UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the fiscal year ended

Commission

File No.

(Exact Name of Registrant as Specified in Its Charter)

(State or Other Jurisdiction Of Incorporation or Organization) | (I.R.S.

Employer |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s

telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.0001 par value per share

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the issuer was required to file such reports), and (2) has

been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| ☒ | Smaller reporting company | |||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in 12b-2 of the Exchange Act.) Yes ☐ No

The

aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which

the common stock was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter was

$

Indicate

the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

Auditor Firm ID: | Auditor Name: | Auditor Location: | ||

TABLE OF CONTENTS

i

CAUTIONARY

NOTE TO INVESTORS REGARDING ESTIMATES OF MEASURED,

INDICATED AND INFERRED RESOURCES AND PROVEN AND PROBABLE MINERAL RESERVES

We are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) and applicable Canadian securities laws, and as a result we report our mineral reserves and mineral resources according to two different standards. U.S. reporting requirements are governed by subpart 1300 of Regulation S-K under the Exchange Act (“S-K 1300”). Canadian reporting requirements for disclosure of mineral properties are governed by NI 43-101. Both sets of reporting standards have similar goals in terms of conveying an appropriate level of confidence in the disclosures being reported, but the standards embody slightly different approaches and definitions.

In our public filings in the U.S. and Canada and in certain other announcements not filed with the SEC, we disclose proven and probable reserves and measured, indicated and inferred resources, each as defined in S-K 1300 and NI 43-101. As currently reported, there are no material differences in our disclosed measured, indicated and inferred resource under each of S-K 1300 and NI 43-101. The estimation of measured resources and indicated resources involve greater uncertainty as to their existence and economic feasibility than the estimation of proven and probable reserves, and therefore investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into S-K 1300-compliant or NI 43-101-compliant reserves. The estimation of inferred resources involves far greater uncertainty as to their existence and economic viability than the estimation of other categories of resources, and therefore it cannot be assumed that all or any part of inferred resources will ever be upgraded to a higher category. Therefore, investors are cautioned not to assume that all or any part of inferred resources exist, or that they can be mined legally or economically.

ii

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the exhibits attached hereto contain “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995, as amended, and “forward-looking information” within the meaning of applicable Canadian securities legislation, collectively “forward-looking statements”. Such forward-looking statements concern our anticipated results and developments in the operations of the Company in future periods, planned exploration activities, the adequacy of the Company’s financial resources and other events or conditions that may occur in the future. Forward-looking statements are frequently, but not always, identified by words such as “expects,” “anticipates,” “believes,” “intends,” “estimates,” “potential,” “possible” and similar expressions, or statements that events, conditions or results “will,” “may,” “could” or “should” (or the negative and grammatical variations of any of these terms) occur or be achieved. These forward looking statements may include, but are not limited to, statements concerning:

| ● | the Company’s strategies and objectives, both generally and in respect of the Bullfrog Gold Project and Reward Gold Project; |

| ● | the recommendations of the Technical Reports for the Bullfrog Gold Project and Reward Gold Project; |

| ● | the Company’s decisions regarding the timing and costs of exploration programs with respect to, and the issuance of the necessary permits and authorizations required for, the Company’s exploration programs at the Bullfrog Gold Project and Reward Gold Project; |

| ● | the Company’s estimates of the quality and quantity of the mineralized materials at its mineral properties; |

| ● | the potential discovery and delineation of mineral deposits/reserves and any expansion thereof beyond the current estimate; |

| ● | the Company’s expectation that it will become a gold producer; |

| ● | the Company’s estimates of future operating and financial performance; |

| ● | the Company’s potential funding requirements and sources of capital, including near-term sources of additional cash and long-term financing through the sale of equity and/or debt financings and through the exercise of stock options and warrants; |

| ● | the Company’s expectation that the Company will continue to raise capital; |

| ● | the Company’s expectation that the Company will continue to incur losses and will not pay dividends for the foreseeable future; |

| ● | the Company’s estimates of its future cash position; |

| ● | the Company’s anticipated general business and economic conditions; |

| ● | the Company’s ability to meet its financial obligations as they come due, and to be able to raise the necessary funds to continue operations; and |

| ● | that the Company will operate at a loss for the foreseeable future. |

Such forward-looking statements reflect the Company’s current views with respect to future events and are subject to certain known and unknown risks, uncertainties and assumptions. Many factors could cause actual results, performance or achievements to be materially different from any future results, performance or achievements that may be expressed or implied by such forward-looking statements, including, among others, risks related to:

| ● | our history of losses; |

| ● | negative cash flow; |

| ● | our limited operating history; |

| ● | increased costs affecting our financial condition; |

| ● | the Bullfrog Gold Project and Reward Gold Project being in the exploration stage; |

| ● | whether the Bullfrog Gold Project and Reward Gold Project are feasible; |

| ● | the Bullfrog Gold Project and Reward Gold Project requiring substantial capital investment; |

| ● | our inability to obtain required permits; |

| ● | our status as a junior mining company; |

| ● | difficulties in managing growth; |

| ● | our potential loss of key persons; |

| ● | risks related to the evolving novel coronavirus (“COVID-19”) pandemic and health crisis and the governmental and regulatory actions taken in response thereto; |

| ● | the risks of mineral exploration; |

iii

| ● | evaluation uncertainty in estimating mineralized material; |

| ● | changes in estimates of mineralized material; |

| ● | our exploration projects not succeeding; |

| ● | price volatility of gold and silver; |

| ● | environmental regulations; |

| ● | challenges to title to our properties; |

| ● | amendments to mining law; |

| ● | supply shortages; |

| ● | inability to maintain infrastructure to conduct exploration activities; |

| ● | new regulation related to climate change; |

| ● | relationships with communities in which we operate; |

| ● | newly adopted mining disclosure regulations; |

| ● | evolving corporate standards; |

| ● | Canadian reporting requirements; and |

| ● | The price of the shares of common stock being volatile. |

Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described herein. This list of factors that may affect any of the Company’s forward-looking statements is not exhaustive. Forward-looking statements are statements about the future and are inherently uncertain, and actual achievements of the Company or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including without limitation those discussed in “Part I, Item 1A, Risk Factors”, of this Annual Report on Form 10-K as well as other factors described elsewhere in this report and the Company’s other reports filed with the SEC.

The Company’s forward-looking statements contained in this Annual Report on Form 10-K are based on the beliefs, expectations and opinions of management as of the date of this Annual Report. The Company does not assume any obligation to update forward-looking statements if circumstances or management’s beliefs, expectations or opinions should change, except as required by law. For the reasons set forth above, investors should not attribute undue certainty to or place undue reliance on forward-looking statements.

iv

GLOSSARY OF SELECTED MINING TERMS

| Ag | Silver |

| Au | Gold |

| Breccia | Broken sedimentary and volcanic rock fragments cemented by a fine-grained matrix |

| Clastic Rock | Fragments, or clasts, of pre-existing minerals |

| Cutoff Grade | The grade (i.e., the concentration of metal or mineral in rock) that determines the destination of the material during mining. For purposes of establishing “prospects of economic extraction,” the cut-off grade is the grade that distinguishes material deemed to have no economic value (it will not be mined in underground mining or if mined in surface mining, its destination will be the waste dump) from material deemed to have economic value (its ultimate destination during mining will be a processing facility). Other terms used in similar fashion as cut-off grade include net smelter return, pay limit, and break-even stripping ratio. |

| Deposit | A mineralized body which has been physically delineated by sufficient drilling, trenching, and/or underground work, and found to contain a sufficient average grade of metal or metals to warrant further exploration and/or development expenditures. Such a deposit does not qualify as a commercially mineable ore body or as containing reserves or ore, unless final legal, technical and economic factors are resolved |

| Detachment Fault | A regionally extensive, gently dipping normal fault that is commonly associated with extension in large blocks of the earth’s crust |

| g/t | Grams per metric tonne |

| Metamorphic Rock | Rock that has transformed to another rock form after intense heat and pressure |

| Miocene | A geologic era that extended from 5 million to 23 million years ago |

| Mineralization | The concentration of metals and their chemical compounds within a body of rock |

| Net Smelter Royalty | A percentage payable to an owner or lessee from the production or net proceeds received by the operator from a smelter or refinery, less transportation, insurance, smelting and refining costs and penalties as set out in a royalty agreement. |

| Paleozoic | A geologic era extending from 230 million to 540 million years ago |

| Photogrammetry | The science of making measurements from photographs; the output is typically a map or a drawing |

| Proterozoic | A geologic era extending from 540 million years to 2,500 million years ago. |

| Reverse Circulation (RC) | A drilling method whereby drill cuttings are returned to the surface through the annulus between inner and outer drill rods, thereby minimizing contamination from wall rock. |

| Rhyolite | An igneous, volcanic extrusive rock containing more than 65% silica. |

| Schist | A group metamorphic rocks that contain more than 50% platy and elongated minerals such as mica. |

| Siliciclastic Rock | Non-carbonate sedimentary rocks that are almost exclusively silicas-bearing, either as quartz or silicate minerals. |

| Tertiary | A geologic era from 2.6 million to 65 million years ago. |

v

S-K 1300 Definitions

| Exploration Stage Issuer | An “exploration stage issuer” is an issuer that has no material property with mineral reserves disclosed. |

| Exploration Stage Property | An “exploration stage property” is a property that has no mineral reserves disclosed. |

| Development Stage Issuer | A “development stage issuer” is an issuer that is engaged in the preparation of mineral reserves for extraction on at least one material property. |

| Development Stage Property | A “development stage property” is a property that has mineral reserves disclosed, pursuant to this subpart, but no material extraction. |

| Indicated Mineral Resource | An “indicated mineral resource” is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of adequate geological evidence and sampling. The level of geological certainty associated with an indicated mineral resource is sufficient to allow a qualified person to apply modifying factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Because an indicated mineral resource has a lower level of confidence than the level of confidence of a measured mineral resource, an indicated mineral resource may only be converted to a probable mineral reserve |

| Inferred Mineral Resource | An “inferred mineral resource” is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. The level of geological uncertainty associated with an inferred mineral resource is too high to apply relevant technical and economic factors likely to influence the prospects of economic extraction in a manner useful for evaluation of economic viability. Because an inferred mineral resource has the lowest level of geological confidence of all mineral resources, which prevents the application of the modifying factors in a manner useful for evaluation of economic viability, an inferred mineral resource may not be considered when assessing the economic viability of a mining project, and may not be converted to a mineral reserve. |

| Measured Mineral Resource | A “measured mineral resource” is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of conclusive geological evidence and sampling. The level of geological certainty associated with a measured mineral resource is sufficient to allow a qualified person to apply modifying factors, as defined in this section, in sufficient detail to support detailed mine planning and final evaluation of the economic viability of the deposit. Because a measured mineral resource has a higher level of confidence than the level of confidence of either an indicated mineral resource or an inferred mineral resource, a measured mineral resource may be converted to a proven mineral reserve or to a probable mineral reserve. |

| Mineral Reserve | A “mineral reserve” is an estimate of tonnage and grade or quality of indicated and measured mineral resources that, in the opinion of the qualified person, can be the basis of an economically viable project. More specifically, it is the economically mineable part of a measured or indicated mineral resource, which includes diluting materials and allowances for losses that may occur when the material is mined or extracted |

vi

| Mineral Resource | A “mineral resource” is a concentration or occurrence of material of economic interest in or on the Earth’s crust in such form, grade or quality, and quantity that there are reasonable prospects for economic extraction. A mineral resource is a reasonable estimate of mineralization, taking into account relevant factors such as cut-off grade, likely mining dimensions, location or continuity, that, with the assumed and justifiable technical and economic conditions, is likely to, in whole or in part, become economically extractable. It is not merely an inventory of all mineralization drilled or sampled. |

| Modifying Factors | Modifying factors are the factors that a qualified person must apply to indicated and measured mineral resources and then evaluate in order to establish the economic viability of mineral reserves. A qualified person must apply and evaluate modifying factors to convert measured and indicated mineral resources to proven and probable mineral reserves. These factors include, but are not restricted to: Mining; processing; metallurgical; infrastructure; economic; marketing; legal; environmental compliance; plans, negotiations, or agreements with local individuals or groups; and governmental factors. The number, type and specific characteristics of the modifying factors applied will necessarily be a function of and depend upon the mineral, mine, property, or project. |

| Probable Reserve | A “probable mineral reserve” is the economically mineable part of an indicated and, in some cases, a measured mineral resource. |

| Production Stage Issuer | A “production stage issuer” is an issuer that is engaged in material extraction of mineral reserves on at least one material property. |

| Production Stage Property | A “production stage property” is a property with material extraction of mineral reserves. |

| Proven Reserve | A “proven mineral reserve” is the economically mineable part of a measured mineral resource and can only result from conversion of a measured mineral resource. |

USE OF NAMES

In this Annual Report on Form 10-K, unless the context otherwise requires, the terms “we”, “us”, “our”, “Augusta Gold”, “Augusta Gold Corp.” or the “Company” refer to Augusta Gold Corp., a Delaware corporation, and its subsidiaries.

CURRENCY

References to CDN or C$ refer to Canadian currency and USD or $ to United States currency.

METRIC CONVERSION TABLE

| To Convert Metric Measurement Units | To Imperial Measurement Units | Multiply by | ||

| Hectares | Acres | 2.4710 | ||

| Meters | Feet | 3.2808 | ||

| Kilometers | Miles | 0.6214 | ||

| Tonnes | Tons (short) | 1.1023 | ||

| Liters | Gallons | 0.2642 | ||

| Grams | Ounces (troy) | 0.0322 | ||

| Grams per tonne | Ounces (troy) per ton (short) | 0.0292 |

vii

PART I

ITEM 1. BUSINESS

General Corporate Overview

Augusta Gold Corp. (“Augusta Gold” or the “Company”) is a gold company that is an exploration stage issuer focused on building a long-term business that delivers stakeholder value through developing the Company’s Bullfrog and Reward gold projects and pursing accretive merger and acquisition opportunities. We are focused on exploration and advancement of gold exploration and potential development projects, which may lead to gold production or strategic transactions such as joint venture arrangements with other mining companies or sales of assets for cash and/or other consideration. At present all our properties are exploration stage properties and we do not mine, produce or sell any mineral products and we do not currently generate cash flows from mining operations.

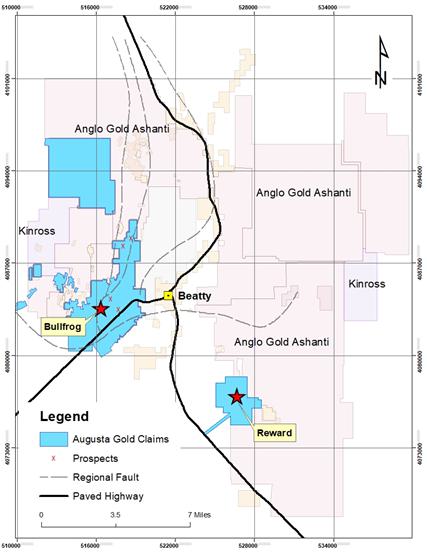

The Bullfrog Gold Project is located approximately 120 miles north-west of Las Vegas, Nevada and 4 miles west of Beatty, Nevada. The Reward Gold Project is located seven miles from the Bullfrog Gold Project. The Company owns, controls or has acquired mineral rights on federal patented and unpatented mining claims in the State of Nevada for the purpose of exploration and potential development of gold, silver, and other metals. The Company plans to review opportunities and acquire additional mineral properties with current or historic precious and base metal mineralization with meaningful exploration potential. See “Part I - Item 2 - Properties” in this Annual Report on Form 10-K for a further description of the Bullfrog and Reward gold projects.

The Company is led by a management team and board of directors with a proven track record of success in financing, exploring and developing mining assets and delivering shareholder value.

Augusta Gold Corp. was incorporated under the laws of the State of Delaware on July 23, 2007 as Kopr Resources Corp. On July 21, 2011, the Company changed its name to “Bullfrog Gold Corp.” On January 26, 2021, the Company changed its name to “Augusta Gold Corp.” and completed a consolidation of its shares of common stock on the basis of one (1) new share of common stock for every six (6) old shares of common stock (the “Consolidation”).

Recent Development of the Business

On October 9, 2020, the Company entered into a membership interest purchase agreement (the “MIPA”) among the Company, Homestake Mining Company of California (“Homestake”), and Lac Minerals (USA) LLC (“Lac Minerals” and together with Homestake, the “Barrick Parties”).

Pursuant to the MIPA, the Company agreed to purchase from the Barrick Parties, and the Barrick Parties agreed to sell to the Company, all of the equity interests (the “Equity Interests”) in Bullfrog Mines LLC (“Bullfrog Mines”), the successor by conversion of Barrick Bullfrog Inc. (the “Acquisition Transaction”).

The Acquisition Transaction closed on October 26, 2020. Through the Company’s acquisition of the Equity Interests, the Company acquired rights to 1,500 acres of land adjoining the Company’s Bullfrog Gold deposit. Additional details on the Acquisition Transaction are set out in this Annual Report under “Part I - Item 2 - Properties” – “Bullfrog Gold Project, Nye County, Nevada” - “Location, Property Description and Ownership” - “Barrick Claims”.

Following closing of the Acquisition Transaction, the Company’s board and management was reconstituted to include Maryse Bélanger as President, CEO and director, and Messrs. Donald Taylor and Daniel Earle as directors of the Company joining Mr. David Beling as the sole pre-existing Company director.

On January 7, 2021, the Company announced the appointment of Mr. Richard Warke, Ms. Poonam Puri and Mr. John Boehner as directors of the Company, the resignation of Mr. David Beling as a director of the Company, and the appointments of new members of management. On January 20, 2021, the Company announced the appointment of Mr. Len Boggio as a director of the Company.

1

On April 13, 2021, the Company announced the appointment of Mr. Donald Taylor as President and Chief Executive Officer of the Company and the resignation of Maryse Belanger as President, Chief Executive Officer and a director.

On June 13, 2022, the Company completed the acquisition of the outstanding membership interests (collectively, the “CR Interests”) of CR Reward LLC, a wholly-owned subsidiary of Waterton (“CR Reward”), pursuant to a membership interest purchase agreement (the “Reward Agreement”) with Waterton Nevada Splitter, LLC (“Waterton”). CR Reward holds the Reward Project located seven miles from the Company’s Bullfrog Project in Nevada. The CR Interests were acquired for the following consideration: (a) $12,500,000 in cash paid at the closing; plus (b) the issuance of 7,800,000 shares of Augusta Gold common stock at the closing; plus (c) $22,121,398 in cash paid on September 14, 2022.

On September 14, 2022, the Company also announced that it had entered into a loan with a company owned by the Company’s executive chairman for $22,232,561. The loan bears interest at a rate of prime plus 3%, is for a maximum period of 12 months, and is secured by the Company’s Bullfrog and Reward projects.

On January 20, 2023, the Company announced that it had closed a bought deal offering of units of Augusta Gold (the “Units”) for aggregate gross proceeds of approximately C$11.5 million, including the full exercise of the over-allotment option in the amount of C$1.5 million. Pursuant to the Offering, a total of 6,725,147 Units were sold at a price of C$1.71 per Unit. Each Unit was comprised of one share of the Company’s common stock and one-half of one common stock purchase warrant (each whole common stock purchase warrant, a “Warrant”). Each Warrant entitles the holder to acquire one share of the Company’s common stock at a price of C$2.30 until January 20, 2026.

Availability of Raw Materials

All of the raw materials we require to carry on our business are readily available through normal supply or business contracting channels in Canada and the United States. As a result, we do not believe that we will experience any shortages of required personnel, equipment or supplies in the foreseeable future.

Dependence on a Few Contracts

Our business is not substantially dependent on any contract such as a contract to sell the major part of the Company’s products or services or to purchase the major part of its requirements for goods, services or raw materials, or on any franchise or license or other agreement to use a patent, formula, trade secret, process or trade name upon which its business depends. Rather, our ability to continue making the holding, assessment, lease and option payments necessary to maintain our interest in our mineral projects is of primary concern. We do not presently anticipate any difficulties in this regard in the current financial year.

Competition

We compete with other mining companies in connection with the acquisition, exploration, financing and development of gold properties. There is competition among mining companies for a limited number of gold acquisition and exploration opportunities. We may compete with other mining companies for mining claims in regions adjacent to our existing claims. Some of these competing mining companies have substantially greater financial and technical resources than us. As a result, we may have difficulty acquiring attractive gold projects at reasonable prices.

We compete with other mining companies to retain expert consultants required to complete our geological, project development, and analytical and metallurgical studies. We also compete with other mining companies to hire mining engineers, geologists and other skilled personnel in the mining industry, and for exploration and development services. In competing for qualified mineral exploration personnel, we may be required to pay compensation or benefits relatively higher than those paid in the past, and the availability of qualified personnel may be limited in high-demand commodity cycles.

We will be subject to competition and unforeseen limited sources of supplies in the industry in the event spot shortages for certain equipment such as bulldozers and excavators and services, such as contract drilling that we will need to conduct exploration. There is also significant competition for power in Beatty, Nevada. If we are unsuccessful in securing the products, equipment, services and power we need, we may have to suspend our exploration plans until we are able to secure them.

2

Compliance with Government Regulation

The exploration and development of a mining property is subject to regulation by a number of federal and state government authorities. These include the United States Environmental Protection Agency (“EPA”) and the United States Bureau of Land Management (“BLM”) as well as the various state environmental protection agencies. The regulations address many environmental issues relating to air, soil and water contamination and apply to many mining related activities including exploration, mine construction, mineral extraction, ore milling, water use, waste disposal and use of toxic substances. In addition, we are subject to regulations relating to labor standards, occupational health and safety, mine safety, general land use, export of minerals and taxation. Many of the regulations require permits or licenses to be obtained and the filing of Notices of Intent and Plans of Operations, the absence of which or inability to obtain will adversely affect the ability for us to conduct our exploration, development and operation activities. The failure to comply with the regulations and terms of permits and licenses may result in fines or other penalties or in revocation of a permit or license or loss of a prospect.

Federal

On lands owned by the United States, mining rights are governed by the General Mining Law of 1872, as amended, which allows the location of mining claims on certain federal lands upon the discovery of a valuable mineral deposit and compliance with location requirements. The exploration of mining properties and development and operation of mines is governed by both federal and state laws. Federal laws that govern mining claim location and maintenance and mining operations on federal lands are generally administered by the BLM. Additional federal laws, governing mine safety and health, also apply. State laws also require various permits and approvals before exploration, development or production operations can begin. Among other things, a reclamation plan must typically be prepared and approved, with bonding in the amount of projected reclamation costs. The bond is used to ensure that proper reclamation takes place, and the bond will not be released until that time. Local jurisdictions may also impose permitting requirements (such as conditional use permits or zoning approvals).

Nevada

In Nevada, initial stage surface exploration activities that do not disturb the surface, do not require any permits. Notice-level exploration permits (“NOI”) are required (through the BLM) for the Bullfrog Gold Project to perform drilling or other surface disturbing activities with less than five acres extent. More extensive disturbance requires submittal and approval of a “Plan of Operations” and “Environmental Assessment” from the BLM.

In Nevada, we are also required to post bonds with the State of Nevada to secure our environmental and reclamation obligations on private land, with amount of such bonds reflecting the level of rehabilitation anticipated by the then proposed activities.

If in the future we are successful in defining a commercially viable mineral deposit on our property interests, then if and when we commence any mineral production, we will also need to comply with laws that regulate or propose to regulate our mining activities, including the management and handling of raw materials, disposal, storage and management of hazardous and solid waste, the safety of our employees and post-mining land reclamation.

We cannot predict the impact of new or changed laws, regulations or permitting requirements, or changes in the ways that such laws, regulations or permitting requirements are enforced, interpreted or administered. Health, safety and environmental laws and regulations are complex, are subject to change and have become more stringent over time. It is possible that greater than anticipated health, safety and environmental capital expenditures or reclamation and closure expenditures will be required in the future. We expect continued government and public emphasis on environmental issues will result in increased future investments for environmental controls at our operations.

Environmental Regulation

Our mineral projects are subject to various federal, state and local laws and regulations governing protection of the environment. These laws are continually changing and, in general, are becoming more restrictive. The development, operation, closure, and reclamation of mining projects in the United States requires numerous notifications, permits, authorizations, and public agency decisions. Compliance with environmental and related laws and regulations requires us to obtain permits issued by regulatory agencies, and to file various reports and keep records of our operations. Certain of these permits require periodic renewal or review of their conditions and may be subject to a public review process during which opposition to our proposed operations may be encountered. We are currently operating under various permits for activities connected to mineral exploration, reclamation, and environmental considerations. Our policy is to conduct business in a way that safeguards public health and the environment. We believe that our operations are conducted in material compliance with applicable laws and regulations.

Changes to current local, state or federal laws and regulations in the jurisdictions where we operate could require additional capital expenditures and increased operating and/or reclamation costs. Although we are unable to predict what additional legislation, if any, might be proposed or enacted, additional regulatory requirements could impact the economics of our projects.

3

U.S. Federal Laws

The Comprehensive Environmental, Response, Compensation, and Liability Act (“CERCLA”), and comparable state statutes, impose strict, joint and several liability on current and former owners and operators of sites and on persons who disposed of or arranged for the disposal of hazardous substances found at such sites. It is not uncommon for the government to file claims requiring cleanup actions, demands for reimbursement for government-incurred cleanup costs, or natural resource damages, or for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by hazardous substances released into the environment. The Federal Resource Conservation and Recovery Act (“RCRA”), and comparable state statutes, govern the disposal of solid waste and hazardous waste and authorize the imposition of substantial fines and penalties for noncompliance, as well as requirements for corrective actions. CERCLA, RCRA and comparable state statutes can impose liability for clean-up of sites and disposal of substances found on exploration, mining and processing sites long after activities on such sites have been completed.

The Clean Air Act (“CAA”), as amended, restricts the emission of air pollutants from many sources, including exploration, development, mining and processing activities. The Company’s current exploration activities and any future development, mining or processing operations by the Company may produce air emissions, including fugitive dust and other air pollutants from stationary equipment, storage facilities and the use of mobile sources such as trucks and heavy construction equipment, which are subject to review, monitoring and/or control requirements under the CAA and state air quality laws. New facilities may be required to obtain permits before development, mining and processing work can begin, and existing facilities may be required to incur capital costs in order to remain in compliance. In addition, permitting rules may impose limitations on our production levels or result in additional capital expenditures in order to comply with the rules.

The National Environmental Policy Act (“NEPA”) requires federal agencies to integrate environmental considerations into their decision-making processes by evaluating the environmental impacts of their proposed actions, including issuance of permits to mining facilities, and assessing alternatives to those actions. If a proposed action could significantly affect the environment, the agency must prepare a detailed statement known as an Environmental Impact Statement (“EIS”). The EPA, other federal agencies, and any interested third parties will review and comment on the scoping of the EIS and the adequacy of and findings set forth in the draft and final EIS. This process can cause delays in issuance of required permits or result in changes to a project to mitigate its potential environmental impacts, which can in turn impact the economic feasibility of a proposed project.

The Clean Water Act (“CWA”), and comparable state statutes, impose restrictions and controls on the discharge of pollutants into waters of the United States. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the EPA or an analogous state agency. The CWA regulates storm water at mining facilities and requires a storm water discharge permit for certain activities. Such a permit requires the regulated facility to monitor and sample storm water run-off from its operations. The CWA and regulations implemented thereunder also prohibit discharges of dredged and fill material in wetlands and other waters of the United States unless authorized by an appropriately issued permit. The CWA and comparable state statutes provide for civil, criminal and administrative penalties for unauthorized discharges of pollutants and impose liability on parties responsible for those discharges for the costs of cleaning up any environmental damage caused by the release and for natural resource damages resulting from the release.

The Safe Drinking Water Act (“SDWA”) and the Underground Injection Control (“UIC”) program promulgated thereunder, regulate the drilling and operation of subsurface injection wells. The EPA directly administers the UIC program in some states and in others the responsibility for the program has been delegated to the state. The program requires that a permit be obtained before drilling a disposal or injection well. Violation of these regulations and/or contamination of groundwater by exploration, development, mining, processing or other related activities may result in fines, penalties, and remediation costs, among other sanctions and liabilities under the SWDA and state laws. In addition, third party claims may be filed by landowners and other parties claiming damages for alternative water supplies, property damages, and bodily injury.

Nevada

Other Nevada regulations govern operating and design standards for the construction and operation of any source of air contamination and landfill operations. Any changes to these laws and regulations could have an adverse impact on our financial performance and results of operations by, for example, requiring changes to operating constraints, technical criteria, fees or surety requirements.

Employees

As of the date of this filing, the Company has 12 employees (including shared employees). We continue to engage various independent contractors and consultants to fulfill additional needs. Additional employees will be hired on an as needed basis.

4

The Company’s management values the benefits that diversity can bring and seeks to maintain a management team and workforce comprised of talented and dedicated executives and employees with a diverse mix of experience, skills and backgrounds collectively reflecting the strategic needs of the business and the nature of the environment in which the Company operates. In identifying qualified candidates for available positions within the Company, the Company’s management will consider prospective candidates based on merit, having regard to those competencies, expertise, skills, background and other qualities identified from time to time by management being important in fostering a diverse and inclusive culture which solicits multiple perspectives and views and is free of conscious or unconscious bias and discrimination. The Company’s management will give due consideration to characteristics, such as gender, age, ethnicity, disability, sexual orientation and geographic representation.

Gold Price History

The price of gold is volatile and is affected by numerous factors, all of which are beyond our control, such as the sale or purchase of gold by various central banks and financial institutions, inflation, recession, fluctuation in the relative values of the U.S. dollar and foreign currencies, changes in global gold demand and political and economic conditions.

The following table presents the high, low and average afternoon fixed prices in U.S. dollars for an ounce of gold on the London Bullion Market over the past five years:

| Year | High | Low | Average | |||||||||

| 2018 | 1,355 | 1,178 | 1,269 | |||||||||

| 2019 | 1,546 | 1,270 | 1,393 | |||||||||

| 2020 | 2,067 | 1,474 | 1,770 | |||||||||

| 2021 | 1,943 | 1,684 | 1,797 | |||||||||

| 2022 | 2,039 | 1,628 | 1,800 | |||||||||

Data Source: www.kitco.com

Seasonality

The Company’s business operations, including exploration of the Bullfrog and Reward gold projects, are not subject to material restrictions on our operations due to seasonality.

Environmental Responsibility

Augusta Gold is committed to effective environmental stewardship. We have implemented and continue to develop business practices that are designed to reduce negative environmental impacts. We believe part of being a good corporate citizen requires a dedicated focus on how our industry, precious metals mining, affects the environment. In planning our development of the Bullfrog and Reward gold projects, we strive towards a more environmentally sound project development plan at the projects and within the local community.

Available Information

We make available, free of charge, on or through our Internet website, at www.augustagold.com, our Annual Report on Form 10-K, our quarterly reports on Form 10-Q and our current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. Our Internet website and the information contained therein or connected thereto are not intended to be, and are not incorporated into this Annual Report on Form 10-K.

5

ITEM 1A. RISK FACTORS

You should carefully consider the following risk factors in addition to the other information included in this Annual Report on Form 10-K. Each of these risk factors could materially and adversely affect our business, operating results and financial condition, as well as materially and adversely affect the value of an investment in our Common Shares. The risks described below are not the only ones facing the Company. Additional risks that we are not presently aware of, or that we currently believe are immaterial, may also adversely affect our business, operating results and financial condition. We cannot assure you that we will successfully address these risks or that other unknown risks exist that may affect our business.

Financial Risks

We have a history of losses and expect to continue to incur losses in the future.

With the exception of the current fiscal year, we have incurred losses since inception, have negative cash flow from operating activities and expect to continue to incur losses in the future.

We have an accumulated deficit of approximately $40,000,000 as of December 31, 2022. We expect to continue to incur losses unless and until such time as our Bullfrog or Reward gold projects or one of our future acquired properties enters into commercial production and generates sufficient revenues to fund continuing operations. We recognize that if we are unable to generate cash flows from mining operations and dispositions of our properties, we will not be able to earn profits or continue operations. At this early stage of our operation, we also expect to face the risks, uncertainties, expenses and difficulties frequently encountered by companies at the start up stage of their business development. We cannot be sure that we will be successful in addressing these risks and uncertainties and our failure to do so could have a materially adverse effect on our financial condition.

Negative Operating Cash Flow

The Company is an exploration stage issuer and has not generated cash flow from operations. The Company is devoting significant resources to the advancement of its Bullfrog and Reward gold projects and to actively pursue exploration and development opportunities, however, there can be no assurance that it will generate positive cash flow from operations in the future. The Company expects to continue to incur negative consolidated operating cash flow and losses until such time as it achieves commercial production at a particular project. The Company currently has negative cash flow from operating activities.

We have a limited operating history on which to base an evaluation of our business and prospects.

Since our inception we have had no revenue from operations. We have no history of producing metals from any of our properties. Our Bullfrog and Reward gold projects are exploration stage properties. Advancing properties from exploration into the development stage requires significant capital and time, and successful commercial production from a property, if any, will be subject to completing feasibility studies, permitting and construction of the mine, processing plants, roads, and other related works and infrastructure. As a result, we are subject to all of the risks associated with developing and establishing new mining operations and business enterprises including:

| ● | completion of feasibility studies to verify reserves and commercial viability, including the ability to find sufficient gold/silver mineral reserves to support a commercial mining operation; |

| ● | the timing and cost, which can be considerable, of further exploration, preparing feasibility studies, permitting and construction of infrastructure, mining and processing facilities; |

| ● | the availability and costs of drill equipment, exploration personnel, skilled labor and mining and processing equipment, if required; |

| ● | the availability and cost of appropriate smelting and/or refining arrangements, if required; |

| ● | compliance with environmental and other governmental approval and permit requirements; |

| ● | the availability of funds to finance exploration, development and construction activities, as warranted; |

| ● | potential opposition from non-governmental organizations, environmental groups, local groups or local inhabitants which may delay or prevent development activities; |

| ● | potential increases in exploration, construction and operating costs due to changes in the cost of fuel, power, materials and supplies; and |

| ● | potential shortages of mineral processing, construction and other facilities related supplies. |

6

The costs, timing and complexities of exploration, development and construction activities may be increased by the location of our properties and demand by other mineral exploration and mining companies. It is common in exploration programs to experience unexpected problems and delays during drill programs and, if commenced, development, construction and mine start-up. Accordingly, our activities may not result in profitable mining operations and we may not succeed in establishing mining operations or profitably producing metals at any of our properties.

We may need to obtain additional financing to fund our exploration programs.

If we raise additional funds by issuing additional equity or convertible debt securities, the ownership of existing stockholders may be diluted and the securities that we may issue in the future may have rights, preferences or privileges senior to those of the current holders of our common stock. If we raise additional funds by issuing debt, we could be subject to debt covenants that could place limitations on our operations and financial flexibility.

Increased costs could affect our financial condition.

We anticipate that costs at our projects and properties that we may explore or develop will frequently be subject to variation from one year to the next due to a number of factors, such as changing grade, metallurgy and revisions to mine plans, if any, in response to the physical shape and location of the body. In addition, costs are affected by the price of commodities such as fuel, steel, rubber, and electricity. Such commodities are at times subject to volatile price movements, including increases that could make production at certain operations less profitable. A material increase in costs at any significant location could have a significant effect on our profitability.

Operating Risks

Our Bullfrog and Reward gold projects are in the exploration stage.

The Bullfrog and Reward gold projects have estimated mineral resources, but there has not been a mineral reserve estimation in accordance with S-K 1300. There is no assurance that we can establish the existence of any mineral reserves on the Bullfrog or Reward gold projects in commercially exploitable quantities. Until we can do so, we cannot earn any revenues from the projects and if we do not do so, we will lose all of the funds that we expend on exploration. If we do not discover any mineral reserves in a commercially exploitable quantity, the exploration component of our business could fail.

The probability of an individual prospect ever having a “reserve” that meets the requirements of the SEC’s S-K 1300 standards is extremely remote; in all probability our projects do not contain any “reserves” and any funds that we spend on exploration could be lost. Even if we do eventually discover a mineral reserve on our project, there can be no assurance that they can be developed into producing mines and extract those minerals. Both mineral exploration and development involve a high degree of risk and few mineral properties which are explored are ultimately developed into producing mines.

The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade and other attributes of the mineral deposit, the proximity of the mineral deposit to infrastructure such as a smelter, roads and a point for shipping, government regulation and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral deposit unprofitable.

We cannot be assured that the Bullfrog or Reward gold projects are feasible or that a feasibility study will accurately forecast economic results.

The Bullfrog and Reward gold projects are our principal assets. Our future profitability depends largely on the economic feasibility of the projects. Before arranging financing for development and production at either the Bullfrog or Reward gold projects, we will have to complete a feasibility study. The results of our feasibility study may not be as favorable as the results of our prior studies. There can be no assurance that mining processes and results including potential gold production rates, revenue, capital and operating costs including taxes and royalties will not vary unfavorably from the estimates and assumptions included in such feasibility study.

7

The Bullfrog and Reward gold projects require substantial capital investment and we may be unable to raise sufficient capital on favorable terms or at all.

The exploration and, if warranted, development and operation of the Bullfrog and Reward gold projects will require significant capital. Our ability to raise sufficient capital and/or secure a development partner on satisfactory terms, if at all, will depend on several factors, including a favorable feasibility study, acquisition of the requisite permits, macroeconomic conditions, and future gold prices. Uncontrollable factors or other factors such as lower gold prices, unanticipated operating or permitting challenges, perception of environmental impact or, illiquidity in the debt markets or equity markets, could impede our ability to finance the Bullfrog or Reward gold projects on acceptable terms, or at all, including the cost of such capital and other conditions of financing arrangements that impose restrictive covenants and security interests that may affect the Company’s ability to operate as intended and ultimately its ability to continue as a going concern.

We may not be able to get the required permits at the Bullfrog and Reward gold projects in a timely manner or at all.

Any delay in acquiring the requisite permits, or failure to receive required governmental approvals could delay or prevent the start of exploration or, if warranted, development of the Bullfrog and Reward gold projects. If we are unable to acquire permits to explore, develop or mine the property, then the projects cannot be developed and operated. In addition, the property would have no reserves under S-K 1300, which could result in an impairment of the carrying value of the project.

We are a junior gold exploration company with no mining operations, and we may never have any mining operations in the future.

Our business is exploring for gold and other minerals. In the event that we discover commercially exploitable gold or other deposits, we will not be able to generate any sales from them unless the gold or other minerals are actually mined, or we sell all or a part of our interest. Accordingly, we will need to find some other entity to mine our properties on our behalf, mine them ourselves or sell our rights to mine to third parties. Mining operations in the United States are subject to many different federal, state, and local laws and regulations, including stringent environmental, health and safety laws. In the event we assume any operational responsibility for mining our properties, it is possible that we will be unable to comply with current or future laws and regulations, which can change at any time. It is possible that changes to these laws will be adverse to any potential mining operations. Moreover, compliance with such laws may cause substantial delays and require capital outlays in excess of those we anticipate, adversely affecting any potential mining operations of ours. Our future mining operations, if any, may also be subject to liability for pollution or other environmental damage. It is possible that we will choose to not be insured against this risk because of high insurance costs or other reasons.

Difficulties we may encounter managing our growth could adversely affect our results of operations.

As our business needs expand, we may need to hire a significant number of employees. This expansion may place a significant strain on our managerial and financial resources. To manage the potential growth of our operations and personnel, we will be required to:

| ● | improve existing, and implement new, operational, financial and management controls, reporting systems and procedures; |

| ● | install enhanced management information systems; and |

| ● | train, motivate and manage our employees. |

We may not be able to install adequate management information and control systems in an efficient and timely manner, and our current or planned personnel, systems, procedures and controls may not be adequate to support our future operations. If we are unable to manage growth effectively, our business would be seriously harmed.

8

If we lose key personnel or are unable to attract and retain additional qualified personnel, we may not be able to successfully manage our business and achieve our objectives.

We believe our future success will depend upon our ability to retain our key management. We may not be successful in attracting and retaining employees in the future and the loss of the key members of management would have a material adverse effect on our operations.

The outbreak of the coronavirus pandemic may impact the Company’s plans and activities

The Company’s exploration and development activities may be affected by existing or threatened medical pandemics, such as the novel coronavirus (COVID-19). A government may impose strict emergency measures in response to the threat or existence of an infectious disease, such as the emergency measures imposed by governments of many countries and states in response to the COVID-19 virus pandemic. As such, there are potentially significant economic and social impacts of infectious diseases, including but not limited to the inability of the Company to develop and operate as intended, shortage of skilled employees or labor unrest, inability to access sufficient healthcare, significant social upheavals or unrest, disruption to operations, supply chain shortages or delays, travel and trade restrictions, government or regulatory actions or inactions (including but not limited to, changes in taxation or policies, or delays in permitting or approvals, or mandated shut downs), declines in the price of precious metals, capital markets volatility, availability of credit, loss of investor confidence and impact on economic activity in affected countries or regions. In addition, such pandemics or diseases represent a serious threat to maintaining a skilled workforce in the mining industry and could be a major health-care challenge for the Company. There can be no assurance that the Company or the Company’s personnel will not be impacted by these pandemic diseases and the Company may ultimately see its workforce productivity reduced or incur increased medical costs/insurance premiums as a result of these health risks. COVID-19 is rapidly evolving and the effects on the mining industry and the Company are uncertain. The Company may not be able to accurately predict the impact of infectious disease, including COVID-19, or the quantum of such risks. There can be no assurance that the Company will not be impacted by adverse consequences that may be brought about by pandemics on global financial markets, which may reduce resources, share prices and financial liquidity and may severely limit the financing capital available to the Company.

Mining Risks

The nature of mineral exploration and production activities involves a high degree of risk and the possibility of uninsured losses.

Exploration for minerals is highly speculative and involves much greater risk than many other businesses. Most exploration programs do not result in the discovery of mineralization, and any mineralization discovered may not be of sufficient quantity or quality to be profitably mined. Our operations are, and any future development or mining operations we may conduct will be, subject to all of the operating hazards and risks normally incident to exploring for and development of mineral properties, such as, but not limited to:

| ● | economically insufficient mineralized material; |

| ● | the ability to find sufficient gold, silver or other metal reserves to support a profitable mining operation; |

| ● | fluctuation in production costs that make mining uneconomical; |

| ● | labor disputes; |

| ● | unanticipated variations in grade and geological characteristics; |

| ● | environmental events such as storms and flooding; |

| ● | water availability; |

| ● | difficult surface or underground conditions; |

| ● | industrial accidents; |

| ● | unexpected metallurgical response; |

| ● | mechanical and equipment performance limitations; |

| ● | geotechnical constraints; and |

| ● | decrease in the value of mineralized material due to lower gold and/or silver prices. |

9

Any of these risks can materially and adversely affect, among other things, the development of properties, production quantities and rates, costs and expenditures, potential revenues and production dates. We currently have very limited insurance to guard against some of these risks. If we determine that capitalized costs associated with any of our mineral interests are not likely to be recovered, we would incur a write-down of our investment in these interests. All of these factors may result in losses in relation to amounts spent which are not recoverable, or result in additional expenses.

Estimates of mineral resources are subject to evaluation uncertainties that could result in project failure.

Unless otherwise indicated, mineral resource figures presented in this Annual Report and in our filings with securities regulatory authorities, press releases and other public statements that may be made from time to time are based upon estimates made by independent geologists and mining engineers. When making determinations about whether to advance any of our projects to development, we must rely upon such estimates as to mineral resources, mineral reserves and grades on our properties.

Our exploration and future mining operations, if any, are and would be faced with risks associated with being able to accurately predict the quantity and quality of resources/reserves using sampling techniques and known resource estimation methodologies. Estimates of resources/reserve on our properties would be made using samples obtained from drilling programs. There is an inherent variability of assays between paired samples (proximal to each other) that cannot be reasonably eliminated. Additionally, there also may be unknown geologic details that have not been identified or correctly defined at the current level of accumulated knowledge about our properties. This could result in uncertainties that cannot be reasonably eliminated from the process of estimating resources/reserves.

Any material changes in resources/reserve estimates and grades will affect the economic viability of placing a property into production and a property’s return on capital.

As we have not completed feasibility studies on our Bullfrog or Reward gold projects and have not commenced actual production, resource estimates may require adjustments or downward revisions. In addition, the grade ultimately mined, if any, may differ from that indicated by our technical reports and drill results. Minerals recovered in small scale tests may not be duplicated in large scale tests under existing on-site conditions or in production scale.

The mineral resource estimates contained in this Annual Report have been determined based on assumed future prices, cut-off grades and operating costs that may prove to be inaccurate. Extended declines in market prices for gold or silver may render portions of our mineral resources uneconomic and result in reduced reported mineralization or adversely affect any commercial viability determinations we may reach. Any material reductions in estimates of mineral resources, or of our ability to extract mineral resources, could have a material adverse effect on our share price and the value of our properties.

Our exploration activities on our properties may not be commercially successful, which could lead us to abandon our plans to develop our properties and our investments in exploration.

Our long-term success depends on our ability to identify mineral deposits on our existing Bullfrog and Reward gold projects and other properties we may acquire, if any, that we can then develop into commercially viable mining operations. Mineral exploration is highly speculative in nature, involves many risks and is frequently non-productive. These risks include unusual or unexpected geologic formations, and the inability to obtain suitable or adequate equipment, or labor. The success of gold, silver and other commodity exploration is determined in part by the following factors:

| ● | the identification of potential mineralization based on surficial analysis; |

| ● | availability of government-granted exploration permits; |

| ● | the quality of our management and our geological and technical expertise; and |

| ● | the capital available for exploration and development work. |

Substantial expenditures are required to establish proven and probable mineral reserves through drilling and analysis, to develop metallurgical processes to extract metal, and to develop the mining and processing facilities and infrastructure at any site chosen for mining. Whether a mineral deposit will be commercially viable depends on a number of factors, which include, without limitation, the particular attributes of the deposit, such as size, grade and proximity to infrastructure; metal prices, which fluctuate widely; and government regulations, including, without limitation, regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. We may invest significant capital and resources in exploration activities and abandon such investments if we are unable to identify commercially exploitable mineral reserves. The decision to abandon a project may have an adverse effect on the market value of our securities and the ability to raise future financing.

10

The volatility of the price of gold and silver could adversely affect our future operations and, if warranted, our ability to develop our properties.

The potential for profitability of our operations, the value of our Bullfrog and Reward gold projects or other properties we may acquire, the market price of our shares of common stock and our ability to raise funding to conduct continued exploration and development, if warranted, are directly related to the market price of gold and silver. Our decision to put a mine into production and to commit the funds necessary for that purpose must be made long before the first revenue from production would be received. A decrease in the price of gold and/or silver may prevent our properties from being economically mined or result in the write-off of assets whose value is impaired as a result of lower gold and silver prices. The prices of gold and silver are affected by numerous factors beyond our control, including inflation, fluctuation of the U.S. dollar and foreign currencies, global and regional demand, the sale of gold by central banks, and the political and economic conditions of major gold and silver producing countries throughout the world.

The volatility in gold prices is illustrated in the table presented under “Part I - Item 1. Business - Gold Price History” above.

The volatility of metal prices represents a substantial risk which no amount of planning or technical expertise can fully eliminate. In the event gold and/or silver prices decline or remain low for prolonged periods of time, we might be unable to develop our properties, which may adversely affect our results of operations, financial performance and cash flows.

We are subject to significant governmental regulations, which affect our operations and costs of conducting our business.

Our current and future operations are and will be governed by laws and regulations, including:

| ● | laws and regulations governing mineral concession acquisition, prospecting, development, mining and production; |

| ● | laws and regulations related to exports, taxes and fees; |

| ● | labor standards and regulations related to occupational health and mine safety; and |

| ● | environmental standards and regulations related to waste disposal, toxic substances, land use and environmental protection. |

Companies engaged in exploration activities often experience increased costs and delays in production and other schedules as a result of the need to comply with applicable laws, regulations and permits. Failure to comply with applicable laws, regulations and permits may result in enforcement actions, including the forfeiture of mineral claims or other mineral tenures, orders issued by regulatory or judicial authorities requiring operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment or costly remedial actions. We may be required to compensate those suffering loss or damage by reason of our mineral exploration activities and may have civil or criminal fines or penalties imposed for violations of such laws, regulations and permits.

Existing and possible future laws, regulations and permits governing operations and activities of exploration companies, or more stringent implementation, could have a material adverse impact on our business and cause increases in capital expenditures or require abandonment or delays in exploration.

Our business is subject to extensive environmental regulations which may make exploring for or mining prohibitively expensive, and which may change at any time.

All our operations are subject to extensive environmental regulations which can make exploration expensive or prohibit it altogether. We may be subject to potential liabilities associated with the pollution of the environment and the disposal of waste products that may occur as the result of exploring and other related activities on our properties. We may have to make payments to remedy environmental pollution, which may reduce the amount of money that we have available to use for exploration. This may adversely affect our financial position, which may cause shareholders to lose their investment. If we are unable to fully remedy an environmental problem, we might be required to suspend operations or to enter into interim compliance measures pending the completion of the required remedy. If our properties are mined and we retain any operational responsibility for doing so, our potential exposure for remediation may be significant, and this may have a material adverse effect upon our business and financial position. We have not purchased insurance for potential environmental risks (including potential liability for pollution or other hazards associated with the disposal of waste products from our exploration activities).

11

If we mine one or more of our properties and retain operational responsibility for mining, then such insurance may not be available to us on reasonable terms or at a reasonable price. All of our exploration and, if warranted, development activities may be subject to regulation under one or more local, state and federal environmental impact analyses and public review processes. Future changes in applicable laws, regulations and permits or changes in their enforcement or regulatory interpretation could have significant impact on some portion of our business, which may require us to re-evaluate our business from time to time. These risks include, but are not limited to, the risk that regulatory authorities may increase bonding requirements beyond our financial capability. Inasmuch as posting of bonding in accordance with regulatory determinations is a condition to the right to operate under all material operating permits, increases in bonding requirements could prevent operations even if we are in full compliance with all substantive environmental laws.

Our property titles may be challenged. We are not insured against any challenges, impairments or defects to our mineral claims or property titles. We have not fully verified title to our properties.

Unpatented claims were created and maintained in accordance with the federal General Mining Law of 1872. Unpatented claims are unique U.S. property interests and are generally considered to be subject to greater title risk than other real property interests because the validity of unpatented claims is often uncertain. This uncertainty arises, in part, out of the complex federal and state laws and regulations under the General Mining Law. Although the annual payments and filings for these claims, permits and patents have been maintained, we have conducted limited title search on our properties. The uncertainty resulting from not having comprehensive title searches on the properties leaves us exposed to potential title suits. Defending any challenges to our property titles may be costly, and may divert funds that we could otherwise use for exploration activities and other purposes. In addition, unpatented claims are always subject to possible challenges by third parties or contests by the federal government, which, if successful, may prevent us from exploiting our discovery of commercially extractable gold. Challenges to our title may increase our costs of operation or limit our ability to explore on certain portions of our properties. We are not insured against challenges, impairments or defects to our property titles, nor do we intend to carry extensive title insurance in the future.

Possible amendments to the General Mining Law could make it more difficult or impossible for us to execute our business plan.

The U.S. Congress has considered proposals to amend the General Mining Law of 1872 that would have, among other things, permanently banned the sale of public land for mining. The proposed amendment would have expanded the environmental regulations to which we are subject and would have given Indian tribes the ability to hinder or prohibit mining operations near tribal lands. The proposed amendment would also have imposed a royalty of 8% of gross revenue on new mining operations located on federal public land, which would have applied to substantial portions of our properties. The proposed amendment would have made it more expensive or perhaps too expensive to recover any otherwise commercially exploitable gold deposits which we may find on our properties. While at this time the proposed amendment is no longer pending, this or similar changes to the law in the future could have a significant impact on our business.

Market forces or unforeseen developments may prevent us from obtaining the supplies and equipment necessary to explore for gold and other minerals.

Gold exploration, and resource exploration in general, requires engaging contractors, and may result in unforeseen shortages of supplies and/or equipment that could result in the disruption of our planned exploration activities. Current demand for exploration drilling services, equipment and supplies is robust and could result in suitable equipment and skilled manpower being unavailable at scheduled times for our exploration program. Fuel prices are extremely volatile as well. We will attempt to locate suitable equipment, materials, manpower and fuel if we have sufficient funds to do so. If we cannot find the equipment and supplies needed for our various exploration programs, we may have to suspend some or all of them until equipment, supplies, funds and/or skilled manpower become available. Any such disruption in our activities may adversely affect our exploration activities and financial condition.

We may not be able to maintain the infrastructure necessary to conduct exploration activities.

Our exploration activities depend upon adequate infrastructure. Reliable roads, bridges, power sources and water supply are important factors which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could adversely affect our exploration activities and financial condition.

12

Regulations and pending legislation governing issues involving climate change could result in increased operating costs, which could have a material adverse effect on our business.