UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION

13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended December 31, 2022

OR

☐ TRANSITION REPORT PURSUANT TO SECTION

13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______ to _______

Commission File Number 001-40701

ECOARK HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Nevada | | 30-0680177 |

(State or other jurisdiction of

incorporation or organization) | | (I.R.S. Employer

Identification No.) |

| | | |

| 303 Pearl Parkway, Suite 200, San Antonio, TX | | 78215 |

| (Address of principal executive offices) | | (Zip Code) |

(800) 762-7293

(Registrant’s telephone number, including

area code)

Securities registered pursuant to Section 12(b)

of the Act:

| Title of each class | | Trading Symbol | | Name of each exchange on which

registered |

| Common Stock | | ZEST | | The Nasdaq Stock Market LLC (The Nasdaq Capital Market) |

Indicate by check mark whether the registrant:

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Sec.232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by checkmark whether the registrant is

a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

As of February 15, 2023, there were 37,666,772

shares of common stock, par value $0.001 per share, outstanding.

PART I — FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

December 31, 2022

Table of Content

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

DECEMBER 31, 2022 (UNAUDITED) AND MARCH 31, 2022

| | |

DECEMBER 31, | | |

MARCH 31, | |

| | |

2022 | | |

2022 | |

| | |

(unaudited) | | |

| |

| ASSETS | |

| | |

| |

| CURRENT ASSETS: | |

| | |

| |

| Cash ($16,000 pledged as collateral for credit as of December 31, 2022 and March 31, 2022, respectively) | |

$ | 32,642 | | |

$ | 85,073 | |

| Investment - White River Energy Corp. | |

| 30,000,000 | | |

| - | |

| Secured note receivable and accrued interest receivable | |

| 1,177,604 | | |

| - | |

| Intangible assets, cryptocurrencies | |

| - | | |

| 19,267 | |

| Prepaid expenses and other current assets, current portion | |

| 829,071 | | |

| 862,944 | |

| Current assets of discontinued operations/held for sale | |

| 1,509,292 | | |

| 2,412,842 | |

| Total current assets | |

| 33,548,609 | | |

| 3,380,126 | |

| | |

| | | |

| | |

| NON-CURRENT ASSETS: | |

| | | |

| | |

| Property and equipment, net | |

| 4,122,365 | | |

| 7,226,370 | |

| Power development costs | |

| 1,000,000 | | |

| 2,000,000 | |

| Secured note receivable and accrued interest receivable, net of current portion | |

| 3,187,500 | | |

| - | |

| Right of use assets - operating leases | |

| 370,315 | | |

| 461,138 | |

| Other assets | |

| 10,905 | | |

| 11,189 | |

| Non-current assets of discontinued operations/held for sale | |

| 7,829,596 | | |

| 22,898,420 | |

| | |

| | | |

| | |

| Total non-current assets | |

| 16,520,681 | | |

| 32,597,117 | |

| | |

| | | |

| | |

| TOTAL ASSETS | |

$ | 50,069,290 | | |

$ | 35,977,243 | |

| | |

| | | |

| | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |

| | | |

| | |

| | |

| | | |

| | |

| LIABILITIES | |

| | | |

| | |

| CURRENT LIABILITIES | |

| | | |

| | |

| Accounts payable | |

$ | 2,998,876 | | |

$ | 2,723,865 | |

| Accrued liabilities | |

| 1,026,100 | | |

| 668,659 | |

| Warrant derivative liabilities | |

| 44,447 | | |

| 4,318,630 | |

| Preferred stock derivative liability | |

| 4,811,875 | | |

| - | |

| Current portion of long-term debt | |

| 303,136 | | |

| 608,377 | |

| Note payable - related parties | |

| 125,000 | | |

| - | |

| Current portion of lease liability - operating leases | |

| 119,975 | | |

| 117,451 | |

| Current liabilities of discontinued operations/held for sale | |

| 3,047,164 | | |

| 3,337,994 | |

| | |

| | | |

| | |

| Total current liabilities | |

| 12,476,573 | | |

| 11,774,976 | |

| | |

| | | |

| | |

| NON-CURRENT LIABILITIES | |

| | | |

| | |

| Lease liability - operating leases, net of current portion | |

| 256,305 | | |

| 345,976 | |

| Long-term debt, net of current portion | |

| 58,662 | | |

| 67,802 | |

| Non-current liabilities of discontinued operations/held for sale | |

| 394,852 | | |

| 1,653,901 | |

| | |

| | | |

| | |

| Total non-current liabilities | |

| 709,819 | | |

| 2,067,679 | |

| | |

| | | |

| | |

| Total Liabilities | |

| 13,186,392 | | |

| 13,842,655 | |

| | |

| | | |

| | |

| COMMITMENTS AND CONTINGENCIES | |

| | | |

| | |

| | |

| | | |

| | |

| STOCKHOLDERS’ EQUITY (DEFICIT) | |

| | | |

| | |

| Series A Preferred stock, $0.001 par value; 5,000,000 shares authorized; 882 and 0 shares issued and outstanding as of December 31, 2022 and March 31, 2022, respectively | |

| - | | |

| - | |

| Common stock, $0.001 par value, 100,000,000 shares authorized, 29,456,342 and 26,364,099 shares issued and 29,456,342 and 26,246,984 shares outstanding as of December 31, 2022 and March 31, 2022, respectively | |

| 29,456 | | |

| 26,364 | |

| Additional paid in capital | |

| 195,532,152 | | |

| 183,246,061 | |

| Accumulated deficit | |

| (157,440,304 | ) | |

| (158,868,204 | ) |

| Treasury stock, at cost | |

| - | | |

| (1,670,575 | ) |

| Total stockholders’ equity before non-controlling interest | |

| 38,121,304 | | |

| 22,733,646 | |

| Non-controlling interest | |

| (1,238,406 | ) | |

| (599,058 | ) |

| Total stockholders’ equity | |

| 36,882,898 | | |

| 22,134,588 | |

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | |

$ | 50,069,290 | | |

$ | 35,977,243 | |

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

FOR THE NINE AND THREE MONTHS ENDED DECEMBER 31, 2022 AND 2021

| | |

NINE MONTHS ENDED | | |

THREE MONTHS ENDED | |

| | |

DECEMBER 31, | | |

DECEMBER 31, | |

| | |

2022 | | |

2021 | | |

2022 | | |

2021 | |

| CONTINUING OPERATIONS: | |

| | |

| | |

| | |

| |

| REVENUES | |

$ | - | | |

$ | 17,455 | | |

$ | - | | |

$ | 17,455 | |

| COST OF REVENUES | |

| 229,534 | | |

| 92,823 | | |

| 47,460 | | |

| 92,823 | |

| GROSS PROFIT | |

| (229,534 | ) | |

| (75,368 | ) | |

| (47,460 | ) | |

| (75,368 | ) |

| | |

| | | |

| | | |

| | | |

| | |

| OPERATING EXPENSES | |

| | | |

| | | |

| | | |

| | |

| Salaries and salaries related costs | |

| 10,998,108 | | |

| 5,504,833 | | |

| 1,280,078 | | |

| 3,159,979 | |

| Professional and consulting fees | |

| 743,403 | | |

| 649,119 | | |

| 287,630 | | |

| 385,576 | |

| Selling, general and administrative costs | |

| 4,440,902 | | |

| 4,455,788 | | |

| 1,424,435 | | |

| 1,092,819 | |

| Depreciation, amortization, and impairment | |

| 1,718,308 | | |

| 164,266 | | |

| 13,779 | | |

| 53,474 | |

| Cryptocurrency impairment losses | |

| 9,122 | | |

| 1,047 | | |

| - | | |

| 1,047 | |

| Total operating expenses | |

| 17,909,843 | | |

| 10,775,053 | | |

| 3,005,922 | | |

| 4,692,895 | |

| | |

| | | |

| | | |

| | | |

| | |

| LOSS FROM CONTINUING OPERATIONS BEFORE OTHER INCOME (EXPENSE) | |

| (18,139,377 | ) | |

| (10,850,421 | ) | |

| (3,053,382 | ) | |

| (4,768,263 | ) |

| | |

| | | |

| | | |

| | | |

| | |

| OTHER INCOME (EXPENSE) | |

| | | |

| | | |

| | | |

| | |

| Change in fair value of warrant derivative liabilities | |

| 4,274,183 | | |

| 15,294,814 | | |

| 1,381,711 | | |

| 10,979,137 | |

| Change in fair value of preferred stock derivative liabilities | |

| 1,864,777 | | |

| - | | |

| 1,864,777 | | |

| - | |

| Derivative income (expense) | |

| 2,878,345 | | |

| - | | |

| 2,878,345 | | |

| - | |

| Loss on conversion of derivative liability to common stock in conversion of preferred stock | |

| (3,923 | ) | |

| - | | |

| (3,923 | ) | |

| - | |

| Gain (loss) on disposal of fixed assets | |

| (570,772 | ) | |

| - | | |

| - | | |

| - | |

| Interest expense, net of interest income | |

| (491,075 | ) | |

| (553,561 | ) | |

| (172,347 | ) | |

| 3,594 | |

| Total other income (expense) | |

| 7,951,535 | | |

| 14,741,253 | | |

| 5,948,563 | | |

| 10,982,731 | |

| | |

| | | |

| | | |

| | | |

| | |

| (LOSS) INCOME FROM CONTINUING OPERATIONS BEFORE PROVISION FOR INCOME TAXES AND DISCONTINUED OPERATIONS | |

| (10,187,842 | ) | |

| 3,890,832 | | |

| 2,895,181 | | |

| 6,214,468 | |

| | |

| | | |

| | | |

| | | |

| | |

| DISCONTINUED OPERATIONS: | |

| | | |

| | | |

| | | |

| | |

| (Loss) income from discontinued operations | |

| (11,020,812 | ) | |

| (2,908,619 | ) | |

| (468,210 | ) | |

| (1,937,100 | ) |

| (Loss) on disposal of discontinued operations | |

| (11,823,395 | ) | |

| - | | |

| - | | |

| - | |

| Total discontinued operations | |

| (22,844,207 | ) | |

| (2,908,619 | ) | |

| (468,210 | ) | |

| (1,937,100 | ) |

| | |

| | | |

| | | |

| | | |

| | |

| (LOSS) INCOME FROM OPERATIONS BEFORE PROVISION FOR INCOME TAXES | |

| (33,032,049 | ) | |

| 982,213 | | |

| 2,426,971 | | |

| 4,277,368 | |

| | |

| | | |

| | | |

| | | |

| | |

| PROVISION FOR INCOME TAXES | |

| - | | |

| - | | |

| - | | |

| - | |

| | |

| | | |

| | | |

| | | |

| | |

| NET (LOSS) INCOME | |

| (33,032,049 | ) | |

| 982,213 | | |

| 2,426,971 | | |

| 4,277,368 | |

| NET LOSS ATTRIBUTABLE TO NON-CONTROLLING INTEREST | |

| 2,642,559 | | |

| 322,635 | | |

| 322,351 | | |

| 322,635 | |

| | |

| | | |

| | | |

| | | |

| | |

| NET (LOSS) INCOME TO CONTROLLING INTEREST | |

$ | (30,389,490 | ) | |

$ | 1,304,848 | | |

$ | 2,749,322 | | |

$ | 4,600,003 | |

| Less: Preferred Stock Dividends | |

| 484,213 | | |

| - | | |

| 99,737 | | |

| - | |

| | |

| | | |

| | | |

| | | |

| | |

| NET (LOSS) INCOME TO CONTROLLING INTEREST OF COMMON STOCKHOLDERS | |

$ | (30,873,703 | ) | |

$ | 1,304,848 | | |

$ | 2,649,585 | | |

$ | 4,600,003 | |

| | |

| | | |

| | | |

| | | |

| | |

| NET (LOSS) INCOME PER SHARE - BASIC | |

| | | |

| | | |

| | | |

| | |

| Continuing operations | |

$ | (0.28 | ) | |

$ | 0.17 | | |

$ | 0.11 | | |

$ | 0.25 | |

| Discontinued operations | |

| (0.83 | ) | |

| (0.12 | ) | |

| (0.02 | ) | |

| (0.07 | ) |

| | |

$ | (1.11 | ) | |

$ | 0.05 | | |

$ | 0.09 | | |

$ | 0.18 | |

WEIGHTED AVERAGE SHARES OUTSTANDING - BASIC AND DILUTED | |

| 27,369,610 | | |

| 24,727,970 | | |

| 28,499,875 | | |

| 26,364,099 | |

| NET (LOSS) PER SHARE - DILUTED (see NOTE 1) | |

$ | (1.11 | ) | |

$ | (0.57 | ) | |

$ | (0.12 | ) | |

$ | (0.24 | ) |

| WEIGHTED AVERAGE SHARES OUTSTANDING - DILUTED (see NOTE 1) | |

| 27,369,610 | | |

| 24,727,970 | | |

| 72,747,922 | | |

| 26,364,099 | |

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY

(DEFICIT) (UNAUDITED)

FOR THE NINE MONTHS ENDED DECEMBER 31, 2022 AND 2021

| | |

| | |

| | |

| | |

Additional | | |

| | |

| | |

| | |

| |

| | |

Preferred | | |

Common Stock | | |

Paid-In | | |

Accumulated | | |

Treasury | | |

Non-controlling | | |

| |

| | |

Shares | | |

Amount | | |

Shares | | |

Amount | | |

Capital | | |

Deficit | | |

Stock | | |

Interest | | |

Total | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| Balance - March 31, 2021 | |

| - | | |

$ | - | | |

| 22,705,775 | | |

$ | 22,705 | | |

$ | 167,587,659 | | |

$ | (148,912,810 | ) | |

$ | (1,670,575 | ) | |

$ | - | | |

$ | 17,026,979 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Shares issued in the exercise of stock options, including cashless exercises | |

| - | | |

| - | | |

| 20,265 | | |

| 20 | | |

| 28,277 | | |

| - | | |

| - | | |

| - | | |

| 28,297 | |

| Shares issued for services rendered, net of amounts prepaid | |

| - | | |

| - | | |

| 114,796 | | |

| 114 | | |

| 674,886 | | |

| - | | |

| - | | |

| - | | |

| 675,000 | |

| Share-based compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 399,173 | | |

| - | | |

| - | | |

| - | | |

| 399,173 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net income for the period | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 2,559,524 | | |

| - | | |

| - | | |

| 2,559,524 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - June 30, 2021 | |

| - | | |

| - | | |

| 22,840,836 | | |

| 22,839 | | |

| 168,689,995 | | |

| (146,353,286 | ) | |

| (1,670,575 | ) | |

| - | | |

| 20,688,973 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Shares issued for services rendered, net of amounts prepaid | |

| - | | |

| - | | |

| 45,000 | | |

| 45 | | |

| 91,955 | | |

| - | | |

| - | | |

| - | | |

| 92,000 | |

| Shares issued in registered direct offering, net of amount allocated to derivative liability | |

| - | | |

| - | | |

| 3,478,261 | | |

| 3,478 | | |

| 8,023,602 | | |

| - | | |

| - | | |

| - | | |

| 8,027,080 | |

| Share-based compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 819,009 | | |

| - | | |

| - | | |

| - | | |

| 819,009 | |

| Fractional adjustment | |

| - | | |

| - | | |

| 2 | | |

| 2 | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 2 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net loss for the period | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (5,854,679 | ) | |

| - | | |

| - | | |

| (5,854,679 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - September 30, 2021 | |

| - | | |

| - | | |

| 26,364,099 | | |

| 26,364 | | |

| 177,624,561 | | |

| (152,207,965 | ) | |

| (1,670,575 | ) | |

| - | | |

| 23,772,385 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Vesting of shares issued in prior quarter | |

| - | | |

| - | | |

| - | | |

| - | | |

| 114,190 | | |

| - | | |

| - | | |

| - | | |

| 114,190 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Shares issued by Agora Digital Holdings, Inc. for services rendered, net of amounts prepaid | |

| - | | |

| - | | |

| - | | |

| - | | |

| 2,280,969 | | |

| - | | |

| - | | |

| - | | |

| 2,280,969 | |

| Share-based compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 493,284 | | |

| - | | |

| - | | |

| - | | |

| 493,284 | |

| Recognition of non-controlling interest | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (30,000 | ) | |

| - | | |

| 30,000 | | |

| - | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net income (loss) for the period | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 4,600,003 | | |

| - | | |

| (322,635 | ) | |

| 4,277,368 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - December 31, 2021 | |

| - | | |

$ | - | | |

| 26,364,099 | | |

$ | 26,364 | | |

$ | 180,513,004 | | |

$ | (147,637,962 | ) | |

$ | (1,670,575 | ) | |

$ | (292,635 | ) | |

$ | 30,938,196 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - March 31, 2022 | |

| - | | |

$ | - | | |

| 26,364,099 | | |

$ | 26,364 | | |

$ | 183,246,061 | | |

$ | (158,868,204 | ) | |

$ | (1,670,575 | ) | |

$ | (599,058 | ) | |

$ | 22,134,588 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Shares issued for commitment for preferred stock offering, net of expenses | |

| - | | |

| - | | |

| 102,881 | | |

| 103 | | |

| 193,313 | | |

| - | | |

| - | | |

| - | | |

| 193,416 | |

| Shares issued by Agora Digital Holdings, Inc. for services rendered, net of amounts prepaid | |

| - | | |

| - | | |

| - | | |

| - | | |

| 5,215,287 | | |

| - | | |

| - | | |

| - | | |

| 5,215,287 | |

| Share-based compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 182,561 | | |

| - | | |

| - | | |

| - | | |

| 182,561 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Net loss for the period | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (10,153,383 | ) | |

| - | | |

| (571,261 | ) | |

| (10,724,644 | ) |

| Preferred stock dividends | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (43,151 | ) | |

| - | | |

| - | | |

| (43,151 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - June 30, 2022 | |

| - | | |

| - | | |

| 26,466,980 | | |

| 26,467 | | |

| 188,837,222 | | |

| (169,064,738 | ) | |

| (1,670,575 | ) | |

| (1,170,319 | ) | |

| 16,958,057 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Shares issued in conversion of preferred stock to common stock | |

| - | | |

| - | | |

| 1,276,190 | | |

| 1,276 | | |

| 2,635,528 | | |

| - | | |

| - | | |

| - | | |

| 2,636,804 | |

| Shares issued in settlement | |

| - | | |

| - | | |

| 432,885 | | |

| 433 | | |

| (626,008 | ) | |

| - | | |

| 1,670,575 | | |

| - | | |

| 1,045,000 | |

| Shares issued by Agora Digital Holdings, Inc. for services rendered, net of amounts prepaid | |

| - | | |

| - | | |

| - | | |

| - | | |

| 2,956,921 | | |

| - | | |

| - | | |

| - | | |

| 2,956,921 | |

| Share-based compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 160,040 | | |

| - | | |

| - | | |

| - | | |

| 160,040 | |

| Disposal of subsidiaries in reverse merger transactions | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 32,301,782 | | |

| - | | |

| 2,003,211 | | |

| 34,304,993 | |

| Net loss for the period | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (22,985,608 | ) | |

| - | | |

| (1,748,947 | ) | |

| (24,734,555 | ) |

| Preferred stock dividends | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (341,325 | ) | |

| - | | |

| - | | |

| (341,325 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - September 30, 2022 | |

| - | | |

| - | | |

| 28,176,055 | | |

| 28,176 | | |

| 193,963,703 | | |

| (160,089,889 | ) | |

| - | | |

| (916,055 | ) | |

| 32,985,935 | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Shares issued in conversion of preferred stock to common stock | |

| - | | |

| - | | |

| 1,140,447 | | |

| 1,140 | | |

| 544,449 | | |

| - | | |

| - | | |

| - | | |

| 545,589 | |

| Shares issued for preferred stock dividends | |

| - | | |

| - | | |

| 139,840 | | |

| 140 | | |

| 104,423 | | |

| - | | |

| - | | |

| - | | |

| 104,563 | |

| Shares issued by Agora Digital Holdings, Inc. for services rendered, net of amounts prepaid | |

| - | | |

| - | | |

| - | | |

| - | | |

| 791,491 | | |

| - | | |

| - | | |

| - | | |

| 791,491 | |

| Share-based compensation | |

| - | | |

| - | | |

| - | | |

| - | | |

| 128,086 | | |

| - | | |

| - | | |

| - | | |

| 128,086 | |

| Net income (loss) for the period | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| 2,749,322 | | |

| - | | |

| (322,351 | ) | |

| 2,426,971 | |

| Preferred stock dividends | |

| - | | |

| - | | |

| - | | |

| - | | |

| - | | |

| (99,737 | ) | |

| - | | |

| - | | |

| (99,737 | ) |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| Balance - December 31, 2022 | |

| - | | |

$ | - | | |

| 29,456,342 | | |

$ | 29,456 | | |

$ | 195,532,152 | | |

$ | (157,440,304 | ) | |

$ | - | | |

$ | (1,238,406 | ) | |

$ | 36,882,898 | |

The accompanying notes are

an integral part of these unaudited condensed consolidated financial statements.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

FOR THE NINE MONTHS ENDED DECEMBER 31, 2022 AND 2021

| | |

DECEMBER 31, | |

| | |

2022 | | |

2021 | |

| | |

| | |

| |

| CASH FLOW FROM OPERATING ACTIVITIES FROM CONTINUING OPERATIONS | |

| | |

| |

| Net (loss) income | |

$ | (30,873,703 | ) | |

$ | 1,304,848 | |

| Adjustments to reconcile net (loss) income to net cash used in operating activities | |

| | | |

| | |

| Change in non-controlling interest | |

| (2,642,559 | ) | |

| (322,635 | ) |

| Depreciation, amortization, and impairment | |

| 1,718,308 | | |

| 164,266 | |

| Cryptocurrency impairment losses | |

| 9,122 | | |

| 1,047 | |

| Debt modification expense | |

| 879,368 | | |

| - | |

| Share-based compensation | |

| 470,687 | | |

| 1,711,466 | |

| Change in fair value of warrant derivative liabilities | |

| (4,274,183 | ) | |

| (15,294,814 | ) |

| Change in fair value of preferred stock derivative liabilities | |

| (1,864,777 | ) | |

| - | |

| Derivative (income) expense | |

| (2,878,345 | ) | |

| - | |

| Loss on conversion of derivative liabilities to common stock | |

| 3,923 | | |

| - | |

| Loss on disposal of fixed assets | |

| 570,772 | | |

| - | |

| (Gain) on disposal of White River and Pinnacle Frac | |

| 12,534,900 | | |

| - | |

| (Gain) on disposal of Trend Discovery Holdings | |

| (711,505 | ) | |

| - | |

| Common shares issued for services | |

| 1,045,000 | | |

| 881,190 | |

| Common shares issued for services - Agora | |

| 8,963,699 | | |

| 2,280,969 | |

| Amortization of discount | |

| 47,515 | | |

| - | |

| Development expenses reduced from refund of power development fee | |

| 155,292 | | |

| - | |

| Warrants granted for interest expense | |

| - | | |

| 545,125 | |

| Warrants granted for commissions | |

| - | | |

| 744,530 | |

| Commitment fees on long-term debt | |

| 17,681 | | |

| - | |

| Changes in assets and liabilities | |

| | | |

| | |

| Prepaid expenses and other current assets | |

| 34,157 | | |

| (42,436 | ) |

| Intangible assets - cryptocurrencies | |

| 10,145 | | |

| (17,455 | ) |

| Amortization of right of use asset - financing leases | |

| - | | |

| - | |

| Amortization of right of use asset - operating leases | |

| 90,823 | | |

| 15,912 | |

| Accrued interest receivable | |

| (115,104 | ) | |

| - | |

| Operating lease expense | |

| (87,147 | ) | |

| (14,996 | ) |

| Accounts payable | |

| 1,130,011 | | |

| 1,758,231 | |

| Accrued liabilities | |

| 1,154,714 | | |

| (1,140,846 | ) |

| Total adjustments | |

| 16,262,497 | | |

| (8,730,446 | ) |

| Net cash used in operating activities of continuing operations | |

| (14,611,206 | ) | |

| (7,425,598 | ) |

| Net cash provided by (used in) discontinued operations | |

| 2,225,257 | | |

| (989,135 | ) |

| Net cash used in operating activities | |

| (12,385,949 | ) | |

| (8,414,733 | ) |

| | |

| | | |

| | |

| CASH FLOWS FROM INVESTING ACTIVITIES | |

| | | |

| | |

| Proceeds from the sale of power development costs | |

| 844,708 | | |

| (2,000,000 | ) |

| Purchase of fixed assets | |

| (40,074 | ) | |

| (7,065,639 | ) |

| Net cash provided by (used in) investing activities of continuing operations | |

| 804,634 | | |

| (9,065,639 | ) |

| Net cash (used in) investing activities of discontinued operations | |

| (287,413 | ) | |

| (327,032 | ) |

| Net cash provided by (used in) investing activities | |

| 517,221 | | |

| (9,392,671 | ) |

| | |

| | | |

| | |

| CASH FLOWS FROM FINANCING ACTIVITIES | |

| | | |

| | |

| Proceeds from the issuance of common stock in a registered direct offering, net of fees | |

| - | | |

| 19,228,948 | |

| Proceeds from exercise of stock options | |

| - | | |

| 28,300 | |

| Proceeds from notes payable - related parties | |

| 741,000 | | |

| - | |

| Repayments of notes payable - related parties | |

| (616,000 | ) | |

| (327,500 | ) |

| Proceeds from long-term debt | |

| 487,500 | | |

| - | |

| Repayment of long-term debt | |

| (819,562 | ) | |

| (23,966 | ) |

| Proceeds from the sale of preferred stock | |

| 12,000,000 | | |

| - | |

| Net cash provided by financing activities of continuing operations | |

| 11,792,938 | | |

| 18,905,782 | |

| Net cash provided by (used in) financing activities of discontinued operations | |

| 23,359 | | |

| (1,474,708 | ) |

| Net cash provided by financing activities | |

| 11,816,297 | | |

| 17,431,074 | |

| | |

| | | |

| | |

| NET (DECREASE) IN CASH AND RESTRICTED CASH | |

| (52,431 | ) | |

| (376,330 | ) |

| | |

| | | |

| | |

| CASH - BEGINNING OF PERIOD | |

| 85,073 | | |

| 809,811 | |

| | |

| | | |

| | |

| CASH - END OF PERIOD | |

$ | 32,642 | | |

$ | 433,481 | |

| | |

| | | |

| | |

| SUPPLEMENTAL DISCLOSURES | |

| | | |

| | |

| Cash paid for interest expense | |

$ | 11,173 | | |

$ | 20,106 | |

| Cash paid for income taxes | |

$ | - | | |

$ | - | |

| | |

| | | |

| | |

| SUMMARY OF NON-CASH ACTIVITIES: | |

| | | |

| | |

| | |

| | | |

| | |

| Reclassification of assets of discontinued operations to current operations in fixed assets | |

$ | - | | |

$ | 193,904 | |

| Recognition of non-controlling interest - Agora | |

$ | - | | |

$ | 30,000 | |

| Lease liability recognized for ROU asset | |

$ | - | | |

$ | 506,610 | |

| Issuance costs on mezzanine equity | |

$ | 193,416 | | |

$ | - | |

| Preferred stock dividend paid in common shares | |

$ | 104,563 | | |

$ | - | |

| Non-controlling interest recorded in consolidation of Enviro Technologies US, Inc. | |

$ | 2,003,211 | | |

$ | - | |

| Preferred shares/derivative liability converted into common stock | |

$ | 3,182,416 | | |

$ | - | |

| Mezzanine equity reclassified to liability upon amendment | |

$ | 9,551,074 | | |

$ | - | |

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

NOTE 1: ORGANIZATION AND SUMMARY OF SIGNIFICANT

ACCOUNTING POLICIES

Ecoark Holdings Inc. (“Ecoark Holdings”

or the “Company”) is a holding company, incorporated in the State of Nevada on November 19, 2007. Through December 31, 2022,

Ecoark Holdings’ former wholly owned subsidiaries with the exception of Agora Digital Holdings, Inc., a Nevada corporation (“Agora”)

and Zest Labs, Inc. (“Zest Labs”) have been treated for accounting purposes as divested. See below in this Note 1 and Note

2 “Discontinued Operations.” As a result of the divestitures, all assets and liabilities of the former subsidiaries have been

reclassified to discontinued operations on the condensed consolidated balance sheet for March 31, 2022 and all operations of these companies

have been reclassified to discontinued operations and gain on disposal on the condensed consolidated statements of operations for the

nine and three months ended December 31, 2022.

The Company’s principal subsidiaries consisted

of Ecoark, Inc. (“Ecoark”), a Delaware corporation which was the parent of Zest Labs, Banner Midstream Corp., a Delaware corporation

(“Banner Midstream”) and Agora which was assigned the membership interest in Trend Discovery Holdings LLC, a Delaware limited

liability corporation (all references to “Trend Holdings” or “Trend” are now synonymous with Agora) from the Company

on September 17, 2021 upon its formation, which includes Bitstream Mining, LLC, the Company’s Bitcoin mining subsidiary.

As disclosed in these Notes, the Company had decided

it was in the best interests of its stockholders that it divest all of its principal operating assets through a series of spin-offs or

stock dividends to the Company’s stockholders. It intended to do so either by engaging in business combinations with existing public

companies which have trading symbols and markets like White River Energy Corp (formerly Fortium Holdings Corp.) (“WTRV”) which

acquired White River Holdings Corp on July 25, 2022, and Wolf Energy Services, Inc. (formerly Enviro Technologies US, Inc.) (“Wolf

Energy”) which acquired Banner Midstream Corp. on September 7, 2022, or by direct dividends. The Company’s plan was also driven

by the dividends it must pay to an investor which provided $12 million on June 8, 2022 in exchange for preferred stock and a warrant,

the former of which was subsequently amended, and the latter of which was subsequently cancelled. Because all spin-offs require the transactions

to be registered with the Securities and Exchange Commission, the Company did not complete any spin-offs in calendar 2022. Because of

the plans to spin-off its principal operating subsidiaries, the Company is searching for one or more operating businesses to acquire.

See Note 20. “Subsequent Events” concerning a proposed acquisition. The Company has decided to leave Agora and Zest Labs in

the Company and to not proceed with the spin-offs of these entities, although it intends to create a trust to distribute at least 95%

of the net proceeds of the pending Zest Labs litigation recoveries, if any, to the Company’s stockholders as of September 30, 2022.

On March 27, 2020, the Company and Banner Energy

Services Corp., a Nevada corporation (“Banner Parent”), entered into a Stock Purchase and Sale Agreement (the “Banner

Purchase Agreement”) to acquire Banner Midstream Corp., a Delaware corporation (“Banner Midstream”). Pursuant to the

acquisition, Banner Midstream became a wholly-owned subsidiary of the Company and Banner Parent received shares of the Company’s

common stock in exchange for all of the issued and outstanding shares of Banner Midstream.

Banner Midstream had four operating subsidiaries:

Pinnacle Frac Transport LLC (“Pinnacle Frac”), Capstone Equipment Leasing LLC (“Capstone”), White River Holdings

Corp (“White River”), and Shamrock Upstream Energy LLC (“Shamrock”). Pinnacle Frac provides transportation of

frac sand and logistics services to major hydraulic fracturing and drilling operations. Capstone procures and finances equipment to oilfield

transportation service contractors. White River is and Shamrock was engaged in oil and gas exploration, production, and drilling operations

on over 30,000 cumulative acres of active mineral leases in Louisiana, and Mississippi. All of these operating subsidiaries have since

been divested in two separate transactions that occurred in July and September 2022.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

For a full description of the operations of White

River as well as Pinnacle Frac and Capstone, refer to the Annual Report filed on Form 10-K for the year ended March 31, 2022 filed on

July 7, 2022.

On July 25, 2022, the Company entered into and

closed a Share Exchange Agreement, by and among the Company, White River and WTRV. As a result, White River became a wholly-owned subsidiary

of WTRV and issued the Company non-voting Series A Convertible Preferred Stock (the “Series A”) which is convertible into

approximately 82% of WTRV’s common stock (not giving effect to the conversion of outstanding common stock equivalents) after the

Company elects to spin-off WTRV common stock to the Company’s stockholders and a registration statement covering the spin-off has

been declared effective. The Company’s Chief Executive Officer is also the Executive Chairman of WTRV, and the Company’s Chief

Financial Officer is the Chief Executive Officer of WTRV. The former Chief Executive Officer and director of WTRV is the son-in-law of

the Company’s Executive Chairman, and he resigned from all positions with WTRV in connection with the closing. The new Board of

Directors (the “Board”) of WTRV includes the Company’s Chief Executive Officer and the Chief Executive Officer’s

daughter as well as three other designees. The Company has determined that it is not the primary beneficiary in this transaction and has

concluded that no consolidation is required for White River as a variable interest entity.

On August

23, 2022 the Company entered into a Share Exchange Agreement (the “Agreement”) with Wolf Energy and Banner Midstream. Pursuant

to the Agreement, upon the terms and subject to the conditions set forth therein, the Company acquired 51,987,832 shares of the Wolf Energy

common stock in exchange for all of the capital stock of Banner Midstream owned by the Company, which represents 100% of the issued and

outstanding shares (the “Exchange”). Following the closing of the Agreement which occurred on September 7, 2022, Banner Midstream

continues as a wholly-owned subsidiary of Wolf Energy. On September 7, 2022, the Exchange was completed, and Banner Midstream became

a wholly-owned subsidiary of Wolf Energy. The shares the Company that were issued by Wolf

Energy represented approximately 70% of the total voting shares of Wolf Energy

that were outstanding as of that time. As a result, the Company consolidates Wolf Energy

in its condensed consolidated financial statements; however because it is the intent of the Company to distribute these shares in Wolf

Energy to the stockholders of the Company upon the effectiveness of a registration statement

filed by Wolf Energy, the Company has classified the assets and liabilities of Wolf Energy

and the results of operations of Wolf Energy in discontinued operations. See Note 2.

On April 9, 2021, a Little

Rock, Arkansas jury awarded Ecoark and Zest a total of $115 million in damages (later reduced to $110 million) which includes $65 million

in compensatory damages and $50 million in punitive damages and found Walmart Inc. (“Walmart”) liable on three counts. The

federal jury found that Walmart misappropriated Zest’s trade secrets, failed to comply with a written contract, and acted willfully

and maliciously in misappropriating Zest’s trade secrets. See Note 15 – Commitments and Contingencies – Legal Proceedings.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

Trend Holdings formed four subsidiaries, including

Bitstream Mining, LLC, a Texas limited liability company (“Bitstream”), on May 16, 2021. In addition, Trend Holdings owned

Barrier Crest, LLC (“Barrier Crest”) which was acquired along with Trend Capital Management, Inc. (“TCM”) which

was acquired by Ecoark Holdings on May 31, 2019. On June 17, 2022, Agora sold Trend Holdings to an entity formed by the investment manager

of Trend Discovery LP and Trend Discovery SPV and sold Trend Discovery Exploration LLC (“Trend Exploration”) to the Company.

See Note 2, “Discontinued Operations”. The Company reclassified the operations of Barrier Crest and TCM, as discontinued operations

as the disposal represents a strategic shift that will have a major effect on the Company’s operations and financial results as

of March 31, 2022.

The Company made this determination for these

segments to be held for sale as the criteria established under ASC 205-20-45-1E have been satisfied as of June 8, 2022. Under ASC 855-10-55,

the Company has reflected the reclassification of assets and liabilities of these entities as held for sale and the operations as discontinued

operations as of and for the year ended March 31, 2022. The Company accounted for this sale as a disposal of the business under ASC 205-20-50-1(a)

upon the closing of the sale on June 17, 2022 at which time the gain was recognized.

The Company assigned its membership interest in

Trend Holdings and its related wholly owned subsidiaries to Agora on September 22, 2021, for the sale of the initial 100 shares for $10.

On October 1, 2021, the Company purchased 41,671,121 shares of Agora common stock for $4,167,112 which Agora used to purchase equipment

to commence the Bitstream operations.

Agora was organized by Ecoark Holdings to enter

the Bitcoin mining business. Because of the plunge in the price of Bitcoin in 2022 and the type of miners Agora acquired during its attempt

to close an initial public offering, Agora determined it was not presently feasible to conduct Bitcoin mining operations and ceased such

activities on March 3, 2022. In September 2022, Agora determined to become a power-centric hosting company and thus, subject to raising

capital, will focus its attention on generating revenues in this capacity.

On August 4, 2021, the Company’s common

stock commenced trading on the Nasdaq Capital Market.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

On October 6, 2021, the Company held a Special

Meeting of Stockholders, at which the stockholders approved (a) an amendment to the Articles of Incorporation to increase the number of

shares of authorized common stock of the Company from 30,000,000 shares to 40,000,000 shares; (b) an amendment to the Ecoark Holdings

2017 Omnibus Incentive Plan to increase the number of shares of common stock authorized for issuance under this plan from 800,000 shares

to 1,300,000 shares; and (c) the issuance of 272,252 restricted stock units and an additional 63,998 restricted stock units to the then

President of Zest Labs and director of the Company under this Plan, in exchange for the cancellation of 672,499 previously issued stock

options.

On September 9, 2022, the Company held an annual

meeting of its stockholders, and the stockholders approved the issuance of the shares of common stock issuable upon conversion of the

Series A Redeemable Convertible Preferred Stock sold on June 8, 2022. Additionally, the stockholders approved increasing authorized common

stock to 100,000,000 shares. Articles of Amendment were filed that day.

On October 28, 2022, the Company and Ecoark, Inc.

assigned all of its residual intellectual property rights and rights in the Zest Labs lawsuits to Zest Labs in connection with the anticipated

spin-off of Zest Labs common stock to the Company’s stockholders. The Board of Directors subsequently determined not to proceed

with the Zest Labs spin-off, however the assignment was not affected by that determination.

Overview of Agora Digital Holdings, Inc.

Bitstream

Bitstream was organized to be our principal Bitcoin

mining subsidiary. Bitstream entered into a series of agreements and arrangements including arranging for a reliable and economical electric

power source needed to efficiently mine Bitcoin, order miners, housing infrastructure and other infrastructure to mine Bitcoin and locate

a third-party hosting service to operate the miners and the service’s more advanced miners.

As discussed in this Note 1, Agora has refocused its efforts and will

become a power-centric hosting company rather than a Bitcoin mining company and will not hold any Bitcoin in its digital wallets. To that

end, Agora entered into a Master Services Agreement (“MSA”) on December 7, 2022 with BitNile, Inc. (“BitNile”),

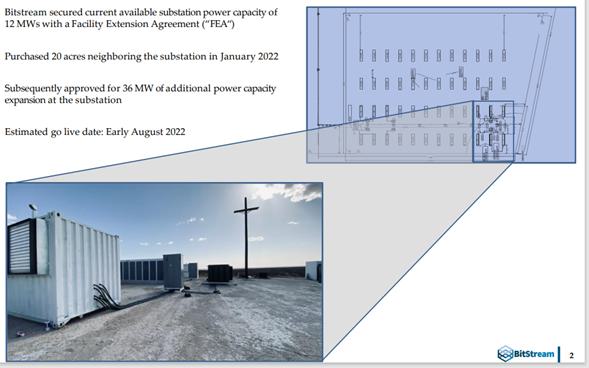

whereby BitNile agreed to provide mining equipment which Agora would host at its West Texas location and supply the electricity for the

cryptocurrency mining. The MSA requires Agora to initially provide up to 12MW of electricity at the West Texas site for BitNile’s

use. An additional 66MW of power can be made available to BitNile as well for a total of 78MW. To meet this obligation, the Company is

required to raise at least $5,000,000 to enable the build out of the hosting facility, including the initial 12MW of power within 45 days

of the date of the MSA. As of the date of this Report, this requirement has not been met.

All significant accounting policies related to

Pinnacle Frac, Capstone, White River, Shamrock, Barrier Crest and Trend Discovery Capital Management have been removed as these entities

are reflected in discontinued operations. For full details on the policies refer to the Annual Report on Form 10-K for the year ended

March 31, 2022 filed on July 7, 2022.

Principles of Consolidation

On May 31, 2019, the Company entered into an Agreement

and Plan of Merger (the “Merger Agreement”) with Trend Discovery Holdings Inc., a Delaware corporation for the Company to

acquire 100% of Trend Discovery Holdings, LLC pursuant to a merger of Trend with and into the Company (the “Merger”). Trend

Discovery Holdings, Inc. ceased doing business upon completion of the merger and Trend Discovery Holdings LLC is the subsidiary of the

Company. Upon the formation of Agora on September 17, 2021, Ecoark assigned the membership interest it owned in Trend Holdings to Agora

on September 22, 2021 when the Company purchased 100 shares of Agora common stock for $10.

On March 27, 2020, the Company and Banner Parent,

entered into the Banner Purchase Agreement to acquire Banner Midstream. Pursuant to the acquisition, Banner Midstream became a wholly

owned subsidiary of the Company and Banner Parent received shares of the Company’s common stock in exchange for all of the issued

and outstanding shares of Banner Midstream. The Company sold all divisions of Banner Midstream in July 2022 and September 2022 as discussed

herein.

The Company applies the guidance of Topic 810

Consolidation of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”)

to determine whether and how to consolidate another entity. Pursuant to ASC Paragraph 810-10-15-10 all majority-owned subsidiaries—all

entities in which a parent has a controlling financial interest—are consolidated except when control does not rest with the parent.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

Pursuant to ASC Paragraph 810-10-15-8, the usual

condition for a controlling financial interest is ownership of a majority voting interest, and, therefore, as a general rule ownership

by one reporting entity, directly or indirectly, of more than 50 percent of the outstanding voting shares of another entity is a condition

pointing toward consolidation. The power to control may also exist with a lesser percentage of ownership, for example, by contract, lease,

agreement with other stockholders, or by court decree.

The Company has utilized the guidance under ASC

810-10-55-4B, Case A for a Change that has resulted in the recognition of non-controlling interest. On October 1, 2021, Agora issued restricted

common stock to non-employee directors, management, employees and advisors. As a result of the restricted common share issuances, the

Company owns now owns less than 100% of Agora (approximately 89%). The Company expects it will continue to control Agora until it completes

the distribution of Agora common stock to its security holders described above; after that event occurs, it may still have sufficient

equity ownership to control Agora unless one or more third parties acquire a larger equity position.

During the six months ended September 30, 2022,

Agora issued 400,000 shares of common stock to consultants and management. As a result of these issuances, the Company’s ownership

percentage in Agora dropped from approximately 90% to approximately 89%.

The Company sold both White River and Banner Midstream (Pinnacle/Capstone)

in July and September 2022, respectively. These entities are no longer subsidiaries of the Company. The Company has investments in WTRV

and Wolf Energy that represent the shares it received for the sale of these entities. The

investment in WTRV is in non-voting preferred shares, and Management has concluded that the Company is not the primary beneficiary in

this transaction, and thus no consolidation is required for White River as a variable interest entity. The Company currently owns approximately

65% of the total issued common shares of Wolf Energy and has consolidated Wolf Energy;

however, the Company expects to distribute these shares to its stockholders of record as of September 30, 2022, and thus has reflected

Wolf Energy in the discontinued operations of the Company for the nine months ended December

31, 2022.

Reclassifications

The Company has reclassified certain amounts in

the December 31, 2021 condensed consolidated financial statements to be consistent with the December 31, 2022 presentation, including

the reclassification of Barrier Crest, TCM, White River, Pinnacle Frac, and Capstone assets and liabilities from continuing operations

to held for sale and reclassifications of operations of Barrier Crest, TCM, White River, Pinnacle Frac, and Capstone to discontinued operations.

The March 31, 2022 consolidated balance sheet has been reclassified to include the assets and liabilities sold for White River, Pinnacle

Frac, and Capstone as well. Additionally, we have removed all rounding of amounts and shares from the December 31, 2021 presentation to

conform to the December 31, 2022 presentation. These changes had no impact on the Company’s financial position or result of operations

for the periods presented.

Noncontrolling Interests

In accordance with ASC 810-10-45 Noncontrolling

Interests in Consolidated Financial Statements, the Company classifies noncontrolling interests as a component of equity within the

consolidated balance sheet. In October 2021 and July 2022, with the issuance of restricted common stock to directors, management and advisors,

the Company no longer owns 100% of Agora. As of December 31, 2022 and March 31, 2022, approximately 11% and 9.1% is reflected as non-controlling

interest of that entity. In addition, we have reflected 30% of Wolf Energy as noncontrolling

interests as the Company represents approximately 65% of the voting interests in Wolf Energy.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

Use of Estimates

The preparation of consolidated financial statements

in conformity with accounting principles generally accepted in the U.S. requires management to make estimates and assumptions that affect

the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial

statements and reported amounts of revenues and expenses during the reporting period. These estimates include, but are not limited to,

management’s estimate of provisions required for uncollectible accounts receivable, fair value of assets held for sale and assets

and liabilities acquired, impaired value of equipment and intangible assets, including goodwill, asset retirement obligations, estimates

of discount rates in lease, liabilities to accrue, fair value of derivative liabilities associated with warrants, cost incurred in the

satisfaction of performance obligations, permanent and temporary differences related to income taxes and determination of the fair value

of stock awards.

Actual results could differ from those estimates.

Revenue Recognition

The Company recognizes revenue under ASC 606,

Revenue from Contracts with Customers. The core principle of the revenue standard is that a company should recognize revenue to depict

the transfer of promised goods or services to customers in an amount that reflects the consideration to which the company expects to be

entitled in exchange for those goods or services.

The following five steps are applied to achieve

that core principle:

| |

● |

Step 1: Identify the contract with the customer |

| |

● |

Step 2: Identify the performance obligations in the contract |

| |

● |

Step 3: Determine the transaction price |

| |

● |

Step 4: Allocate the transaction price to the performance obligations in the contract |

| |

● |

Step 5: Recognize revenue when the Company satisfies a performance obligation |

In order to identify the performance obligations

in a contract with a customer, a company must assess the promised goods or services in the contract and identify each promised good or

service that is distinct. A performance obligation meets ASC 606’s definition of a “distinct” good or service (or

bundle of goods or services) if both of the following criteria are met: The customer can benefit from the good or service either on its

own or together with other resources that are readily available to the customer (i.e., the good or service is capable of being distinct),

and the entity’s promise to transfer the good or service to the customer is separately identifiable from other promises in the contract

(i.e., the promise to transfer the good or service is distinct within the context of the contract).

If a good or service is not distinct, the good

or service is combined with other promised goods or services until a bundle of goods or services is identified that is distinct.

The transaction price is the amount of consideration

to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer. The consideration promised

in a contract with a customer may include fixed amounts, variable amounts, or both. When determining the transaction price, an entity

must consider the effects of all of the following:

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

| |

● |

Constraining estimates of variable consideration |

| |

● |

The existence of a significant financing component in the contract |

| |

● |

Consideration payable to a customer |

Variable consideration is included in the transaction

price only to the extent that it is probable that a significant reversal in the amount of cumulative revenue recognized will not occur

when the uncertainty associated with the variable consideration is subsequently resolved.

The transaction price is allocated to each performance

obligation on a relative standalone selling price basis. The standalone selling price is the price at which the Company would sell a promised

service separately to a customer. The relative selling price for each performance obligation is estimated using observable objective evidence

if it is available. If observable objective evidence is not available, the Company uses its best estimate of the selling price for the

promised service. In instances where the Company does not sell a service separately, establishing standalone selling price requires significant

judgment.

The Company estimates the standalone selling price

by considering available information, prioritizing observable inputs such as historical sales, internally approved pricing guidelines

and objectives, and the underlying cost of delivering the performance obligation. The transaction price allocated to each performance

obligation is recognized when that performance obligation is satisfied, at a point in time or over time as appropriate.

Management judgment is required when determining

the following: when variable consideration is no longer probable of significant reversal (and hence can be included in revenue); whether

certain revenue should be presented gross or net of certain related costs; when a promised service transfers to the customer; and the

applicable method of measuring progress for services transferred to the customer over time.

Although, Agora since March 3, 2022, has not recognized

revenue from its mining operations, prior to this time, it recognized revenue upon satisfaction of its performance obligation over time

in accordance with ASC 606-10-25-27 for its contracts with mining pool operators.

The Company accounts for incremental costs of

obtaining a contract with a customer and contract fulfillment costs in accordance with ASC 340-40, Other Assets and Deferred Costs.

These costs should be capitalized and amortized as the performance obligation is satisfied if certain criteria are met. The Company elected

the practical expedient, to recognize the incremental costs of obtaining a contract as an expense when incurred if the amortization period

of the asset that would otherwise have been recognized is one year or less, and expenses certain costs to obtain contracts when applicable.

The Company recognizes an asset from the costs to fulfill a contract only if the costs relate directly to a contract, the costs generate

or enhance resources that will be used in satisfying a performance obligation in the future and the costs are expected to be recovered.

The Company recognizes the cost of sales of a contract as expense when incurred or when a performance obligation is satisfied. The incremental

costs of obtaining a contract are capitalized unless the costs would have been incurred regardless of whether the contract was obtained,

are not considered recoverable, or the practical expedient applies.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

Bitcoin Mining

The discussion here should be understood as being

applicable while Agora was conducting mining operations which it ceased beginning March 3, 2022. On September 16, 2022, the Company determined

to conduct operations as a power-centric hosting company, rather than a Bitcoin mining company. For the past revenue recognition, refer

to the Company’s Annual Report on Form 10-K filed on July 7, 2022.

Hosting Revenues

Agora effective in September 2022 began efforts to

generate revenue via hosting agreements. Agora entered into a MSA on December 7, 2022 with BitNile, whereby BitNile agreed to provide

mining equipment which Agora would host at its West Texas location and supply the electricity for the cryptocurrency mining, subject to

the Company raising $5 million to support the hosting operations. See Note 1. “Organization and Summary of Significant Accounting

Policies.”

When Agora generates hosting revenues, it will

follow ASC 606 as outlined above and recognize revenue upon the completion of the performance obligations as stipulated under the MSA.

For the nine months ended December 31, 2022 and 2021, no revenue has been recognized under any hosting agreements.

All Bitcoin that is mined under these arrangements

will be transmitted directly into the third-party digital wallets and the Company will not hold any Bitcoin in its accounts.

Accounts Receivable and Concentration of

Credit Risk

The Company considers accounts receivable, net

of allowance for doubtful accounts, to be fully collectible. The allowance is based on management’s estimate of the overall collectability

of accounts receivable, considering historical losses, credit insurance and economic conditions. Based on these same factors, individual

accounts are charged off against the allowance when management determines those individual accounts are uncollectible. Credit extended

to customers is generally uncollateralized, however credit insurance is obtained for some customers. Past-due status is based on contractual

terms.

Fair Value Measurements

ASC 820 Fair Value Measurements defines

fair value, establishes a framework for measuring fair value in accordance with U.S. generally accepted accounting principles (“GAAP”),

and expands disclosure about fair value measurements. ASC 820 classifies these inputs into the following hierarchy:

| |

Level 1 inputs: Quoted prices for identical instruments in active markets. |

| |

Level 2 inputs: Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs are observable or whose significant value drivers are observable. |

| |

Level 3 inputs: Instruments with primarily unobservable value drivers. |

The carrying values of the Company’s financial

instruments such as cash, investments, prepaid expenses, accounts payable, and accrued expenses approximate their respective fair values

because of the short-term nature of those financial instruments.

Bitcoin assets will be presented in current assets.

Fair value will be determined by taking the price of the coins from the trading platforms which Agora will most frequently use.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

Bitcoin

Prior to March 3, 2022 when the Company was mining

Bitcoin, it included the Bitcoin in current assets in the consolidated balance sheets as intangible assets with indefinite useful lives.

Bitcoin was recorded at cost less impairment. For the past Bitcoin accounting policies, refer to the Company’s Annual Report on

Form 10-K filed on July 7, 2022. As of December 31, 2022, the Company neither owns nor mines any Bitcoin.

Impairment of Long-lived Assets

Management reviews long-lived assets for impairment

whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets

to be held and used is measured by a comparison of the carrying amount of an asset to the undiscounted future cash flows expected to be

generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured by the amount by which

the carrying amount of the assets exceeds the fair value of the assets.

Segment Information

The Company follows the provisions of ASC 280-10 Segment Reporting. The

Company classified its reporting segments in these three divisions through March 31, 2022, when the Company determined that pursuant to

ASC 205-20-45-1E that the operations related to the Financial Services segment would be reclassified as held for sale as those criteria

identified in the pronouncement had been satisfied as of June 8, 2022. Under ASC 855-10-55, the Company has reflected the reclassification

of assets and liabilities of these entities as held for sale and the operations as discontinued operations as of and for the year ended

March 31, 2022. As a result of this reclassification, the Company’s segment reporting has removed the Financing segment for the

nine months ended December 31, 2021. Effective April 1, 2022, the Company has classified its segments in the Commodity Segment, Technology

Segment and Bitcoin Mining Segment. It now charges a monthly overhead charge to the Technology Segment and to the Transportation component

and Oil and Gas Production component (each part of the Commodities Segment). On July 25, 2022, the Company sold its oil and gas production

business (White River) which is part of the Commodities segment, and on September 7, 2022, the Company sold the remaining part (Pinnacle

Frac and Capstone) of the Commodities Segment. Under ASC 855-10-55, the Company has reflected the sale of these entities and the operations

as discontinued operations as of and for the nine months ended December 31, 2022. As a result of the share exchanges involving White River

and Wolf Energy, and the immaterial nature of the operations of Zest Labs, the Company no longer segregates its operations as most of

the limited continuing operations are related to Agora.

Earnings (Loss) Per Share of Common Stock

Basic net income (loss) per common share is computed

using the weighted average number of common shares outstanding. Diluted earnings (loss) per share (“EPS”) include additional

dilution from common stock equivalents, such as convertible notes, preferred stock, stock issuable pursuant to the exercise of stock options

and warrants.

Common stock equivalents are not included in the

computation of diluted earnings per share when the Company reports a loss because to do so would be anti-dilutive for periods presented,

so only the basic weighted average number of common shares are used in the computations.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

The Company has adjusted the diluted EPS for the

nine and three months ended December 31, 2021 and three months ended December 31, 2022 for warrants classified as derivative liabilities

as well as the preferred stock classified as derivative liabilities in accordance with ASC 260-10-45 as follows. No calculation is necessary

for the nine months ended December 31, 2022 because to do so would be anti-dilutive.

| |

December 31,

2021 | |

| Nine months ended December 31, 2021 | |

| |

| Diluted EPS: | |

| |

| Net income to controlling interest | |

$ | 1,304,848 | |

| Change in fair value of derivative liability | |

| (15,294,814 | ) |

| | |

| | |

| Adjusted net loss | |

$ | (13,989,966 | ) |

| | |

| | |

| Weighted Average Shares Outstanding | |

| 24,727,970 | |

| Adjusted (loss) per share | |

$ | (0.57 | ) |

| |

December 31,

2021 | |

| Three months ended December 31, 2021 | |

| |

| Diluted EPS: | |

| |

| Net income to controlling interest | |

$ | 4,600,003 | |

| Change in fair value of derivative liability | |

| (10,979,137 | ) |

| | |

| | |

| Adjusted net loss | |

$ | (6,379,134 | ) |

| | |

| | |

| Weighted Average Shares Outstanding | |

| 26,364,099 | |

| Adjusted (loss) per share | |

$ | (0.24 | ) |

| | |

December 31,

2022 | |

| Three months ended December 31, 2022 | |

| |

| Diluted EPS: | |

| |

| Net income to controlling interest | |

$ | 2,749,322 | |

| Change in fair value of derivative liability and derivative income | |

| (6,124,833 | ) |

| | |

| | |

| Adjusted net loss | |

$ | (3,375,511 | ) |

| | |

| | |

| Weighted Average Shares Outstanding | |

| 28,499,875 | |

| Adjusted (loss) per share | |

$ | (0.12 | ) |

Derivative Financial Instruments

The Company does not currently use derivative

instruments to hedge exposures to cash flow, market, or foreign currency risks. Management evaluates all of the Company’s financial

instruments, including warrants, to determine if such instruments are derivatives or contain features that qualify as embedded derivatives.

The Company generally uses a Black-Scholes model, as applicable, to value the derivative instruments at inception and subsequent valuation

dates when needed. The classification of derivative instruments, including whether such instruments should be recorded as liabilities

or as equity, is re-measured at the end of each reporting period. The Black-Scholes model is used to estimate the fair value of the derivative

liabilities.

Recently Issued Accounting Standards

In August 2020, the Financial Accounting Standards

Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2020-06, Debt with Conversion and Other Options

(Subtopic 470-20) and Derivatives and Hedging-Contracts in Entity’s Own Equity (Subtopic 815-40), Accounting for Convertible Instruments

and Contract’s in an Entity’s Own Equity. The ASU simplifies accounting for convertible instruments by removing major separation

models required under current GAAP. Consequently, more convertible debt instruments will be reported as a single liability instrument

with no separate accounting for embedded conversion features. The ASU removes certain settlement conditions that are required for equity

contracts to qualify for the derivative scope exception, which will permit more equity contracts to qualify for it. The ASU simplifies

the diluted net income per share calculation in certain areas.

ECOARK HOLDINGS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

DECEMBER 31, 2022

The ASU is effective for annual and interim periods

beginning after December 31, 2021, and early adoption is permitted for fiscal years beginning after December 15, 2020, and interim periods

within those fiscal years. The Company does not believe this new guidance will have a material impact on its consolidated financial statements.

In May 2021, the Financial Accounting Standards

Board (“FASB”) issued ASU 2021-04 “Earnings Per Share (Topic 260), Debt—Modifications and Extinguishments (Subtopic

470-50), Compensation— Stock Compensation (Topic 718), and Derivatives and Hedging—Contracts in Entity’s Own Equity

(Subtopic 815- 40) Issuer’s Accounting for Certain Modifications or Exchanges of Freestanding Equity-Classified Written Call Options”

which clarifies and reduces diversity in an issuer’s accounting for modifications or exchanges of freestanding equity-classified

written call options (for example, warrants) that remain equity classified after modification or exchange. An entity should measure the

effect of a modification or an exchange of a freestanding equity-classified written call option that remains equity classified after modification

or exchange as follows: i) for a modification or an exchange that is a part of or directly related to a modification or an exchange of

an existing debt instrument or line-of-credit or revolving-debt arrangements (hereinafter, referred to as a “debt” or “debt

instrument”), as the difference between the fair value of the modified or exchanged written call option and the fair value of that

written call option immediately before it is modified or exchanged; ii) for all other modifications or exchanges, as the excess, if any,

of the fair value of the modified or exchanged written call option over the fair value of that written call option immediately before

it is modified or exchanged. The amendments in this Update are effective for all entities for fiscal years beginning after December 15,

2021, including interim periods within those fiscal years. An entity should apply the amendments prospectively to modifications or exchanges

occurring on or after the effective date of the amendments. The Company does not believe this new guidance will have a material impact

on its consolidated financial statements.

The Company does not discuss recent pronouncements

that are not anticipated to have an impact on or are unrelated to its financial condition, results of operations, cash flows or disclosures.

Liquidity

For the nine months ended December 31, 2022 and

2021, the Company had a net (loss) income to controlling interest of common stockholders of $(30,389,490) and $1,304,848, respectively,

has working capital (deficit) of $21,072,036 and $(8,394,850) as of December 31, 2022 and March 31, 2022, respectively, and has an accumulated

deficit as of December 31, 2022 of $(157,440,304). As of December 31, 2022, the Company has $32,642 in cash and cash equivalents. The

working capital at December 31, 2022 is the direct result of the investment in WTRV valued at $30,000,000. This positive working capital

is based upon Generally Accepted Accounting Principles and should not be viewed as reflecting available cash or other short term assets.

These represent the value of the 1,200 shares of Series A that are expected to be distributed to the Company’s stockholders, as

discussed in Note 5.

The Company’s

financial statements are prepared using accounting principles generally accepted in the United States (“U.S. GAAP”) applicable

to a going concern, which contemplates the realization of assets and liquidation of liabilities in the normal course of business. The

Company sold its interests in Banner Midstream in two separate transactions on July 25, 2022 and September 7, 2022. In addition, it sold

the non-core business of Trend Discovery on June 17, 2022. The Company expects to distribute the common stock it received (or issuable

upon conversion of preferred stock) in the sales to its stockholders upon the effective registration statements for the two entities the

companies were sold to. See Note 13, “Series A Convertible Redeemable Preferred Stock” for information on the Company’s

recent $12 million convertible preferred stock financing. That financing has restrictive covenants that require approval of the investor

for the Company to engage in any equity or debt financing.

The Company

believes that the current cash on hand is not sufficient to conduct planned operations for one year from the issuance of the consolidated

financial statements, and it needs to raise capital to support their operations. The Company has recently established a potential source

of revenue upon entering into the MSA with BitNile If revenue is generated from the MSA, management expects that it will go towards covering

the Company’s operating costs and to allow it to continue as a going concern. However, in order to proceed under the MSA, the Company