorded at the lower of cost and net realizable value. The cost of inventories is based on the first-in first-out principle, and includes expenditures incurred in acquiring the inventories, production or conversion costs and other costs incurred in bringing them to their existing location and condition. In the case of manufactured inventories and work in progress, cost includes materials, labor and appropriate share of production overhead based on normal operating capacity. Costs of materials are determined on an average per unit basis.

Net realizable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and selling expenses. In establishing any impairment of inventory, management estimates the likelihood that inventory carrying values will be affected by changes in market demand, technology and design, which would impair the value of inventory on hand.

(e) Property, plant and equipment:

(i) Recognition and measurement

Items of property, plant and equipment are measured at cost less accumulated depreciation and any accumulated impairment losses. The cost of self-constructed assets includes the cost of materials, costs directly attributable to bringing the assets to a working condition for their intended use, and the costs of dismantling and removing items and restoring the site on which they are located. If significant parts of an item of property, plant and equipment have different useful lives, then they are accounted for as separate items (major components) of property, plant and equipment.

Any gain or loss on disposal of an item of property, plant and equipment is recognized in profit or loss.

(ii) Subsequent expenditures

Subsequent expenditures are capitalized only if it is probable that the future economic benefits associated with the expenditures will flow to the Corporation.

(iii) Depreciation

Depreciation is calculated to write-off the cost of items of property, plant and equipment less their estimated residual values using the straight-line method over their estimated useful lives, and is recognized in profit or loss.

16

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(e) Property, plant and equipment (cont'd):

(iii) Depreciation (cont'd)

The estimated useful lives of property, plant and equipment for current and comparative periods are as follows:

| Computer equipment | |||||

| Furniture and fixtures | |||||

| Leasehold improvements | The shorter of initial term of the respective lease and | ||||

| estimated useful life | |||||

| Production and test equipment | |||||

Leased assets are depreciated over the shorter of the lease term or their useful lives unless it is reasonably certain that the Corporation will obtain ownership by the end of the lease term.

| Right-of-use asset - Property | |||||

| Right-of-use asset - Office equipment | |||||

| Right-of-use asset - Vehicles | |||||

Depreciation methods, useful lives and residual values are reviewed at each reporting date and adjusted if appropriate.

(f) Leases:

IFRS 16 Leases introduced a single, on-balance sheet accounting model for lessees. As a result, the Corporation, as a lessee, has recognized right-of-use assets representing its rights to use the underlying assets, and lease liabilities representing its obligation to make lease payments. Lessor accounting remains similar to previous accounting policies.

At inception of a contract, the Corporation assesses whether a contract is, or contains, a lease. A contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration. To assess whether a contract conveys the right to control the use of an identified asset, the Corporation assesses whether:

•the contract involves the use of an identified asset - this may be specified explicitly or implicitly, and should be physically distinct or represent substantially all of the capacity of a physically distinct asset. If the supplier has a substantive substitution right, then the asset is not identified;

•the Corporation has the right to obtain substantially all of the economic benefits from use of the asset throughout the period of use; and

•the Corporation has the right to direct the use of the asset. The Corporation has this right when it has the decision-making rights that are most relevant to changing how and for what purpose the asset is used. In rare cases where all the decisions about how and for what purpose the asset is used are predetermined, the Corporation has the right to direct the use of the asset if either:

◦the Corporation has the right to operate the asset; or

◦the Corporation designed the asset in a way that predetermines how and for what purpose it will be used.

17

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(f) Leases (cont'd):

i. As a Lessee

The Corporation recognizes a right-of-use asset and a lease liability at the lease commencement date. The right-of-use asset is initially measured at cost, which comprises the initial amount of the lease liability adjusted for any lease payments made at or before the commencement date, plus any initial direct costs incurred and an estimate of costs to dismantle and remove the underlying asset or to restore the underlying asset or the site on which it is located, less any lease incentives received.

The right-of-use asset is subsequently depreciated using the straight-line method from the commencement date to the earlier of the end of the useful life of the right-of-use asset or the end of the lease term. The estimated useful lives of right-of-use assets are determined on the same basis as those of property and equipment. In addition, the right-of-use asset is periodically reduced by impairment losses, if any, and adjusted for certain remeasurements of the lease liability.

The lease liability is initially measured at the present value of the lease payments that are not paid at the commencement date, discounted using the interest rate implicit in the lease or, if that rate cannot be readily determined, the Corporation’s incremental borrowing rate. Generally, the Corporation uses its incremental borrowing rate as the discount rate.

Lease payments included in the measurement of the lease liability comprise:

•Fixed payments, including in-substance fixed payments;

•Variable lease payments that depend on an index or a rate, initially measured using the index or rate at the commencement date;

•Amounts expected to be payable under a residual value guarantee; and

•The exercise price under a purchase option that the Corporation is reasonably certain to exercise, lease payments in an optional renewal period if the Corporation is reasonably certain to exercise an extension option, and penalties for early termination of a lease unless the Corporation is reasonably certain not to terminate early.

The lease liability is subsequently measured at amortized cost using the effective interest method. It is remeasured when there is a change in future lease payments arising from a change in an index or rate, if there is a change in the Corporation’s estimate of the amount expected to be payable under a residual value guarantee or if the Corporation changes its assessment of whether it will exercise a purchase, extension or termination option. When the lease liability is remeasured in this way, a corresponding adjustment is made to the carrying amount of the right-of-use asset, or is recorded in profit or loss if the carrying amount of the right-of-use asset has been reduced to zero.

The Corporation presents right-of-use assets in ‘Property, plant and equipment’ and lease liabilities in ‘Lease liability’ in the statement of financial position.

The Corporation has elected not to recognize right-of-use assets and lease liabilities for short-term leases of properties, equipment and vehicles that have a lease term of 12 months or less. The Corporation has elected not to recognize right-of-use assets and lease liabilities for low value leases that have initial values of less than $5,000. The Corporation recognizes the lease payments associated with these leases as an operating expense on a straight-line basis over the lease term.

18

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(f) Leases (cont'd):

ii. As a Lessor

When the Corporation is an intermediate lessor, it accounts for its interests in the head lease and the sub-lease separately. It assesses the lease classification of a sub-lease with reference to the right-of-use asset arising from the head lease, not with reference to the underlying asset, and makes an overall assessment of whether the lease transfers to the lessee substantially all of the risks and rewards of ownership incidental to ownership of the underlying asset. If this is the case, then the lease is a finance lease; if not, then it is an operating lease. As part of this assessment, the Corporation considers certain indicators such as whether the lease is for the major part of the economic life of the asset.

(g) Goodwill and intangible assets:

(i) Recognition and measurement

| Goodwill | Goodwill arising on the acquisition of subsidiaries is measured at cost less accumulated impairment losses. | ||||

| Research and development | Expenditure on research activities is recognized in profit or loss as incurred. | ||||

| Development expenditure is capitalized only if the expenditure can be measured reliably, the product or process is technically and commercially feasible, future economic benefits are probable and the Corporation intends to and has sufficient resources to complete development and to use or sell the asset. Otherwise, it is recognized in profit or loss as incurred. Subsequent to initial recognition, development expenditure is measured at cost less accumulated amortization and any accumulated impairment losses. | |||||

| Intangible assets | Intangible assets, including patents, know-how, in-process research and development, trademarks and service marks, customer contracts and relationships, non-compete agreements, and software systems that are acquired or developed by the Corporation and have finite useful lives are measured at cost less accumulated amortization and any accumulated impairment losses. | ||||

(ii) Subsequent expenditure

Subsequent expenditure is capitalized only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditures, including expenditures on internally generated goodwill, are recognized in profit or loss as incurred.

(iii) Amortization

Amortization is calculated to write-off the cost of intangible assets less their estimated residual values using the straight-line method over their estimated useful lives, and is recognized in profit or loss. Goodwill is not amortized.

The estimated useful lives for current and comparative periods are as follows:

| Acquired patents, know-how and in-process research & development | |||||

| ERP management reporting software system | |||||

| Acquired customer contracts and relationships | |||||

| Acquired non-compete agreements | |||||

| Domain names | |||||

| Acquired trademarks and service marks | |||||

| Internally generated fuel cell intangible assets | |||||

Amortization methods, useful lives and residual values are reviewed at each reporting date and adjusted if appropriate.

19

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

(h) Impairment:

(i) Financial assets

An ‘expected credit loss’ ("ECL") model applies to financial assets measured at amortized cost and debt investments at FVOCI, but not to investments in equity instruments. The Corporation's financial assets measured at amortized cost and subject to the ECL model consist primarily of trade receivables and contract assets.

In applying the ECL model, loss allowances are measured on either of the following bases:

•12-month ECLs: these are ECLs that result from possible default events within the 12 months after the reporting date; and

•lifetime ECLs: these are ECLs that result from all possible default events over the expected life of a financial instrument.

The Corporation measures loss allowances for trade receivables and contract assets at an amount equal to lifetime ECLs.

When determining whether the credit risk of a financial asset has increased significantly since initial recognition and when estimating ECLs, the Corporation considers reasonable and supportable information that is relevant and available without undue cost or effort. This includes both quantitative and qualitative information and analysis, based on historical experience and informed credit assessment and including forward-looking information.

ECLs are a probability-weighted estimate of credit losses. Credit losses are measured as the present value of all cash shortfalls (i.e. the difference between the cash flows due to the entity in accordance with the contract and the cash flows that the Corporation expects to receive). ECLs are discounted at the effective interest rate of the financial asset. At each reporting date, we assess whether financial assets carried at amortized cost are credit-impaired. A financial asset is ‘credit-impaired’ when one or more events that have a detrimental impact on the estimated future cash flows of the financial asset have occurred. Loss allowances for financial assets measured at amortized cost are deducted from the gross carrying amount of the assets. Impairment (losses) recoveries related to trade receivables and contract assets are presented separately in the statement of profit or loss.

(ii) Non-financial assets

The carrying amounts of the Corporation’s non-financial assets other than inventories are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. For goodwill and intangible assets that have indefinite useful lives, the recoverable amount is estimated annually.

The recoverable amount of an asset or cash-generating unit is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. Fair value less costs to sell is defined as the estimated price that would be received on the sale of the asset in an orderly transaction between market participants at the measurement date. For the purposes of impairment testing, assets that cannot be tested individually are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other groups of assets.

The allocation of goodwill to cash-generating units reflects the lowest level at which goodwill is monitored for internal reporting purposes.

20

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(h) Impairment (cont'd):

(ii) Non-financial assets (cont'd)

An impairment loss is recognized if the carrying amount of an asset or its cash-generating unit exceeds its estimated recoverable amount. Impairment losses are recognized in profit or loss. Impairment losses recognized in respect of the cash generating units are allocated first to reduce the carrying amount of any goodwill allocated to the units, and then to reduce the carrying amounts of the other assets in the unit on a pro-rata basis.

An impairment loss in respect of goodwill is not reversed. In respect of other assets, impairment losses recognized in prior periods are assessed at each reporting date for any indications that the loss has decreased or no longer exists. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortization, if no impairment loss had been recognized.

(i) Provisions:

A provision is recognized if, as a result of a past event, the Corporation has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and the risk specific to the liability. The unwinding of the discount is recognized as a finance expense.

Warranty provision

A provision for warranty costs is recorded on product sales at the time the sale is recognized. In establishing the warranty provision, management estimates the likelihood that products sold will experience warranty claims and the estimated cost to resolve claims received, taking into account the nature of the contract and past and projected experience with the products.

Decommissioning liabilities

Legal obligations to retire tangible long-lived assets are recorded at the net present value of the expected costs of settlement at acquisition with a corresponding increase in asset value. These include assets leased under operating leases. The liability is accreted over the life of the asset to the ultimate settlement amount and the increase in asset value is depreciated over the remaining useful life of the asset.

(j) Revenue recognition:

The Corporation generates revenues primarily from product sales, the license and sale of intellectual property and fundamental knowledge, and the provision of engineering services and technology transfer services. Product revenues are derived primarily from standard product sales contracts and from long-term fixed price contracts. Intellectual property and fundamental knowledge license revenues are derived primarily from standard licensing and technology transfer agreements. Engineering service and technology transfer services revenues are derived primarily from cost-plus reimbursable contracts and from long-term fixed price contracts.

Revenue is recognized when a customer obtains control of the goods or services. Determining the timing of the transfer of control, at a point in time or over time, requires judgment. On standard product sales contracts, revenues are recognized when customers obtain control of the product, that is when transfer of title and risks and rewards of ownership of goods have passed and when obligation to pay is considered certain. Invoices are generated and revenue is recognized at that point in time. Provisions for warranties are made at the time of sale.

21

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(j) Revenue recognition (cont'd):

On standard licensing and technology transfer agreements, revenues are recognized on the transfer of rights to a licensee, when it is determined to be distinct from other performance obligations, and if the customer can direct the use of, and obtain substantially all of the remaining benefits from the license as it exists at the time of transfer. In other cases, the proceeds are considered to relate to the right to use the asset over the license period and the revenue is recognized over that period. If it is determined that the license is not distinct from other performance obligations, revenue is recognized over time as the customer simultaneously receives and consumes the benefit.

On cost-plus reimbursable contracts, revenues are recognized as costs are incurred, and include applicable fees earned as services are provided.

On long-term fixed price contracts, the customer controls all of the work in progress as the services are being provided. This is because under these contracts, the deliverables are made to a customer’s specification, and if a contract is terminated by the customer, then the Corporation is entitled to reimbursement of the costs incurred to date plus the applicable gross margin. Therefore, revenue from these contracts and the associated costs are recognized as the costs are incurred over time.

On long-term fixed price contracts, revenues are recognized over time using cumulative costs incurred to date relative to total estimated costs at completion to measure progress towards satisfying performance obligations. Generally, revenue is recognized by multiplying the expected consideration by the ratio of cumulative costs incurred to date to the sum of incurred and estimated costs for completing the performance obligation. The cumulative effect of changes to estimated revenues and estimated costs for completing a contract are recognized in the period in which the revisions are identified. In the event that the estimated costs for completing the contract exceed the expected revenues on a contract, such loss is recognized in its entirety in the period it becomes known.

Deferred revenue (i.e. contract liabilities) represents cash received from customers in excess of revenue recognized on uncompleted contracts.

(k) Finance income and expense:

Finance income comprises interest income on funds invested, gains (losses) on the disposal of available-for-sale financial assets, foreign exchange gains (losses), and changes in the fair value of financial assets at fair value through profit or loss, pension administration expense, and employee future benefit plan expense. Interest income is recognized as it accrues in income, using the effective interest method.

Finance expense comprises interest expense on leases and the unwinding of the discount on provisions.

(l) Income taxes:

The Corporation follows the asset and liability method of accounting for income taxes. Under this method, deferred income taxes are recognized for the deferred income tax consequences attributable to differences between the financial statement carrying values of assets and liabilities and their respective income tax bases (temporary differences) and for loss carry forwards. The resulting changes in the net deferred tax asset or liability are included in income.

Deferred tax assets and liabilities are measured using enacted, or substantively enacted, tax rates expected to apply to taxable income in the years in which temporary differences are expected to be recovered or settled. The effect on deferred income tax assets and liabilities, of a change in tax rates, is included in income in the period that includes the substantive enactment date. Deferred income tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realized.

22

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(m) Employee benefits:

Defined contribution plans

A defined contribution plan is a post-employment benefit plan under which an entity pays fixed contributions into a separate entity and will have no legal or constructive obligation to pay further amounts.

Obligations for contributions to defined contribution pension plans are recognized as an employee benefit expense in profit or loss in the periods during which services are rendered by employees. Prepaid contributions are recognized as an asset to the extent that a cash refund or a reduction in future payments is available. Contributions to a defined contribution plan that are due more than 12 months after the end of the period in which the employees render the service are discounted to their present value.

Defined benefit plans

A defined benefit plan is a post-employment pension plan other than a defined contribution plan. The Corporation’s net obligation in respect of defined benefit pension plans is calculated separately for each plan by estimating the amount of future benefit that employees have earned in return for their service in the current and prior periods; that benefit is discounted to determine its present value. Any unrecognized past service costs and the fair value of any plan assets are deducted. The discount rate is the yield at the reporting date on AA credit-rated bonds that have maturity dates approximating the terms of the Corporation’s obligations and that are denominated in the same currency in which the benefits are expected to be paid. The calculation is performed annually by a qualified actuary using the projected unit credit method.

When the calculation results in a benefit to the Corporation, the recognized asset is limited to the total of any unrecognized past service costs and the present value of economic benefits available in the form of any future refunds from the plan or reductions in future contributions to the plan. In order to calculate the present value of economic benefits, consideration is given to any minimum funding requirements that apply to any plan in the Corporation. An economic benefit is available to the Corporation if it is realizable during the life of the plan, or on settlement of the plan liabilities.

The Corporation recognizes all remeasurements arising from defined benefit plans, which comprise actuarial gains and losses, immediately in other comprehensive income. Remeasurements recognized in other comprehensive income are not recycled through profit or loss in subsequent periods.

Other long-term employee benefits

The Corporation’s net obligation in respect of long-term employee benefits other than pension plans is the amount of future benefit that employees have earned in return for their service in the current and prior periods; that benefit is discounted to determine its present value, and the fair value of any related assets is deducted. The discount rate is the yield at the reporting date on AA credit-rated bonds that have maturity dates approximating the terms of the Corporation’s obligations. The calculation is performed using the projected unit credit method. Any actuarial gains and losses are recognized in other comprehensive income or loss in the period in which they arise.

Termination benefits

Termination benefits are recognized as an expense (restructuring expense recorded in other operating expense) when the Corporation is committed demonstrably, without realistic possibility of withdrawal, to a formal detailed plan to either terminate employment before the normal retirement date, or to provide termination benefits as a result of an offer made to encourage voluntary redundancy. Termination benefits for voluntary redundancies are recognized as an expense if the Corporation has made an offer of voluntary redundancy, it is probable that the offer will be accepted, and the number of acceptances can be estimated reliably. If benefits are payable more than 12 months after the reporting period, then they are discounted to their present value.

23

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(m) Employee benefits (cont'd):

Short-term employee benefits

Short-term employee benefit obligations are measured on an undiscounted basis and are expensed as the related service is provided.

A liability is recognized for the amount expected to be paid under short-term cash bonus or profit sharing plans if the Corporation has a present legal or constructive obligation to pay this amount as a result of past service provided by the employee, and the obligation can be estimated reliably.

(n) Share-based compensation plans:

The Corporation uses the fair-value based method of accounting for share-based compensation for all awards of shares, share options, restricted share units, and deferred share units granted. The resulting compensation expense, based on the fair value of the awards granted, excluding the impact of any non-market service and performance vesting conditions, is charged to income over the period that the employees unconditionally become entitled to the award, with a corresponding increase to contributed surplus.

Fair values of share options are calculated using the Black-Scholes valuation method as of the grant date and adjusted for estimated forfeitures. Restricted share units and deferred share units are valued at the fair-value price at grant date. For awards with graded vesting, the fair value of each tranche is calculated separately and recognized over its respective vesting period. Non-market vesting conditions are considered in making assumptions about the number of awards that are expected to vest. At each reporting date, the Corporation reassesses its estimates of the number of awards that are expected to vest and recognizes the impact of any revision in the income statement with a corresponding adjustment to contributed surplus.

The Corporation issues shares, share options, restricted share units, and deferred share units under its share-based compensation plans as described in note 21. Any consideration paid by employees on exercise of share options or purchase of shares, together with the amount initially recorded in contributed surplus, is credited to share capital. The redemption of restricted share units and deferred share units are non-cash transactions that are recorded in contributed surplus and share capital.

(o) Earnings (loss) per share:

Basic earnings (loss) per share is computed using the weighted average number of common shares outstanding during the period, adjusted for treasury shares. Diluted earnings per share is calculated using the treasury stock method.

Under the treasury stock method, the dilution is calculated based upon the number of common shares issued should deferred share units (“DSUs”), restricted share units (“RSUs”), and “in the money” options, if any, be exercised. When the effects of outstanding stock-based compensation arrangements would be anti-dilutive, diluted loss per share is not shown separately.

(p) Government assistance and investment tax credits:

24

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

4. Significant accounting policies (cont'd):

(q) Segment reporting:

5.Critical judgments in applying accounting policies and key sources of estimation uncertainty:

Critical judgments in applying accounting policies:

Critical judgments that management has made in the process of applying the Corporation’s accounting policies and that have the most significant effect on the amounts recognized in the consolidated financial statements are limited to management’s assessment of the Corporation’s ability to continue as a going concern (note 2(e)).

Key sources of estimation uncertainty:

The following are key assumptions concerning the future and other key sources of estimation uncertainty that have significant risk of resulting in a material adjustment to the reported amount of assets, liabilities, income and expenses within the next financial year.

(a)Revenue recognition:

On long-term fixed price contracts, revenues are recorded over time using costs incurred to date relative to total estimated costs at completion to measure progress towards satisfying performance obligations. Revenue is recognized by multiplying the expected consideration by the ratio of cumulative costs incurred to date to the sum of incurred and estimated costs for completing the performance obligation. The cumulative effect of changes to expected revenues and expected costs for completing a contract are recognized in the period in which the revisions are identified. If the expected costs exceed the expected revenues on a contract, such loss is recognized in its entirety in the period it becomes known.

(i) The determination of expected costs for completing a contract is based on estimates that can be affected by a variety of factors such as variances in the timeline to completion, the cost of materials, the availability and cost of labour, as well as productivity.

(ii) The determination of potential revenues includes the contractually agreed amount and may be adjusted based on the estimate of the Corporation’s attainment on achieving certain defined contractual milestones. Management’s estimation is required in determining the amount of consideration to which the Corporation expects to be entitled and in determining when a performance obligation has been met.

Estimates used to determine revenues and costs of long-term fixed price contracts involve uncertainties that ultimately depend on the outcome of future events and are periodically revised as projects progress. There is a risk that a customer may ultimately disagree with management’s assessment of the progress achieved against milestones, or that the Corporation's estimates of the work required to complete a contract may change.

25

BALLARD POWER SYSTEMS INC. Notes to Consolidated Financial Statements Years ended December 31, 2022, and 2021 (Tabular amounts expressed in thousands of U.S. dollars, except per share amounts and numbers of shares) | ||

5.Critical judgments in applying accounting policies and key sources of estimation uncertainty (cont'd):

Key sources of estimation uncertainty (cont'd):

(b) Asset impairment: