Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 001-34129

CENTRAIS ELÉTRICAS BRASILEIRAS S.A. – ELETROBRAS

(exact name of registrant as specified in its charter)

BRAZILIAN ELECTRIC POWER COMPANY

(translation of registrant’s name into English)

Federative Republic of Brazil

(jurisdiction of incorporation or organization)

Avenida Presidente Vargas, 409 – 9th floor, Edifício Herm. Stoltz – Centro, CEP 20071-003, Rio de Janeiro, RJ, Brazil

(address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| American Depositary Shares, evidenced by American Depositary Receipts, each representing one Common Share | New York Stock Exchange | |

| Common Shares, no par value* | New York Stock Exchange | |

| American Depositary Shares, evidenced by American Depositary Receipts, each representing one Class B Preferred Share | New York Stock Exchange | |

| Preferred Shares, no par value* | New York Stock Exchange | |

| * | Not for trading but only in connection with the registration of the American Depositary Shares pursuant to the requirements of the SEC. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None.

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of December 31, 2011 was:

| 1,087,050,297 | Common Shares | |

| 146,920 | Class A Preferred Shares | |

| 265,436,883 | Class B Preferred Shares |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Indicate by checkmark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No x

Indicate by check mark whether the registrant is a large accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12-b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ¨ IFRS x Other ¨

Indicate by check mark which financial statement item the registrant has elected to follow. ¨ Item 17 x Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.). ¨ Yes x No

Table of Contents

| Page | ||||

| ITEM 1. Identity of Directors, Senior Management and Advisers |

7 | |||

| 7 | ||||

| 7 | ||||

| 22 | ||||

| 66 | ||||

| 66 | ||||

| 88 | ||||

| 93 | ||||

| 94 | ||||

| 99 | ||||

| 108 | ||||

| ITEM 11. Quantitative and Qualitative Disclosures About Market risk |

123 | |||

| ITEM 12. Description of Securities Other than Equity Securities |

123 | |||

| 123 | ||||

| 124 | ||||

| ITEM 14. Material Modifications to the Rights of Security Holders and Use of Proceeds |

124 | |||

| 124 | ||||

| 127 | ||||

| 127 | ||||

| 127 | ||||

| 127 | ||||

| ITEM 16D. Exemption from the Listing Standards for Audit Committees |

128 | |||

| ITEM 16E. Purchases of Equity Securities by the Issuer and Affiliated Purchasers |

128 | |||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| 128 | ||||

| 129 | ||||

- i -

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

In this annual report, unless otherwise indicated or the context otherwise requires, all references to “we,” “our,” “ours,” “us” or similar terms refer to Centrais Elétricas Brasileiras S.A. – Eletrobras and its consolidated subsidiaries.

We prepare our consolidated annual financial statements in compliance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

These consolidated financial statements are the second Eletrobras financial statements to be prepared in compliance with IFRS. Until December 31, 2009, our consolidated financial statements were prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). U.S. GAAP differs in certain respects from IFRS. When preparing our 2010 consolidated IFRS financial statements, management has amended certain accounting, valuation and consolidation methods in the U.S. GAAP financial statements to comply with IFRS. Reconciliations and descriptions of the effect of the transition from U.S. GAAP to IFRS are set out in Note 43 to the consolidated financial statements. We have also included a reconciliation of previous Brazilian GAAP to IFRS in Note 43 to our financial statements.

The last consolidated financial statements available under U.S. GAAP which were filed with the United States Securities and Exchange Commission were those for the year ended December 31, 2009.

Beginning in 2011, we adopted certain changes to the presentation of our financial statements in an effort to make the presentation of the financial statements of each company within our group more consistent. Accordingly, we added and deleted a limited number of line items in our balance sheet, income of statement and cash flow statement as of and for the years ended December 31, 2011 and 2010.

As a result of this change in presentation, for the year ended December 31, 2010, R$236 million of current assets were improperly classified as non-current assets. With respect to the income statement, for the year ended December 31, 2010, the subsidy of fuel account (“CCC”) was presented as an other operating expense, but it is now presented as other operating revenue, which resulted in a R$82 million decrease in operating expenses and a corresponding R$82 million increase in operating revenues. In our cash flow statement for the year ended December 31, 2010 and 2009, dividends received were originally classified as investing activities, and, due to the fact that we are a holding company, we now present them as operating activities. This resulted in a R$601 million decrease in investing activities in 2010 and a corresponding R$731 million increase in operating activities in 2009 as permitted by paragraph 14 of IAS 7. No conforming changes to our balance sheet or income statement as of and for the year ended December 31, 2009 were necessary with respect to this change in presentation.

In this annual report, the term “Brazil” refers to the Federative Republic of Brazil and the phrase “Brazilian Government” refers to the federal government of Brazil. The term “Central Bank” refers to the Central Bank. The terms “real” and “reais” and the symbol “R$” refer to the legal currency of Brazil. The terms “U.S. dollar” and “U.S. dollars” and the symbol “U.S.$” refer to the legal currency of the United States of America.

Certain figures in this document have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be an arithmetic aggregation of the figures that precede them.

Terms contained within this annual report have the following meanings:

| • | Eletrobras Amazonas Energia, or Amazonas Energia: Amazonas Energia S.A., a distribution company wholly owned by Eletrobras and operating in the State of Amazonas. Amazonas Energia was formed in 2008 as a result of the merger between Ceam and Manaus Energia S.A.; |

| • | ANDE: Administración Nacional de Electricidad; |

| • | ANEEL: Agência Nacional de Energia Elétrica, the Brazilian Electric Power Agency; |

| • | Average tariff or rate: total sales revenue divided by total MWh sold for each relevant period, including unbilled electricity. Total sales revenue, for the purpose of computing average tariff or rate, includes both gross billings before deducting VAT and other taxes and unbilled electricity sales upon which such taxes have not yet accrued; |

| • | Basic Network: interconnected transmission lines, dams, energy transformers and equipment with voltage equal to or higher than 230 kV, or installations with lower voltage as determined by ANEEL; |

1

Table of Contents

| • | BNDES: Banco Nacional de Desenvolvimento Econômico e Social, the Brazilian Development Bank; |

| • | Brazilian Corporate Law: Collectively, Law No. 6,404 of December 15, 1976, Law No. 9,457 of May 5, 1997 and Law No. 10,303 of October 31, 2001; |

| • | Capacity charge: the charge for purchases or sales based on contracted firm capacity whether or not consumed; |

| • | CCC Account: Conta de Consumo de Combustivel, or Fuel Consumption Account; |

| • | CCEAR: Contratos de Comercialização de Energia no Ambiente Regulado, contracts for the commercialization of energy in the Regulated Market; |

| • | CDE Account: Conta de Desenvolvimento Energetico, the energy development account; |

| • | Ceam: Eletrobras Amazonas Energia, a distribution company that used to operate in the State of Amazonas. In March 2008, Ceam merged with Manaus Energia S.A. The resulting entity is Amazonas Energia S.A.; |

| • | CGE: Câmara de Gestão da Crise de Energia Elétrica, the Brazilian Energy Crisis Management Committee; |

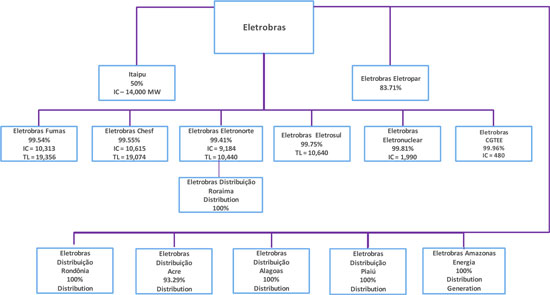

| • | Eletrobras CGTEE, or CGTEE: Companhia de Geração Térmica de Energia Elétrica, a generation subsidiary of Eletrobras; |

| • | CMN: Conselho Monetario Nacional, the highest authority responsible for Brazilian monetary and financial policy; |

| • | CNEN: Comissão Nacional de Energia Nuclear S.A., the Brazilian national commission for nuclear energy; |

| • | CNPE: Conselho Nacional de Política Energética, the advisory agency to the President of the Republic of Brazil for the formulation of policies and guidelines in the Energy sector; |

| • | Concessionaires or concessionaire companies: companies to which the Brazilian Government transfers rights to supply electrical energy services (generation, transmission, distribution) to a particular region in accordance with agreements entered into between the companies and the Brazilian Government pursuant to Law No. 8,987 (dated February 1995) and Law No. 9,074 (the Power Sector Law, dated July 7, 1995) (together, the “Concessions Laws”); |

| • | Distribution: the transfer of electricity from the transmission lines at grid supply points and its delivery to consumers through a distribution system. Electricity reaches consumers such as residential consumers, small industries, commercial properties and public utilities at a voltage of 220/127 volts; |

| • | Distributor: an entity supplying electrical energy to a group of customers by means of a distribution network; |

| • | DNAEE: Departamento National de Águas e Energia Elétrica, the Brazilian national department of water and electrical energy; |

| • | Electricity Regulatory Law: Law No. 10,848 (Lei do Novo Modelo do Setor Elétrico), enacted on March 15, 2004, and which regulates the operations of companies in the electricity industry; |

| • | Eletrobras Distribuição Alagoas, or Distribuição Alagoas: Companhia Energética de Alagoas, a distribution company operating in the State of Alagoas (Ceal); |

| • | Cepel: Centro de Pesquisas de Energia Elétrica, a research center of the Brazilian electric sector; |

| • | Eletrobras: Centrais Elétricas Brasileiras S.A. – Eletrobras; |

2

Table of Contents

| • | Eletrobras Chesf, or Chesf: Companhia Hidro Elétrica do São Francisco, a generation and transmission subsidiary of Eletrobras; |

| • | Eletrobras Distribuição Acre, or Distribuição Acre: Companhia de Eletricidade de Acre, a distribution company operating in the State of Acre (Eletroacre); |

| • | Eletrobras Distribuição Piauí, or Distribuição Piauí: Companhia Energética de Piauí, a distribution company operating in the State of Piauí (Cepisa); |

| • | Eletrobras Distribuição Rondônia, or Distribuição Rondônia: Centrais Elétricas de Rondônia, a distribution company operating in the State of Rondônia (Ceron); |

| • | Eletrobras Distribuição Roraima, or Distribuição Roraima, formally known as Boa Vista Energia S.A., a distribution company operating in the city of Boa Vista, in the State of Roraima; |

| • | Eletrobras Eletronorte, or Eletronorte: Centrais Elétricas do Norte do Brasil S.A., a generation and transmission subsidiary of Eletrobras; |

| • | Eletrobras Eletronuclear, or Eletronuclear: Eletrobras Termonuclear S.A., a generation subsidiary of Eletrobras; |

| • | Eletrobras Eletropar, or Eletropar: Eletrobras Participações S.A., a holding company subsidiary created to hold equity investments (formerly, Light Participações S.A. – LightPar); |

| • | Eletrobras Eletrosul, or Eletrosul: Eletrosul Centrais Elétricas S.A., a generation and transmission subsidiary of Eletrobras; |

| • | Eletrobras Furnas, or Furnas: Furnas Centrais Elétricas S.A., a generation and transmission subsidiary of Eletrobras; |

| • | Energy charge: the variable charge for purchases or sales based on actual electricity consumed; |

| • | Environmental Crimes Act: Law No. 9,605, dated February 12, 1998; |

| • | Final consumer (end user): a party who uses electricity for its own needs; |

| • | FND: Fundo National do Desestatização, the national privatization fund; |

| • | Free consumers: customers that were connected to the system after July 8, 1995 and have a contracted demand above 3 MW at any voltage level; or customers that were connected to the system prior to July 8, 1995 and have a contracted demand above 3 MW at voltage level higher than or equal to 69 kV; |

| • | Gigawatt ( GW): one billion watts; |

| • | Gigawatt hour ( GWh): one gigawatt of power supplied or demanded for one hour, or one billion watt hours; |

| • | High voltage: a class of nominal system voltages equal to or greater than 100,000 volts (100 kVs) and less than 230,000 volts (230 kVs); |

| • | Hydroelectric plant or hydroelectric facility or hydroelectric power unity (HPU): a generating unit that uses water power to drive the electric generator; |

| • | IGP-M: Indice Geral de Precos-Mercado, the Brazilian general market price index, similar to the retail price index; |

| • | INB: Indústrias Nucleares Brasileiras, a Brazilian Government-owned company responsible for processing uranium used as power to provide electricity at Angra I and Angra II Nuclear Plants; |

| • | Installed capacity: the level of electricity which can be delivered from a particular generating unit on a full-load continuous basis under specified conditions as designated by the manufacturer; |

3

Table of Contents

| • | Interconnected Power System: systems or networks for the transmission of energy, connected together by means of one or more links (lines and/or transformers); |

| • | Isolated system: generation facilities in the North of Brazil not connected to the national transmission grid; |

| • | Itaipu: Itaipu Binacional, the hydroelectric generation facility owned equally by Brazil and Paraguay; |

| • | Kilowatt (kW): 1,000 watts; |

| • | Kilowatt Hour (kWh): one kilowatt of power supplied or demanded for one hour; |

| • | Kilovolt (kV): one thousand volts; |

| • | Megawatt (MW): one million watts; |

| • | Megawatt hour (MWh): one megawatt of power supplied or demanded for one hour, or one million watt hours; |

| • | Mixed capital company: pursuant to Brazilian Law No. 6,404 of December 15, 1976, a company with public and private sector shareholders, but controlled by the public sector; |

| • | MME: Ministério de Minas e Energia, the Brazilian Ministry of Mines and Energy; |

| • | MRE: Mercado Regulado de Energia, the Brazilian Energy Regulated Market; |

| • | National Environmental Policy Act: Law No. 6,938, dated August 31, 1981; |

| • | Northeast region: the States of Alagoas, Bahia, Ceará, Maranhão, Paraíba, Pernambuco, Piauí, Rio Grande do Norte and Sergipe; |

| • | ONS: Operador Nacional do Sistema, the national system operator; |

| • | Power Sector Law: Law No. 9,074 of July 7, 1997; |

| • | Procel: Programa Nacional de Combate ao Desperdício de Energia Elétrica, the national electrical energy conservation program; |

| • | Proinfa: Programa de Incentivo as Fontes Alternativas de Energia, the program for incentives to develop alternative energy sources; |

| • | RGR Fund: Reserva Global de Reversão, a fund we administer, funded by consumers and providing compensation to all concessionaires for non-renewal or expropriation of their concessions used as source of funds for the expansion and improvement of the electrical energy sector; |

| • | Selic rate: an official overnight government rate applied to funds traded through the purchase and sale of public debt securities established by the special system for custody and settlement; |

| • | Small Hydroelectric Power Plants: power plants with capacity from 1 MW to 30 MW; |

| • | Substation: an assemblage of equipment which switches and/or changes or regulates the voltage of electricity in a transmission and distribution system; |

| • | TFSEE: Taxa de Fiscalização de Serviços de Energia Elétrica, the fee for the supervision of electricity energy services; |

| • | Thermoelectric plant or thermoelectric power unity (TPU): a generating unit which uses combustible fuel, such as coal, oil, diesel natural gas or other hydrocarbon as the source of energy to drive the electric generator; |

4

Table of Contents

| • | Transmission: the bulk transfer of electricity from generating facilities to the distribution system at load center station by means of the transmission grid (in lines with capacity between 69 kV and 525 kV); |

| • | TWh: Terawatt hour (1,000 Gigawatt hours); |

| • | UBP Fund: Fundo de Uso de Bem Publico, the public asset use fund; |

| • | U.S. GAAP: generally accepted accounting principles in the United States; |

| • | Volt (V): the basic unit of electric force analogous to water pressure in pounds per square inch; and |

| • | Watt: the basic unit of electrical power. |

5

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This annual report includes certain forward-looking statements, including statements regarding our intent, belief or current expectations or those of our officers with respect to, among other things, our financing plans, trends affecting our financial condition or results of operations and the impact of future plans and strategies. These forward-looking statements are subject to risks, uncertainties and contingencies including, but not limited to, the following:

| • | general economic, regulatory, political and business conditions in Brazil and abroad; |

| • | interest rate fluctuations, inflation and the value of the real in relation to the U.S. dollar; |

| • | changes in volumes and patterns of customer electricity usage; |

| • | competitive conditions in Brazil’s electricity generation, transmission and distribution markets; |

| • | the effects of competition; |

| • | our level of debt; |

| • | the likelihood that we will receive payment in connection with account receivables; |

| • | changes in rainfall and the water levels in the reservoirs used to run our hydroelectric power generation facilities; |

| • | our financing and capital expenditure plans; |

| • | our ability to serve our customers on a satisfactory basis; |

| • | existing and future governmental regulation as to electricity rates, electricity usage, competition in our concession area and other matters; |

| • | our ability to execute our business strategy, including our growth strategy; |

| • | adoption of measures by the granting authorities in connection with our concession agreements; |

| • | changes in other laws and regulations, including, among others, those affecting tax and environmental matters; |

| • | future actions that may be taken by the Brazilian Government, our controlling shareholder; |

| • | the outcome of our tax, civil and other legal proceedings; and |

| • | other risk factors as set forth under “Item 3.D, Risk Factors.” |

The forward-looking statements referred to above also include information with respect to our capacity expansion projects that are in the planning and development stages. In addition to the above risks and uncertainties, our potential expansion projects involve engineering, construction, regulatory and other significant risks, which may:

| • | delay or prevent successful completion of one or more projects; |

| • | increase the costs of projects; and |

| • | result in the failure of facilities to operate or generate income in accordance with our expectations. |

The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect” and similar words are intended to identify forward-looking statements. We undertake no obligation to update publicly or revise any forward-looking statements as a result of new information, future events or otherwise. In light of these risks and uncertainties, the forward-looking information, events and circumstances discussed in this annual report might not occur. Our actual results and performance could differ substantially from those anticipated in our forward-looking statements.

6

Table of Contents

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

Background

The selected financial information presented herein should be read in conjunction with our financial statements and related notes, which appear elsewhere in this annual report.

The following paragraphs discuss some important features of the presentation of the selected financial information and our financial statements. These features should be considered when evaluating the selected financial information.

A. Selected Financial Data

Consolidated Balance Sheet Information

| As of December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (R$ thousands) | ||||||||||||

| Assets |

||||||||||||

| Current |

||||||||||||

| Cash and cash equivalents |

4,959,787 | 9,220,169 | 8,617,294 | |||||||||

| Restricted cash |

3,034,638 | 2,058,218 | 1,341,719 | |||||||||

| Marketable securities |

11,252,504 | 6,774,073 | 7,662,640 | |||||||||

| Accounts Receivable |

4,352,024 | 3,779,930 | 3,102,079 | |||||||||

| Financial asset of concession agreements |

2,017,949 | 1,723,522 | 1,570,376 | |||||||||

| Loans and financings |

2,082,054 | 1,359,269 | 1,926,193 | |||||||||

| Fuel consumption account – CCC |

1,184,936 | 1,428,256 | 877,833 | |||||||||

| Investment remuneration |

197,863 | 178,604 | 78,726 | |||||||||

| Taxes recoverable |

1,947,344 | 1,825,905 | 1,326,933 | |||||||||

| Reimbursement rights |

3,083,157 | 1,704,239 | 221,519 | |||||||||

| Warehouse (storeroom) |

358,724 | 378,637 | 350,470 | |||||||||

| Stock of nuclear fuel |

388,663 | 297,972 | 324,634 | |||||||||

| Prepaid expenses |

46,322 | 40,418 | 58,765 | |||||||||

| Financial instruments |

195,536 | 283,220 | 227,540 | |||||||||

| Other |

1,561,171 | 1,517,439 | 1,114,505 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total current assets |

36,662,672 | 32,569,871 | 28,801,226 | |||||||||

| Non-current |

||||||||||||

| Long term assets |

||||||||||||

| Reimbursement rights |

500,333 | 371,599 | 99,178 | |||||||||

| Loans and financings |

7,651,336 | 8,300,171 | 9,839,828 | |||||||||

| Accounts receivable |

1,478,994 | 1,706,292 | 1,431,080 | |||||||||

| Marketable securities |

398,358 | 769,905 | 687,188 | |||||||||

| Stock of nuclear fuel |

435,633 | 523,957 | 755,434 | |||||||||

| Deferred tax assets |

5,774,286 | 4,338,682 | 4,493,223 | |||||||||

| Judicial deposit |

2,316,324 | 1,750,678 | 1,521,317 | |||||||||

| Fuel consumption account – CCC |

727,136 | 785,327 | 1,173,580 | |||||||||

| Financial asset of concession of agreements |

46,149,379 | 40,643,712 | ||||||||||

| Financial instruments |

185,031 | 297,020 | 228,020 | |||||||||

| Advances for future capital increase |

4,000 | 7,141 | ||||||||||

| Other |

701,763 | 1,165,529 | 666,967 | |||||||||

|

|

|

|

|

|

|

|||||||

| 66,322,573 | 60,660,013 | 59,996,755 | ||||||||||

| Investments |

4,570,959 | 4,724,647 | 5,288,107 | |||||||||

| Property, plant and equipment |

53,214,861 | 46,682,498 | 41,597,605 | |||||||||

| Intangible assets |

2,371,367 | 2,263,972 | 2,024,683 | |||||||||

| Total non-current assets |

126,479,760 | 53,671,117 | 48,910,395 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total assets |

163,142,432 | 146,901,001 | 137,708,376 | |||||||||

|

|

|

|

|

|

|

|||||||

7

Table of Contents

| As of December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (R$ thousands) | ||||||||||||

| Liabilities and shareholders’ equity |

||||||||||||

| Current |

||||||||||||

| Borrowings |

4,005,326 | 1,868,465 | 1,115,274 | |||||||||

| Debentures |

739,237 | — | — | |||||||||

| Compulsory loan |

16,331 | 16,925 | 13,675 | |||||||||

| Suppliers |

6,338,102 | 5,165,765 | 3,079,614 | |||||||||

| Advances from clients |

413,041 | 341,462 | 63,400 | |||||||||

| Taxes and social contributions |

1,032,521 | 1,102,672 | 963,365 | |||||||||

| Fuel consumption account – CCC |

3,079,796 | 2,579,546 | 923,535 | |||||||||

| Shareholders’ remuneration |

4,373,773 | 3,424,520 | 3,214,450 | |||||||||

| National Treasury Credits |

109,050 | 92,770 | 76,036 | |||||||||

| Estimated liabilities |

802,864 | 772,071 | 672,214 | |||||||||

| Reimbursement Obligations |

1,955,966 | 759,214 | 857,001 | |||||||||

| Complementary pension plans |

451,801 | 330,828 | 351,149 | |||||||||

| Provision for contingencies |

240,190 | 257,580 | 252,708 | |||||||||

| Regulatory fees |

901,692 | 584,240 | 589,433 | |||||||||

| Leasing |

142,997 | 120,485 | 108,827 | |||||||||

| Concessions payable |

35,233 | 25,098 | — | |||||||||

| Derivative financial instruments |

269,718 | 237,209 | 40,050 | |||||||||

| Personnel voluntary dismissal |

93,137 | — | — | |||||||||

| Research and development |

274,722 | 219,538 | 240,684 | |||||||||

| Profit sharing |

296,547 | 227,563 | 194,752 | |||||||||

|

|

|

|

|

|

|

|||||||

| Other |

552,765 | 243,560 | 513,680 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total current liabilities |

26,124,809 | 18,369,511 | 13,269,847 | |||||||||

| Non-current |

||||||||||||

| Borrowings |

38,408,352 | 31,269,971 | 28,392,542 | |||||||||

| National Treasury credits |

155,676 | 250,485 | 311,306 | |||||||||

| Debentures |

279,410 | 710,536 | — | |||||||||

| Advances from clients |

879,452 | 928,653 | 978,980 | |||||||||

| Compulsory loan |

211,554 | 141,425 | 127,358 | |||||||||

| Decommission obligations |

408,712 | 375,968 | 323,326 | |||||||||

| Fuel consumption account – CCC |

954,013 | 785,327 | 1,344,380 | |||||||||

| Provision for contingencies |

4,652,176 | 3,901,289 | 3,528,917 | |||||||||

| Complementary pension plans |

2,256,132 | 2,066,702 | 1,992,012 | |||||||||

| Reimbursement obligations |

1,475,262 | 1,091,271 | 435,548 | |||||||||

| Leasing |

1,775,544 | 1,694,547 | 1,639,448 | |||||||||

| Shareholders’ remuneration |

3,143,222 | 5,601,077 | 7,697,579 | |||||||||

| Concessions payable |

1,234,426 | 1,089,726 | 761,131 | |||||||||

| Advances for future capital increase |

148,695 | 5,173,856 | 4,712,825 | |||||||||

| Derivative financial instruments |

197,965 | 303,331 | 228,020 | |||||||||

| Personnel voluntary dismissal |

726,291 | 273,671 | 259,220 | |||||||||

| Research and development |

370,714 | 284,820 | 261,909 | |||||||||

| Taxes and social contributions |

1,902,522 | 1,217,649 | 1,273,890 | |||||||||

| Other |

635,184 | 840,776 | 791,091 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total non-current liabilities |

59,815,302 | 58,001,080 | 55,059,480 | |||||||||

| Shareholders’ equity |

||||||||||||

| Share capital |

31,305,331 | 26,156,567 | 26,156,567 | |||||||||

| Capital reserves |

26,048,342 | 26,048,342 | 26,048,342 | |||||||||

| Profit reserves |

18,571,011 | 17,329,661 | 15,663,924 | |||||||||

| Asset valuation adjustment |

220,915 | 163,335 | 179,427 | |||||||||

| Additional Proposed Dividend |

706,018 | 753,201 | 370,755 | |||||||||

| Other comprehensive income |

(8,108 | ) | (146,992 | ) | 827,491 | |||||||

| Non-controlling shareholders’ interest |

358,812 | 226,296 | 132,543 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total shareholders’ equity |

77,202,321 | 70,530,410 | 69,379,050 | |||||||||

| Total liabilities and shareholders’ equity |

163,142,432 | 146,901,001 | 137,708,376 | |||||||||

|

|

|

|

|

|

|

|||||||

8

Table of Contents

Consolidated Income Statement

| For the year ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| (R$ thousands) | ||||||||||||

| Net operating revenue |

29,532,744 | 26,832,085 | 23,140,905 | |||||||||

| Operating expenses |

||||||||||||

| Personnel, supplies and services |

7,670,716 | 7,370,713 | 6,486,218 | |||||||||

| Profit sharing for employees and management |

317,035 | 296,270 | 284,534 | |||||||||

| Electricity purchased for reselling |

3,386,289 | 4,315,084 | 3,581,396 | |||||||||

| Fuel for electricity production |

162,673 | 252,502 | 756,285 | |||||||||

| Use of the grid |

1,420,934 | 1,353,839 | 1,263,408 | |||||||||

| Remuneration and reimbursement |

1,328,994 | 1,087,341 | 1,188,032 | |||||||||

| Depreciation and amortization |

1,723,885 | 1,592,476 | 1,624,246 | |||||||||

| Construction |

4,279,608 | 2,953,484 | 1,723,960 | |||||||||

| Operating provisions |

2,848,749 | 2,497,262 | 2,140,406 | |||||||||

| Itaipu’s income to offset |

655,290 | 441,057 | 669,675 | |||||||||

| Donations and contributions |

289,964 | 261,006 | 237,978 | |||||||||

| Other |

1,305,765 | 669,434 | 704,449 | |||||||||

|

|

|

|

|

|

|

|||||||

| 25,389,902 | 23,090,468 | 20,660,585 | ||||||||||

| Operating result before financial result |

4,142,842 | 3,741,617 | 2,480,320 | |||||||||

| Financial result |

||||||||||||

| Financial revenue |

||||||||||||

| Revenue from interest, commissions and fees |

757,450 | 781,872 | 1,035,487 | |||||||||

| Revenue from financial investments |

1,664,517 | 1,537,435 | 1,464,782 | |||||||||

| Arrears surcharge on electricity |

359,208 | 393,987 | 228,145 | |||||||||

| Monetary restatement |

652,949 | 616,141 | 356,023 | |||||||||

| Exchange rate variation gain |

669,731 | — | — | |||||||||

| Other financial revenues |

158,471 | 394,890 | 736,766 | |||||||||

| Financial expenses |

||||||||||||

| Debt charges |

(1,708,670 | ) | (1,675,821 | ) | (1,758,473 | ) | ||||||

| Leasing charges |

(350,861 | ) | (332,449 | ) | (213,470 | ) | ||||||

| Charges on shareholders’ resources |

(1,178,989 | ) | (1,298,647 | ) | (1,468,713 | ) | ||||||

| Exchange rate variation loss |

— | (431,497 | ) | (4,018,643 | ) | |||||||

| Other financial expenses |

(789,353 | ) | (350,033 | ) | — | |||||||

|

|

|

|

|

|||||||||

| 234,453 | (364,122 | ) | (3,638,097 | ) | ||||||||

| Result/loss before participation in associates and other investments |

4,377,295 | 3,377,495 | (1,157,777 | ) | ||||||||

|

|

|

|

|

|

|

|||||||

| Result of participation in associates and other investments |

482,785 | 669,755 | 1,571,032 | |||||||||

|

|

|

|

|

|

|

|||||||

| Income before income tax and social contribution |

4,860,080 | 4,047,250 | 413,255 | |||||||||

|

|

|

|

|

|

|

|||||||

| Income tax |

(796,252 | ) | (1,074,606 | ) | 635,875 | |||||||

| Social contribution on net income |

(301,809 | ) | (419,659 | ) | 201,010 | |||||||

|

|

|

|

|

|

|

|||||||

| Net income for the year |

3,762,019 | 2,552,985 | 1,250,140 | |||||||||

|

|

|

|

|

|

|

|||||||

| Attributable to controlling shareholders |

3,732,565 | 2,247,913 | 911,467 | |||||||||

| Attributable to non-controlling shareholders |

29,454 | 305,072 | 338,673 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net earning per share |

R$ | 2.78 | R$ | 2.25 | R$ | 1.10 | ||||||

|

|

|

|

|

|

|

|||||||

Brazilian Corporate Law and our by-laws provide that we must pay our shareholders mandatory dividends equal to at least 25% of our adjusted net income for the preceding fiscal year. In addition, our by-laws require us to give: (i) class “A” preferred shares a priority in the distribution of dividends, at 8% each year over the capital linked to those shares; and (ii) class “B” preferred shares that were issued on or after June 23, 1969 a priority in the distribution of dividends, at 6% each year over the capital linked to those shares. In addition, preferred shares must receive a dividend 10% over the dividend paid to the common shares.

9

Table of Contents

The following table sets out our declared dividends for the periods indicated:

| Year | ||||||||||||

| 2011(1) | 2010(1) | 2009(1) | ||||||||||

| (R$) | ||||||||||||

| Common Shares |

1.23 | 0.83 | 0.41 | |||||||||

| Class A Preferred Shares |

2.17 | 2.17 | 2.17 | |||||||||

| Class B Preferred Shares |

1.63 | 1.63 | 1.63 | |||||||||

| (1) | Interest on own capital. |

The following table sets forth a summary of dividends/interest on own capital declared per share for the periods presented, both at the time declared and as adjusted for our 500:1 reverse stock split effected in 2007.

Dividend per Share

| Declared | Paid(2) | |||||||||||||||||||||||||||||||

| On 12/31/2007 | Equivalent on 08/20/2007(1) | On 06/15/2008 | Equivalent on 08/20/2007(1) | |||||||||||||||||||||||||||||

| R$ | U.S.$ | R$ | U.S.$ | R$ | U.S.$ | R$ | U.S.$ | |||||||||||||||||||||||||

| Common |

0.40155520020 | 0.22670084130 | 0.40155520020 | 0.22670084130 | 0.41587767968 | 0.24648985282 | 0.41587767968 | 0.24648985282 | ||||||||||||||||||||||||

| Preferred A |

2.01949731106 | 1.14012155539 | 2.01949731106 | 1.14012155539 | 2.09152777855 | 1.23964424997 | 2.09152777855 | 1.23964424997 | ||||||||||||||||||||||||

| Preferred B |

1.51462298231 | 0.85509116599 | 1.51462298231 | 0.85509116599 | 1.56864583289 | 0.92973318687 | 1.56864583289 | 0.92973318687 | ||||||||||||||||||||||||

| Declared | Paid(2) | |||||||||||||||||||||||||||||||

| On 12/31/2008 | Equivalent on 08/20/2007(1) | On 04/30/2009(3) | Equivalent on 08/20/2007(1) | |||||||||||||||||||||||||||||

| R$ | U.S.$ | R$ | U.S.$ | R$ | U.S.$ | R$ | U.S.$ | |||||||||||||||||||||||||

| Common |

1.484883733 | 0.635380288 | 1.484883733 | 0.635380288 | 1.548692924 | 0.662684178 | 1.548692924 | 0.662684178 | ||||||||||||||||||||||||

| Preferred A |

2.174044374 | 0.930271448 | 2.174044374 | 0.930271448 | 2.267468532 | 0.970247553 | 2.267468532 | 0.970247553 | ||||||||||||||||||||||||

| Preferred B |

1.630533280 | 0.697703586 | 1.630533280 | 0.697703586 | 1.703562217 | 0.728952596 | 1.703562217 | 0.728952596 | ||||||||||||||||||||||||

| Declared | Paid | Declared | Paid | |||||||||||||||||||||||||||||

| On 12/31/2009 | On 05/18/2010 | On 12/31/2010 | On 06/29/2011 | |||||||||||||||||||||||||||||

| R$ | U.S.$ | R$ | U.S.$ | R$ | U.S.$ | R$ | U.S.$ | |||||||||||||||||||||||||

| Common |

0.4096631540 | 0.713305484 | 1.548692924 | 0.662684178 | 0.832245170 | 1.386686902 | 0.877358220 | 1.380084480 | ||||||||||||||||||||||||

| Preferred A |

2.1740443750 | 3.785446066 | 2.267468532 | 0.970247553 | 2.174043683 | 3.622391585 | 2.291890859 | 3.605144321 | ||||||||||||||||||||||||

| Preferred B |

1.6305332814 | 2.839084549 | 1.703562217 | 0.728952596 | 1.630533280 | 2.716794551 | 1.718918690 | 2.703859099 | ||||||||||||||||||||||||

| Declared(4) | ||||||||

| On 12/31/2011 | ||||||||

| R$ | U.S.$ | |||||||

| Common |

1.231779162 | 2.310571353 | ||||||

| Preferred A |

2.178256581 | 4.085973695 | ||||||

| Preferred B |

1.633692440 | 3.064480279 | ||||||

| (1) | Adjusted to reflect the reverse stock split. |

| (2) | Adjusted by Selic rate variation. |

| (3) | General Stockholders Meeting. |

| (4) | Expected to be paid in June 2012, pursuant to the Management Proposal filed with the CVM. |

Exchange Controls and Foreign Exchange Rates

The Brazilian foreign exchange system allows the purchase and sale of foreign currency and the international transfer of reais by any person or legal entity, regardless of the amount, subject to certain regulatory procedures.

Since 1999, the Central Bank has allowed the real/U.S. dollar exchange rate to float freely, and since then, the real/U.S. dollar exchange rate has fluctuated considerably. Until early 2003, the value of the real declined relative to the U.S. dollar and then began to stabilize. The real appreciated against the U.S. dollar in 2004-2007. In 2008, as a result of the worsening of the global financial and economic crisis the real depreciated 31.9% against the U.S. dollar, and on December 31, 2008 the exchange rate of the real in relation to the U.S. dollar was R$2.34 per U.S.$1.00. In 2009, the real appreciated 25.5% against the U.S. dollar, due to improved economic conditions in Brazil. In 2010, the real appreciated 4.3% against the U.S. dollar. In 2011, the real depreciated 13.62% against the U.S. dollar. In the past, the Central Bank has intervened occasionally to control instability

10

Table of Contents

in foreign exchange rates. We cannot predict whether the Central Bank or the Brazilian Government will continue to allow the real to float freely or will intervene in the exchange rate market through a currency band system or otherwise. We cannot assure that the real will not depreciate substantially or continue to appreciate against the U.S. dollar in the near future.

The following table sets forth the period end, average, high and low selling rates published by the Central Bank expressed in reais per U.S.$ for the periods and dates indicated.

| Reais per U.S. Dollar | ||||||||||||||||

| Year Ended |

Period-end | Average(1) | Low | High | ||||||||||||

| December 31, 2007 |

1.7713 | 1.9483 | 1.7325 | 2.1556 | ||||||||||||

| December 31, 2008 |

2.3370 | 1.8374 | 1.5593 | 2.5004 | ||||||||||||

| December 31, 2009 |

1.7412 | 1.9905 | 1.7024 | 2.4218 | ||||||||||||

| December 31, 2010 |

1.6662 | 1.7593 | 1.6554 | 1.8811 | ||||||||||||

| December 31, 2011 |

1.8758 | 1.6746 | 1.5345 | 1.9016 | ||||||||||||

| (1) | Represents the average of month-end rates beginning with December of the previous period through last month of period indicated. |

The following table sets forth the period end, high and low commercial market/foreign exchange market selling rates published by the Central Bank expressed in reais per U.S.$ for the periods and dates indicated.

| Reais per U.S. Dollar | ||||||||||||||||

| Month |

Period-end | Average | Low | High | ||||||||||||

| November 2011 |

1.8109 | 1.7905 | 1.7270 | 1.8937 | ||||||||||||

| December 2011 |

1.8758 | 1.8369 | 1.7830 | 1.8758 | ||||||||||||

| January 2012 |

1.7391 | 1.7897 | 1.7389 | 1.8683 | ||||||||||||

| February 2012 |

1.7092 | 1.7184 | 1.7024 | 1.7376 | ||||||||||||

| March 2012 |

1.8221 | 1.7953 | 1.7152 | 1.8267 | ||||||||||||

| April 2012 |

1.8918 | 1.8548 | 1.8256 | 1.8918 | ||||||||||||

| May 2012 (through May 10, 2012) |

1.9581 | 1.9347 | 1.9149 | 1.9581 | ||||||||||||

Brazilian law provides that, whenever there is a serious imbalance in Brazil’s balance of payments or there are serious reasons to foresee a serious imbalance, temporary restrictions may be imposed on remittances of foreign capital abroad. We cannot assure you that such measures will not be taken by the Brazilian Government in the future. See “Item 3.D, Risk Factors – Risks Relating to Brazil.”

We currently maintain our financial books and records in reais. For ease of presentation, however, certain consolidated financial information contained in this annual report has been presented in U.S. dollars. See “Item 8, Financial Information.”

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Risks Relating to our Company

Some of our concessions are due to expire in 2015 and renewal of these concessions is not guaranteed; if we are unable to renew those concessions our results of operations would be materially adversely affected.

We carry out our generation, transmission and distribution activities pursuant to concession agreements entered into with the Brazilian Government through ANEEL. These concessions range in duration from 20 to 35 years. Our concession agreements with the earliest expiration dates are due to expire in 2015 and have already been renewed once (see “Item 4.B, Business Overview – Generation – Concessions”), with the exception of our concession agreement for Corumbá I, which expires in November 2014 and has not been previously renewed. Our concession agreement for Itumbiara, which expires in February 2020, and Corumbá I have contractual provisions allowing renewal of the concession since they have not been previously renewed. On May 10, 2011, ANEEL dismissed our request for extension of the concession period for our Xingó plant, and as of December 31, 2011 there has been no update as to this request. Eletrobras Furnas requested the renewal for a period of twenty-nine years of Serra da Mesa three years ago in accordance with the

11

Table of Contents

timeframe established by law. ANEEL has completed its review of this process and has issued a recommendation to the MME in favor of the renewal of the Serra da Mesa concession. As of the date of this report, we were awaiting approval from the MME. In our generation business, concessions expiring in 2015 or before represent approximately 31% of our total installed capacity as of December 31, 2011, and 87% and 38% of the installed capacity of our subsidiaries Eletrobras Chesf and Eletrobras Furnas, respectively. For a further discussion of Eletrobras Chesf and Eletrobras Furnas, see “Item 4.C, Organizational Structure.” Presently, Law No. 10.848 of 2004 only permits concessions to be renewed once. However, we formed working groups in 2010, which are currently examining proposals to amend this law. If the law is not amended, we would be unable to renew certain concessions and would have to take part in auctions for these concessions again. If we are unable to renew any of our concessions and were unable to successfully bid for the concessions in any of the auctions for these concessions, we would lose the business derived from these concessions, which would adversely affect our financial condition and results of operations.

We are controlled by the Brazilian Government, the current policies and priorities of which directly affect our operations and may conflict with interests of our investors.

The Brazilian Government, as our controlling shareholder, has pursued (and may continue to pursue) some of its macroeconomic and social objectives through us using principally Brazilian Government funds, which we administer. These funds are the RGR Fund, the CCC Account and the CDE Account.

The Brazilian Government also has the power to appoint eight out of the 10 members of our Conselho de Administração (or Board of Directors) and, through them, a majority of the executive officers responsible for our day-to-day management. Additionally, the Brazilian Government currently holds the majority of our voting shares. Consequently, the Brazilian Government has the majority of votes at our shareholders’ meetings, which empowers it to approve most matters prescribed by law, including the following: (i) the partial or total sale of the shares of our subsidiaries; (ii) increase of our capital stock through a subscription of new shares; (iii) our dividend distribution policy, as long as it complies with the minimum dividend distribution regulated by law; (iv) issuances of securities in the domestic market and internationally; (v) corporate spin-offs and mergers; (vi) swaps of our shares or other securities; and (vii) the redemption of different classes of our shares, independent from approval by holders of the shares and classes that are subject to redemption. Our operations impact the commercial, industrial and social development promoted by the Brazilian Government. The Brazilian Government has in the past and may in the future require us to make investments, incur costs or engage in transactions (which may include, for example, requiring us to make acquisitions) that may not be consistent with our objective of maximizing our profits.

We are subject to rules limiting borrowing by public sector companies and may not be able to obtain sufficient funds to complete our proposed capital expenditure programs.

Our current budget anticipates capital expenditures of approximately R$13.3 billion in 2012. We cannot assure you that we will be able to finance our proposed capital expenditure programs from either our cash flow or external resources. Moreover, as a state controlled company, we are subject to certain rules limiting our indebtedness and investments and must submit our proposed annual budgets, including estimates of the amounts of our financing requirements and sources of our financing, to the Ministry of Planning, Budget and Management and the Brazilian Congress for approval. Thus, if our operations do not fall within the parameters and conditions established by such rules and the Brazilian Government, we may have difficulty in obtaining the necessary financing authorizations, which could create difficulties in raising funds. If we are unable to obtain such funds, our ability to invest in capital expenditures for expansion and maintenance may be adversely impacted, which would materially adversely affect the execution of our growth strategy, particularly large scale projects such as the construction of the new nuclear plant, Angra III, the development of the Belo Monte hydroelectric complex and the continuing construction of the Jirau and Santo Antônio hydroelectric plants.

We own a number of subsidiaries whose performance significantly influences our results.

We conduct our business mainly through our operating subsidiaries, including Eletrobras Eletronorte, Eletrobras CGTEE, Eletrobras Eletronuclear, Eletrobras Chesf, Eletrobras Furnas and Eletrobras Eletrosul and through Itaipu. Our ability to meet our financial obligations is therefore related in part to the cash flow and earnings of those subsidiaries and the distribution or other transfer of those earnings to us in the form of dividends, loans or other advances and payment. Some of our subsidiaries are, or may in the future be, subject to loan agreements that require that any indebtedness of these subsidiaries to us be subordinate to the indebtedness under those loan agreements. Our subsidiaries are separate legal entities. Any right we may have to receive assets of any subsidiary or other payments upon its liquidation or reorganization will be effectively subordinated to the claims

12

Table of Contents

of that subsidiary’s creditors (including tax authorities, trade creditors and lenders to such subsidiaries), except to the extent that we are a creditor of that subsidiary, in which case our claims would still be subordinated to any security interest in the assets of that subsidiary and indebtedness of that subsidiary senior to that held by us.

The amounts we receive from the Fuel Consumption Account may decrease.

The Brazilian Government introduced the Fuel Consumption Account, or CCC Account, in 1973. The purpose of the CCC Account is to generate financial reserves payable to distribution companies and some generation companies (all of which must make annual contributions to the CCC Account) to cover some of the costs of the operation of thermoelectric plants in the event of adverse hydrological conditions. Although the Brazilian Government has announced that the CCC Account is to be gradually phased out, we (together with other companies in our industry) continue to receive reimbursements from that account. In recent periods, the amounts we have received as reimbursements from the CCC Account have exceeded our contributions to that account. However, we cannot assure you that we will continue to receive reimbursements from the CCC Account (in amounts that exceed our contributions or at all), and any decrease in the amounts we receive may materially adversely affect our financial condition and results of operations.

If any of our assets were deemed assets dedicated to providing an essential public service, they would not be available for liquidation in the event of our bankruptcy and could not be subject to attachment to secure a judgment.

On February 9, 2005, the Brazilian Government enacted Law No. 11,101, or the New Bankruptcy Law. The New Bankruptcy Law, which came into effect on June 9, 2005, governs judicial recovery, extrajudicial recovery and liquidation proceedings and replaces the debt reorganization judicial proceeding known as concordata (reorganization) for judicial recovery and extrajudicial recovery. The New Bankruptcy Law provides that its provisions do not apply to government owned and mixed capital companies (such as Eletrobras). However, the Brazilian Federal Constitution establishes that mixed capital companies, such as Eletrobras, which operate a commercial business, will be subject to the legal regime applicable to private corporations in respect of civil, commercial, labor and tax matters. Accordingly it is unclear whether or not the provisions relating to judicial and extrajudicial recovery and liquidation proceedings of the New Bankruptcy Law would apply to us. For a further description about the New Bankruptcy Law, please see “Item 4.B, Business Overview – The Effects of the New Bankruptcy Law on Us.”

We believe that a substantial portion of our assets, including our generation assets, our transmission network and our limited distribution network, would be deemed by Brazilian courts to be related to providing an essential public service. Accordingly, these assets would not be available for liquidation in the event of our bankruptcy or available for attachment to secure a judgment. In either case, these assets would revert to the Brazilian Government pursuant to Brazilian law and the terms of our concession agreements. Although the Brazilian Government would in such circumstances be under an obligation to compensate us in respect of the reversion of these assets, we cannot assure you that the level of compensation received would be equal to the market value of the assets and, accordingly, our financial condition and results of operations may be affected.

We may be liable for damages, subject to further regulation and have difficulty obtaining financing if there is a nuclear accident involving our subsidiary Eletrobras Eletronuclear.

Our subsidiary Eletrobras Eletronuclear, as an operator of two nuclear power plants, is subject to strict liability under Brazilian law for damages in the event of a nuclear accident. The Vienna Convention on Civil Liability for Nuclear Accidents (or the Vienna Convention) became binding in Brazil in 1993. The Vienna Convention provides that an operator of a nuclear installation, such as Eletrobras Eletronuclear, in a jurisdiction which has adopted legislation implementing the Vienna Convention, will be strictly liable for damages in the event of a nuclear accident (except as covered by insurance). Eletrobras Eletronuclear is regulated by several federal and state agencies. As of December 31, 2011, Eletrobras Eletronuclear’s Angra I and Angra II plants were insured for an aggregate amount of U.S.$307 million in the event of a nuclear accident (see “Item 4.B, Business Overview – Generation – Nuclear Plants”). In addition to the liability for damages in the event of a nuclear accident, Eletrobras Eletronuclear has acquired insurance to cover operational risks due to potential equipment failure, in the amount of U.S.$426 million for each unit. We cannot assure that this coverage will be sufficient in the event of a nuclear accident. Accordingly, any nuclear accident may have a material adverse effect on our financial condition and results of operations.

The incident at the Fukushima Dai-ichi Nuclear Power Plant in Japan in March 2011 and Germany’s subsequent announcement in May 2011 that it will no longer rely on nuclear power by the year 2022 could lead to more

13

Table of Contents

stringent safety regulations of nuclear power plants and a trend toward reliance on non-nuclear power. If global public sentiment continues to favor tougher regulations for nuclear power or a trend towards non-nuclear power, our ability to finance and profitably expand our nuclear power operations could be materially adversely affected.

We do not have alternative supply sources for the key raw materials that our thermal and nuclear plants use.

Our thermal plants operate on coal and/or oil and our nuclear plants operate on processed uranium. In each case, we are entirely dependent on third parties for the provision of these raw materials. In the event that supplies of these raw materials become unavailable for any reason, we do not have alternative supply sources and, therefore, the ability of our thermal and/or nuclear plants, as applicable, to generate electricity would be materially adversely affected, which may materially adversely affect our financial condition and results of operations.

Our distribution companies operate under challenging market conditions and historically, in the aggregate, have incurred losses.

Our distribution activities are carried out in the northern and northeastern regions of Brazil, representing 8.36% of our consolidated net revenue as of December 31, 2011. The northern and northeastern regions of Brazil are the poorest regions in the country, and our distribution subsidiaries incur significant commercial losses due to illegal connections, as well as relatively high levels of default by consumers in those regions. Historically, in the aggregate, our distribution subsidiaries have incurred losses which have adversely affected our consolidated results of operations. In May 2008, we implemented a new management structure for our distribution activities. As a result, several measures have been taken in order to reduce commercial losses and to renegotiate debts due by consumers in default with our distribution subsidiaries. However, we cannot be certain that such measures will succeed, and that the losses suffered by our distribution subsidiaries will be substantially reduced. We also cannot be certain that the conditions in the market where theses subsidiaries operate will not deteriorate.

In addition, the tariffs we charge for sales of electricity to customers are determined by ANEEL pursuant to concession agreements and to Brazilian law, which establish mechanisms that permit adjustment periodically. ANEEL determines the level of any adjustment by analyzing the costs of each distribution company and their weighted average cost of capital, or WACC. The third tariff review cycle for energy distribution companies resulted in a WACC of 7.5%. Given that the macroeconomic indicators of Brazil have improved in the recent past, the new WACC could lead to lower energy costs while other costs remain stable. Therefore, our electrical power distribution subsidiaries may incur losses, and may continue to adversely affect our financial condition and results of our operations.

We may incur losses and spend time and money defending pending litigation and administrative proceedings.

We are currently a party to numerous legal proceedings relating to civil, administrative, environmental, labor and tax claims filed against us. These claims involve substantial amounts of money and other remedies. Several individual disputes account for a significant part of the total amount of claims against us. We have established provisions for all amounts in dispute that represent a probable loss in the view of our legal advisors and in relation to those disputes that are covered by laws, administrative decrees, decrees or court rulings that have proven to be unfavorable. As of December 31, 2011, we provisioned a total aggregate amount of approximately R$4,892 million in respect of our legal proceedings, of which R$374 million were related to tax claims, R$3,360 million were related to civil claims and R$854 million were related to labor claims. (See “Item 8.A, Consolidated Financial Statements and Other Information – Litigation”).

In the event that claims involving a material amount and for which we have no provisions were to be decided against us, or in the event that the losses estimated turn out to be significantly higher that the provisions made, the aggregate cost of unfavorable decisions could have a material adverse effect on our financial condition and results of operations. In addition, our management may be required to direct its time and attention to defending these claims, which could preclude them from focusing on our core business. Depending on the outcome, certain litigation could result in restrictions in our operations and have a material adverse effect on certain of our businesses.

Our insurance coverage may be insufficient to cover potential losses.

Our business is generally subject to a number of risks and hazards, including industrial accidents, labor disputes, unexpected geological conditions, changes in the regulatory environment, environmental hazards and weather and other natural phenomena. Additionally, we and our subsidiaries are liable to third parties for losses and damages caused by any failure to provide generation, transmission and distribution services.

14

Table of Contents

Our insurance covers only part of the losses that we may incur. We maintain insurance in amounts that we believe to be adequate to cover damages to our plants caused by fire, general third-party liability for accidents and operational risks. If we are unable to renew our insurance policies from time to time or losses or other liabilities occur that are not covered by insurance or that exceed our insurance limits, we could be subject to significant unexpected additional losses.

Judgment may not be enforceable against our directors or officers.

All of our directors and officers named in this annual report reside in Brazil. We, our directors and officers and our Fiscal Council members, have not agreed to accept service of process in the United States. Substantially all of our assets, as well as the assets of these persons, are located in Brazil. As a result, it may not be possible to effect service of process within the United States or other jurisdictions outside Brazil upon these persons, attach their assets, or enforce against them or us in United States courts, or the courts of other jurisdictions outside Brazil, judgments predicated upon the civil liability provisions of the securities laws of the United States or the laws of other jurisdictions.

We do not have an established history of preparing IFRS financial statements and we lack in-depth internal expertise on IFRS.

Historically, our financial statements have been prepared in accordance with accounting practices adopted in Brazil and in accordance with U.S. GAAP for the purposes of our Form 20-F filing, the accounting standards issued by the Instituto dos Auditores Independentes do Brasil (or Brazilian Institute of Independent Accountants) and the standards and procedures of the CVM. We do not have IFRS financial data for any period prior to the year ended December 31, 2009.

As a result, we currently lack in-depth internal expertise with IFRS. As of the date of this annual report, we use a third party consultancy firm to assist us in preparing IFRS financial statements. If we are unable to develop this expertise internally or through external hires, we may face challenges in certain areas such as making the assessments required by IFRS in consolidating the results of our operating subsidiaries. If we are unable to train, hire and retain the appropriate personnel, our ability to prepare IFRS financial statements in a consistent and timely manner might be jeopardized.

If we are unable to remedy the material weaknesses in our internal controls, the reliability of our financial reporting and the preparation of our financial statements may be materially adversely affected.

Pursuant to SEC regulations, our management, including our Chief Executive Officer and Chief Financial Officer, evaluate the effectiveness of our disclosure controls and procedures, including the effectiveness of our internal control over financial reporting. Our internal controls over financial reporting are designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. As a result of our management’s evaluation of the effectiveness of our disclosure, controls and procedures in 2011, our management determined that these controls and procedures were not effective due to material weaknesses in our internal controls over financial reporting. These material weaknesses included our lack of design and maintenance of effective operating controls over:

| • | financial reporting based criteria established by the Committee of Sponsoring Organizations of the Treadway Commission, or COSO, including: internal control deficiencies not remedied in a timely manner; lack of adequately defined responsibility with respect to our internal controls over financial reporting and the necessary lines of communication; lack of adequate performance of an assessment to ensure effectively defined and implemented controls to prevent and detect material misstatements to our financial statements; lack of adequate design and maintenance of effective information technology policies, including those related to segregation of duties, security and access (grant and monitor) to our financial application programs and data; |

| • | completeness and accuracy of period-end financial reporting, specifically relating to the recording of recurring and non-recurring journal entries; |

15

Table of Contents

| • | the completeness and accuracy of information regarding judicial deposits and lawsuits, including periodic reviews and updates of this information, including updates of expected losses for accrual purposes; |

| • | the completeness and accuracy and the review and monitoring of post-retirement benefit plans (pension plans) sponsored by us, including the failure to perform a detailed review of the actuarial assumptions, reconciliation between actuarial valuation reports and accounting records, as well as cash flows from contribution payments; |

| • | our accounting for property, plant and equipment, specifically, to ensure the completeness, accuracy and validation of these acquisitions; |

| • | the completeness, accuracy, validity and valuation of the purchase of and payments for goods and services due to changes related to the implementation of new software; |

| • | the completeness and accuracy of changes in transmission services accounts receivable associated with the adjustment factor related to the availability of the transmission lines not included in the fixed transmission revenue fee (Receita Annual Permitida); |

| • | the appropriate review and monitoring related to the preparation of our IFRS financial statements and disclosures, including lack of internal accounting staff with adequate knowledge of IFRS to supervise and review the accounting process; and |

| • | the accuracy over the identification of the amounts of repayments for subsidy related to the Fuel Consumption Account (CCC). |

In response to these findings by our management, we have begun to implement steps to remedy each of these material weaknesses. In the event we are unable to remedy these material weaknesses, the reliability of our financial reporting and the preparation of our financial statements may be materially adversely affected, which may materially adversely affect our company and our reputation.

Risks Relating to Brazil

The Brazilian Government has exercised, and continues to exercise, significant influence over the Brazilian economy. Brazilian economic and political conditions have a direct impact on our business, financial condition, results of operations and prospects.

The Brazilian economy has been characterized by the significant involvement of the Brazilian Government, which often changes monetary, credit and other policies to influence Brazil’s economy. The Brazilian Government’s actions to control inflation and effect other policies have often involved wage and price controls, depreciation of the real, controls over remittances of funds abroad, intervention by the Central Bank to affect base interest rates and other measures. We have no control over, and cannot predict, what measures or policies the Brazilian Government may take in the future. Our business, financial condition, results of operations and prospects may be adversely affected by changes in Brazilian Government policies, as well as general factors including, without limitation:

| • | Brazilian economic growth; |

| • | inflation; |

| • | interest rates; |

| • | variations in exchange rates; |

| • | exchange control policies; |

| • | liquidity of the domestic capital and lending markets; |

| • | fiscal policy and changes in tax laws; and |

| • | other political, diplomatic, social and economic policies or developments in or affecting Brazil. |

16

Table of Contents

Changes in, or uncertainties regarding the implementation of, the policies listed above could contribute to economic uncertainty in Brazil, thereby increasing the volatility of the Brazilian securities market and the value of Brazilian securities traded abroad.

The stability of the Brazilian real is affected by its relationship with the U.S. dollar, inflation and Brazilian Government policy regarding exchange rates. Our business could be adversely affected by any recurrence of volatility affecting our foreign currency-linked receivables and obligations.

The Brazilian currency has experienced high degrees of volatility in the past. The Brazilian Government has implemented several economic plans, and has used a wide range of foreign currency control mechanisms, including sudden devaluation, small periodic devaluation during which the occurrence of the changes varied from daily to monthly, floating exchange market systems, exchange controls and parallel exchange market. From time to time, there was a significant degree of fluctuation between the U.S. dollar and the Brazilian real and other currencies. On December 31, 2011, the exchange rate between the real and the dollar was R$1.8758 to U.S.$1.00.

The real may not maintain its current value or the Brazilian Government may implement foreign currency control mechanisms. Any governmental interference with the exchange rate, or the implementation of exchange control mechanisms, could lead to a depreciation of the real, which could reduce the value of our receivables and make our foreign currency-linked obligations more expensive. Other than in respect of our revenues and receivables denominated in U.S. dollars, such devaluation could materially adversely affect our business, operations or prospects.

On December 31, 2011, approximately 44.3% of our consolidated indebtedness, which equals R$18,390 million as of such date, was denominated in foreign currencies, of which R$17,963 million (or approximately 42.4%) was denominated in U.S. dollars, and approximately R$9 billion (or approximately 48.9%) of such foreign indebtedness related to Itaipu indebtedness.

Inflation, and the Brazilian Government’s measures to curb inflation, may contribute significantly to economic uncertainty in Brazil and materially adversely impact our operating results.

Brazil has historically experienced high rates of inflation. Inflation and some of the Brazilian Government’s measures taken in an attempt to curb inflation have had significant negative effects on the Brazilian economy generally. Since the introduction of the real in 1994, Brazil’s rate of inflation has been substantially lower than in previous periods. However, inflationary pressures persist, and policies adopted to contain inflationary pressures and uncertainties regarding possible future governmental intervention have contributed to economic uncertainty.

Brazil may experience high levels of inflation in the future. Inflationary cost pressures may lead to further government intervention, including the introduction of policies that could adversely affect our business, financial condition, results of operations and prospects.

The market value of securities issued by Brazilian companies is influenced by the perception of risk in Brazil and by the risk of other emerging economies.

Adverse events in the Brazilian economy and in market conditions of other emerging markets, especially in Latin America, may adversely affect the market prices of securities issued by Brazilian companies. Even if economic conditions in these countries differ considerably from economic conditions prevailing in Brazil, investors’ reactions to events in those countries may have a negative effect on the market prices of securities of Brazilian issuers. Crisis in other emerging countries may reduce investor demand for securities of Brazilian issuers, including securities issued by us. This may negatively affect the market price of our shares. In addition, it may make it more difficult for us to access the international capital markets and to obtain financing on acceptable terms in the future.

The Brazilian economy is also affected by general global economic conditions, particularly those in the United States. For instance, the stock prices on BM&FBOVESPA have historically been vulnerable to interest rate fluctuations in the United States, as well as to fluctuation in the main U.S. stock indices.

These factors could affect the trading price of our common and preferred shares and ADSs and could make it more difficult for us to access capital markets and finance future operations.

17

Table of Contents

Risks Relating to the Brazilian Power Industry

We cannot predict whether the constitutionality of the Electricity Regulatory Law will be upheld; if it is not, we may face both uncertainty and costs in re-aligning our business.

In 2004, the Brazilian Government enacted the Electricity Regulatory Law, a far reaching piece of legislation that provides the framework for regulation of the electricity sector in Brazil. Among other changes, the new legislation (i) modifies the rules regarding the purchase and sale of electric power between generation companies and distribution companies; (ii) established new rules for the auction of generation companies; (iii) created the Electric Power Commercialization Chamber (“CCEE”) and new divisional bodies; and (iv) modified the responsibilities of the Energy and Mining Ministry and ANEEL. We have aligned our business within this framework. However, the constitutionality of the Electricity Regulatory Law is being challenged in the Brazilian Supreme Court. The Supreme Court has not yet issued a final ruling in this case although it recently agreed to deny a request to suspend the effectiveness of the Electricity Regulatory Law while the challenge is pending. If the Supreme Court were to hold that the Electricity Regulatory Law is unconstitutional, this would result in significant uncertainty in Brazil as to the appropriate regulatory framework for the electricity sector, which could materially adversely affect the operation of our business. Moreover, we have no way of predicting the terms of any alternative framework for the regulation of electricity in Brazil. We would likely face costs in re-aligning our business to meet the requirements of any such framework, which would materially adversely affect our financial condition and results of operations.

We could be penalized by ANEEL for failing to comply with the terms of our concession agreements and we may not recover the full value of our investment in the event that any of our concession agreements are terminated.

We carry out our generation, transmission and distribution activities in accordance with concession agreements we execute with the Brazilian Government through ANEEL. The length of such concessions varies from 20 to 35 years. ANEEL may impose penalties on us in the event that we fail to comply with any provision of our concession agreements. Depending on the extent of the non-compliance, these penalties could include substantial fines (in some cases up to two percent of our gross revenues in the fiscal year immediately preceding the assessment), restrictions on our operations, intervention or termination of the concession. For example, on May 22, 2010, our subsidiary Eletrobras Furnas received a R$53,700 fine from ANEEL, as a result of ANEEL determining that there were two malfunctions in the protection system of the Itaberá and Ivaiporã substations that led to power outages and disruption in generation on November 10, 2009. ANEEL may also terminate our concessions prior to their due date in the event that we fail to comply with their provisions, are declared bankrupt or are dissolved, or in the event that ANEEL determines that such termination would serve the public interest (see “Item 4.B, Business Overview – Generation – Concessions”).

As of December 31, 2011, we believe we were in compliance with all material terms of our concession agreements. However, we cannot assure you that we will not be penalized by ANEEL for a future breach of our concession agreements or that our concessions will not be terminated in the future. In the event that ANEEL were to terminate any of our concessions before their expiration date, the compensation we recover for the unamortized portion of our investment may not be sufficient for us to recover the full value of our investment and, accordingly, could have a material adverse affect on our financial condition and results of operations.