UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

For the quarterly period ended March 31, 2024

OR

For the Transition Period from to

Commission File Number: 001-34949

(Exact Name of Registrant as Specified in Its Charter)

| (State or Other Jurisdiction of | (I.R.S. Employer | |||||||

| Incorporation or Organization) | Identification No.) | |||||||

(Address of Principal Executive Offices and Zip Code)

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| | ||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | Accelerated filer | Smaller reporting company | Emerging growth company | |||||||||||

| ☐ | ☐ | ☒ | ||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

As of April 30, 2024, the registrant had 188,717,409 common shares, without par value, outstanding.

ARBUTUS BIOPHARMA CORPORATION

| Page | ||||||||

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS (UNAUDITED)

ARBUTUS BIOPHARMA CORPORATION

Condensed Consolidated Balance Sheets

(Unaudited)

(In thousands of U.S. Dollars, except share amounts)

| March 31, 2024 | December 31, 2023 | ||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Investments in marketable securities, current | |||||||||||

| Accounts receivable | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

Property and equipment, net of accumulated depreciation of $ (December 31, 2023: $ | |||||||||||

| Investments in marketable securities, non-current | |||||||||||

| Right of use asset | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and stockholders’ equity | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable and accrued liabilities | $ | $ | |||||||||

| Deferred license revenue, current | |||||||||||

| Lease liability, current | |||||||||||

| Total current liabilities | |||||||||||

| Liability related to sale of future royalties | |||||||||||

| Contingent consideration | |||||||||||

| Lease liability, non-current | |||||||||||

| Total liabilities | |||||||||||

| Stockholders’ equity | |||||||||||

| Common shares | |||||||||||

| Authorized: unlimited number without par value | |||||||||||

Issued and outstanding: (December 31, 2023: | |||||||||||

| Additional paid-in capital | |||||||||||

| Deficit | ( | ( | |||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

See accompanying notes to the condensed consolidated financial statements.

1

ARBUTUS BIOPHARMA CORPORATION

Condensed Consolidated Statements of Operations and Comprehensive Loss

(Unaudited)

(In thousands of U.S. Dollars, except share and per share amounts)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Revenue | |||||||||||

| Collaborations and licenses | $ | $ | |||||||||

| Non-cash royalty revenue | |||||||||||

| Total Revenue | |||||||||||

| Operating expenses | |||||||||||

| Research and development | |||||||||||

| General and administrative | |||||||||||

| Change in fair value of contingent consideration | |||||||||||

| Total operating expenses | |||||||||||

| Loss from operations | ( | ( | |||||||||

| Other income | |||||||||||

| Interest income | |||||||||||

| Interest expense | ( | ( | |||||||||

| Foreign exchange gain | ( | ||||||||||

| Total other income | |||||||||||

| Net loss | $ | ( | $ | ( | |||||||

| Loss per share | |||||||||||

| Basic and diluted | $ | ( | $ | ( | |||||||

| Weighted average number of common shares | |||||||||||

| Basic and diluted | |||||||||||

| Comprehensive loss | |||||||||||

| Unrealized gain on available-for-sale securities | $ | $ | |||||||||

| Comprehensive loss | $ | ( | $ | ( | |||||||

See accompanying notes to the condensed consolidated financial statements.

2

ARBUTUS BIOPHARMA CORPORATION

Condensed Consolidated Statements of Stockholders’ Equity

(Unaudited)

(In thousands of U.S. Dollars, except share amounts)

| Common Shares | |||||||||||||||||||||||||||||||||||

| Number of Shares | Share Capital | Additional Paid-In Capital | Deficit | Accumulated Other Comprehensive Loss | Total Stockholders' Equity | ||||||||||||||||||||||||||||||

| Balance December 31, 2023 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | |||||||||||||||||||||||||||||||

| Issuance of common shares pursuant to the Open Market Sale Agreement | — | — | — | ||||||||||||||||||||||||||||||||

| Issuance of common shares pursuant to exercise of options | ( | — | — | ||||||||||||||||||||||||||||||||

| Issuance of common shares pursuant to ESPP | ( | — | — | ||||||||||||||||||||||||||||||||

| Issuance of common shares upon vesting of RSUs | ( | — | — | ||||||||||||||||||||||||||||||||

| Unrealized gain on available-for-sale securities | — | — | — | — | |||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Balance March 31, 2024 | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||

| Common Shares | ||||||||||||||||||||||||||||||||||||||

| Number of Shares | Share Capital | Additional Paid-In Capital | Deficit | Accumulated Other Comprehensive Loss | Total Stockholders' Equity | |||||||||||||||||||||||||||||||||

| Balance December 31, 2022 | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||

| Stock-based compensation expense | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Issuance of common shares pursuant to the Open Market Sale Agreement | — | — | — | |||||||||||||||||||||||||||||||||||

| Issuance of common shares pursuant to exercise of options | ( | — | — | |||||||||||||||||||||||||||||||||||

| Issuance of common shares pursuant to ESPP | ( | — | — | |||||||||||||||||||||||||||||||||||

| Unrealized gain on available-for-sale securities | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Net loss | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Balance March 31, 2023 | $ | $ | $ | ( | $ | ( | $ | |||||||||||||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

3

ARBUTUS BIOPHARMA CORPORATION

Condensed Consolidated Statements of Cash Flows

(Unaudited)

(In thousands of U.S. Dollars)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| OPERATING ACTIVITIES | |||||||||||

| Net loss | $ | ( | $ | ( | |||||||

| Non-cash items: | |||||||||||

| Depreciation | |||||||||||

| Stock-based compensation expense | |||||||||||

| Change in fair value of contingent consideration | |||||||||||

| Non-cash royalty revenue | ( | ( | |||||||||

| Non-cash interest expense | |||||||||||

| Net accretion and amortization of investments in marketable securities | ( | ( | |||||||||

| Net change in operating items: | |||||||||||

| Accounts receivable | ( | ( | |||||||||

| Prepaid expenses and other assets | ( | ( | |||||||||

| Accounts payable and accrued liabilities | ( | ( | |||||||||

| Change in deferred license revenue | ( | ( | |||||||||

| Other liabilities | ( | ( | |||||||||

| Net cash used in operating activities | ( | ( | |||||||||

| INVESTING ACTIVITIES | |||||||||||

| Purchase of investments in marketable securities | ( | ( | |||||||||

| Disposition of investments in marketable securities | |||||||||||

| Acquisition of property and equipment | ( | ( | |||||||||

| Net cash provided by investing activities | |||||||||||

| FINANCING ACTIVITIES | |||||||||||

| Issuance of common shares pursuant to the Open Market Sale Agreement | |||||||||||

| Issuance of common shares pursuant to exercise of stock options | |||||||||||

| Issuance of common shares pursuant to exercise of ESPP | |||||||||||

| Net cash provided by financing activities | |||||||||||

| Effect of foreign exchange rate changes on cash and cash equivalents | ( | ||||||||||

| Increase in cash and cash equivalents | |||||||||||

| Cash and cash equivalents, beginning of period | |||||||||||

| Cash and cash equivalents, end of period | $ | $ | |||||||||

See accompanying notes to the condensed consolidated financial statements.

4

ARBUTUS BIOPHARMA CORPORATION

Notes to Condensed Consolidated Financial Statements

(Tabular amounts in thousands of U.S. Dollars, except share and per share amounts)

1. Nature of business and future operations

Description of the Business

Arbutus Biopharma Corporation (“Arbutus” or “the Company”) is a clinical-stage biopharmaceutical company leveraging its extensive virology expertise to identify and develop novel therapeutics with distinct mechanisms of action, which can potentially be combined to provide a functional cure for patients with chronic hepatitis B virus (cHBV) infection. The Company believes the key to success in developing a functional cure involves suppressing hepatitis B virus deoxyribonucleic acid, reducing hepatitis B surface antigen and boosting HBV-specific immune responses. The Company’s pipeline of internally developed, proprietary compounds includes an RNAi therapeutic, imdusiran (AB-729), and an oral PD-L1 inhibitor, AB-101. Imdusiran has generated meaningful clinical data demonstrating an impact on both surface antigen reduction and reawakening of the HBV-specific immune response. Imdusiran is currently in three Phase 2a combination clinical trials. AB-101 is currently being evaluated in a Phase 1a/1b clinical trial.

The Company continues to protect and defend its intellectual property, which is the subject of the Company’s on-going lawsuits against Moderna and Pfizer/BioNTech for their use of its patented LNP technology in their COVID-19 vaccines. With respect to the Moderna lawsuit, the claim construction hearing occurred on February 8, 2024. On April 3, 2024, the Court provided its claim construction ruling, in which it construed the disputed claim terms and agreed with Arbutus’ position on most of the disputed claim terms. Fact discovery is on-going and next steps include expert reports and depositions. A trial date has been set for April 21, 2025, and is subject to change. The lawsuit against Pfizer/BioNTech is ongoing and a date for a claim construction hearing has not been set.

Liquidity

At March 31, 2024, the Company had an aggregate of $137.9 million in cash, cash equivalents and investments in marketable securities. The Company had no outstanding debt as of March 31, 2024. The Company believes it has sufficient cash resources to fund its operations for at least the next 12 months.

The success of the Company is dependent on obtaining the necessary regulatory approvals to bring its products to market and achieve profitable operations. The Company’s research and development activities and the commercialization of its products are dependent on its ability to successfully complete these activities and to obtain adequate financing through a combination of financing activities and operations. It is not possible to predict either the outcome of the Company’s existing or future research and development programs or the Company’s ability to continue to fund these programs in the future.

2. Significant accounting policies

Basis of presentation and principles of consolidation

These unaudited condensed consolidated financial statements have been prepared in accordance with United States generally accepted accounting principles for interim financial statements and accordingly, do not include all disclosures required for annual financial statements. These statements should be read in conjunction with the Company’s audited consolidated financial statements and notes thereto for the year ended December 31, 2023 included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023. These unaudited condensed consolidated financial statements include the accounts of Arbutus Biopharma Corporation and its one wholly-owned subsidiary, Arbutus Biopharma, Inc., and reflect, in the opinion of management, all adjustments and reclassifications necessary to fairly present the Company’s financial position as of March 31, 2024 and December 31, 2023, the Company’s results of operations for the three months ended March 31, 2024 and 2023, and the Company’s cash flows for the three months ended March 31, 2024 and 2023. Such adjustments are of a normal recurring nature. The results of operations for the three months ended March 31, 2024 are not necessarily indicative of the results for the full year. These unaudited condensed consolidated financial statements follow the same significant accounting policies as those described in the notes to the audited consolidated financial statements of the Company for the year ended December 31, 2023, except as described below under Recent Accounting Pronouncements.

5

Net loss per share

Revenue from collaborations and licenses

The Company generates revenue through certain collaboration agreements and license agreements. Such agreements may require the Company to deliver various rights and/or services, including intellectual property rights or licenses and research and development services. Under such agreements, the Company is generally eligible to receive non-refundable upfront payments, funding for research and development services, milestone payments and royalties.

The Company’s collaboration agreements fall under the scope of Accounting Standards Codification (ASC) Topic 808, Collaborative Arrangements (ASC 808, when both parties are active participants in the arrangement and are exposed to significant risks and rewards. For certain arrangements under the scope of ASC 808, the Company analogizes to ASC Topic 606, Revenue from Contracts with Customers (ASC 606), for some aspects, including for the delivery of a good or service (i.e., a unit of account).

ASC 606 requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers under a five-step model: (i) identify contract(s) with a customer; (ii) identify the performance obligations in the contract; (iii) determine the transaction price; (iv) allocate the transaction price to the performance obligations in the contract; and (v) recognize revenue when or as a performance obligation is satisfied.

In contracts where the Company has more than one performance obligation to provide its customer with goods or services, each performance obligation is evaluated to determine whether it is distinct based on whether (i) the customer can benefit from the good or service either on its own or together with other resources that are readily available and (ii) the good or service is separately identifiable from other promises in the contract. The consideration under the contract is then allocated between the distinct performance obligations based on their respective relative stand-alone selling prices. The estimated stand-alone selling price of each deliverable reflects the Company’s best estimate of what the selling price would be if the deliverable was regularly sold on a stand-alone basis and is determined by reference to market rates for the good or service when sold to others or by using an adjusted market assessment approach if the selling price on a stand-alone basis is not available.

The consideration allocated to each distinct performance obligation is recognized as revenue when control is transferred to the customer for the related goods or services. Consideration associated with at-risk substantive performance milestones, including sales-based milestones, is recognized as revenue when it is probable that a significant reversal of the cumulative revenue recognized will not occur. Sales-based royalties received in connection with licenses of intellectual property are subject to a specific exception in the revenue standards, whereby the consideration is not included in the transaction price and recognized in revenue until the customer’s subsequent sales or usages occur.

Deferred Revenue

When consideration is received or is unconditionally due from a customer, collaborator or licensee prior to the Company completing its performance obligation to the customer, collaborator or licensee under the terms of a contract, deferred revenue is recorded. Deferred revenue expected to be recognized as revenue within the 12 months following the balance sheet date is classified as a current liability. Deferred revenue not expected to be recognized as revenue within the 12 months following the balance sheet date is classified as a long-term liability. In accordance with ASC Topic 210-20, Balance Sheet - Offsetting (ASC 210-20) the Company’s deferred revenue is offset by a contract asset as further discussed in Note 9.

Segment information

6

Recent accounting pronouncements

In June 2016, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2016-13, Financial Instruments - Credit Losses: Measurement of Credit Losses in Financial Instruments (ASC 326). The guidance was effective for the Company beginning January 1, 2023 and it changed how entities account for credit losses on the financial assets and other instruments that are not measured at fair value through net income, including available-for-sale debt securities. The adoption of ASC 326 did not have a material impact on the Company’s results of operations or financial position.

In November 2023, the FASB issued ASU No. 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures (ASU 2023-07), which requires disclosure of significant segment expenses and other segment items on an annual and interim basis under ASC 280. ASU 2023-07 is effective for fiscal years beginning after December 15, 2023, and for interim periods beginning after December 15, 2024. Early adoption is permitted and the amendments in this ASU should be applied on a retrospective basis to all periods presented. The Company has not determined the impact ASU 2023-07 may have on the Company’s financial statement disclosures.

In December 2023, the FASB issued ASU No. 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures (ASU 2023-09), which improves income tax disclosures by requiring: (1) consistent categories and greater disaggregation of information in the rate reconciliation, and (2) income taxes paid disaggregated by jurisdiction. It also includes certain other amendments to improve the effectiveness of income tax disclosures. ASU 2023-09 is effective for annual periods beginning after December 15, 2024. Early adoption is permitted. The ASU indicates that all entities will apply the guidance prospectively with an option for retroactive application to each period presented in the financial statements. The Company has not determined the impact ASU 2023-09 may have on the Company’s financial statement disclosures.

The Company has reviewed all other recently issued standards and has determined that such standards will not have a material impact on the Company’s financial statements or do not otherwise apply to the Company’s operations.

3. Fair value measurements

The Company measures certain financial instruments and other items at fair value.

To determine the fair value, the Company uses the fair value hierarchy for inputs used in measuring fair value that maximize the use of observable inputs and minimize the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are inputs market participants would use to value an asset or liability and are developed based on market data obtained from independent sources. Unobservable inputs are inputs based on assumptions about the factors market participants would use to value an asset or liability. The three levels of inputs that may be used to measure fair value are as follows:

•Level 1 inputs are quoted market prices for identical instruments available in active markets.

•Level 2 inputs are inputs other than quoted prices included within Level 1 that are observable for the asset or liability either directly or indirectly. If the asset or liability has a contractual term, the input must be observable for substantially the full term. An example includes quoted market prices for similar assets or liabilities in active markets.

•Level 3 inputs are unobservable inputs for the asset or liability and will reflect management’s assumptions about market assumptions that would be used to price the asset or liability.

Assets and liabilities are classified based on the lowest level of input that is significant to the fair value measurements. Changes in the observability of valuation inputs may result in a reclassification of levels for certain securities within the fair value hierarchy.

The carrying values of cash and cash equivalents, accounts receivable, accounts payable and accrued liabilities approximate their fair values due to the immediate or short-term maturity of these financial instruments.

To determine the fair value of the contingent consideration (Note 8), the Company uses a probability weighted assessment of the likelihood the milestones would be met and the estimated timing of such payments, and then the potential contingent payments are discounted to their present value using a probability adjusted discount rate that reflects the early stage nature of

7

The following tables present information about the Company’s assets and liabilities that are measured at fair value on a recurring basis, and indicates the fair value hierarchy of the valuation techniques used to determine such fair value:

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||

| As of March 31, 2024 | (in thousands) | ||||||||||||||||||||||

| Assets | |||||||||||||||||||||||

| Cash and cash equivalents | $ | $ | $ | $ | |||||||||||||||||||

| Investments in marketable securities, current | |||||||||||||||||||||||

| Investments in marketable securities, non-current | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Liabilities | |||||||||||||||||||||||

| Contingent consideration | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||||||||||

| As of December 31, 2023 | (in thousands) | ||||||||||||||||||||||

| Assets | |||||||||||||||||||||||

| Cash and cash equivalents | $ | $ | $ | $ | |||||||||||||||||||

| Investments in marketable securities, current | |||||||||||||||||||||||

| Investments in marketable securities, non-current | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

| Liabilities | |||||||||||||||||||||||

| Contingent consideration | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

The following table presents the changes in fair value of the Company’s contingent consideration:

| Liability at beginning of the period | Change in fair value of liability | Liability at end of the period | |||||||||||||||

| (in thousands) | |||||||||||||||||

| Three Months Ended March 31, 2024 | $ | $ | $ | ||||||||||||||

| Three Months Ended March 31, 2023 | $ | $ | $ | ||||||||||||||

8

4. Investments in marketable securities

Investments in marketable securities consisted of the following:

| Amortized Cost | Gross Unrealized Gain(1) | Gross Unrealized Loss(1) | Fair Value | ||||||||||||||||||||

| As of March 31, 2024 | (in thousands) | ||||||||||||||||||||||

| Cash equivalents | |||||||||||||||||||||||

| Money market | $ | $ | — | $ | — | $ | |||||||||||||||||

| US treasury bills | $ | $ | — | $ | ( | $ | |||||||||||||||||

| Total | $ | $ | — | $ | ( | $ | |||||||||||||||||

| Investments in marketable short-term securities | |||||||||||||||||||||||

| US government agency bonds | $ | $ | $ | ( | $ | ||||||||||||||||||

| US corporate bonds | ( | ||||||||||||||||||||||

| US treasury bills | ( | ||||||||||||||||||||||

| Yankee bonds | ( | ||||||||||||||||||||||

| Total | $ | $ | $ | ( | $ | ||||||||||||||||||

| Investments in marketable long-term securities | |||||||||||||||||||||||

| US corporate bonds | ( | ||||||||||||||||||||||

| Total | $ | $ | $ | ( | $ | ||||||||||||||||||

(1) Gross unrealized gain (loss) is pre-tax and is reported in accumulated other comprehensive loss.

| Amortized Cost | Gross Unrealized Gain(1) | Gross Unrealized Loss(1) | Fair Value | ||||||||||||||||||||

| As of December 31, 2023 | (in thousands) | ||||||||||||||||||||||

| Cash equivalents | |||||||||||||||||||||||

| Money market fund | $ | $ | — | $ | — | $ | |||||||||||||||||

| Total | $ | $ | — | $ | — | $ | |||||||||||||||||

| Investments in marketable short-term securities | |||||||||||||||||||||||

| US government agency bonds | $ | $ | $ | ( | $ | ||||||||||||||||||

| US corporate bonds | ( | ||||||||||||||||||||||

| Yankee bonds | ( | ||||||||||||||||||||||

| US government bonds | $ | $ | $ | ( | $ | ||||||||||||||||||

| Total | $ | $ | $ | ( | $ | ||||||||||||||||||

| Investments in marketable long-term securities | |||||||||||||||||||||||

| US corporate bonds | ( | ||||||||||||||||||||||

| Total | $ | $ | $ | ( | $ | ||||||||||||||||||

(1) Gross unrealized gain (loss) is pre-tax and is reported in accumulated other comprehensive loss.

The contractual term to maturity of the $86.1 million of short-term marketable securities held by the Company as of March 31, 2024 is less than one year. As of March 31, 2024, the Company held $8.7 million of long-term marketable securities with contractual maturities of more than one year, but less than five years. As of December 31, 2023, the Company’s $99.7 million of short-term marketable securities had contractual maturities of less than one year, while the Company’s $6.3 million of long-term marketable securities had maturities of more than one year, but less than five years.

9

At March 31, 2024 and December 31, 2023, the Company had 42 and 37 , respectively, available-for-sale investment debt securities in an unrealized loss position without an allowance for credit losses. Unrealized losses on the Company’s investments in debt securities have not been recognized into income as the issuers’ bonds are of high credit quality and the decline in fair value is largely due to market conditions and/or changes in interest rates. The Company does not intend to sell and it is more likely than not that the Company will not be required to sell the securities prior to the anticipated recovery of their amortized cost basis. The issuers continue to make timely interest payments on the bonds. The fair value is expected to recover as the bonds approach maturity.

Accrued interest receivable on investments in marketable securities of $0.6

The Company had realized gains of less than $0.1 million for the three months ended March 31, 2024 and no realized gains or losses for the same period in 2023.

5. Investment in Genevant

In April 2018, the Company entered into an agreement with Roivant Sciences Ltd. (Roivant), its largest shareholder, to launch Genevant Sciences Ltd. (Genevant), a company focused on a broad range of RNA-based therapeutics enabled by the Company’s lipid nanoparticle (LNP) and ligand conjugate delivery technologies. The Company licensed rights to its LNP and ligand conjugate delivery platforms to Genevant for RNA-based applications outside of HBV, except to the extent certain rights had already been licensed to other third parties (the Genevant License). The Company retained all rights to its LNP and conjugate delivery platforms for HBV.

Under the Genevant License, as amended, if a third party sublicensee of intellectual property licensed by Genevant from the Company commercializes a sublicensed product, the Company becomes entitled to receive a specified percentage of certain revenue that may be received by Genevant for such sublicense, including royalties, commercial milestones and other sales-related revenue, or, if less, tiered low single-digit royalties on net sales of the sublicensed product. The specified percentage is 20 % in the case of a mere sublicense (i.e., naked sublicense) by Genevant without additional contribution and 14 % in the case of a bona fide collaboration with Genevant.

Additionally, if Genevant receives proceeds from an action for infringement by any third parties of the Company’s intellectual property licensed to Genevant, the Company would be entitled to receive, after deduction of litigation costs, 20 % of the proceeds received by Genevant or, if less, tiered low single-digit royalties on net sales of the infringing product (inclusive of the proceeds from litigation or settlement, which would be treated as net sales).

The Company accounts for its interest in Genevant as equity securities without readily determinable fair values. Accordingly, an estimate of the fair value of the securities is based on the original cost less previously recognized equity method losses, less impairments, plus or minus changes resulting from observable price changes in orderly transactions for identical or a similar Genevant securities. As of March 31, 2024, the carrying value of the Company’s investment in Genevant was zero and the Company owned approximately 16 % of the common equity of Genevant.

6. Accounts payable and accrued liabilities

Accounts payable and accrued liabilities are comprised of the following:

| March 31, 2024 | December 31, 2023 | ||||||||||

| (in thousands) | |||||||||||

| Trade accounts payable | $ | $ | |||||||||

| Research and development accruals | |||||||||||

| Professional fee accruals | |||||||||||

| Payroll accruals | |||||||||||

| Total accounts payable and accrued liabilities | $ | $ | |||||||||

10

7. Sale of future royalties

On July 2, 2019, the Company entered into a Purchase and Sale Agreement (the Agreement) with the Ontario Municipal Employees Retirement System (OMERS), pursuant to which the Company sold to OMERS part of its royalty interest on future global net sales of ONPATTRO® (Patisiran) (ONPATTRO), an RNA interference therapeutic currently being sold by Alnylam Pharmaceuticals, Inc. (Alnylam).

ONPATTRO utilizes the Company’s LNP technology, which was licensed to Alnylam pursuant to the Cross-License Agreement, dated November 12, 2012, by and between the Company and Alnylam (the LNP License Agreement). Under the terms of the LNP License Agreement, the Company is entitled to tiered royalty payments on global net sales of ONPATTRO ranging from 1.00 % to 2.33 % after offsets, with the highest tier applicable to annual net sales above $500 million. This royalty interest was sold to OMERS, effective as of January 1, 2019, for $20 million in gross proceeds before advisory fees. OMERS will retain this entitlement until it has received $30 million in royalties, at which point 100 % of such royalty interest on future global net sales of ONPATTRO will revert to the Company. OMERS has assumed the risk of collecting up to $30 million of future royalty payments from Alnylam and the Company is not obligated to reimburse OMERS if they fail to collect any such future royalties.

The $30 million in royalties to be paid to OMERS is accounted for as a liability, with the difference between the liability and the gross proceeds received accounted for as a discount. The discount, as well as $1.5 million of transaction costs, will be amortized as interest expense based on the projected balance of the liability as of the beginning of each period. As of March 31, 2024, the Company estimated an effective annual interest rate of approximately 2.0 %. Over the course of the Agreement, the actual interest rate will be affected by the amount and timing of royalty revenue recognized and changes in the timing of forecasted royalty revenue. On a quarterly basis, the Company will reassess the expected timing of the royalty revenue, recalculate the amortization and effective interest rate and adjust the accounting prospectively as needed.

The Company recognizes non-cash royalty revenue related to the sales of ONPATTRO during the term of the Agreement. As royalties are remitted to OMERS from Alnylam, the balance of the recognized liability is effectively repaid over the life of the Agreement. From the inception of the royalty sale through March 31, 2024, the Company has recorded an aggregate of $23.3 million of non-cash royalty revenue for royalties earned by OMERS. There are a number of factors that could materially affect the amount and timing of royalty payments from Alnylam, none of which are within the Company’s control.

During the three months ended March 31, 2024, the Company recognized non-cash royalty revenue of $0.6 million and related non-cash interest expense of less than $0.1 million. During the three months ended March 31, 2023, the Company recognized non-cash royalty revenue of $1.2 million and related non-cash interest expense of $0.2 million.

The table below shows the activity related to the net liability for the three months ended March 31, 2024 and 2023:

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (in thousands) | |||||||||||

| Net liability related to sale of future royalties - beginning balance | $ | $ | |||||||||

| Non-cash royalty revenue | ( | ( | |||||||||

| Non-cash interest expense | |||||||||||

| Net liability related to sale of future royalties - ending balance | $ | $ | |||||||||

In addition to the royalty from the LNP License Agreement, the Company is also receiving a second royalty interest ranging from 0.75 % to 1.125 % on global net sales of ONPATTRO, with 0.75 % applying to sales greater than $500 million, originating from a settlement agreement and subsequent license agreement with Acuitas Therapeutics, Inc. (Acuitas). The royalty from Acuitas has been retained by the Company and was not part of the royalty sale to OMERS.

11

8. Contingencies and commitments

Stock Purchase Agreement with Enantigen

In October 2014, Arbutus Inc., the Company’s wholly-owned subsidiary, acquired all of the outstanding shares of Enantigen Therapeutics, Inc. (Enantigen) pursuant to a stock purchase agreement. The amount paid to Enantigen’s selling shareholders could be up to an additional $102.5 million in sales performance milestones in connection with the sale of the first commercialized product by the Company for the treatment of HBV, regardless of whether such product is based upon assets acquired under this agreement, and a low single-digit royalty on net sales of such first commercialized HBV product, up to a maximum royalty payment of $1.0 million that, if paid, would be offset against the Company’s milestone payment obligations. Certain other development milestones related to the acquisition were tied to programs which are no longer under development by the Company, and therefore the contingency related to those development milestones is zero .

The contingent consideration is a financial liability and is measured at its fair value at each reporting period, with any changes in fair value from the previous reporting period recorded in the statements of operations and comprehensive loss (see Note 3).

The fair value of the contingent consideration was $7.8 million as of March 31, 2024.

9. Collaborations, contracts and licensing agreements

Collaborations

Qilu Pharmaceutical Co., Ltd.

In December 2021, the Company entered into a technology transfer and licensing agreement (the License Agreement) with Qilu Pharmaceutical Co., Ltd. (Qilu), pursuant to which the Company granted Qilu a sublicensable, royalty-bearing license, under certain intellectual property owned by the Company, which is non-exclusive as to development and manufacturing and exclusive with respect to commercialization of imdusiran, including pharmaceutical products that include imdusiran, for the treatment or prevention of hepatitis B in China, Hong Kong, Macau and Taiwan (the Territory).

In partial consideration for the rights granted by the Company, Qilu paid the Company a one-time upfront cash payment of $40.0 million, net of withholding taxes, on January 5, 2022, and agreed to pay the Company milestone payments totaling up to $245.0 million, net of withholding taxes, upon the achievement of certain technology transfer, development, regulatory and commercialization milestones. Qilu paid $4.4 million of withholding taxes to the Chinese taxing authority on the Company’s behalf, related to the upfront cash payment. In addition, Qilu agreed to pay the Company double-digit royalties into the low twenties percent based upon annual net sales of imdusiran in the Territory. The royalties are payable on a product-by-product and region-by-region basis, subject to certain limitations.

Qilu is responsible for all costs related to developing, obtaining regulatory approval for, and commercializing imdusiran for the treatment or prevention of hepatitis B in the Territory. Qilu is required to use commercially reasonable efforts to develop, seek regulatory approval for, and commercialize at least one imdusiran product candidate in the Territory. A joint development committee has been established between the Company and Qilu to coordinate and review the development, manufacturing and commercialization plans. Both parties also have entered into a supply agreement and related quality agreement pursuant to which the Company will manufacture or have manufactured and supply Qilu with all quantities of imdusiran necessary for Qilu to develop and commercialize in the Territory until the Company has completed manufacturing technology transfer to Qilu and Qilu has received all approvals required for it or its designated contract manufacturing organization to manufacture imdusiran in the Territory.

Concurrent with the execution of the License Agreement, the Company entered into a Share Purchase Agreement (the Share Purchase Agreement) with Anchor Life Limited, a company established pursuant to the applicable laws and regulations of Hong Kong and an affiliate of Qilu (the Investor), pursuant to which the Investor purchased 3,579,952 of the Company’s common shares at a purchase price of USD $4.19 per share, which was a 15 % premium on the thirty-day average closing price of the common shares as of the close of trading on December 10, 2021 (the Share Transaction). The Company received $15.0 million of gross proceeds from the Share Transaction on January 6, 2022. The common shares sold to the Investor in the Share Transaction represented approximately 2.5 % of the common shares outstanding immediately prior to the execution of the Share Purchase Agreement.

12

The License Agreement falls under the scope of ASC 808 as both parties are active participants in the arrangement and are exposed to significant risks and rewards. While this arrangement is in the scope of ASC 808, the Company analogizes to ASC 606 for some aspects of this arrangement, including for the delivery of a good or service (i.e., a unit of account). In accordance with the guidance, the Company identified the following commitments under the arrangement: (i) rights to develop, use, sell, have sold, offer for sale and import any product comprised of Licensed Product (as defined in the License Agreement) (the Qilu License) and (ii) drug supply obligations and manufacturing technology transfer (the Manufacturing Obligations). The Company determined that these two commitments are not distinct performance obligations for purposes of recognizing revenue as the manufacturing process is highly specialized and Qilu would not be able to benefit from the Qilu License without the Company’s involvement in the manufacturing activities until the transfer of the manufacturing know-how is complete. As such, the Company will combine these commitments into one performance obligation to which the transaction price will be allocated to and will recognize this transaction price associated with the bundled performance obligation over time using an inputs method based on labor hours expended by the Company on its Manufacturing Obligations.

The Company determined the initial transaction price of the combined performance obligation to be $50.4 million, which includes the $40.0 million upfront fee, $4.4 million of withholding taxes paid by Qilu on behalf of the Company, the premium paid for the Share Transaction of $4.1 million. The Company determined the milestone payments to be variable consideration subject to constraint at inception. At the end of each subsequent reporting period, the Company will reevaluate the probability of achievement of the future development, regulatory, and sales milestones subject to constraint and, if necessary, will adjust its estimate of the overall transaction price. Any such adjustments will be recorded on a cumulative catch-up basis, which would affect revenues and earnings in the period of adjustment.

| Transaction Price | Cumulative Collaboration Revenue Recognized | Deferred License Revenue | |||||||||||||||

| (in thousands) | |||||||||||||||||

| Combined performance obligation | $ | $ | $ | ||||||||||||||

| Less contract asset | ( | ||||||||||||||||

| Total deferred license revenue | |||||||||||||||||

The Company recognized $0.2 million of revenue based on labor hours expended by the Company on its Manufacturing Obligations during the three months ended March 31, 2024 and $4.1 million during the three months ended March 31, 2023.

As of March 31, 2024, the balance of the deferred license revenue was $13.5 million, which, in accordance with ASC 210-20, was partially offset by the contract asset associated with the manufacturing cost reimbursement of $2.0 million, resulting in a net deferred license revenue liability of $11.5 million.

The Company incurred $0.6 million of incremental costs in obtaining the Qilu License, which the Company capitalized in other current assets and other assets and amortizes as a component of general and administrative expense commensurate with the recognition of the combined performance obligation. The Company recognized amortization expense of less than $0.1

The Company reevaluates the transaction price and the total estimated labor hours expected to be incurred to satisfy the performance obligations and adjusts the deferred revenue at the end of each reporting period. Such changes will result in a change to the amount of collaboration revenue recognized and deferred revenue.

Barinthus Biotherapeutics plc

In July 2021, the Company entered into a clinical collaboration agreement with Barinthus Biotherapeutics plc (Barinthus), formerly Vaccitech plc, to evaluate imdusiran followed by Barinthus’ VTP-300, an HBV antigen specific immunotherapy, and ongoing nucleos(t)ide analogue therapy in patients with cHBV. Recently, the clinical trial was amended and is now dosing patients in an additional treatment arm that includes an approved PD-1 monoclonal antibody inhibitor, nivolumab (Opdivo®).

The Company is responsible for managing this Phase 2a proof-of-concept clinical trial, subject to oversight by a joint development committee comprised of representatives from the Company and Barinthus. The Company and Barinthus retain full

13

rights to their respective product candidates and will split all costs associated with the clinical trial. The Company incurred $0.5 million and $0.6 million of expenses, net of Barinthus’s 50% share, during the three months ended March 31, 2024 and 2023, respectively, and reflected those costs in research and development in the statements of operations and comprehensive loss.

Royalty Entitlements

Alnylam Pharmaceuticals, Inc. and Acuitas Therapeutics, Inc.

The Company has two royalty entitlements to Alnylam’s global net sales of ONPATTRO.

In 2012, the Company entered into the LNP License Agreement with Alnylam that entitles Alnylam to develop and commercialize products with the Company’s LNP technology. Alnylam launched ONPATTRO, the first approved application of the Company’s LNP technology, in 2018. Under the terms of this license agreement, the Company is entitled to tiered royalty payments on global net sales of ONPATTRO ranging from 1.00 % - 2.33 % after offsets, with the highest tier applicable to annual net sales above $500 million. This royalty interest was sold to OMERS, effective as of January 1, 2019, for $20 million in gross proceeds before advisory fees. OMERS will retain this entitlement until it has received $30 million in royalties, at which point 100 % of this royalty entitlement on future global net sales of ONPATTRO will revert back to the Company. OMERS has assumed the risk of collecting up to $30 million of future royalty payments from Alnylam and the Company is not obligated to reimburse OMERS if they fail to collect any such future royalties. If this royalty entitlement reverts to the Company, it has the potential to provide an active royalty stream or to be otherwise monetized again in full or in part. From the inception of the royalty sale through March 31, 2024, an aggregate of $23.3 million of royalties have been earned by OMERS.

The Company also is receiving a second royalty interest of 0.75 % to 1.125 % on global net sales of ONPATTRO, with 0.75 % applying to sales greater than $500 million, originating from a settlement agreement and subsequent license agreement with Acuitas. This royalty entitlement from Acuitas has been retained by the Company and was not part of the royalty entitlement sale to OMERS.

Revenues are summarized in the following table:

| Three Months Ended March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| (in thousands) | ||||||||||||||

| Revenue from collaborations and licenses | ||||||||||||||

| Acuitas Therapeutics, Inc. | $ | $ | ||||||||||||

| Qilu Pharmaceutical Co., Ltd. | ||||||||||||||

| Non-cash royalty revenue | ||||||||||||||

| Alnylam Pharmaceuticals, Inc. | ||||||||||||||

| Total revenue | $ | $ | ||||||||||||

10. Shareholders’ equity

Authorized share capital

The Company’s authorized share capital consists of an unlimited number of common shares and preferred shares, without par value, and 1,164,000 Series A participating convertible preferred shares, without par value.

Open Market Sale Agreement

The Company has an Open Market Sale AgreementSM with Jefferies LLC (Jefferies) dated December 20, 2018, as amended by Amendment No. 1, dated December 20, 2019, Amendment No. 2, dated August 7, 2020 and Amendment No. 3, dated March 4, 2021 (as amended, the Sale Agreement), under which the Company may issue and sell common shares, from time to time.

14

On December 23, 2019, the Company filed a shelf registration statement on Form S-3 with the Securities and Exchange Commission (the SEC) (File No. 333-235674) and accompanying base prospectus, which was declared effective by the SEC on January 10, 2020 (the January 2020 Registration Statement), for the offer and sale of up to $150.0 million of the Company’s securities. The January 2020 Registration Statement also contained a prospectus supplement for an offering of up to $50.0 million of the Company’s common shares pursuant to the Sale Agreement. This prospectus supplement was fully utilized during 2020. On August 7, 2020, the Company filed a prospectus supplement with the SEC (the August 2020 Prospectus Supplement) for an offering of up to an additional $75.0 million of its common shares pursuant to the Sale Agreement under the January 2020 Registration Statement. The August 2020 Prospectus Supplement was fully utilized during 2020. The January 2020 Registration Statement expired in January 2023.

On August 28, 2020, the Company filed a shelf registration statement on Form S-3 with the SEC (File No. 333-248467) and accompanying base prospectus, which was declared effective by the SEC on October 22, 2020 (the October 2020 Registration Statement), for the offer and sale of up to $200.0 million of the Company’s securities. On March 4, 2021, the Company filed a prospectus supplement with the SEC (the March 2021 Prospectus Supplement) for an offering of up to an additional $75.0 million of its common shares pursuant to the Sale Agreement under the October 2020 Registration Statement. The March 2021 Prospectus Supplement was fully utilized during 2021. On October 8, 2021, the Company filed a prospectus supplement with the SEC (the October 2021 Prospectus Supplement) for an offering of up to an additional $75.0 million of its common shares pursuant to the Sale Agreement under the October 2020 Registration Statement. The October 2020 Registration Statement expired in October 2023 with $29.3 million that was not utilized under the October 2021 Prospectus Supplement.

On November 4, 2021, the Company filed a shelf registration statement on Form S-3 with the SEC (File No. 333-260782) and accompanying base prospectus, which was declared effective by the SEC on November 18, 2021 (the November 2021 Registration Statement), for the offer and sale of up to $250.0 million of the Company’s securities.

On March 3, 2022, the Company filed a prospectus supplement with the SEC (the March 2022 Prospectus Supplement) for an offering of up to an additional $100.0 million of its common shares pursuant to the Sale Agreement under: (i) the January 2020 Registration Statement; (ii) the October 2020 Registration Statement; and (iii) the November 2021 Registration Statement, of which only the November 2021 Registration Statement remains active.

During the three months ended March 31, 2024, the Company issued 8,666,077 common shares pursuant to the Sale Agreement resulting in net proceeds of approximately $21.8 million. During the three months ended March 31, 2023, the Company issued 7,423,622 19.9 7,833,922 common shares pursuant to the Sale Agreement resulting in net proceeds of approximately $22.4 million.

As of April 30, 2024, there was approximately $25.4 million of common shares remaining available in aggregate under the March 2022 Prospectus Supplement, pursuant to the November 2021 Registration Statement.

Stock-based compensation

The table below summarizes information about the Company’s stock-based compensation for the three months ended March 31, 2024 and 2023 and the expense recognized in the condensed consolidated statements of operations:

15

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| (in thousands, except share and per share data) | |||||||||||

| Stock options | |||||||||||

| Options granted during period | |||||||||||

| Weighted average exercise price | $ | $ | |||||||||

| Restricted stock units (RSUs) | |||||||||||

| Restricted stock units granted during period | |||||||||||

| Grant date fair value | $ | $ | |||||||||

| Stock compensation expense | |||||||||||

| Research and development | $ | $ | |||||||||

| General and administrative | |||||||||||

| Total stock compensation expense | $ | $ | |||||||||

16

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion and analysis by our management of our financial position and results of operations in conjunction with our audited consolidated financial statements and related notes thereto included as part of our Annual Report on Form 10-K for the year ended December 31, 2023 and our unaudited condensed consolidated financial statements for the three months ended March 31, 2024. Our consolidated financial statements have been prepared in accordance with United States generally accepted accounting principles and are presented in U.S. dollars.

REFERENCES TO ARBUTUS BIOPHARMA CORPORATION

Throughout this Quarterly Report on Form 10-Q (Form 10-Q), the “Company,” “Arbutus,” “we,” “us,” and “our,” except where the context requires otherwise, refer to Arbutus Biopharma Corporation and its consolidated subsidiaries, and “our board of directors” refers to the board of directors of Arbutus Biopharma Corporation.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-Q contains “forward-looking statements” or “forward-looking information” within the meaning of applicable United States and Canadian securities laws (we collectively refer to these items as “forward-looking statements”). Forward-looking statements are generally identifiable by use of the words “believes,” “may,” “plans,” “will,” “anticipates,” “intends,” “budgets,” “could,” “estimates,” “expects,” “forecasts,” “projects” and similar expressions that are not based on historical fact or that are predictions of or indicate future events and trends, and the negative of such expressions. Forward-looking statements in this Form 10-Q, including the documents incorporated by reference, include statements about, among other things:

•our strategy, future operations, preclinical research, preclinical studies, clinical trials, prospects and the plans of management;

•the potential for our product candidates to achieve their desired or anticipated outcomes;

•the expected cost, timing and results of our clinical development plans and clinical trials, including our clinical collaborations with third parties;

•the discovery, development and commercialization of a curative combination regimen for chronic hepatitis B infection, a disease of the liver caused by the hepatitis B virus;

•the potential of our product candidates to improve upon the standard of care and contribute to a functional curative combination treatment regimen;

•obtaining necessary regulatory approvals;

•obtaining adequate financing through a combination of financing activities and operations;

•the expected returns and benefits from strategic alliances, licensing agreements, and research collaborations with third parties, and the timing thereof;

•our expectations regarding our technology licensed to third parties, and the timing thereof;

•our anticipated revenue and expense fluctuation and guidance;

•our expectations regarding the timing of announcing data from our ongoing clinical trials;

•our expectations regarding current patent disputes and litigation;

•our expectation of a net cash burn between $63 million and $67 million in 2024, excluding any proceeds from our Open Market Sale AgreementSM with Jefferies LLC dated December 20, 2018, as amended; and

•our belief that we have sufficient cash resources to fund our operations through the second quarter of 2026,

as well as other statements relating to our future operations, financial performance or financial condition, prospects or other future events. Forward-looking statements appear primarily in the sections of this Form 10-Q entitled “Part I, Item 1-Financial

17

Statements (Unaudited),” and “Part I, Item 2-Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Forward-looking statements are based upon current expectations and assumptions and are subject to a number of known and unknown risks, uncertainties and other factors that could cause actual results to differ materially and adversely from those expressed or implied by such statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in this Form 10-Q and our Annual Report on Form 10-K for the year ended December 31, 2023 (the Form 10-K), and in particular the risks and uncertainties discussed under “Item 1A-Risk Factors” of this Form 10-Q and the Form 10-K. As a result, you should not place undue reliance on forward-looking statements.

Additionally, the forward-looking statements contained in this Form 10-Q represent our views only as of the date of this Form 10-Q (or any earlier date indicated in such statement). While we may update certain forward-looking statements from time to time, we specifically disclaim any obligation to do so, even if new information becomes available in the future. However, you are advised to consult any further disclosures we make on related subjects in the periodic and current reports that we file with the Securities and Exchange Commission.

The foregoing cautionary statements are intended to qualify all forward-looking statements wherever they may appear in this Form 10-Q. For all forward-looking statements, we claim protection of the safe harbor contained in the Private Securities Litigation Reform Act of 1995.

This Form 10-Q also contains estimates, projections and other information concerning our industry, our business, the markets for certain diseases, including data regarding the estimated size of those markets, and the incidence and prevalence of certain medical conditions. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained this industry, business, market and other data from reports, research surveys, studies and similar data prepared by market research firms and other third parties, industry, medical and general publications, government data and similar sources.

18

OVERVIEW

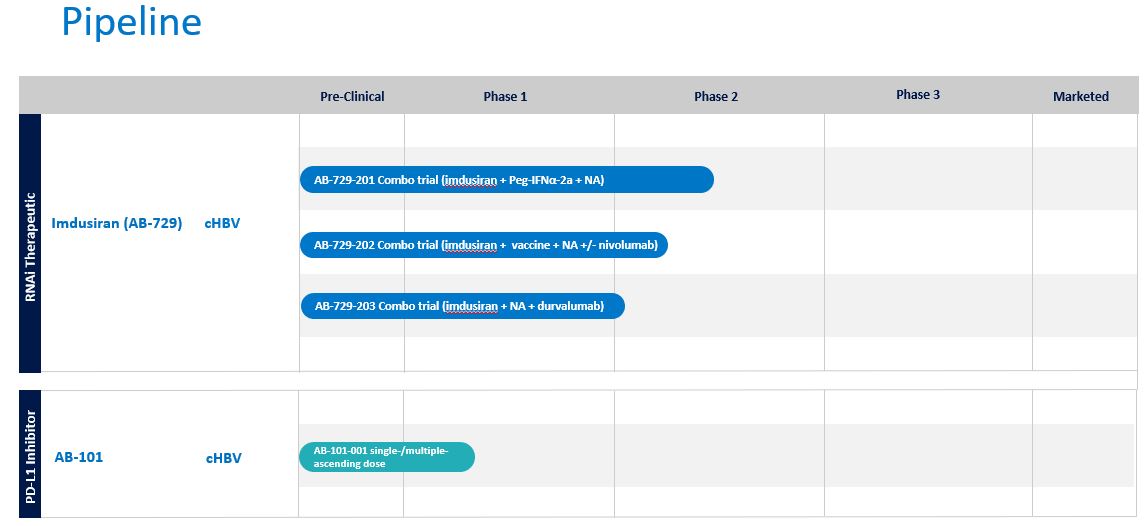

Arbutus Biopharma Corporation (“Arbutus”, the “Company”, “we”, “us”, and “our”) is a clinical-stage biopharmaceutical company leveraging its extensive virology expertise to identify and develop novel therapeutics with distinct mechanisms of action, which can potentially be combined to provide a functional cure for patients with chronic hepatitis B virus (cHBV) infection. We believe the key to success in developing a functional cure involves suppressing hepatitis B virus deoxyribonucleic acid (HBV DNA), reducing hepatitis B surface antigen (HBsAg) and boosting HBV-specific immune responses. Our pipeline of internally developed, proprietary compounds includes an RNAi therapeutic, imdusiran (AB-729), and an oral PD-L1 inhibitor, AB-101. Imdusiran has generated meaningful clinical data demonstrating an impact on both surface antigen reduction and reawakening of the HBV-specific immune response. Imdusiran is currently in three Phase 2a combination clinical trials. AB-101 is currently being evaluated in a Phase 1a/1b clinical trial.

We continue to protect and defend our intellectual property, which is the subject of our on-going lawsuits against Moderna and Pfizer/BioNTech for their use of our patented LNP technology in their COVID-19 vaccines. With respect to the Moderna lawsuit, the claim construction hearing occurred on February 8, 2024. On April 3, 2024, the Court provided its claim construction ruling, in which it construed the disputed claim terms and agreed with Arbutus’ position on most of the disputed claim terms. Fact discovery is on-going and next steps include expert reports and depositions. A trial date has been set for April 21, 2025, and is subject to change. The lawsuit against Pfizer/BioNTech is ongoing and a date for a claim construction hearing has not been set.

Strategy

The two core elements of our strategy are: 1) developing a portfolio of compounds that target HBV; and 2) combining therapeutic product candidates with complementary mechanisms of action to develop a functional cure for people with cHBV infection.

We believe that a combination of compounds that can suppress HBV DNA replication and HBsAg expression as well as boost patients’ HBV-specific immune response could address the most important elements to achieving a functional cure. Functional cure is defined as undetectable HBV DNA and HBsAg levels six months after discontinuation of all treatment. We are developing imdusiran as a cornerstone in a combination therapy that also includes antivirals and immunologics. We believe that a combination therapy delivered over a finite treatment period that results in a significant increase in the functional cure rate (i.e., a cure rate of at least 20%) would be a meaningful advancement for patients with cHBV infection.

Our HBV product pipeline includes the following:

•Imdusiran is our proprietary, conjugated GalNAc, subcutaneously-delivered RNAi therapeutic product candidate that suppresses all HBV antigens, including HBsAg expression, which is thought to be a key prerequisite to enable reawakening of a patient’s immune system to respond to HBV. Over 170 patients with cHBV infection have been dosed with imdusiran in our Phase 1 and ongoing Phase 2a clinical trials. Clinical data generated thus far has shown imdusiran to be generally safe and well-tolerated, while also providing meaningful reductions in HBsAg and HBV DNA.

•AB-101 is our oral PD-L1 inhibitor that has the potential to reawaken patients’ HBV-specific immune response by inhibiting PD-L1. AB-101 is currently in a Phase 1a/1b clinical trial (AB-101-001) evaluating the safety, tolerability, pharmacokinetics (PK), and pharmacodynamics (PD) of single- and multiple-ascending oral doses in healthy subjects and patients with cHBV infection. Part 1 of this clinical trial enrolled four sequential cohorts of eight healthy subjects each (6 active: 2 placebo) receiving a single dose of AB-101 at increasing dose levels up to 25 mg. The data showed that AB-101 was well-tolerated with evidence of dose-dependent receptor occupancy. In the 25mg cohort, all five evaluable subjects showed evidence of receptor occupancy between 50-100%. We have moved into Part 2 of this clinical trial which evaluates multiple-ascending doses of AB-101 in healthy subjects and we expect to report this preliminary data in the second half of 2024.

Our strategy is to position imdusiran as a potential cornerstone therapeutic in combination with AB-101 or other agents with potentially complementary mechanisms of action. We are currently conducting three Phase 2a clinical trials combining imdusiran with other agents. Upon successful completion of our AB-101-001 clinical trial, we intend to initiate a Phase 2 clinical trial combining imdusiran, AB-101 and nucleos(t)ide analogue (NA) therapy in patients with cHBV infection. The intent of these trials is to initially lower HBsAg levels with imdusiran and then administer a complementary agent, in this case an immune modulator or a therapeutic vaccine, to further lower HBsAg levels and promote anti-HBV immunity. We believe

19

that if we can lower HBsAg and promote immunity, we may achieve and sustain undetectable HBV DNA and HBsAg levels, potentially leading to a functional cure.

Our imdusiran development program includes the following Phase 2a clinical trials:

•Imdusiran in combination with Peg-IFNα-2a and ongoing standard-of-care NA therapy in patients with cHBV infection (AB-729-201). Preliminary data reported from this clinical trial suggest that the addition of Peg-IFNα-2a to imdusiran treatment was generally well-tolerated and appears to result in continued HBsAg declines in some patients.

•Imdusiran in combination with VTP-300, Barinthus Biotherapeutics plc’s (Barinthus and formerly Vaccitech plc), HBV antigen specific immunotherapy, and ongoing standard-of-care NA therapy in patients with cHBV infection (AB-729-202). Preliminary data reported from this clinical trial showed that dosing with imdusiran and then VTP-300 provided a meaningful reduction of HBsAg levels that are maintained well below baseline. We are also dosing patients in an additional cohort of this clinical trial that, in addition to imdusiran and VTP-300, includes up to two low doses of nivolumab (Opdivo®), an approved PD-1 monoclonal antibody inhibitor. Preliminary end-of-treatment data from this additional cohort are expected in the second half of 2024.

•Imdusiran in combination with durvalumab, an approved anti-PD-L1 monoclonal antibody, and ongoing standard-of-care NA therapy in patients with cHBV infection (AB-729-203). Screening has been initiated in this Phase 2a clinical trial. Insights gained from this clinical trial and the amended portion of the AB-729-202 clinical trial with nivolumab may inform dosing for a planned Phase 2 clinical trial combining imdusiran and AB-101.

Our Product Candidates

Our pipeline consists of two product candidates that are designed to suppress HBV DNA, reduce HBsAg and/or boost HBV-specific immune responses, as follows:

We continue to explore expansion opportunities for our pipeline through internal discovery and development activities and through potential strategic alliances.

RNAi therapeutic (imdusiran, AB-729)

RNAi therapeutics represent a significant advancement in drug development. RNAi therapeutics utilize a natural pathway within cells to silence genes by eliminating the disease-causing proteins that they code for. We are developing RNAi therapeutics that are designed to reduce HBsAg expression and other HBV antigens in people with cHBV infection. Reducing HBsAg is widely believed to be a key prerequisite to enable a patient’s immune system to reawaken and respond against the virus.

20

Imdusiran (AB-729) is a subcutaneously-delivered single-trigger RNAi therapeutic targeted to hepatocytes using our proprietary covalently conjugated GalNAc delivery technology. Imdusiran reduces all HBV antigens and inhibits viral replication.

Data from our Phase 1a/1b clinical trial evaluating single and multiple doses of imdusiran in healthy subjects and patients with cHBV (AB-729-001) showed that repeat dosing of 60mg and 90mg of imdusiran at different dosing intervals was well-tolerated and resulted in robust and comparable HBsAg declines and supported our view that 60mg every 8 weeks was an appropriate dose to move forward in our Phase 2a clinical trials.

Phase 2a proof-of-concept clinical trial to evaluate imdusiran in combination with Peg-IFNα-2a (AB-729-201)

We have completed enrollment in a randomized, open label, multicenter Phase 2a proof-of-concept clinical trial investigating the safety and antiviral activity of imdusiran in combination with short courses of Peg-IFNα-2a and ongoing NA therapy in 43 stably NA-suppressed, HBeAg negative, non-cirrhotic patients with cHBV infection. The primary objective of this trial is to initially lower HBsAg levels with imdusiran and then administer Peg-IFNα-2a as an immunomodulator to promote anti-HBV immune reawakening. We believe that if we can lower HBsAg and promote immune reawakening, we may achieve and sustain undetectable HBV DNA and HBsAg levels, potentially leading to a functional cure. After 24-weeks of dosing with imdusiran (60mg every 8 weeks), patients are randomized into one of four arms to receive ongoing Peg-IFNα-2a plus NA therapy for either 12 or 24 weeks, with or without additional doses of imdusiran. After completion of the assigned Peg-IFNα-2a treatment period, all patients will remain on NA therapy for the initial 24-week follow-up period, and will then discontinue NA treatment, provided they meet protocol-defined stopping criteria. Patients who stop NA therapy will enter an intensive follow-up period for 48 weeks.

At the European Association for the Study of the Liver (EASL) Congress in June 2023, we presented preliminary data from this clinical trial that suggests that the addition of Peg-IFNα-2a to imdusiran treatment was generally safe, well-tolerated and resulted in continued HBsAg declines in some patients. The mean HBsAg decline from baseline during the imdusiran lead-in phase was -1.6 log10 at week 24 of treatment which is comparable to what was previously seen in other clinical trials with imdusiran. Four patients reached HBsAg below the lower limit of quantitation (LLOQ) for at least one timepoint during Peg-IFNα-2a treatment.

We expect to provide end-of-treatment data for this clinical trial at the EASL Congress in June 2024.

Phase 2a proof-of-concept clinical trial to evaluate imdusiran in combination with Barinthus’ VTP-300 (AB-729-202)

Through a clinical collaboration agreement with Barinthus that we entered into in July 2021, we have completed enrollment in AB-729-202, a Phase 2a proof-of-concept clinical trial evaluating the safety, antiviral activity and immunogenicity of Barinthus’ VTP-300, an HBV antigen specific immunotherapy, administered after imdusiran in patients with cHBV infection. The initial trial design enrolled 40 NA-suppressed, HBeAg negative or positive, non-cirrhotic cHBV infected patients. The primary objective of this trial is to initially lower HBsAg levels with imdusiran and then administer VTP-300 as an immunomodulator to promote anti-HBV immune reawakening. We believe that if we can lower HBsAg and promote immune reawakening, we may achieve and sustain undetectable HBV DNA and HBsAg levels, potentially leading to a functional cure. All patients will receive imdusiran (60mg every 8 weeks, 4 doses) plus NA therapy for 24 weeks. After week 24, treatment with imdusiran will stop. Patients will continue only on NA therapy and will be randomized to receive VTP-300 or placebo at week 26 and week 30. At week 48, all patients will be evaluated for eligibility to discontinue NA therapy and will be followed for an additional 24 to 48 weeks.

Preliminary data from this clinical trial were presented at the AASLD Liver Meeting in November 2023 and included a subset of patients that received the two-dose VTP-300 regimen (28/40 patients) and available follow-up data to week 48 (12/40 patients) and showed the following:

•Robust reductions of HBsAg were seen during the imdusiran treatment period (-1.86 log10 mean reduction from baseline after 24 weeks of treatment). This decline in HBsAg is comparable to the declines seen with imdusiran in other clinical trials conducted to date.

•97% of the imdusiran treated patients (33/34) had HBsAg <100 IU/mL at the time of the first VTP-300/placebo dose. One patient reached <LLOQ with 24 weeks of imdusiran plus NA therapy alone.

•VTP-300 treatment appears to contribute to the maintenance of low HBsAg levels in the early post-treatment period, as the mean HBsAg levels in the placebo group begin to increase starting ~12 weeks after the last dose of imdusiran.

21

•All VTP-300 treated patients have maintained HBsAg <100 IU/mL through week 48, 60% have maintained HBsAg <10 IU/mL, and all have qualified to stop NA therapy.

•The preliminary safety data from this trial demonstrate that imdusiran and VTP-300 were both safe and well-tolerated. There were no serious adverse events, Grade 3 or 4 adverse events or treatment discontinuations.

End-of-treatment data from this portion of the clinical trial are expected to be reported at the EASL Congress in June 2024.

Additionally, we amended the AB-729-202 protocol to include another cohort that will receive imdusiran, VTP-300 and low dose nivolumab (Opdivo®), an approved PD-1 inhibitor. In this additional cohort, patients will receive imdusiran (60mg every 8 weeks, 4 doses) plus NA therapy for 24 weeks, followed by administration of VTP-300 plus up to two low doses of nivolumab while remaining on NA therapy. At week 48, all patients will be evaluated for eligibility to discontinue NA therapy, and will be followed for an additional 24 to 48 weeks. Preliminary end-of-treatment data from this additional cohort are expected in the second half of 2024.

This clinical trial is being managed by us, subject to oversight by a joint development committee comprised of representatives from both companies. We and Barinthus retain full rights to our respective product candidates and will split all costs associated with the clinical trial. Pursuant to the agreement, the parties may undertake a larger Phase 2b clinical trial depending on the results of the initial Phase 2a clinical trial.

Phase 2a proof-of-concept clinical trial to evaluate imdusiran in combination with durvalumab (AB-729-203)

We have initiated a Phase 2a clinical trial evaluating the safety, tolerability and antiviral activity of intermittent low doses of durvalumab, an approved anti-PD-L1 monoclonal antibody, in combination with imdusiran and ongoing standard-of-care NA therapy in patients with cHBV infection (AB-729-203). We are currently screening patients for this clinical trial that will enroll 30 patients in three separate cohorts where all patients will receive 60mg of imdusiran every 8 weeks for 48 weeks and 2 doses of 1.5 mg/kg of durvalumab given via IV infusion at two pre-specified times during the imdusiran treatment period that will differ by cohort. After completion of treatment, all patients will be assessed for potential discontinuation of NA therapy and followed for at least 24 to 48 weeks. Insights gained from this clinical trial and the amended portion of the AB-729-202 clinical trial with nivolumab may inform dosing for a planned Phase 2 clinical trial combining imdusiran and AB-101.

Oral PD-L1 Inhibitor (AB-101)

PD-L1 inhibitors complement our pipeline of agents and could potentially be an important part of a combination therapy for the treatment of HBV by reawakening the immune system. Highly functional HBV-specific T-cells within our immune system are believed to be required for long-term HBV viral resolution. However, HBV-specific T-cells become functionally defective, and greatly reduced in their frequency during cHBV infection. One approach to boost HBV-specific T-cells is to prevent PD-L1 proteins from binding to PD-1 and thus inhibiting the HBV-specific immune function of T-cells. Immune checkpoints such as PD-1/PD-L1 play an important role in the induction and maintenance of immune tolerance and in T-cell activation.

AB-101 is our proprietary oral small-molecule PD-L1 inhibitor candidate that we believe will allow for controlled checkpoint blockade while minimizing the systemic safety issues typically seen with checkpoint inhibitor antibody therapies. AB-101 is differentiated from monoclonal antibody checkpoint inhibitors such as durvalumab (anti-PD-L1) and nivolumab (anti-PD-1) because it is liver centric, has a much shorter duration of effect which may provide dosing and safety advantages, and has a novel mechanism of action as it binds to PD-L1 on the surface of cells causing dimerization and internalization of the PD-L1 protein followed by degradation within hours.

Preclinical data generated thus far indicates that AB-101 mediates activation and reinvigoration of HBV-specific T-cells from cHBV infected patients. In June 2022, we presented a poster at the 2022 EASL ILC highlighting data from a study that was designed to assess the preclinical activity of AB-101 and the compound’s ability to reinvigorate patient HBV-specific T-cells. Studies were conducted using a transgenic MC38 tumor mouse model and peripheral blood mononuclear cells (PBMCs) from cHBV infected patients. The data presented showed that once daily oral administration of AB-101 resulted in profound tumor reduction that was associated with T-cell activation. In addition, AB-101 activates and reinvigorates HBV-specific T-cells in vitro. Additionally, preclinical data in an HBV mouse model were presented at the 2022 AASLD Liver Meeting showing that monotherapy with AB-101 reduced PD-L1 in liver immune cells, confirming liver target engagement of the compound. Combination treatment with AB-101 and an HBV-targeting GalNAc-siRNA agent resulted in activation and increased frequency of HBV-specific T-cells and greater anti-HBsAg antibody production. This favorable preclinical profile supports further development of AB-101 as a therapeutic modality for cHBV infection treatment. We believe AB-101, when used in

22

combination with imdusiran or other approved and investigational agents, could potentially lead to a functional cure in HBV chronically infected patients.