Use these links to rapidly review the document

TABLE OF CONTENTS

Index to Consolidated Financial Statements of Ironwood Pharmaceuticals, Inc.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2011 |

||

OR |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission File Number 001-34620

IRONWOOD PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

04-3404176 (I.R.S. Employer Identification Number) |

|

301 Binney Street Cambridge, Massachusetts (Address of Principal Executive Offices) |

02142 (Zip Code) |

Registrant's telephone number, including area code: (617) 621-7722

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Class A common stock, $0.001 par value | The NASDAQ Stock Market LLC (NASDAQ Global Select Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

Aggregate market value of voting stock held by non-affiliates of the Registrant as of June 30, 2011: $1,375,964,667

As of February 15, 2012, there were 75,186,090 shares of Class A common stock outstanding and 31,770,641 shares of Class B common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the definitive proxy statement for our 2012 Annual Meeting of Stockholders are incorporated by reference into Part III of this report.

i

Our Company

We are an entrepreneurial pharmaceutical company that discovers, develops and intends to commercialize differentiated medicines that improve patients' lives. In order to be successful, we will need to overcome the enormous challenges inherent in the pharmaceutical product development model. Developing a novel therapeutic agent can take a decade or more and cost hundreds of millions of dollars, and most drug candidates fail to reach the market. We recognize that most companies undertaking this endeavor fail, yet despite the significant risks and our own experiences with multiple failed drug candidates, we are enthusiastic and passionate about our mission to deliver life-changing medicines to patients. To achieve our mission, we are building a team, a culture and processes centered on creating and marketing important new drugs. If we are successful getting medicines to patients and generating substantial returns for our stockholders, we plan to reinvest a portion of our future cash flows into our research and development efforts in order to accelerate and enhance our ability to bring new products to market. If we meet our goals, we hope to earn the right to continue building an enduring pharmaceutical company, an outstanding business that will thrive well beyond our lifetimes.

We are pioneers in the area of guanylate cyclase type-C, or GC-C, agonists and in the science and treatment of gastrointestinal diseases. Our development team has substantial expertise with the pharmacological profile associated with GC-C agonists, and they are complemented by our global operations and commercial teams that have significant experience in the associated therapeutic modalities. Our two most advanced GC-C agonists are linaclotide and IW-9179.

We believe that linaclotide, our GC-C agonist being developed for the treatment of patients with irritable bowel syndrome with constipation, or IBS-C, and chronic constipation, or CC, could present patients and healthcare practitioners with a unique therapy for a major medical need not yet met by existing therapies. IBS-C and CC are gastrointestinal disorders that affect millions of sufferers worldwide, according to our analysis of studies performed by N.J. Talley (published in 1995 in the American Journal of Epidemiology), P.D.R. Higgins (published in 2004 in the American Journal of Gastroenterology) and A.P.S. Hungin (published in 2003 in Alimentary Pharmacology and Therapeutics) as well as 2007 U.S. census data. Linaclotide was designed by Ironwood scientists to target the defining attributes of IBS-C: abdominal pain, discomfort, bloating and constipation. Linaclotide acts locally in the gut with no detectable systemic exposure in humans at therapeutic doses.

In eight Phase 2 and Phase 3 clinical studies involving almost 3,700 IBS-C and CC patients, linaclotide, with once-daily oral dosing, demonstrated sustained improvement of the pain and bloating as well as the constipation symptoms that define these chronic gastrointestinal disorders. In 2010, linaclotide completed the clinical efficacy portion of its development program, achieving favorable efficacy and safety results in all four of its Phase 3 clinical trials (two IBS-C clinical trials and two CC clinical trials), meeting all U.S. and European Union, or E.U., primary and secondary endpoints.

In each of the 12-week and 26-week Phase 3 studies involving patients with IBS-C, linaclotide reduced abdominal pain, abdominal discomfort and bloating within the first week, and these reductions were sustained throughout the entire treatment period. In the 12-week trial, 50% of linaclotide-treated patients had at least a 30% reduction in abdominal pain for at least six of the 12 weeks, and in the 26-week trial, 49% of linaclotide-treated patients had at least a 30% reduction in abdominal pain for at least six of the first 12 weeks of the treatment period. In the 26-week trial, linaclotide elicited a 40% mean decrease in abdominal pain by the sixth week, a 46% mean decrease by the twelfth week, and a 50% mean decrease at the twenty-sixth week.

As with abdominal pain, linaclotide-treated patients experienced a significant improvement in constipation symptoms during the first week of treatment in each of the Phase 3 IBS-C and CC clinical trials, and this improvement was sustained throughout the whole treatment period.

1

In the four Phase 3 studies, diarrhea was the most frequently reported adverse event (seen in 14% to 20% of linaclotide-treated patients), and the most frequently reported adverse event that led to study discontinuation (in 3% to 6% of linaclotide-treated patients). 90% of patients who had diarrhea described their diarrhea as mild to moderate.

In August 2011, we and our U.S. collaboration partner, Forest Laboratories, Inc., or Forest, submitted a New Drug Application, or an NDA, with the U.S. Food and Drug Administration, or the FDA, for linaclotide for the treatment of IBS-C and CC. In October 2011, the FDA accepted the NDA for review, and the FDA Prescription Drug User Fee Act, or PDUFA, target action date is expected to occur in June 2012. On February 8, 2012, we were informed that the FDA will not schedule an advisory committee meeting in connection with its review of our NDA. If linaclotide is approved for IBS-C and CC patients age 18 and older in the U.S., we may seek to expand linaclotide's market opportunity by exploring its utility in other gastrointestinal indications and in the pediatric population.

In September 2011, our European partner, Almirall S.A., or Almirall, submitted a Marketing Authorization Application, or an MAA, with the European Medicines Agency, or the EMA, for linaclotide for the treatment of IBS-C.

We have pursued a partnering strategy for commercializing linaclotide that has enabled us to retain significant control over linaclotide's development and commercialization, share the costs with high-quality collaborators whose capabilities complement ours, and retain approximately half of linaclotide's future long-term value in the major pharmaceutical markets, should linaclotide meet our sales expectations. As of December 31, 2011, licensing fees, milestone payments, related equity investments and development costs received from our linaclotide partners totaled approximately $350 million.

In September 2007, we entered into a partnership with Forest to co-develop and co-market linaclotide in the U.S. Under the terms of the collaboration agreement, we and Forest are jointly and equally funding the development and commercialization of linaclotide in the U.S., with equal share of any profits. Forest also has exclusive rights to develop and commercialize linaclotide in Canada and Mexico. If linaclotide is successfully developed and commercialized in the U.S., total licensing, milestone payments and related equity investments to us under the Forest collaboration agreement could total up to $330 million, including the $120 million that Forest has already paid to us and the $25 million of our capital stock that Forest has already purchased.

In April 2009, we entered into a license agreement with Almirall to develop and commercialize linaclotide in Europe (including the Commonwealth of Independent States countries and Turkey). If linaclotide is successfully developed and commercialized in the Almirall territory, total licensing, milestone payments and related equity investments to us could total up to $95 million, including the $57 million, net of foreign withholding taxes, that Almirall has already paid to us and the $15 million of our capital stock that Almirall has already purchased.

In November 2009, we entered into a license agreement with Astellas Pharma Inc., or Astellas, to develop and commercialize linaclotide in Japan, South Korea, Taiwan, Thailand, the Philippines and Indonesia. If linaclotide is successfully developed and commercialized in the Astellas territory, total licensing and milestone payments to us could total up to $75 million, including the $30 million that has already been paid to us.

We have retained all rights to linaclotide outside of the territories discussed above and continue to evaluate partnership opportunities in those unpartnered regions.

If linaclotide is approved by the FDA, we will receive five years of exclusivity under the Drug Price Competition and Patent Term Restoration Act of 1984, or the Hatch-Waxman Act. In addition, linaclotide is covered by a U.S. composition of matter patent that expires in 2025, subject to possible patent term extension. Linaclotide is also covered by E.U. and Japanese composition of matter patents, both of which expire in 2024, subject to possible patent term extension.

2

We invest carefully in our pipeline, and the commitment of funding for each subsequent stage of our development programs is dependent upon the receipt of clear, supportive data. Linaclotide is our only product candidate that has demonstrated clinical proof of concept. IW-9179 is a second generation GC-C agonist discovered by Ironwood scientists that is in early development for the treatment of painful disorders of the small intestine, such as dyspepsia and gastroparesis. We are also investing in several additional early development candidates in multiple therapeutic areas, including gastrointestinal disease, central nervous system, or CNS, disorders, and respiratory disease. We are also conducting discovery research in these therapeutic areas, as well as in the area of cardiovascular disease. Finally, we are actively engaged in evaluating and licensing rights to externally-discovered drug candidates at all stages of development. In evaluating potential assets, we apply the same criteria as those used for investments in internally-discovered assets.

We were incorporated in Delaware on January 5, 1998.

Owner-related Business Principles

We encourage all current and potential stockholders to read the owner-related business principles below that guide our overall strategy and decision making.

1. Ironwood's stockholders own the business; all of our employees work for them.

Each of our employees also has equity in the business, aligning their interests with their fellow stockholders. As employees and co-owners of Ironwood, our management and employee team seek to effectively allocate scarce stockholder capital to maximize the average annual growth of per share value.

Through our policies and communication, we seek to attract like-minded owner-oriented stockholders. We strive to effectively communicate our views of the business opportunities and risks over time so that entering and exiting stockholders are doing so at a price that approximately reflects our intrinsic value.

2. We believe we can best maximize long-term stockholder value by building a great pharmaceutical franchise.

We believe that Ironwood has the potential to deliver outstanding long-term returns to stockholders who are sober to the risks inherent in the pharmaceutical product lifecycle and to the potential dramatic highs and lows along the way, and who focus on superior long-term, per share cash flows.

Since the pharmaceutical product lifecycle is lengthy and unpredictable, we believe it is critical to have a long-term strategic horizon. We work hard to embed our long-term focus into our policies and practices, which may give us a competitive advantage in attracting like-minded stockholders and the highest caliber employees. Our current and future employees may perceive both financial and qualitative advantages in having their inventions or hard work result in marketed drugs that they and their fellow stockholders continue to own. Some of our key policies and practices that are aligned with this imperative include:

a. Our dual class equity voting structure (which provides for super-voting rights of our pre-IPO stockholders only in the event of a change of control vote) is designed to concentrate change of control decisions in the hands of long-term focused owners who have a history of experience with us.

b. Compensation is weighted to equity over salary for all of our employees, and many employees have a significant portion of their incentive compensation in milestone-based equity grants that reward achievement of major value-creating events a number of years out from the time of grant.

3

c. We have adopted a change of control severance plan for all of our employees that is intended to encourage them to bring forward their best ideas by providing them with the comfort that if a change of control occurs and their employment is terminated, they will still have an opportunity to share in the economic value that they have helped create for stockholders.

d. All of the members of our board of directors are substantial investors in the company. Furthermore, each director is required to hold all shares of stock acquired as payment for his or her service as a director throughout his or her term on the board.

e. Our partnerships with Forest, Almirall and Astellas all include standstill agreements, which serve to protect us from an unwelcome acquisition attempt by one of our partners. In addition, we have change of control provisions in our partnership agreements in order to protect the economic value of linaclotide should the acquirer of one of our partners be unable or unwilling to devote the time and resources required to make the program successful.

3. We are and will remain careful stewards of our stockholders' capital.

We work intensely to allocate capital carefully and prudently, continually reinforcing a lean, cost-conscious culture.

While we are mindful of the declining productivity and inherent challenges of pharmaceutical research and development, we intend to invest in discovery research for many years to come. Our singular passion is to create, develop and commercialize novel drug candidates, seeking to integrate the most successful drugmaking and marketing practices of the past and the best of today's cutting-edge technologies and basic research, development and commercialization advances.

While we hope to improve the productivity and efficiency of our drug creation efforts over time, our discovery process revolves around small, highly interactive, cross-functional teams. We believe that this is one area where our relatively small size is a competitive advantage, so for the foreseeable future, we do not expect our drug discovery team to grow beyond 100-150 scientists. We will continue to prioritize constrained resources and maintain organizational discipline. Once internally- or externally-derived candidates advance into development, compounds follow careful stage-gated plans, with further advancement depending on clear data points. Since most pharmaceutical research and development projects fail, it is critical that our teams are rigorous in making early go/no go decisions, following the data, terminating unsuccessful programs, and allocating scarce dollars and talent to the most promising efforts, thus enhancing the likelihood of late phase development success.

Our global operations and commercial teams take a similar approach to capital allocation and decision-making. By ensuring redundancy at each critical node of the linaclotide supply chain, our global operations team is mitigating against a fundamental risk inherent with pharmaceuticals—unanticipated shortages of commercial product. Likewise, we are building a high-quality commercial organization dedicated to bringing innovative, highly-valued healthcare solutions to all of our customers. Our commercial organization works closely and methodically with our global commercialization partners, striving to maximize linaclotide's commercial potential through focused efforts aimed at educating patients, payors and healthcare providers.

4. We believe commercializing our drugs is a crucial element of our long-term success.

For the foreseeable future, we intend to play an active role in the commercialization of our products in the U.S., and to out-license commercialization rights for other territories. We believe in the long-term value of our drug candidates, so we seek collaborations that provide meaningful economics and incentives for us and any potential partner. Furthermore, we seek partners who share our values, culture, processes, and vision for our products, which we believe will enable us to work with those partners successfully for the entire potential patent life of our drugs.

4

5. Our financial goal is to maximize long-term per share cash flows.

Our goal is to maximize long-term cash flows per share, and we will prioritize this even if it leads to uneven short-term financial results from an accounting perspective. If and when we become profitable, we expect and accept uneven earnings growth. Our underlying product development model is risky and unpredictable, and we have no intention to advance marginal development candidates or consummate suboptimal in-license transactions in an attempt to fill anticipated gaps in revenue growth. Successful drugs can be enormously beneficial to patients and highly profitable and rewarding to stockholders, and we believe strongly in our ability to occasionally (but not in regular or predictable fashion) create and commercialize great medicines that make a meaningful difference in patients' lives.

If and when we reach profitability, we do not intend to issue quarterly or annual earnings guidance, however we plan to be transparent about the key elements of our performance, including near-term operating plans and longer-term strategic goals.

Our Strategy

Our goal is to discover, develop and commercialize differentiated medicines that improve patients' lives, and to generate outstanding returns for our stockholders. Key elements of our strategy include:

- •

- attract and incentivize a team with a singular passion for creating and commercializing medicines that can make a

significant difference in patients' lives;

- •

- solidify and expand our position as the leader in the field of GC-C agonists;

- •

- successfully commercialize linaclotide in collaboration with Forest in the U.S.;

- •

- support our international partners to commercialize linaclotide outside of the U.S.;

- •

- harvest the maximum value of linaclotide outside of our partnered territories;

- •

- if approved for IBS-C and CC, develop linaclotide for the treatment of other gastrointestinal disorders and

for the pediatric population;

- •

- invest in our pipeline of novel product candidates and evaluate candidates outside of the company for

in-licensing or acquisition opportunities;

- •

- maximize the commercial potential of our drugs and participate in an important way in the economics when they reach the

market; and

- •

- execute our strategy with our stockholders' long-term interests in mind by seeking to maximize long-term per share cash flows.

Linaclotide Overview

IBS-C and CC are functional gastrointestinal disorders that afflict millions of sufferers worldwide. IBS-C is characterized by frequent and recurrent abdominal pain and/or discomfort and constipation symptoms (e.g. infrequent bowel movements, hard/lumpy stools, straining during defecation). CC is primarily characterized by constipation symptoms, but a majority of these patients report experiencing bloating and abdominal discomfort as among their most bothersome symptoms. Available treatment options primarily improve constipation, leading healthcare providers to diagnose and manage IBS-C and CC based on stool frequency. However, patients view these conditions as multi-symptom disorders, and while laxatives can be effective at relieving constipation symptoms, they do not necessarily improve abdominal pain, discomfort or bloating, and can often exacerbate these symptoms. This disconnect between patients and physicians, amplified by patients' embarrassment to discuss all of their gastrointestinal symptoms, often delays diagnosis and may compromise treatment, possibly causing additional suffering and disruption to patients' daily activities.

5

IBS-C and CC are chronic conditions characterized by frequent and bothersome symptoms that dramatically affect patients' daily lives. We believe that gastroesophageal reflux disease, or GERD, serves as a reasonable analogue to illustrate the potential for a treatment that effectively relieves chronic gastrointestinal symptoms. Based on a study performed by M. Camilleri published in 2005 in Clinical Gastroenterology and Hepatology and 2007 U.S. census data, we estimate that in 2007, approximately 40 million people in the U.S. suffered from GERD. The typical GERD sufferer, who experiences frequent episodes of heartburn poorly controlled by over the counter products, will commonly seek medical care and is generally treated with a proton pump inhibitor, such as Prilosec (omeprazole), Nexium (esomeprazole magnesium), Prevacid (lansoprazole), or Protonix (pantoprazole). According to IMS Health, peak sales of the proton pump inhibitor class reached $12.8 billion in November 2007. The proton pump inhibitors generally provide relief of key heartburn symptoms within the first week of treatment and have a favorable safety and tolerability profile. Once GERD patients experience relief of heartburn, they tend to be highly adherent to therapy, taking a proton pump inhibitor for approximately 200 days a year, according to IMS Health. The relief of bothersome symptoms and the recurrence of symptoms following discontinuation, serve to reinforce patient adherence to chronic therapy for functional disorders, like GERD, IBS-C and CC.

U.S. IBS-C and CC Opportunity

Based on the Talley and Higgins studies, studies performed by F.A. Luscombe (published in 2000 in Quality of Life Research) and J.F. Johanson (published in 2007 in Alimentary Pharmacology and Therapeutics), and 2007 U.S. census data, we estimate that in 2007, approximately 35 million to 46 million people in the U.S. suffered from symptoms of IBS-C or CC, of whom between 9 million to 15.5 million patients sought medical care. As a result of the less than optimal treatment options currently available, patients seeking care experienced a very low level of satisfaction. Due to patients' lack of satisfaction with existing treatment options, about 70% of patients stop prescription therapy within one month, according to IMS Health. It is estimated that patients seek medical care from five or more different healthcare providers over the course of their illness with limited or no success, as shown in a 2009 study by D.A. Drossman in the Journal of Clinical Gastroenterology. Many of the remaining patients are too embarrassed to discuss the full range of their symptoms, or for other reasons do not see the need to seek medical care and continue to suffer in silence while unsuccessfully self-treating with fiber, OTC laxatives and other remedies which improve constipation, but often exacerbate pain and bloating.

Irritable Bowel Syndrome with Constipation. Based on the Talley study and 2007 U.S. census data, we estimate that in 2007, approximately 12 million people or 5.2% of the U.S. adult population suffered from symptoms associated with IBS-C. As shown in a study conducted by the International Foundation of Functional Gastrointestinal Disorders, or IFFGD, in 2002, almost 35% of all IBS-C patients report suffering from some related symptoms daily. Based on this data and the Luscombe study, we estimate that up to 7 million of these patients sought medical attention for their symptoms. Based on the Talley, Luscombe and Johanson studies and 2007 U.S. census data, we estimate that between 5 million to 9 million sufferers have not consulted a physician and attempt to manage their symptoms with over the counter fiber and laxatives. Patients with IBS-C who seek medical care receive either a recommendation from their physician for an over the counter product or a prescription medication. As shown in a study conducted by the IFFGD in 2007, for all treated IBS-C patients, there continues to be a low rate of satisfaction with relief of their symptoms, with 92% of patients reporting that they are not fully satisfied with their treatments and 77% of patients reporting that they were unsatisfied with overall care by their physician.

6

Chronic Constipation. Based on the Higgins study and 2007 U.S. census data, we estimate that in 2007, 23 million to 34 million people, or 10% to 15% of the U.S. adult population, were suffering from CC. Based on this data and the Johanson study, we estimate that of the total CC sufferers, only 6 million to 8.5 million patients suffering from CC sought medical care. Almost all of these patients, whether or not seeking medical care for their symptoms, took an over the counter or prescription treatment, or both. Similar to IBS-C, there continues to be a low rate of treatment satisfaction, with over 70% of those taking over the counter and prescription laxatives reporting that they are not fully satisfied with their treatment results as shown in the Johanson study.

As shown in the figure below, according to L.E. Brandt in a study published in 2005 in the American Journal of Gastroenterology, the symptoms underlying both disorders can be viewed on a continuum. During a consultation, patients will often discuss only the predominant symptom, making it difficult for physicians to effectively diagnose and treat. For most patients, constipation is also accompanied by a set of symptoms broader than straining and infrequency of bowel movements. Given the limitations of available treatment options in addressing multiple symptoms, physicians tend to focus on the most easily treatable symptom, constipation. Our market research suggests that most physicians view abdominal pain and bloating as difficult to treat. We believe that linaclotide's profile could offer health care providers the opportunity to identify, diagnose, and treat the other important symptoms experienced by IBS-C and CC patients.

IBS-C and CC Opportunity Outside of U.S. We believe that the prevalence rates of IBS-C in Europe and Japan are similar to the prevalence rates in the U.S.

Burden of Illness. Both IBS-C and CC adversely affect the quality of life of patients, leading to increased absenteeism from work or school and increased costs to the healthcare system. According to both a study by A.P.S. Hungin published in 2005 in Alimentary Pharmacology & Therapeutics and the Johanson study, patients with IBS-C and CC reportedly suffer from their symptoms on average 166 and 97 days per year, respectively, and, according to the Drossman study, over one third have experienced their symptoms for more than ten years. In a typical month, IBS-C and CC patients will miss an average of one to three days of school or work, according to Johanson's study and a study by B. Cash published in 2005 in The American Journal of Medical Care, and their productivity will be disrupted an additional four to five days per month, according to the Cash study. When the level of suffering becomes acutely overwhelming for patients, they seek care at an ambulatory care facility. In 2004, CC was the second most common cause for ambulatory care visits after GERD, according to a 2008 article by J.E. Everhart published in Functional Intestinal Disorders. According to the Everhart article, CC accounted for 6.3 million ambulatory care visits (when considered as part of any listed diagnosis) and IBS accounted for 3 million ambulatory care visits. Estimates of the indirect and direct costs associated with these conditions range upwards of $25 billion, according to a study published in 2000 by M. Camilleri and D.E. Williams in Pharmacoeconomics.

Treatment Options for IBS-C and CC. By the time patients seek care from a physician, they have typically tried a number of available remedies and remain unsatisfied. Most IBS-C and CC patients initially attempt self-treatment with over the counter medications such as laxatives, stool softeners or fiber supplementation, as well as attempts to modify their diet. While some of these therapies offer

7

limited success in transit-related symptoms, they offer little to no effect on other bothersome symptoms from which patients are suffering. Unfortunately, physicians have very limited treatment options beyond what is readily available to the patient alone. Physicians typically rely on fiber and laxatives, which can exacerbate bloating and abdominal pain, the same symptoms from which many patients are seeking relief and which are the most troubling to treat. In an attempt to help alleviate the more severe abdominal symptoms associated with IBS-C and CC, healthcare providers sometimes prescribe medications that have not been approved by the FDA for these indications, such as anti-depressant or antispasmodic agents.

Polyethylene glycol, or PEG (such as Miralax), and lactulose, account for the majority of prescription and over the counter laxative treatments. Both agents demonstrate an increase in stool frequency and consistency but do not improve bloating or abdominal discomfort. Clinical trials and product labels document several adverse effects with PEG and lactulose, including exacerbation of bloating, cramping and, according to the Brandt study, up to a 40% incidence of diarrhea. Overall, up to 75% of patients taking prescription laxatives report not being completely satisfied with the predictability of when they will experience a bowel movement on treatment, and 50% were not completely satisfied with relief of the multiple symptoms associated with constipation, according to the Johanson study.

In 2002, the FDA approved Zelnorm, the first new drug for the treatment of IBS-C, and in 2004, Zelnorm was approved for the treatment of CC. Zelnorm is a serotonin 5-HT4 receptor agonist, with a mechanism of action completely separate and distinct from the mechanism of action underlying linaclotide's activity. As a newly available treatment option to potentially address some of the symptoms beyond the scope of laxatives and fiber, Zelnorm achieved great success in raising patient and physician awareness of IBS-C and CC. During the five years that Zelnorm was promoted, total prescriptions in the category grew three fold, and in 2006, there were more than 16 million total prescriptions written for treating patients with IBS-C and CC, according to IMS Health. In 2006, Zelnorm total sales were approximately $561 million. In 2007, Zelnorm was withdrawn from the market by its manufacturer due to an analysis that found a higher chance of heart attack, stroke and chest pain in patients treated with Zelnorm as compared to placebo. Despite modest effectiveness relieving abdominal pain (1% to 10% of patients responding to treatment as compared to placebo) and bloating (4% to 11% of patients responding to treatment as compared to placebo) as described on the Zelnorm product label, Zelnorm succeeded in establishing a symptom-based approach highlighting the need to recognize and treat, on a chronic basis, both the abdominal and constipation symptoms afflicting these patients.

Currently, the only available prescription therapy for IBS-C and CC is Amitiza, which was approved for the treatment of CC in 2006, and for IBS-C in 2008. Amitiza sales have been modest in comparison to Zelnorm sales prior to its withdrawal from the market, according to IMS Health.

Although a significant unmet need exists for better treatments for IBS-C and CC, there are very few treatments in late-stage clinical development. The most recent entrant to the CC marketplace, solely in Europe, is Resolor (prucalopride). Resolor was approved in 2009 by the EMA and is indicated for the treatment of CC in women for whom laxatives have failed to provide adequate relief. Resolor, which is marketed by Shire-Movetis, is a serotonin 5-HT4 receptor agonist like Zelnorm. Resolor is being launched in other European nations in 2012 and is currently in Phase 3 trials as a potential treatment for CC in males and for opioid induced constipation (OIC). Shire has recently announced it acquired rights to develop and commercialize prucalopride in the U.S. for the CC indication. The U.S. patent covering the composition of matter expires in 2015.

The Linaclotide Opportunity. Linaclotide is a promising potential treatment for patients suffering from both abdominal and constipation symptoms related to IBS-C and CC. Based on the clinical profile we have observed to date, we believe linaclotide is well positioned to provide IBS-C and CC patients with much needed reduction in abdominal and constipation symptoms, with a low incidence of adverse events, and a once daily, oral dosing regimen.

8

Annually, we estimate that over 30 million 30-day units of laxative and fiber medications are purchased in an effort to relieve chronic abdominal and constipation symptoms. Based on our analysis of data from IMS Health, The Nielsen Company and abstracts by P. Schoenfeld, et al. and W. Chey, et al. for the American College of Gastroenterology 2010 Annual Meeting and the 18th United European Gastroenterology Week, respectively, these 30 million units are comprised of 7-8 million laxative prescriptions for patients with constipation and abdominal symptoms and approximately 22 million over-the-counter (OTC) laxative and fiber units for chronic patients. Assuming a price comparable to those for branded prescription drugs for other gastrointestinal indications that are made available in Redbook and First Databank, the daily cost for linaclotide treatment per patient could range from $5.50 to $8.50 per day, with a prescription cost of $165 to $250 per month. Applying these assumptions to the potential market as a whole, these 30 million units could represent a potential U.S. commercial opportunity for a safe and effective IBS-C/CC drug in excess of $6 billion per year. Since many of these 30 million units are taken episodically or as rescue medications, there exists a potential upside in the market if the annual days of therapy increases, assuming that certain patients desire to manage and control their symptoms chronically. There is also the possibility that new patients could enter the marketplace as awareness of a new therapy increases.

Mechanism of Action

The underlying causes of the abdominal pain, discomfort and bloating suffered by patients with lower gastrointestinal disorders like IBS-C and CC are poorly understood. Further, because current therapeutic agents offer limited improvement in these symptoms, there has been limited medical research in this area. Since our clinical studies indicate that linaclotide provides rapid and sustained improvement of these symptoms, we have invested significant effort to define the mechanisms of linaclotide's physiological effects.

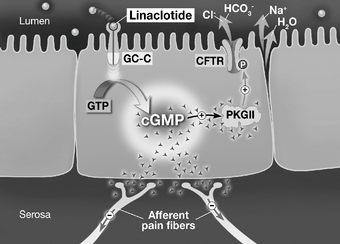

Linaclotide is a 14 amino acid peptide agonist of GC-C, a receptor found on the epithelial cells that line the intestine. Activation of GC-C leads to increases in intracellular and extracellular cyclic guanosine monophosphate, or cGMP, levels. cGMP is a well characterized "second messenger" that relays and amplifies signals received at receptors on the cell surface to target molecules in the cytosol and/or nucleus of a cell. We believe increased cGMP has dual effects on intestinal function. First, as the figure below shows, cGMP can exit the epithelial cells to block pain signaling by inhibiting the pain-sensing neurons that carry signals from the gastrointestinal tract to the central nervous system (afferent pain fibers). Second, cGMP can remain inside the epithelial cell to activate protein kinase GII, or PKGII, which activates the protein Cystic Fibrosis Transmembrane conductance Regulator, or CFTR, by phosphorylation, or P, to stimulate electrolyte (Na+ = sodium, Cl- = chloride, and HCO3- = bicarbonate) and fluid (H2O = water) secretion into the intestinal lumen. The resulting increase in intestinal fluid volume accelerates intestinal transit.

9

Our preclinical work supports the above model for the actions of linaclotide. Regarding the effect on pain sensation, we have found that increased extracellular cGMP inhibited noxious-stimulus-induced firing of afferent pain fibers. In addition, oral dosing with either linaclotide or directly with cGMP significantly reduced abdominal pain responses in a number of preclinical models. We hypothesize that the reduction in abdominal pain, abdominal discomfort, and visceral hypersensitivity seen both preclinically and clinically is a result of increased extracellular cGMP, which may reduce firing of pain-sensing neurons and thus decrease sensitivity to otherwise painful stimuli.

Additionally, in other preclinical studies, linaclotide was shown to increase intracellular cGMP, leading to activation of channels in intestinal cell membranes that resulted in the secretion of ions and fluid out of intestinal cells and into the intestinal lumen. Increased fluid in the intestinal lumen causes accelerated intestinal transit.

Importantly, linaclotide's effects on pain sensation and gastrointestinal transit/secretion are dependent on the presence of the GC-C receptor; in preclinical experiments where the GC-C receptor was genetically deleted, the effects of linaclotide on pain sensation and secretion were eliminated.

The binding and activity of linaclotide at the GC-C receptor is highly specific. Linaclotide has no effect on the serotonin system, unlike Zelnorm, Resolor, cisapride (Propulsid, which was approved for heartburn caused by GERD), or alosetron (Lotronex, which was approved for irritable bowel syndrome with diarrhea), each of which work through serotonin receptors in the intestine. Zelnorm, Propulsid and Lotronex were all withdrawn from the market because of safety concerns.

Clinical

Linaclotide completed the efficacy portion of its clinical development program in 2010, and two long-term safety studies are still ongoing. The clinical development program includes over 4,800 subjects across 13 studies: three in healthy volunteers, four in IBS-C patients, four in CC patients, and two long-term safety studies in IBS-C and CC patients.

Manufacturing and Supply

It is our goal to produce consistent, high-quality, stable drugs on a worldwide basis, with redundancy built into each critical step of the process. We currently manage our global supply of linaclotide through a combination of independent third party suppliers and our collaboration partners. We believe that we have sufficient in-house expertise to manage our global supply chain for linaclotide on an ongoing basis to meet worldwide demand, should it be approved by the regulatory authorities.

Pharmaceutical manufacturing consists of three phases—manufacturing of the active pharmaceutical ingredient, or API (sometimes referred to as drug substance), manufacturing of drug product and manufacturing of finished goods. We have entered into arrangements with multiple contract manufacturers for the production of linaclotide API, as it is a fundamental element of our strategy to maintain redundancy at all critical steps in the manufacturing supply chain. Linaclotide is a 14 amino acid peptide, manufactured via solid phase synthesis using naturally occurring amino acids. We have entered into commercial supply agreements with PolyPeptide Laboratories, Inc. and Polypeptide Laboratories (SWEDEN) AB, and with Corden Pharma Colorado, Inc. (formerly known as Roche Colorado Corporation), each for the manufacture of the linaclotide API that is being used to seek regulatory approval of linaclotide, and, pending any such approval, that will be incorporated into the finished product for commercialization in both our partnered and our unpartnered territories. We continue to pursue additional commercial supply agreements with additional manufacturers for linaclotide API for U.S. and worldwide use. We believe our commercial suppliers will have the capabilities to produce linaclotide API in accordance with current good manufacturing practices, or GMP, on a sufficient scale to meet our commercial needs.

10

Each of our collaboration partners, Forest, Almirall and Astellas, is responsible for linaclotide drug product and finished goods manufacturing in its respective territory. In addition, we have entered into an agreement with Almac Pharma Services Limited, or Almac, for linaclotide drug product manufacturing in the parts of the world outside of our partnered territories and to introduce redundancy into our supply chain within our partnered territories. We will be dependent upon the success of our partners and Almac in producing drug product for commercial sale.

We believe our efforts to date have led to a formulation that is both cost effective and able to meet the stability requirements for pharmaceutical products. Our work in this area has created an opportunity to seek additional intellectual property protections around the linaclotide program. In conjunction with Forest, we have filed patent applications worldwide to cover the current commercial formulation of linaclotide as well as related formulations. If these claims are allowed, they would expire in 2029 in the U.S. These patent rights would be subject to any potential patent term adjustments or extensions and/or supplemental protection certificates extending such term extensions in countries where such extensions may become available.

Sales and Marketing

For the foreseeable future, we intend to develop and commercialize our drugs in the U.S. alone or with partners, and will evaluate our commercialization opportunities for other territories. In executing our strategy, our goal is to retain significant control over the development process and commercial execution for our products, while participating in a meaningful way in the economics of all drugs that we bring to the market.

We plan to develop our commercial organization around linaclotide, with the intent to leverage this organization for future products. To deliver on our strategy, we intend to create a high-quality commercial organization dedicated to bringing innovative, highly-valued healthcare solutions to our customers, including patients, payors, and healthcare providers.

We are coordinating efforts with our partners Forest in North America and Almirall in Europe to ensure that we launch an integrated, global linaclotide brand. By leveraging the knowledge-base and expertise of our experienced commercial team and the insights of each of our linaclotide commercialization partners, we continually improve our collective marketing strategies.

Maximizing the Value of Linaclotide in the U.S.

We plan to establish linaclotide, if approved, as the prescription product of choice for both IBS-C and CC. We, together with our U.S. commercialization partner Forest, plan to build awareness that patients suffer from multiple, highly bothersome symptoms of IBS-C and CC, and that these symptoms can dramatically impair sufferers' quality of life.

Forest has demonstrated the ability to successfully launch innovative products, penetrate primary care markets and drive the growth of multiple brands in highly competitive markets. Forest brings large and experienced sales, national accounts, trade relations, operations and management teams providing ready access to primary care offices and key managed care accounts. We are building our own sales force and commercial presence to complement Forest's existing primary care expertise. We have strong alignment with Forest and a shared vision for linaclotide. The combined Ironwood and Forest marketing team possesses a deep understanding of gastroenterology and primary care customers, and this knowledge will be utilized to develop a compelling medical message and promotional campaign in the hope of delivering an effective treatment for patients suffering with the defining symptoms of IBS-C and CC.

11

In order to maximize linaclotide's value in the U.S. as quickly after commercial launch as possible, and to sustain such value over the long term, we and Forest will focus our initial commercialization efforts in the following areas:

- •

- Physician education: Our physician education plan encompasses efforts to reach out to over

70,000 of the highest prescribing primary care physicians and gastroenterologists in the U.S., with the goal of helping them identify appropriate patients, educating them on linaclotide's clinical

profile and enabling them to assess the clinical benefits of linaclotide.

- •

- Patient education: Our patient education plan encompasses efforts to reach out to

IBS-C and CC patients to enable them to more effectively communicate symptoms and treatment history to their physicians. Based on our research to date, these patients are high information

seekers, pursuing multiple information channels in order to learn about the disease state and potential therapies in order to have productive conversations with their doctors.

- •

- Payor value proposition: Based on the existing burden of illness associated with IBS-C and CC, and the efficacy and safety profile of linaclotide that was demonstrated through its clinical development program, we and Forest intend to provide a strong value proposition to governmental authorities, private health insurers and other third-party payors. We understand that sufficient access and reasonable reimbursement are essential in order to optimize linaclotide's commercial potential.

Maximizing the Value of Linaclotide Outside the U.S.

We have out-licensed commercialization rights for territories outside of the U.S. to Almirall in Europe and Astellas in Japan, South Korea, Taiwan, Thailand, the Philippines and Indonesia.

Almirall provides access to the highest potential European markets with an established direct presence in each of the United Kingdom, Italy, France, Germany and Spain, and also has a presence in Austria, Belgium, the Nordics, Poland, Portugal and Switzerland. Almirall plans to coordinate sales and marketing efforts from its central office in an effort to ensure consistency of the overall brand strategy and objectively assess performance. Almirall's knowledge of the local markets should help to facilitate regulatory access, reimbursement and market penetration through a customized approach to implementing promotional and selling campaigns in the E.U.

Astellas is one of Japan's largest pharmaceutical companies and has top commercial capabilities in both primary care and specialty categories throughout Asia. Their demonstrated ability to market innovative medicines and their growing gastrointestinal franchise in Japan make them an ideal partner for Ironwood.

We have retained all rights to linaclotide outside of the territories discussed above and we continue to evaluate partnership opportunities in those unpartnered regions.

Pipeline Strategy

We invest significant effort defining and refining our research and development process and teaching internally our approach to drug-making. We favor programs with early decision points, well validated targets, predictive preclinical models, initial chemical leads and clear paths to approval, all in the context of a target product profile that can address significant unmet or underserved clinical needs. We emphasize data-driven decision making, strive to advance or terminate projects early based on clearly defined go/no go criteria, prioritize programs at all stages and fluidly allocate our capital to the most promising programs. We continue to work diligently to ensure this disciplined approach is ingrained in our culture and processes and expect that our research productivity will continue to improve as our team gains more experience and capabilities. Moreover, we hope that as our passion and style of drug-making becomes better validated and more widely known, we will be able to attract additional like-minded researchers to join our cause.

12

To date, almost all of our product candidates have been discovered internally. We believe our discovery team has created a number of promising candidates over the past few years and has developed an extensive intellectual property estate in each of these areas.

In addition we have in-licensed, and are actively seeking to identify additional, attractive external opportunities. We utilize the same critical filters for investment when evaluating external programs as we do with our own, internally-discovered candidates.

Pipeline

We aim to create differentiated, first-in-class/best-in-class medicines that provide relief and clear therapeutic benefits to patients suffering from chronic diseases. To support this vision, we have ongoing efforts to identify product candidates that strengthen our pipeline, including treatments for gastrointestinal disorders, CNS disorders, respiratory disease and cardiovascular disease. Linaclotide is our only product candidate that has demonstrated clinical proof of concept. We have several early development candidates in multiple therapeutic areas, including gastrointestinal disease, CNS disorders and respiratory disease, including IW-9179, which is in early development for the treatment of painful gastrointestinal disorders of the small intestine such as dyspepsia and gastroparesis. We are also conducting discovery research in the afore-mentioned therapeutic areas, as well as in the area of cardiovascular disease.

Patents and Proprietary Rights

We actively seek to protect the proprietary technology that we consider important to our business, including pursuing patents that cover our products and compositions, their methods of use and the processes for their manufacture, as well as any other relevant inventions and improvements that are commercially important to the development of our business. We also rely on trade secrets that may be important to the development of our business.

Our success will depend significantly on our ability to obtain and maintain patent and other proprietary protection for the technology, inventions and improvements we consider important to our business; defend our patents; preserve the confidentiality of our trade secrets; and operate without infringing the patents and proprietary rights of third parties.

Linaclotide and GC-C Patent Portfolio

Our linaclotide patent portfolio is currently composed of eight issued U.S. patents, two granted European patents (each of which has been validated in 31 European countries and in Hong Kong), a granted Japanese patent, 11 issued patents in other foreign jurisdictions, and numerous pending provisional, U.S. non-provisional, foreign and PCT patent applications. We own all of the issued patents and own or jointly own all of the pending applications.

The issued U.S. patents, which will expire between 2024 and 2028, contain claims directed to the linaclotide molecule, pharmaceutical compositions thereof, methods of using linaclotide to treat gastrointestinal disorders and processes for making the molecule. If our pending patent application covering the current commercial formulation of linaclotide is allowed, it will expire in August 2029 or later, based upon a patent term adjustment. The granted European patents, which will expire in 2024, contain claims directed to the linaclotide molecule, pharmaceutical compositions thereof and uses of linaclotide to prepare medicaments for treating gastrointestinal disorders. The pending provisional, U.S. non-provisional, foreign and PCT applications contain claims directed to linaclotide and related molecules, pharmaceutical formulations thereof, methods of using linaclotide to treat various diseases and disorders and processes for making the molecule. These patent applications, if issued, will expire between 2024 and 2031.

13

The patent term of a patent that covers an FDA-approved drug may also be eligible for patent term extension, which permits patent term restoration as compensation for the patent term lost during the FDA regulatory review process. The Hatch-Waxman Act permits a patent term extension of up to five years beyond the expiration of the patent. The length of the patent term extension is related to the length of time the drug is under regulatory review. Patent extension cannot extend the remaining term of a patent beyond a total of 14 years from the date of product approval and only one patent applicable to an approved drug may be extended. Similar provisions are available in Europe and other foreign jurisdictions to extend the term of a patent that covers an approved drug. We expect to apply for patent term extensions for some of our current patents, depending upon the length of clinical trials and other factors involved in the submission of an NDA.

In addition to the patents and patent applications related to linaclotide, we currently have two issued U.S. patents and a number of pending provisional, U.S. non-provisional, foreign and PCT applications directed to other GC-C agonist molecules, pharmaceutical compositions thereof, methods of using these molecules to treat various diseases and disorders and processes of synthesizing the molecules. One of these two patents was issued in January 2012, and it covers the use of plecanatide, another GC-C agonist, for the treatment of IBS-C and constipation. Both of the issued U.S. patents will expire in 2024. The patent applications, if issued, will expire between 2024 and 2029.

Additional Intellectual Property

Our pipeline patent portfolio is currently composed of three issued U.S. patents; five issued patents in other foreign jurisdictions; and numerous pending provisional, U.S. non-provisional, foreign and PCT patent applications. We own all of the issued patents and own or jointly own all of the pending applications. The issued U.S. patents expire in 2022, 2024 and 2026. The foreign issued patents expire in 2024 and 2026. The pending patent applications, if issued, will expire between 2024 and 2032.

The term of individual patents depends upon the legal term of the patents in the countries in which they are obtained. In most countries in which we file, the patent term is 20 years from the date of filing the non-provisional application. In the U.S., a patent's term may be lengthened by patent term adjustment, which compensates a patentee for administrative delays by the U.S. Patent and Trademark Office in granting a patent, or may be shortened if a patent is terminally disclaimed over an earlier-filed patent. We also expect to apply for patent term extensions for some of our patents once issued, depending upon the length of clinical trials and other factors involved in the submission of an NDA.

Government Regulation

In the U.S., pharmaceutical products are subject to extensive regulation by the FDA. The Federal Food, Drug, and Cosmetic Act and other federal and state statutes and regulations, govern, among other things, the research, development, testing, manufacture, storage, recordkeeping, approval, labeling, promotion and marketing, distribution, post-approval monitoring and reporting, sampling, and import and export of pharmaceutical products. The FDA has very broad enforcement authority and failure to abide by applicable regulatory requirements can result in administrative or judicial sanctions being imposed on us, including warning letters, refusals of government contracts, clinical holds, civil penalties, injunctions, restitution, disgorgement of profits, recall or seizure of products, total or partial suspension of production or distribution, withdrawal of approval, refusal to approve pending applications, and criminal prosecution.

14

FDA Approval Process

We believe that our product candidates, including linaclotide, will be regulated by the FDA as drugs. No manufacturer may market a new drug until it has submitted an NDA to the FDA, and the FDA has approved it. The steps required before the FDA may approve an NDA generally include:

- •

- preclinical laboratory tests and animal tests conducted in compliance with FDA's good laboratory practice requirements;

- •

- development, manufacture and testing of active pharmaceutical product and dosage forms suitable for human use in

compliance with current GMP;

- •

- the submission to the FDA of an IND for human clinical testing, which must become effective before human clinical trials

may begin;

- •

- adequate and well-controlled human clinical trials to establish the safety and efficacy of the product for its

specific intended use(s);

- •

- the submission to the FDA of an NDA; and

- •

- FDA review and approval of the NDA.

Preclinical tests include laboratory evaluation of the product candidate, as well as animal studies to assess the potential safety and efficacy of the product candidate. The conduct of the pre-clinical tests must comply with federal regulations and requirements including good laboratory practices. We must submit the results of the preclinical tests, together with manufacturing information, analytical data and a proposed clinical trial protocol to the FDA as part of an IND, which must become effective before we may commence human clinical trials. The IND will automatically become effective 30 days after its receipt by the FDA, unless the FDA raises concerns or questions before that time about the conduct of the proposed trial. In such a case, we must work with the FDA to resolve any outstanding concerns before the clinical trial can proceed. We cannot be sure that submission of an IND will result in the FDA allowing clinical trials to begin, or that, once begun, issues will not arise that will cause us or FDA to suspend or terminate such trials. The study protocol and informed consent information for patients in clinical trials must also be submitted to an institutional review board for approval. An institutional review board may also require the clinical trial at the site to be halted, either temporarily or permanently, for failure to comply with the institutional review board's requirements or if the trial has been associated with unexpected serious harm to subjects. An institutional review board may also impose other conditions on the trial.

Clinical trials involve the administration of the product candidate to humans under the supervision of qualified investigators, generally physicians not employed by or under the trial sponsor's control. Clinical trials are typically conducted in three sequential phases, though the phases may overlap or be combined. In Phase 1, the initial introduction of the drug into healthy human subjects, the drug is usually tested for safety (adverse effects), dosage tolerance and pharmacologic action, as well as to understand how the drug is taken up by and distributed within the body. Phase 2 usually involves studies in a limited patient population (individuals with the disease under study) to:

- •

- evaluate preliminarily the efficacy of the drug for specific, targeted conditions;

- •

- determine dosage tolerance and appropriate dosage as well as other important information about how to design larger

Phase 3 trials; and

- •

- identify possible adverse effects and safety risks.

Phase 3 trials generally further evaluate clinical efficacy and test for safety within an expanded patient population. The conduct of clinical trials is subject to extensive regulation, including compliance with good clinical practice regulations and guidance.

15

The FDA may order the temporary or permanent discontinuation of a clinical trial at any time or impose other sanctions if it believes that the clinical trial is not being conducted in accordance with FDA requirements or presents an unacceptable risk to the clinical trial patients. We may also suspend clinical trials at any time on various grounds.

The results of the preclinical and clinical studies, together with other detailed information, including the manufacture and composition of the product candidate, are submitted to the FDA in the form of an NDA requesting approval to market the drug. FDA approval of the NDA is required before marketing of the product may begin in the U.S. If the NDA contains all pertinent information and data, the FDA will "file" the application and begin review. On October 24, 2011, we and Forest announced that the FDA filed the linaclotide NDA. Most such applications for non-priority drug products like linaclotide are reviewed by FDA within its PDUFA goal of 10 months. The current FDA PDUFA target action date for linaclotide is expected to occur in June 2012. The review process, however, may be extended by FDA requests for additional information, preclinical or clinical studies, clarification regarding information already provided in the submission, or submission of a risk evaluation and mitigation strategy. The FDA may refer an application to an advisory committee for review, evaluation and recommendation as to whether the application should be approved. The FDA is not bound by the recommendations of an advisory committee, but it considers such recommendations carefully when making decisions. Before approving an NDA, the FDA will typically inspect the facilities at which the product candidate is manufactured and will not approve the product candidate unless GMP compliance is satisfactory. FDA also typically inspects facilities responsible for performing animal testing, as well as clinical investigators who participate in clinical trials. The FDA may refuse to approve an NDA if applicable regulatory criteria are not satisfied, or may require additional testing or information. The FDA may also limit the indications for use and/or require post-marketing testing and surveillance to monitor the safety or efficacy of a product. Once granted, product approvals may be withdrawn if compliance with regulatory standards is not maintained or problems are identified following initial marketing.

The testing and approval process requires substantial time, effort and financial resources, and our product candidates may not be approved on a timely basis, if at all. The time and expense required to perform the clinical testing necessary to obtain FDA approval for regulated products can frequently exceed the time and expense of the research and development initially required to create the product. The results of preclinical studies and initial clinical trials of our product candidates, including linaclotide, are not necessarily predictive of the results from large-scale clinical trials, and clinical trials may be subject to additional costs, delays or modifications due to a number of factors, including difficulty in obtaining enough patients, investigators or product candidate supply. Failure by us or our collaborators, licensors or licensees, including Forest, Almirall and Astellas, to obtain, or any delay in obtaining, regulatory approvals or in complying with requirements could adversely affect the commercialization of product candidates and our ability to receive product or royalty revenues.

Hatch-Waxman Act

The Hatch-Waxman Act established abbreviated approval procedures for generic drugs. Approval to market and distribute these drugs is obtained by submitting an Abbreviated New Drug Application, or ANDA, with the FDA. The application for a generic drug is "abbreviated" because it need not include preclinical or clinical data to demonstrate safety and effectiveness and may instead rely on the FDA's previous finding that the brand drug, or reference drug, is safe and effective. In order to obtain approval of an ANDA, an applicant must, among other things, establish that its product is bioequivalent to an existing approved drug and that it has the same active ingredient(s), strength, dosage form, and the same route of administration. A generic drug is considered bioequivalent to its reference drug if testing demonstrates that the rate and extent of absorption of the generic drug is not significantly different from the rate and extent of absorption of the reference drug when administered under similar experimental conditions.

16

The Hatch-Waxman Act also provides incentives by awarding, in certain circumstances, certain legal protections from generic competition. This protection comes in the form of a non-patent exclusivity period, during which the FDA may not accept, or approve, an application for a generic drug, whether the application for such drug is submitted through an ANDA or a through another form of application, known as a 505(b)(2) application.

The Hatch-Waxman Act grants five years of exclusivity when a company develops and gains NDA approval of a new chemical entity that has not been previously approved by the FDA. This exclusivity provides that the FDA may not accept an ANDA or 505(b)(2) application for five years after the date of approval of previously approved drug, or four years in the case of an ANDA or 505(b)(2) application that challenges a patent claiming the reference drug (see discussion below regarding patent challenges). The Hatch-Waxman Act also provides three years of exclusivity for approved applications for drugs that are not new chemical entities, if the application contains the results of new clinical investigations (other than bioavailability studies) that were essential to approval of the application. Examples of such applications include applications for new indications, dosage forms (including new drug delivery systems), strengths, or conditions of use for an already approved product. This three-year exclusivity period only protects against FDA approval of ANDAs and 505(b)(2) applications for generic drugs that include the innovation that required new clinical investigations that were essential to approval; it does not prohibit the FDA from accepting or approving ANDAs or 505(b)(2) NDAs for generic drugs that do not include such an innovation.

Paragraph IV Certifications. Under the Hatch-Waxman Act, NDA applicants and NDA holders must provide information about certain patents claiming their drugs for listing in the FDA publication, "Approved Drug Products with Therapeutic Equivalence Evaluations," also known as the "Orange Book." When an ANDA or 505(b)(2) application is submitted, it must contain one of several possible certifications regarding each of the patents listed in the Orange Book for the reference drug. A certification that a listed patent is invalid or will not be infringed by the sale of the proposed product is called a "Paragraph IV" certification.

Within 20 days of the acceptance by the FDA of an ANDA or 505(b)(2) application containing a Paragraph IV certification, the applicant must notify the NDA holder and patent owner that the application has been submitted, and provide the factual and legal basis for the applicant's opinion that the patent is invalid or not infringed. The NDA holder or patent holder may then initiate a patent infringement suit in response to the Paragraph IV notice. If this is done within 45 days of receiving notice of the Paragraph IV certification, a one-time 30-month stay of the FDA's ability to approve the ANDA or 505(b)(2) application is triggered. The FDA may approve the proposed product before the expiration of the 30-month stay only if a court finds the patent invalid or not infringed, or if the court shortens the period because the parties have failed to cooperate in expediting the litigation.

Patent Term Restoration. Under the Hatch-Waxman Act, a portion of the patent term lost during product development and FDA review of an NDA or 505(b)(2) application is restored if approval of the application is the first permitted commercial marketing of a drug containing the active ingredient. The patent term restoration period is generally one-half the time between the effective date of the IND and the date of submission of the NDA, plus the time between the date of submission of the NDA and the date of FDA approval of the product. The maximum period of restoration is five years, and the patent cannot be extended to more than 14 years from the date of FDA approval of the product. Only one patent claiming each approved product is eligible for restoration and the patent holder must apply for restoration within 60 days of approval. The U.S. Patent and Trademark Office, in consultation with the FDA, reviews and approves the application for patent term restoration.

Other Regulatory Requirements

After approval, drug products are subject to extensive continuing regulation by the FDA, which include company obligations to manufacture products in accordance with GMP, maintain and provide to

17

the FDA updated safety and efficacy information, report adverse experiences with the product, keep certain records and submit periodic reports, obtain FDA approval of certain manufacturing or labeling changes, and comply with FDA promotion and advertising requirements and restrictions. Failure to meet these obligations can result in various adverse consequences, both voluntary and FDA-imposed, including product recalls, withdrawal of approval, restrictions on marketing, and the imposition of civil fines and criminal penalties against the NDA holder. In addition, later discovery of previously unknown safety or efficacy issues may result in restrictions on the product, manufacturer or NDA holder.

We and any manufacturers of our products are required to comply with applicable FDA manufacturing requirements contained in the FDA's GMP regulations. GMP regulations require among other things, quality control and quality assurance as well as the corresponding maintenance of records and documentation. The manufacturing facilities for our products must meet GMP requirements to the satisfaction of the FDA pursuant to a pre-approval inspection before we can use them to manufacture our products. We and any third-party manufacturers are also subject to periodic inspections of facilities by the FDA and other authorities, including procedures and operations used in the testing and manufacture of our products to assess our compliance with applicable regulations.

With respect to post-market product advertising and promotion, the FDA imposes a number of complex regulations on entities that advertise and promote pharmaceuticals, which include, among others, standards for direct-to-consumer advertising, prohibitions on promoting drugs for uses or in patient populations that are not described in the drug's approved labeling (known as "off-label use"), and principles governing industry-sponsored scientific and educational activities. Failure to comply with FDA requirements can have negative consequences, including adverse publicity, enforcement letters from the FDA, mandated corrective advertising or communications with doctors or patients, and civil or criminal penalties. Although physicians may prescribe legally available drugs for off-label uses, manufacturers may not market or promote such off-label uses.

Changes to some of the conditions established in an approved application, including changes in indications, labeling, or manufacturing processes or facilities, require submission and FDA approval of a new NDA or NDA supplement before the change can be implemented. An NDA supplement for a new indication typically requires clinical data similar in type and quality to the clinical data supporting the original application for the original indication, and the FDA uses similar procedures and actions in reviewing such NDA supplements as it does in reviewing NDAs.

Adverse event reporting and submission of periodic reports is required following FDA approval of an NDA. The FDA also may require post-marketing testing, known as Phase 4 testing, risk minimization action plans, and surveillance to monitor the effects of an approved product or to place conditions on an approval that restrict the distribution or use of the product.

Outside the U.S., our and our collaborators' abilities to market a product are contingent upon receiving marketing authorization from the appropriate regulatory authorities. The requirements governing marketing authorization, pricing and reimbursement vary widely from jurisdiction to jurisdiction. At present, foreign marketing authorizations are applied for at a national level, although within the E.U. registration procedures are available to companies wishing to market a product in more than one E.U. member state.

18

Employees

As of December 31, 2011, we had 276 employees. Approximately 66 were scientists engaged in discovery research, 117 were in our drug development organization, 16 were in our commercial team, and 77 were in general and administrative functions. None of our employees are represented by a labor union, and we consider our employee relations to be good.

Executive Officers of the Registrant

The following table sets forth the name, age and position of each of our executive officers as of February 15, 2012:

Name

|

Age | Position | |||

|---|---|---|---|---|---|

| Peter M. Hecht, Ph.D. | 48 | Chief Executive Officer, Director | |||

| Michael J. Higgins | 49 | Senior Vice President, Chief Operating Officer and Chief Financial Officer | |||

| Mark G. Currie, Ph.D. | 57 | Senior Vice President, R&D and Chief Scientific Officer | |||

| Thomas A. McCourt | 54 | Senior Vice President, Marketing and Sales and Chief Commercial Officer | |||

Peter M. Hecht has served as our chief executive officer and a director since our founding in 1998. Prior to founding Ironwood, Dr. Hecht was a research fellow at Whitehead Institute for Biomedical Research. Dr. Hecht currently serves on the board of directors of Whitehead Institute. Dr. Hecht earned a B.S. in mathematics and an M.S. in biology from Stanford University, and holds a Ph.D. in molecular biology from the University of California at Berkeley.

Michael J. Higgins has served as our senior vice president, chief operating officer and chief financial officer since joining Ironwood in 2003. Prior to 2003, Mr. Higgins held a variety of senior business positions at Genzyme Corporation, including vice president of corporate finance. Mr. Higgins earned a B.S. from Cornell University and an M.B.A. from the Amos Tuck School of Business Administration at Dartmouth College.

Mark G. Currie serves as our senior vice president of research and development and chief scientific officer, and has led our R&D efforts since joining us in 2002. Prior to joining Ironwood, Dr. Currie directed cardiovascular and central nervous system disease research as vice president of discovery research at Sepracor Inc. Previously, Dr. Currie initiated, built and led discovery pharmacology and also served as director of arthritis and inflammation at Monsanto Company. Dr. Currie earned a B.S. in biology from the University of South Alabama and holds a Ph.D. in cell biology from the Bowman-Gray School of Medicine of Wake Forest University.